Embed Size (px)

Citation preview

Distribution or sharing of this material is strictly prohibited and may result in the assignment of a failing grade and/or termination of membership in the Institute for Professionals in Taxation®.

SALES TAX SCHOOL I: Introduction to Sales & Use Taxes

Administration of Sales & Use Taxes Georgia Tech Conference Center Atlanta, Georgia Learning Objectives At the end of this section, the learner will be able to:

List powers and identify taxes administered by governmental agencies Identify the various components of the Streamlined Sales Tax Agreement Identify registration issues Know the concept of nexus and how it relates to sales/use tax registration Recognize issues to consider when collecting sales tax List steps in developing a tax collection system Recognize issues related to exemption documentation Recognize issues relating to requesting refunds of sales/use taxes

IPT, Sales Tax School I Administration of Sales & Use Taxes

1

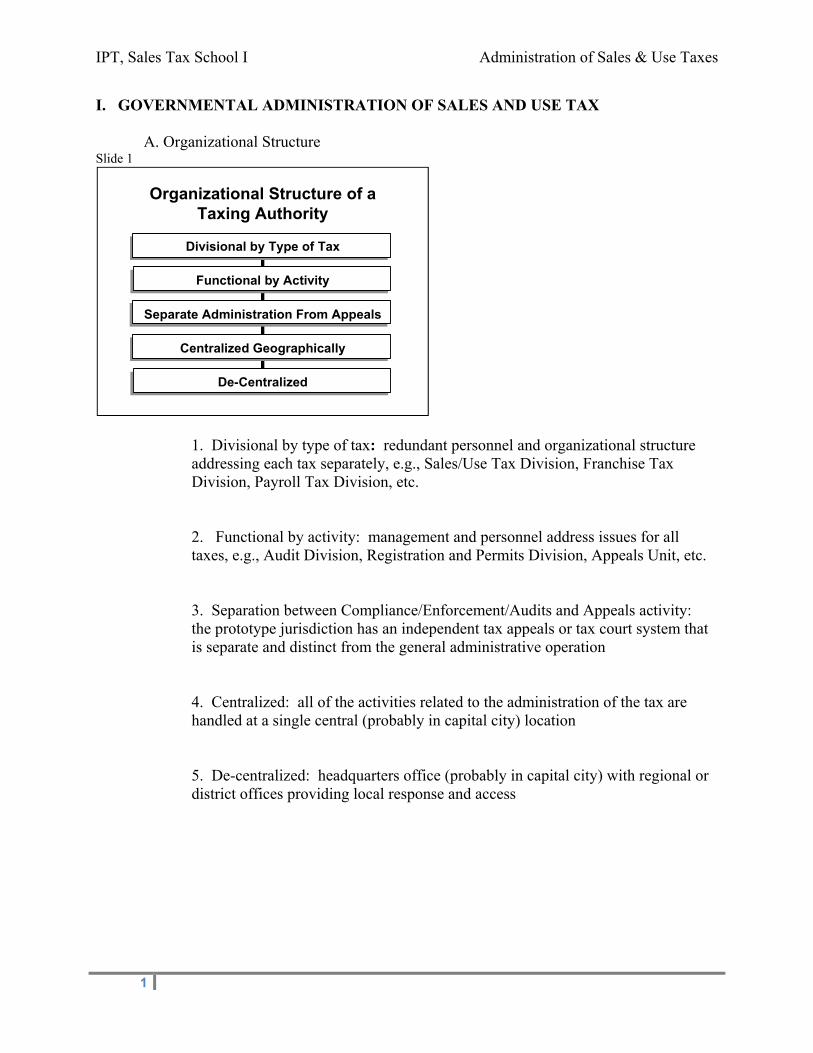

I. GOVERNMENTAL ADMINISTRATION OF SALES AND USE TAX

A. Organizational Structure Slide 1

1. Divisional by type of tax: redundant personnel and organizational structure addressing each tax separately, e.g., Sales/Use Tax Division, Franchise Tax Division, Payroll Tax Division, etc. 2. Functional by activity: management and personnel address issues for all taxes, e.g., Audit Division, Registration and Permits Division, Appeals Unit, etc.

3. Separation between Compliance/Enforcement/Audits and Appeals activity: the prototype jurisdiction has an independent tax appeals or tax court system that is separate and distinct from the general administrative operation

4. Centralized: all of the activities related to the administration of the tax are handled at a single central (probably in capital city) location

5. De-centralized: headquarters office (probably in capital city) with regional or district offices providing local response and access

Organizational Structure of aTaxing Authority

Divisional by Type of Tax

Functional by Activity

Separate Administration From Appeals

Centralized Geographically

De-Centralized

Administration of Sales & Use Taxes IPT, Sales Tax School I

2

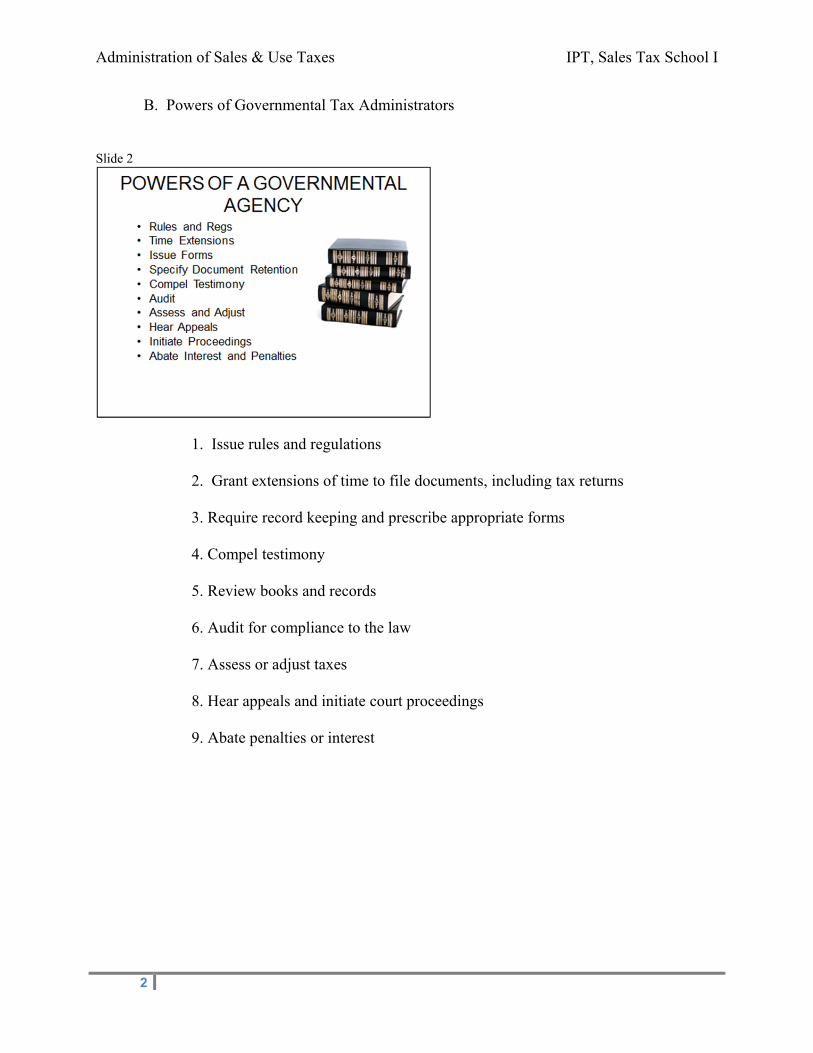

B. Powers of Governmental Tax Administrators Slide 2

1. Issue rules and regulations 2. Grant extensions of time to file documents, including tax returns 3. Require record keeping and prescribe appropriate forms 4. Compel testimony 5. Review books and records 6. Audit for compliance to the law 7. Assess or adjust taxes 8. Hear appeals and initiate court proceedings 9. Abate penalties or interest

MC31

IPT, Sales Tax School I Administration of Sales & Use Taxes

3

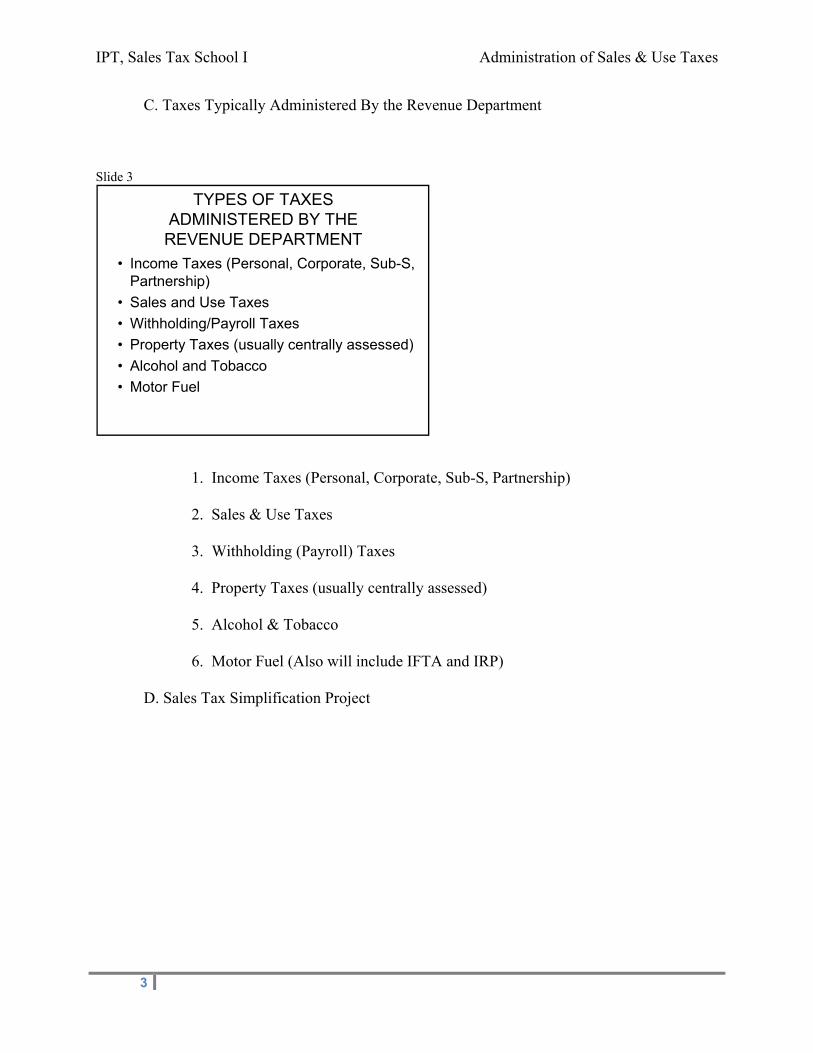

C. Taxes Typically Administered By the Revenue Department

Slide 3

1. Income Taxes (Personal, Corporate, Sub-S, Partnership)

2. Sales & Use Taxes 3. Withholding (Payroll) Taxes

4. Property Taxes (usually centrally assessed) 5. Alcohol & Tobacco 6. Motor Fuel (Also will include IFTA and IRP)

D. Sales Tax Simplification Project

TYPES OF TAXES ADMINISTERED BY THE

REVENUE DEPARTMENT

• Income Taxes (Personal, Corporate, Sub-S, Partnership)

• Sales and Use Taxes

• Withholding/Payroll Taxes

• Property Taxes (usually centrally assessed)

