Embed Size (px)

Citation preview

1

Roles, Attitudes, and Competencies of Managers of CSR-Implementing Companies in

Malaysia

Maimunah Ismail, Professor Dr Department of Professional Development and Continuing Education

Faculty of Educational Studies Universiti Putra Malaysia

43400 UPM Serdang, Selangor, Malaysia. [email protected]

Muhammad Ibnu Kassim

Department of Professional Development and Continuing Education Faculty of Educational Studies

Universiti Putra Malaysia 43400 UPM Serdang, Selangor, Malaysia

Mohd Rozi Mohd Amit Department of Professional Development and Continuing Education

Faculty of Educational Studies Universiti Putra Malaysia

43400 UPM Serdang, Selangor, Malaysia [email protected]

Roziah Mohd Rasdi, Dr

Department of Professional Development and Continuing Education Faculty of Educational Studies

Universiti Putra Malaysia 43400 UPM Serdang, Selangor, Malaysia.

Stream: Innovation, Sustainability & HRD Submission type: Refereed paper Abstract

Managers play a vital role in helping organizations deal with various corporate social responsibility (CSR) initiatives to stakeholders in communities. Despite the extant literature on CSR and its strategies undertaken by business companies, including multinational corporations (MNCs), little is known about the roles, attitudes, and competencies of CSR managers in executing their CSR tasks in the Malaysian context. This exploratory study investigates the relationship between the corresponding roles, attitudes, and competencies of CSR managers and the CSR orientations of economic, legal, ethical, and philanthropic responsibilities. The study involved 112 managers of CSR-implementing companies in the Klang Valley, a highly industrialized region in Malaysia. We found that the level of perception of roles and competencies of CSR managers is high whereas that for attitudes is moderate. Further, competency is found to be significantly correlated with all CSR

2

orientations. Recommendations for practice and future research on CSR managers are put forth. Keywords: Business company, corporate social responsibility, roles, attitudes, competencies, managers, Malaysia INTRODUCTION The Research Context Corporate social responsibility (CSR) is an interesting area for seeking empirical evidence on

the characteristics of CSR managers. This is due to its multidisciplinary nature and the

multiple types of business corporations involved in CSR as well as the fact that CSR

managers are the middlemen between corporations and society. Conventionally, CSR is

defined as the social involvement, responsiveness, and accountability of companies apart

from their core businesses and beyond the requirements of the law and what is otherwise

required by government (Chapple & Moon, 2005). Specifically, CSR is identified by its

underlying strategic purposes (e.g., legitimacy, responsibility for social externality, and

competitive advantage), its drivers (e.g., market, social regulation, and government

regulation), and its orientations (e.g., economic, legal, ethical, and philanthropy) (Carroll,

1998; Visser, 2008). Studying CSR managers would provide evidence on one of the business-

society relations within companies. It is argued that the personal initiatives of CSR managers

can make a difference in company performance (Hemingway & Maclagan, 2004). This

indicates the importance of identifying the roles, attitudes, and competencies of individual

managers.

A great deal of research has now been conducted on CSR in Western countries

(Anglo-American business systems), but relatively little is focused on Asia, particularly in

Malaysia. With a population of 29.0 million in 2012, it is interesting to note that Malaysia has

undergone tremendous economic changes at the turn of the century. Based on the Human

Development Index (HDI), Malaysia is ranked the highest among Southeast Asian countries

3

(61st) compared to Thailand (103rd), the Philippines (112th), and Indonesia (124th). In 2008,

Malaysia’s foreign direct investment (FDI) was 3.3% of GDP (net inflows) (UNDP, 2011),

which implies that it has a significant influence on the roles of MNCs as investors that bring

in capital in CSR. Furthermore, with the launch of Government Transformation Programs

(GTP) as part of the New Economic Model (NEM) at the beginning of 2010 in Malaysia, the

significance of CSR has increased. CSR is categorized as one of the Strategic Reform

Initiatives (SRIs), one of which is “re-energizing the private sector” in mainstream

development (NEAC, 2010). Therefore, it is envisaged that CSR providers in Malaysia, such

as MNCs and medium and large-scale industrial firms, should complement the tasks of

government-linked companies (GLCs) and government ministries in speeding up the GTPs to

attain the three ambitious policy goals of attaining high income status, inclusiveness, and

sustainability in the society.

In Malaysia, CSR research seems to be limited in its coverage. The available studies

particularly conducted in the twenty-first century are confined to aspects of CSR disclosures

of industrial companies (Nik Ahmad et al., 2003; Mohd Ghazali, 2008). However, these

studies were heavily dependent on annual report documents and information derived from the

companies’ websites. Studies on the development of corporate social reporting of companies

are closely related to the above (Amran & Suppiah, 2007; Amran & Abdul Khalid, 2009).

Other available CSR studies in Malaysia include awareness of CSR among selected

companies (Nik Ahmad & Abdul Rahim, 2005), consumer behavior toward CSR (Abdul

Rahim et al., 2010), and CSR practices among business organizations (Siwar & Md Harizan,

2009). These studies do support our understanding of CSR in the country; however, they are

limited in their scope as they do not address elements of CSR from the perspective of primary

stakeholders, particularly managers.

4

The only relevant studies are on managers’ perception of CSR in the Islamic context

(Dusuki & Dar, 2005; Dusuki, 2006; Siwar & Hossain, 2009) as well as attitudes of

Malaysian managers and executives toward CSR (Abdul Rashid & Abdullah, 1991; Abdul

Rashid & Ibrahim 2002). However, these studies have their own limitations and a lot more on

the perspective of CSR managers remains unexplored. For example, little is known regarding

the roles, attitudes, and competencies of CSR managers as these characteristics are important

for them to function effectively.

The article addresses the following research questions: i) What is the level of roles,

attitudes, and competencies of CSR managers? ii) How do CSR managers perceive the core

CSR orientations of corporations in terms of economic, legal, ethical, and philanthropic

responsibilities? iii) What is the relationship between the level of the roles, attitudes, and

competencies of CSR managers and perceived CSR orientations? This study is significant

because to understand CSR, it is necessary to examine the manner in which managers view

the role of business in society from the perspective of CSR orientations and their own

perceptions of roles, attitudes, and competencies. Most importantly, this study provides

empirical evidence on CSR managers’ characteristics as this may have an implication on the

performance of corporations as the latter is important in responding to the calls of NEM for

the greater contribution of corporations to the country’s economic development.

The remainder of this article is structured in the following manner: The next

subsection continues to describe CSR managers as stakeholders, what drives CSR in

Malaysia, and the study context. Thereafter, a literature review is presented on the mixed

reactions of managers toward CSR particularly in community involvement, the importance of

knowing the characteristics of CSR managers, and the expectations related to the

characteristics of CSR managers in terms of roles, attitudes, and competencies. Then, the

stakeholder theory is discussed as the underlying theory used in this study as well as the CSR

5

orientations based on Visser’s (2008) model. The article proceeds to present the

methodological procedures undertaken, followed by the results of the analysis and

discussions. The article ends with a conclusion that discusses the roles, attitudes, and

competencies of CSR managers and recommendations for practice and future research.

Managers as CSR Stakeholders

Managers are one of the groups of CSR stakeholders. There are two types of CSR

stakeholders: primary and secondary stakeholders (Clarkson, 1995). The primary stakeholder

group is one without whose continuing participation, the company cannot survive as an

ongoing concern. Primary stakeholder groups typically comprise employees such as the

company managers in various job departments, shareholders and investors, customers, and

suppliers, together with what is defined as the public stakeholder group: the government and

communities that provide infrastructures and markets, whose laws and regulations must be

obeyed, and to whom taxes and other obligations may be due. The primary stakeholder

groups have a complex set of relationships among interest groups with different rights,

objectives, expectations, and responsibilities. Dahlsrud’s (2008) definition of CSR includes

stakeholder as one of the five dimensions along with social, economic, environmental, and

voluntariness.

Secondary stakeholders are defined as those who influence or affect, or are influenced

or affected by, the corporation; however, they are not engaged in transactions with the

corporation and are not essential for the survival of the corporation. The media and a wide

range of special interest groups are considered as secondary stakeholders under this

definition. They have the capacity to mobilize public opinion in favor of, or in opposition to a

corporation. Secondary stakeholders may be opposed to the policies or programs that a

6

corporation has adopted to fulfill its responsibilities toward, or to satisfy the needs and

expectations of its primary stakeholder groups.

