Embed Size (px)

Citation preview

SCHOOL DISTRICTOF

BETHLEHEM TOWNSHIP

BOARD OF EDUCATION

COUNTY OF HUNTERDONASBURY, NEW JERSEY

COMPREHENSIVE ANNUAL FINANCIAL REPORTFOR THE FISCAL YEARENDED JUNE 30, 2014

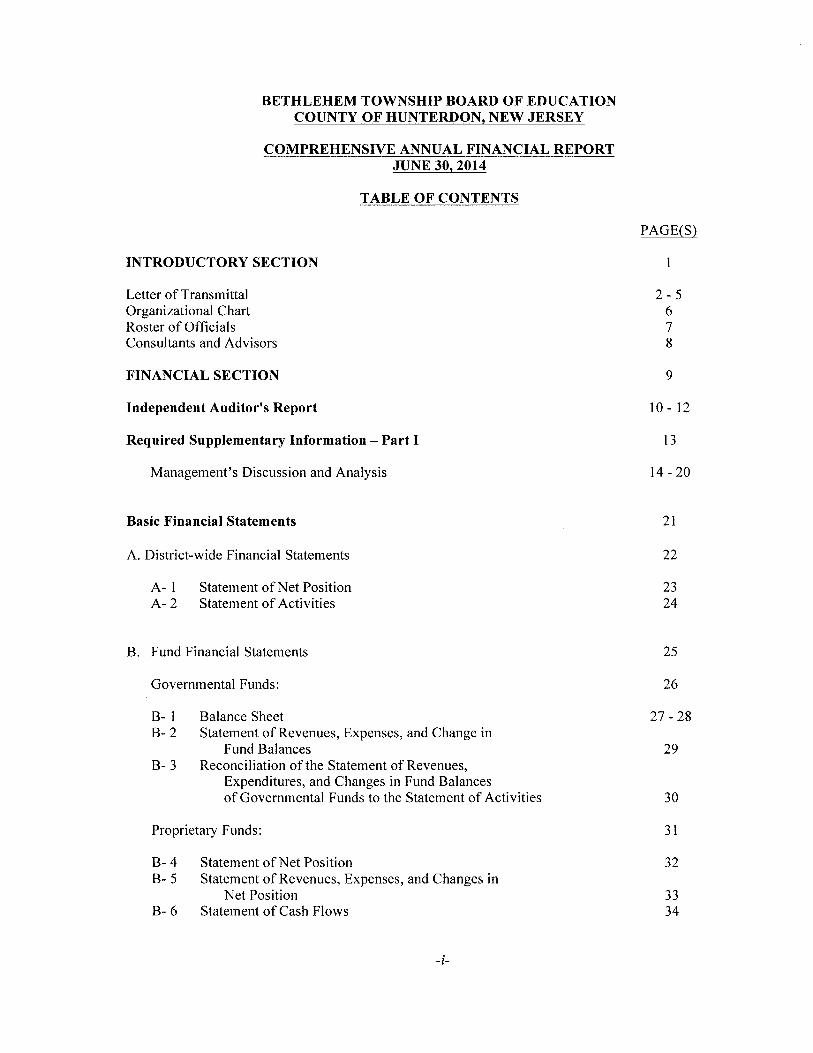

BETHLEHEM TOWNSHIP BOARD OF EDUCATIONCOUNTY OF HUNTERDON, NEW JERSEY

COMPREHENSIVE ANNUAL FINANCIAL REPORTJUNE 30, 2014

TABLE OF CONTENTS

INTRODUCTORY SECTION

Letter of TransmittalOrganizational ChartRoster of OfficialsConsultants and Advisors

FINANCIAL SECTION

Independent Auditor's Report

Required Supplementary Information - Part I

Management's Discussion and Analysis

Basic Financial Statements

A. District-wide Financial Statements

A- 1 Statement of Net PositionA- 2 Statement of Activities

B. Fund Financial Statements

Governmental Funds:

B- 1 Balance SheetB- 2 Statement of Revenues, Expenses, and Change in

Fund BalancesB- 3 Reconciliation of the Statement of Revenues,

Expenditures, and Changes in Fund Balancesof Governmental Funds to the Statement of Activities

Proprietary Funds:

B- 4 Statement of Net PositionB- 5 Statement of Revenues, Expenses, and Changes in

Net PositionB- 6 Statement of Cash Flows

-i-

PAGE(S)

2-5678

9

10 - 12

13

14 - 20

21

22

2324

25

26

27 - 28

29

30

31

32

3334

Fiduciary Funds:

B- 7 Statement of Fiduciary Net PositionB- 8 Statement of Changes in Fiduciary Net Position

Notes to the Financial Statements

Required Supplementary Information - Part II

C. Budgetary Comparison Schedules

C- 1C- la

Budgetary Comparison Schedule - General FundCombining Schedule of Revenues, Expenditures, and

Changes in Fund Balance - Budget and ActualAmerican Recovery and Reinvestment Act - Budget and ActualBudgetary Comparison Schedule - Special Revenue Fund

C-lbC-2

Notes to the Required Supplementary Information

C- 3 Budgetary Comparison Schedule - Note to RSI

Other Supplementary Information

D. School Level Schedules:

0- 10-2

Combining Balance SheetBlended Resource Fund - Schedule of Expenditures

Allocated by Resource Type - ActualBlended Resource Fund - Schedule of Blended ExpendituresSchedule of DEOA Expenditures - Budget and Actual

0-30-4

E. Special Revenue Fund:

E- 1 Combining Schedule of Revenues and ExpendituresSpecial Revenue Fund - Budgetary Basis

E- 2 Demonstrably Effective Program Aid Schedule of Expenditures- Budgetary Basis

E- 3 Early Childhood Program Aid Schedule of Expenditures- Budgetary Basis

E- 4 Distance Learning Network Aid Schedule ofExpenditures - Budgetary Basis

E- 5 Instructional Supplement Aid Schedule of Expenditures- Budgetary Basis

F. Capital Projects Fund:

F- 1 Summary Statement of Project ExpendituresF- 2 Summary Schedule of Revenues, Expenditures, and Change

in Fund Balance - Budgetary BasisF- 2a Summary Schedule of Revenues, Expenditures, and Change

in Fund Balance - Budgetary Basis-ii-

PAGE(S)

35

3637

38 - 58

59

60

61 - 69

N/AN/A70

71

72

73

74

N/A

N/AN/AN/A

75

76

N/A

N/A

N/A

N/A

77

N/A

N/A

N/A

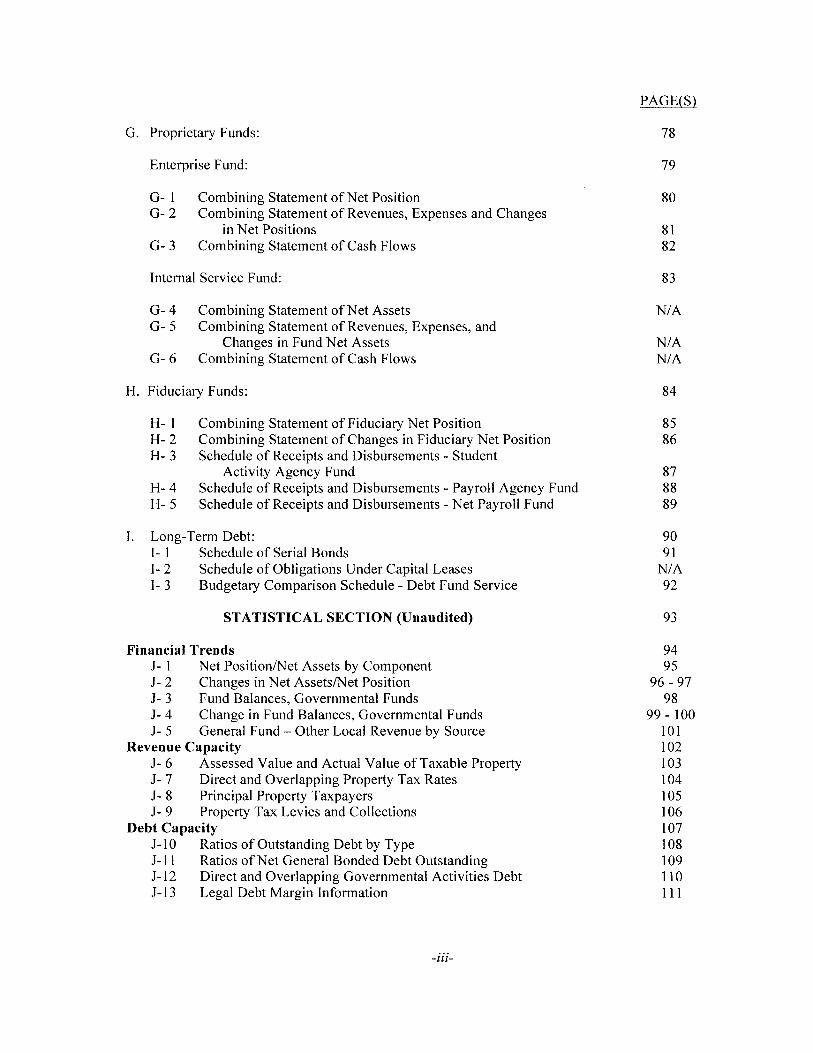

G. Proprietary Funds:

Enterprise Fund:

G- 1G-2

Combining Statement of Net PositionCombining Statement of Revenues, Expenses and Changes

in Net PositionsCombining Statement of Cash FlowsG-3

Internal Service Fund:

G-4G-5

Combining Statement of Net AssetsCombining Statement of Revenues, Expenses, and

Changes in Fund Net AssetsCombining Statement of Cash FlowsG-6

H. Fiduciary Funds:

H- 1H-2H-3

Combining Statement of Fiduciary Net PositionCombining Statement of Changes in Fiduciary Net PositionSchedule of Receipts and Disbursements - Student

Activity Agency FundSchedule of Receipts and Disbursements - Payroll Agency FundSchedule of Receipts and Disbursements - Net Payroll Fund

