Embed Size (px)

Citation preview

2/5/2018

1

Sales and Use Tax for Manufacturers

February 2018Minnesota Business Tax Education

Disclaimer

This presentation is for educational purposes only. It is meant to accompany an oral presentation and not to be used as a standalone document.

This presentation is based on the facts and circumstances being discussed, and on the laws in effect when it is presented. It does not supersede or alter any provisions of Minnesota laws, administrative rules, court cases, or revenue notices.

If you have any questions, contact us at [email protected] , 651-296-6181, or 1-800-657-3777 (toll-free).

Minnesota Business Tax Education ProgramProviding education opportunities about Minnesota tax laws.

2

Introduction

This class is intended for businesses that make products intended to be sold ultimately at retail.

3

2/5/2018

2

Tell us about yourself …

Your name

Business and/or industry

What you do at your business relating to sales/use tax

Business location (city)

List the resources available to help answer my sales and use tax questions

4

Course Objectives

After completing this class you will: Recognize when you owe sales or use tax

Recognize the differences between the “industrial production process” and the “integrated production process”

Identify the exemptions available to manufacturers

Distinguish how the use of an item determines if it qualifies for an exemption

Identify how to use and accept exemption certificates

Identify when you have paid tax in error and how to get a refund

List the resources available to help answer sales and use tax questions 5

Part 1

Sales and Use Tax Basics

6

2/5/2018

3

Sales and Use Tax Basics

Tax charged by the seller

Applies to retail sales of

Most tangible personal property

Some services and

Some digital products

Made in (or sourced to) Minnesota

7

What is sales tax?

Sales and Use Tax Basics

Complement to sales tax

Self-assessed

Paid directly to the state

Applies to taxable purchases when sales tax was not charged

8

What is use tax?

Sales and Use Tax Basics

9

Sales and Use Tax is a Transaction Tax

2/5/2018

4

6.875%

Sales and Use Tax Basics

10

What is the tax rate?

Sales and Use Tax Basics

Sourcing determines where the sale takes place and which taxes are imposed on the sale.

.

Minnesota Statutes 297A.668 and 297A.669

11

1. Seller’s Address (if that’s where title to or possession of item takes place)

2. Delivery Address (if item is shipped or delivered to customer or where service is performed)

3. Billing Address(based on the address that the seller has in their records for the customer)

How do I determine what taxes apply to the sale?

Sourcing rules for leases or rentals of TPP

Sales and Use Tax Basics

1st PaymentGeneral Sourcing

Rules

(where transfer of property

occurs)

Subsequent Payments

Primary Property Location

(address provided to

lessor by lessee)

How do I determine what taxes apply to the sale?

12

2/5/2018

5

Sales and Use Tax Basics

Operating Lease vs. Capital Lease

CharacteristicsOperating Lease (Rental Agreement)

Capital Lease (Financing Agreement)

What is being transferred? Transfer of possession only; not title

Transfer of title upon possession or at the end of the lease agreement

Who owns property at the end of the lease?

Lessor owns property but lessee generally has a nominal buy-out option

The customer is required to buy the item at the end of the lease agreement

When is tax charged? Applied to each lease payment

Due up front13

What is a lease?

Type of Labor Examples Is it taxable?Repair labor Car repair

Equipment repair Calibrating equipment Sharpening tools

Construction labor Build an office building Kitchen remodel

Fabrication labor Custom sawing Bending sheet metal

Installation labor Computer equipment Modular furniture

Sales and Use Tax Basics

No (if separately stated)

Yes

Yes

No

14

When is labor taxed?

Sales and Use Tax Basics

When are repair and maintenance contracts taxed?

15

Type of Contract Is the contract taxable?Optional maintenance contracts (bundled – one nonitemized price)

Yes. Tax is due when the contracted maintenance is sold.

Optional maintenance contracts (unbundled – separate itemized prices)

No. The service provider charges sales tax to the customer on the taxable items when the repair is performed.

Extended warranty contracts No. The service provider owes tax on the parts provided under the contract.

2/5/2018

6

Part 2

Overview of Sales and Use Tax for Manufacturers

16

Manufacturing Overview

Who are manufacturers?Anyone who creates a tangible product to be sold ultimately at retail is considered a manufacturer. Examples include: Crafters Fabricators Miners Paper mills Refiners

Note: Making prepared food does not qualify.

