Embed Size (px)

Citation preview

Rovio FinlandTelecom Equipment and IT

Commissioned Equity Research • 19 June 2019

KEY DATA

FinlandStock countryROVIO FHBloombergROVIO.HEReutersEUR 7.31 Share price (close)

Free FloatEUR 0.58/EUR 0.58Market cap. (bn)

http://www.rovio.com/Website08 Aug 2019Next report date

PERFORMANCE

Sep17 Apr18 Nov18 Jun192

4

6

8

10

12

Rovio

Finland OMX Helsinki All-Share (Rebased)

Source: Thomson Reuters

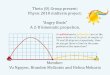

VALUATION APPROACH

6.6

7.2

6.1

6.9

9.5

9.4

8.5

10.4

4 6 8 10 12

DCF Monte Carlosimulation, 10th-90th percentiles

DCF

EV/EBIT

P/E

Source: Nordea estimates

ESTIMATE CHANGES

2021E2020E2019EYearn.a.n.a.n.a.Salesn.a.n.a.n.a.EBIT (adj)

Source: Nordea estimates

Casual games leader's quest for golden eggs

Having been around for about ten years, the Angry Birds brand has proved its longevity and Rovio its ability to monetise the entertainment franchise through engaging casual mobile games and brand licensing. The solid balance sheet and positive cash flow allow the company to pursue growth objectives through organic and inorganic means. We believe the biggest risks for the company relate to rising user acquisition costs, a possible decline of the Angry Birds brand and failure to diversify the game portfolio to include new genres.

Rovio is still all about Angry Birds which we view as a strengthOf Rovio's 22 live mobile games, the top five are based on the Angry Birds (AB) brand. The two top-grossing games in 2018, AB 2 and AB Friends, are slingshot games that were launched in 2015 and 2012, respectively. The success of these games proves Rovio's solid category leadership, capability to monetise its brand, and its ability to run live operations to engage gamers and prolong the lifetime of its games. Its brand and slingshot genre leadership create a stable cash-generating core for Rovio.

Upside from a flock of upcoming game titles and bolt-on M&A In order to achieve meaningful growth, Rovio aims to diversify its game portfolio from the casual and AB-themed games through in-house development and bolt-on M&A. Current initiatives include the launch of AB Dream Blast in Q1 2019, the acquisition of strategy game developer PlayRaven in Q4 2018, and incubation of the Hatch mobile game streaming service. Rovio should launch a new game in H2, after which we expect two new game launches per year. We estimate the new games to have a slightly weaker KPI performance on average than the recently launched AB Dream Blast, leading to a 7% sales CAGR on a group level during 2018-21E, and an EBIT margin of 13% (14% ex-Hatch) in 2021E, from 11% in 2018.

DCF and peer multiples suggest valuation range of EUR 6.8-9.4We derive a DCF valuation range of EUR 7.6-8.7 per share by applying a WACC of 8-12%. We perform a Monte Carlo simulation with game KPIs (MAU, DAU/MAU and ARPDAU) and calculate the 10th-90th percentile values to be EUR 6.6-9.5 per share. We also include relative valuation with P/E and EV/EBIT multiples derived from relevant Nordic gaming companies and global mobile gaming companies. The averages of the upper and lower limits for different valuation approaches equal a valuation range of EUR 6.8-9.4.

Nordea Markets - AnalystsSami SarkamiesSenior Analyst

Veikkopekka SilvastiAnalyst

Ville TiainenSenior Analyst

SUMMARY TABLE - KEY FIGURES

2021E2020E2019E2018201720162015EURm347333315281297192142Total revenue

515050486535-6EBITDA (adj)444037313617-22EBIT (adj)

12.7%12.1%11.8%11.1%12.1%8.8%-15.2%EBIT (adj) margin0.440.400.370.300.330.14-0.24EPS (adj)

9.5%8.4%23.6%-7.7%130.7%158.8%-323.7%EPS (adj) growth0.130.120.110.090.060.060.00DPS (ord)1.01.21.30.72.2n.a.n.a.EV/Sales8.29.711.45.917.8n.a.n.a.EV/EBIT (adj)

16.518.119.612.727.6n.a.n.a.P/E (adj)2.52.83.21.95.2n.a.n.a.P/BV

1.8%1.7%1.5%2.4%0.7%n.a.n.a.Dividend yield (ord)6.7%6.7%7.8%14.0%8.2%n.a.n.a.FCF Yield bef A&D, lease -218-188-158-120-88-10-10Net debt-4.2-3.8-3.2-2.5-1.5-0.31.5Net debt/EBITDAn.m.n.m.91.5%53.6%43.9%18.5%-31.6%ROIC after tax

Source: Company data and Nordea estimates

Marketing material commissioned by Rovio

Rovio19 June 2019

Contents

Factors to consider 3

Valuation 7

Estimates 12

Rovio's market 20

Rovio in brief 30

Game portfolio – fewer, bigger and better 38

Business model 44

Risk factors 48

Reported numbers and forecasts 49

Disclaimer and legal disclosures 52

Marketing material commissioned by Rovio 2

Rovio19 June 2019

Factors to considerRovio is best known for the global Angry Birds brand, which started out as a popular mobile game in 2009, and has since evolved to include various entertainment and consumer products through brand licensing and movies. We believe that the well-recognised Angry Birds brand, the company's leading position within the slingshot games genre, its solid net cash position and its experienced team of developers will drive growth ahead. The main risks, in our view, lie in rising user acquisition costs, potential deterioration of the global Angry Birds brand, failure to diversify into new game genres and potential risks related to bolt-on M&A activity.

We believe Angry Birds is Rovio's "secret sauce", enabling better organic user acquisition and a profitable product and content licensing business

Angry Birds is a global brand with high recognitionWe believe that the strong brand value of Angry Birds benefits the company in two ways. Firstly, the global awareness of the brand improves organic user acquisition in the hyper-competitive mobile games market. Given that the cost of acquiring a paying customer has been steadily rising, all leverage that can generate organic downloads is highly valuable. Secondly, a strong brand enables the company to run a profitable product and content licensing business, which also further strengthens the brand awareness. Thus, we view the Angry Birds brand as Rovio's "secret sauce" in terms of discoverability and user acquisition challenges. The upcoming Angry Birds Movie 2 in August and the ten-year Angry Bird anniversary celebrations in December are testimonies to the brand's versatility and longevity.

RECOGNITION OF SELECTED "MOBILE-BORN" BRANDS, %

97%

80%

70%

0%

20%

40%

60%

80%

100%

Angry Birds Candy Crush saga Clash of Clans

Source: Lieberman Research Worldwide, 2017

RECOGNITION OF SELECTED GLOBAL BRANDS, %

97% 96%94% 93%

91%

70%

75%

80%

85%

90%

95%

100%

Angry Birds Star Wars Frozen Hello Kitty Pokemon

Source: Lieberman Research Worldwide, 2017

Rovio has a robust portfolio of core games that has proven its ability to generate stable gross sales...

...but every game has a lifetime and new games need to be constantly added to maintain and grow the business

Core portfolio ensures stable cash flow but requires constant refreshmentRovio's current game portfolio includes 22 titles. However, in line with its "fewer, bigger and better" logic for the game portfolio, significant resources (developer hours and marketing expenses) are invested in just the top four or five games. As illustrated below, Rovio's game portfolio has delivered relatively stable quarterly gross sales of EUR 60m or above since Q2 2017. However, every game carries a lifetime, and Rovio cannot expect to keep on delivering such robust gross sales without launching new games. The portfolio received a much needed boost when Rovio launched AB Dream Blast in Q1 2019 and we expect another game to be unveiled before year-end. Furthermore, we forecast that Rovio will launch two games per year in 2020 and 2021.

Marketing material commissioned by Rovio 3

Rovio19 June 2019

GROSS SALES PER GAME, EURm

6 9 12 16 20 21 18 20 2230 31 35 32

68

810

8 98 8 7

8 88

711 119 8 6

10 9

7

67 7

77

57

88

7 65

44 3

337

1212

1213

1016 15 15

1516 14

14 10

2936

40

47

56

63 65 67

6065 63

67 66

0

10

20

30

40

50

60

70

80

Q12016

Q22016

Q32016

Q42016

Q12017

Q22017

Q32017

Q42017

Q12018

Q22018

Q32018

Q42018

Q12019

Angry Birds 2 Angry Birds Friends Angry Birds Blast Angry Birds Evolution

Angry Birds Match Angry Birds Pop! Angry Birds Dream Blast Other

Source: Company data and Nordea estimates

AB Dream Blast has been making progress recentlyLooking at the top grossing rank of all games from the US App Store (App Annie), we conclude that Rovio's top games at present have performed quite stably over the past three months. AB 2 has maintained its position as the top grossing game by Rovio (since Q1 2016) and ranks among the top 100 grossing games on the US App Store, with the top grossing rank varying between the 80th and 48th position. This means that out of all of the games on the US App Store, AB 2 ranks 55th when sorted by revenue. AB Dream Blast has enjoyed a slight upward trend recently, implying that it may very well take over as Rovio's second-largest game during Q2. In addition, AB Match is still in growth stage and has performed slightly better over the past three months. We have not included AB Friends in the chart as the US is not the game's main market.

