Embed Size (px)

Citation preview

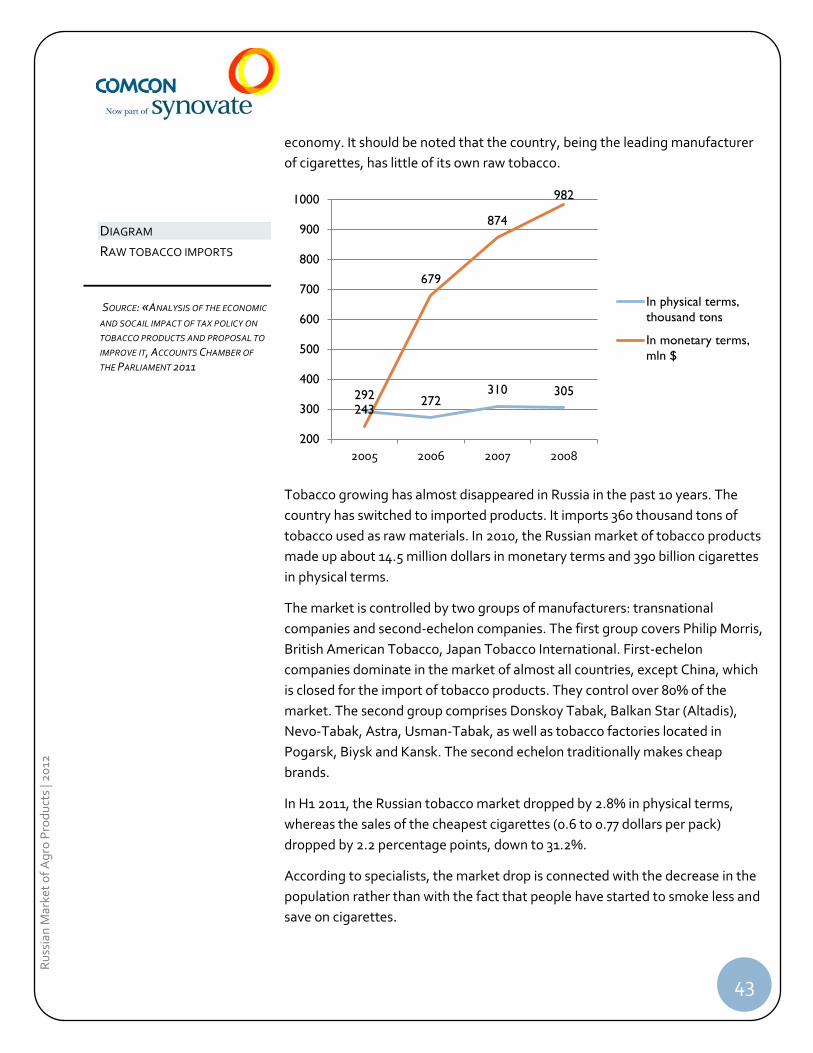

July 2012

Russian Market of Agro Products

Desk Research

1

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

TABLE OF CONTENTS ABSTRACT .......................................................................................................................................... 2

KEY FACTS ABOUT RUSSIA .................................................................................................................... 3

CROP RAISING AND FOOD PROCESSING INDUSTRIES ................................................................................. 5

GRAIN CROPS ...................................................................................................................................... 6

WHEAT ........................................................................................................................................... 7

RYE ................................................................................................................................................ 8

BARLEY .......................................................................................................................................... 8

RICE ............................................................................................................................................. 10

GRAIN CROPS PROCESSING .............................................................................................................. 17

BREWING INDUSTRY ....................................................................................................................... 21

OIL-BEARING CROPS .......................................................................................................................... 23

OIL-BEARER CULTURES PROCESSING ................................................................................................ 25

VEGETABLE CROPS ............................................................................................................................ 27

POTATO CROPS ............................................................................................................................. 30

ETHANOL AND ETHYL ALCOHOL INDUSTRY ........................................................................................ 32

SUGAR INDUSTRY ........................................................................................................................... 34

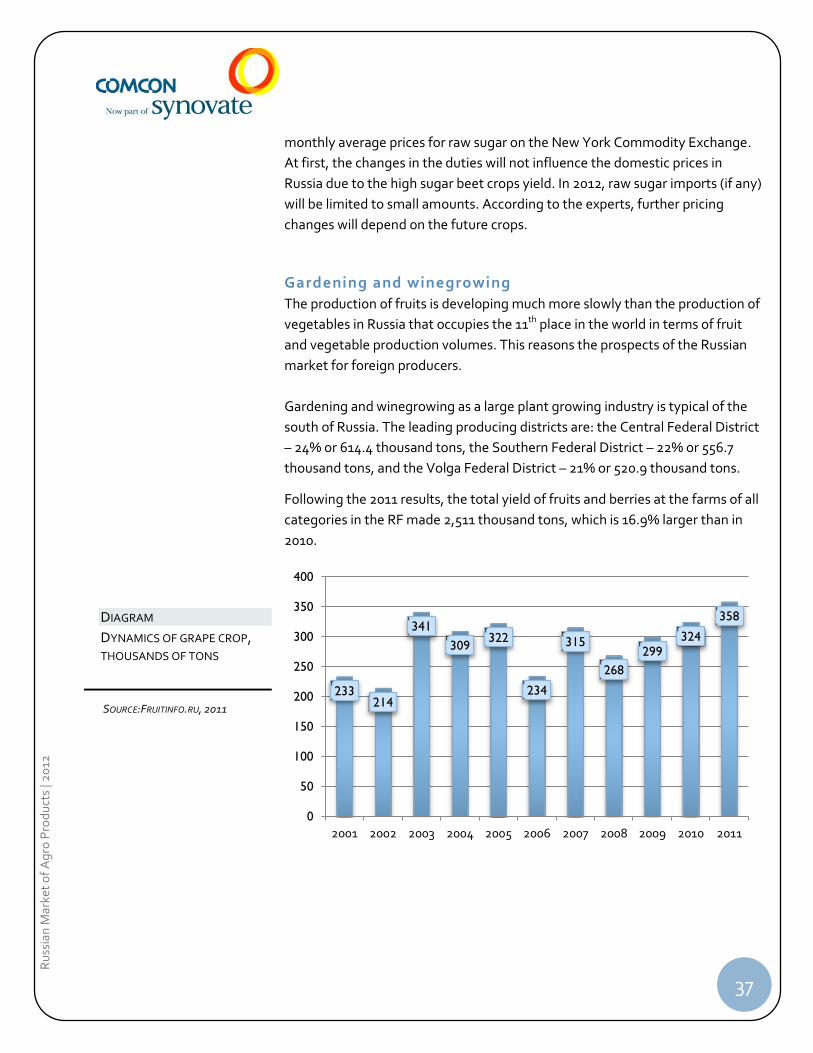

GARDENING AND WINEGROWING ....................................................................................................... 37

MEDICAL HERBS ............................................................................................................................. 41

TOBACCO ..................................................................................................................................... 42

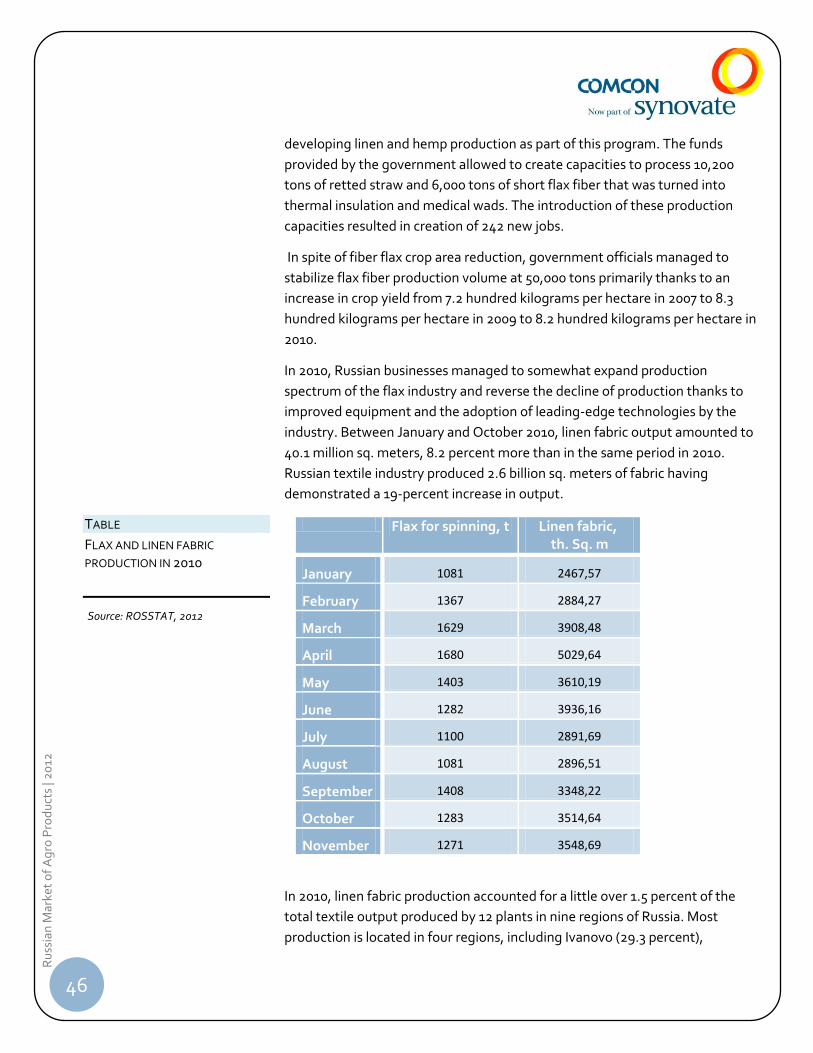

FLAX ............................................................................................................................................ 45

LIVESTOCK BREEDING ......................................................................................................................... 47

MEAT PRODUCTION ............................................................................................................................ 47

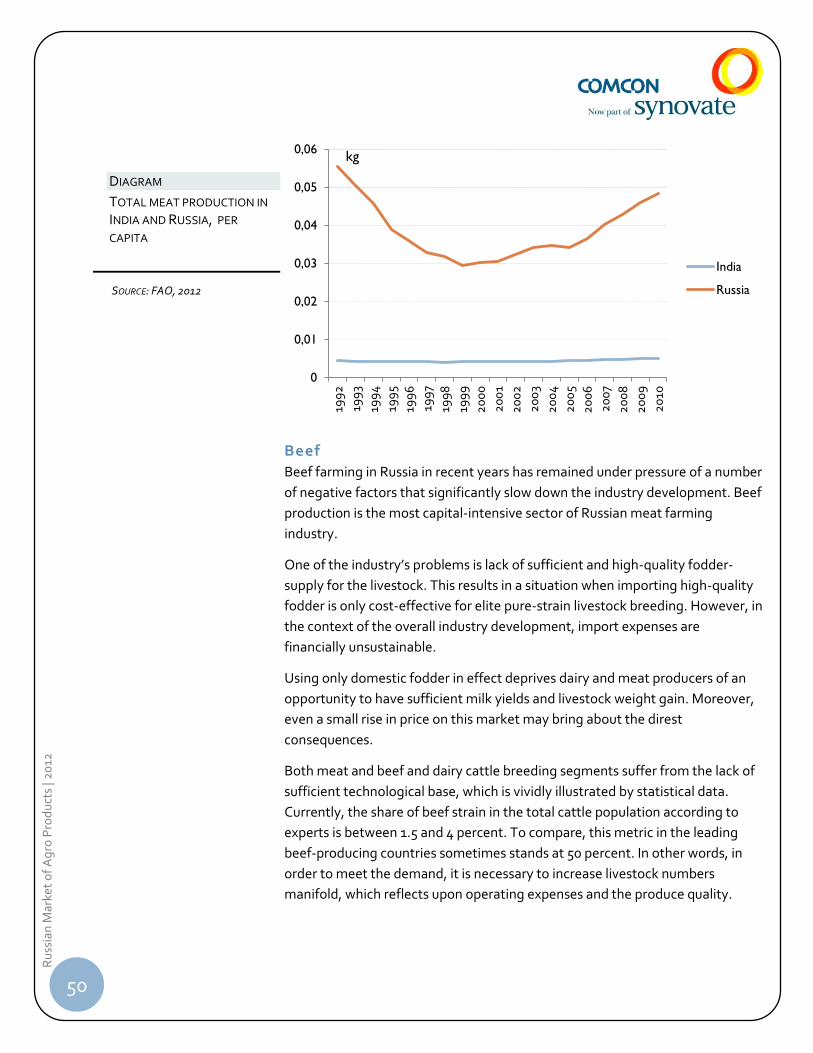

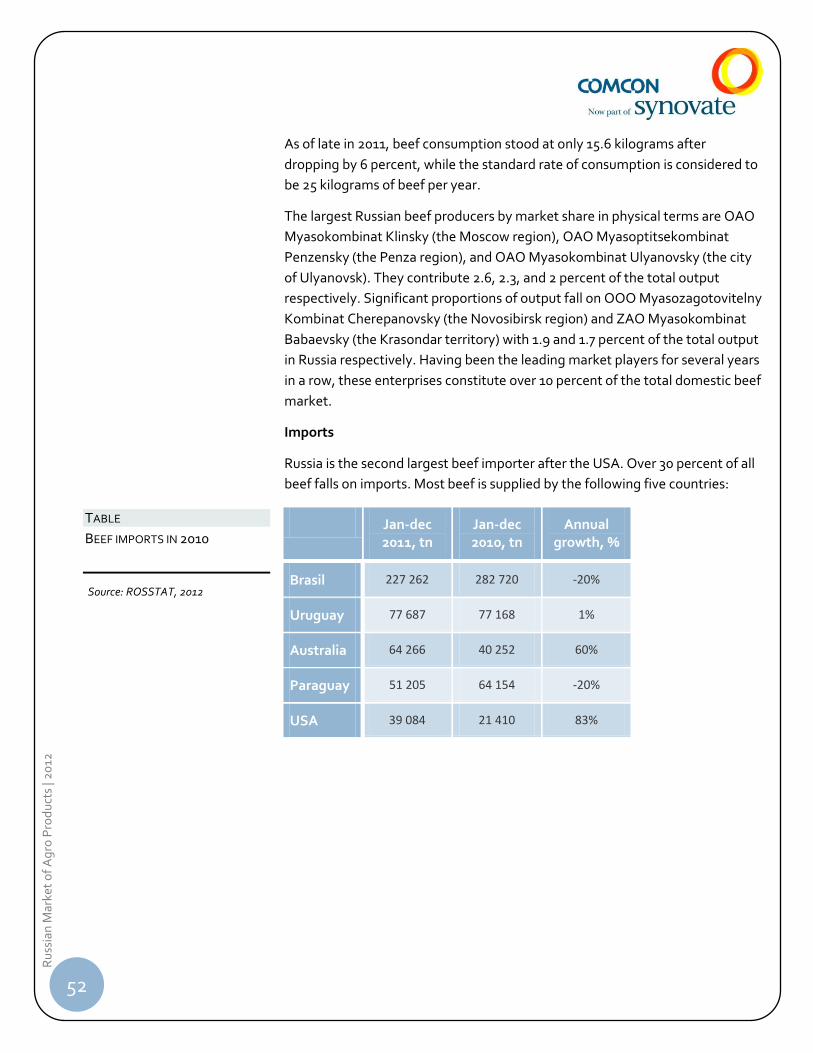

BEEF ............................................................................................................................................ 50

PORK ........................................................................................................................................... 54

POULTRY ...................................................................................................................................... 56

