Embed Size (px)

Citation preview

ROUBINI GLOBAL ECONOMICSWWW.RGEMONITOR.COM131 VARICK STREET, SUITE 1005NEW YORK, NY 10013T: 212.645.0010F: [email protected]

The Role of Financial Derivatives In The Origin And Spreading of the Subprime Crisis

Elisa Parisi-Capone

Content

1. Macroeconomic Environment

2. Financial Innovation

3. Risk Management Issues

4.The Crisis Hits And Spreads

5. Outlook

Main Conclusions

1) Derivatives are not the direct cause of the credit crisis as debt levels have been building since the 1980s. But unregulated derivatives facilitate leverage and thus the potential for contagion to unrelated markets and the real economy.

2) At the center of the latest crisis were lax lending standards together with regulatory capital arbitrage facilitated by financial innovation and securitization. Result: ‘Shadow Banking’ system of the same size as traditional one but with no capital requirements or lender of last resort.

3) Opaque OTC derivatives helped fuel complexity and compound the mispricing of risk. The interaction of market and credit risk is not fully understood yet. The most complex structured products, such as CDOs of asset-backed securities, are not likely to return.

4) The sheer size of the OTC derivatives market binds limited resources and poses the question of opportunity costs. Full cost internalization through central clearing, insurance margining, and price transparency is likely to lead to a cost-benefit reassessment.

1. Macroeconomic Environment

Inflation Targeting, ‘Great Moderation’Source: William White (2006); Procyclicality in the financial system: do we need a new macrofinancial stabilisation framework?; BIS

After the Great Inflation of the 1970s, central banks put a high premium on price-stability. BIS argues this paradigm is characterized by the four stylized facts:

1) A general reduction in both level and volatility of inflation;

2) robust and less volatile real economic growth interrupted by fewer recessions (both 1 and 2 referred to as “The Great Moderation");

3) an increased prominence of credit, asset price and investment "boom and busts" often accompanied by financial crises of various types (i.e. Minsky cycle);

4) increased global trade imbalances.

Consumer and Mortgage Debt Since 1980s Source: M. White ( 2008); Bankrupty: Past Puzzles, Recent Reforms, and the Mortgage Crisis; UCSD and NBER

Low Risk Premia Source: P. McCulley (2006); Moral Hazard Interruptus; PIMCO

Three central bank policy pre-commitments removed three major risks from the global markets:

1) Starting in 1995, the PBOC pre-committed to absorbing dollar depreciation risk via a pegged exchange rate regime for the Renminbi;

2) Starting in February 2001, the BoJ pre-committed to absorbing Japanese short-term interest rate risk via its Zero Interest Rate Policy (ZIRP), reinforced by its Quantitative Easing (QE) policy;

3) Starting in August 2003, the Fed pre-committed to holding short rates accommodative for a “considerable period and after that to hiking only at a measured pace” (‘Greenspan Put’).

Search For Yield Source: R. Rajan (2006); Monetary Policy and Incentives; IMF

As a consequence, four main types of incentives enhance the pro-cyclicality of the financial system :

1) Risk shifting: shifting portfolios, particularly those held by insurance companies and pension funds, towards higher-yielding, thus riskier, assets or instruments in order to meet pre-contracted rates of return on their liabilities, since the risk-free yield is now very low;

2) Tail risk seeking: selling disaster insurance in derivatives markets that produce positive returns most of the time as compensation for a rare but disastrous negative return;

3) Herding: engaging in short-term remunerative bets at the expense of diversification;

4) Illiquidity seeking (“poor man’s alpha”): taking advantage of the ample liquidity supply to engage in financial arbitrage activities with less liquid instruments or markets, such as emerging markets or commodities.

All these strategies are enhanced by the use of derivatives

Bond Yield Conundrum And Agency Debt FreezeSource: Richard Duncan (2006); The Bond Yield Conundrum – How It Started. Why It Ended.

