Embed Size (px)

Citation preview

Risk Management Training

Clearing Risk Management Department 23 May 2016

2

Agenda

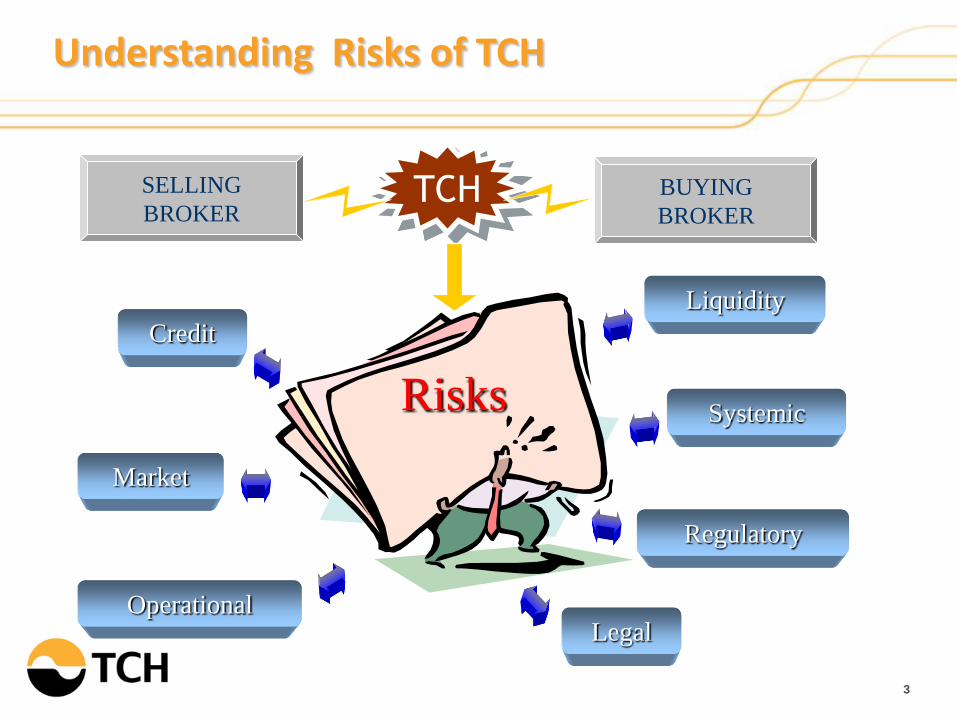

Understanding Risks of TCH

Risk Management Tools

Member Financial Status Monitoring

Financial Resources

Collateral Call Calculation

Types of Collateral

แนวทางในการปฎบตงานของสมาชกตามขอก าหนดของส านกหกบญช

TCH BUYING

BROKER

SELLING

BROKER

Operational

Credit

Market

Liquidity

Systemic

Regulatory

Legal

Risks

3

Understanding Risks of TCH

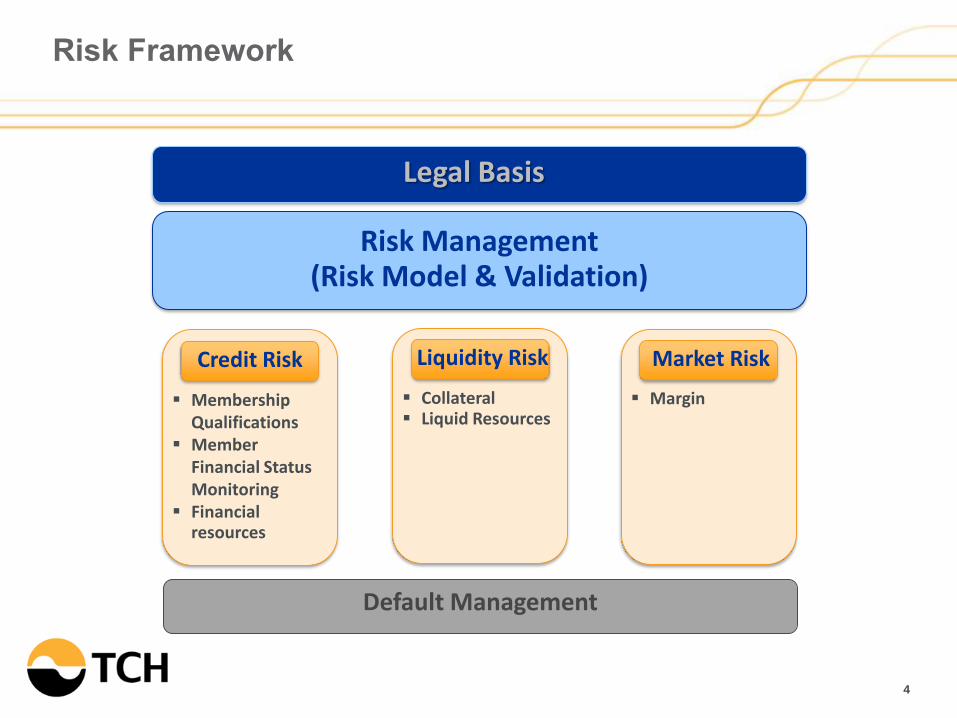

Risk Framework

4

Default Management

Legal Basis

Risk Management (Risk Model & Validation)

Credit Risk

Membership Qualifications

Member Financial Status Monitoring

Financial resources

Liquidity Risk

Collateral Liquid Resources

Market Risk

Margin

5

Agenda

Understanding Risks of TCH

Risk Management Tools

Member Financial Status Monitoring

Financial Resources

Collateral Call Calculation

Types of Collateral

แนวทางในการปฎบตงานของสมาชกตามขอก าหนดของส านกหกบญช

Risk Management Tools

6

Daily

Early Warning System Uncovered Risk Settlement Cap

Monthly

Quarterly Revise Clearing Fund Contribution Rate

Clearing Fund Contribution Financial Reports (i.e. BorLor 2, 2/1, 4/1)

Revise Securities Haircut rate Revise EWS’s parameters (i.e. EWS trigger) Annually