TOP GROSSING GAMES RANK FROM US APP STORE

5548

56 55 54 56 57 6352

80

62 59 5468 72

55

161150

137144 144 138 138 136 137

127119 119 117

127

110126

213200

193184

202195

184

165172

180171 172

179171 165

193

20

40

60

80

100

120

140

160

180

200

220

AB 2 AB Dream Blast AB Match

Source: App Annie

Hundreds of mobile games are launched every day, making discoverability one of main hurdles for mobile gaming companies

Challenges in terms of discoverability and rising UA costs will persistThe gaming apps space is crowded and competitive. In this arena, the ability to acquire and engage highly valuable audiences can make or break a business. According to mobile app marketing platform Liftoff, the average cost of acquiring a paying customer in a gaming app rose from USD 65.9 to USD 101.6 during 2016-18. On an industry level, this is a good sign as rising costs reflect higher expected lifetime value (LTV) per customer. However, on a company level, inflating UA costs elevate the required LTV of new gamers, which in turn requires developers to come up with new and ingenious games or continuously improve their existing ones. However, the soaring UA costs can also act as a barrier of entry for newcomers, strengthening the position of already established companies with an existing gamer base, brand and good cash position, such as Rovio.

Marketing material commissioned by Rovio 4

Rovio19 June 2019

PER CUSTOMER ACQUISITION COSTS IN MOBILE GAMES, USD

4.19.4

65.9

3.88.9

76.4

2.9 5.1

101.6

0

20

40

60

80

100

120

Install Register In-App-Purchase

2016 2017 2018

Source: Liftoff (2018 Mobile App Engagement Index)

IN-APP PURCHASE: MONTHLY COSTS AND ENGAGEMENT RATES, USD AND %

0%

1%

2%

3%

4%

5%

0

20

40

60

80

100

120

140

Monthly costs Engagement rates

Source: Liftoff (2018 Mobile App Engagement Index)

According to industry experts, the ability to run efficient live operations to prolong the lifetime of games is scarce

Ability to engage and monetiseDespite Rovio not releasing any new games in 2018, sales in the Games segment increased 1% y/y that year. This illustrates Rovio's ability to run good live operations of existing games so that gamers keep coming back to their AB-themed slingshot or puzzle games, and spending money while doing so. However, for the company to achieve growth of 1% for the Games segment, Rovio needed to invest another EUR 9m in user acquisition (UA), ie 13% more y/y. The rapid growth in UA investments reflects the tightening competition in the mobile gaming industry, which has led to bigger UA costs.

Solid portfolio of core games supports Rovio's cash position

Strong net cash position supports game development and M&A activity We note that Rovio's strong balance sheet is strategically important in the mobile gaming industry, where development and user acquisition costs require front-loaded investments. In addition to the aforementioned activities, Rovio's net cash position of EUR 122m (as of Q1 2019) provides M&A firepower if and when the company wants to diversify into new game genres or businesses.

CASH AND NET GEARING, EURm AND %

-78%

-76%

-74%

-72%

-70%

-68%

-66%

-64%

-62%

-60%

-58%

0

20

40

60

80

100

120

140

Q1 18 Q2 18 Q3 18 Q4 18 Q1 19

Cash at the end of the period Net gearing %

Source: Company data

Mature games enjoy higher marginsWhile some mobile games thrive for several years, others start declining much faster. Eventually, every game matures, but that does not necessarily need to be negative. Once a game matures, Rovio needs to invest far less in marketing, while retaining long-tail earnings for a long time after the game has reached peak sales. This means that revenue from some mature assets can decline each year, but without any UA costs, thus leading to gross margins of almost 70% (after the 30% cut taken by app stores). In other words, high margins should offset periods of negative revenue growth.

Marketing material commissioned by Rovio 5

Rovio19 June 2019

We expect group revenue to grow at a CAGR of 7% in 2018-21, with sales growth driven mainly by the Games unit as we expect Brand Licensing sales to decline after the 2019 movie launch

Group revenue to grow at a CAGR of 7% during 2018-21EFor the Games unit, we model 2019E-21E revenue using a bottom-up approach, whereas for 2022E-24E, we apply a conservative steady growth rate of 5%. Moreover, we estimate that gross profit will remain around 68% during the entire forecast period of 2019-24. We base this on the current competitive situation in the platform market. On a group level, we model that revenue will grow at a CAGR of 7% during 2018-21E. We believe the group revenue growth will be driven solely by the Games business unit during 2020-21 as we model declining sales for Brand Licensing after the launch of the AB Movie 2 in 2019. Growth in operational expenses should remain in line with revenue growth, though we believe user acquisition costs will create upwards pressure. In addition, we expect the company to achieve an EBIT margin of 13% (14% excluding Hatch) by 2021, after 11% in 2018 (14% excluding Hatch). For 2019, Rovio expects to achieve sales of EUR 300-330m (7-17% growth) with an EBIT margin of 9-11% (12-14% excluding Hatch). For 2019, we estimate sales growth of 12%, in line with company guidance, with an EBIT margin of 12% (15% excluding Hatch), which is slightly above guidance.

Consensus expects slowing growth and an improving EBIT margin in 2020-21

Our estimates are ahead of consensus on growth but below on marginsThompson Reuters consensus currently expects decelerating growth and an improving EBIT margin for 2020-21. We believe that Rovio will be able to remain on its growth path and forecast a lower EBIT margin than consensus. Consensus expects sales to grow by 13% in 2019 (-5% in 2018), while estimates for 2020 and 2021 are at 7% and -1%, respectively. We estimate sales will grow 12% in 2019, while 2020 and 2021 estimates are at 6% and 4%, respectively. Along with slowing sales growth estimates, consensus expects the EBIT margin to improve from 10% in 2019E (11% in 2018) to 21% in 2021E. We estimate that Rovio will deliver an EBIT margin of 12% (15% excluding Hatch) in 2019, with only slight margin expansion to 13% (14% excluding Hatch) for 2021. We note that Rovio's long-term financial goals from 2016-17 target growth above that of the western mobile gaming market and a 30% EBIT margin. The company has made little progress on this front, however.

Despite significant operational changes and transformations, management has not been able to expand the company's offering beyond casual slingshot and puzzle games

Management still needs to prove ability to expand outside of core genresOver the years, management has carried out some significant operational changes and transformations, such as fully transitioning the games monetisation model to free-to-play, growing the Games business unit, restructuring the Brand Licensing business unit to regain focus on core operations and products, and transforming the business model for movies and animated series to full licensing. Moreover, the team's newest addition, head of Games, Alexandre Pelletier-Normand, has a strong background from global giants Gameloft and Vivendi. However, so far, the management team has been focussed on operating the AB brand and existing games, and has not been able to expand the company's offering beyond the casual slingshot and puzzle games.

Rovio aims to acquire smaller game studios to attain new talent and enable faster time to market for new games

Bolt-on M&A complements in-house developmentRovio views smaller bolt-on acquisitions as a means to acquire new talent, which speeds up expansion into new gaming genres. Recently acquired PlayRaven, a gaming company focused on strategy games, is an embodiment of an optimal takeover target in terms of business logic and risk. In addition, Rovio has indicated that it is seeking external investors to fund Hatch Entertainment's mobile game streaming service and is willing to dilute its 80% stake. We view Hatch as a binary project that will prove to be a major success or a flop. Our estimates do not include revenue from Hatch. Overall, we believe that potential problems in terms of cultural fit between Rovio, PlayRaven and other possible targets represent the largest risk in terms of M&A activity.

DCF and peer multiples suggest a valuation range of EUR 6.8-9.4We derive a DCF valuation range of EUR 7.6-8.7 per share by applying a WACC of 8-12%. We perform a Monte Carlo simulation using game KPIs (MAU, DAU/MAU and ARPDAU) and calculate the 10th-90th percentile values to be EUR 6.6-9.5 per share. We also include relative valuation with P/E and EV/EBIT multiples derived from relevant Nordic gaming companies and global mobile gaming companies. The averages of upper and lower limits for different valuation approaches yield a valuation range of EUR 6.8-9.4.

Marketing material commissioned by Rovio 6

Rovio19 June 2019

ValuationOur valuation is based on two fundamental assumptions: 1) on a group level, revenue should grow at a CAGR of 4% during 2019E-24E; and, 2) we expect the company to deliver a 12-16% adjusted EBIT margin over the forecast period. Using primarily a DCF valuation and assuming a WACC of 8-12%, we derive an equity value range of EUR 7.2-9.4 per share. We also complement our DCF framework with a multiples-based relative valuation approach and a Monte Carlo simulation.

DCF model points to a value of EUR 7.2-9.4 per shareOur bottom-up valuation of Rovio focuses on current game titles, pipeline potential and licensing. In our view, the solid strategy, which centres on the strong Angry Birds brand, strong cash flow, ample liquidity and a capable management, bodes well for future performance. Using a WACC of 8-12%, we derive an equity value range of EUR 7.2-9.4 per share.

Furthermore, we add weight to our DCF valuation by conducting a Monte Carlo simulation with 10,000 draws. The probabilistic variables simulated are the three main KPIs: monthly active users (MAU), user engagement (DAU-to-MAU ratio) and average revenue per daily active user (ARPDAU). All variables are simulated on a portfolio level annually in order to derive a probability distribution for our DCF valuation. The valuation range is based on the 10th and 90th percentile cut-off values of EUR 6.6 to EUR 9.5 per share, respectively. In our simulation, revenue from the Brand Licensing unit is modelled at 5% of the Gaming unit's revenue per fiscal year, whereas revenue from the Other segment is expected to remain zero.

We also complement our DCF approach with a multiples-based relative valuation but note that a direct peer comparison is difficult owing to the different release cycles, accounting principles and risks related to the IP and games portfolios.

Valuation reflects our expectation of steady performanceWe base our DCF valuation on a bottom-up approach, where we forecast current and upcoming quarterly revenue for games on a game-by-game basis during 2019-21. User acquisition and marketing costs are modelled with the same approach for the corresponding period. Valuation of the Brand Licensing business is conducted with a similar bottom-up approach, where we forecast quarterly revenue, profitability and capex for the business unit.