Starting Q1 2004: GSE accounting irregularities wrt interest rate swaps led to investment portfolio deleveraging net agency debt issuance decreases

Riskier private sector RMBS replace implicitly government-guaranteed GSE debt while interest rates are kept low throughout ‘bond yield conundrum’

(see also R.Caballero, A. Krishnamurthy (2009); Global Imbalances and Financial Fragility, MIT/NBER, for discussion)

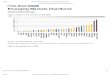

Subprime Loan Explosion Source: Goldman Sachs Global Markets Institute (2009); Avoiding Anorther Meltdown – Part 1

Subprime loans originated in 2005-2007 reached $1.4 trillion;Alt-A loans another $600 billion

Lending Standard Erosion Source: Goldman Sachs Global Markets Institute (2009); Avoiding Anorther Meltdown – Part 1

Same dynamics with commercial real estate loans, consumer/auto loans, leveraged loans for LBOs

U.S. Home PricesGraph: www.calculatedriskblog.com

House prices increase loan to value (LTV) ratio down higher rating

House prices fall negative equity, LTV up credit quality/rating down

2. Financial Innovation

Growth of OTC Financial Derivatives

Own graph based on: BIS, OTC Derivatives Market Survey H2 2008

End December 2008 CDS notional outstanding of $41.8 trillion. CDS Gross market value at current prices (or replacement value) is $5.6 trillion. Underlying debt instruments outstanding are $3.2 trillion (IMF).

by January 2009, TriOptima –through its portfolio compression service- reduced the outstanding CDS notional amount to $28 trillion.

OTC Financial Derivatives Notionals,in trillions

0100200300400500600700800

Dec2004

June2005

Dec2005

June2006

Dec2006

June2007

Dec2007

June2008

Dec2008

010203040506070

Total Contracts Interest Rate Contracts CDS (right scale)

Key Rules and Legislation - Supply

Eric Dinallo, New York Superintendent of Insurance: “The Commodity Futures Modernisation Act of 2000 exempted credit default

swaps from the old ‘bucket shop’ laws. The act also exempted them from regulation by the Commodities and Futures Trading Commission and the Securities and Exchange Commission. Unregulated, the market grew enormously.” (Financial Times, March 30, 2009)

Robert Bliss/George Kaufman on Bankruptcy Act of 2005: Source: R. Bliss, G. Kaufman (2005); Derivatives and Systemic Risk: Netting, Collateral, and Closeout; Chicago Fed.

“It is not clear whether netting, collateral, and close-out lead to reduced systemic risk, once the impact of these protections on the size and structure of the derivatives market has been taken into account.”

Basel I and II Bank Capital Requirement Frameworks (Source: Goldman Sachs (2009); Avoiding Another Meltdown – Part 1)

Both frameworks offer capital relief for: 1) e.g. securitizing a pool of mortgage loans into RMBS;2) further securitizing a pool of RMBS into CDOs; ‘originate-to-distribute’ and arbitrage incentives (shadow banking system)

Total capital and collateral requirements in the financial system lower for given economic risk

Shadow Banking System – Demand Source: Restoring Confidence in the Securitization Market, SIFMA/ASF, Dec2008

Geithner: “The structure of the financial system changed fundamentally during the boom, with dramatic growth in the share of assets outside the traditional banking system.” By early 2007:

1) Asset-backed commercial paper conduits (ABCP conduit), structured investment vehicles (SIV), auction-rate preferred securities (ARS), tender option bonds (TOB) and variable rate demand notes (VRDN) combined asset size of roughly $2.2 trillion

2) Assets financed overnight in triparty repo grew to $2.5 trillion. 3) Assets held in hedge funds grew to roughly $1.8 trillion.