Drivers of CSR in Malaysia

In Malaysia, CSR is a new concern; the growth of CSR in the country can be attributed to

recent influences that are divided into two categories: internal and external influences. The

internal influences include development initiatives, which as a whole represent the outcome

of the development policies of the country. These initiatives include the development of the

Bursa Malaysia framework in 2006, the emergence of Silver Book in 2006, and the

inauguration of the CSR awards in 2007. On the other hand, the external influences are the

direct and indirect results of globalization, such as the expansion of CSR waves, the spread of

MNCs to developing countries, and the emergence of The Global Compact Network

Malaysia (GCNM).

The most influential internal driver of CSR is The Prime Minister’s CSR Awards

launched by the Ministry of Women, Family, and Community Development in 2007. The

purpose of the awards is to recognize companies that have made a substantial impact on

communities in which they are active through their CSR-related programs. Other equally

significant drivers of CSR in Malaysia are the establishment of CSR guidelines by

institutions such as the National Integrity Plan (NIP) by the Institute Integrity of Malaysia

(IIM) in April 2004, the Silver Book by the Putrajaya Committee on GLC High Performance

(PCG) in September 2006, and the CSR Framework for GLCs by Bursa Malaysia in late 2006

(PEMANDU, 2010). These guidelines strengthen CSR management undertaken by the

various corporations in the country, even though several acts, as indicated above, have

already been in place since the 1970s.

7

The term “waves of CSR” refers to three types of CSR: community involvement,

socially responsible production processes, and socially responsible employee relations

(Chambers et al., 2003; Chapple & Moon, 2005). Waves of CSR appear to be due to the

“multiplier effect” of business conducted by MNCs in the country of operation. Community

involvement, a traditional form of CSR, is generally assumed to refer to philanthropy or

charity (Chapple & Moon, 2005). However, currently, there are other aspects involved in

building business-community relations, for example, partnerships and alliances that go

beyond philanthropy. Socially responsible production reflects the ability of the company to

conduct both its supply chain and on-site operations, in matters related to the environment,

health and safety, human resources, and ethics, in a socially responsible manner. Employee

relations pertain to issues of employee welfare and employee engagement. Socially

responsible employee relations refer to the status of the workforce as stakeholders in the

company’s decision-making process and in the development of CSR practices. This CSR

wave includes initiatives taken by CSR managers and not only aims to improve the well-

being of the employees within the company but also other stakeholders in the community.

This is where CSR managers need to possess relevant behavioral qualities in terms of roles,

attitudes, and competencies.

Other external drivers that corroborate the growth of CSR in Malaysia are the spread

of MNCs in developing countries and the influences of the GCNM. The spread of MNCs is

believed to have been caused by the globalization phenomenon, which affects FDI brought in

by MNCs and by the growth in CSR academic research (Chambers et al., 2003). The GCNM

is a network that functions to promote the principles of the United Nations Global Compact

(UNGC) (UN Global Compact, 2009) concerning human rights, rights of workers,

preservation of the environment, and anti-corruption in Malaysian companies. By connecting

to the network, business companies get an opportunity to showcase their CSR activities

8

internationally and gain access to an arena for interaction with companies and businesses. In

this context, managers help in protecting the interests of their companies and that of

companies’ stakeholders in CSR-related functions.

LITERATURE REVIEW This literature reviews section consists of two parts. The first part discusses the evidence on

the mixed reactions of managers toward CSR and the second part discusses the importance of

knowing their expected roles, attitudes, and competencies in CSR.

Evidence on the Mixed Reactions of Managers toward CSR, Particularly in Community Involvement Lee’s (2008) analysis on the evolutionary path of CSR, as reported by Friedman (1970),

considered CSR managers a liability with highly uncertain outcomes. This led to a significant

resistance toward CSR from companies until the late 1970s. One of the reasons was the

danger of misappropriation of funds by managers because they were perceived as not

possessing sufficient skills and expertise on CSR at the time. An analysis of Friedman’s

(1970) results revealed that the foremost responsibility of corporate managers was to

maximize shareholders’ wealth; managers perceived that community problems should be the

functions of politicians and other community leaders. Hence, managers’ commitment toward

CSR was also low.

Further, managers view that their responsibilities toward employees, customers, and

the government are much easier to visualize and manage than their responsibilities toward

society (Lee, 2008). The reason for this is that the managers’ responsibilities toward the

primary stakeholders are structured in the mission and vision documents of the corporation.

9

However, managers’ responsibilities toward society through CSR are occasionally described

in an ad hoc manner and have a flexible period of accomplishment.

Friedman (1970, cited in McWilliams, Siegel and Wright, 2006) expressed the same

sentiment and added that the mere existence of CSR was a sign of an agency problem within

the firm. The agency theory perspective implies that CSR is a misuse of corporate resources

that would be better spent on valued-added internal projects or returned to shareholders. The

theory also suggests that CSR is an executive perk in the sense that managers may use CSR

to advance their other personal agendas such as selling company’s product which is beyond

their official task.

However, Freeman’s (1984, cited in McWilliams, Siegel and Wright, 2006) assertion

which is in line with stakeholder theory, presented a more positive view of managers’ support

for CSR. He asserted that managers must satisfy a variety of stakeholders such as employees,

customers, suppliers, and local community organizations who can influence the company’s

outcomes. This idea implies that firm engagement in certain CSR activities may enable the

firm to garner support particularly from non-financial stakeholders. The stakeholder theory

was expanded by including the moral and ethical dimensions of CSR, thereby emphasizing

the idea that there is a moral significance for managers to “do the right thing” in their

endeavors.

The Importance of Roles, Attitudes, and Competencies of CSR Managers

The resources in a corporation and its environment, including the community, are linked

through CSR. Hence, the role of management is a key factor in ensuring the success of CSR.

Characteristics specifically roles, attitudes, and competencies of managers, affect the CSR

functions of corporations because these characteristics are considered inputs to the system

10

and performance outputs based on the system theory in management (Fernández, Junquera, &

Ordiz, 2006).

Characteristics of managers are important criteria to be considered in the practice of

human resource development (HRD). In addition, a manager is one of the human resources in

the CSR workplace environment (Bursa Malaysia, 2006; Chapple & Moon, 2005). This

implies that a corporation should ensure a quality work environment in which the roles,

attitudes, and competencies of the employees, including the managers of various job

departments, as one of the primary concerns of the corporation’s management in the pursuit

of creating a knowledgeable workforce. Furthermore, a socially responsible employer

requires functional CSR managers with appropriate roles, attitudes, and competencies.

Expected Roles, Attitudes, and Competencies of CSR Managers

The expected roles, attitudes, and competencies of CSR managers can be described in the

following manner:

i) Fernández et al.’s (2006) study on the profile of an environmental strategies manager

revealed three groups of characteristics: a) managerial attitudes and social influence, b)

individual characteristics, and c) organizational characteristics. Managerial attitudes imply

that managers should have positive attitudes toward creating norms that would clarify the

objectives of environmental management and enable compliance with legislation. Social

influence refers to the sense of duty generated in the environment of the person with

management responsibilities to continue supporting environmental actions. Individual

characteristics relate to knowledge, skills, creativity and efficiency, leadership capability,

individual entrepreneurial ability, and international awareness. Of particular importance

among the individual characteristics is the attitude as it explains the manager’s emotional

11

involvement in and contribution toward CSR issues, as well as the manager’s ability to

identify opportunities that are internal or external to the manager’s organization. Even certain

personal attitudes, such as hedonism, are considered associated with openness to change,

particularly toward CSR innovations (Egri & Herman, 2000).

ii) It has also been revealed that CSR managers should possess technical, interpersonal, and

communication skills because managers need to communicate with external stakeholders

(Egri & Herman, 2000). Technical skills are those related to the company’s products and

processes. They are skills such as those that allow the application of computers to rural

residents and the systematic solving of problems in relation to bridging the digital divide.

iii) There are a number of organizational characteristics that should be possessed by CSR

managers. Two of these are the capability of integrating CSR into the business strategy of the

organization (Cordano & Frieze, 2000) and possessing transformational leadership qualities

(Egri & Herman, 2000; Fernández et al., 2006). The first characteristic is when a manager is

capable of influencing the business strategy, for example, to include environmental

protection. For example, a manager of a pharmaceutical company has the capability of

influencing his company on the use of biodegradable raw material (such as palm oil) in the

production of vitamin E. The second characteristic is very fundamental to organizational

management. Transformational leadership refers to roles of CSR leaders as innovators

(creative problem solving and adjustment), brokers (link groups to obtain resources),

mediators (exercise influence in managing conflict), and mentors (develop human resources),

which as a whole bring innovations to the organization.

iv) Another characteristic that is important for a CSR manager to possess is entrepreneurial

ability. This is considered both a personal and organizational quality. Entrepreneurial ability

is very pertinent for those who perform marketing tasks in addition to CSR tasks.