• Alcohol and Tobacco

• Motor Fuel

MC106

Administration of Sales & Use Taxes IPT, Sales Tax School I

4

Slide 4

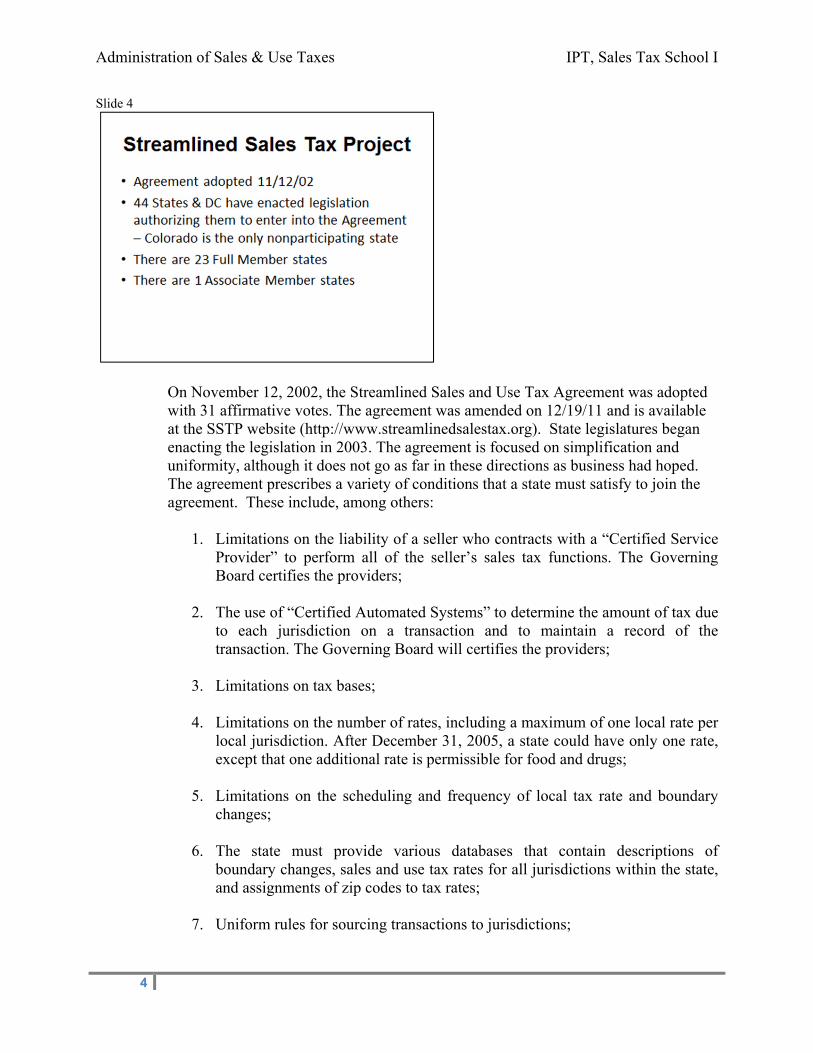

On November 12, 2002, the Streamlined Sales and Use Tax Agreement was adopted with 31 affirmative votes. The agreement was amended on 12/19/11 and is available at the SSTP website (http://www.streamlinedsalestax.org). State legislatures began enacting the legislation in 2003. The agreement is focused on simplification and uniformity, although it does not go as far in these directions as business had hoped. The agreement prescribes a variety of conditions that a state must satisfy to join the agreement. These include, among others:

1. Limitations on the liability of a seller who contracts with a “Certified Service

Provider” to perform all of the seller’s sales tax functions. The Governing Board certifies the providers;

2. The use of “Certified Automated Systems” to determine the amount of tax due

to each jurisdiction on a transaction and to maintain a record of the transaction. The Governing Board will certifies the providers;

3. Limitations on tax bases;

4. Limitations on the number of rates, including a maximum of one local rate per

local jurisdiction. After December 31, 2005, a state could have only one rate, except that one additional rate is permissible for food and drugs;

5. Limitations on the scheduling and frequency of local tax rate and boundary

changes;

6. The state must provide various databases that contain descriptions of boundary changes, sales and use tax rates for all jurisdictions within the state, and assignments of zip codes to tax rates;

7. Uniform rules for sourcing transactions to jurisdictions;

MC113 TF105

IPT, Sales Tax School I Administration of Sales & Use Taxes

5

8. Restrictions on departure from definitions of terms in exempting transactions, and uniform rules regarding administration of exemptions;

9. Restrictions on the variation and content in tax returns and filing dates;

10. Uniform rules for remittances;

11. Uniform rules for bad debts;

12. Restrictions on sales tax holidays, caps and thresholds, rounding;

13. Provisions for simplified registration.

II. TAXPAYER ADMINISTRATION OF SALES AND USE TAX Slide 5

Compliance Definition

Compliance generally refers to the functions performed to adhere to the sales and use tax laws, including but not limited to registration, filing of sales and use tax returns, and documentation of exemptions.

A. Compliance

1. Compliance generally refers to the functions performed to adhere to the sales and use tax laws, including but not limited to registration, filing of sales and use tax returns, and documentation of exemptions.

Administration of Sales & Use Taxes IPT, Sales Tax School I

6

Slide 6

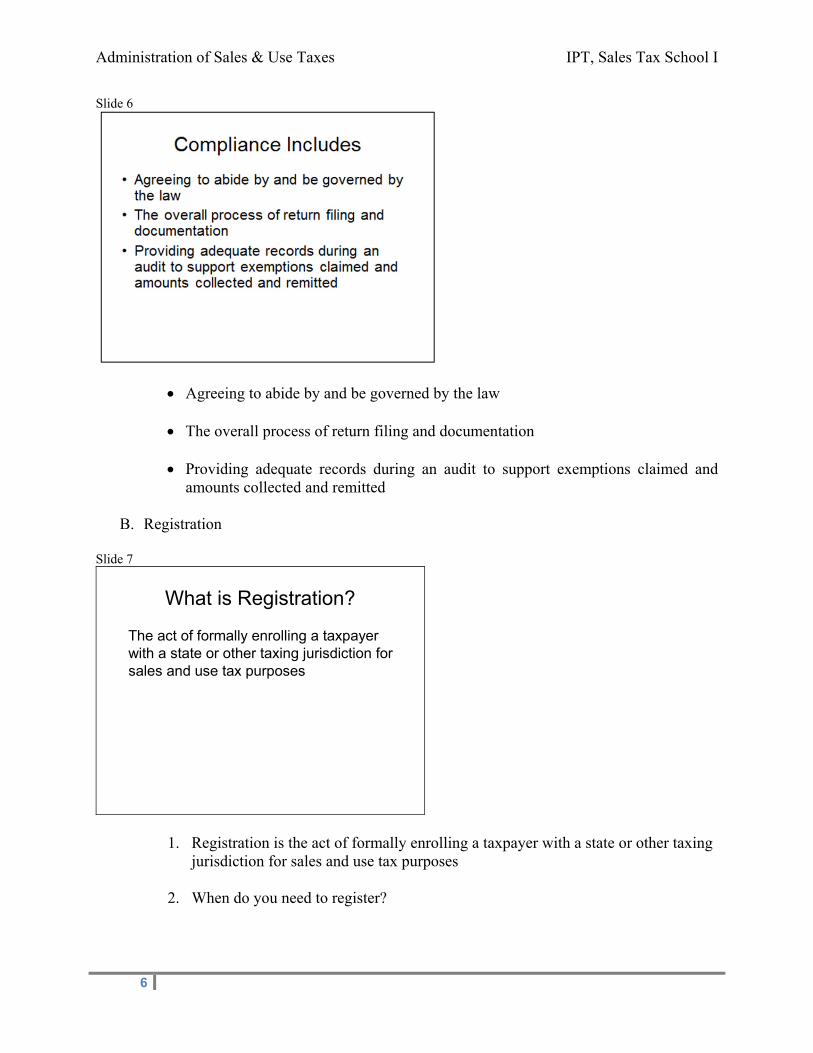

Agreeing to abide by and be governed by the law

The overall process of return filing and documentation

Providing adequate records during an audit to support exemptions claimed and amounts collected and remitted

B. Registration

Slide 7

What is Registration?

The act of formally enrolling a taxpayer with a state or other taxing jurisdiction for sales and use tax purposes

1. Registration is the act of formally enrolling a taxpayer with a state or other taxing jurisdiction for sales and use tax purposes

2. When do you need to register?

MC14

IPT, Sales Tax School I Administration of Sales & Use Taxes

7

Slide 8

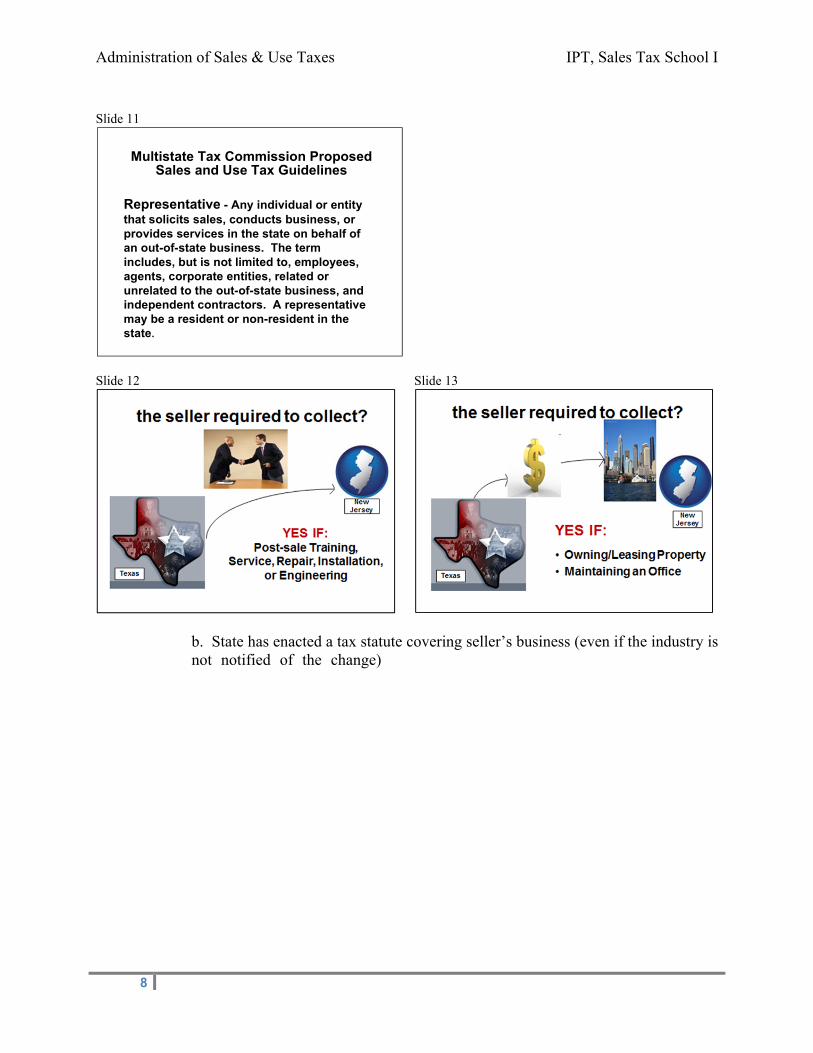

a. Seller is making sales into the state and has nexus with the state (people, property or facilities; includes sales solicitation by commissioned representatives)

Slide 9

Slide 10

REGISTRATION IS REQUIRED IF…

The seller is making sales into thestate and has nexus with the state.

TF47

Administration of Sales & Use Taxes IPT, Sales Tax School I

8

Slide 11

Slide 12

Slide 13

b. State has enacted a tax statute covering seller’s business (even if the industry is

not notified of the change) (such as taxation of real property services or computer services)

Multistate Tax Commission ProposedSales and Use Tax Guidelines

Representative - Any individual or entitythat solicits sales, conducts business, orprovides services in the state on behalf ofan out-of-state business. The termincludes, but is not limited to, employees,agents, corporate entities, related orunrelated to the out-of-state business, andindependent contractors. A representativemay be a resident or non-resident in thestate.

TF59

IPT, Sales Tax School I Administration of Sales & Use Taxes

9

Slide 14

3. How do you register?

Slide 15

a. States require companies or individuals to register for various taxes if they have nexus with the state or municipality.

b. Some states require (or allow) taxpayers to register electronically through

their website. 1) Massachusetts only allows online registration 2) South Carolina has a user friendly online registration program 3) States participating in the Streamlined Sales Tax Project allow

online registration at www.sstregister.org/sellers

REGISTRATION IS REQUIREDIF…

The state has enacted a taxstatute covering seller’s business.

