-

7/28/2019 Sample Calculation Part Working Capital

1/31

A. LIQUIDITY RATIOS

1. CURRENT RATIO

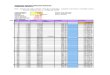

CURRENT RATIO = CURRENT ASSETS / CURRENT LIABILITIES

Table No: 5.1

Source: Annual Report of HMT Ltd., From 2008-12

Graph No: 5.1

Interpretation: The ratio is equal to or near to 2:1, i.e.,

current assets double the current

liabilities is considered to be idle for the research period.

The firm is not maintaining the

current assets as per idle levels over the period of the study.

It is too low for year 2010-11 ie.,

0.65.

2.ACID TEST OR QUICK RATIO :

Table No: 5.2

YEAR QUICK ASSETS CURRENT

LIABILITIES

QUICK RATIO

(In times)

47

YEAR CURRENT

ASSETS (Rs)

CURRENT

LIABILITIES (Rs)

CURRENT RATIO

(In times)

2008-2009 3,99,12,174 4,93,99,123 0.80

2009-2010 6,00,80,235 6,00,95,467 0.99

2010-2011 6,37,29,138 8,06,58,227 0.79

2011-2012 7,90,80,195 12,14,00,470 0.65

-

7/28/2019 Sample Calculation Part Working Capital

2/31

2008-2009 85,02,095 4,93,99,123 0.172

2009-2010 1,86,06,435 6,00,95,467 0.309

2010-2011 1,07,24,367 8,06,58,227 0.132

2011-2012 1,95,94,503 12,14,00,470 0.161

Source: Annual Report of HMT Ltd., From 2008-12

ACID TEST RATIO= QUICKASSETS / CURRENT LIABILITIES

Graph No: 5.2

Interpretation: The quick ratio is high in the year 2009-10 when

compared to other years

next best year for quick ratio is 2007 to 08 followed by 06-07,

and 09-10. In the year 08-09

quick ration is very less because current liabilities has

decreased. But from last 4 years firm is

in a position to maintain the idle levels that is 1: 1.

1. Cash ratio: Cash ratio = Cash and bank balances / Current

liabilities

Table No: 5.3

48

YEAR Cash and bank

balances

Current

liabilities

Cash Ratio

(In times)

2008-2009 9,88,418 4,93,99,123 0.022009-2010 6,90,661

6,00,95,467 0.011

2010-2011 5,03,843 8,06,58,227 0.007

2011-2012 3,27,889 12,14,00,470 0.004

-

7/28/2019 Sample Calculation Part Working Capital

3/31

Source: Annual Report of HMT Ltd., From 2008-12

Graph No: 5.3

Interpretation: The overall year from 2008-2012, the operating

ratio was in positive trend.

Where as in the year 2008-2009 the operating ratio was higher

then other 4 years, and it

indicates the ratio operating profits and sales is more in the

year 2008-2009 is the highest

compared to the other years.

B. TURN OVER RATIOS

COST OF GOODS SOLD

INVENTORY TURN OVER RATIO =

AVGERAGE INVENTORY

Table No: 5.4

49

YEAR COST OF

GOODS

SOLD

AVGERAGE

INVENTORY

RATIO

(In times)

2008-2009 34,01,717 85,02,095 0.40

2009-2010 42,87,638 13,55,426.5 0.32

2010-2011 41,00,613 69,95,440.5 0.59

2011-2012 46,15,472 58,84,272.5 0.79

-

7/28/2019 Sample Calculation Part Working Capital

4/31

-

7/28/2019 Sample Calculation Part Working Capital

5/31

Source: Annual Report of HMT Ltd., From 2008-12

Graph No: 5.5

Interpretation: Debtors turnover ratio is the ratio between

Debtors and Credit sales, as the

ratio is the positive it shows the collection of debts.

Comparing to all the above 4 years 2009-

10 is least collection and in the year 2010-11 the rate of

collection is high.