4) Assets held by the then five major investment banks totaled $4 trillion. Total ‘shadow banking’ assets amount to $10.5 trillion compared

to total commercial banks’ assets: about $10 trillion

McKinsey/ASF/SIFMA Study: - Securitization financed up to 50% of new lending activity in

2005-2007;- Lack of securitization leaves $2 trillion financing shortfall in

2009-2011

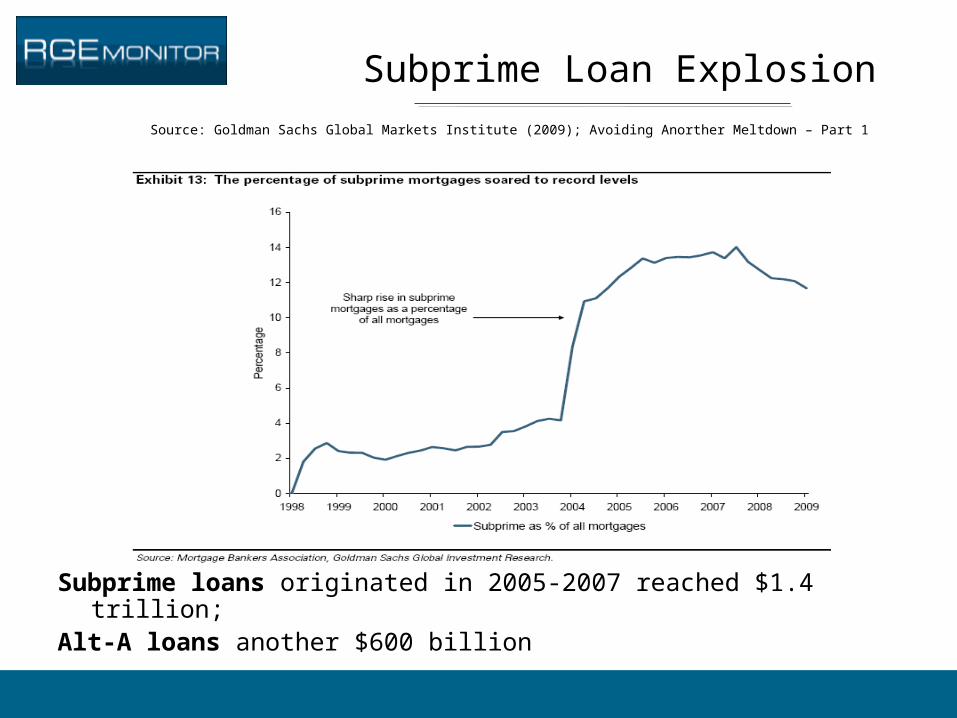

Example: Structured Investment Vehicle (SIV)Source: FitchRatings (2007); SIVs — Assessing Potential Exposure of Sponsor Banks

Assets on average consist of 50% financial institutions debt, 46% structured finance assets, 2% sovereign debt, and 2% others

Liabilities consist of 8% equity notes, 14% short-term asset-backed commercial paper (ABCP), 12% repos, 66% medium-term notes

Credit Risk Transfer Building Blocks

Corporate:1) Single-Name Credit Default Swaps (CDS)2) Multi-Mame CDS (Indices and Index Tranches)Asset-Backed Securities:3) Collateralized Debt Obligations (CDO), incl.

leveraged loans (CLO), consumer loans (ABS)4) Residential/Commercial Mortgage Backed

Securities (RMBS / CMBS)Re-Securitizations:5) Structured Finance Products (CDO of ABS, CDO of

CDO or CDO2, CDO of RMBS or CMO)6) Hybrids (e.g. CDS and loans etc.)7) Single-Tranche CDOs

CDO TechnologySource: SIFMA Securities Industries and Financial Markets Association

1) Special-Purpose Vehicle (SPV):Ensures bankruptcy remoteness, no regulatory capital requirements,

separates (enhances) portfolio rating from loan originator rating.

2) Internal Credit Enhancement/Overcollateralization:Subordination through channeling portolio credit risk into first-loss (equity),

mezzanine, senior tranche. Rating agencies bestow AAA rating only if the tranche keeps a certain subordination buffer at all times.

