Embed Size (px)

Citation preview

PreparedforSaltLakeCity‐DivisionofSustainabilityByCarbaughAssociates,inc.

AUGUST 2013

SALTLAKECITYCULINARYKITCHENBUSINESSINCUBATORSTUDY

2

INTRODUCTION.................................................................................................................. 2

METHODOLOGY ................................................................................................................. 3

Pageleftblank

3

SALTLAKECITYCULINARYKITCHENBUSINESSINCUBATOR

PreparedforSaltLakeCity,DivisionofSustainability

CarbaughAssociates,inc.+Zion’sBankPublicFinance

August18,2013

Whenreferencingthisreport,pleaseuseSaltLakeCity,DivisionofSustainability:CulinaryKitchenBusinessIncubatorStudy,August18,2013.

ENTREPRENURIALBASE/JOBCREATION………………………………………………………………….

INCUBATORASSESSMENTRESULTS………………………………………………………………………….

INCUBATORCASESTUDY…………………………………………………………………………………………

4

Introduction 6

Methodology 7

CurrentMarketFoodTrends 8

ShiftingFoodCulture 9

Income,JobsandFoodSales 11

LocalMarketConditions 12

LocalCommunityEvaluations 13

EconomicOpportunity 21

BestManagementPractices‐Conclusion 24

APPENDIXA–Survey 26 APPENDIXB‐KitchenInventory 32 APPENDIXC‐FundingSources 33

ENDNOTES 34

ArticleI. TableofContents

5

Pageleftblank

INTRODUCTION

6

IncitiesandtownsaroundtheUnitedStates,atypeofbusinessincubatorfocusedonfoodproductionischanginghowfoodentrepreneursgettheirstart.Thesebusinessincubators,calledculinaryincubatorkitchens,oracceleratorkitchens,arelicensed,inspectedcommercialkitchenfacilitieswhereculinaryprocessorspreparefoodand/ornaturalproductsforwholesaleorretailsales.Mostoften,thesefacilitiesareusedbyarangeofexistinglocalspecialtyfoodservices,emergingfoodentrepreneurs,aswellasnaturalproductsbusinessstart‐ups.Anincubatorkitchenisdesignedtogivesmallfoodbusinessesacompetitiveadvantagewhenenteringorcontinuinginthelocalmarketplacebyprovidinganaffordablecertifiedkitchenspace.IncubatorslikeBonnerBusinessCenter,BlueRidgeFoodVentures,TheBusinessIncubatorCenter,andLaCocinaareallexamplesofincubatorswhohelpremoverestrictivebarriersofhighcostcapitalinvestmentassociatedwithleasingorpurchasingakitchenandkitchenequipment.Incubatorsliketheseallowsspecialtyfoodbusinesseslikeprocessors,farmers,caterers,foodcartvendors,andmobilefoodtruckstheopportunitytostartfromnothingandgrow.Aculinaryincubatorkitchenfurtherreducestheriskoffailurebyremovingadditionalstartupbarriersassociatedwithno,orlowskillsintheareasofmanagingandmaintainingonesowncommercialkitchen,aswellas,knowledgegapssurroundingdistribution,branding,marketing,accounting,andfinancing.Knowledgetransferisanimportantcomponenttoincreasingthesuccessforincubatortenants,andawelldevelopedincubatorkitchenprovideseducationandtrainingforemergingfoodentrepreneurstolearnhowtorefinerecipes,testmarkets,expandtheirproductlineandacceleratetheirbusinesscapacitysotheycanoutgrowtheincubator,andeventuallylaunchintothemarketontheirown.Byusingaculinaryincubatorkitchen,foodpurveyor’sbenefitfromcapitalaffordability,aswellasbenefitingfromadditionalknowledgebasedresourceslikeculinarybusinessandtechnicalskillbuildingthathelpsincreasechancesforlongtermbusinesssuccess.Culinarybusinessincubatorsmaybefundedthroughvariousmechanisms,including,public,private,orpublic/privatepartnerships.Additionally,thereareseveralpossibleowner‐operatorformatsforthesefacilitiesandrangefromsolelyownedandoperatedasaprivate,forprofitbusiness,ownedandoperatedbyanon‐profitorganizations,or,theymaybeownedandoperatedthroughsmallbusinessdevelopmentcenters,communityandeconomicdevelopmentcenters(CED’s),aswellasthroughhighereducationfacilities,primarilyuniversitiesfooddevelopmentcentersorextensions.

INTRODUCTION

7

Themethodologytodeterminethefeasibilityofanincubatorincludedfourconfidentialfocusgroupdiscussions,asmallsurveyandcurrentmarketresearch.

AnimportantconsiderationinfindingoutmoreaboutwhetheraSaltLakeCityculinaryincubatorkitchenisrecommendedandrelevantwastoaskcurrentandpotentialfoodprocessorsabouttheirthoughtsregardingtheneedanddemandforsuchafacility.TounderstandmoreaboutthepotentialforaculinaryincubatorkitcheninSaltLakeCity,four,twohour,focusgroupdiscussionswereconvenedduringthemonthsofMarchandMay2013.CarbaughAssociatesrecruitedparticipantswhohavevariousconnectionstolocalfoodandcommunityandincludedpeoplewhoarethinkingaboutstartingaculinarybusiness,thosecurrentlyinvolvedinoperatingaculinarybusiness,suchaslocalcaterers,restaurantowners,foodcartvendors,mobilefoodtruckoperators,inadditionto,localfarmers,fooddistributors,andknowledgeablecommunityleaders.StafffromtheSaltLakeDivisionofSustainabilityandtheSaltLakeCityFoodPolicyTaskForceprovidedadditionalreferralsforparticipants.Atotalof48invitationswereextended,resultinginatotalof24participants.Eachfocusgroupwaspresentedwiththeexactsamesetof10specificquestionsrelatedtothelocalfoodenvironmentandapotentialculinaryincubatorkitchen.Confidentialityallowedindividualstofreelysharetheiropinionsandknowledgeaboutthelocalculinarykitchenenvironmentalongwithfactorstheybelievearecriticaltoanyplanninganddevelopmentofacommunitykitcheninthecity.

Allfocusgroupparticipantsandsurveyrespondentssharedtheirculinaryaffiliationsandinterests.Informationtargetsoftheincubatorinquiryincludedopinionsaboutthelocalfoodenvironment,aswellasfactorsrelatedtoapotentialkitchen.

ImpressionsofSaltLakeCity’sfoodculture Typesoffacilitiescurrentlybeingusedbyemergingfoodbusinesses Whatareequipmentandbuildingneedsthatwillmakeapotentialfacilityuseful? Servicesotherthankitchenspacethatcouldbehelpfulinbuildinguplocalfood

businesses Whoareessentialregulatoryagenciesthatneedtobeconsulted? Identificationofoperator(s)andmanager(s) Inacriticalpathforwardtodeveloping,launching,operating,andmanagingsuch

afacility,whatisthebestroleforSaltLakeCityinanyfuturedevelopmentofaculinaryincubatorkitchen?

WhoismightbethebestoperatorandmanagerforaSaltLakeCitybasedculinaryincubatorkitchen?

Whereisthebestlocationforthispotentialfacility,and Arethereanyreasonswhythedevelopmentofthisfacilityshouldnotmove

forward?

CURRENTMARKETFOODTRENDS

METHODOLOGY

8

8% 2010 US Increase in Organic Food + Drink Sales

10% 2011 Increase in Organic Food + Drink Sales

United States - 2013 Organic Sales 4% of Total Food Sales

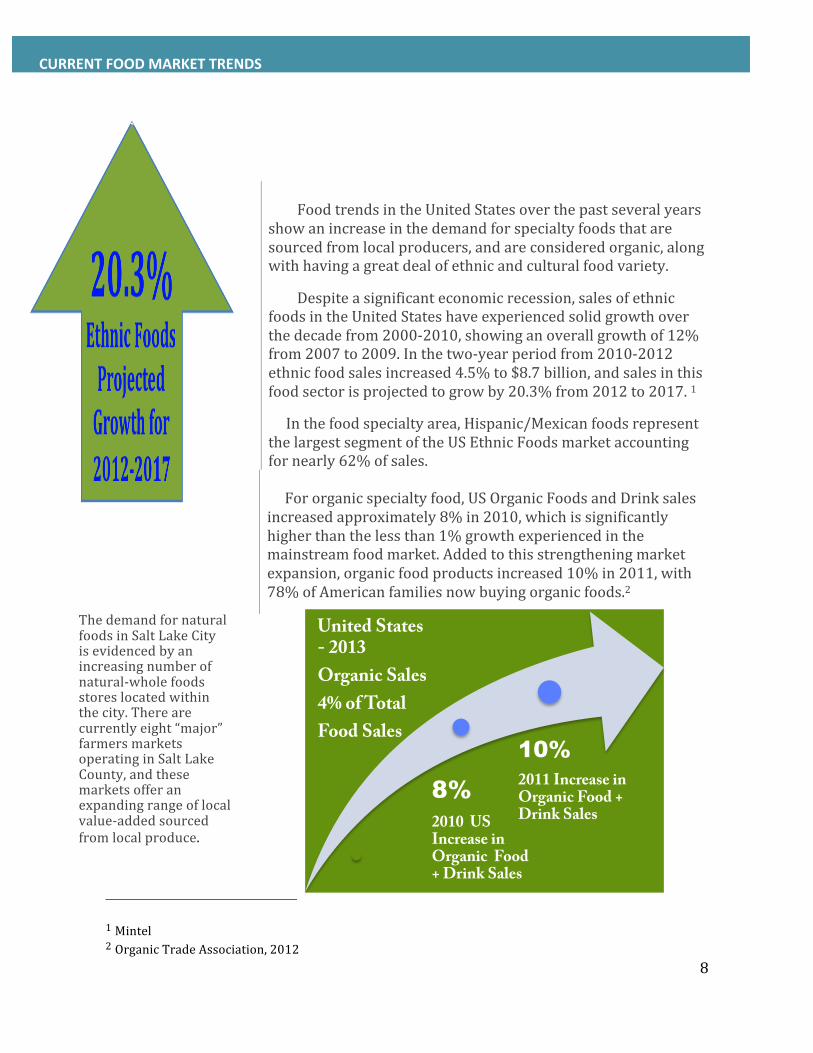

FoodtrendsintheUnitedStatesoverthepastseveralyearsshowanincreaseinthedemandforspecialtyfoodsthataresourcedfromlocalproducers,andareconsideredorganic,alongwithhavingagreatdealofethnicandculturalfoodvariety.

Despiteasignificanteconomicrecession,salesofethnicfoodsintheUnitedStateshaveexperiencedsolidgrowthoverthedecadefrom2000‐2010,showinganoverallgrowthof12%from2007to2009.Inthetwo‐yearperiodfrom2010‐2012ethnicfoodsalesincreased4.5%to$8.7billion,andsalesinthisfoodsectorisprojectedtogrowby20.3%from2012to2017.1

Inthefoodspecialtyarea,Hispanic/MexicanfoodsrepresentthelargestsegmentoftheUSEthnicFoodsmarketaccountingfornearly62%ofsales.Fororganicspecialtyfood,USOrganicFoodsandDrinksalesincreasedapproximately8%in2010,whichissignificantlyhigherthanthelessthan1%growthexperiencedinthemainstreamfoodmarket.Addedtothisstrengtheningmarketexpansion,organicfoodproductsincreased10%in2011,with78%ofAmericanfamiliesnowbuyingorganicfoods.2

1Mintel2OrganicTradeAssociation,2012

ThedemandfornaturalfoodsinSaltLakeCityisevidencedbyanincreasingnumberofnatural‐wholefoodsstoreslocatedwithinthecity.Therearecurrentlyeight“major”farmersmarketsoperatinginSaltLakeCounty,andthesemarketsofferanexpandingrangeoflocalvalue‐addedsourcedfromlocalproduce.

CURRENTFOODMARKETTRENDS

!

