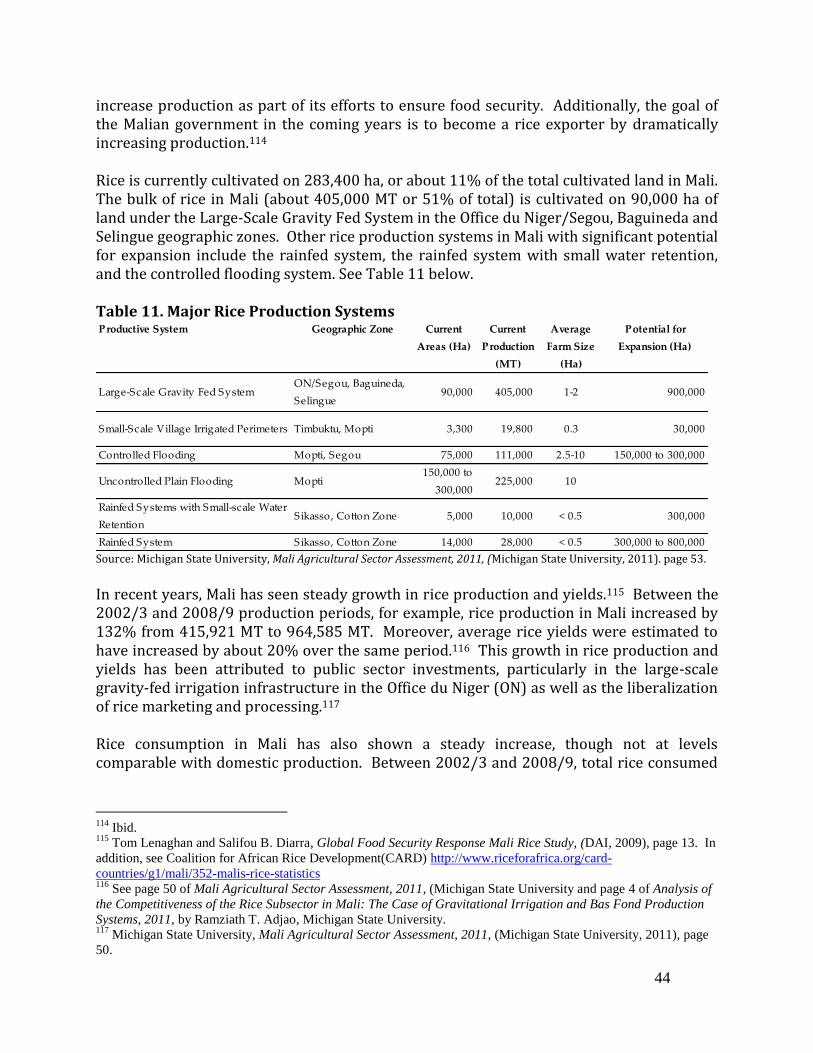

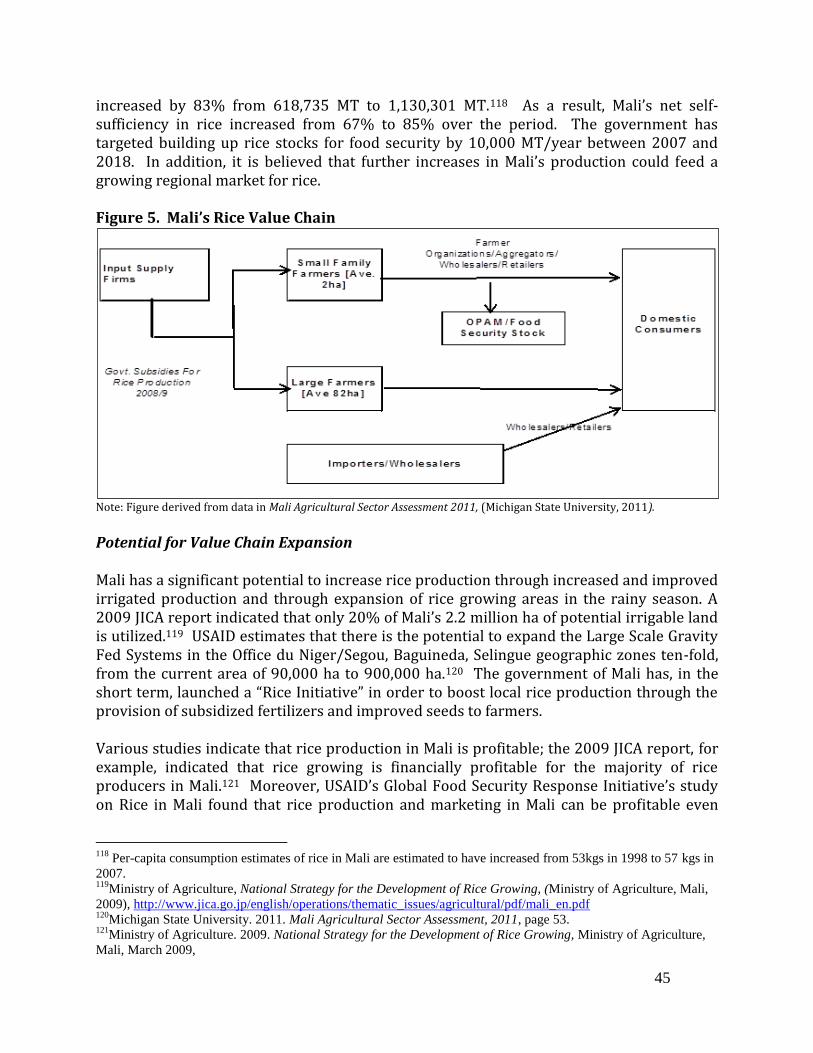

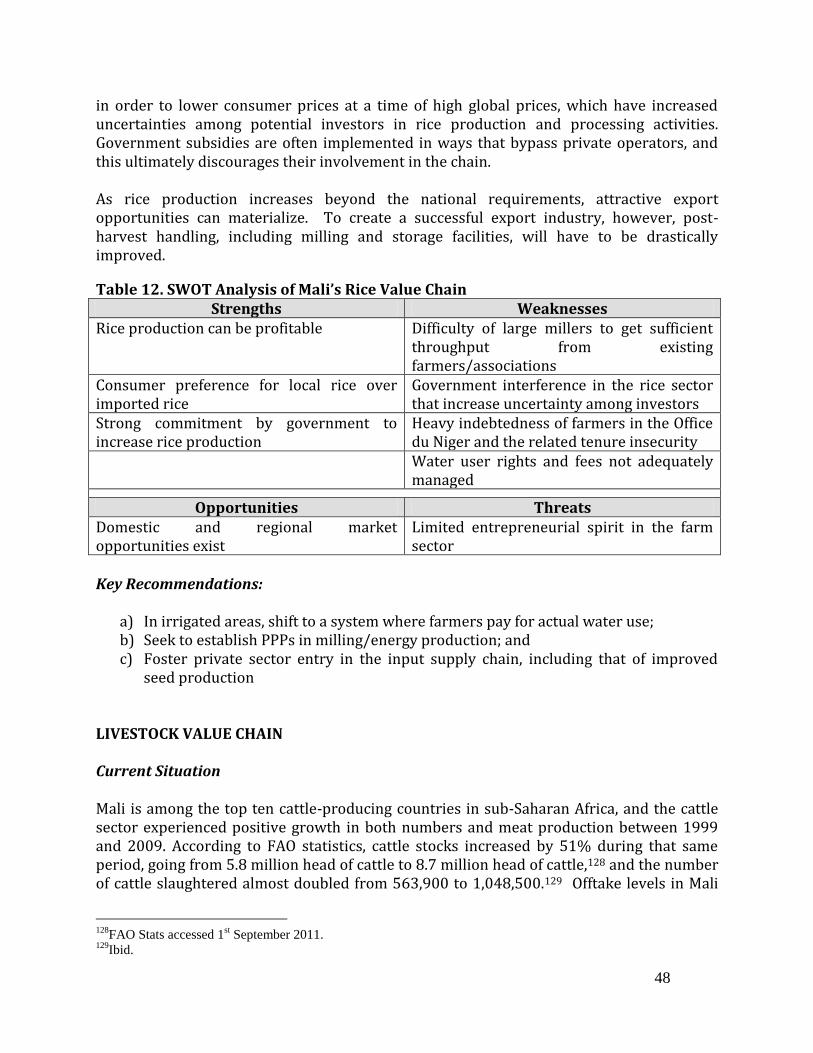

Embed Size (px)

Citation preview

PRIVATE SECTOR PERSPECTIVES FOR

STRENGTHENING AGRIBUSINESS VALUE CHAINS IN AFRICA

CASE STUDIES FROM ETHIOPIA, GHANA, KENYA, AND MALI

Mima Nedelcovych and David Shiferaw

May 2012

2

BACKGROUND The Partnership to Cut Hunger and Poverty in Africa (“the Partnership”) recognizes that increasing the level of foreign assistance and African government spending on agricultural development is critical to achieving long-term, sustained economic growth in Africa. In addition, private investments – both domestic and foreign – are increasingly becoming important drivers of agricultural productivity and income growth. From the private sector perspective, the role of donors and national governments in Africa is to improve the investment climate, institutions and policies for private business owners, including smallholder farmers, to thrive and expand their businesses. Such enabling environment includes investments in:

roads and ports that provide market access and reduce the transaction costs of getting products from farms to consumers;

energy that allows commodities to be processed, chilled, dried, packaged, and sold with minimal wastage;

research and extension services that enable producers and agribusinesses access new, productive technologies; and

education and training that results in a growing group of agricultural professionals capable of providing needed services and entrepreneurial leadership.

But perhaps the most critical role of governments is establishing systems of laws, regulation and governance, which:

set rules for fair and competitive markets and trade, and ensure the rules are followed;

reduce investors’ financial uncertainties and risks, e.g., through enforceable contracts, and fair and transparent judicial procedures; and

permit business owners (farmers, marketing agents, processors, and others) to acquire and secure property rights.

Value chains have been accepted as an effective way of focusing on measures to improve the scale and impact of private sector investments, which include the investments made by smallholder farmers themselves as well as those made by larger-scale domestic or foreign agribusiness investors. Development partners have adopted value chain approaches when designing interventions and project implementation to coordinate their support to specific sectors and commodities. Particularly due to the emphasis on targeted value chains by the US Government’s Feed the Future Initiative, a better understanding of the linkages being made (or missed) along a value chain will be essential to realizing the returns that they promise. In September 2010, the Partnership decided to investigate the constraints impeding greater private sector investment within specific value chains in several African countries. Partnership Board member Dr. Mima Nedelcovych and research fellow David Shiferaw held a series of interviews with a wide range of representatives from the public and private sectors over a five-month period, and complemented outcomes from these interviews with

3

information from literature and other printed resources. Although there is a growing commitment to private sector investments in agricultural development in general and to specific value chains, these results of the interviews pointed towards a number of constraints that continue to limit progress. The interviews identified several areas where, from a private business perspective, governments could better support private sector investments through their actions and policies in order to grow the agricultural sector. This report is a summary of observations made in four country studies: Mali, Ghana, Kenya and Ethiopia. The findings suggest that African governments have significant opportunities to take actions that would directly stimulate private investments in agriculture. The private investors interviewed believed that, with greater government support in creating an enabling environment and less direct government intervention in value chains, critical barriers to their businesses would be reduced or eliminated. Observations specific to the four countries and four agricultural commodity value chains are summarized below and call for practical reforms that promote the growth of successful agribusinesses and more productive farming in Africa.

METHODOLOGY AND OBJECTIVES This study involved four countries with some record of success in promoting private investments and, within each country, meetings with participants engaged in selected value-chains deemed as high priority by the respective governments. The selected value chains include two grains (maize and rice), in order to represent commodities that had large domestic markets, and livestock and horticulture value chains due to their volume of export trade in each country. Countries were paired for comparison purposes. The two country-pairs selected for study were Ethiopia and Kenya in East Africa, and Mali and Ghana in West Africa. Each country pair included a coastal and a landlocked country, and all the countries are part of the US Feed the Future priority countries. Historically, each country has pursued different approaches toward private sector development, although all of them have indicated deep commitment to greater private investment in the selected value chains. The fact that Ethiopia and Kenya are members of the regional Common Market for Eastern and Southern Africa (COMESA) and Mali and Ghana belong to the Economic Community of West African States (ECOWAS) allows for consideration of some regional issues. Table 1. Countries and Value Chains Selected for Analysis

Ethiopia

Kenya Ghana Mali

Livestock (Export) Rice Rice Livestock (Export)

Maize Maize Maize Rice

Horticulture Horticulture Horticulture Horticulture

4

Field interviews of agribusiness leaders and government officials in the four countries took place between December 2010 and January 2011. The specific objectives of the consultations were to explore the following:

Existing levels of private sector investments in the selected value chains; Policies and actions by governments, donors and development partners that

encouraged or discouraged private sector investment; and Lessons learned from successful efforts of promoting agribusiness investments, and

their possible relevance for other countries and value chains.