We believe that Rovio will deliver good organic revenue growth with a healthy operating margin of 12-16%. We expect that the upcoming Angry Birds Movie 2, which is to be released in August 2019, will give a notable boost to the company's EBIT through the content and consumer products' licensing businesses. We expect the company to exceed its guidance range of 9-11% adjusted operating profitability and deliver a 12% EBIT margin for the full-year 2019. Furthermore, we forecast that the operating margin will improve gradually throughout our explicit forecast period of 2019-24, reaching 16% in 2023.

In addition to decent organic growth prospects and healthy operating margins, the company's ample liquidity, negative net debt and limited capex needs support our valuation. More detailed estimates are presented in the 'Estimates' section of this report.

The WACC we apply to our DCF valuation is 10%. The figure assumes 100% equity weight, a 4.0% market risk premium, a risk-free rate of 2.5% and an equity beta of 1.875.

Marketing material commissioned by Rovio 7

Rovio19 June 2019

DCF VALUATION

DCF value Value Per share

NPV FCFF 491 6.2(Net debt) 120 1.5Market value of associates 0 0.0(Market value of minorities) 0 0.0Surplus values 0 0.0(Market value preference shares) 0 0.0Share based adjustments 0 0.0Other adjustments 0 0.0Time value 27 0.3DCF Value 638 8.1

Source: Company data and Nordea estimates

WACC COMPONENTS

Risk-free interest rate 2.5%Market risk premium 4.0%Forward looking asset beta -Beta debt 20.0%Forward looking equity beta 187.5%Cost of equity 10.0%Cost of debt 7.0%Tax-rate used in WACC 20.0%Equity weight 100.0%WACC 10.0%

Source: Company data and Nordea estimates

DCF ASSUMPTIONS

Averages and assumptions 2019-24 2025-29 2030-34 2035-39 2040-44 2045-49 Sust.

Sales growth, CAGR 4.50% 3.5% 3.5% 3.5% 3.0% 2.5%EBIT-margin, excluding associates 14.0% 12.5% 12.5% 12.5% 12.5% 0.0%Capex/depreciation, x 0.6 0.60 0.70 0.80 0.90 1.00Capex/sales 1.1% 0.0% 0.0% 0.0% 0.0% 0.0%NWC/sales -1.8% -1.8% -1.8% -1.8% -1.8% -1.8%FCFF, CAGR 2.0% -1.3% 3.5% 3.5% 3.1% -71.7% 2.5%

Source: Company data and Nordea estimates

Monte Carlo simulation adds depth to our DCF-derived valueUnlike a scenario analysis, where we would look at the values under discrete scenarios, simulations allow for more flexibility in how we deal with uncertainty. We believe that a simulation provides a bigger picture of the risk related to an asset or investment. This is especially true for young and small mobile gaming companies with limited track records.

We opt to use MAU, DAU-to-MAU and ARPDAU as our probabilistic variables for which we define probability distributions and parameters. Furthermore, we model zero correlation between the variables. All variables are simulated on the portfolio level annually. We assign gamma, uniform and normal distributions for MAU, DAU-to-MAU and ARPDAU, respectively. Histograms, descriptive statistics and relevant percentiles for all probabilistic variables are presented below.

ARPDAU HISTOGRAM, EUR AND NUMBER OF OBSERVATIONS

0

500

1000

1500

2000

2500

0.03 0.04 0.05 0.06 0.07 0.08 0.09 0.10 0.11 0.12 0.13 0.14 0.15 0.16 0.17

ARDPAU

Source: Company data and Nordea estimates

ARPDAU PERCENTILES AND CUT-OFF VALUES, % AND EUR

10th 0.0720th 0.0830th 0.0940th 0.1050th 0.1060th 0.1170th 0.1180th 0.1290th 0.1399th 0.15

Source: Company data and Nordea estimates

Marketing material commissioned by Rovio 8

Rovio19 June 2019

MAU HISTOGRAM, MILLION PLAYERS AND OBSERVATIONS

0

500

1000

1500

2000

2500

3000

3500

10 20 30 40 50 60 70 80 90 100

MAU

Source: Company data and Nordea estimates

MAU PERCENTILES AND CUT-OFF VALUES, % AND MILLION PLAYERS

10th 30.820th 35.030th 38.040th 40.950th 43.760th 46.770th 50.280th 54.490th 60.599th 76.0

Source: Company data and Nordea estimates

DAU/MAU HISTOGRAM, % AND OBSERVATIONS

1200

1400

1600

17% 18% 19% 20% 21% 22% 23%

DAU/MAU

Source: Company data and Nordea estimates

DAU/MAU PERCENTILES AND CUT-OFF VALUES, % AND %

10th 16.7%20th 17.4%30th 18.1%40th 18.8%50th 19.5%60th 20.2%70th 20.9%80th 21.6%90th 22.3%99th 22.9%

Source: Company data and Nordea estimates

The parameters in our Monte Carlo simulation are calibrated so that the median value of 10,000 simulations equals our primary DCF valuation. The share price distribution and relevant descriptive statistics based on 10,000 simulations are presented below.

SHARE PRICE DISTRIBUTION, EUR AND NUMBER OF OBSERVATIONS

0

500

1000

1500

2000

2500

3000

3500

4000

4-5 5-6 6-7 7-8 8-9 9-10 10-11 11-12 12-13

Share price range

Source: Company data and Nordea estimates

SHARE PRICE PERCENTILES AND CUT-OFF VALUES, % AND EUR

1st 5.910th 6.850th 8.190th 9.699th 10.9

Source: Nordea estimates

SHARE PRICE DESCRIPTIVE STATISTICS

Mean 8.2Median 8.1Min 4.6Max 12.2St.Dev 1.1

Source: Nordea estimates

Marketing material commissioned by Rovio 9

Rovio19 June 2019

Relative valuation complements our DCF modelOur peer group valuation consists of listed Nordic gaming companies and relevant international mobile gaming companies. For an optimal comparable company, we would need to find a peer with a similar gaming market, product strategy and release schedule. This is a challenging task, to say the least; therefore, we consider a multiples-based valuation to be a good complement to a DCF valuation, which we consider the most relevant option when valuing gaming companies' earnings potential.

In terms of benchmarking, we regard enterprise value (EV)-based multiples, such as EV/EBITDA and EV/sales, as the most relevant multiples for the gaming sector. The advantage of the former is that it is not affected by the large accounting differences with regards to amortisation and depreciation across the companies. The latter is interesting thanks to its stability – from time to time, other multiples can be inflated as a result of timing effects in revenue recognition and game releases, while EV/sales, although also volatile, varies far less. Other multiples can swing higher due to margin profiles when titles reach peak sales. EV multiples are also neutral to a company's financial gearing. We also add the traditional P/E multiple to complement our EV-based relative valuation framework.

Relevant peer group consists of Nordic gaming companies...As mentioned above, to add granularity to our relative valuation, we divide our peer universe into listed Nordic gaming companies and relevant international mobile gaming companies. As can be seen from the standard deviation of different pricing multiples and market capitalisation, comparable companies comprise a homogenous group.

A key highlight from the Nordic peer comparison is that, based on our DCF valuation, Rovio's P/E, EV/EBIT, EV/EBITDA and EV/sales multiples are all in line with Nordic peer medians for 2020 estimates.

NORDIC GAMING COMPANIES

P/E EV/EBIT EV/EBITDA EV/SALESName Country Mcap EURt 19E 20E 19E 20E 19E 20E 19E 20ETHQ Nordic (NDEA) Sweden 2001 22.5 18.2 15.1 12.6 14.6 11.1 3.5 2.9Paradox Interactive Sweden 1458 34.9 28.6 26.6 21.8 18.4 14.6 11.0 9.1Stillfront Group (NDEA) Sweden 569 19.3 15.9 13.7 10.9 9.4 7.6 3.4 2.8G5 Entertainment Sweden 72 7.0 6.5 5.2 4.7 2.7 2.5 0.5 0.5Starbreeze (NDEA) Sweden 45 61.7 107.7 26.3 3.7 1.9 1.3MAG Interactive Sweden 31 21.9 8.8 3.5 0.8 0.7Next Games (NDEA) Finland 30 46.1 31.4 8.3 0.9 0.7Remedy Entertainment Finland 103 14.7 12.0 9.2 7.6 9.2 7.6 2.5 2.2

Rovio Entertainment (NDEA) Finland 638 21.7 20.0 12.9 11.2 9.6 9.0 1.5 1.4

Average 539 19.7 26.3 14.0 25.7 13.4 7.4 3.1 2.5Median 88 19.3 20.0 13.7 11.7 12.0 7.6 2.2 1.7Min 30 7.0 6.5 5.2 4.7 2.7 2.5 0.5 0.5Max 2001 34.9 61.7 26.6 107.7 26.3 14.6 11.0 9.1

Source: Thomson Reuters and Nordea estimates (18 June 2019)

...and global mobile gaming companies In addition to Nordic gaming companies, global mobile gaming companies constitute another relevant peer group for Rovio. In general, as with the Nordic peers, the median multiples based on 2020 estimates reflect Rovio's corresponding multiples. As mentioned above, we consider the comparative valuation as a complement and sanity check to our DCF valuation and the related Monte Carlo simulation.