Entrepreneurial ability also depends on technical skills, particularly in relation to a

12

company’s product processing, manufacturing, and marketing activities (Egri & Herman,

2000). This ability is necessary as it helps the company in promoting its products while

interacting with people in social activities.

The Stakeholder Theory and CSR Orientations The Stakeholder Theory. The theoretical framework of this article is based primarily on the

stakeholder theory. The stakeholder theory proposes that the nature of an organization’s

stakeholders, their values, their relative influence on decisions, their personal and

professional characteristics are among relevant information necessary for predicting

organizational behavior and outcomes (Gioia, 1999; Hung, 2011). Based on Garriga and

Mele’s (2004) analysis, the stakeholder approach combines the integrative and ethical

theories, where the former emphasizes the integration of social demands and the latter

focuses on the right ethics to create a good society. These are supported by the work of

Mitchel, Agle, and Wood (1997), in which balancing the interests of stakeholders is the major

concern, including monitoring and identification of skills and competencies required. The

pluralistic nature of the stakeholder theory is based on the notion that there are many groups

in society apart from owners and employees to whom the corporation is responsible (Jawahar

& McLaughlin, 2001). As a descriptive theory, the stakeholder theory has been used to

describe not only the nature of stakeholders but also the characteristics and profiles of the

managers (Fernández et al., 2006). The stakeholder theory has been used in developing

strategies to improve management of firms and create effective managers who, according to

Bierema and D’abundo (2004), are a group of human resource professionals. Further, the

stakeholder theory considers a firm an interconnected web of different interests where firm

and community interact interdependently and altruism among individuals is a norm (Hung,

2011).

13

Companies should be aware of the fact that CSR does not mean the same thing to all

stakeholders, not even to all employees, including CSR managers. Thus, companies have to

communicate on different policies with concrete examples. They should also develop CSR

training to stimulate exchange and discussion among their employees and contribute to the

creation of a common culture (Sobczak, Debucquet, & Havard, 2006).

Orientation on the CSR Pyramid. This article adopts CSR orientations based on the CSR

pyramid for developing countries (Visser, 2008), which are arranged according to economic,

philanthropic, legal, and ethical responsibilities. It is basically based on the classic Carroll’s

CSR pyramid (Carroll, 1991) ordered as economic, legal, ethical, and philanthropic

responsibilities. Economic responsibility is emphasized the most in all developed and

developing countries and is highly acknowledged by both governments and communities.

Specifically in Malaysia, business companies are expected to function as one of the economic

enablers in the implementation of the NEM through their participation in CSR (PEMANDU,

2010).

Philanthropic responsibility is the second emphasis in developing countries (Visser,

2008). The reasons for this can be described in the following manner: First, there is a strong

indigenous tradition of philanthropy, and in Malaysia it is the old form of CSR known by the

society (Ismail, 2009). Second, philanthropy is considered the most direct way to improve the

well-being of the communities in which corporations’ businesses operate. Third, in the past

five decades, many developing countries have become familiar with donor assistance; hence,

there is an ingrained culture of philanthropy in the community. Furthermore, the term is

almost synonymous with CSR because, generally, developing countries are still at an early

maturity stage of CSR (Visser, 2008).

14

Legal responsibility is the third aspect of this pyramid. Many developing countries are

behind the developed world in terms of incorporating human rights and other CSR issues into

their legislation. However, some countries have made significant progress in strengthening

the social and environmental aspects of their legislation (Visser, 2008). In Malaysia, several

acts have already been in place since the 1970s, such as the Environment Quality Act (1974),

Anti-corruption Act (1977), and Human Rights Commission of Malaysia Act (1999) (Lu &

Castka, 2009).

Ethical responsibility is related to activities and practices that are expected or

prohibited by society for companies to run their businesses (Carroll, 1991). In developing

countries, ethics seems to have the least influence on CSR activities. Accountability to

shareholders, corruption, and transparency in terms of tax payment to the government remain

problematic issues. In contrast, western countries have ascribed a much higher priority to

ethical responsibility in CSR (Visser, 2008).

METHOD

Instrument

The study instrument is a questionnaire that is divided into five sections. The first section

deals with questions on CSR orientations of economic, philanthropic, legal, and ethical

responsibilities. This CSR concept has emerged as an inclusive and global concept that

encompasses corporate social performance, responsiveness, and the entire spectrum of

socially beneficial activities of corporations. An example of item in this section that relates to

economic orientation is, “Our business has a procedure in place to respond to every customer

complaint.” For philanthropic responsibility, an example of item is, “It is important to

perform in a manner consistent with the charitable expectations of society.” Likewise for

15

legal orientation, an example of item is, “It is important to be a law-abiding corporate

citizen”. Finally, an example of item for ethical responsibility is, “It is important to perform

in a manner consistent with expectations of societal mores and ethical norms.”

Questions on roles, attitudes, and competencies of CSR managers are adapted from

Bytheway and Lambert (1998) and Juechter et al. (1998). The second section contains eight

items on roles specifically, the understanding of and views on managers’ roles toward CSR in

community development. An example of an item is, “The CSR manager should take

responsibility to develop a formal policy on sustainable practices toward the community.”

The third section deals with managers’ attitude toward CSR and includes 10 items. An

example of a statement is, “Involvement of business in improving the community’s quality of

life will also improve its long run profitability.” The fourth section contains 16 items on

managers’ competencies in executing CSR in community development. An example of an

item is, “Make CSR plans that are clear and realistic.” Items in all these sections used a

seven-point Likert scale in measuring the CSR orientations and behaviors of managers. The

seven-point Likert scale is chosen over the five-point Likert scale as it increases the

variability of the answers (Grover & Vriens, 2006).

Respondents were required to rate all items based on a scale from 1–7 where “1 =

absolutely untrue” and “7 = absolutely true.” The following are few examples of items

included in the questionnaire: i) Economic responsibility: “It is important for each company

to maintain a strong competitive position”; ii) Legal responsibility: “It is important for each

company to assist the arts and cultural activities”; iii) Legal responsibility: “It is important for

each company to be a law-abiding corporate citizen”; and iv) Ethical responsibility: “It is

important for each company to perform in a manner consistent with expectations of societal

mores and ethical norms.” It is important to relate managers’ perception of CSR orientations

16

with their roles, attitudes, and competencies because the former is related to the fundamental

elements of CSR and the latter is related to the behavioral characteristics of managers. The

relationship between the two aspects is significant in determining the performance of CSR

managers and their companies.

The last section of the questionnaire comprises items on the socio-demographic

profiles of managers. It includes items on the demographic and job information of

respondents such as gender, age, marital status, educational attainment, race, religion,

position in company, nature of organization, industrial sector, monthly income, and years of

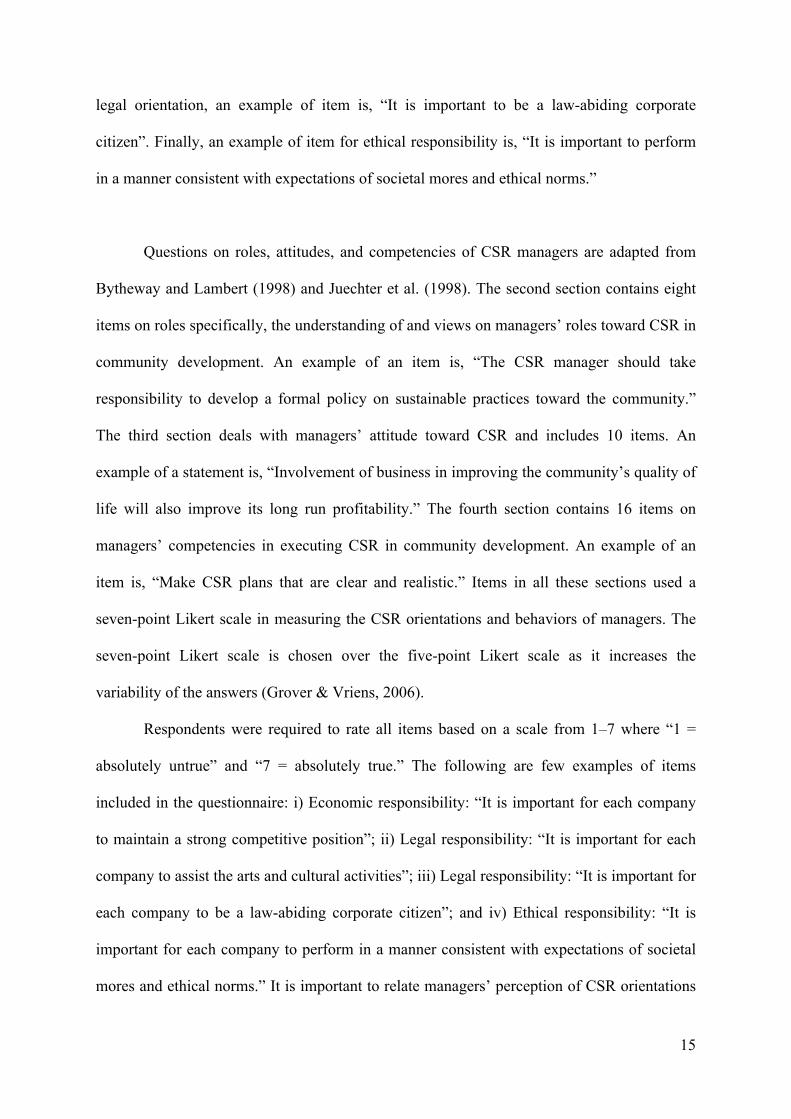

involvement in CSR programs. Based on a pilot test and the actual study, it was found that

the reliabilities of the instruments are acceptable which Cronbach Alpha ranges from .76 to

.87 (in pilot test) and .86 to .90 (in the actual study). Table 1 presents the reliability values for

each section in the pilot test and the actual study.