!"#$%#&'($))*(+,-%,./(

9

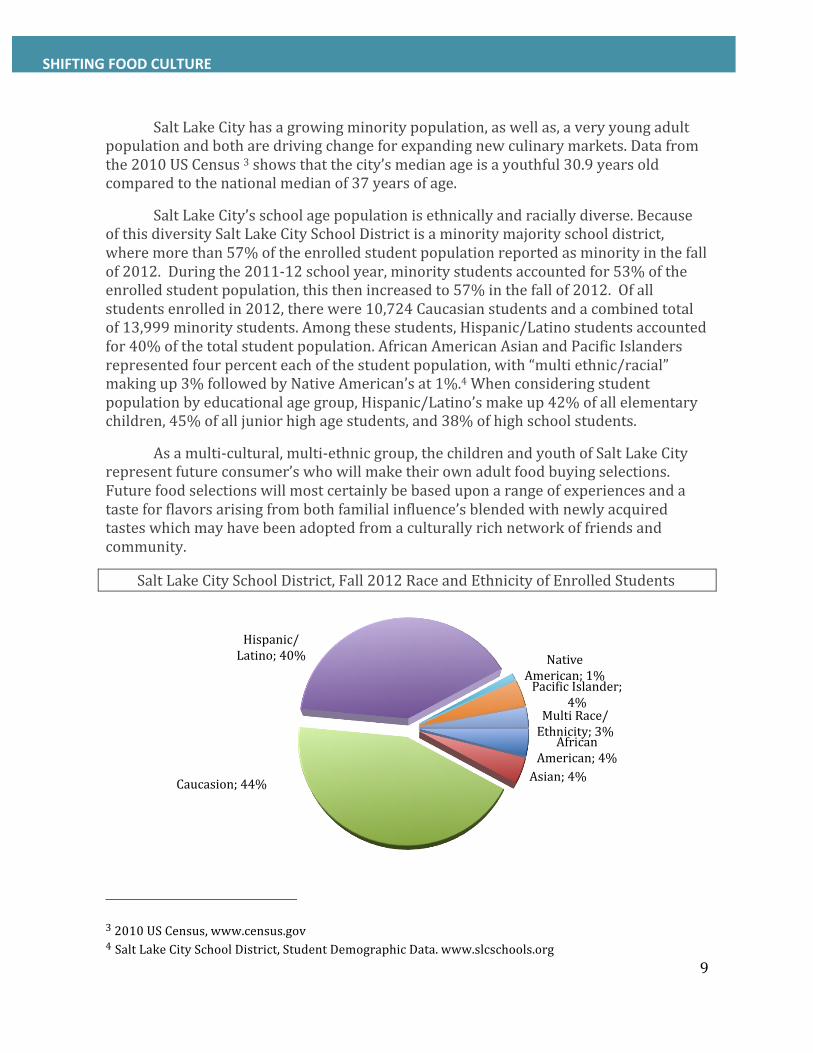

SaltLakeCityhasagrowingminoritypopulation,aswellas,averyyoungadultpopulationandbotharedrivingchangeforexpandingnewculinarymarkets.Datafromthe2010USCensus3showsthatthecity’smedianageisayouthful30.9yearsoldcomparedtothenationalmedianof37yearsofage.

SaltLakeCity’sschoolagepopulationisethnicallyandraciallydiverse.BecauseofthisdiversitySaltLakeCitySchoolDistrictisaminoritymajorityschooldistrict,wheremorethan57%oftheenrolledstudentpopulationreportedasminorityinthefallof2012.Duringthe2011‐12schoolyear,minoritystudentsaccountedfor53%oftheenrolledstudentpopulation,thisthenincreasedto57%inthefallof2012.Ofallstudentsenrolledin2012,therewere10,724Caucasianstudentsandacombinedtotalof13,999minoritystudents.Amongthesestudents,Hispanic/Latinostudentsaccountedfor40%ofthetotalstudentpopulation.AfricanAmericanAsianandPacificIslandersrepresentedfourpercenteachofthestudentpopulation,with“multiethnic/racial”makingup3%followedbyNativeAmerican’sat1%.4Whenconsideringstudentpopulationbyeducationalagegroup,Hispanic/Latino’smakeup42%ofallelementarychildren,45%ofalljuniorhighagestudents,and38%ofhighschoolstudents.

Asamulti‐cultural,multi‐ethnicgroup,thechildrenandyouthofSaltLakeCityrepresentfutureconsumer’swhowillmaketheirownadultfoodbuyingselections.Futurefoodselectionswillmostcertainlybebaseduponarangeofexperiencesandatasteforflavorsarisingfrombothfamilialinfluence’sblendedwithnewlyacquiredtasteswhichmayhavebeenadoptedfromaculturallyrichnetworkoffriendsandcommunity.

SaltLakeCitySchoolDistrict,Fall2012RaceandEthnicityofEnrolledStudents

32010USCensus,www.census.gov4SaltLakeCitySchoolDistrict,StudentDemographicData.www.slcschools.org

AfricanAmerican;4%Asian;4%Caucasion;44%

Hispanic/Latino;40% Native

American;1%PacimicIslander;

4%MultiRace/Ethnicity;3%

SHIFTINGFOODCULTURE

!

!"#$%#&'($))*(+,-%,./(

10

Asarefugeeresettlementcommunity,SaltLakeCityisnowhometoagrowingpopulationofforeignbornresidents.RefugeesfromAfrica,Asia,theMiddleEastandotherregionsaroundtheworldhavearrivedinSaltLakeCitytostartnewlives.EvidenceoftheglobalfoodinfluencearisingfromnewimmigrantscanbeseenintheemergenceofAfricanmarketsandrestaurants,newHalalmarketsandthedevelopmentofsuccessfulimmigrantfarmsandvalueaddedfoods Asisreflectedbytheexpansionoflocalvalueaddedproducts,ethnicmarketsandrestaurants,thelocalconsumerpaletteisbroadening. Foodmarketsareshowntobecloselyrelatedtocommunitydemographics.Nationalfoodtrendsalsohelpinformthepotentialforfoodinthelocalmarket.AndgivenSaltLakeCity’syouthfulness,itsculturalandclassdistinctions,demandforanexpandingrangeofethnic,organicandotherspecialtyfoodsshouldbeexpectedtogrow.

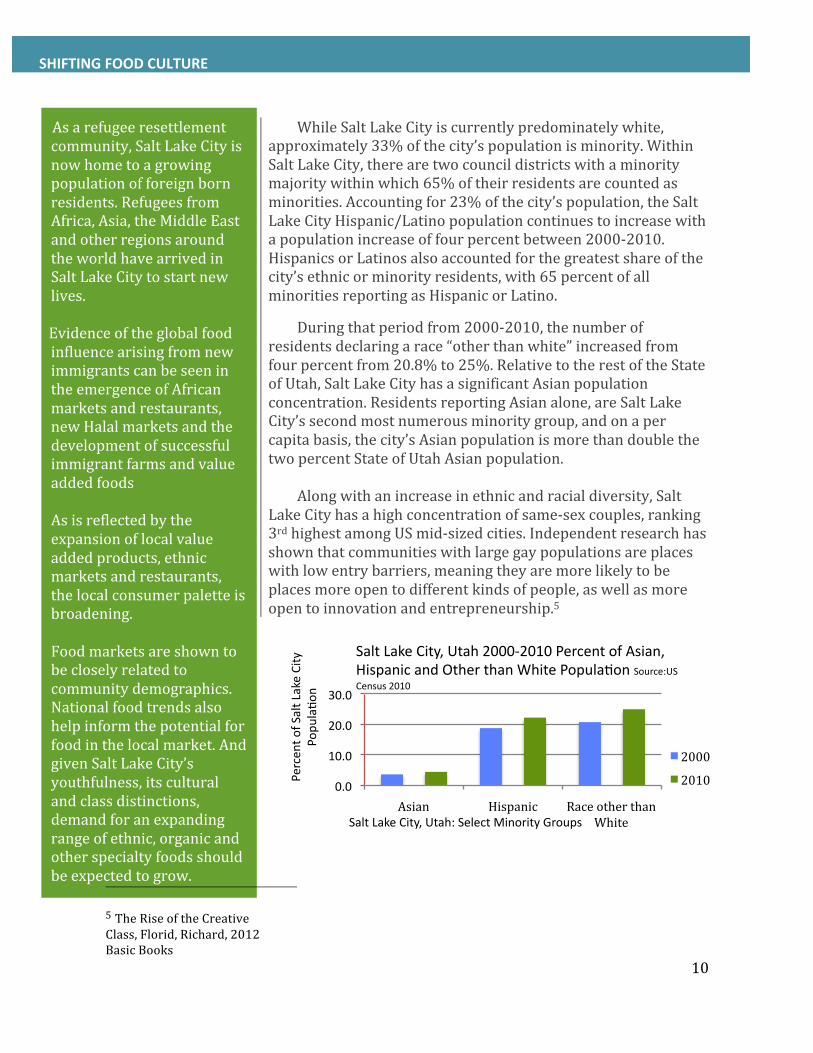

WhileSaltLakeCityiscurrentlypredominatelywhite,approximately33%ofthecity’spopulationisminority.WithinSaltLakeCity,therearetwocouncildistrictswithaminoritymajoritywithinwhich65%oftheirresidentsarecountedasminorities.Accountingfor23%ofthecity’spopulation,theSaltLakeCityHispanic/Latinopopulationcontinuestoincreasewithapopulationincreaseoffourpercentbetween2000‐2010.HispanicsorLatinosalsoaccountedforthegreatestshareofthecity’sethnicorminorityresidents,with65percentofallminoritiesreportingasHispanicorLatino.

Duringthatperiodfrom2000‐2010,thenumberofresidentsdeclaringarace“otherthanwhite”increasedfromfourpercentfrom20.8%to25%.RelativetotherestoftheStateofUtah,SaltLakeCityhasasignificantAsianpopulationconcentration.ResidentsreportingAsianalone,areSaltLakeCity’ssecondmostnumerousminoritygroup,andonapercapitabasis,thecity’sAsianpopulationismorethandoublethetwopercentStateofUtahAsianpopulation. Alongwithanincreaseinethnicandracialdiversity,SaltLakeCityhasahighconcentrationofsame‐sexcouples,ranking3rdhighestamongUSmid‐sizedcities.Independentresearchhasshownthatcommunitieswithlargegaypopulationsareplaceswithlowentrybarriers,meaningtheyaremorelikelytobeplacesmoreopentodifferentkindsofpeople,aswellasmoreopentoinnovationandentrepreneurship.5

5TheRiseoftheCreativeClass,Florid,Richard,2012BasicBooks

SHIFTINGFOODCULTURE

0.0

10.0

20.0

30.0

Asian Hispanic RaceotherthanWhite

Percen

tofSaltLakeCity

Popu

laFo

n

SaltLakeCity,Utah:SelectMinorityGroups

SaltLakeCity,Utah2000‐2010PercentofAsian,HispanicandOtherthanWhitePopulaFonSource:USCensus2010