Marketing material commissioned by Rovio 10

Rovio19 June 2019

MOBILE GAMING COMPANIES

P/E EV/EBIT EV/EBITDA EV/SALESName Country Mcap EURt 19E 20E 19E 20E 19E 20E 19E 20EG5 Entertainment Sweden 72 7.0 6.5 5.2 4.7 2.7 2.5 0.5 0.5MAG Interactive Sweden 31 21.9 8.8 3.5 0.8 0.7Next Games (NDEA) Finland 30 46.1 31.4 8.3 0.9 0.7Zynga U.S. 5174 27.2 22.4 21.9 17.8 21.0 16.7 3.9 3.5Glu Mobile U.S. 919 20.4 13.2 17.4 10.9 16.7 10.4 2.1 1.8

Rovio Entertainment (NDEA) Finland 638 21.7 20.0 12.9 11.2 9.6 9.0 1.5 1.4

Average 1245 18.2 22.0 14.8 14.7 13.5 8.3 1.6 1.4Median 72 20.4 21.9 17.4 10.9 16.7 8.3 0.9 0.7Min 30 7.0 6.5 5.2 4.7 2.7 2.5 0.5 0.5Max 5174 27.2 46.1 21.9 31.4 21.0 16.7 3.9 3.5

Source: Thomson Reuters and Nordea estimates (18 June 2019)

DCF and peer multiples imply an average valuation range of EUR 6.8-9.4We derive a DCF valuation range of EUR 7.2-9.4 per share by applying a WACC of 8-12%. We also complement our DCF model with relative valuation multiples – P/E and EV/EBIT – derived from relevant Nordic gaming companies and global mobile gaming companies. The averages of the upper and lower limits for different valuation approaches equal EUR 6.8-9.4. Our Monte Carlo simulation conducted with our DCF model implies 10th and 90th percentile values of EUR 6.6 and EUR 9.5, respectively.

VALUATION APPROACHES, EUR PER SHARE

6.6

7.2

6.1

6.9

9.5

9.4

8.5

10.4

4 5 6 7 8 9 10 11

DCF Monte Carlo simulation,10th-90th percentiles

DCF

EV/EBIT

P/E

Source: Company data and Nordea estimates

Marketing material commissioned by Rovio 11

Rovio19 June 2019

EstimatesFor the Games unit, we model 2019E-21E revenue using a bottom-up approach, whereas for 2022E-24E we apply a conservative steady growth rate of 5%. Moreover, we estimate that gross profit will remain around 68% during the entire forecast period (2019-24). We base this on the current competitive situation in the platform market. On a group level, we model that revenue will grow at a CAGR of 7% during 2018-21E. Growth in operational expenses should remain in line with revenue growth, though we believe user acquisition costs will create upward pressure. Lastly, we expect the company to reach a 13% EBIT margin by 2021.

Game unit's implied revenue CAGRs for 2018-21E and 2021E-24E are 10% and 5%, respectively, in our bottom-up approach

Games unit estimated to grow at a CAGR of 10% during 2018-21For the Games unit, we base our 2019-21 revenue estimates on a bottom-up approach, namely our forecasts for monthly average users (MAU), engagement (daily active users (DAU)-to-MAU ratio) and monetisation (average revenue per daily active user, ARPDAU). Furthermore, we apply steady churn rates to estimate q/q retention in the MAU figure. In addition to Angry Birds Dream Blast, we expect the company to launch another game in H2 this year and forecast that it will launch two new games per year during 2020-21. We believe that the new games may raise both revenue and user acquisition costs, whereas we expect the more established titles to provide a steady, albeit declining, revenue stream. Using our bottom-up approach, we derive implied revenue CAGRs for 2018-21E and 2021E-24E of 10% and 5%, respectively.

We expect the gross margin in the Games unit to remain around 68% for the forecast period

For our gross margin estimates, we adjust revenue for fees paid to app stores and sales agents. Even though we note that there is downward pressure on the platform fee (ie the amount that platforms charge for hosting/selling the game to clients), we model a constant cut of 30% for Apple and Google. Moreover, we expect sales agents' commissions to correspond to roughly ~2% of revenue. Consequently, we expect the gross margin to remain around 68% for the forecast period.

GAMES QUARTERLY GROSS BOOKINGS AND LTM, EURm

0

50

100

150

200

250

300

350

400

0102030405060708090

100

Q1

17Q

2 17

Q3

17Q

4 17

Q1

18Q

2 18

Q3

18Q

4 18

Q1

19Q

2 19

EQ

3 19

EQ

4 19

EQ

1 20

EQ

2 20

EQ

3 20

EQ

4 20

EQ

1 21

EQ

2 21

EQ

3 21

EQ

4 21

E

Gross bookings - Total Rolling 12M - Total

Source: Company data and Nordea estimates

GAMES REVENUE, ADJ. EBITDA AND MARGIN, EURm AND %

0%

5%

10%

15%

20%

25%

0102030405060708090

100

Q1

17Q

2 17

Q3

17Q

4 17

Q1

18Q

2 18

Q3

18Q

4 18

Q1

19Q

2 19

EQ

3 19

EQ

4 19

EQ

1 20

EQ

2 20

EQ

3 20

EQ

4 20

EQ

1 21

EQ

2 21

EQ

3 21

EQ

4 21

E

Revenue Adj. EBITDA Adj. EBITDA margin (%)

Source: Company data and Nordea estimates

Engagement and monetisation should remain goodRovio has demonstrated time and again that it can engage and monetise players. For instance, according to GameAnalytics, the median DAU-to-MAU and ARPDAU figures for more than 60,000 mobile games from June 2017 to June 2018 were 8% and USD 0.03, respectively. The corresponding figures for Rovio were 13% and USD 0.08 (EUR/USD 1.12) on average for Q2 2016 to Q1 2019.

Marketing material commissioned by Rovio 12

Rovio19 June 2019

DAU, MAU AND DAU-TO-MAU, MILLIONS AND %

12%

13%

14%

15%

16%

0

10

20

30

40

50

60

70

80

90

Q1

17Q

2 17

Q3

17Q

4 17

Q1

18Q

2 18

Q3

18Q

4 18

Q1

19Q

2 19

EQ

3 19

EQ

4 19

EQ

1 20

EQ

2 20

EQ

3 20

EQ

4 20

EQ

1 21

EQ

2 21

EQ

3 21

EQ

4 21

E

DAU - All MAU - All DAU/MAU - All

Source: Company data and Nordea estimates

ARPDAU, EUR

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

Q1

17Q

2 17

Q3

17Q

4 17

Q1

18Q

2 18

Q3

18Q

4 18

Q1

19Q

2 19

EQ

3 19

EQ

4 19

EQ

1 20

EQ

2 20

EQ

3 20

EQ

4 20

EQ

1 21

EQ

2 21

EQ

3 21

EQ

4 21

E

ARPDAU - All

Source: Company data and Nordea estimates

We do not expect any major changes to the current KPIs for the upcoming titles. We assume churn of 4% q/q in MAU figures and slightly improving engagement (ie the DAU/MAU ratio). In terms of monetisation, we believe the ARPDAU of the top-five games will increase by 1% q/q during 2019-21 and beyond, whereas we expect the rest of the game portfolio to grow 0-1% q/q. Overall, the company has disclosed that it intends to publish at least two titles per year in 2020 and 2021. It expects the second title this year to be Angry Birds POP 2, which had a soft launch in Q2 2019. More detailed estimates about Rovio's top-five games currently and its entire games portfolio are presented at the end of this section.

No investment or distribution costs associated with the Angry Birds sequel, as it has been licensed to Columbia Pictures Industries

Angry Birds Movie 2 should boost revenue growth in Brand LicensingBrand Licensing will receive a boost from the world premiere of Angry Birds Movie 2, which will open in theatres globally in August 2019. Unlike the first movie, the sequel has been licensed to Sony-owned Columbia Pictures Industries. This practically cuts out the financial risk, as Rovio does not need to invest in production or distribution. Furthermore, the licensing model enables faster revenue recognition and the company expects to recognise ~50% of the total revenue during Q3-Q4 2019. Overall, we expect Brand Licensing to deliver ~50% revenue and ~65% EBITDA growth in 2019. We expect the movie sequel to grow both the content and product licensing businesses and boost organic downloads of games. Furthermore, for 2020E-21E, we model that product licensing revenue will decline at a pace corresponding to that of the two years following the first movie.

BRAND LICENSING REVENUE, ADJ. EBITDA AND MARGIN, EURm AND %

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

5

10

15

20

25

30

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219E

Q319E

Q419E

Q120E

Q220E

Q320E

Q420E

Q121E

Q221E

Q321E

Q421E

Revenue Adj. EBITDA Adj. EBITDA margin

Source: Company data and Nordea estimates

So far, Hatch has generated zero revenue for Rovio

Hatch reflects one future gaming trend but the payoff is hard to estimate The Other segment consists of the group’s subsidiary Hatch Entertainment and expenses that are not allocated to other segments. Hatch, Rovio's 80%-owned subsidiary, is developing a cloud-based game streaming service for Android mobile devices and TVs. So far, Hatch has generated zero revenue for Rovio and the company is currently looking for external funding to boost the growth prospects of the service.

Marketing material commissioned by Rovio 13

Rovio19 June 2019

In 2018, Hatch's operating expenses amounted to around EUR 7.3m. If Rovio's ownership of Hatch were below 50%, the company would not need to consolidate the unit's numbers on its balance sheet and income statement, which would reduce operating expenses and the asset base. The segment reported capex of EUR 1m for 2018. We expect the unit's expenses to amount to EUR 9.5m, EUR 7.0m and EUR 4.5m for 2019-21, respectively. We do not model any additional costs or investments in Hatch after 2021E. Though Rovio has recently announced collaboration initiatives with Vodafone in the UK and Samsung in the US, we do not assume any revenue from Hatch in our model. However, we derive a USD 45m back-of-the-envelope valuation for Hatch, which reflects the strategic value of the platform. The underlying assumptions for this calculation are shown in the table below.

