Embed Size (px)

Citation preview

Presenting a live 110‐minute teleconference with interactive Q&A

Sales Tax Affiliate Nexus: Latest Developments Sales Tax Affiliate Nexus: Latest Developments Adjusting Multi‐State Compliance Under New State Laws for Online Business Partnerships

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, DECEMBER 15, 2011

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Arthur Rosen Partner McDermott Will & Emery New YorkArthur Rosen, Partner, McDermott Will & Emery, New York

Shirley Sicilian, General Counsel, Multistate Tax Commission, Washington, D.C.

Annie Huang, Partner, Pillsbury Winthrop Shaw Pittman, San Francisco

Brian Toman, Partner, Reed Smith, San Francisco

For this program, attendees must listen to the audio over the telephone.

Brian Toman, Partner, Reed Smith, San Francisco

Please refer to the instructions emailed to the registrant for the dial-in information.Attendees can still view the presentation slides online. If you have any questions, pleasecontact Customer Service at1-800-926-7926 ext. 10.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits FOR LIVE EVENT ONLY

Attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online but there is no online audio for this program.

Please refer to the instructions emailed to the registrant for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.at 1 800 926 7926 ext. 10.

Tips for Optimal Quality

S d Q litSound Quality

For this program, you must listen via the telephone by dialing 1-866-873-1442 and entering your PIN when prompted. There will be no sound over the web connection.co ect o .

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key againpress the F11 key again.

S l T Affili t N L t t Sales Tax Affiliate Nexus: Latest Developments Seminar

Dec. 15, 2011

Annie Huang, Pillsbury Winthrop Shaw [email protected]

Shirley Sicilian, Multistate Tax [email protected]

Brian Toman, Reed [email protected]

Arthur Rosen, McDermott Will & Emery [email protected]

Today’s Program

O i A d L t t St t A ti Slid 7 Slid 20Overview And Latest State Actions[Shirley Sicilian and Annie Huang]

State Attempts To Tax Remote Business: Background[A i H ]

Slide 7 – Slide 20

Slide 21 – Slide 25[Annie Huang]

Legal Issues[Arthur Rosen and Brian Toman]

Slide 26 – Slide 30

Political Implications[Arthur Rosen]

Slide 31 – Slide 33

Federal Sales And Use Tax Legislation

[Arthur Rosen and Shirley Sicilian]

Slide 34 – Slide 37

Practical Considerations[Brian Toman and Annie Huang]

Slide 38 – Slide 39

Shi l Si ili M l i T C i i

OVERVIEW AND LATEST STATE

Shirley Sicilian, Multistate Tax CommissionAnnie Huang, Pillsbury Winthrop Shaw Pittman

OVERVIEW AND LATEST STATE ACTIONS

I d iIntroduction

I Generally what states are attempting to doI. Generally what states are attempting to do

A. General concept: Nexus based on agreements with “affiliates”

B. Pursuant to so-called “click-through” nexus laws, state l gi l t h tt t d t t t i g j i di ti legislatures have attempted to exert taxing jurisdiction over certain out-of-state, Internet retailers based upon the retailer’s agreements with in-state residents to refer customers via a link to the retailer’s Web siteto the retailer s Web site.

C. This type of legislation typically provides that: (1) a remote seller has to register as a vendor and collect sales and use tax if the remote seller contracts with residents who link to the the remote seller contracts with residents who link to the remote seller’s Web page and are paid a commission; and (2) thereby generate over a threshold number of sales for the remote seller.

8

remote seller.

Efforts To Address QuillAnd Role Of ‘Click Throu h’ Le islationAnd Role Of ‘Click‐Through’ Legislation

Working within Working to change QuillgQuill reality

G id D fi PP

reality

Congress: Guidance: Define PP in Internet Age

Congress: • MSFA (H.R. 2701 – SST)• MEA (H.R. 3179)• MFA (H.R. 1832)

Courts:

PP Yes: Collect• Affiliate entity nexus• “Click-through” nexus

Courts:• Oklahoma statute?• Colorado statute?

PP No: Notice/report• General statute: CO, OK,

SC SD VT

9

SC, SD, VT • Ad-hoc: e.g., NC

‘Click‐Through’ Nexus Overview‘Click‐Through’ Nexus OverviewClick Through Nexus OverviewClick Through Nexus Overview

Oregon

CTCT

NHNHVT

Michigan

Oregon

Minnesota

CTMass.

N.H.Vt.

New York

Wisconsin

MichiganWyoming

North Dakota

South DakotaIdaho

Montana Maine

Washington

MD

CTCT

Pennsylvania

W. VA

Michigan

NevadaUtah

Iowa

IndianaOhio

Del.

N.J.

CTPA

W. Va.

Missouri

Illinois

Michigan

VirginiaKentucky

Wyoming

Colorado

South Dakota

Nebraska

KansasCalifornia

R.I.

D C

MD

Legend

N l gi l ti d

Miss.Alabama

Missouri

Miss.Alabama Georgia

TNS. Carolina

N. Carolina

Kentucky

OklahomaArizonaNew Mexico Arkansas

D.C.