Example: Real Property Services Data Processing

TF104

Administration of Sales & Use Taxes IPT, Sales Tax School I

10

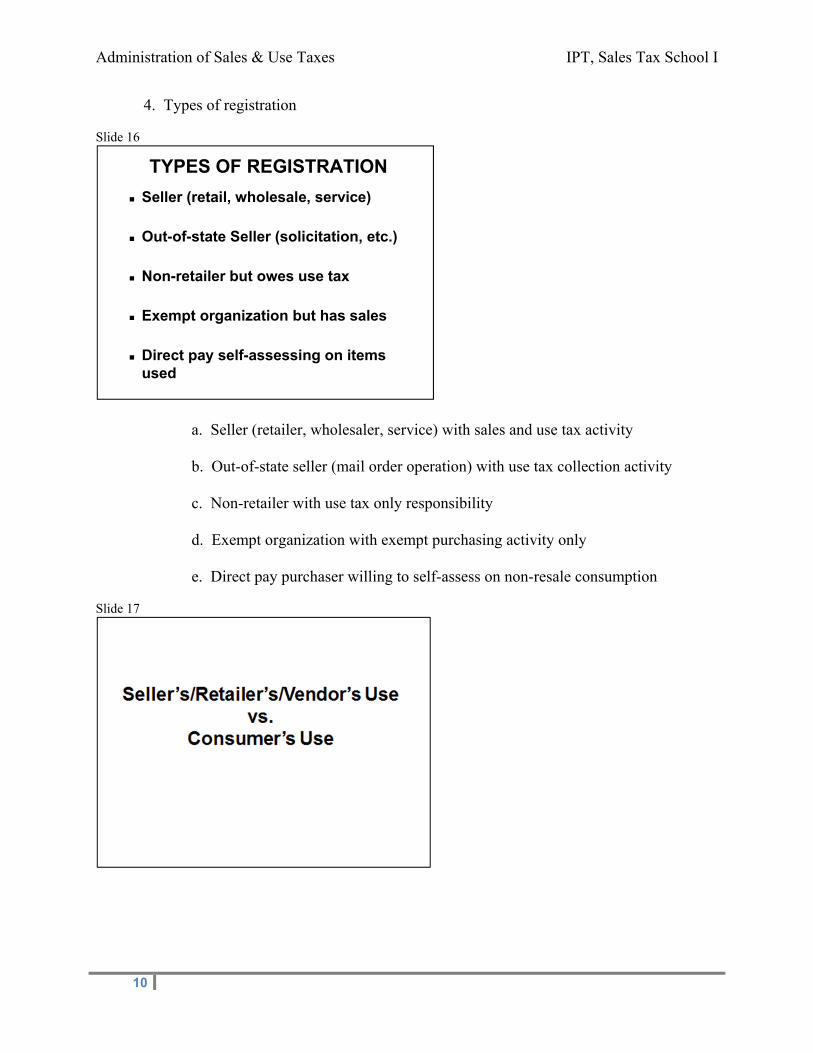

4. Types of registration Slide 16

a. Seller (retailer, wholesaler, service) with sales and use tax activity b. Out-of-state seller (mail order operation) with use tax collection activity c. Non-retailer with use tax only responsibility d. Exempt organization with exempt purchasing activity only e. Direct pay purchaser willing to self-assess on non-resale consumption Slide 17

TYPES OF REGISTRATION

Seller (retail, wholesale, service)

Out-of-state Seller (solicitation, etc.)

Non-retailer but owes use tax

Exempt organization but has sales

Direct pay self-assessing on itemsused

IPT, Sales Tax School I Administration of Sales & Use Taxes

11

Slide 18

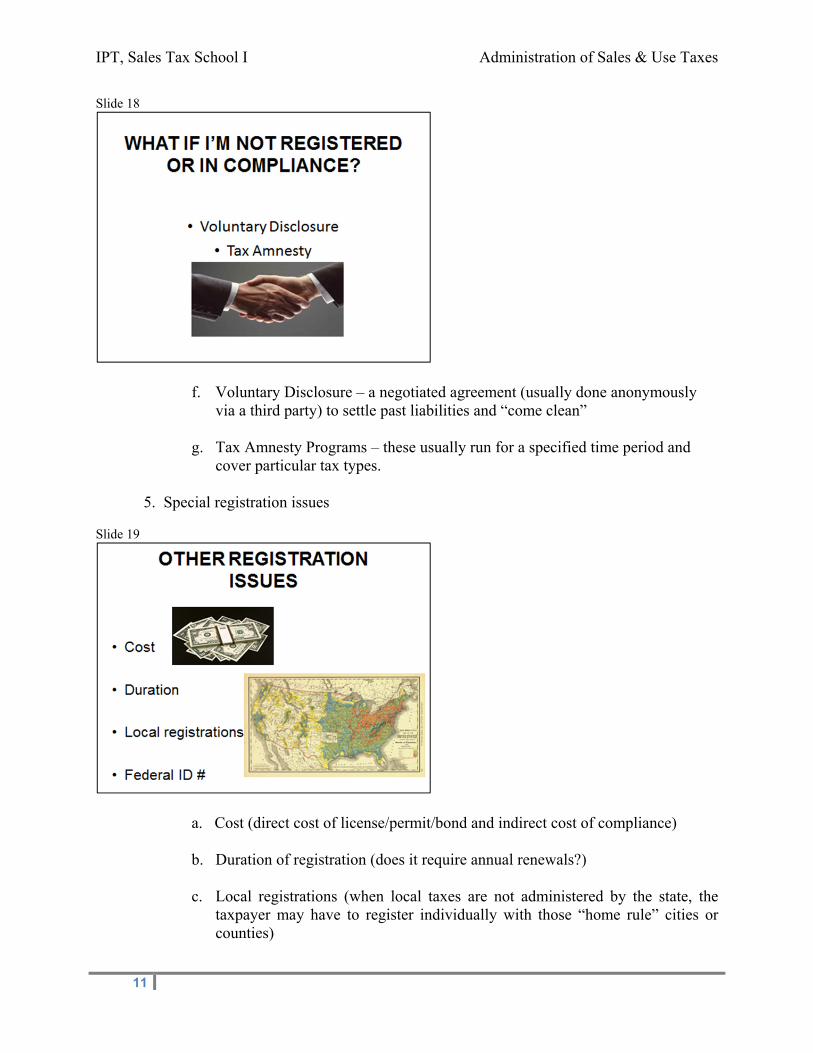

f. Voluntary Disclosure – a negotiated agreement (usually done anonymously via a third party) to settle past liabilities and “come clean”

g. Tax Amnesty Programs – these usually run for a specified time period and

cover particular tax types.

5. Special registration issues Slide 19

a. Cost (direct cost of license/permit/bond and indirect cost of compliance) b. Duration of registration (does it require annual renewals?) c. Local registrations (when local taxes are not administered by the state, the

taxpayer may have to register individually with those “home rule” cities or counties) (examples: Colorado, Arizona, Alabama, Louisiana)

TF51

Administration of Sales & Use Taxes IPT, Sales Tax School I

12

d. Registering for sales/use tax is not the same thing as applying for a business license or qualifying to do business in a state. A Federal ID number is not the same as a sales and use tax registration number (although a State may happen to assign the Federal ID number as the sales and use tax registration number once registration has occurred). (may vary widely from state to state)

e. Some states require separate registration for each location and do not allow

registration certificates to be transferred from one location to another

6. Result of Registration Process Slide 20

TF45

TF16

IPT, Sales Tax School I Administration of Sales & Use Taxes

13

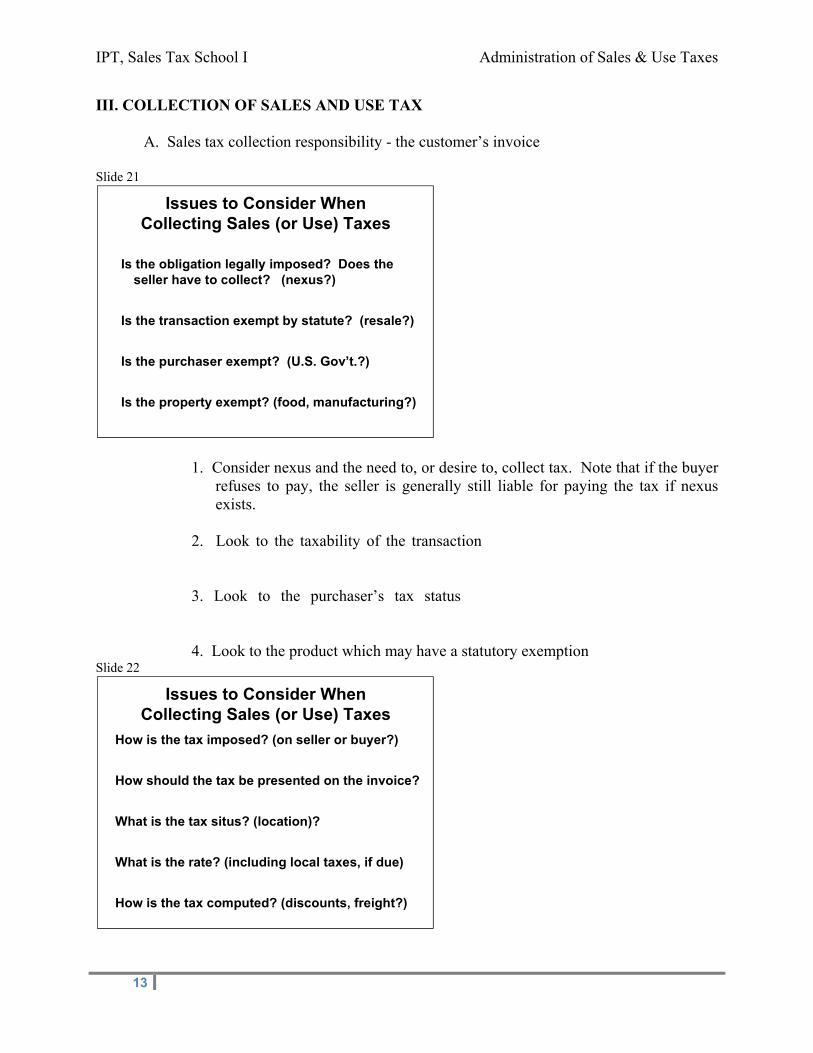

III. COLLECTION OF SALES AND USE TAX A. Sales tax collection responsibility - the customer’s invoice Slide 21

1. Consider nexus and the need to, or desire to, collect tax. Note that if the buyer refuses to pay, the seller is generally still liable for paying the tax if nexus exists.

2. Look to the taxability of the transaction (as represented by the appropriate

documentation)

3. Look to the purchaser’s tax status (as represented by the appropriate documentation)

4. Look to the product which may have a statutory exemption Slide 22

Issues to Consider WhenCollecting Sales (or Use) Taxes

Is the obligation legally imposed? Does the seller have to collect? (nexus?)

Is the transaction exempt by statute? (resale?)

Is the purchaser exempt? (U.S. Gov’t.?)

Is the property exempt? (food, manufacturing?)

Issues to Consider WhenCollecting Sales (or Use) Taxes

How is the tax imposed? (on seller or buyer?)

How should the tax be presented on the invoice?

What is the tax situs? (location)?

What is the rate? (including local taxes, if due)

How is the tax computed? (discounts, freight?)

