Embed Size (px)

Citation preview

Kehoe & Whitten

34

ROMI: CONCEPT, IMPLEMENTATION AND IMPLICATIONS

Kehoe. William J.

University of Virginia [email protected]

Whitten, Linda K.

Skyline College [email protected]

ABSTRACT This manuscript examines the issue of measurability in marketing. It elucidates the concept of return on investment (ROI) as a platform for introducing the concept of return on marketing investment (ROMI). It examines the implementation of ROMI and considers managerial implications. INTRODUCTION In a survey by Forrester Consulting (Marketing Briefs, 2004) about the challenges faced by marketing managers, a respondent asked the following question: “How can you measure what you can’t touch?” That question reflects the frustration of some managers in contemporary business organizations about the issue of measurability in marketing. Fifty-five percent of the survey’s respondents indicated that measurability in marketing was their greatest challenge, no matter the size of the firm (Marketing Briefs, 2004). A Business Week article (Brady, 2004) confirms the seriousness of the challenge in that, “marketers want to know the actual return on investment (ROI) of each dollar” invested in marketing. The article continues, “They want to know it often, not just annually.” Achieving measurability in marketing is a demanding and important task, particularly “to know it often, not just annually.” Arguably, measurability in marketing is an imperative for business success, particularly in a demanding global environment (Jeannet, 2000; Daniels, Radebaugh and Sullivan, 2002; Yip, 2003; Czinkota, Ronkainen and Donath, 2004; Quelch and Deshpande, 2004). This manuscript addresses the issue of measurability in marketing and posits the concept of ROMI (Return On Marketing Investment) as a metric for achieving measurability in marketing. In exploring the concept of ROMI, first is a presentation of the variables in a marketing decision. Then, there is an examination of the concept of ROI (Return on Investment) as a platform for introducing the concept of ROMI. The manuscript moves next to a discussion the concept of ROMI, including a critical examination of its implementation. The manuscript concludes with consideration of managerial implications in the use of a ROMI metric. OVERVIEW OF MARKETING VARIABLES The 4P’s of marketing - Product, Price, Promotion and Place - provide a prism through which to view the management of an organization’s marketing activities (O’Dell, et al., 1988; Nylen, 1990; Kotler, 2003; Peter and Donnelly, 2003; Kotler and Armstrong, 2004; Albaum, Duerr and Strandskov, 2005; Keegan and Green, 2005; Perreault and McCarthy, 2005; Wood, 2005;

ASBBS E-Journal, Volume 1, No. 1, 2005

35

Hoffman, et al., 2006; Kerin, et al., 2006). Marketing managers influence these four variables in driving organizations forward. The variables combine to yield a cohesive marketing program. In such a cohesive marketing program, a manager “crafts customer value” through careful management of the four marketing variables in a manner to achieve a superior supply chain performance (Malhotra, Gosain and ElSawy (2005), exceptional business growth (McGrath and MacMillan, 2005), and a target return on investment (Duchessi, 2002). Seeking a target return on investment for marketing reflects an emergence of a new conceptualization of marketing as an investment rather than a cost or expense, even though an income statement reflects marketing as an expense. Martyn Straw, Chief Strategy Officer for BBDO Worldwide advertising, in a Business Week article (Brady, 2004), pointedly expresses this new conceptualization as follows: “Marketing has gone from being a cost or expense to an investment. Call marketing an equity investment, and suddenly there’s lots of accountability in the room.” This accountability drives from an emerging imperative for justifying investments in marketing projects in financial terms (Young, 2005) and reflects a different way of thinking about marketing. Rather than viewing money spent on marketing as an expense, an enlightened manager views it as an investment that is measurable through ROI metrics. While the four marketing variables combine in a cohesive marketing program, a manager’s ability to use the marketing variables mediates temporally in that some variables find utilization primarily in the short run while other are more long-run in application. The temporal mediation of the marketing variables affects an organization’s marketing plan as well as its ROI metric. Short-Run Variable : Of the four marketing variables (product, price, promotion and place), the variable price is a short-run variable. As an example of the use of price in the short run, if a firm connects electronically to its retail customers’ inventory control systems, it may be possible to communicate price changes instantly to retail customers, or, failing that, to do so almost instantly through an email distribution list of retail customers. While the variable price is available in the short run, some managers are hesitant to use price. This is true particularly when facing a non-price sensitive demand (i.e., inelastic) and in situations of a manager’s strategy involving large expenditures on consumer advertising. An objective of such advertising is to shift a demand curve to the right (increase units sold), while rotating the demand curve from elastic to a more inelastic configuration. In such an advertising situation, a manger likely will seek to use non-price competition rather than using price as a competitive variable. Therefore, while the execution of price changes occur easily in the short run, other strategic considerations may mitigate the use of price as a competitive option in the short run. Mid-Run Variables: The variables promotion and place are available for managerial intervention in the mid run (i.e., one to two years). Changes in the promotion variable might involve a change in copy or graphics in a particular advertisement, a change in the prevailing theme of an advertising campaign, a change in the scheduling of advertising, a change in advertising budget, or even a change of an advertising agency. The latter change typically requires more time to plan and implement than simply changing a particular ad or modifying a prevailing theme. Changes in the place (distribution) variable may require one to several years for implementation. The time span necessary for changes in the place variable is a function of the quality of the relationships among channel intermediaries, the locus of control in a channel, the amount of inventory in a channel of distribution, the willingness of management to offer inducement to retailers and consumers to stimulate movement of inventory in a channel, and the likelihood of a competitive reaction to a firm’s changes in distribution. All of these considerations suggest that