3. CREDITORS TURNOVER RATIO:

NET CREDIT PURCHASES

CREDITORS TURNOVER RATIO =

AVERAGE CREDITORS

Table No: 5.6

YEAR NET CREDIT

PURCHASES

AVERAGE

CREDITORS

RATIO

(In times)

2008-2009 2,57,92,594 2,57,92,594 1

2009-2010 3,31,95,823 2,94,96,709 1.125

51

-

7/28/2019 Sample Calculation Part Working Capital

6/31

-

7/28/2019 Sample Calculation Part Working Capital

7/31

-

7/28/2019 Sample Calculation Part Working Capital

8/31

-

7/28/2019 Sample Calculation Part Working Capital

9/31

Interpretation: Fixed assets turnover ratio in the year

2011-2012 was the highest that is 1.67

and the other years were comparatively low. And the fixed asset

turn over ratio is low in the

year 2007-08.

7. CURRENT ASSETS TURN OVER:-

CURRENT ASSETS TURN OVER = SALES / CURRENT ASSETS

Table No: 5.11

YEAR SALES Current Assets RATIO

(In times)

2008-2009 114097329 3,99,12,174 2.85

2009-2010 154652721 6,00,80,235 2.57

2010-2011 138763846 6,37,29,138 2.18

2011-2012 215787862 7,90,80,195 2.73

Source: Annual Report of HMT Ltd., From 2008-12

Graph No: 5.11

55

-

7/28/2019 Sample Calculation Part Working Capital

10/31

-

7/28/2019 Sample Calculation Part Working Capital

11/31

1) Operating activates of Cash flow for the Year 2007-08 (Rs/-

in Crores)

Table No: 5.12

Cash Flow from Operating Activities

YEAR

ENDED

31-03-2007

YEAR

ENDED

31-03-2008

Profit /(Loss) as per the profit & Loss a/c 95.2 93.77

Adjustment for depreciation 122.76 119.76

Fringe Benefits tax provision - 1.75

Interest and financial charges Paid 4.97 12.43

Loss on sail on fixed assets - 1.39

Interest Earned 1.28 0.2

Operating Profit/(Loss) before working

Capital Charges 31.25 37.86

Add Extra-Ordinary Items -

Benefits under OTS-Principal Waiver - 566.33

Benefits under OTS-Principal Waiver - 241.31

Insurance claim Receiver - 34.6

Interest on Insurance claim received - 26.5

Creditors Written off 1042.59

Profit after extra-Ordinary items but before

working charges 31.25 -

Adjustments for -

Increased/Decrease in Sundry Debtors 37.78 17.83

Increased/Decrease in Inventory 12.07 101.04Increased/Decrease

in Current Liabilities 65.58 106.96

Increased/Decrease in Loans& Advances 7.64 140.63

Cash Generated from Operations 54.62 925.29

Interest and Financial Charges Paid 4.97 12.43

Net Cash from Operating Activities 49.65 913.29

Source: Annual Report of HMT Ltd., From 2007-08

1) By comparing Net cash from operations activities of 2007-08

the cash balances are so

high due to the increase in Cash generation from Operations are

high.

2) Comparing to 2007-08 the overall operations i.e.. Increase in

Sundry Debtors,

Inventory, Current Liabilities and Loans and advances.

Investing activates of Cash flow for the year 2007-08 ( Rs/- in

Crores)

57

-

7/28/2019 Sample Calculation Part Working Capital

12/31

Table No: 5.13

Cash Flow from investing Activities 2007 2008

Purchases of Fixed assets including CWP 20.34 51.55

Proceeds From sale of fixed Assets - 0.9

Interest Earned 1.28 0.2

Deferred Revenue expenditure 14.61 5.64

Cash used in Investing activities 4.45 44.81

Source: Annual Report of HMT Ltd., From 2007-08

The investments are so high in the year due to the cash

generations from operations

are so high.

58

-

7/28/2019 Sample Calculation Part Working Capital

13/31

Financing Activates of Cash Flow for the year 2007-08 (Rs/- in

Crores)

Table No: 5.14

Cash Flow from Financing activities 2007 2008

Principal and Interest weiver from Banks 10.11 809.65

Increases in Share Application Money - 210

Amount paid under OTS - 127.25

Increase/(Decrease) in other secured loans 49.6 21.52

Prior period adjustment - 12.2

Increased/(Decrease) Unsecured Loans 6.67 148.95

Interest and financial charges Paid 53.04 866.54

Cash used in Investing activities

Net Increase/(Decrease) in cash & cash equilents 7.84

1.94

Opening cash & cash equilents 12.87 5.04Closing cash &

cash equilents 5.04 6.98

Source: Annual Report of HMT Ltd., From 2007-08

The principal and interest weaver from Banks are so high in

financing activities in

2006 due to cash generations are so high in the year 2008

59

-

7/28/2019 Sample Calculation Part Working Capital

14/31

2) Operating activates of Cash flow for the Year 2007 2008 (Rs/-

in Crores)