Nexus without statute

Legislation under consideration

Nexus legislation passed

Legislation considered but not passed or passed then

Louisiana FloridaTexas

HawaiiAlaska

* V i l i ff if 15 h

10

vetoed

Other (incl. notification requirement)

* Vermont is only in effect if 15 other states enac.** California’s legislation is delayed until 2012, subject to passage of federal legislation.*** South Carolina has enacted a limited-notice requirement, and legislation is under consideration.

H S H D IHow States Have Done It

I State statutes State Effective Date Affiliate Threshold StatuteI. State statutes

A. Enacted in NY, CA, IL, CT, AR,

Arkansas Oct. 24, 2011 More than $10,000 Ark. Code Ann. § 26-52-117

California Jan. 1, 2013 if federal legislation is enacted by July 31, 2012.

More than $10,000 and more than $1,000,000 in annual in-state sales

Cal. Rev. & Tax. §6203(c)

RI, NC and VT

II. Two approaches: (1) rebuttable

y y ,

Sept. 15, 2012 if federal legislation is not enacted.

Connecticut July 1, 2011 More than $2,000 Conn. Gen. Stat. §12-407(a)(12)(L)

( )presumption; (2) irrebuttable presumption

12-407(a)(12)(L)

Illinois July 1, 2011 More than $10,000 35 ILCS 105/2 and 110/2

New York June 1, 2008 More than $10,000 N.Y. Tax Law §1101(b)(8)(vi)presumption

A. All have sales thresholds

North Carolina

Aug. 7, 2009 More than $10,000 N.C. Gen. Stat. § 105-164.8

Rhode Island July 1, 2009 More than $5,000 R.I. Gen. Laws § 44-18-15

Vermont When adopted in 15 More than $10,000 Vt. Stat. Ann. tit. 32,

11

other states. § 9701(9)(I) (H.B. 436)

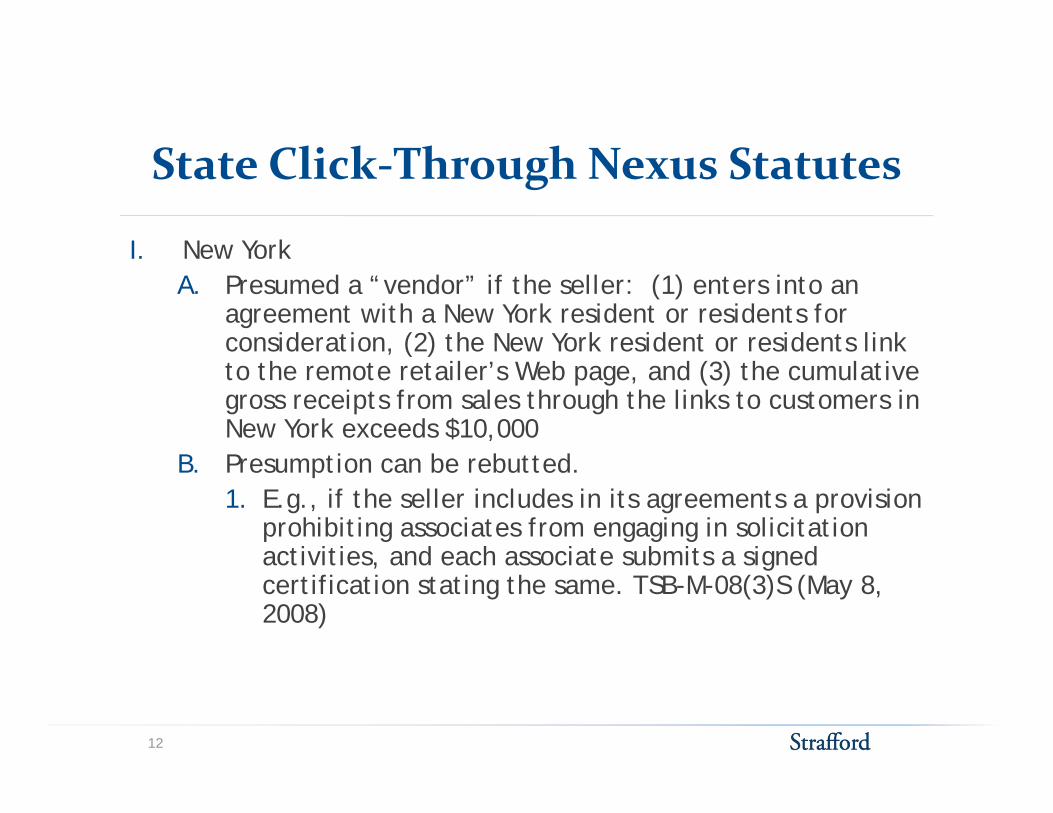

S Cli k Th h N SState Click‐Through Nexus Statutes

I New YorkI. New YorkA. Presumed a “vendor” if the seller: (1) enters into an

agreement with a New York resident or residents for consideration, (2) the New York resident or residents link , ( )to the remote retailer’s Web page, and (3) the cumulative gross receipts from sales through the links to customers in New York exceeds $10,000

B P ti b b tt d B. Presumption can be rebutted. 1. E.g., if the seller includes in its agreements a provision

prohibiting associates from engaging in solicitation activities and each associate submits a signed activities, and each associate submits a signed certification stating the same. TSB-M-08(3)S (May 8, 2008)

12

S Cli k h h S (C )

I Illinois

State Click‐Through Nexus Statutes (Cont.)