Kehoe & Whitten

36

changes in place or distribution do not occur easily in the short run; rather changes in place tend to be of a mid-run nature. Long-Run Variable : Product most often is a long-run variable. While some firms might easily change a product in the short run, a product change typically requires long-term planning. Activities such as developing engineering specifications, building a prototype, market testing the prototype, making modifications to production equipment and processes, acquiring materials, employee training, and other activities, all combine to make a change in a product to be of a long-run nature. In each of these marketing variable situations, whether short, mid, or long run in perspective, a manager is in a decision situation of taking action to drive an organization forward. Whatever the action taken and whether within the venue of product, price, promotion, or place, the survey cited at the onset of this manuscript suggests that measurability of results is a primary concern. That is, given the action taken on any of the marketing variables, what is the return on investment as the result of a particular action? Understanding ROI is important because it is a measurement of effectiveness. Measuring marketing effectiveness by ROI-type metrics arguably enables differentiation of superior organizations from competitors. It also mitigates the uncertainty present in some marketing decision situations (Leland, 1972; O’Dell et al., 1988; Nylen, 1990; Jagpal, 1999). CONCEPT OF ROI From a level of abstraction perspective, the concept of ROI is either parsimonious or more complex in application. That is, ROI might simply be the return for a monetary unit invested or it may be more complex in nature. Below are expositions of both a parsimonious and a complex approach to the concept of return on investment. Concept of ROI - Parsimonious : In its most parsimonious presentation, the concept of ROI simply is the amount of return divided by the amount invested (Jablonsky, 1988; Montgomery and Whitten, 1988; Higgins, 2001; Evans, 2002; Reimess, 2003; Baginski and Hassell, 2004; Brigham and Ehrhardt, 2004; Werner and Jones, 2004; Burns, 2005; Horngren, 2005). The amount of return is the income for a year or operating period, while the amount invested is the average amount invested during a year. Analysts may use net income, income before taxes, or operating income in the numerator. It does not matter which income figure is in the numerator as long it is consistently used. The denominator, average amount invested, is either total assets or total operating assets. ROI is one of the most critical measures of a company’s annual performance, although it does not offer many clues as to where a firm is successful or where it may be failing. Evans (2002) describes ROI as a managerial tool that is “application dependent, process dependent, and user dependent” in its calculation and use. That is, in some business organizations, demonstration of a strong ROI is required for a project’s approval. However, in other organizations, ROI is not as significant a hurdle to a project’s initiation. Some managers may require ROI calculation for every project, while other may be selective in its application and use. In sum, the application of ROI varies from company to company and from manager to manager. Evans (2002) suggests that ROI’s application and prominence is cyclical, with greater utilization as a business metric when the economy is slower rather than more robust. Bragg (1999) focuses on situations of “explosive corporate growth” and the value of metrics such a ROI in managing during such periods of growth.