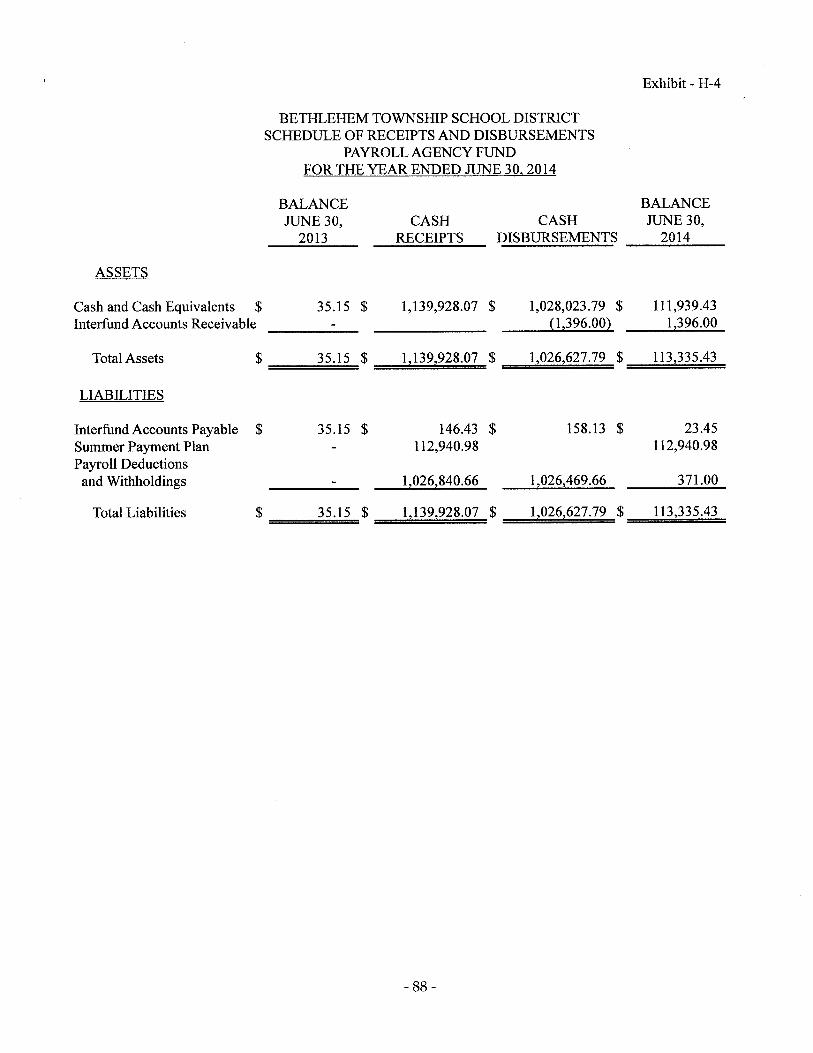

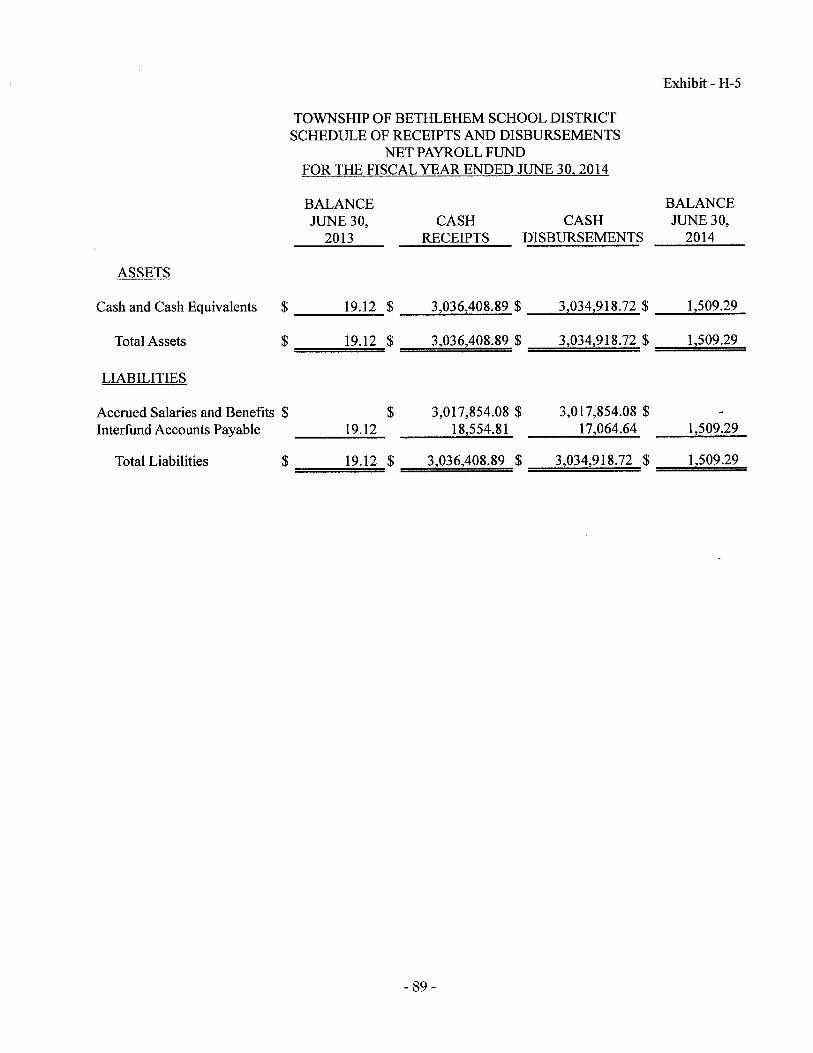

H-4H-5

I. Long-Term Debt:J- 1 Schedule of Serial Bonds1- 2 Schedule of Obligations Under Capital Leases1- 3 Budgetary Comparison Schedule - Debt Fund Service

STATISTICAL SECTION (Unaudited)

Financial TrendsJ- 1 Net PositionlNet Assets by ComponentJ- 2 Changes in Net AssetslNet PositionJ- 3 Fund Balances, Governmental FundsJ- 4 Change in Fund Balances, Governmental FundsJ- 5 General Fund - Other Local Revenue by Source

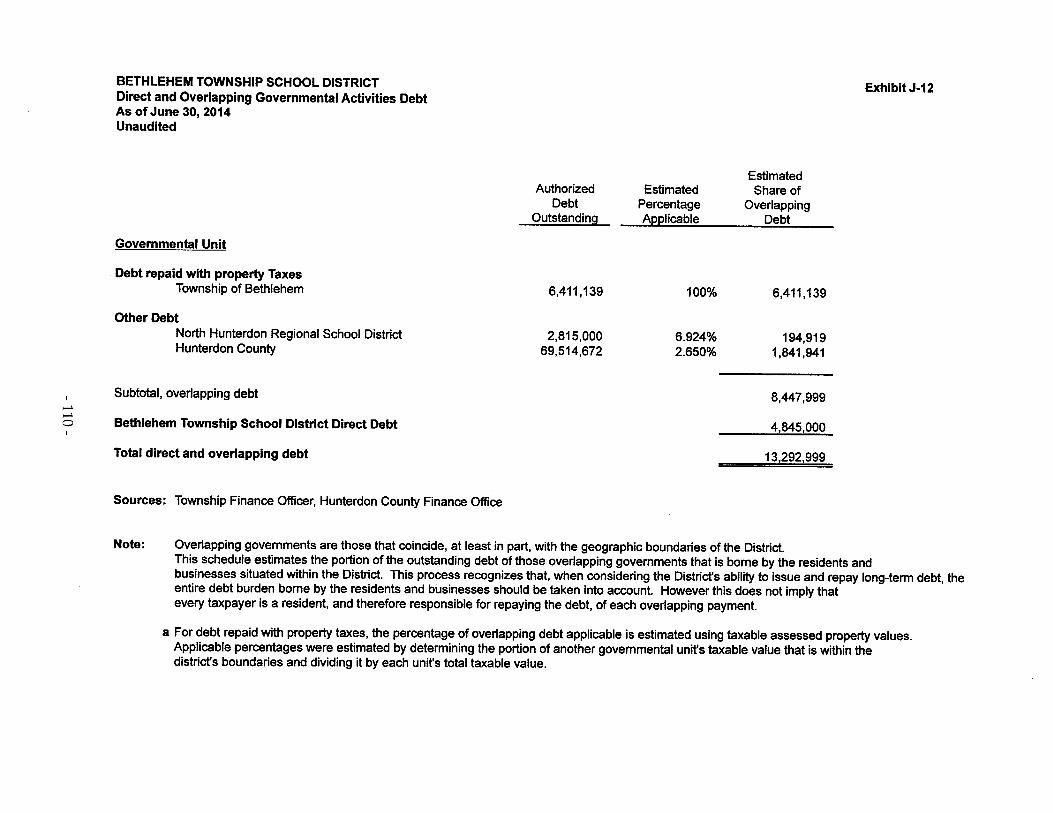

Revenue CapacityJ- 6 Assessed Value and Actual Value of Taxable PropertyJ- 7 Direct and Overlapping Property Tax RatesJ- 8 Principal Property TaxpayersJ- 9 Property Tax Levies and Collections

Debt CapacityJ-10 Ratios of Outstanding Debt by TypeJ-ll Ratios of Net General Bonded Debt OutstandingJ-12 Direct and Overlapping Governmental Activities DebtJ-13 Legal Debt Margin Information

-iii-

PAGE(S)

78

79

80

8182

83

N/A

N/AN/A

84

8586

878889

9091N/A92

93

9495

96 - 9798

99 - 100101102103104105106107108109110111

PAGE(S)

STATISTICAL SECTION (Unaudited) (Cont'd)

Demographic and Economic InformationJ-14 Demographic and Economic StatisticsJ-15 Principal Employers

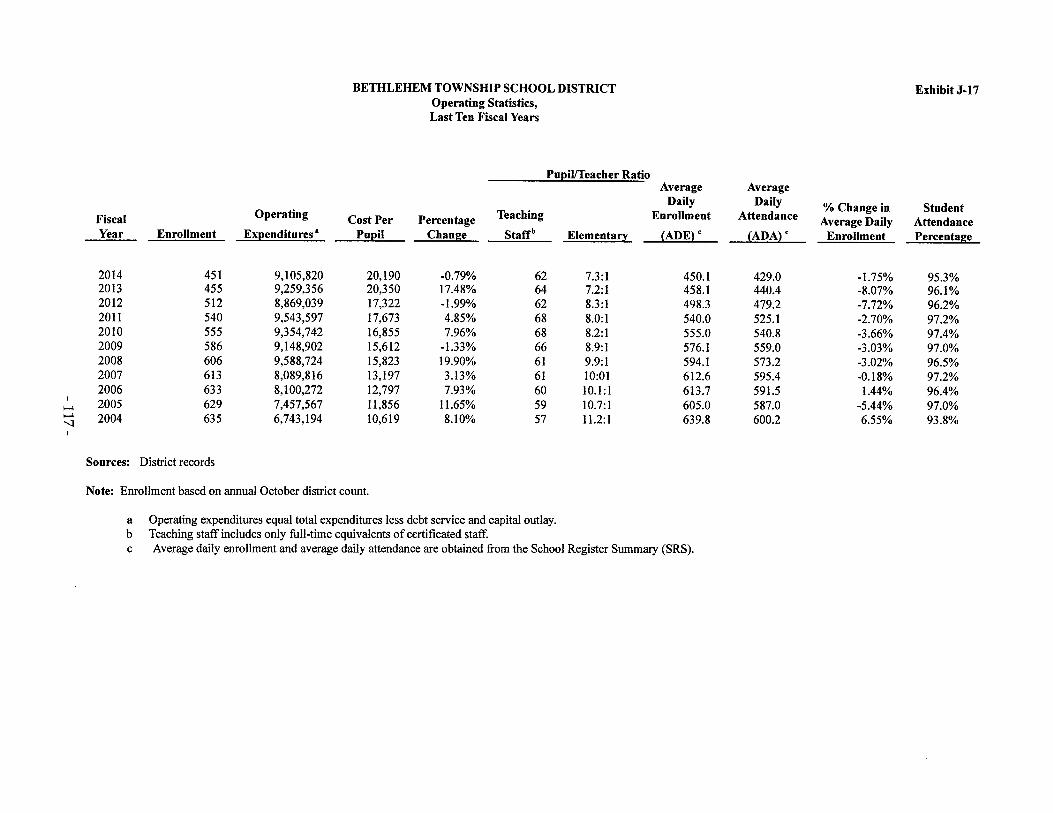

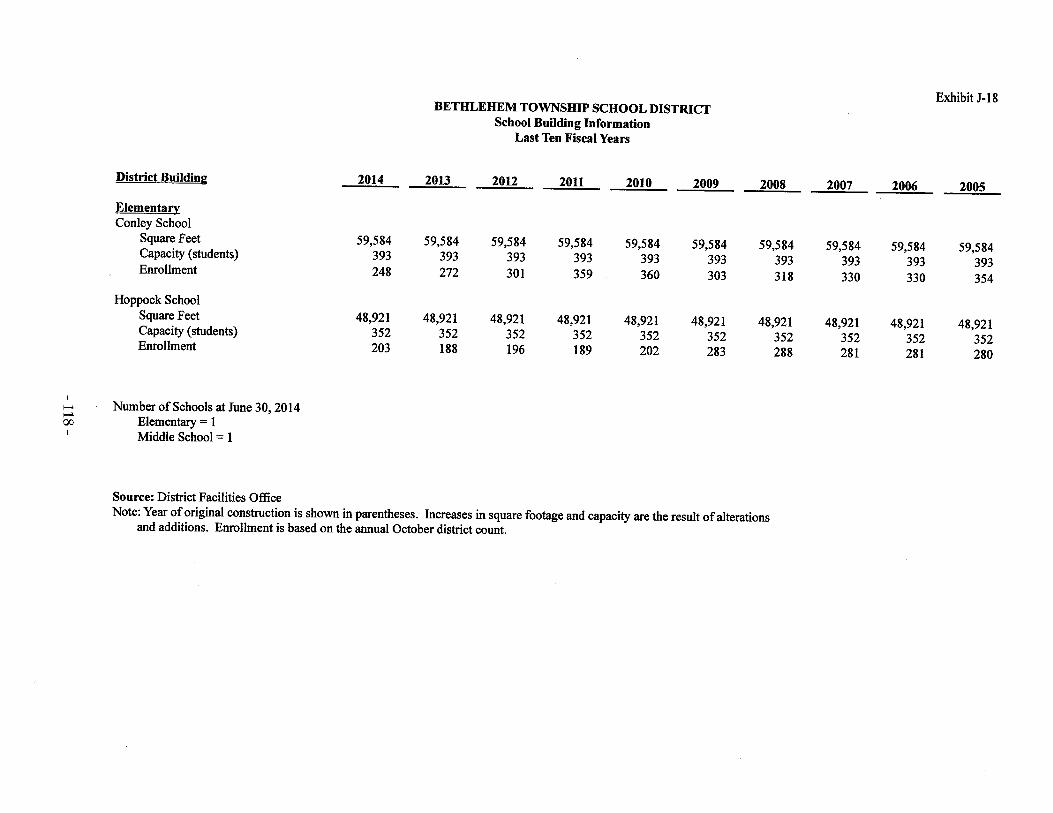

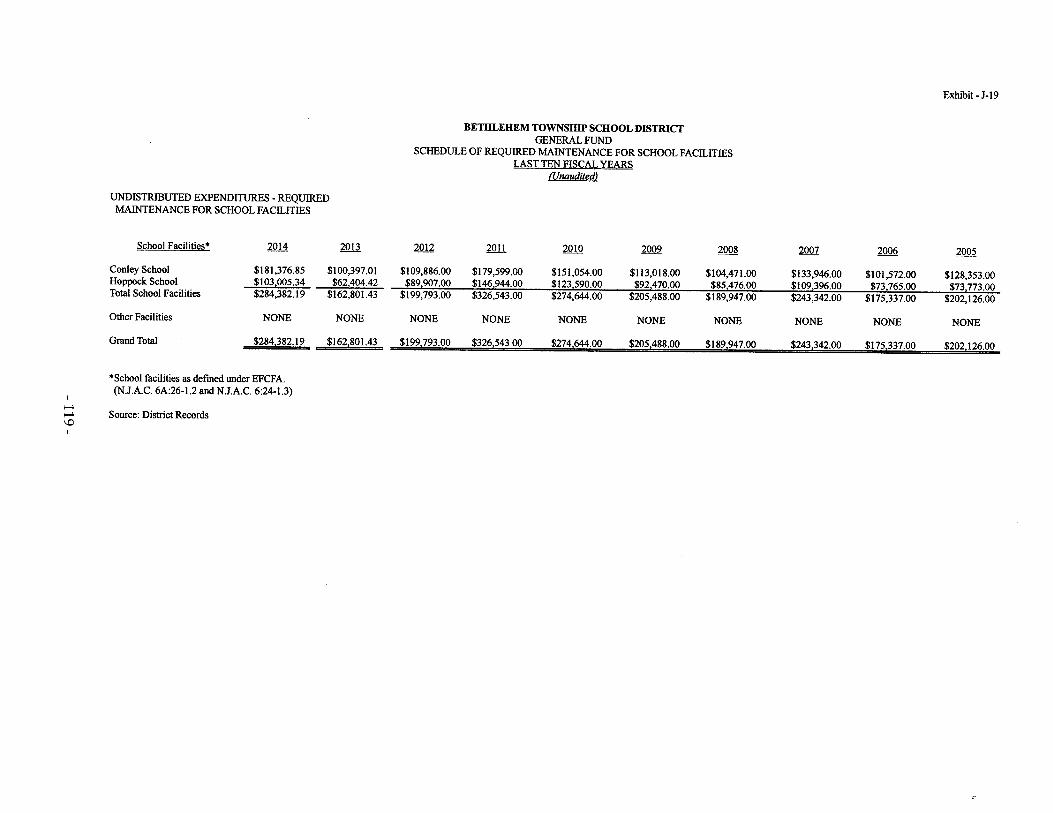

Operating InformationJ-16 Full-time Equivalent District Employees by Function/ProgramJ-17 Operating StatisticsJ-18 School Building InformationJ-19 Schedule of Required MaintenanceJ-20 Insurance Schedule

