Embed Size (px)

DESCRIPTION

Brief History of Urban Cooperative Banks in IndiaThe term Urban Co-operative Banks (UCBs), though not formally defined, refers to primary cooperative banks located in urban and semi-urban areas. These banks, till 1996, were allowed to lend money only for non-agricultural purposes. This distinction does not hold today. These banks were traditionally centred around communities, localities work place groups. They essentially lent to small borrowers and businesses. Today, their scope of operations has widened considerably.The origins of the urban cooperative banking movement in India can be traced to the close of nineteenth century when, inspired by the success of the experiments related to the cooperative movement in Britain and the cooperative credit movement in Germany such societies were set up in India. Cooperative societies are based on the principles of cooperation, - mutual help, democratic decision making and open membership. Cooperatives represented a new and alternative approach to organisaton as against proprietary firms, partnership firms and joint stock companies which represent the dominant form of commercial organisation.The BeginningsThe first known mutual aid society in India was probably the ‘Anyonya Sahakari Mandali’ organised in the erstwhile princely State of Baroda in 1889 under the guidance of Vithal Laxman also known as Bhausaheb Kavthekar. Urban co-operative credit societies, in their formative phase came to be organised on a community basis to meet the consumption oriented credit needs of their members. Salary earners’ societies inculcating habits of thrift and self help played a significant role in popularising the movement, especially amongst the middle class as well as organized labour. From its origins then to today, the thrust of UCBs, historically, has been to mobilise savings from the middle and low income urban groups and purvey credit to their members - many of which belonged to weaker sections.The enactment of Cooperative Credit Societies Act, 1904, however, gave the real impetus to the movement. The first urban cooperative credit society was registered in Canjeevaram (Kanjivaram) in the erstwhile Madras province in October, 1904. Amongst the prominent credit societies were the Pioneer Urban in Bombay (November 11, 1905), the No.1 Military Accounts Mutual Help Co-operative Credit Society in Poona (January 9, 1906). Cosmos in Poona (January 18, 1906), Gokak Urban (February 15, 1906) and Belgaum Pioneer (February 23, 1906) in the Belgaum district, the Kanakavli-Math Co-operative Credit Society and the Varavade Weavers’ Urban Credit Society (March 13, 1906) in the South Ratnagiri (now Sindhudurg) district. The most prominent amongst the early credit societies was the Bombay Urban Co-operative Credit Society, sponsored by Vithaldas Thackersey and Lallubhai Samaldas established on January 23, 1906..The Cooperative Credit Societies Act, 1904 was amended in 1912, with a view to broad basing it to enable organisation of non-credit societies. The Maclagan Committee of 1915 was appointed to review their performance and suggest measures for strengthening them. The committee observed that such institutions were eminently suited to cater to the needs of the lower and middle income strata of society and would inculcate the principles of banking amongst the middle classes. The committee also felt that the urban cooperative credit movement was more viable than agricultural credit societies. The recommendations of the Committee went a long way in establishing the urban cooperative credit movement in its own right.In the present day context, it is of interest to recall that during the banking crisis of 1913-14, when no fewer than 57 joint stock banks collapsed, there was a there was a flight of deposits from joint stock banks to cooperative urban banks. Maclagan Committee chronicled this event thus:“As a matter of fact, the crisis had a contrary effect, and in most provinces, ther

Citation preview

1

EXECUTIVE SUMMARY

Day in and day out, numerous newspapers, magazines and news channels have some information on “role of urban cooperative banks”. This just proceeds to show us the magnitude of role of UCB”S. That is why it is necessary to study role of UCB”S and its regulation and challenges.

The objective of this project is to have deeper understanding, as to what role is, the importance of UCB”S, the challenges they face and also the ways they prevent from restrictions.

The banking sector in India has an extremely bright future; however Role of UCB”S has a dynamic industry from growing further.

The report gives a brief introduction to UCB”S, helps us understand what and how many UCB”S are, the different circular and the supervision. The report also contains it in detail giving us a brief knowledge on this topic.

2

MEANING OF UCB’S

The term urban co-operative banks (UCBs), though not formally defined, refer to primary cooperative banks located in urban and semi urban areas. These banks, till 1996 were allowed to lend money only for non-agricultural purposes. This distinction does not hold today. These banks were traditionally centered around communities, localities work place groups. They essentially lent to small borrowers and businesses. today, their scope of operations had widened considerably.

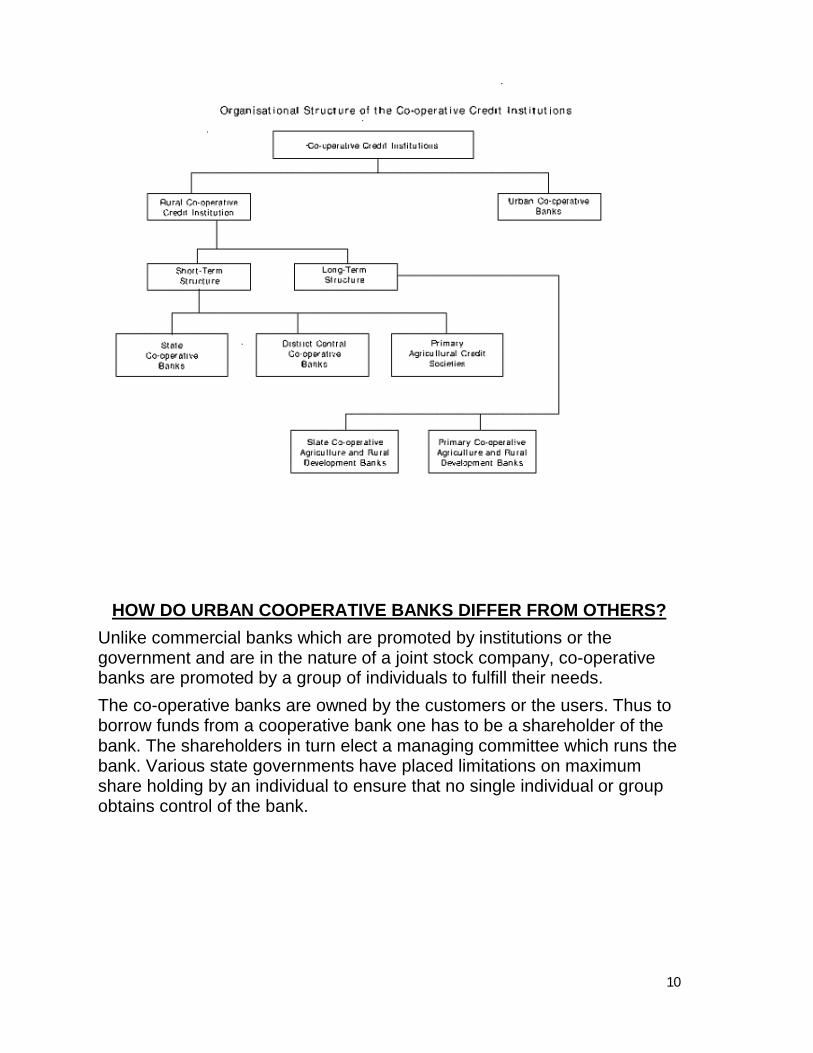

The co-operative banking structure in India comprises urban co-operative banks and rural co-operative credit institutions. Urban co-operative banks consist of single tier viz. primary co-operative, commonly referred to as urban co-operative banks (UCBs).

The rural co-operative credit structure has traditionally been bifurcated into two parallel wings viz. short term and long term. Short term co-operative and credit institutions have a federal three tier structure consisting of a large number of primary agricultural credit societies (PACS) at the grassroot level, central co-operative banks (CCBs) at the district level and State co-operative banks (StCBs) at the state/apex level. The smaller States and union territories have a two tier structure with the StCBs directly meeting the credit requirements of PACS. The long term rural co-operative structure has two tiers, viz. State co-operative agriculture and rural development banks (SCARDBs) at the state level and primary co-operative and rural development banks (PCARDBs) at the taluka/tehsil level. However some states have a unitary structure with the State level banks operating through their own branches: three States have a mixed structure incorporating both unitary and federal systems.

INTRODUCTION

The urban co-operative banks were first started in Germany in 1888 and in Italy in 1898. Thus urban co-operative banks are more than 100 years old.

Credit cooperatives are the oldest and most numerous of all the types of cooperatives in India. The cooperative credit institutions in the country may be broadly classified into urban credit cooperatives and rural credit cooperatives. There are about 2090 urban credit cooperatives and these societies together constitute for about 10 percent of the aggregate banking business and therefore regarded as an important segment of the banking system. The urban credit cooperatives are also popularly known as Urban Cooperative Banks.

3

In India first urban co-operative bank was started by Mr Vitthal Laxman Kavthekar in 1889. The guiding principles of voluntary and open membership, equal economic participation and concern for the community were the basis.

Co-operative Banks in India have come a long way since the enactment of the agricultural Credit Co-operative Societies Act 1904. The century old co-operative banking structure is viewed as an important instrument of banking access to the rural masses and thus a vehicle for democratization of Indian financial System. Co-operative Banks mobilize deposits and purvey agricultural and rural credit with a wider outreach. They have also been an important instrument for various development schemes, particularly subsidy based programmes for the poor.

Primary urban co-operative banks play an important role in meeting the growing credit needs of urban and semi-urban areas. UCBs mobilize savings from the middle and lower income groups and purvey credit to small sections of the society.

The basic idea of establishing the co-operative bank is still relevant but they have to change their working style and adopt modern means of ICT. Hence it would be useful to discuss in brief the basic philosophy behind establishing the cooperative institutions. Today there are over 2000 primary urban cooperative banks with a deposit of over Rs 60000 crores.

Till end of March 2005 the number of UCBs was 1872 and till end of March 2004 the count of rural co-operative credit institutions was 1,06,919 with short term having a majority share of 1,06,131 institutions and long term having 788.Out of short term StCBs had 31 CCBs had 365 and PACS had 1,05,735 institutions respectively. In long term SCARDBs had 20 and PCARDBs had 768 institutions respectively.

Credit cooperatives are the oldest and most numerous of all the types of cooperatives in India. The cooperative credit institutions in the country may be broadly classified into urban credit cooperatives and rural credit cooperatives. There are about 2090 urban credit cooperatives and these societies together constitute for about 10 percent of the aggregate banking business and therefore regarded as an important segment of the banking system. The urban credit cooperatives are also popularly known as Urban Cooperative Banks.

The rural credit cooperatives may be further divided into short-term credit cooperatives and long-term credit cooperatives. With regard to short-term credit cooperatives, at the grass-root level there are around 92,000 Primary Agricultural Credit Societies (PACS) dealing directly with the individual borrowers. At the central level (district level) District Central

4

Cooperative Banks (DCCB) function as a link between primary societies and State Cooperative Apex Banks (SCB). It may be mentioned that DCCB and SCB are the federal cooperatives and thus the objective is to serve the member cooperatives. As against three-tier structure of short-term credit cooperatives, the long-term cooperative credit structure has two tiers in many states with Primary Cooperative Agriculture and Rural Development Banks (PCARDB) at the primary level and State Cooperative Agriculture and Rural Development Bank at the state level. However, some states in the country have unitary structure with state level cooperative operating with through their own branches and in one state an integrated structure prevails. The organizational structure of the credit cooperatives in India is illustrated in chart I. Interestingly, under the Banking Regulation Act 1949, only State Cooperative Apex Banks, District Central Cooperative Banks and select Urban Credit Cooperatives are qualified to be called as banks in the cooperative sector. In other words, only these banks are licensed to conduct full-fledged banking business.

