Embed Size (px)

Citation preview

SAP GST India Forum

Neel Ratan

Executive Director

PricewaterhouseCoopers,

e-Governance in India

India on Brink of GST Some unanswered questions…

www.pwc.in

PwC

Content

Section 1 Enactment Timelines

Section 2 GSTN Processes

Section 3 Rate debate

Section 4 Place of supply rules and credit

Section 5 Transition provisions

Slide 3

March 2015

`

PwC

Content

Slide 4

March 2015

`

Section 1 Enactment Timelines

Section 2 GSTN Processes

Section 3 Rate debate

Section 4 Place of supply rules and credit

Section 5 Transition provisions

PwC

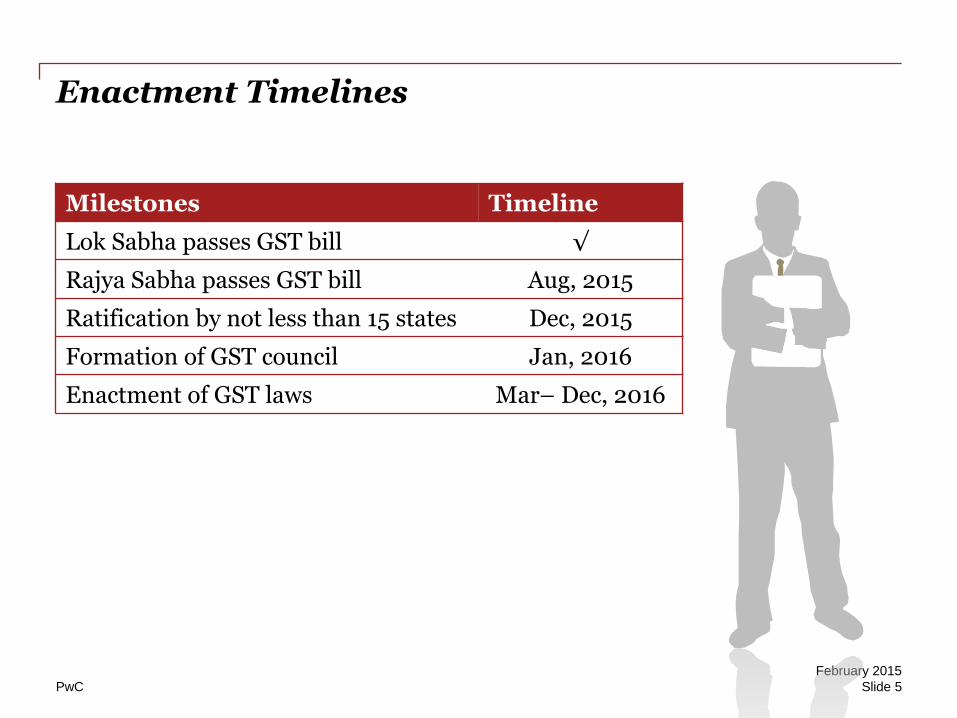

Enactment Timelines

Milestones Timeline

Lok Sabha passes GST bill √

Rajya Sabha passes GST bill Aug, 2015

Ratification by not less than 15 states Dec, 2015

Formation of GST council Jan, 2016

Enactment of GST laws Mar– Dec, 2016

February 2015

Slide 5

PwC

Content

Section 1 Enactment Timelines

Section 2 GSTN Processes

Section 3 Rate Debate

Section 4 Place of supply rules and credit

Section 4 Transition provisions

Slide 6

March 2015

`

PwC

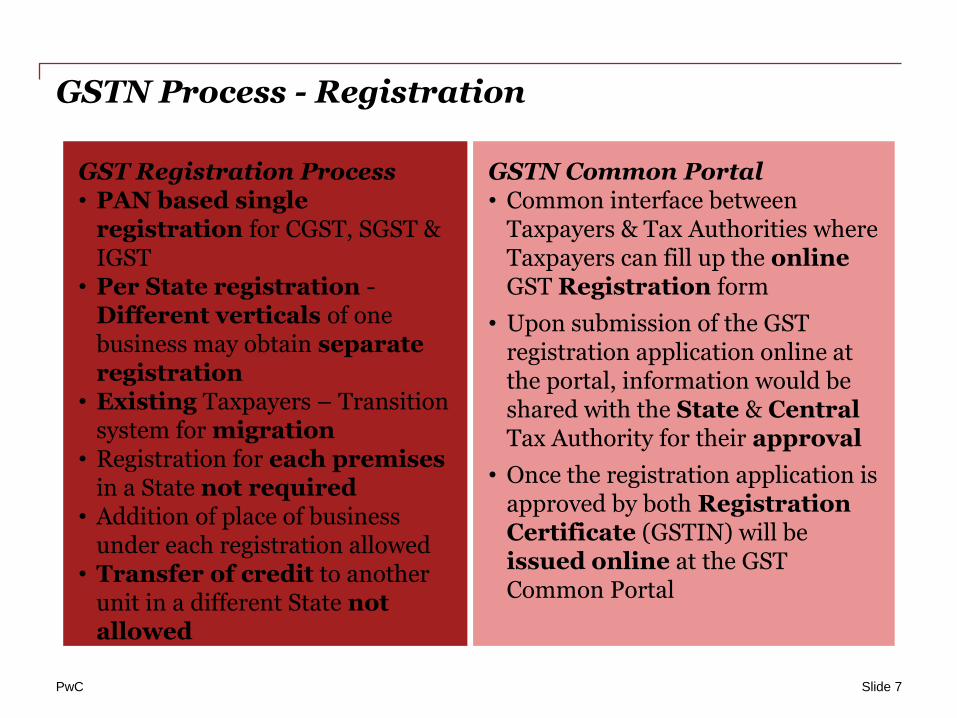

GSTN Process - Registration

Slide 7

GSTN Common Portal • Common interface between

Taxpayers & Tax Authorities where Taxpayers can fill up the online GST Registration form

• Upon submission of the GST registration application online at the portal, information would be shared with the State & Central Tax Authority for their approval

• Once the registration application is approved by both Registration Certificate (GSTIN) will be issued online at the GST Common Portal

GST Registration Process • PAN based single

registration for CGST, SGST & IGST

• Per State registration - Different verticals of one business may obtain separate registration

• Existing Taxpayers – Transition system for migration

• Registration for each premises in a State not required

• Addition of place of business under each registration allowed

• Transfer of credit to another unit in a different State not allowed

PwC

GSTN Process - Returns

Slide 8

GSTN Common Portal • Interface for GST registered

taxpayers to upload their invoice level sales details by a specified cut-off date

• Based on the sales details uploaded by the supplier, GSTN Common Portal would auto-draft the purchase statement of the counterparty purchaser on a near real time basis

• Draft return of a taxpayer to be generated at the Common Portal after sales-purchase details are captured

GST Returns Process • Unified return form for all

States/ One Return for CGST, SGST & IGST

• All returns to be electronic • Return expected to be Monthly

(Quarterly for compounding dealers)/ Annual

• All details of sale (invoice wise) to be submitted, purchase details to be populated from sales of counterparty dealers

