Embed Size (px)

Citation preview

Risk Management

Risk Management Readings

• “Beyond Value at Risk” Kevin Dowd Wiley 1998

• “Mastering Risk Volume 1 and 2” FT Prentice Hall 2001

• “Risk Management for Company Executives” John Smullen FT Prentice Hall 2000

Risk Management Readings

• “The Revolution in Risk Management” Anthony Santomero in “Mastering Finance” FT Prentice Hall 1998

• “A Brief History of Downside Risk Measures” David Nawrocki Journal of Investing 1999

Lecture Summary

• The Nature of Risks

• The Measurement of Risk

• Attitudes to Risk

The Nature of Risk

A Story• In 1530 Atahuallpa defeated his half brother Huascar to

gain control of the Inca Empire• He had conquered what he thought was the overwhelming

bulk of the civilised world and ruled an Empire some have compared to the Roman Empire in Size

• He let Francisco Pizarro with 100 soldiers and 60 horsemen meet him at the village of Cajamar which he surrounded with 40,000 troops

• The Spanish were surrounded but they attacked and killed 6-7,000 within a day.

• That led to the demise of the Inca Empire

Risk Related Thoughts

• Lightning Strikes• The Arrogance of Success Leads to Risk

Taking• Cultures may be Brittle• Other individuals and organisations may see

things radically differently• Technological Change can have major

impacts

Risk and Finance

Is there a Valuable Distinction Between Risk and Uncertainty ?

The Continuum of Risks

• A Sensible Vision of Outcomes and Their Probabilities - Day to Day Movements in Equities

• A Sensible Vision of Outcomes but not Their Probabilities - Collapse in Housing Market

• No Vision of Outcomes or their Probabilities - Chicago Board of Trade 1992

The Sources of Risk

• Market Risk - Interest Rate, Forex, Commodity, Equity, Liquidity Risk (?), etc.

• Credit Risk - Risk of Counterparty Default

• Operational Risk - All other Risks

Market and Credit Risk

Knowledge Of Outcomes

Knowledge of Probabilities

Operational Risk

Knowledge Of Outcomes

Knowledge of Probabilities

Risk Measurement and Attitudes to Risk

Risk Measures and Attitudes to Risk

Returns in % terms reflecting distribution from which returnsdrawn

Year 1 2 3 4 5 6 7 8 9 10

A 10 11 10 11 11 10 11 2 10 11B 5 13 5 9 7 12 9 6 14 9

E(Ra) = 9.7 SD(Ra) = 2.61E(Rb) = 9.2 SD(Rb) = 2.87

Consider Data on Last Slide and Evaluate the Nature of the Choice between the two

distributions of Returns ?

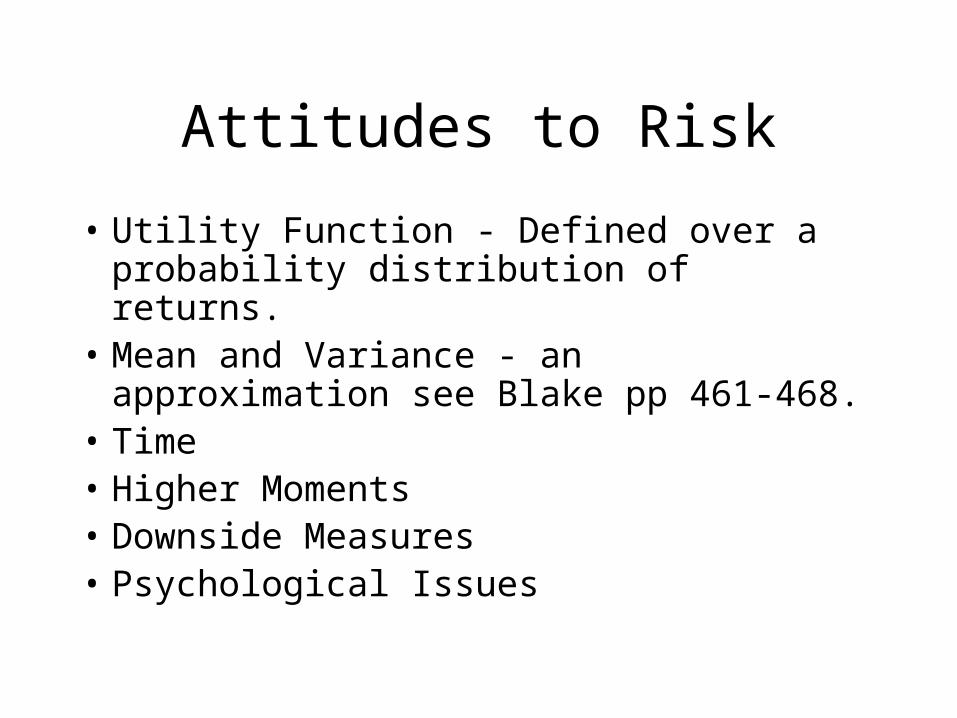

Attitudes to Risk

• Utility Function - Defined over a probability distribution of returns.