I. IllinoisA. Amends the definition of “retailer maintaining a place of

business” to specify that a business becomes a ‘‘retailer maintaining a place of business’’ in Illinois and is maintaining a place of business in Illinois, and is therefore required to collect tax, when it contracts with a person located in Illinois to pay a commission in return for the person’s direct or indirect referral of customers pthrough a Web site link.

B. Applies only when the retailer’s quarterly gross receipts from click-through referral sales through persons in Illinois

$exceed $10,000 in each of the previous four quartersC. No rebuttable presumption and no exception

13

S Cli k h h S (C )

I Connecticut

State Click‐Through Nexus Statutes (Cont.)

I. Connecticut

A. The definition of “retailer” includes every person making sales of tangible personal property through an “agreement with another person located in this state under which such person located in this state, for a commission or other consideration that is based upon the sale of tangible personal property or services by the retailer, directly or indirectly refers potential customers, whether by a link on an Internet web site or otherwise, to ythe retailer.”

B. No rebuttable presumption (final enacted legislation eliminated the presumption that was included in a prior

14

eliminated the presumption that was included in a prior version of the law)

S Cli k h h S (C )

I. California (and “the deal”)

State Click‐Through Nexus Statutes (Cont.)

A. Initial click-through legislation (AB X1 28) enacted on June 29, 2011.

B. Recently enacted (signed Sept. 23, 2011) AB 155 repeals AB X1 28 and effectively “delays” the implementation of click-through until Sept. 20122012.

1. Amends “retailer engaged in business”

a. $10,000 from commissioned referrals; $1 million in total annual in-state sales in state sales

i. Up from $500,000 in AB X1 28

b. No presumption; exception for referrals that do not satisfy the requirements of the constitutionq

c. Also enacts affiliate nexus

C. If federal legislation is enacted by July 31, 2012 (and California does not elect to implement that law on or before Sept. 14, 2012), then click-

15

through is effective Jan. 1, 2013.

D. If a federal bill is not enacted, then AB 155 is effective Sept. 15, 2012.

O h S S A d S G id

I. Other state statutes

Other State Statutes And State Guidance

A. Arkansas

1. $10,000 in-state sale requirement

2. Rebuttable presumption

B. Rhode Island

1. $5,000 in-state sale requirement

2. Rebuttable presumption

C. North Carolina

1. $10,000 in-state sale requirement

2. Rebuttable presumption

D. Vermont

1. Enacted when similar legislation is adopted in 15 other states

II. State guidance

16

A. Pennsylvania

1. “Pa. Sales and Use Tax Bulletin,” 2011-01 (Dec. 1, 2011)

E l Of R L i l i A

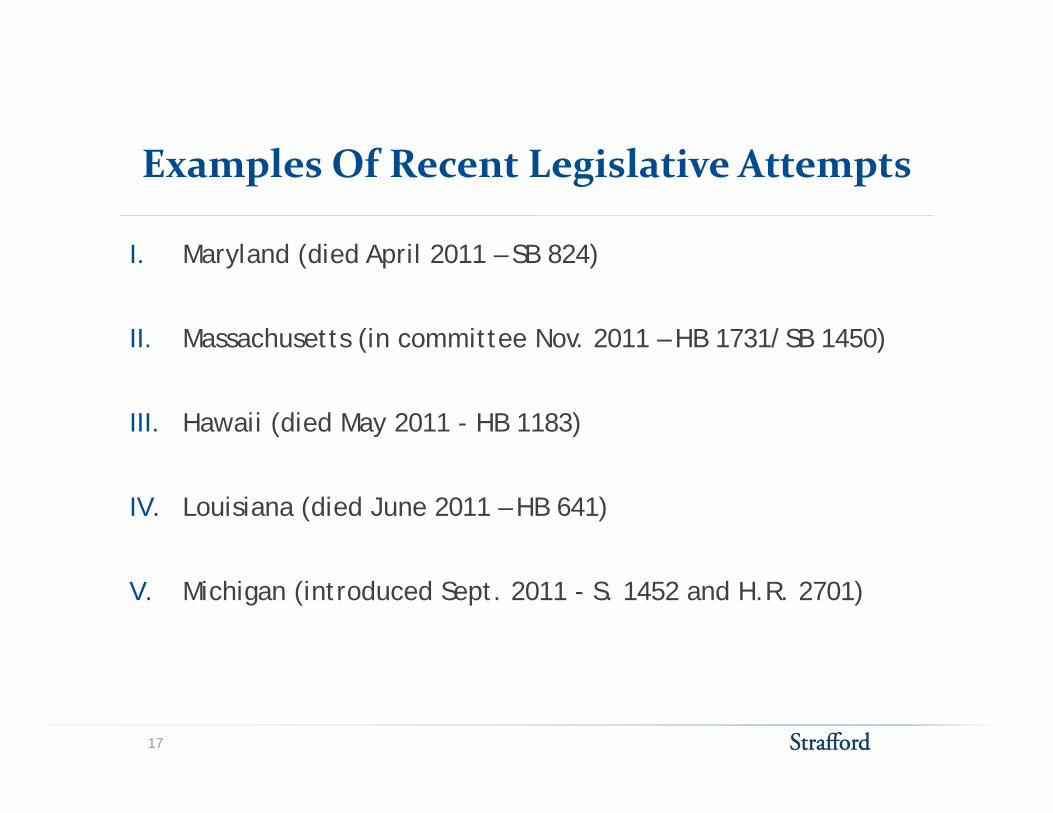

I Maryland (died April 2011 SB 824)