URBAN COOPERATIVE BANKS

Urban cooperative banks (UCBs) are managed, governed, and regulated in India to enable them to enhance their contributions to achieving greater degree of financial inclusion, and more broad-based growth. Design/methodology/approach – The paper first surveys the quantitative importance of the UCBs in India, and their key performance indicators. Various official reports by the country's Central Bank, the Reserve Bank of India (RBI), and other relevant organizations are used extensively. The paper then identifies key areas of reforms, centering primarily on the current business model, governance and regulation practices, and capital adequacy. It then argues for a change in a paradigm shift by the UCBs, and how better governance and regulatory structure can assist this shift. Findings – The paper finds that if the UCBs are to remain relevant and play a significant developmental role in India, they will require same quality of governance and regulation as well as professionalism and modernization as the mainstream commercial banks. The governance and regulatory structures need to be brought in conformity with India's current and prospective economic structure; and relevant laws modernized. This requires a paradigm shift in the role of UCBs. Research limitations/implications – The research has been based primarily on secondary sources, particularly various reports by the RBI, the country's Central Bank. Better understanding of the reasons for differences between well-governed and financially sound UCBs on one hand, and those that are not, requires focused interviews and more searching examination of the operating environment and financial statements of a sample of the UCBs. This could be the next stage of research. Originality/value – This paper

5

represents a part of public debate on ways of integrating the UCBs into the mainstream banking sector. This is an important public policy issue as even though the UCBs represent relatively small proportion of the total banking assets, they still represent a systemic risk to India's financial system, and without reforming them, broad-based economic growth would be difficult to achieve.

HISTORY OF URBAN COOPERATIVE BANKS IN INDIA

Urban co-operative banks are registered under Co-operatives Societies Act of the respective State Governments. Prior to 1966, UCBs were exclusively under the purview of State Governments.

The term Urban Co-operative Banks (UCBs), though not formally defined, refers to primary cooperative banks located in urban and semi-urban areas. These banks, till 1996, were allowed to lend money only for non-agricultural purposes. They essentially lend to small borrowers and businesses. Today, their scope of operations has widened considerably.

The origins of the urban cooperative banking movement in India can be traced to the close of nineteenth century when, inspired by the success of the experiments related to the cooperative movement in Britain and the cooperative credit movement in Germany such societies were set up in India. Cooperative societies are based on the principles of cooperation, -mutual help, democratic decision making and open membership. Cooperatives represented a new and alternative approach to organization as against proprietary firms, partnership firms and joint stock companies which represent the dominant form of commercial organization.

The first study of Urban Co-operative Banks was taken up by RBI in the year 1958-59. The Report published in 1961 acknowledged the widespread and financially sound framework of urban co-operative banks; emphasized the need to establish primary urban cooperative banks in new centers and suggested that State Governments lend active support to their development. In 1963, Varde Committee recommended that such banks should be organized at all Urban Centre’s with a population of 1 lakh or more and not by any single community or caste. The committee introduced the concept of minimum capital requirement and the criteria of population for defining the urban centre where UCBs were incorporated.

6

BRIEF HISTORY OF URBAN COOPERATIVE BANKS IN INDIA

FUNCTIONAL

The term Urban Co-operative Banks (UCBs), though not formally defined, refers to primary cooperative banks located in urban and semi-urban areas. These banks, till 1996, were allowed to lend money only for non-agricultural purposes. This distinction does not hold today. These banks were traditionally centred around communities, localities work place groups. They essentially lent to small borrowers and businesses. Today, their scope of operations has widened considerably.

The origins of the urban cooperative banking movement in India can be traced to the close of nineteenth century when, inspired by the success of the experiments related to the cooperative movement in Britain and the cooperative credit movement in Germany such societies were set up in India. Cooperative societies are based on the principles of cooperation, -mutual help, democratic decision making and open membership. Cooperatives represented a new and alternative approach to organisaton as against proprietary firms, partnership firms and joint stock companies which represent the dominant form of commercial organisation.

THE BEGINNINGS

The first known mutual aid society in India was probably the ‘Anyonya Sahakari Mandali’ organised in the erstwhile princely State of Baroda in 1889 under the guidance of Vithal Laxman also known as Bhausaheb Kavthekar. Urban co-operative credit societies, in their formative phase came to be organised on a community basis to meet the consumption oriented credit needs of their members. Salary earners’ societies inculcating habits of thrift and self help played a significant role in popularising the movement, especially amongst the middle class as well as organized labour. From its origins then to today, the thrust of UCBs, historically, has been to mobilize savings from the middle and low income urban groups and purvey credit to their members - many of which belonged to weaker sections.

The enactment of Cooperative Credit Societies Act, 1904, however, gave the real impetus to the movement. The first urban cooperative credit society was registered in Canjeevaram (Kanjivaram) in the erstwhile Madras province in October, 1904. Amongst the prominent credit societies were the Pioneer Urban in Bombay (November 11, 1905), the No.1 Military Accounts Mutual Help Co-operative Credit Society in Poona (January 9,

7

1906). Cosmos in Poona (January 18, 1906), Gokak Urban (February 15, 1906) and Belgaum Pioneer (February 23, 1906) in the Belgaum district, the Kanakavli-Math Co-operative Credit Society and the Varavade Weavers’ Urban Credit Society (March 13, 1906) in the South Ratnagiri (now Sindhudurg) district. The most prominent amongst the early credit societies was the Bombay Urban Co-operative Credit Society, sponsored by Vithaldas Thackersey and Lallubhai Samaldas established on January 23, 1906..

The Cooperative Credit Societies Act, 1904 was amended in 1912, with a view to broad basing it to enable organisation of non-credit societies. The Maclagan Committee of 1915 was appointed to review their performance and suggest measures for strengthening them. The committee observed that such institutions were eminently suited to cater to the needs of the lower and middle income strata of society and would inculcate the principles of banking amongst the middle classes. The committee also felt that the urban cooperative credit movement was more viable than agricultural credit societies. The recommendations of the Committee went a long way in establishing the urban cooperative credit movement in its own right.

UNDER STATE PURVIEW

The constitutional reforms which led to the passing of the Government of India Act in 1919 transferred the subject of “Cooperation” from Government of India to the Provincial Governments. The Government of Bombay passed the first State Cooperative Societies Act in 1925 “which not only gave the movement its size and shape but was a pace setter of cooperative activities and stressed the basic concept of thrift, self help and mutual aid.” Other States followed. This marked the beginning of the second phase in the history of Cooperative Credit Institutions.

There was the general realization that urban banks have an important role to play in economic construction. This was asserted by a host of committees. The Indian Central Banking Enquiry Committee (1931) felt that urban banks have a duty to help the small business and middle class people. The Mehta-Bhansali Committee (1939), recommended that those societies which had fulfilled the criteria of banking should be allowed to work as banks and recommended an Association for these banks. The Co-operative Planning Committee (1946) went on record to say that urban banks have been the best agencies for small people in whom Joint stock banks are not generally interested. The Rural Banking Enquiry Committee (1950), impressed by the low cost of establishment and operations

8

recommended the establishment of such banks even in places smaller than taluka towns.

The first study of Urban Co-operative Banks was taken up by RBI in the year 1958-59. The Report published in 1961 acknowledged the widespread and financially sound framework of urban co-operative banks; emphasized the need to establish primary urban cooperative banks in new centers and suggested that State Governments lend active support to their development. In 1963, Varde Committee recommended that such banks should be organised at all Urban Centres with a population of 1 lakh or more and not by any single community or caste. The committee introduced the concept of minimum capital requirement and the criteria of population for defining the urban centre where UCBs were incorporated.

DUALITY OF CONTROL

However, concerns regarding the professionalism of urban cooperative banks gave rise to the view that they should be better regulated. Large cooperative banks with paid-up share capital and reserves of Rs.1 lakh were brought under the perview of the Banking Regulation Act 1949 witheffect from 1st March, 1966 and within the ambit of the Reserve Bank’s supervision. This marked the beginning of an era of duality of control over these banks. Banking related functions (viz. licensing, area of operations, interest rates etc.) were to be governed by RBI and registration, management, audit and liquidation, etc. governed by State Governments as per the provisions of respective State Acts. In 1968, UCBS were extended the benefits of Deposit Insurance.

Towards the late 1960s there was much debate regarding the promotion of the small scale industries. UCBs came to be seen as important players in this context. The Working Group on Industrial Financing through Co-operative Banks, (1968 known as Damry Group) attempted to broaden the scope of activities of urban co-operative banks by recommending that these banks should finance the small and cottage industries. This was reiterated by the Banking Commisssion (1969).

The Madhavdas Committee (1979) evaluated the role played by urban co-operative banks in greater details and drew a roadmap for their future role recommending support from RBI and Government in the establishment of such banks in backward areas and prescribing viability standards.

The Hate Working Group (1981) desired better utilisation of banks' surplus funds and that the percentage of the Cash Reserve Ratio (CRR) & the Statutory Liquidity Ratio (SLR) of these banks should be brought at par with commercial banks, in a phased manner. While the Marathe

9

Committee (1992) redefined the viability norms and ushered in the era of liberalization, the Madhava Rao Committee (1999) focused on consolidation, control of sickness, better professional standards in urban co-operative banks and sought to align the urban banking movement with commercial banks.

A feature of the urban banking movement has been its heterogeneous character and its uneven geographical spread with most banks concentrated in the states of Gujarat, Karnataka, Maharashtra, and Tamil Nadu. While most banks are unit banks without any branch network, some of the large banks have established their presence in many states when at their behest multi-state banking was allowed in 1985. Some of these banks are also Authorised Dealers in Foreign Exchange.

RECENT DEVELOPMENTS

Over the years, primary (urban) cooperative banks have registered a significant growth in number, size and volume of business handled. As on 31st March, 2003 there were 2,104 UCBs of which 56 were scheduled banks. About 79 percent of these are located in five states, - Andhra Pradesh, Gujarat, Karnataka, Maharashtra and Tamil Nadu. Recently the problems faced by a few large UCBs have highlighted some of the difficulties these banks face and policy endeavours are geared to consolidating and strengthening this sector and improving governance.

Priority Sector Lending

UCBs are required to channelize 60 per cent of total loans and advances towards priority sector. Furthermore, within the priority sector lending, lending to weaker sections should constitute 15 per cent of the total loansand advances of UCBs. Fulfilment of priority sector lending targets by individual UCBs are taken into consideration by the RBI while granting permission for branch expansion, expansion of areas of operation, scheduled status, etc.

10

HOW DO URBAN COOPERATIVE BANKS DIFFER FROM OTHERS?

Unlike commercial banks which are promoted by institutions or the government and are in the nature of a joint stock company, co-operative banks are promoted by a group of individuals to fulfill their needs.

The co-operative banks are owned by the customers or the users. Thus to borrow funds from a cooperative bank one has to be a shareholder of the bank. The shareholders in turn elect a managing committee which runs the bank. Various state governments have placed limitations on maximum share holding by an individual to ensure that no single individual or group obtains control of the bank.

11

OBJECTIVES OF URBAN CO-OPERATIVE BANKS

The co-operative system world over has emerged with a distinct objective namely to safeguard the interests of its members and to provide financial assistance to those who are unable to get financial help from other institutions. Still a large number of people in the urban, semiurban and villages are unable to receive the benefits. They have not benefited from the new developments to a desired extent. The co-operatives can play a very significant role in the traditional areas like small borrowers; retail and petty traders transport operators and other weaker sections of the society.