Table No: 5.15

Cash Flow from Operating ActivitesYEARENDED

31-03-2008YEARENDED

31-03-2009

Profit /(Loss) as per the profit & Loss a/c93.77 92.68

Adjustment for depreciation 119.76 121.79

Fringe Benefits tax provision 1.75 0

Interest and financial charges Paid 12.43 4.15

Loss on sail on fixed assets 1.39 0.84

Interest Earned 0.2 0.04

Operating Profit/(Loss) before working

Capital Charges 37.86 34.06

Add Extra-Ordinary Items

Benefits under OTS-Principal Waiver 566.33 135.89

Benefits under OTS-Principal Waiver 241.31 0

Insurance claim Receiver 34.6 0

Interest on Insurance claim received 26.5 0

Creditors Written off 1042.59 0

Profit after extra-Ordinary items but before

working charges - 169.95

Adjustments for -

Increased/Decrease in Sundry Debtors 17.83 45.52

Increased/Decrease in Inventory 101.04 78.82

Increased/Decrease in Current Liabilities 106.96 36.34

Increased/Decrease in Loans& Advances 140.63 118.43

Cash Generated from Operations 925.29 358.02

60

-

7/28/2019 Sample Calculation Part Working Capital

15/31

-

7/28/2019 Sample Calculation Part Working Capital

16/31

Financing Activates of Cash Flow for the year 2008 2009 (Rs/- in

Crores)

Table No: 5.17

Cash Flow from Financing activities 2008 2009

0

Principal and Interest weiver from Banks 809.65 135.89

Increases in Share Application Money 210 0

Amount paid under OTS 127.25 265.09

Increase/(Decrease) in other secured loans 21.52 16.82

Prior period adjustment 12.2 25.87

Increased/(Decrease) Unsecured Loans 148.95 74.61

Interest and financial charges Paid 866.54 4.15

Cash used in Investing activities 339.57

Net Increase/(Decrease) in cash & cash equilents 1.94

1.93

Opening cash & cash equilents 5.04 6.97Closing cash &

cash equilents 6.98 5.04

Source: Annual Report of HMT Ltd., From 2010-11

The interest and financial charges paid are so high in the year

2008 that compared to

2009. Due to the unsecured loans are high in the year 2008.

62

-

7/28/2019 Sample Calculation Part Working Capital

17/31

3) Operating activates of Cash flow for the Year 2009 2010 (Rs/-

in Crores)

Table No: 5.18

Cash Flow from Operating Activites

YEAR

ENDED

31-03-2009

YEAR

ENDED

31-03-2010

Profit /(Loss) as per the profit & Loss a/c 92.68 111.09

Adjustment for depreciation 121.79 123.13

Fringe Benefits tax provision 0 0

Interest and financial charges Paid 4.15 12.85

Loss on sail on fixed assets 0.84 0

Interest Earned 0.04 0.22

Operating Profit/(Loss) before working Capital

Charges 34.06 246.84Add Extra-Ordinary Items

Benefits under OTS-Principal Waiver 135.89 0

Profit after extra-Ordinary items but before

working charges 169.95 246.84

Adjustments for

Increased/Decrease in Sundry Debtors 45.52 154.3

Increased/Decrease in Inventory 78.82 88.71

Increased/Decrease in Current Liabilities 36.34 153.51

Increased/Decrease in Loans& Advances 118.43 22.64

Cash Generated from Operations 358.02 179.98Interest and

Financial Charges Paid - 179.98

Net Cash from Operating Activities 358.02 179.98

Source: Annual Report of HMT Ltd., From 2010-11

The net cash from operating activities of 2009 are almost all

doubled that compared to

2010. Due to the investments is less than that to 2009 to

2010.