2000

2010

11

0%

20%

40%

60%

80%

16‐39 40‐44 45‐49 50‐54 55‐59 60‐69

PercentofTotalNumberFoodServiceWorkers

AgeofFoodServiceWorker

SaltLakeCountyFoodServiceWorkersSource:NAICS722,2013

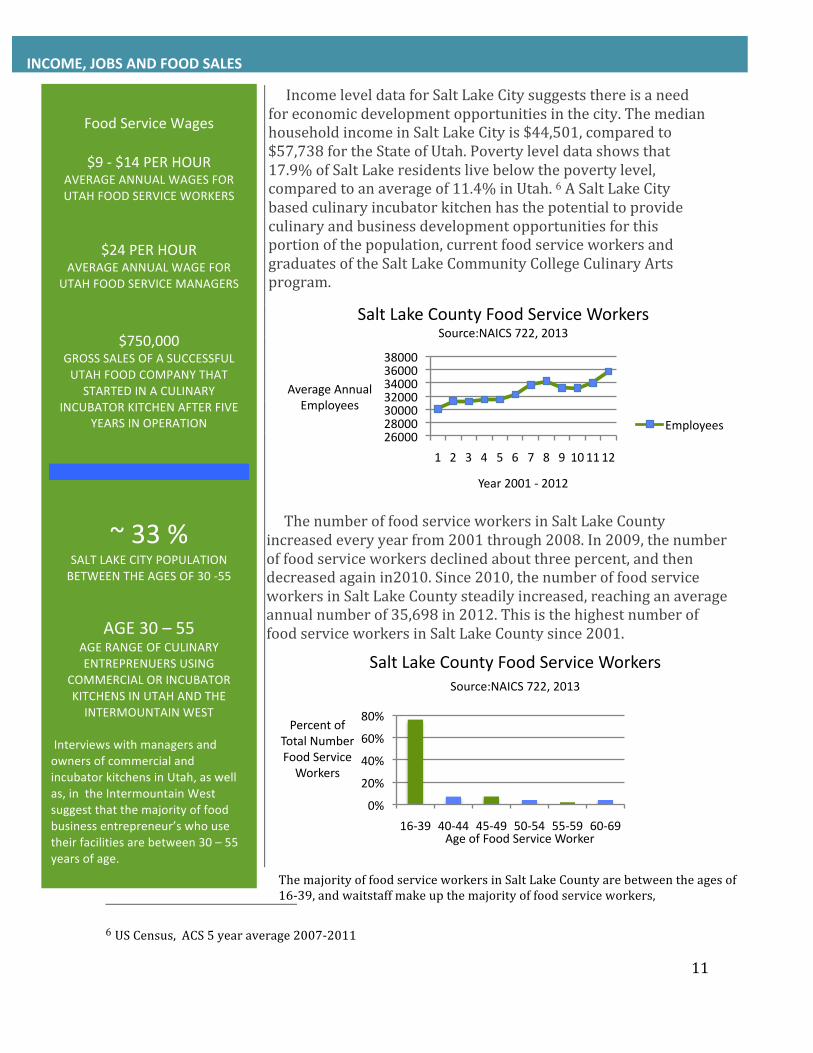

IncomeleveldataforSaltLakeCitysuggeststhereisaneedforeconomicdevelopmentopportunitiesinthecity.ThemedianhouseholdincomeinSaltLakeCityis$44,501,comparedto$57,738fortheStateofUtah.Povertyleveldatashowsthat17.9%ofSaltLakeresidentslivebelowthepovertylevel,comparedtoanaverageof11.4%inUtah.6ASaltLakeCitybasedculinaryincubatorkitchenhasthepotentialtoprovideculinaryandbusinessdevelopmentopportunitiesforthisportionofthepopulation,currentfoodserviceworkersandgraduatesoftheSaltLakeCommunityCollegeCulinaryArtsprogram.

6USCensus,ACS5yearaverage2007‐2011

ThemajorityoffoodserviceworkersinSaltLakeCountyarebetweentheagesof16‐39,andwaitstaffmakeupthemajorityoffoodserviceworkers,

INCOME,JOBSANDFOODSALES

FoodServiceWages

$9‐$14PERHOUR

AVERAGEANNUALWAGESFORUTAHFOODSERVICEWORKERS

$24PERHOUR

AVERAGEANNUALWAGEFORUTAHFOODSERVICEMANAGERS

$750,000GROSSSALESOFASUCCESSFULUTAHFOODCOMPANYTHATSTARTEDINACULINARY

INCUBATORKITCHENAFTERFIVEYEARSINOPERATION

~33%

SALTLAKECITYPOPULATIONBETWEENTHEAGESOF30‐55

AGE30–55AGERANGEOFCULINARYENTREPRENUERSUSING

COMMERCIALORINCUBATORKITCHENSINUTAHANDTHEINTERMOUNTAINWEST

InterviewswithmanagersandownersofcommercialandincubatorkitchensinUtah,aswellas,intheIntermountainWestsuggestthatthemajorityoffoodbusinessentrepreneur’swhousetheirfacilitiesarebetween30–55yearsofage.

ThenumberoffoodserviceworkersinSaltLakeCountyincreasedeveryyearfrom2001through2008.In2009,thenumberoffoodserviceworkersdeclinedaboutthreepercent,andthendecreasedagainin2010.Since2010,thenumberoffoodserviceworkersinSaltLakeCountysteadilyincreased,reachinganaverageannualnumberof35,698in2012.ThisisthehighestnumberoffoodserviceworkersinSaltLakeCountysince2001.

26000280003000032000340003600038000

1 2 3 4 5 6 7 8 9 101112

AverageAnnualEmployees

Year2001‐2012

SaltLakeCountyFoodServiceWorkersSource:NAICS722,2013

Employees

12

CulinaryBusinessOperations

UtahcurrentlyoperatesunderthefoodcottageindustrylawwhichallowsUtahresidentstoproducenon‐potentiallyhazardousfoodproductsintheirhomekitchens,andthenofferthemforsalewithintheStateatoutletssuchasfarmer’smarkets.However,notallhomekitchensmeettherequirementsoftheUtahStatelawforhomefoodproduction.Additionally,inordertolegallysellfoodproductstogrocerystoresorrestaurants,foodmustbeproducedinanFDAandUSDA(formeat)approvedkitchen.Atthistime,theUtahDepartmentofAgricultureandFoodcurrentlyhas45LettersofAuthorizationallowingfoodentrepreneurstoproducefoodinakitchenotherthantheirown.WiththeexceptionofanintermittentrangeoffivetotenpeopleproducingfoodintheProvo,UtahCommunityActionAgencyKitchen,themajorityofLettersofAuthorizationareforfoodproducersinSaltLakeCountyworkingatlicensedkitchens.AsofMay2013,theUtahDepartmentofAgricultureandFoodhas208licensesforhome‐basedbusinessesintheState.InSaltLakeCitythereareanincreasingnumberoffoodvendorsandmobilefoodtruckvendorswhorequirealicensedkitchenorcommissaryforfoodpreparationandstorage.Licensingrecordsshowthattherearecurrently48permittedvendorsinSaltLakeCityand9licensedmobilefoodtrucks.Asreportedthroughfocusgroupsdiscussion,foodcartandmobilevendorsareusinglocalprivatecommissarieswithvaryingdegreesofsatisfaction.Somestartupandsmall‐scalevalueaddedprocessorsarerentingcommercialkitchenspaceonanasavailablebasis,whichmeansutilizingkitchensduringnon–operatinghours.MarketStrengthOnemethodforevaluatingthestrengthoftheSaltLakeCityfoodservicesectoristocompareaveragepercapitafoodsalesinthecityagainststatewidesales.AreviewoftheaveragepercapitafoodsalesinSaltLakeCity,comparedtotheaveragepercapitasalesfortheStateofUtahindicatesthatresidentsfromsurroundingareasarecomingintothecitytopurchasefoodservices.ThissuggeststhatthefoodservicesectorinSaltLakeCityisanadvantagethatcanbebuiltupon.

Capture Rates for Food Service Business Category in Salt Lake City NAICS 722

Food Service Category Capture Rate

Full Service Restaurants 296%

Limited Service Restaurants 177%

Caterers and Other Specialty Food Services 246%

LOCALMARKETCONDITIONS

13

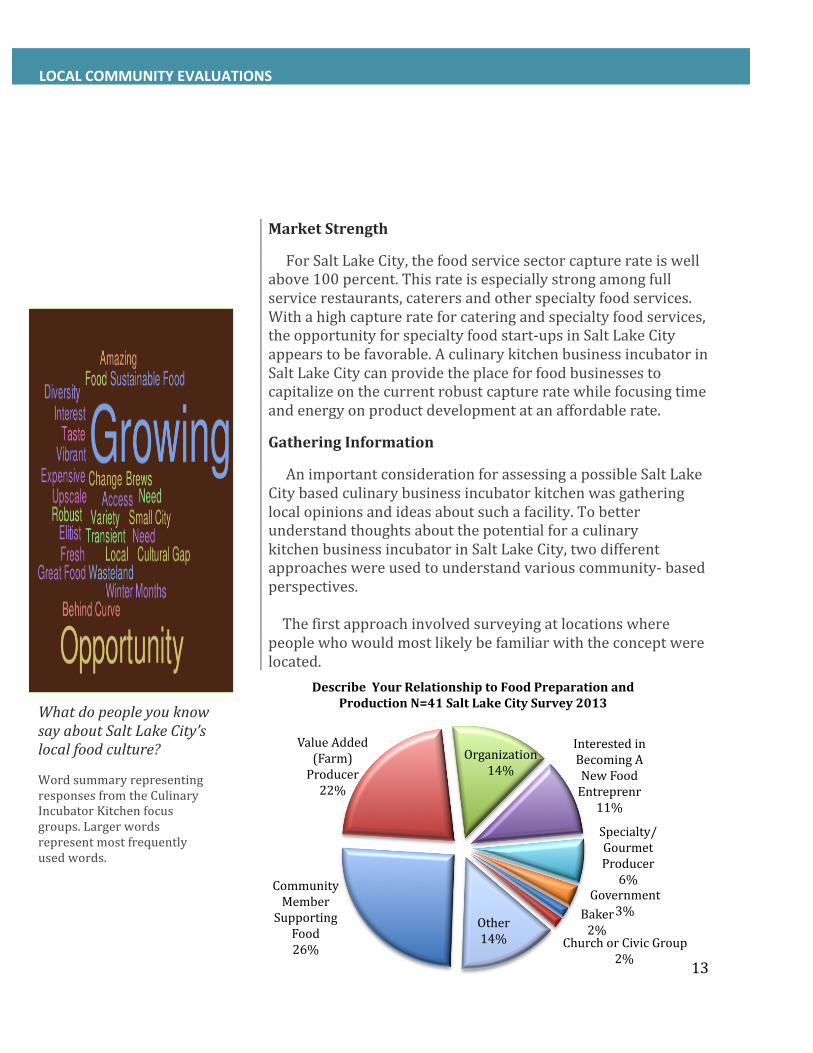

WhatdopeopleyouknowsayaboutSaltLakeCity’slocalfoodculture?

WordsummaryrepresentingresponsesfromtheCulinaryIncubatorKitchenfocusgroups.Largerwordsrepresentmostfrequentlyusedwords.

CommunityMemberSupporting

Food26%

ValueAdded(Farm)Producer22%

Organization14%

InterestedinBecomingANewFoodEntreprenr

11%

Specialty/GourmetProducer6%

Government3%Baker

2%ChurchorCivicGroup

2%

Other14%

DescribeYourRelationshiptoFoodPreparationandProductionN=41SaltLakeCitySurvey2013

MarketStrength

ForSaltLakeCity,thefoodservicesectorcapturerateiswellabove100percent.Thisrateisespeciallystrongamongfullservicerestaurants,caterersandotherspecialtyfoodservices.Withahighcapturerateforcateringandspecialtyfoodservices,theopportunityforspecialtyfoodstart‐upsinSaltLakeCityappearstobefavorable.AculinarykitchenbusinessincubatorinSaltLakeCitycanprovidetheplaceforfoodbusinessestocapitalizeonthecurrentrobustcaptureratewhilefocusingtimeandenergyonproductdevelopmentatanaffordablerate.

GatheringInformation

AnimportantconsiderationforassessingapossibleSaltLakeCitybasedculinarybusinessincubatorkitchenwasgatheringlocalopinionsandideasaboutsuchafacility.Tobetterunderstandthoughtsaboutthepotentialforaculinary kitchenbusinessincubatorinSaltLakeCity,twodifferentapproacheswereusedtounderstandvariouscommunity‐basedperspectives. Thefirstapproachinvolvedsurveyingatlocationswherepeoplewhowouldmostlikelybefamiliarwiththeconceptwerelocated.

LOCALCOMMUNITYEVALUATIONS

14

Thesecondinformationgatheringapproachinvolvedconveningfourfocusgroupsessions,whichwereheldduringthemonthsofMarchandMay2013.Thesegroupswerecomprisedofpotentialandcurrentfoodbusinessprofessionalsandincludedknowledgeablecommunityfoodleadersmadeupofcurrentandpotentialcaterers,restaurantowners,foodcartandmobilefoodtruckvendors,valueaddedfoodproducers,farmers,fooddistributors,andnon‐profitfoodleaders.Eachfocusgroupsessionlastedtwohours,andparticipantswereaskedtenspecificquestionsrelatedtothelocalfoodenvironmentandfactorsrelatedtoplanninganddevelopmentofapotentialculinaryincubatorkitcheninthecity.