Primary urban co-operative banks play an important role in meeting the growing credit needs of urban and semi-urban areas. UCBs mobilize savings from the middle and lower income groups and purvey credit to small sections of the society.

The basic idea of establishing the co-operative bank is still relevant but they have to change their working style and adopt modern means of ICT. Hence it would be useful to discuss in brief the basic philosophy behind establishing the cooperative institutions. Today there are over 2000 primary urban cooperative banks with a deposit of over Rs 60000 crores.

Early history of cooperative movement through out the world shows that cooperative organizations began with consumers cooperatives. The first Co-operative society known as Rochdale Pioneer was formed by 28 flannel weavers in England in 1843 to protect themselves against the organized sector. The movement later spread on to the other fields of economic activities. But the ultimate aim of co-operatives was the protection of poor sections of the society by pooling the available sources with them to help their members by providing financial assistance to face the competition from the organized sector.

CHARACTERISTICS OF UCB

• Registered under State Cooperative Societies Acts

• No controlling interest since the board of management is elected by share holders in a democratic manner

• One member one vote irrespective of number of shares held by a member

• Duality of command – RCS / CRCS and RBI

Borrowing restricted to members

• Restricted area of operation

12

• Share linking to borrowing

• No listing / no trading of shares

• Strong in helping financially weaker section

REASONS WHY UCBS WERE BROUGHT UNDER RBI’S CONTROL

Effective from March 1,1966, provisions of B.R. Act

Rapid growth of the cooperative banking sector necessitated better monitoring

Demand for introduction of deposit insurance to cooperative banks (1949) were extended to UCBs

This resulted in dual command, cooperation being a state subject

The prime objective of the Urban Cooperative Banks is to render minimum baking services of urban and semi-urban areas with a view to creating opportunity for self-employment.

Urban Cooperative Banks functioning in the State are providing finances for Self-employment to the unemployed youths and other minimum banking services like acceptance of deposit etc. in urban and sub-urban areas. During the year 2009-10, The Dhenknal Urban Cooperative Bank was liquidated in pursuance of the direction of the RBI. Bhadrak UCB was also not permitted by RBI for under taking banking activities. Achievement in this sector is furnished below.

Statutory authority :

The Urban Cooperative Banks function under the control and supervision of two authority i.e. the Reserve Bank of India and the Registrar of Cooperative Societies, Orissa. The RBI is the regulatory authority in respect of Sec.l 1 , Sec. 18, Sec.24 and Sec.35 of the B.R.Act.

Out of the 13 Urban Cooperative Banks functioning in the State, 7 UCBs are earning profit. 6 UCBs are in loss. Financial status of all the UCB is enclosed in the statement.

1. Dhenkanal UCB.

Dhenkanal UCB has been put under liquidation by R.C.S.,Orissa vide order No.3663 dated 17.2.2010 on receipt of requisition from RBI under section 133-A (ii) of the O.C.S.Act, 1962. The D.R.C.S.,Dhenkanal has

13

been appointed as Liquidator of the Bank. As on the date of liquidation, the Bank has to refund Rs. 188.24 lakhs to 1085.89 depositors. As the Bank is an insured Bank, claim statement for 11098 deposited accounts amounting to Rs.828.99 lakhs have been submitted by the Liquidator to the DICGC , Mumbai. Against the liabilities of the Bank, there are Rs. 1078.79 lakhs outstanding on 559 members in shape of loans.

2. Bhadrak UCB.

The RBI after rejecting the application of license for doing banking business made requisition under section 133-A(ii) of the Act to put the Bhadrak Urban Coop.Bank under liquidation. Due to pendency of various litigations in different Courts the liquidation order has not yet been issued. Even though the tenure of the last management expired since 22.6.2008 and Authorised Officer has been appointed, the Authorised Officer i.e. A.R.C.S.,Bhadrak could not be able to function as the Management due to various litigations in different Courts. Although the Bank had been registered as an insured Bank under DICGC Act, no premium has yet been deposited in the DICGC ,Mumbai. Presently the Bank is at dormant /non-functional stage.

3. ChhalrapMir Coop. Bank.

Due to high deteriorating financial condition, RBI imposed restriction u/s 35-A of the B.R.Act since 2007 for which the Bank is unable to tap further deposits and advance loans alongwith restriction on withdrawal above Rs.3000/- per account. Subsequently ,notice under section 22 of the B.R. Act has been issued by the RBI to show cause as to why the license of the Bank to do Banking business shall not be rejected. The Bank has submitted its reply to RBI which is under consideration by its Central office.

There is an elected committee of management in the Bank headed by Sri P.Ch.Senapati as President. One Inspector of CS Sri B.B.Sahoo is working as Secretary of the Bank on attachment basis.

14

URBAN COOPERATIVE BANKS TO ADOPT CORE BANKING SOLUTIONS

Having overcome the turmoil in the cooperative banking sector, urban cooperative banks (UCBs) are all set to adopt the modern technology of core banking solutions (CBS) to expand their reach.

The National Federation of Urban Cooperative Banks and Credit Societies Limited has planned to help relatively weak and smaller UCBs to adopt modern technology and interlinking through the Applications ServiceProvider (ASP) system which would be economical for such banks, Federation president H.K. Patil, and chairman of the Gujarat Urban Cooperative Bank Federation Jyotindra Mehta, said.

The core banking solutions system for UCBs will be formally launched by Union Agriculture Minister Sharad Pawar at a two-day ‘Co-op Core 2010' camp to be held here from December .

Mr. Patil expressed confidence that UCBs in large numbers would opt for the CBS system, and by the end of the next year, at least 300 UCBs, including about 55 in Gujarat, would implement it for the benefit of their account holders.

At present, there are 1,674 UCBs in India with 6,900 branches, including 112 in Gujarat. Only about 80-90 bigger UCBs have implemented the CBS nationally. In Karnataka, however, almost all UCBs have already implemented the CBS system, Mr. Patil said.

He said the CBS interlinking was expected to double the deposits of UCBs from the present Rs.1.82 lakh crore to about Rs.3.60 lakh crore in the next five years.

The introduction of the CBS system will help modernise UCBs, and their six-crore-odd account holders will have access to state-of-the-art banking, including 48,000-odd ATMs of various banks across the country on par with other national and private banks, Mr. Patil said.

The UCBs also plan to appoint “business correspondents” to reach out to unbanked people, who constitute about 55 per cent of the total population in India.

15

Mr. Patil said that under the ASP system, the CBS system will be provided at a monthly rental of Rs.12,900 per branch, which is affordable considering that it was costing anything between Rs.35,000 and Rs.70,000 per month earlier. The banks will now be able to focus only on banking without worrying about the technological aspects of CBS, he said.

Replying to questions, Mr. Patil said about 90 UCBs have merged with other banks over the last five years, and 20-30 per cent had closed down.

Mr. Mehta said that however, after the liquidation of the Madhavpura Cooperative Mercantile Bank following the Ketan Parikh scam about a decade ago, the deposits with cooperative banks in Gujarat — which had been around Rs.14,000 crore — had gone up to over Rs.17,000. He said the UCBs in Gujarat had overcome the problems and were moving forward.

URBAN COOPERATIVE BANKS

Urban cooperative banks, also referred to as primary co-operative banks, play an important role in meeting the growing credit needs of urbanand semi-urban areas of the country. They mobilise savings from themiddle and lower income groups and purvey credit to small borrowers,including weaker sections of the society.These banks in India arefinancial cooperatives akin to credit unions found abroad, except thatthey can also accept deposits from non-members and form a part of the payments systems.

MARKET SHARE OF UCB’S

As on March 31, 2006 there were 1853 UCBs, 84 scheduled commercialbanks, 133 Regional Rural Banks (RRBs) and 398 Rural CooperativeBanks (including 31 State Cooperative Banks and 367 DistrictCooperative Banks) in India. An analysis of market share of various bankgroups indicates that the share of UCBs in total bank deposits isrelatively low. Nevertheless, their market share grew steadily from 3.3%in 1990-91 to a high of 6.6% in 1999-2000, but thereafter graduallydeclined to 4.8% (provisional) in 2005-06, as shown in the following Table.

16

GROWTH

In 1966 when the Banking Regulation Act was made applicable toUCBs, there were about 1100 UCBs with deposits and advances ofRs.167 crore and Rs.153 crore respectively. As at the end of 1996, thenumber of UCBs increased to 1501 and their deposits and advances rose significantly to Rs.24,161 crore and Rs.17,927 crore.The UCBs continuedto grow at a fast pace till 2003, when their number increased to 1941 andtheir deposits and advances to Rs.1,01,546 crore and Rs.64,880 crorerespectively. Subsequently, the number of UCBs declined in 2006 to1853 with total deposits of Rs.1,12,237 crore and advances of Rs.70,379 crore. An overview of their growth since the 1990s is given in Table 2 below.

17

The spectacular growth of UCBs in the late nineties and up to 2003,which had resulted in increasing their penetration, ironically, also led to certain weaknesses in the sector that adversely affected public perception and thereby, their competitiveness. A major reason for thedecline in public confidence was the crisis faced in 2001 by a large multi-state bank in the state of Gujarat, when the bank witnessed a sudden‘run’ on its branches, following rumours of its large exposure to a leadingbroker who had suffered huge losses in the share market. The large-scale withdrawal of deposits within short time had resulted in severeliquidity problems for the bank. The bank was also holding about Rs.800crore of inter-bank deposits from a large number of UCBs in the Stateand from other States, which posed a systemic risk. In order to protectthe interests of the general public and also that of the other co- operativebanks, RBI had issued directions to the bank restricting certainoperations (acceptance of fresh deposits, restricting payments to anysingle depositor to Rs.1000 and ban on fresh lending) and requisitionedthe Central Registrar of Co-operative Societies, New Delhi to supersedethe Board of Directors and appoint an Administrator. An order of moratorium was also enforced on the bank by the Central Governmentfor a short period. The bank was subsequently placed under a scheme of reconstruction with the approval of Reserve Bank of India.

SALIENT FEATURES OF UCB SECTOR

The UCB sector is unique in that there is significant degree ofheterogeneity among the banks in this sector in terms of size,geographical distribution, performance and financial strength. There is also diversity among the urban cooperative banks in the levels ofprofessionalism, standards of corporate governance and access to advanced technology. Most importantly, the banks in this sector areunder dual control, with a part of the powers vested in the StateGovernment and a part with Reserve Bank.

The Reserve Bank is, therefore, continuously evolving the regulatoryand supervisory framework for UCBs to ensure their soundness withoutsacrificing their competitiveness. But before, stepping into the realm ofregulation/ supervision, I would like to elaborate further on the aspect of heterogeneity of UCBs, which would help in better understanding of thesector.

18

HETEROGENEITY

While on the one hand, there are a number of small neighbourhood banks functioning for mutual interest of their members, on the other,there are several large UCBs with a wide network of branches, largenumber of depositors and borrowers, many of whom are medium/largecorporates. In the latter kind of UCBs, the cooperative structureremains only as an organizational arrangement and their businessmodel and goals are more akin to commercial banks. The extent ofheterogeneity can be gauged by size-wise, region-wise and grading-wise analysis of the UCBs.