Global games market by 2021 174,000

% of mobile gaming 52%Global mobile gaming market by 2021 90,480

% of streaming 2%Global streamed mobile gaming 1,810

Hatch's market share 1%Hatch sales (USDm) 18EV/Sales multiple 5EV (USDm) 90Net debt 0Equity value 90Rovio's expected ownership 50%Value of Hatch for Rovio in 2021 45

% of current market value 8%

ESTIMATE OF HATCH VALUE, USDm

Source: Nordea estimates and Newzoo

User acquisition costs drive the opex increase in 2019E We estimate user acquisition costs will rise from EUR 79m in 2018 to EUR 100m in 2019. Rising UA costs, reported under Other operating expenses, reflect our bullish view on the recently launched AB Dream Blast and the soft launch of AB Pop 2. However, we expect the movie sequel to boost the number of organic downloads of selected Angry Birds titles during Q3-Q4 2019. After 2019, we model UA costs will equal roughly 35-36% of the revenue generated by the Games unit over the forecast period (2020-24). Otherwise, we do not see any major cost pressure on a company level and forecast that opex will remain at ~55% of revenue.

COMPANY OPERATING EXPENSES BY SOURCE, EURm

0

10

20

30

40

50

60

70

80

90

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219E

Q319E

Q419E

Q120E

Q220E

Q320E

Q420E

Q121E

Q221E

Q321E

Q421E

Materials and servives Employee benefits expense Other operating expenses

Source: Company data and Nordea estimates

Upcoming Angry Birds Movie 2 will notably boost group EBIT

Brand licensing business should boost full-year 2019 EBIT We believe that the upcoming Angry Birds Movie 2, which is set for release in August 2019, will notably boost group EBIT through the content and consumer products' licensing businesses. We expect the company to exceed its guidance range of 9-11% adjusted operating profitability and deliver a 12% margin for the full-year 2019. Furthermore, we forecast a similar margin throughout our explicit forecast period of 2019-21.

Marketing material commissioned by Rovio 14

Rovio19 June 2019

Unlike the first movie, the sequel is licensed to Sony-owned Columbia Pictures Industries Inc., which bears the majority of the financial risk. However, Rovio's upside is limited to royalties, which we estimate to be 3% of total box office revenue during Q3-Q4 2019. Moreover, we expect the sequel to attract an audience similar to the first movie and forecast that it will pull in USD 350m in box office revenue. In addition to content licensing, the ramped-up consumer product licensing business should drive Rovio's profitability up.

With regards to the Games unit, we expect the adjusted operating margin to be 13% in 2019, just below the 2018 figure of 15%. We believe this margin decline will be caused by higher user acquisition costs (36% of games revenue), whereas we expect other costs to grow in line with revenue in 2019. Nonetheless, we believe user acquisition costs will level out after 2019 and should amount to 33% of games revenue during 2020-24.

Lastly, we do not model any revenue from the Other segment in our forecasts. In 2018, Hatch's operating expenses amounted to around EUR 7.3m. We expect Hatch-related expenses to amount to EUR 9.5m, EUR 7.0m and EUR 4.5m in 2019-21, respectively, after which point we do not model any costs from the unit. Historical and expected operating profit excluding Hatch is presented below.

COMPANY OPERATIONAL PERFORMANCE, EURm AND %

0%

5%

10%

15%

20%

25%

0

10

20

30

40

50

60

70

80

90

100

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219E

Q319E

Q419E

Q120E

Q220E

Q320E

Q420E

Q121E

Q221E

Q321E

Q421E

Revenue Adj. EBIT Adj. EBIT margin EBIT margin (excl. Hatch)

Source: Company data and Nordea estimates

Growing EPS, moderate payout ratio and solid liquidityWe forecast EPS will double from EUR 0.31 to EUR 0.60 during 2018-24, which equals a CAGR of 12%. We believe this growth will be driven by revenue, while we assume profitability and financial costs will remain stable relative to revenue.

We see a high probability of higher annual dividends equalling roughly one third of the company's adjusted net profit

The company paid annual dividends of EUR 0.06 for 2016-17 and EUR 0.09 for 2018-19. Rovio's long-term goal is to distribute around 30% of annual adjusted net profit as dividends and equity returns. Given the company's healthy business model, hefty cash position and limited capex needs in the next few years, we see a high probability of higher annual dividends equalling roughly one third of the company's adjusted net profit.

Considering our expectations for improving operating income, limited capex needs and a moderate payout ratio, we expect Rovio's cash position to remain solid throughout our forecast period. The company's ample liquidity lends it some flexibility in terms of game development, user acquisition and M&A. We note that these attributes are strategic benefits in the mobile gaming industry and that they enable Rovio to sit in the driver's seat in a rapidly growing industry.

Marketing material commissioned by Rovio 15

Rovio19 June 2019

DILUTED EPS, DIVIDEND AND PAYOUT RATIO, EUR AND %

0%

5%

10%

15%

20%

25%

30%

35%

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

EPS, diluted DPS Payout ratio

Source: Company data and Nordea estimates

NET CASH AND GEARING, EURm AND %

-100%

-80%

-60%

-40%

-20%

0%

0

50

100

150

200

250

300

350

Net cash and equivalents Net gearing

Source: Company data and Nordea estimates

ESTIMATED KPIs FOR ROVIO'S TOP-FIVE GAMES CURRENTLY, MILLION AND %

GAME KPIs Q1 19 Q2 19E Q3 19E Q4 19E Q1 20E Q2 20E Q3 20E Q4 20E Q1 21E Q2 21E Q3 21E Q4 21E

AB2Gross bookings 32.0 32.9 35.2 33.8 33.1 32.7 32.7 32.4 30.7 30.1 29.5 28.6

MAU 9.8 10.2 12.3 11.7 11.4 11.2 11.0 10.8 10.3 9.9 9.5 9.1DAU/MAU 20% 20% 18% 18% 18% 18% 18% 18% 18% 18% 18% 18%DAU 2.0 2.0 2.2 2.1 2.1 2.0 2.0 1.9 1.9 1.8 1.7 1.6ARPDAU (EUR) 0.18 0.18 0.17 0.17 0.18 0.18 0.18 0.18 0.18 0.19 0.19 0.19

AB FriendsGross bookings 7.2 6.3 6.6 6.3 6.1 5.9 5.8 5.6 5.2 5.0 4.8 4.5

MAU 2.2 2.1 2.2 2.1 2.0 1.9 1.8 1.8 1.7 1.6 1.5 1.4DAU/MAU 20% 18% 18% 18% 18% 18% 18% 18% 18% 18% 18% 18%DAU 0.4 0.4 0.4 0.4 0.4 0.3 0.3 0.3 0.3 0.3 0.3 0.2ARPDAU 0.18 0.18 0.18 0.18 0.19 0.19 0.19 0.19 0.19 0.19 0.20 0.20

AB Dream BlastGross bookings 6.9 11.3 13.4 12.9 12.6 12.5 12.5 12.4 11.7 11.5 11.3 10.9

MAU 2.1 3.8 4.6 4.4 4.3 4.2 4.1 4.0 3.9 3.7 3.6 3.4DAU/MAU 20% 20% 20% 20% 20% 20% 20% 20% 20% 20% 20% 20%DAU 0.4 0.8 0.9 0.9 0.9 0.8 0.8 0.8 0.8 0.7 0.7 0.7ARPDAU (EUR) 0.18 0.16 0.16 0.16 0.16 0.16 0.17 0.17 0.17 0.17 0.17 0.17

AB MatchGross bookings 6.8 6.0 6.3 6.0 5.8 5.6 5.5 5.3 5.0 4.8 4.7 4.5

MAU 2.1 2.0 2.1 2.0 1.9 1.8 1.7 1.7 1.6 1.5 1.4 1.3DAU/MAU 20% 18% 18% 18% 18% 18% 18% 18% 18% 18% 18% 18%DAU 0.4 0.4 0.4 0.4 0.3 0.3 0.3 0.3 0.3 0.3 0.2 0.2ARPDAU (EUR) 0.18 0.18 0.18 0.18 0.19 0.19 0.19 0.19 0.20 0.20 0.20 0.21

AB POPGross bookings 3.3 2.7 2.9 2.8 2.7 2.6 2.5 2.5 2.3 2.2 2.2 2.1

MAU 1.0 0.9 1.0 0.9 0.9 0.8 0.8 0.8 0.7 0.7 0.6 0.6DAU/MAU 20% 18% 18% 18% 18% 18% 18% 18% 18% 18% 18% 18%DAU 0.2 0.2 0.2 0.2 0.2 0.1 0.1 0.1 0.1 0.1 0.1 0.1ARPDAU (EUR) 0.18 0.19 0.18 0.19 0.19 0.19 0.19 0.19 0.20 0.20 0.20 0.21

Source: Company data and Nordea estimates

Marketing material commissioned by Rovio 16

Rovio19 June 2019

ESTIMATED KPIs FOR THE WHOLE GAME PORTFOLIO, MILLION AND %

GAME KPIs Q1 19 Q2 19E Q3 19E Q4 19E Q1 20E Q2 20E Q3 20E Q4 20E Q1 21E Q2 21E Q3 21E Q4 21E

BookingsGross bookings - TOP 5 56 59 64 62 60 59 59 58 55 54 52 51Gross bookings - All 66 67 73 71 76 74 81 79 82 80 86 83Rolling 12M - TOP5 223 227 237 241 245 245 240 236 231 226 219 212Rolling 12M - All 261 263 273 277 287 294 302 311 317 323 328 331