MEAT PROCESSING ..........................................................................................................................57

DAIRY MARKET .............................................................................................................................. 59

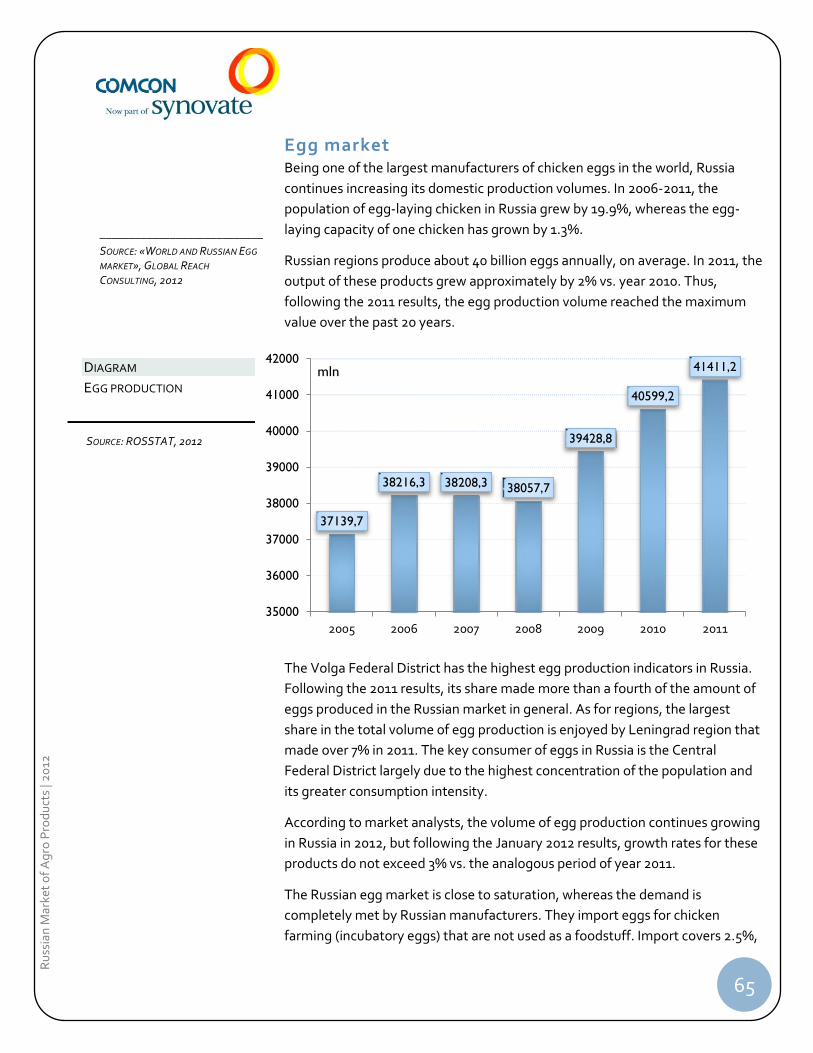

EGG MARKET ..................................................................................................................................... 65

FISH PRODUCTION .............................................................................................................................. 68

STATE SUPPORT FOR AGRICULTURE ...................................................................................................... 74

INVESTMENT POTENTIAL ...................................................................................................................... 77

INVESTMENT ATTRACTIVENESS EVALUATION WITH A BREAKDOWN INTO INDUSTRIES ................................ 78

EXPERTS OPINION ON THE PROSPECTS OF RUSSIAN-INDIAN RELATIONS IN TRADE AND INVESTMENTS ............. 83

APPENDIXES .................................................................................................................................. 85

REFERENCES .................................................................................................................................... 110

EXPERTS ...................................................................................................................................... 110

OFFICIAL RESOURCES AND STATISTICS ............................................................................................. 110

ANALYTICAL REVIEWS ................................................................................................................... 110

INTERNET RESOURCES ................................................................................................................... 111

2

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

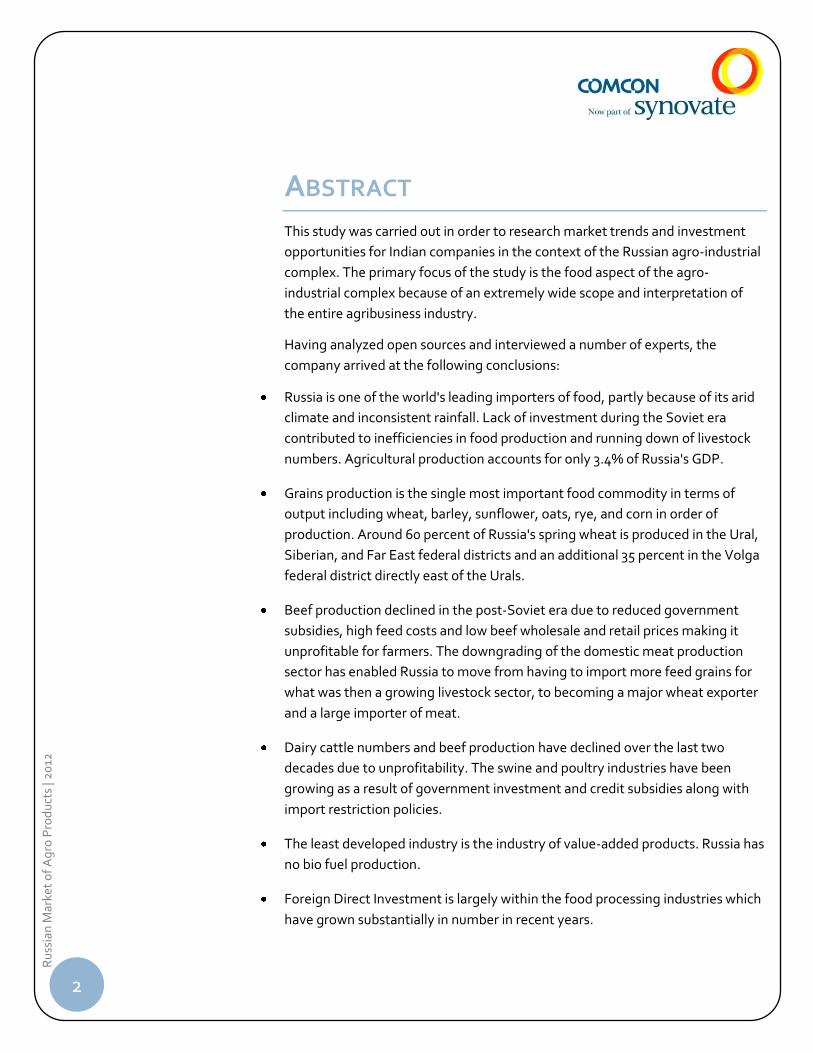

ABSTRACT This study was carried out in order to research market trends and investment

opportunities for Indian companies in the context of the Russian agro-industrial

complex. The primary focus of the study is the food aspect of the agro-

industrial complex because of an extremely wide scope and interpretation of

the entire agribusiness industry.

Having analyzed open sources and interviewed a number of experts, the

company arrived at the following conclusions:

Russia is one of the world's leading importers of food, partly because of its arid

climate and inconsistent rainfall. Lack of investment during the Soviet era

contributed to inefficiencies in food production and running down of livestock

numbers. Agricultural production accounts for only 3.4% of Russia's GDP.

Grains production is the single most important food commodity in terms of

output including wheat, barley, sunflower, oats, rye, and corn in order of

production. Around 60 percent of Russia's spring wheat is produced in the Ural,

Siberian, and Far East federal districts and an additional 35 percent in the Volga

federal district directly east of the Urals.

Beef production declined in the post-Soviet era due to reduced government

subsidies, high feed costs and low beef wholesale and retail prices making it

unprofitable for farmers. The downgrading of the domestic meat production

sector has enabled Russia to move from having to import more feed grains for

what was then a growing livestock sector, to becoming a major wheat exporter

and a large importer of meat.

Dairy cattle numbers and beef production have declined over the last two

decades due to unprofitability. The swine and poultry industries have been

growing as a result of government investment and credit subsidies along with

import restriction policies.

The least developed industry is the industry of value-added products. Russia has

no bio fuel production.

Foreign Direct Investment is largely within the food processing industries which

have grown substantially in number in recent years.

3

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

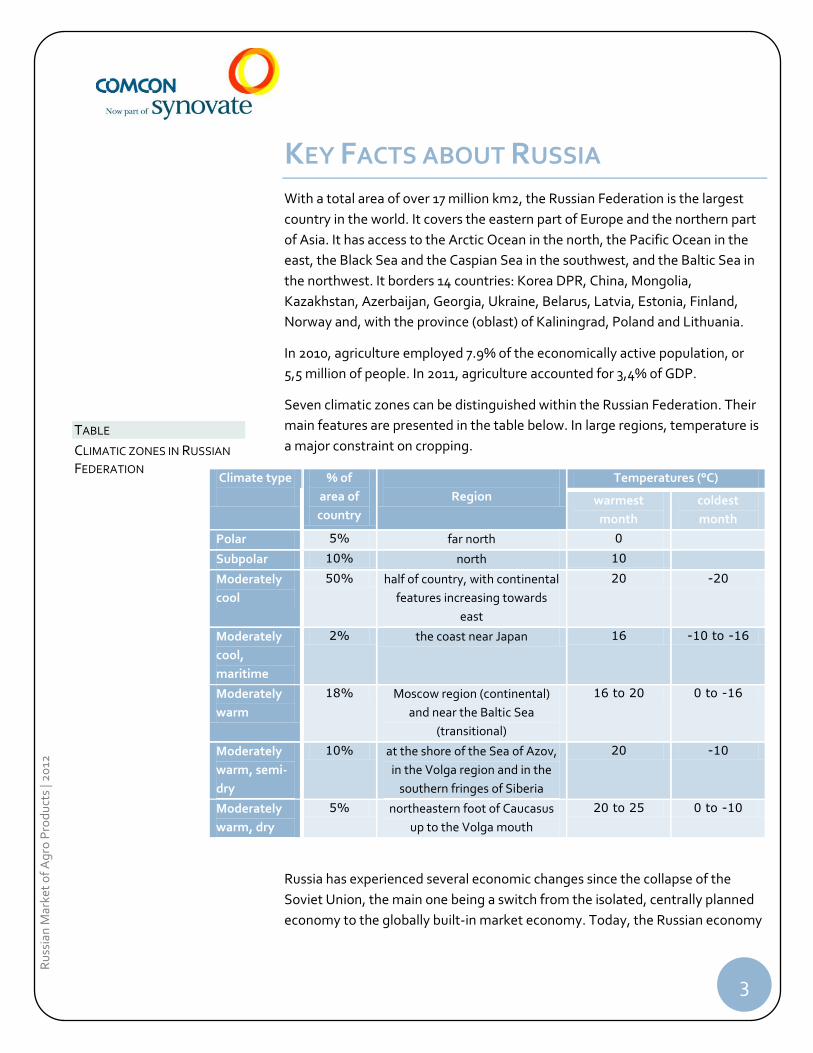

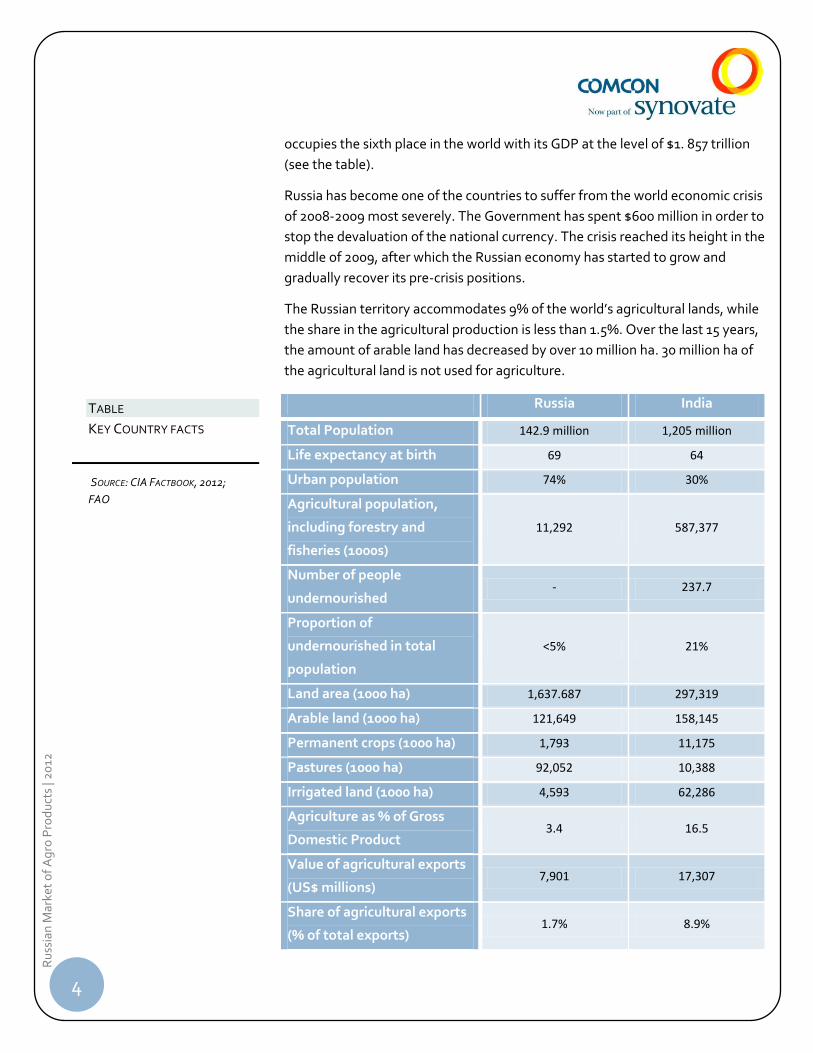

KEY FACTS ABOUT RUSSIA With a total area of over 17 million km2, the Russian Federation is the largest

country in the world. It covers the eastern part of Europe and the northern part

of Asia. It has access to the Arctic Ocean in the north, the Pacific Ocean in the

east, the Black Sea and the Caspian Sea in the southwest, and the Baltic Sea in

the northwest. It borders 14 countries: Korea DPR, China, Mongolia,

Kazakhstan, Azerbaijan, Georgia, Ukraine, Belarus, Latvia, Estonia, Finland,

Norway and, with the province (oblast) of Kaliningrad, Poland and Lithuania.

In 2010, agriculture employed 7.9% of the economically active population, or

5,5 million of people. In 2011, agriculture accounted for 3,4% of GDP.

Seven climatic zones can be distinguished within the Russian Federation. Their

main features are presented in the table below. In large regions, temperature is

a major constraint on cropping.

Climate type

% of

area of

country

Region

Temperatures (°C)

warmest

month

coldest

month

Polar 5% far north 0

Subpolar 10% north 10

Moderately

cool

50% half of country, with continental

features increasing towards

east

20 -20

Moderately

cool,

maritime

2% the coast near Japan 16 -10 to -16

Moderately

warm

18% Moscow region (continental)

and near the Baltic Sea

(transitional)

16 to 20 0 to -16

Moderately

warm, semi-

dry

10% at the shore of the Sea of Azov,

in the Volga region and in the

southern fringes of Siberia

20 -10

Moderately

warm, dry

5% northeastern foot of Caucasus

up to the Volga mouth

20 to 25 0 to -10

Russia has experienced several economic changes since the collapse of the

Soviet Union, the main one being a switch from the isolated, centrally planned

economy to the globally built-in market economy. Today, the Russian economy

TABLE

CLIMATIC ZONES IN RUSSIAN

FEDERATION

4

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

occupies the sixth place in the world with its GDP at the level of $1. 857 trillion

(see the table).