ASBBS E-Journal, Volume 1, No. 1, 2005

37

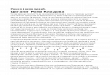

Concept of ROI - Complex: Figure 1 below, adapted from Nickols (2000), depicts a complex presentation of the concept of return on investment. This figure represents the original return on assets portion of the DuPont ROI model, developed in 1919 at E.I. DuPont de Nemours and Co. Implicit in the model is that ROI comprises a measurement of the return on total investment across all operations of a firm (Montgomery and Whitten, 1988; Nickols, 2000; Higgins, 2001; Reimess, 2003; Brigham and Ehrhardt, 2004; Ingram, Albright and Baldwin, 2004; Stickney, Brown and Whalen, 2004; Burns, 2005; Horngren 2005). Many business organizations use the return on assets portion of the model as a primary performance measure when establishing operating objectives. Figure 1: Complex ROI Model - Return on Assets Portion (Adapted from Nickols, 2000) The value of the DuPont Model is that it allows managers to conceptualize and visualize the interaction of the relationships between asset turnover, profit margin, and return on equity (Montgomery and Whitten, 1988). Profit margin measures the profitability of sales, while asset turnover measures the efficiency of assets in generating sales. Return on equity is the relationship between return on assets and the assets to equity ratio. The equity multiplier extends the formula to factor the relationship between debt and equity. Therefore, overall profitability or ROI is a function of profitability of sales, the efficient use of assets, and the extent of debt leverage. The DuPont Model enables management to analyze ways of improving a firm’s performance by evaluating these ratios and considering their implications in making decisions to drive an organization forward. In evaluating profit margin, management can project the effects of changing prices, lowering the cost of inventory, and variations in operating expenses. Possibilities include, for example, raising prices while increasing advertising frequency or lowering prices and offering incentives to increase sales volume. Lowering inventory costs may require strengthening a firm’s purchasing power with current suppliers, developing new supply channels, or, in the case of manufacturers,

Kehoe & Whitten

38

developing more efficient manufacturing processes or outsourcing some or all of the manufacturing process to more efficient suppliers. Analysis of operating expenses, including selling and administrative expenses, requires management to consider the efficiency of a firm’s personnel and measure their productivity in generating revenue and profit. Asset turnover involves measuring the efficient use of assets in generating sales. Inefficient or even under utilization of assets weakens a firm’s ability to achieve a satisfactory asset turnover. While a firm’s engineers may develop more efficient manufacturing processes or better uses for existing plant capacity, management evaluates whether to expand or replace assets. Management may also evaluate alternative means of acquiring manufacturing components and/or raw materials. Decisions on financial leverage require management to analyze the alternative costs of financing strategies and the risk of using debt for leveraging to increase the rate of return on equity. If the firm has no debt, then the ROA and ROE will move together and both then are measure of business risk. Management must determine a firm’s overall risk position. Generally, the uncertainty of future returns on assets is an important consideration in management’s capital structure policy. Management sets targets for the relationship between debt and equity that is within the comfort level of a firm’s stockholders. Debt, or financial leverage, adds risk to the stockholder above business risk. The higher the debt, the higher the potential return will be for the stockholder. Therefore, the optimal debt structure balances risk and return. Usually, this optimal structure is near the industry average for debt/equity. Although higher financial leverage raises overall risk for a firm, it also raises the market expectations for a firm’s future profits. Therefore, management will target a capital structure within the stockholder risk tolerance that will maximize future returns. In summary, the complex concept of ROI aids management in analyzing a firm’s position by considering the relationship between individual ratios and overall return on investment. The DuPont model enables visualization of interrelations of business decisions during a year, allowing management to understand better where strengths and weaknesses exist in order to initiate action within a firm’s financial policies to improve future ROI performance. CONCEPT OF ROMI Given the platform of the concept of ROI, attention turns to the question of effectively integrating ROI as a metric in marketing decision-making. A recent article (Accenture, 2003) reports that 68% of marketing executives have difficulty measuring the ROI of their marketing programs, while 66% of marketing executives realize the importance of being able to demonstrate the financial impact of their decisions. Another article (Brady, 2004) suggests that it is an imperative for marketing managers to address measurability The concept of ROMI reduces the abstraction venue of a marketing decision from analysis at the level of enterprise (as in the situation of complex ROI) to analysis at the level of an individual marketing variable. That is, instead of calculating ROI on the total investments of a firm, ROMI examines the return from a specific investment in particular marketing variables, as in determining the ROMI on an investment in promotion. Underpinning ROMI is a reality in today’s competitive business landscape that managers need to leverage the impact of every currency unit expended. Likewise, as part of the planning process, it