63

-

7/28/2019 Sample Calculation Part Working Capital

18/31

Investing activates of Cash flow for the year 2009 (Rs/- in

Crores)

Table No: 5.19

Cash Flow from investing Activities 2009 2010

Purchases of Fixed assets including CWP 25.86 69.34

Proceeds From sale of fixed Assets 5.13 0

Interest Earned 0.04 0.22

Deferred Revenue expenditure 0.31 0

Cash used in Investing activities 20.38 69.11

Source: Annual Report of HMT Ltd., from 2010-11

The purchases of fixed assets are less that compared to 2010 to

2009. At the same time

the differed Revenue Expenditure are more due to the less

purchases of fixed assets.

Financing Activates of Cash Flow for the year 2009 (Rs/- in

Crores)

Table No: 5.20

Cash Flow from Financing activities 2009 2010

Principal and Interest waiver from Banks 135.89 0

Amount paid under OTS 265.09 230

Increase/(Decrease) in other secured loans 16.82 36.86

Prior period adjustment 25.87 1

Increased/(Decrease) Unsecured Loans 74.61 89.12

Interest and financial charges Paid 4.15 12.85Cash used in

Investing activities 339.57 115.87

Net Increase/(Decrease) in cash & cash equivalents 1.93

5

Opening cash & cash equivalents 6.97 5.04

Closing cash & cash equivalents 5.04 0.04

Source: Annual Report of HMT Ltd., From 2010-11

The closing Cash and cash equivalents are having huge difference

due to the purchases of

fixed assets in the year of 2010.

ANALYSIS OF WORKING CAPITAL MANAGEMENT IN HMT:

Figures in lakhs 2005 2006 2007 2008 2009 2010 2011

Particulars

CURRENT ASSETS:

Inventories 3733.17 4831.75 5736.59 2861.75 3056.24 3261.66

2873.02

Sundry Debtors 845.18 917.17 1045.87 1417.74 1526.91 1364.52

1695.27

64

-

7/28/2019 Sample Calculation Part Working Capital

19/31

Other Current

Assets4.23 5.18 7.96 50.67 126.68 274.77 95.39

Loans and

Advances96.14 122.13 196.25 366.78 473.99 533.66 649.56

CURRENT LIABILITIES:Acceptances - - - 61.95 7.49 9.76 3.67

Sundry Creditors314.91 451.81 574.18

549.05807.54 1120.77 1205.88

HMT Ltd

(Subsidiary

companies)

10.28 4.35 19.58 5.39 13.32 12.77 12.15

Advance against

sales2893.97 2451.83 3680.84 1906.86 2010.03 2207.09 1671.40

Other Liabilities 322.24 299.26 484.22 203.19 544.61 551.85

971.71Interest accrued

but not due8.45 3.43 12.48 7.23 4.21 2.88 63.94

Provisions 33.12 143.24 66.66 247.38 382.39 704.85 869.41

2345.96 1647.50 4837.96 2981.50 3767.59 4609.97 4798.16

Gross Working

Capital2341.34 3786.56 7059.50 4798.35 5311.36 5466.27

5337.47

Net Working

Capital1225.18 1678.45 2221.54 1816.85 1543.77 856.03 539.31

ANALYSIS OF WORKING CAPITAL IN HMT (HYDERABAD)

2007: -

Gross working capital is 7059.54lakhs and this mainly consisted

of inventories worth

5736.59 and sundry debtors amounting to 1045.87lakhs.

Net working capital is 2221.54lakhs. The current liabilities are

574.96lakhs. Sundry creditors

are 574.18lakhs while advance against sales is 3680.84lakhs.

2008: -

65

-

7/28/2019 Sample Calculation Part Working Capital

20/31

Gross working capital is 4798.35lakhs and this mainly consisted

of inventories worth

2861.75lakhs and sundry debtors amounting to 1417.741lakhs.

Net working capital is 1816.85lakhs. The current liabilities

amounted to 2981.50lakhs

of which major part is constituted by advance against sales,

which was 1906.86lakhs.

2009: -

Gross working capital is 5311.36lakhs and this mainly consisted

of inventories worth

3056.24lakhs and sundry debtors worth 1526.91lakhs.

Net working capital is 1543.77lakhs. Current liabilities

amounted to 3767.59lakhs of

which major part is constituted by advances against sales which

amounted to 2010.03lakhs

followed by sundry creditors worth 807.54lakhs.