112113114115116117118119120

SINGLE AUDIT SECTION 121

K- 1 Report Internal Control Over Financial Reporting and onCompliance and Other Matters Based on an Audit ofFinancial Statements Performed in Accordance WithGovernment Auditing Standards 122 - 123

K-2 Report on Compliance for Each Major State Program; Reporton Internal Control Over Compliance; and Report onthe Schedule of Expenditures of State Financial AssistanceRequired by New Jersey OMB Circular 04-04 124 - 125

K - 3 Schedule of Expenditures of Federal Awards, Schedule A N/A

K- 4 Schedule of Expenditures of State Financial Assistance,Schedule B 126

K- 5 Notes to the Schedules of Awards and Financial Assistance 127 - 128

K-6 Schedule of Findings and Questioned Costs 129 - 130

K -7 Summary Schedule of Prior Audit Findings 131

-iv-

INTRODUCTORY SECTION

-1-

Bethlehem Township Sehool DistrictThomas.B. Conley School Ethe1Hoppock Middle School940 Iron Sridge Road 280 A~bllfylWest Portal RoadAsbury, New Jersey 08802 Asbury, New Jersey 08802Phone: (908) 537-4044 Phone: (9Q8) 419~.6336Fax: (90S) 537.:4309 Fax: (908) 419-1021

Edward Keegan. Ed.D.Chief Sphool Administrator/Principal

Jane Smith. PtincipalEthel HoppockMiddk School

.Edward D. KentBusiness AdlllinistratorlBoard Secretary

S;:Illy KleO) 111Supervisor of Special Services

November 24, 2014

Honorable President andMembers of the Board of EducationBethlehem Township School District940 11'011 Bridge RoadAsbtlry, NJ 08802

Dear Members of'the Board of Education:

The Comprehensive Annual Financial Report (C .A..F,R.}of the ToWl1ship ofBethlehell1 PUblic School District forthe fiscal yeaI' ended June 30, 2014, is hereby submitted. Responsibility for both the accuracy of the data andcompleteness and fainless of the presentation, including all disclosures, rests with the management of the Board ofEducation. To the best of our knowledge and belief, the d&ta presented in the auditor's .repot1:are accurate in allmaterial respects and are reported in a. manner designed to fairly present the financial position and results ofoperations of the various funds and accQ\ll~tgroups of the District. All disclosures necessary to enable the reader togain all.understanding of the District's financial.activities.have.been included.

The C.A.F.R. is presented in four sections: Introductory, finaIlcial. s~tistical. and single au.dit. The introductorysection jllcludes this transmittal letter. the District's organizational chart, and. a list of principal officials. Thefinancial section includes the gl:llleral-put:pose financial stat()ffienlS, management's discussion and analysis, andschedules, as well as the auditor's report thereon. The statistical section includes selected financial anddemographic infonnaticll}, generally presented on a multiyear basis. The District is required t.o undergo an annualsingle audit in conformity with the provisions of the 1996.Single AUQitAct and the.U.S. Off1.ce of Management andBudget Circular A~ 133, Apdits ofSta!e and Local..Govemments, and New Jersey OMB's Circular 04~04, "SingleAudit .Folicy for Recipients of Federal Grants, State Gr~nts, and State Aid." Informati.on related to this single audit,including the auditor's report on the internal control structure and compliance with applicable law!?and regulations,and findings and recommendations, i$ included ill tbe single alJdits¢ctiol1 of this report.

L REPORTING ENTITY AND ITS SERVICES:The Township of Bethlehem Public School District is an independent reporting entity within the criteria adopted byG.A.S.B .. [Governmental Accounting Standards Board) established by Statement No. 14. All funds and accountgroups of the District are included in this repor], The Township of Bethlehem Board of Education and all itsschools constitute the District's reporting/entity.

The Districtprovides a full range of'edueational services appropriate to grade levels K through 8.

-2-

These services incluqe gcnentI.as. well as special education (grades K through 8) programs. The District completedthe 2012-2013 fiscal year witll, an in district em-oUment of 460 $tu(ll':mts,which is 52 (-10.1 %) students less theprevious year's enrollment. The following details the changes in the student enrollment of the District over a tell-year period. These figures do 110t include those students sent eM of district tor special education placements.

Average Daily Enrcllmen]

FiscalYearStudent

EnrollmentPercentChange

2013-20142012,,20132011~201220.10-20112009~20102008-20092007-20082006-20072005-20062004~2005

451460512540555586606613633629

-2.0-10.1-5.2~2;7- 5.3~4.5-1.1-3.2+0.1- 0.1

2. ECONOMIC CONDITION AND OUTLOOK:

As noted above, the District has-had a decliningenrollment; The entollment decHne in out district is Consistellt Withthe ov¢rall decline in Hunterdon County. As a result. we have tried to attract more students through School Choiceas well as implemeutation pf a full day ki,ndergarten program, This y¢a).', w¢ enrolled five School Choice studentsand, unfortunately, the NJDOE has capped our Choice enrollment at four students for the 2015-16 school year. Wehav!;: had to place at least 10 students 011 our Waitingljst.

3. MAJOR INITIATIVES:

Our most important initiative this year and in. the foreseeable future is our 1:1 IP<id progl(lm. This year, gradesthree through eight received !Pads from the District and are using them during the school day. Students in gradessix through eight may also use their Il'ads at home.

4. INTERNAL ACCOUNTING CONTROLS:Management of the District is responsible for e~tablishing and l'uaintaihing an internal control structure designed toellSI.U·cthat the assets .o£the District are protected from loss, theft, or misuse and to ensure that adequatel:\cc(luntingdata are compiled to a119w for tlw· preparatiQn of fmancial statem¢u.ts in conformity with Generally AcceptedAccounting Principles (G.A.A.P.). An internal control structure is design¢<i to provide reasonable, put not absolute,assurance that these objectives lire met. The concept of reas.onable assurance recognizes that: (1) the cost of acontrol should not exceed the benefit$ likely to be derived; and (2) the valuation of c6s(:'<;and benefits requiresestimates and judgments by management.

As a recipient of federal and state Il11ancial.assistance; the District also is responslble forensuring that an adequateinternal control. structure is in place to ensure compliance with applicable laws and regnlatiQllS related to thoseprograms. This Int~rh&l control structure is also subjectto pei'iodic evaluation by the Districtananagement,

As part of the District single audit described earlier, tests are made to determine the adequacy of the intenml controlstructure, including that portion related to federal and state financial assistance programs, as well as to determinethat the District has complied with applicable laws and regulations.

- 3-

5. BUDGETARY CONTROLS:In addition to internal accounting controls, the District m",i:ntnins budgetary controls .. The objective of thesebudgetary controls is to ensure compliance with legal provisions embodied in the annual appropriated budgetapproved by the. voters of the municipality. Annual appropriated budgets are adopted for the general fUi1{l, thespecial revenue fund, and the debt service fund. Proj¢ct length budgets are. approved for the capital improvementsaccounted for in the capital projects fund. The final budget amount as amended for the fiscal Year is reflected in thefinancial Section. .

An encumbrance a¢90unting system is used to record Qutstanding purchase commitments on a line item basis. Openencumbrances at year-end are t':ither cancelled or aze included as a re-appropriation of fund balances in thesUbsequent year. Those amounts to be 're-appropriated are reported as reservations of fu:n.d balance at Ju:n.e 30,2014.

6. ACCOUNTING SYSTEM AND REPORTS:A District's accounting records must reflect generally accepted principles, as promulgated by the GovernmentalAccounting Standards. Board (G.A.S.B.). The accounjil1g syst~m of the District is organized on the basis cf fundsand account groups. These fimds and account grQUps are explained in "Notes to the Financial Statements,'; Note 1.

Ail effective and efficient system of internal controls is essential to accurate, timely reporting of all relevanttransactions on an accounting system and the r¢Sultant administrative and external reports generated from thatsystem.

7. FINANCIAL INFORMATION AT FISCAL YEAR-END:As demonstrated hy the various statements and schedules included in the financial section of this report, the.Districtcontinu¢S to meet its responsibiUties for sound financialll1l:)nagement. The following schedule presents a summaryof the general fund, special revenue fund, and debt service fund revenues for the fiscal year ended June 30, 2014,ami the amount and percentage of increas.e!(decrease) in relation to the prior year.

Revenue2013-2014Amount

Percentof

Total

Local SourcesState SourcesFederal Sources

7,356,7862,283,875219,169

74.6%23.2%2.2%

Totals

Increase(Decrease)From 2012-13

Percent ofIncrease(Decrease)

(122,331)(65,961)(23,244)

-16.36%-2.81%-9.59%

The following schedule presents a summary ·of the general fund, special revenue fund, and. debt service fundexpenditures for the fiscal year ended June.30, 2013, and the amount-and percentage of increase/ (decrease) inrelation to the prior year.

Expenditures2013-2014Amount

Percentof

Total

Current ExpenseCapital OutlaysSpecial RevenuesDebt Service

8,886,65188,385

219.169396,225

92.7%0.9%2.3%4.1%

Totals

Increase(Decrease)From 20 12~13

Percent OfIncrease(Decrease)

(121,692)(24,584)(31,.844)(2,50l)