• State specific return as State unit is an independent unit

• IGST assessment by State where return is filed

PwC

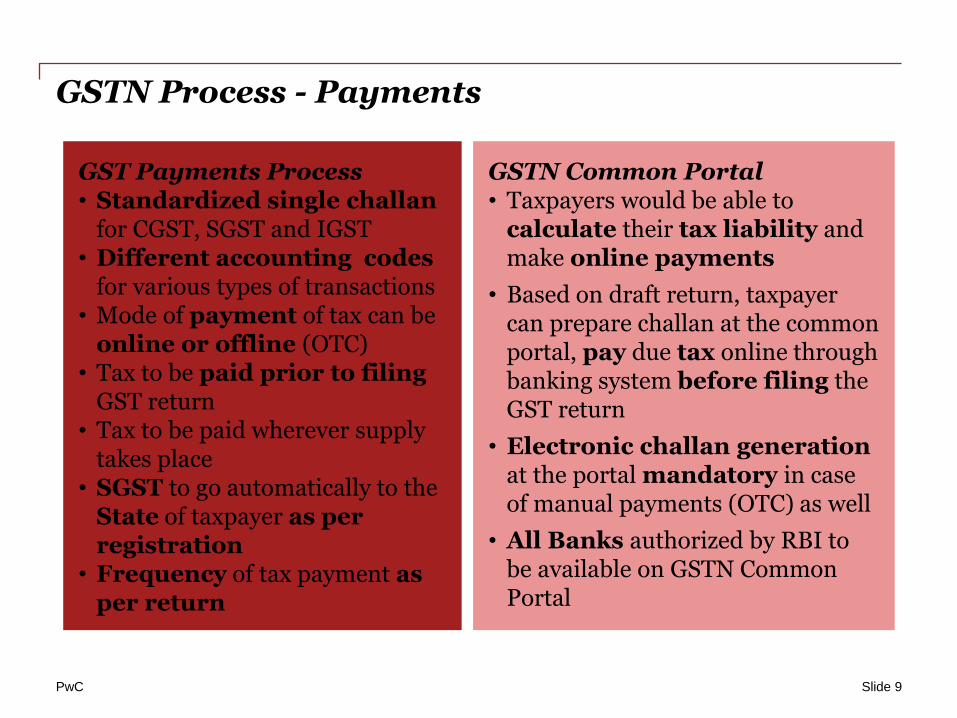

GSTN Process - Payments

Slide 9

GSTN Common Portal • Taxpayers would be able to

calculate their tax liability and make online payments

• Based on draft return, taxpayer can prepare challan at the common portal, pay due tax online through banking system before filing the GST return

• Electronic challan generation at the portal mandatory in case of manual payments (OTC) as well

• All Banks authorized by RBI to be available on GSTN Common Portal

GST Payments Process • Standardized single challan

for CGST, SGST and IGST • Different accounting codes

for various types of transactions • Mode of payment of tax can be

online or offline (OTC) • Tax to be paid prior to filing

GST return • Tax to be paid wherever supply

takes place • SGST to go automatically to the

State of taxpayer as per registration

• Frequency of tax payment as per return

PwC

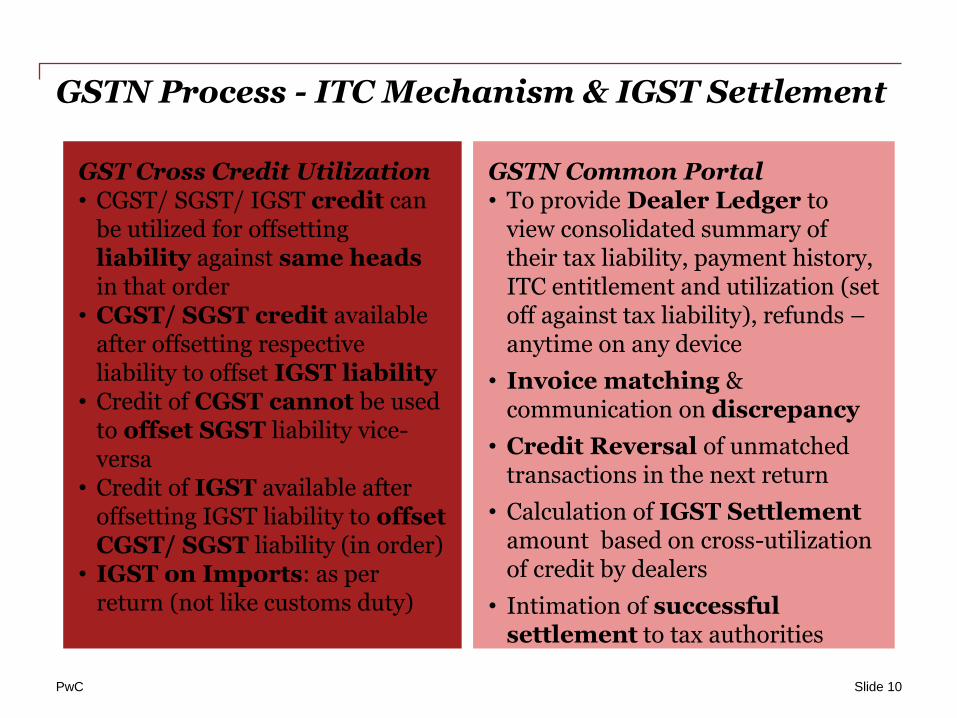

GSTN Process - ITC Mechanism & IGST Settlement

Slide 10

GSTN Common Portal • To provide Dealer Ledger to

view consolidated summary of their tax liability, payment history, ITC entitlement and utilization (set off against tax liability), refunds – anytime on any device

