Embed Size (px)

Citation preview

8/6/2019 Royal Ceramics Lanka PLC

http://slidepdf.com/reader/full/royal-ceramics-lanka-plc 1/11

Page 1

Equity Research Report

20 May 201165, Braybrooke Place, Colombo 2, Sri Lanka

[email protected], +94 11 5220200

Equity Research-Q4 2011 Earnings Review

Royal Ceramics Lanka PLC (RCL: LKR 155.60)

Disclaimer: In compiling this report, Bartleet Mallory Stockbrokers (Pvt) Ltd (BMS) has made every endeavour to

ensure its accuracy, but cannot hold ourselves for any errors that may be found herein. We further disclaim all respon-

sibilities for any loss or damage which may be suffered by any person relying upon such information or any options,

conclusions or recommendations herein whether that loss or damage is caused by any fault or negligence on the part

of BMS.

RCL Price Vs ASPI Movement

Sector PER and PBV Trend

BMS Research Team

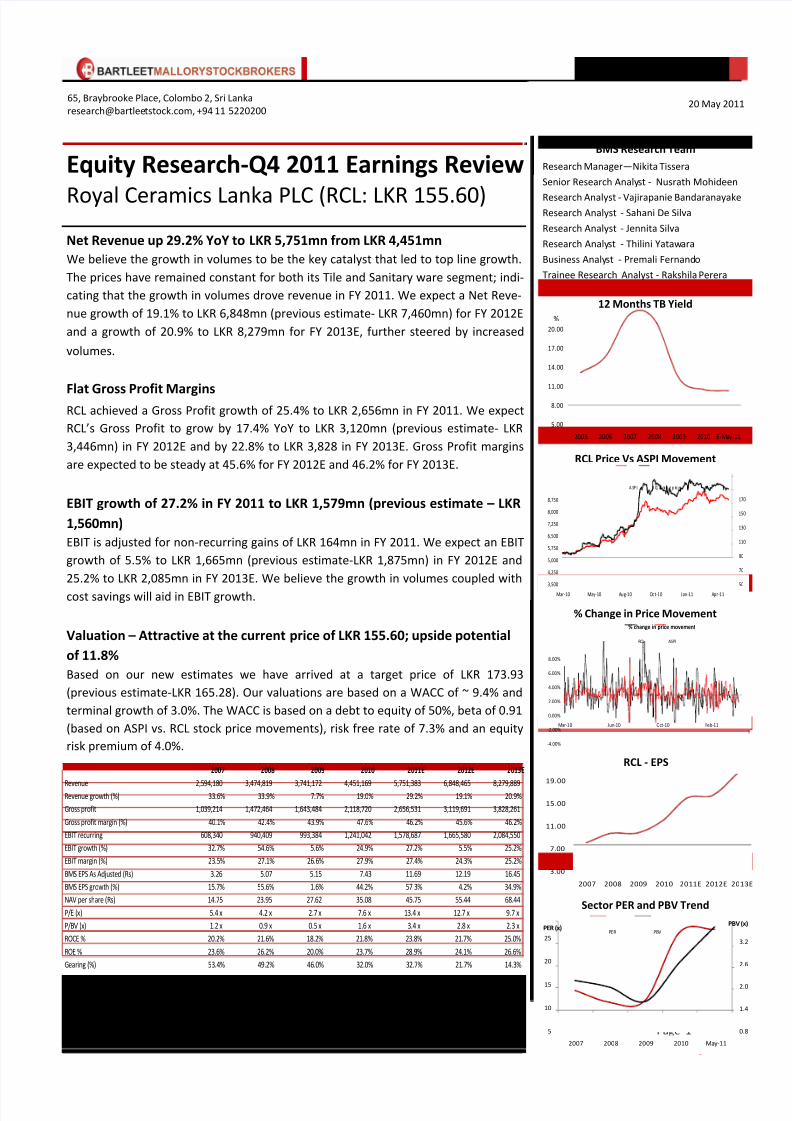

Net Revenue up 29.2% YoY to LKR 5,751mn from LKR 4,451mn

We believe the growth in volumes to be the key catalyst that led to top line growth.

The prices have remained constant for both its Tile and Sanitary ware segment; indi-

cating that the growth in volumes drove revenue in FY 2011. We expect a Net Reve-

nue growth of 19.1% to LKR 6,848mn (previous estimate- LKR 7,460mn) for FY 2012E

and a growth of 20.9% to LKR 8,279mn for FY 2013E, further steered by increased

volumes.

Flat Gross Profit MarginsRCL achieved a Gross Profit growth of 25.4% to LKR 2,656mn in FY 2011. We expect

RCL’s Gross Profit to grow by 17.4% YoY to LKR 3,120mn (previous estimate- LKR

3,446mn) in FY 2012E and by 22.8% to LKR 3,828 in FY 2013E. Gross Profit margins

are expected to be steady at 45.6% for FY 2012E and 46.2% for FY 2013E.

EBIT growth of 27.2% in FY 2011 to LKR 1,579mn (previous estimate – LKR

1,560mn)

EBIT is adjusted for non-recurring gains of LKR 164mn in FY 2011. We expect an EBIT

growth of 5.5% to LKR 1,665mn (previous estimate-LKR 1,875mn) in FY 2012E and

25.2% to LKR 2,085mn in FY 2013E. We believe the growth in volumes coupled with

cost savings will aid in EBIT growth.

Valuation – Attractive at the current price of LKR 155.60; upside potential

of 11.8%

Based on our new estimates we have arrived at a target price of LKR 173.93

(previous estimate-LKR 165.28). Our valuations are based on a WACC of ~ 9.4% and

terminal growth of 3.0%. The WACC is based on a debt to equity of 50%, beta of 0.91

(based on ASPI vs. RCL stock price movements), risk free rate of 7.3% and an equity

risk premium of 4.0%.

% Change in Price Movement

RCL - EPS

Research Manager—Nikita Tissera

Senior Research Analyst - Nusrath Mohideen

Research Analyst - Vajirapanie BandaranayakeResearch Analyst - Sahani De Silva

Research Analyst - Jennita Silva

Research Analyst - Thilini Yatawara

Business Analyst - Premali Fernando

Trainee Research Analyst - Rakshila Perera

5.00

8.00

11.00

14.00

17.00

20.00

2005 2006 2007 2008 2009 2010 6-May-11

%

12 Months TB Yield

0.8

1.4

2.0

2.6

3.2

5

10

15

20

25

2007 2008 2009 2010 May-11

PBV (x)PER (x)