2010: -

Gross Working Capital is 5466.27lakhs consisting mainly of

inventories worth

3261.66lakhs and sundry debtors worth 1364.52lakhs.

Net working capital is 856.31lakhs. This year networking capital

is low compared to

previous three years mainly due to higher current liabilities

which amounted to 4609.97lakhsof which major part is constituted by

advance against sales amounting to 2207.09lakhs

followed by sundry creditors worth 1120.77lakhs.

2011: -

Gross working capital is 5337.47lakhs consisting mainly of

inventories worth

2873.02lakhs and sundry debtors worth 1695.27lakhs.

Net working capital is 539.31lakhs. It has declined further due

to rise in current

liabilities which amounted to 4796.16lakhs of which major part

is constituted by advance

against sales amounting to 167.40lakhs followed by sundry

creditors worth 1205.88lakhs.

COMPARITIVE BALANCE SHEET

66

-

7/28/2019 Sample Calculation Part Working Capital

21/31

The effect of conduct of a business is reflected in its balance

sheet by increase or

decrease in assets, liabilities and proprietary capital. These

changes can be known by a

comparison of the balance sheets of two or more different dates

of previous years. Knowledge

of this change is of considerable value in framing an operation

regarding the progress of the

business unit, while a single balance sheet reveals the

financial status at a specified point of

time, a comparative balance sheet analysis shows the changes in

it. These changes may be

result of operations, the conversion of assets, liabilities and

capital. In the comparative

balance sheet not only the absolute changes (in terms of rupees)

the relative changes are more

important than others to the analyst. Information regarding

relative changes must modify the

analysis of operations based on absolute changes.

In the computation of percentages it should be noted that if a

certain item has a value

in one year and does not exist in the next year, the percentage

of decrease in 100%. But if the

item has no value in the first year and has a value in the

second year, no percentage can be

shown because if zero divides a number, the quotient is

infinity.

COMPARITIVE STATEMENT OF BALANCE SHEETS FOR 2008 AND 2009:

Figures in Lakhs

Particulars 2007 2008 Increase/ Decrease%Increase /

Decrease

Fixed Assets - - - -

Gross Block 2763.56 2763.16 - -

Less: Depreciation 2337.07 2425.80 - -

Net Block 426.49 337.36 (89.13)(20.89)

Capital Work in 64.39 100.09 36.51 56.07

Progress (at Cost) - - - -

Machine and 1.47 - (1.47) (100)

Equipment in

Transit- - - -

And under

inspection (at cost)- - - -

Investment - - - -

Current Assets: 492.35 438.26 (54.09) (10.98)

67

-

7/28/2019 Sample Calculation Part Working Capital

22/31

Inventories 5736.59 286175 (2874.84) (50.11)

Sundry debtors10445.8

71417.74 371.87 35.56

Cash and Bank

Balance 7.96 50.67 42.71 536.55

Other Current

Assets72.83 101.41 28.58 39.24

Loans and

Advances196.25 366.78 170.52 86.09

Fixed Liabilities 7059.50 4798.35 (2261.15) (32)

Capital - - - -

Reserves and

Surplus4.84 12.14 7.03 150.08

Head office

Current a/c 1516.45 972.93 (543.52) (35.08)

Secured Loans 1199.05 1178.42 (20.63) (1.72)

Unsecured Loans - 61.95 92.31 -

Current Liabilities: 2720.34 2255.80 (464.54) (17.00)

Acceptances - - - -

Sundry Creditors 574.18 549.50 (24.68) (4.298)

HMT (Subsidiary

Companies)19.58 5.39 (14.19) (72.47)

Advance against

sales

3680.84 1906.86 (1773.98) (48.19)

Other Liabilities 484.22 203.19 (281.03) (58.04)

Interest accrued but

Not due

Provisions

12.48

66.66

7.23

247.38

(5.25)

180.72

(42.07)

71.11

4837.96 2981.50 (1856.46) (38.37)

Miscellaneous

Expenditure (to the

Extent not written

Off or Adjusted)

6.43 0.07 (5.73) (89.11)