Russia has become one of the countries to suffer from the world economic crisis

of 2008-2009 most severely. The Government has spent $600 million in order to

stop the devaluation of the national currency. The crisis reached its height in the

middle of 2009, after which the Russian economy has started to grow and

gradually recover its pre-crisis positions.

The Russian territory accommodates 9% of the world’s agricultural lands, while

the share in the agricultural production is less than 1.5%. Over the last 15 years,

the amount of arable land has decreased by over 10 million ha. 30 million ha of

the agricultural land is not used for agriculture.

Russia India

Total Population 142.9 million 1,205 million

Life expectancy at birth 69 64

Urban population 74% 30%

Agricultural population,

including forestry and

fisheries (1000s)

11,292 587,377

Number of people

undernourished - 237.7

Proportion of

undernourished in total

population

<5% 21%

Land area (1000 ha) 1,637.687 297,319

Arable land (1000 ha) 121,649 158,145

Permanent crops (1000 ha) 1,793 11,175

Pastures (1000 ha) 92,052 10,388

Irrigated land (1000 ha) 4,593 62,286

Agriculture as % of Gross

Domestic Product 3.4 16.5

Value of agricultural exports

(US$ millions) 7,901 17,307

Share of agricultural exports

(% of total exports) 1.7% 8.9%

TABLE

KEY COUNTRY FACTS

SOURCE: CIA FACTBOOK, 2012;

FAO

5

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

Value of agricultural imports

(US$ millions) 31,389 9,141

Share of agricultural imports

(% of total imports) 10.8 2.8

CROP RAISING AND FOOD PROCESSING

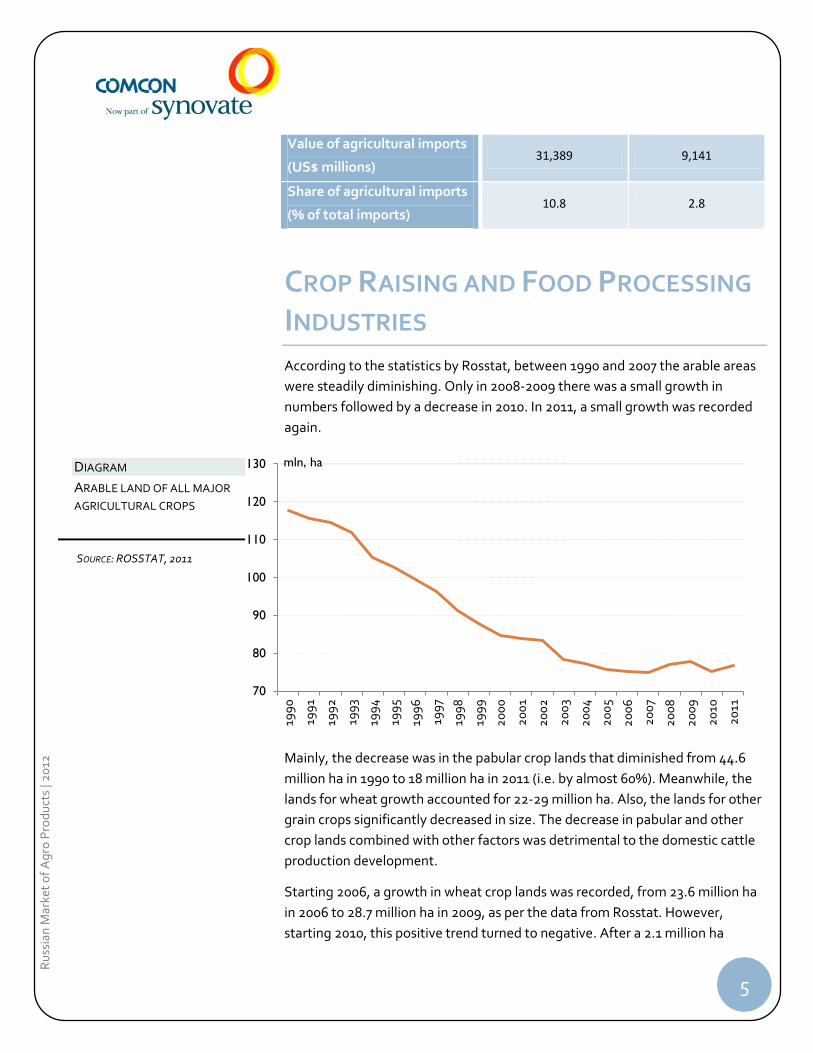

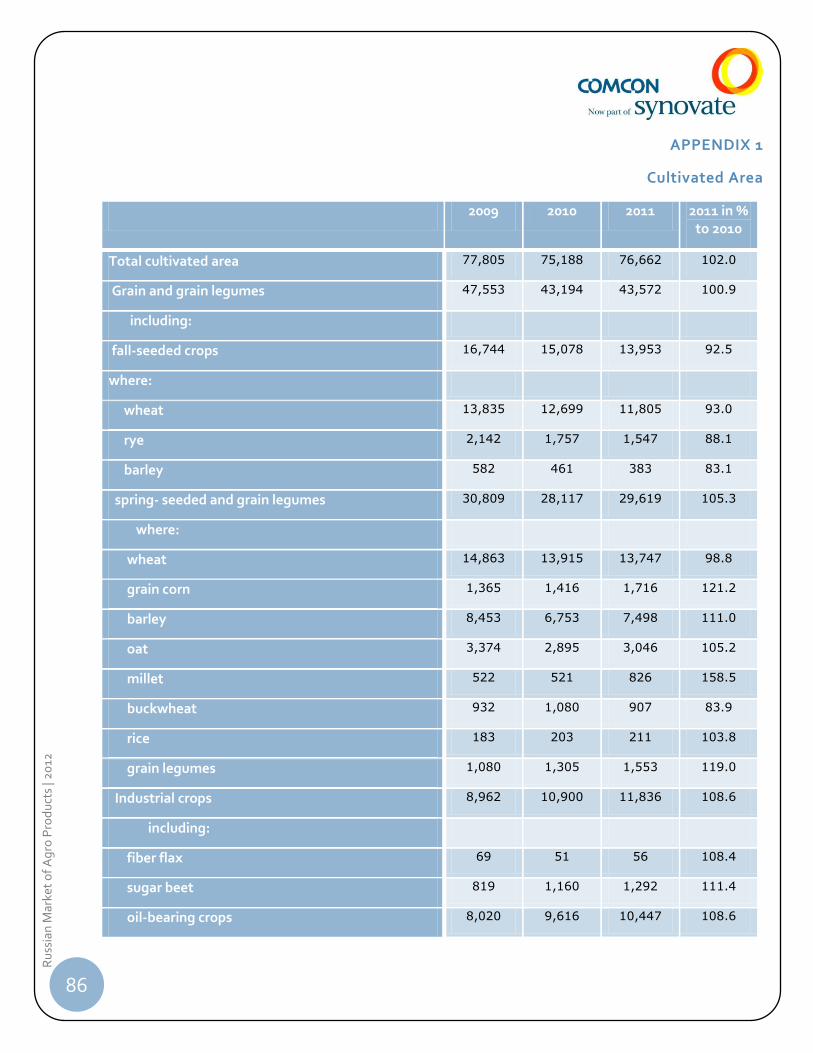

INDUSTRIES According to the statistics by Rosstat, between 1990 and 2007 the arable areas

were steadily diminishing. Only in 2008-2009 there was a small growth in

numbers followed by a decrease in 2010. In 2011, a small growth was recorded

again.

Mainly, the decrease was in the pabular crop lands that diminished from 44.6

million ha in 1990 to 18 million ha in 2011 (i.e. by almost 60%). Meanwhile, the

lands for wheat growth accounted for 22-29 million ha. Also, the lands for other

grain crops significantly decreased in size. The decrease in pabular and other

crop lands combined with other factors was detrimental to the domestic cattle

production development.

Starting 2006, a growth in wheat crop lands was recorded, from 23.6 million ha

in 2006 to 28.7 million ha in 2009, as per the data from Rosstat. However,

starting 2010, this positive trend turned to negative. After a 2.1 million ha

70

80

90

100

110

120

130

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

mln, ha DIAGRAM

ARABLE LAND OF ALL MAJOR

AGRICULTURAL CROPS

SOURCE: ROSSTAT, 2011

6

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

decrease in 2010 (down to 26.6 million ha), Rosstat recorded a further 1 million

ha decrease in 2011. Still, a small overall growth in the grains crop lands (by 0.9

million ha or 2.1%, as per the data from Rosstat) is expected.

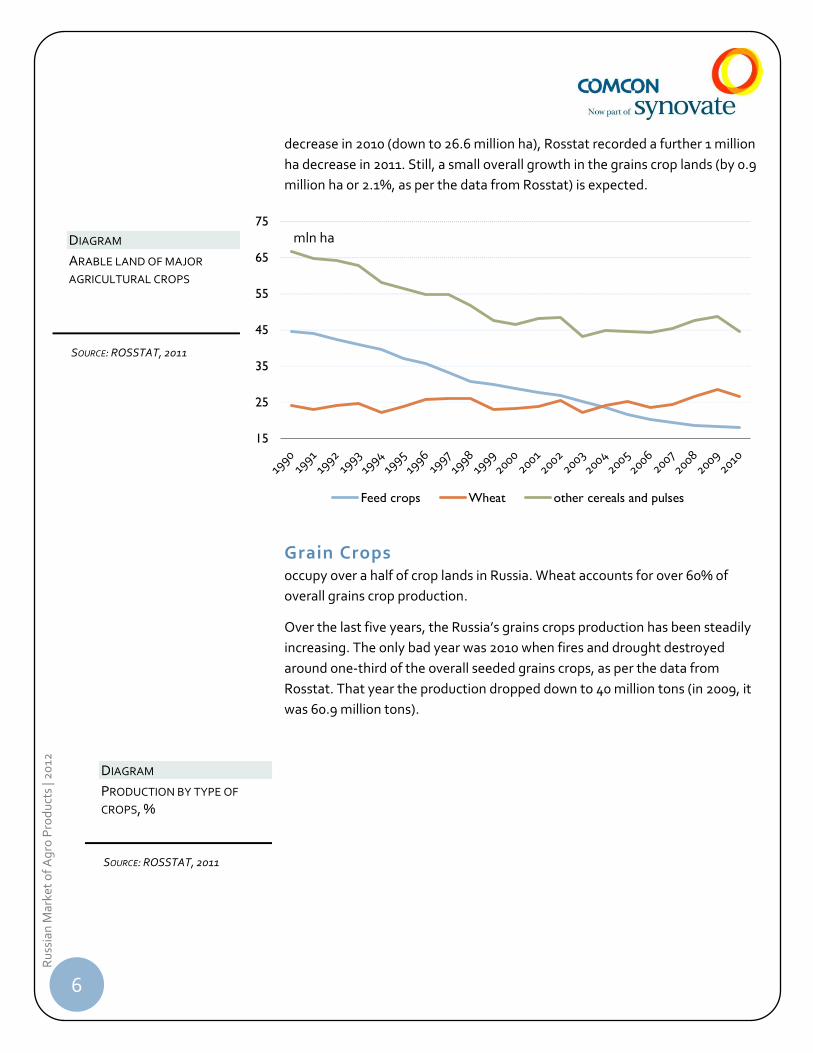

Grain Crops occupy over a half of crop lands in Russia. Wheat accounts for over 60% of

overall grains crop production.

Over the last five years, the Russia’s grains crops production has been steadily

increasing. The only bad year was 2010 when fires and drought destroyed

around one-third of the overall seeded grains crops, as per the data from

Rosstat. That year the production dropped down to 40 million tons (in 2009, it

was 60.9 million tons).

15

25

35

45

55

65

75

Feed crops Wheat other cereals and pulses

mln ha DIAGRAM

ARABLE LAND OF MAJOR

AGRICULTURAL CROPS

SOURCE: ROSSTAT, 2011

DIAGRAM

PRODUCTION BY TYPE OF

CROPS, %

SOURCE: ROSSTAT, 2011

7

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

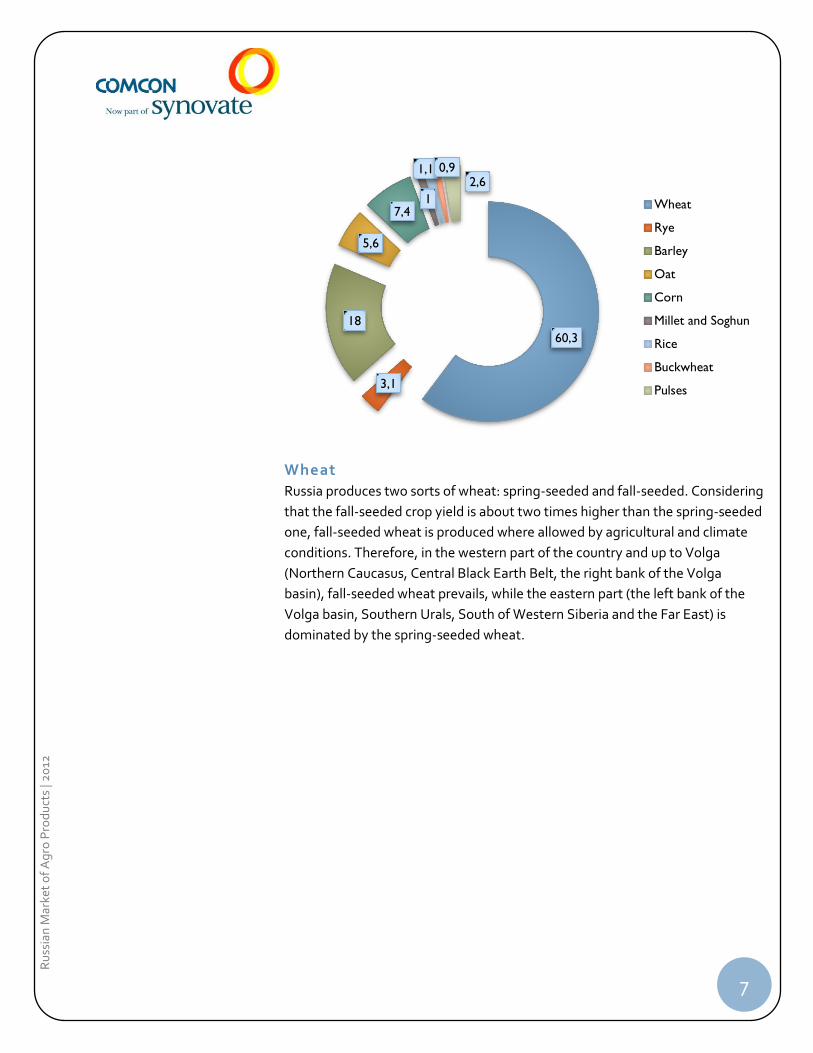

Wheat

Russia produces two sorts of wheat: spring-seeded and fall-seeded. Considering

that the fall-seeded crop yield is about two times higher than the spring-seeded

one, fall-seeded wheat is produced where allowed by agricultural and climate

conditions. Therefore, in the western part of the country and up to Volga

(Northern Caucasus, Central Black Earth Belt, the right bank of the Volga

basin), fall-seeded wheat prevails, while the eastern part (the left bank of the

Volga basin, Southern Urals, South of Western Siberia and the Far East) is

dominated by the spring-seeded wheat.

