Embed Size (px)

Citation preview

Deloitte Research Centre | Seventh issue | 2Q 2017

Russia through a lensMacroeconomic outlookKey Russian macroeconomic indicators in 2Q 2017

Page 04

Innovations and digitalization40 RUB billion is R&D expenses planned by the surveyed companies in 2017

Page 16

Steel and iron marketOver the first three months of 2017 saw global steel output reach 410.5 mln tonnes, up 5.7 % from the same period in 2016

Page 22

Pharmaceutical MarketNew trends in strategic development: focus on R&D activities and deeper localization

Page 24

Russia through a lens

02

03

Russia through a lens

Content

04Russia in figuresMacroeconomic outlook (GDP, inflation, trade indicators, currency rate, Central Bank key rate, top-pricing, etc.)

14Research Centre market analysis"CFO Survey in Russia""Overview of steel and iron market""Russian Pharmaceutical Market Trends in 2017"

27Global windTop news: China and RussiaTop news: Europe and Russia

30Contacts

28Useful stickers

26Top M&AsTop-5 deals in Russia

Page 14 Page 22 Page 24

We are pleased to present the latest edition of Russia Through a Lens, the macroeconomic journal produced by Deloitte Research Centre in Moscow.

Established in December 2015, the journal is published quarterly and falls under the Research Centre’s monitoring activities.

In Russia Through a Lens, we focus on current key trends in the Russian economy and present our research key findings.

If you have any questions or suggestions regarding this research, please do not hesitate to contact us:[email protected]

Designed by the Deloitte Design Group, Moscow

Russia through a lens | Russia in figures

04

Russia in figuresGDPGDP per year

The data for the period from 2011 includes changes related to the implementation of the international methodology for housing services evaluation, the evaluation of capital consumption taking into account its current market value, and the conformation of data on exports and imports with the data presented

in the balance of payments developed according to the methodology provided by the Sixth Edition of the Balance of Payments and International Investment Position Manual (BPM6) introduced by the International Monetary Fund.

Forecasts for 2017:

Period The Ministry of Economic Development

Central Bank

Russian Academy of Sciences Institute of Economic Forecasting (IEF RAS)

Standard & Poors

Moody’s Eurocomission World Bank

International Monetary Fund

JPMorgan EBRD Gaidar Institute

2017 +2.0%+1.3% to +1.8%

+1.5% +1.4% +1.5% +1.2% +1.3% +1.4% +1.0% +1.2% +1.2%

2018 +1.7%+ 1.0% to +1,5%

+1.6% +1.7% +1.5% +1.4% +1.4% +1.4% n/a +1.4% +1.8%

150, 000

130, 000

110, 000

90, 000

70, 000

50, 000

30, 000

10, 000

0

21,61026,917

25%

33,248

24% 24%

41,277

–6%

38,807

19%

46,309

29%

59,698

12%

66,927

6%

71,017

12%

79,200

5%

–2.8%83,233

3.4% 2.0%–0.2%86,044 87,765

50%

30%

10%

–10%

–30%

–50%

–70%

–90%

–110%

–130%

0.7%1.3%3.5%4.3%4.5%–7.8%

5.2%8.5%8.2%

2005 2006 20102008 2012 2015 2007 2011 20142009 2013 2016 2017F*

GDP, bln RUB GDP growth (at current prices) GDP volume indicesSource: Rosstat, Ministry of Economic Development (*forecast)

Source: Rosstat, Central Bank of Russia (*forecast)

2Q GDP

20,000

19,000

17,000

15,000

13,000

11,000

9,000

7,000

5,0006,368

7,768

10,2389,245

10,977

14,314

16,14917,015

19,128 19,85820,430

20,634

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017F*

GDP, bln RUB

«According to the Central Bank assessment, GDP quarterly growth rate in the second quarter of 2017 comprised 0.3-0.5% considering elimination of a seasonal and calendar factors. It corresponds to approximately 1% growth of GDP as compared to the respective period of the last year.»

Source: Central Bank (Banki.ru)

Russia through a lens | Russia in figures

05

InflationInflation, %

Forecast:

Source 2017

International Monetary Fund 4.0%

World Bank 3.9%

VEB 3.7%

Bloomberg 4.3%

Inflation in May 2017*: 4.1%Inflation target** in 2017: 4.0%

*The inflation figure is the consumer price growth rate over the corresponding month of the previous year.**The inflation target is set for the consumer price growth rate over the corresponding month of the previous year (Central Bank).

14.0

12.0

10.0

8.0

6.0

4.0

2.0

0.02006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017F* 2018F* 2019F*2020F*

9.0

13.3

8.8

8.8

6.16.6

6.5

12.9

12.2

5.44.0 4.04.03.8

4.0

5.85.6

Rosstat (Fact) Central Bank (*forecast) Ministry of Economic Development (*forecast)

11.911.4

Russia through a lens | Russia in figures

06

Trade structurePeriod January – April 2017

• Foreign trade turnover: USD 172.8 billion (+28.0 percent YoY)

• Trade balance: surplus of USD 46.9 billion (+USD 13.6 billion YoY)

• Exports: USD 109.9 billion (+30.5 percent YoY)

• Imports: USD 62.9 billion (+23.7 percent YoY)

Imports from non-CIS countries (period Jan - Apr 2017):

Source: Federal Customs Service

Percentage in imports from non–CIS countries

In monetary terms YoY

In physical terms YoY

Categories (in physical terms) YoY

Textiles and footwear 6.2% 19.5% 11.6%

Metal products 5.6% 25.5% 41.6% • Ferrous metals (47.2%) • Flat iron non-alloy steel (12.2%) • Pipes (–3.1%)

Chemical products 19.5% 20.3% 5.0%

• Organic materials (16.3%) • Perfume beauty products (6.2%) • Soap (5.5%) • Pharmaceuticals (2.4%) • Fertilizers (-17.8%)

Machinery and auto 48.6% 28.7% N/A

• Mechanical equipment (31.2%) • Electrical equipment (17.7%) • Optical instruments and apparatus (18%) • Passenger cars (-20.4%) • Trucks (32.5%)

Food and raw materials for food production

13.1% 10.3% 1.9%

• Milk (230%) • Citrus (7%) • Fish (14.7%) • Cheese and curd (-7.2%)

Source: Federal Customs Service

Imports from CIS countries (period Jan - Apr 2017):

Percentage in imports from CIS countries

In monetary terms YoY

In physical terms YoY

Categories (in physical terms) YoY

Energy products 4.8% 34.5% 3.8%

Metal products 16.3% 85.8% 52.3% • Pipes (37.3%) • Flat rolled products of iron

or non-alloy steel (59.4%)

Chemical products 13.5% 19.2% 11.7%

• Inorganic chemistry (7.2%) • Plastics (13.2%) • Pharmacy (–4.0%) • Perfumery and cosmetic (20.8%)

Machinery and auto 22.2% 16.2% N/A • Optical instruments and apparatus (–24%) • Ground transportation (67%) (monetary) • Trucks (43.7%)

Food and raw materials for food production

22.1% N/A -5.6%

• Milk (–16.8%) • Cheese and curd (–2.3%) • Butter (–6.9%) • Poultry meat (32.6%)

Textiles and footwear 7.5% 23.9% 34.5%

Source: AgroInvestor

Share of energy products in total exports to non-CIS/CIS countries (January 2006 – April 2017)

Source: Federal Customs ServicePercentage in Exports to non-CIS countries Percentage in Exports to CIS countries

80

70

60

50

40

30

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 Apr

32.6 36.939.5

54.2

42.343.6

55.3

40.947.0

53.0

35.5

62.0

67.566.473.0

69.673.472.772.4 74.5

70.868.070.3

44.0

Increase in non-CIS import of milk powder was boosted primarily due to supplies from Turkey, Iran and New Zealand. Cheaper prices, as compared to Belorussian prices on milk powder, became the main reason of growth, market experts think. However, the quality of milk powder from these countries is lower.

Russia through a lens | Russia in figures

07

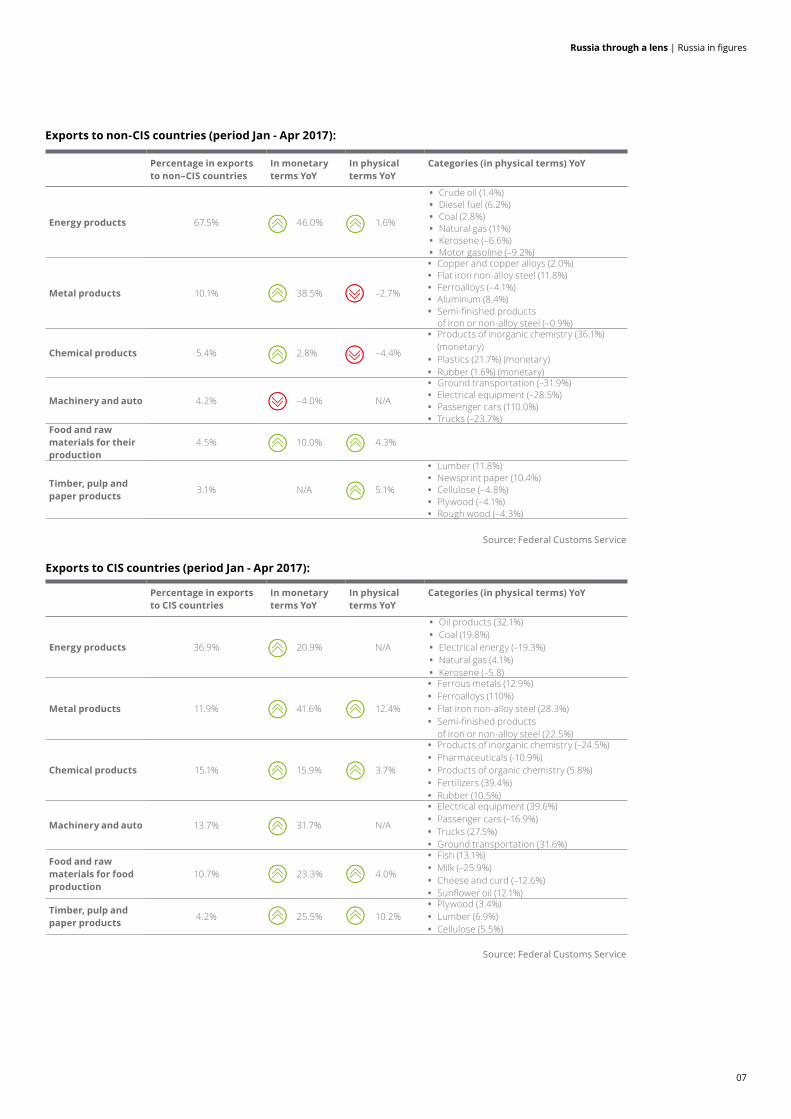

Exports to non-CIS countries (period Jan - Apr 2017):