COMPARITIVE STATEMENTS OF BALANCE SHEETS FOR 2008 AND 2009

Figures in Lakhs

Particulars 2008 2009 Increase/ Decrease%Increase

/Decrease

68

-

7/28/2019 Sample Calculation Part Working Capital

23/31

Fixed Assets

Gross Block 2763.16 2761.84 - -

Less: 2425.80 2498.61 - -

Depreciation

Net Block 337.36 107.67 (73.09) (21.09)

Capital Work inProgress (at Cost) - - - -

Machine and - 9.01 9.01 -

Equipment in

Transit- - - -

And under

inspection (at cost)- - - -

Investment - - - -

Current Assets: 438.28 380.00 (58.26) (13.29)

Inventories 2861.75 3056.24 194.49 6.79

Sundry debtors 1417.74 1526.91 109.177.07

Cash and Bank

Balance 50.67 126.68 76.01 150

Other Current

Assets101.41 127.54 26.13 25.77

Loans and

Advances366.79 476.99 107.21 29.23

Fixed Liabilities 4798.35 5311.36 516.01 10.75

Capital - - - -Reserves and

Surplus12.14 12.14 - -

Head office

Current a/c972.93 688.89 (284.04) (29.19)

Secured Loans 1178.42 1222.95 (44.53) (3.78)

Unsecured Loans 92.31 - (92.31) (100)

2255.80 193.98 (331.82) (14.07)

Miscellaneous

Expenditure (to the

Extent not written

Off or Adjusted)

0.07- (0.07) (100)

Current Liabilities:

Acceptances 61.95 7.49 (54.45) (87.09)

Sundry Creditors549.50

807.54 258.04 46.96

69

-

7/28/2019 Sample Calculation Part Working Capital

24/31

HMT

(Subsidiary

Companies)

5.39 13.32 7.93147.12

Advance

Against sales1906.86 2010.03 101.17 5.03

Other Liabilities 7.23 4.21 (3.02) (41.77)

Interest accrued

But not due

Provisions 247.38 382.39 135.01 54.58

2981.50 3767.14 785.64 26.35

COMPARITIVE STATEMENT OF BALANCE SHEET FOR 2009 AND 2010

Figures in Lakhs

Particulars 2009 2010 Increase/ Decrease%Increase /

Decrease

Fixed Assets

Gross Block 2761.84 2769.56 - -

Less: 2425.80 2498.61 - -

Depreciation

Net Block 263.23 213.73 (49.05) (18.80)

Capital Work in

Progress (at Cost) - - - -

Machine and 9.01 9.03 0.02 2.19

Equipment in

Transit- - - -

And under

inspection (at cost)- - - -

Investment - - - -

Current Assets: 380.00 334.97 (45.03) (11.85)

Inventories 3056.24 3261.66 205.42 6.72

Sundry debtors 1526.91 1364.52 (162.39) (10.64)

Cash and Bank

Balance 126.68 274.77 148.09 116.90Other Current

Assets127.54 29.66 (97.88) (76.94)

Loans and

Advances476.99 535.66 58.67 12.09

Fixed Liabilities 5311.36 5466.27 154.91 2.92

Capital - - - -

70

-

7/28/2019 Sample Calculation Part Working Capital

25/31

Reserves and

Surplus12.14 12.14 - -

Head office

Current a/c688.89 10.01 (678.88) -

Secured Loans 1222.95 1146.60 (76.38) (6.24)Unsecured Loans - -

- -

1923.98 1158.73 (765.04) (39.76)

Miscellaneous

Expenditure (to the

Extent not written

Off or Adjusted)

0.07- (0.07) (100)

Current Liabilities:

Acceptances 7.49 9.76 2.26 30.54Sundry Creditors 807.54 1120.77

313.23 38.79

HMT

(Subsidiary

Companies)

13.32 12.77 (0.55) (4.13)

Advance

Against sales2010.03 2207.09 199.06 9.91

Other Liabilities 544.61 551.85 7.69 1.41

Interest accrued

But not due

4.21 2.88 (1.33) (31.59)

Provisions 382.39 704.85 322.47 84.33

3767.14 4609.97 842.33 22.35

Miscellaneous

Expenditure (to

The extent not

Written off or

Adjusted)