MC53

Administration of Sales & Use Taxes IPT, Sales Tax School I

14

5. Look to imposition section of the law (this explains on what the tax is imposed) -- on seller, on transaction, on consumer, on gross receipts

6. Consider the manner of the presentation -- separate tax from value of sale,

possibly absorb tax, shift the tax burden to the customer 7. Type of tax to be collected and sales location -- proper state or locality

a. Destination (ship to)

b. Origination (ship from)

c. Place of principle negotiation (sales office, main office, salesperson’s car)

d. Place of service (service center or depot v. customer’s location)

8. Rate of tax and tracking to the general ledger for reporting purposes

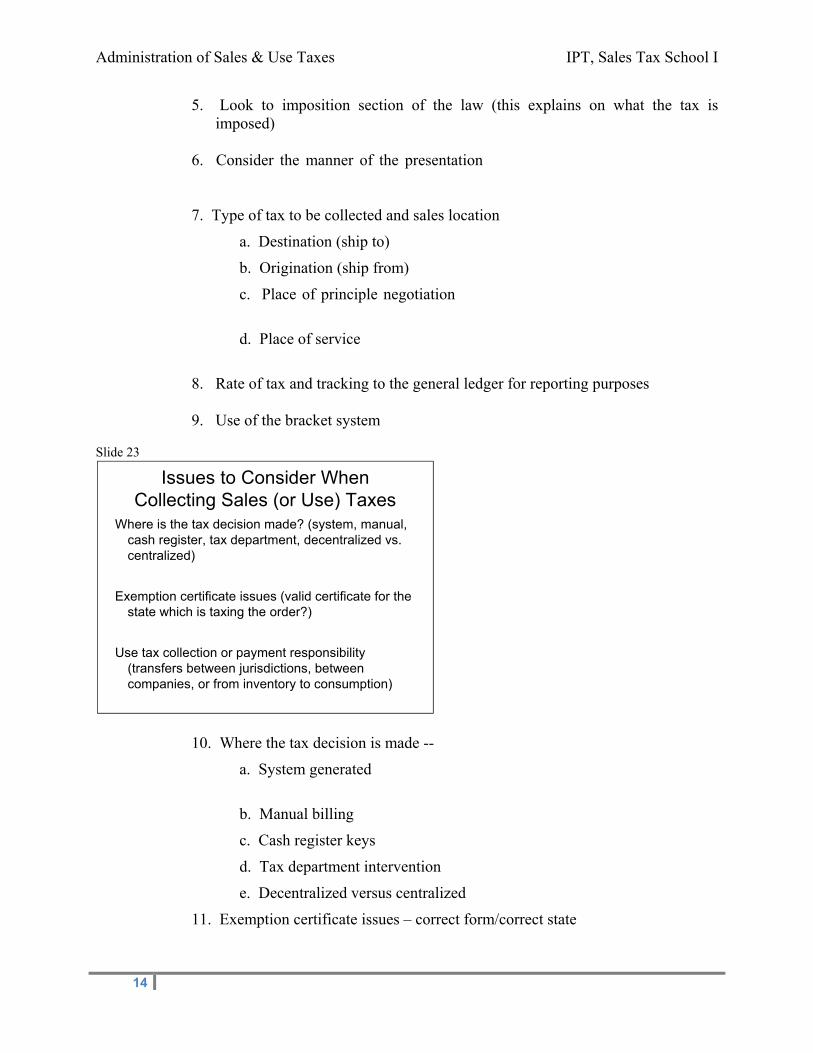

9. Use of the bracket system Slide 23

10. Where the tax decision is made --

a. System generated (item table, taxability table, ship-to address, and tax rate computation table)

b. Manual billing

c. Cash register keys

d. Tax department intervention

e. Decentralized versus centralized

11. Exemption certificate issues – correct form/correct state

Issues to Consider When Collecting Sales (or Use) Taxes

Where is the tax decision made? (system, manual, cash register, tax department, decentralized vs. centralized)

Exemption certificate issues (valid certificate for the state which is taxing the order?)

Use tax collection or payment responsibility (transfers between jurisdictions, between companies, or from inventory to consumption)

TF 54

IPT, Sales Tax School I Administration of Sales & Use Taxes

15

B. Use tax collection or payment responsibility

1. Transfers between jurisdictions within the same company -- journal voucher.

2. Transfers (sales) between companies within or between jurisdictions -- sales invoices or intercompany accounts receivable.

3. Transfers of property from inventory of self-consumption -- journal voucher.

4. Use tax collected from customers -- normal billing system -- are you properly registered?

5. Reciprocity -- is the tax really due?

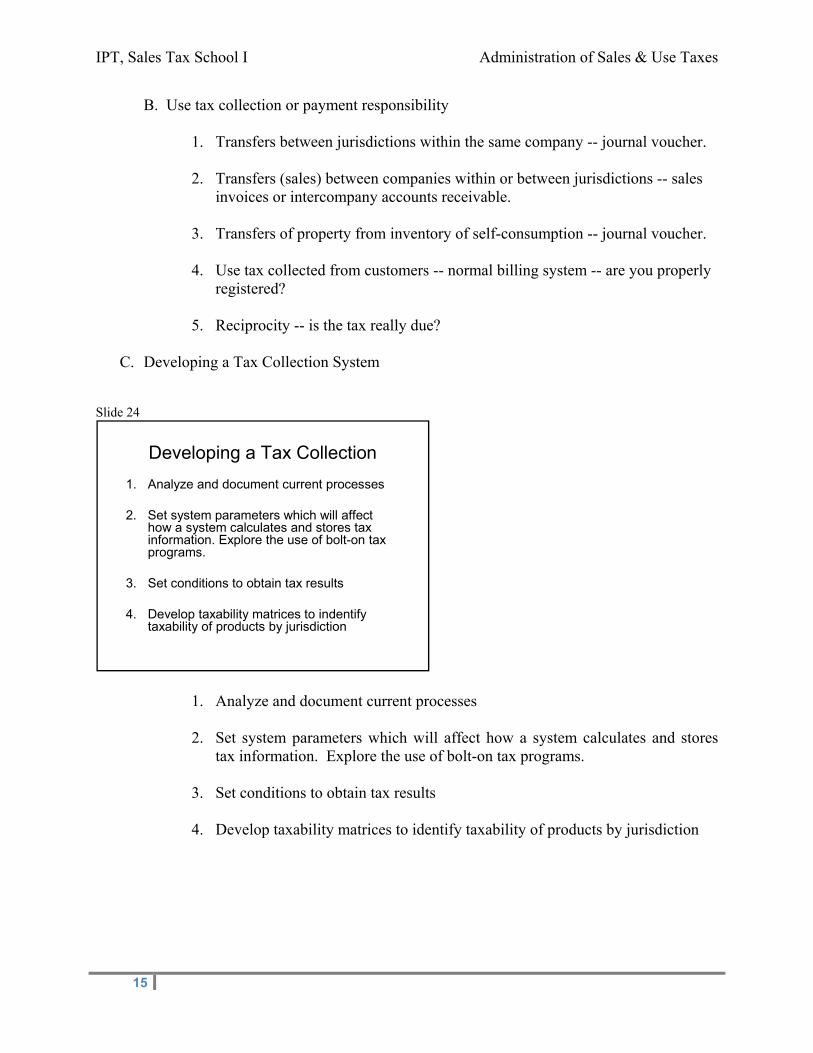

C. Developing a Tax Collection System Slide 24

1. Analyze and document current processes

2. Set system parameters which will affect how a system calculates and stores

tax information. Explore the use of bolt-on tax programs. 3. Set conditions to obtain tax results 4. Develop taxability matrices to identify taxability of products by jurisdiction

Developing a Tax Collection

1. Analyze and document current processes

2. Set system parameters which will affect how a system calculates and stores tax information. Explore the use of bolt-on tax programs.

3. Set conditions to obtain tax results

4. Develop taxability matrices to indentify taxability of products by jurisdiction

TF120

Administration of Sales & Use Taxes IPT, Sales Tax School I

16

Slide 25

5. Organize and manage exemption documentation and registration information 6. Create reporting and/or audit data files 7. Consider automation of tax reporting directly from reporting database

8. Update processes and procedures and train personnel on the use of the system

D. Filing & Reporting Requirements Slide 26

IPT, Sales Tax School I Administration of Sales & Use Taxes

17

1. Return Filing Requirements:

Each state has set requirements for when a return is due. Most state returns are due on the 20th of the month.

2. Prepayment Requirements:

Some states have prepayment requirements depending upon the company’s liability. (CA requires a quarterly return with monthly prepayments for certain taxpayers) (MN has a prepayment due each June in addition to the monthly sales/use tax return)

3. Electronic Funds Transfers:

States require certain taxpayer’s to remit liabilities due via Electronic Funds Transfer. Taxpayer’s must coordinate with their bank to ensure that money is electronically transmitted by a certain time. (usually 3 pm of the due date of the return) Note: Thresholds for EFT varies by state. Some states take into consideration all tax types when determining EFT requirements while others may only address sales and use tax.

4. Electronic Filing Requirements or Other Methods:

Some states require (while others allow) taxpayers to file returns electronically. Some states also allow taxpayers to file returns via telephone.

5. Late Filing & Penalties:

States will impose a late filing penalty if a return or payment is received after the due date. Most states consider a return to be timely filed if it is postmarked on or before the due date of the return but some states require the return to be received by the due date to be considered timely filed. Some states may waive penalties for taxpayers that have not had late payments/returns, others may have policies in place that spell out how many times a taxpayer may be late to allow waiver while other states may not allow penalty waivers of any kind.

TF55

Administration of Sales & Use Taxes IPT, Sales Tax School I

18

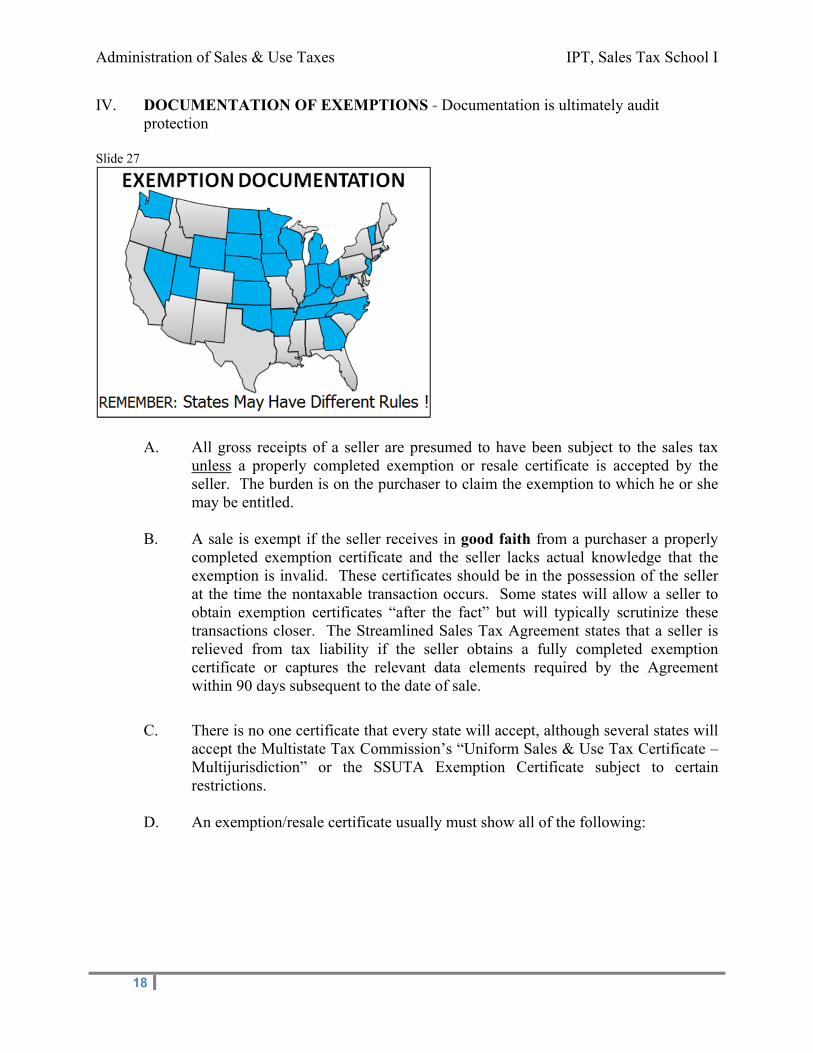

IV. DOCUMENTATION OF EXEMPTIONS - Documentation is ultimately audit protection

Slide 27

A. All gross receipts of a seller are presumed to have been subject to the sales tax

unless a properly completed exemption or resale certificate is accepted by the seller. The burden is on the purchaser to claim the exemption to which he or she may be entitled.