FocusGroupsandSurveys: WhatwasLearnedAboutaPotentialSaltLakeCityCulinaryIncubatorKitchen?

FromFocusGroupsBasedonwhatyouknow,whattypeoffacilitiesarefoodbusinesseslikelocalfarmers,caterer’s,valueaddedprocessors,foodtruckowners,sidewalkcartvendors,andothersusingtopackageandpreparetheirproducts?

Fewgoodoptionsexist Cottageregulationsarereallylimiting–toomanyhoops Groupsareteaminguptofindfacilities Somepreliminaryprepfromhomeforfoodcarts Commissariesarecrowded,expensiveprivatelyownedfaculties Somerequirepurchasingagreementssotherearefeesforsoda,drinks,andthe

facility Somecommissariesaredirty,ornotpermitted,soIboughtacommissaryofmy

own Rentingabakeryspace,lookingforabiggerkitchen Wanttotakeoveranoldkitchen Leasingcateringspace Ifitssomeone’shome,orsharingacommercialkitchen,theoptionsarelimited

andshortterm Alotoftrucksprepareinsideoftruck,anditscertified,butnotideal Itisarealchallenge,rentingspaceisexpensive‐$800‐$1200/month

LOCALCOMMUNITYEVALUATIONS

LOCALCOMMUNITYEVALUATIONS

15

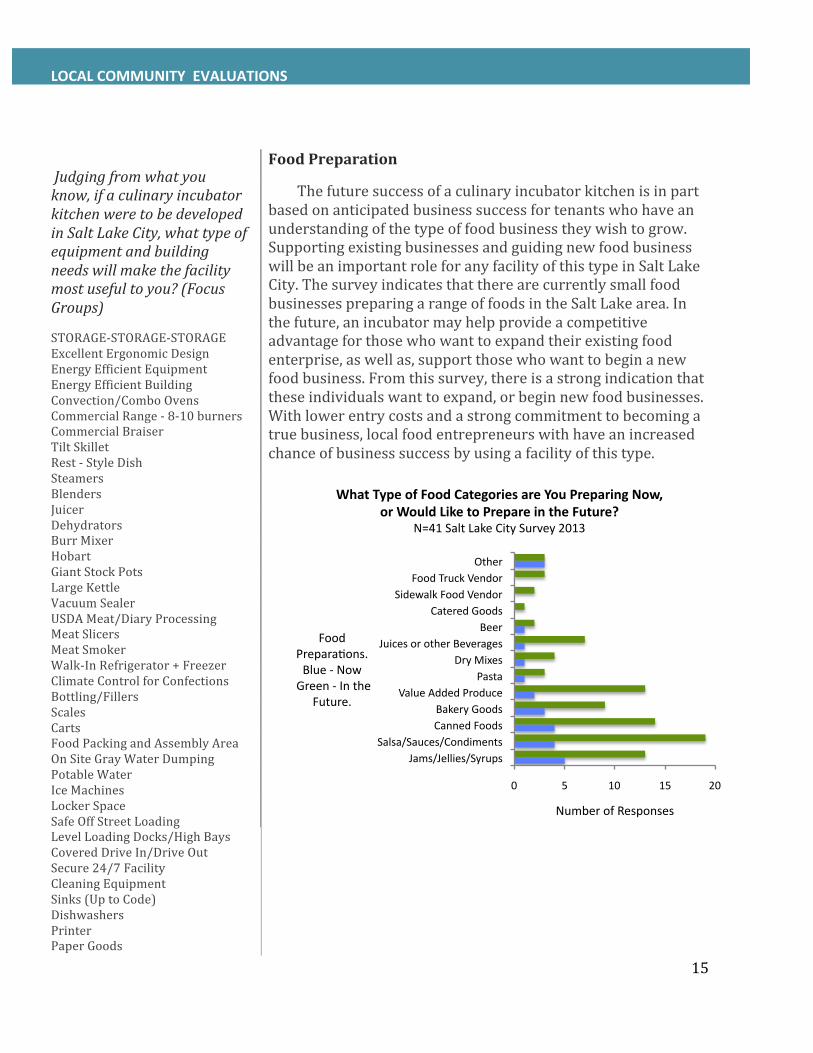

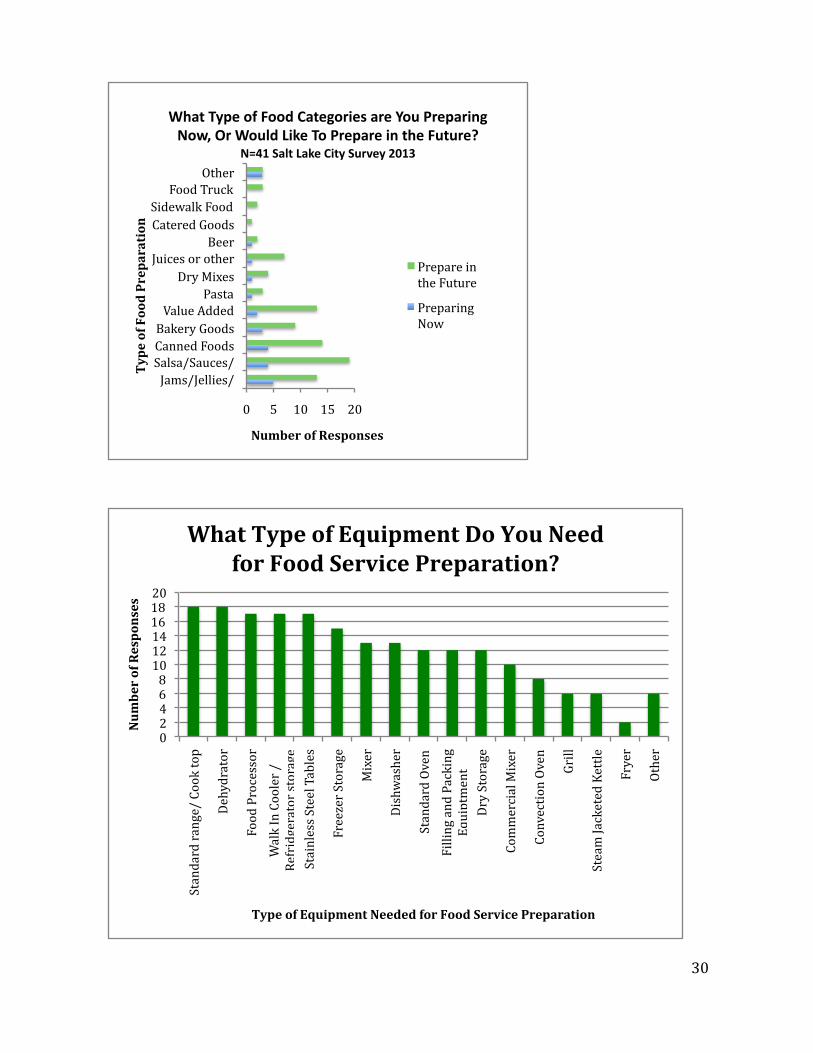

Judgingfromwhatyouknow,ifaculinaryincubatorkitchenweretobedevelopedinSaltLakeCity,whattypeofequipmentandbuildingneedswillmakethefacilitymostusefultoyou?(FocusGroups)

STORAGE‐STORAGE‐STORAGEExcellentErgonomicDesignEnergyEfficientEquipmentEnergyEfficientBuildingConvection/ComboOvensCommercialRange‐8‐10burnersCommercialBraiserTiltSkilletRest‐StyleDishSteamersBlendersJuicerDehydratorsBurrMixerHobartGiantStockPotsLargeKettleVacuumSealerUSDAMeat/DiaryProcessingMeatSlicersMeatSmokerWalk‐InRefrigerator+FreezerClimateControlforConfectionsBottling/FillersScalesCartsFoodPackingandAssemblyAreaOnSiteGrayWaterDumpingPotableWaterIceMachinesLockerSpaceSafeOffStreetLoadingLevelLoadingDocks/HighBaysCoveredDriveIn/DriveOutSecure24/7FacilityCleaningEquipmentSinks(UptoCode)DishwashersPrinterPaperGoods

FoodPreparation

Thefuturesuccessofaculinaryincubatorkitchenisinpartbasedonanticipatedbusinesssuccessfortenantswhohaveanunderstandingofthetypeoffoodbusinesstheywishtogrow.SupportingexistingbusinessesandguidingnewfoodbusinesswillbeanimportantroleforanyfacilityofthistypeinSaltLakeCity.ThesurveyindicatesthattherearecurrentlysmallfoodbusinessespreparingarangeoffoodsintheSaltLakearea.Inthefuture,anincubatormayhelpprovideacompetitiveadvantageforthosewhowanttoexpandtheirexistingfoodenterprise,aswellas,supportthosewhowanttobeginanewfoodbusiness.Fromthissurvey,thereisastrongindicationthattheseindividualswanttoexpand,orbeginnewfoodbusinesses.Withlowerentrycostsandastrongcommitmenttobecomingatruebusiness,localfoodentrepreneurswithhaveanincreasedchanceofbusinesssuccessbyusingafacilityofthistype.

0 5 10 15 20

Jams/Jellies/SyrupsSalsa/Sauces/Condiments

CannedFoodsBakeryGoods

ValueAddedProducePasta

DryMixesJuicesorotherBeverages

BeerCateredGoods

SidewalkFoodVendorFoodTruckVendor

Other

NumberofResponses

FoodPreparaFons.Blue‐Now

Green‐IntheFuture.

WhatTypeofFoodCategoriesareYouPreparingNow,orWouldLiketoPrepareintheFuture?

N=41SaltLakeCitySurvey2013

LOCALCOMMUNITYEVALUATIONS

16

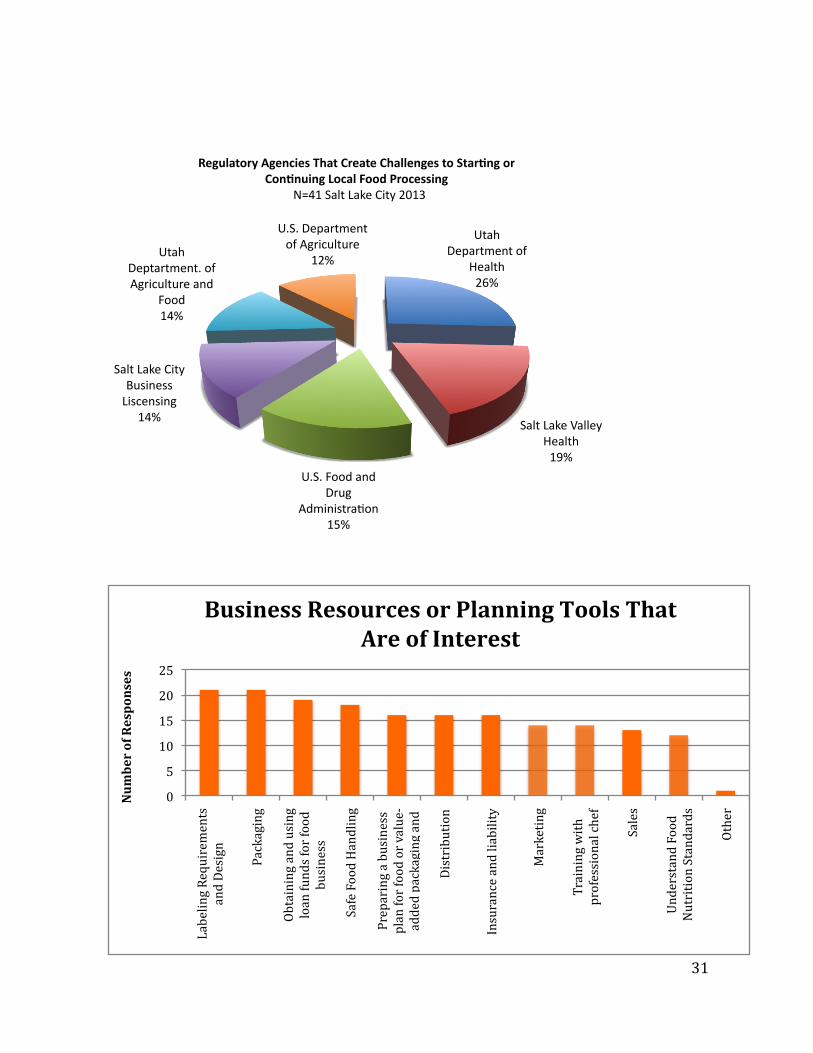

UtahDepartmentofHealth26%

SaltLakeValleyHealth

19%

U.S.FoodandDrugAdministraFon15%

SaltLakeCityBusinessLiscensing

14%

UtahDeptartment.ofAgricultureandFood

14%

U.S.DepartmentofAgriculture12%

RegulatoryAgenciesthatCreateChallengestoStarVngorConVnuingLocalFoodProcessingN=41SaltLakeCity