SUMMARY FINDINGS AND COMPARISONS In each of the four countries, the government played a key role in either assisting or constraining private investment in the identified value chains. By prioritizing investments in selected value chains, governments have the ability to focus public investments on key constraints impeding the expansion or efficiency of those value chains. Expanding irrigation facilities has been important for value chain development in all the countries, especially for horticulture exports in Ethiopia and rice production in Kenya, Mali, and Ghana, mainly for the domestic markets. Public sector research was also important in supporting growth and expansion of private investments, especially for the key staple crops, e.g., maize in Kenya and Ethiopia. Effective regulatory institutions helped private exporters comply with international sanitary and phyto-sanitary standards and facilitated trade relationships with competitive markets, e.g. the case of Mali’s mango exports, Kenya’s horticultural exports, and Ethiopia’s livestock/meat exports. However, in all four countries, lack of adequate roads and electricity continued to raise transaction costs of marketing the commodities and limit growth in the value chains in both export and domestic markets. Public investment in transport, availability and cost of electricity, water, telecommunications, and physical storage could significantly mitigate risks of private investment, and aid scaling up production. 1 This signals a dire need for sustained attention to critical infrastructure development and maintenance, and also an opportunity for public-private partnership in infrastructure investment. Access to land and tenure security emerged as a common constraint to increased private investment in all the countries, in some ways more important for domestic investors than for foreign investors, it would appear. Even smallholders who acquired rights to grow rice in government-managed schemes, as in Mali and Kenya, did not have adequate security to invest in maintaining the land at maximum productive capacity. Farmers who wanted to increase their holdings size had no clear path for doing so. Lack of transparency with government land allocation procedures and potential conflicts with traditional land rights was a barrier to scaling up large-scale operations to profitability levels, especially in processing operations. Rules and regulations for establishing out-growers schemes, contract farming or successful incorporation of smallholders into larger agribusiness

1 In Mali, the government made large investments in infrastructure in the rice value chain, which between 2002/3

and 2008/9, yielded a 132% increase in production.

5

operations were problematic. In Mali and Ghana, these institutional and organizational issues limited the success of the export horticulture value chains. Even with justifiable concern about land grabbing, current practices and institutional constraints hinder private investments in these value chains. All four countries compete for high-value horticultural products in European markets. Ethiopia has also oriented its high-value livestock/meat export value chain towards Middle Eastern markets. Non-African export markets are demanding in terms of quality, timing, and cost. In spite of the European market requirements becoming tougher, these export markets had potential for significant expansion. Both Mali (livestock/meat and rice) and Ethiopia (maize) also had opportunities for significant expansion into regional markets, although actions needed to increase the volume, improve the quality and reduce market transaction costs were absent. The rice value chains in Ghana and Kenya were oriented toward import substitution, effectively making local producers and private investors compete with the highly efficient rice value chains in Thailand, Vietnam, and Pakistan that already export into Ghana and Kenya. This poses a steep challenge to the nascent rice value chains in Ghana and Kenya and has engendered somewhat erratic policy decisions by governments struggling to protect local production. The maize value chain stories in Ghana and Ethiopia demonstrate the challenge of developing cost-efficient value chains by increasing farm-level productivity without, at the same time, building more robust, diversified market outlets. In both cases, greater private sector investment in post-harvest processing could respond to a variety of local demands, such as animal feed, brewery, other processed maize food products, and strengthen producer incentives to target production for those markets. Governments’ interventions in staple crop value chains tended to increase uncertainties for private investors at all levels, from production to marketing. The Kenya government’s attempt to simultaneously raise prices for producers while reducing prices for consumers is perhaps the most extreme example of mixed signals, but ad hoc price controls, export bans, and import tariffs are also common. Public sector interventions in export value chains, on the other hand, tended to be more supportive, but often incomplete or misdirected, leaving private investors and donors to fill gaps and provide additional assistance.2 A stronger engagement and institutionalized communication between the private and public sectors is needed in all of the countries. Where large amounts of capital or other investments, such as technology or know-how, are involved, the public and private sectors should partner to lower risks. Indeed,

2 The scope of the public sector intervention tends to differ as a result of a country’s development ideology and

public sector capacity. Ethiopia with its emphasis on priority export sectors provides technical and market-related

assistance as well as attractive investment incentives to actors within the priority sectors. Kenya, on the other hand,

tends to focus more on institutional arrangements, e.g. export processing zones and special economic zones, and the

business environment. Ghana, like Kenya, tends to emphasize Free Zones and the business environment – however,

its public sector tends to actively assist (through equity or the use of development banks) private sector operators

within key priority value chains. Mali’s comparatively weak public sector capacity on the other hand has left private

investors and development partners filling the gaps.

6

governments must walk a fine line between stimulating and encouraging the private sector to play a bigger role in the agricultural growth sector, and “crowding out” the private sector in countries like Kenya, where the private sector is more vibrant, willing and capable of doing more. Below are suggested key reforms, by country and value chain: Ethiopia Maize value chain:

a) Facilitate access to breeder’s seed including development of a supportive regulatory environment for private seed producers;

b) Facilitate investments in storage capacity at all levels through PPPs; and c) Encourage cross-border trade in cereals and the entry of institutional buyers

Livestock value chain:

a) Invest in strengthening pastoralist associations; b) Encourage entry of private sector service providers for veterinary services, animal

feed processing, etc.; c) Enlist the private sector assistance in disease surveillance; and d) Facilitate sector investments by promoting certifications and structural upgrading

through PPPs.

Horticulture value chain: a) Provide incentives to private sector ancillary service providers (graders, inspectors,

transport and packaging companies); b) Develop PPPs in human resources development programs; and c) Ease foreign exchange controls to facilitate international transactions.

Ghana: Maize value chain:

a) Facilitate varietal release protocols for maize seed and encourage private seed production;

b) Develop PPPs in transport, milling and storage infrastructure; and c) Streamline process for obtaining land rights, including those for aggregating land

holdings. Rice value chain:

a) Continue efforts to improve varietal releases and encourage private seed production; b) Encourage PPPs in irrigation, processing, etc.; and c) Streamline and facilitate process for aggregating land holdings.

Horticulture value chain

a) Continue efforts to improve varietal releases and encourage private seed production;

b) Encourage PPPs in transportation, pack-house development, and irrigation; and c) Streamline and facilitate process for aggregating land holdings.

7

Kenya: Maize sector:

a) Encourage investments in storage facilities at all levels; b) Develop aflotoxin testing capacity, including among private sector value chain

participants such as at the farmer association level and private trader level; and c) Build on Kenya’s regional orientation by promoting a structured East African grain

marketing system. Rice value chain:

a) Clarify and secure land tenure rights in government run rice schemes; b) Encourage PPPs in electricity and transport; and c) Build on Kenya’s regional orientation by promoting a structured East African grain

marketing system. Horticulture value chain:

a) Revise investment climate so as not to discriminate against foreign interests; b) Seek to establish PPPs in transport, communication and energy sectors; and c) Encourage direct air links with the U.S. and freighter competition to broaden

horticultural market reach. Mali: Rice value chain:

a) In irrigated areas, shift to a system where farmers pay for actual water use b) Seek to establish PPPs in milling/energy production c) Foster private sector entry in the input supply chain, including that of improved

seed production Livestock value chain:

a) Government to refrain from setting prices b) Encourage investments in transportation and cold storage infrastructure through

PPPs or other

Horticulture value chain: a) Assist the establishment of small holder farmer associations b) Assist farmer associations with extension services for mangoes and other crops

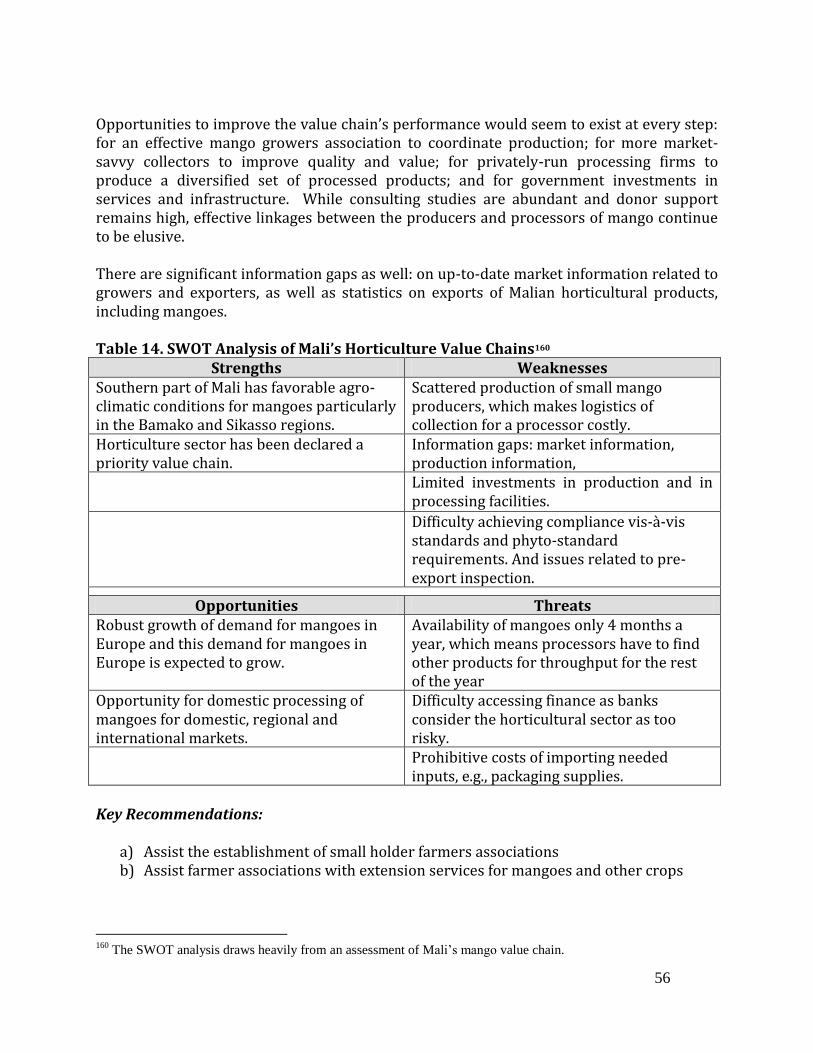

Below are the overriding themes and suggestions across value chains and countries: Setting priorities. Often with encouragement from donors and development partners, all countries’ governments have played a role in identifying and setting out plans to support selected value chains and priority sectors for development. This is also evident through on-going development of CAADP Investment Plans. Although “picking winners” is sometimes considered ineffective, all the governments have practiced this with evidence that it works, e.g., Kenya´s success in the horticulture value chain. Some private investors interviewed stated that without a clear government vision or strategy for development in a particular sector or value chain, the government is often unwilling to create the kind of

8

dynamic growth environment that private investors need. Another setback noted was that governments’ designation of “key” value chains made it difficult for some private investors to participate in agribusinesses supplying different markets, e.g., maize for animal feed production rather than supply of food, and firms that process mangoes that cannot be exported in the fresh markets. Incentives for private investors. In the past, governments have provided specific incentives to producers and processors to expand production, processing and marketing. This is most typical for export products. But for domestic markets, governments offered little support for market development. In some cases, governments provided mixed signals, e.g., pricing, in a way that discouraged investments. There was perception that foreign investors get more support than local investors, giving the former comparative advantage. Some local private investors believed that they were not trusted or respected by their governments, and the formation of business associations is one way to build their voice, influence and respect. Infrastructure. Governments must accept the responsibility to provide adequate infrastructure, particularly transport/roads and power. Lack of infrastructure limited agribusiness growth in all countries especially through uncertainty and high transactions costs. The specific infrastructure services identified as limiting varied by country. In Ghana, for example, the cost of electricity, the quality of the interior road network, and the adequacy of storage for cereals were cited as major constraints. In Ethiopia, however, the cost of transportation and the poor quality of telecommunication were the culprits. Further, all governments under-invested in irrigation development. Although all of them were taking steps to remedy that, forging public-private partnerships in supporting infrastructure development is crucial to making progress. Other countries have made great strides through developing transport corridors that entail scaling up other complementary infrastructure investments such as energy and water alongside these road networks. Land. The ability to acquire suitable land for production is a major constraint for agricultural investors, especially when developing larger farms is necessary to achieve economies of scale. Quite often, there are conflicting rules governing property rights (e.g. customary or tribal rights versus written laws or rights; and rural versus urban use) that make acquisition of land a time-consuming and costly. Some countries, such as Kenya, have restrictions on the ability of foreigners to own land. Leasing land to foreign or diaspora investors has become common, but is often non-transparent, confusing and having potential for long disputes and litigation. Uncertain land and land use rights greatly inhibit private investment. When other related services such as the provision of irrigation water are involved, negotiations become even more constrained and drawn out for timely investment decisions. Integrating smallholders into an agribusiness. The inability of smallholder farmers to organize themselves into efficient associations or groupings, or produce consistently quality products hinders the capacity of integrating them into larger operations. Many smallholders are even unfamiliar with requirements of agribusinesses. Contacts in Ethiopia and Mali indicated that one of the greatest difficulties was ensuring sufficient smallholder