PER PBV

3.00

7.00

11.00

15.00

19.00

2007 2008 2009 2010 2011E 2012E 2013E

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

Mar-10 Jun-10 Oct-10 Feb-11

% change in price movement

RCL ASPI

50

70

90

110

130

150

170

3,500

4,250

5,000

5,750

6,500

7,250

8,000

8,750

Mar-10 May-10 Aug-10 Oct-10 Jan-11 Apr-11

A SP I R CL Cl os in g p ric es

2007 2008 2009 2010 2011E 2012E 2013E

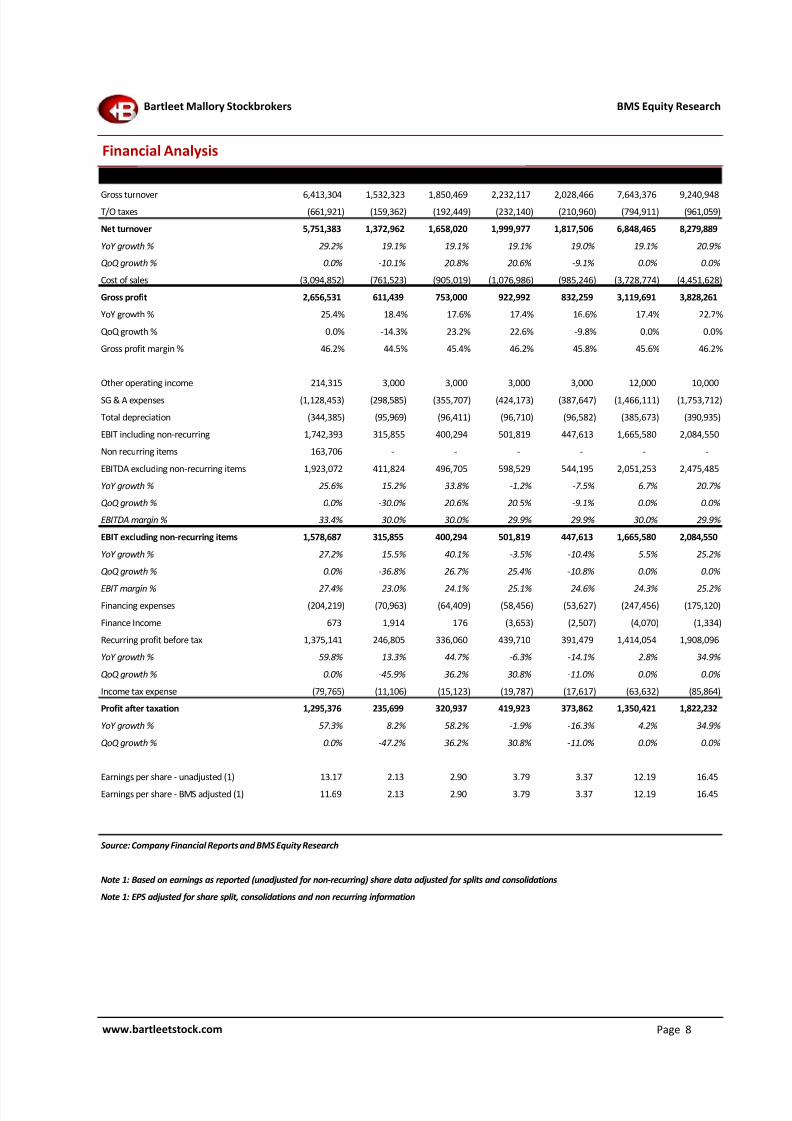

Revenue 2,594,180 3,474,819 3,741,172 4,451,169 5,751,383 6,848,465 8,279,889 Revenue growth (%) 33.6% 33.9% 7.7% 19.0% 29.2% 19.1% 20.9%

Gross profit 1,039,214 1,472,464 1,643,484 2,118,720 2,656,531 3,119,691 3,828,261

Gross profit margin (%) 40.1% 42.4% 43.9% 47.6% 46.2% 45.6% 46.2%

EBIT recurring 608,340 940,409 993,384 1,241,042 1,578,687 1,665,580 2,084,550

EBIT growth (%) 32.7% 54.6% 5.6% 24.9% 27.2% 5.5% 25.2%

EBIT margin (%) 23.5% 27.1% 26.6% 27.9% 27.4% 24.3% 25.2%

BMS EPS As Adjusted (Rs) 3.26 5.07 5.15 7.43 11.69 12.19 16.45

BMS EPS growth (%) 15.7% 55.6% 1.6% 44.2% 57.3% 4.2% 34.9%

NAV per share (Rs) 14.75 23.95 27.62 35.08 45.75 55.44 68.44

P/E (x) 5.4 x 4.2 x 2.7 x 7.6 x 13.4 x 12.7 x 9.7 x

P/BV (x) 1.2 x 0.9 x 0.5 x 1.6 x 3.4 x 2.8 x 2.3 x

ROCE % 20.2% 21.6% 18.2% 21.8% 23.8% 21.7% 25.0%

ROE % 23.6% 26.2% 20.0% 23.7% 28.9% 24.1% 26.6%

Gearing (%) 53.4% 49.2% 46.0% 32.0% 32.7% 21.7% 14.3%

8/6/2019 Royal Ceramics Lanka PLC

http://slidepdf.com/reader/full/royal-ceramics-lanka-plc 2/11

Page 2

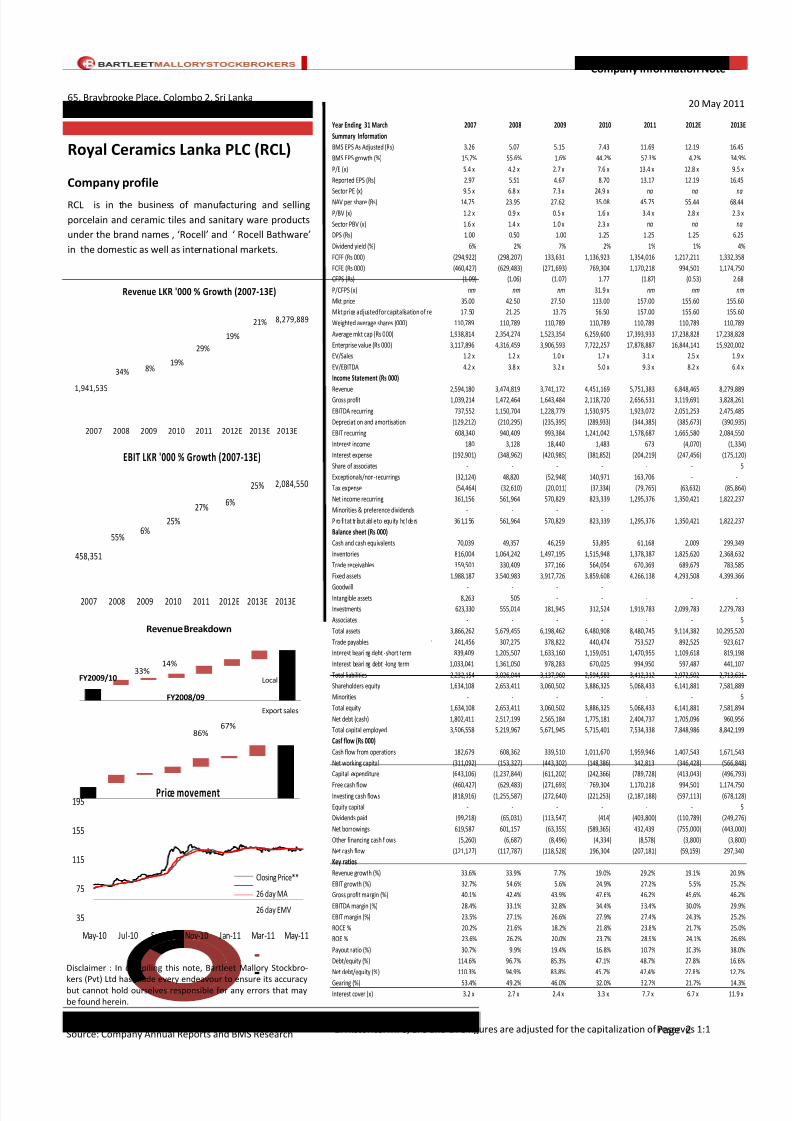

Royal Ceramics Lanka PLC (RCL)

Company profile

RCL is in the business of manufacturing and selling

porcelain and ceramic tiles and sanitary ware products

under the brand names , ‘Rocell’ and ‘ Rocell Bathware’

in the domestic as well as international markets.

Company Information Note

20 May 2011

Source: Company Annual Reports and BMS Research

Disclaimer : In compiling this note, Bartleet Mallory Stockbro-

kers (Pvt) Ltd has made every endeavour to ensure its accuracybut cannot hold ourselves responsible for any errors that may

be found herein.