2013

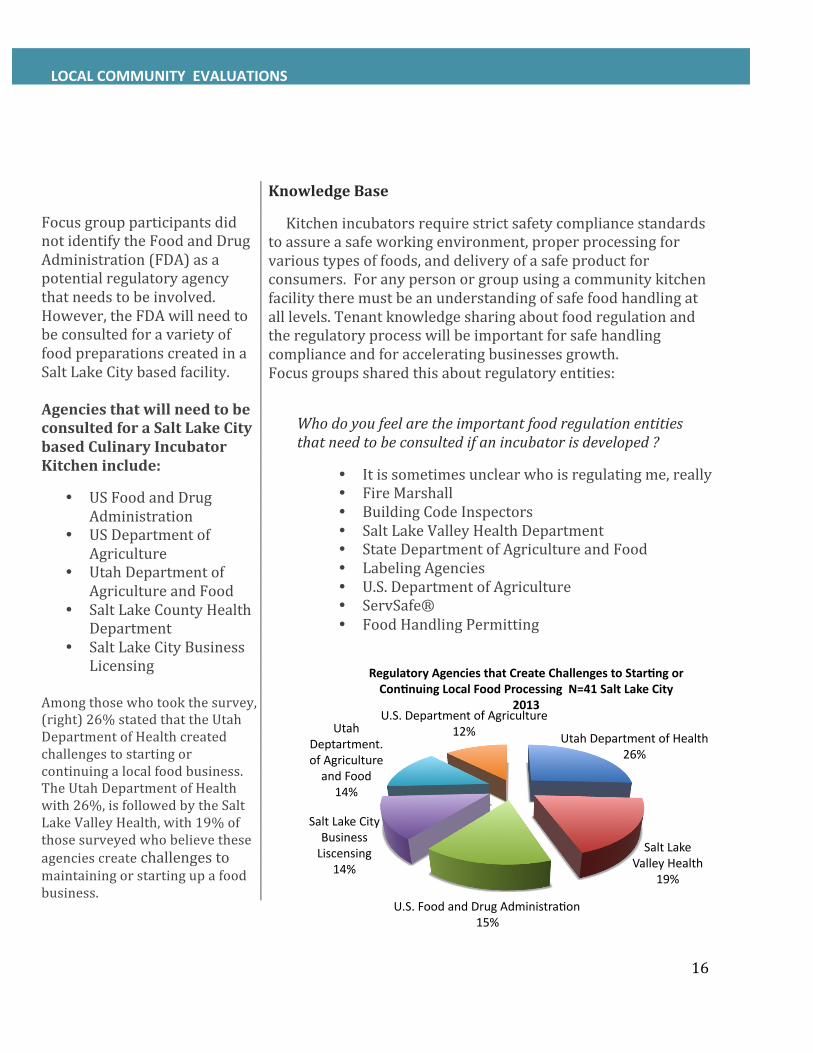

KnowledgeBase

Kitchenincubatorsrequirestrictsafetycompliancestandardstoassureasafeworkingenvironment,properprocessingforvarioustypesoffoods,anddeliveryofasafeproductforconsumers.Foranypersonorgroupusingacommunitykitchenfacilitytheremustbeanunderstandingofsafefoodhandlingatalllevels.Tenantknowledgesharingaboutfoodregulationandtheregulatoryprocesswillbeimportantforsafehandlingcomplianceandforacceleratingbusinessesgrowth.Focusgroupssharedthisaboutregulatoryentities:

Whodoyoufeelaretheimportantfoodregulationentities thatneedtobeconsultedifanincubatorisdeveloped?

FocusgroupparticipantsdidnotidentifytheFoodandDrugAdministration(FDA)asapotentialregulatoryagencythatneedstobeinvolved.However,theFDAwillneedtobeconsultedforavarietyoffoodpreparationscreatedinaSaltLakeCitybasedfacility.AgenciesthatwillneedtobeconsultedforaSaltLakeCitybasedCulinaryIncubatorKitcheninclude:

USFoodandDrugAdministration

USDepartmentofAgriculture

UtahDepartmentofAgricultureandFood

SaltLakeCountyHealthDepartment

SaltLakeCityBusinessLicensing

Amongthosewhotookthesurvey,(right)26%statedthattheUtahDepartmentofHealthcreatedchallengestostartingorcontinuingalocalfoodbusiness.TheUtahDepartmentofHealthwith26%,isfollowedbytheSaltLakeValleyHealth,with19%ofthosesurveyedwhobelievetheseagenciescreatechallengestomaintainingorstartingupafoodbusiness.

LOCALCOMMUNITYEVALUATIONS

LOCALCOMMUNITYEVALUATIONS

Itissometimesunclearwhoisregulatingme,really FireMarshall BuildingCodeInspectors SaltLakeValleyHealthDepartment StateDepartmentofAgricultureandFood LabelingAgencies U.S.DepartmentofAgriculture ServSafe® FoodHandlingPermitting

17

AccordingtotheU.S.SmallBusinessAdministration,morethan80percentofsmallbusinessesfailwithintheirfirstfiveyearsbecauseoflackofmoneyorskillssuchas,productmarketing,businessand/orfinanceskills.However,nearly87percentofbusinessincubatorgraduatesremaininbusiness.Bymitigatingstart‐upcostsandprovidingasupportiveandeducationalenvironment,businessincubatorshavesuccessfullygraduatedover87%oftheirfirms,andhavekeptanoutstanding84%ofthesethrivingbusinessesintheirlocalcommunities.Tobesuccessful,kitchenincubatorsmustbeactiveparticipantsinhelpingtheirtenants.Throughoutthecountrythisisaccomplishedbyprovidingserviceslikebusinessplanninganddevelopment,marketingandfinancialtraining,accesstocapitalandconnectionsinthelocaleconomy.

Aculinaryincubatorkitchenisinfactafoodbusinessincubatorwhosepurposeistohelpstart,guide,adviseandgrowlocalfoodbusinesses.Tobetterjudgeifthelocalcommunityneedsorwantstheseresources,focusgroupswereasked:Arethereanyclassesorbusinesseducationprogramsrelatedtoaculinaryincubatorthatcouldbehelpfulinbuildinguplocalfoodbusinesses?Focusgroupparticipantswereveryrealisticaboutthechallengesofstartingorcontinuingafoodbusinessalongwiththeneedfortechnologyandbusinessskillbuilding.Theneedforsmallbusinesseducationisveryimportantintheculinaryincubatorsetting,anditmustnotbeundervaluedasanecessaryresourcefortenantsofaSaltLakeCityculinaryincubatorkitchen.

LOCALCOMMUNITYEVALUATIONS

FoodPrepGuidelinesandWeightsandMeasurementTraining

SafeFoodHandlingandServSafe®classesinmultiplelanguages.On‐lineclassesdonotwork.ESLparentsarehavingtheirkidstaketheonlineclassesforthem

Professionalassistanceonhowtoscaleuprecipes GeneralFoodBusinessEducation: Whatarerealisticworkhours Howtocreateafoodbusinessplanandstrategy Neededsupplies Distribution Marketing Branding Financingoptions Classesonsourcinglocalproducts Howtoplanforyearroundaccesstolocalfruitsand

vegetables Industryexpertleadclasses Figureouthowtopartnerwithexistingprograms,like

SaltLakeCommunityCollege,LarryMillerBusinessSchoolandDiversifiedAgriculture

Howtonetworkorbuildconnectionsinthebusiness Insurance,liabilityandotherlegalissues Classesormentoringonhowtoworkthrough“red

tape”orgetthroughbureaucratichoops Socialmediahelp

18

Focusgroupstalkedaboutwhomightbethebestoperatorandmanagerofthefacility,aswellasthebestroleforSaltLakeCityinanyfutureincubator.Arangeofopinionsarose,buttheresponsesgeneratednoclearconsensusofopinionastowhomaybethebestmanagementoperator.ThebestroleforSaltLakeCitytendstowardtheareaoforganizational,financialplanninganddevelopmentactivities.TherewerestrongopinionsexpressedthatSaltLakeCityshouldnotrunthisfacility.Ifthisprojectmovesforward,whodoyouthinkisbestsuitedtooperateandmanagethisincubatorkitchen?Why?

UtahStateUniversitybecauseoftheirprograms Non‐profitwouldbemorecosteffective CommunityandEconomicDevelopment/Government Keepingcostsdownwouldrequirethegovernmenttobeinvolvedsincethey

havealltheresources Notthecity,butthecityshouldhaveanoversightboard Anadvisoryboardneedstobediverse,peoplewhoknowthewholepicture Non‐foodspecificbusinessfolksshouldserveontheboard Governmentshouldhavenothingtodowiththisprojectbecauseitwouldsetupa

falseexpectationofwhatittakestorunafoodbusiness Thegovernmentmovesslowandhasahardtimemakingmoney,ifitwasrunby

apublicsectorthatwouldcompromisetheprospectsofthefacility SaltLakeCountyHealthshouldrunthekitchen Facilitymanagerneedstobeafoodserviceveteran

WhatdoyouseeasthebestroleforSaltLakeCityinanyfuturedevelopmentofanincubatorkitchen?

SaltLakeCityshouldstartitandturnitovertosomeoneelsewhocancreatethisasaneconomicdevelopmentresource

Citylacksagility‐thisisaproblemformanagingthistypeoffacility SaltLakeCityshouldaidinprocessesoflocationandinfrastructure Thecityshouldpromotethisasanasset SaltLakeCityshouldhaveaseatatthetable,butnotcompleteoversight Thecityshouldrunit Provideacertifiedlegalspace,butnotofferbusinessadvice Creatingaonestopshopforallculinaryfoodbusinessneeds Cityshouldhelpwithsitting Planningforthisfacilityinaneighborhood/districtarea Cityshouldbeworkingatamacrolevelonfoodissues

LOCALCOMMUNITYEVALUATIONS

LOCALCOMMUNITYEVALUATIONS

19

IMPORTANTLOCATIONThefocusgroupswerealsoaskedaboutwhereafuturekitchenmightbelocated.Onthistopictherewasasignificantamountofconsensusaroundtransportationneedsandthreegenerallocationsstated,withtheareaofStateStreetto300Westfrom600Southto900Southbeingmostfavored.You’vetoldmewhoyouthinkmightbestoperateaculinaryincubatorkitchen,whereisagoodlocationtoconsiderlocatingthistypeoffacility?

TheIntermodalHubarea MarmaladeDistrict Granary AreaaroundStateStreettothe“Westside”and800/900South Accesstothefreewayandtrainsisveryimportant Don’tlocateitonone‐waystreetsorrightdowntownwherethereiscongested

traffic Notinthephysicalepicenterofthecity,butcentralizedwitheasytrafficflowand

freewayaccess Accesstotransitisimportant Don’tburyitinaneighborhood Putitinanareawherepeoplewhomakefoodcantakeittonearbystores–

incubateaneighborhoodwhileincubatingfoodbusinessesBasedonanevaluationofthecity’stransportationnetwork,foodwholesale,foodretaillocations,aswellas,emergingdevelopmentpatternsandcommunityneeds,theconsultantteamsupportsalocationwithintheareaboundedbyapproximatelyStateStreetto400Westandfrom600Southto1300South.Locatingafacilityinthisareaisideal,butintheeventthatotherviablelocationspresentthemselves,substantialtransportationaccessibilityinconjunctionwithotherelementsstatedinthisreport,includingcommunityplanning,shouldbeclearlyevident.Integrationofthisfacilitywithothersustainablefoodplanninganddevelopmentisstronglyadvisedbytheconsultant.