-1.4%-21.8%~12.7%-0.6%

-4-

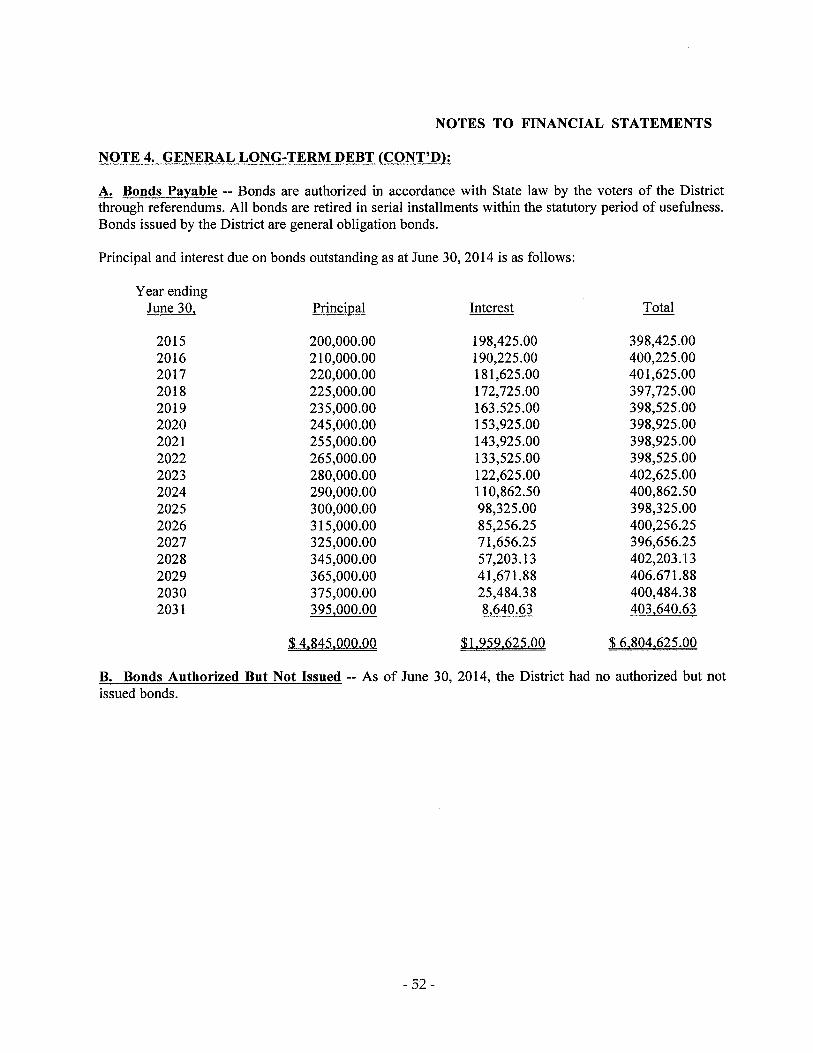

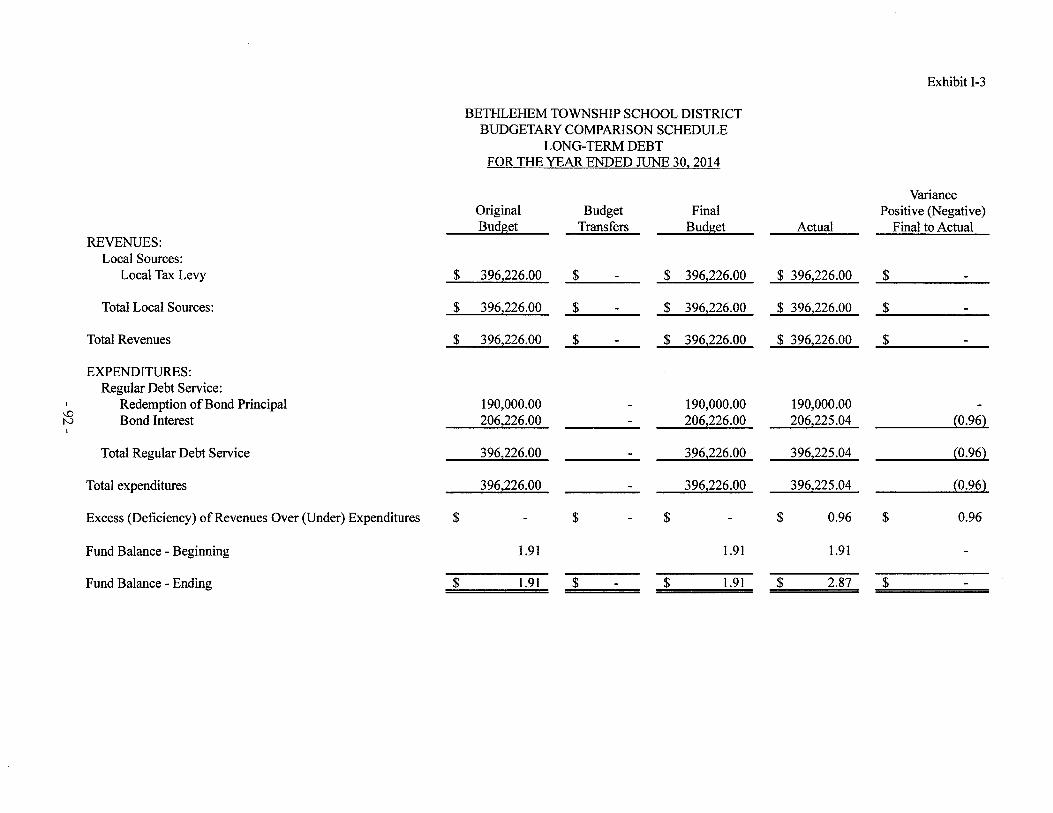

8. DEBT ADMINISTRATION:During the 2013-2014 school year, the District retired $190,000.00 of the principal balance all its 2005 Refun<1ingBonds. These bonds bear interest at.rates ranging from 4.0% t04.375% and mature in annual inslallmcntsthroughJuly 1, 2030. At June 30, 2014,. a principal balance of $4, 845,000.00 remalna outstanding. Manager)j~nt continuesto monitor marke; con<Jitlons to identity any additionalteful1ding opportullities.thatmay arise.

9, CASH MANAGEMENT:The investment policy of the Di&tricLis guided in large part by state statl.lte as detailed in "Notes. to the FinancialStatements," Note T. The District has adopted a cash management plan, which requires it to deposilpllJ:,lic funds inpUblic ..dePQsitories l?rotected frOln loss .under the provisions of {he Governmental Unit. Deposit Protection Act("GUDPA"). GUDPA was initially enacted in 1970 to protect Gove111mcntal unitsJrom a loss of funds .on .depositwith a failed blinking institution in New Jersey. The law requires governmental units to deposit public funds only inpublic dep9sitqdes· located in New Jersey where the fun4s ewe secured. in accordi:lllce. with the .Act, 2009(lluendments to the Act established a sliding collateralization scale for public depositOt1eS acc(,lptillg gov¢flUJ:)ent!:11deposits that is based upon the capitaliZation level ofthe depository.

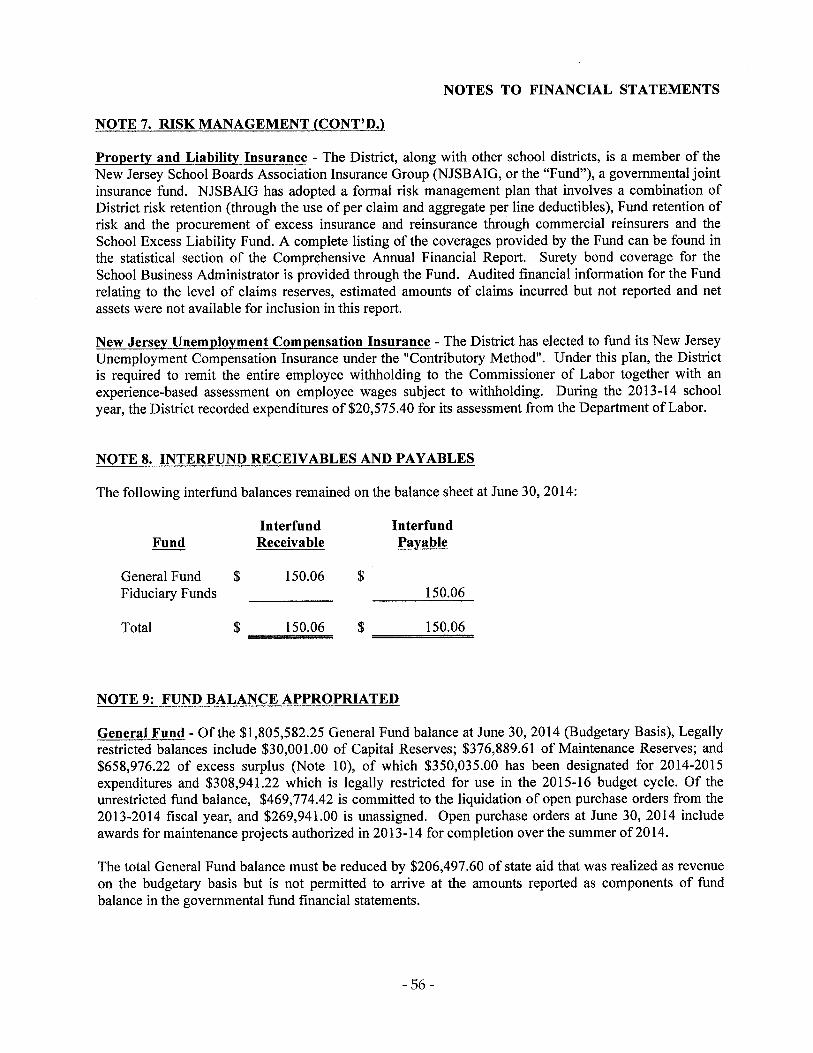

10. RISK MANAGEMENT:The Board carries various forms of insurance, including but not limited to, general liability and comprehensivecollision, hazard and theft insurance on property and contents, and fidelity bonds. Exhibit J-20 provides a sutntnaryofthe coverlige ll!l10unts and dednctibles.

11. OTHER INFORMATION:State statutes require till annual audit by independent certified public accountants. or registered municipalaccountant'). The-accounting firm ofHoduHk&Morrison,.P.A. was selected by the Board ofEducafion. In additionto meeting the reqllirel11ents set forth in state statutes, the audit also was designed to meet the requirements of theSingle Audit-Act and the related OMB Circular A-133 and New .Jersey OMB's Circular 04~04. the auditor's reporton the general-purpose financial statements and combining and individual fund statements and schedules is includedin the financial section of the report. 'Ihe auditor's reporta related specifically to the single audit ate included in thesingle audit section ofthis report.

12. ACKNOWLEDGEMENTS:We wQuldlike to express our appreciation to the members efthe Township of Bethlehem Board of Education fortaking initiative to pl'Ovide fiscal accountability to, the taxpayers ofthe Disttict and thereby contributing their fullsupporttQ the. development and maintenance of our financial operation. Further, the preparation of this report couldnot have been accomplished without the efficient anQ dc4icatt-'d services of our business office staff members,

CC&IJALf{w4Edward KentActing School Business AdministratorlBoard secretary

-5-

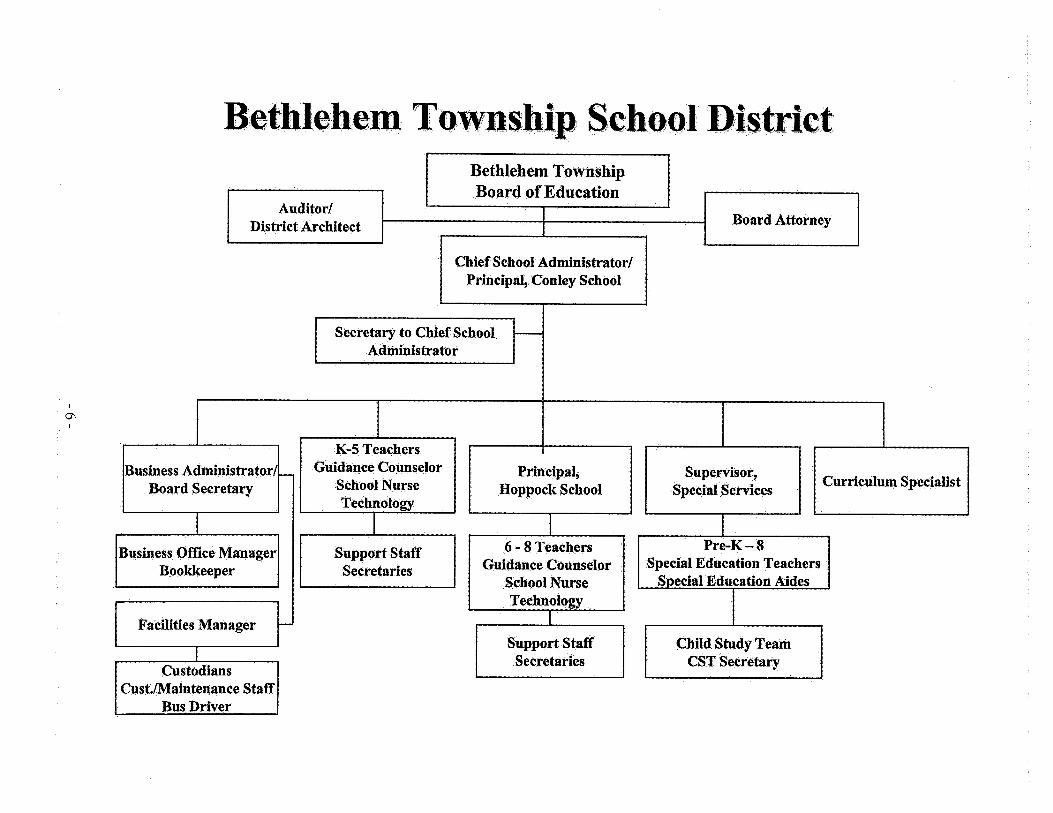

Bethlehem TownshipBoard ofEducation

Auditor!District Architect Board Attorney

Business AdministratOl"/1-jJoard Secretary

Business Office ManagerBookkeeper

Facilities Manager r-

JCustodians

CJlst./Maintcnance StaffBus Driver

Chief School Administra.tor!Principal,. Conley·School

Secretary to Chief School t--

Administrator

IK-5 Teachers

Guidance CounselorSchool NurseTechnology

ISupport StaffSecretaries

Principal,Hoppoek School

I6 - 8.Teachers

Guidallce CounselorSchool NUrse'Techllology

ISupPort StaffSecretaries

SUPervisor,Special Services Curriculum Specialist

Pre-K ....8Special Education TeachersSneclal Education Aides

IChild Study TeamCST Secretary

TOWNSHIP OF BETHLEHEM BOARD OF EDUCATIONHUNTERDON COUNTY, NEW JERSEY

ROSTER OF OFFICIALSJUNE 30,2014

Members of the Board of Education Term Expires

John Logars, PresidentGlenn Graham, Vice-PresidentJeffrey BlomkvistChristopher ConnersJennifer GlaserJennifer SeibertKimberly Solino

2014201620162015201420142014

Other Officials

Dr. Edward Keegan, Chief School AdministratorCarolyn B. Joseph, Interim Board Secretary/School Business AdministratorBrenda Liss, Esq., Board Attorney

-7-

TOWNSHIP OF BETHLEHEM SCHOOL DISTRICTConsultants and Advisors

Attorney

Brenda C. Liss, Esq.Riker Danzig Scherer Highland Perretti, LLC

One Speedwell AvenueHeadquarters Plaza

Morristown, NJ 07962

Audit Firm

Hodulik & Morrison. P.A.1102 Raritan Avenue

P.O. Box 1450Highland Park, NJ 08904

Bond Counsel

Anthony Pannella, Esq.Wi lentz, Goldman & Spitzer90 Woodbridge Center Drive

Woodbridge, NJ 07095

Official Depository

Investors Bank101 JFK Parkway

Short Hills, NJ 07078

- 8-

FINANCIAL SECTION

- 9-

HODULIK & MORRISON,P.A.CERTIFIED PUBLIC ACCOUNTANTS

REGISTERED MUNICIPAL ACCOUNTANTSPUBLIC SCHOOL ACCOUNTANTS

1102 RARITAN AVENUE,P.O.BOX 1450HIGHLAND PARK, NJ 08904

(732) 393-1000(732) 393-1196 (FAX)

ANDREW G. HODULIK, CPA, RMA, PSAROBERT S.MORRISON, CPA, RMA, PSA

MEMBERS OF:AMERICAN INSTITUTE OF CPA'SNEW JERSEY SOCIEIY OF CPA'S

REGISTERED MUNICIPAL ACCOUNTANTS OFNJ.10ANN BOOS, CPA. PSA

INDEPENDENT AUDITOR'S REPORT

Honorable President and Membersof the Board of Education

Bethlehem Township School DistrictCounty of Hunter don, New Jersey

REPORT ON FINANCIAL STATEMENTS

We have audited the accompanying fmancial statements of the governmental activities, thebusiness-type activities, each major fund and the aggregate remaining fund information of theBoard of Education of the Township of Bethlehem School District, in the County of Hunterdon,State of New Jersey, as of and for the fiscal year ended June 30, 2014, and the related notes to thefinancial statements, which collectively comprise the district's basic financial statements as listedin the table of contents.