Percentage in exports to non–CIS countries

In monetary terms YoY

In physical terms YoY

Categories (in physical terms) YoY

Energy products 67.5% 46.0% 1.6%

• Crude oil (1.4%) • Diesel fuel (6.2%) • Coal (2.8%) • Natural gas (11%) • Kerosene (–6.6%) • Motor gasoline (–9.2%)

Metal products 10.1% 38.5% –2.7%

• Copper and copper alloys (2.0%) • Flat iron non-alloy steel (11.8%) • Ferroalloys (–4.1%) • Aluminum (8.4%) • Semi-finished products

of iron or non-alloy steel (–0.9%)

Chemical products 5.4% 2.8% –4.4%

• Products of inorganic chemistry (36.1%) (monetary)

• Plastics (21.7%) (monetary) • Rubber (1.6%) (monetary)

Machinery and auto 4.2% –4.0% N/A

• Ground transportation (–31.9%) • Electrical equipment (–28.5%) • Passenger cars (110.0%) • Trucks (–23.7%)

Food and raw materials for their production

4.5% 10.0% 4.3%

Timber, pulp and paper products 3.1% N/A 5.1%

• Lumber (11.8%) • Newsprint paper (10.4%) • Cellulose (–4.8%) • Plywood (–4.1%) • Rough wood (–4.3%)

Source: Federal Customs Service

Exports to CIS countries (period Jan - Apr 2017):

Percentage in exports to CIS countries

In monetary terms YoY

In physical terms YoY

Categories (in physical terms) YoY

Energy products 36.9% 20.9% N/A

• Oil products (32.1%) • Coal (19.8%) • Electrical energy (–19.3%) • Natural gas (4.1%) • Kerosene (–5.8)

Metal products 11.9% 41.6% 12.4%

• Ferrous metals (12.9%) • Ferroalloys (110%) • Flat iron non-alloy steel (28.3%) • Semi-finished products

of iron or non-alloy steel (22.5%)

Chemical products 15.1% 15.9% 3.7%

• Products of inorganic chemistry (–24.5%) • Pharmaceuticals (-10.9%) • Products of organic chemistry (5.8%) • Fertilizers (39.4%) • Rubber (10.5%)

Machinery and auto 13.7% 31.7% N/A

• Electrical equipment (39.6%) • Passenger cars (–16.9%) • Trucks (27.5%) • Ground transportation (31.6%)

Food and raw materials for food production

10.7% 23.3% 4.0%

• Fish (13.1%) • Milk (–25.9%) • Cheese and curd (–12.6%) • Sunflower oil (12.1%)

Timber, pulp and paper products 4.2% 25.5% 10.2%

• Plywood (3.4%) • Lumber (6.9%) • Cellulose (5.5%)

Source: Federal Customs Service

Russia through a lens | Russia in figures

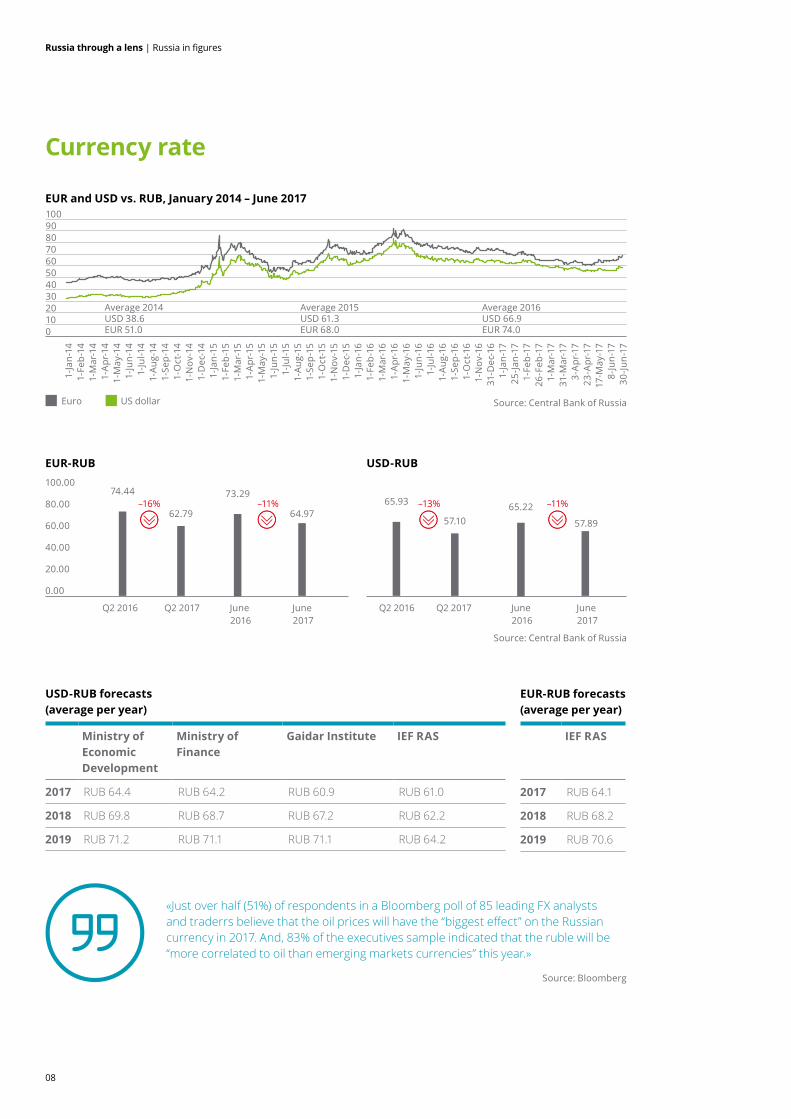

08

EUR-RUB USD-RUB

EUR and USD vs. RUB, January 2014 – June 2017

Currency rate

USD-RUB forecasts (average per year)

EUR-RUB forecasts (average per year)

Ministry of Economic Development

Ministry of Finance

Gaidar Institute IEF RAS

2017 RUB 64.4 RUB 64.2 RUB 60.9 RUB 61.0

2018 RUB 69.8 RUB 68.7 RUB 67.2 RUB 62.2

2019 RUB 71.2 RUB 71.1 RUB 71.1 RUB 64.2

IEF RAS

2017 RUB 64.1

2018 RUB 68.2

2019 RUB 70.6

Source: Central Bank of Russia

100.00

80.00

60.00

40.00

20.00

0.00

74.44

Q2 2016 Q2 2016

65.93

June 2016

June 2016

73.2965.22

Q2 2017 Q2 2017

62.7957.10

–13%–16% –11% –11%

June 2017

June 2017

64.9757.89

Source: Bloomberg

Source: Central Bank of Russia

1009080706050403020100

1-Ja

n-14

1-Fe

b-14

1-M

ar-1

41-

Apr

-14

1-M

ay-1

41-

Jun-

141-

Jul-1

41-

Aug-

141-

Sep-

141-

Oct

-14

1-N

ov-1

41-

Dec

-14

1-Ja

n-15

1-Fe

b-15

1-M

ar-1

51-

Apr

-15

1-M

ay-1

51-

Jun-

151-

Jul-1

51-

Aug-

151-

Sep-

151-

Oct

-15

1-N

ov-1

51-

Dec

-15

1-Ja

n-16

1-Fe

b-16

1-M

ar-1

61-

Apr

-16

1-M

ay-1

61-

Jun-

161-

Jul-1

61-

Aug-

161-

Sep-

161-

Oct

-16

1-N

ov-1

631

-Dec

-16

1-Ja

n-17

25-Ja

n-17

1-Fe

b-17

26-F

eb-1

71-

Mar

-17

31-M

ar-1

73-

Apr

-17

23-A

pr-1

717

-May

-17

8-Ju

n-17

30-Ju

n-17

Euro US dollar

Average 2014USD 38.6EUR 51.0

Average 2015USD 61.3EUR 68.0

Average 2016USD 66.9EUR 74.0

«Just over half (51%) of respondents in a Bloomberg poll of 85 leading FX analysts and traderrs believe that the oil prices will have the “biggest effect” on the Russian currency in 2017. And, 83% of the executives sample indicated that the ruble will be “more correlated to oil than emerging markets currencies” this year.»