65, Braybrooke Place, Colombo 2, Sri Lanka

[email protected], +94 11 5220200

Information Notes:

1. Historical MPS, EPS and DPS figures are adjusted for the capitalization of reserves 1:1

1,941,535

8,279,889

34%

21%

8%

19%

19%

29%

2007 2008 2009 2010 2011 2012E 2013E 2013E

Revenue LKR '000 % Growth (2007-13E)

458,351

6%

2,084,550

55%6%

25%

27%

25%

2007 2008 2009 2010 2011 2012E 2013E 2013E

EBIT LKR '000 % Growth (2007-13E)

86%

14%

67%

33%

Revenue Breakdown

Local sales

Export sales

FY2008/09

FY2009/10

35

75

115

155

195

May-10 Jul-10 Sep-10 Nov-10 Jan-11 Mar-11 May-11

Price movement

Closing Price**

26 day MA

26 day EMV

Year Ending 31 March 2007 2008 2009 2010 2011 2012E 2013E

Summary Information

BMS EPS As Adjusted (Rs) 3.26 5.07 5.15 7.43 11.69 12.19 16.45

BMS EPS growth (%) 15.7% 55.6% 1.6% 44.2% 57.3% 4.2% 34.9%

P/E (x) 5.4 x 4.2 x 2.7 x 7.6 x 13.4 x 12.8 x 9.5 x

Reported EPS (Rs) 2.97 5.51 4.67 8.70 13.17 12.19 16.45

Sector PE (x) 9.5 x 6.8 x 7.3 x 24.9 x na na na

NAV per share (Rs) 14.75 23.95 27.62 35.08 45.75 55.44 68.44

P/BV (x) 1.2 x 0.9 x 0.5 x 1.6 x 3.4 x 2.8 x 2.3 x

Sector PBV (x) 1.6 x 1.4 x 1.0 x 2.3 x na na na

DPS (Rs) 1.00 0.50 1.00 1.25 1.25 1.25 6.25

Dividend yield (%) 6% 2% 7% 2% 1% 1% 4%

FCFF (Rs 000) (294,922) (298,207) 133,631 1,136,923 1,354,016 1,217,211 1,332,358

FCFE (Rs 000) (460,427) (629,483) (271,693) 769,304 1,170,218 994,501 1,174,750

CFPS (Rs) (1.09) (1.06) (1.07) 1.77 (1.87) (0.53) 2.68

P/CFPS (x) nm nm nm 31.9 x nm nm nm

Mkt price 35.00 42.50 27.50 113.00 157.00 155.60 155.60

Mkt price adjusted for capitalisation of re 17.50 21.25 13.75 56.50 157.00 155.60 155.60

Weighted average shares (000) 110,789 110,789 110,789 110,789 110,789 110,789 110,789

Average mkt cap (Rs 000) 1,938,814 2,354,274 1,523,354 6,259,600 17,393,933 17,238,828 17,238,828

Enterprise value (Rs 000) 3,117,896 4,316,459 3,906,593 7,722,257 17,878,887 16,844,141 15,920,002

EV/Sales 1.2 x 1.2 x 1.0 x 1.7 x 3.1 x 2.5 x 1.9 x

EV/EBITDA 4.2 x 3.8 x 3.2 x 5.0 x 9.3 x 8.2 x 6.4 x

Income Statement (Rs 000)

Revenue 2,594,180 3,474,819 3,741,172 4,451,169 5,751,383 6,848,465 8,279,889 Gross profit 1,039,214 1,472,464 1,643,484 2,118,720 2,656,531 3,119,691 3,828,261

EBITDA recurring 737,552 1,150,704 1,228,779 1,530,975 1,923,072 2,051,253 2,475,485

Depreciation and amortisation (129,212) (210,295) (235,395) (289,933) (344,385) (385,673) (390,935)

EBIT recurring 608,340 940,409 993,384 1,241,042 1,578,687 1,665,580 2,084,550

Interest income 180 3,128 18,440 1,483 673 (4,070) (1,334)

Interest expense (192,901) (348,962) (420,985) (381,852) (204,219) (247,456) (175,120)

Share of associates - - - - - - 5

Exceptionals/non-recurrings (32,124) 48,820 (52,948) 140,971 163,706 - -

Tax expense (54,464) (32,610) (20,011) (37,334) (79,765) (63,632) (85,864)

Net income recurring 361,156 561,964 570,829 823,339 1,295,376 1,350,421 1,822,237

Minorities & preference dividends - - - -

P ro fi t at tr ibut abl e to equ ity hol de rs 36 1,1 56 561,964 570,829 823,339 1,295,376 1,350,421 1,822,237

Balance sheet (Rs 000)

Cash and cash equivalents 70,039 49,357 46,259 53,895 61,168 2,009 299,349

Inventories 816,004 1,064,242 1,497,195 1,515,948 1,378,387 1,825,620 2,368,632

Trade receivables 359,501 330,409 377,166 564,054 670,369 689,679 783,585

Fixed assets 1,988,187 3,540,983 3,917,726 3,859,608 4,266,138 4,293,508 4,399,366

Goodwill - - - - Intangible assets 8,263 505 - - - - -

Investments 623,330 555,014 181,945 312,524 1,919,783 2,099,783 2,279,783

Associates - - - - - - 5

Total assets 3,866,262 5,679,455 6,198,462 6,480,908 8,480,745 9,114,382 10,295,520

Trade payables 241,456 307,275 378,822 440,474 753,527 892,525 923,617

Interest beari ng debt -short term 839,409 1,205,507 1,633,160 1,159,051 1,470,955 1,109,618 819,198

Interest beari ng debt -long term 1,033,041 1,361,050 978,283 670,025 994,950 597,487 441,107

Total liabilities 2,232,154 3,026,044 3,137,960 2,594,583 3,412,312 2,972,502 2,713,631

Shareholders equity 1,634,108 2,653,411 3,060,502 3,886,325 5,068,433 6,141,881 7,581,889

Minorities - - - - - - 5

Total equity 1,634,108 2,653,411 3,060,502 3,886,325 5,068,433 6,141,881 7,581,894

Net debt (cash) 1,802,411 2,517,199 2,565,184 1,775,181 2,404,737 1,705,096 960,956

Total capital employed 3,506,558 5,219,967 5,671,945 5,715,401 7,534,338 7,848,986 8,842,199

Casf flow (Rs 000)

Cash flow from operations 182,679 608,362 339,510 1,011,670 1,959,946 1,407,543 1,671,543

Net working capital (311,092) (153,327) (443,302) (148,386) 342,813 (346,428) (566,848)

Capital expenditure (643,106) (1,237,844) (611,202) (242,366) (789,728) (413,043) (496,793)

Free cash flow (460,427) (629,483) (271,693) 769,304 1,170,218 994,501 1,174,750 Investing cash flows (818,916) (1,255,587) (272,640) (221,253) (2,187,188) (597,113) (678,128)

Equity capital - - - - - - 5

Dividends paid (99,218) (65,031) (113,547) (414) (403,800) (110,789) (249,276)

Net borrowings 619,587 601,157 (63,355) (589,365) 432,439 (755,000) (443,000)

Other financing cash flows (5,260) (6,687) (8,496) (4,334) (8,578) (3,800) (3,800)

Net cash flow (121,127) (117,787) (118,528) 196,304 (207,181) (59,159) 297,340

Key ratios

Revenue growth (%) 33.6% 33.9% 7.7% 19.0% 29.2% 19.1% 20.9%

EBIT growth (%) 32.7% 54.6% 5.6% 24.9% 27.2% 5.5% 25.2%

Gross profit margin (%) 40.1% 42.4% 43.9% 47.6% 46.2% 45.6% 46.2%

EBITDA margin (%) 28.4% 33.1% 32.8% 34.4% 33.4% 30.0% 29.9%

EBIT margin (%) 23.5% 27.1% 26.6% 27.9% 27.4% 24.3% 25.2%

ROCE % 20.2% 21.6% 18.2% 21.8% 23.8% 21.7% 25.0%

ROE % 23.6% 26.2% 20.0% 23.7% 28.9% 24.1% 26.6%

Payout ratio (%) 30.7% 9.9% 19.4% 16.8% 10.7% 10.3% 38.0%

Debt/equity (%) 114.6% 96.7% 85.3% 47.1% 48.7% 27.8% 16.6%

Net debt/equity (%) 110.3% 94.9% 83.8% 45.7% 47.4% 27.8% 12.7%

Gearing (%) 53.4% 49.2% 46.0% 32.0% 32.7% 21.7% 14.3%Interest cover (x) 3.2 x 2.7 x 2.4 x 3.3 x 7.7 x 6.7 x 11.9 x