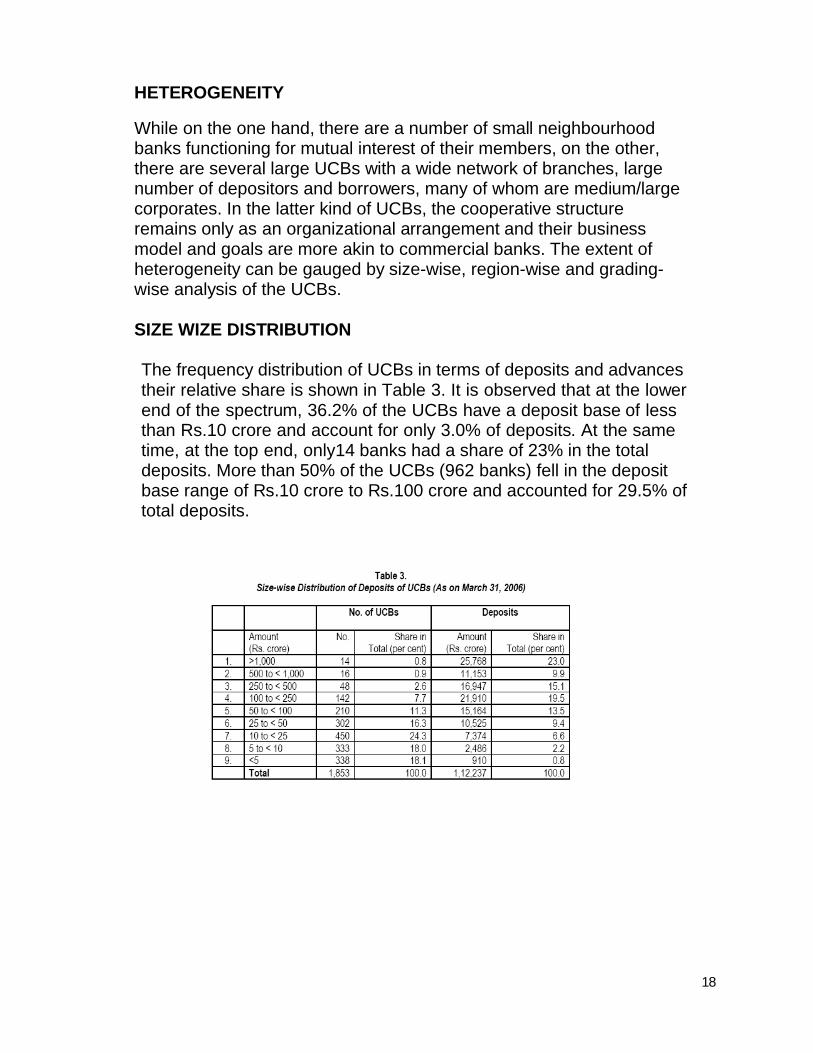

SIZE WIZE DISTRIBUTION

The frequency distribution of UCBs in terms of deposits and advancestheir relative share is shown in Table 3. It is observed that at the lowerend of the spectrum, 36.2% of the UCBs have a deposit base of lessthan Rs.10 crore and account for only 3.0% of deposits. At the sametime, at the top end, only14 banks had a share of 23% in the totaldeposits. More than 50% of the UCBs (962 banks) fell in the deposit base range of Rs.10 crore to Rs.100 crore and accounted for 29.5% of total deposits.

19

REGION WISE DISTRIBUTION

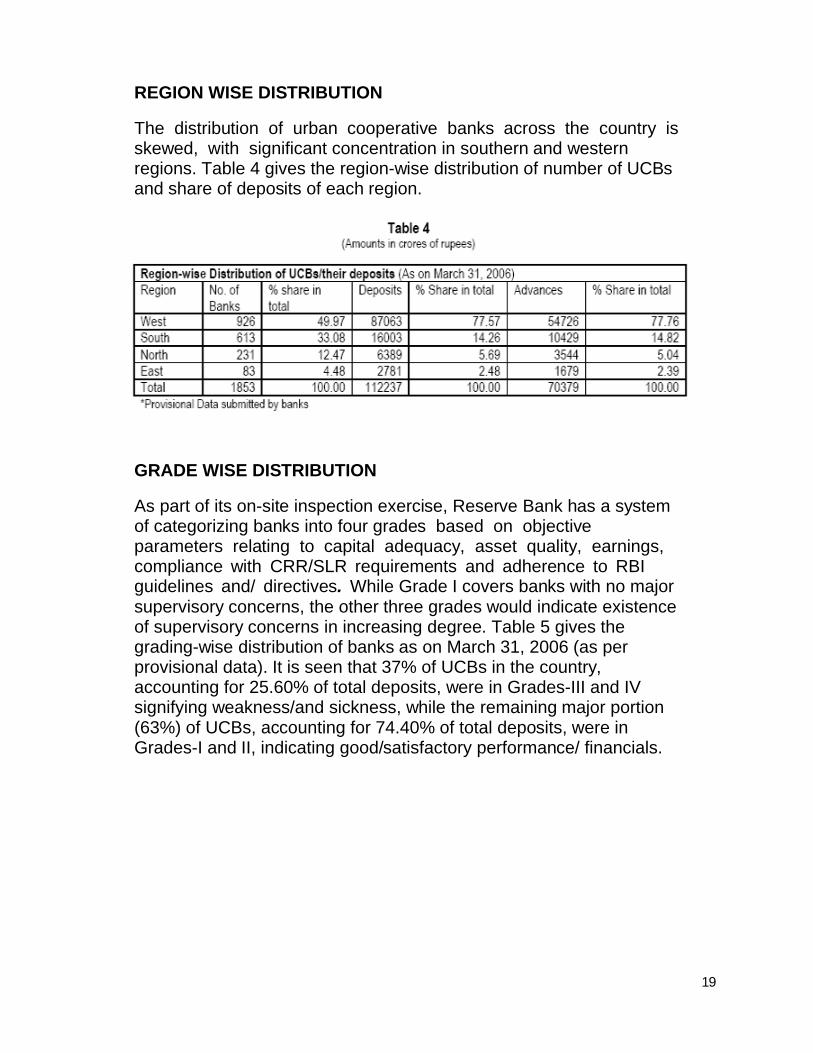

The distribution of urban cooperative banks across the country is skewed, with significant concentration in southern and westernregions. Table 4 gives the region-wise distribution of number of UCBs and share of deposits of each region.

GRADE WISE DISTRIBUTION

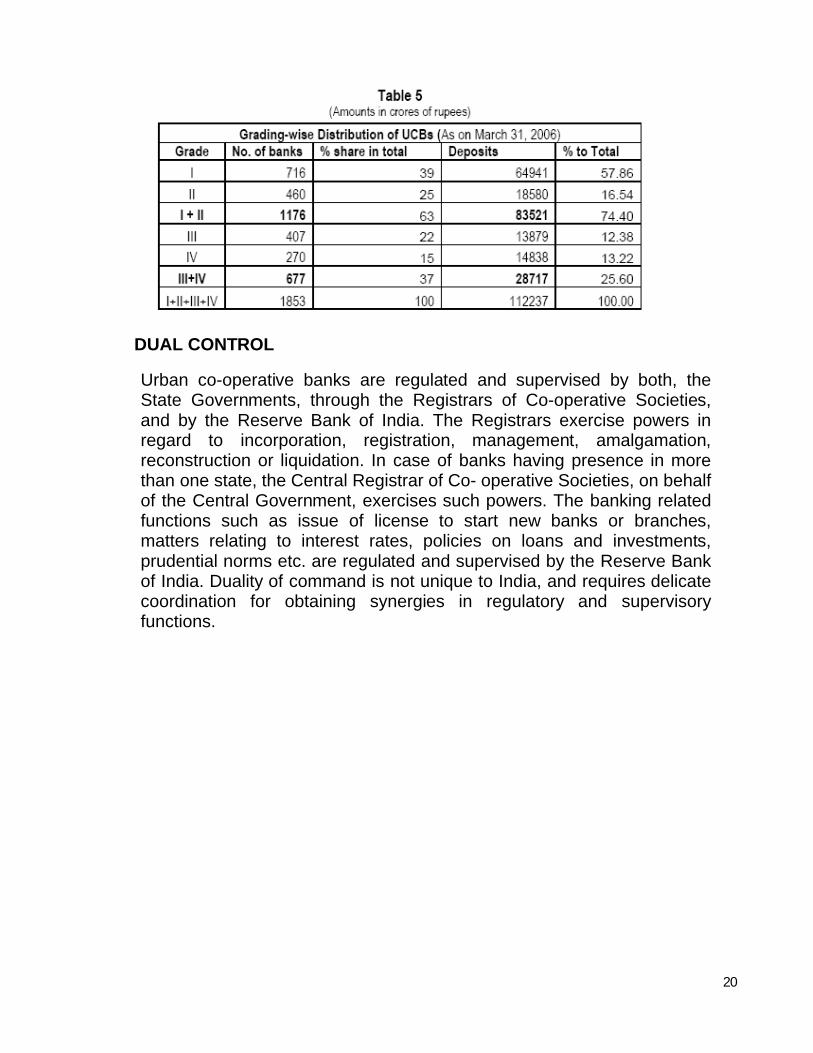

As part of its on-site inspection exercise, Reserve Bank has a system of categorizing banks into four grades based on objective parameters relating to capital adequacy, asset quality, earnings, compliance with CRR/SLR requirements and adherence to RBIguidelines and/ directives. While Grade I covers banks with no major supervisory concerns, the other three grades would indicate existenceof supervisory concerns in increasing degree. Table 5 gives thegrading-wise distribution of banks as on March 31, 2006 (as perprovisional data). It is seen that 37% of UCBs in the country, accounting for 25.60% of total deposits, were in Grades-III and IVsignifying weakness/and sickness, while the remaining major portion(63%) of UCBs, accounting for 74.40% of total deposits, were in Grades-I and II, indicating good/satisfactory performance/ financials.

20

DUAL CONTROL

Urban co-operative banks are regulated and supervised by both, theState Governments, through the Registrars of Co-operative Societies, and by the Reserve Bank of India. The Registrars exercise powers in regard to incorporation, registration, management, amalgamation, reconstruction or liquidation. In case of banks having presence in morethan one state, the Central Registrar of Co- operative Societies, on behalfof the Central Government, exercises such powers. The banking related functions such as issue of license to start new banks or branches,matters relating to interest rates, policies on loans and investments,prudential norms etc. are regulated and supervised by the Reserve Bankof India. Duality of command is not unique to India, and requires delicatecoordination for obtaining synergies in regulatory and supervisory functions.

21

COMPETITION AND UCB’S

MARKET SCENARIO

Since 1991, the financial system has seen several reforms. The process ofliberalization was set in motion with gradual removal of restrictions on the operation of the pricing mechanism, especially interest rates and statutoryliquidity and reserve requirements – a process which is still underway. Enhanced competition in both banking and non-banking financial sectors has been gradually introduced – through a dynamic mix of publicand private as well as domestic and foreign ownership – along withderegulation or adaptive regulations. Simultaneously, regulation and supervision of banks, financial markets and infrastructure were improved toincreasingly align them with international standards and best practices. Themarket driven economy, through deployment of more capital, advancedtechnology and skilled human resources, is posing stiff and increasingcompetition to all traditional institutions.