7

Agenda

Understanding Risks of TCH

Risk Management Tools

Member Financial Status Monitoring

Financial Resources

Collateral Call Calculation

Types of Collateral

แนวทางในการปฎบตงานของสมาชกตามขอก าหนดของส านกหกบญช

8

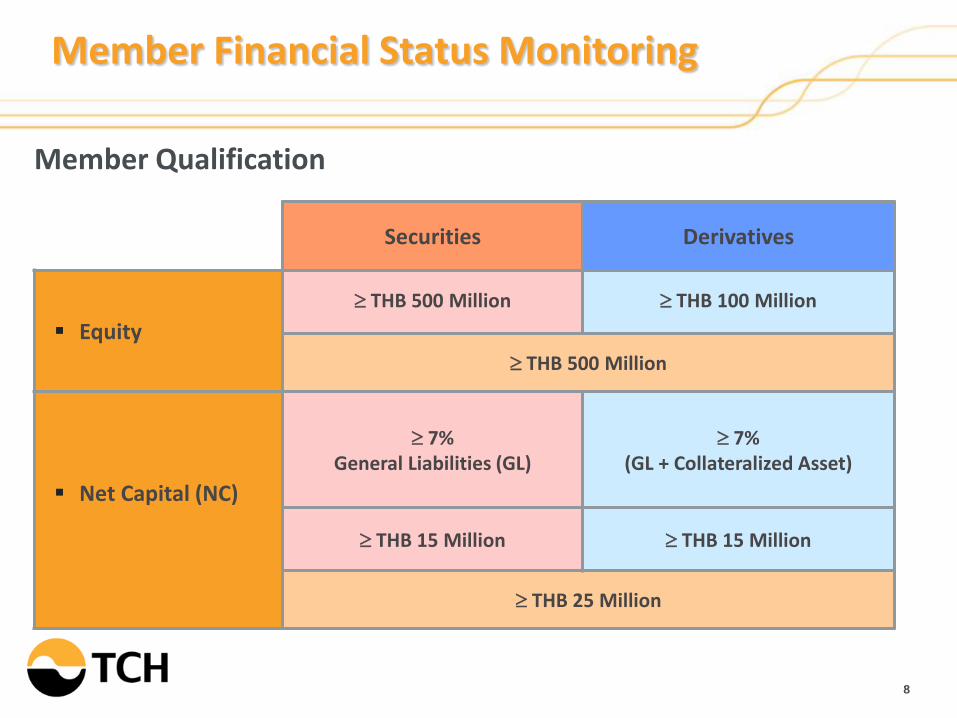

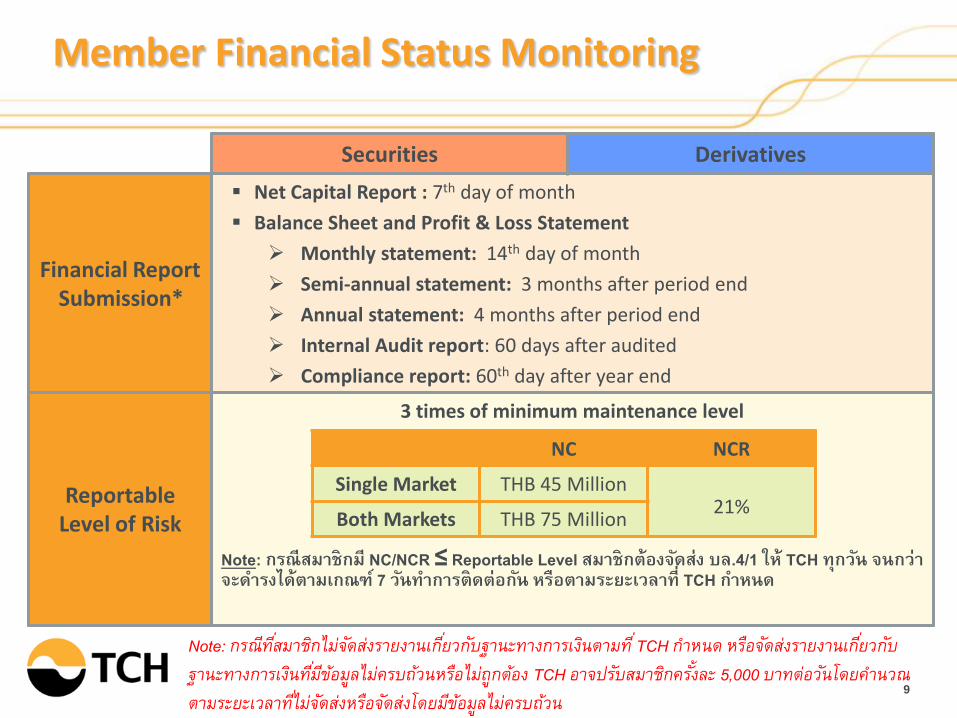

Member Financial Status Monitoring

Securities Derivatives

Equity

THB 500 Million THB 100 Million

THB 500 Million

Net Capital (NC)

7% General Liabilities (GL)

7% (GL + Collateralized Asset)

THB 15 Million THB 15 Million

THB 25 Million

Member Qualification

9

Member Financial Status Monitoring

Securities Derivatives

Financial Report Submission*

Net Capital Report : 7th day of month

Balance Sheet and Profit & Loss Statement

Monthly statement: 14th day of month

Semi-annual statement: 3 months after period end

Annual statement: 4 months after period end

Internal Audit report: 60 days after audited

Compliance report: 60th day after year end

Reportable Level of Risk

3 times of minimum maintenance level

Note: กรณสมาชกม NC/NCR ≤ Reportable Level สมาชกตองจดสง บล.4/1 ให TCH ทกวน จนกวาจะด ารงไดตามเกณฑ 7 วนท าการตดตอกน หรอตามระยะเวลาท TCH ก าหนด

NC NCR

Single Market THB 45 Million 21%

Both Markets THB 75 Million

Note: กรณทสมาชกไมจดสงรายงานเกยวกบฐานะทางการเงนตามท TCH ก าหนด หรอจดสงรายงานเกยวกบฐานะทางการเงนทมขอมลไมครบถวนหรอไมถกตอง TCH อาจปรบสมาชกครงละ 5,000 บาทตอวนโดยค านวณตามระยะเวลาทไมจดสงหรอจดสงโดยมขอมลไมครบถวน

10

Agenda

Understanding Risks of TCH

Risk Management Tools

Member Financial Status Monitoring

Financial Resources

Collateral Call Calculation

Types of Collateral

แนวทางในการปฎบตงานของสมาชกตามขอก าหนดของส านกหกบญช

11

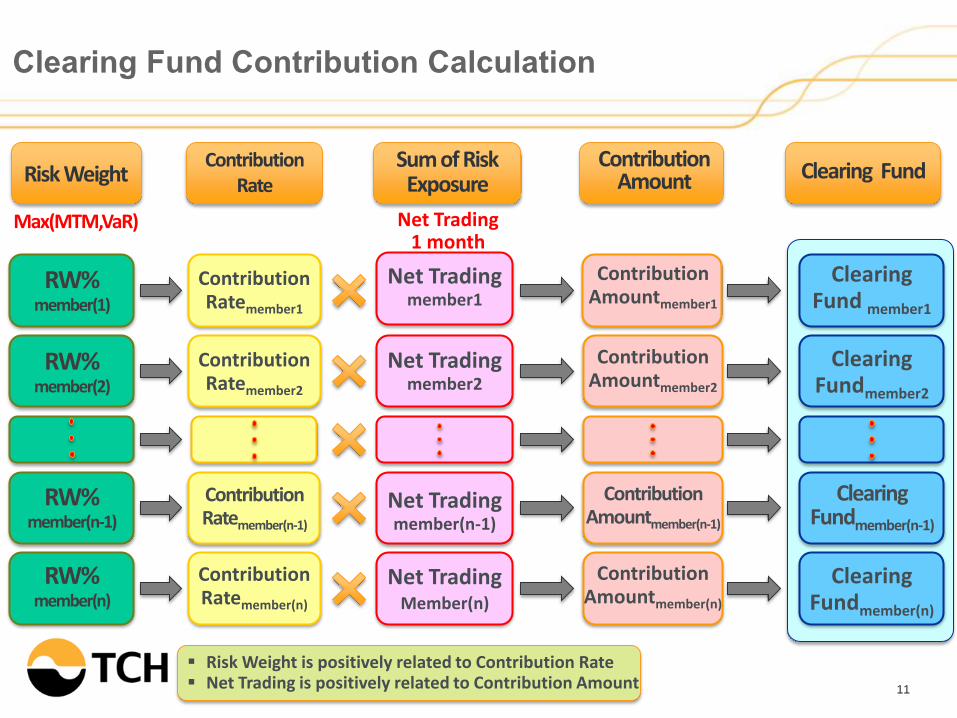

Clearing Fund Contribution Calculation

Risk Weight is positively related to Contribution Rate Net Trading is positively related to Contribution Amount