LOCALCOMMUNITYEVALUATIONS

20

RISKSANDCAUTIONSFinally,focusgroupparticipantswhereaskedtooffercriticalcandidcommentsaboutfuturerisksorcautionsassociatedwithapotentialfacility.Alloftheparticipantsofferedclearsupport,forakitchen,butwerecautionaryandacutelyawareofthepotentiallyhighcapitalcostinvestmentandoverallplanningthatneedstogointocreatingacompellingSaltLakeCitybasedculinaryincubatorkitchen.Planning,financingandmanagementwerekeyconcerns,andifthesecannotbeadequatelyputinplace,Focusgroupparticipantsurgedcaution.Overall,theexpectationisthatSaltLakeCitywillbetheresponsiblepartyforcreatinganddeliveringonawellthoughtoutplan.Theimportanceofnear,andlongtermfacilityreputationalsuccesswasdeemedasveryimportant,withanemphasisonnotmovingforwardifanexcellentfacilitywithanexcellentreputationcan’tbebuilt.Asonefocusgroupparticipantstated,“Anunsuccessfulkitchencoulddestroyanysupportforakitcheninthefuture” Ifanalysiscomesbackpositive,orsupportingaculinaryincubatorkitcheninSaltLakeCity,canyouthinkofanyreasonswhythedevelopmentofthisfacilityshouldnotmoveforward?

Amissionandveryclearbusinessplanisneeded Ifthereisnotenoughfunding,donotmoveforwardwiththisproject Managementandfundingtogetherarecritical,ifmanagementcan’tbesupported

thekitchenshouldnotbecreated Themotivationhastobeclear,ifthemotivationistogenerateincome,itshould

notmoveforward Profitinthestrictestsenseneedstobeputaside,balancemustbestruckbetween

coveringcostsandofferingaccessibleratesandsustainingbusiness Definesustainable–viabilityandoperationalaspectsareimportant Iamanxioustohavethistypeoffacility,butIwanttohaveoperational

confidence IftheCottageFoodLawgetstooloose,itwillunderminethiseffort Ifthisfacilityisnotuptocodeitwillbeanightmare Itisimportantfordecisionmakerstounderstandhowmuchofacommunity

assetandresourceafacilityofthistypeshouldbecome Thisshouldn’tjustbeaplacetomakefood,ifresourcesandeducationaren’t

availablethenitshouldn’tgoforward Stakeholdersupportwillbeimportant Anunsuccessfulkitchencoulddestroyanysupportforakitcheninthefuture

LOCALCOMMUNITYEVALUATIONS

ECONOMICOPPORTUNITY

LOCAL

COMMUNITYEVALUATIONSLOCALCOMMUNITYEVALUATIONS

21

Thereareseveralwaysaculinaryincubatorkitchencreatesjobsandaddsbenefitstoalocalcommunity.Itcan:

Removerestrictivebarriersofhighstartupcostsandregulatorydifficultiesassociatedwithstartingafoodbusiness–allowingentrepreneurstostartsmallandgrowwithambition

Allowentrepreneurstoretainmoreindividualcapitaltoinvestintheirproduct

Providebusiness,technical,culinary,andotherknowledgebasedtrainingthatincreasesthesuccessrateforstartupfoodbusinesses

Createanexcellentstartupenvironmentwithlowentrycostsandbusinesstrainingwheresmallfoodbusinessescanexpandduringtheirtenureattheincubator–generallygraduatingafteratwoyearcycle–andmovetoalargerfacilityorbuy/buildtheirownkitchen

Whiletherearemanywaysinwhichanincubatorcanbuildlocalculinarybusinesscapacity,therearealsosignificantupfrontinvestmentandongoingoperatingexpenseswhichmustbeconsideredinordertoincreasethelikelihoodthatsuchafacilitycanitselfbecomeasuccessfulenterprise.Asacommunityinvestment,aculinaryincubatorkitchenisacapitalintensiveinvestmentprojectrequiringfundingforfacilityplanning,developmentandequipmentacquisition.Forthisstudy,areviewofculinaryincubatorsoperatingwithintheregionandaroundthecountryreveledthatcapitalinvestmentandequipmentcostswithinthepast11yearshaverangedfromapproximately$400,000(BusinessIncubatorCenterinGrandJunctionColorado)to$8milliontobuildandequiptheNewJerseybasedRutgersFoodInnovationCenter.

Intermsofoperation,culinaryincubatorkitchensaroundthecountryvarywidelyinthetypeofcookingresourcesofferedintheirkitchens.Someincludealimitedamountofspaceandequipmentforanarrowrangeoffoodpreparationswithoutbusinessornetworkingsupport,whileothersincludemultiplepreparationareasforrawfood,wetfood,dryfood,meatsanddairy,refrigeratedstorage,drystorage,specialclimatecontrols,24/7secureaccess,comprehensiveequipmentresources,packingroomsthatbeusedforspecialdietaryrequirementsincludingglutenfreefoodpreparationandpackingandextensivebusinessandtechnologytraining.

Becausetherangeofopportunitycanvarywidelybetweenfacilities,thesquarefootspacepertenantisequallyasvariable.BasedonasamplingofUtah,IntermountainWestandseveralnationalculinaryincubatorkitchens,theaveragenumberofannualtenantsforanincubatoraroundthecountryrangesfromapproximatelyonetenantpersquarefootofkitchenspaceto14tenantspersquarefootofkitchenspace.

ECONOMICOPPORTUNITY

22

AndalthoughdatatrackingonjobscreationislackingformostUSculinaryincubatorkitchens,someculinarykitchensarekeepingtrack,andbasedonasamplingoftheseincubatorkitchensitisestimatedthatannualjobsperyearrangefrom.5jobsper1000squarefeetofkitchenspace,to25jobsperyearper1,000squarefeetofkitchenspace.Averagejobcreationisapproximately6.4FTE’sofjobsannuallyper1,000squarefeetofkitchenspace.Usingthisinformationandassuminga4,000squarefootkitchen,26jobswouldbecreatedannually.ForaSaltLakeCityincubator,carefulscreeningofapplicantscombinedwiththerequireduseofbusinessfinancetraining,andefficientaccess,willhelpincreaseannualjobsinthelocalmarket.

Asanexample,LaCocina,a4,000squarefootfacilityinSanFrancisco,reportsthatitsupported39businessesthatcreated110jobsand$3.35millioninrevenuein2012.Thesetotalsonbusinessandjobcreationalongwithtotalrevenueindicatethatapproximately25jobsper1,000squarefeetofspacewerecreatedfromtheLaCocinaculinarybusinessincubator.

WithintheIntermountainWest,ownersofseveralUtahfoodservicebusinesseswhowereinterviewedconfidentiallyforthisstudy,statedthattheywereestablishedinthepastfiveyearsandprojecthiringanaverageof20‐25employeesoverthenextfiveyears.Additionally,accordingtoJasonTalcott,DirectoroftheSaltLakeCommunityCollege,CulinaryArtsProgram,thisprogramhasanapproximateenrollmentof250studentsperyear,andgraduatesabout60studentsannually.Manyoftheseculinarystudentsareconsideringfutureopportunitiestostarttheirownfoodbusinesses,andhestatedthataculinaryincubatorkitchenwouldbeagoodplaceforthemtobegin.

ECONOMICOPPORTUNITY

23

SPINOFF

Economicactivity,suchasnewfoodbusiness,startsachainreactionthatgeneratesmoreeconomicactivityinacommunity.Moneyspentintheeconomydoesn’tjuststopwiththefirsttransaction,butinsteadstaysinthecommunitywhereitfiltersthroughtoaccelerateopportunityatmanylevels.Economistscallthisamultipliereffect,andinthelocalfoodservices,thisisevidencedbylong‐termconnectionslinkingbetweenproducers,distributors,processorsandconsumers.InUtah,researchconductedbyUtah’sOwnshowsthatevery$1.00spentonlocalproductshastheeffectofadding$4.00to$6.00intotheUtaheconomy.Becausethistypeoffoodconnectionissolocalizedithastheadditionalbenefitofreducingthecarbonfootprint.

Inadditiontospecificfoodbusinesses,localjobsandbusinessopportunitiesgeneratedthroughthecreationofasuccessfulfoodservicebusinessincubatorinclude:

FoodGrower/Suppliers–Foodservicebusinesseswillpurchasefoodproductsandwherepossiblewillideallybuyfromlocalgrowersandsuppliers

Marketing–Emergingfoodbusinesseswillpurchasemarketingservicesformarketingtoolssuchaslogoandwebsitedesign,productbrandingandplacement

Printing–Foodservicebusinesseswillpurchaseprintingservicessuchasproductlabels,businesscards,advertisementcardsandflyers,bannersorposters,etc.

Packaging–Foodservicespurchasepackagingproductssuchasbottling,boxes,wrapping,sealingproducts

ProfessionalOrganizations–NewfoodbusinessownerswilljoinlocalbusinessorganizationssuchasVestPocketBusinessCoalition,ChambersofCommerce,WomeninBusiness,UtahMagazine,etc.Partneringwithlocalretailoutlets–Newfoodserviceproductscanbeplacedinexistingretailoutletstoincreasesalesforboththeexistingretailoutletandthenewfoodserviceprovider.Forexample,bakedgoodsmaybesoldinalocalcoffeeshoptoexpandthemarketappealofthecoffeeshopandprovideavenueforsalesofanewfoodproduct.Historically,evensmallfoodoperationsareabletoselltheirproductstoretailoutlets,wholesaledistributors,restaurantsandinstitutions

LocalRestaurants–Newfoodbusinesseswillsupportexistingfoodservicebusinessesasthepurchasefoodforworkpantries,employeemeals,meetingsandevents

ECONOMICOPPORTUNITY

24

CONCLUSIONSaltLakeCity,likemostmidsizedAmericancitiescontainsassetsthatgiveitadvantagesinfoodservicedevelopmentsuchasimporting,storing,processing,wholesalingandfooddelivery.SaltLakeCity’smetropolitangeographiclocation,arobusttransportationnetwork,alargeworkforce,centralwholesaledistribution,technologyinfrastructure,farmersmarkets,localrestaurants,marketsandcafes,anoverallstronglocalbusinesseconomyandadiversepopulationareallbenefitstosupportingaculinarybusinessincubatorkitchen.Inaddition,locatedinSaltLakeCityisthestatesflagshipuniversity,aswellas,colleges,non‐profitentitiesandtechnicalassistanceavailabletoassistwithdevelopmentandtraining.Manykitchenincubatorsthatofferculinaryandotherbusinesstrainingalongwithnetworkingarerunthroughcommunityandeconomicprograms,suchasuniversityfoodtechnologycentersornon‐profitsandarerarelyfinanciallyselfsustaining.Inordertoencouragenewentrepreneursintheseprograms,rentalratesusuallyarenotsufficientlyhighenoughtocoveroperationalcosts.Furthermore,inordertocreatesmallbusinessesandincreaselocalemployment,akitchenincubatormayhavetoabsorbpartoftheproductioncost.Ahighnumberofkitchenincubatorsaroundthecountryrelyongrantsandotherfundingtobreakeven.Manyofferadditionalservicessuchascommunitycookingclasses,demonstrationcenters,facilityrentals,consulting,andresearchanddevelopmentforexistingbusinessestohelpsupporttheongoingoperations.Privatekitchenincubatorscanbeveryprofitable,butmostoftendonotprovideculinary,businessandtechnologyassistancealongwithknowledgesharingthatisneededformostsmallfoodbusinessestogrowandsucceed.ConditionsinSaltLakeCityarefavorableforaculinaryincubatorkitchen.Thefollowingisasummaryof“bestpractices”learnedbysharedculinarybusinessincubatorkitchensaroundtheCountrythatmayservetoguideaSaltLakeCitybasedfacility:

SizeandOperatingHours–Thekitchenshouldbesufficientlylargetoaccommodatemorethanonetenantatatimeandbeavailableforrent24hourssevendaysaweek.Forallhours,akeyless–secureentryisbest.BasedonSaltLakeCity’sdemographicandeconomicevaluationforthisreportakitchenwithatleast3500sfofkitchenspaceisrecommendedforaSaltLakeCityculinaryincubator.Focusgroupparticipantsandthosesurveyedexpressedadesireforawiderangeofkitchenopportunitiesincluding,meatanddairyprocessing,aswellascontrolledpackingspaceforallergens.Afacilitythatsupportsnaturalproductmanufacturing(tinctures,oils,lotions)processingwouldbeanadvantage.