• Mean and Variance - an approximation see Blake pp 461-468.

• Time• Higher Moments• Downside Measures• Psychological Issues

Real Returns on US Assets 1802-1996

AverageReal Retrun

SD One YearHolding

SD TwentyYear Holding

Stocks 6.9 18 2.7

Bonds 3.4 8.5 3

Bills 2.9 6 2.8

Higher Moments

rMr = 1/N (xi –E(xi))

i = 1

N

Moments – To what extent is investor utility defined over

moments• 1st. Mean

• 2nd. Variance

• 3rd. Skewness – Degree of Asymmetry

• 4th. Kurtosis – Degree of Peakedness

Downside Measures

• Worst Case

• Value at Risk

• Lower Downside Moments

• Extreme Values

VAR Definition

The Value at Risk (VAR) is the level of expected loss over a

given time horizon which will only be exceeded in a specified

proportion of instances.J.P.Morgan’s 4.15 Report

Definitions and Measures of Risk

Likelihood

Return

a

x 0 y

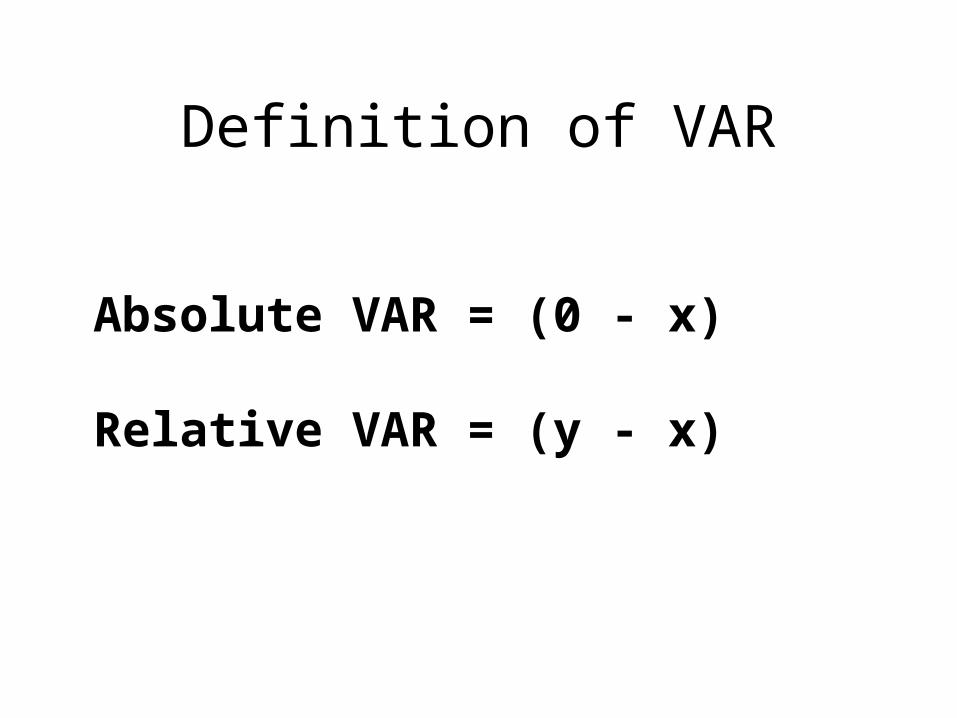

Definition of VAR

Absolute VAR = (0 - x)

Relative VAR = (y - x)