Contribution Rate

Contribution Ratemember1

Contribution Ratemember2

Contribution Ratemember(n-1)

Contribution Ratemember(n)

RW% member(1)

RW% member(2)

RW% member(n-1)

RW% member(n)

Risk Weight

Max(MTM,VaR)

Clearing Fund

Clearing Fund member1

Clearing Fundmember2

Clearing Fundmember(n-1)

Clearing Fundmember(n)

Sum of Risk Exposure

Net Trading 1 month

Net Trading member1

Net Trading member2

Net Trading member(n-1)

Net Trading Member(n)

Contribution Amountmember1

Contribution Amountmember2

Contribution Amountmember(n-1)

Contribution Amountmember(n)

Contribution Amount

12

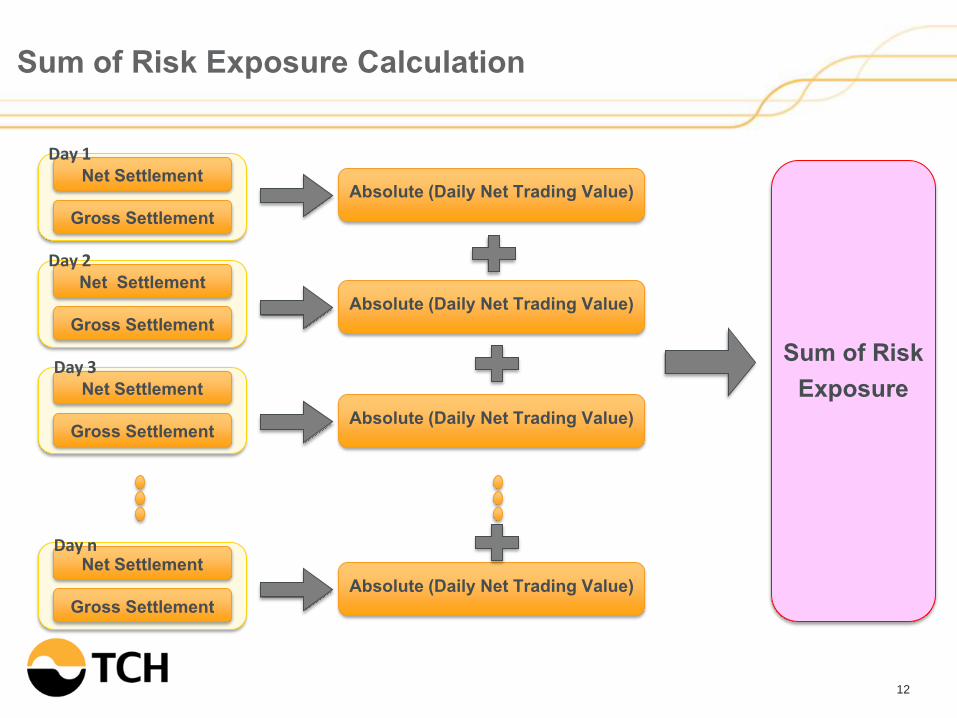

Sum of Risk Exposure Calculation

Sum of Risk Exposure

Absolute (Daily Net Trading Value) Net Settlement

Gross Settlement

Net Settlement

Gross Settlement

Net Settlement

Gross Settlement

Net Settlement

Gross Settlement

Day 1

Day 2

Day 3

Day n

Absolute (Daily Net Trading Value)

Absolute (Daily Net Trading Value)

Absolute (Daily Net Trading Value)

13

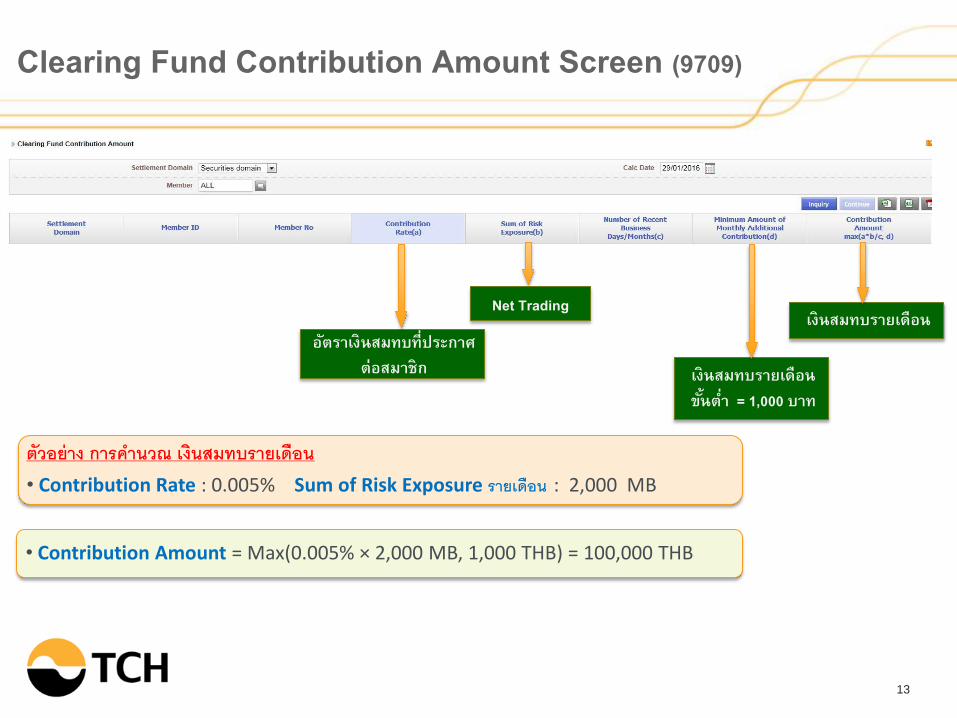

Clearing Fund Contribution Amount Screen (9709)

อตราเงนสมทบทประกาศตอสมาชก

Net Trading เงนสมทบรายเดอน

ตวอยาง การค านวณ เงนสมทบรายเดอน • Contribution Rate : 0.005% Sum of Risk Exposure รายเดอน : 2,000 MB