User amountDAU - TOP 5 3.5 3.7 4.1 3.9 3.8 3.7 3.6 3.5 3.3 3.2 3.1 2.9DAU - All 7.0 6.6 7.0 6.7 6.9 6.7 6.9 6.7 6.8 6.4 6.5 6.2MAU - TOP 5 17.1 19.0 22.1 21.0 20.5 20.0 19.5 19.0 18.2 17.3 16.6 15.8MAU - All 49.3 48.0 51.1 48.7 49.1 47.4 48.2 46.5 46.5 44.0 44.2 41.9

EngagementDAU/MAU - TOP 5 20% 19% 18% 18% 18% 18% 18% 18% 18% 18% 18% 18%DAU/MAU - All 14% 14% 14% 14% 14% 14% 14% 14% 15% 15% 15% 15%

RetentionMAU retention - TOP5 95% 111% 116% 95% 98% 98% 98% 98% 96% 96% 96% 96%MAU retention - All 98% 97% 106% 95% 101% 97% 102% 96% 100% 95% 100% 95%

ConversionMUP - TOP 5 0.4 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.4 0.4 0.4 0.4MUP - All 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.5 0.4 0.4 0.4Conversion rate (TOP5) 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5% 2.5%Conversion rate (All) 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0%

MonetizationARPDAU - TOP 5 0.18 0.18 0.17 0.17 0.18 0.18 0.18 0.18 0.18 0.18 0.19 0.19ARPDAU - All 0.10 0.11 0.11 0.12 0.12 0.12 0.13 0.13 0.14 0.14 0.14 0.14MARPPU - TOP 5 39.0 42.0 39.3 39.7 39.7 40.1 40.9 41.3 40.9 41.8 42.7 43.2MARPPU - All 38.5 46.6 47.3 48.1 51.3 52.0 55.9 56.7 58.8 60.4 64.5 65.5

Source: Company data and Nordea estimates

Negative consensus estimate revision trend since IPOConsensus estimate revisions have been negative since the IPO in September 2017. Estimates were downgraded sharply in February 2018 when Rovio published its Q4 2017 financials and provided guidance for 2018. The main reason has been that so far Rovio has not delivered on its long-term financial goals from 2016, of growth above that of the Western mobile gaming market (~10%) and a 30% EBIT margin.

SALES: CONSENSUS ESTIMATES, EURm

250

300

350

400

450

500

May19

Mar19

Jan19

Nov18

Sep18

Jul18

May18

Mar18

Jan18

Nov17

FY2018 FY2019 FY2020

Source: Thomson Reuters

EBIT: CONSENSUS ESTIMATES, EURm

0

20

40

60

80

100

120

May19

Mar19

Jan19

Nov18

Sep18

Jul18

May18

Mar18

Jan18

Nov17

FY2018 FY2019 FY2020

Source: Thomson Reuters

Marketing material commissioned by Rovio 17

Rovio19 June 2019

EBIT MARGIN: CONSENSUS ESTIMATES, %

0%

5%

10%

15%

20%

25%

May19

Mar19

Jan19

Nov18

Sep18

Jul18

May18

Mar18

Jan18

Nov17

FY2018 FY2019 FY2020

Source: Thomson Reuters

EPS REVISIONS AND NUMBER OF ESTIMATES

-20-15-10-505101520253035

30dMD 18SJMD 17SJ

Upward Downward Num Ests

Source: Thomson Reuters

Our estimates are ahead of consensus on growth but below on marginsThe Thomson Reuters consensus currently expects decelerating growth and an improving EBIT margin for 2020-21. We believe that Rovio will be able to remain on its growth path and forecast a lower EBIT margin than consensus. Consensus expects sales to grow by 13% in 2019 (-5% in 2018), while estimates for 2020 and 2021 are at 7% and -1%, respectively. We estimate sales will grow 12% in 2019, while our 2020 and 2021 estimates are at 6% and 4%, respectively. Along with slowing sales growth estimates, consensus expects the EBIT margin to improve from 10% in 2019 (11% in 2018) to 21% in 2021. We estimate that Rovio will deliver an EBIT margin of 12% (15% excluding Hatch) in 2019, expanding only slightly to 13% (14% excluding Hatch) in 2021.

ROVIO ENTERTAINMENT: OUR ESTIMATES VS CONSENSUS

Nordea estimates Consensus estimates Difference

EURm Q2 2019E 2019E 2020E 2021E Q2 2019E 2019E 2020E 2021E Q2 2019E 2019E 2020E 2021ESales 71.5 315.1 332.6 346.7 74.5 319.0 342.0 338.0 -4% -1% -3% 3%EBITDA 6.5 50.2 50.1 51.3 7.0 46.0 67.0 75.0 -7% 9% -25% -32%EBITDA margin 9% 16% 15% 15% 9% 14% 20% 22% -0.3pp 1.5pp -4.5pp -7.4ppEBIT 2.8 37.2 40.3 44.1 4.0 33.0 54.0 70.0 -29% 13% -25% -37%EBIT margin 4% 12% 12% 13% 5% 10% 16% 21% -1.4pp 1.4pp -3.7pp -8.0ppAdj. EBIT (Excl. Hatch) 5.4 46.6 47.2 48.6 4.0 33.0 54.0 70.0 -29% 13% -25% -37%Adj. EBIT margin (Excl. Hatch) 8% 15% 14% 14% 5% 10% 16% 21% 2.2pp 4.4pp -1.6pp -6.7ppPTP 2.8 37.3 40.2 44.1 6.0 33.0 54.0 70.0 -53% 13% -25% -37%EPS 0.03 0.37 0.40 0.44 0.03 0.32 0.52 0.68 14% 17% -22% -35%Adj. EPS 0.03 0.37 0.40 0.44 0.03 0.32 0.52 0.68 14% 17% -22% -35%DPS 0.11 0.12 0.13 0.10 0.16 0.17 17% -23% -25%

Source: Thomson Reuters and Nordea estimates

Marketing material commissioned by Rovio 18

Rovio19 June 2019

Reported numbers and estimates

REPORTED QUARTERLY NUMBERS AND ESTIMATES, EURm AND %

Company Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18 Q4 18 Q1 19 Q2 19E Q3 19E Q4 19E

Revenue 66 86 71 74 66 72 71 73 71 71 90 83Materials and services 19 20 21 22 18 21 21 20 20 21 24 23Employee benefits expense 13 14 11 14 11 10 10 11 9 10 9 11Other operating expenses 24 23 33 24 22 32 26 33 31 33 36 36EBITDA 10 30 6 14 14 9 15 9 11 6 20 12Adj. EBITDA 10 32 9 14 15 9 15 9 11 6 20 12EBIT 5 14 2 10 9 6 10 6 8 3 17 9Adj. EBIT 5 16 4 11 10 6 10 5 8 3 17 9Adj. EBIT (excl. Hatch) 6 15 3 12 10 8 12 9 9 5 19 12PTP 5 13 -1 10 9 7 10 6 8 3 17 9Net Profit 4 10 -1 8 7 5 8 4 6 2 13 7EPS, diluted 0.05 0.13 -0.01 0.10 0.09 0.07 0.10 0.05 0.07 0.03 0.17 0.09DPSPayout ratio 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%Adj. EBITDA margin 15% 37% 12% 19% 22% 13% 21% 12% 15% 9% 22% 15%Adj. EBIT margin 8% 19% 6% 14% 15% 8% 15% 7% 11% 4% 19% 11%Adj. EBIT margin (excl. Hatch) 10% 18% 4% 16% 16% 10% 17% 12% 13% 8% 21% 14%

Source: Company data and Nordea estimates

REPORTED ANNUAL NUMBERS AND ESTIMATES, EURm AND %

Company 2017 2018 2019E 2020E 2021E 2022E 2023E 2024ECAGR

18-21ECAGR

21E-24ERevenue 297 281 315 333 347 360 376 393 5% 4%Materials and services 82 80 88 97 103 108 114 119 7% 5%Employee benefits expense 52 43 40 40 39 40 40 41 -2% 1%Other operating expenses 104 112 137 145 152 152 158 166 8% 3%EBITDA 60 48 50 50 51 60 63 66 2% 9%Adj. EBITDA 65 48 50 50 51 60 63 66 2% 9%EBIT 31 32 37 40 44 55 59 63 9% 12%Adj. EBIT 36 31 37 40 44 55 59 63 9% 12%Adj. EBIT (excl. Hatch) 36 39 47 47 49 55 59 63 6% 4%PTP 27 32 37 40 44 55 59 63 8% 12%Net Profit 21 25 30 32 36 44 47 50 10% 12%EPS, diluted 0.27 0.31 0.36 0.39 0.43 0.54 0.58 0.62 9% 13%DPS 0.06 0.09 0.11 0.12 0.13 0.16 0.17 0.19 10% 13%Payout ratio 22% 29% 31% 31% 30% 30% 30% 30%Adj. EBITDA margin 22% 17% 16% 15% 15% 17% 17% 17%Adj. EBIT margin 12% 11% 12% 12% 13% 15% 16% 16%Adj. EBIT margin (excl. Hatch) 12% 14% 15% 14% 14% 15% 16% 16%Net cash and equivalents 88 120 158 188 218 253 287 323Net gearing -63% -75% -87% -91% -94% -95% -96% -96%

Source: Company data and Nordea estimates

Marketing material commissioned by Rovio 19

Rovio19 June 2019

Rovio's market Rovio operates in three main entertainment markets: mobile gaming, brand & character licensing, and movies. Because Rovio is a games-first entertainment company, we take a deep dive into the gaming industry in this section, and then introduce the large but mature markets of brand licensing. We take a look at the gaming market as a whole to understand its significant growth history and potential. We believe that mobile gaming is the fastest-growing segment of the gaming market, but this market segment also faces the toughest competition and has the highest user acquisition costs (UAC). According to the mobile marketing platform, Liftoff, paying users in the mobile gaming segment generate average revenue of USD 70 over 90 days, while the cost of acquiring a paying customer was USD 102 in 2018. However, the average lifetime value (LTV) of truly engaged gamers exceeds the 90-day average revenue, as gamers continue to spend money on the games for prolonged periods. Rovio uses a 12-month payback time for its UA investment decisions.