Table 1: Results of the pilot test and actual study

Pilot test (n = 24) Actual Study (n = 112)

Scale Number of items

Cronbach’s Alpha ( )

Number of items

Cronbach’s Alpha ( )

CSR Orientations:

-Economic

7

.78

7

.89

-Legal 7 .77 7 .88

-Ethical 7 .76 7 .87

-Philanthropic 8 .78 8 .87

Roles 8 .85 8 .90

Attitudes 10 .87 10 .90

Competencies 16 .86 16 .86

Population and Sampling

17

The study population is the CSR managers of local companies and MNCs in the Klang

Valley. The expected total of business companies that are involved in CSR in the Klang

Valley is 350. The average number of respondents from each company is assumed to be two.

Therefore, the population of CSR managers is 700 (350 companies multiplied by 2). Hence,

based on the sampling procedure of Krejcie and Morgan (1970), the sample size required is

248. The sampling and data collection procedures that were undertaken in this study are

described in Figure 1.

The first step was the identification of companies involved in CSR. The second step

was telephonically contacting CSR managers from selected companies. The third step was

setting up an appointment with the respective companies. The fourth and fifth steps involved

the distribution of questionnaires and subsequent collection from the contacted managers of

the companies, respectively.

Respondents were asked to respond to all questions by circling answers that were

most applicable to them. The process of data collection involved “drop-and-pick” technique

and online survey which took place throughout March 2012. The response rate of this study is

quite low (16.7%) given the demanding workload of the samples.

18

Figure 1: The data collection procedure of the study Profile of the Respondents

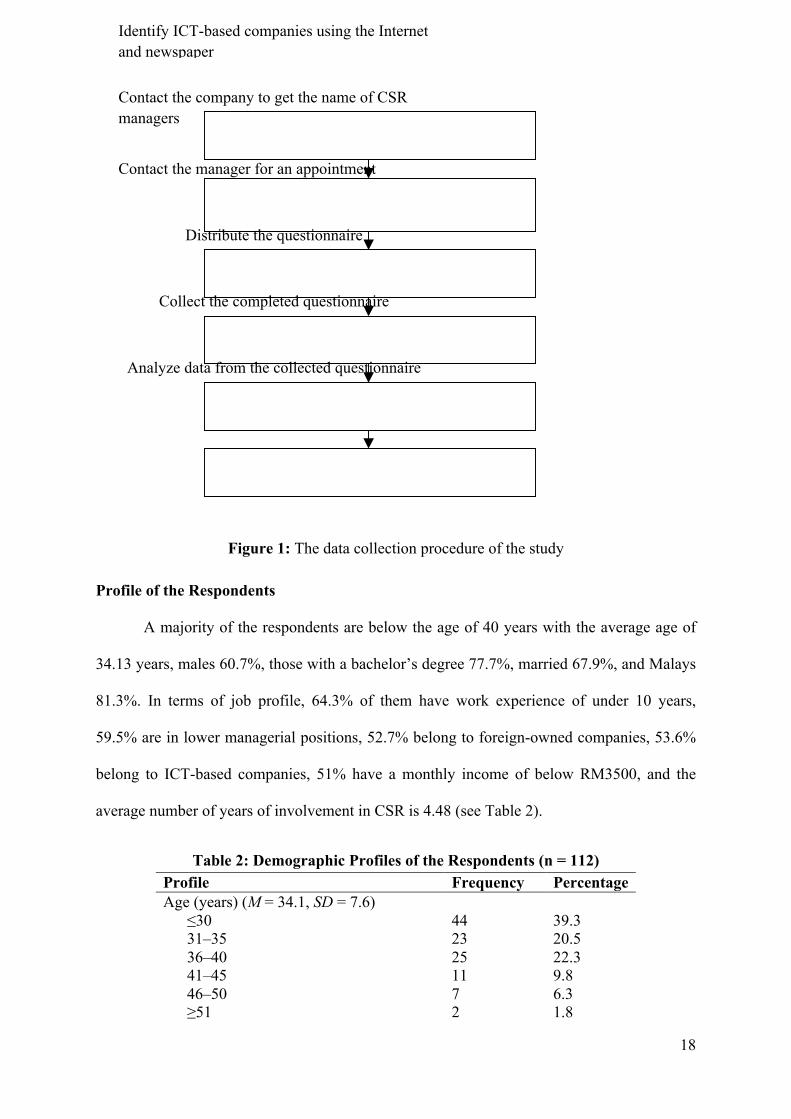

A majority of the respondents are below the age of 40 years with the average age of

34.13 years, males 60.7%, those with a bachelor’s degree 77.7%, married 67.9%, and Malays

81.3%. In terms of job profile, 64.3% of them have work experience of under 10 years,

59.5% are in lower managerial positions, 52.7% belong to foreign-owned companies, 53.6%

belong to ICT-based companies, 51% have a monthly income of below RM3500, and the

average number of years of involvement in CSR is 4.48 (see Table 2).

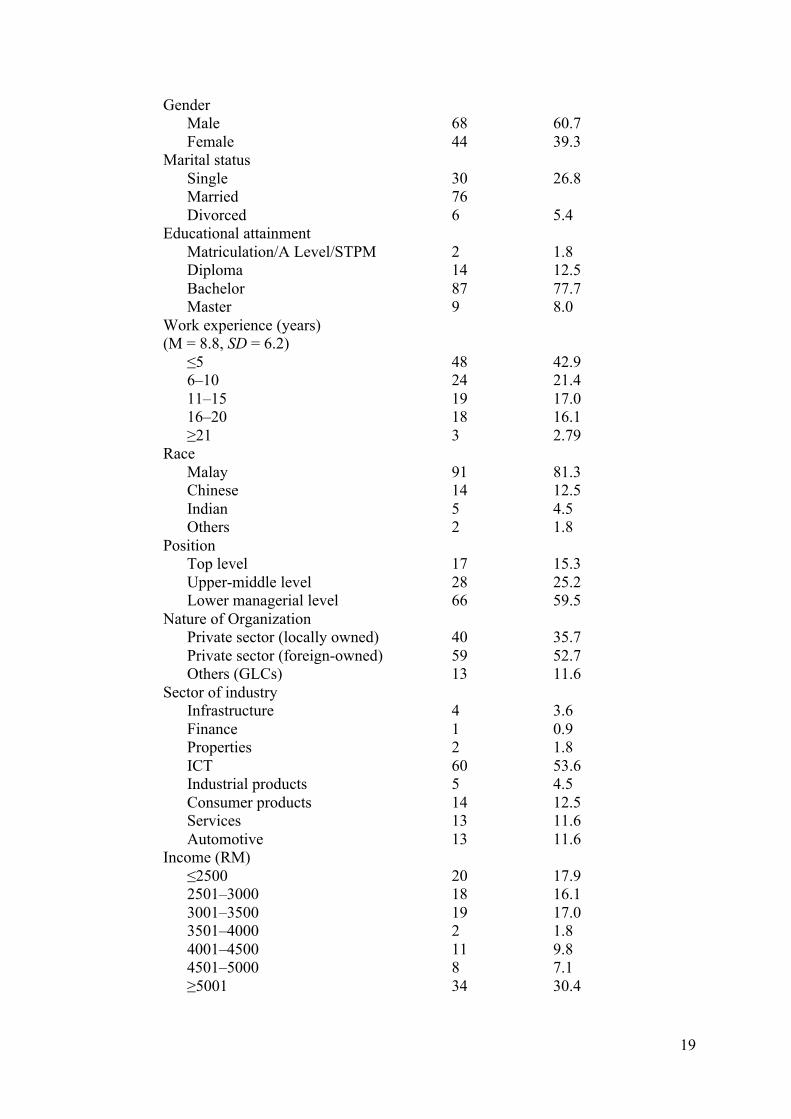

Table 2: Demographic Profiles of the Respondents (n = 112) Profile Frequency Percentage Age (years) (M = 34.1, SD = 7.6) ≤30 31–35 36–40 41–45 46–50 ≥51