Examples Of Recent Legislative Attempts

I. Maryland (died April 2011 – SB 824)

II. Massachusetts (in committee Nov. 2011 – HB 1731/SB 1450)

III. Hawaii (died May 2011 - HB 1183)

IV. Louisiana (died June 2011 – HB 641)

V. Michigan (introduced Sept. 2011 - S. 1452 and H.R. 2701)

17

Variation: Reporting Approaches

I Sales and use tax information notice and reporting (and

g(Colorado And Oklahoma)

I. Sales and use tax information notice and reporting (and affiliate nexus)

II. ColoradoA. Must provide notice to customers that use tax not A. Must provide notice to customers that use tax not

collected and may be due; $5 penalty per failureB. Must provide customers with annual statements of

purchases; $10 penalty per failureC. Must provide the department with annual statements; $10

penalty per failure D. De minimis rule exempts retailers that made less than

$100 000 i t t l l i C l d i th i $100,000 in total gross sales in Colorado in the prior calendar year and reasonably expect that total gross sales in Colorado in current calendar year less than $100,000

a Includes all sales of goods by all entities under

18

a. Includes all sales of goods by all entities under common control

Variation: Reporting Approachesg(Colorado And Oklahoma), Cont.

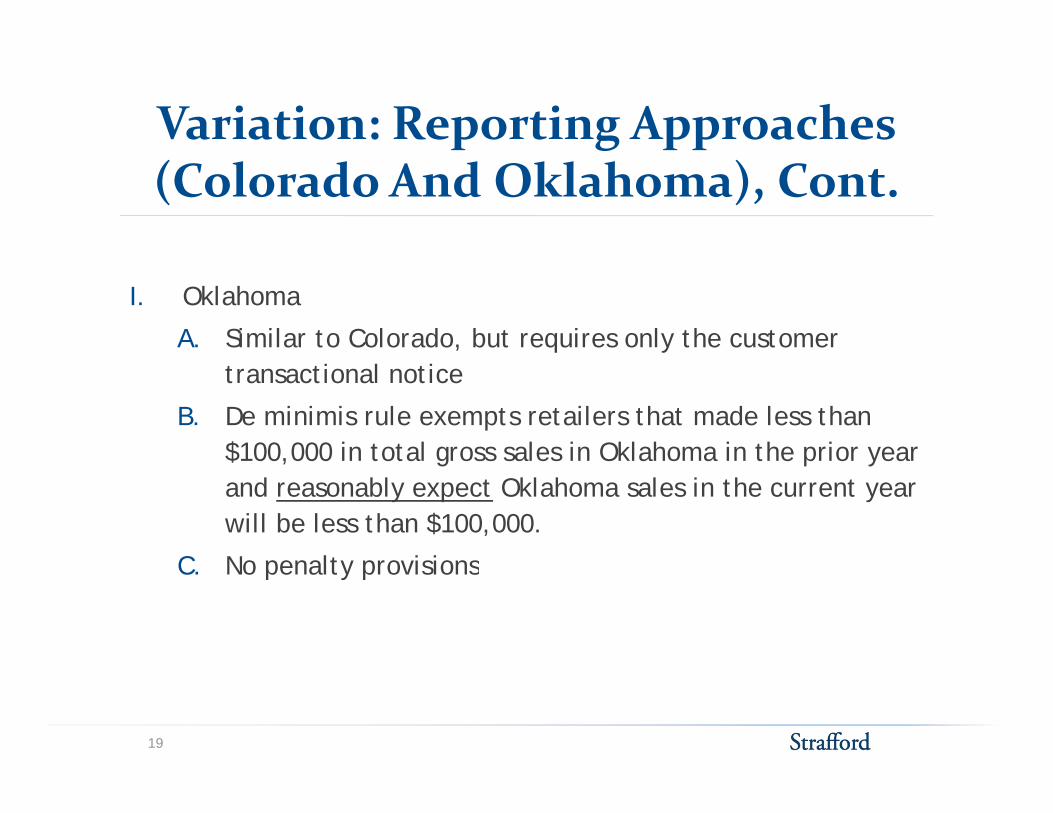

I. Oklahoma

A. Similar to Colorado, but requires only the customer transactional notice

B. De minimis rule exempts retailers that made less than $100,000 in total gross sales in Oklahoma in the prior year $100,000 in total gross sales in Oklahoma in the prior year and reasonably expect Oklahoma sales in the current year will be less than $100,000.