17

Manufacturing Overview

Our primary focus is to explain: The Industrial Production Process

- What qualifies for the Industrial Production Exemption

The Integrated Production Process- What qualifies for the Capital Equipment Exemption

18

2/5/2018

7

19

Overview of Sales and Use Tax for Manufacturers

Industrial Production is the process of taking raw materials out of inventory and creating a product intended to be sold ultimately at retail.

The Integrated Production Process involves a series of activities that result in making a product intended to be sold ultimately at retail.

19

Production Flow

Raw Materials

Manufacturing Overview

Distribution

Industrial Production Process

Integrated Production Process

Production

20

Part 3

Pre-production

21

2/5/2018

8

Pre-Production

Items used or consumed in R & D activities

Purchases of prototypes or materials used to make prototypes

Machinery, equipment and tools used primarily in R & D activities

22

Research & Development (R & D)

3D CAD Design Engineering Software 23

Consumable materials (which would also include electricity) used to create your prototype on a 3D printer.

24

2/5/2018

9

Pre-Production

What items do you use in R & D activities that may qualify for an exemption?

25

Pre-Production

Exempt purchases include: Component parts and ingredients of a product (inventory)

Taxable purchases include items used to: Receive raw materials

Store or preserve raw materials before the production process begins

Facilitate loading, unloading, handling, transportation or storage of products before the manufacturing process begins

26

Managing Raw Materials

Pre-Production

Examples of taxable purchases:A forklift or industrial crane used primarily for raw materials management.

27

2/5/2018

10

Pre-Production

Examples of taxable purchases: The propane used in the forklift that is used primarily for raw materials management. Shelving or storage bins used to store raw materials inventory.

28

Pre-Production

Do you have any items you use in raw materials inventory at your facility that may qualify for the capital equipment exemption?

29

Pre-Production

Do you have items consumed in raw materials inventory that you should verify that you are not claiming the industrial production exemption?

30

2/5/2018

11

31

Please be back in 10 minutes.

Part 4

Production of the Product

32

Production of the Product

Where does the production process BEGIN?

The production process begins with the removal of raw materials from inventory.

This is true for both the:

Integrated production process and

Industrial production process

33

Start of the Production Process

2/5/2018

12

Production of the Product

Exempt purchases include: Industrial production exemption (M.S. 297A.68, Subd. 2)

Items used or consumed in production Utilities Product packaging

Separate detachable units

Capital equipment exemption (M.S. 297A.68, Subd. 5)

Special tooling (M.S. 297A.68, Subd. 6)

34

Production Activities

Production of the Product

Propane and industrial gases used in production

35

Production of the Product

Petroleum products and lubricants used in production equipment36

2/5/2018

13

Production of the Product

Utilities used to operate equipment, machines and tools that are used directlyin the industrial production process (e.g. electricity, water, and gas.)

37

Production of the Product

Materials that directly affect the product 38

Short-lived accessory items for qualifying capital equipment that have a direct affect on the product

Production of the Product

39

2/5/2018

14

Production of the Product

Capital Equipment ExemptionExempt purchases include equipment and machinery that Are essential to producing the product