ASBBS E-Journal, Volume 1, No. 1, 2005

39

is necessary to specify measurable objectives to determine through ROMI the effectiveness of a marketing initiative (Kavanaugh, 2001). IMPLEMENTATION OF ROMI Taking a parsimonious approach, ROMI is simply the return of currency units from an investment of a currency unit. For an investment of a currency unit in advertising, what is the return of currency units from the investment? For example, for an investment of a currency unit in advertising, what is the return in sales revenue? Consider a situation of $1 million investment in advertising bringing a return is $15 million in sales revenue, versus a situation where for a $1 million investment the return only is $450,000. Which ROMI would a manager prefer: $15 million/$1 million versus $450,000/$1 million? The answer is axiomatic and demonstrative of parsimonious ROMI. Using a complex approach to ROMI, the DuPont model provides a platform to enable a manager to think creatively and expansively about marketing decisions and the likely return for a currency unit invested. When considering use of any of the four variables of marketing (product, price, promotion, or place), management can visualize the impact of marketing decisions in these variables on return on marketing investment. A marketing manager likely will consider the following financial indices very seriously during a ROMI analysis utilizing a DuPont model frame:

• Total Revenue = Price x Quantity Sold • Total Profit = Total Revenue - Total Cost • Gross Profit Margin = (Sales - COGS)/Net Sales • Operating Profit Margin = Operating Income/Net Sales • Net Profit Margin = Net Income/Net Sales • Inventory Turnover = COGS/Average Inventory • Asset Turnover = Net Sales/Average Total Assets • Return on Assets = Net Income/Average Total Assets • Return on Equity = Net Income/Total Stockholders’ Equity • Return on Beginning Equity = Net Income/Beginning Equity • Equity Multiplier = Total Assets/Total Common Equity

Consider, for example, situations of managing with the price variable and/or with the promotion variable in the context of ROMI utilizing a DuPont model frame. In an examination of the price variable in the context of ROMI with the DuPont model frame, a manager will realize that price changes affect both volume and total sales. At the most efficient price point, total unit sales volume times the selling price theoretically produces the highest short-term revenue for a firm, thereby maximizing total income. A maximizing strategy does not always include an increase in sales volume, but there is virtue in selecting the most efficient point on the demand curve. It depends on a firm’s degree of operating leverage how a change in sales volume affects income. The degree of operating leverage is the relationship of fixed to variable costs. A firm with a higher level of fixed costs in comparison to variable costs, will have a higher operating leverage and therefore a change in sales volume will produce a greater change in income than for those firms with lower operating leverages. As a generalization, firms that are capital intensive or have automated their manufacturing process will have higher levels of operating leverage. Considering the promotion variable in the context of ROMI with a DuPont model frame, the effect of promotion on ROI depends on whether the sales volume changes. When sales volume changes, then both sales and cost of sales will reflect the change in volume. Selling expenses must also increase in the model. If the promotion investment is successful, then profit margin will

Kehoe & Whitten

40

increase due to increased profits. Success also could be measured by dividing the change in gross margin by the change in the promotion costs. If the number is greater than one, then the promotion is successful and net income will increase. If the result is less than one, then the promotion should not be maintained because income will decrease. An added advantage of a successful promotion investment is that as sales volume increases, turnover also increases. Hence, ROMI is improved by both turnover and profit margin gains. MANAGERIAL IMPLICATIONS ROMI utilizing a DuPont model frame is an effective tool for bringing managers to the same point on the same page during the process of making business decisions. Jablonsky (1998) describes it as “a way of visualizing financial information so everyone can see it.” That is, ROMI set in a DuPont model frame provides a unifying conceptual framework for integrating diverse managerial viewpoints in a decision-making setting. Positive Aspects of ROMI: There are many positives to ROMI utilizing DuPont model frame. Blumenthal (1998), writing in CFO Magazine, reports on the experiences of managers in two firms. Caterpillar, Inc. using “return on assets as a primary performance measure and setting targets for each part of the organization, can determine when a problem is related to operating efficiency versus asset utilization.” Caterpillar reports “phenomenal” results using a DuPont model approach. Similarly, managers at Nucor Corporation report “salutary results” in using the model. The company’s CFO says, “All our people understand it.” Brady (2004) reports on successful utilization of ROI-centric marketing measurement by such companies as diverse as Procter & Gamble, Kraft Foods, Gillette, Xerox Corporation, Home Depot, and General Motors. She reports that Procter & Gamble, Kraft, and Gillette use ROI-centric marketing measurement to evaluate marketing effort to sales and brand awareness, while Xerox uses a Six Sigma type ROI metric to analyze return on marketing expenditures. In each of these situations, the objective is to achieve actionable, defensible, and timely ROMI reports. Caveats of ROMI: Caution is necessary when making marketing decisions on a ROI-centric basis. Although some marketing expenditures may increase income, a firm’s ROI may actually decrease. In other words, in such a situation, a marketing plan is marginally successful. Overall, a firm’s net income and EPS increase, but, using the DuPont model, ROI actually decreases. This is why ROMI is superior as a metric for evaluating a marketing program. If ROMI measurement were the change in sales or gross margin divided by the change in marketing expenditures, demonstration of success of marketing strategy would be from a positive change in ROMI. Management, of course, must set realistic time frames for measuring this change. Moreover, it is necessary that management consider the purposes of marketing expenditures. For example, consider expectations for advertising investments. These must be measured based on purpose. Ongoing or reminder advertising would be successful even if the ROMI did not change, reflecting that sales revenue did not decrease. On the other hand, an expectation for new product and/or line extension advertising is higher sales revenues and an increasing ROMI in order to demonstrate success. CONCLUSION As companies move toward implementation of a ROMI or ROI-centric marketing measurement, management will realize accountability and measurement for marketing investments. ROMI is a useful measurement metric for achieving the goal of knowing the return on each dollar of marketing investment “often, not just annually.”