Storage–Insufficientstoragecanlimittheabilityforexistingtenantstofunction,

andcanlimittheabilitytoaddnewtenants.Storageshouldincludecoldstoragewalkinrefrigerationandfreezing,aswellasasignificantamountofdrystorage.Akitchenspacetodrystorageratioof2:1upto1:1isneeded.

CONCLUSION–BESTMANAGEMENTPRACTICES

25

KitchenSpace–Equipment–Inadditiontotheequipmentlistprovidedbyfocus

groupandsurveyparticipants,additionalitemssuchasapastamaker,heatbandsealer,weighinpackingmachines,juicepulper,grinder,aswellashighbayaccessandvehiclestorage.

Population–Kitchensinareaswithlargerpopulationsgenerallyhavean

advantageoverkitchensinsparselypopulatedareas.SaltLakeCityhasapopulationreachofover1.5millionpeoplewithina60‐minutedrivetothecity.

ModelforSuccess–Commercialkitchensthathavefollowedthebusiness

incubatorconcepthavebeenthemostsuccessfulovertheyears.Kitchensthatfollowtheculinarybusinessincubatormodelprovidesupportsuchasculinary/recipeassistance,businessandtechnicaltraining,connectionstogrowersanddistributors,accesstocapital,andnetworking.

FDA/USDAApproval–AlmostallfacilitiesareFDAapprovedandsomeareUSDA

approved.Itiscriticaltohaveafacilitythatallowsformultipletypesoffoodbusinesstenants.

RentalRates–Rentalratesgenerallyrangefrom$5.00‐$24perhourtoashigh

as$1,750.00perday.Somefacilitieshavevaryingand/orslidingfeeratesdependingonthehoursofuseoreconomiccircumstancesofatenant.Tenantswhousemorehoursmaypayalowerhourlyratecomparedtothosewhousethekitchenlessfrequently.Basedonexperiencesofotherkitchens,arentalrateofapproximately$15.00‐$20.00perhourwasimportantforakitchensabilitytomaintainfinancialsecurity.

AnchorTenants–Manysuccessfulkitchenshave“anchortenants”(cateringand

mobilefoodvendors).Anchortenantsprovidesustainedrentrevenueandstabilitytothefacility.Generally,ananchortenantrentsafacilityanywherefrom15–150hourspermonth.Catererscanbeagoodsourceforanchortenants.

Management–Inadditiontoexcellentbudgeting,fundraising,andgrantwriting

techniques,thesuccessofasharedculinarykitchenincludesexcellentmarketing.ManytenantscurrentlyusingsharedcommercialkitchensinSaltLakeCitysaidthatittookthemaconsiderablelengthoftimetofindasharedkitchenduetopoormarketingbyexistingcommercialkitchens.Marketingtechniquesforthekitchenneedtomirrorthoseforaprofitorganizationusingcommunicationssuchasnetworkingandpresentingwithexistingbusinessandnon‐profitorganizations,aggressiveradio,earnedTVandprintmediaaswellassocialnetworkingstrategies.Inadditiontothesetechniques,cleanlinessandsafetymustbeapriority.Asafe,secureenvironment,alongwithmaintainingcooperationamongtenants,andassuringregulatorycomplianceandcleanlinessismandatoryforthedevelopmentofaculinaryincubatorinSaltLakeCity.

CONCLUSION–BESTMANAGEMENTPRACTICES

26

AppendixASurvey,February2013

AQUICKSURVEYTOASSESSINTERESTINTHE

SALTLAKECITYCULINARYINCUBATORKITCHENPROJECT

Whichbestdescribesyourrelationshiptofoodpreparationproduction?

Iama:

_____ValueAdded(Farm)Producer _____Restaurant

_____Catering _____FoodTruckVendor

______StreetCartVendor _____Baker

______Specialty/GourmetFoodProducer ______Government

______Organization _____ChurchorCivic

Group

______InterestedInBecomingaNewFoodEntrepreneur

______Communitymembersupportingfood _______Other(describe)

Whattypeoffoodcategoriesareyoupreparingnow,orwouldyouliketopreparein

thefuture?

(CHECKALLTHATAPPLY)

PreparingNowInterestedInPreparingintheFuture

BakeryGoods _______ _______

Jams/Jellies/Syrups _______ _______

APPENDIXA–INCUBATORKITCHENUSERGROUPSURVEY

27

Salsa/Sauces/Condiments _______ _______

CannedFoods _______ _______

ValueAddedProduce _______ _______

Pasta _______ _______

DryMixes _______ _______

CateredGoods _______ _______

SidewalkFoodVendor _______ _______

FoodTruckVendor _______ _______

Juices,orotherbeverages _______ _______

Beer _______ _______

Other_____________

IfaCulinaryIncubatorKitchenisdevelopedinSaltLakeCity,whereisagoodlocationforthistypeoffacility?Why?________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Whattypeofequipmentdoyouorothersneedforfoodserviceproduction?Checkallthatapply.

StandardOven FillingandPackagingEquipment

ConvectionOven DryStorage StandardRange/Cooktop WalkInCooler/Refrigerator Mixer FreezerStorage Grill Dishwasher Fryer StainlessSteelTables SteamJacketKettle Other CommercialMixer

______________________________________ FoodProcessor ‐

_______________________________________ Dehydrator

28

Doyouknowifanyoftheseregulatoryagenciescreatechallengestostartingorcontinuinglocalfoodprocessingbusinesses?

UtahDepartmentofHealth UtahDepartmentofAgriculture SaltLakeCountyHealthDepartment UnitedStateFoodandDrug

Administration SaltLakeCityBusinessLicensing UnitedStatesDepartmentofAgriculture

Wouldanyofthefollowingresourcesorplanningtoolsbeofinteresttoyouoryourgroup?

PreparingaBusinessPlanforfood Sales orvalue‐addedpackingandprocessing Distribution Marketing Obtainingandusingloanfundsfor

foodSafeFoodHandling business UnderstandingFoodNutritionStandards InsuranceandLiability LabelingRequirementsandDesign TrainingwithProfessionalChef Packaging Other

AdditionalComments______________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________Yes,IaminterestedinstayinginvolvedintheSaltLakeCityCulinaryIncubatorKitchendiscussion.Pleasekeepmeinformedbycontactingme.Name______________________________________________________________Phone:AreaCode()______________________Email___________________________________________

THANK YOU

29

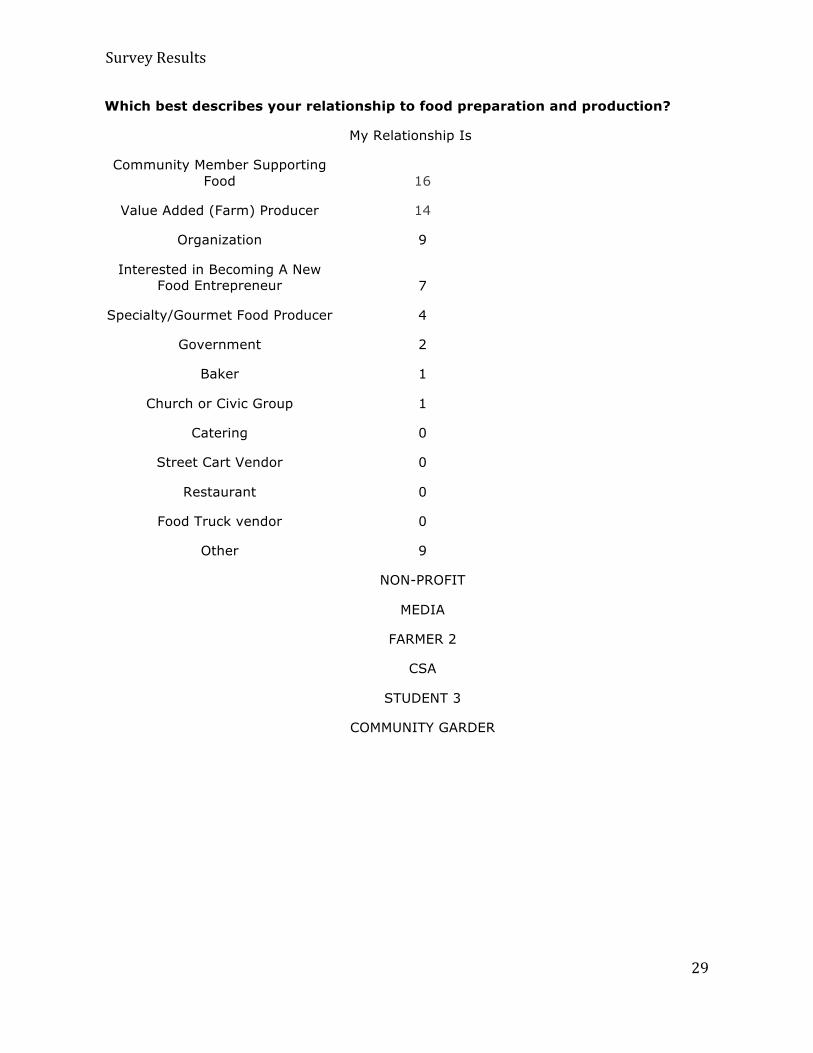

SurveyResults

Which best describes your relationship to food preparation and production?

My Relationship Is

Community Member Supporting Food 16

Value Added (Farm) Producer 14

Organization 9

Interested in Becoming A New Food Entrepreneur 7

Specialty/Gourmet Food Producer 4

Government 2

Baker 1

Church or Civic Group 1

Catering 0

Street Cart Vendor 0

Restaurant 0

Food Truck vendor 0

Other 9

NON-PROFIT

MEDIA

FARMER 2

CSA

STUDENT 3

COMMUNITY GARDER

30

0 5 10 15 20

Jams/Jellies/Syrups

Salsa/Sauces/Condiments

CannedFoodsBakeryGoodsValueAddedProduce

PastaDryMixes

JuicesorotherBeverages

BeerCateredGoodsSidewalkFood

Vendor

FoodTruckVendor

Other

NumberofResponses

TypeofFoodPreparation

WhatTypeofFoodCategoriesareYouPreparingNow,OrWouldLikeToPrepareintheFuture?

N=41SaltLakeCitySurvey2013

PrepareintheFuture

PreparingNow

02468101214161820

Standardrange/Cooktop

Dehydrator

FoodProcessor

WalkInCooler/

Refridgeratorstorage

StainlessSteelTables

FreezerStorage

Mixer

Dishwasher

StandardOven

FillingandPacking

Equiptment

DryStorage

CommercialMixer

ConvectionOven

Grill

SteamJacketedKettle

Fryer

Other

NumberofResponses

TypeofEquipmentNeededforFoodServicePreparation

WhatTypeofEquipmentDoYouNeedforFoodServicePreparation?