B. A sale is exempt if the seller receives in good faith from a purchaser a properly

completed exemption certificate and the seller lacks actual knowledge that the exemption is invalid. These certificates should be in the possession of the seller at the time the nontaxable transaction occurs. Some states will allow a seller to obtain exemption certificates “after the fact” but will typically scrutinize these transactions closer. The Streamlined Sales Tax Agreement states that a seller is relieved from tax liability if the seller obtains a fully completed exemption certificate or captures the relevant data elements required by the Agreement within 90 days subsequent to the date of sale.

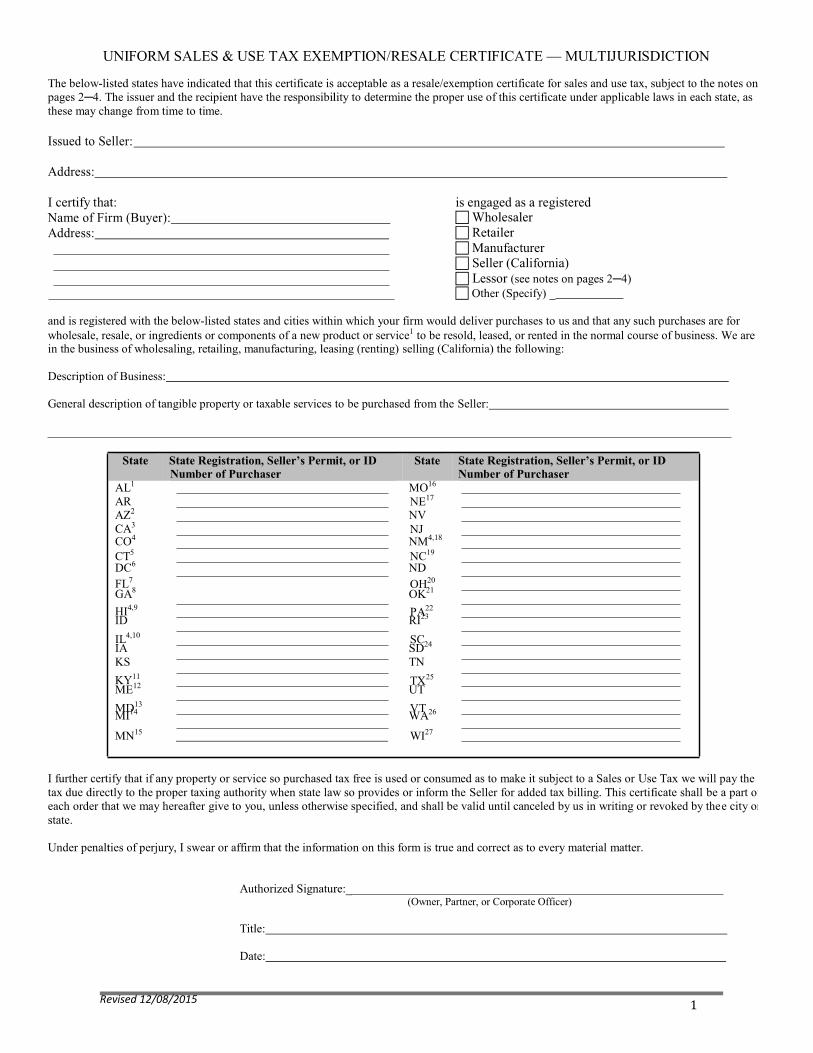

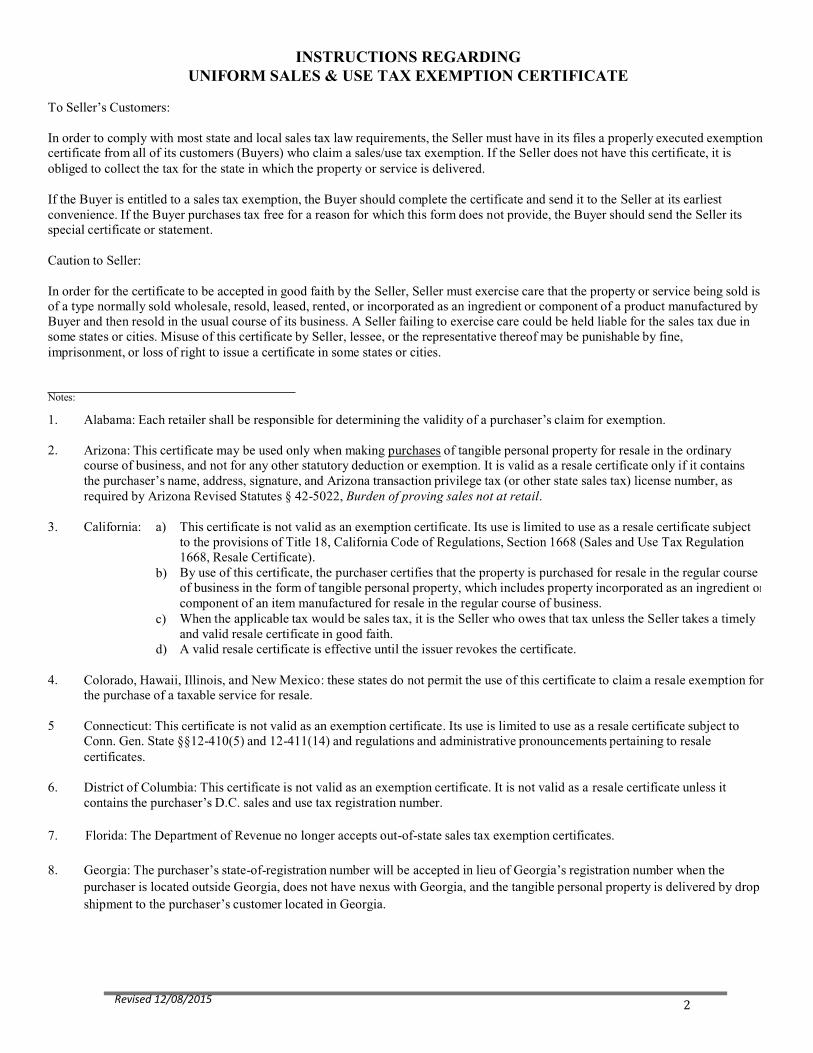

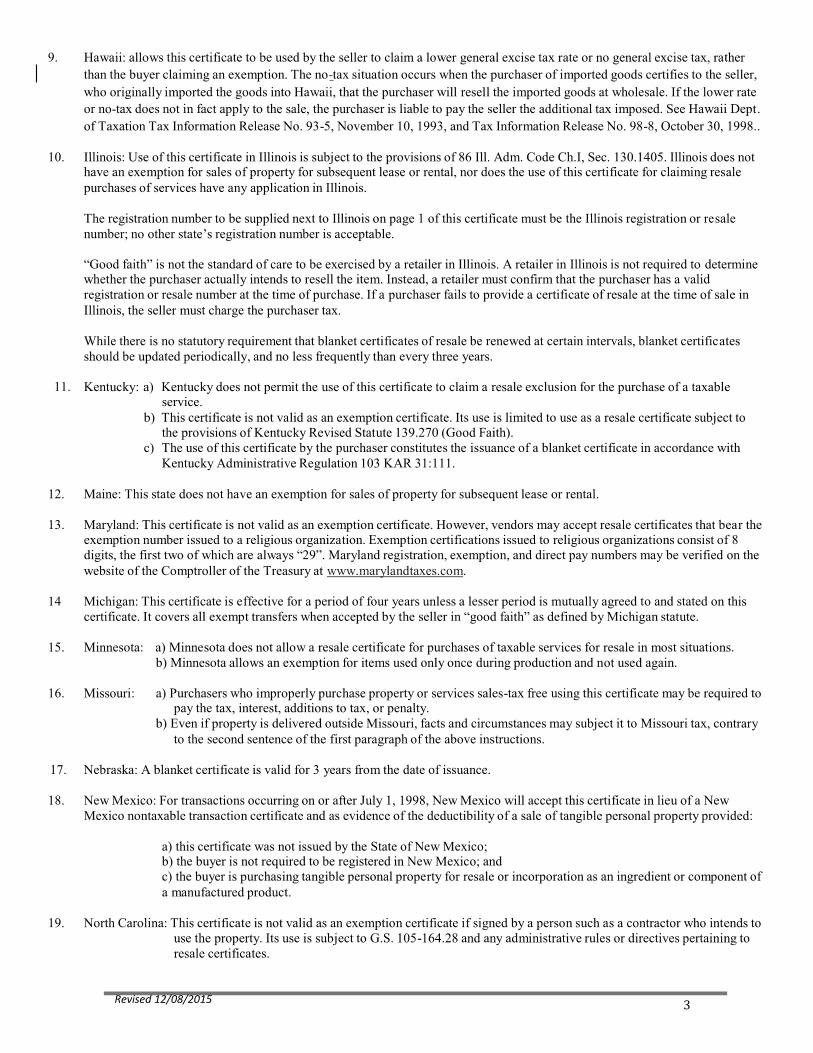

C. There is no one certificate that every state will accept, although several states will accept the Multistate Tax Commission’s “Uniform Sales & Use Tax Certificate – Multijurisdiction” or the SSUTA Exemption Certificate subject to certain restrictions.

D. An exemption/resale certificate usually must show all of the following:

TF56

IPT, Sales Tax School I Administration of Sales & Use Taxes

19

Slide 28

Name and address of Purchaser; Seller’s Permit Number (necessary for resale certificates); Name and address of the seller; Description of Purchaser’s Business; Description of Property being purchased; Reason the purchase is exempt from tax; and Signature of Purchaser and the date.

E. Many states provide that an offense is committed by a person who (1)

intentionally or knowingly makes a false entry in, or a fraudulent alteration of a resale or exemption certificate, (2) makes, presents, or uses an exemption or resale certificate with knowledge that it is false and with the intent that it be accepted as a valid certificate, or (3) intentionally conceals, removes, or impairs the verity of legibility of an exemption or resale certificate or unreasonably impedes the availability of a certificate.

F. Exemption certificates should be filed alphabetically by state. This ensures easy accessibility to certificates for a particular state upon audit. Also, because of the various renewal requirements for each state, this methodology will simplify the renewal process. If a multijurisdictional form is presented, then it will be necessary to make a copy for each of the prospective states.

G. Generally, an audit period is in three or four year cycles. All relevant books and

records necessary to determine the amount of tax liability should be maintained for a period not less than four years. Often, an auditor will request the taxpayer to extend the statute of limitations; therefore, it is recommended that records be retained for a period no less than seven years.

MC29

Administration of Sales & Use Taxes IPT, Sales Tax School I

20

Slide 29

H. Notes of Caution

Verify that the certificate uses the state’s wording “See Purchase Order” is a red flag Update certificates on a regular basis Subsidiaries must issue separate resale certificates Be sure the “sold to” name matches the name on the certificate Blanket certificate vs. unit certificate. “Blanket certificate” is from a

purchaser covering all purchases and a “Unit Certificate” is from a purchaser covering a specific order only. Make sure your order processing personnel and system understand the difference between the two types of certificates

Verbal representation – verbal representation that a purchase “is for resale” is not acceptable for not taxing the sale.