9

production to supply to established food processors. The skill level among smallholders, as well as among technicians and managers along the value chain, were cited as insufficient to achieve desired value chain performance. Capacity building at all levels, from production to processing and marketing was a major need. Government participation. Government interventions in some value chains, especially those of staple foods, increased market uncertainties and risks, and thereby discouraged private investment. There were a range of opinions, both positive and negative, on whether governments should subsidize inputs such as seeds and fertilizer, maintain buffer stocks of inputs or commodities to stabilize prices, or participate in warehousing and storage. Examples of poorly-located warehousing or processing facilities were cited as evidence that public investment in such infrastructure was inadequately geared to market conditions and needs. Others cited direct government interventions, e.g., in seed production and distribution, as crowding out potential private investment. Finance. Financing was a major issue for some private investors. Some believed that public agricultural development banks could provide more financial resources, especially medium to long term capital. However, these public banks lacked the capacity to perform needed due diligence across the wide range of agricultural value chains. Moreover, their political orientation made them vulnerable to crony capitalism. This is one reason why private investors have had to turn to international Development Finance Institutions (DFIs) and other sources of patient capital to seek concessional financing for longer-term needs of agricultural development. Financing for smallholders and cooperatives are also important. However, the costs and risks associated with financing these actors discouraged the involvement of private sources of financing. Where agriculture was prioritized, acquiring financing for services not directly linked to agricultural production was hard. For example, pre-production financing and financing for transportation are critical but were often not supported, even when contracts had been signed. Under-developed staple crop value chains. All of the value chains oriented to domestic markets were under-developed. There were not adequately meeting national or regional demand, producing the range of consumer products desired, or minimizing market price volatility through effective storage and processing operations. In many ways, Mali’s rice value chain was the most developed, but issues of achieving economies of scale, regional market development, and greater productivity were identified by private investors as hampering the realization of potential. Staple crop markets were subject to political interventions that responded to short-term changes in the national food security situation, e.g., export bans, price controls, state-led imports, or the establishment of public buffer stocks. While understandable, these interventions raised the risks for private investors in these staple crop value chains and undermined the confidence of farmers in markets. In fact, some staple crop value chains were only marginally competitive with imports, e.g., rice in Ghana and Kenya and maize in Kenya. But many investors believed that, given the growing food demand, there were great opportunities to increase efficiencies and productivity through greater private investment in these value chains. However,

10

government support in the form of tax holidays or concessional financing for certain nascent agro-industries, albeit on a phase out basis, was essential for food production for the local market. Competitiveness. All of the export horticulture value chains organized faced stiff competition from exporters in other countries. Only East African horticultural producers had begun to orient themselves toward Middle Eastern markets (taking advantage of their geographic proximity), but all the countries continued to see Europe as their major market. This competitive forced producers, processors, and shippers to maintain high quality standards and expedited delivery schedules. Meat export value chains – beef from Mali, beef, sheep, and goat meat from Ethiopia – were not mainly focused on European markets. Mali’s products were targeting regional markets in West Africa while Ethiopia was targeting the Middle East. Health standards, cold chain maintenance, and variable markets (with much competition from other sources) all posed serious problems to the performance of these value chains. Governments’ role in promoting and constraining investments and competitiveness in the agribusiness sector extends from overall macroeconomic stewardship and investment promotion to specific government actions throughout the value chain.

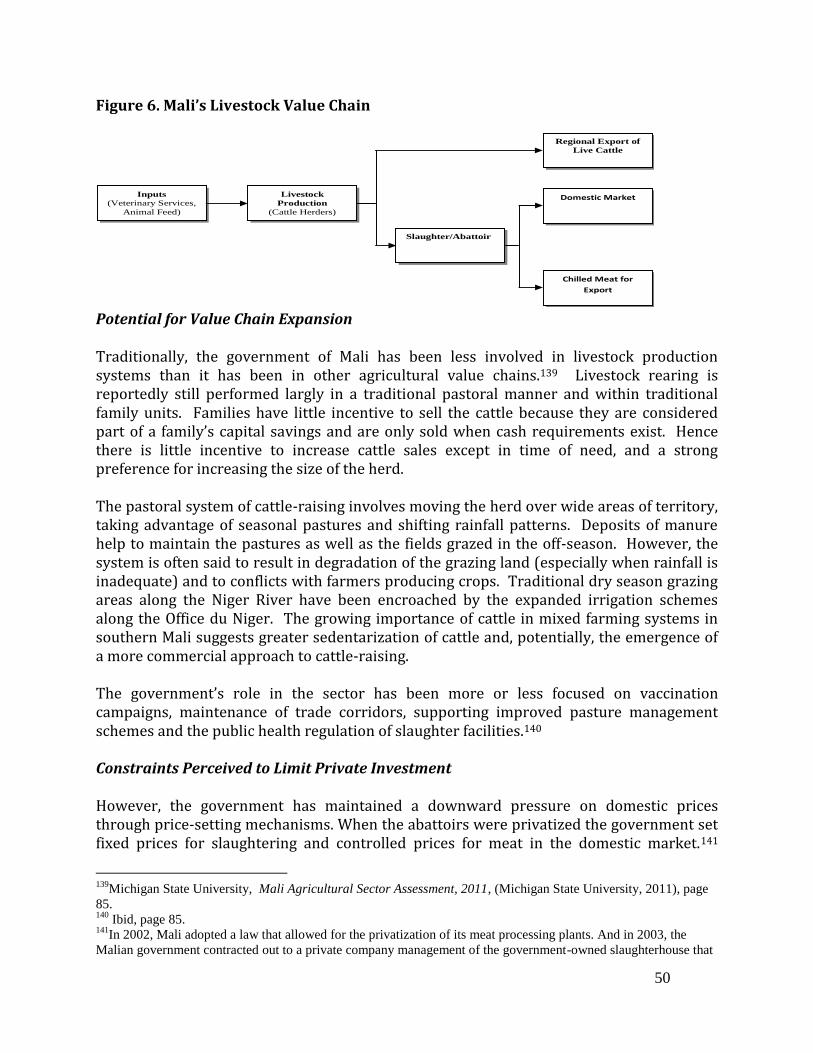

FINDINGS RELATING TO SPECIFIC VALUE CHAINS, BY COUNTRY In this section, we review briefly, by country: the current state of a key value chain; the potential for value chain expansion or growth; and the main constraints perceived to limit private sector investment in the value chain. We end with key recommendation(s).

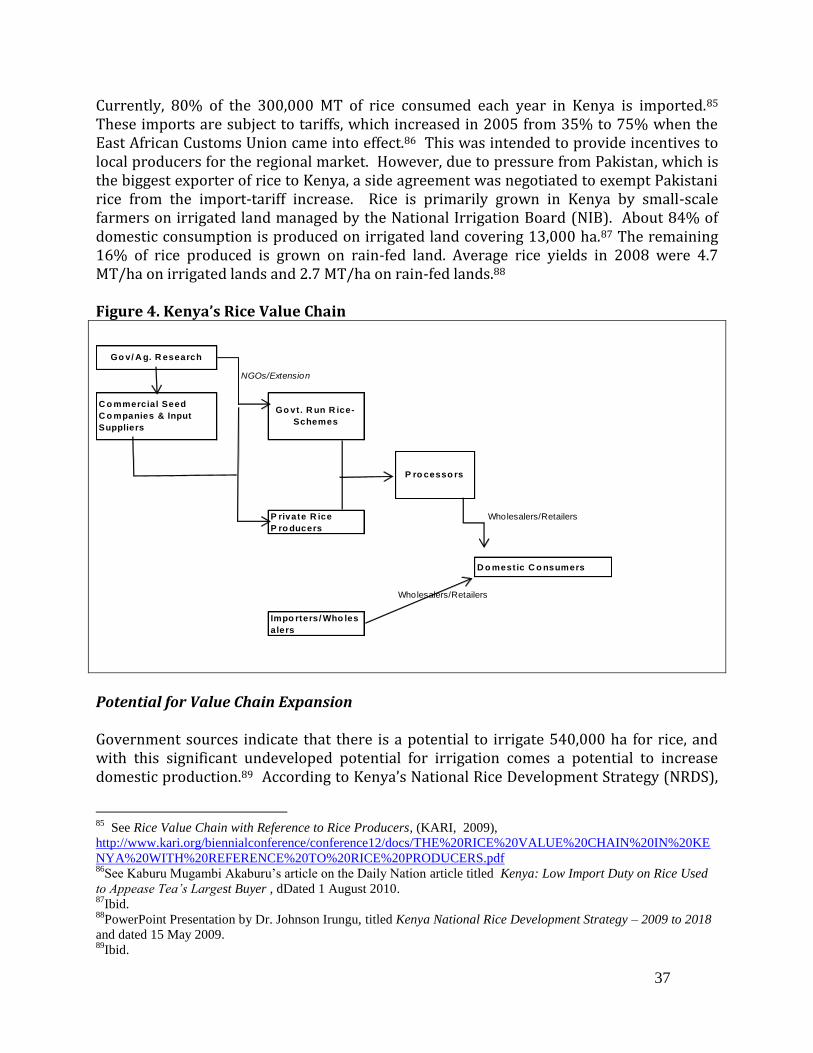

ETHIOPIA

MAIZE VALUE CHAIN Current Situation Maize is the most widely grown cereal crop in Ethiopia and has the highest current and potential yield from available inputs.3 An IFPRI diagnostic study of maize in Ethiopia indicated that a considerable yield gap still exists, however, and increases in maize productivity could help address the nation’s food security challenges. On-farm trial yields of maize resulted in yields of 4.7 tons/ha compared to the current average yield of 2.2 tons/ha.4

3 In 2008, Ethiopia was ranked third largest maize producer in Africa after South Africa and Nigeria, respectively.

The FAO estimates that in 2008, maize production in Ethiopia was 3.8 million metric tonnes. 4 Shahidur Rashid et al, Maize Value Chain Potential in Ethiopia - Constraints and Opportunities for Enhancing the

System, (IFPRI, 2010), page 2.