UCB’S POSITION

Market competition and the need to retain good clientele are affecting the UCBs too leading to squeezing of the margins on many banks, especially the larger ones. The larger private sector commercial banks,with their ability to invest more in technology and offer betterremuneration to attract skilled persons, are better off in fending competition.Understandably, therefore, the UCBs that are competing in the same space,especially in cities and towns, are also being aggressively targeted by thecommercial banks and face tough competition. The smaller unit banks onthe other hand, by and large, manage to retain their niche role through personalized service and informal approach.

CORPORATE GOVERNANCE ISSUES IN UCB’S

Most of the problems faced by the UCBs are due to governance issues andconnected lending. In UCBs borrowers have a significant say in the managements of the banks. This has the potential of influencing the Boardsto take decisions that may not always be in the interest of the depositors who constitute the most important stakeholders of a bank. Also, unlike thecase of institutions the shares of which can be listed in a stock exchangeand can change hands without affecting the capital base, in case of UCBs,the shareholders can withdraw their contribution to capital and shrink thecapital of the bank and thereby limit its ability to increase risk weighted assets and expand business.

22

URBAN BANKS DEPARTMENT

The Urban Banks Department of the Reserve Bank of India is vested with the responsibility of regulating and supervising primary (urban) cooperative banks, which are popularly known as Urban Cooperative Banks (UCBs).

While overseeing the activities of 1926 primary (urban) cooperative banks, the Urban Banks Department performs three main functions : regulatory, supervisory and developmental. The Department performs these functions through its 17 regional offices.

I. Regulatory Functions

(i) Licensing of New Primary (Urban) Cooperative BanksFor commencing banking business, a primary (urban) cooperative bank, as in the case of commercial bank, is required to obtain a licence from the Reserve Bank of India, under the provisions of Section 22 of the Banking Regulation Act, 1949 (As Applicable to Cooperative Societies).

(ii) Licensing of Existing Primary (Urban) Co-operative BanksIn terms of sub-section (2) of Section 22 of the Banking Regulation Act, 1949 (As Applicable to Cooperative Societies), the primary (urban) cooperative banks existing in the country as on March 1, 1966, (when some banking laws were applied to UCBs), were required to apply to the Reserve Bank of India. They were given three months to obtain a licence to carry on banking business. Similarly, a primary credit society which becomes a primary (urban) cooperative bank by virtue of its share capital and reserves reaching Rs. one lakh (Rs.1,00,000) and above was to apply to the Reserve Bank of India for a licence within three months from the date on which its share capital and reserves reach Rs. one lakh. The existing unlicensed primary (urban) cooperative banks can carry on banking business till they are refused a licence by the Reserve Bank of India.

(iii) Branch Licensing

Under the provisions of Section 23 of the Banking Regulation Act, 1949 (As Applicable to Cooperative Societies), primary (urban)

23

cooperative banks are required to obtain permission from the Reserve Bank of India for opening branches.

(iv) Statutory Provisions

The regulatory functions of Urban Banks Department relate to monitoring compliance with the provisions of the Banking Regulation Act, 1949 (As Applicable to Cooperative Societies) by urban cooperative banks. These provisions include :

a. Minimum Share Capital

Under the provisions of Section 11 of the Banking Regulation Act, 1949 (As Applicable to Cooperative Societies), no primary (urban) cooperative bank can commence or carry on banking business if the real or exchangeable value of its paid-up capital and reserves is less than Rs.one lakh.

b. Maintenance of CRR and SLR

As in the case of commercial banks, primary (urban) cooperative banks are also required to maintain certain amount of cash reserve and liquid assets. The scheduled primary (urban) cooperative banks are required to maintain with the Reserve Bank of India anaverage daily balance, the amount of which should not be less than 5 per cent of their net demand and time liabilities in India in terms of Section 42 of the Reserve Bank of India Act, 1934. Non-scheduled (urban) cooperative banks, under the provision of Section 18 of Banking Regulation Act, 1949 (As Applicable to Cooperative Societies) should maintain a sum equivalent to at least 3 per cent of their total demand and time liabilities in India on day-to-day basis. For scheduled cooperative banks, CRR is required to be maintained in accounts with Reserve Bank of India, whereas for non-scheduled cooperative banks, it can be maintained by way of either cash with themselves or in the form of balances in a current account with the Reserve Bank of India or

24

the state co-operative bank of the state concerned or the central cooperative bank of the district concerned or by way of net balances in current accounts with public sector banks. In addition to the cash reserve, every primary (urban) cooperative bank (scheduled/non-scheduled) is required to maintain liquid assets in the form of cash, gold or unencumbered approved securities which should not be less than 25 per cent of the total of its demand and time liabilities in accordance with the provisions of Section 24 ofthe Banking Regulation Act, 1949 (As Applicable to Cooperative Societies).

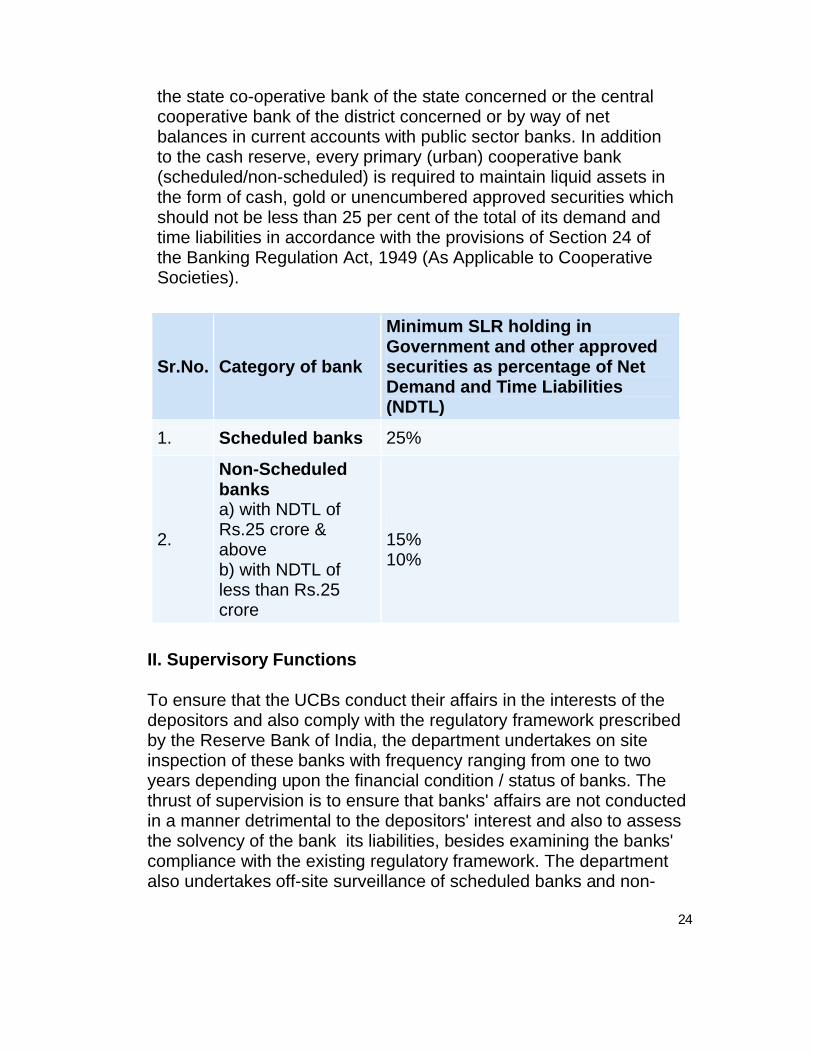

Sr.No. Category of bank

Minimum SLR holding in Government and other approved securities as percentage of Net Demand and Time Liabilities (NDTL)

1. Scheduled banks 25%

2.

Non-Scheduled banksa) with NDTL of Rs.25 crore & aboveb) with NDTL of less than Rs.25 crore

15%10%

II. Supervisory Functions

To ensure that the UCBs conduct their affairs in the interests of the depositors and also comply with the regulatory framework prescribed by the Reserve Bank of India, the department undertakes on site inspection of these banks with frequency ranging from one to two years depending upon the financial condition / status of banks. The thrust of supervision is to ensure that banks' affairs are not conducted in a manner detrimental to the depositors' interest and also to assess the solvency of the bank its liabilities, besides examining the banks' compliance with the existing regulatory framework. The department also undertakes off-site surveillance of scheduled banks and non-

25

scheduled banks with a deposit base of Rs 100 crore and above based on a set of quarterly and annual returns.

III. Developmental Functions

With a view to extending institutional credit support to tiny and cottage units, the Reserve Bank of India grants refinance facilities to urban cooperative banks under the provisions of Section 17 of the Reserve Bank of India Act, 1934. The refinance is given at the Bank Rate.

Training is imparted to the middle and top management of urban cooperative banks through College of Agricultural Banking, Pune.

IV. Sections / Divisions of Urban Banks Department

1. Administration

This Section handles staff matters of the department.

2. New Bank Licensing and Branch Licensing

This section frames policies for issue of bank licence /allots centres for opening of branches and authorizes regional offices to take action accordingly. It also deals with conversion of cooperative credit societies into urban banks.

3. Returns

Returns section at each of the regional offices is responsible for monitoring receipt of various statutory returns under the provisions of Banking Regulation Act, 1949, (AACS) and Sec 42 of Reserve Bank of India Act 1934 in case of scheduled UCBs. They also verify compliance with the provisions of the Acts, ibid, and take suitable action against non-compliant UCBs.

4. Banks Supervision

This section frames policies on prudential norms, investment policies, monitoring priority sector targets, refinancing, issue of directives on

26

interest rates, CRR/SLR, etc. Policies relating to para banking activities such as merchant banking, hire purchase, leasing, insurance business, etc. are also formulated by this division. Besides, the section also attends to compliance with the directions of Local Board / Central Board / BFS, furnishes requisite material for Bank's publications such as Annual Report, Report on Trend and Progress of Banking in India, Currency and Finance, etc.

PROVIDE LICENCES TO NEW UCBS

A Reserve Bank of India-appointed panel has recommended that the existing financially healthy and well managed co-operative credit societies should get priority to start new urban cooperative banks (UCBs). It said new urban banks should be opened only in under-banked and unbanked areas.

In an effort to curb interference by directors (read political elements) with the workings of the bodies, the panel headed by Y H Malegam said the ownership and management in new urban banks should be segregated.

RBI would have unfettered powers to control and regulate the functioning of the new UCBs, management and chief executives. This arrangement will be exactly the same way as RBI controls and regulates a commercial bank.

UCBs, which want to operate only in one state, would need a capital of Rs 50 lakh. The bank which wishes to operate in more than one state after five years would have to start with a capital of Rs 5 crore.

Referring to the organizational structure for the new banks, the committee said it would have a board of management in addition to the board of directors. The management with a chief executive will direct and control the day-to-day workings of the bank. The appointment of the CEO shall be subject to RBI’s approval.

The panel said credit societies, which intent to start urban banks, must satisfy stringent financial health norms before the banking regulator considers their application for license. Such societies should have

27

capital adequacy of not less than 12 per cent. They must have reported net profit for at least three financial years and have net non-performing assets below five per cent of advances. Their credit-deposit ratio must be below 60 per cent

URBAN COOPERATIVE BANKS SCAMS

Urban Cooperative Banks (UCBs) have been in the news for quitesome time for wrong reasons.The collapse of a number of UCBs inMaharashtra, Gujarat and Andhra Pradesh has seriously jeopardizedfinancial interests of millions of small investors. Many desperateinvestors have committed suicide. In September 2003, Aruna andVinita – two sisters ended their lives by consuming poison.Next daytheir brother Achyuta and mother Jana also committed suicide. Thecause of suicide: dejected over not getting back Rs.4 lakhs they haddeposited in the scam hit Charminar Urban Cooperative Bank. In January 2004, a retired employee Mohd.Abdul Basith set himselfablaze and died. He too failed to get his hard earned moneydeposited in Prudential Urban Cooperative Bank, which he needed desperately for performing marriage of his grown up daughters.