Expected Tail Loss

• When the outturn is worse than the VAR cut-off value what is the average loss

• Focuses on tail of distribution

• Better on discontinuous distributions

Key Choice Parameters

• Time Period

• Confidence Level

Time Period

• Liquidity of Portfolio

• Regulatory Framework

• Measurement Technique – Does one Assume Normality

• How does one deal with portfolio composition

• Required Data for Testing

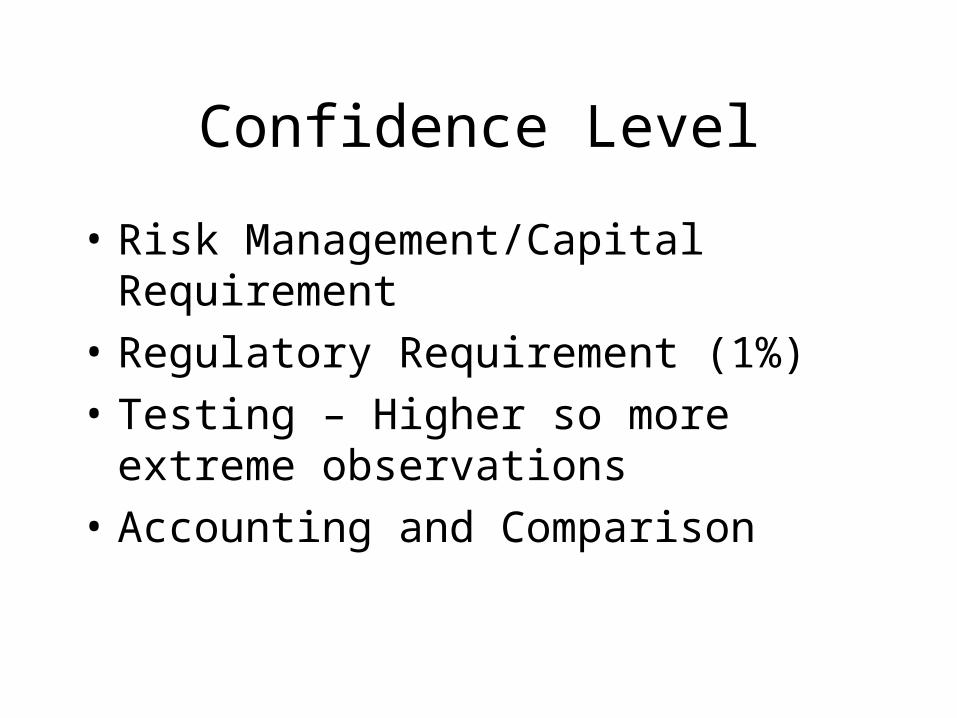

Confidence Level

• Risk Management/Capital Requirement

• Regulatory Requirement (1%)

• Testing – Higher so more extreme observations

• Accounting and Comparison

Measuring Value at Risk

• Variance/Covariance

• Historical

• Monte Carlo Simulation

Issues with Value at Risk and ETL

• How does it deal with non-normality?

• How does it deal with financial crises ?

• How does it deal with shifting parameter values?

• What types of risk is it best applied to?

• If distributions are normal VAR and ETL are just a multiples of the standard deviation