60,3

3,1

18

5,6

7,4 1

1,1 0,9 2,6

Wheat

Rye

Barley

Oat

Corn

Millet and Soghun

Rice

Buckwheat

Pulses

8

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

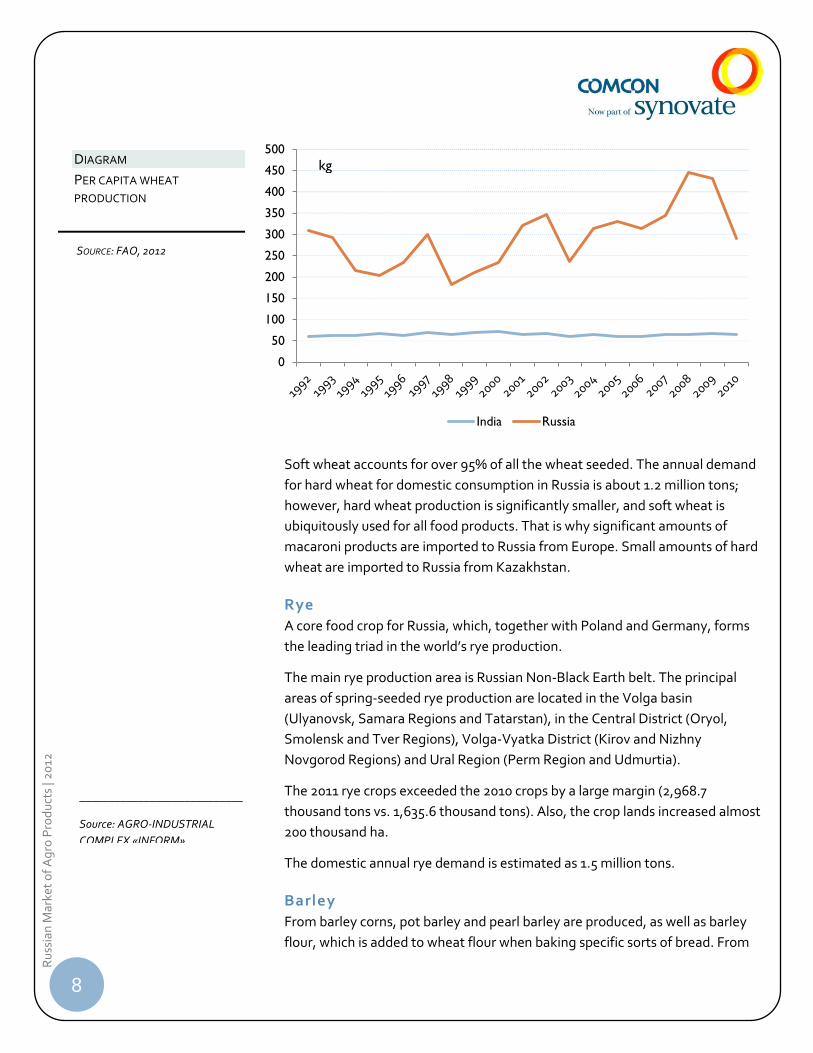

Soft wheat accounts for over 95% of all the wheat seeded. The annual demand

for hard wheat for domestic consumption in Russia is about 1.2 million tons;

however, hard wheat production is significantly smaller, and soft wheat is

ubiquitously used for all food products. That is why significant amounts of

macaroni products are imported to Russia from Europe. Small amounts of hard

wheat are imported to Russia from Kazakhstan.

Rye

A core food crop for Russia, which, together with Poland and Germany, forms

the leading triad in the world’s rye production.

The main rye production area is Russian Non-Black Earth belt. The principal

areas of spring-seeded rye production are located in the Volga basin

(Ulyanovsk, Samara Regions and Tatarstan), in the Central District (Oryol,

Smolensk and Tver Regions), Volga-Vyatka District (Kirov and Nizhny

Novgorod Regions) and Ural Region (Perm Region and Udmurtia).

The 2011 rye crops exceeded the 2010 crops by a large margin (2,968.7

thousand tons vs. 1,635.6 thousand tons). Also, the crop lands increased almost

200 thousand ha.

The domestic annual rye demand is estimated as 1.5 million tons.

Barley

From barley corns, pot barley and pearl barley are produced, as well as barley

flour, which is added to wheat flour when baking specific sorts of bread. From

0

50

100

150

200

250

300

350

400

450

500

India Russia

kg

____________________________

Source: AGRO-INDUSTRIAL

COMPLEX «INFORM»

DIAGRAM

PER CAPITA WHEAT

PRODUCTION

SOURCE: FAO, 2012

9

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

barley, the amylum and molasses industry produces amylum. The products

extracted from the barley corn as malt extracts are used in textile,

confectionary and pharmaceutical industries. However, the biggest amounts of

barley are decorticated and processed to be used as a valuable concentrated

feed compound for pig and poultry farming.

Most barley is grown in the Central Federal District (36.4%) and in the Volga

Federal District (24%). In Russia, mostly fall-seeded barley is produced, which

accounts for around 90% of the total seeded barley.

One-fifth of the domestically harvested barley is exported. The main share in

the export structure belongs to the fodder barley.

The principle destination country for the barley exported from Russia is Saudi

Arabia. The share of the country is 58.8%. In particular, the geographic location

of the country allows further resale of Russian barley farther abroad. The

second largest buyer of domestically produced barley is Iran (9.9%). The CIS

countries account for buying less than 1% of the Russian barley.

The main barley exporting company is LLC Rosinteragroservis with 15.8%. The

second place (12%) is held by International Grain Company created by the Swiss

company Glencore International AG in 2004. Barley imports are insignificant

compared to barley exports. Russia mostly imports barley from Kazakhstan

(90% of all the barley imported). The second place is held by Sweden (8%).

The main consumers of barley are the leading brewing companies that account

for over 35% of the amounts purchased. The first place in the purchases (19%) is

occupied by the Baltika brewing company. The barley purchase share by forage

feed plants is as high as 10%.

Although barley cultivation is widespread in Russia, the suppliers have

significant problems selling these crops. Also, this market has less support by

the state compared to a number of other crops.

Russia is one of the leading consumers of brewer’s malt. Only ten years ago, the

share of imported malt was reaching 70%; however, this raw stock import

boosted breweries’ expenses, so the breweries started investing into agriculture

and malt and barley production. Currently, 75% of the malt demand is covered

by the domestically produced raw stock; however, despite all effort, only up to

one-third of the domestic brewer’s malt meets the world quality standards.

The Russian brewing companies and malt producers try to abandon raw stock

imports but, given the unstable quality of domestically produced barley, it is

still deemed impossible.

10

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

Rice

The rice market is the largest among other grain markets. Rice is the single

most consumed grain in Russia. The rice market is more than twice as large as

the buckwheat market, the second most popular cereal among consumers.

However, the share of rice crop acreage amounts to less than 0.5 percent of the

total grain cultivation area.

2009 2010 2011

Area under rice crop (thousand ha)

183 203 211

Share of cultivated area (%)

0.2 0.3 0.3

Gross harvest of paddy rice (mln ton)

913 1,061 1,056

According to the official data, an all-time high volume of output was delivered

onto the Russian rice market in 2010. The total output delivered by Russian rice

producers onto the market amounted to approximately 380 thousand tons in

2010. Rice harvest increased due to continue expansion of crops and increased

productivity of land from 5140 kg / ha to 5280 kg / ha. This metric equaled a

little under 345 thousand tons in 2011.

Over 88 percent of the total rice output is accounted for by the Krasnodar

territory; 4.0 percent – by the Rostov region, and 3.9 percent – by the

Chelyabinsk region.

The supply of rice in Russia went up 24 percent between 2006 and 2010 from

1.1 to 1.4 million tons. 2007 was the only year when rice supply on the Russian

market shrank demonstrating a contraction of 7 percent. The decline of supply

was attributed to reduced imports of polished and semi-polished rice in Russia

from China in 2007. The reason for the shipment volume decline was gross

infringement of import regulations as delivered goods failed to comply with

quarantine security rules.

The demand for rice in Russia grew by 26 percent between 2006 and 2010 from

1 to 1.3 million tons. The biggest surge in demand against a previous year was

observed in 2010 and equaled 13 percent.

TABLE

DYNAMICS OF RICE

PRODUCTION

SOURCE: ROSSTAT, 2011

11

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

The rice market in Russia is taken by a number of producers including the

Razgulyay Group, the Grana Association, the SoyuzPishcheprom Association,

and some others.

Beginning in 2010, the rice market has been recovering from the consequences

of the financial crisis. Currently, rice consumption is rising in Russia. Apart from

that, a rapid expansion of the instant-cereal market is an additional factor that

has a positive effect on the rice market. Experts forecast steady rice market

growth in 2012 and 2013.

Imports-exports

Between 2005 and 2010, the volume of rice imports tended to decline. The

imported rice share of the total supply volume in 2006 – 2010 was reduced

almost by half from 29 percent to 16 percent. State support of rice growing in

Russia contributed to a drop in the share of imported rice.

The rice market has the largest volume of imported rice compared to other

grain markets. Thailand, Vietnam, and China are the key importers of rice into

the Russian market.

The major receiving companies on the Russian rice market are the

ProdGamma-Grain company, the Agroalliance company, Angstrom Trading,

and Mistral Trading. The ProdGamma-Grain company receives over two thirds

of the total produce supplied to the Russian rice market.

There is an import of those types of rice that Russia does not produce. Now it is

long-grain rice and rare varieties (jasmine, basmati, Arborio). In 2010 they had

92% of imports. Whereas in 2005, these varieties accounted for 52% of

imported volumes, and almost as many (48%) were in the medium grain and

short grain rice, which can be produced in Russia.

There was a maximum rice imports in 2002 and 2003, at the level of 470

thousand tons. Throughout the following years, it declined, and in 2010 it was

only 220 thousand tons, surpassing the export of 150 tons.

According to experts, Russia will have to import long grain rice for at least

another 4-5 years until there are analogues of the national selection.

12

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

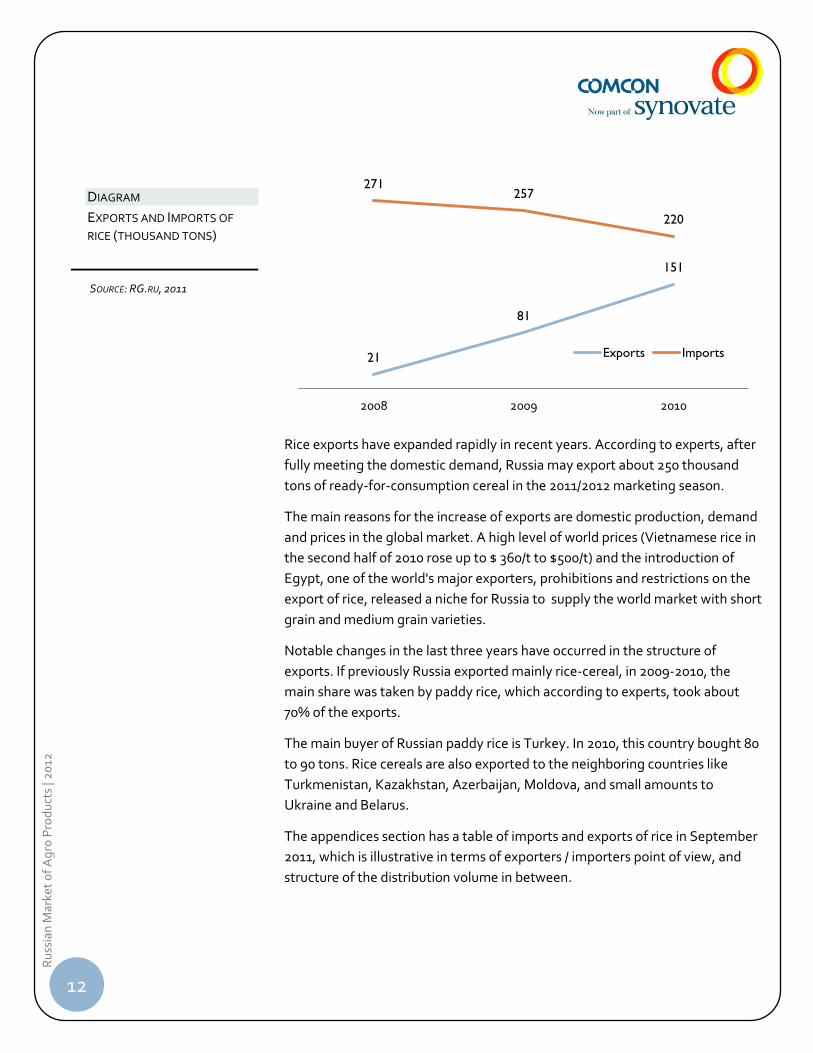

Rice exports have expanded rapidly in recent years. According to experts, after

fully meeting the domestic demand, Russia may export about 250 thousand

tons of ready-for-consumption cereal in the 2011/2012 marketing season.

The main reasons for the increase of exports are domestic production, demand

and prices in the global market. A high level of world prices (Vietnamese rice in

the second half of 2010 rose up to $ 360/t to $500/t) and the introduction of

Egypt, one of the world's major exporters, prohibitions and restrictions on the

export of rice, released a niche for Russia to supply the world market with short

grain and medium grain varieties.

Notable changes in the last three years have occurred in the structure of

exports. If previously Russia exported mainly rice-cereal, in 2009-2010, the

main share was taken by paddy rice, which according to experts, took about

70% of the exports.

The main buyer of Russian paddy rice is Turkey. In 2010, this country bought 80

to 90 tons. Rice cereals are also exported to the neighboring countries like

Turkmenistan, Kazakhstan, Azerbaijan, Moldova, and small amounts to

Ukraine and Belarus.

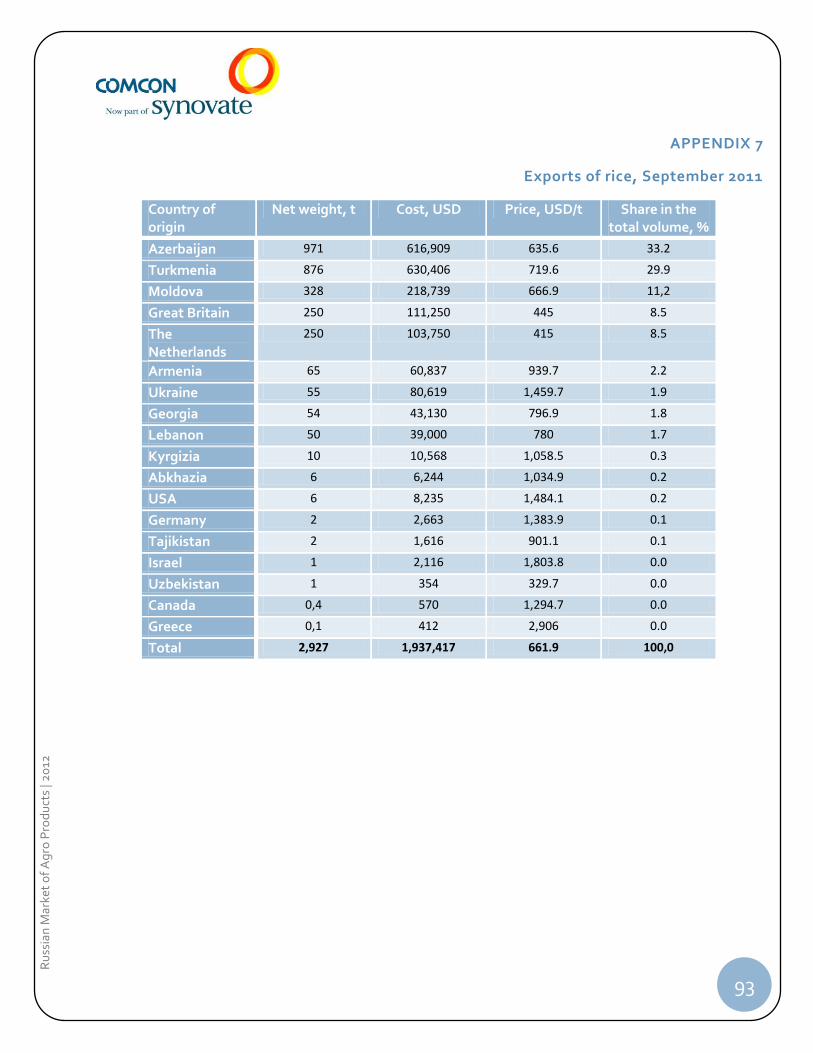

The appendices section has a table of imports and exports of rice in September

2011, which is illustrative in terms of exporters / importers point of view, and

structure of the distribution volume in between.