Perform an indispensable phase/stage in production

Are used in Minnesota

Are used at least 50% of the time in production

Produce a product ultimately sold at retail

Regulatory Equipment ≠ Essential Equipment 40

Printing press 41

Laser cutter 42

2/5/2018

15

Plastic injection molding machine

43

Metal lathe 44

Turn-key line machine 45

2/5/2018

16

Food processing equipment

46

47

Meat slicer

47

48Key duplicating machine

2/5/2018

17

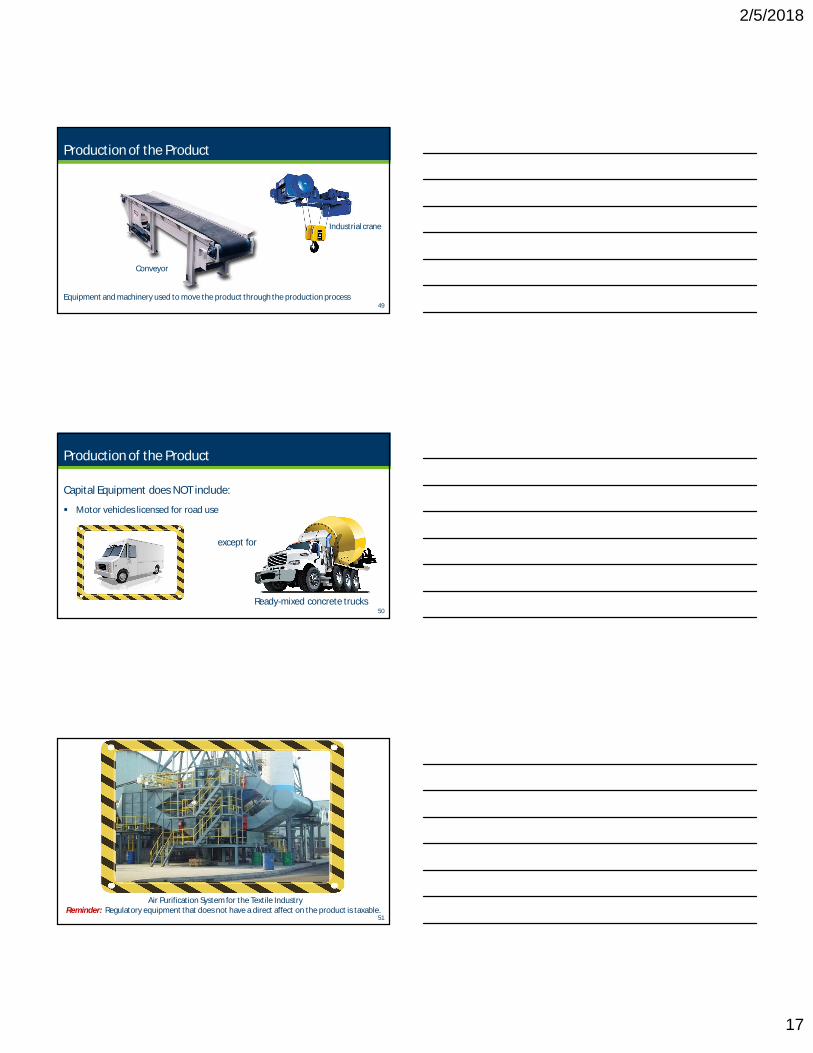

Production of the Product

Equipment and machinery used to move the product through the production process

Conveyor

Industrial crane

49

Ready-mixed concrete trucks

Production of the Product

Capital Equipment does NOT include:

Motor vehicles licensed for road use

except for

50

Air Purification System for the Textile IndustryReminder: Regulatory equipment that does not have a direct affect on the product is taxable.

51

2/5/2018

18

Production of the Product

Capital Equipment ≠ Capital Assets

The term “capital equipment” is not the same as capitalized assets.

Items capitalized for accounting purposes do not automatically qualify as capital equipment.

Items that you expense for accounting purposes, such as leased equipment, may be considered “capital equipment."

52

Production of the Product

Special Tooling Exemption

Exempt purchases

Dies, jigs, patterns, gauges, and other special tools that have value and use only for the buyer and use for which they are made.

Note: Materials purchased to make your own special tooling are taxable because “materials” are not “special tools."

53

Production of the Product

What equipment do you have that may qualify for the special tooling exemption?

54

2/5/2018

19

Production of the Product

Industrial shelving used to store work-in-progress 55

Storing Work-in-Progress

Reusable items used for handling or moving materials through production may qualify for the capital equipment exemption.

Note: Reusable items used to store raw materials along the production line do not qualify for the industrial production exemption or the capital equipment exemption.

Production of the Product

56

Storing Work-in-Progress

Production of the Product

Do you have any items you use at your facility to store work-in-progress that may qualify for an exemption?

57

2/5/2018

20

Production of the Product

Exempt purchases Outsourced fabrication services that are essential to producing their product.

58

Outside Fabrication Labor

Production of the Product

Does your company subcontract with another business to perform fabrication labor for you?

If so, are there any items you can claim an exemption for that are used at their plant?

59

Production of the Product

Exempt purchases

Quality control and testing activities done on the product

Calipers – used to measure thickness of an item60

Quality Control and Product Testing

2/5/2018

21

Laboratory equipment and supplies 61

Disposable lab testing supplies

Disposable latex and vinyl gloves

(suitable for general use)

62

Dust Collector (Vacuum)

Equipment that performs a quality control function and has a direct affect on the product is exempt.

63

2/5/2018

22

Production of the Product

Do you have any items used in quality control that may qualify for an exemption?