11

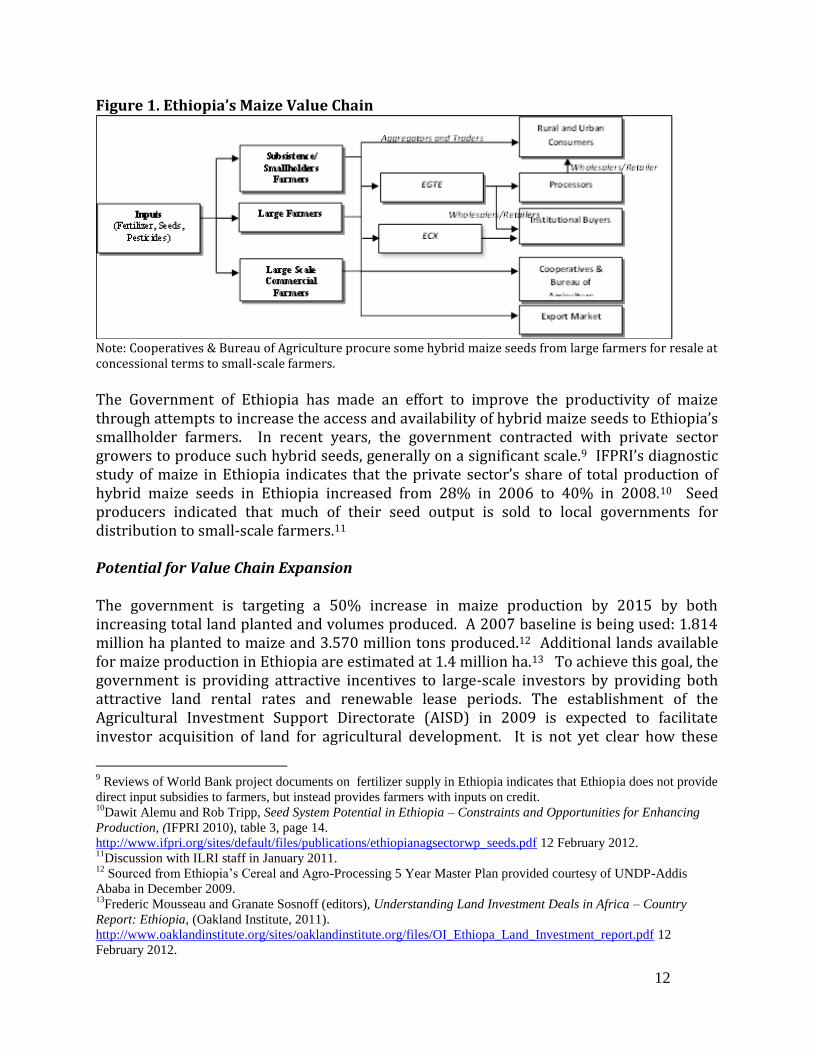

Maize production in Ethiopia is predominantly carried out by smallholders who produce for both home consumption and local markets.5 On average, these producers have access to small plots of land (between 2 ha and 5 ha), utilize very limited amounts of purchased inputs, and market approximately 20% of their produce at harvest.6 Land tenure security has been improved in recent years through a process of land certification, but there is no private market for farmland and acquisition of additional land is difficult. However, there is a relatively small number of maize farmers who operate farms between 50 ha and 500 ha in size. Some of the large farms specialize in the production of maize seeds for distribution to small-scale farmers by Ethiopia’s regional governments, and others produce maize for institutional buyers, processing companies, wholesale/retail markets in Ethiopia, and export. Recently, the Ethiopian government actively solicited the interest of large-scale private investors to produce a variety of crops, including maize.7 These investors are primarily foreign investors or members of the Ethiopian diaspora, and are encouraged, with a number of incentives, to develop large tracts of land in western Ethiopia (particularly in the regions of Gambella, western Oromia and Benishangul Gumuz). Figure 1 provides a schematic of Ethiopia’s maize value chain and shows a diversity of buyers. In terms of volume, rural and urban consumers account for the vast majority of buyers. Maize, a comparatively low cost source of calories and protein,8 is the food of poor consumers. The World Food Program (WFP) is an institutional buyer of the commodity for distribution through food assistance programs.

5Shahidur Rashid et al indicate that approximately 8 million holders grow maize in Ethiopia, compared to 5.8

million for teff and 4.2 million for wheat. Moreover, their study indicates that subsistence farmers grow maize on

plots that average 2ha and market-oriented smallholders grow maize on plots that average 5ha. Source: Shahidur

Rashid et al, Maize Value Chain Potential in Ethiopia – Constraints and Opportunities for Enhancing the System

(IFPRI, 2010), page 2. 6 Ibid, page 16.

7 One of these companies is Karuturi Global, which is growing primarily maize on land over 20,000ha around Bako,

Oromia in Ethiopia. In addition, Karuturi plans to grow maize among other crops in its large Gambella land holding. 8 Shahidur Rashid et al estimate that maize provides 1.5 times and 2 times the calories per dollar of teff and wheat,

respectively. Source: Shahidur Rashid et al, Maize Value Chain Potential in Ethiopia – Constraints and

Opportunities for Enhancing the System, (IFPRI, 2010), page 2.

12

Figure 1. Ethiopia’s Maize Value Chain

Note: Cooperatives & Bureau of Agriculture procure some hybrid maize seeds from large farmers for resale at concessional terms to small-scale farmers.

The Government of Ethiopia has made an effort to improve the productivity of maize through attempts to increase the access and availability of hybrid maize seeds to Ethiopia’s smallholder farmers. In recent years, the government contracted with private sector growers to produce such hybrid seeds, generally on a significant scale.9 IFPRI’s diagnostic study of maize in Ethiopia indicates that the private sector’s share of total production of hybrid maize seeds in Ethiopia increased from 28% in 2006 to 40% in 2008.10 Seed producers indicated that much of their seed output is sold to local governments for distribution to small-scale farmers.11 Potential for Value Chain Expansion The government is targeting a 50% increase in maize production by 2015 by both increasing total land planted and volumes produced. A 2007 baseline is being used: 1.814 million ha planted to maize and 3.570 million tons produced.12 Additional lands available for maize production in Ethiopia are estimated at 1.4 million ha.13 To achieve this goal, the government is providing attractive incentives to large-scale investors by providing both attractive land rental rates and renewable lease periods. The establishment of the Agricultural Investment Support Directorate (AISD) in 2009 is expected to facilitate investor acquisition of land for agricultural development. It is not yet clear how these

9 Reviews of World Bank project documents on fertilizer supply in Ethiopia indicates that Ethiopia does not provide

direct input subsidies to farmers, but instead provides farmers with inputs on credit. 10

Dawit Alemu and Rob Tripp, Seed System Potential in Ethiopia – Constraints and Opportunities for Enhancing

Production, (IFPRI 2010), table 3, page 14.

http://www.ifpri.org/sites/default/files/publications/ethiopianagsectorwp_seeds.pdf 12 February 2012. 11

Discussion with ILRI staff in January 2011. 12

Sourced from Ethiopia’s Cereal and Agro-Processing 5 Year Master Plan provided courtesy of UNDP-Addis

Ababa in December 2009. 13

Frederic Mousseau and Granate Sosnoff (editors), Understanding Land Investment Deals in Africa – Country

Report: Ethiopia, (Oakland Institute, 2011).

http://www.oaklandinstitute.org/sites/oaklandinstitute.org/files/OI_Ethiopa_Land_Investment_report.pdf 12

February 2012.

13

incentives will promote the growth of smaller-scale commercial maize production by Ethiopian farmers, or how they might be encompassed in the larger agro-industrial schemes. The government’s efforts to encourage private sector participation in the production and distribution of hybrid maize seeds have already resulted in a number of large private farms competitively producing hybrid maize in Ethiopia. However, private sector operators noted their lack of adequate access to breeder seeds, the difficult regulatory framework governing production and sale of improved seeds, and the difficulties they face in accessing commercial financing.14 All agreed that there is still a need for an improved maize seed system which effectively supports private sector participation and appropriate regulation by the government. The Ethiopian government continues to encourage the entry of large institutional buyers such as the World Food Program (WFP) into the Ethiopian maize market, and specifically that such purchases take place through the recently-established Ethiopian Commodity Exchange (ECX). Despite this, recent government interventions in the national maize market, such as banning cereal exports and instituting price controls on cereals, including maize, create disincentives to scaled-up “commercial” production and diminish the government’s credibility in effectively formalizing the market. Donors and development partners appear engaged in strengthening maize value chains, with the bulk of donor attention supporting public interventions to increase smallholder yields and improve market coordination. There is less emphasis placed on supporting and enhancing private sector participation throughout the value chain, and expanding the size of the market for greater development of the maize sector.

Contacts also indicated that there is significant demand for commercially produced maize as feed for Ethiopia’s livestock industry (particularly poultry), but current volumes going to this market appeared to be low. As Ethiopia’s urban populations grow and incomes rise and increase demands for animal-sourced foods, there appear to be new outlets for maize producers in Ethiopia’s poultry and animal feed agribusinesses. In addition, it was reported that there is opportunity for increased regional trade within COMESA. It was suggested that maize exports to countries such as Kenya and Sudan could be expanded. Help from development organizations working within Ethiopia and neighboring countries could contribute to developing mechanisms that would enable cross-border trade in maize to grow. Constraints Limiting Private Investment Maize production is usually small-scale and of subsistence nature, and markets are typically local and are not well integrated across the country. The lack of a fully integrated

14

Dawit Alemu and Rob Tripp, Seed System Potential in Ethiopia – Constraints and Opportunities for Enhancing

Production, (IFPRI 2010), table 3, page 14.

14

maize market in Ethiopia has resulted in significant price volatility (with intra-annual price swings up to 40- 50%). Partly due to the lack of proper storage, most trading activity is conducted within three to four months after harvest and is not consistently available in markets. In addition, Ethiopian consumers with greater disposable income often prefer teff and wheat, which has put maize in the position of a non-preferred, low-price commodity. Trade of maize has only a few large buyers and limited maize processing activities (for food) in Ethiopia. The fragmentation of farms in Ethiopia and the limited use of modern inputs mean that relatively small volumes of grain are produced and even smaller amounts are marketed. The market is dominated by a series of traders or aggregators who work along the maize value chain, trading in small volumes of maize without the ability to effectively store maize. This augments the levels of risks and costs associated with marketed maize. The lack of appropriate storage facilities has reportedly resulted in high-post harvest losses of about 15-30%. 15 The Ethiopian government has experienced significant difficulty instituting transparent market interventions that reinforce farmer’s confidence in the market. The Ethiopian Grain Trade Enterprise (EGTE) was established by the government to lead price stabilization, but it has been criticized in its handling of past supply shocks by (1) not instituting a clearly defined price floor (in 2001/2), and (2) intervening on an ad hoc basis, rather than on a transparent and predictable basis.16 EGTE has also been responsible for instituting price controls and export bans, adding further uncertainty to maize markets in the country. Limited urban demand for maize and the underdeveloped maize agro-processing sector has meant that the servicing of the animal feed sector with crushed maize or byproducts from maize processing for food has been limited. While the Ministry of Agriculture has placed significant emphasis on expanding extension services and has programs to provide improved seed and fertilizer for maize production, input supply (and credit) has been irregular. Private sector involvement in input supply has been limited. There have, however, been recent efforts to encourage private sector participation in input supply (e.g., hybrid seeds and livestock semen). The new Agriculture Transformation Agency also envisions the clarification of public and private roles in input supplies as is evident in the recently released “5 Year Roadmap toward Vision for the Seed Sector”.

15

Shahidur Rashid et al, Maize Value Chain Potential in Ethiopia – Constraints and Opportunities for Enhancing the

System, (IFPRI, 2010), page 2. 16

Ibid.

15

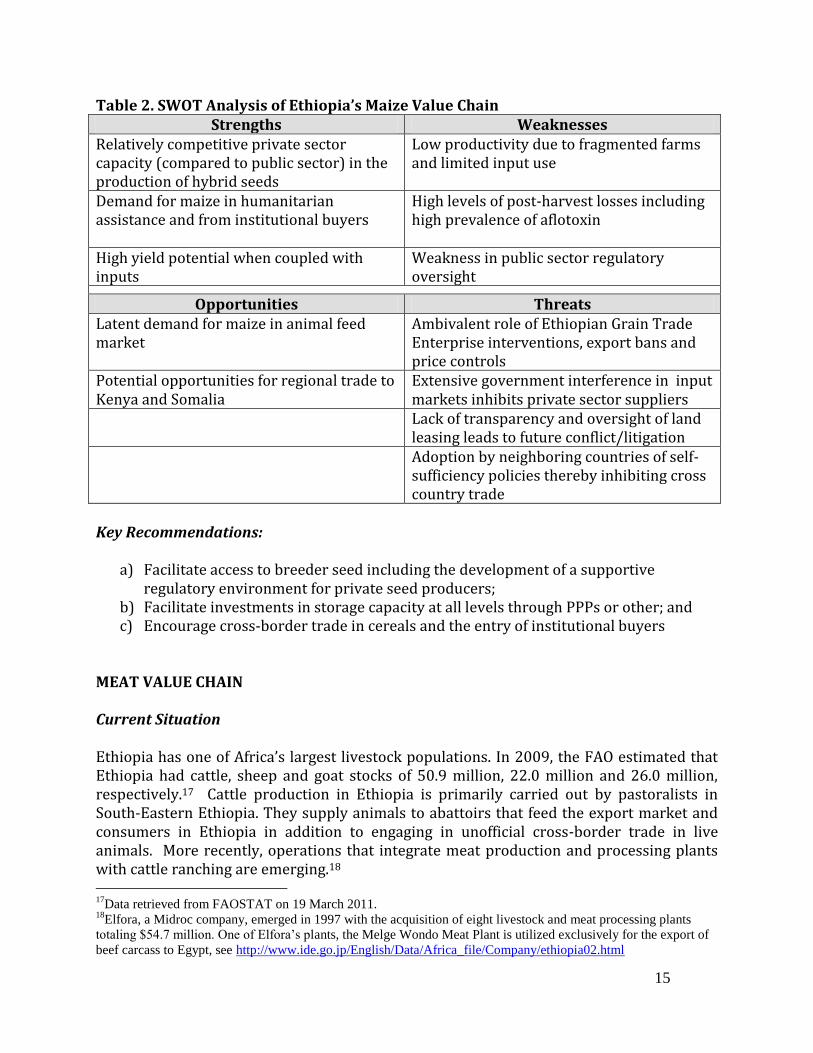

Table 2. SWOT Analysis of Ethiopia’s Maize Value Chain Strengths Weaknesses

Relatively competitive private sector capacity (compared to public sector) in the production of hybrid seeds