• Contribution Amount = Max(0.005% × 2,000 MB, 1,000 THB) = 100,000 THB

เงนสมทบรายเดอนขนต า = 1,000 บาท

14

Agenda

Understanding Risks of TCH

Risk Management Tools

Member Financial Status Monitoring

Financial Resources

Collateral Call Calculation

Types of Collateral

แนวทางในการปฎบตงานของสมาชกตามขอก าหนดของส านกหกบญช

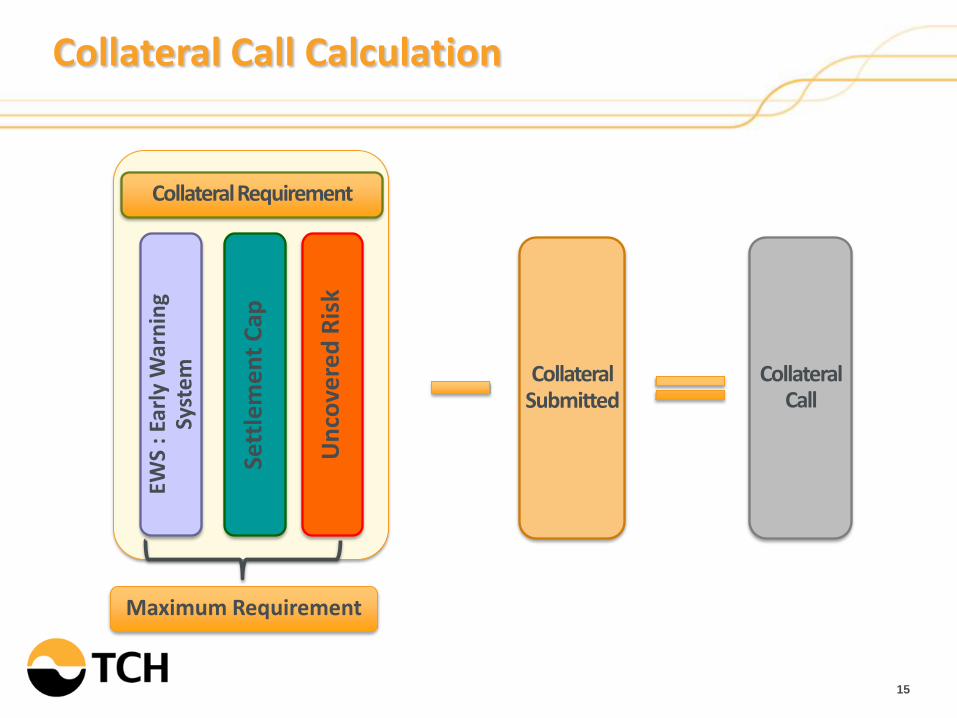

Collateral Call Calculation

15

Collateral Submitted

Collateral Call

Collateral Requirement

EWS

: Ea

rly

War

nin

g Sy

ste

m

Un

cove

red

Ris

k

Sett

lem

en

t C

ap

Maximum Requirement

16

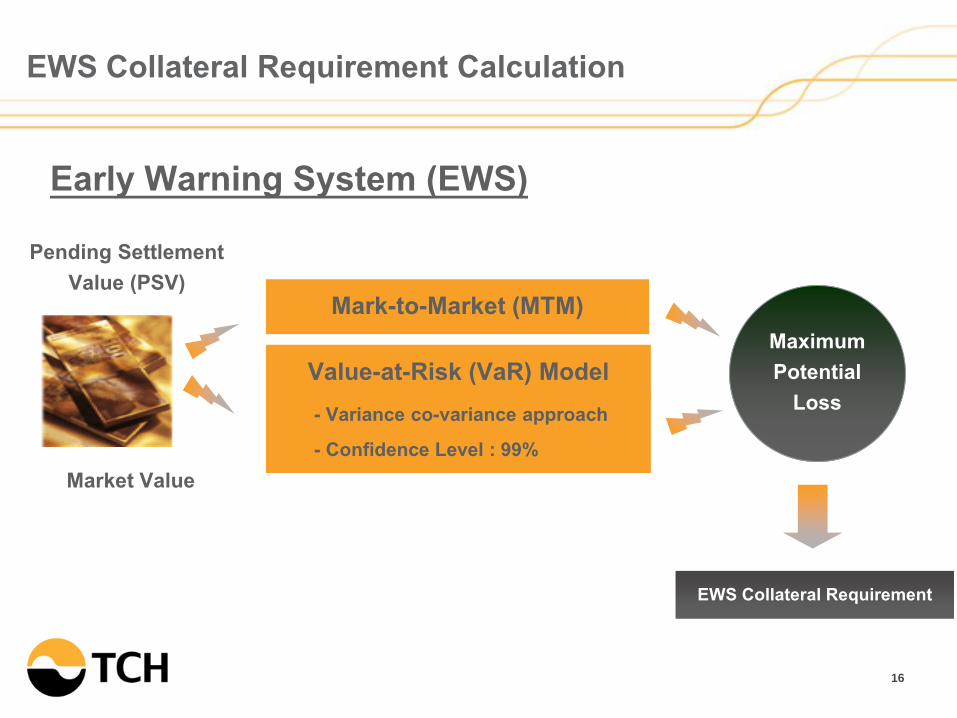

Pending Settlement Value (PSV)

Maximum Potential

Loss

Mark-to-Market (MTM)

Value-at-Risk (VaR) Model

EWS Collateral Requirement

Early Warning System (EWS)