64

Production of the Product

Exempt purchases A structure within the integrated production process

Serve or perform a function essential to the production process, and

Used in producing products intended to be sold ultimately at retail

65

Special Purpose Buildings

66

Clean room

66

2/5/2018

23

Paint booth

67

Production of the Product

Exempt Purchases Product packaging

Nonreturnable internal packaging materials that shape, form, stabilize and protect the contents

68

Product Packaging

Production of the Product

Exempt Purchases

Warranty cards

Owners manuals

Content lists

Instruction sheets

Material safety data sheets

69

Product Packaging

2/5/2018

24

Production of the Product

Exempt Purchases Product identification labels (e.g.

combination labels that identify the product and price for customers)

Expiration date labels (includes stickers or ink for labeling)

70

Product Packaging

Production of the Product

Taxable Purchases Returnable containers such as steel drums,

barrels, bottles, gas cylinders, boxes, tanks, sacks, cans (except when used to package food and beverages)

71

Product Packaging

Production of the Product

Do you have any taxable product packaging?

72

2/5/2018

25

Production of the Product

Where does the production process END?

In general, the industrial production process ends with the placement of the product in finished goods inventory.

vs. The integrated production process ends when the last process prior to loading

for shipment has been completed.

73

End of the Production Process

Please be back in 10 minutes.

Part 5

Post-Production

75

2/5/2018

26

Post-Production

Taxable purchases

Items used primarily to facilitate loading, unloading, handling, transportation or storage of products after the manufacturing process ends.

Fuel to operate the equipment after the industrial production process ends. 76

Finished Goods Inventory (or Warehousing)

Industrial shelving used in finished goods inventory does NOT qualify.

77

Post-Production

Exempt purchases

Equipment used to maintain conditions in finished goods (e.g. refrigerators, freezers, etc.)

Taxable purchases

Utilities used in the equipment that maintains the conditions in finished goods.

78

Finished Goods Inventory (or Warehousing)

2/5/2018

27

Post-Production

Do you have any items used in finished goods inventory that may qualify for the capital equipment exemption?

79

Post-Production

Are there items consumed in finished goods inventory that you should verify that you are not claiming the industrial production exemption on?

80

Finished Goods Inventory (or Warehousing)

Post-Production

Disposal of scrap is outside the production process.

The equipment, machinery, and other items used to dispose of the scrap is taxable unless the scrap is:

Reused in the production process (i.e. “closed loop system”)

Used to make a different product that is ultimately sold at retail

81

Disposal of Scrap

2/5/2018

28

Post-Production

Have you incorrectly claimed the capital equipment exemption on any equipment and machinery used to dispose of scrap and waste?

82

Post-Production

Are there any circumstances in your production process where equipment used to dispose of scrap qualifies for the capital equipment exemption?

83

Post-production

Exempt Purchases include: Nonreturnable pallets and skids

Nonreusable external packaging materials

84

Shipping and Distribution

2/5/2018

29

Post-production

Exempt Purchases include: Dunnage that protects, braces, pads,

or cushions against damage

Stuffing materials such as straw, dry ice, shredded paper, cotton batting, “packing peanuts”, etc.

85

Shipping and Distribution

Post-production

Exempt purchases include: Strapping machine

Wrapping materials such as paper or plastic wrap, wire, tape, staples, etc.

Taxable purchases include: Forklifts and industrial cranes used

primarily in shipping and distribution

Strapping Machine86

Shipping and Distribution

87

Industrial cranes

87

2/5/2018

30

Post-Production

Taxable purchases include:

Returnable containers and packaging (except for food manufacturers)

Returnable skids and pallets

88

Shipping and Distribution

Post-Production

Taxable purchases include:

Address labels, invoices, packing slips, and envelopes

89

Shipping and Distribution

Post-Production

Taxable purchases include:

Warning labels that give shipping directions

90

Shipping and Distribution

2/5/2018

31

Post-Production

Are there items you buy from your vendors without sales tax that are used in shipping and distribution that you need to accrue use tax on?