C No penalt pro isionsC. No penalty provisions

19

D l Of MTC M d l S

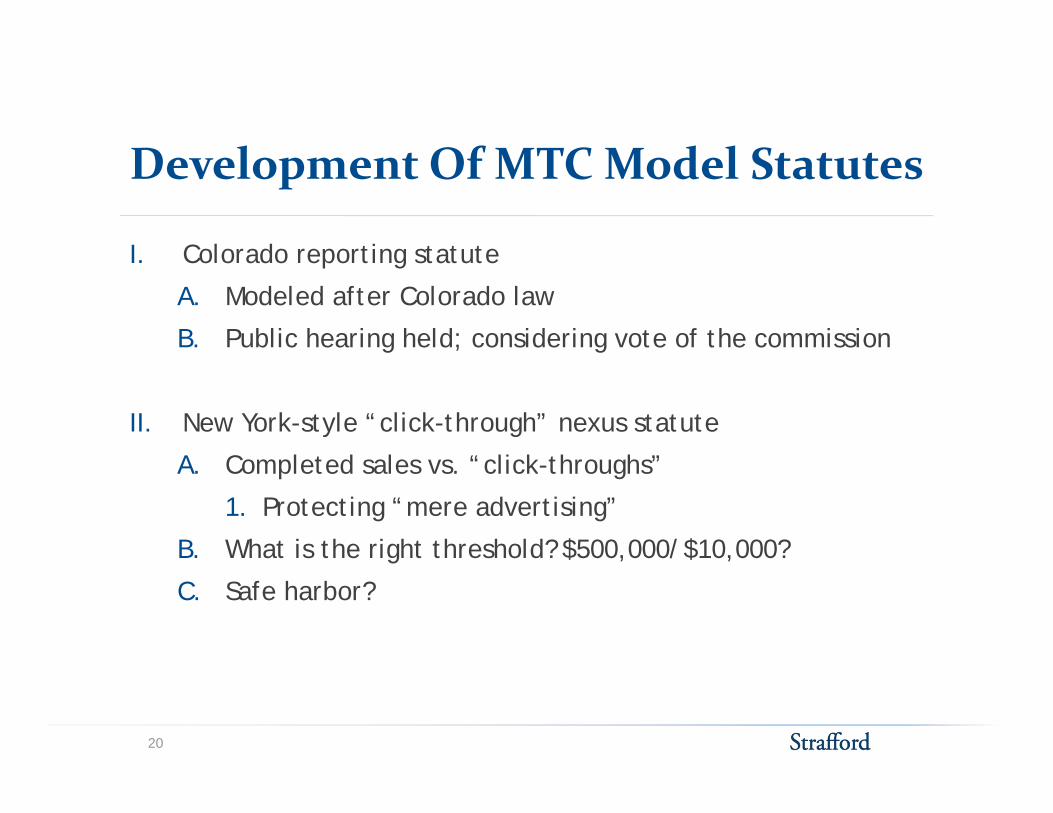

I Colorado reporting statute

Development Of MTC Model Statutes

I. Colorado reporting statute

A. Modeled after Colorado law

B. Public hearing held; considering vote of the commission

II. New York-style “click-through” nexus statute

A C l t d l “ li k th h ” A. Completed sales vs. “click-throughs”

1. Protecting “mere advertising”

B. What is the right threshold? $500,000/$10,000?g $ , $ ,

C. Safe harbor?

20

STATE ATTEMPTS TO TAX Annie Huang, Pillsbury Winthrop Shaw Pittman

STATE ATTEMPTS TO TAX REMOTE BUSINESS: BACKGROUND

History Of State Attempts To Tax

1942 Nelson v. Sears, Roebuck & Co.Nelson v. Montgomery Ward & Co. Northwestern States

P l d C 1959

yRemote Businesses

1967

1980s

National Bellas Hess, Inc. v. Department of Revenue of the State of Illinois

States break the law

Portland Cement Company v. Minnesota

1959

Bloomingdale’s by Mail v. Dept. of Rev1989

1992Quill Corporation v.

North Dakota1992

L t 1990

Geoffrey v. SC1993

1991 SFA Folio v. Bannon

SFA Folio v. Tracy1994

Late 1990s

2000 - Present

E-Commerce

Streamlined Sales

Late 1990s1999 - 2000

2000 - Present

Advisory Commission on Electronic Commerce

2004

1995Current v. CA

2000 - PresentTax and Related Federal Legislation

20042005

2007200820092010

MTC Factor Nexus Proposal

OH Commercial Activity Tax

MBNA v. West VirginiaCapital One v. MA DOR; CA & CT enact econ. nexus

NY enacts “click-through” nexus

Amazon v. NY

22

2010

History Of State Attempts To Tax

I The physical presence requirement

yRemote Businesses (Cont.)

I. The physical presence requirement

A. Quill Corp. v. North Dakota, 504 U.S. 298 (1992)

B. Stare decisis: “Stare decisis is usually the wise policy, because in t tt it i i t t th t th li bl l f most matters it is more important that the applicable rule of

law be settled than that it be settled right ... But in cases involving the Federal Constitution, where correction through legislative action is practically impossible this Court has often legislative action is practically impossible, this Court has often overruled its earlier decisions.” Burnet v. Coronado Oil & Gas Co., 285 U.S. 393, 406- 407 (1932) (Brandeis, J., dissenting)

1 What does stare decisis mean for the current debate?1. What does stare decisis mean for the current debate?

a. Remember, Oklahoma declared that its statute did notviolate Quill, because there is no “undue burden” on out-of-state retailers

23

out-of-state retailers.

2. What does stare decisis mean more generally?

History Of State Attempts To Tax

I Attributional nexus

yRemote Businesses (Cont.)