Market Value

- Variance co-variance approach - Confidence Level : 99%

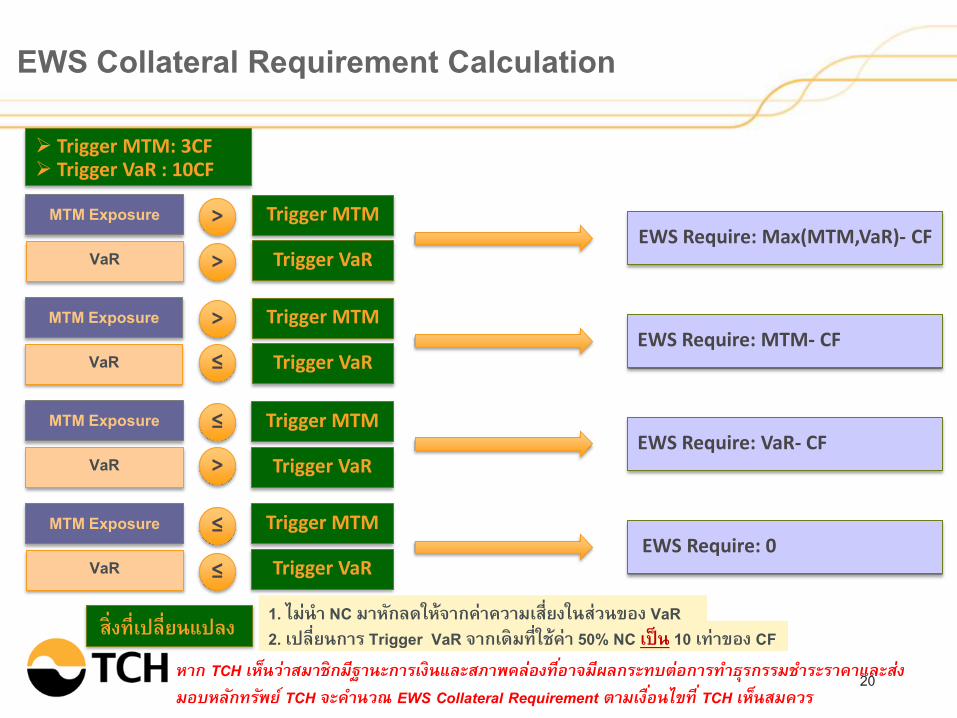

EWS Collateral Requirement Calculation

17

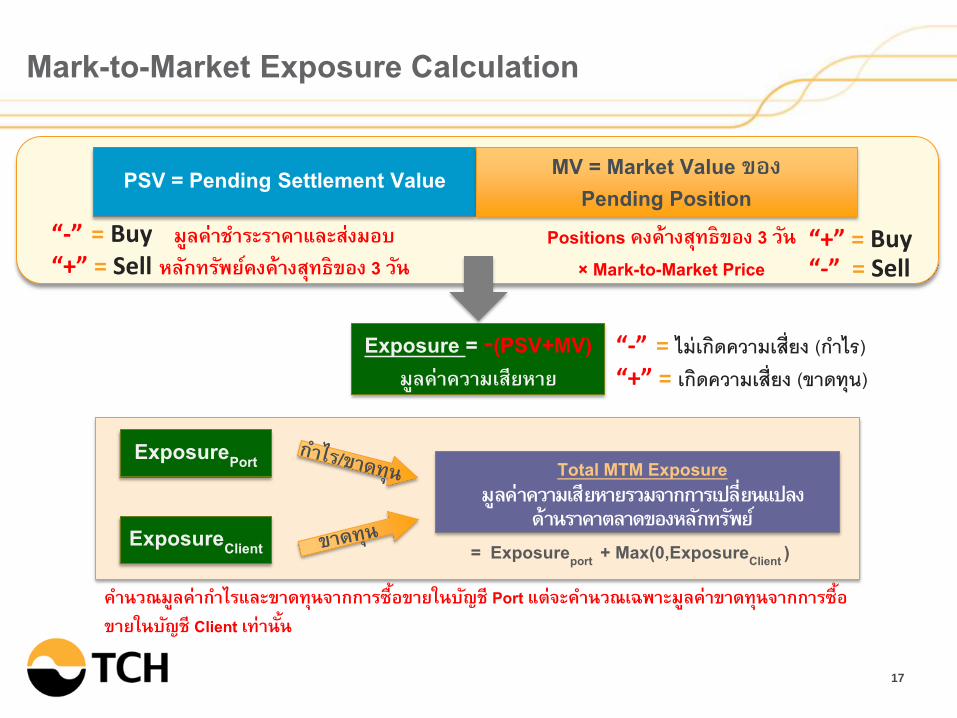

Mark-to-Market Exposure Calculation

Exposure = -(PSV+MV) มลคาความเสยหาย

PSV = Pending Settlement Value MV = Market Value ของ Pending Position

มลคาช าระราคาและสงมอบหลกทรพยคงคางสทธของ 3 วน

“-” = Buy “+” = Sell

Positions คงคางสทธของ 3 วน × Mark-to-Market Price

“+” = Buy “-” = Sell

“-” = ไมเกดความเสยง (ก าไร) “+” = เกดความเสยง (ขาดทน)

Total MTM Exposure มลคาความเสยหายรวมจากการเปลยนแปลง

ดานราคาตลาดของหลกทรพย = Exposureport + Max(0,ExposureClient )

ExposurePort

ExposureClient

ค านวณมลคาก าไรและขาดทนจากการซอขายในบญช Port แตจะค านวณเฉพาะมลคาขาดทนจากการซอขายในบญช Client เทานน

EWS Collateral Requirement Calculation

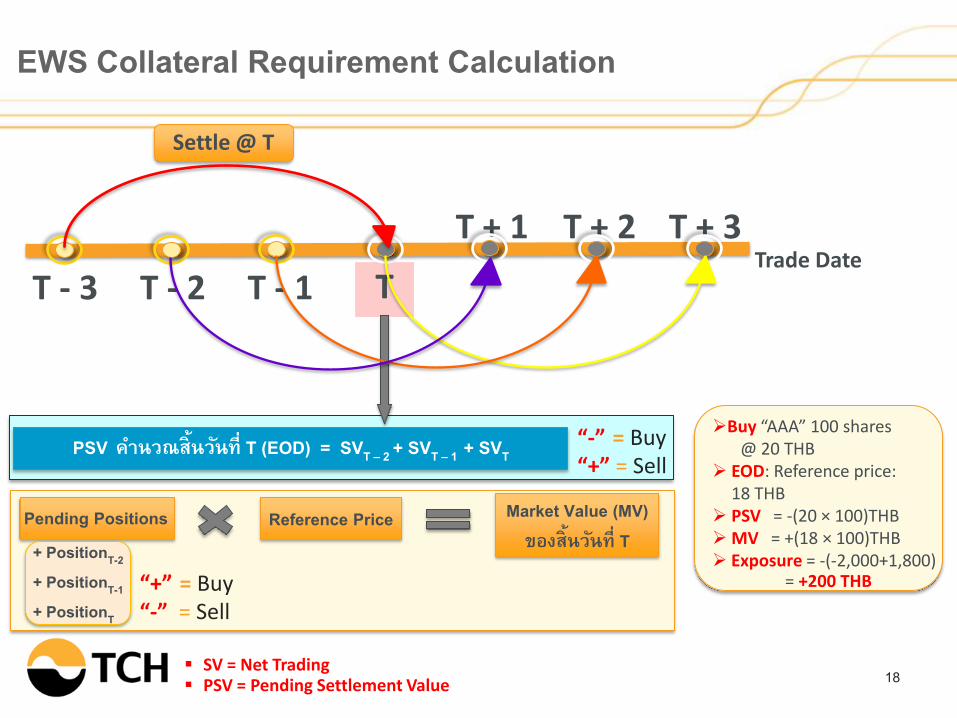

18

T - 3

T + 1 T + 2 T + 3

Settle @ T

T - 2 T - 1 T

PSV ค านวณสนวนท T (EOD) = SVT – 2 + SVT – 1 + SVT

SV = Net Trading PSV = Pending Settlement Value

Trade Date

“-” = Buy “+” = Sell

Buy “AAA” 100 shares @ 20 THB

EOD: Reference price: 18 THB

PSV = -(20 × 100)THB MV = +(18 × 100)THB Exposure = -(-2,000+1,800) = +200 THB

Pending Positions Reference Price

+ PositionT + PositionT-1 + PositionT-2

Market Value (MV) ของสนวนท T

“+” = Buy “-” = Sell

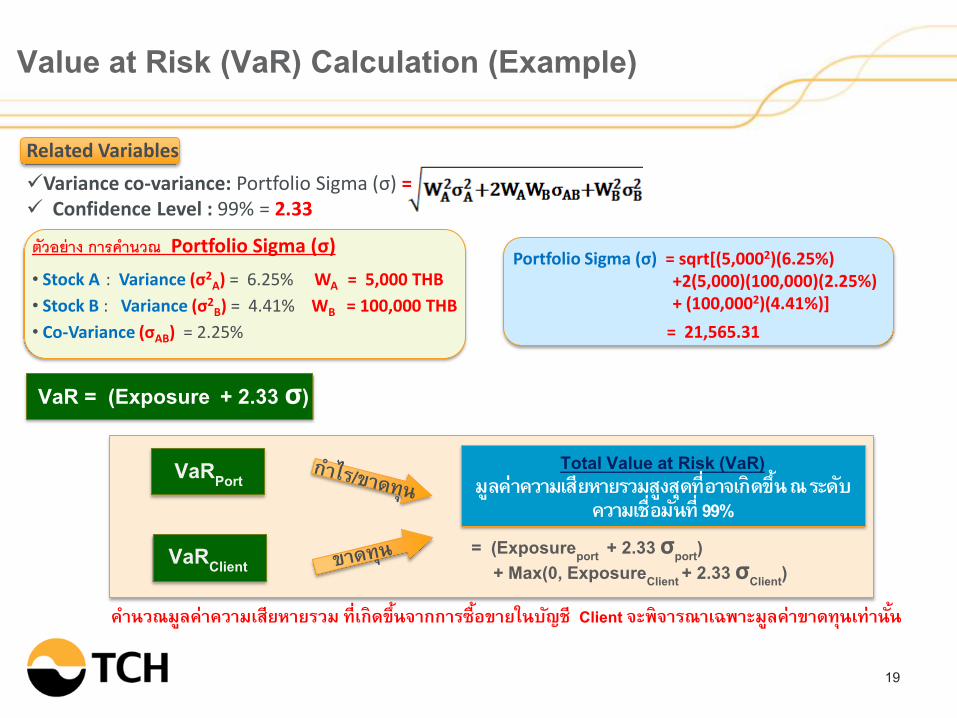

Value at Risk (VaR) Calculation (Example)