Again, there is no universal resale certificate, however, some states will accept the Multistate Tax Commission’s “Uniform Sales & Use Tax Certificate – Multijurisdiction” or SSUTA Exemption Certificate subject to certain restrictions

MC54

IPT, Sales Tax School I Administration of Sales & Use Taxes

21

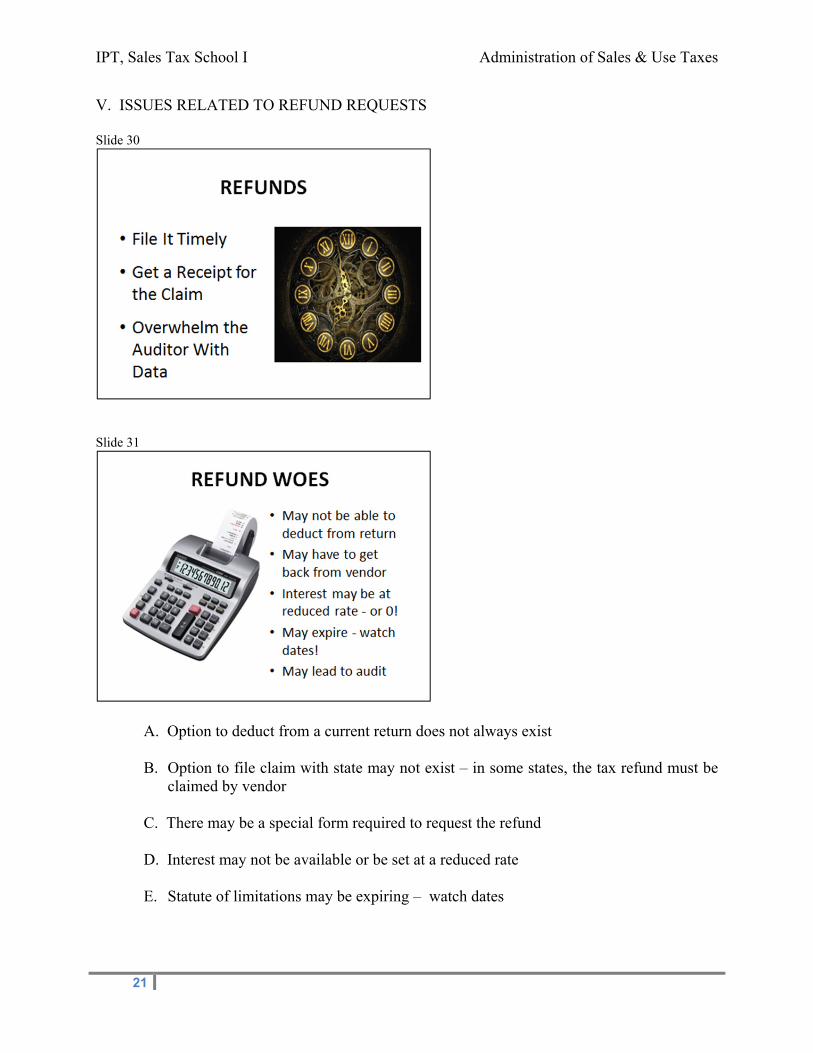

V. ISSUES RELATED TO REFUND REQUESTS Slide 30

Slide 31

A. Option to deduct from a current return does not always exist

B. Option to file claim with state may not exist – in some states, the tax refund must be claimed by vendor

C. There may be a special form required to request the refund D. Interest may not be available or be set at a reduced rate

E. Statute of limitations may be expiring – watch dates

MC55

TF20

Administration of Sales & Use Taxes IPT, Sales Tax School I

22

F. Correspondence should be sent certified, return receipt. Note that, like returns, in some states the claim must be received on or before the due date, not just postmarked on or before the due date.

G. May result in an audit 1. Full field audit 2. Desk audit 3. Refund audit only H. Claims to vendors may strain relations if handled poorly

I. Credit memoranda - Cash refunds may not be given - credit memoranda only (which may be saleable to other taxpayers)

J. In the case of audits 1. May require a formal claim for refund 2. Auditor may require taxpayer to schedule credits 3. Sampling to gain a refund may not be allowed 4. Determination will be final without formal protest 5. May require a payment and suit for refund VI. TAX ACCOUNTING AND CONTROLS - SARBANES-OXLEY

A. Because the sales/use tax processes have a material impact on the accuracy of financial reporting, tax department operations are subject to senior management and external auditor scrutiny.

B. Tax function readiness activities must be coordinated with overall company readiness

activities to ensure compliance with Section 404.

Sarbanes Oxley 404 (SOX404) has increased the areas of documentation, segregation of duties and control points in Sales/Use Taxes. Each step in the return processing should be handled by a separate person, and that person should initial and date the appropriate document when they have completed their step such as:

a. Return and/or funds request preparation b. Review of return and/or funds request c. Approval and sign-off of the return and/or funds request by management

IPT, Sales Tax School I Administration of Sales & Use Taxes

23

d. Submission of funds request to Accounts Payable e. Copying and filing of information for taxpayer files f. Mailing or electronic submission of return and/or check/EFT payment

The return processing should also be documented in a central file with the initials and dates being entered by the person completing each step of the process. The segregation of duties incorporates the necessary controls that need to be in place in order to comply with SOX404. Account reconciliation is another area affected by SOX404. The reconciliation should be prepared by a staff member who initials and dates the reconciliation upon completion. The reconciliation should then be reviewed and approved by appropriate management who initial and date the reconciliation. Any journal entries should be entered by a staff member and then submitted to management with appropriate documentation for them to be able to review and approve. The segregation of duties, the control points and the documentation are the key elements for SOX404 in both return processing and account reconciliation.

C. Sales/Use Tax Internal Controls Readiness Review Slide 32

1. Identify locations/business units and sales/use tax processes that affect

significant financial statement account balances. Processes that could be material to a company’s financial reports include data integrity, exemption certificate management, return preparation, tax remittance, audits/appeals and tax planning.

2. Identify the risks related to each significant sales/use tax account (i.e.

aggressive tax planning strategies, failure to register/file in multiple jurisdictions, failure to maintain exemption documentation).

3. Define sales/use tax control objectives in place to minimize identified risks.

TF119

Administration of Sales & Use Taxes IPT, Sales Tax School I

24

4. Identify existing controls activities and institute additional control activities as

necessary. The following words generally indicate the existence of a control: reconcile, review, document, compare, sign-off, authorize, calendar, log, verify and tracking list.

5. Ensure sufficient documentation of the design and operating effectiveness of

the control activities to allow for testing. Testing generally involves interviews of key personnel and examination of supporting documentation.

IPT, Sales Tax School I Administration of Sales & Use Taxes

25

NOTES

Administration of Sales & Use Taxes IPT, Sales Tax School I

26

NOTES

1

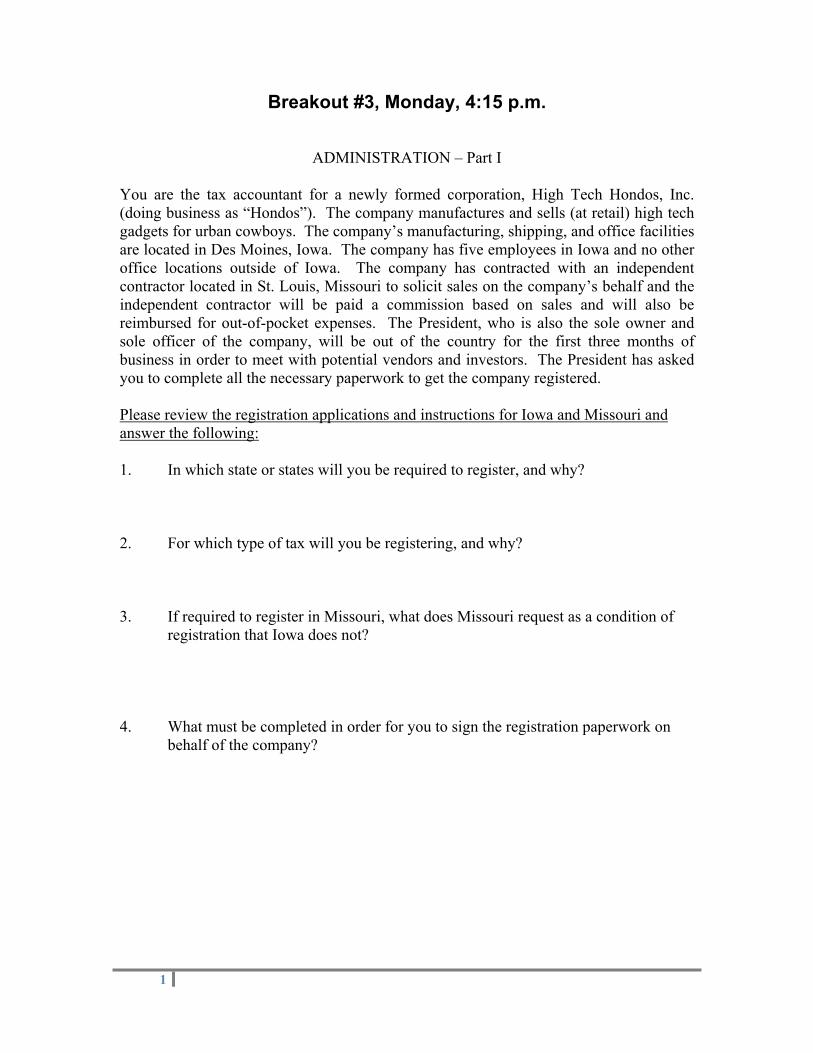

Breakout #3, Monday, 4:15 p.m.