In Andhra Pradesh, Charminar Urban Cooperative Bank, Krushi Urban Cooperative Bank, Vasavi Urban Cooperative Bank,Prudential Urban Cooperative Bank and a host of other UrbanCooperative Banks collapsed in quick succession. With over Rs.4000Crores deposits of lakhs of small investors in the UCBs at risk inAndhra Pradesh alone, the State Government took a slew of measures to improve functioning of the UCBs besides initiating civil and criminal action against the wrongdoers.

The sleuths of CID assigned to probe the criminal misdeeds of thescamsters unravelled the whole gamut of criminal activities as well asfinancial mismanagement, which led to the collapse of these Urban Cooperative Banks and arraigned fraudsters to face justice.

GROWTH OF UCBs IN THE STATE:The growth in UCBs since 1997-98 can be ascribed to theliberalization of RBI norms for UCBs and tightening of Non-BankingFinancial Companies (NBFCs) in the wake of CRB scam in 1997. While 69 UCBs came into existence, in nine decades (1906 to

28

1995), as many as 101 UCBs were given licences in just six years.In Hyderabad City and

Ranga Reddy District alone 42 new banks sprung up during thisperiod. Not surprisingly many unscrupulous promoters with dubiouspast obtained licences from the RBI only to loot the public money. And almost all of them are either weak/sick or under liquidation.

FRAUD UNRAVELED

In-depth and thorough investigations revealed a series of illegalitiescommitted by the management and staff of the banks in collusionwith borrowers, which led to the collapse of these banks. Following are some of the glaring acts of criminalities:

• Directors themselves siphoned off crores of rupees never torepay.The loans were availed by them against the specificdirection of the RBI not to sanction big loans to Directors.

• Many of the Directors used the money taken from the bankfor construction of their palatial houses and buying cars.

• Some Directors purchased farmhouses and deposited theamount in their personal accounts.

• The information regarding Directors availing loan was eithernot intimated or partly furnished to the RBI.

• Many of the Directors got crores of rupees sanctioned to their Class-IV employees, though the latter had no credit worthiness and source of income generation. Notsurprisingly these amounts reached the pockets of theirmasters and the amounts were never repaid.

• Term loans were converted into overdrafts and loan amounts were enhanced without any formal request from the borrowers.

• Most of the properties mortgaged were grossly over valued bythe valuators of the banks.

• Single individuals borrowed 25-30 crores from the banks andused the funds for the purpose other than indicated in the proposals.

• In some instances, banks did not enquire about existence ofborrowers let alone about the nature of business mentioned by them.

29

• The Chairman of a Bank purchased shares worth Rs.3.75Crores in his name from the money siphoned off from the bank.

IMPRUDENT BANKING

Prudence is central to banking. But the Prudential Urban Co-operative Bank and other UCBs that collapsed were anything butprudent. In fact, the Prudential Banking norms of the RBI were followed more in breach than in practice.

• The application for sanction of big loans were received in thehead office directly by Chairman / Managing Director and theloan amounts of crores of rupees were sanctioned on thesame day without obtaining any verification reports from the field officers regarding viability of the project / business,repaying capacity, credit worthiness etc. of the applicant.

• The UCBs offered unviable very high interest rates as well asincentives to the depositors.

• The banks continuously defaulted in the maintenance of CRR and SLR.• The CEO sanctioned several advances far in excess of delegated authority.• Observations made by the RBI in its inspection report were ignored.• Establishment costs of banks were far in excess of 2% of the working capital.

• Ignoring the RBI directive, the Banks sanctioned huge loansto the prohibited and risky sectors.

• Many borrowers with no capacity to run business and repay amounts were sanctioned huge loans.

• Some of the big advances sanctioned against mortgage ofimmovable properties without considering the end use.

• Loan proposals instead of routing through the BranchManagers were directly recommended by the Directors.

• In several instances crores of rupees were sanctioned to theindividuals, who were not even income-tax payers.

The Bank placed its funds with other cooperative banks in violation of the RBI directive.

30

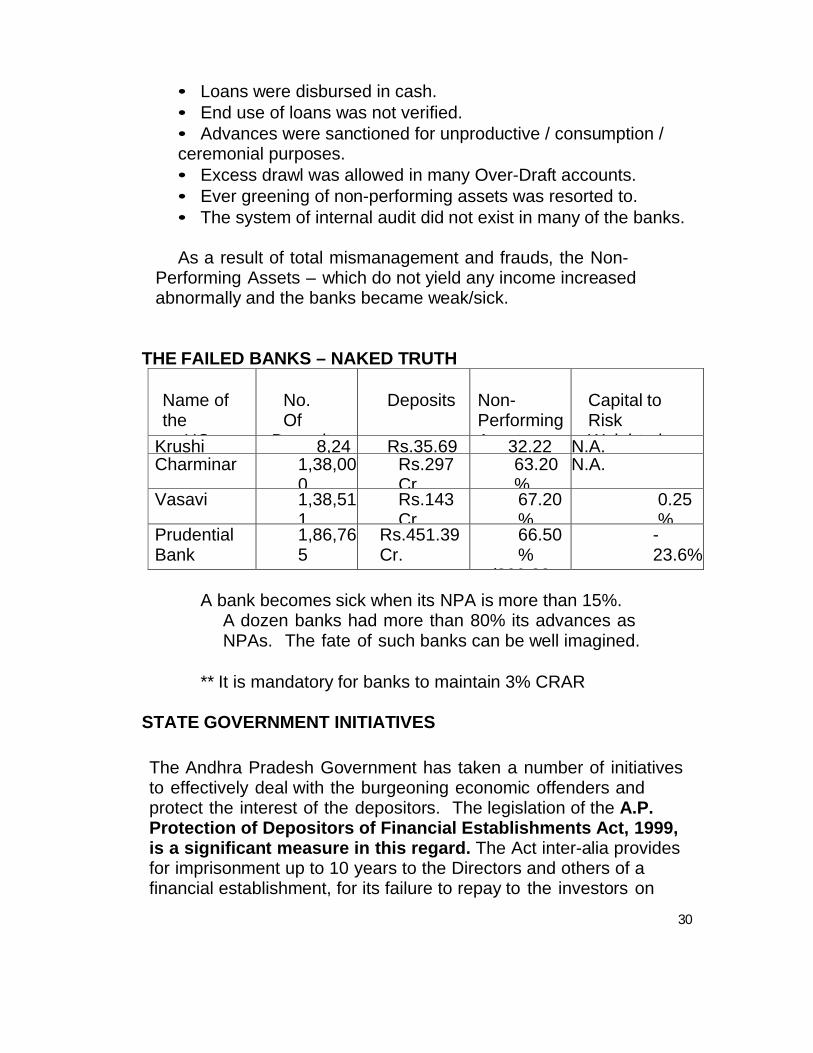

• Loans were disbursed in cash.• End use of loans was not verified.• Advances were sanctioned for unproductive / consumption / ceremonial purposes.• Excess drawl was allowed in many Over-Draft accounts.• Ever greening of non-performing assets was resorted to.• The system of internal audit did not exist in many of the banks.

As a result of total mismanagement and frauds, the Non-Performing Assets – which do not yield any income increased abnormally and the banks became weak/sick.

THE FAILED BANKS – NAKED TRUTH

Name of the

UC

No.Of

Deposito

Deposits Non-Performing Assets

Capital to Risk Weighted Krushi 8,24 Rs.35.69 32.22 N.A.

Charminar 1,38,000

Rs.297Cr.

63.20%

N.A.

Vasavi 1,38,511

Rs.143Cr.

67.20%

0.25%

PrudentialBank

1,86,765

Rs.451.39Cr.

66.50%

(300.22

-23.6%

A bank becomes sick when its NPA is more than 15%.A dozen banks had more than 80% its advances asNPAs. The fate of such banks can be well imagined.

** It is mandatory for banks to maintain 3% CRAR

STATE GOVERNMENT INITIATIVES

The Andhra Pradesh Government has taken a number of initiativesto effectively deal with the burgeoning economic offenders andprotect the interest of the depositors. The legislation of the A.P.Protection of Depositors of Financial Establishments Act, 1999, is a significant measure in this regard. The Act inter-alia providesfor imprisonment up to 10 years to the Directors and others of afinancial establishment, for its failure to repay to the investors on

31

maturity of their deposits. The Act also provides attachment of the properties of the borrowers and disbursement of the liquidated properties on pro-rata basis to the depositors.The State Governmentis likely to enact a special Act for improving functioning of the UrbanCooperative Banks.

The proposed Act prescribes ceilings on the individual exposure as follows:

1) In case of bank having deposit up to Rs.5 Crores - Rs.2 Lakhs

2) In case of banks having deposits above Rs.5 Crores but below Rs.25

Crores – Rs.10 Lakhs

3) In case of bank having deposits above Rs.25 Crores –Rs.20 Lakhs

OR 1% of lendable resources of the bank, whichever is less.

4) Banks having deposits above Rs.100 Crores – Rs.40Lakhs. Further, the offences listed in the proposed Act are being made cognizable.

GENESIS OF URBAN COOPERATIVE BANKING MOVEMENT

2.3 Evolution of urban cooperative banking movement in India canbe traced through 3 distinct phases which are discussed in thesucceeding paragraphs.

Phase I (1904-1966):Inspired by the success of urban cooperative credit movement inGermany and Italy, the first mutual aid society 'ANYONYASAHAKARI MANDALI' was organised in the then princelyState of Baroda in 1889 under the guidance of Late Shri VithalLaxman Kavthekar. The enactment of Cooperative CreditSocieties Act, 1904, however, gave the real impetus to themovement as the first urban cooperative credit society was

32

registered in Canjeevaram town in the then Madras province inOctober, 1904. Thereafter, few more societies were organised inMadras and Bombay provinces.

2.4 In 1912, some major amendments were brought in the Act witha view to broad basing it to enable organisation of non-creditsocieties. The Maclagan Committee's recommendations, as mentioned above, have much to contribute in evolving the urbancooperative credit movement. With the transfer of the subject of"Cooperation" from Central to Provincial Governments, as a sequelto the constitutional reforms popularly known as "MontagueChelmsford Reforms" and passing of the Act of 1919, the thenprovincial Govt. of Bombay passed the first State Cooperative

Societies Act in 19255 " which not only gave the movement its sizeand shape but was a pace setter of cooperative activities and

stressed the basic concept of thrift, self help and mutual aid."6

2.5 In the formative phase, urban cooperative credit societies cameto be organised on community basis and their lending operationswere confined to meeting the consumption oriented credit needs oftheir members. The term 'bank' was very loosely used by manysocieties in the initial phase. Many urban banks which wereorganised in the early part of this century were essentially creditsocieties but later converted themselves into UCBs. Many urbancreditsocieties which were not engaged in any banking functions, also usedthe word 'bank' or 'banker'.There was no well defined concept of urban cooperative bank. It wasthe Joint Reorganisation Committee popularly known as MehtaBhansali Committee (1939) in the then Bombay province, which, forthe first time, made an attempt to define an urban cooperative bank. Itdefined a credit society as an Urban Cooperative Bank (UCB) whosepaid up share capital was Rs.20000 or more and was acceptingdeposits of money on current accounts or otherwise subject towithdrawals by cheque, draft or order. In Madras province, urbancooperative credit societies accepting current account deposits andmaintaining certain amount of liquid resources, as prescribed byRegistrarof Cooperative Societies, had come to be known as UrbanCooperative Banks (UCBs), irrespective of size of their share capital.