MANAGEMENT'S RESPONSIBILITY FOR THE FINANCIAL STATEMENTS

Management is responsible for the preparation and fair presentation of these financial statementsin accordance with accounting principles generally accepted in the United States of America; thisincludes the design, implementation, and maintenance of internal control relevant to thepreparation and fair presentation of financial statements that are free from material misstatement.

AUDITOR'S RESPONSIBILITY

Our responsibility is to express opinions on these financial statements based on our audit. Weconducted our audit in accordance with auditing standards generally accepted in the United Statesof America; the standards applicable to financial audits contained in Government AuditingStandards, issued by the Comptroller General of the United States; and audit requirements asprescribed by the Division of Finance, Department of Education, State of New Jersey. Thosestandards require that we plan and perform the audit to obtain reasonable assurance about whetherthe financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts anddisclosures in the financial statements. The procedures selected depend on the auditor's judgment,including the assessment of the risks of material misstatement of the financial statements, whetherdue to fraud or error. In making these risk assessments, the auditor considers internal controlrelevant to the entity's preparation and fair presentation of the financial statements in order todesign audit procedures that are appropriate in the circumstances, but not for the purpose ofexpressing an opinion on the effectiveness of the entity's internal control. Accordingly, weexpress no such opinion. An audit also includes evaluating the appropriateness of accountingpolicies used and the reasonableness of significant accounting estimates made by management, aswell as evaluating the overall presentation of the fmancial statements.

-10 -

We believe that our audit evidence we have obtained is sufficient and appropriate to provide abasis for our audit opinions.

OPINIONS

In our opinion, the financial statements referred to above present fairly, in all material respects,the respective financial position of the governmental activities, business-type activities, eachmajor fund, and the aggregate remaining fund information of the Township of Bethlehem SchoolDistrict, in the County of Hunterdon, State of New Jersey, as ofJune 30, 2014 and the respectivechanges in financial position and cash flows, where applicable, for the year then ended III

conformity with accounting principles generally accepted in the United States of America.

OTHER MATTERS

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that themanagement's discussion and analysis and budgetary comparison information, as listed in thetable of contents, be presented to supplement the basic financial statements. Such information,although not a part of the basic financial statements, is required by the Governmental AccountingStandards Board, who considers it to be an essential part of financial reporting for placing thebasic financial statements in an appropriate operational, economic, or historical context. We haveapplied certain limited procedures to the required supplementary information in accordance withauditing standards generally accepted in the United States of America, which consisted ofinquiries of management about the methods of preparing the information and comparing theinformation for consistency with management's responses to our inquires, the basic financialstatements, and other knowledge we obtained during our audit of the basic financial statements.We do not express an opinion or provide any assurance on the information because the limitedprocedures do not provide us with sufficient evidence to express an opinion or provide anyassurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements thatcollectively comprise the Township of Bethlehem School District's basic financial statements as awhole. The accompanying other supplementary information, consisting of the combing andindividual fund financial statements, and long-term debt schedules, as listed in the table ofcontents, the schedule of state financial assistance, required by New Jersey OMB Circular 04-04,and the other information, including the introductory section and the statistical section arepresented for purpose of additional analysis and are not a required part of the financial statements.

The combing and individual fund financial statements, long-term debt schedules and the scheduleof state financial assistance are the responsibility of management and were derived from andrelate directly to the underlying accounting and other records used to prepare the basic financialstatements. Such information has been subjected to the auditing procedures applied in the audit ofthe financial statements and certain additional procedures, including comparing and reconcilingsuch information directly to the underlying accounting and other records used to prepare thefinancial statements or to the financial statements themselves, and other additional procedures inaccordance with auditing standards generally accepted in the United States of America. In ouropinion, the combing and individual fund financial statements, long-term debt schedules and theschedule of state financial assistance are fairly stated in all material respects in relation to thefinancial statements as a whole.

The introductory section and statistical section have not been subjected to the auditing proceduresapplied in the audit of the basic financial statements and, accordingly, we do not express anopinion or provide any assurance on them.

-11-

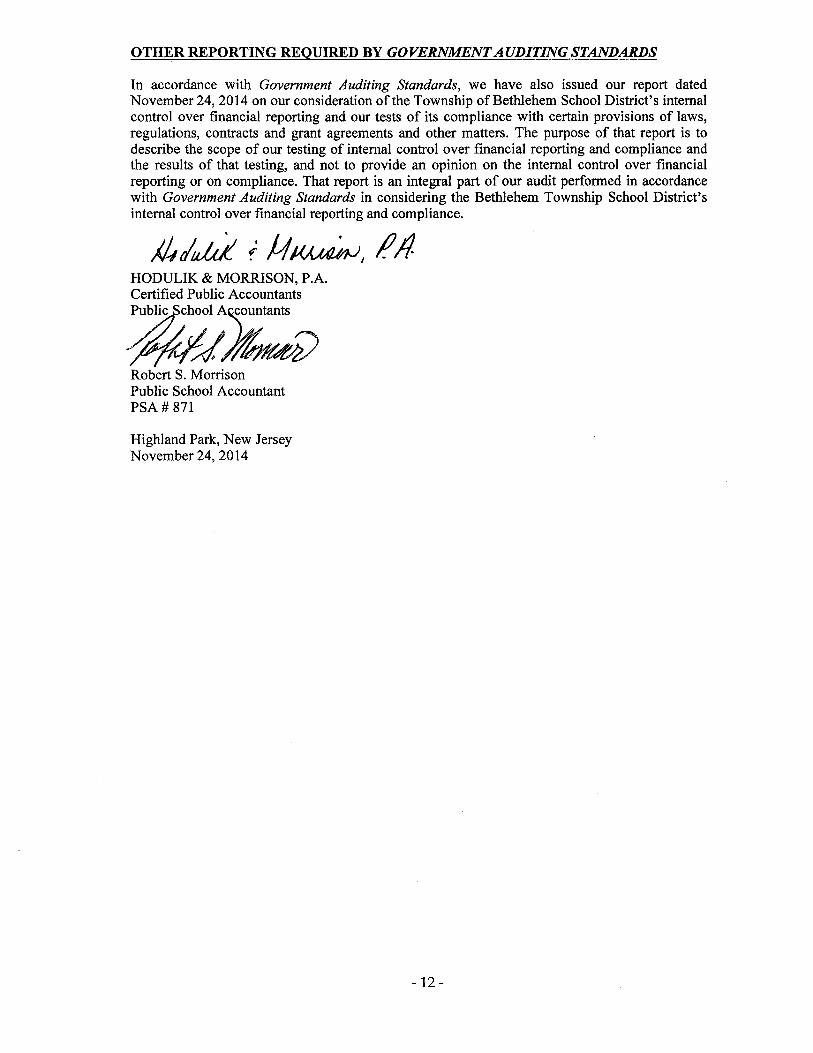

OTHER REPORTING REQUIRED BY GOVERNMENT AUDITING STANDARDS

In accordance with Government Auditing Standards, we have also issued our report datedNovember 24,2014 on our consideration of the Township of Bethlehem School District's internalcontrol over financial reporting and our tests of its compliance with certain provisions of laws,regulations, contracts and grant agreements and other matters. The purpose of that report is todescribe the scope of our testing of internal control over financial reporting and compliance andthe results of that testing, and not to provide an opinion on the internal control over financialreporting or on compliance. That report is an integral part of our audit performed in accordancewith Government Auditing Standards in considering the Bethlehem Township School District'sinternal control over financial reporting and compliance.

HODULIK & MORRISON, P.A.Certified Public Accountants

~;,~Robert S. MorrisonPublic School AccountantPSA # 871

Highland Park, New JerseyNovember 24,2014

-12 -

REQUIRED SUPPLEMENTARYINFORMATION

PART I

-13 -

BETHLEHEM TOWNSHIP SCHOOL DISTRICTAsbury, New JerseyHunterdon County

MANAGEMENT DISCUSSION & ANALYSIS (MD&A)June 30, 2014

The Township of Bethlehem School District (the "District") discussion and analysis is designed to providean overview of the District's financial activities for the year ended June 30, 2014, identify changes in theDistrict's financial position, identify any material deviations from the financial plan (the approved budget),and identify individual fund issues or concerns.

The focus of the Management Discussion and Analysis (MD&A) is on current year activities, resultingchanges and currently known facts. The MD&A should be read in conjunction with the Transmittal Letterand the District's Financial Statements.

Financial Highlights

The district's governmental activities net position increased by $356,707 as reflected in Table 2, Changes inNet Position. This increase is primarily attributable to favorable variances (budget v. actual) in currentoperations of $269,398. An additional $91,697 is attributable to the excess of long-term liability reductionsand capital equipment acquisitions over depreciation. These increases were offset by an increase in accruedliabilities of $4,389. The district's business-type activity expenses exceeded related revenues by $11,607.This amount was entirely comprised of the net loss from food service operations. The District entered into a"break-even" contract with its food service management company for the year, and as a result, the reportednet loss is comprised of depreciation and equipment repair expenses, which are excluded from the contractual"break-even" formula. The breakdown of the governmental and business-type activity amounts are reflectedin Schedule A-2 of the District-wide Financial Statements. The District's General Fund reported an increasein Fund Balance of $269,398 for the year as reflected in Schedule B-2 of the District-wide FinancialStatements.

Understanding the Annual Report

New Jersey state law and administrative code require that school districts follow Generally AcceptedAccounting Principles (GAAP.) The format focuses on the district as a whole (government-wide financialstatements) and refocuses the fund financial statements on major funds. Major funds are defined as those inwhich total assets and liabilities or revenues and expenditures/expenses are 10% or more of the total assetsand liabilities or revenues and expenditures/expenses of all funds of that type (governmental, proprietary,etc.) and at least 5% of the assets and liabilities or revenues and expenditures/expenses for all governmentaland enterprise funds combined.

Government-Wide Financial Statements

The government-wide financial statements (see financial statements A-I and A-2) are designed to becorporate-like in that all government and business-type activities are consolidated into columns, which addto a total for the district. The focus of the Statement of Net Position is designed to be similar to a bottomline for the district and its governmental and business type activities. This statement combines andconsolidates governmental fund's current financial resources (short-term spendable resources) with capitalassets and long-term obligations.

The Statement of Activities is focused on both the gross and net costs of various activities (includinggovernmental and business-type), which are provided by the government's general tax and other revenues.This statement is intended to summarize and simplify the user's analysis of the cost of variousgovernmental services and/or subsidy to various business type activities. All changes in net position arereported as soon as the underlying event giving rise to the change occurs, regardless of the timing of therelated cash flows. Over time, increases or decreases in net position may serve as a useful indicator ofwhether the financial position of the district is improving or deteriorating.

-14 -

Fund Financial Statements

A fund is a grouping of related accounts that is used to maintain control over resources that have beensegregated for specific activities or objectives. As required by accounting principles generally accepted inthe U.S and New Jersey state law and regulation, the district uses fund accounting to ensure anddemonstrate compliance with finance related legal requirements. All of the funds of the district can bedivided into three categories: governmental funds, proprietary funds and fiduciary funds.

The governmental funds are used to account for essentially the same functions reported as governmentalactivities in the government-wide financial statements. However, unlike the government-wide financialstatements, governmental fund financial statements focus on near-term inflows and outflows of spendableresources and balances of spendable resources available at the end of the fiscal year. This is the manner inwhich the District's financial plan (budget) is typically developed. The flow and availability of currentfinancial resources is a clear and appropriate focus of any analysis of a government. The financialstatements include reconciliations of the differences between the fund balance of the governmental fundsand the net position of the governmental activities in the government-wide financial statements (Exhibit B-1) and a reconciliation of the differences between the net changes in government fund balances and thechange in net position in the government-wide financial statements (Exhibit B-3).