3) External Credit Enhancement/Bond Insurance:Buy financial guarantees from AAA-rated monolines for a fee so that insured

tranche carries the same rating as the insurer (underlying must at least be rated investment grade)

4) Strict Payment Waterfall / Cash Flow Prioritization:Interest and principal proceeds from the underlying portfolio are prioritized to

senior tranche holders until they are fully paid before the mezzanine investors and so on. If the cash flow is not enough to cover all claims, any losses are first borne by equity investors until they are fully wiped out. The mezzanine tranche is next in line to suffer losses and so on.

Credit Default Swaps – Single NameSource: Gibbs

Remember: Credit Risk Transfer, Not Elimination

Bilateral OTC contract introduces counterparty risk

Collateralized Debt Obligations (CDO) -Portfolio Credit Risk Transfer

Source:E. Benmelech, J. Dlugosz (2008), The Alchemy of CDO Credit Ratings, Harvard University

Fully funded tranches (‘true sale’), i.e. investors pay the full amount of the tranche principal at inception (proceeds) No counterparty risk, investor bears full market and credit risk of his tranche.

Synthetic, partially funded CDO

Synthetic credit risk transfer via CDS either as refernce portfolio, or as unfunded sale of tranches to investors introduces counterparty risk.

Amplification of Subprime Exposure

Source: BIS Credit Risk Transfer – Developments from 2005-2007, July 2008

Demand for high-yielding mezzanine tranches beyond available issuance is met with synthetic reproduction via derivatives.

Global CDO Issuance By UnderlyingOwn graph, data source: SIFMA Securities Industry and Financial Markets Association

Global CDO Issuance By TypeSource: Securities Industry and Financial Markets Association (SIFMA)

CDO Implied Leverage and Risk Transfer

E.g. Equity Tranche: 30 million notional, highest first-loss risk and highest return, i.e. 12% p.a.

tranche’s mark-to-market sensitivity to underlying spread changes = delta => 1200bp/60bp= 20x = equity tranche’s implied leverage in this example

Use iTraxx or CDX indices for dynamic delta-hedging with multiple of notional

Notional vs Economic Risk TransferSource: IMF Global Financial Stability Report, October 2006

Total ‘Effective’ LeverageSource: R. Merritt, E. Fahey; FitchRatings (June 2007), Hedge Funds: The Credit Market’s New Paradigm

CDS Hedge: Standardized CDX Index TranchesSource: Christopher Finger (2009); Testing Hedges under the Standard Trnached Credit Pricing Model; RiskMetrics Group

Subprime RMBS Hedge: Markit ABX.HE IndicesGraph source: FitchRatings (2006)

Structured Product Hedge: Markit TABX IndexGraph source: FitchRatings (2006)

If underlying subprime delinquencies/defaults reach 12-20%, the residual and mezzanine RMBS tranches face a cash flow shortfall all TABX tranches lose, including those rated AAA.

3. Risk Management Issues

Main Risk Management Issues

1) ‘Alchemy in the CDO Market’

2) (Mis)Pricing of Systematic Risk

3) Correlation

4) Risk Concentration

5) Counterparty Risk / Collateral

6) OTC Settlement Infrastructure

“Alchemy in the CDO Market”Graph source: E. Benmelech, Jennifer Dlugosz (2008), The Alchemy of CDO Credit Ratings, Harvard University

Ratings Arbitrage (indicated by 85% of CDO issuers as motivation, SIFMA):

Spread income from riskier red portfolio > cost of blue portfolio Win-Win: Distribute ‘excess spread’ such that AAA investor receives more

than similar-rated bond, and equity investor/issuer the rest

CDO Ratings Distribution Graph source: E. Benmelech, Jennifer Dlugosz (2008); The Alchemy of CDO Credit Ratings; Harvard University

60-70% of CDO tranches were AAA-rated compared to less than 1% of corporate bonds

(FitchRatings (2007) cited in Coval, Jurek, Stafford (2009)

Challenge: CorrelationSource: ECB Financial Stability Review 2006

Degree of diversification benefits within portfolio depends on default correlation among underlying credit instruments

correlation is subject to jumps and non-linearities; very hard to estimate correctly across several assets over time within a joint default probability distribution

A low implied correlation increases diversification and emphasizes the risk of firm-specific events and thus the likelihood of isolated defaults occurring that affect the equity tranche only

the value of the first-loss equity tranche falls with low correlation.