8/6/2019 Royal Ceramics Lanka PLC

http://slidepdf.com/reader/full/royal-ceramics-lanka-plc 3/11

Page 3

BMS Equity Research

www.bartleetstock.com

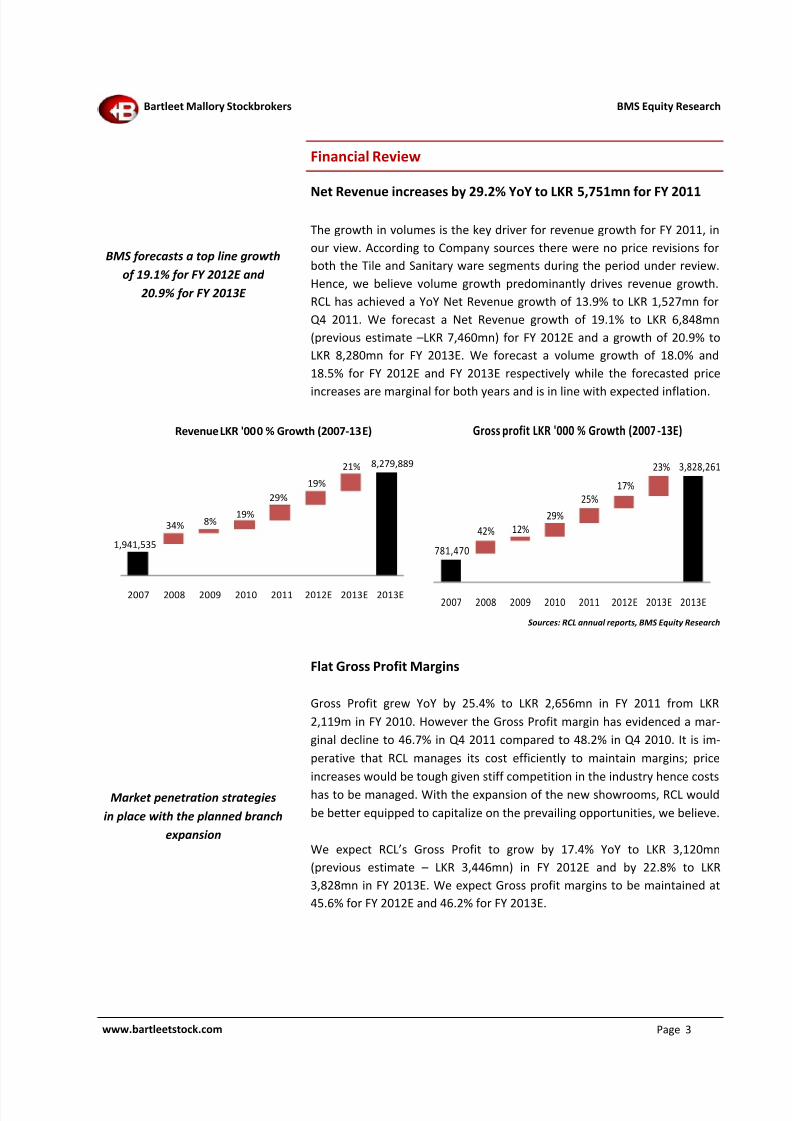

Net Revenue increases by 29.2% YoY to LKR 5,751mn for FY 2011

The growth in volumes is the key driver for revenue growth for FY 2011, in

our view. According to Company sources there were no price revisions for

both the Tile and Sanitary ware segments during the period under review.

Hence, we believe volume growth predominantly drives revenue growth.

RCL has achieved a YoY Net Revenue growth of 13.9% to LKR 1,527mn for

Q4 2011. We forecast a Net Revenue growth of 19.1% to LKR 6,848mn

(previous estimate –LKR 7,460mn) for FY 2012E and a growth of 20.9% to

LKR 8,280mn for FY 2013E. We forecast a volume growth of 18.0% and

18.5% for FY 2012E and FY 2013E respectively while the forecasted price

increases are marginal for both years and is in line with expected inflation.

Flat Gross Profit Margins

Gross Profit grew YoY by 25.4% to LKR 2,656mn in FY 2011 from LKR

2,119m in FY 2010. However the Gross Profit margin has evidenced a mar-

ginal decline to 46.7% in Q4 2011 compared to 48.2% in Q4 2010. It is im-

perative that RCL manages its cost efficiently to maintain margins; price

increases would be tough given stiff competition in the industry hence costs

has to be managed. With the expansion of the new showrooms, RCL would

be better equipped to capitalize on the prevailing opportunities, we believe.

We expect RCL’s Gross Profit to grow by 17.4% YoY to LKR 3,120mn

(previous estimate – LKR 3,446mn) in FY 2012E and by 22.8% to LKR

3,828mn in FY 2013E. We expect Gross profit margins to be maintained at

45.6% for FY 2012E and 46.2% for FY 2013E.

BMS forecasts a top line growth

of 19.1% for FY 2012E and

20.9% for FY 2013E

Financial Review

Market penetration strategies

in place with the planned branch

expansion

Bartleet Mallory Stockbrokers

Sources: RCL annual reports, BMS Equity Research

1,941,535

8,279,889

34%

21%

8%

19%

19%

29%

2007 2008 2009 2010 2011 2012E 2013E 2013E

Revenue LKR '000 % Growth (2007-13E)

781,470

17%

3,828,261

42% 12%

29%

25%

23%

2007 2008 2009 2010 2011 2012E 2013E 2013E

Gross profit LKR '000 % Growth (2007-13E)

8/6/2019 Royal Ceramics Lanka PLC

http://slidepdf.com/reader/full/royal-ceramics-lanka-plc 4/11

Page 4

BMS Equity Research

www.bartleetstock.com

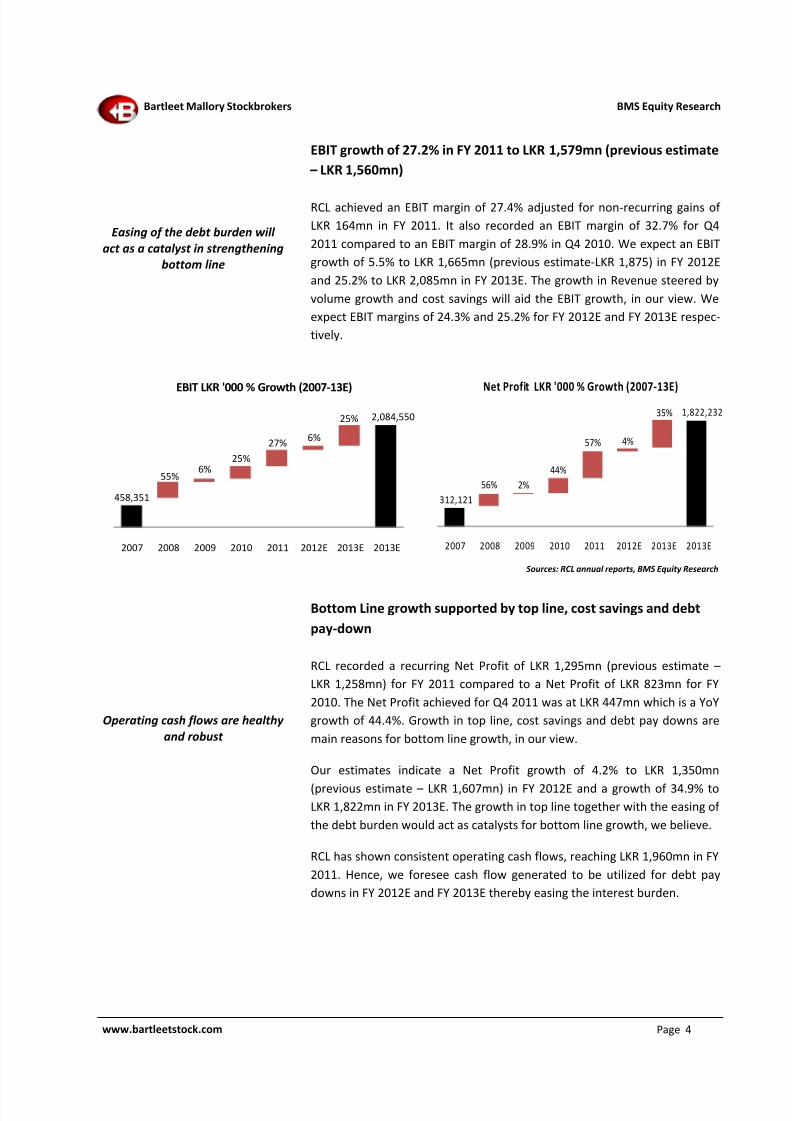

Easing of the debt burden will

act as a catalyst in strengthening

bottom line

EBIT growth of 27.2% in FY 2011 to LKR 1,579mn (previous estimate

– LKR 1,560mn)

RCL achieved an EBIT margin of 27.4% adjusted for non-recurring gains of

LKR 164mn in FY 2011. It also recorded an EBIT margin of 32.7% for Q4

2011 compared to an EBIT margin of 28.9% in Q4 2010. We expect an EBIT

growth of 5.5% to LKR 1,665mn (previous estimate-LKR 1,875) in FY 2012E

and 25.2% to LKR 2,085mn in FY 2013E. The growth in Revenue steered by

volume growth and cost savings will aid the EBIT growth, in our view. We

expect EBIT margins of 24.3% and 25.2% for FY 2012E and FY 2013E respec-

tively.