21

81

151

271 257

220

2008 2009 2010

Exports Imports

DIAGRAM

EXPORTS AND IMPORTS OF

RICE (THOUSAND TONS)

SOURCE: RG.RU, 2011

13

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

Investments

In July 2012, Krasnodar region completed the first construction stage of the

largest plant in the country that will allow processing of up to 100 tons of raw

rice in one day. This may boost sowing and production of long-grain rice

varieties as demand for them currently accounts for most of rice import. The

project is unique in its focus on rare rice varieties and exclusive types of

production, which may prove an advantage for the investor. Indeed, there are

no facilities in the southern Russia that produce parboiled rice.

Several market participants point out that the rice-processing project poses

additional risks without own sources of raw rice.

“Processing capacities in the region are twice as high as the raw-produce volume.

The volume of raw rice left undistributed across production facilities is declining.

The market is nearing a point when up to 80 percent of rice will be accumulated by

large producers with own processing facilities.”

However, if the processer offers the agricultural producer exotic rice varieties

and ensures a buy-back, it becomes unnecessary for the producer to own

production facilities.

The rest of the grain crops that include rice and corn are not commonly raised

due to the harsh climate conditions. Corn is seeded in the Northern Caucasus,

the only region in Russia that resembles the renowned Corn Belt in the U.S. The

rest of the regions of the country produce corn for green fodder and ensilage.

Rice is seeded in the flux flow of the Kuban River, the Volga-Aqtobe bottom-

land and the near-Khanka lowland.

EXPERT OPINION

14

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

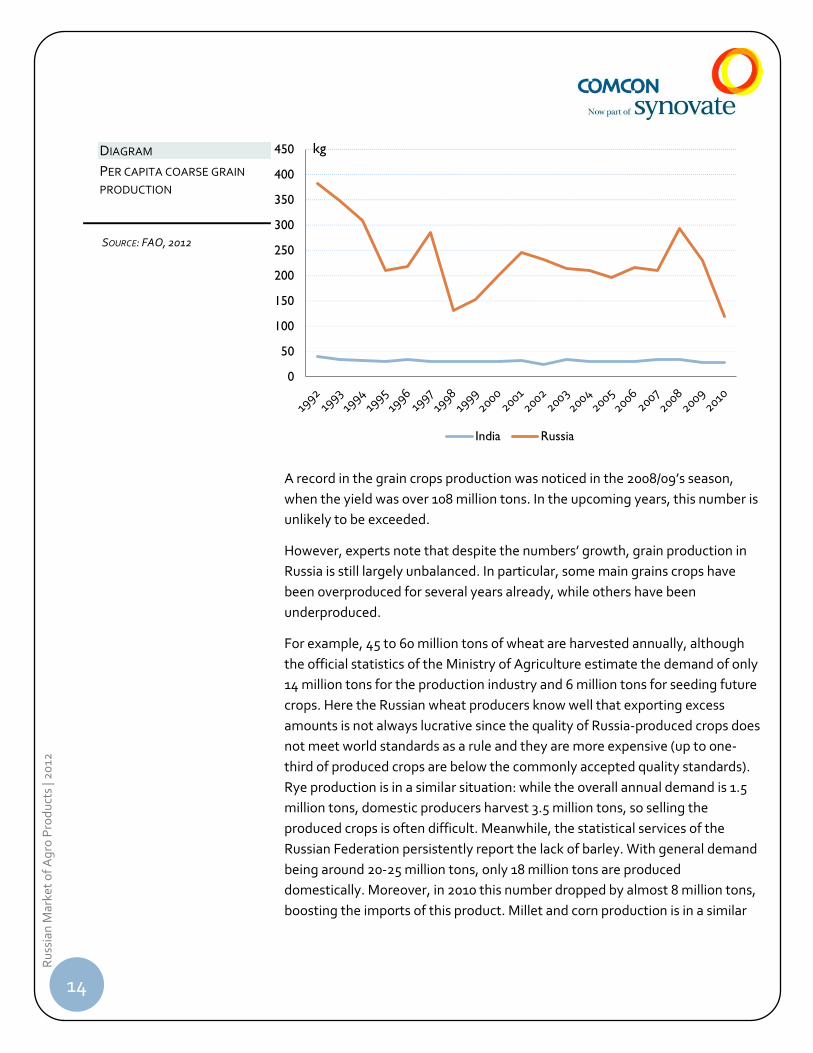

A record in the grain crops production was noticed in the 2008/09’s season,

when the yield was over 108 million tons. In the upcoming years, this number is

unlikely to be exceeded.

However, experts note that despite the numbers’ growth, grain production in

Russia is still largely unbalanced. In particular, some main grains crops have

been overproduced for several years already, while others have been

underproduced.

For example, 45 to 60 million tons of wheat are harvested annually, although

the official statistics of the Ministry of Agriculture estimate the demand of only

14 million tons for the production industry and 6 million tons for seeding future

crops. Here the Russian wheat producers know well that exporting excess

amounts is not always lucrative since the quality of Russia-produced crops does

not meet world standards as a rule and they are more expensive (up to one-

third of produced crops are below the commonly accepted quality standards).

Rye production is in a similar situation: while the overall annual demand is 1.5

million tons, domestic producers harvest 3.5 million tons, so selling the

produced crops is often difficult. Meanwhile, the statistical services of the

Russian Federation persistently report the lack of barley. With general demand

being around 20-25 million tons, only 18 million tons are produced

domestically. Moreover, in 2010 this number dropped by almost 8 million tons,

boosting the imports of this product. Millet and corn production is in a similar

0

50

100

150

200

250

300

350

400

450

India Russia

kg DIAGRAM

PER CAPITA COARSE GRAIN

PRODUCTION

SOURCE: FAO, 2012

15

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

situation: only 3.5 million tons of corn are produced annually. This amount is by

far not sufficient to cover the internal demand of domestic producers.

The internal consumption of grain crops in Russia increased from 75-76 million

tons (2009-2010) to 77-78 million tons (2010-2011). According to the expert

estimations, the consumption will annually grow by 2-3 million tons.

As per the data from the Russian Grain Union (RGU), between 2001 and 2010,

average internal annual grain consumption was 70.1 million tons. The main

share (over 50%) was used as feedstock. Consumption by the food production

industry and seeding consumption were around 30% and 16-17%, respectively.

In fact, the grain exporting capability first of all depends on the crop yield and

on the amount of grain in stock by the beginning of the crop year.

The estimations of future grain consumption are contradictory. One source

suggests a decrease in the grain consumed for grinding flour in the upcoming 7

years, due to decreasing population and dropping bread consumption. By 2011

(as compared to 2008) the bread consumption decreased by 1.5 million tons

and totaled 12.5 million tons. However, in the future an increase in the flour

production (up to 13.5-14 million tons) is possible, both for export and domestic

use. A decrease in the consumption can be mitigated if Russia does not tighten

its migration policy.

According to other data, internal grain consumption in Russia has increased

from 75-76 million tons (in the 2009-2010 crop year) to 77-78 (in the 2010-2011

crop year); it is also estimated to annually grow by 2-3 million tons on average

in the upcoming years.

Imports

The Russian imports of the main grain crops over the last several years tend to

decrease, except for 2010 (a year of crisis), when a draught forced Russia to

import about 2 million tons of grains; moreover, initial estimations suggested

this number to be over 3.5 million tons. The low numbers have been achieved

through a ban by the domestic Ministry of Agriculture that prevented the

exportation of crops. In the structure of the Russian grain imports, the largest

importers from the CIS countries are predominant. As per the official 2005-

2009 statistics by the Ministry of Agriculture, about 55% of Russia’s imported

grain crops are imported from Kazakhstan, while China accounts for another

15-16% and Ukraine, Belarus, Germany and Poland, for 7-7.5% each.

____________________________

SOURCE: INSTITUTE OF AGRARIAN

MARKET

____________________________

SOURCE: ANALITICAL DEPARTMENT

AGRORU.COM

16

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

Exports

In April 2010, an event took place that was a milestone for both Russian and the

entire world’s grain market. At the annual meeting of the International Grains

Council, Russia was officially transferred from the category of grain importers

to that of grain exporters. From being the largest net grains importer, the

nation turned into a steadily 3rd-4th largest wheat exporter and the 2nd-3rd

largest barley exporter.

As for the 2011/12 season, the Russian grain exports reached 23.5 million tons,

breaking the historical grain exportation record. By the middle of April, a

historical wheat exportation record of 18.5 million tons was set. Previous

exportation record was set in the 2009/10 season when 18.1 million tons were

exported (excl. the grain calculated from the flour exports). Record breaking

grain legumes exports of over 600 thousand tons have been noted. Corn

exportation as of mid April was also close to the historical records, reaching

over 1.2 million tons.

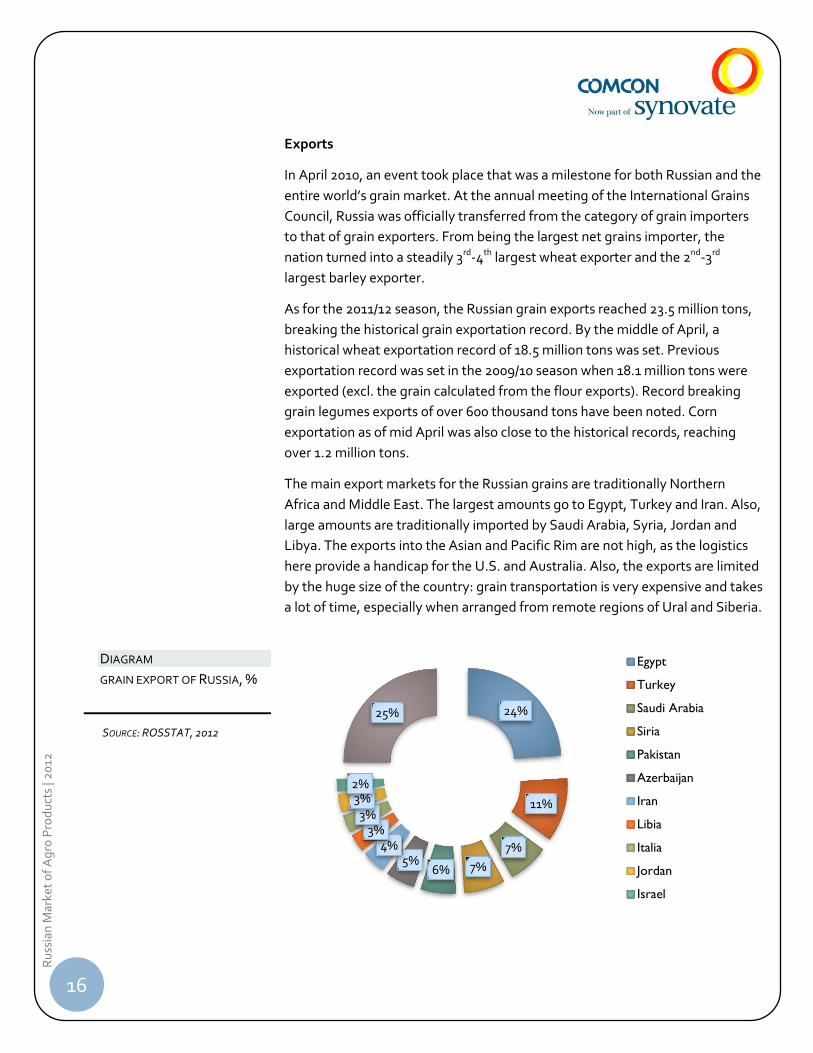

The main export markets for the Russian grains are traditionally Northern

Africa and Middle East. The largest amounts go to Egypt, Turkey and Iran. Also,

large amounts are traditionally imported by Saudi Arabia, Syria, Jordan and

Libya. The exports into the Asian and Pacific Rim are not high, as the logistics

here provide a handicap for the U.S. and Australia. Also, the exports are limited

by the huge size of the country: grain transportation is very expensive and takes

a lot of time, especially when arranged from remote regions of Ural and Siberia.

24%

11%

7%

7% 6% 5%

4% 3%

3% 3% 2%

25%

Egypt

Turkey

Saudi Arabia

Siria

Pakistan

Azerbaijan

Iran

Libia

Italia

Jordan

Israel

DIAGRAM

GRAIN EXPORT OF RUSSIA, %

SOURCE: ROSSTAT, 2012

17

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

State regulation

The Russian government pays close attention to the grain production industry,

providing conditions for sustained growth and for the realization of existing

potential. These were the measures that made Russia one of the largest grain

producers, and they will allow for even better results in the future. According to

the official position of the domestic Ministry of Agriculture, the push up of the

grain exports in the upcoming years has high perspectives and, hence, priority.

In the upcoming 10-15 years, Russia is planning to double the grain exports.

According to the ministry’s estimations, by 2016 the Russian grains exports will

have reached over 39 million tons, which accounts for 15 per cent of the world’s

market. The Russian government will continue the support of the Russian

grains exports in the long term; to this end, the expenses for building new linear

granaries are planned for as well as for improving seaport throughput in the

European part of the country and for building a new seaport grain terminal in

the Far East. The government also envisages the subsidies of loan rates and

railway transportation rates and it invites foreign investors to take part in

upgrading the seaport and granaries’ infrastructure.

Grain Crops Processing

Russia has a fairly well developed flour and grit grinding industry.

The flour market in Russia is shrinking. The last time this market grew stronger

was in 2006 (a 2.3% increase). Starting 2007, flour sales have been dropping

every year. In 2010, flour sales were 9.6 million tons, which is 2.1% lower than

the previous year. In the foreseeable future, the market diminishing rate will

slow down. According to the BusinesStat estimations, by 2014 the flour sales

will drop down to 9.3 million tons.

The main reasons for the flour market to diminish are the decrease in

population and the increase in the household income. These factors do not only

lower the bakery products consumption but also cause the retail flour purchase

(used for home-bake products) to drop.

In the recent years, the flour market has been changing: bread and bakery

producers cause the flour consumption to decrease, while the macaroni and

pastry producers increase their flour purchase. The demand by other food

industries such as the producers of pelmeni, pizza and pancakes is also growing.

In physical terms, wheat and rye-and-wheat flour account for 90% of the

market share, the rest of the market is occupied by the rye flour. This market

structure is virtually identical to the previous years’ structure, since the flour

____________________________

Source: RBC. Market Analysis

Department

18

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

market is traditional and long-settled.

The Russian flour market is independent from the imports. Domestic products

occupy almost the entire market volume. The monopoly of the domestic

producers in the domestic market virtually rules out the risks for the production

volume expansion and opens up a further business development prospect for

the entrepreneurs.