19

ตวอยาง การค านวณ Portfolio Sigma (σ)

• Stock A : Variance (σ2A) = 6.25% WA = 5,000 THB

• Stock B : Variance (σ2B) = 4.41% WB = 100,000 THB

• Co-Variance (σAB) = 2.25%

Portfolio Sigma (σ) = sqrt[(5,0002)(6.25%) +2(5,000)(100,000)(2.25%) + (100,0002)(4.41%)]

= 21,565.31

Related Variables

Variance co-variance: Portfolio Sigma (σ) = Confidence Level : 99% = 2.33

VaR = (Exposure + 2.33 σ)

ค านวณมลคาความเสยหายรวม ทเกดขนจากการซอขายในบญช Client จะพจารณาเฉพาะมลคาขาดทนเทานน

Total Value at Risk (VaR) มลคาความเสยหายรวมสงสดทอาจเกดขน ณ ระดบ

ความเชอมนท 99% = (Exposureport + 2.33 σport)

+ Max(0, ExposureClient + 2.33 σClient)

VaRPort

VaRClient

EWS Collateral Requirement Calculation

20

Trigger MTM: 3CF Trigger VaR : 10CF

VaR

MTM Exposure EWS Require: MTM- CF

Trigger MTM

Trigger VaR ≤

>

VaR

MTM Exposure EWS Require: VaR- CF

Trigger MTM

Trigger VaR >

≤

VaR

MTM Exposure Trigger MTM EWS Require: Max(MTM,VaR)- CF

Trigger VaR

>

>

VaR

MTM Exposure EWS Require: 0

Trigger MTM

Trigger VaR

≤

≤

หาก TCH เหนวาสมาชกมฐานะการเงนและสภาพคลองทอาจมผลกระทบตอการท าธรกรรมช าระราคาและสงมอบหลกทรพย TCH จะค านวณ EWS Collateral Requirement ตามเงอนไขท TCH เหนสมควร

1. ไมน า NC มาหกลดใหจากคาความเสยงในสวนของ VaR 2. เปลยนการ Trigger VaR จากเดมทใชคา 50% NC เปน 10 เทาของ CF สงทเปลยนแปลง

21

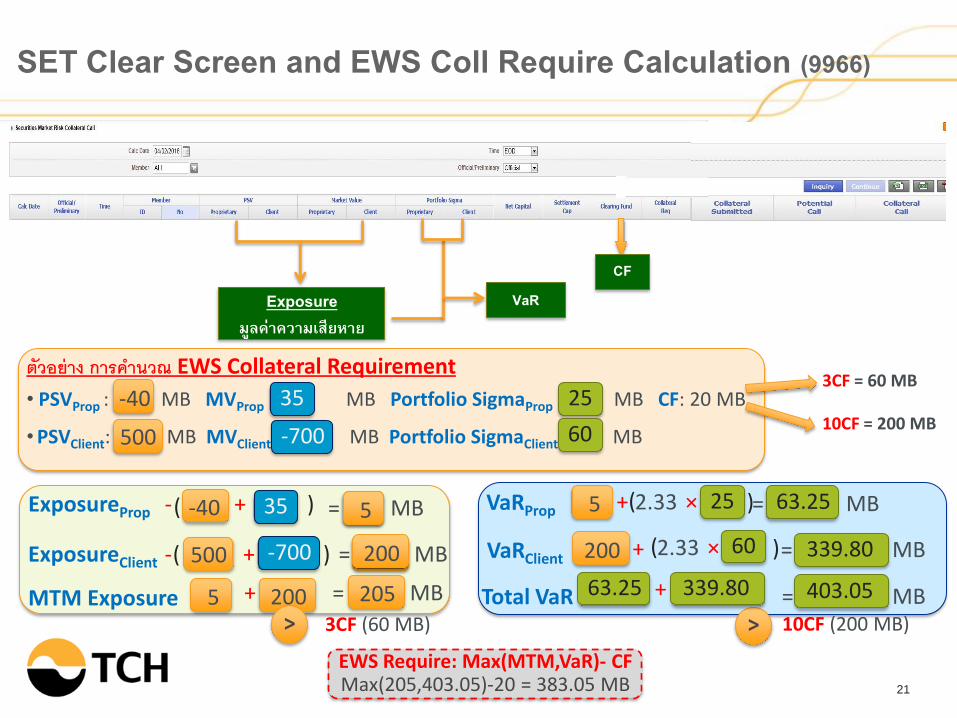

SET Clear Screen and EWS Coll Require Calculation (9966)

ตวอยาง การค านวณ EWS Collateral Requirement • PSVProp : -40 MB MVProp : 35 MB Portfolio SigmaProp : 25 MB CF: 20 MB

• PSVClient: 500 MB MVClient: -700 MB Portfolio SigmaClient : 60 MB

Exposure มลคาความเสยหาย

CF VaR

> 10CF (200 MB)

EWS Require: Max(MTM,VaR)- CF Max(205,403.05)-20 = 383.05 MB

-40

500

35

-700

25

60

- ExposureProp (

+ )

ExposureClient - (

= 5 MB

+ ) = 200 MB

MTM Exposure

5

200

+

VaRProp 5

200

) = 63.25 MB 63.25

VaRClient ) = 339.80 MB 339.80

Total VaR + = MB

+ ( 2.33 × )

( 2.33 × +

-40 35

500 -700

5 200 > 3CF (60 MB)