Russia through a lens | Russia in figures

09

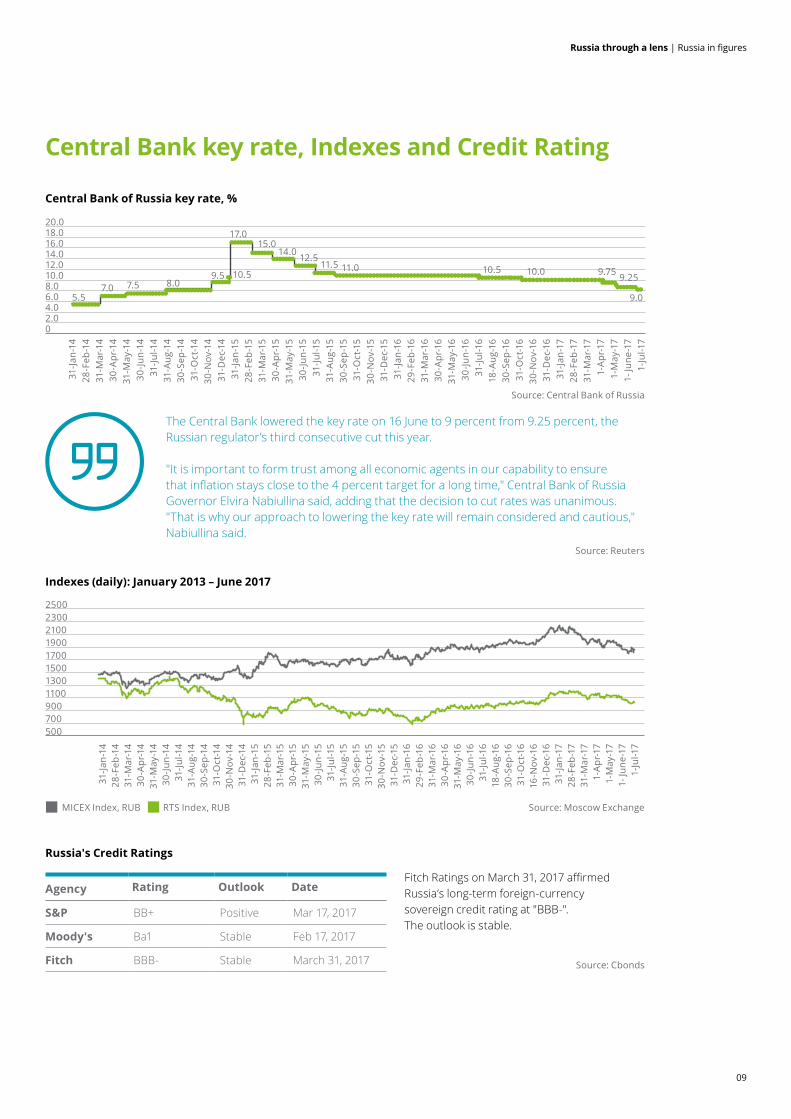

Central Bank of Russia key rate, %

Indexes (daily): January 2013 – June 2017

Russia's Credit Ratings

Central Bank key rate, Indexes and Credit Rating

Agency Rating Outlook Date

S&P BB+ Positive Mar 17, 2017

Moody's Ba1 Stable Feb 17, 2017

Fitch BBB- Stable March 31, 2017

Source: Reuters

Source: Central Bank of Russia

31-Ja

n-14

28-F

eb-1

431

-Mar

-14

30-A

pr-1

431

-May

-14

30-Ju

n-14

31-Ju

l-14

31-A

ug-1

430

-Sep

-14

31-O

ct-1

430

-Nov

-14

31-D

ec-1

431

-Jan-

1528

-Feb

-15

31-M

ar-1

530

-Apr

-15

31-M

ay-1

530

-Jun-

1531

-Jul-1

531

-Aug

-15

30-S

ep-1

531

-Oct

-15

30-N

ov-1

531

-Dec

-15

31-Ja

n-16

29-F

eb-1

631

-Mar

-16

30-A

pr-1

631

-May

-16

30-Ju

n-16

31-Ju

l-16

18-A

ug-1

630

-Sep

-16

31-O

ct-1

630

-Nov

-16

31-D

ec-1

631

-Jan-

1728

-Feb

-17

31-M

ar-1

71-

Apr

-17

1-M

ay-1

71-

June

-17

1-Ju

l-17

20.018.016.014.012.010.08.06.04.02.00

Source: Moscow Exchange

Source: Cbonds

MICEX Index, RUB RTS Index, RUB

9.5 10.5

5.57.0 7.5 8.0

17.015.0

12.511.5 11.0 10.5 10.0 9.25

9.0

9.75

14.0

31-Ja

n-14

28-F

eb-1

431

-Mar

-14

30-A

pr-1

431

-May

-14

30-Ju

n-14

31-Ju

l-14

31-A

ug-1

430

-Sep

-14

31-O

ct-1

430

-Nov

-14

31-D

ec-1

431

-Jan-

1528

-Feb

-15

31-M

ar-1

530

-Apr

-15

31-M

ay-1

530

-Jun-

1531

-Jul-1

531

-Aug

-15

30-S

ep-1

531

-Oct

-15

30-N

ov-1

531

-Dec

-15

31-Ja

n-16

29-F

eb-1

631

-Mar

-16

30-A

pr-1

631

-May

-16

30-Ju

n-16

31-Ju

l-16

18-A

ug-1

630

-Sep

-16

31-O

ct-1

616

-Nov

-16

31-D

ec-1

6 31

-Jan-

1728

-Feb

-17

31-M

ar-1

71-

Apr

-17

1-M

ay-1

71-

June

-17

1-Ju

l-17

25002300210019001700150013001100900700500

The Central Bank lowered the key rate on 16 June to 9 percent from 9.25 percent, the Russian regulator’s third consecutive cut this year.

"It is important to form trust among all economic agents in our capability to ensure that inflation stays close to the 4 percent target for a long time," Central Bank of Russia Governor Elvira Nabiullina said, adding that the decision to cut rates was unanimous."That is why our approach to lowering the key rate will remain considered and cautious," Nabiullina said.

Fitch Ratings on March 31, 2017 affirmed Russia’s long-term foreign-currency sovereign credit rating at "BBB-". The outlook is stable.

Russia through a lens | Russia in figures

10

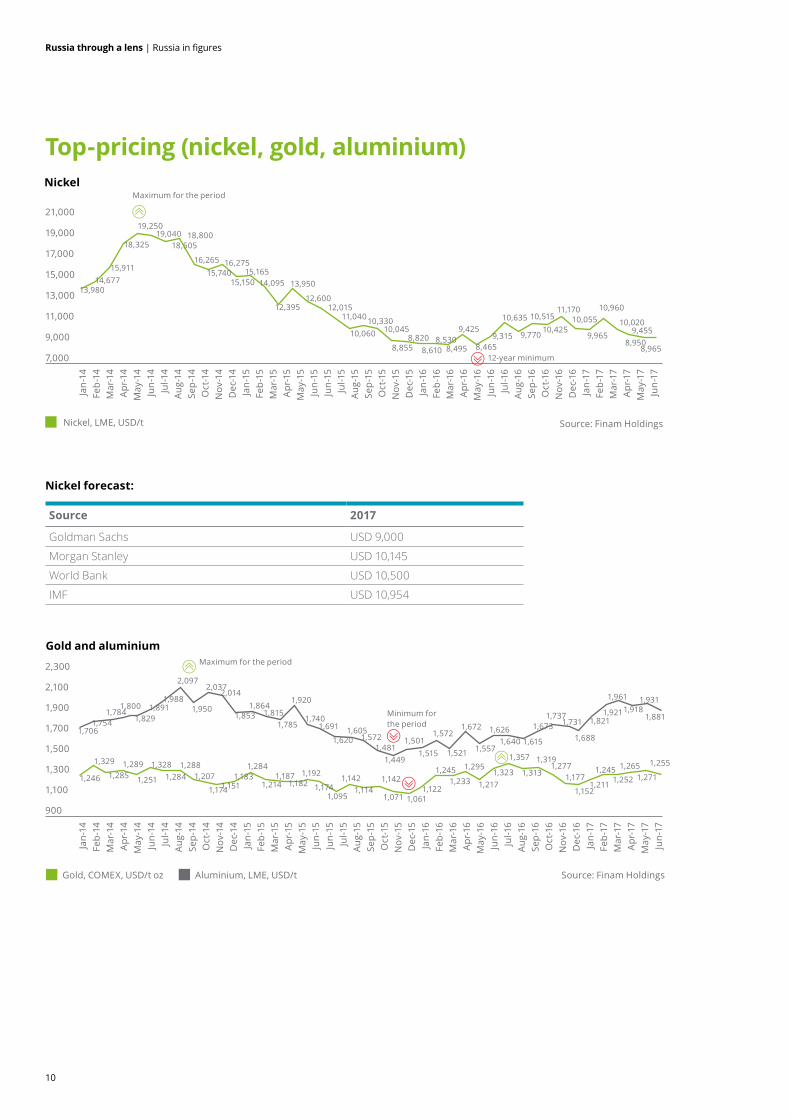

Top-pricing (nickel, gold, aluminium)

Nickel forecast:

Source 2017

Goldman Sachs USD 9,000

Morgan Stanley USD 10,145

World Bank USD 10,500

IMF USD 10,954

Source: Finam Holdings

2,300

2,100

1,900

1,700

1,500

1,300

1,100

900

Gold and aluminium

Gold, COMEX, USD/t oz Aluminium, LME, USD/t

1,706

1,246

1,329

1,2851,289

1,251

1,3281,284

1,2881,207

1,1741,151

1,7541,784

1,8001,829

1,8911,988

2,097

1,950

2,0372,014

1,8531,864

1,8151,785

1,920

1,7401,691

1,6201,605

1,5721,481

1,449

1,5011,572

1,521

1,672

1,557

1,6261,640 1,615

1,6731,737

1,277

1,731

1,177

1,688

1,9611,918

1,931

1,8811,9211,821

1,1521,211

1,2451,252

1,2651,271

1,2551,515

1,1831,284

1,2141,187

1,1821,192

1,1741,095

1,1421,114

1,142

1,071 1,0611,122

1,2451,233

1,295

1,2171,323

1,357

1,313

1,319

Maximum for the period

Minimum for the period

Nickel

21,000

19,000

17,000

15,000

13,000

11,000

9,000

7,000

Maximum for the period

12-year minimum

13,98014,677

15,911

18,325

19,25019,040

18,50518,800

16,26515,740

16,275

15,15015,165

14,095

12,395

13,950

12,60012,015

11,040

10,06010,330

10,045

8,8558,820

8,6108,530

8,495

9,425

8,4659,315

10,635

9,770

10,515

Nickel, LME, USD/t Source: Finam Holdings

Jan-

14Fe

b-14

Mar

-14

Apr

-14

May

-14

Jun-

14Ju

l-14

Aug-

14Se

p-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15Fe

b-15

Mar

-15

Apr

-15

May

-15

Jun-

15Ju

n-15

Jul-1

5Au

g-15

Sep-

15O

ct-1

5N

ov-1

5D

ec-1

5Ja

n-16

Feb-

16M

ar-1

6A

pr-1

6M

ay-1

6Ju

n-16

Jul-1

6Au

g-16

Sep-

16O

ct-1

6N

ov-1

6D

ec-1

6Ja

n-17

Feb-

17M

ar-1

7A

pr-1

7M

ay-1

7Ju

n-17

Jan-

14Fe

b-14

Mar

-14

Apr

-14

May

-14

Jun-

14Ju

l-14

Aug-

14Se

p-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15Fe

b-15

Mar

-15

Apr

-15

May

-15

Jun-

15Ju

n-15

Jul-1

5Au

g-15

Sep-

15O

ct-1

5N

ov-1

5D

ec-1

5Ja

n-16

Feb-

16M

ar-1

6A

pr-1

6M

ay-1

6Ju

n-16

Jul-1

6Au

g-16

Sep-

16O

ct-1

6N

ov-1

6D

ec-1

6Ja

n-17

Feb-

17M

ar-1

7A

pr-1

7M

ay-1

7Ju

n-17

10,425

11,17010,055

9,965 9,4558,950

8,965

10,960

10,020

Russia through a lens | Russia in figures

11

Source 2017 2018

Morgan Stanley USD 1,243 USD 1,250

World Bank USD 1,225 USD 1,206

Goldman Sachs Group USD 1,227 USD 1,250

Credit Suisse USD 1,323 USD 1,375

Oxford Economics USD 1,250 USD 1,265

Source 2017 2018

Goldman Sachs Group USD 2,100 USD 1,950

World Bank USD 1,800 USD 1,828

Morgan Stanley USD 1,808 USD 1,852

IMF USD 1,893 USD 1,928

Oxford Economics USD 1,700 USD 1,766

Gold forecasts:

Aluminium forecasts:

Source: Financial Times

Aluminium has emerged as the best performing industrial metal of 2017, as growing confidence that China will take steps to end a supply glut pushes prices to the highest level in almost three years. Since the financial crisis, a glut of supply has cast a shadow on the market as Chinese producers have spent billions investing in new capacity and the latest smelting technology. Now, after tackling excess capacity in coal and steel industries, there are signs Chinese authorities are turning their focus to the lightweight metal.

Russia through a lens | Russia in figures

12

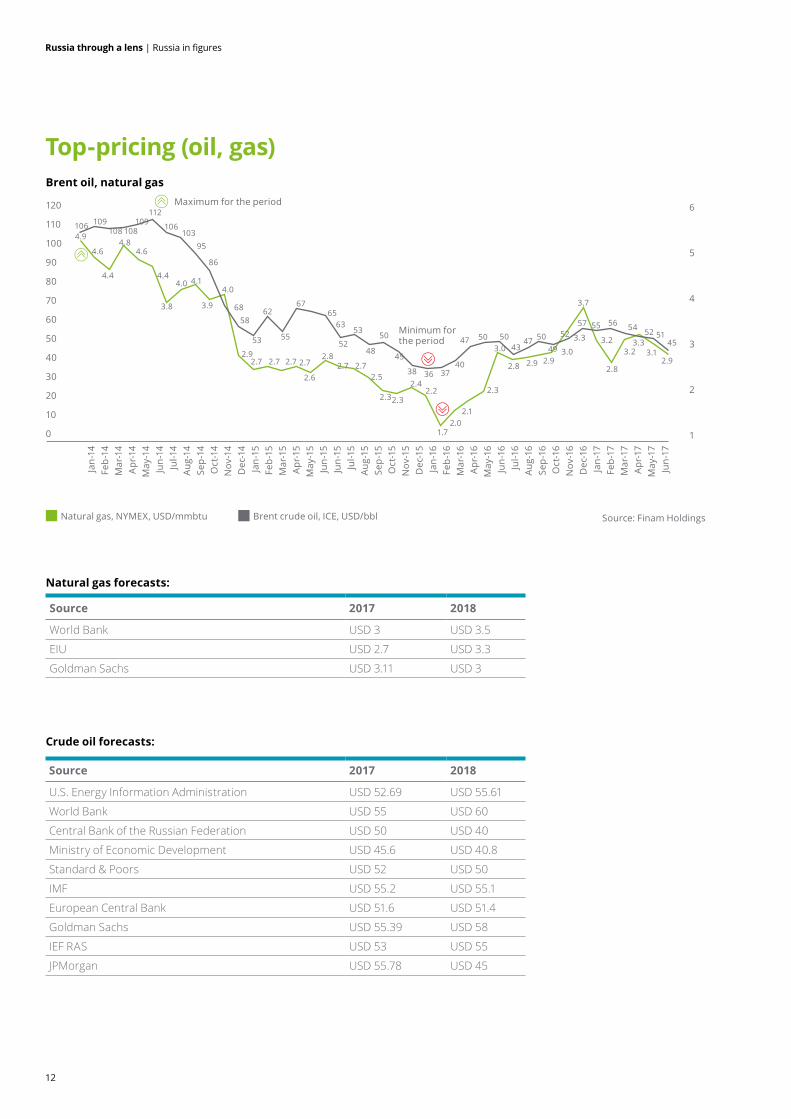

Natural gas forecasts:

Crude oil forecasts:

Source 2017 2018

U.S. Energy Information Administration USD 52.69 USD 55.61

World Bank USD 55 USD 60

Central Bank of the Russian Federation USD 50 USD 40

Ministry of Economic Development USD 45.6 USD 40.8

Standard & Poors USD 52 USD 50

IMF USD 55.2 USD 55.1

European Central Bank USD 51.6 USD 51.4

Goldman Sachs USD 55.39 USD 58

IEF RAS USD 53 USD 55

JPMorgan USD 55.78 USD 45

Top-pricing (oil, gas)

Source 2017 2018

World Bank USD 3 USD 3.5

EIU USD 2.7 USD 3.3

Goldman Sachs USD 3.11 USD 3

120

110

100

90

80

70

60

50

40

30

20

10

0

6

5

4

3

2

1

Brent oil, natural gasMaximum for the period

Minimum for the period

Source: Finam Holdings Natural gas, NYMEX, USD/mmbtu Brent crude oil, ICE, USD/bbl

4.9

4.6

4.4

4.84.6

4.4

3.8

4.0 4.1

3.9

4.0

2.7 2.7 2.7 2.72.5

2.32.3

2.4

1.7

2.7

2.6

2.72.82.9

106

2.02.1

2.3

3.0

2.8

3.0

3.3

2.92.9

3.2

2.2

109108 108

109112

68

53

62

55

6765

63

5248

50

45

38 36 3740

47 50 50 5043 49

4752

57 55 56 54 52 5145

53

106103

95

86

58

2.8

3.23.3

3.12.9

3.7

Jan-

14Fe

b-14

Mar

-14

Apr

-14

May

-14

Jun-

14Ju

l-14

Aug-

14Se

p-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15Fe

b-15

Mar

-15

Apr

-15

May

-15

Jun-

15Ju

n-15

Jul-1

5Au

g-15

Sep-

15O

ct-1

5N

ov-1

5D

ec-1

5Ja

n-16

Feb-

16M

ar-1

6A

pr-1

6M

ay-1

6Ju

n-16

Jul-1

6Au

g-16

Sep-

16O

ct-1

6N

ov-1

6D

ec-1

6Ja

n-17

Feb-

17M

ar-1

7A

pr-1

7M

ay-1

7Ju

n-17

Russia through a lens | Russia in figures

1313

Russia through a lens | Russia in figures

Russia through a lens | Research Centre market analysis

14

Deloitte CFO Survey of the Leading Companies in Russia

Key findings

Research Centre market analysis

Financial climate in 2017 Uncertainties, risks, and development strategies in 2017

The moderate optimism observed half a year ago has continued and strengthened:

• 51 percent of companies are optimistic about the situation

• Consumer companies (67 percent) and companies with a staff of less than 100 (62 percent) are most pessimistic.

Confidence in future operating revenue growth has increased 24 pp compared to the spring of 2015:

• 66 percent of respondents expect the operating revenue to increase in 2017, while 14 percent expect the revenue to shrink in their companies

• 73 percent expect an increase in their real income

The situation with the HR policy can be described as stable and optimistic. Companies try to maintain both their headcount and payroll levels:

• Almost every third company (30 percent) plans to increase their number of staff

• Most companies (70 percent) plan to increase the average payroll

Almost half of our experts (49 percent) expect prices to remain at the current levels, while 41 percent of the companies plan to hike prices by 12 percent on average.