91

Part 6

Production Support

Functions

92

Production Support Functions

Exempt purchases Equipment, machinery, and tools

used to construct, maintain, and repair qualifying capital equipment

Taxable purchases

Items used or consumed in these activities do not qualify for the industrial production exemption

93

Tool Room Operations

2/5/2018

32

94

Production Support Functions

Taxable purchases include items used for:

Internal product and production tracking

Inventory management

Production analysis

95

Production Administrative Support

Production Support Functions

Taxable purchases include items used for:

Protective equipment

Clean room apparel and equipment (reusable and disposable)

96

Protective and Safety Items

2/5/2018

33

Protective safety clothing 97

Production Support Functions

Taxable purchases include:

Sprinkler system components

Fire alarm monitoring

First aid kits and eye wash stations

98

Fire Prevention, First Aid, and Hospital Stations

Production Support Functions

Taxable purchases include utilities used to:

Heat the manufacturing facility in the winter

Cool the plant in the summer

Provide overhead lighting on the production floor

99

General Heating, Cooling, and Lighting

2/5/2018

34

Production Support Functions

Did you include general heating, cooling, and lighting in your utility exemption percentage?

100

Production Support Functions

Items that do not qualify for exemption include:

Dust Collections Systems

Emission control systems

Welding ventilation systems

101

Pollution Control, Prevention, and Abatement

Production Support Functions

Exempt purchases

Chemicals

Materials

Supplies

Taxable purchases

Equipment and machinery

102

Waste Treatment

2/5/2018

35

Production Support Functions

Are there items consumed in treating waste that you should verify that you are claiming the industrial production exemption?

103

Part 7

Administrative Support

Functions

104

Administrative Support Functions

Examples of administrative activities include: Customer service activities

General office administration

Managerial functions

Taxable items used to perform these activities include: Furniture

Office equipment and supplies

Prewritten computer software

Training materials and supplies

105

General Administrative Activities

2/5/2018

36

Computer

Computer Printer

106

Administrative Support Functions

Taxable purchases:

Chemicals and cleaning agents used to clean: Production tools and equipment (except food processing equipment)

Areas around food processing equipment

Buildings and other structures

Janitorial cleaning materials and services

Materials used to construct or remodel real property107

Building Cleaning and Maintenance

Pressure Washer 108

2/5/2018

37

Administrative Support Functions

Taxable purchases:

PA systems

Telecommunications equipment and services

Two-way radios

109

Communications

Administrative Support Functions

Taxable purchases:

Business cards Coffee mugs, key chains, and pens Order forms Point of sale displays

110

Sales Operations

Administrative Support Functions

Taxable purchases:

Employee security services Plant security Security access equipment and badges Security system maintenance and monitoring

111

Security

2/5/2018

38

Part 8

Exemption Certificates

112

Exemption Certificates

All sales of tangible personal property and taxable services are taxable unless:

The item is exempt by Minnesota Statutes, or

The purchaser provides the seller with a completed exemption certificate

113

Do I need an exemption certificate?

Exemption Certificates

The following are examples of use-based exemptions:

Capital equipment Industrial production/manufacturing Utilities used in production

114

Use-based exemptions

2/5/2018

39

The green boxes identify the fields that are required for a complete exemption certificate.

The purchasing agent must retain the contract as supporting documentation.

The seller’s information is not required but it doesn’t hurt to complete these fields.

Jane Smith

115

Exemption Certificates

Certificate of Exemption, Form ST3(Minnesota Department of Revenue form)

Certificate of Exemption, Form F0003 (Streamlined Sales Tax form)

Uniform Sales and Use Tax Certificate (Multistate Tax Commission form)

Other state’s exemption certificates (if all required elements are included)

Self-prepared exemption certificate (if all required elements are included) 116

Different Types of Exemption Certificates

Exemption Certificates

Required elements for a complete exemption certificate:

Purchaser's name and address

Purchaser's Minnesota tax ID number

Purchaser’s type of business

Reason for exemption

Purchaser's signature & Date

117

Complete Exemption Certificates

2/5/2018

40

Exemption Certificates

Know if you qualify to claim an exemption

Complete an exemption certificate

Give it to the seller at the time of purchase

Liable for any use tax, interest, and penalties

118

Purchaser’s Responsibilities

Exemption Certificates

You should review all exemption certificates and verify:

All required fields are complete.

That the certificate is signed

119

Seller’s Responsibilities

Part 9

Refund Requestsand

Amended Returns

120

2/5/2018

41

Review your invoices

Refund Requests and Amended Returns

121

How far back can I request a refund?

Refund Requests and Amended Returns

3 ½ years*

*Exceptions to the general rule apply in cases of an audit if you paid an assessment order in full or signed, Form ST21, Consent to Extend Statute . 122

Statute of Limitations

Refund Requests and Amended Returns

How is the 3 ½ year statute of limitations calculated?