Bottom Line growth supported by top line, cost savings and debt

pay-down

RCL recorded a recurring Net Profit of LKR 1,295mn (previous estimate –

LKR 1,258mn) for FY 2011 compared to a Net Profit of LKR 823mn for FY

2010. The Net Profit achieved for Q4 2011 was at LKR 447mn which is a YoY

growth of 44.4%. Growth in top line, cost savings and debt pay downs are

main reasons for bottom line growth, in our view.

Our estimates indicate a Net Profit growth of 4.2% to LKR 1,350mn

(previous estimate – LKR 1,607mn) in FY 2012E and a growth of 34.9% to

LKR 1,822mn in FY 2013E. The growth in top line together with the easing of

the debt burden would act as catalysts for bottom line growth, we believe.

RCL has shown consistent operating cash flows, reaching LKR 1,960mn in FY

2011. Hence, we foresee cash flow generated to be utilized for debt pay

downs in FY 2012E and FY 2013E thereby easing the interest burden.

Operating cash flows are healthy

and robust

Bartleet Mallory Stockbrokers

Sources: RCL annual reports, BMS Equity Research

458,351

6%

2,084,550

55%6%

25%

27%

25%

2007 2008 2009 2010 2011 2012E 2013E 2013E

EBIT LKR '000 % Growth (2007-13E)

312,121

4%

1,822,232

56% 2%

44%

57%

35%

2007 2008 2009 2010 2011 2012E 2013E 2013E

Net Profit LKR '000 % Growth (2007-13E)

8/6/2019 Royal Ceramics Lanka PLC

http://slidepdf.com/reader/full/royal-ceramics-lanka-plc 5/11

Page 5

BMS Equity Research

www.bartleetstock.com

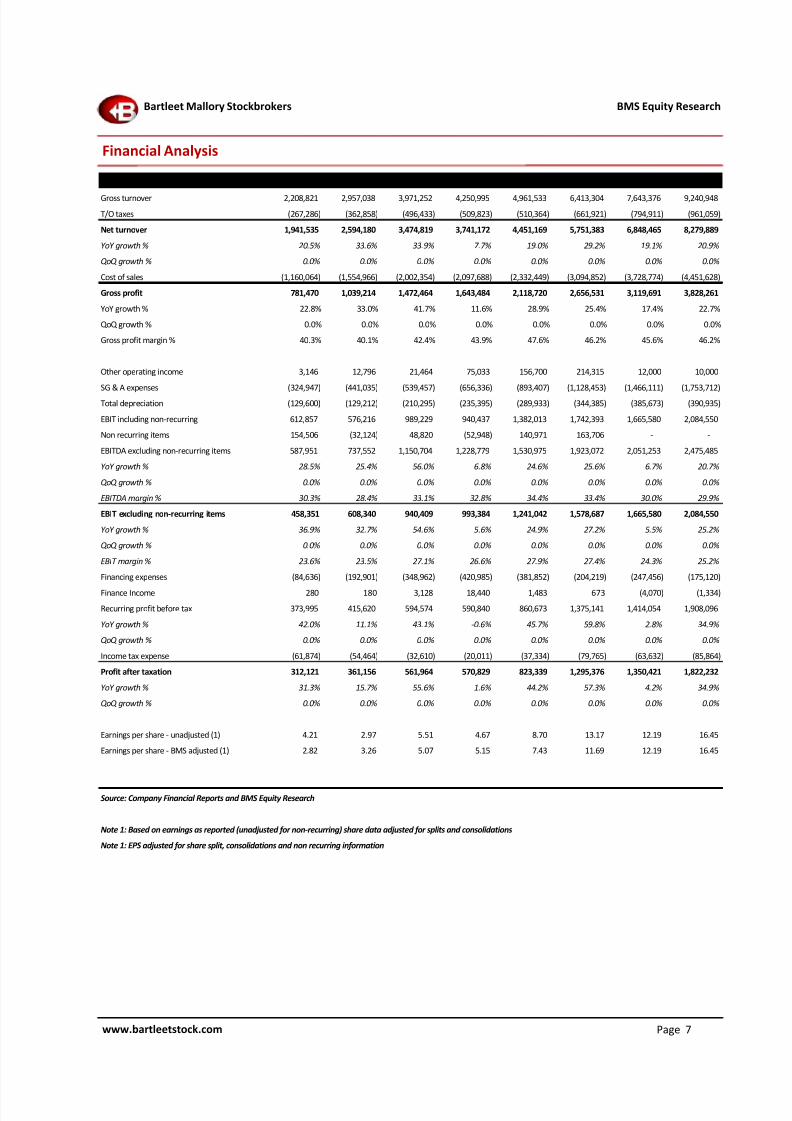

EPS estimates – LKR 12.19 (previous estimate LKR 14.50) FY 2012E

and LKR 16.45 FY 2013E

The expected increase in Revenue led by volume growth is the primary fac-

tor contributing to the EPS growth. The expansions currently taking place in

the country mainly driven by the resurgence of the Hotel sector coupled

with RCL’s new ventures into the sanitary ware market are the main drivers,

we believe. RCL has achieved a recurring EPS of LKR 11.69 for FY 2011.

Valuation – Attractive at the current price of LKR 155.60; upsidepotential of 11.8%

Our main method of valuation is Free Cash Flow basis. Based on our new

estimates we have arrived at a potential value of LKR 173.93 (previous esti-

mate - LKR 165.28). Our valuations are based on a WACC of ~ 9.4% and ter-

minal growth of 3.0%. The WACC is based on a debt to equity of 50%, beta

of 0.91 (based on ASPI vs. RCL stock price movements), risk free rate of

7.3% and an equity risk premium of 4.0%. In addition, our estimates factor

in normalized sales growth 20% and EBIT margins of 20% for both FY 2014E

and FY 2015E. On a relative valuation basis, the stock has a forward PE mul-

tiple of 12.8x based on FY 2012E EPS of LKR 12.19 and current price of LKR

155.60. Based on FY 2013E EPS of LKR 16.45 the stock has a PE multiple of

9.5x. The sector PE stands at 22.9x as at 13 May 2011. The expected NAV

per share for FY 2012E and FY 2013E is LKR 55.44 and LKR 68.44 respec-

tively.

Valuations

Capex

We have factored in ~ LKR 413mn as capital expenditure for FY 2012E and~LKR 497mn for FY 2013E, which amounts to ~6% of the Net Revenue. RCL

has incurred a total capital expenditure of LKR 790mn for the FY 2011. The

Company’s plans to invest in capacity expansion at its manufacturing facility

in Horana, is in process. The expansion would add a further 3,500sqm/day,

increasing total capacity to 14,300sqm/day from the current capacity levels

of 10,800sqm/day (Eheliyagoda 3,500sqm/day and Horana 7,300sqm/day).