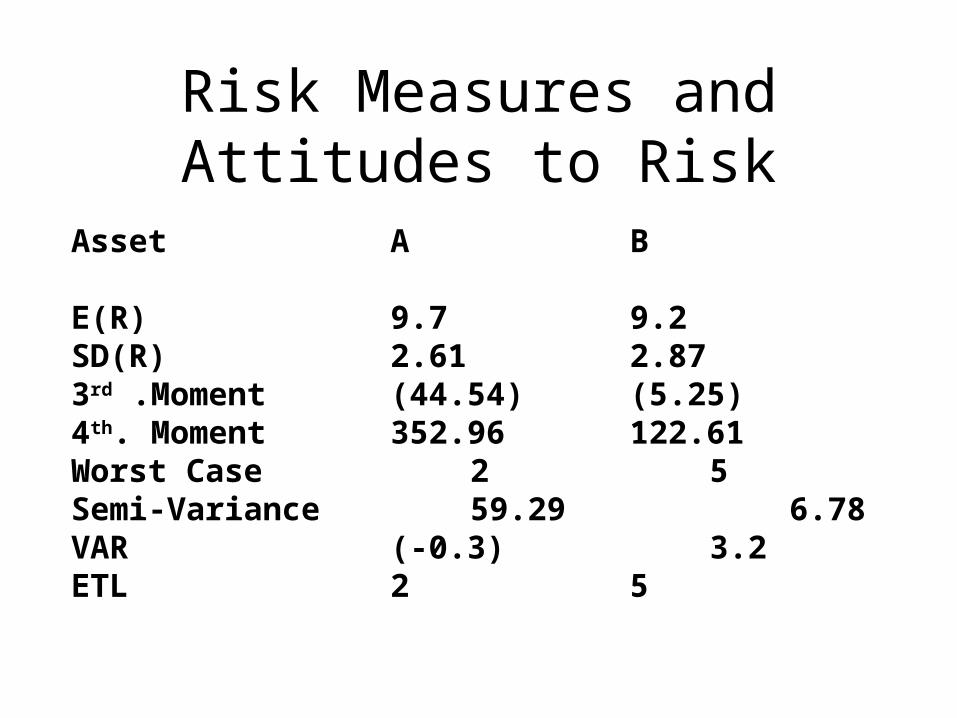

Risk Measures and Attitudes to Risk

Asset A B

E(R) 9.7 9.2SD(R) 2.61 2.873rd .Moment (44.54) (5.25)4th. Moment 352.96 122.61Worst Case 2 5Semi-Variance 59.29 6.78VAR (-0.3) 3.2ETL 2 5

Psychological Issues

• Economic Man

• Cognitive Dissonance

• Depends on Situation

• Too focused on Recent Data

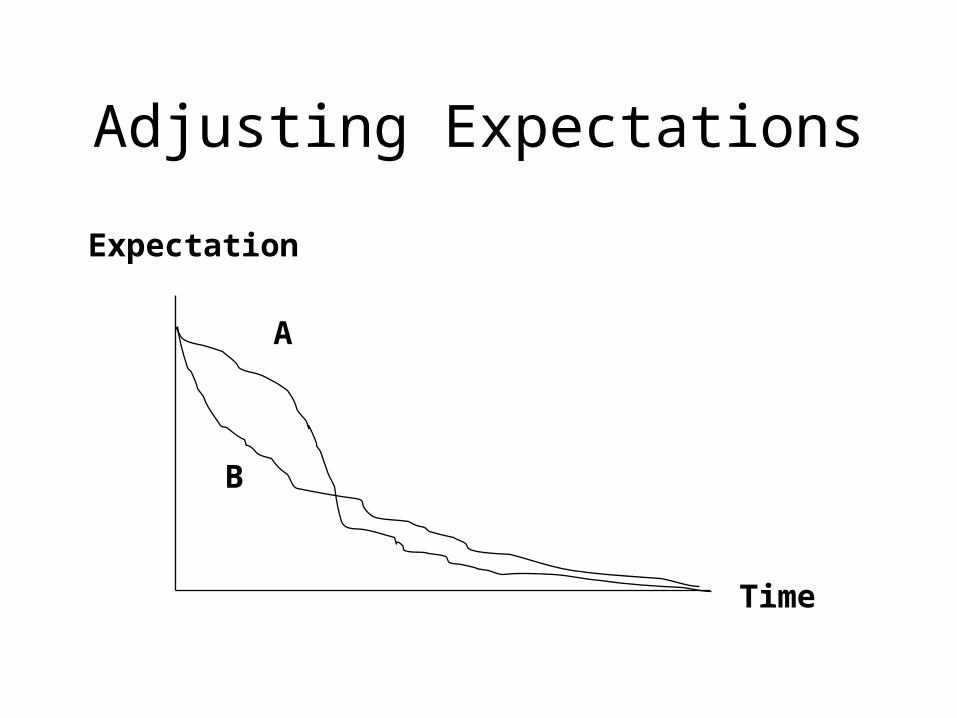

Adjusting Expectations

Expectation

Time

A

B

Definition and Measurement of Risk

• Distributional Measures of Risk

• Calculus Based Measures of Risk

• Some Speciality Measures like Gap Analysis for Particular Risks

Calculus Based Measures of Risk

Derivative Measures of Risk

UnderlyingRisk Factor

Value of FinancialObligation

a

b

Calculus Based Measures of Risk

• First Derivative measures the rate with which the value of an obligation changes with changes in an Underlying Risk Factor

• Second Derivative Measure how sensitive is the First Derivative Measure to changes in the Underlying Risk Factor

Issues in Relation to Calculus Calculus Based Measures

• Need to Specify Mathematical Relationship so require a Pricing Model - Bond Valuation, Option Pricing Models

• Thus difficult to apply to complicated portfolios of obligations

• Applies to Localised Measurement of Risk

• An approximation of the function

Summary

• The Nature of Risk

• The Attitude towards Risk

• The Measurement of Risk

![Risk Management (3C05/D22) Unit 3: Risk Management · 2004. 4. 29. · Risk-management planning Risk resolution [Boehm 1991] Risk monitoring Software risk management steps & techniques](https://img.pdfslide.net/doc/110x75/6122993708b35f7a264d6759/risk-management-3c05d22-unit-3-risk-2004-4-29-risk-management-planning.jpg)