I. Attributional nexus

A. Nexus based on the activities of others

B. Foundational cases: Tyler Pipe Industries v. Washington State Dep’t. Rev., 483 U.S. 232 (1987); Scripto, Inc. v. Carson, 362 U.S. 207 (1960)

C. Constitutional standard: Whether the activities performed C. Constitutional standard: Whether the activities performed by the in-state person on behalf of the out-of-state company are “significantly associated with the taxpayer’s ability to establish and maintain a market in [the] state ability to establish and maintain a market in [the] state for the sales”

D. General advertising does not create nexus. Miller Bros. C M l d 347 U S 340 (1954)

24

Co. v. Maryland, 347 U.S. 340 (1954)

History Of State Attempts To Tax

I Attributional nexus (Cont )

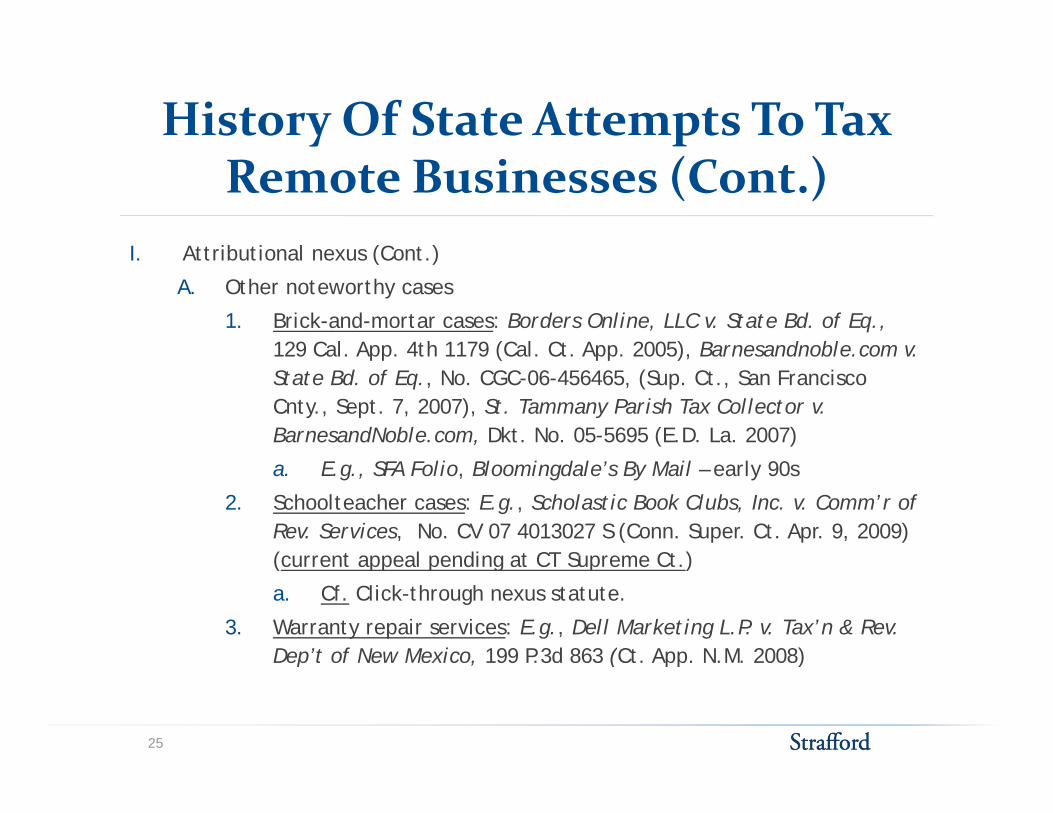

Remote Businesses (Cont.)I. Attributional nexus (Cont.)

A. Other noteworthy cases

1. Brick-and-mortar cases: Borders Online, LLC v. State Bd. of Eq., 129 Cal. App. 4th 1179 (Cal. Ct. App. 2005), Barnesandnoble.com v. 129 Cal. App. 4th 1179 (Cal. Ct. App. 2005), Barnesandnoble.com v. State Bd. of Eq., No. CGC-06-456465, (Sup. Ct., San Francisco Cnty., Sept. 7, 2007), St. Tammany Parish Tax Collector v. BarnesandNoble.com, Dkt. No. 05-5695 (E.D. La. 2007)

a. E.g., SFA Folio, Bloomingdale’s By Mail – early 90s

2. Schoolteacher cases: E.g., Scholastic Book Clubs, Inc. v. Comm’r of Rev. Services, No. CV 07 4013027 S (Conn. Super. Ct. Apr. 9, 2009) (current appeal pending at CT Supreme Ct )(current appeal pending at CT Supreme Ct.)

a. Cf. Click-through nexus statute.

3. Warranty repair services: E.g., Dell Marketing L.P. v. Tax’n & Rev. Dep’t of New Mexico, 199 P.3d 863 (Ct. App. N.M. 2008)

25

p f , 99 6 (C pp )

Arthur Rosen, McDermott Will & Emery

LEGAL ISSUES

Arthur Rosen, McDermott Will & EmeryBrian Toman, Reed Smith

Legal Issues And Arguments Associated

I. Background legal issues

g gWith Click‐Through Nexus

A. Attributional nexus1. The importance of market enhancement –

“significantly associated with the taxpayer’s ability to t bli h d i t i k t”establish and maintain a market”

II. Constitutional concerns/issues

A. Ultimate issue is whether the arrangements satisfy Tyler Pipe

III. States’ positions on “click-through”A. The activities of the in-state affiliates satisfy the Tyler A. The activities of the in state affiliates satisfy the Tyler

Pipe/Scripto constitutional standards (or at least are presumed to), because the in-state affiliates establish and maintain a market for the remote sellers’ sales.