RCL also intends to open 10 new showrooms outside the Western Province;

however they have not incurred any expenditure on the showrooms to

date. The management of RCL is of the view that one of the showrooms will

be opened during Q1 2012E. The estimated cost is ~ LKR 50mn with an

BMS adjusted EPS is LKR 12.19 for FY 2012E

RCL has a value ~ LKR 173.93

based on free cash flow

valuations

Capex is estimated at 6% of Net

Revenue for FY 2012E

Capex and Risk Evaluation

Bartleet Mallory Stockbrokers

8/6/2019 Royal Ceramics Lanka PLC

http://slidepdf.com/reader/full/royal-ceramics-lanka-plc 6/11

Page 6

BMS Equity Research

www.bartleetstock.com

Cheap imports from rivalry

nations is the biggest threat to

RCL

Escalating crude oil prices could

have adverse impacts to the

bottom line, in our view

average cost of LKR 5mn per showroom. RCL plans to fund capex through me-

dium term debt at floating interest rates, spanning a 5-year period.

Risk Evaluation

We feel the cheap imports from overseas rivals such as China and India invad-

ing the local Ceramic market as the prime risk faced by RCL. According to the

sources from the Department of Commerce, under the Indo Lanka Free Trade

Agreement, Indian ceramic tiles receive a 100% duty concession by the GOSL

effective from 31 March, 2008; making the Ceramic Tile market more com-

petitive. In such a backdrop we find that RCL’s recent diversification strategy

to venture in to the Bath Ware market, a forward looking decision. As low

cost imports and high end brands are dominant in the market, RCL’s successin this area depends on how they position themselves and price their prod-

ucts.

In RCL’s cost structure, ~ 33% constitutes of energy cost, thus, any fluctuation

in the crude oil prices and electricity has a direct and significant impact on the

Bottom Line. Even in a rising energy cost scenario, RCL will find it difficult to

go for a price revision, owing to fierce competition, in our view. Due to the

global economic recovery, rising demand from vibrant economies of China

and India, and the upheaval in the Middle East, crude oil prices crossed the

USD 100 mark during April 2011. This is a hike of over 35% compared to the

price levels in April 2010. However rising energy cost is a systematic risk,

hence availability of risk minimization strategies are minimal, we believe.

RCL’s exposure to FOREX risk is insignificant, as exports contribute only ~5%

to total sales. Since the management concentration is to expand the foothold

in the domestic market, we expect the export sales to remain in its existing

levels; also as RCL’s raw material imports are limited to only chemicals, we

see no notable risk pertaining to RCL’s foreign exchange transactions.

FOREX risk is insignificant

for RCL

Bartleet Mallory Stockbrokers

8/6/2019 Royal Ceramics Lanka PLC

http://slidepdf.com/reader/full/royal-ceramics-lanka-plc 7/11

Page 7www.bartleetstock.com

BMS Equity Research

Financial Analysis

Bartleet Mallory Stockbrokers

All numbers in LKR '000 2006 2007 2008 2009 2010 2011 2012E 2013E

Gross turnover 2,208,821 2,957,038 3,971,252 4,250,995 4,961,533 6,413,304 7,643,376 9,240,948

T/O taxes (267,286) (362,858) (496,433) (509,823) (510,364) (661,921) (794,911) (961,059)

Net turnover 1,941,535 2,594,180 3,474,819 3,741,172 4,451,169 5,751,383 6,848,465 8,279,889

YoY growth % 20.5% 33.6% 33.9% 7.7% 19.0% 29.2% 19.1% 20.9%

QoQ growth % 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Cost of sales (1,160,064) (1,554,966) (2,002,354) (2,097,688) (2,332,449) (3,094,852) (3,728,774) (4,451,628)

Gross profit 781,470 1,039,214 1,472,464 1,643,484 2,118,720 2,656,531 3,119,691 3,828,261

YoY growth % 22.8% 33.0% 41.7% 11.6% 28.9% 25.4% 17.4% 22.7%

QoQ growth % 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Gross profit margin % 40.3% 40.1% 42.4% 43.9% 47.6% 46.2% 45.6% 46.2%

Other operating income 3,146 12,796 21,464 75,033 156,700 214,315 12,000 10,000

SG & A expenses (324,947) (441,035) (539,457) (656,336) (893,407) (1,128,453) (1,466,111) (1,753,712)

Total depreciation (129,600) (129,212) (210,295) (235,395) (289,933) (344,385) (385,673) (390,935)

EBIT including non-recurring 612,857 576,216 989,229 940,437 1,382,013 1,742,393 1,665,580 2,084,550

Non recurring items 154,506 (32,124) 48,820 (52,948) 140,971 163,706 - -

EBITDA excluding non-recurring items 587,951 737,552 1,150,704 1,228,779 1,530,975 1,923,072 2,051,253 2,475,485

YoY growth % 28.5% 25.4% 56.0% 6.8% 24.6% 25.6% 6.7% 20.7%

QoQ growth % 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

EBITDA margin % 30.3% 28.4% 33.1% 32.8% 34.4% 33.4% 30.0% 29.9%

EBIT excluding non-recurring items 458,351 608,340 940,409 993,384 1,241,042 1,578,687 1,665,580 2,084,550

YoY growth % 36.9% 32.7% 54.6% 5.6% 24.9% 27.2% 5.5% 25.2%

QoQ growth % 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

EBIT margin % 23.6% 23.5% 27.1% 26.6% 27.9% 27.4% 24.3% 25.2%

Financing expenses (84,636) (192,901) (348,962) (420,985) (381,852) (204,219) (247,456) (175,120)

Finance Income 280 180 3,128 18,440 1,483 673 (4,070) (1,334)

Recurring profit before tax 373,995 415,620 594,574 590,840 860,673 1,375,141 1,414,054 1,908,096

YoY growth % 42.0% 11.1% 43.1% -0.6% 45.7% 59.8% 2.8% 34.9%

QoQ growth % 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Income tax expense (61,874) (54,464) (32,610) (20,011) (37,334) (79,765) (63,632) (85,864)

Profit after taxation 312,121 361,156 561,964 570,829 823,339 1,295,376 1,350,421 1,822,232

YoY growth % 31.3% 15.7% 55.6% 1.6% 44.2% 57.3% 4.2% 34.9%

QoQ growth % 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Earnings per share - unadjusted (1) 4.21 2.97 5.51 4.67 8.70 13.17 12.19 16.45

Earnings per share - BMS adjusted (1) 2.82 3.26 5.07 5.15 7.43 11.69 12.19 16.45

Source: Company Financial Reports and BMS Equity Research

Note 1: Based on earnings as reported (unadjusted for non-recurring) share data adjusted for splits and consolidations

Note 1: EPS adjusted for share split, consolidations and non recurring information

8/6/2019 Royal Ceramics Lanka PLC

http://slidepdf.com/reader/full/royal-ceramics-lanka-plc 8/11

Page 8www.bartleetstock.com

BMS Equity Research

Financial Analysis

Bartleet Mallory Stockbrokers

All numbers in LKR '000 2011 Q1 11/12E Q2 11/12E Q3 11/12E Q4 11/12E 2012E 2013E

Gross turnover 6,413,304 1,532,323 1,850,469 2,232,117 2,028,466 7,643,376 9,240,948

T/O taxes (661,921) (159,362) (192,449) (232,140) (210,960) (794,911) (961,059)

Net turnover 5,751,383 1,372,962 1,658,020 1,999,977 1,817,506 6,848,465 8,279,889

YoY growth % 29.2% 19.1% 19.1% 19.1% 19.0% 19.1% 20.9%

QoQ growth % 0.0% -10.1% 20.8% 20.6% -9.1% 0.0% 0.0%

Cost of sales (3,094,852) (761,523) (905,019) (1,076,986) (985,246) (3,728,774) (4,451,628)

Gross profit 2,656,531 611,439 753,000 922,992 832,259 3,119,691 3,828,261

YoY growth % 25.4% 18.4% 17.6% 17.4% 16.6% 17.4% 22.7%

QoQ growth % 0.0% -14.3% 23.2% 22.6% -9.8% 0.0% 0.0%

Gross profit margin % 46.2% 44.5% 45.4% 46.2% 45.8% 45.6% 46.2%

Other operating income 214,315 3,000 3,000 3,000 3,000 12,000 10,000

SG & A expenses (1,128,453) (298,585) (355,707) (424,173) (387,647) (1,466,111) (1,753,712)