44 23 25 11 7 2

39.3 20.5 22.3 9.8 6.3 1.8

Identify ICT-based companies using the Internet and newspaper

Contact the company to get the name of CSR managers

aainvolved Contact the manager for an appointment

Distribute the questionnaire

Collect the completed questionnaire

Analyze data from the collected questionnaire

19

Gender Male Female

68 44

60.7 39.3

Marital status Single Married Divorced

30 76 6

26.8 5.4

Educational attainment Matriculation/A Level/STPM Diploma Bachelor Master

2 14 87 9

1.8 12.5 77.7 8.0

Work experience (years) (M = 8.8, SD = 6.2) ≤5 6–10 11–15 16–20 ≥21

48 24 19 18 3

42.9 21.4 17.0 16.1 2.79

Race Malay Chinese Indian Others

91 14 5 2

81.3 12.5 4.5 1.8

Position Top level Upper-middle level Lower managerial level

17 28 66

15.3 25.2 59.5

Nature of Organization Private sector (locally owned) Private sector (foreign-owned) Others (GLCs)

40 59 13

35.7 52.7 11.6

Sector of industry Infrastructure Finance Properties ICT Industrial products Consumer products Services Automotive

4 1 2 60 5 14 13 13

3.6 0.9 1.8 53.6 4.5 12.5 11.6 11.6

Income (RM) ≤2500 2501–3000 3001–3500 3501–4000 4001–4500 4501–5000 ≥5001

20 18 19 2 11 8 34

17.9 16.1 17.0 1.8 9.8 7.1 30.4

20

Data Analysis Exploratory Data Analysis was first conducted to test all assumptions of parametric analysis.

The levels of roles, attitudes, and competencies of the respondents were described

descriptively as high (5.00 to 7.0), medium (3.00 to 4.99), and low (1 to 2.99). The Pearson

Product Moment Correlation Coefficient was used to identify relationship between the

orientations of CSR practices and the three characteristics of CSR managers. The .05 level of

significance was used in the analysis.

RESULTS AND DISCUSSION

Roles

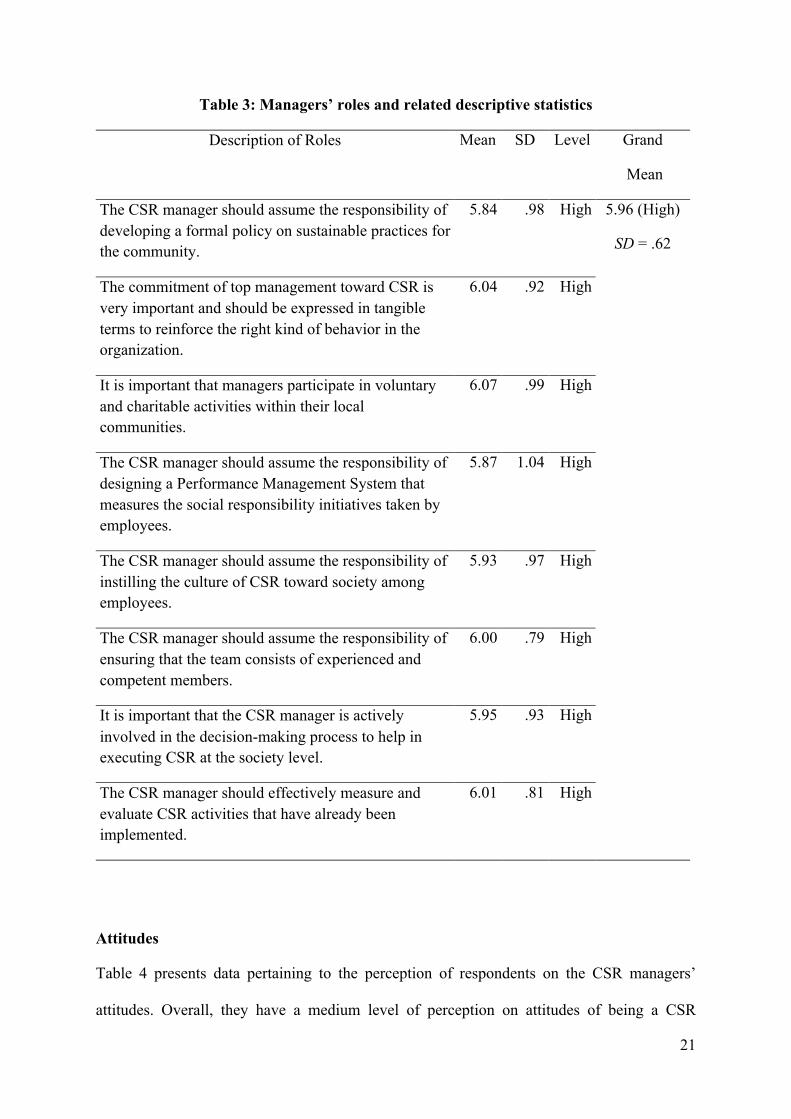

Table 3 shows data pertaining to the perception of respondents on CSR managers’ roles.

Overall, they have a high perception on the eight roles of being a CSR manager with a special

emphasis on the statement that managers should participate in voluntary and charitable

activities within their local communities (M = 6.07, SD =.99). The lowest perceived role is

that the CSR manager should assume the responsibility of developing a formal policy on

sustainable practices for the community (M = 5.84, SD = .98).

Number of years of CSR involvement (M = 4.58, SD = 3.45) ≤5 6–10 11–15 ≥16

81 24 6 1

72.3 21.4 5.4 0.9

21

Table 3: Managers’ roles and related descriptive statistics

Description of Roles Mean SD Level Grand

Mean

The CSR manager should assume the responsibility of developing a formal policy on sustainable practices for the community.

5.84 .98 High 5.96 (High)

SD = .62

The commitment of top management toward CSR is very important and should be expressed in tangible terms to reinforce the right kind of behavior in the organization.

6.04 .92 High

It is important that managers participate in voluntary and charitable activities within their local communities.

6.07 .99 High

The CSR manager should assume the responsibility of designing a Performance Management System that measures the social responsibility initiatives taken by employees.

5.87 1.04 High

The CSR manager should assume the responsibility of instilling the culture of CSR toward society among employees.

5.93 .97 High

The CSR manager should assume the responsibility of ensuring that the team consists of experienced and competent members.

6.00 .79 High

It is important that the CSR manager is actively involved in the decision-making process to help in executing CSR at the society level.

5.95 .93 High

The CSR manager should effectively measure and evaluate CSR activities that have already been implemented.