Type of tax paid Calculation of 3½ year statuteSales tax(paid to seller)

You have 3½ years from the 20th day of the month following the purchase invoice date.

Use tax(paid directly to state)

You have 3½ years from the original tax return due date.

123

2/5/2018

42

124

Capital Equipment Refund

124

Note: If you paid sales tax on capital equipment purchased after June 30, 2015 (last four highlighted entries), it needs to be claimed as a purchaser request for refund rather than a capital equipment request for refund.

Refund Requests and Amended Returns

Supporting Worksheet

Complete a separate worksheet for each type of request

Use a separate column for each taxing jurisdiction

126

Capital Equipment Refund

2/5/2018

43

127

Purchaser Refund

128

Refund Requests and Amended Returns

Where do I send Form ST11?

To file a refund request electronically, send it to [email protected] Refund requests in paper form should be mailed to:

Minnesota Department of Revenue525 Lake Avenue SouthSuite 405

Duluth, MN 55802

Remember to attach all required documentation!

129

2/5/2018

44

Refund Requests and Amended Returns

File an amended return if: Made an error on a previously filed return

Paid too much or too little

Use a separate column for each taxing jurisdiction Number of periods How do I file the amended return?One Adjust your return in e-Services

Multiple Send Form ST11 with a worksheet detailing the adjustment for each period.

130

Amended Returns

Part 10

Communicating with the

Department of Revenue

131

Communicating with the Department of Revenue

Have a sales and use tax question?

132

2/5/2018

45

Communicating with the Department of RevenueSales and Use Tax Division

Minnesota Revenue website: revenue.state.mn.us Questions relating to Sales and Use Tax Law?

Email: [email protected] Questions relating to your Sales and Use Tax account activity?

Email: [email protected] Prefer telephone assistance?

Phone: 651-296-6181 or 800-657-3777

133

Communicating with the Department of Revenuefor Other Divisions

Business Income Taxes (Corporation Franchise Tax, Partnership Tax, S Corporation Tax, Estate Tax, Fiduciary Tax)651-556-3075 Email: [email protected]

Withholding Tax 651- 282-9999 or 1-800-657-3594 Email: [email protected]

Business Registration651-282-5225 or 1-800-657-3605 Email: [email protected]

134

Minnesota Department of Revenue Website revenue.state.mn.us

135

2/5/2018

46

Minnesota Department of Revenue Website GovDelivery

Choose the updates you want - by tax type and publication type

Choose the frequency of notifications

Sign in directly or use your social media account –

Facebook, Yahoo! or Google

136

Minnesota Department of Revenue WebsiteSales and Use Tax Videos youtube.com/MNRevenue

Available Videos: e-Services Instructional Videos

Education Video Series

Inside Scoop: Streamlined Sales Tax

Training Videos

137

Minnesota Department of Revenue Website Social Media

Keep up with the latest news from the Minnesota Department of Revenue on Twitter, Facebook, and LinkedIn.

twitter.com/MNRevenue

facebook.com/MNRevenue

linkedin.com/company/minnesota-department-of-revenue

138

2/5/2018

47

Communicating with the Department of Revenue

Please notify us if you have changes to any of the following: Mailing address(es)

Business location(s)

Legal organization

NAICS code

Contact information

Owners and/or officers139

Part 11

Course Review

140

Course Review

Manufacturers often mistakenly claim the capital equipment exemption on these items:

Access-required devices (e.g., catwalks, ladders, and man lifts)

Cabinets and other storage items

Regulatory-required equipment (e.g., OSHA, pollution control)

141

Equipment commonly taxed incorrectly

2/5/2018

48

Course Review

Items to look for when reviewing invoices:

Multi-use equipment, including qualifying and non- qualifying activities (e.g., computers, forklifts, hand tools)

Capital Equipment is:

Machinery and equipment

Used at least 50% of the time

In the integrated production process142

Equipment commonly taxed incorrectly

Course Review

These items commonly qualify for the capital equipment exemption but are often overlooked:

Repair parts, including replacement parts that are on the original equipment

143

Equipment commonly taxed incorrectly

Course Review

These items are commonly mistaken as qualifying for the industrial production exemption:

