Embed Size (px)

Citation preview

October 2017

APRA has released a second consultation package on

the role of the Appointed Actuary (AA), following its initial

consultation in June 2016. There is little change from the

original proposals.

APRA’s proposals respond to issues that developed in

the life insurance AA space, but they apply across general,

life and health insurance.

Role of the AppointedActuary

In this edition we:

Focus on the proposed

changes for general insurers

Discuss the impact for private health insurance

Give Finity’s views – overall, we are supportive of the changes.

General insurersWe don’t expect any major differences in the way general insurers use actuaries. APRA’s changes are:

• Each insurer will develop a Board-approved Actuarial Advice Framework (AAF)

• The ILVR has been ‘rebranded’ as the Actuarial Valuation Report (AVR)

• The requirements of the FCR are less specific in a number of areas.

Private health insurers• If an insurer wishes to continue working

with its AA in the same way, it simply needs to document current practice in the AAF

• Health insurers can slightly reduce the scope of the AA role, due to new flexibility around notifiable circumstances

• Documentation of insurance liabilities will continue to be at the discretion of the insurer and the AA.

| APRA Regulation AA role | October 2017 02

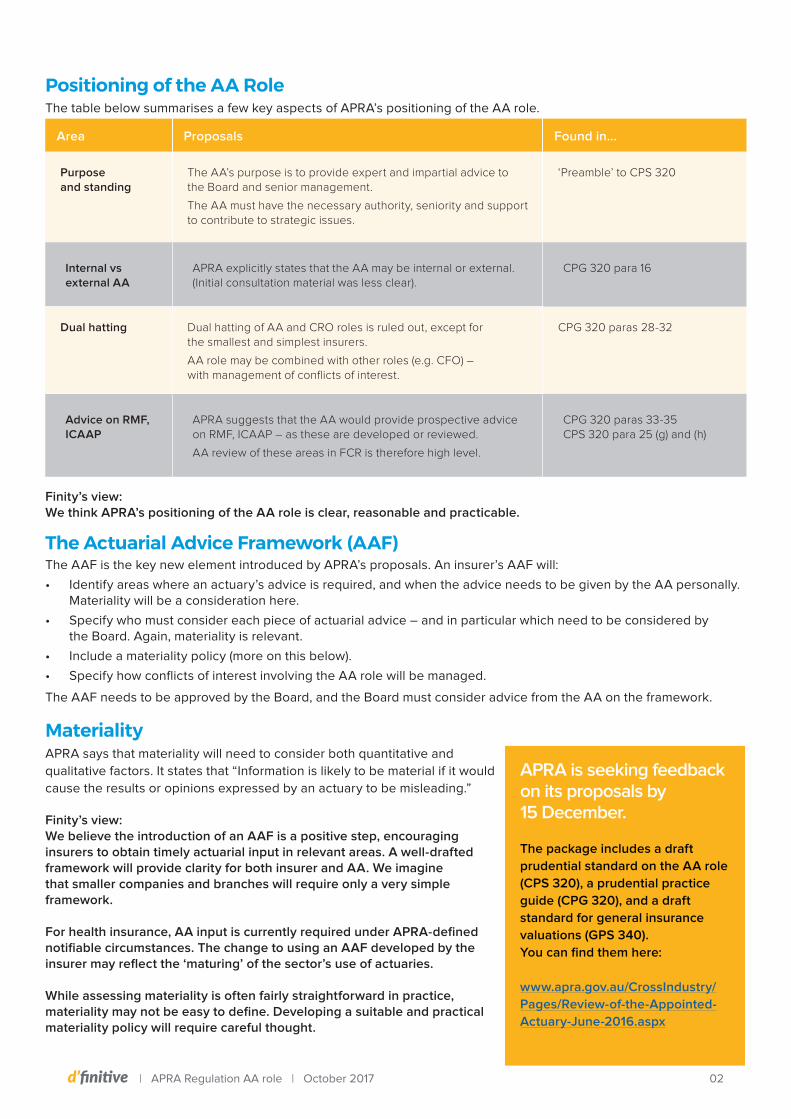

Positioning of the AA Role The table below summarises a few key aspects of APRA’s positioning of the AA role.

Area Proposals Found in...

Purpose and standing

The AA’s purpose is to provide expert and impartial advice to the Board and senior management.

The AA must have the necessary authority, seniority and support to contribute to strategic issues.

‘Preamble’ to CPS 320

Internal vs external AA

APRA explicitly states that the AA may be internal or external. (Initial consultation material was less clear).

CPG 320 para 16

Dual hatting Dual hatting of AA and CRO roles is ruled out, except for the smallest and simplest insurers.