• Invoice matching & communication on discrepancy

• Credit Reversal of unmatched transactions in the next return

• Calculation of IGST Settlement amount based on cross-utilization of credit by dealers

• Intimation of successful settlement to tax authorities

GST Cross Credit Utilization • CGST/ SGST/ IGST credit can

be utilized for offsetting liability against same heads in that order

• CGST/ SGST credit available after offsetting respective liability to offset IGST liability

• Credit of CGST cannot be used to offset SGST liability vice-versa

• Credit of IGST available after offsetting IGST liability to offset CGST/ SGST liability (in order)

• IGST on Imports: as per return (not like customs duty)

PwC

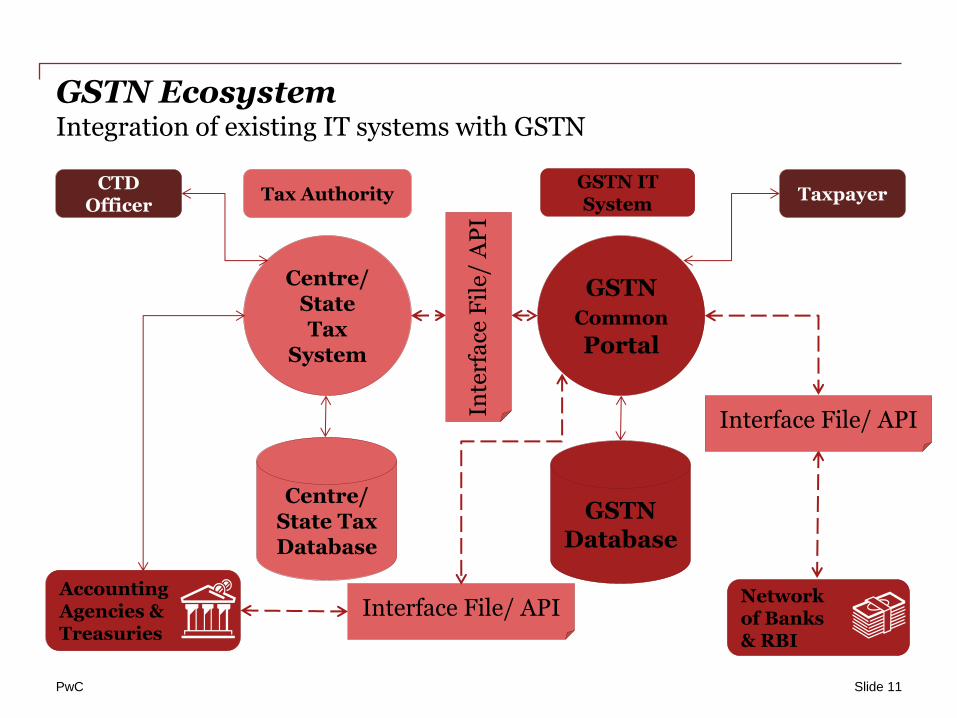

GSTN Ecosystem Integration of existing IT systems with GSTN

Slide 11

Taxpayer GSTN IT System

Tax Authority CTD

Officer

GSTN Common Portal

GSTN Database

Network of Banks & RBI

Accounting Agencies & Treasuries

Centre/ State Tax

System

Centre/ State Tax Database

Interface File/ API

Inte

rfa

ce F

ile

/ A

PI

Interface File/ API

PwC

Content

Slide 12

March 2015

`

Section 1 Enactment Timelines

Section 2 GSTN Processes

Section 3 Rate debate

Section 4 Place of supply rules and credit

Section 5 Transition provisions

PwC

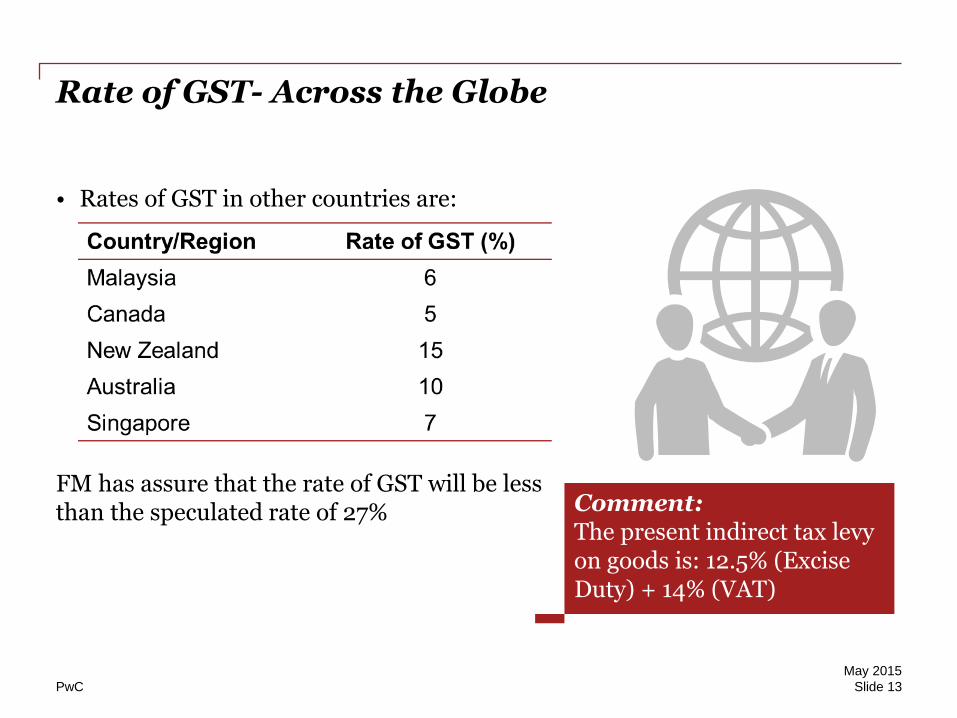

Rate of GST- Across the Globe

• Rates of GST in other countries are:

FM has assure that the rate of GST will be less than the speculated rate of 27%

May 2015

Slide 13

Comment: The present indirect tax levy on goods is: 12.5% (Excise Duty) + 14% (VAT)

PwC

Rate of GST – Concessions/incentives

What would happen to current incentives:

• State incentives:

- Area based exemptions

- VAT deferment schemes

• Central incentives:

- Product specific concessions

- Area based incentives

May 2015

Slide 14

PwC

Content

Section 1 Enactment Timelines

Section 2 GSTN Processes