The proprietary funds consist of a major program (food services enterprise fund) Proprietary funds areused to account for activities and programs that are financed primarily through user fees. The activityreported in the proprietary funds utilizes the same basis of accounting as that of the business-type activitiesreported in the government-wide financial statements. The "Total" column on the business-type fundfinancial statements is the same as the business-type column on the government-wide financial statements.

Fiduciary funds are used to account for resources held for the benefit of parties outside of the government.Fiduciary funds are not reported in the government-wide financial statements because the resources ofthose funds are not available to support the programs of the district. The district's fiduciary funds includethe student activities fund, the payroll agency fund, and the employee benefit flexible spending trust fund.

The District as a Whole

Table I reflects the condensed Statement of Net Assets. In this statement the district is divided into twokinds of activities:

Governmental Activities-These activities consist of instruction and those services, which supportinstruction such as maintenance, transportation and administration.

Business-Type Activities- These activities consist of the district's cafeteria operations, childcare program,summer camp program and summer enrichment program. Each of the aforementioned programs and thecafeteria charge fees for the services provided that are intended to cover most or all of the cost of servicesprovided.

The condensed Statement of Net Position reflects assets, deferred outflows of resources, liabilities anddeferred inflows of resources of the district on an accrual basis of accounting. This statement, whichreflects the district's net financial position, is a yardstick of measuring the district's net worth. It meansthat if the district were forced to liquidate on June 30,2014 and sell all its assets at book value, after payingall known bills and liabilities, including long-term bonds and lease obligations, the District would have atotal of $691,964 remaining.

-15 -

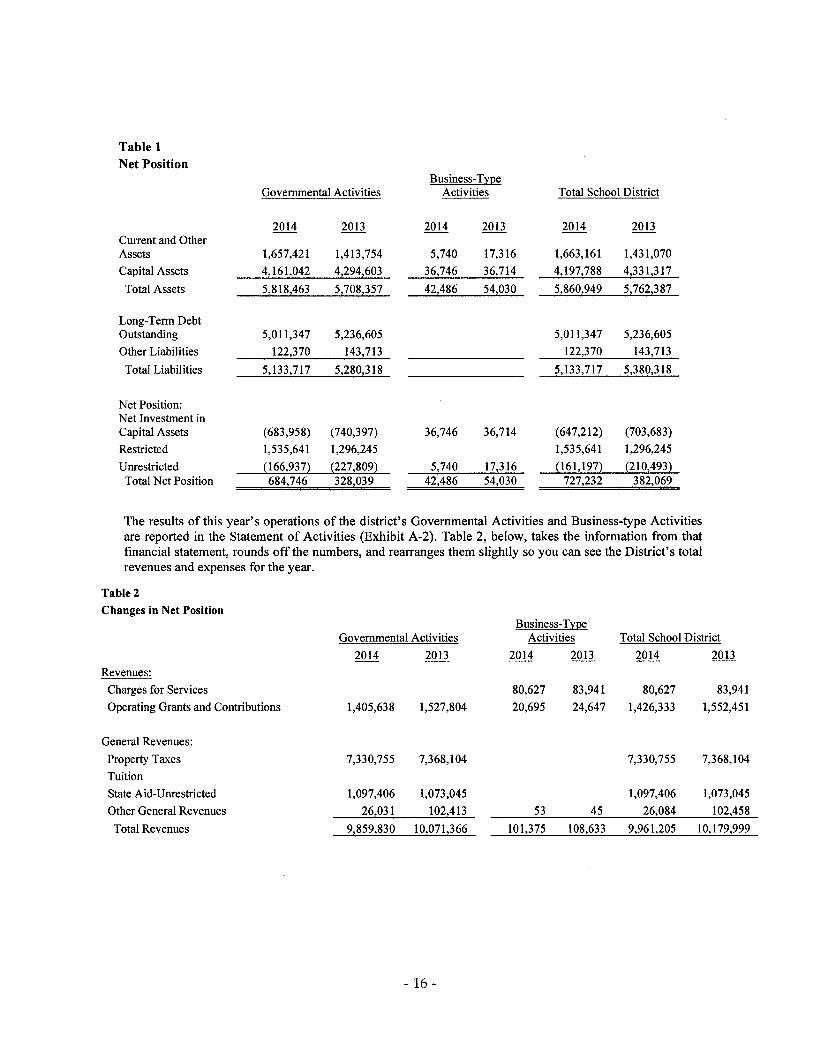

Table 1Net Position

Business-TypeGovernmental Activities Activities Total School District

2014 2013 2014 2013 2014 2013Current and OtherAssets 1,657,421 1,413,754 5,740 17,316 1,663,161 1,431,070Capital Assets 4,161,042 4,294,603 36,746 36,714 4,197,788 4,331,317

Total Assets 5,818,463 5,708,357 42,486 54,030 5,860,949 5,762,387

Long-Term DebtOutstanding 5,011,347 5,236,605 5,011,347 5,236,605

Other Liabilities 122,370 143,713 122,370 143,713

Total Liabilities 5,133,717 5,280,318 5,133,717 5,380,318

Net Position:Net Investment inCapital Assets (683,958) (740,397) 36,746 36,714 (647,212) (703,683)

Restricted 1,535,641 1,296,245 1,535,641 1,296,245

Unrestricted {l66,937} {227,809} 5,740 17,316 {161,197} {210,493}Total Net Position 684,746 328,039 42,486 54,030 727,232 382,069

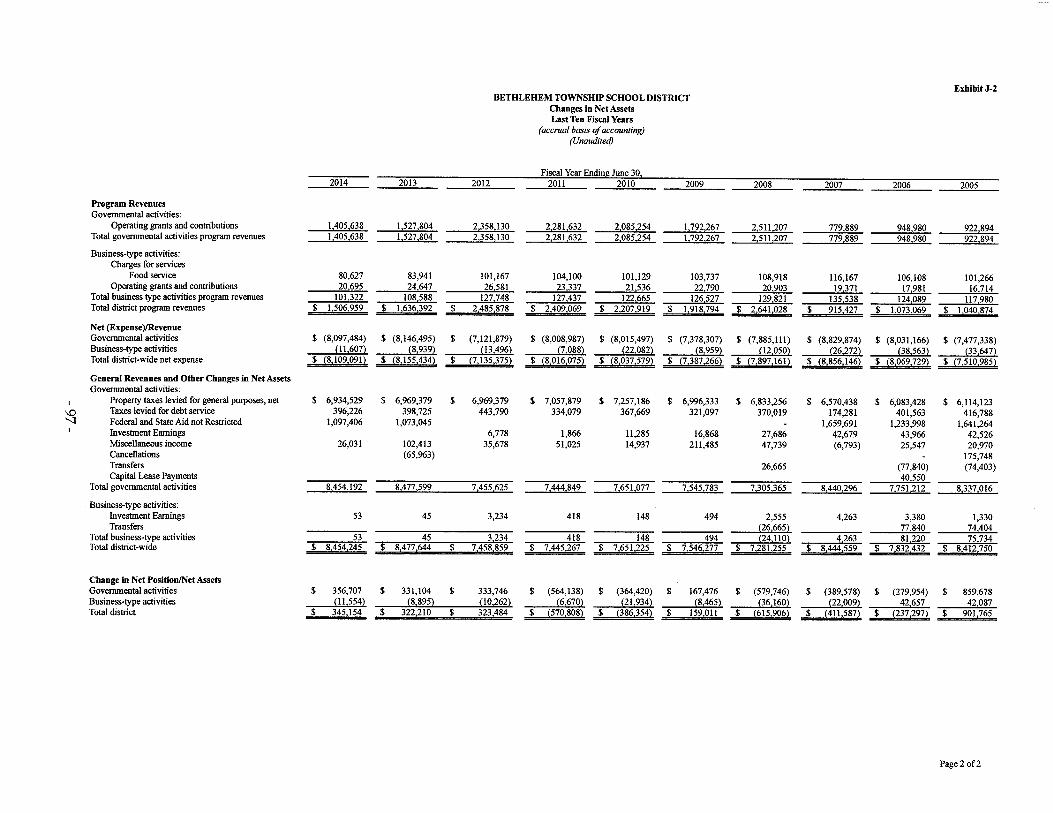

The results of this year's operations of the district's Governmental Activities and Business-type Activitiesare reported in the Statement of Activities (Exhibit A-2). Table 2, below, takes the information from thatfinancial statement, rounds off the numbers, and rearranges them slightly so you can see the District's totalrevenues and expenses for the year.

Table 2Changes in Net Position

Business-TypeGovernmental Activities Activities Total School District

2014 2013 2014 2013 2014 2013Revenues:Charges for Services 80,627 83,941 80,627 83,941Operating Grants and Contributions 1,405,638 1,527,804 20,695 24,647 1,426,333 1,552,451

General Revenues:Property Taxes 7,330,755 7,368,104 7,330,755 7,368,104

TuitionState Aid-Unrestricted 1,097,406 1,073,045 1,097,406 1,073,045

Other General Revenues 26,031 102,413 53 45 26084 102,458

Total Revenues 9,859,830 10,071:366 101,375 108,633 9,961,205 10,179,999

-16 -

2014 2013 2014 2013 2014 2013Program Expenses IncludingIndirect Expenses:

Instruction:Regular 2,233,645 2,692,768 2,233,645 2,692,768Special Education 1,083,447 1,047,824 1,083,447 1,047,824Other Instruction 82,785 88,197 82,785 88,197

Support Services:Tuition 259,797 356,896 259,797 356,896Student & Instruction Related Services 1,292,832 1,032,608 1,292,832 1,032,608School Administrative Services 320,198 216,477 320,198 216,477General and Business Admin. Services 501,287 571,839 501,287 571,839

Plant Operations and Maintenance 846,671 792,657 846,671 792,657Pupil Transportation 438,127 511,592 438,127 511,592Unallocated Benefits 2,017,592 1,971,803 2,017,592 1,971,803

Interest on Long-Term Debt 233,499 210,333 233,499 210,333Unallocated Depreciation & Amortization 193,241 181,305 193,241 181,305Business-Type Activities:

Food Service 112,928 117,527 112,938 117,527

Total Expenses 9,5303,122 9,6741299 112,928 117,527 9,616,050 9,791,826Special Item - Prior Year RevenueAdjustment {65,963} {65,963}

Increase (Decrease) in Net Position 356,707 331,104 {11,554} {8,894} 345,154 322,210

During FY 2014 the net position ofthe District's governmental activities increased by $356,707. Favorablebudget variances and the excess of debt repayment and capital equipment acquisitions over depreciationexpenses were offset by the write-off of state building aid revenues accrued in prior periods and deemeduncollectible during the current fiscal period. The net position of the food service (business-type) activitiesdecreased by $11,554 in the current fiscal period. The food service fund has been operating at a deficit forseveral years. At June 30, 2014, the unrestricted net position of the food service fund was $5,740.