Low productivity due to fragmented farms and limited input use

Demand for maize in humanitarian assistance and from institutional buyers

High levels of post-harvest losses including high prevalence of aflotoxin

High yield potential when coupled with inputs

Weakness in public sector regulatory oversight

Opportunities Threats Latent demand for maize in animal feed market

Ambivalent role of Ethiopian Grain Trade Enterprise interventions, export bans and price controls

Potential opportunities for regional trade to Kenya and Somalia

Extensive government interference in input markets inhibits private sector suppliers

Lack of transparency and oversight of land leasing leads to future conflict/litigation

Adoption by neighboring countries of self-sufficiency policies thereby inhibiting cross country trade

Key Recommendations:

a) Facilitate access to breeder seed including the development of a supportive regulatory environment for private seed producers;

b) Facilitate investments in storage capacity at all levels through PPPs or other; and c) Encourage cross-border trade in cereals and the entry of institutional buyers

MEAT VALUE CHAIN Current Situation Ethiopia has one of Africa’s largest livestock populations. In 2009, the FAO estimated that Ethiopia had cattle, sheep and goat stocks of 50.9 million, 22.0 million and 26.0 million, respectively.17 Cattle production in Ethiopia is primarily carried out by pastoralists in South-Eastern Ethiopia. They supply animals to abattoirs that feed the export market and consumers in Ethiopia in addition to engaging in unofficial cross-border trade in live animals. More recently, operations that integrate meat production and processing plants with cattle ranching are emerging.18 17

Data retrieved from FAOSTAT on 19 March 2011. 18

Elfora, a Midroc company, emerged in 1997 with the acquisition of eight livestock and meat processing plants

totaling $54.7 million. One of Elfora’s plants, the Melge Wondo Meat Plant is utilized exclusively for the export of

beef carcass to Egypt, see http://www.ide.go.jp/English/Data/Africa_file/Company/ethiopia02.html

16

Overall, Ethiopia is well located geographically in order to meet the demands of the very large animal and animal product importers in the Middle East and North Africa (MENA) region. The United Arab Emirates and Saudi Arabia are currently Ethiopia’s top two meat export destinations. These two countries alone imported $294.6 million worth of cattle, sheep and goat meat in 2008. Across the MENA region, beef imports in 2009 and 2010 were estimated at 1 million tons and 1.3 million tons, respectively.19 The Potential for Value Chain Expansion The Ethiopian government designated meat exports as a high priority for growth, due to the size of the livestock resource base and the majority of the rural population relying on livestock for their livelihoods. The creation of a Livestock Development Master Plan Study is intended to guide this development. To date, the government has collected and inventoried sector-wide data and is currently contracting services for the development of a livestock investment master-plan that covers the next twenty years.20 Bankable livestock value chain investment projects are to receive attractive tax incentives, priority land access, and attractive financing terms from the Development Bank of Ethiopia. Exporters, including livestock and meat exporters, are generally provided with the following tax incentives:

a 100% exemption from import customs duty and other taxes levied on the importation of raw materials. Taxes and duties paid on raw materials and packaging materials are drawn back at the time of export of finished goods;

the exemption of income tax on income derived from a new approved investment for two to eight years, depending on the area of investment, volume of export and the location in which the investment is undertaken;

the exemption of income tax on income derived from expansion or upgrading an existing manufacturing, agro-industrial or agricultural enterprise for a period of two years if it exports at least 50% of its products and increases, in value, its production by 25%;

ability of business enterprises that suffer losses during the tax holiday period to carry forward such losses for half of the income tax exemption period, after the expiry of such period; and

foreign investors are entitled to make remittances out of Ethiopia in convertible currency at the prevailing rate of exchange on the date of remittance.

To monitor progress toward established agricultural export goals, including the goal of increased live animal and processed meat exports, a National Export Committee chaired by

19

See news article http://www.thebeefsite.com/news/33038/middle-east-north-africa-beef-imports-to-grow 20

Request for Expression of Interest – The Federal Democratic Republic of Ethiopia Ministry of Agriculture and

Rural Development Livestock Development Master Plan Study, African Development Bank, 2009,

http://www.afdb.org/fileadmin/uploads/afdb/Documents/Project-related-

Procurement/EOIEthiopiaLivestock%20%2012-09.pdf 8 April 2011

17

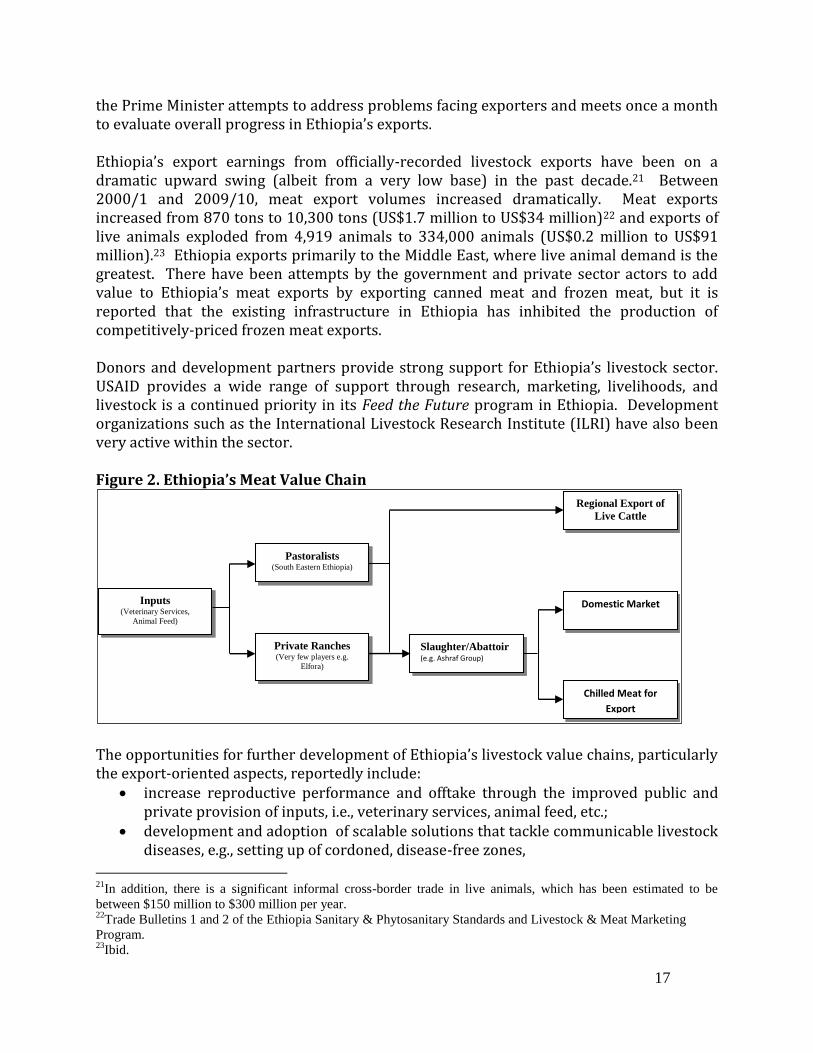

the Prime Minister attempts to address problems facing exporters and meets once a month to evaluate overall progress in Ethiopia’s exports. Ethiopia’s export earnings from officially-recorded livestock exports have been on a dramatic upward swing (albeit from a very low base) in the past decade.21 Between 2000/1 and 2009/10, meat export volumes increased dramatically. Meat exports increased from 870 tons to 10,300 tons (US$1.7 million to US$34 million)22 and exports of live animals exploded from 4,919 animals to 334,000 animals (US$0.2 million to US$91 million).23 Ethiopia exports primarily to the Middle East, where live animal demand is the greatest. There have been attempts by the government and private sector actors to add value to Ethiopia’s meat exports by exporting canned meat and frozen meat, but it is reported that the existing infrastructure in Ethiopia has inhibited the production of competitively-priced frozen meat exports. Donors and development partners provide strong support for Ethiopia’s livestock sector. USAID provides a wide range of support through research, marketing, livelihoods, and livestock is a continued priority in its Feed the Future program in Ethiopia. Development organizations such as the International Livestock Research Institute (ILRI) have also been very active within the sector. Figure 2. Ethiopia’s Meat Value Chain

The opportunities for further development of Ethiopia’s livestock value chains, particularly the export-oriented aspects, reportedly include:

increase reproductive performance and offtake through the improved public and private provision of inputs, i.e., veterinary services, animal feed, etc.;

development and adoption of scalable solutions that tackle communicable livestock diseases, e.g., setting up of cordoned, disease-free zones,

21

In addition, there is a significant informal cross-border trade in live animals, which has been estimated to be

between $150 million to $300 million per year. 22

Trade Bulletins 1 and 2 of the Ethiopia Sanitary & Phytosanitary Standards and Livestock & Meat Marketing

Program. 23

Ibid.

Inputs (Veterinary Services,

Animal Feed)

Chilled Meat for

Export

Domestic Market

Regional Export of

Live Cattle

e.g. Middle East

Slaughter/Abattoir (e.g. Ashraf Group)

Private Ranches (Very few players e.g.

Elfora)

Pastoralists (South Eastern Ethiopia)

18

increase the organization, communication, and trust among various actors in the value chains, and

upgrade logistical infrastructures to enable private sector actors to compete more effectively in higher-value export markets, perhaps through public-private partnerships with the Ethiopian government.

Constraints Limiting Private Investment A diagnostic study of Ethiopia’s live cattle value chain indicated that input constraints (feed and water) and limited access to appropriate health services are primarily responsible for the currently- low reproductive performance of animals. 24 The lack of publicly-provided animal health care services and disease surveillance by the Ministry of Agriculture has reportedly dramatically impacted exports. The low provision of vaccinations and treatments to cattle and the limited capacity to administer national-level disease surveillance in Ethiopia’s livestock have led to outbreaks of common diseases in the region, e.g., Rift Valley fever or foot and mouth disease. These strongly affect the potential of Ethiopian animals to enter into international trade. Outbreaks in recent years resulted in blanket bans being imposed on Ethiopia’s key exports by buyers in the United Arab Emirates (UAE) and Saudi Arabia, for example, during the period January to September 2007 and from the first week of March to the first week of May 2009.25 There is some question whether these bans were imposed for reasons of health and food safety, as asserted, or whether they were motivated by political or other market reasons26. Despite some setbacks, the government has taken steps to establish Disease Free Zones (DFZs) of around 125,000 square km in Ethiopia’s cattle-producing areas of Afar, Borena and Ogaden. These will be demarcated in order to monitor livestock and necessary disease surveillance. DFZs will be complemented by designated Export Zones, where certain areas are declared free of certain diseases and measures are in place to satisfy the requirements of a particular importing country, and will administer a system of examination and certification of livestock for export. Pastoralists’ cultural attitudes toward commercialization of cattle are also believed to constrain supply chain development. Short-term thinking, lack of organization at the pastoralist level, and high-levels of mistrust among value-chain actors have hindered coordination of efforts to increase value in the animal/meat supply chains. Abattoir owners mentioned, for example, that pastoralists attempt to increase the weight of their cattle by providing them with significant water prior to sale. The government has identified support to pastoral cooperatives as a way to help improve coordination and collaboration between the export-oriented abattoirs and cattle-producers in Ethiopia.