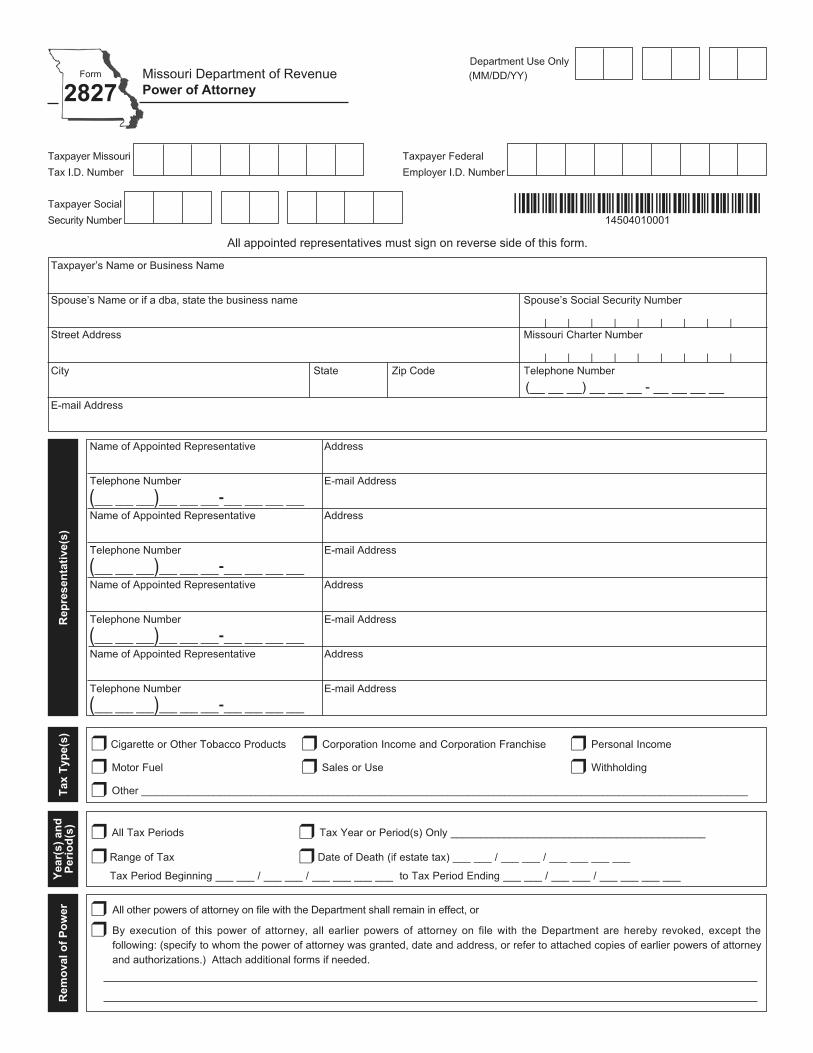

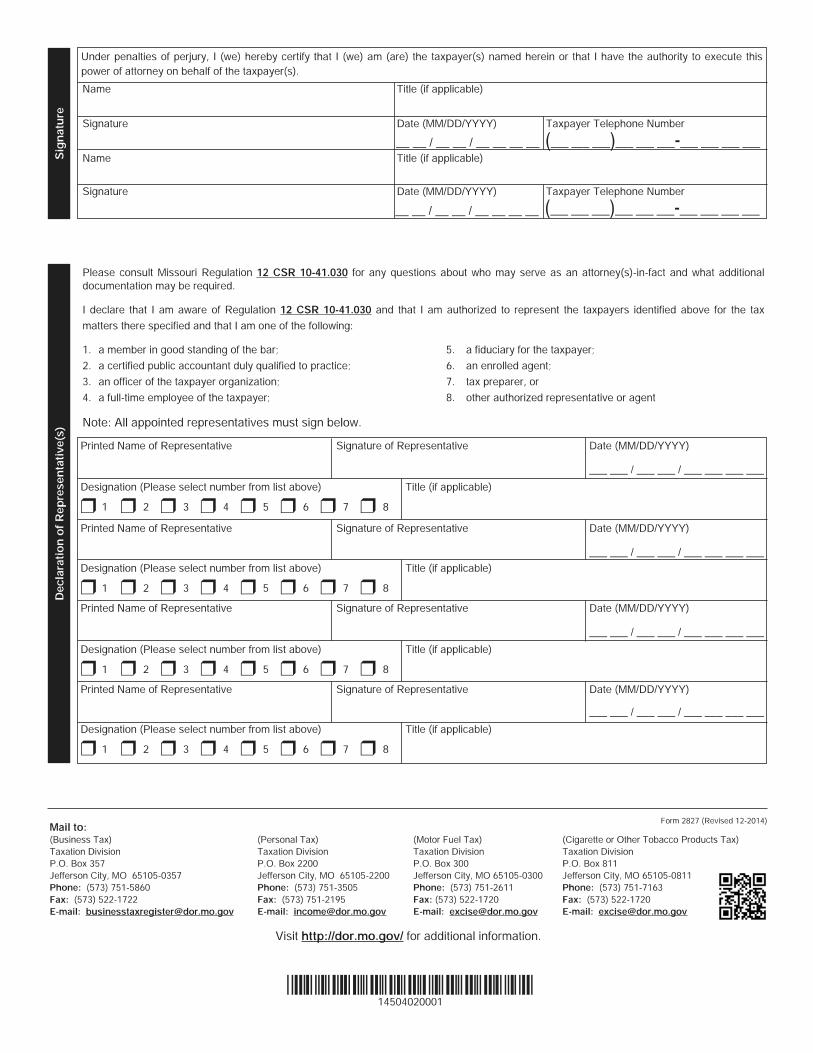

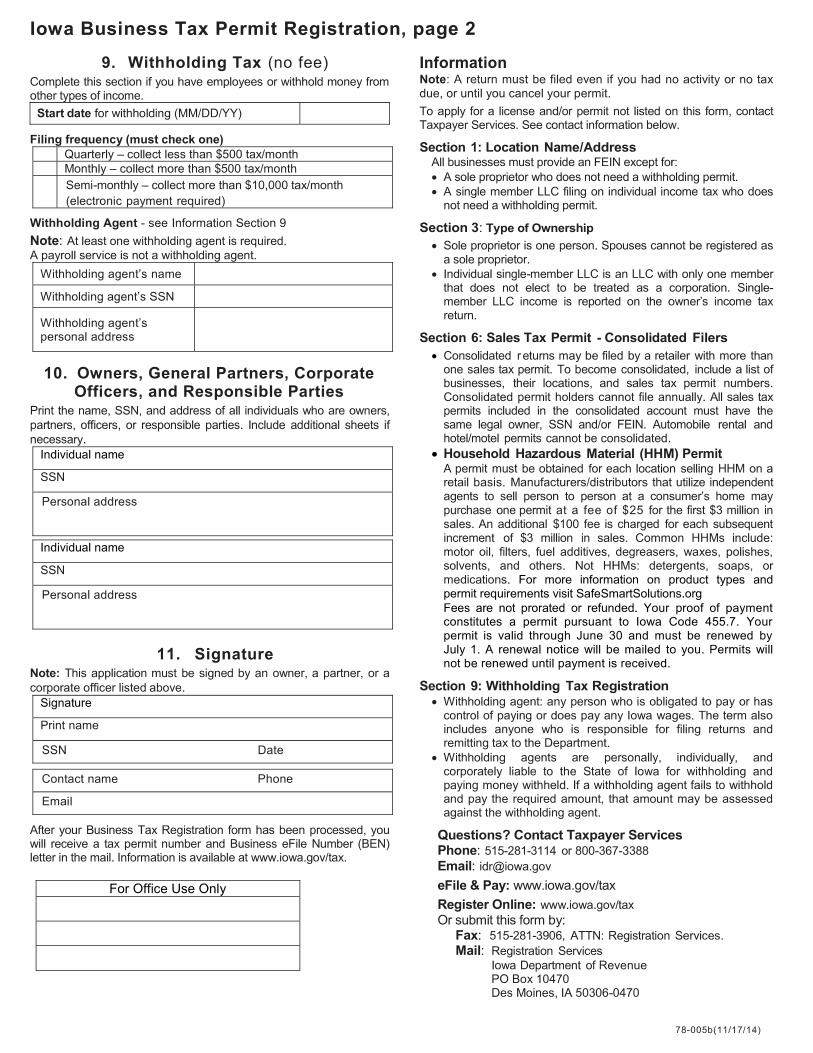

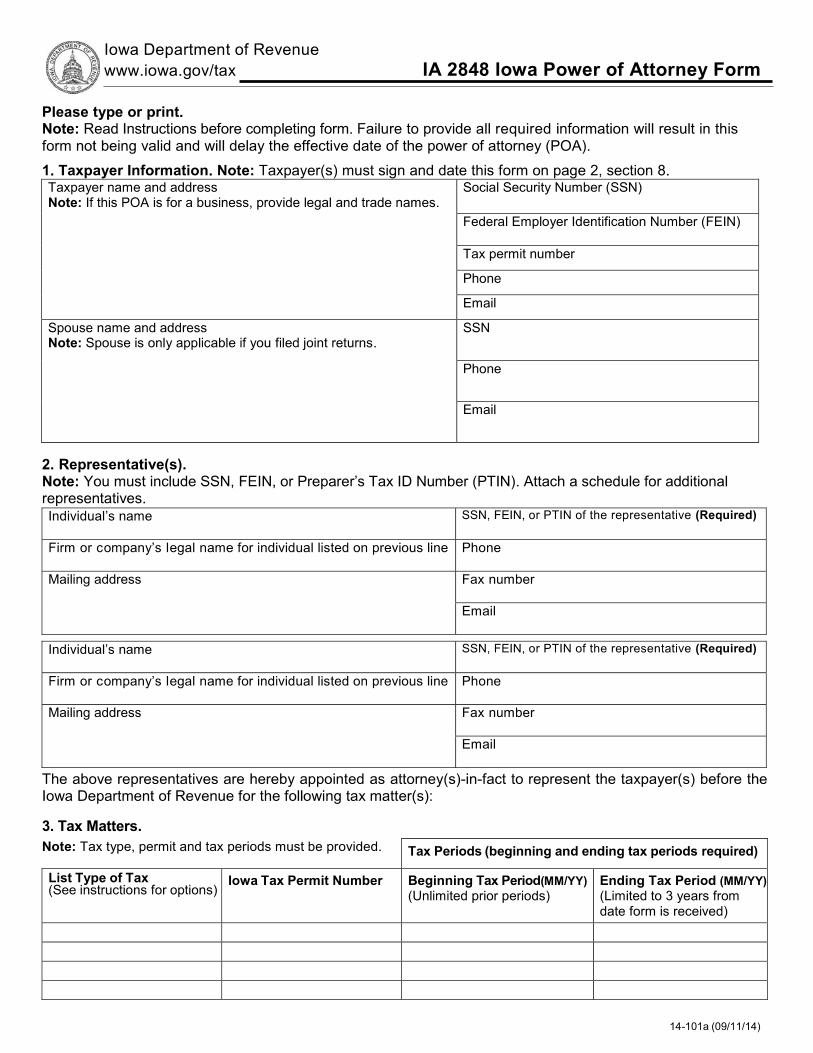

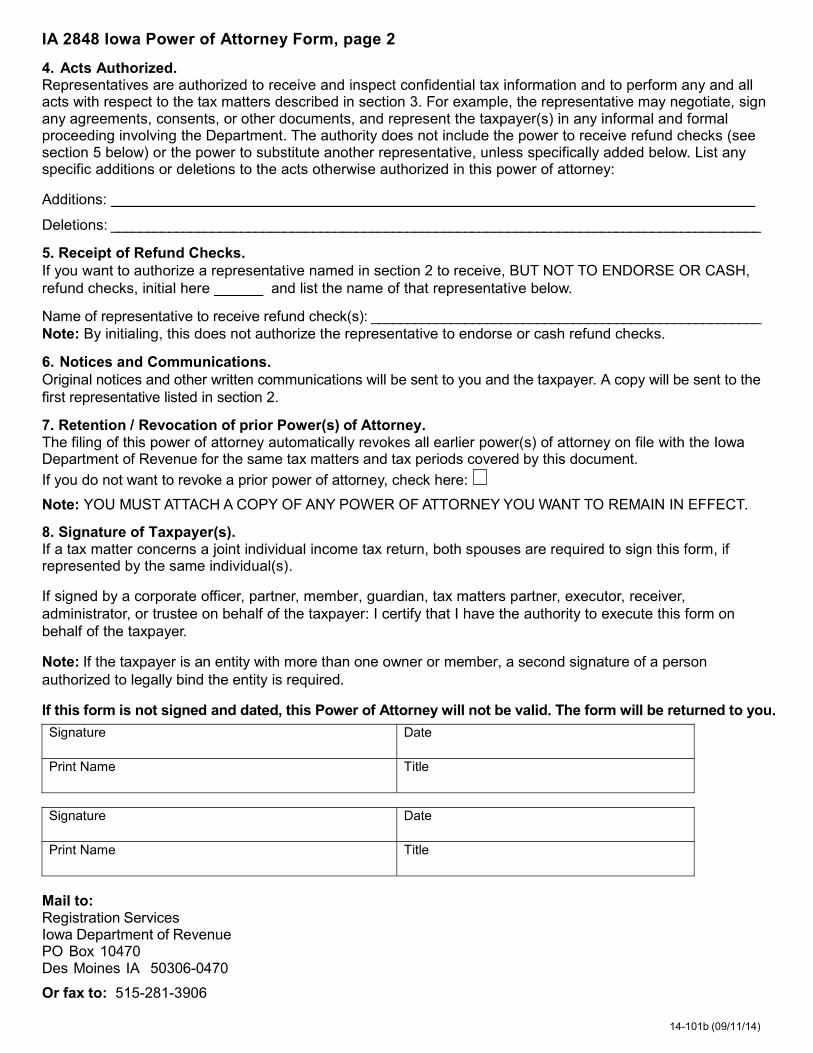

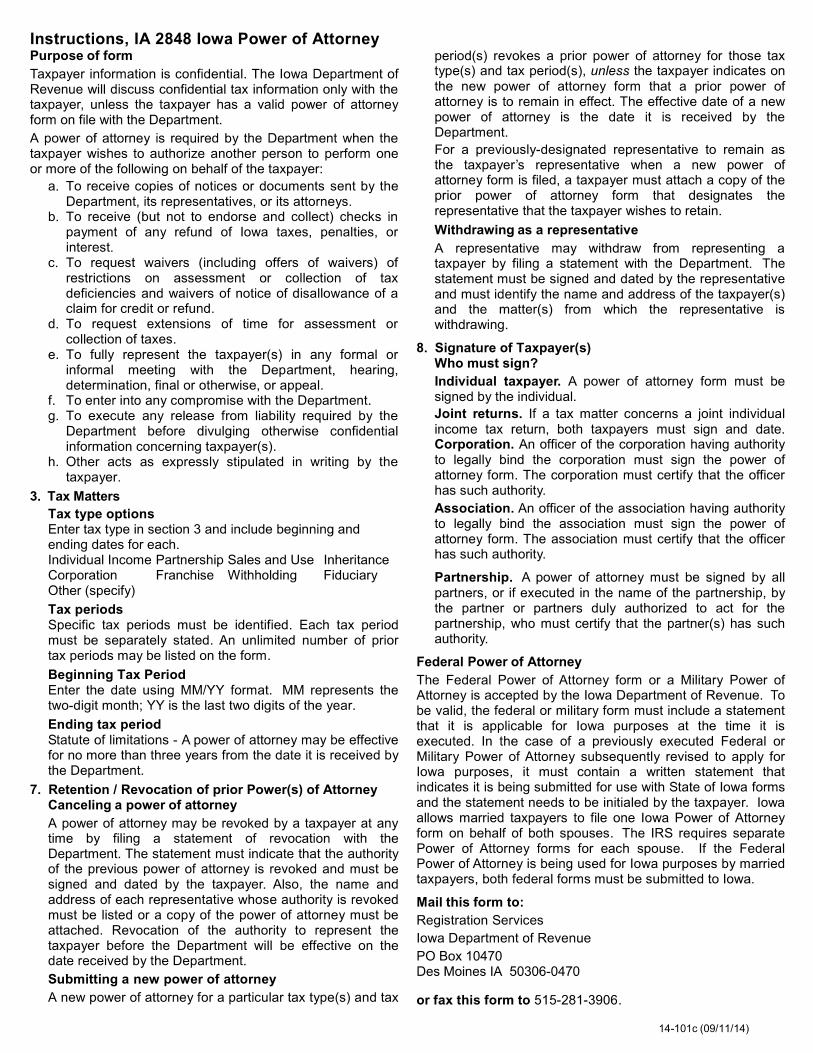

ADMINISTRATION – Part I You are the tax accountant for a newly formed corporation, High Tech Hondos, Inc. (doing business as “Hondos”). The company manufactures and sells (at retail) high tech gadgets for urban cowboys. The company’s manufacturing, shipping, and office facilities are located in Des Moines, Iowa. The company has five employees in Iowa and no other office locations outside of Iowa. The company has contracted with an independent contractor located in St. Louis, Missouri to solicit sales on the company’s behalf and the independent contractor will be paid a commission based on sales and will also be reimbursed for out-of-pocket expenses. The President, who is also the sole owner and sole officer of the company, will be out of the country for the first three months of business in order to meet with potential vendors and investors. The President has asked you to complete all the necessary paperwork to get the company registered. Please review the registration applications and instructions for Iowa and Missouri and answer the following: 1. In which state or states will you be required to register, and why? 2. For which type of tax will you be registering, and why? 3. If required to register in Missouri, what does Missouri request as a condition of