Total depreciation (344,385) (95,969) (96,411) (96,710) (96,582) (385,673) (390,935)

EBIT including non-recurring 1,742,393 315,855 400,294 501,819 447,613 1,665,580 2,084,550

Non recurring items 163,706 - - - - - -

EBITDA excluding non-recurring items 1,923,072 411,824 496,705 598,529 544,195 2,051,253 2,475,485

YoY growth % 25.6% 15.2% 33.8% -1.2% -7.5% 6.7% 20.7%

QoQ growth % 0.0% -30.0% 20.6% 20.5% -9.1% 0.0% 0.0%

EBITDA margin % 33.4% 30.0% 30.0% 29.9% 29.9% 30.0% 29.9%

EBIT excluding non-recurring items 1,578,687 315,855 400,294 501,819 447,613 1,665,580 2,084,550

YoY growth % 27.2% 15.5% 40.1% -3.5% -10.4% 5.5% 25.2%

QoQ growth % 0.0% -36.8% 26.7% 25.4% -10.8% 0.0% 0.0%

EBIT margin % 27.4% 23.0% 24.1% 25.1% 24.6% 24.3% 25.2%

Financing expenses (204,219) (70,963) (64,409) (58,456) (53,627) (247,456) (175,120)

Finance Income 673 1,914 176 (3,653) (2,507) (4,070) (1,334)

Recurring profit before tax 1,375,141 246,805 336,060 439,710 391,479 1,414,054 1,908,096

YoY growth % 59.8% 13.3% 44.7% -6.3% -14.1% 2.8% 34.9%

QoQ growth % 0.0% -45.9% 36.2% 30.8% -11.0% 0.0% 0.0%

Income tax expense (79,765) (11,106) (15,123) (19,787) (17,617) (63,632) (85,864)

Profit after taxation 1,295,376 235,699 320,937 419,923 373,862 1,350,421 1,822,232

YoY growth % 57.3% 8.2% 58.2% -1.9% -16.3% 4.2% 34.9%

QoQ growth % 0.0% -47.2% 36.2% 30.8% -11.0% 0.0% 0.0%

Earnings per share - unadjusted (1) 13.17 2.13 2.90 3.79 3.37 12.19 16.45

Earnings per share - BMS adjusted (1) 11.69 2.13 2.90 3.79 3.37 12.19 16.45

Source: Company Financial Reports and BMS Equity Research

Note 1: Based on earnings as reported (unadjusted for non-recurring) share data adjusted for splits and consolidations

Note 1: EPS adjusted for share split, consolidations and non recurring information

8/6/2019 Royal Ceramics Lanka PLC

http://slidepdf.com/reader/full/royal-ceramics-lanka-plc 9/11

Page 9www.bartleetstock.com

BMS Equity Research

Financial Analysis

Bartleet Mallory Stockbrokers

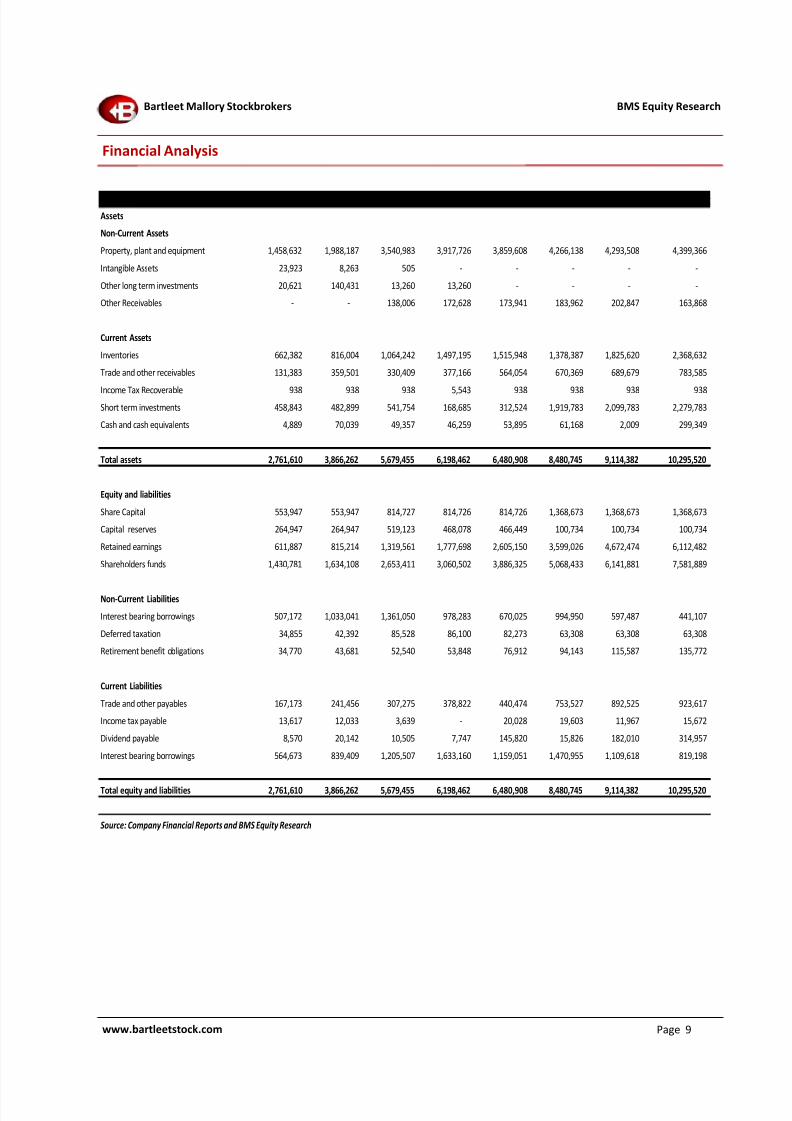

All numbers in LKR '000 2006 2007 2008 2009 2010 2011 2012E 2013E

Assets

Non-Current Assets

Property, plant and equipment 1,458,632 1,988,187 3,540,983 3,917,726 3,859,608 4,266,138 4,293,508 4,399,366

Intangible Assets 23,923 8,263 505 - - - - -

Other long term investments 20,621 140,431 13,260 13,260 - - - -

Other Receivables - - 138,006 172,628 173,941 183,962 202,847 163,868

Current Assets

Inventories 662,382 816,004 1,064,242 1,497,195 1,515,948 1,378,387 1,825,620 2,368,632

Trade and other receivables 131,383 359,501 330,409 377,166 564,054 670,369 689,679 783,585

Income Tax Recoverable 938 938 938 5,543 938 938 938 938 Short term investments 458,843 482,899 541,754 168,685 312,524 1,919,783 2,099,783 2,279,783

Cash and cash equivalents 4,889 70,039 49,357 46,259 53,895 61,168 2,009 299,349

Total assets 2,761,610 3,866,262 5,679,455 6,198,462 6,480,908 8,480,745 9,114,382 10,295,520

Equity and liabilities

Share Capital 553,947 553,947 814,727 814,726 814,726 1,368,673 1,368,673 1,368,673

Capital reserves 264,947 264,947 519,123 468,078 466,449 100,734 100,734 100,734

Retained earnings 611,887 815,214 1,319,561 1,777,698 2,605,150 3,599,026 4,672,474 6,112,482

Shareholders funds 1,430,781 1,634,108 2,653,411 3,060,502 3,886,325 5,068,433 6,141,881 7,581,889

Non-Current Liabilities

Interest bearing borrowings 507,172 1,033,041 1,361,050 978,283 670,025 994,950 597,487 441,107

Deferred taxation 34,855 42,392 85,528 86,100 82,273 63,308 63,308 63,308

Retirement benefit obligations 34,770 43,681 52,540 53,848 76,912 94,143 115,587 135,772

Current Liabilities

Trade and other payables 167,173 241,456 307,275 378,822 440,474 753,527 892,525 923,617

Income tax payable 13,617 12,033 3,639 - 20,028 19,603 11,967 15,672

Dividend payable 8,570 20,142 10,505 7,747 145,820 15,826 182,010 314,957

Interest bearing borrowings 564,673 839,409 1,205,507 1,633,160 1,159,051 1,470,955 1,109,618 819,198