33

Subsequently, in 1966, when banking laws wher made applicable tocooperative banks, provisions of section 5(CCV) of BankingRegulation Act, 1949 [ As Applicable to Cooperative Societies (AACS)] defined an Urban Cooperative Bank, as a primary cooperative bankother than a primary agricultural credit society:

(i) the primary object of which is the transaction of bankingbusiness;

(ii) The paid up share capital and reserves of which are not lessthan Rs.1 lakh and

(iii) the by-laws of which do not permit admission of any othercooperative society as a member.

2.6 With the economic boom created by IInd World War, theurban banking sector received tremendous impetus and starteddiversifying its credit portfolio, branching out from meetingtraditional consumption oriented credit needs into catering to theneeds of artisans, small businessmen and small traders.

Phase II (1966-93)2.11 During this period, the demand for extension of depositinsurance was gaining momentum on account of significant increasein the operations of Urban Cooperative Banks and theirvolume of deposits and more particularly in the context of sadexperience of Palai Central Bank failure. As extension of depositinsurance to cooperative banking sector presupposes somesemblance of Reserve Bank control over them, some provisions ofB.R. Act,1949 were made applicable to Urban Cooperative banksin 1966 after an intense debate among StateGovernments, Government of India and RBI. This was a landmark inthe evolution of urban banking movement in India. Consequently, thecooperative banks came under duality of control.

34

The banking related functions such as licensing, branch licensing,area of operation, exposure norms, interest rates etc. are governedby RBI directives and regulations; incorporation and registration ofcooperative banks, audit, management, liquidation, winding up,amalgamation etc., these functions are governed by the StateGovernments by virtue of powers conferred on them by therespective State Cooperative Societies Acts. Ironically, irritantsthrown up by this dual control regime, have become one of the mostvexatious issues before the UCBs and cooperators. The Committeedeals with this very important aspect later in this Report in ChapterVIII.

2.12 It is interesting to note that the Banking Regulation Act doesnot recognise the term 'urban cooperative bank' and defines it as aprimary cooperative bank. The word "primary" is used to denote thatthe bank performs the role of a primary unit in a 3-tier cooperativecredit structure. By this definition, the Urban Cooperative Bankswere made an intergral part of the well developed 3-tier cooperativecredit structure which was developed to cater to the needs of rural India. The Urban Cooperative Banks, by implication, have to beaffiliated to District Central Cooperative Bank (DCCB) at district leveland to State Cooperative Bank (SCB )at apex level and thesebanks, in turn, were supposed to help, nurse and guide the UCBs.Historically, UCBs were organised in semi-urban, urban andmetropolitan centres. This was the reason why they came to bepopularly known as urban cooperative banks. However, thecooperators, UCBs and their federations have, strongly pleaded fordeleting the word 'primary' from the statute in viewof phenomenal increase in their size and operations surpassing evenDistrict Central Cooperative Banks (DCCBs). This issue is examinedlater in Chapter VIII.

2.13 Between 1966-93, the resources mobilised by way of depositsby the UCBs have registered a phenomenal growth. From a meagreRs.153 crores as at the end of June 1967, they rose to Rs.13531crores by the end of March 1993. The credit base surged fromRs.167 crores to Rs.10132 crores during this period. Year wise keyfinancial indicators of UCBs are given in Annexure IV. Theannualised average growth of deposits and advances was found tobe quite impressive. The number of urban cooperative banks hadgrown from 1106 to 1399 during the corresponding period.

35

2.14 A class of urban cooperative banks, which are popularly called,Salary Earners Banks also emerged as a matter of course and hadtheir own place in the urban cooperative banking system over theyears. These banks are essentially thrift societies set up byemployees of governmental departments/ PSUs/large establishmentsfor mutual help on the principles of cooperation. These societies alsostarted using the word 'bank' and were accepting deposits frommembers of public. Since Reserve Bank of India did not find anyrationale for their continuing as banking entities, as they wereessentially thrift societies, they were advised to go out of the purviewof the B.R. Act, after returning the deposits to non-members. As aresult, 599 salary earners banks went outside the purview of the B.R.Act, during the period 1 March, 1966 to 30 June, 1977 by convertingthemselves in to cooperative credit societies. Marathe Committeehad also endorsed this view.As on 31 March,1999, there were 90 salary earners banks.

2.16 The only difference between a primary credit society and anurban cooperative bank is the level of owned funds. If the ownedfunds of primary credit society reaches Rs.1 lakh, automatically, ithas to apply to RBI for a licence to carry on banking business. If aprimary credit society, after attaining Rs.l lakh of owned funds, doesnot meet the criteria laid down by the RBI, it can carry on bankingbusiness till its licence application is rejected by RBI. Due to thispeculiar statutory dispensation, a large number of primary creditsocieties had necessarily to be brought under the ambit of B.R. Act.

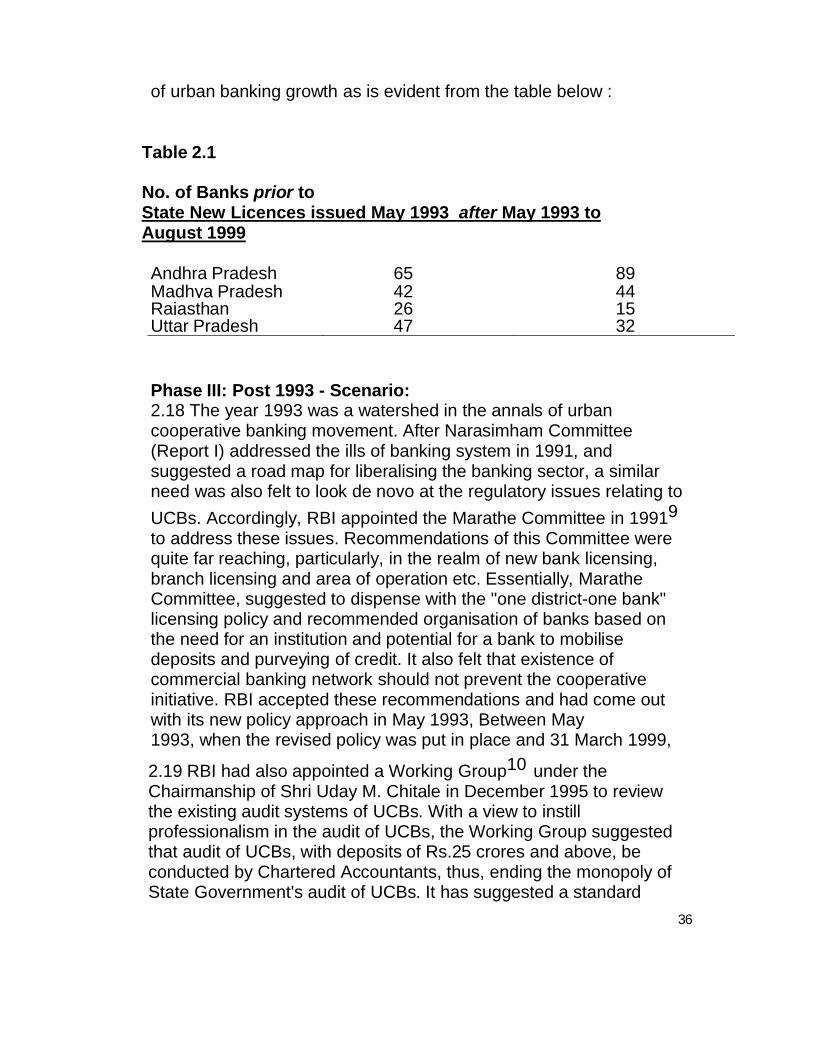

2.17 The period between 1966-1993 can be termed as an overregulated regime. Branch licensing policy was linked to the "plannedexpansion of branches". There were also restrictions on deploymentof UCBs' surplus resources outside the cooperative fold. Growth ofurban banking sector was confined to the states of Maharashtra,Karnataka, Gujarat and Tamil Nadu where the cooperativemovement had already taken strong roots. The regional disparities inthe growth of urban cooperative movement was mostly due to strongcooperative initiative exhibited in these states and absence of similarcooperative leadership in other states. But with liberal licensingpolicy stance of RBI,from May 1993, some states such as MadhyaPradesh, Andhra Pradesh and a few other States have shown signs

36

of urban banking growth as is evident from the table below :

Table 2.1

No. of Banks prior toState New Licences issued May 1993 after May 1993 toAugust 1999

Andhra Pradesh 65 89Madhya Pradesh 42 44Rajasthan 26 15Uttar Pradesh 47 32

Phase III: Post 1993 - Scenario:2.18 The year 1993 was a watershed in the annals of urbancooperative banking movement. After Narasimham Committee(Report I) addressed the ills of banking system in 1991, andsuggested a road map for liberalising the banking sector, a similarneed was also felt to look de novo at the regulatory issues relating to

UCBs. Accordingly, RBI appointed the Marathe Committee in 19919

to address these issues. Recommendations of this Committee werequite far reaching, particularly, in the realm of new bank licensing,branch licensing and area of operation etc. Essentially, MaratheCommittee, suggested to dispense with the "one district-one bank" licensing policy and recommended organisation of banks based onthe need for an institution and potential for a bank to mobilisedeposits and purveying of credit. It also felt that existence ofcommercial banking network should not prevent the cooperativeinitiative. RBI accepted these recommendations and had come outwith its new policy approach in May 1993, Between May1993, when the revised policy was put in place and 31 March 1999,

2.19 RBI had also appointed a Working Group10 under theChairmanship of Shri Uday M. Chitale in December 1995 to reviewthe existing audit systems of UCBs. With a view to instillprofessionalism in the audit of UCBs, the Working Group suggestedthat audit of UCBs, with deposits of Rs.25 crores and above, beconducted by Chartered Accountants, thus, ending the monopoly ofState Government's audit of UCBs. It has suggested a standard

37

No. of Deposits % to totalReporting (Rs. in deposits

format of audit for all the states. The Working Group also suggestedrevised audit rating model for UCBs. Regrettably, none of thestates, not even the cooperatively advanced states, hasimplemented the recommendations of Chitale Working Group.