Generally, Russia is not a large flour exporter. Over the last 6 years, the

average annual exports have not exceeded 400-450 thousand tons. In 2010

flour exports dropped down to 150 thousand tons; however, in 2011 flour

exports set a new record, reaching 600 thousand tons due to the high

production and the ban on grain exports as well as high prices.

The main importers of the Russian flour are the near abroad countries, such as

Azerbaijan, Tajikistan and Mongolia. A part of the products (approx. 21% of the

overall exportation volume) is supplied to Tunisia.

The main types of grits in the Russian market are semolina, rice, buckwheat,

corn grits, as well as oat, wheat, barley grits and slotted peas.

The structure of the grits sales is gradually changing: in 2006 the main grits for

sale were semolina (30%) and buckwheat (28%), while rice (20%) was

significantly falling behind. In 2010, however, the first place was taken by rice

and semolina (31%), while buckwheat surrendered about one-third of its share.

At year-end 2010, the volume of the Russian grits market was practically 1

million tons. As compared to the previous year’s mark, the market volume has

grown by almost 2%. Meanwhile, the domestic production volume continued to

decrease (in 2010, by another 8%). The decrease is compensated for by

constantly increasing prices. Here, the pricing of buckwheat grits is exemplary:

they showed a quadruple (!) retail price growth, reaching the peak of 112 rubles

for a kilogram in May, 2011. Also, the prices for semolina were increasing (about

10% during 2010-2011) as well as the oatmeal prices (about 25%). It allowed the

producers to recompense for the decrease in the production volumes but it

caused increased attention to the industry by the state.

The 2010 retail grits sales in Russia surpassed the 2009’s sales by 15%. Overall,

from 2007 through 2010, the retail sales of grits in the Russian Federation

showed a significant growth. Over the 6 months of 2011, the retail grits sales

surpassed those over the same months of 2010 by more than a half.

____________________________

Source: GLOBAL REACH

CONSULTING

____________________________

Source: «The Russian and world

market of cereals», 2012 Intesco

Research Group

19

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

In 2010, the imported products’ share on the market was about 23% from the

overall available grits consumption potential in Russia. The principal volume of

the Russian market was taken by the domestically manufactured products. As

per the final results of the first half of 2011, the share of imported products in

the Russian market increased, which was the result of a significant increase in

the buckwheat imports to Russia.

Rice grits are imported into the Russian Federation by Vietnam, Thailand,

Pakistan, Uruguay and Brazil. Here, the leading importer is Vietnam, which

boasts 36% of the overall rice supply. Practically all other grits shipped to Russia

are brought from Ukraine. Ukraine’s share in the Russian import is 89%.

Hungary supplies about 8% of other grits.

In Russia, the segment of deep grain processing is completely undeveloped.

Products with high added value of the segment are mostly imported.

The discussions over the development of this industry have been held for a few

years already; however, the subsidies for building the plants are not provided,

and the investments are insignificant. One of the reasons behind the absence of

implemented projects for deep processing of grains (and other crops) in Russia

is that the investors have few possibilities to attract readily available funding

from the banks. The banks, including state-owned ones, are not interested in

lending money for such projects.

”We have all kinds of cereals in the market: rice, corn, wheat. Still, there is not a

single plant producing cereals in Russia; the nearest ones are located in the Baltic

States and Poland.”

However, Russia’s recent entrance into the WTO is pushing forward the

development of this segment. Currently, more than 10 deep grain processing

plant construction projects are being carried out, although all of them are very

far from completion.

Deep processing projects are very capital intensive: a plant with the annual

production of 200 thousand tons of grain costs about $330 thousand.

Therefore, the investors need support by the state: the optimal way here is co-

financing a part of the investment expenses from the state budget, for instance,

co-financing infrastructure construction and subsidizing long-term (8-10 year)

loans.

According to the data provided by the experts, a potential annual capacity of

the deep processed products market is 15-20 million tons of grain. The

EXPERT OPINION

20

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

bioethanol fuel market could consume 50-80 million tons of grain crops

annually.

The experts say that it makes sense to locate new production facilities in the

regions of Western Siberia. Those will produce such high added value products

as lysine, organic acids, bioplastics and gluten. These regions produce a lot of

grain. Here they can increase both the yield and the productivity of land, but

exportation is an issue while the domestic consumption is limited.

”Without new consumers, the agricultural producers will not intensify crop raising:

additional volumes only cause the grain prices to collapse. The producers must be

sure that they will always be able to sell the wheat at a good price, at least higher

than the prime cost (for Western Siberia, it is around $33 thousand per ton.”

In exportation -oriented southern regions, there is no necessity for deep

processing projects.

”First of all, the implementation of these projects will be hindered by the high cost

of raw stock. Secondly, in the Southern Federal District, it is reasonable to load the

grain into trucks and drive it 200-300 to the seaport and then sell them to the

exporter at a good price. Taking risks for building such a capital intensive

production plant does not make sense. Constructing such plants in the south is

unjustified in terms of economy.”

Corn can be the only exception here: the south produces up to 65-70% of overall

domestic corn crops. Such a focus brings logic into locating corn processing

plants in the Southern Federal District. Agrico, a Stavropol-based holding, has a

deep corn processing project with the cost of $83.3 mln.

Project examples:

Pava, an Altay-based grain processing company, is ready to invest up to $330

thousand into a deep grain processing project on the site of the Rebrikhin flour

mill. Pava wants to produce dry wheat gluten, syrups, ethyl alcohol s, feedstock

and liquefied carbon dioxide. The production capacity of the plant is 1.5

thousand tons of wheat per day, or 500 thousand tons per annum.

Bagansky Holding Group from the Novosibirsk Region announced a deep wheat

processing project. The plant to be built will be able to produce 6 thousand tons

of dry gluten, 24.8 tons of wheat amylum and 9.2 thousand tons of feedstock

for animal husbandry. The projected production capacity is scheduled to be

reached in 2014.

EXPERT OPINION

EXPERT OPINION

21

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

In the Penza Region, the PenzaAgroBio Company is planning to build a plant for

the production of syrups, amylum, gluten and feedstock ingredients. The

overall announced cost is $154 mln; the annual production capacity is 240

thousand tons of raw stock. Almost all the categories planned for production

are currently being imported from other countries.

Last year, a German chemical company Evonik created a joint venture with the

Russian Agroindustrial Trust. The companies plan to build an amino acid plant

in the Rostov Region for $200 mln that will annually process 300 thousand tons

of wheat into lysine. The commissioning of the plant is scheduled for the late

2013 or early 2014.

The Agrico Holding already has a project for building two plants for deep

processing of sugar beet and corn. A foreign company will take part in the

project (its name, form of partnership, project share and other details are not

disclosed by Agrico). The company possesses the deep processing technology

and the expertise in building such plants. The construction of the first plant can

start this year. It will daily process 250 tons of corn receiving 50 tons of native

and 25 tons of modified amylum, 70 tons of glucose and maltose products and

50 tons of fructose as well as feedstock. 250 tons per day is the first stage. The

project envisages a second stage, which will double the production capacity

after commissioning. Agrico plans to offset the plant cost in 6-7 years.

Brewing Industry

It is one of the most well-developed grain processing industries (barley, malt).

The brewing industry in Russia exists in rather unfriendly conditions. On the one

hand, the business activities of the breweries are tightly regulated by the state,

given the aggravating alcohol abuse problem. The government is introducing

limitations year after year and increasing the excise tax. On the other hand, the

brewing industry faces competition from vodka and strong alcohol producers

who lobby their interest in the government and who do not want to surrender

their share in the domestic alcohol market.

Russia is the fourth world’s annual producer of beer, losing the leadership only

to the U.S., China and Brazil. In Q1 2012 Russia produced 180.7 million tons of

lager beer, which accounts for 92% of the previous year’s production from

January till March. The production decline in the start of the year is the reaction

of the industry to the 20% increase in the beer excise tax effective starting

January 1, 2012. Similarly, the industry reacted to the threefold increase of the

excise tax at the beginning of 2010, which also led to a significant increase in

the retail beer prices.

22

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

As per the results of Q1 2012, beer showed the worst production numbers as

compared to the other excised beverages, especially to strong alcohol. Thus,

the production of vodka increased by 6.8%, and cognac production by 3.3%.

Meanwhile, wine producers cut their production by 3.3%.

Starting July 1, 2012, new industry standards come into force. Beer producers

will have malt percentage in the beverage raw stock checked. The minimum

allowed percentage will be 50% and it will increase to at least 80% in a year.

Until now the compound has not been regulated by the legislation. The brewers

estimate a 10-15% growth in the product prices. The beer production standard

should bring Russia closer to the world’s recognized beer producers, Germany

and Czechia. Germans still have the “On Beer Purity” law being enforced which

only allows putting malt, hop and water in the traditional German beer. In

Czechia malt must constitute no less than two-thirds of the beverage

ingredients. In Russia the majority of the low and middle cost beer is brewed

using rice or corn.

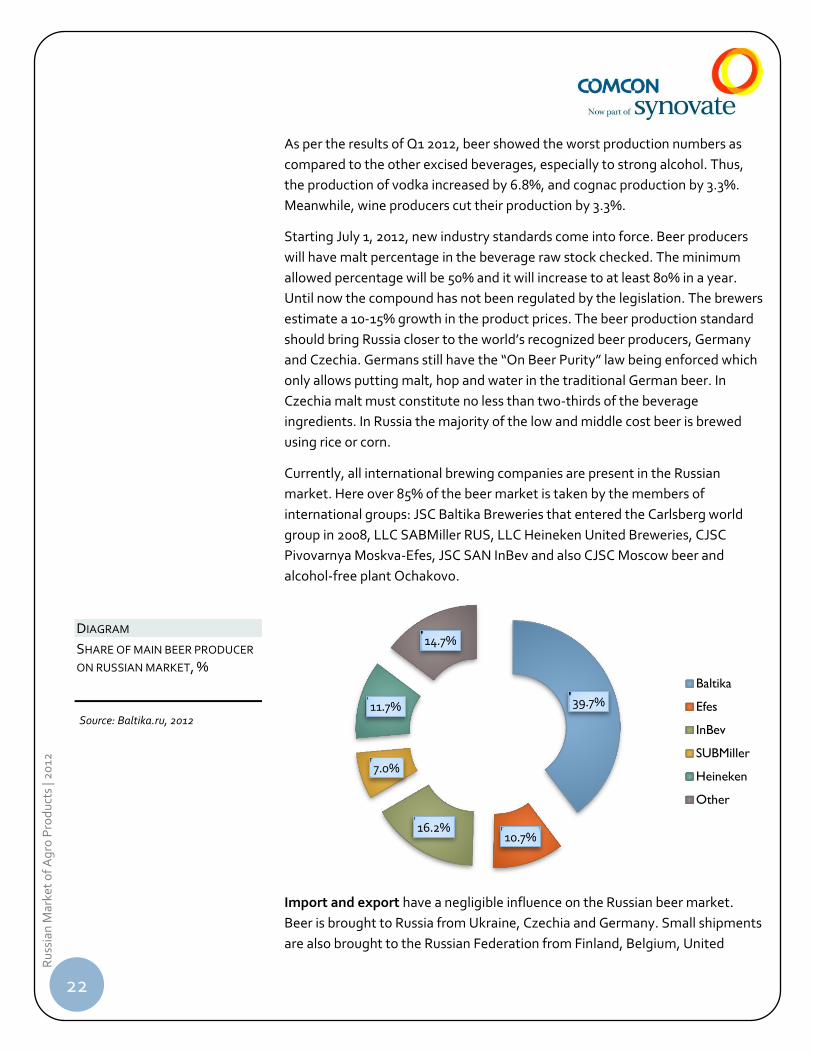

Currently, all international brewing companies are present in the Russian

market. Here over 85% of the beer market is taken by the members of

international groups: JSC Baltika Breweries that entered the Carlsberg world

group in 2008, LLC SABMiller RUS, LLC Heineken United Breweries, CJSC

Pivovarnya Moskva-Efes, JSC SAN InBev and also CJSC Moscow beer and

alcohol-free plant Ochakovo.

Import and export have a negligible influence on the Russian beer market.

Beer is brought to Russia from Ukraine, Czechia and Germany. Small shipments

are also brought to the Russian Federation from Finland, Belgium, United

39.7%

10.7% 16.2%

7.0%

11.7%

14.7%

Baltika

Efes

InBev

SUBMiller

Heineken

Other

DIAGRAM

SHARE OF MAIN BEER PRODUCER

ON RUSSIAN MARKET, %

Source: Baltika.ru, 2012

23

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

Kingdom and Ireland. The share of imported products in the beer market does

not exceed 3%. Less than 1% of the produced beer is exported abroad. The

main partners that import beer from Russia are the CIS countries: Kazakhstan,

Kyrgyzstan, Moldova, Ukraine and Abkhazia.

Over the last 10 years, the investments in the brewing industry have totaled

13.3 billion dollars. As claimed by the industry insiders, brewing companies

annually invest about 17 million dollars into their own agricultural projects in

Russia. Russian brewing companies own 16 malt production plants, and the

investments into the plants total 900 million dollars.

The beginning of year 2012 was marked by important corporate beer market

events, which speak of a positive evaluation of the Russian industry by the

foreign investors. Carlsberg, a Danish brewing company, announced its

intention to buy the remaining 15% of the Russian Baltika brand. The overall

deal amount for brining the share in the company to 100% is 6.5 billion Danish

crowns ($1.15 billion). The deal is associated with the successful results of the

corporate group in 2011.

In March 2012, according to the earlier agreements, PJSC Miller Brands,

Ukraine, changed ownership for Anadolu Efes, a member of the Anadolu

Group. According to the terms of the strategic alliance between SABMiller plc

and Anadolu Group created in the end of 2011, SABMiller transfers its assets in

Ukraine and Russia to Anadolu Efes. In its turn, Anadolu Efes transfers 24% of

its stock to SABMiller through increasing its equity share capital.

Oil-bearing Crops The principle oil-bearing crop, the sunflower, is raised in the forest steppe and

steppe belt of the country (Central Black-earth belt, Northern Caucasus).

In Russia the domestic market demand for sunflower seeds is almost

completely closed by the domestic production. The volume of the sunflower

market (and the oil-bearing crops market as a whole) has been dynamically

increasing over the last several years. This was instigated by the increase in the

consumption of the products derived from the sunflower, primarily by the food

industry; sunflower oil, mayonnaise sauces, soft margarines (dairy product

substitutes).