B S k h i i h b d

27

B. States take the position these arrangements go beyond mere advertising.

C R di Cli k Th h N

I. Case: The Direct Marketing Association v. Huber, No. 10-cv-01546-REB-CBS

Cases Regarding Click‐Through Nexus

I. Case: The Direct Marketing Association v. Huber, No. 10 cv 01546 REB CBS (D. Colo., Jan. 26, 2011) (order granting motion for preliminary injunction)A. The U.S. District Court for the District of Colorado granted a motion for

preliminary injunction enjoining the Colorado Department of Revenue from enforcing its lawfrom enforcing its law.

II. Case: Amazon.com LLC v. Lay, 758 F. Supp. 2d 1154 (W.D. Was. 2010)A. Amazon filed a federal lawsuit alleging the North Carolina DOR’s

attempts to obtain names, addresses and purchases of customers violated the First Amendment, Article I, §§ 4, 5 of the Washington State Constitution; and federal Video Privacy Protection Act, 18 USC § 2710.

B. Declaratory judgment sought1 U S District Court stated “[T]o the extent the [DOR] demands that 1. U.S. District Court stated, [T]o the extent the [DOR] demands that

Amazon disclose its customers' names, addresses or any other personal information, it violates the First Amendment and the Video Privacy Protection Act, only as long as the DOR continues to have access to or possession of detailed purchase records obtained from

28

access to or possession of detailed purchase records obtained from Amazon ...”

d l k h h ( )

III Case: Amazon com LLC v New York State Dep’t of Taxation and

Cases Regarding Click‐Through Nexus (Cont.)

III. Case: Amazon.com LLC v. New York State Dep t of Taxation and Finance, 877 NYS2d 842 (N.Y. App. Div. 2010)A. The facial challenges to the constitutionality of the statute (Due

Process Clause, Commerce Clause and equal protection) were rejectedrejected.

B. The as-applied challenges were remanded to the lower court for fact-finding with respect to whether the in-state residents referring customers to the Amazon Web site solicited sales for A i N Y k Amazon in New York. 1. Is the presumption reasonable?

2. Thoughts on the as-applied challenge

IV. Case: Performance Marketing Association v. Hamer (filed in Cir. Ct. of Cook County, Illinois, July 27, 2011)A. The PMA has filed a suit in federal District Court challenging the

29

constitutionality of the Illinois click-through nexus law.

Legal Issues And Arguments Associated

I. Difference between solicitation and advertising

Legal Issues And Arguments AssociatedWith Click‐Through Nexus

I. Difference between solicitation and advertisingII. Is method of compensation relevant?

III Are “click-through” nexus statutes necessary for a state to impose its III. Are click-through nexus statutes necessary for a state to impose its jurisdiction to tax?

A. See recent Pa. Sales and Use Tax Bulletin, 2011-01 (Dec. 1, 2011)

1. Prospective enforcement?

30

p

POLITICAL IMPLICATIONSArthur Rosen, McDermott Will & Emery

P li i l I li iI. Click-through nexus laws

Political ImplicationsI. Click through nexus laws

A. Why states believe that it’s “fair”B. What small businesses and large brick and mortar retailers sayC. Who is really driving the effort? D Weighing the termination of in-state affiliate relationships vs taxation of D. Weighing the termination of in state affiliate relationships vs. taxation of

remote sellers1. What promotes business?2. Job creation?

32

P li i l I li i (C )I. Contracting Around Quill and nexus

Political Implications (Cont.)I. Contracting Around Quill and nexus

A. Distribution center exemptions (and other nexus exemptions).1. Private agreements (e.g., Tennessee) and legislative exemptions

(e.g., South Carolina) a Are such incentives constitutional? Or fair? a. Are such incentives constitutional? Or fair? b. Can a state “waive” its obligation to collect tax by contract?

i. Tennessee Attorney General Opinion No. 11-55 (July 11, 2011)

B Balancing economic development with just administration of the laws B. Balancing economic development with just administration of the laws 1. Use of related-party distributors. See Lyon Metal Products, Inc. v.