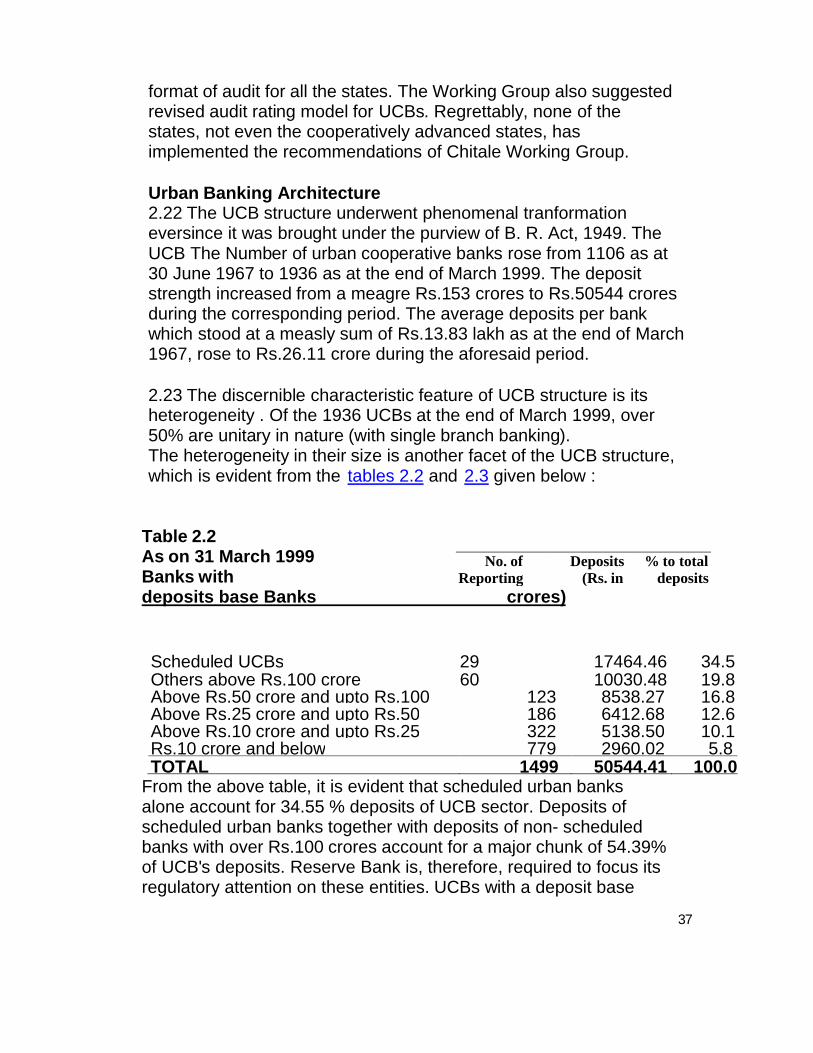

Urban Banking Architecture2.22 The UCB structure underwent phenomenal tranformationeversince it was brought under the purview of B. R. Act, 1949. TheUCB The Number of urban cooperative banks rose from 1106 as at30 June 1967 to 1936 as at the end of March 1999. The depositstrength increased from a meagre Rs.153 crores to Rs.50544 croresduring the corresponding period. The average deposits per bankwhich stood at a measly sum of Rs.13.83 lakh as at the end of March1967, rose to Rs.26.11 crore during the aforesaid period.

2.23 The discernible characteristic feature of UCB structure is itsheterogeneity . Of the 1936 UCBs at the end of March 1999, over50% are unitary in nature (with single branch banking).The heterogeneity in their size is another facet of the UCB structure,which is evident from the tables 2.2 and 2.3 given below :

Table 2.2As on 31 March 1999Banks withdeposits base Banks crores)

Scheduled UCBs 29 17464.46 34.5Others above Rs.100 crore 60 10030.48 19.8Above Rs.50 crore and upto Rs.100 123 8538.27 16.8Above Rs.25 crore and upto Rs.50 186 6412.68 12.6Above Rs.10 crore and upto Rs.25 322 5138.50 10.1Rs.10 crore and below 779 2960.02 5.8TOTAL 1499 50544.41 100.0

From the above table, it is evident that scheduled urban banksalone account for 34.55 % deposits of UCB sector. Deposits ofscheduled urban banks together with deposits of non- scheduledbanks with over Rs.100 crores account for a major chunk of 54.39%of UCB's deposits. Reserve Bank is, therefore, required to focus itsregulatory attention on these entities. UCBs with a deposit base

38

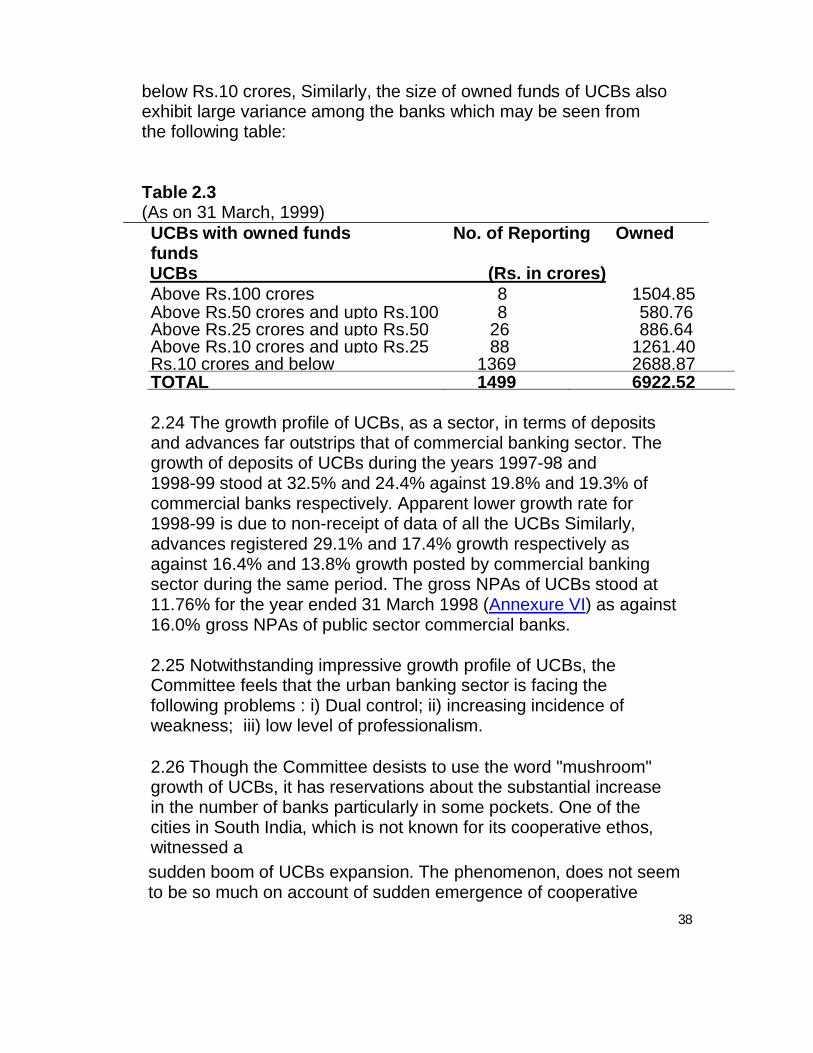

below Rs.10 crores, Similarly, the size of owned funds of UCBs alsoexhibit large variance among the banks which may be seen fromthe following table:

Table 2.3(As on 31 March, 1999)UCBs with owned funds No. of Reporting OwnedfundsUCBs (Rs. in crores)Above Rs.100 crores 8 1504.85Above Rs.50 crores and upto Rs.100 8 580.76Above Rs.25 crores and upto Rs.50 26 886.64Above Rs.10 crores and upto Rs.25 88 1261.40Rs.10 crores and below 1369 2688.87TOTAL 1499 6922.52

2.24 The growth profile of UCBs, as a sector, in terms of depositsand advances far outstrips that of commercial banking sector. Thegrowth of deposits of UCBs during the years 1997-98 and1998-99 stood at 32.5% and 24.4% against 19.8% and 19.3% ofcommercial banks respectively. Apparent lower growth rate for1998-99 is due to non-receipt of data of all the UCBs Similarly,advances registered 29.1% and 17.4% growth respectively asagainst 16.4% and 13.8% growth posted by commercial bankingsector during the same period. The gross NPAs of UCBs stood at11.76% for the year ended 31 March 1998 (Annexure VI) as against16.0% gross NPAs of public sector commercial banks.

2.25 Notwithstanding impressive growth profile of UCBs, theCommittee feels that the urban banking sector is facing thefollowing problems : i) Dual control; ii) increasing incidence ofweakness; iii) low level of professionalism.

2.26 Though the Committee desists to use the word "mushroom"growth of UCBs, it has reservations about the substantial increasein the number of banks particularly in some pockets. One of thecities in South India, which is not known for its cooperative ethos,witnessed a

sudden boom of UCBs expansion. The phenomenon, does not seemto be so much on account of sudden emergence of cooperative

39

spirit/ leadership and entrepreneurial capabilities, as due to stringentnorms regulating NBFCs. Market reports also tend to corroboratethis thinking. The Committee is of the view that the regulator shouldprobe into this phenomenon so as to prevent the spread of weeds incooperative sector.

2.28 The urban cooperative banking sector has come to occupy aformidable place in cooperative structure. It is going to emerge as animportant segment of banking sector in the nextmillennium. The sustainable growth of this buoyant sector,however, depends to a great extent on efficacy of regulation.

REGULATION AND SUPERVISION OF PRIMARY (URBAN)COOPERATIVE BANKS (UCBS)

Primary Cooperative Banks, popularly known as Urban Cooperative Banks (UCBs) are registered as cooperative societiesunder the provisions of, either the State Cooperative Societies Act ofthe State concerned or the Multi State Cooperative Societies Act,2002. They are regulated and supervised by the Registrar ofCooperative Societies (RCS) of State concerned or by the CentralRegistrar of Cooperative Societies (CRCS), as the case may be. Theapplicability of banking laws to cooperatives societies since March 1,1966 ushered in ‘duality of control’ over UCBs between the Registrarof Cooperative Societies/Central Registrar of Cooperative Societiesand the Reserve Bank of India. The Reserve Bank regulates andsupervises the banking functions of UCBs under the provisions ofBanking regulation Act, 1949(AACS). Within the Reserve Bank, aseparate department, viz. Urban Banks Department, has been entrusted with these functions. Urban Banks Department functions inclose coordination with other regulators viz., RCSs and CRCS. Thefunctions of the department can be broadly divided into (i) regulatory(ii) supervisory and (iii) developmental.

The Reserve Bank has been vested powers to issues licence to UCBsunder Section 22 and

23 Banking Regulation Act, 1949 (AACS) to carry on bankingbusiness and to open new places of business(branches, extension

40

counters, etc.) respectively.For this purpose, guidelines on the eligibility crieteria for issue of banking licence / branch licence areissued to UCBs from time to time. As a regulator, the Reserve Bankhas prescribed prudential norms in various areas, e.g. capitaladequacy, income recognition, asset classification and provisioning, exposure to single/group borrowers, exposures tosensitive sectors, loans and advances, investments, liquidityrequirements, etc. Considering the heterogeneity in the sector, adifferentiated regulatory regime is being adopted by Reserve Bank incertain aspects by grouping the UCBs under two Tiers (Tier I and II)based on their branch network, area of operation and the level ofdeposits.

The Banking Regulation Act, 1949(AACS) provides for submissionof periodical returns by UCBs to the Reserve Bank of India. Further,under the powers vested in the Reserve Bank, it has prescribed various other periodical returns to be submitted by UCBs.

The Reserve Bank carries out on-site inspections and off-sitesurveillance of UCBs. It also issues directions and operational instructions to UCBs, wherever necessary to streamline thefunctioning and to protect the interests of the depositors.

As a part of developmental functions, the Reserve Bank impartstraining to the officials ofUCBs to upscale their knowledge, skill and expertise.

The Reserve Bank has entered into memorandum of understanding(MOU) with Central Government and various State Governments forharmonization of regulation and supervision.