Despite the positive trends resulting from lower uncertainty, the share of respondents pointing to high uncertainty in strategic decision making remains rather high (36 percent).

The risk appetite remained unchanged, totaling a negative –6 percent.

Companies adjust their risk management strategies to the current market situation: more than half of the respondents (57 percent) voted for retaining the foreign currency clause in contracts.

Risk factors that had the most negative impact on Russian business in 2017:

• Increased competition on the market

• Competition from innovative products

Priority business strategy to recover the market position in Russia in 2017:

• Making acquisitions abroad

Almost half of the companies (51 percent) plan to expand the geography of their business ties:

• Priority markets include Asia and Latin America

Russia through a lens | Research Centre market analysis

15

Drivers and barriers for business in Russia in 2017

Innovations in Russia in 2017

The long-term impact of the global crisis gradually fades away: in 1H17 currency risks were not identified within the top-5 barriers.

Drivers of business development in Russia:

• Cost optimization

• Expansion into new markets

• Focus on core operations

• Innovative products

• Digitalization

Barriers for business development in Russia:

• Increase in the cost of capital

• Financial condition

• Production in Russia

• Production abroad

• Innovations

One out of every three companies (34 percent) that implemented structural and organizational changes grew in value.

TMT and manufacturing companies won the highest ratings among other industries for implementing disruptive technologies.

More than half of the surveyed companies (58 percent) said they spent up to one percent of their annual revenue on R&D.

According to 58 percent of the poll participants, most innovations come from dedicated divisions within companies.

The experts rated the level of function automation in leading Russian companies slightly below the average (0.43 out of 1).

The administrative function was rated as the most advanced (after the financial function) in terms of the quality of analytics.

The key obstacle for implementing innovations in companies is the shortage of talent.

The key drivers for implementing innovations are the market and competition.

Russia through a lens | Research Centre market analysis

16

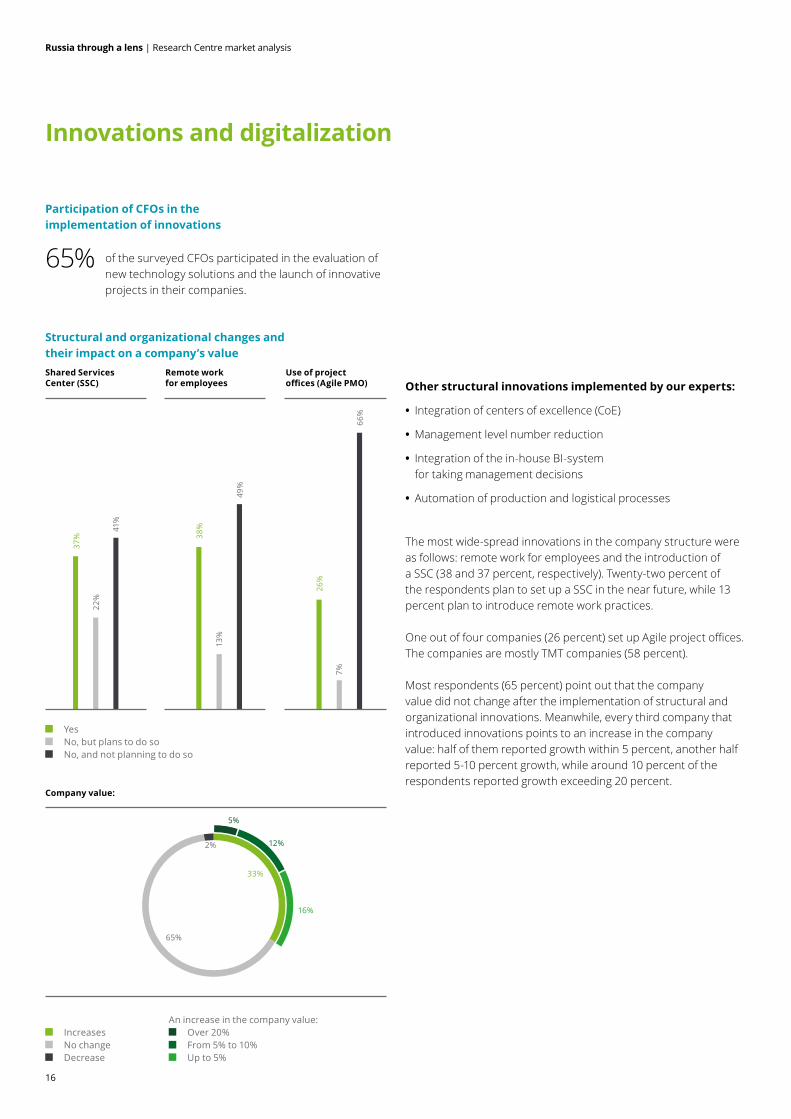

Innovations and digitalization

Participation of CFOs in the implementation of innovations

Structural and organizational changes and their impact on a company’s value

of the surveyed CFOs participated in the evaluation of new technology solutions and the launch of innovative projects in their companies.

Other structural innovations implemented by our experts:

• Integration of centers of excellence (CoE)

• Management level number reduction

• Integration of the in-house BI-system for taking management decisions

• Automation of production and logistical processes

The most wide-spread innovations in the company structure were as follows: remote work for employees and the introduction of a SSC (38 and 37 percent, respectively). Twenty-two percent of the respondents plan to set up a SSC in the near future, while 13 percent plan to introduce remote work practices.

One out of four companies (26 percent) set up Agile project offices. The companies are mostly TMT companies (58 percent).

Most respondents (65 percent) point out that the company value did not change after the implementation of structural and organizational innovations. Meanwhile, every third company that introduced innovations points to an increase in the company value: half of them reported growth within 5 percent, another half reported 5-10 percent growth, while around 10 percent of the respondents reported growth exceeding 20 percent.

Remote work for employees

Use of project offices (Agile PMO)

Shared Services Center (SSC)

Company value:

37%

22%

41%

38%

26%

13%

7%

49%

66%

Yes No, but plans to do so No, and not planning to do so

Increases No change Decrease

An increase in the company value: Over 20% From 5% to 10% Up to 5%

33%

5%

12%

16%

65%

2%

65%

Russia through a lens | Research Centre market analysis

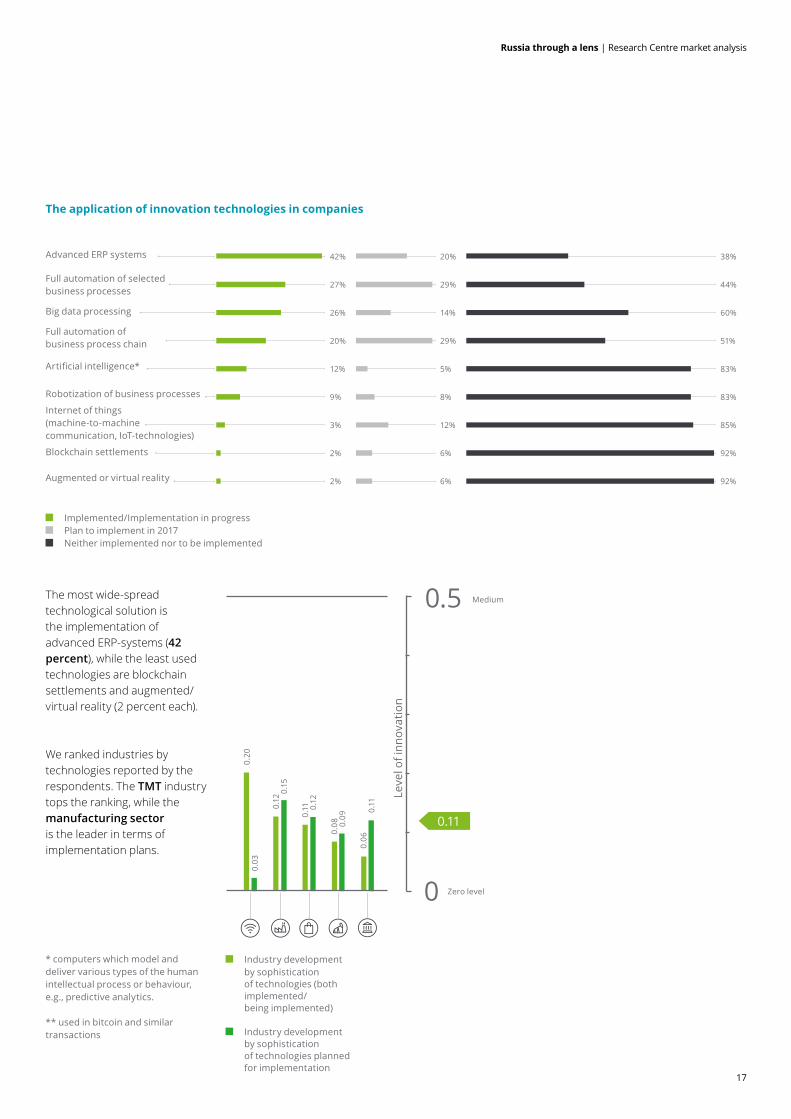

17

Advanced ERP systems

Full automation of selected business processes

Big data processing

Full automation of business process chain

Artificial intelligence*

Robotization of business processes

Internet of things (machine-to-machine communication, IoT-technologies)

Blockchain settlements

Augmented or virtual reality

The application of innovation technologies in companies

The most wide-spread technological solution is the implementation of advanced ERP-systems (42 percent), while the least used technologies are blockchain settlements and augmented/virtual reality (2 percent each).