Percentage of utilities used in equipment that performs qualifying and non-qualifying activities, during the non-qualifying activities(e.g., conveyors, cranes, and forklifts)

Multi-use items purchased with an exemption certificate (e.g., all “keep fill“, bolts, ink cartridges, lube, and nuts )

144

Materials consumed in production taxed incorrectly

2/5/2018

49

Course Review

Items to look for when reviewing invoices: Utilities for overhead lighting and space heating

Utilities consumed in non-production equipment (updated utility study recommended)

Utilities consumed in equipment that qualifies for the integrated production process but not the industrial production process (e.g., freezer at a meat processing plant)

Utilities study for one utility used to pro-rate taxability for another utility (e.g., electrical percentage applied to gas and/or water) 145

Materials consumed in production taxed incorrectly

Scenario Discussions

146

Scenario 1 – DDD Windows

You’re an accounts payable clerk for a company that manufactures windows. This company also installs windows. You have vendor invoices for a manlift and shelving that do not have sales tax.

Do you need to accrue use tax on these items?

147

2/5/2018

50

Scenario 2 – New World Meat Processing

You’re an accounts payable clerk for a meat processing plant. The plant uses a computer system to track their inventory. Your co-worker states that the inventory computer system is exempt under quality control because they must be able to track the meat if it gets recalled. If they do not track the meat, the FDA will not allow them to sell it.

Does the tracking system qualify for an exemption?

148

Scenario 3 – Fast Print and Mailing

You work for a store that offers mail box rental, package service, custom printing, and copying. You are not paying tax on any of your printing or copy machines. You also do not pay tax on any of the ink or supplies for the machines

Some machines are used only by employees for custom jobs.

Other machines are available to the public for per copy fees and also used by employees for large custom jobs.

Do the printers and copiers qualify for the capital equipment exemption? Does the ink qualify for the industrial production exemption?

149

Scenario 4 – Sawmill Wood Furniture Manufacturing

You work for a small furniture manufacturer that expanded their wood furniture line to include custom finishes. To provide custom finishes they moved to a bigger location with several buildings.

They saw and assemble unfinished furniture pieces in the wood shop building.

They custom finish the pieces in the finishing building.

Both buildings have dust control systems to protect the equipment and the product.

Do either of the dust control systems qualify for the capital equipment exemption?

150

2/5/2018

51

Scenario 5 – ABC Manufacturing

You work for a large manufacturer who has given a blanket exemption certificate to the welding supply store.

The invoices include charges for welding gases, tanks, and cutting tips.

The welding gases are used to repair qualifying capital equipment.

Would all these items qualify for either the capital equipment exemption or the industrial production exemption?

151

Scenario 6 - Smith Gravel Company

You work for a road contractor who has multiple gravel pits. The company sells class 5, crushed rock, and pit run and also uses these materials in their construction jobs.

The company has never requested a capital equipment refund.

The company is giving exemption certificates to many of their suppliers after the exemption for capital equipment became an upfront exemption.

The company keeps a breakdown of retail sales versus construction contracts.

From this information can you determine if the equipment used in the gravel pit qualifies for the capital equipment exemption?

152

Scenario 7 - Just Turkeys

You work for a turkey processing plant that must maintain a temperature of 37 degrees on the processing floor. The processed turkeys are flash frozen and stored in freezers until they are shipped out. You are reviewing the electric bills and utility studies and find that all of the electricity associated with the cooling and freezers was purchased exempt.

Are you allowed to purchase all of your electricity for cooling and freezers exempt?

153

2/5/2018

52

Scenario 8 - Clear Water

You work for a bottled water company that has a proprietary filter system. The company is building a new building for all of the pipes and filters for the system. You are purchasing all of the building materials exempt from tax under the special purpose building exemption.

Do the building materials qualify for this exemption?

154

Course Summary

We discussed… When sales and use taxes are owed The capital equipment and industrial

production exemptions The refunds and exemptions available

to businesses engaged in “industrial production."

How to request a refund of taxes paid using Form ST11

155

Questions?

156

2/5/2018

53

Thank you!Permission of the Minnesota Department of Revenue must be secured

before exhibiting, reproducing, distributing or making any other use of any part of this presentation.

Produced by the Minnesota Department of Revenue600 North Robert Street, St. Paul, Minnesota 55146

©Copyright 2018, Minnesota Department of Revenue, All Rights Reserved

Minnesota Business Tax Education157