ASBBS E-Journal, Volume 1, No. 1, 2005

41

To know the return on investment “often, not just annually” requires more than the implementation of a ROMI metric. Management must be able easily and readily to input, use, and retrieve ROMI-type data. The use of Excel’s Scenario Manager and Scenario Pivot Tables facilitates ease of use and retrieval in analysis of ROMI data (Weisel, 2005). An emergent technology for ease of input of ROMI data and information is utilization of ROMI-dedicated corporate portal technology. As discussed in a recent article (Goff, 2004), the development of such portal technology is occurring across industry. For example, Mazda North America has a portal to gather ROI data for review sessions with its dealers. Pratt & Whitney uses a portal to gather quarterly reporting information. There are reports of similar portal technology applications by Bank of America, Halliburton, and other companies. Corporate portal technology enable managers at any level easily and readily to input, use, and retrieve return on marketing investment information. Such portals empower managers and stimulate an interest in achieving measurability in marketing. Achieving measurability in marketing is an imperative for business success, particularly in a demanding global environment. REFERENCES Accenture (2003). “Using Customer Insights to Build Brand Loyalty and Increase Marketing

ROI,” Hudson River Group, Valhalla, New York Albaum, Gerald, Edwin Duerr and Jesper Strandskov (2005). International Marketing and Export

Management. Essex, England UK: Prentice Hall/Financial Times Baginski, Stephen P. and John M. Hassell (2004). Management Decisions and Financial

Accounting. Mason, OH: Thomson/South-Western. Blumenthal, Robin (1998). “Tis the Gift to be Simple: Why the 80-year old DuPont Model Still

has Fans,” CFO Magazine, January 1998. Brady, Diane (2004). “Making Marketing Measure Up,” Business Week , December 13, 112-113. Bragg, Steven M. (1999). Managing Explosive Corporate Growth . New York, NY: John Wiley &

Sons, Inc. Brigham, Eugene F. and Michael C. Ehrhardt (2004). Financial Management. Austin, TX:

Harcourt Publishers. Burns, William T., Jr. (2005). Accounting for Managers. Mason, OH: Thomson/South-Western. Czinkota, Michael R., Ilkka A. Ronkainen and Bob Donath (2004). Mastering Global Markets.

Mason, OH: Thomson/South-Western. Daniels, John D., Lee H. Radebaugh and Daniel P. Sullivan (2002). Globalization and Business.

Upper Saddle River, NJ: Prentice-Hall, Inc. Duchessi, Peter (2002). Crafting Customer Value. West Lafayette, IN: Purdue University Press. Evans, Nicholas D. (2002). Business Agility. London, UK: Financial Times/Prentice-Hall, Inc. Goff, John (2004). “Portals: Cutting Through the Clutter,” CFO Magazine, November, 81-88.

Kehoe & Whitten

42

Higgins, Robert C. (2001). Analysis For Financial Management. New York, NY: McGraw-Hill/Irwin.

Hoffman, et al. (2006). Marketing Principles & Best Practices. Mason, OH: Thomson/South-

Western Horngren, Charles T. (2005). Accounting. Upper Saddle River, NJ: Prentice-Hall, Inc. Ingram, Robert W., Thomas L. Albright and Bruce A. Baldwin (2004). Financial Accounting.