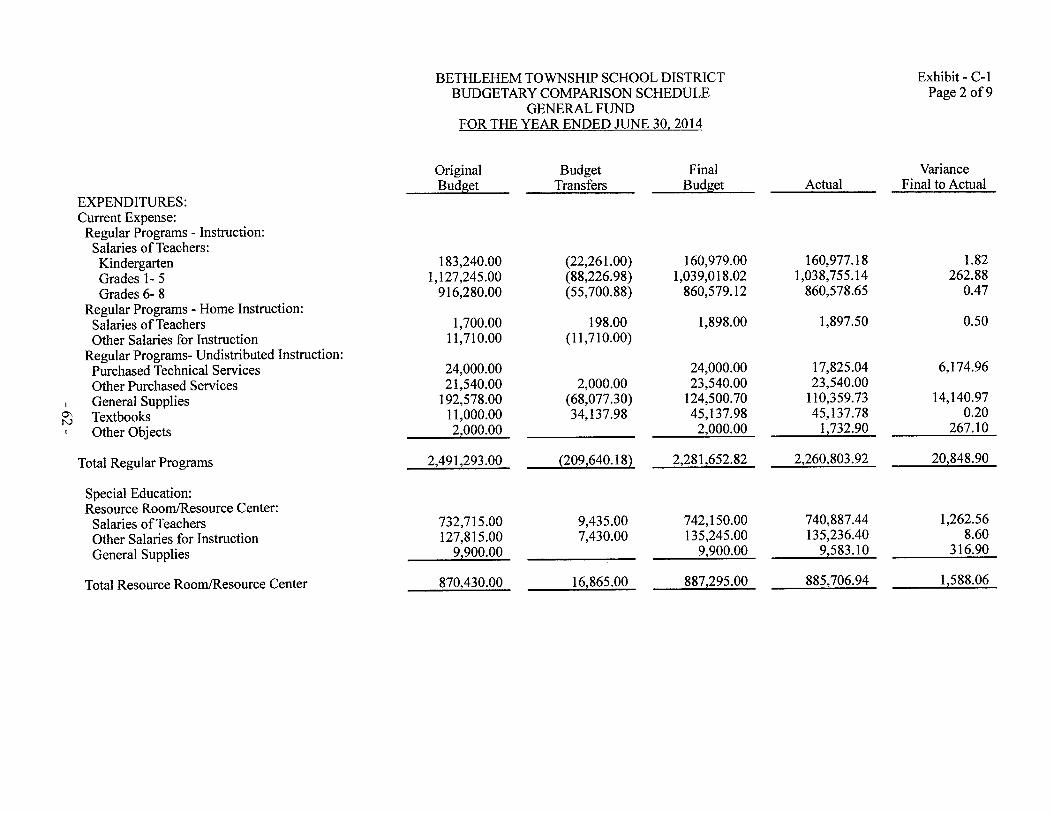

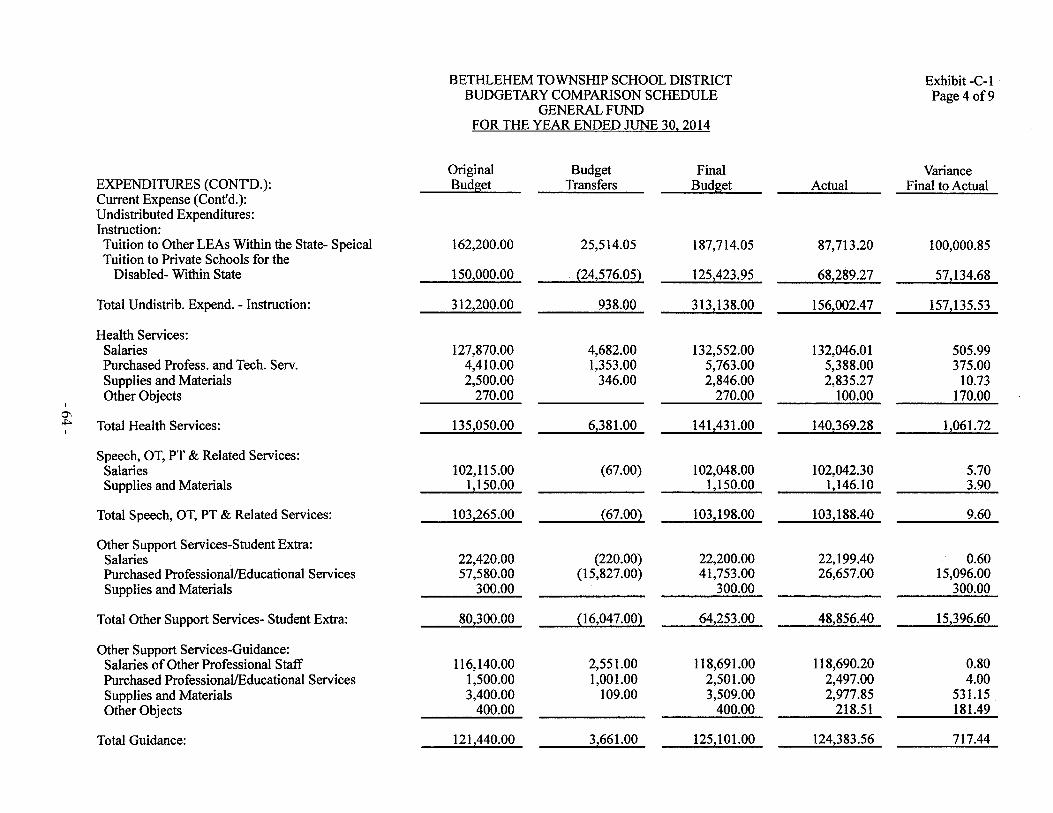

The balance generated in current operations was primarily driven by savings throughout the budget. ExhibitC-l provides a breakdown of the budget line items included in the District's approved 2013-2014 budgetand the variances in actual revenues and expenditures. Revenue realization for the 2013-2014 school yeardeclined for governmental activities when compared to the 2012-2013 school year. As shown in Table 3,the Tax needed to support the District's budget decreased by 0.61% for the 2012-2013 school year. The taxlevy for general operations was held at the prior year levels, and required debt service levies declined by$45,065. Non-tax revenues of the District remain a small percentage of total revenues, however,unrestricted non-tax local revenues increased by $60,512 during the current year. Additionally, the districtrealized $21,836 more then anticipated for Extraordinary Aid.

-17 -

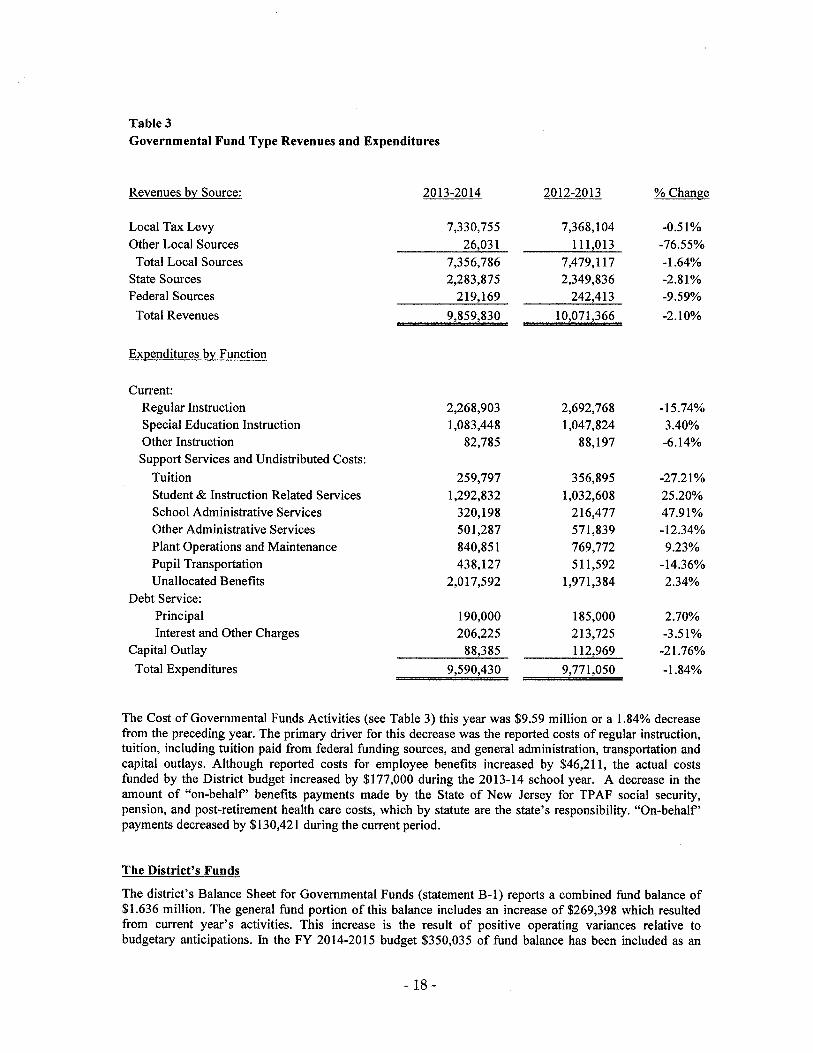

Table 3Governmental Fund Type Revenues and Expenditures

Revenues by Source:

Local Tax LevyOther Local SourcesTotal Local Sources

State SourcesFederal SourcesTotal Revenues

2013-2014 2012-2013 % Change

7,330,755 7,368,104 -0.51%26,031 111,013 -76.55%

7,356,786 7,479,117 -1.64%2,283,875 2,349,836 -2.81%219,169 242,413 -9.59%

9,859,830 10,071,366 -2.10%

Expenditures by Function

Current:Regular InstructionSpecial Education InstructionOther InstructionSupport Services and Undistributed Costs:

TuitionStudent & Instruction Related ServicesSchool Administrative ServicesOther Administrative ServicesPlant Operations and MaintenancePupil TransportationUnallocated Benefits

Debt Service:PrincipalInterest and Other Charges

Capital OutlayTotal Expenditures

2,268,903 2,692,768 -15.74%1,083,448 1,047,824 3.40%

82,785 88,197 -6.14%

259,797 356,895 -27.21%1,292,832 1,032,608 25.20%320,198 216,477 47.91%501,287 571,839 -12.34%840,851 769,772 9.23%438,127 511,592 -14.36%

2,017,592 1,971,384 2.34%

190,000 185,000 2.70%206,225 213,725 -3.51%88,385 112,969 -21.76%

9,590,430 9,771,050 -1.84%

The Cost of Governmental Funds Activities (see Table 3) this year was $9.59 million or a 1.84% decreasefrom the preceding year. The primary driver for this decrease was the reported costs of regular instruction,tuition, including tuition paid from federal funding sources, and general administration, transportation andcapital outlays. Although reported costs for employee benefits increased by $46,211, the actual costsfunded by the District budget increased by $177,000 during the 2013-14 school year. A decrease in theamount of "on-behalf' benefits payments made by the State of New Jersey for TPAF social security,pension, and post-retirement health care costs, which by statute are the state's responsibility. "On-behalf'payments decreased by $130,421 during the current period.

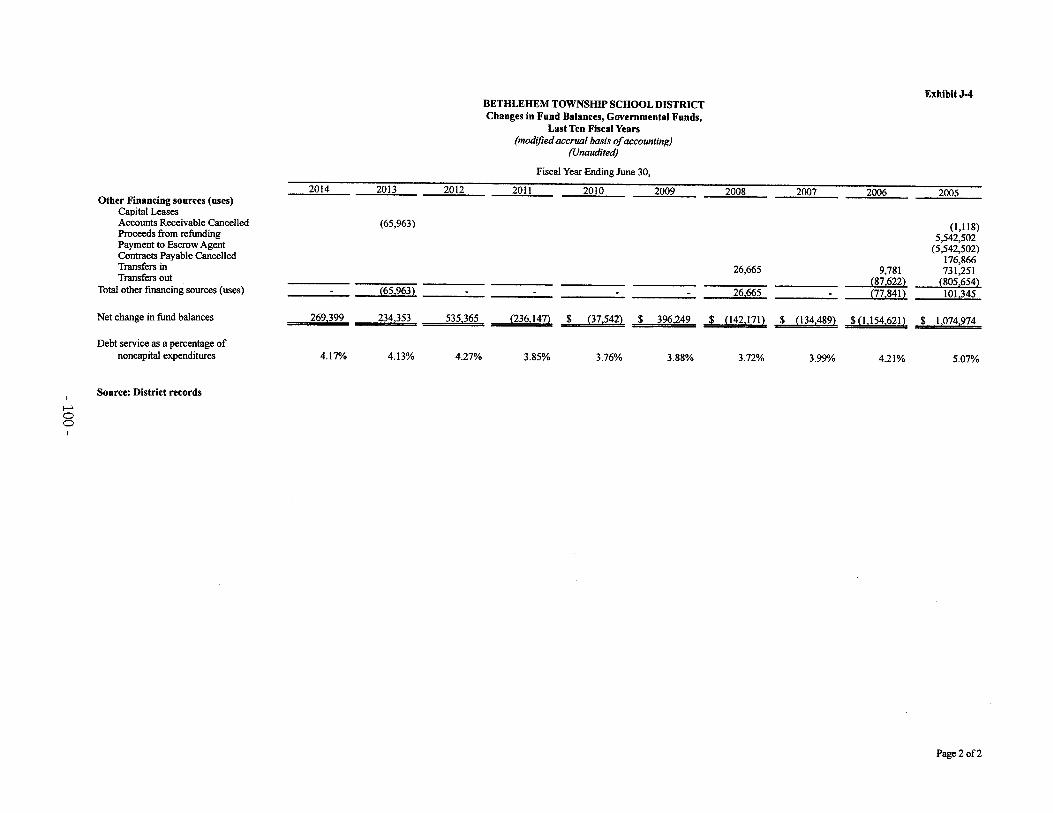

The District's Funds

The district's Balance Sheet for Governmental Funds (statement B-1) reports a combined fund balance of$1.636 million. The general fund portion of this balance includes an increase of $269,398 which resultedfrom current year's activities. This increase is the result of positive operating variances relative tobudgetary anticipations. In the FY 2014-2015 budget $350,035 of fund balance has been included as an

-18 -

offset to local taxes. An additional $308,941 is set-aside for FY 15-16 to stabilize the local tax levy on aGAAP basis.

General Fund Budgetary Highlights

The 2013-2014 revenues of the General fund amounted to $9.244 million or a 2.55% decrease from theprior year. Decreases were reported in every category of revenue, including property taxes, which weredecreased in the Board approved budget.

The 2013-2014 expenditures of the General fund amounted to $8.975 million, an decrease of $143,276(1.6%) from the prior year. Instructional, Tuition, General Administration and Transportation costs werethe largest cost drivers for the decrease. Excluding In-Kind costs, which are not budgeted, the Districtunderspent its available appropriation by $743,630 in 2013-2014.

Capital Asset and Debt Administration

Capital Assets

The District engaged an inventory valuation firm to identify and value its fixed assets as of June 30, 2013and for the current and prior school years. As the new inventory data did not conform to the amountsreported in the prior Comprehensive Annual Financial Statement, a restatement of the June 30, 2013 NetPosition of the District was required. The District's net investment in fixed assets and total net positionincreased by $896,708 as a result of this restatement. At the end of 2013, the district had $4,331,317invested in capital assets as shown on Table 4, Capital Assets Net of Depreciation at June 30, 2013 and2014. During 2013-2014, the District capitalized the costs of equipment and architectural fees totaling$59,680 in its governmental activities. Depreciation expense for 2013-2014 totaled $202,190, whichincluded $193,241 for governmental activities and $8,948 for business-type activities. During the 2013-2014 school year, the $190,000 of capital related debt retired was short of depreciation expenses by $3,421,decreasing the net increase in the District's financial position at year-end.