24

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

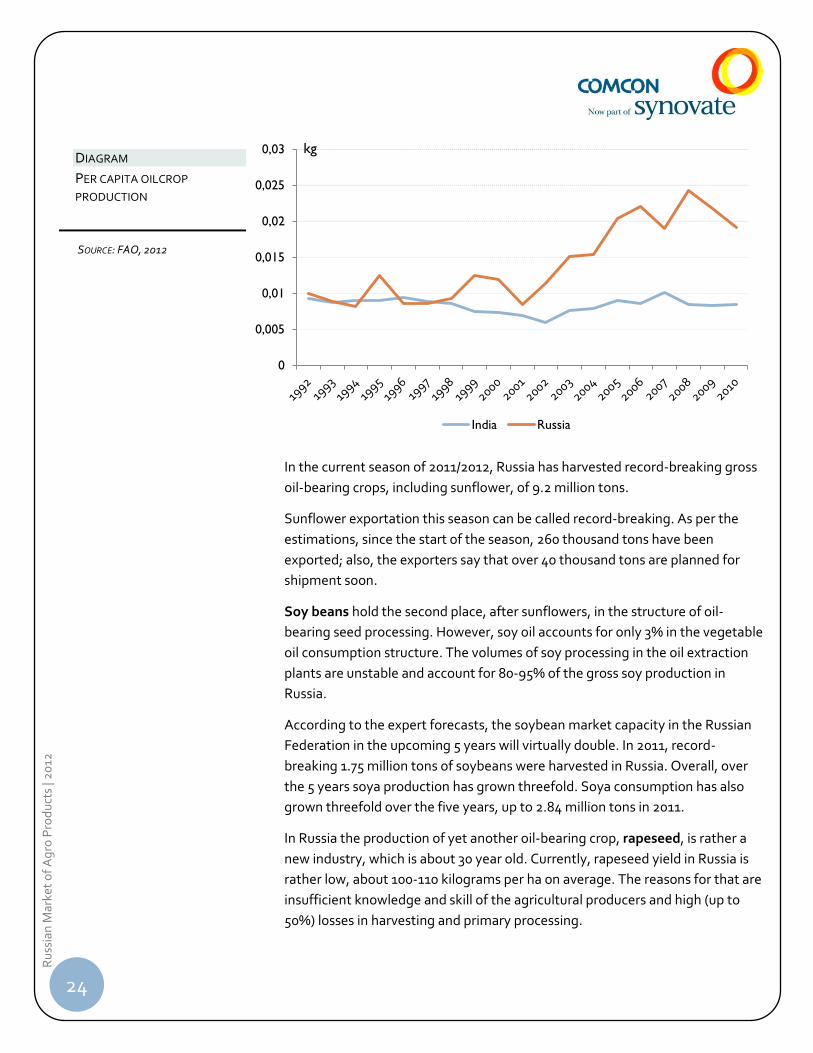

In the current season of 2011/2012, Russia has harvested record-breaking gross

oil-bearing crops, including sunflower, of 9.2 million tons.

Sunflower exportation this season can be called record-breaking. As per the

estimations, since the start of the season, 260 thousand tons have been

exported; also, the exporters say that over 40 thousand tons are planned for

shipment soon.

Soy beans hold the second place, after sunflowers, in the structure of oil-

bearing seed processing. However, soy oil accounts for only 3% in the vegetable

oil consumption structure. The volumes of soy processing in the oil extraction

plants are unstable and account for 80-95% of the gross soy production in

Russia.

According to the expert forecasts, the soybean market capacity in the Russian

Federation in the upcoming 5 years will virtually double. In 2011, record-

breaking 1.75 million tons of soybeans were harvested in Russia. Overall, over

the 5 years soya production has grown threefold. Soya consumption has also

grown threefold over the five years, up to 2.84 million tons in 2011.

In Russia the production of yet another oil-bearing crop, rapeseed, is rather a

new industry, which is about 30 year old. Currently, rapeseed yield in Russia is

rather low, about 100-110 kilograms per ha on average. The reasons for that are

insufficient knowledge and skill of the agricultural producers and high (up to

50%) losses in harvesting and primary processing.

0

0,005

0,01

0,015

0,02

0,025

0,03

India Russia

kg DIAGRAM

PER CAPITA OILCROP

PRODUCTION

SOURCE: FAO, 2012

25

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

In 2011 Russia harvested 6 million tons of corn and 1.1 tons of rapeseed,

showing an essential increase over 2010, a crisis year for agriculture, even

breaking the records for the rapeseed.

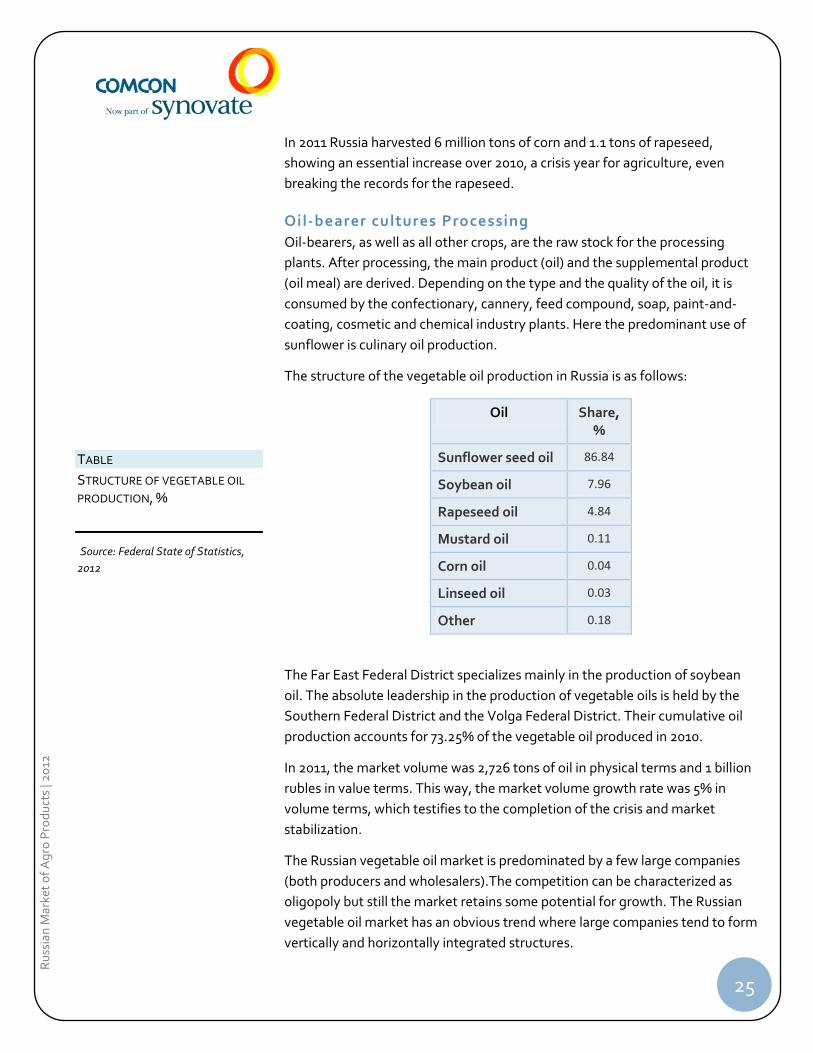

Oil-bearer cultures Processing

Oil-bearers, as well as all other crops, are the raw stock for the processing

plants. After processing, the main product (oil) and the supplemental product

(oil meal) are derived. Depending on the type and the quality of the oil, it is

consumed by the confectionary, cannery, feed compound, soap, paint-and-

coating, cosmetic and chemical industry plants. Here the predominant use of

sunflower is culinary oil production.

The structure of the vegetable oil production in Russia is as follows:

Oil Share, %

Sunflower seed oil 86.84

Soybean oil 7.96

Rapeseed oil 4.84

Mustard oil 0.11

Corn oil 0.04

Linseed oil 0.03

Other 0.18

The Far East Federal District specializes mainly in the production of soybean

oil. The absolute leadership in the production of vegetable oils is held by the

Southern Federal District and the Volga Federal District. Their cumulative oil

production accounts for 73.25% of the vegetable oil produced in 2010.

In 2011, the market volume was 2,726 tons of oil in physical terms and 1 billion

rubles in value terms. This way, the market volume growth rate was 5% in

volume terms, which testifies to the completion of the crisis and market

stabilization.

The Russian vegetable oil market is predominated by a few large companies

(both producers and wholesalers).The competition can be characterized as

oligopoly but still the market retains some potential for growth. The Russian

vegetable oil market has an obvious trend where large companies tend to form

vertically and horizontally integrated structures.

TABLE

STRUCTURE OF VEGETABLE OIL

PRODUCTION, %

Source: Federal State of Statistics,

2012

26

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

The five largest producers are represented exclusively by the Russia-renowned

brands: Aston Company with Zateya trademark, Bunge Ltd. with Ideal and

Zateya trademarks, WJ Group of companies with Milora trademark, Efko

company (Altero trademark) and also Yug Rusi (Zlata and Zolotaya Semechka

trademarks). The degree of the market consolidation is the highest in the

Russian oil production structure. Thus, in the largest segment (sunflower oil

production), the consolidation is minimal and is only 63%, while rapeseed oil is

in between, with 5 largest producers accounting for 72% of overall production.

For rapeseed oil, the set of 5 leaders is the same with the exception of Aston,

replaced by Ussuriysk MZhK with Maslava trademark.

The utilization of the oil processing plants’ production capacity is 60-65% on

average. Incomplete utilization is due to the seasonal character of oil-bearing

crops harvesting. The latter prevents all the industry plants from evenly

distributing the raw stock processing load within a year. Not all production-

capable facilities are effective, over a half of the facilities have outdated

equipment.

The main vegetable oils consumption sector is industry, which purchased 1,393

thousand tons of oils in 2010. 1,434 thousand tons of oils were sold via retail

outlets, and HoReCa account for 133 thousand tons. The industry consumes

large amounts of soybean, palm, coconut and rapeseed oil. In retail, mostly

olive and sunflower oil are sold. Sunflower oil accounts for about 70% of the

overall market turnover.

In Russia, there is a drastic growth in the production of deep-processed oils.

While in 2006 refined and hydrogenated oils only accounted for 41% of the

overall production, by 2010 the share of those was 60%. As the experts say, by

2015 the share of refined and hydrogenated oils in the overall vegetable oil

production volume will amount to 71%.

Imports and Exports

63% of vegetable oil produced by the Russian companies is sold domestically

and 37% is shipped abroad (it is mostly exported and it is mostly the sunflower

oil).

The imports of vegetable oil in 2011 were $1,188 million in value terms and

841.7 thousand tons in volume terms. Compared to the results of 2010 ($1,078

and 963.3 thousand tons), the imports grew by 10% in value terms, however,

declining in volume terms by 13%. Russia has mostly been importing palm and

coconut oil, the import volumes of those growing year after year.

____________________________

Source: «Analysis of the Russian

market of vegetable oils in Russia»,

2012, BusinesStat

____________________________

SOURCE: «ANALYSIS OF THE RUSSIAN

MARKET OF VEGETABLE OILS IN

RUSSIA», 2012, BUSINESSTAT

27

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

The main buyers of the Russian oils are Turkey (36 per cent) and Egypt (23 per

cent).

The 2011’s vegetable oils export volume was 1,349.1 million USD in value terms

and 1,127.2 thousand tons in physical terms. Compared to 2010 (803.9 million

and 892.1 thousand tons), the exports grew by 68% in value terms. Only a small

share of Russian-produced vegetable oil products is exported. However, in 2011

the supply of sunflower oil grew by 77% (in value terms) compared to the

previous year, also growing by 37% in physical terms.

----

When speaking about the grain and oil-bearer processing industry as a whole,

Russia is missing on the entire crops processing industries, and above all, the

production of fuel ethanol. Without this sort of processing, the agricultural

producers do not have a high demand outlet, and the cattle farming industry

lacks a cheap protein concentrate, hence being less competitive. This results in

the high volatility of the balance numbers. The weakness of the processing

industry renders the market volatility – the superfluous yield makes the prices

collapse and forces into performing purchasing interventions.

Vegetable Crops Over the last decade, vegetable market in Russia has shown a steady growth

despite serious problems in the industry.

In 2010, a draught had a strong impact on the industry cutting down the

resulting numbers by 20% by the end of the year.

On the contrary, in 2011 Russia harvested record-breaking vegetable crops,

which has caused the domestic prices on the main vegetable items to collapse,

leading to the market oversaturation. As per the experts’ estimation, potato

crop yield surpassed the 2010’s numbers by 25-27%, cabbage yield grew 10-

12%, and carrot and beetroot yield increased 5-7%.

____________________________

Source: AIC, “INFORM”

28

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

“The main characteristic of the current season is the overproduction of potato

crops and vegetables of the “beetroot soup set”, which has instigated a massive

drop in the involved products’ prices. We have survived the production crisis

multiple times, and it happens in the horticultural industry once in 2-3 years on

average. However, this season will be unprecedentedly hard for the producers who

have invested the capital they have been accumulating for the last two seasons

into storage construction; and quite a lot of farmers have done it. Taking into

account the negative potato and vegetable crops price estimation for the second

half of the season, we cannot even speak about the return of these investments.”

“Next season we are expecting a drastic cut in the potato and all “beetroot soup”

(cabbage, onions, beetroot, carrot) vegetable crops production. Many farmers just

cannot raise the same volume of vegetables as this year due to large financial

problems. No doubt, this will lead to increased prices, and the vegetables will be

undoubtedly more expensive than this year.”

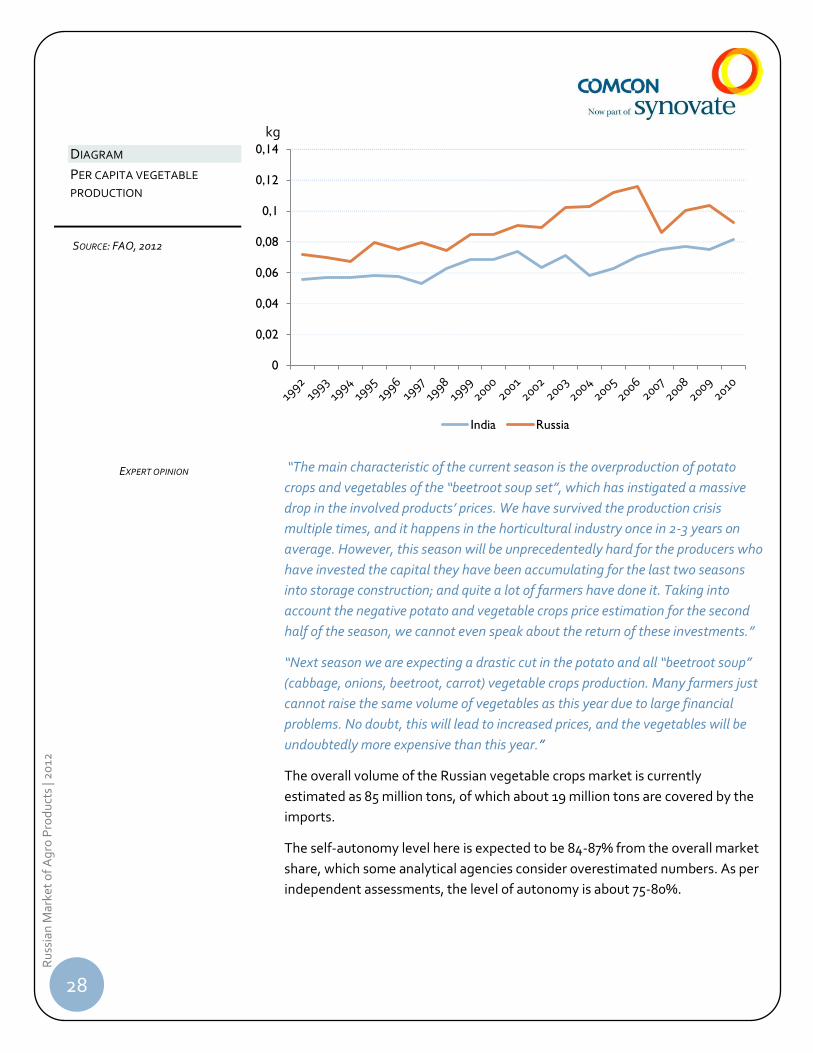

The overall volume of the Russian vegetable crops market is currently

estimated as 85 million tons, of which about 19 million tons are covered by the

imports.

The self-autonomy level here is expected to be 84-87% from the overall market

share, which some analytical agencies consider overestimated numbers. As per

independent assessments, the level of autonomy is about 75-80%.