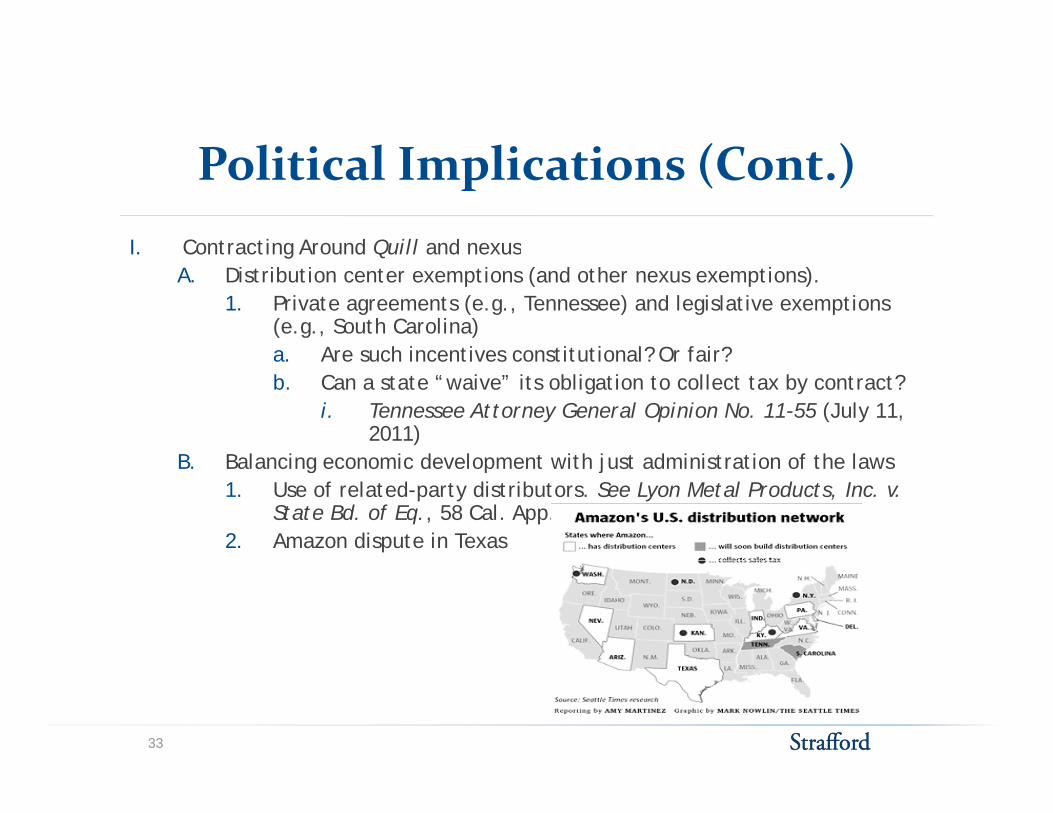

State Bd. of Eq., 58 Cal. App. 4th 906 (Cal. Ct. App. 1997).2. Amazon dispute in Texas

33

Arthur Rosen, McDermott Will & Emery

FEDERAL SALES AND USE TAX

yShirley Sicilian, Multistate Tax Commission

LEGISLATION

F d l L i l iI. Main Street Fairness Act (MSFA), H.R. 2701

A I t d d J l 29 2011

Federal Legislation

A. Introduced on July 29, 2011B. Referred to the Subcommittee on Courts, Commercial and Administrative Law on

Aug. 25, 2011 1. Independent from, but somewhat parallel with, SST

II M k t l E it A t (MEA) H R 3179II. Marketplace Equity Act (MEA), H.R. 3179A. Introduced on Oct. 13, 2011B. Referred to the Subcommittee on Courts, Commercial and Administrative Law on

Oct. 24, 2011 III M k l F i A (MFA) S B 1832III. Marketplace Fairness Act (MFA), S.B. 1832

A. Introduced on Nov. 9, 2011B. Hybrid of MSFA and MEA

IV. Overstock.com billA. Not yet introduced

1. MSFA +++++V. ? (New draft legislation)

A. Not yet introduced

35

1. Simplified MEA

F d l L i l i A C iFederal Legislation: A Comparison

Additional MSFA MEA ?¹MFA

O t kAdditional Consideration: Do thresholds apply at

Streamlined Non-streamlined

SponsorStatewide Administration Statewide Tax Base

MSFA MEA ?¹Overstock

Conyers (MI) Womack (AR) ?Enzi (WY) TBD

pp yindividual seller level or platform level?

Statewide Tax Base Local Rates:

• Zip Code • Blended + • Software

Vendor Discount Threshold 500KSST Governing Board SST Simplification

20MM

TBD

1MM/0.1MM

1MM/0.1MM

(uniform definitions, forms and bundling rules)

Uniform Sourcing No Liability if Rely on I f i F S

maybe

36

Information From State Federal Court

¹ Based on recent draft legislation.

F d l L i l i (C )

I Does the focus on “click through” take away from any

Federal Legislation (Cont.)

I. Does the focus on click-through take away from any momentum that STT or Main Street Fairness may have?

A. If states like New York can collect revenue on e-commerce sales through other means, what is the incentive to join a compact that requires them to modify their laws?

B. Importance of New York litigation and Illinois litigation

II The more bills the better?II. The more bills the better?

37

Brian Toman, Reed Smith

PRACTICAL CONSIDERATIONSAnnie Huang, Pillsbury Winthrop Shaw Pittman

P i l C id i

I Compliance

Practical Considerations

I. Compliance

A. Recommendations for responding to state enactment of a “click-through” nexus law (or a state’s stated position – e.g., Pennsylvania)Pennsylvania)

II. Planning

A. Review affiliate agreements; include in agreements a provision prohibiting associates from engaging in solicitation activitiesprohibiting associates from engaging in solicitation activities

B. Changing the method of compensation

C. Suspend affiliate relationship before in-state threshold is reached (rather than cancel program)

D. Distribution and fulfillment activities

E. Use of links to the remote seller

39