6.01 .81 High

Attitudes

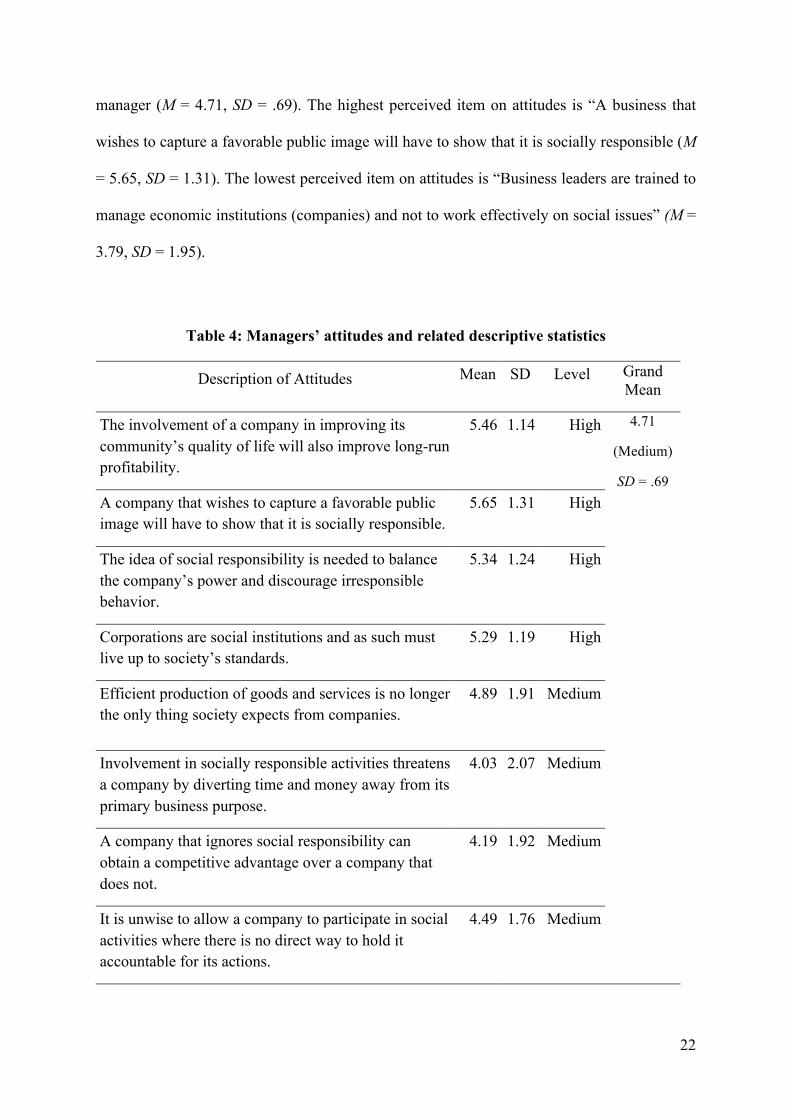

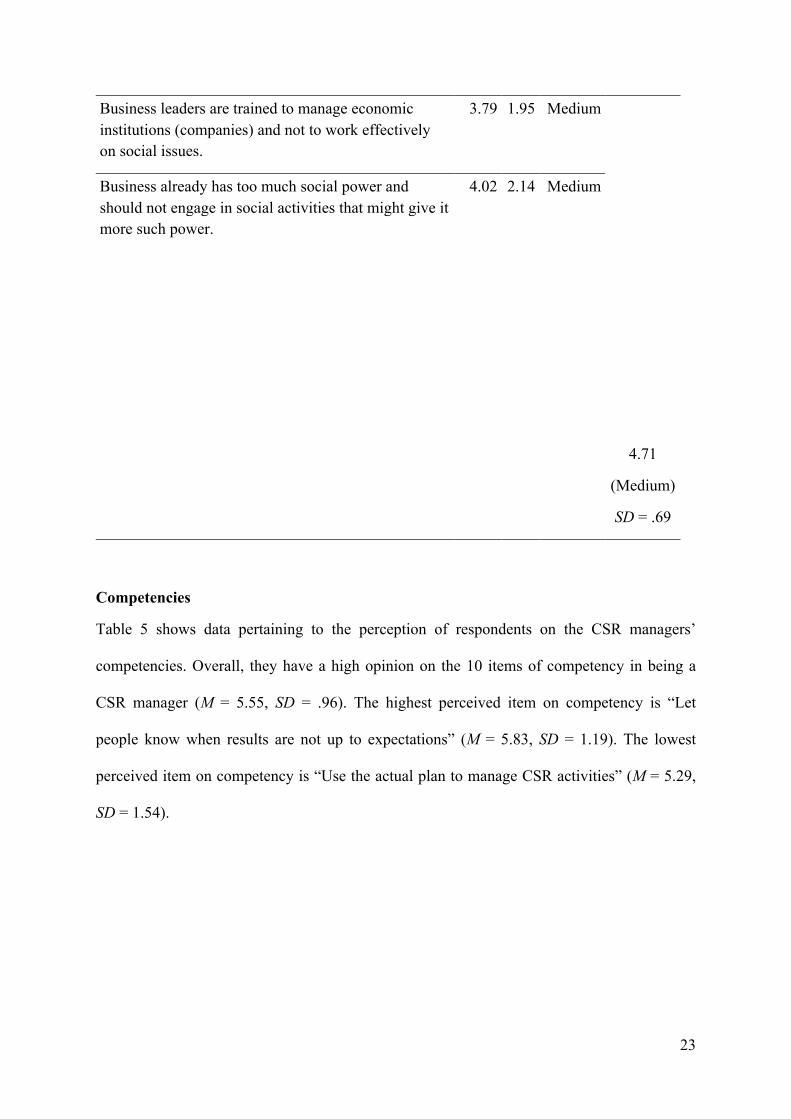

Table 4 presents data pertaining to the perception of respondents on the CSR managers’

attitudes. Overall, they have a medium level of perception on attitudes of being a CSR

22

manager (M = 4.71, SD = .69). The highest perceived item on attitudes is “A business that

wishes to capture a favorable public image will have to show that it is socially responsible (M

= 5.65, SD = 1.31). The lowest perceived item on attitudes is “Business leaders are trained to

manage economic institutions (companies) and not to work effectively on social issues” (M =

3.79, SD = 1.95).

Table 4: Managers’ attitudes and related descriptive statistics

Description of Attitudes Mean SD Level Grand Mean

The involvement of a company in improving its community’s quality of life will also improve long-run profitability.

5.46 1.14 High 4.71

(Medium)

SD = .69

A company that wishes to capture a favorable public image will have to show that it is socially responsible.

5.65 1.31 High

The idea of social responsibility is needed to balance the company’s power and discourage irresponsible behavior.

5.34 1.24 High

Corporations are social institutions and as such must live up to society’s standards.

5.29 1.19 High

Efficient production of goods and services is no longer the only thing society expects from companies.

4.89 1.91 Medium

Involvement in socially responsible activities threatens a company by diverting time and money away from its primary business purpose.

4.03 2.07 Medium

A company that ignores social responsibility can obtain a competitive advantage over a company that does not.

4.19 1.92 Medium

It is unwise to allow a company to participate in social activities where there is no direct way to hold it accountable for its actions.

4.49 1.76 Medium

23

Business leaders are trained to manage economic institutions (companies) and not to work effectively on social issues.

3.79 1.95 Medium

4.71

(Medium)

SD = .69

Business already has too much social power and should not engage in social activities that might give it more such power.

4.02 2.14 Medium

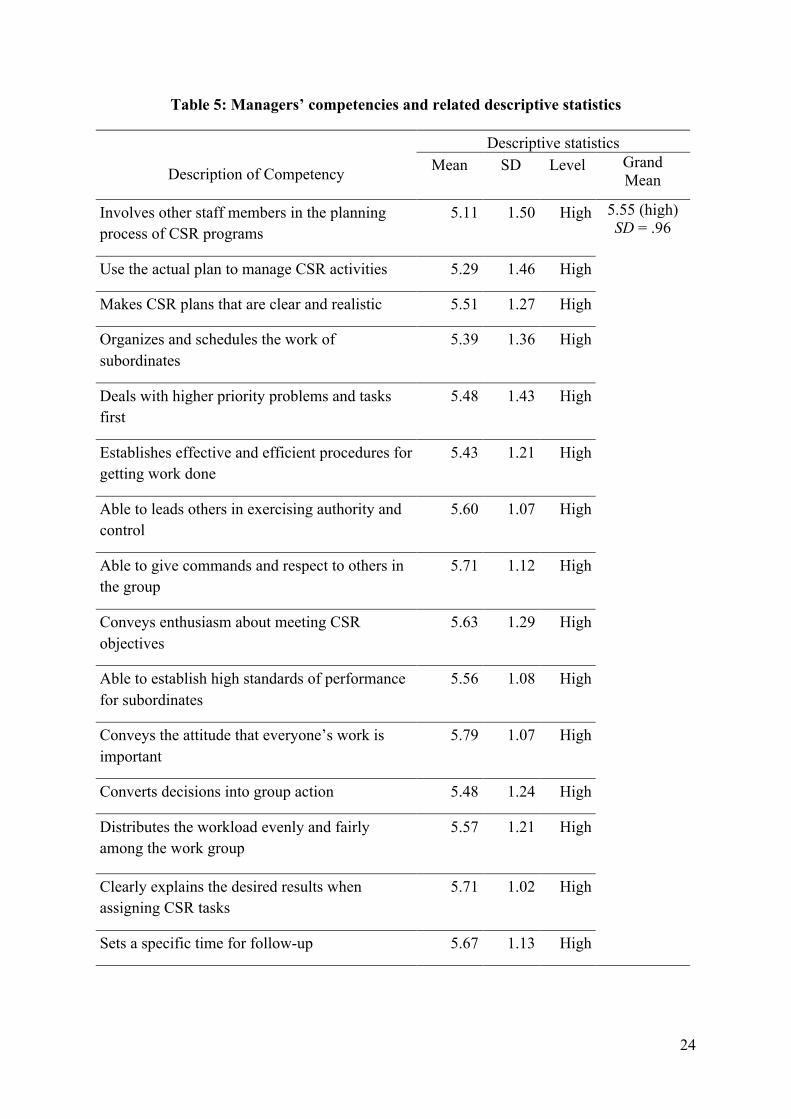

Competencies

Table 5 shows data pertaining to the perception of respondents on the CSR managers’

competencies. Overall, they have a high opinion on the 10 items of competency in being a

CSR manager (M = 5.55, SD = .96). The highest perceived item on competency is “Let

people know when results are not up to expectations” (M = 5.83, SD = 1.19). The lowest

perceived item on competency is “Use the actual plan to manage CSR activities” (M = 5.29,

SD = 1.54).