24

See Diagnostic Study of Live Cattle and Beef Production and Marketing – Constraints and Opportunities for

Enhancing the System (ILRI, 2010) 25

See page 2 of Trade Bulletin 1of Ethiopia Sanitary & Phytosanitary Standards and Livestock & Meat Marketing

Program 26

Based on discussion with sector expert Dr. Wondwossen of SPS-LMM

19

Issues regarding the location, design and capacity of the abattoirs27 processing meat for export also emerged as undermining Ethiopia’s competitive position in chilled/frozen meat exports. Only two abattoirs in Ethiopia were identified as modern, large and well-designed: the Abergele International Livestock Development Plc. (AILD PLC) in Mekelle and Ashraf Group’s in Bahir Dar. However, these abattoirs are not located where the livestock are produced for export, i.e., in South-East Ethiopia. Two other abattoirs, Luna Export and Mojo, are better suited for export processing due to their more central location, but they are inadequate in size and in need of capital investments to improve design. Further infrastructure constraints noted surrounded logistical capacity (trucks, cold storage, etc.). Some contacts believed that these areas need significant upgrades and investment before the country is able to competitively export, especially perishable (chilled/frozen) meat products. Presently, some processors believe that Ethiopia is only competitive in air-freighting chilled sheep/lamb by air to the Middle East. Infrastructure investments might be most usefully prioritized through closer consultation between public and private actors in the value chain, or through public-private partnerships (PPPs) which would reduce risks for the private sector while mobilizing additional public support. One such example is a USAID-supported project that is working together with the Ethiopian government and Ethiopian Meat Producer and Exporters Association (EMPEA) to develop cold-storage logistical solutions to enable Ethiopia to competitively market, produce and export beef and other perishable meat products by sea. However, there are questions around the Development Bank of Ethiopia’s capacity to effectively determine bankable projects when providing loans to this sector, as evidenced by the investments in poorly-located abattoirs.

27

Abattoir design is critical for meat quality and there are only two large, well-designed, modern abattoirs in

Ethiopia; these are Abergele in Tigray region, which is owned by EFFORT and Ashrafe in Amhara region, which is

owned by a private Sudanese investor

20

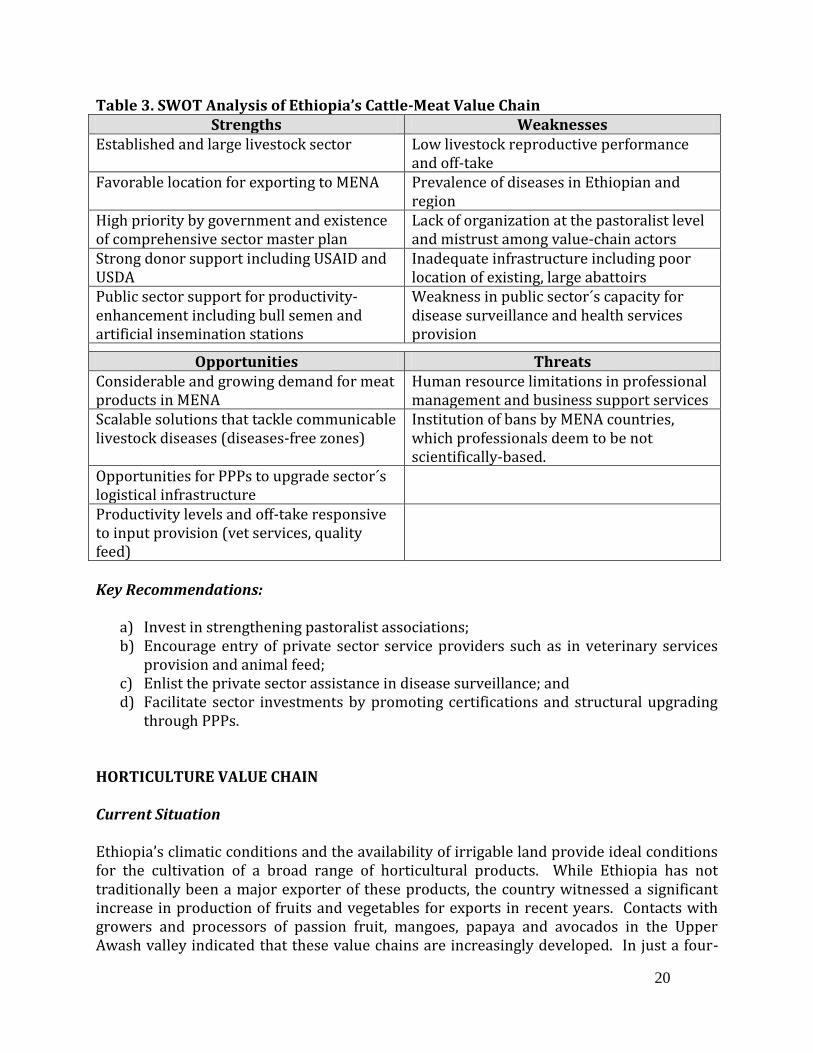

Table 3. SWOT Analysis of Ethiopia’s Cattle-Meat Value Chain Strengths Weaknesses

Established and large livestock sector Low livestock reproductive performance and off-take

Favorable location for exporting to MENA Prevalence of diseases in Ethiopian and region

High priority by government and existence of comprehensive sector master plan

Lack of organization at the pastoralist level and mistrust among value-chain actors

Strong donor support including USAID and USDA

Inadequate infrastructure including poor location of existing, large abattoirs

Public sector support for productivity-enhancement including bull semen and artificial insemination stations

Weakness in public sector´s capacity for disease surveillance and health services provision

Opportunities Threats Considerable and growing demand for meat products in MENA

Human resource limitations in professional management and business support services

Scalable solutions that tackle communicable livestock diseases (diseases-free zones)

Institution of bans by MENA countries, which professionals deem to be not scientifically-based.

Opportunities for PPPs to upgrade sector´s logistical infrastructure

Productivity levels and off-take responsive to input provision (vet services, quality feed)

Key Recommendations:

a) Invest in strengthening pastoralist associations; b) Encourage entry of private sector service providers such as in veterinary services

provision and animal feed; c) Enlist the private sector assistance in disease surveillance; and d) Facilitate sector investments by promoting certifications and structural upgrading

through PPPs. HORTICULTURE VALUE CHAIN Current Situation Ethiopia’s climatic conditions and the availability of irrigable land provide ideal conditions for the cultivation of a broad range of horticultural products. While Ethiopia has not traditionally been a major exporter of these products, the country witnessed a significant increase in production of fruits and vegetables for exports in recent years. Contacts with growers and processors of passion fruit, mangoes, papaya and avocados in the Upper Awash valley indicated that these value chains are increasingly developed. In just a four-

21

year period, starting in 2005, horticultural exports increased as a share of Ethiopia’s agricultural exports from 3% to 12%.28 The Ethiopian government has taken the lead in identifying Ethiopia’s horticulture sector as a priority export sector and supporting its growth. Bankable investment projects in horticultural production for export are provided attractive tax incentives, priority in land access, and attractive financing terms from the Development Bank of Ethiopia. In addition, the recently-created Horticultural Development Agency, an autonomous agency within the Ministry of Agriculture, is mandated to ensure the sector’s fast and sustainable growth. The government has also played a central role in shaping the sector’s development by identifying the main crops and setting targets around the total land to be allocated. In the 2005/6 to 2009/10 five-year plan, a total of 3,000 ha of land were allocated for fruits and vegetables. Mangoes, avocados, bananas, pineapples, apples and vegetables (such as green beans, tomatoes and zucchini) were deemed priority crops.29 In the 5-year period from 2010/11 to 2014/15, the government intends to bring a total of 15,000 ha allocated to fruit and vegetables for export. The government is also attempting to mitigate skill-deficiencies in the labor market by establishing centers for technical training such as the Horticulture Practical Training Center (HPTC) and clustering development in certain geographical zones.

Potential for Value Chain Expansion Ethiopia offers competitive advantages in supplying horticultural products to Europe and the Middle East. This is supported in part by a well-developed air transport system out of Addis Ababa, where Ethiopian Airlines is constructing a new perishable cargo center at the airport. There are also plans to develop a larger, central facility for sorting, grading, packaging, pre-cooling, and storage. Timing of production seasons in Ethiopia is also advantageous. Vegetables for export in Ethiopia are mainly harvested from September/October to March, which coincides with winter in Europe. Moreover, Ethiopia’s geographic proximity to the Middle East and Gulf markets provides an advantage, as there is significant demand for fresh horticultural products in those markets. The head of the Ethiopian Investment Agency underscored the abundant, trainable labor-force in Ethiopia as well as the efforts by the Ethiopian government to ramp up Ethiopia’s infrastructure (electricity, roads, and water) in support of Ethiopia’s ambitious growth plan. A genuine effort by government to attract private sector investments into any export-oriented horticultural production is widely perceived. In addition to production, there are thought to be opportunities for public-private partnerships in the horticultural sector to: (1) upgrade needed infrastructures (e.g., cold storage facilities) and (2) promote sector-wide best practices that would improve the conduciveness for investment and improve the marketability of the Ethiopian brand. Anecdotal evidence suggests that private sector

28

Tsegay Lubelu, Ethiopian National Position Paper - (Ethiopian Horticulture Development Agency, 2010),

http://www.globalhort.org/media/uploads/File/Video%20Conferences/VC4_Position%20Paper%20Ethiopia2.pdf 29

Frank Joosten, Development Strategy for the Export-Oriented Horticulture in Ethiopia,(Wageningen Ur, 2007),

http://library.wur.nl/way/bestanden/clc/1891396.pdf

22

investors in Ethiopia’s horticulture sector are inhibited by continued experiences of delays in acquiring land leases and difficulties in negotiating the length of the lease period. In addition, government efforts to discourage speculation on land by repossessing uncultivated land have been deemed by some private sector investors as problematic. Constraints Limiting Private Investment Many of the foreign investors in Ethiopia’s export-oriented30 horticulture sector have criticized Ethiopia’s tight foreign exchange regime and limitations on the participation of foreign banks as it makes international transactions and transfers cumbersome, and curtail the repatriation of foreign exchange earned on exports. Institution of policies that would increase foreign participation in the banking and telecommunication sectors has been met with stiff resistance by policy makers. In addition, there are several concerns around the absence of trained workers in the labor market, as well as shortages on the logistical side such as the transfer, storage, and inspection of goods. Across the horticultural value chain, there is a lack of well-trained individuals and business service providers. As a result, a significant number of enterprises bring in their skilled manpower from abroad, particularly, Kenya and India. For example, AFRICAJuice brought processing-line engineers from India because the skilled personnel were not available in Ethiopia. Local packing supplies that meet international standards are lacking, and there are a limited number of appropriate cold storage facilities in Ethiopia. There is a lack of adequate pesticide regulation and weak phyto-sanitary inspection being provided by the government. These hurt the “Ethiopian” brand name overseas. Effectively marketing horticultural products in the highly competitive international market requires an ability by producers to respond quickly to changes. This ability to respond by Ethiopian horticultural producers is severely constrained by (i) the skill levels across the value chain and (ii) a weak telecommunication infrastructure.

30

Our interviews highlighted that export-oriented horticulture and floriculture in Ethiopia incorporated a greater

number of established foreign investors as compared to other agricultural value chains. There are, however, such as

Karuturi and Midroc Group that have been involved in the horticulture sector and are expanding into other

agricultural value chains.