Section 3 Rate debate

Section 4 Place of supply rules and credit

Section 5 Transition provisions

Slide 15

March 2015

`

PwC

Distribution of accumulated credit at corporate office?

• Head office would incur standard costs and accumulate input credit

• HO might have Nil or marginal output tax liability

Credit utilization dependent on seller declaration?

• Auto-drafting of purchase statement of a dealer from the invoice based sales details uploaded by the counterparty dealers

Credit on Businesses’ indirect spends by employees?

Place of supply rules and credit

May 2015

Slide 16

PwC

Content

Section 1 Enactment Timelines

Section 2 Rate debate

Section 3 Place of supply rules and credit

Section 4 Transition provisions

Slide 17

March 2015

`

PwC

Transition provisions

• Refund, not credit – Accumulated credit at the cut off date cannot be carried forward

- Input and input services - CENAVT

- Capital goods – CENVAT and VAT

- VAT credit

• Defer capital expenditure/purchases

• Treatment of Way-Bill/ C-Form/ Checkposts

• Treatment of Existing Area based Exemptions/ Benefits under State Industrial Policy

• Dual Assessment for the Taxpayer?

May 2015

Slide 18

Thank You

© 2015 PricewaterhouseCoopers Private Ltd. All rights reserved. “PwC”, a registered

trademark, refers to PricewaterhouseCoopers Private Limited (a limited company in India) or,

as the context requires, other member firms of PwC International Limited, each of which is a

separate and independent legal entity.

Panel Discussion: GST Regime:

Are we ready?

Dr J N Singh

Additional Chief Secretary, Finance Dept., with

additional charge of post of Revenue Dept.,

Commissioner of Land Reforms in Gujarat

Shashank Priya,

Commissioner, CBEC

Dr H P Kumar,

Chairman-cum-Managing Director,

National Small Industries

Corporation

Vimal Goel

EVP, GSTN

Arun Subramanian

VP, Globalization Services, SAP Labs India