Total equity and liabilities 2,761,610 3,866,262 5,679,455 6,198,462 6,480,908 8,480,745 9,114,382 10,295,520

Source: Company Financial Reports and BMS Equity Research

8/6/2019 Royal Ceramics Lanka PLC

http://slidepdf.com/reader/full/royal-ceramics-lanka-plc 10/11

Page 10www.bartleetstock.com

BMS Equity Research

Financial Analysis

Bartleet Mallory Stockbrokers

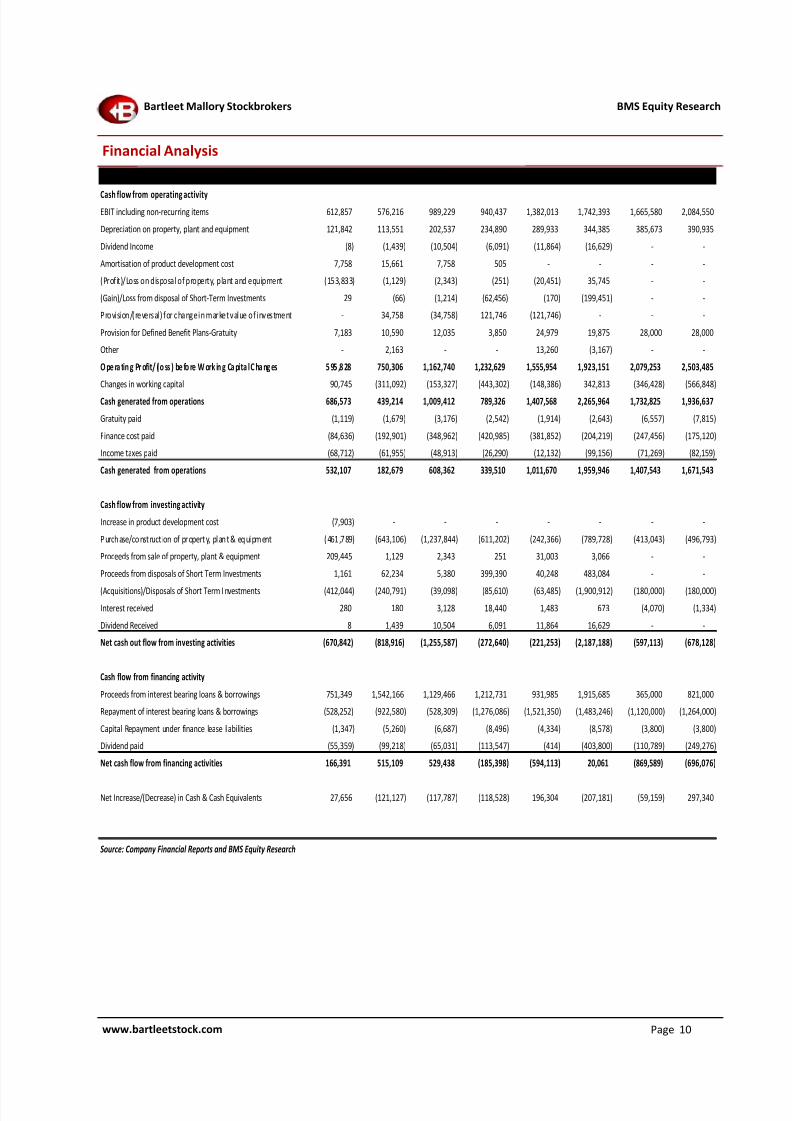

All numbers in LKR '000 2006 2007 2008 2009 2010 2011 2012E 2013E

Cash flow from operating activityEBIT including non-recurring items 612,857 576,216 989,229 940,437 1,382,013 1,742,393 1,665,580 2,084,550

Depreciation on property, plant and equipment 121,842 113,551 202,537 234,890 289,933 344,385 385,673 390,935

Dividend Income (8) (1,439) (10,504) (6,091) (11,864) (16,629) - -

Amortisation of product development cost 7,758 15,661 7,758 505 - - - -

(Profit)/Loss on disposal of property, plant and equipment (153,833) (1,129) (2,343) (251) (20,451) 35,745 - -

(Gain)/Loss from disposal of Short-Term Investments 29 (66) (1,214) (62,456) (170) (199,451) - -

Provision/(reversal) for change in market value of investment - 34,758 (34,758) 121,746 (121,746) - - -

Provision for Defined Benefit Plans-Gratuity 7,183 10,590 12,035 3,850 24,979 19,875 28,000 28,000

Other - 2,163 - - 13,260 (3,167) - -

O pe ra tin g Pr ofit/ (lo ss ) be fo re W ork in g Ca pita l C ha ng es 5 95 ,8 28 750,306 1,162,740 1,232,629 1,555,954 1,923,151 2,079,253 2,503,485

Changes in working capital 90,745 (311,092) (153,327) (443,302) (148,386) 342,813 (346,428) (566,848)

Cash generated from operations 686,573 439,214 1,009,412 789,326 1,407,568 2,265,964 1,732,825 1,936,637

Gratuity paid (1,119) (1,679) (3,176) (2,542) (1,914) (2,643) (6,557) (7,815)

Finance cost paid (84,636) (192,901) (348,962) (420,985) (381,852) (204,219) (247,456) (175,120)

Income taxes paid (68,712) (61,955) (48,913) (26,290) (12,132) (99,156) (71,269) (82,159)

Cash generated from operations 532,107 182,679 608,362 339,510 1,011,670 1,959,946 1,407,543 1,671,543

Cash flow from investing activity

Increase in product development cost (7,903) - - - - - - -

P urchase/construct ion of property, plant & equipm ent (461,789) (643,106) (1,237,844) (611,202) (242,366) (789,728) (413,043) (496,793)

Proceeds from sale of property, plant & equipment 209,445 1,129 2,343 251 31,003 3,066 - -

Proceeds from disposals of Short Term Investments 1,161 62,234 5,380 399,390 40,248 483,084 - -

(Acquisitions)/Disposals of Short Term I nvestments (412,044) (240,791) (39,098) (85,610) (63,485) (1,900,912) (180,000) (180,000)

Interest received 280 180 3,128 18,440 1,483 673 (4,070) (1,334)

Dividend Received 8 1,439 10,504 6,091 11,864 16,629 - -

Net cash out flow from investing activities (670,842) (818,916) (1,255,587) (272,640) (221,253) (2,187,188) (597,113) (678,128)

Cash flow from financing activity

Proceeds from interest bearing loans & borrowings 751,349 1,542,166 1,129,466 1,212,731 931,985 1,915,685 365,000 821,000

Repayment of interest bearing loans & borrowings (528,252) (922,580) (528,309) (1,276,086) (1,521,350) (1,483,246) (1,120,000) (1,264,000)

Capital Repayment under finance lease liabilities (1,347) (5,260) (6,687) (8,496) (4,334) (8,578) (3,800) (3,800)

Dividend paid (55,359) (99,218) (65,031) (113,547) (414) (403,800) (110,789) (249,276)

Net cash flow from financing activities 166,391 515,109 529,438 (185,398) (594,113) 20,061 (869,589) (696,076)

Net Increase/(Decrease) in Cash & Cash Equivalents 27,656 (121,127) (117,787) (118,528) 196,304 (207,181) (59,159) 297,340

Source: Company Financial Reports and BMS Equity Research

8/6/2019 Royal Ceramics Lanka PLC

http://slidepdf.com/reader/full/royal-ceramics-lanka-plc 11/11

Page 11

Bartleet Mallory Stockbrokers (Pvt) Ltdwww.bartleetstock.com

BMS Equity Research - [email protected]

![Sri Lanka Telecom PLC · Sri Lanka Telecom PLC Annual Report 2015 [ 03 ] Welcome to Sri Lanka Telecom PLC’s Annual Report 2015 This Annual Report 2015 of Sri Lanka Telecom PLC is](https://img.pdfslide.net/doc/110x75/5ec1c7bf44f9c177e824dbb3/sri-lanka-telecom-plc-sri-lanka-telecom-plc-annual-report-2015-03-welcome-to.jpg)