24

Table 5: Managers’ competencies and related descriptive statistics

Description of Competency

Descriptive statistics Mean SD Level Grand

Mean

Involves other staff members in the planning process of CSR programs

5.11 1.50 High 5.55 (high) SD = .96

Use the actual plan to manage CSR activities 5.29 1.46 High

Makes CSR plans that are clear and realistic 5.51 1.27 High

Organizes and schedules the work of subordinates

5.39 1.36 High

Deals with higher priority problems and tasks first

5.48 1.43 High

Establishes effective and efficient procedures for getting work done

5.43 1.21 High

Able to leads others in exercising authority and control

5.60 1.07 High

Able to give commands and respect to others in the group

5.71 1.12 High

Conveys enthusiasm about meeting CSR objectives

5.63 1.29 High

Able to establish high standards of performance for subordinates

5.56 1.08 High

Conveys the attitude that everyone’s work is important

5.79 1.07 High

Converts decisions into group action 5.48 1.24 High

Distributes the workload evenly and fairly among the work group

5.57 1.21 High

Clearly explains the desired results when assigning CSR tasks

5.71 1.02 High

Sets a specific time for follow-up 5.67 1.13 High

25

Lets people know when results are not up to expectations

5.83 1.19 High

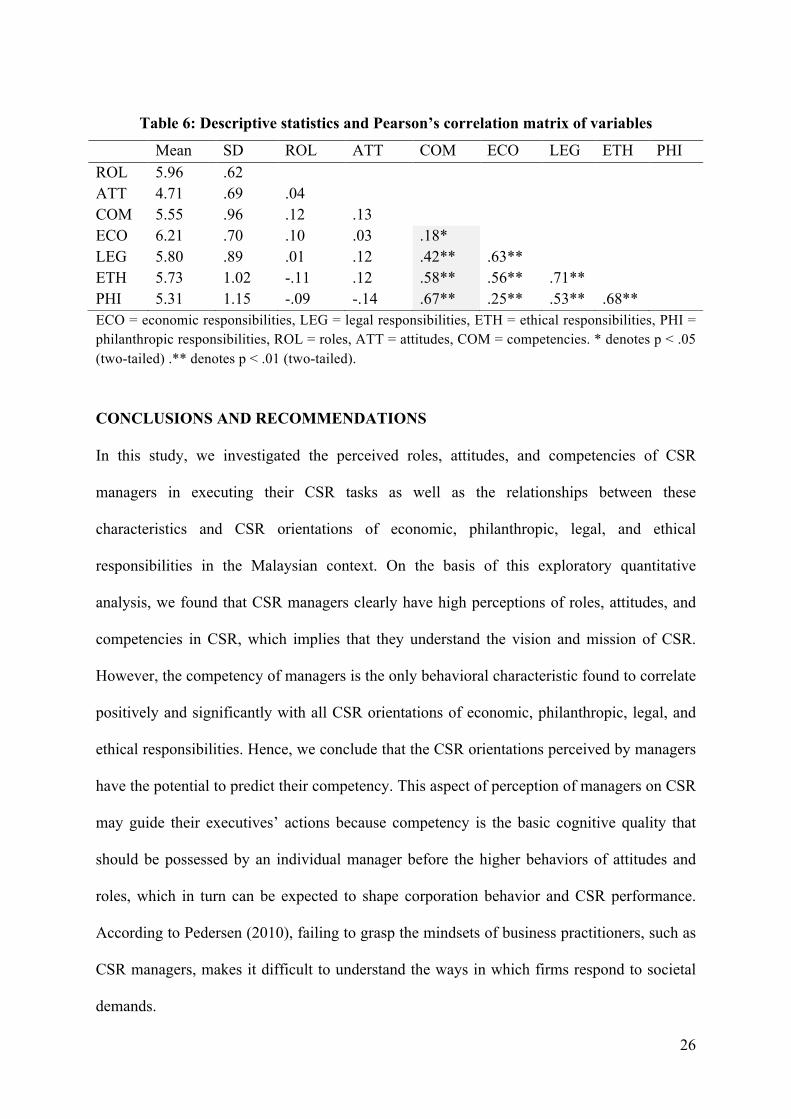

Table 6 presents the means of specific CSR orientations and the coefficients of

correlation among the perceived roles, attitudes, and competencies of CSR managers and the

respective CSR orientations. Respondents reported perceiving CSR orientations in the order

of economic, legal, ethical, and philanthropic responsibilities (M = 6.21, SD = .70; M = 5.80,

SD = .89; M = 5.73, SD = 1.02; and M = 5.31; SD = 1.15). This clearly concurs with Carroll’s

(1991) pyramid in which economic responsibility is at the base and philanthropic

responsibility is at the top. The analysis further revealed that competency of CSR managers

was the only characteristic found to correlate positively and significantly with all the CSR

orientations of economic, legal, philanthropic, and ethical responsibilities (r = .18 to r = .67);

philanthropic responsibility and competency showed the highest correlation. This is

explained by the fact that the former is the oldest form of CSR known by Malaysian society

in general and specifically by CSR managers; ethical and legal responsibilities are the latest

forms of CSR orientations realized in Malaysian society.

26

Table 6: Descriptive statistics and Pearson’s correlation matrix of variables

ECO = economic responsibilities, LEG = legal responsibilities, ETH = ethical responsibilities, PHI = philanthropic responsibilities, ROL = roles, ATT = attitudes, COM = competencies. * denotes p < .05 (two-tailed) .** denotes p < .01 (two-tailed).

CONCLUSIONS AND RECOMMENDATIONS

In this study, we investigated the perceived roles, attitudes, and competencies of CSR

managers in executing their CSR tasks as well as the relationships between these

characteristics and CSR orientations of economic, philanthropic, legal, and ethical

responsibilities in the Malaysian context. On the basis of this exploratory quantitative

analysis, we found that CSR managers clearly have high perceptions of roles, attitudes, and

competencies in CSR, which implies that they understand the vision and mission of CSR.

However, the competency of managers is the only behavioral characteristic found to correlate

positively and significantly with all CSR orientations of economic, philanthropic, legal, and

ethical responsibilities. Hence, we conclude that the CSR orientations perceived by managers

have the potential to predict their competency. This aspect of perception of managers on CSR

may guide their executives’ actions because competency is the basic cognitive quality that

should be possessed by an individual manager before the higher behaviors of attitudes and

roles, which in turn can be expected to shape corporation behavior and CSR performance.

According to Pedersen (2010), failing to grasp the mindsets of business practitioners, such as

CSR managers, makes it difficult to understand the ways in which firms respond to societal

demands.

Mean SD ROL ATT COM ECO LEG ETH PHI ROL 5.96 .62 ATT 4.71 .69 .04 COM 5.55 .96 .12 .13 ECO 6.21 .70 .10 .03 .18* LEG 5.80 .89 .01 .12 .42** .63** ETH 5.73 1.02 -.11 .12 .58** .56** .71** PHI 5.31 1.15 -.09 -.14 .67** .25** .53** .68**

27

An implication of this study to HRD is relevant to the fact that managers in CSR-

implementing companies are also responsible in bringing about a socially conscious HRD, to

use the words of Bierema and D’abundo (2004), in which the concept should be expanded to

activities beyond the organizations to the community. The appropriate level of roles, attitudes

and competencies are the prerequisite qualities of managers to have before they embark on

CSR practices involving the stakeholders. To that end, the companies should conduct some

in-house education on issues related to social consciousness (e.g. diversity training for

various types of stakeholders), and seeks socially, legally as well as ethically responsible

practices and policies when the practices are clearly profitable.

This study is limited to CSR managers’ perception of CSR orientations and their

relationships with characteristics of managers in terms of roles, attitudes, and competencies.

There is a need to investigate the potential of these characteristics of managers in predicting

the performance of the corporation in CSR including the extent to which CSR brings non-

formal education within the specific segments of CSR stakeholders, such as community at

large or school community. Evaluation on CSR programs involving CSR providers and

participants, such as students from public and private universities and recipients in the

community are suggested due to the importance of those participants in CSR chain and its

sustainability.