= MB 205

25 5

200 60

63.25 339.80 403.05

3CF = 60 MB 10CF = 200 MB

22

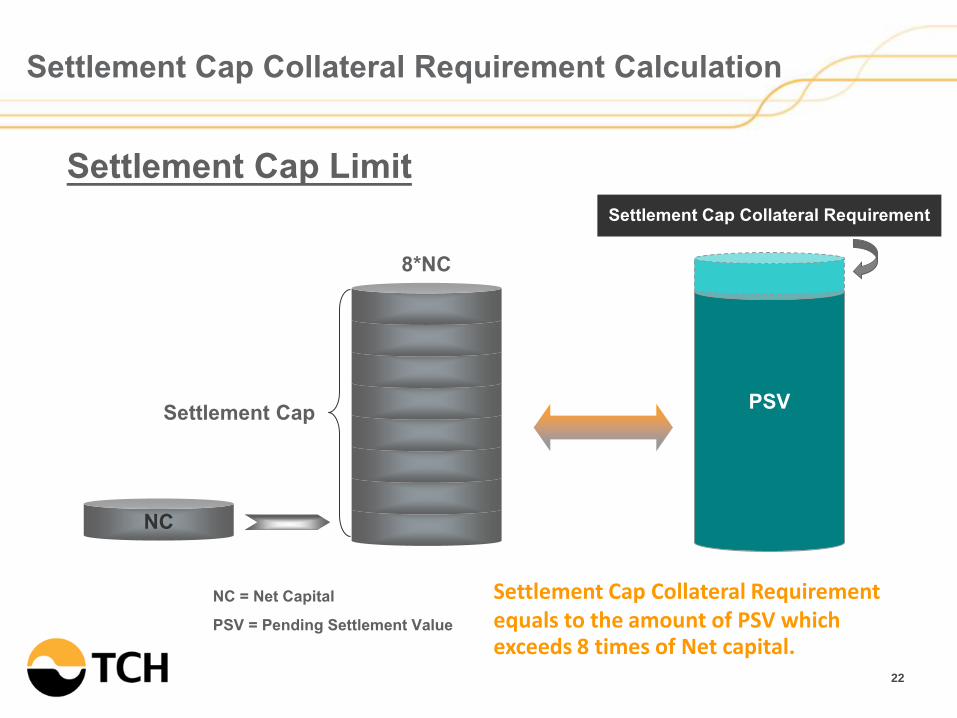

Settlement Cap Limit

8*NC

PSV

NC

NC = Net Capital PSV = Pending Settlement Value

Settlement Cap Collateral Requirement

Settlement Cap

Settlement Cap Collateral Requirement Calculation

Settlement Cap Collateral Requirement equals to the amount of PSV which exceeds 8 times of Net capital.

23

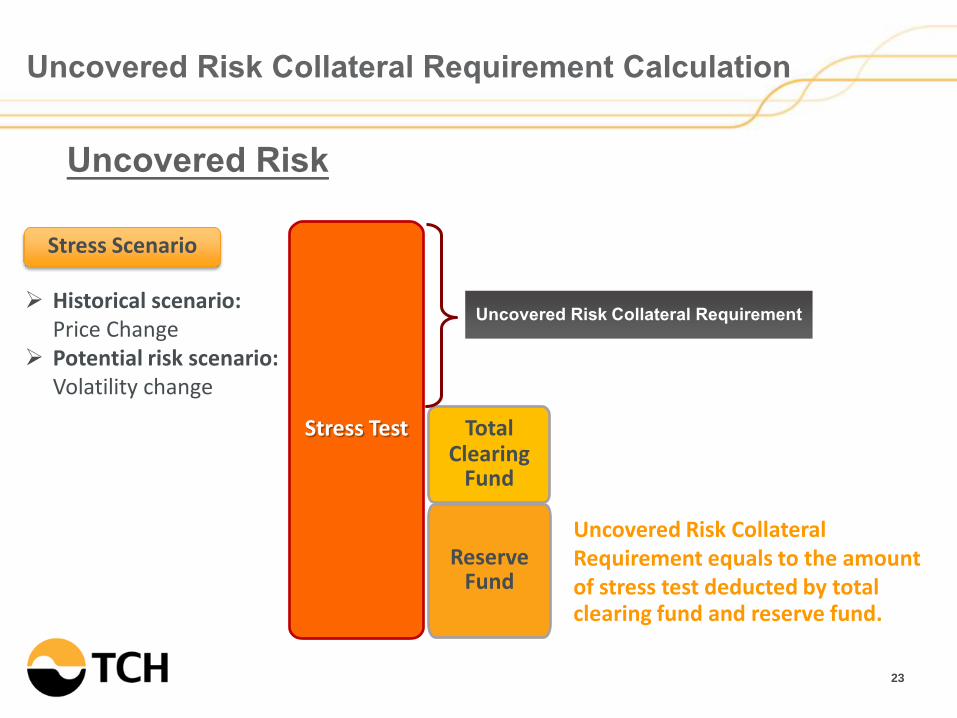

Uncovered Risk

Stress Test Total Clearing

Fund

Reserve Fund

Uncovered Risk Collateral Requirement

Uncovered Risk Collateral Requirement Calculation

Stress Scenario

Historical scenario: Price Change

Potential risk scenario: Volatility change

Uncovered Risk Collateral Requirement equals to the amount of stress test deducted by total clearing fund and reserve fund.

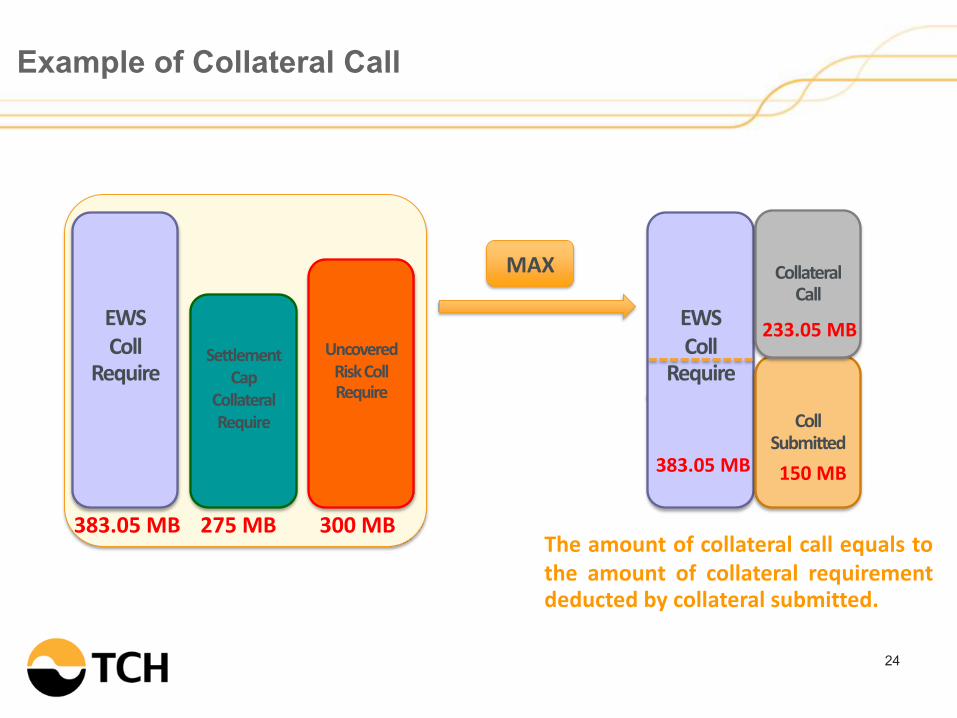

Example of Collateral Call

24

MAX

EWS Coll

Require

383.05 MB

Uncovered Risk Coll Require

300 MB

Settlement Cap

Collateral Require

275 MB

EWS Coll

Require

Coll Submitted

Collateral Call

383.05 MB 150 MB

233.05 MB

The amount of collateral call equals to the amount of collateral requirement deducted by collateral submitted.