23

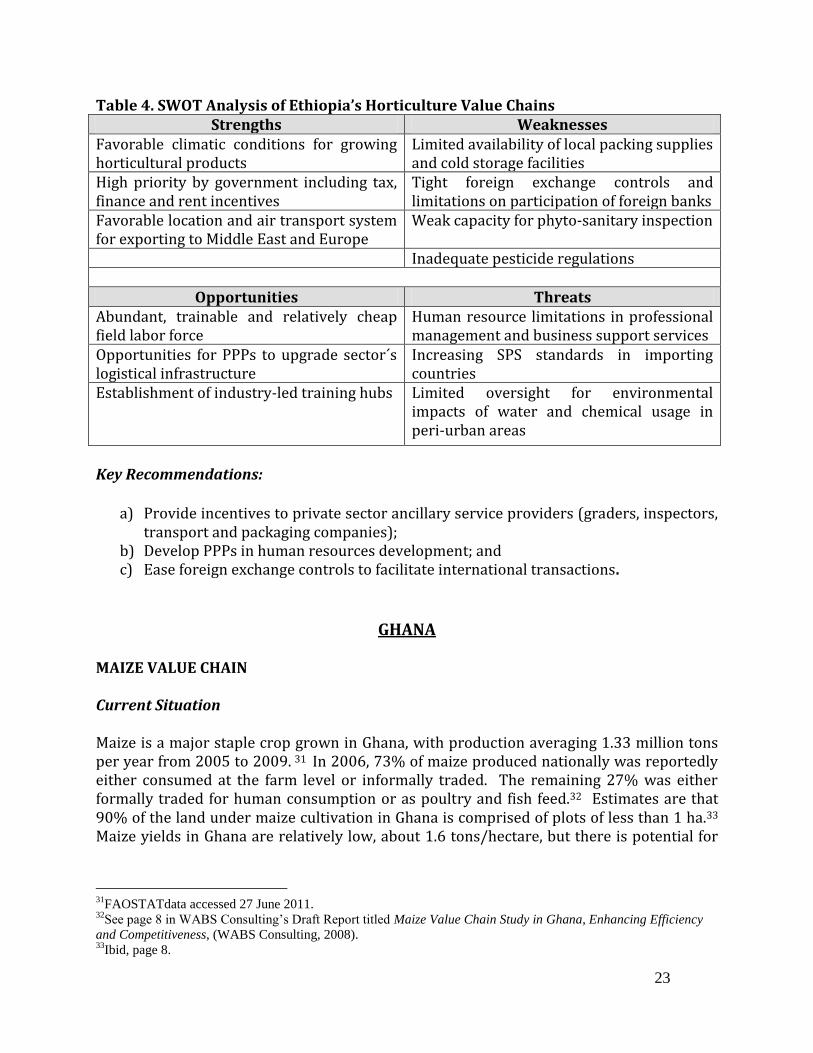

Table 4. SWOT Analysis of Ethiopia’s Horticulture Value Chains Strengths Weaknesses

Favorable climatic conditions for growing horticultural products

Limited availability of local packing supplies and cold storage facilities

High priority by government including tax, finance and rent incentives

Tight foreign exchange controls and limitations on participation of foreign banks

Favorable location and air transport system for exporting to Middle East and Europe

Weak capacity for phyto-sanitary inspection

Inadequate pesticide regulations

Opportunities Threats Abundant, trainable and relatively cheap field labor force

Human resource limitations in professional management and business support services

Opportunities for PPPs to upgrade sector´s logistical infrastructure

Increasing SPS standards in importing countries

Establishment of industry-led training hubs Limited oversight for environmental impacts of water and chemical usage in peri-urban areas

Key Recommendations:

a) Provide incentives to private sector ancillary service providers (graders, inspectors, transport and packaging companies);

b) Develop PPPs in human resources development; and c) Ease foreign exchange controls to facilitate international transactions.

GHANA MAIZE VALUE CHAIN Current Situation

Maize is a major staple crop grown in Ghana, with production averaging 1.33 million tons per year from 2005 to 2009. 31 In 2006, 73% of maize produced nationally was reportedly either consumed at the farm level or informally traded. The remaining 27% was either formally traded for human consumption or as poultry and fish feed.32 Estimates are that 90% of the land under maize cultivation in Ghana is comprised of plots of less than 1 ha.33 Maize yields in Ghana are relatively low, about 1.6 tons/hectare, but there is potential for

31

FAOSTATdata accessed 27 June 2011. 32

See page 8 in WABS Consulting’s Draft Report titled Maize Value Chain Study in Ghana, Enhancing Efficiency

and Competitiveness, (WABS Consulting, 2008). 33

Ibid, page 8.

24

increased productivity, with yields of over 8 tons/hectare recorded in demonstration farms.34 Maize farming in Ghana today is perceived to be inefficient and uncompetitive.35 Small farm sizes are believed to pose significant obstacles to increasing needed investments in agricultural inputs; conflicting regulations over land rights make it difficult to scale up farm sizes. Moreover, aggregating production from the various small-scale producers augments the transaction costs of getting the maize to market. Size is not the only barrier to competitiveness, however, as even large, commercially-oriented maize farms in Ghana find it hard to compete with imported maize. Ghana’s largest maize farm, Ejura Farms, which produces on over 14,000 acres36 (~5,665 ha), has found itself unable to meet import prices, in part because of the high costs of imported production inputs, but also because agricultural subsidies for maize farmers elsewhere (as in the U.S.) enable low-price exports.37 Despite this outlook, the government is actively supporting private investors to establish large-scale farms in order to increase food production and contribute to food security. In 2009, for example, Kwanim Ghana Denmark (GDK) Farm, a joint Ghanaian-Danish private investment, was established on 22,000 ha, with active support from the Ghanaian government, for the purpose of cultivating maize and soybeans.38 Potential for Value Chain Expansion In general, experts believe it is possible for Ghana’s farmers to more than double yields from the national average levels by improving farming practices and utilizing higher-yielding varieties. Whether this increased productivity will translate into a reduction in farm acreage planted to maize (with the released land devoted to other crops) or to an expanded volume of marketed maize will depend on the demand and the capacities of the agribusiness players in the maize value chain. There is evidence which suggests that demand for maize is stagnant, meaning that land would be converted to other crops. Still, it appears that a sizeable national population (25 million), and a growing urban population that is increasingly removed from farms and rural village roots, would support the development of commercial mills providing easy-to-cook maize meal. Population growth, however, appears to be balanced by annual declines in per capita maize consumption. A growing middle class will want to eat more protein in the form of poultry or fish, the local production of which will increase the need for locally-milled maize as the basis of animal feed. The Ministry of Food and Agriculture estimated that 110,000 tons of

34

Ibid, page 7. 35

Ibid, page 11. 36

See news article titled Give Ejura Farms Water to Survive, Article on Ghana Districts.com at

http://www.ghanadistricts.com/news/?read=8287 37

See video titled Competing with Imported Maize in Ghana, on 5 minLife Videopaedia,

http://www.5min.com/Video/Competing-with-Imported-Maize-in-Ghana-458397579 38

See news article titled Multi-purpose farm is established at Afram Plain on Ghana Web

http://www.ghanaweb.com/GhanaHomePage/NewsArchive/artikel.php?ID=161783 .

25

poultry and beef products and 130,000 tons of fish products are imported annually. According to most contacts, however, the broiler industry is very weak and underdeveloped at this time and is not purchasing large amounts of maize as feed. Only 150,000 tons are currently sold for commercial feed production. These sizeable markets could be attractive for investments into local production for import substitution, and could drive up the demand for maize as a feed product. The consumption of beer is also projected to rise with growing incomes, which could create an additional commercial market for maize. Again, there is a significant potential for growth of local inputs. Now, just 25-40,000 tons of local maize goes to breweries, when their annual requirement surpasses 200,000 tons.39 Constraints Limiting Private Investment Constraints to building a more robust value chain include: issues with input supplies for farmers, a mismatch between the qualities of maize demanded and those supplied, lack of irrigation in potential production zones, and, possibly, producer credit. Input supplies to support production do not seem to be a problem at first glance. There is a robust presence of agricultural input retail service providers throughout Ghana which are mostly supplied by large national importers.40 There is a strategic alliance between Wienco (general agri-supplier) and Yara (fertilizer importer and distributor) to supply improved seed, fertilizer and other inputs to farmers, through commercial associations, in northern Ghana on the basis of advances against purchase contracts for future maize production. This partnership has been very successful in encouraging surplus commercial production and demonstrates a positive role for private sector investment in the sector. Since 2007, the Ghanaian government has also implemented a subsidized fertilizer voucher system (worth approximately 50% of the fertilizers’ price). In addition, it has increased the provision of capital inputs such as tractors and established mechanization centers across the country. But lack of improved seeds is a large constraint to increasing production. The history and experience of private seed companies in Ghana has not been very successful. The commercial market for improved maize seed is only now becoming a reality with the passage of the new Seed Law, and more attention will have to be paid to matching production capacities with demand. For example, Ghana’s farmers produce primarily white maize, which is used for food, while imported yellow maize is used in animal feed. There will be a need to develop and integrate new seed varieties into production and to shape value chains toward specific markets. Recent steps by the government to encourage local supply have been broad-brush, such as the banning of the importation of white maize and import restrictions on yellow maize. It is not clear that these will contribute to appropriate differentiation of maize value chains.

39

See page 8 in WABS Consulting’s Draft Report titled Maize Value Chain Study in Ghana, Enhancing Efficiency

and Competitiveness, (WABS Consulting, 2008). 40

Ibid, page 25.

26

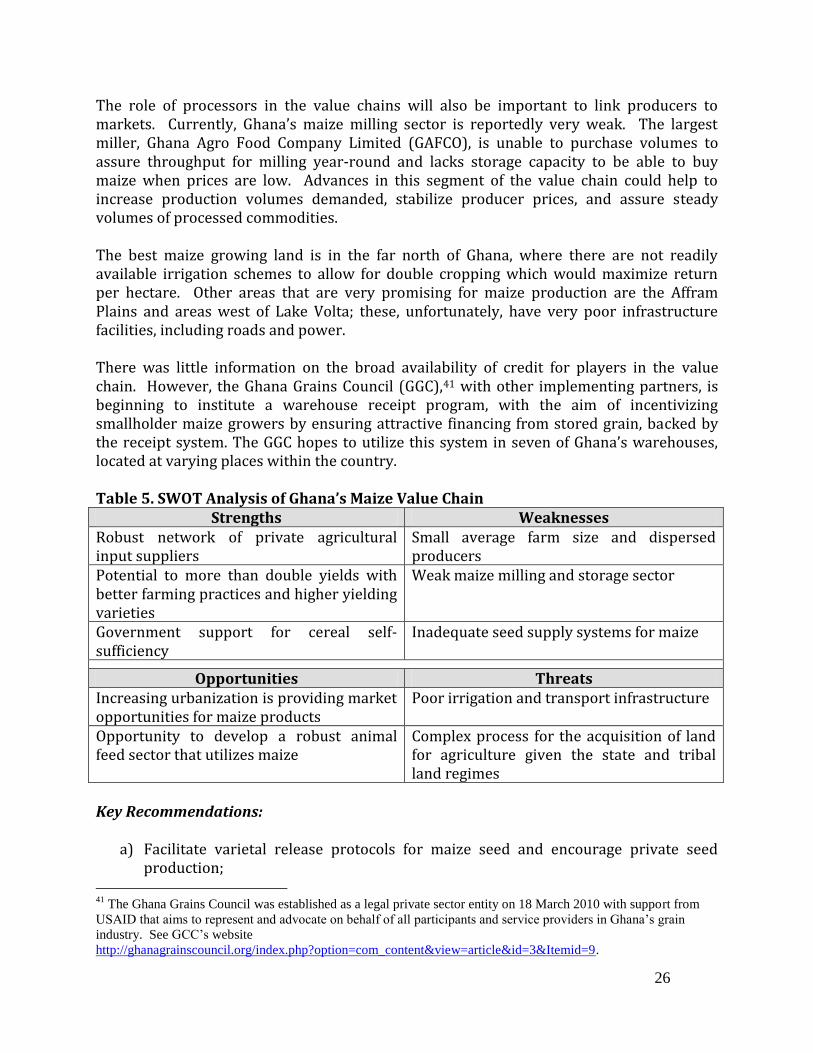

The role of processors in the value chains will also be important to link producers to markets. Currently, Ghana’s maize milling sector is reportedly very weak. The largest miller, Ghana Agro Food Company Limited (GAFCO), is unable to purchase volumes to assure throughput for milling year-round and lacks storage capacity to be able to buy maize when prices are low. Advances in this segment of the value chain could help to increase production volumes demanded, stabilize producer prices, and assure steady volumes of processed commodities. The best maize growing land is in the far north of Ghana, where there are not readily available irrigation schemes to allow for double cropping which would maximize return per hectare. Other areas that are very promising for maize production are the Affram Plains and areas west of Lake Volta; these, unfortunately, have very poor infrastructure facilities, including roads and power. There was little information on the broad availability of credit for players in the value chain. However, the Ghana Grains Council (GGC),41 with other implementing partners, is beginning to institute a warehouse receipt program, with the aim of incentivizing smallholder maize growers by ensuring attractive financing from stored grain, backed by the receipt system. The GGC hopes to utilize this system in seven of Ghana’s warehouses, located at varying places within the country. Table 5. SWOT Analysis of Ghana’s Maize Value Chain

Strengths Weaknesses Robust network of private agricultural input suppliers

Small average farm size and dispersed producers

Potential to more than double yields with better farming practices and higher yielding varieties

Weak maize milling and storage sector

Government support for cereal self-sufficiency

Inadequate seed supply systems for maize

Opportunities Threats Increasing urbanization is providing market opportunities for maize products

Poor irrigation and transport infrastructure

Opportunity to develop a robust animal feed sector that utilizes maize

Complex process for the acquisition of land for agriculture given the state and tribal land regimes

Key Recommendations:

a) Facilitate varietal release protocols for maize seed and encourage private seed production;

41

The Ghana Grains Council was established as a legal private sector entity on 18 March 2010 with support from

USAID that aims to represent and advocate on behalf of all participants and service providers in Ghana’s grain

industry. See GCC’s website

http://ghanagrainscouncil.org/index.php?option=com_content&view=article&id=3&Itemid=9.