References

Abdul Rahim, R., Jalaludin, F. W., & Tajuddin, K. (2010). Consumer behaviour towards

corporate social responsibility in Malaysia. International Conference on Business and

Economic Research (ICBER) (pp. 1-17). Kuching: Conference Master. Retrieved

from http://www.internationalconference.com.my/past/icber2010.htm

28

Abdul Rashid, M.Z. & Abdullah, I. (1991). Managers’ attitudes towards corporate social

responsibility. Proceedings of Pan Pacific Conference, June, Kuala Lumpur, pp.218-

220.

Abdul Rashid, M.Z. & Ibrahim, S. (2002). Executive and management attitudes towards

corporate social responsibility in Malaysia. Corporate governance, 2 (4), 10-16.

Bierema L. L. & D'abundo, M. L. (2004). HRD with a conscience: practicing socially

responsible HRD. International Journal of Lifelong Education, 23, (5) (September–

October 2004), 443–458.

Bursa Malaysia. (2006). Corporate social responsibility (CSR) framework for Malaysian

public listed companies. Kuala Lumpur.

Bytheway, A. & Lambert, R. (1998). Organisational competencies for harnessing IS/IT.

Retrieved on May 21, 2012 from

http://www.imbok.org/docs/CompetenciesGoodPracticeGuide.pdf

Carroll, A. B. (1979). A three-dimensional conceptual model of corporate performance.

Academy of Management Review, 4(4), 497-505. http://www.jstor.org/stable/257850

Carroll, A.B. (1991). The pyramid of corporate social responsibility: Toward the moral

management of organizational stakeholders, Business Horizons, July-August, pp. 39-

48.

Carroll, A. B. (1998). The Four Faces of Corporate Citizenship. Business and Society

Review, 100(1), p. 1-7.

Chambers, E., Chapple, W., Moon, J., & Sullivan, M. (2003). CSR in Asia: A seven country

study of CSR website reporting. United Kingdom: International Centre for Corporate

Social Responsibility.

29

Chapple, W. & Moon, J. (2005). Corporate social responsibility (CSR) in Asia: A seven-

country study of CSR web site reporting. Business & Society, 44 (4), December 2005

415-441. DOI: 10.1177/0007650305281658

Clarkson, M. B. E. (1995). A stakeholder framework for analyzing and evaluating corporate

social performance. Academy of Management Review, 20, (1), 92-117.

Cordano, M. and Frieze, I.H. (2000). Pollution reduction preferences of U.S. environmental

managers: Applying Ajzen’s theory of planned behaviour. Academy of Management

Journal, 43, 627-641.

Dahlsrud, A. (2008). How corporate social responsibility is defined: an analysis of 37

definitions’, Corporate Social Responsibility and Environmental Management 15(1),

1–13.

Dusuki, A. W., & Dar, H. (2005). Stakeholders’ Perceptions of Corporate Social

Responsibility of Islamic Banks: Evidence from Malaysian Economy. 389-417.

Dusuki, A. W. (2006). Stakeholders' expectation towards corporate social responsibility of

Islamic Banks. International Accounting Conference III (INTAC 3) (pp. 1-26). Kuala

Lumpur: IIUM.

Egri , C.P. & Herman, S. (2000). Leadership in the North American environmental sector:

values, leadership styles, and context of environmental leaders and their

organizations. Academy of Management Journal, 43, 571-604.

Fernández, E., Junquera, B. & Ordiz, M. (2006). Managers’ Profile in Environmental

Strategy: A Review of the Literature. Corporate Social Responsibility and

Environmental Management 13, 261–274.

Friedman, M. (1970). The social responsibility of business is to increase its profits. The New

York Times Magazine, 13 September, 32–33.

30

Garriga, E. & Mele, D. (2004) Corporate social responsibility theories: Mapping and

territory. Journal of Business Ethics, 53, 51-74.

Gioia, D. A. (1999). Practicability, paradigms, and problems in stakeholder theorizing’,

Academy of Management Review, 24(2), 228–232.

Grover, R., & Vriens, M. (2006). The handbook of marketing research: Uses, misuses, and

future advances. Thousand Oak: Sage Publication. Inc.

Hemingway, C. A. & Maclagan, P. W. (2004). Managers’ personal values as drivers of

corporate social responsibility. Journal of Business Ethics 50: 33–44.

Hung, H. (2011). Directors’ roles in corporate social responsibility: A stakeholder

perspective. Journal of Business Ethics, 103:385–402 .DOI 10.1007/s10551-011-

0870-5

Ismail, M. (2009). Corporate social responsibility and its role in community development: An

international perspective. The Journal of International Research, 2(9), 199-209.

Jawahar, I. M. & McLaughlin, G. L. (2001). Toward a Descriptive Stakeholder Theory: An

Organizational Life Cycle Approach, Academy of Management Review 26(3), 397–

415.

Juechter, W. M., Caroline, F., Alford, R. J. (1998). Five conditions for high performance

cultures. Training and Development, 52(5), 63-67.

Lee, P.M-D. (2008). A review of the theories of corporate social responsibility: Its

evolutionary path and the road ahead. International Journal of Management Reviews,

10(1), 53-73, doi:10.1111/j.1468-2370.2007.00226.x

Lu, J. Y. & Castka, P. (2009). Corporate social responsibility in Malaysia: Experts’ views

and perspectives. Corporate Social Responsibility and Environmental Management,

16, 146-154.

31

McWilliams, A., Siegel, D. S., & Wright, P. M. (2006). Guest editors’ introduction.

Corporate social responsibility: Strategic implications. Journal of Management

Studies, 43:1, 1-18.

Mitchell, R. K., Agle, B. R. & Wood, D. J. (1997). Towards a theory of stakeholder

identification and salience: Defining the principle of who and what really counts,

Academy of Management Review, 22(4),853-886.

National Economic Advisory Council (NEAC) (2010). New Economic Model for Malaysia –

Part 1. Kuala Lumpur: Percetakan Nasional Malaysia Berhad. Available at

http://www.neac.gov.my

Nik Ahmad, N. N., Sulaiman, M., & Siswantoro, D. (2003). Corporate social responsibility

disclosure in Malaysia: An Analysis of Annual Reports of KLSE Listed Companies.

IIUM Journal of Economic and Management , 11 (1), 1-37.

Nik Ahmad, N. N., & Abdul Rahim, N. A. (2005). Awareness of Corporate social

responsibility among selected companies in Malaysia: An Exploratory Note.

Malaysian Accounting Review , 4 (1), 11-24.

Mohd Ghazali, N. A. (2008). Voluntary disclosure in Malaysian corporate annual reports:

Views of stakeholders. Social Responsibility Journal, 4(4), 504-516. doi:

10.1108/17471110810909902

Pedersen, E. R.( 2010). Modelling CSR: How Managers Understand the Responsibilities of

Business towards Society, Journal of Business Ethics, 91,155–166 _ Springer DOI

10.1007/s10551-009-0078-0

Performance Management and Delivery Unit (PEMANDU) (2010). Economic transformation

program. Putrajaya, Malaysia: Performance Management and Delivery Unit

(PEMANDU), Prime Minister’s Department.

32

Sahabat Alam Malaysia (Friends of the Earth Malaysia). Retrieved from

http://www.foei.org/en/who-we-are/member-directory/groups-by-region/asia-

pacific/malaysia.html on 1 June, 2012

Secchi, D. (2007). Utilitarian, managerial and relational theories of corporate social

responsibility. International Journal of Management Reviews, 9, 4, 347-373.

Siwar, C., & Md Harizan, S. H. (2009). A study on corporate social responsibility practices

amongst business organizations in Malaysia. Bangi, Selangor: Institute for

Environment and Development (LESTARI), Universiti Kebangsaan Malaysia.

Siwar, C., & Hossain, T. M. (2009). An analysis of Islamic CSR concept and the opinions of

Malaysian managers. Management of Environmental Quality: An International

Journal , 20(3), 290-298. doi: 10.1108/14777830910950685

Sobczak, A., Debucquet, G. & Havard, C. (2006). The impact of higher education on

students’ and young managers’ perception of companies and CSR: an exploratory

analysis. Corporate Governance. 6 (4), 463-474, DOI 10.1108/14720700610689577

United Nations Global Compact (2009), “Overview of the UN Global Compact” available at

http://www.unglobalcompact.org/AboutTheGC/index.html (accessed 12 December

2008).

United Nations Development Programs (UNDP) (2011). Human Development Report 2011 -

Sustainability and equality: A better future for all. New York: United Nations

Development Programs (21th Anniversary Edition).

Visser, W. (2008) Corporate social responsibility in developing countries, in A. Crane, A.

McWilliams, D. Matten, J. Moon, and D. Siegel, eds., The Oxford Handbook of CSR,

Oxford University Press, Oxford, UK, pp.473-499.