AA role may be combined with other roles (e.g. CFO) – with management of conflicts of interest.

CPG 320 paras 28-32

Advice on RMF, ICAAP

APRA suggests that the AA would provide prospective advice on RMF, ICAAP – as these are developed or reviewed.

AA review of these areas in FCR is therefore high level.

CPG 320 paras 33-35CPS 320 para 25 (g) and (h)

Finity’s view:We think APRA’s positioning of the AA role is clear, reasonable and practicable.

The Actuarial Advice Framework (AAF)The AAF is the key new element introduced by APRA’s proposals. An insurer’s AAF will:

• Identify areas where an actuary’s advice is required, and when the advice needs to be given by the AA personally. Materiality will be a consideration here.

• Specify who must consider each piece of actuarial advice – and in particular which need to be considered by the Board. Again, materiality is relevant.

• Include a materiality policy (more on this below).

• Specify how conflicts of interest involving the AA role will be managed.

The AAF needs to be approved by the Board, and the Board must consider advice from the AA on the framework.

MaterialityAPRA says that materiality will need to consider both quantitative and

qualitative factors. It states that “Information is likely to be material if it would

cause the results or opinions expressed by an actuary to be misleading.”

Finity’s view:We believe the introduction of an AAF is a positive step, encouraging insurers to obtain timely actuarial input in relevant areas. A well-drafted framework will provide clarity for both insurer and AA. We imagine that smaller companies and branches will require only a very simple framework.

For health insurance, AA input is currently required under APRA-defined notifiable circumstances. The change to using an AAF developed by the insurer may reflect the ‘maturing’ of the sector’s use of actuaries.

While assessing materiality is often fairly straightforward in practice, materiality may not be easy to define. Developing a suitable and practical materiality policy will require careful thought.

APRA is seeking feedback on its proposals by 15 December.

The package includes a draft

prudential standard on the AA role

(CPS 320), a prudential practice

guide (CPG 320), and a draft

standard for general insurance

valuations (GPS 340).

You can find them here:

www.apra.gov.au/CrossIndustry/

Pages/Review-of-the-Appointed-

Actuary-June-2016.aspx

| APRA Regulation AA role | October 2017 03

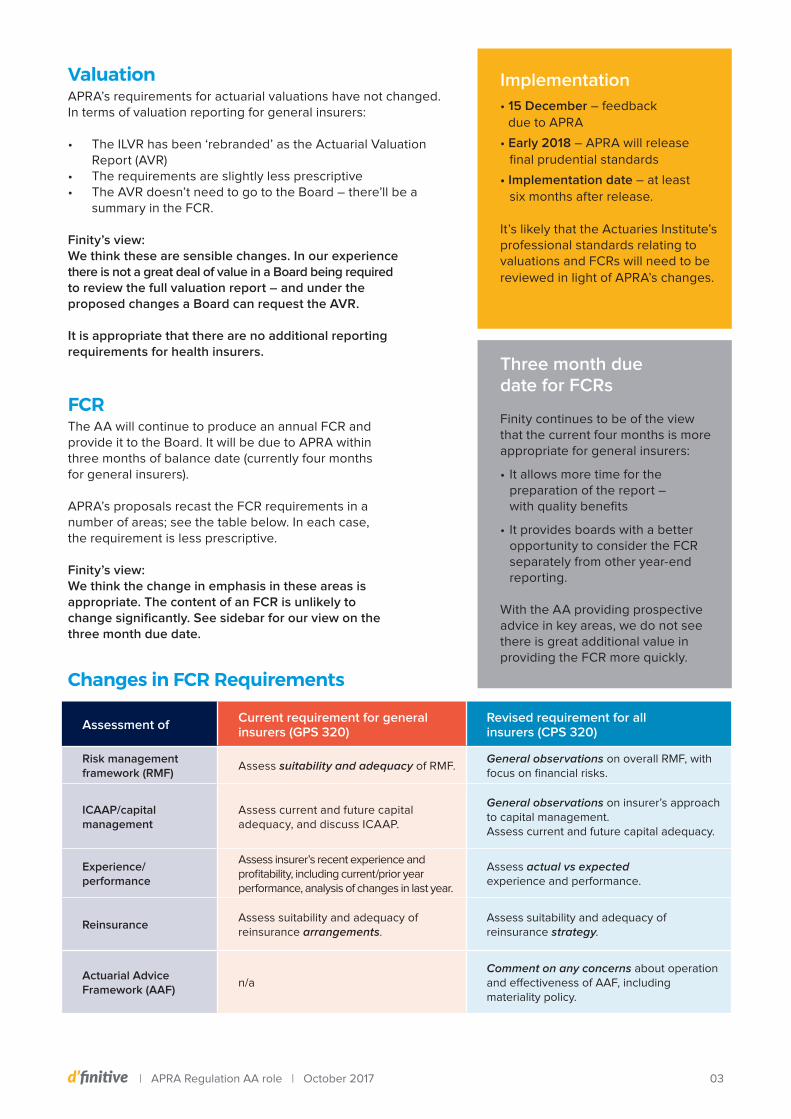

ValuationAPRA’s requirements for actuarial valuations have not changed. In terms of valuation reporting for general insurers:

• The ILVR has been ‘rebranded’ as the Actuarial Valuation Report (AVR)

• The requirements are slightly less prescriptive• The AVR doesn’t need to go to the Board – there’ll be a

summary in the FCR.

Finity’s view: We think these are sensible changes. In our experience there is not a great deal of value in a Board being required to review the full valuation report – and under the proposed changes a Board can request the AVR.

It is appropriate that there are no additional reporting requirements for health insurers.

Assessment of Current requirement for general insurers (GPS 320)

Revised requirement for all insurers (CPS 320)

Risk management framework (RMF)

Assess suitability and adequacy of RMF.General observations on overall RMF, with focus on financial risks.

ICAAP/capital management

Assess current and future capital adequacy, and discuss ICAAP.

General observations on insurer’s approach to capital management.Assess current and future capital adequacy.

Experience/performance

Assess insurer’s recent experience and profitability, including current/prior year performance, analysis of changes in last year.

Assess actual vs expected experience and performance.

ReinsuranceAssess suitability and adequacy of reinsurance arrangements.

Assess suitability and adequacy of reinsurance strategy.

Actuarial Advice Framework (AAF)

n/aComment on any concerns about operation and effectiveness of AAF, including materiality policy.

Implementation

• 15 December – feedback due to APRA

• Early 2018 – APRA will release final prudential standards

• Implementation date – at least six months after release.

It’s likely that the Actuaries Institute’s professional standards relating to valuations and FCRs will need to be reviewed in light of APRA’s changes.

FCRThe AA will continue to produce an annual FCR and provide it to the Board. It will be due to APRA within three months of balance date (currently four months for general insurers).

APRA’s proposals recast the FCR requirements in a number of areas; see the table below. In each case, the requirement is less prescriptive.

Finity’s view:We think the change in emphasis in these areas is appropriate. The content of an FCR is unlikely to change significantly. See sidebar for our view on the three month due date.

Changes in FCR Requirements

Three month due date for FCRs

Finity continues to be of the view that the current four months is more appropriate for general insurers:

• It allows more time for the preparation of the report – with quality benefits

• It provides boards with a better opportunity to consider the FCR separately from other year-end reporting.

With the AA providing prospective advice in key areas, we do not see there is great additional value in providing the FCR more quickly.

| APRA Regulation AA role | October 2017 04

Jamie Reid

+61 2 8252 3309

Health Insurance

Gae Robinson

+61 2 8252 3369

General Insurance

Contact us

2016 ANZIIF Professional Services Firm of the Year (NZ) 2015 ANZIIF Professional Services Firm of the Year (AUS) Six time winner ANZIIF Service Provider of the Year

ANZIIF Hall of Fame

AUSTRALIA

Sydney

Level 7, 68 Harrington StreetThe Rocks NSW 2000+61 2 8252 3300

Melbourne

Level 3, 30 Collins StreetMelbourne VIC 3000+61 3 8080 0900

Adelaide

Level 30, Westpac House 91 King William Street Adelaide SA 5000+61 8 8233 5817

NEW ZEALAND

Auckland

Level 5, 79 Queen Street Auckland 1010+64 9 306 7700

What should you do now?Apart from providing feedback to APRA, it’s an opportune time to reflect

on the way you use your AA:

• Are there additional areas where your AA could offer valuable

insights and advice?

• Are there areas where you currently receive advice that is not

adding value, and could be de-emphasised in future?

• For AAs – how does your current role align with the aspirations of

APRA’s purpose statement?

While it appears that implementation is around a year away, considering

these questions now will be helpful in formulating the feedback on

APRA’s proposals.

Finity Consulting is the largest independent general and health insurance

actuarial consultancy in Australia. Our expertise is highly regarded and has

been developed working in the industry since the early 1980s.

Through our industry publications we seek to share our insights into the key

drivers of industry trends and to help our clients stay abreast of the latest

issues that are important to their business.

While Finity has taken reasonable care in compiling the information presented,

Finity does not warrant that the information is correct.

Copyright © 2017 Finity Consulting Pty Limited.