27

b) Develop PPPs in transport, milling and storage infrastructure; and c) Streamline process for obtaining land rights, including those for aggregating land

holdings.

RICE VALUE CHAIN Current Situation A fast-growing demand for rice by Ghana’s increasingly wealthy consumers is driving interest in expanding Ghana’s own rice production. The country’s National Rice Development Strategy projects rice consumption to increase to 1.68 million MT by 2015 as Ghanaians continue to move into urban areas and enjoy higher levels of income, a trend that will likely be accelerated with the discovery of offshore oil.42 At a per-capita level, rice consumption is projected to increase from 30 kg in 2008 to 63 kg in 2018.43 Ghana’s rice production in 2008 provided approximately 30% of the 600,000 MT consumed that year, with between 120,000MT and 180,000 MT of rice milled from locally grown rice. 44 Rice is presently grown in the Accra Plains east of Accra and in the northern regions of Ghana. Commercial rice mills are available in Tamale, in the north, and in Wora Wora in Eastern Volta.45 With the exception of two irrigated schemes in Tamale and in the Prairie Volta in Aveyime, which cultivate about 1000 acres each and have plans to add up to 800 acres, the predominant method of rice production is on rain-fed lands managed by smallholder farmers. 84% of Ghana’s total production is rain-fed and the remaining 16% is irrigated.46 Through the Ghana Investment Promotion Center (GIPC), Ghanaian authorities are making a concerted attempt to attract private investments in rice production and processing. GIPC is providing incentives such as duty-free imports of agricultural equipment, fiscal incentives and tailored assistance to investors. According to GIPC officials, there are nearly 7 million acres (~2.8 million ha) of arable land in Ghana presently not being cultivated, so expanding acreage for rice cultivation is an option. The Ministry of Food and Agriculture (MOFA) is reported to be able to assist in accessing arable land. Ghana, alongside development partners, is attempting to improve the land

42

See page 3 of the Ghanaian government’s National Rice Development Strategy,

http://www.jica.go.jp/english/operations/thematic_issues/agricultural/pdf/ghana_en.pdf 43

Olfa Kula and Emmanuel Dormon, Attachment I to the Global Food Security Response – West Africa Rice Value

Chain Analysis,(ACDI/VOCA, 2009), page 3 44

Ministry of Food and Agriculture’s National Rice Development Strategy, (Ministry of Food and Agriculture-

Ghana, 2009), page 1. 45

Many of Ghana’s large rice mills have been privatized with the government of Ghana, however, holding a

minority share interest. Aveyime Rice Project, for example, is owned 40% by Prairie Volta of the U.S., 30% by

Ghana’s Commercial Bank, and 30% by the Ghanaian government. See article on Ghana Districts titled Aveyime

Rice Project, Ahwoi Upbeat http://www.ghanadistricts.com/news/?read=24515. 46

Olfa Kula and Emmanuel Dormon, Attachment I to the Global Food Security Response – West Africa Rice Value

Chain Analysis,(ACDI/VOCA, 2009), page 3

28

tenure system. Currently, Ghana is implementing Phase II of the Ghana Land Administration Project – a World Bank and Canadian International Development Agency (CIDA) funded project – that attempts to remove business bottlenecks, promote transparency and address various challenges in Ghana’s land tenure system.47 Attention is reportedly also being directed to other interventions that could support the rice value chain: improving research and extension, promoting micro-finance, building rice-stakeholder capacity, improving communication and collaboration, promoting private sector partnership, developing rice information systems, improving seed supply, and addressing gender, human health and sound environment management.48 Potential for Value Chain Expansion Generally speaking, the soils around the Volta Lake and downstream from the Akwosombo Dam are very fertile and accessible to irrigation schemes. With improved varieties and double-cropping, yields of 7-8 tons per acre are believed to be achievable. Quality standards for production must also be achieved. Current rice imports to Ghana are typically high-quality rice (i.e., low percentage of broken rice) from Vietnam, Thailand and Taiwan. A 2006 study indicated that 5.5% of all rice imported to Ghana was Grade 1 and 51% was Grade 2. According to one large-scale producer in Ghana, Prairie Volta Rice, there is a strong preference by the consumer for locally-produced rice when high quality is maintained, and specific varieties such as perfumed, long grain rice are preferred. With such discerning local consumers, where price sensitivity is not as critical as in many other African countries, there seems to be ample opportunity to expand the Ghanaian rice value chain to meet their needs. Constraints Limiting Private Investment Key challenges reportedly lie in organizing sufficient production of paddy, either on nucleus estates or in assemblages of small growers, and improving seed variety development and distribution. In addition to encouraging private investors to acquire land for production, the government appears to be ready to leave input supply totally in private hands which creates attractive opportunities for the private sector, as evidenced by Wienco and Yara. Further, the West Africa Rice Institute is testing and developing new rice varieties, with a focus on a new variety incorporating material from Vietnam that could yield up to 8-10 tons/acre. This rosy outlook is tempered by Ghana’s record of poor performance of rice production in recent years. Both the total quantity and the average quality of Ghanaian rice have been well below expectations. The GFSR Ghana report indicates that Ghana does not produce any Grade 1 rice and that only 4.3% of Ghana’s domestic rice is of Grade 2 quality. 82.6% of

47

See the World Bank’s reports on Ghana’s Land Administration Projects (i.e., 1 and 2) on the World Bank’s

website. 48

See Annex 2 of the Implementation Completion and Results for Phase 1 of Ghana’s Land Administration Project,

World Bank report no. ICR00002083.

29

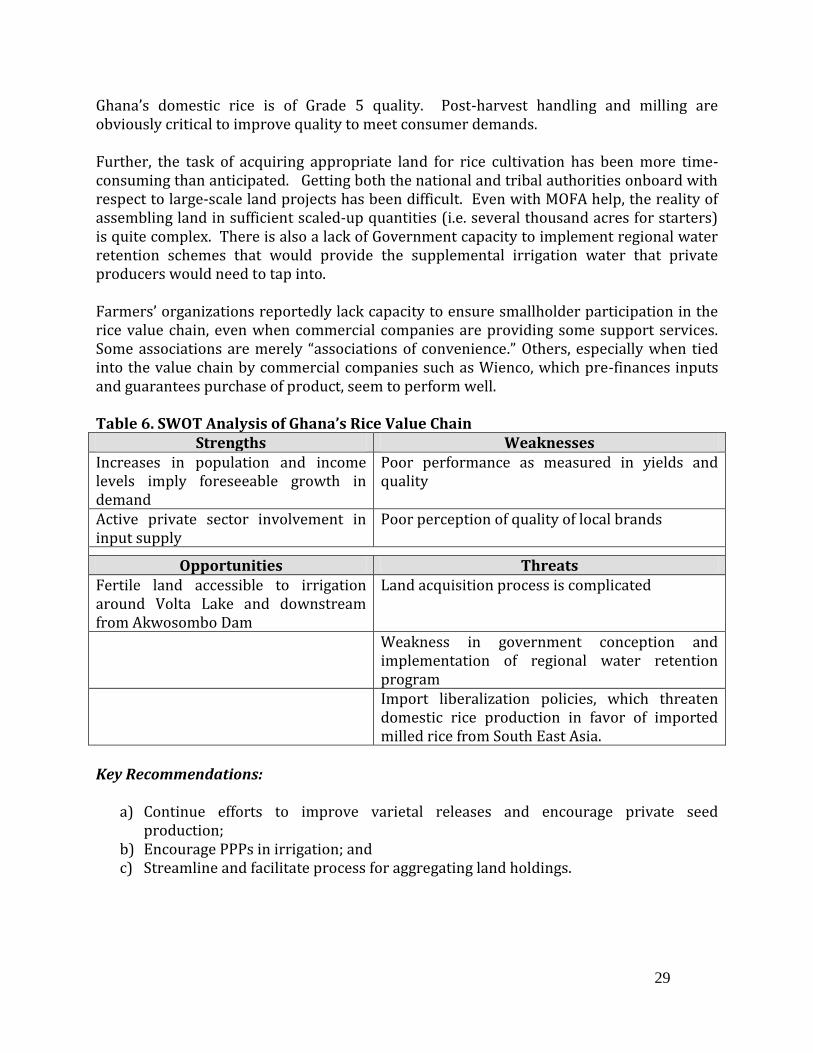

Ghana’s domestic rice is of Grade 5 quality. Post-harvest handling and milling are obviously critical to improve quality to meet consumer demands. Further, the task of acquiring appropriate land for rice cultivation has been more time-consuming than anticipated. Getting both the national and tribal authorities onboard with respect to large-scale land projects has been difficult. Even with MOFA help, the reality of assembling land in sufficient scaled-up quantities (i.e. several thousand acres for starters) is quite complex. There is also a lack of Government capacity to implement regional water retention schemes that would provide the supplemental irrigation water that private producers would need to tap into. Farmers’ organizations reportedly lack capacity to ensure smallholder participation in the rice value chain, even when commercial companies are providing some support services. Some associations are merely “associations of convenience.” Others, especially when tied into the value chain by commercial companies such as Wienco, which pre-finances inputs and guarantees purchase of product, seem to perform well. Table 6. SWOT Analysis of Ghana’s Rice Value Chain

Strengths Weaknesses Increases in population and income levels imply foreseeable growth in demand

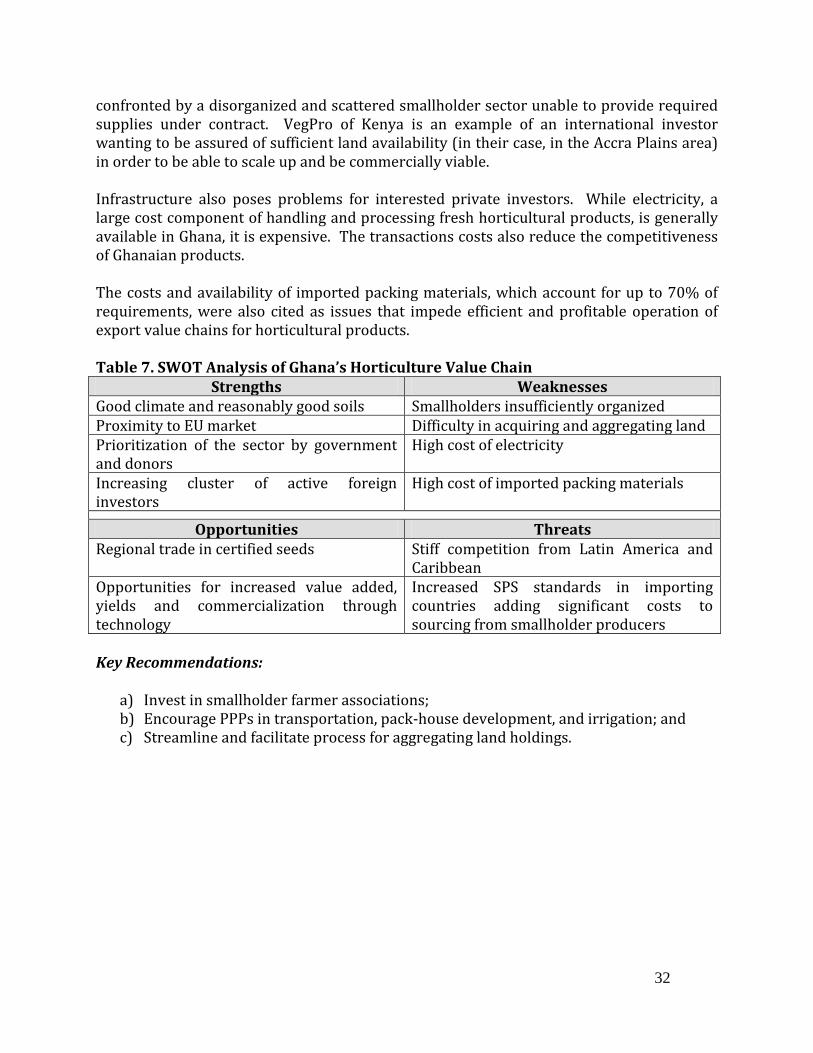

Poor performance as measured in yields and quality

Active private sector involvement in input supply

Poor perception of quality of local brands

Opportunities Threats Fertile land accessible to irrigation around Volta Lake and downstream from Akwosombo Dam

Land acquisition process is complicated

Weakness in government conception and implementation of regional water retention program

Import liberalization policies, which threaten domestic rice production in favor of imported milled rice from South East Asia.

Key Recommendations:

a) Continue efforts to improve varietal releases and encourage private seed production;

b) Encourage PPPs in irrigation; and c) Streamline and facilitate process for aggregating land holdings.

30