- - - -

COMPARITIVE STATEMENT OF BALANCE SHEET FOR 2010 AND 2011

Figures in Lakhs

Particulars 2010 2011 Increase/ Decrease%Increase /

Decrease

Fixed Assets

71

-

7/28/2019 Sample Calculation Part Working Capital

26/31

Gross Block 2769.65 2775.53 - -

Less: 2555.83 2585.12 - -

Depreciation

Net Block 213.73 190.41 (23.32) (10.91)

Capital Work in

Progress (at Cost) 111.94 111.94 - -Machine and 9.03 2.03 (7.00)

(75.27)

Equipment in

Transit- - - -

And under

inspection (at cost)- - - -

Investment - - - -

Current Assets: 334.97 304.65 (30.32) (9.05)

Inventories 3261.66 2873.02 (388.64) (11.92)

Sundry debtors 1364.52 1695.27 330.75 24.24

Cash and BankBalance 274.77 95.39 (179.38) (65.28)

Other Current

Assets29.66 24.23 (5.43) (18.30)

Loans and

Advances535.66 649.56 113.09 21.26

Fixed Liabilities 5466.27 5337.47 (128.08) (2.36)

Capital - - - -

Reserves and

Surplus

12.14 12.14 - -

Head office

Current a/c-10.01 -1696.43 (1686.42) -

Secured Loans 1146.60 1393.38 246.78 21.52

Unsecured Loans - - - -

1158.74 1405.52 246.78 21.29

Miscellaneous

Expenditure (to the

Extent not written

Off or Adjusted)

0.07 - (0.07) (100)

Current Liabilities:

Acceptances 9.76 3.67 (6.09) 62.30)

Sundry Creditors 1120.77 1205.88 85.11 7.59

HMT

(Subsidiary

Companies)

12.77 12.15 (0.62) (4.86)

72

-

7/28/2019 Sample Calculation Part Working Capital

27/31

Advance

Against sales2207.09 1671.40 (535.69) (24.27)

Other Liabilities 551.85 971.71 419.86 76.08

Interest accrued

But not due

2.88 63.94 61.06 2120.13

Provisions 704.85 869.41 164.56 23.35

3767.14 4609.97 888.19 4.08

Miscellaneous

Expenditure (to

The extent not

Written off or

Adjusted)

- - - -

ANALYSIS OF COMPARITIVE STATEMENT OF BALANCE SHEETS

2007 2008

Fixed assets in 2007 were at 492.3lakhs but in 2008 it decreased

to 438.26lakhs. This

is because there is reduction in the rate of depreciation.

Current assets in 2007 were at 7059.52lakhs but they decreased

to 4798.35lakhs. This

is mainly due to decrease in levels of inventories.

Fixed liabilities in 2007 were at 2720.34lakhs while in 2008 it

was 22565.80lakhs,

there was decreased in head office current a / c by

543.52lakhs.

Current liabilities in 2007 were at 4937.96lakhs but decreased

to 2981.50lakhs in 2007

mainly because of decrease in advance against sales.

2008 -09

Fixed assets in 2008 were at 438.26lakhs but it decreased to

380lakhs in 2009.

Current assets in 2008 were at 4798.35lakhs but increased to

5311.36lakhs in 2009

mainly because of decrease in head office current a / c by

284.04lakhs.

73

-

7/28/2019 Sample Calculation Part Working Capital

28/31

Current liabilities in 2008 were 2481.50lakhs which increased to

37667.14lakhs in

2009 due to increase in sundry creditors by 258.04lakhs followed

by other liabilities which

were 341.42lakhs.

2009 -10

Fixed assets in 2009 were at 380lakhs decreased to 334.97lakhs

in 2010.

Current assets in 2009 were at 5311.36lakhs which increased to

5466.27lakhs in 2010.

This is because of increase in inventories by 205.42lakhs

followed by cash and bank balance

148.04lakhs.

Fixed liabilities in 2009 were at 1923.77lakhs which declined to

1168.75lakhs in 2010.

This is due to decrease in head office current a / c by

678.88lakhs.

Current liabilities in 2009 were at 3767.64lakhs which increased

to 4609lakhs in 2010.

This is mainly due to increase in sundry creditors by

313.23lakhs.

2010 -11

Fixed assets in 2010 were at 334.97lakhs which decreased to

304.65lakhs in 2011.