A high implied correlation of default within the CDO reference portfolio implies a higher risk of many names defaulting at the same time (i.e. systematic risk), with the potential to inflicting losses on the senior tranche

High correlation reduces the value of the senior tranche relative to equity tranche.

Example: CDX Base CorrelationsSource: Christopher Finger (2009); Testing Hedges Under the Standard Tranched Credit Pricing Model, RiskMetrics Group

(Mis)Pricing of Systematic Risk Source: J.Coval, J.Jurek, E.Stafford (2009); The Economics of Structured Finance; Harvard/Princeton University

Source: BIS: Findings on the interaction of market and credit risk; May 2009

CDO technology subject to two fundamental flaws:

1) The high systematic risk component of AAA-rated tranches after all firm-specific risk is diversified away (i.e. industry standard model), requires far larger risk premium based on instruments with similar payout structure (e.g. digital call options);

2) Structured finance ratings are extremely fragile to small inaccuracies in underlying probability of default and correlation assumptions (e.g. ‘Wrong Way’ risk)

BIS: “Securitization transforms credit risk into market risk but diversification benefits between the two should be regarded with great caution.”

Credit Risk Transfer To Whom?Source: Adrian Blundell Wignall (2007), Structured Products: Implications for Financial Markets, OECD

Fitch Credit Derivatives Survey:- large dealer banks buy and sell large amounts of derivatives

as market-makers largely hedged net exposure;- insurers/monolines main net protection sellers [but without

mandatory coverage ratio as with other insurance products.]

Counterparty Risk ManagementGraph source: Gary Gorton (2009); Slapped in the Face by the Invisible Hand: The Banking Panic of 2007; Yale/NBER

ISDA, 2009: “For all OTC derivatives, 65 % of trades are subject to collateral agreements. Further, 66% of OTC derivative credit exposure is now covered by collateral.” Gross CDS replacement value is $5 trillion

Note: Collateral (mostly cash) can by re-hypothecated to another counterparty. Mind also opportunity costs

OTC Settlement InfrastructureSource: IMF Global Financial Stability Report, April 2009, Chapter 2; Box 2.4: Basics of OTC Counterparty Risk Mitigation

Bilateral close-out netting and central clearinghouse (CCP):

Bilateral netting: The systemic counterparty risk is $30 although maximum potential loss for any bank is only $10 potential for trade compression (i.e. eliminate circular/redundant trades)

CCP reduces domino effect with margin requirements, capital funds, and loss-sharing. However: watch transition costs!

3. The Crisis Hits And Spreads

Example: ABX.HE.06-02 Performance

Source: I.Fender/ M.Scheicher (2009); The Pricing of Subprime Mortgage Risk in Good Times and Bad: Evidence from the ABX.HE Indices; BIS

Run On the Shadow Banking SystemSource: Markus Brunnermeier (2008); Deciphering the 2007-2008 Liquidity and Credit Crunch; Princeton University

Source: Gary Gorton (2009); Slapped in the Face by the Invisible Hand: Banking and the Panic of 2007; Yale and NBER

Short-term commercial paper is equivalent to deposits in traditional banking system

Interbank Liquidity Dries Up

Investment Bank Dominoes FallGraph Source: IMF Global Financial Stability Report, April 2009; Chapter 2

Bailout Of AIG and Derivatives Counterparties

Mary Williams Walsh, New York Times, March 15, 2009:

“Financial companies that received multibillion-dollar payments owed by A.I.G. include Goldman Sachs ($12.9 billion), Merrill Lynch ($6.8 billion), Bank of America ($5.2 billion), Citigroup ($2.3 billion) and Wachovia ($1.5 billion).”