registration that Iowa does not? 4. What must be completed in order for you to sign the registration paperwork on

behalf of the company?

2

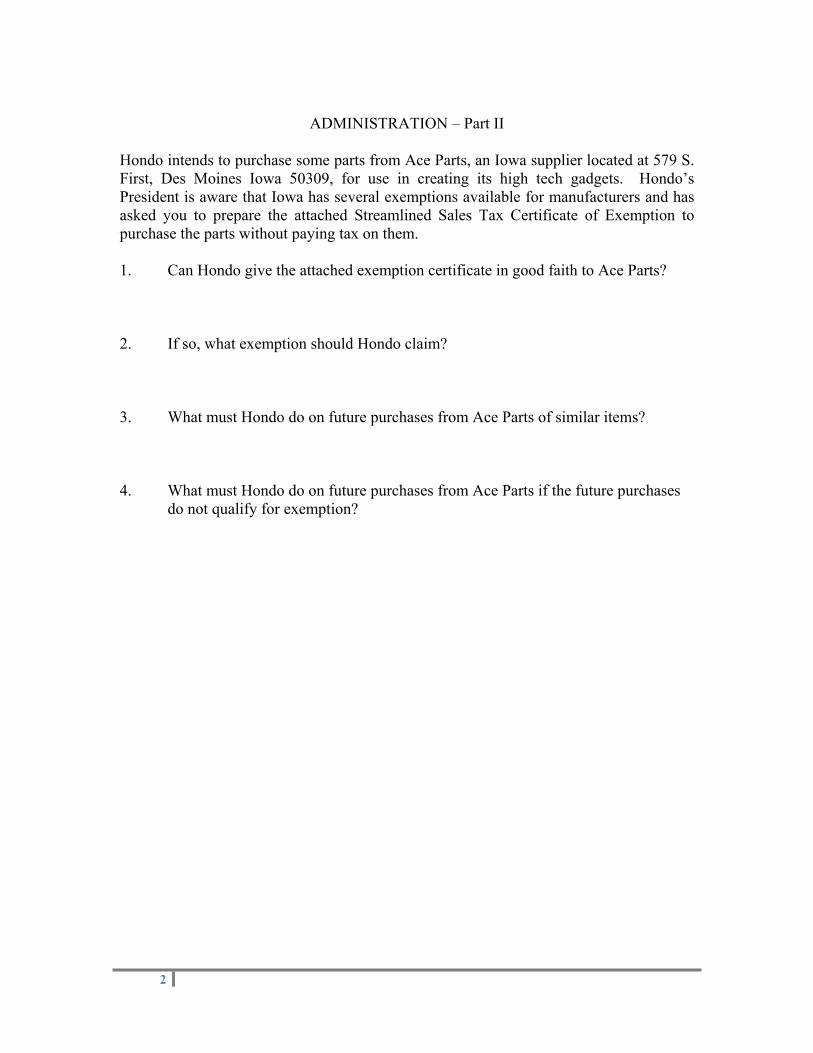

ADMINISTRATION – Part II

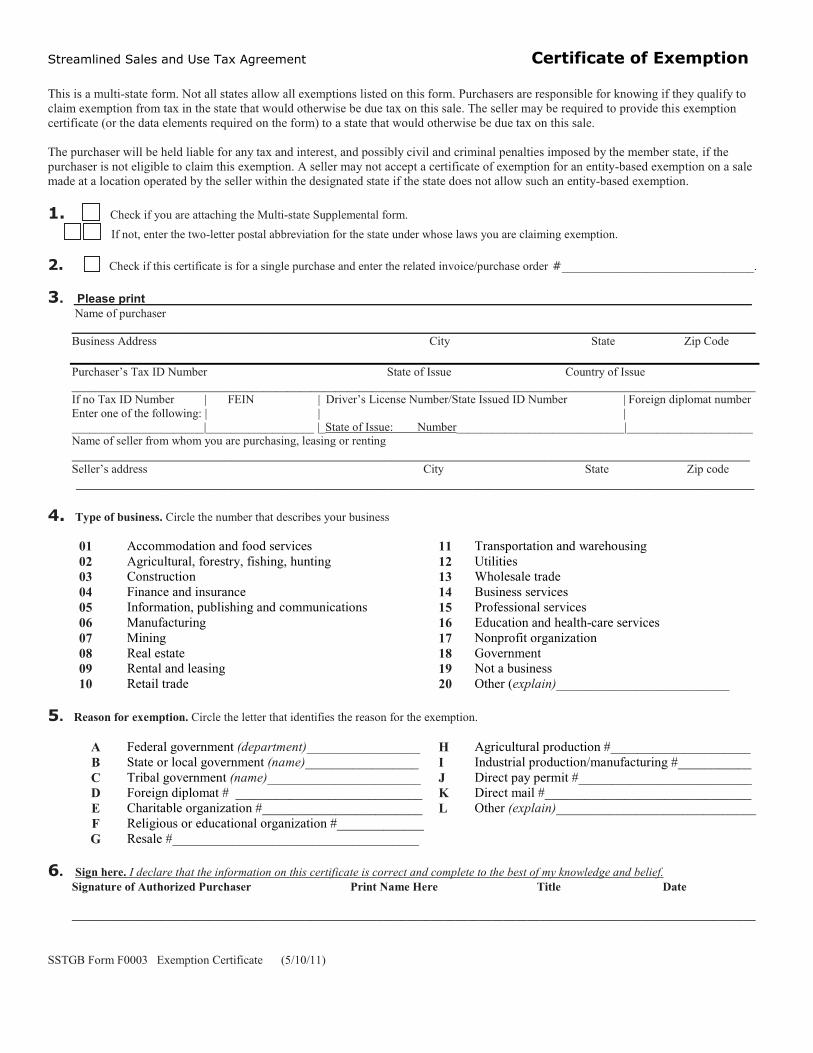

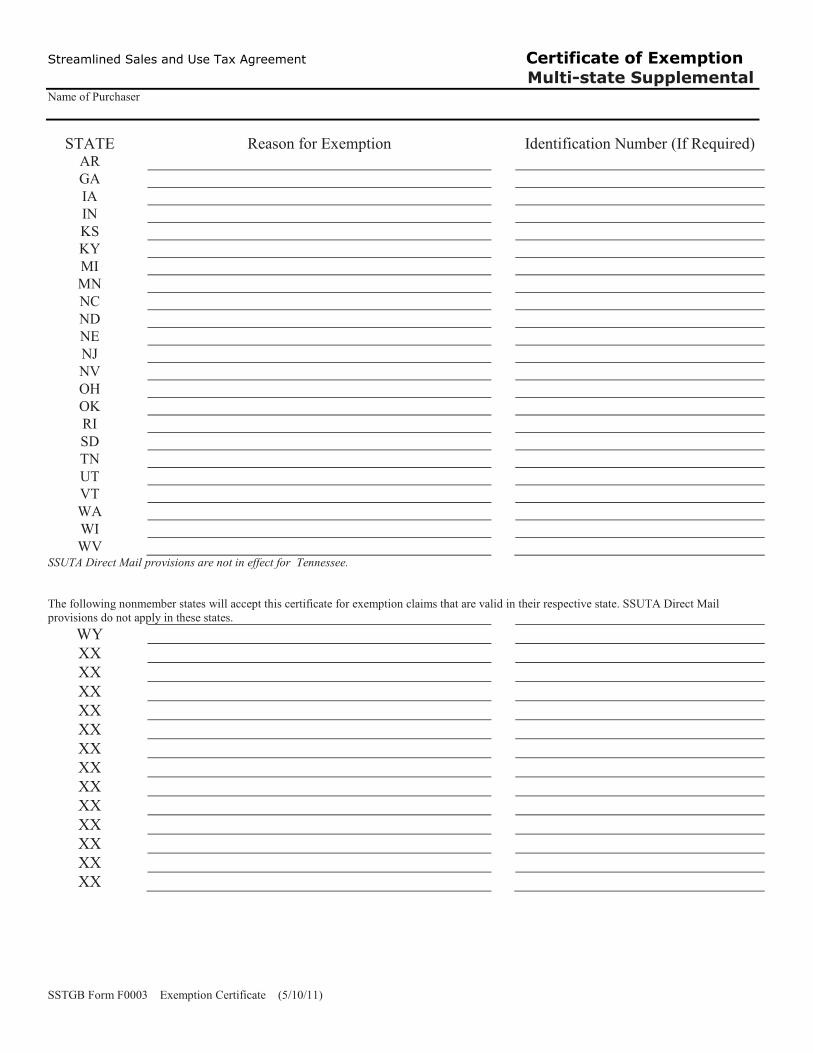

Hondo intends to purchase some parts from Ace Parts, an Iowa supplier located at 579 S. First, Des Moines Iowa 50309, for use in creating its high tech gadgets. Hondo’s President is aware that Iowa has several exemptions available for manufacturers and has asked you to prepare the attached Streamlined Sales Tax Certificate of Exemption to purchase the parts without paying tax on them. 1. Can Hondo give the attached exemption certificate in good faith to Ace Parts?

2. If so, what exemption should Hondo claim?

3. What must Hondo do on future purchases from Ace Parts of similar items?

4. What must Hondo do on future purchases from Ace Parts if the future purchases do not qualify for exemption?

![1]What is value Added Tax or VAT A new form of indirect Tax. A new form of indirect Tax. Replaces sales Tax. Replaces sales Tax. It Taxes only the value](https://img.pdfslide.net/doc/110x75/5516ed5e550346f5558b49d4/1what-is-value-added-tax-or-vat-a-new-form-of-indirect-tax-a-new-form-of-indirect-tax-replaces-sales-tax-replaces-sales-tax-it-taxes-only-the-value.jpg)