0

0,02

0,04

0,06

0,08

0,1

0,12

0,14

India Russia

kg

DIAGRAM

PER CAPITA VEGETABLE

PRODUCTION

SOURCE: FAO, 2012

EXPERT OPINION

29

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

A large share in the vegetable raising market is occupied by the numerous

private farms (71%); large companies only accounting for 17.1%, and

professional farmers contributing 11%.

Currently, by rough estimations the total volume of the Russian vegetable crops

market is $50 billion in value terms, the imports accounting for $1 billion, and

the exportation from Russia is approximately $37 mln, all figures calculated per

annum. The largest share in the imports is taken by tomatoes (40%) followed

by onions and garlic. The largest exporters of tomatoes into Russia are Turkey

and China, and the rest of the vegetables are mainly imported from the EU

countries, mostly Germany and the Netherlands.

“We buy tomatoes as well, since growing tomatoes domestically is currently very

expensive. Buying readymade tomato paste from China or Uzbekistan is way

cheaper.”

As per the experts’ opinion, the largest shares in the export market are taken by

potato crops (54%). Russia exports most of the potato production into

Azerbaijan and Kazakhstan. Overall, 90 to 95% of total exports go to the near-

abroad countries.

As of today, the principle amounts of vegetable crops are produced in the Volga

Federal District (2.7 million tons on average in the last three years, accounting

for 21% of the total production in Russia), the Central Federal District (2.6

million tons or 20,3%), the Southern Federal District (2.5 million tons or 20%),

the Siberian Federal District (1.6 million tons or 13%), North Caucasus Federal

District (1.6 million tons or 12%).

Processing (Vegetable Conservation)

From 2006 through 2010, the value volume of the vegetable conservation has

grown by 52%, from $2.7 to 4.1 billion. The value volume of canned vegetable

sales has been growing at a rate far exceeding the market growth in terms of

volume. This outrunning growth has been due to the fast increase in the canned

vegetables’ prices: from 2006 through 2010 the mean price of 1 kilogram of

canned vegetables has grown by 50%, from $2.96 to 4.5.

In 2010 the volume sales of canned vegetables reached 906 thousand tons.

Here, the capacity of the canned vegetables market in 2010 amounted to 2.3

million tons. This difference between the market volume and the capacity in

Russia is explained by the presence of homemade canned vegetables. In other

words, a part of the preserves is made from homegrown vegetables and such

EXPERT OPINION

____________________________

SOURCE: «ANALYSIS OF THE RUSSIAN

MARKET OF CANNED VEGETABLES»,

2011, BUSINESSTAT

30

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

preserves are not reported in the sales. About 1.4 million tons of canned

vegetables are produced in the Russian households annually.

The experts believe that this market stands out for its high competition. The

largest players are Bonduelle, Le Group CECAB, the owner of the Globus and

D'aucy trademarks, and EKO, a producer from Hungary. Among the domestic

producers, the leadership is held by Baltimor.

Currently, the Russian market of canned vegetables largely relies on imports. In

2010 the supply of canned vegetables included 373.6 thousand tons of domestic

production and 593.7 of imports. In the perspective, the share of imported

canned vegetables will decrease and will account for 51.5% of overall supply in

2015.

“Refreshment salads include 80% of domestically produced ingredients;

peas/corn: 50% are imports. If we take Siberia and the area east of the Urals, it is

on the Chinese (or sometimes Thai) imports. They do not have plants there at all.

Central Russia is 50/50. Kamchatka is 80% on imports.”

The producers have an acute lack of domestically produced raw stock. The

possibilities of raising raw stock crops domestically are hindered by the

authorities.

“Virtually no one is raising it, except for Bonduelle. They don’t have enough supply

and they are still buying, even from us. Very few have their own farmholds.”

“Some simply do not have a possibility to enter into a region and acquire farmland.

No one would sell. At best, this would be long-term rental, for 49 years. When you

come to a region without having connections with the authorities, it means you

are bound to fail. No one will support you. The only attention you will get is that of

the tax authorities and the fire safety inspections that will constantly fine you

(hidden corruption). You will need to be on friendly terms with the local

authorities, and not many are on those.”

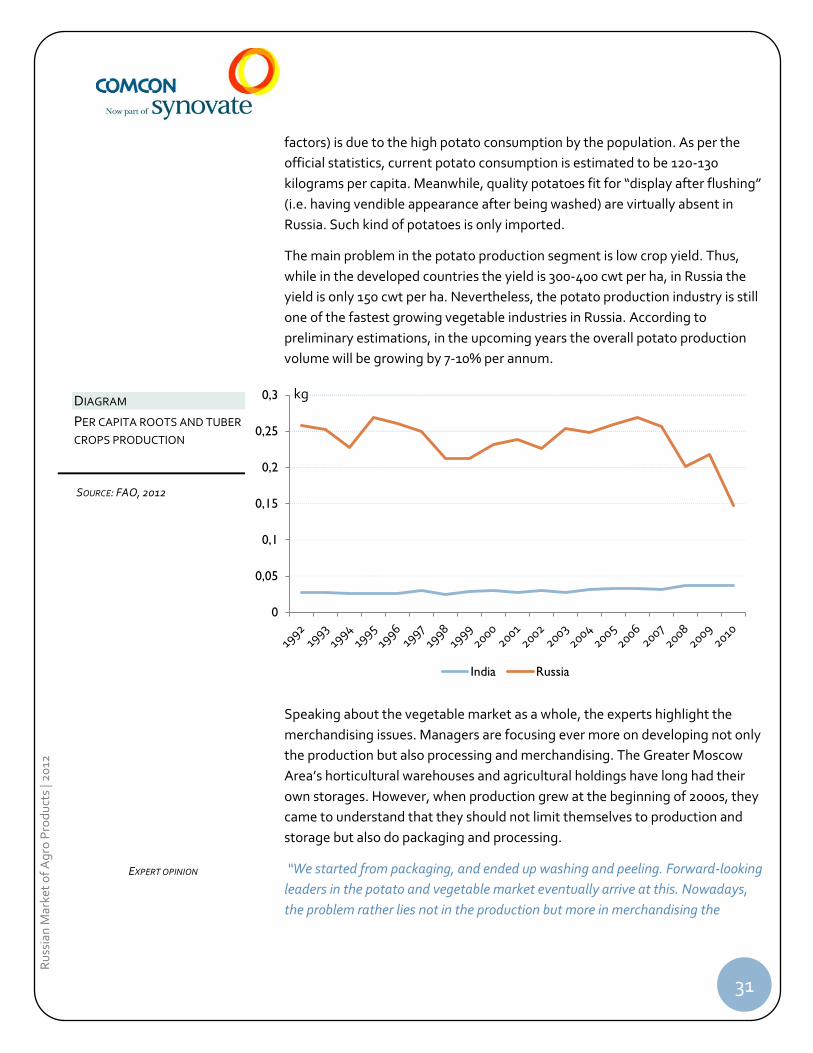

Potato Crops

Potatoes are essential food and feedstock crops produced by the vegetable

and gourd raising industry. Potatoes are referred to as “the second best bread”

in Russia. These crops are ubiquitously seeded, the largest part, however, is

located in the Central Russia and also near the cities where vegetable raising is

being developed.

Russia is currently producing about 34 million tons of potatoes per annum,

being the second largest potato producer after China. This (among other

EXPERT OPINION

EXPERT OPINION

31

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

factors) is due to the high potato consumption by the population. As per the

official statistics, current potato consumption is estimated to be 120-130

kilograms per capita. Meanwhile, quality potatoes fit for “display after flushing”

(i.e. having vendible appearance after being washed) are virtually absent in

Russia. Such kind of potatoes is only imported.

The main problem in the potato production segment is low crop yield. Thus,

while in the developed countries the yield is 300-400 cwt per ha, in Russia the

yield is only 150 cwt per ha. Nevertheless, the potato production industry is still

one of the fastest growing vegetable industries in Russia. According to

preliminary estimations, in the upcoming years the overall potato production

volume will be growing by 7-10% per annum.

Speaking about the vegetable market as a whole, the experts highlight the

merchandising issues. Managers are focusing ever more on developing not only

the production but also processing and merchandising. The Greater Moscow

Area’s horticultural warehouses and agricultural holdings have long had their

own storages. However, when production grew at the beginning of 2000s, they

came to understand that they should not limit themselves to production and

storage but also do packaging and processing.

“We started from packaging, and ended up washing and peeling. Forward-looking

leaders in the potato and vegetable market eventually arrive at this. Nowadays,

the problem rather lies not in the production but more in merchandising the

0

0,05

0,1

0,15

0,2

0,25

0,3

India Russia

kg DIAGRAM

PER CAPITA ROOTS AND TUBER

CROPS PRODUCTION

SOURCE: FAO, 2012

EXPERT OPINION

32

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

product to the consumer.”

Still, the production of biofuel from the potatoes is deemed low-perspective by

the experts.

“Here, the issue lies in the breeds, the GMO, because raising culinary potatoes for

ethanol makes no sense. Also, it makes no sense to promote bioethanol as a

competitive fuel in a petroleum producing country, when there’s Brazil with the

U.S. as a potential marketing outlet and sugar cane that’s cheap, next to being

completely free to produce.”

However, the experts note a high potential of processing the product into

amylum, provided that modern technologies and quality standards apply.

“Processing into amylum is another pair of shoes. The potential for the processing

market is huge. For example, in the Greater Moscow Area, mayonnaise producers

buy imported amylum since there are no domestically produced offers of required

quality. We do not have our own technologies, so we need to acquire and develop

those from abroad.”

Ethanol and ethyl alcohol Industry

A part of the processed raw stock potatoes (and a part of grain raw stock, to a

lesser extent) is used in producing ethanol. This industry is tightly regulated

and supervised by the state.

From 2007 till 2011, the demand for ethanol in Russia dropped by almost 6%:

from 895 down to 843 million liters. The greatest decline (by almost 6%) in the

demand was recorded in 2009.

As the liquor and ethyl alcohol s industry is the largest consumer of ethanol and

ethyl alcohol in Russia, the marketing experts note the changes in the

customary ways of alcohol consumption to be among other reasons behind the

decline in the demand for ethanol. The demand for strong alcohol is

decreasing, while the consumption of low-alcohol beverages, beer and cocktails

displays a growth.

In 2011, the number of ethanol production plants has substantially decreased:

while by the beginning of the year, there were about 100 licensed plants, only

69 remained by the end of year after a license re-issuance. The experts reckon

that the state is thus regaining control over the industry and pushes away small

EXPERT OPINION

EXPERT OPINION

EXPERT OPINION

33

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

regional players. The authority representatives declare that it is only the first

stage in the population ‘de-alcoholization’ program.

“Market monopolization – for both vodka and ethanol production – is on the way.

The state is consciously taking steps to eliminate the producers.”

Region Owners

Production

in January-

September

2011

Change to

the similar

period of

2010 (%)

Mark

et

share

(%)

Zernoproduct Tula

Region

Centrol Ltd

(Beliz)

2.4 2.3 9.3

Spirtovoy

Kombinat

Kemerovo

Region

No data 2.2 8 8.8

Tulaspirt

(alcohol plant

Pavlovskiy)

Tula

Region

No data 2.2 13.7 8.7

Bashspirt Bashkiria Ministry of the

land property

of

Bashkortostan

1.7 -7.5 6.8

Tatspirtprom Tatarstan Ministry of the

land property

of

Bashkortostan

1.7 9.4 6.7

Total market 25.3 -8.3 100

In the Russian market, ethanol is mostly sold via the domestic outlets. In 2007-

2011, the share of the domestic sales in the demand structure fluctuated up to

99% in 2007 and up to 95%, in 2011.

Indicator 2006 2007 2008 2009 2010

Import(mln $) 8.9 0.0 0.0 21.9 5.2

Dynamics of import (%

previous year)

- -99.5 - - -76.4

TABLE

MAJOR PLAYERS IN THE

MARKET OF ALCOHOL

SOURCE: COMMERSANT, 10.11.2011

TABLE

ETHANOL IMPORTS

SOURCE: ETHANOL MARKET ANALYSIS

IN 2007-2011, BUSINESSTAT

____________________________

SOURCE: ETHANOL MARKET ANALYSIS

IN 2007-2011, BUSINESSTAT

34

Ru

ssia

n M

arke

t o

f A

gro

Pro

du

cts

| 20

12

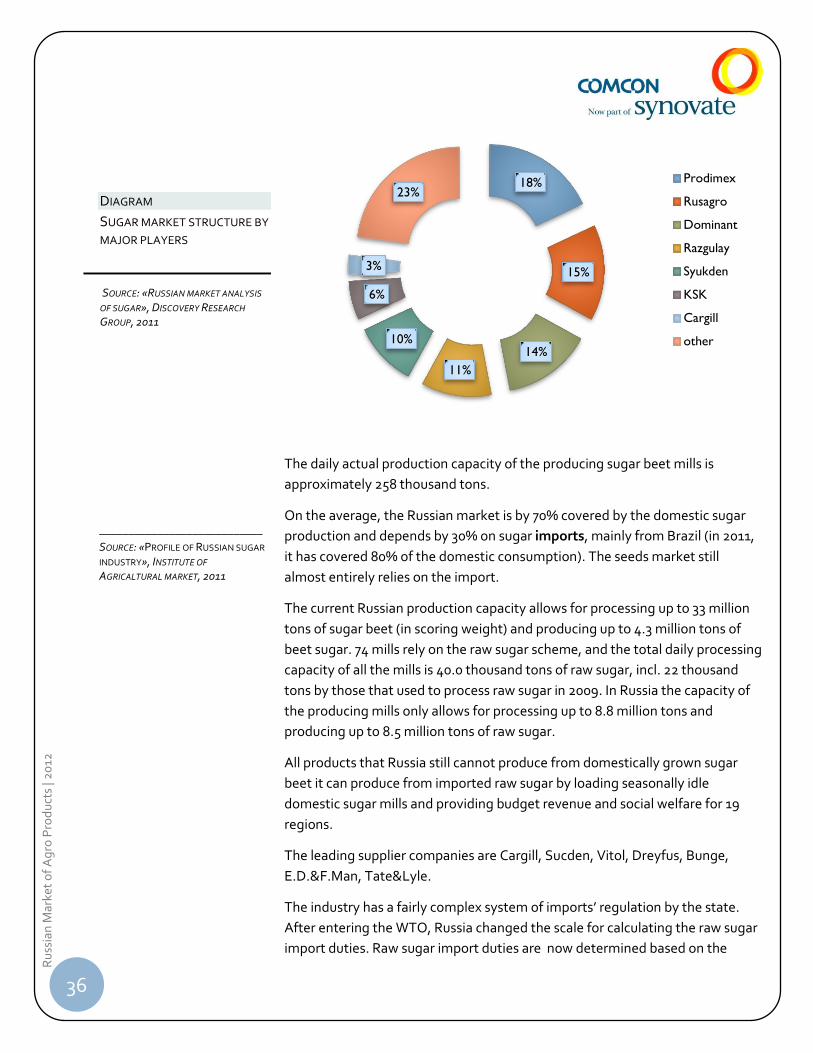

Sugar Industry

In the Russian Federation, sugar beet is one of the principal industrial crops

providing root crops rich in carbohydrates that are used to produce sugar. In

storage or in transportation, sugar beet quality is swiftly deteriorating, so sugar

mills are located close to the raw stock sources.

Overall, about 20 regions of the Russian Federation are seeding sugar beet, and

those are where the sugar mills are located. Clearly, we can highlight two belts

of the sugar industry in Russia: the northern one that pierces the Central Black-

earth Belt and Volga Region up to the Cis-Urals region (Bashkiria) and the