31

UtahDepartmentof

Health26%

SaltLakeValleyHealth19%

U.S.FoodandDrug

AdministraFon15%

SaltLakeCityBusinessLiscensing

14%

UtahDeptartment.ofAgricultureand

Food14%

U.S.DepartmentofAgriculture

12%

RegulatoryAgenciesThatCreateChallengestoStarVngorConVnuingLocalFoodProcessing

N=41SaltLakeCity2013

0

5

10

15

20

25

LabelingRequirem

ents

andDesign

Packaging

Obtainingandusing

loanfundsforfood

business

SafeFoodHandling

Preparingabusiness

planforfoodorvalue‐

addedpackagingand

Distribution

Insuranceandliability

Marketing

Trainingwith

professionalchef

Sales

UnderstandFood

NutritionStandards

Other

NumberofResponses

BusinessResourcesorPlanningToolsThatAreofInterest

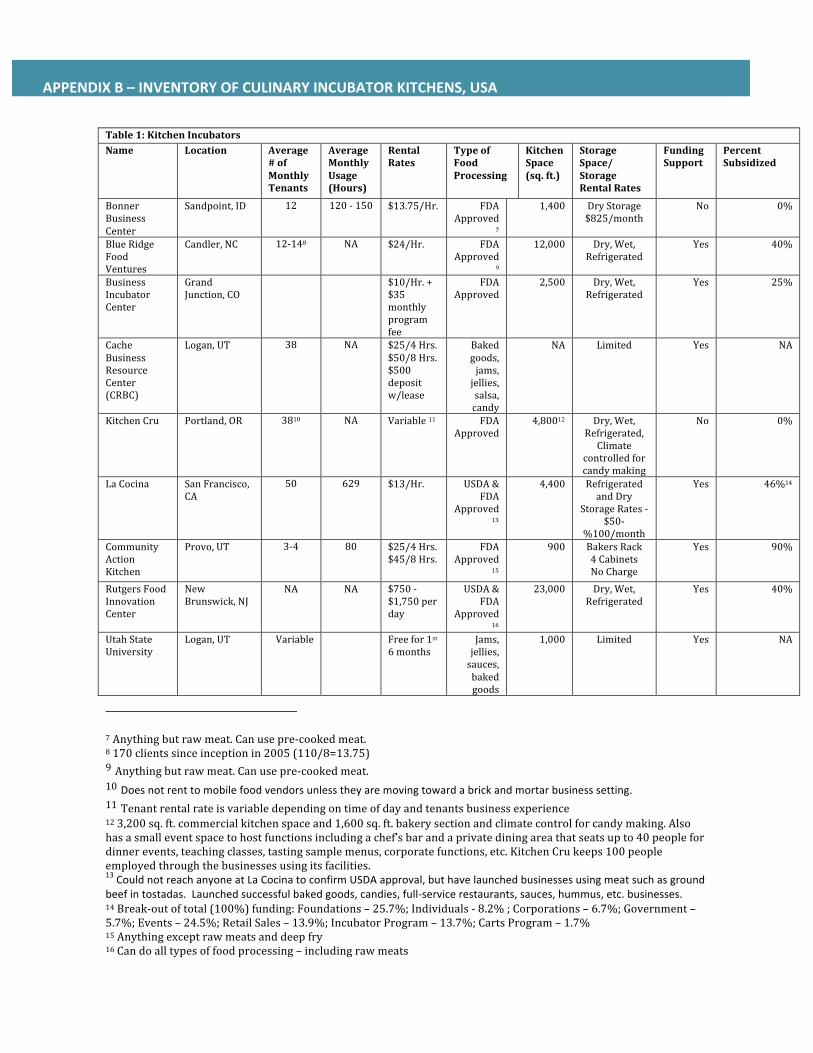

Table1:KitchenIncubatorsName Location Average

#ofMonthlyTenants

AverageMonthlyUsage(Hours)

RentalRates

TypeofFoodProcessing

KitchenSpace(sq.ft.)

StorageSpace/StorageRentalRates

FundingSupport

PercentSubsidized

BonnerBusinessCenter

Sandpoint,ID 12 120‐150 $13.75/Hr. FDAApproved

7

1,400 DryStorage$825/month

No 0%

BlueRidgeFoodVentures

Candler,NC 12‐148 NA $24/Hr. FDAApproved

9

12,000 Dry,Wet,Refrigerated

Yes 40%

BusinessIncubatorCenter

GrandJunction,CO

$10/Hr.+$35monthlyprogramfee

FDAApproved

2,500 Dry,Wet,Refrigerated

Yes 25%

CacheBusinessResourceCenter(CRBC)

Logan,UT 38 NA $25/4Hrs.$50/8Hrs.$500depositw/lease

Bakedgoods,jams,jellies,salsa,candy

NA Limited Yes NA

KitchenCru Portland,OR 3810

NA Variable11 FDAApproved

4,80012 Dry,Wet,Refrigerated,Climate

controlledforcandymaking

No 0%

LaCocina SanFrancisco,CA

50 629 $13/Hr. USDA&FDA

Approved13

4,400 RefrigeratedandDry

StorageRates‐$50‐

%100/month

Yes 46%14

CommunityActionKitchen

Provo,UT 3‐4 80 $25/4Hrs.$45/8Hrs.

FDAApproved

15

900 BakersRack4CabinetsNoCharge

Yes 90%

RutgersFoodInnovationCenter

NewBrunswick,NJ

NA NA $750‐$1,750perday

USDA&FDA

Approved16

23,000 Dry,Wet,Refrigerated

Yes 40%

UtahStateUniversity

Logan,UT Variable Freefor1st6months

Jams,jellies,sauces,bakedgoods

1,000 Limited Yes NA

7Anythingbutrawmeat.Canusepre‐cookedmeat.8170clientssinceinceptionin2005(110/8=13.75)9Anythingbutrawmeat.Canusepre‐cookedmeat.10Doesnotrenttomobilefoodvendorsunlesstheyaremovingtowardabrickandmortarbusinesssetting.11Tenantrentalrateisvariabledependingontimeofdayandtenantsbusinessexperience123,200sq.ft.commercialkitchenspaceand1,600sq.ft.bakerysectionandclimatecontrolforcandymaking.Alsohasasmalleventspacetohostfunctionsincludingachef’sbarandaprivatediningareathatseatsupto40peoplefordinnerevents,teachingclasses,tastingsamplemenus,corporatefunctions,etc.KitchenCrukeeps100peopleemployedthroughthebusinessesusingitsfacilities.13CouldnotreachanyoneatLaCocinatoconfirmUSDAapproval,buthavelaunchedbusinessesusingmeatsuchasgroundbeefintostadas.Launchedsuccessfulbakedgoods,candies,full‐servicerestaurants,sauces,hummus,etc.businesses.14Break‐outoftotal(100%)funding:Foundations–25.7%;Individuals‐8.2%;Corporations–6.7%;Government–5.7%;Events–24.5%;RetailSales–13.9%;IncubatorProgram–13.7%;CartsProgram–1.7%15Anythingexceptrawmeatsanddeepfry16Candoalltypesoffoodprocessing–includingrawmeats

APPENDIXB–INVENTORYOFCULINARYINCUBATORKITCHENS,USA

33

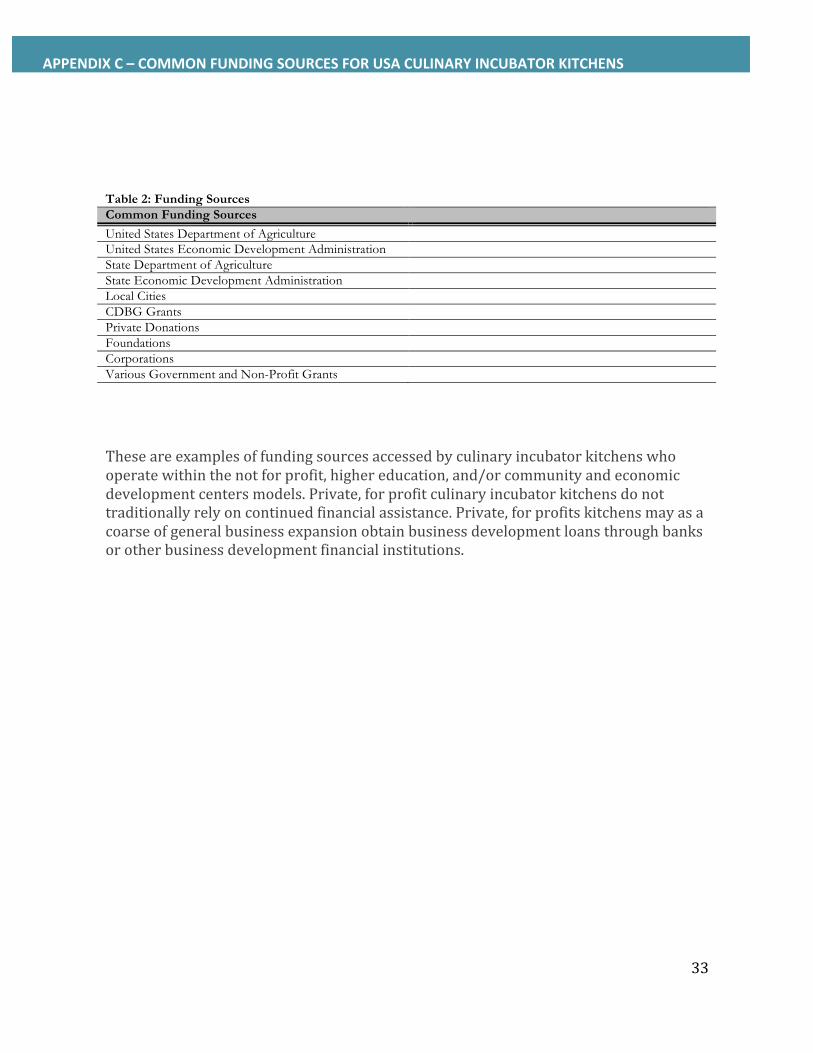

Table 2: Funding Sources Common Funding Sources

United States Department of Agriculture United States Economic Development Administration State Department of Agriculture State Economic Development Administration Local Cities CDBG Grants Private Donations Foundations Corporations Various Government and Non-Profit Grants

Theseareexamplesoffundingsourcesaccessedbyculinaryincubatorkitchenswhooperatewithinthenotforprofit,highereducation,and/orcommunityandeconomicdevelopmentcentersmodels.Private,forprofitculinaryincubatorkitchensdonottraditionallyrelyoncontinuedfinancialassistance.Private,forprofitskitchensmayasacoarseofgeneralbusinessexpansionobtainbusinessdevelopmentloansthroughbanksorotherbusinessdevelopmentfinancialinstitutions.

APPENDIXC–COMMONFUNDINGSOURCESFORUSACULINARYINCUBATORKITCHENS

34

Resourceinformationforthisreportisdrawnfromoneinpersonandphoneinterviewswithculinaryincubatorkitchenandhighereducationdirectorsandstaff,andthefollowingsources.

1. AgriculturalMarketingResourceCenter,www.agmre.org/business_development/strategy_and_analysis/analysis/blue‐ridge‐food‐ventures

2. Mintel

3. NationalAssociationfortheSpecialtyFoodTrade

4. NorthAmericanIndustryClassificationSystem(NAICS)http://www.census.gov/cgi‐bin/sssd/naics

5. NortheastCenterforFoodEntrepreneurship,necfe.foodscience.cals.cornell.edu

6. OrganicTradeAssociation

7. PhoneinterviewswithDirectorsandSupportStaffofallCulinaryIncubatorKitchensreferencedinthisAppendixB

8. PhoneinterviewwithJasonTalcott,DirectorofCulinaryArts,SaltLakeCommunity

College

9. PhoneinterviewwithUtahbasedfoodenterprises

10. 2010,USCensusandAmericanCommunitySurvey,census.gov

11. SaltLakeCityCensus2010Atlas,Downen,John;Perlich,Pamela,Bureauof

EconomicandBusinessResearch,DavidEcclesSchoolofBusiness

12. SaltLakeCommunityCollege,CulinaryArtsProgram

13. SaltLakeCitySchoolDistrict,StudentDemographicData,www.slcschools.org

14. USDepartmentofCommerce

15. USDepartmentofAgriculture,www.usda.gov

16. UtahDepartmentofAgricultureandFood,DivisionofRegulatoryServices

17. USFoodandDrugAdministration,FoodGuidanceRegulationwww.fda.gov

18. UtahCode4‐5‐9.5

19. UtahDepartmentofWorkforceServices

20. TheNationalBusinessIncubationAssociation

21. TheRiseoftheCreativeClass,Florida,Richard,2011

ENDNOTES

35

THEEND

36