“Big foreign banks also received large sums from the rescue, including Société Générale of France and Deutsche Bank of Germany, which each received nearly $12 billion; Barclays of Britain ($8.5 billion); and UBS of Switzerland ($5 billion).”

In total, AIG counterparties received about $100bn out of the $180bn in bail-out funds

Foreign Claims On U.S. BanksSource: BIS 2008 Annual Report

Flow of Funds data: about 40% of U.S. originated securities are held abroad

Source: D. Beltran, L.Pounder, C.Thomas (2008): Foreign Exposure to Asset-Backed Securities of U.S. Origin; Fed Board.

Hedge Fund DeleveragingSource: R. Merritt, E. Fahey; (June 2007), Hedge Funds: The Credit Market’s New Paradigm; FitchRatings

Vicious Deleveraging CycleSource: Restoring Confidence in the Securitization Markets; SIFMA/American Securitization Forum (ASF) et al.(2008)

U.S. Government Bailout FundsSource: Mark Pittman, Bob Ivry, March 31, 2009; Financial Rescue Nears GDP as Pledges Top $12.8 Trillion; Bloomberg

see also: Elizabeth Warren et al, April 2009; Congressional Oversight Report; Assessing the Treasury’s Strategy: Six Months of TARP

Total

of which:

Amount pledged:

(billions)

$12,798

Current amount:

(billions)

$4,169

Federal Reserve $7,765 $1,678

FDIC $2,038 $357

Treasury

HUD

$2,694

$300

$1.833

$300

4. Outlook

Proposed Basel II EnhancementsSource: Basel Committee on Banking Supervision; January 2009; Proposed Enhancements to the Basel II Framework

http://www.bis.org/publ/bcbs150.htm

Pillar 1 (minimum capital requirements):• Higher capital charge for re-securitizations (ABS of CDOs or

structured finance CDOs);• increase capital requirements for liquidity lines extended to

support asset-backed commercial paper (ABCP) conduits;Pillar 2 (supervisory review process):• Extension of risk-management to off-balance sheet

exposures;• Include sound liquidity risk management to supervisionPillar 3 (market discipline):• enhance disclosures regarding securitization holdings in

trading book, sponsorship of off-balance sheet vehicles, resecuritization exposures, valuations, pipeline and warehousing risk

Proposed Regulation of OTC DerivativesSource: Regulatory Reform Over-the-Counter (OTC) Derivatives; May 13, 2009; www.financailstability.gov

Treasury Secretary Geithner Proposal (May 13):

1) “Commodity Exchange Act (CEA) and the securities laws should be amended to require clearing of all standardized OTC derivatives through regulated central counterparties (CCPs).” e.g. CDS, CDS Indexes

2) “Requirements for all trades not cleared by CCPs to be reported to a regulated trade repository. Aggregated data must be made available to public, detailed individual counterparty positions to regulators.” e.g. ABX, CMBX

3) SEC Chairman Mary Shapiro points to TRACE system for corporate bond price transparency as possible standard.

Important Regulatory ProposalsSource: U.S. Treasury Otlines Framework for Regulatory Reform, March 26

1) Regulation by activity:Borrowing long and lending should be subject to

regulation regardless of the institution

2) Congress is considering re-institution of leverage cap (e.g. Switzerland adopted one)

3) Systemic regulator or extra capital charge for systemically important institutions

4) New resolution regime for non-banks and holding companies.

Future of Structured Finance Source: Restoring Confidence in the Securitization Markets; SIFMA/American Securitization Forum (ASF) et al.(2008)

Ratings arbitrage window is likely closed now. Adequate risk pricing reduces AAA-rated supply.

ROUBINI GLOBAL ECONOMICSWWW.RGEMONITOR.COM131 VARICK STREET, SUITE 1005NEW YORK, NY 10013T: 212.645.0010F: [email protected]

Thank You!Elisa Parisi-Capone