Current assets in 2010 were at 5466.27lakhs which decreased to

5337.47lakhs. This isdue to decrease in inventories and cash and

bank balance by 388.64lakhs and 179.38lakhs

respectively, even though there was an increase in sundry

debtors by 330.75lakhs.

Fixed liabilities in 2010 were at 1158.74lakhs which increased

to 1405.52lakhs in

2011. This is mainly due to increase in secured loans by

246.78lakhs.

Current liabilities in 2010 were at 4609.97lakhs but increased

to 4798.16lakhs in 2011

mainly because of increase in other liabilities by

419.86lakhs.

ANALYSIS OF THE PROJECT

The analysis of the project is being made with reference to the

theory of working

capital management. The theory is used here to understand the

current assets and current

74

-

7/28/2019 Sample Calculation Part Working Capital

29/31

liabilities and working capital; also it is helpful to

Receivable management and Cash budget

frosting we will analyze about the current assets ratio and

quick ratio.

The current ratio is also called the working capital ratio,

since it is related to the

working capital of firm. The current ratio of the firm managers

its short term solvency., its

ability to meet short term obligations. It implies that for

every rupee of current liabilities what

amount of the current assets is available to meet them. Here we

find that the current ratio has

increased for the past two years. It indicates adequate margin

of safety between assets that

will be available to liquidate claims.

The Quick ratio is a rigorous measure of a firms ability to

service short term

liabilities. The usefulness of the ratio lies in the fact that

it is widely accepted as the best

available test of the liquidity position of a firm. In this case

low ratio can be interpreted as

large part of the current assets of the firm is tied up in slow

moving and unsolvable

inventories and slow paying debts. The firm would find it

difficult to pay its current liabilities.

ANALYSIS OF RECEIVABLE MANAGEMENT IN HINDUSTHAN MACHINE

TOOLS LIMITED:

A firm investment in Accounts Receivables depends on

(a) Volume of Credit Sales and

(b) The Collection Period

The volume of credit sales is a function of the firms total

sales depends on the market

size. The firms market share, product quality intensity of

competition, economic condition

etc. The percentage of credit sales to total sales is mostly

influenced by nature of business and

industry norms.

At HMT, the volume of Credit Sales constitutes to percent of

total sales. Much of

the business is generated because of the credit facility

provided by the firm.

The collection period is the average time taken the customer to

make the payment for

the credit purchases.

At HMT, the present collection period is 72 days.

75

-

7/28/2019 Sample Calculation Part Working Capital

30/31

There is one way in which the financial manager can affect the

volumes of Credit

Sales and Collection period and consequently, investment in

accounts receivable. This is

through changes in credit policy. The term credit policy is used

to refer the combination of

three decision variables.

1) Credit standards

2) Credit terms and

3) Collection efforts

Referee we discus about the decision variable it is important to

about a credit policy is,

a firm may follow lenient or stringent credit policy.

At HMT, the credit policy, which is being followed, has an

inclination towards the

lenient credit policy. The reason behind it is the customers to

whom they are catering.

GOALS OF CREDIT POLICY:

The main goal of the Credit Policy is additional sales and at

the same time reduction in

costs due to additional sales. Additional sales should add to

the firms operating profits there

are three types of costs involved.

1) Production and selling costs

2) Administrative costs

3) Bad debt losses

At HINDUSTHAN MACHINE TOOLS LIMITED, the losses from bad debts

are

relatively less because of two reasons. The clients of this firm

who constitution % of their

sales has proven track record for credit worthiness and other

reasons is that companys

product is shortage product and the customers dont want their

names dropped from the

customers list because their production will come to stand

still.

CREDIT TERMS:

76

-

7/28/2019 Sample Calculation Part Working Capital

31/31

The second decision is account receivable management is the

credit terms. After the

credit worthiness of the customers has been assessed, the

management must determine the

terms and conditions on which the trade credit will be made

available. The stipulation under

which the credit is made available is called credit terms.

The stimulations include:

1) The credit period

2) The cash discount

At HINDUSTHAN MACHINE TOOLS LIMITED, the firms credit period is

sixty

days. Most of the customers pay their bills within the credit

but some credit sales do result in

debtors outstanding for more than 3 months or 90 day.