Games segment's market overviewGaming is now the largest entertainment industry in the world

The global gaming market has grown substantially in recent years. In 2018, it generated around USD 135bn, rendering it the largest industry in the entertainment business measured in revenue terms. It also marked the first year ever that revenue from the video game industry surpassed that of the movie industry. Gaming market research provider, Newzoo, forecasts a CAGR of 9.3% for the global gaming market in 2017-21, expecting growth to stem from a larger customer base and a higher willingness to spend.

GLOBAL GAMING REVENUE, USDbn

0%

5%

10%

15%

20%

25%

0

20

40

60

80

100

120

140

160

180

200

2012 2013 2014 2015 2016 2017 2018E 2019E 2020E 2021E

US

Db

n

Global gaming market revenue Growth Y/Y

Source: Newzoo estimates

North America had the largest growth rate in 2018

Gaming market by geographyNorth America, along with Europe, the Middle East, and Africa, enjoyed the greatest growth y/y in 2018. Measured in revenue, China has the biggest market share. Combined with the rest of the APAC region, China accounted for around half of the total global gaming revenue generated in 2018. It goes without saying that China is an interesting market, offering a lucrative opportunity for western gaming companies, especially due to its large player base. North America and EMEA account for roughly 25% and 22% of total global gaming revenue, respectively, while Latin America, with a large player base, still lags significantly in terms of revenue, as it has less than a 4% market share.

Marketing material commissioned by Rovio 20

Rovio19 June 2019

GLOBAL GAMING REVENUE BY REGION, 2018

EMEA22%

LATAM4%

NAM25%

APAC ex. China24%

China25%

Source: Newzoo estimates

GLOBAL GAMING REVENUE GROWTH BY REGION, 2018

13%

11%

14%

8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Growth y/y

EMEA LATAM NAM APAC

Source: Newzoo estimates

According to Newzoo, there are a total of 2.2 billion gamers or gaming enthusiasts globally, ie 1.1 billion excluding APAC. Newzoo defines a gamer as anyone who has installed a game on their smartphone, inflating the number of players who likely account for a decent share of the wallet.

Asia-Pacific is the biggest region measured by number of gamers

As mentioned earlier, the strong growth in the gaming market can be explained by fundamental factors, such as a growing population and continuous online penetration. China is the largest country in terms of revenue, followed by the US, Japan, South Korea, and Germany. We argue that there is more to give in terms of growth, however, as online penetration of countries such as China and India has not yet reached the same levels as in western countries, where online penetration is above or around 90% of the population. With online penetration of 60% for China, and as low as 30% for India and Indonesia, around 1.6 billion people are still 'unconnected', meaning the potential for further growth in the gaming market is enormous.

LARGEST COUNTRIES IN TERMS OF GAMING REVENUE, USDm

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

US

Dm

Total Revenue

Source: Newzoo estimates

ONLINE POPULATION AND PENETRATION, MILLIONS

0%

20%

40%

60%

80%

100%

120%

0

200

400

600

800

1 000

1 200

1 400

1 600

Mill

ions

Population Online Population Online Penetration

Source: Newzoo estimates

Mobile gaming accounted for a whopping 48% of global gaming revenue in 2018

Gaming market by segmentAt 48%, mobile gaming accounted for the largest share of the global gaming market's revenue in 2018. With 2.2 billion players worldwide, smartphone and tablet games together generated revenue of more than USD 63bn during 2018. This represented steady growth y/y, with smartphone and tablet revenue for the year increasing by 14% and 11%, respectively.

The future is not as bright for browser gaming

Breaking down total revenue by platform, Newzoo estimates that smartphones and tablets will experience solid growth during 2017-21. It also forecasts that gaming revenue generated through smartphones will grow the fastest in this period, at a CAGR of 14.4%, while it expects tablet revenue to grow by 7.1% during the same period. Newzoo also forecasts that the overall global gaming market will grow at an annual pace of 9.3% up until 2021, but it expects the worst for browser games, at a CAGR of -19.1%.

With the rise of multi-platform gaming and streaming, the lines between platforms will become increasingly blurred in the future and revenue/statistics may not be categorised in the same way as they are today.

Marketing material commissioned by Rovio 21

Rovio19 June 2019

GLOBAL GAMING REVENUE BY SEGMENT, USDbn

44 50 58 66 75

3338

4143

4728

3031

3233

1213

1516

16

54

33

2

0

20

40

60

80

100

120

140

160

180

200

2017 2018 2019E 2020E 2021E

Smartphone Console PC Tablet Browser

121.7134.9

148.1160.5

174.0

Source: Newzoo estimates

REVENUE CAGR PER SEGMENT, 2017-21E

9.3%

14.4%

9.6%

4.5%7.1%

-19.1%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Total market Smartphone Console PC Tablet Browser

Source: Newzoo estimates

Mobile gamingMobile gaming set to grow the most in the next few years, according to Newzoo

Rovio operates in the mobile gaming market (smartphone and tablet games). Newzoo estimates that mobile gaming will generate total global revenue of USD 91bn by 2021, representing a CAGR of ~13% during 2017-21. The rapid increase in the number of smartphone users around the world has been one of the main drivers behind the solid mobile gaming growth in recent years. Smartphone user growth is being driven by the APAC region, with India leading the pack. Newzoo forecasts a CAGR of 17% for the APAC region during 2018-21.

GLOBAL MOBILE GAMING REVENUE, USDbn

1318

2531

41

5663

7382

91

0102030405060708090

100

Mobile Gaming

Source: Newzoo estimates

GLOBAL SMARTPHONE USERS BY REGION, MILLIONS

0

500

1000

1500

2000

2500

3000

3500

4000

2016 2017 2018 2019E 2020E 2021E

China India

Asia Pacific ex. IND and CHN Middel East & Africa

Eastern Europe Western Europe

Latin America North America

Source: Newzoo estimates

Marketing material commissioned by Rovio 22

Rovio19 June 2019

Monetisation of mobile gamesThe most widely used monetisation methods for mobile are video ads, in-app purchases, and display ads

According to a 2017 survey by AdColony, in which the respondents were mostly gaming developers (90%), the top-three most common methods for monetising apps are video ads, in-app purchases (IAP), and display ads. Self-reported use of these methods was 100%, 91% and 80%, respectively.

These three methods account for 90% of total revenue generated in the mobile apps industry. In-app purchases account for an impressive 39% of revenue generated. In the context of mobile gaming, this could involve purchasing in-game currencies, boosts, timed promotions, themes etc.

MONETISATION TYPE: FREQUENCY OF USE IN MOBILE APPS

100%91%

80%

43%36%

27% 25% 23%

0%

20%

40%

60%

80%

100%

120%

Source: AdColony (Mobile Publishing Survey, 2017) and Nordea

REVENUE PER MONETISATION TYPE IN MOBILE APPS

Video Ads31%

In-app Purchases

39%Display Ads

20%

Native Ads5%

Other5%

Source: AdColony (Mobile Publishing Survey, 2017) and Nordea

In-app purchases are more predominant in gaming than in other mobile apps

The survey also shows considerable differences in how gaming apps monetise their apps relative to other non-gaming apps. Free-to-play games represent another general trend in the industry, whereby developers generate revenue for their free games by offering special features and exclusive content for players who are willing to spend extra. The gap can also be explained by the natural integration of in-game transactions, where the purchase value is immediate and obvious for gamers.

REVENUE % PER MONETISATION, MOBILE GAMING

Video Ads31%

In-app Purchases & mCommerce

43%

Display Ads19%

Native Ads3%

Other4%

Source: AdColony (Mobile Publishing Survey, 2017) and Nordea

REVENUE % PER MONETISATION, OTHER APPS

Video Ads36%

In-app Purchases & mCommerce

21%

Display Ads30%

Native Ads10%

Other3%

Source: AdColony (Mobile Publishing Survey, 2017) and Nordea

Casual games generate the majority of Rovio's revenueDelving deeper into mobile gaming revenue and how it is split, we find that the puzzle and slingshot subcategories – Rovio's main focus – rely heavily on In-app-advertising (IAA). According to data from mobile marketing analytics and attribution platform AppsFlyer, casual games generate 31-58% of their revenue from IAA as opposed to IAP. In this sense, Rovio could increase its share of advertisement revenue as it generated 11% of its revenue through IAA in 2018. However, Rovio's game portfolio is diverse, and includes games from the mid-core and strategy genre too, but the top-five grossing games belong to the casual category at the moment.