We ranked industries by technologies reported by the respondents. The TMT industry tops the ranking, while the manufacturing sector is the leader in terms of implementation plans.

* computers which model and deliver various types of the human intellectual process or behaviour, e.g., predictive analytics. ** used in bitcoin and similar transactions

42% 20% 38%

27% 29% 44%

26% 14% 60%

20% 29% 51%

12% 5% 83%

9% 8% 83%

3% 12% 85%

2% 6% 92%

2% 6% 92%

Implemented/Implementation in progress Plan to implement in 2017 Neither implemented nor to be implemented

Industry development by sophistication of technologies (both implemented/ being implemented)

Industry development by sophistication of technologies planned for implementation

Lev

el o

f inn

ovat

ion

Zero level

Medium

0.15

0.12

0.11 0.

12

0.08 0.

09

0.11

0.06

0.20

0.03

0.5

0

0.11

Russia through a lens | Research Centre market analysis

18

58%

87%

61%

57%

33%

17%

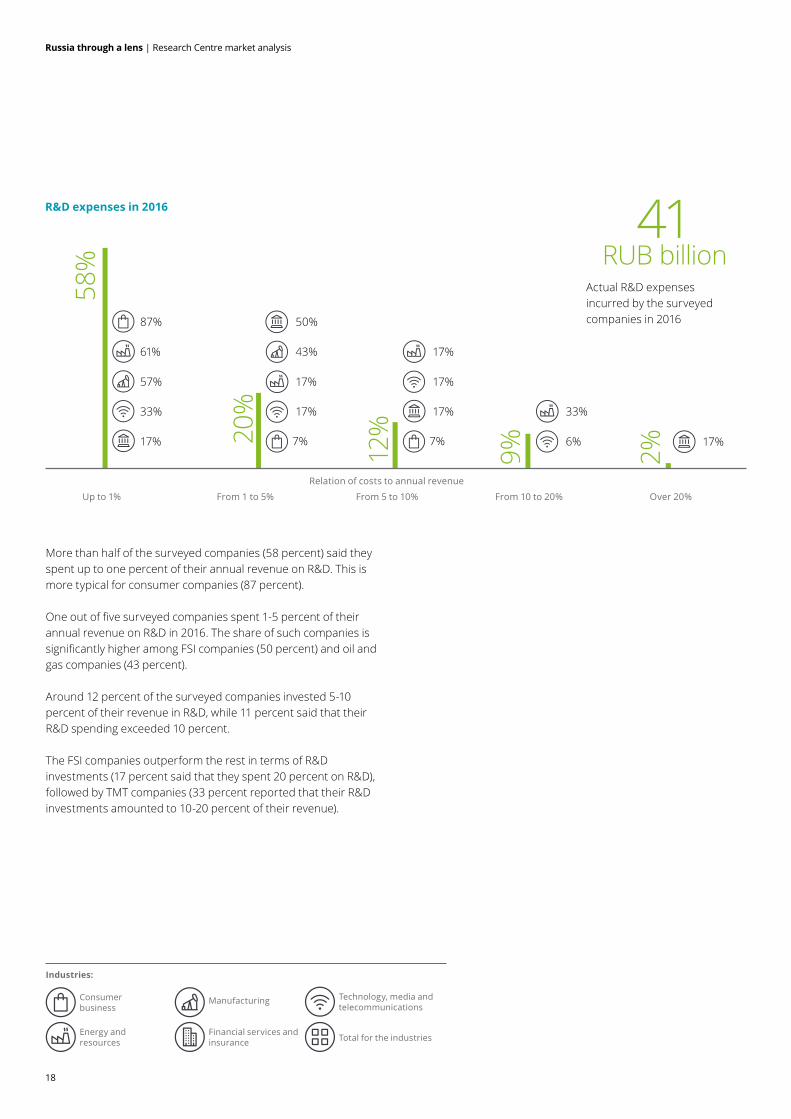

R&D expenses in 2016

More than half of the surveyed companies (58 percent) said they spent up to one percent of their annual revenue on R&D. This is more typical for consumer companies (87 percent).

One out of five surveyed companies spent 1-5 percent of their annual revenue on R&D in 2016. The share of such companies is significantly higher among FSI companies (50 percent) and oil and gas companies (43 percent).

Around 12 percent of the surveyed companies invested 5-10 percent of their revenue in R&D, while 11 percent said that their R&D spending exceeded 10 percent.

The FSI companies outperform the rest in terms of R&D investments (17 percent said that they spent 20 percent on R&D), followed by TMT companies (33 percent reported that their R&D investments amounted to 10-20 percent of their revenue).

Up to 1% From 1 to 5% From 5 to 10% From 10 to 20% Over 20%

Actual R&D expenses incurred by the surveyed companies in 2016

41RUB billion

9%

33%

6%

2%

17%20%

50%

43%

17%

17%

7%

12%

17%

17%

17%

7%

Relation of costs to annual revenue

Consumer business

Manufacturing

Energy and resources

Financial services and insurance

Technology, media and telecommunications

Industries:

Total for the industries

Russia through a lens | Research Centre market analysis

19

55%

80% 50% 17%

8%

25%

57% 29% 17%

17%56% 28% 14%

33% 17% 11%

6%17% 13% 7%

Planned R&D expenses in 2017

In 2017, 55 percent of major Russian companies plan to spend up to one percent of their revenue on R&D. The share of such companies is higher among consumer companies (80 percent).

Twenty-three percent of respondents plan to spend 1-5 percent of their revenue on R&D. Interestingly, the share of such companies is higher in the FSI industry (50 percent).

The planned expenditures on R&D are to reach 5-10 percent of the revenue, according to one out of ten respondents. They are mostly TMT and FSI companies (17 percent for each industry, respectively).

The remaining 11 percent of respondents plan to invest over 10 percent of their revenue in R&D. FSI companies are more inclined (17 percent) to invest in R&D, over 20 percent of their revenue.

Overall, the survey responses show that the structure of the R&D expenses will remain almost unchanged in 2017.

Up to 1% From 1 to 5% From 5 to 10% From 10 to 20% Over 20%

R&D expenses planned by the surveyed companies in 2017

40RUB billion

5% 6%

23%

12%

Relation of costs to annual revenue

Russia through a lens | Research Centre market analysis

20

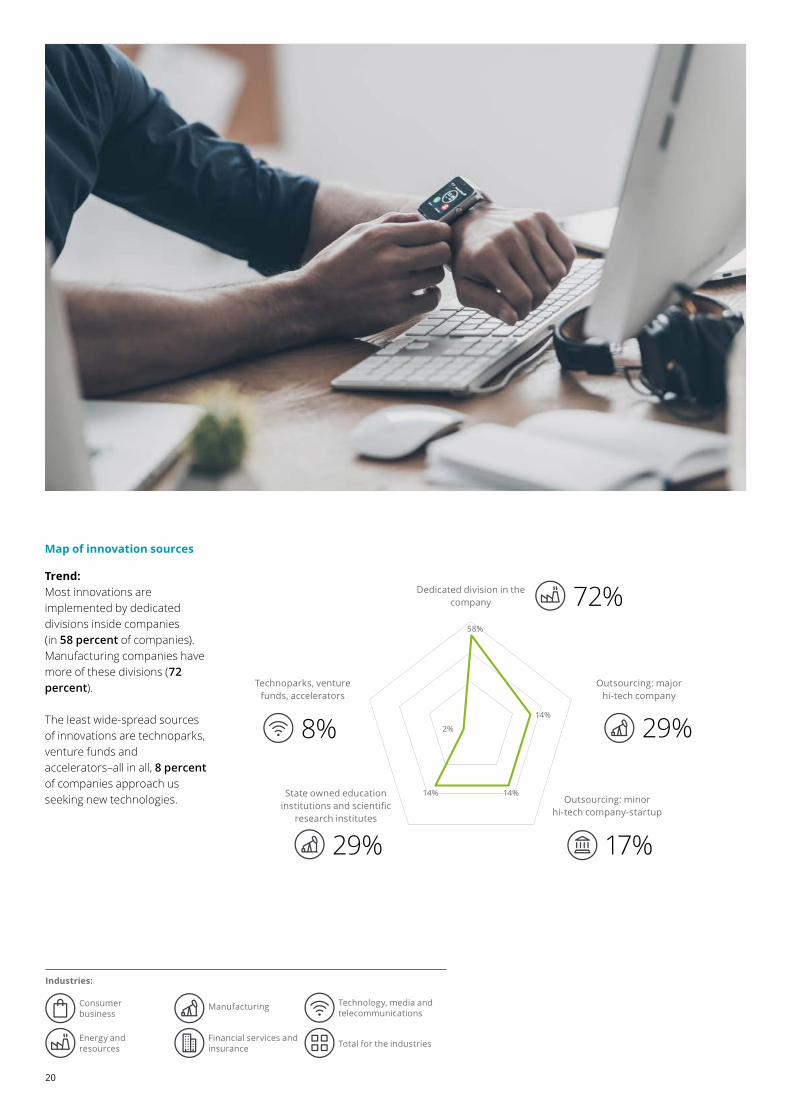

Map of innovation sources

Trend:Most innovations are implemented by dedicated divisions inside companies (in 58 percent of companies). Manufacturing companies have more of these divisions (72 percent).

The least wide-spread sources of innovations are technoparks, venture funds and accelerators–all in all, 8 percent of companies approach us seeking new technologies.