Mason, OH: Thomson/South-Western. Jablonsky, Stephen (1998). The Manager’s Guide to Financial Statement Analysis. New York,

NY: John Wiley & Sons. Jeannet, Jean-Pierre (2000). Managing with a Global Mindset. London, UK: Financial

Times/Prentice Hall, Inc. Kavanaugh, Shannon (2001). “Best Laid Plans,” Marketing News, August, 1. Keegan, Warren J. and Mark C. Green (2005). Global Marketing. Upper Saddle River, NJ:

Prentice Hall/Pearson Education, Inc. Kerin, Roger A., Eric N. Berkowitz, Steven W. Hartley and William Rudelius (2006). Marketing.

Boston, MA: McGraw-Hill/Irwin. Kotler, Philip (2003). A Framework for Marketing Management. Upper Saddle River, NJ:

Prentice Hall/Pearson Education, Inc. Kotler, Philip and Gary Armstrong (2004). Principles of Marketing. Upper Saddle River, NJ:

Prentice Hall/Pearson Education, Inc. Malhotra, Arvind, Sanjay Gosain and Omar A. ElSawy (2005). “Absorptive Capacity

Configurations in Supply Chains”, MIS Quarterly, Volume 29 (March), 145-187. Marketing Briefs (2004). “The ROI Challenge,” Marketing Management, October, 4. McGrath, Rita Gunther and Ian C. MacMillan (2005). “Market Busting: Strategies for

Exceptional Business Growth,” Harvard Business Review, Volume 83 (March), 70-79. Montgomery, A. Thompson and Linda K. Whitten (1988). Financial Accounting Information: An

Introduction to Its Preparation and Use. Dubuque, Iowa: Kendall/Hunt Publishing Company.

Nickols, Fred (2000). “The DuPont ROI Model,” http://home.att.net/~nickols/dupont.htm

Nylen, David W. (1990). Marketing Decision-Making Handbook. Englewood Cliffs, NJ: Prentice-Hall, Inc.

O’Dell, William F., Andrew C. Ruppel, Robert H. Trent and William J. Kehoe (1988). Marketing

Decision Making: Analytical Framework and Cases. Cincinnati, OH: South-Western Publishing Company.

ASBBS E-Journal, Volume 1, No. 1, 2005

43

Perreault, William D., Jr. and E. Jerome McCarthy (2005). Basic Marketing: A Global-Managerial Approach. New York, NY: McGraw-Hill/Irwin.

Peter, J. Paul and James H. Donnelly, Jr. (2003). A Preface to Marketing Management. New

York, NY: McGraw-Hill/Irwin Quelch, John and Rohit Deshpande (2004). The Global Market. San Francisco, CA: Jossey-Bass. Reimess, Jane L. (2003). Financial Accounting Integrated. Upper Saddle River, NJ: Prentice-

Hall, Inc. Saloner, Garth, Andrea Shepard and Joel Podolny (2001). Strategic Management. New York,

NY: John Wiley & Sons, Inc. Stickney, Clyde P., Paul Brown and James M. Wahlen (2004). Financial Reporting and

Statement Analysis. Mason, OH: Thomson/South-Western. Weisel, James A. (2005). “Add Even More Muscle to What-If Analyses,” Journal of

Accountancy, Volume 199 (March), 76-79. Werner, Michael L. and Kumen H. Jones (2004). Introduction to Financial Accounting. Upper

Saddle River, NJ: Prentice-Hall, Inc. Wood, Marian Burk (2005). The Marketing Plan Handbook. Upper Saddle River, NJ: Prentice

Hall/Pearson Education, Inc. Yip, George S. (2003). Total Global Strategy. Upper Saddle River, NJ: Prentice Hall, Inc. Young, Debby (2005). “Money Matters: The Importance of Justifying Projects in Financial

Terms,” Enterprise Leadership , Volume 3 (1), 18-22. Acknowledgements : A presentation of an earlier version of this manuscript was in February 2005 at the 12th Annual Meeting of the American Society of Business and Behavioral Sciences. The manuscript received a Best Paper Award at that meeting and an invitation for publication in the ASBBS E-Journal. The authors thank anonymous reviewers for their helpful and thoughtful comments about the manuscript. The authors acknowledge and thank Dean Carl P. Zeithaml, Senior Associate Dean Ellen M. Whitener, and Area Coordinator John H. Lindgren, Jr., all of the McIntire School of Commerce, University of Virginia, for their encouragement and for providing a grant to support this research. We acknowledge also the encouragement received from Dean Margery Meadows of Skyline College.