25

Agenda

Understanding Risks of TCH

Risk Management Tools

Member Financial Status Monitoring

Financial Resources

Collateral Call Calculation

Types of Collateral

แนวทางในการปฎบตงานของสมาชกตามขอก าหนดของส านกหกบญช

26

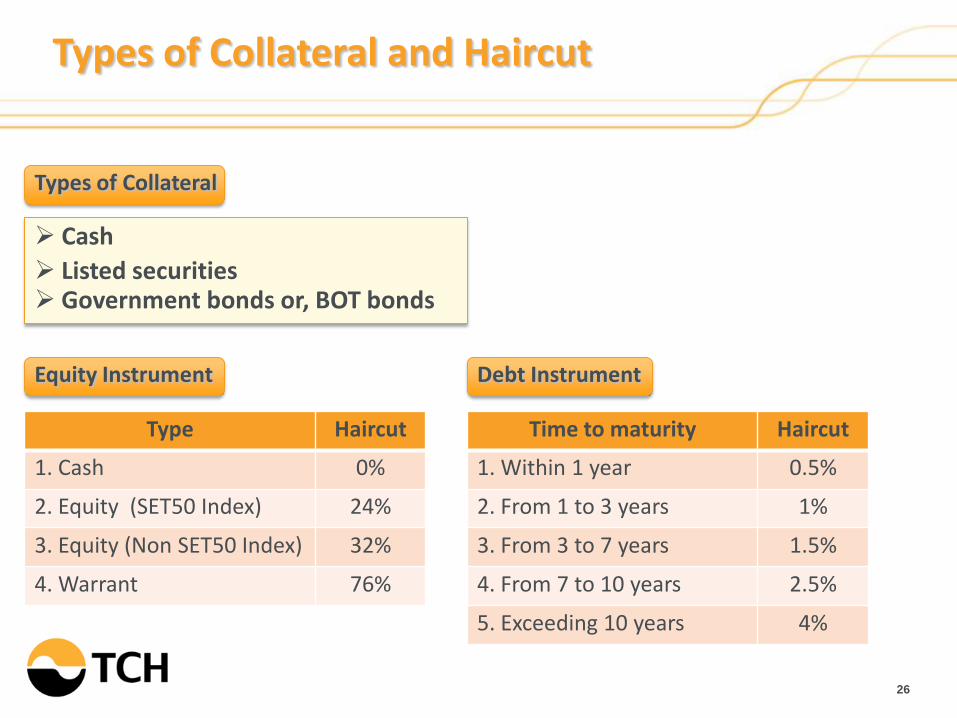

Types of Collateral and Haircut

Cash

Listed securities Government bonds or, BOT bonds

Types of Collateral

Type Haircut

1. Cash 0%

2. Equity (SET50 Index) 24%

3. Equity (Non SET50 Index) 32%

4. Warrant 76%

Time to maturity Haircut

1. Within 1 year 0.5%

2. From 1 to 3 years 1%

3. From 3 to 7 years 1.5%

4. From 7 to 10 years 2.5%

5. Exceeding 10 years 4%

Equity Instrument Debt Instrument

27

Agenda

Understanding Risks of TCH

Risk Management Tools

Member Financial Status Monitoring

Financial Resources

Collateral Call Calculation

Types of Collateral

แนวทางในการปฎบตงานของสมาชกตามขอก าหนดของส านกหกบญช

28

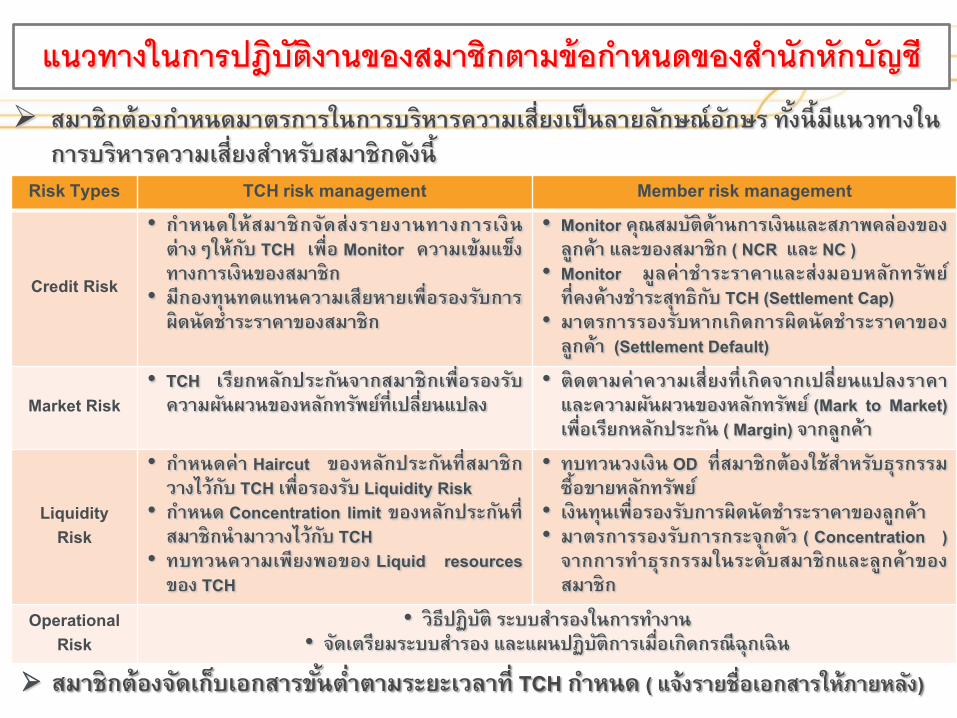

แนวทางในการปฎบตงานของสมาชกตามขอก าหนดของส านกหกบญช

สมาชกตองก าหนดมาตรการในการบรหารความเสยงเปนลายลกษณอกษร ทงนมแนวทางในการบรหารความเสยงส าหรบสมาชกดงน

Risk Types TCH risk management Member risk management

Credit Risk

• ก าหนดใหสมาชกจดสงรายงานทางการเงนตางๆใหกบ TCH เพอ Monitor ความเขมแขงทางการเงนของสมาชก

• มกองทนทดแทนความเสยหายเพอรองรบการผดนดช าระราคาของสมาชก

• Monitor คณสมบตดานการเงนและสภาพคลองของลกคา และของสมาชก ( NCR และ NC )

• Monitor มลคาช าระราคาและสงมอบหลกทรพย ทคงคางช าระสทธกบ TCH (Settlement Cap)

• มาตรการรองรบหากเกดการผดนดช าระราคาของลกคา (Settlement Default)

Market Risk • TCH เรยกหลกประกนจากสมาชกเพอรองรบความผนผวนของหลกทรพยทเปลยนแปลง

• ตดตามคาความเสยงทเกดจากเปลยนแปลงราคาและความผนผวนของหลกทรพย (Mark to Market) เพอเรยกหลกประกน ( Margin) จากลกคา

Liquidity Risk

• ก าหนดคา Haircut ของหลกประกนทสมาชกวางไวกบ TCH เพอรองรบ Liquidity Risk

• ก าหนด Concentration limit ของหลกประกนทสมาชกน ามาวางไวกบ TCH

• ทบทวนความเพยงพอของ Liquid resources ของ TCH

• ทบทวนวงเงน OD ทสมาชกตองใชส าหรบธรกรรมซอขายหลกทรพย

• เงนทนเพอรองรบการผดนดช าระราคาของลกคา • มาตรการรองรบการกระจกตว ( Concentration )จากการท าธรกรรมในระดบสมาชกและลกคาของสมาชก

Operational Risk

• วธปฏบต ระบบส ารองในการท างาน • จดเตรยมระบบส ารอง และแผนปฏบตการเมอเกดกรณฉกเฉน

สมาชกตองจดเกบเอกสารขนต าตามระยะเวลาท TCH ก าหนด ( แจงรายชอเอกสารใหภายหลง)