72%

29%

17% 29%

8%

Dedicated division in the company

Outsourcing: major hi-tech company

Technoparks, venture funds, accelerators

Outsourcing: minor hi-tech company-startup

State owned education institutions and scientific

research institutes

58%

2%

14% 14%

14%

Consumer business

Manufacturing

Energy and resources

Financial services and insurance

Technology, media and telecommunications

Industries:

Total for the industries

Russia through a lens | Research Centre market analysis

21

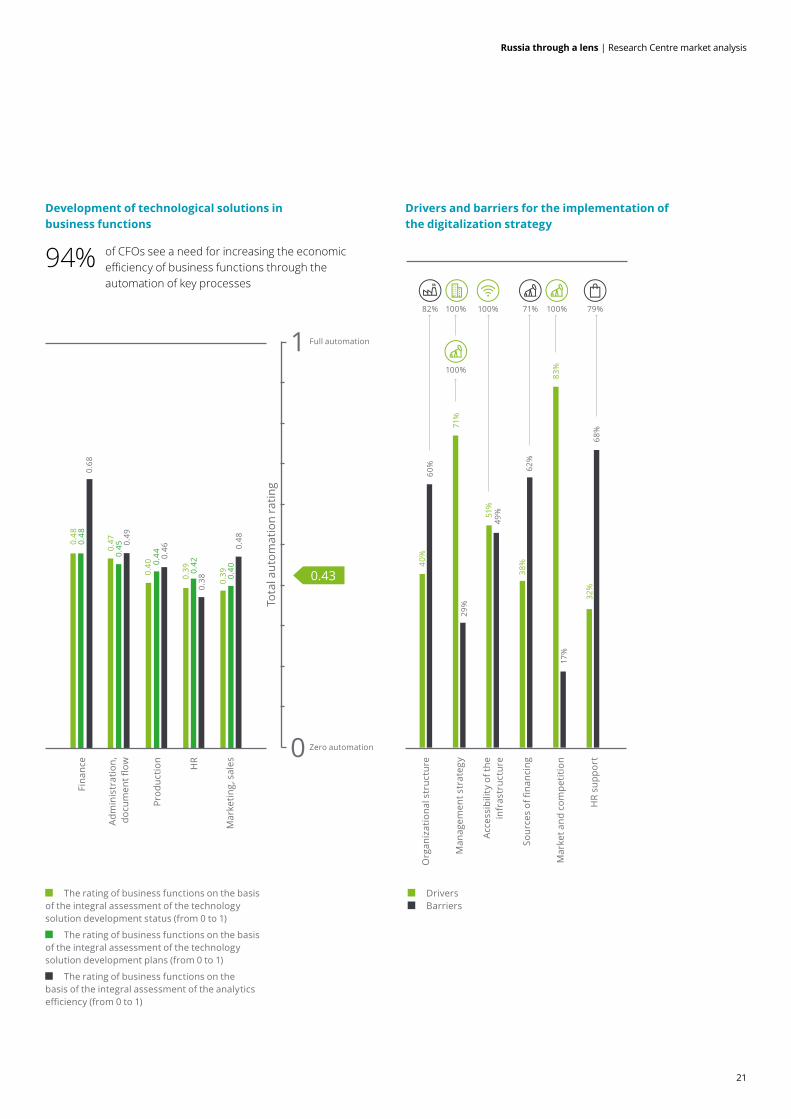

Development of technological solutions in business functions

of CFOs see a need for increasing the economic efficiency of business functions through the automation of key processes

94%

Zero automation

Full automation1

0

Adm

inis

trat

ion,

do

cum

ent fl

ow

Prod

uctio

n

HR

Mar

ketin

g, s

ales

Fina

nce

0.39 0.

420.

38 0.39 0.

400.

48

0.40 0.

44 0.46

0.48

0.48

0.68

0.47

0.45 0.

49

Tota

l aut

omat

ion

ratin

g

The rating of business functions on the basis of the integral assessment of the technology solution development status (from 0 to 1)

The rating of business functions on the basis of the integral assessment of the technology solution development plans (from 0 to 1)

The rating of business functions on the basis of the integral assessment of the analytics efficiency (from 0 to 1)

Drivers and barriers for the implementation of the digitalization strategy

Man

agem

ent s

trat

egy

Acce

ssib

ility

of t

he

infr

astr

uctu

re

Sour

ces

of fi

nanc

ing

Mar

ket a

nd c

ompe

titio

n

HR

supp

ort

Org

aniz

atio

nal s

truc

ture

Drivers Barriers

82% 71% 100% 79%

100%

100%100%

40%

38%

32%

71%

51%

83%

60% 62

%

68%

29%

49%

17%

0.43

Russia through a lens | Research Centre market analysis

22

Overview of steel and iron market

From a strategic perspective, the steel and iron industry depends on global industralisation, which primarily involves the demand for metals from countries that are ready to make an investment leap (e.g. India, Vietnam and Indonesia). From a tactical perspective, the industry is dependent on actions China and global companies might take and how some countries would respond in terms of protectionism.

While being potential regions of growth, India, Iran and Vietnam have limited opportunities to raise capital. The search for a solution is on, with a way out likely to be found in 2018-2019. However, these countries will not have a significant impact on the global metals market. Growing demand will drive the rise of local industry. Countries in the Middle East and Africa represent potential growth areas that will be attracting global resources to meet the demand. Investment mechanisms may start emerging in these countries after 2020.

Re-industrialisation of the industrialised nations is expected to involve a fundamentally different technology platform. This effort would require materials that are substantially different from the existing offerings on the global market. The development of a resource platform for cutting-edge manufacturing applications is currently driven by projects aimed at manufacturing metal products with the use of rare earth elements and producing metal powders to support additive technologies and increase the output of products with higher technological availability (e.g. products and fabricated metals with complex structures).

Demand limitations in 2017 highlight the importance of corporate policy as a tool for gaining a competitive edge. Companies price their products to solve the tasks at hand, which leads to volatility in prices.

In a situation with prices fluctuating rapidly over a limited period, forecasts are driven by institutional factors. Such volatile prices benefit vertically integrated companies. Fluctuating prices create a barrier to new market entrants and complicate investment decision making. It is particularly important in the context of China’s programme to restructure the steel-making industry, as well as India’s and Iran’s plans to develop their steel-making industries.

Reaching a normal level after a price hike or collapse is indicative of a general trend towards a relative decrease in prices. Steel-makers have limited opportunities to transfer a price impulse to metal product consumers as they experience issues with end-user demand. When choosing between lower prices and lower output companies are increasingly going for lower prices.

However, the existing trends towards lower prices on the global market do not exclude a stronger price differentiation across regions and countries. This is driven by protectionist efforts taken over 2016-2017.

The most likely trend for 2017 would involve a gradual decrease in prices down to a level enabling an efficient production of coking coal in China (above USD 100 per tonne).

Prof. I.A.Budanov,Doctor of Economics (INP RAN)

Igor BudanovProfessor, Doctor of EconomicsInstitute for Economic Forecasting of the Russian Academy of Sciences(INP RAN)

Russia through a lens | Research Centre market analysis

23

In 2016 the downward trend in output and consumption that had been continuing from 2015 gave way to greater stability, with industry indicators changing by less than 2 percent:

• Steel output grew by 0.8 percent up to 1,629 million tonnes

• Steel consumption grew by 1.3 percent up to 1,600 million tonnes.

Over the first three months of 2017 saw global steel output reach 410.5 million tonnes, up 5.7 percent from the same period in 2016.

In 2016 China saw an increase of 1.8 percent in domestic consumption of steel amidst the continuing incentives and growth in loans.

Driven by a decrease in government incentives, an expected gradual weakening in the demand from China will create an oversupply, forcing prices down.

In 2016 steel output in Russia has grown by 0.3 percent to 69.6 million tonnes.

The apparent domestic consumption of steel dropped by 3.9 percent to 34.6 million tonnes. However, 4Q2016 saw a YoY increase of 3.7 percent as a result of the slightly improved situation in the construction industry and the Russian economy as a whole.

Exports and imports totaled 43.3 million tonnes and 11,3 million tonnes, respectively.

*Based on the annual survey by Deloitte CIS.

Top-5* issues for the industry in 2017:

• Prospects of weaker domestic demand

• Stagnation in the Russian economy

• Decrease in core business revenue

• Higher production costs in Russia

• Stricter government regulation in Russia

Top-5* priority business strategies in 2017:

• Ongoing cost control

• Business development through organic growth

• Cost cutting

• Increase in domestic output

• Expansion into new markets

Key findings

Russia through a lens | Research Centre market analysis

24

Russian Pharmaceutical Market Trends in 2017

Key findings

Market snapshot

In 2016 the pharmaceutical market grew by 6.7 percent in ruble terms while remaining unchanged from 2015 in unit terms.

Market growth forecasts for 2017 (in ruble terms): • DSM Group: up by 8-9 percent • RNC Pharma: up by 10 percent • QuintilesIMS: up by 9.2 percent

Market growth forecasts for 2017 (in unit terms): • DSM Group: up by 1-2 percent • QuintilesIMS: up by 4.8 percent; • IPT Group: up by 4-6 percent.

In 2016 pharmaceutical price inflation was 5 percent.

The share of local medicines grew by 1.2 pp in monetary terms.

The Russian market is ranked 14th in the world in terms of size.

In Russia pharmaceutical output increased by 23.8 percent to RUB 286 billion while medical product output grew by 15 percent to RUB 52.8 billion.

Output forecast for 2017 by the Russian Ministry of Industry and Trade: • Medicines: up by 8 percents • Medical products: up by 4 percent

By the end of 2016 medicines produced in Russia accounted for 77 percent of the Essential Drug List.