Marketing material commissioned by Rovio 23

Rovio19 June 2019

REVENUE SPLIT, CASUAL MOBILE GAMES

69% 65%52%

44% 42% 44%

31% 35%48%

56% 58% 56%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18

IAP IAA

Source: AppsFlyer (The state of Gaming App Marketing, 2018) and Nordea

REVENUE SPLIT, MID-CORE AND STRATEGY MOBILE GAMES

74% 70% 72% 72% 72% 70%

26% 30% 28% 28% 28% 30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18

IAP IAA

Source: AppsFlyer (The state of Gaming App Marketing, 2018) and Nordea

Customer revenue in mobile gamingIn mobile gaming, 10% of customers generate 90% of the revenue

The revenue distribution across gamers in the industry is highly concentrated. Based on a sample of ~400,000 gamers, Rakuten Intelligence reports that 10% of mobile gamers generates around 90% of total gaming revenue, while the top 1% account for a whopping 58% of revenue.

The chart below depicts the nature of mobile gaming market. Because games are free to download and an average player does not spend money on IAPs, most of the players do not generate any meaningful revenue for the gaming companies. According to player analysis platform GameAnalytics, the daily conversion rate, ie the percentage of players that convert to paying users each day, is only 1.2% for the top converting games, while the median daily conversion rate is below 0.4%. This leads to a market where a very small percentage of gamers generate the bulk of total revenue.

SPEND DISTRIBUTION BY PERCENTAGE OF MOBILE GAMERS

0%

20%

40%

60%

80%

100%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

% o

f Rev

enue

% of Users

Source: Rakuten Intelligence (2016) and Nordea estimates

The median 90-day average revenue per paying customer in gaming is USD 70.3, although 90 days is a relatively short time to measure the LTV of engaged gamers

Average revenue per paying customer (ARPPU) is one of the core KPIs in the industry. The metric is used to measure the small segment of customers that contribute to revenue in the industry. According to AppsFlyer, for both organic customers (acquired through app store searches) and non-organic customers (acquired through advertisements), the 90-day average revenue per paying user is USD 70.3.

However, the games-as-a-service business model has become increasingly popular in the mobile gaming industry, which leads to longer lives of games. The best games are able to engage their gamers for multiple years. Thus, the true LTV of engaged gamers is distributed across a prolonged period of time in, for example, games with skilled, live operations teams that continue to add new and interesting content to keep the players engaged. For example, Rovio uses a 12-month payback time for its return on investment calculations when it plans UA investments.

Marketing material commissioned by Rovio 24

Rovio19 June 2019

Organic users spend more money than non-organic users, which is positive for Rovio, as its Angry Birds IP attracts organic downloads

Isolating only non-organic customers, we see values from USD 49.3 to USD 25.7 depending on the country, as the graph below shows. This implies that organic users generate notably higher revenue than non-organic users on average. This is positive for Rovio as the company has a large organic user base bolstered by the global Angry Birds brand.

NON-ORGANIC AVERAGE REVENUE PER PAYING USER, USD

Source: AppsFlyer (2018 LTV Benchmarks)

Across the whole user base, the average revenue is USD 1.7 per customer

Looking at the total user base (ie both paying and non-paying customers), AppsFlyer reports a 90-day average revenue per user (ARPU) of USD 1.7 for organic and non-organic traffic. Below, we outline AppsFlyer's data for average non-organic users only, noting that the US and UK markets are above the other major markets. The global average is reported to be USD 1.31 per non-organic user.

NON-ORGANIC REVENUE PER USER (AVERAGE OF ALL USERS), USD

Source: AppsFlyer (2018 LTV Benchmarks)

The winner takes it all with the top performers accounting for the lion's share of revenue

According to GameAnalytics, which enables the tracking, analysis, and reporting of game metrics, the median purchase volume for the mobile industry is around USD 7, while the top 15% of companies report an average of USD 25 and the bottom 15% report an average of USD 2 per customer. The large gap between the top performers and the median value illustrates the winner-takes-all nature of the industry, as it seems most of the revenue is concentrated at the top.

Customer acquisition costsCustomer acquisition cost (CAC) is one of the core KPIs for e-businesses. As the name suggests, it is the cost associated with acquiring a new customer. As digital companies

Marketing material commissioned by Rovio 25

Rovio19 June 2019

can proactively target their marketing campaigns, CAC is a useful tool that can be used to track the efficiency and effectiveness of marketing efforts. Subtracting the CAC from the customer's lifetime value (LTV) gives the ROI per user, which, for example, drives investment decisions for each game.

Rovio's games are usually easy to pick up and play, so the registration step is not too relevant for Rovio

In the context of mobile games, the acquisition cost is divided into the three stages of customer engagement: installation, registration, and in-app purchasing. In 2018, acquisition costs in terms of installation and registration were down 24% and 42%, respectively, compared with 2017. When acquiring in-app-purchasing (IAP) customers in the industry (which is the critical stage for monetising mobile games), however, the cost rises from USD 76 up to USD 102, representing a 33% increase. The negative trend continues in the engagement rates for the industry, with Liftoff reporting that only ~3% of total customers were willing to make in-app purchases in 2018 compared with 5% the previous year.

MOBILE GAMES: CUSTOMER ACQUISITION COSTS, USD

4.19.4

65.9

3.88.9

76.4

2.9 5.1

101.6

0

20

40

60

80

100

120

Install Register In-App-Purchase

US

D

Axis Title2016 2017 2018

Source: Liftoff (2018 Mobile App Engagement Index) and Nordea

MOBILE GAMES: CUSTOMER ENGAGEMENT RATES, %

44.1%

6.3%

43.2%

5.0%

57.1%

2.9%

0%

10%

20%

30%

40%

50%

60%

Register In-App-Purchase

2016 2017 2018

Source: Liftoff (2018 Mobile App Engagement Index) and Nordea

High demand for mobile ads will lead to higher advertising prices, we believe

We believe increased advertising prices can be expected, as the high segmentation and competitiveness in the market, which have only accelerated in the past few years, are generating high demand for mobile ads. For example, App Annie, which provides global app market data, reports that in 2017, the cumulative number of apps released amounted to 4.5 million, 77% of which were gaming apps.

Efficient customer acquisition strategy is key; this requires adequate cash, especially during game launch

The substantial growth in the number of gaming apps underlines the need for Rovio and other publishers to stand out from the crowd with efficient customer acquisition strategies. To ensure this, companies require sufficient headroom in terms of cash position, especially during the launch phase of new games. We see that Rovio is in a good position to launch new games with its solid expertise in user acquisition and strong balance sheet with a cash position of EUR 128.8m at the end of Q1 2019.

APPS RELEASED ON iOS APP STORE WORLDWIDE

0.0 0.20.4

0.71.1

1.5

2.1

2.8

3.8

4.5

0

1

2

3

4

5

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Mill

ions

Game Apps Other Apps

Source: App Annie (2018) and Nordea estimates

NON-ORGANIC INSTALLS PER CATEGORY, %

Midcore & Strategy

52%Casual37%

Hyper Casual

6%

Casino5%

Source: AppsFlyer (The state of Gaming App Marketing, 2018) and Nordea

Below, we show the monthly trend for the acquisition cost of in-app-purchasing customers, based on Liftoff data for the whole mobile industry. We see an identical trend for the isolated gaming data, with IAP costs on the rise and engagement rates decreasing.

Marketing material commissioned by Rovio 26

Rovio19 June 2019

MONTHLY IN-APP-PURCHASING CAC AND ENGAGEMENT RATES, USD

6169

9198

90 93101

119113 111

128

1134%

4%

3% 3% 3% 3% 3%

3% 3% 3%

2% 2%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

0

20

40

60

80

100

120

140

US

D

IAP Cost Engagement Rate

Source: Liftoff (2018 Mobile App Engagement Index) and Nordea

Acquiring a paying customer is becoming cheaper for most industries, but not for gaming

Below we show the acquisition cost trends for the past three years for the major mobile app categories. For installation and registration, it seems that the gaming subcategory is following the general trend in the market, ie prices are dropping. The cost of acquiring paying customers, however, is showing a decline, which is not visible in the gaming vertical.

INSTALL: USER ACQUISITION COST

01234567

US

D

2016 2017 2018

Source: Liftoff (Mobile Engagement Index) and Nordea

REGISTER: USER ACQUISITION COST

0

5

10

15

20

25

US

D

Axis Title2016 2017 2018

Source: Liftoff (Mobile Engagement Index) and Nordea

PAYMENT: USER ACQUISITION COST

0

50

100

150

US

D

Axis Title2016 2017 2018

Source: Liftoff (Mobile Engagement Index) and Nordea

There are significant cost differences across geographical markets

In terms of regional differences, we find considerable variations in acquisition costs, highlighting the different geographical dynamics. For example, in the APAC region, we see an impressive 99% penetration rate for registered users and the lowest installation and registration costs compared with other regions. Users willing to make in-app purchases in the region are the most expensive to acquire and represent only ~2% of the total user base.

MOBILE CUSTOMER ACQUISITION COST PER REGION, USD

1.6

1.6

110.0

2.5

3.4

83.7

2.5

4.8

91.9

3.9

6.9

105.5

0 20 40 60 80 100 120

Install

Register

In-App Purchase

NAR LATAM EMEA APAC

Source: Liftoff (2018 Mobile App Engagement Index) and Nordea

MOBILE ENGAGEMENT RATES PER REGION

99%

2%

74%

3%

51%

3%

56%

4%

0% 20% 40% 60% 80% 100%

Install

Register

In-App Purchase

NAR LATAM EMEA APAC

Source: Liftoff (2018 Mobile App Engagement Index) and Nordea

Marketing material commissioned by Rovio 27

Rovio19 June 2019

Global licensing marketAccording to LIMA, the licensing industry’s global association, global retail sales of licensed merchandise and services reached USD 271.6bn in 2017, representing growth of 3.3% from the previous year. Altogether, the global licensing industry has grown at a CAGR of 4.0% during 2014-17.