In 2016 almost 80 percent of imports came from Europe, primarily from France and Germany.

The post-Soviet countries remain the major export markets for Russian medicines, accounting for 86 percent of the total exports.

Pharmaceutical market perception

View of the current state of: • Pharma industry–positive perception (a balance of +52 percent)

• Pharmaceutical businesses–positive perception (a balance of +82 percent)

View of the future prospects of: • Pharma industry–neutral perception (a balance of +7 percent)

• Pharmaceutical businesses–positive perception (a balance of +42 percent)

Change in the share of imports as expected by the Russian market: down by 3 percent in monetary terms and by 4 percent in unit terms.

Demand for regulatory measures aimed at reducing the share of pharmaceutical imports: localization incentives and privileges for foregn companies, as well as subsidies and privileges for Russian companies.

Demand for more efficient regulation • Medicine pricing (87 percent) • Public procurement regulation (74 percent) • Regulation of on-line sales of medicines and telehealth (67 percent)

• State registration of medicines (67 percent) • Mandatory track & trace framework (67 percent)

Russia through a lens | Research Centre market analysis

25

Business development strategy

Medicine labelling is a new regulatory trend that is likely to have an impact on how companies and the industry as a whole will develop.

A focus on new product launches is the top development strategy for pharmaceutical companies in Russia.

New trends in strategic development: focus on R&D activities and deeper localization.

Top challenges: stronger competition and a shift of the focus to gaps in the industry regulation.

Expectations for key indicators: • Most companies (82 percent) expect an average growth of 13 percent in ruble terms in 2017

• Of those surveyed, 39 percent expect that operating costs will see an average growth of 16 percent while another 26 percent anticipate an average decrease of 11 percent

• Most companies (59 percent) are not planning any headcount adjustments while another 33 percent expect that their headcount will increase on average by 7 percent

• Most companies (63 percent) are planning to increase pay levels by 7 percent on average

Russia through a lens

26

Top 5 M&As*

Target company Industry Bidder company Seller company Deal value (USD, mln)

Additional information

PJSC Polyus (10% Stake)

Mining Fosun International Limited

Polyus Gold International Ltd

887 The transaction will allow Fosun Group to expand its portfolio and business operations, and to enhance its expertise. The transaction is set to benefit the company and its shareholders.

NK KondaNeft JSC Energy Rosneft Oil Company OAO

The Independent Petroleum Company

698 The acquisition is in line with Rosneft’s aim to maximise resource development efficiency in its main oil and gas producing region. The transaction will boost synergies and accelerate the development of existing resources and infrastructure.

Uralorgsintez JSC Chemicals Ektos Group SIBUR Holding OJSC

391 The divestment of Uralorgsintez is in line with SIBUR’s strategy to concentrate on its core businesses.

Joint Stock Company EVRAZ Nakhodka Trade Sea Port

Transportation Lanebrook Limited EVRAZ Plc 354 The transaction will allow EVRAZ to further optimise its asset portfolio and focus on its core business. The sale of this non-core asset will improve EVRAZ’s overall financial position as it reduces leverage.

RBC Information Systems OAO (65.43% Stake)

Media ESN Group The ONEXIM Group 281 The completion of the deal marks the end of a seven-year period when RBC, under the ownership of Prokhorov, published hard-hitting investigations, including into the business affairs of Putin's inner circle. (Source: NYTimes)

(Russian companies)

*Open information about deal value

Source: Merger Market

Russia through a lens

27

Global windTop news: China and Russia

Top news: Europe and Russia

31 May 2017A Beijing company to build three plants in the Penza regionShemysheika Industrial Complex to put about 30 thousand hectares of land into a crop rotation in the Penza Region and to construct three factories for production of flour, oil and potato processing.

30 May 2017Chinese investors intend to build light railway in RussiaAt present, two light railway projects are under construction. These projects envisage building a light railway running to Sertolovo through Bugry and Devyatkino and to Vsevolozhsk through Rzhevka and Kudrovo. The Sertolovo project is estimated at nearly 17 billion rubles ($300 million). The Leningrad region authorities are aiming for the projects’ construction to launch as soon as investment contracts are signed.

20 June 2017Germany's Daimler began construction of a new Mercedes-Benz plant near MoscowDaimler said in February that it will invest more than 250 million euros ($279 million) into the factory. These contrasts with widespread skepticism among international investors about the Russian auto market after a prolonged downturn brought on by the sanctions and a collapse in global oil prices.

01 June 2017Turkish-Italian ICA to take part in road construction projects in RussiaThe head of Russia’s Federal Road Transport Agency (Rosavtodor) Roman Starovoit and Chairman of the Board of ICA Firat Cecen signed a cooperation agreement on road construction investment projects. The Turkish-Italian investors were particularly interested

25 May 2017Hilong oilfield services group to open factory in RussiaBy the end of 2017, Hilong Group, a Chinese oilfield services company, will open a factory in Surgut, a city in the Khanty-Mansiysk autonomous region. Investment into the project will total 600 million rubles. In addition, the company also plans to begin the construction of a plant in another city in the region, Nizhnevartovsk, in the near future.

16 May 2017The Chinese are set to build a $120m plant in the Russian Far EastJoybay Agricultural Holding Limited, a Chinese company, is investing $120 million into a new Russian plant for deep processing of soybeans and production of soy protein isolate. The facility will be located in the Jewish autonomous region situated in the Russian Far East.

13 May 2017A Chinese investor to build a marine biotechnopark in the Primorye territoryAccording to the local administration, China’s Wen Lian Aquaculture intends to create a marine biotechnopark on the island of Popov in the Primorye territory.

27 April 2017Russia is ready to significantly increase its exports to ChinaThe Chinese market continues to demonstrate demand for Russian agricultural products and foodstuffs. “The Chinese consumer has got a positive perception of Russian products. There is a well-established idea that our food products are of high quality, they are free of genetically modified organisms (GMOs), and this is regulated at the legislative level. In addition, they are organic and, as a general rule, are much less expensive than their foreign counterparts,” according to Mikhail Mamonov, managing director for international projects at the Russian Export Center (REC).

in the Agency’s regional projects being undertaken as public-private partnerships.

01 June 2017Philips signs deal on localization of CT scanners production in RussiaGovernor of the Moscow region, Andrei Vorobyov, and Director General of Philips Russia, Arman Voskerchyan, signed a localisation agreement for the production of innovative ultrasound systems and CT scanners under the Philips brand in Istra.

31 May 2017Innothera to establish production in RussiaFrance’s Innothera Holding plans to start production of its medicines in Russia. This will help the company to boost its drug production in the fields of gynecology (Polygynax, Pharmatex), hematology (Totema), phlebology (Phlebodia 600) and other areas of medicine.

31 May 2017Mapei S.P.A bought a factory in the Leningrad regionMapei S.p.A, an Italian building materials conglomerate, purchased the plant in Leningrad region’s Volosovo district from Austria’s Baumit Company, and will invest RUB 450 million into its modernisation.

31 May 2017Switzerland’s Sika invests in the Moscow region’s construction industrySika, a Swiss chemical company, launched the manufacture of high-tech floor epoxy coatings in the Moscow regional city of Lobnya. Investment into this production line totalled 50 million rubles (over $880,000). This allowed the company to begin manufacturing of products that previous been imported to Russia.

Russia through a lens

28

Useful stickers

BP Statistical Review of World Energy (June 2017)We project Russia remains the world’s largest energy exporter, with exports meeting over 4% of global energy demand by 2035.

Outcomes of SPIEF 2017The global economy in search of a new balance.

The 10 Top Research Universities

Since May 2017, Deloitte CIS has become the official intellectual partner of the department of Economics at the Novosibirsk State University.

V Expert RA Russian Universities Ranking 2017 Leading economic universities demonstrate a stable positive shift in demand from applicants who, one year after graduation, earn 28% more than graduates from other RAEX top 30 universities.

(In Russian)

1 Lomonosov Moscow State University

2 National Research Nuclear University MEPhI

3 Moscow Institute of Physics and Technology (State University)

4 Tomsk State University

5 Saint Petersburg State University

6 Novosibirsk State University

7 Tomsk Polytechnic University

8 Peter the Great St.Petersburg Polytechnic University

9 Ural Federal University

10 Kazan (Volga region) Federal University

Russia through a lens

29

Useful stickers regarding innovations in Russia

The market in Initial Coin Offerings (ICO) risks becoming a bubble

Russia and China May Digitize Their Currencies With Ethereum

Start-up market encyclopedia (In Russian)

Top-5 largest deals with Russian companies Q2 2017:

Data Company Deal value, USD, mln

Investor

April 2017 Drchrono 12.0 Runa Capital, Maxfield Capital

May 2017 am.ru 10.0 Mail.ru Group

April 2017 VIST Group 7.1 Rosnano

March 2017 InfoWatch 3.2 The Russian Direct Investment Fund

March 2017 OneTwoTrip 3.0 Bank Saint-Petersburg

Russia through a lens

30

ContactsJoe [email protected]

Lora ZemlyanskayaResearch Centre [email protected]

Dmitriy KasatkinSenior Research [email protected]

Mikhail GordeevSenior Research [email protected]

Vladimir SokolovSenior Research [email protected]

Artyom [email protected]

deloitte.ruAbout Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries. Deloitte serves four out of five Fortune Global 500® companies through a globally connected network of member firms in more than 150 countries bringing world-class capabilities, insights, and high-quality service to address clients’ most complex business challenges. To learn more about how Deloitte’s approximately 244,000 professionals make an impact that matters, please connect with us on Facebook, LinkedIn, or Twitter.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2017 ZAO Deloitte & Touche CIS. All rights reserved.