Capital AssetsTable 4

Capital Assets at Year-End(Net of Depreciation)

Governmental Activities

2014 2013

Land 139,200 139,200Land Improvements 94,829 94,829Buildings & Improvements 7,475,660 7,475,660Machinery & Equipment 688,240 628,560

Subtotal 8,397,929 8,338,249Accumulated Depreciation {4,236,887) {4,043,646)

Totals 4,161,042 4,294,603

Business-Type Activities Total School District

139,20094,829

7,475,660896,543208,303

199,323

071,557)

36,746

199,323

199,323

062,609)

36,714

8,606,232

{4,408,444)

4,197,788

-19 -

139,20094,829

7,475,660827,883

8,537,572

{4,206,255)

4,331,317

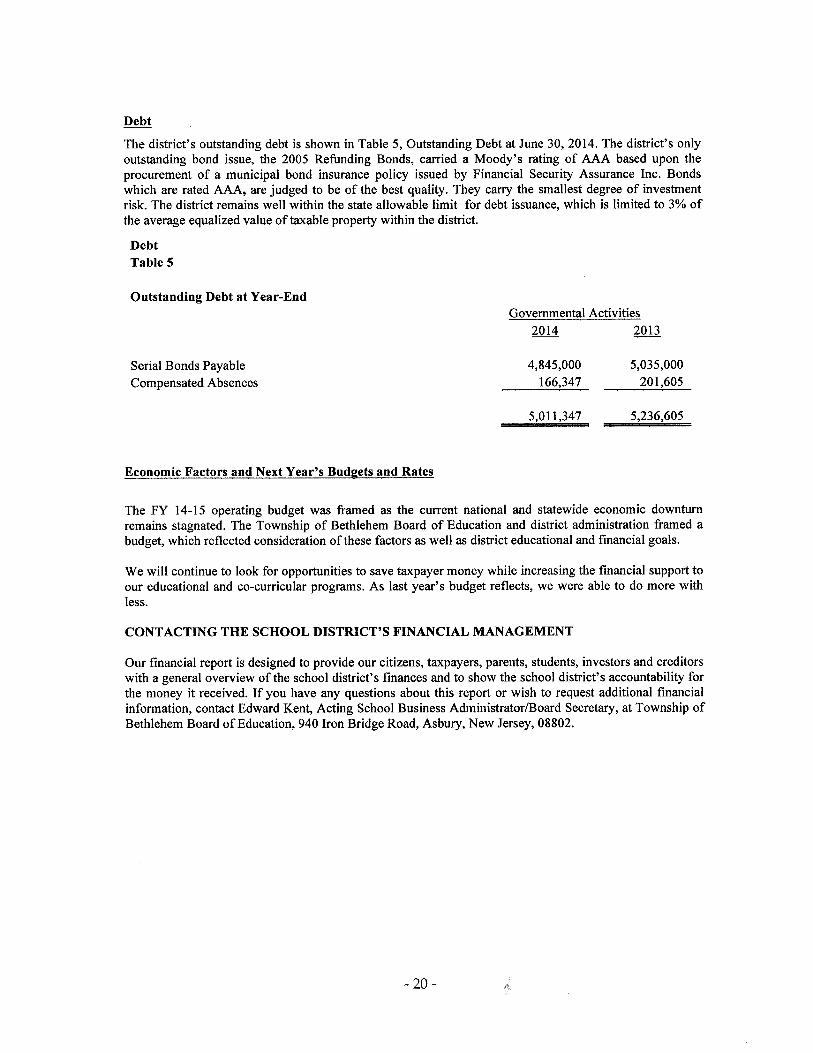

Debt

The district's outstanding debt is shown in Table 5, Outstanding Debt at June 30, 2014. The district's onlyoutstanding bond issue, the 2005 Refunding Bonds, carried a Moody's rating of AAA based upon theprocurement of a municipal bond insurance policy issued by Financial Security Assurance Inc. Bondswhich are rated AAA, are judged to be of the best quality. They carry the smallest degree of investmentrisk. The district remains well within the state allowable limit for debt issuance, which is limited to 3% ofthe average equalized value of taxable property within the district.

DebtTable 5

Outstanding Debt at Year-EndGovernmental Activities

2014 2013

Serial Bonds PayableCompensated Absences

4,845,000166,347

5,035,000201,605

5,011,347 5,236,605

Economic Factors and Next Year's Budgets and Rates

The FY 14-15 operating budget was framed as the current national and statewide economic downturnremains stagnated. The Township of Bethlehem Board of Education and district administration framed abudget, which reflected consideration of these factors as well as district educational and financial goals.

We will continue to look for opportunities to save taxpayer money while increasing the financial support toour educational and co-curricular programs. As last year's budget reflects, we were able to do more withless.

CONTACTING THE SCHOOL DISTRICT'S FINANCIAL MANAGEMENT

Our financial report is designed to provide our citizens, taxpayers, parents, students, investors and creditorswith a general overview of the school district's finances and to show the school district's accountability forthe money it received. If you have any questions about this report or wish to request additional financialinformation, contact Edward Kent, Acting School Business AdministratorlBoard Secretary, at Township ofBethlehem Board of Education, 940 Iron Bridge Road, Asbury, New Jersey, 08802.

- 20-

BASIC FINANCIAL STATEMENTS

- 21-

DISTRICT-WIDE FINANCIAL STATEMENTS

SECTION-A

- 22-

Exhibit A-I

BETHLEHEM TOWNSHIP SCHOOL DISTRICTSTATEMENT OF NET POSITION

JUNE 30, 2014

GOVERNMENTAL BUSINESS-TYPEACTIVITIES ACTIVITIES TOTAL

ASSETSCash and Cash Equivalents $ 1,613,806.12 $ 1,080.65 $ 1,614,886.77Receivables, Net 43,464.94 2,876.64 46,341.58Receivables from Other Funds 150.06 150.06Inventory 1,782.32 1,782.32Capital Assets, Net (Note 3): 4,161,042.15 36,746.30 4,197,788.45

Total Assets 5,818,463.27 42,485.91 5,860,949.18

LIABILITIESAccounts Payable 21,720.00 21,720.00Accrued Interest Payable 100,650.21 100,650.21Noncurrent Liabilities (Note 4):

Due Within One Year 257,065.40 257,065.40Due Beyond One Year 4,754,281.34 4,754,281.34

Total liabilities 5,133,716.95 5,133,716.95

NET POSITIONInvested in capital assets, net of related debt (683,957.85) 36,746.30 (647,211.55)Restricted for:

Other Purposes 1,535,641.25 1,535,641.25Unrestricted (Deficit) (166,937.08) 5739.61 (161,197.47)

Total Net Position $ 684:746.32 $ 42:485.91 $ 727:232.23

The accompanying Notes to Financial Statements are an integral part of this statement.

- 23-

FunctionslPrograms

Governmental Activities:Instruction:RegularSpecial EducationOther Instruction

Support Services:TuitionStudent & Instruction Related ServicesSchool Administrative ServicesGeneral and Business Administrative ServicesPlant Operations and MaintenancePupil TransportationUnallocated Benefits

Interest on Long-Term DebtUnallocated Depreciation and Amortization

Total Governmental Activities

Business-Type Activities:Food Service

Total Business-Type Activities

Total Primary Government

BETHLEHEM TOWNSHIP SCHOOL DISTRICTSTATEMENT OF ACTIVITIES

FOR THE YEAR ENDED JUNE 30, 2014

PROGRAM REVENUES

EXPENSES

CHARGES OPERATINGFOR GRANTS AND

SERVICES CONTRIBUTIONS

$2,233,644.90 8,099.001,083,447.57 354,078.00

82,785.27

259,797.47 103,795.001,292,831. 73 107,274.74320,197.75501,287.34846,670.96 38,403.00438,126.71 88,973.60

2,017,592.33 705,014.28233,498.79193,241.29

9,503,122.11 1,405,637.62

112,928.37 80:626.80 20694.73

112:928.37 80:626.80 20694.73

$9:616,050.48 $80:626.80 $1:426:332.35

General Revenues:Taxes:Property Taxes, Levied for General Purposes,NetTaxes Levied for Debt Service

Federal and State Aid not RestrictedInvestment EarningsMiscellaneous Income

Total General Revenues and Special Items

Change in Net Position

Net Position-Beginning

Net Position-Ending

The accompanying Notes to Financial Statements are an integral part of this statement.

ExhibitA-2

NET (EXPENSE) REVENUE ANDCHANGE IN NET ASSETS

GOVERNMENTAL BUSINESS-TYPEACTIVITIES ACTIVITIES

($2,225,545.90)(729,369.57)(82,785.27)

(156,002.47)(1,185,556.99)(320,197.75)(501,287.34)(808,267.96)(349,153.11)

(1,312,578.05)(233,498.79)(193:241.29)

(8:097,484.49)

(11:606.84)

(11:606.84)

TOTAL

($2,225,545.90)(729,369.57)(82,785.27)

(156,002.47)(1,185,556.99)(320,197.75)(501,287.34)(808,267.96)(349,153.11)

(1,312,578.05)(233,498.79)(193:241.29)

(8:097,484.49)

(11:606.84)

(11:606.84)

($8,097,484.49) ($11,606.84) ($8,109,091.33)

$6,934,529.00 $6,934,529.00396,226.00 396,226.00

1,097,406.00 1,097,406.0053.14 53.14

26:030.83 26:030.83

8,45991.83 53.14 8:454:244.97

356,707.34 (11,553.70) 345,153.64

328:038.98 54:029.61 382:068.59

$68946.32 $42:475.91 $727:222.23

FUND FINANCIAL STATEMENTS

SECTION -B

- 25-

GOVERNMENTAL FUNDS

-~-

Exhibit B-1Page 1 of2

BETHLEHEM TOWNSHIP SCHOOL DISTRICTBALANCE SHEET

GOVERNMENTAL FUNDSJUNE 30, 2014

SPECIAL DEBT TOTALGENERAL REVENUE SERVICE GOVERNMENTAL

FUND FUND FUND FUNDS

ASSETSCash and Cash Equivalents (Deficit) $ 1,643,509.25 $ (29,706.00) $ 2.87 $ 1,613,806.12Interfund Accounts Receivable 150.06 150.06Receivables from Other Governments 132758.94 292706.00 43464.94

Total Assets 126572418.25 2.87 126572421.12

LIABILITIES AND FUND BALANCESLiabilities:

N Accounts Payable 212720.00 212720.00'1

Total Liabilities 212720.00 212720.00

Fund Balances:Restricted:Reserved Excess Surplus 308,941.22 308,941.22Reserved Excess Surplus-Designated forSubsequent Year Expenditures 350,035.00 350,035.00

Capital Reserve Account 30,001.00 30,001.00Maintenance Reserve Account 376,889.61 376,889.61

Committed:Reserve for Encumbrances 469,774.42 469,774.42

Unassigned:Debt Service Fund 2.87 2.87General Fund 1002057.00 1002057.00

Total Fund Balances 126352698.25 2.87 126352701.12

Total Liabilities and Fund Balances $ 12657A18.25 $ $ 2.87 $ 12657A21.12

The accompanying Notes to Financial Statements are an integral part of this statement.

BETHLEHEM TOWNSHIP SCHOOL DISTRICTBALANCE SHEET

GOVERNMENTAL FUNDSJUNE 30, 2014

Amounts reported for governmental activities in the statement ofnet position (A-I) are different because:

Capital assets used in governmental activities are not fmancialresources and therefore are not reported in the funds. The carrying valueof the assets is $8,397,929.2 , and the accumulated depreciationis $4,236,887.06 .

Long-term liabilities, including bonds and judgments payable, are not due andpayable in the current period and therefore are not reported asliabilties in the funds.

N00 Short-term Liabilities, including accrued interest on long-term debt,

are not due payable in the current period and therefore are notreported as liabilities in the funds.

Net position of governmental activities

The accompanying Notes to Financial Statements are an integral part of this statement.

Exhibit B-1Page 2 of2

$ 1,635,701.12

4,161,042.15

(5,011,346.74)

(100,650.21)

$ ==~6=84=,7=4=6.=32;::

Exhibit B-2BETHLEHEM TOWNSHIP SCHOOL DISTRICT

STATEMENT OF REVENUES, EXPENSES, AND CHANGE IN FUND BALANCESGOVERNMENTAL FUNDS

FOR THE YEAR ENDED JUNE 30, 2014

SPECIAL DEBT TOTALGENERAL REVENUE SERVICE GOVERNMENTAL

FUND FUND FUND FUNDSREVENUES

Local Tax Levy $ 6,934,529.00 $ $ 396,226.00 $ 7,330,755.00Other Local Sources 26,030.83 26,030.83State Sources 2,283,874.88 2,283,874.88Federal Sources 219z168.74 219168.74

Total Revenues 9z244z434.71 219z168.74 396z226.00 9z859z829.45

EXPENDITURESCurrent:

Regular Instruction 2,260,803.92 8,099.00 2,268,902.92Special Education Instruction 1,083,447.57 1,083,447.57Other Instruction 82,785.27 82,785.27

tv Support Services and Undistributed Costs:\0 Tuition 156,002.47 103,795.00 259,797.47

Student & Instruction Related Services 1,185,556.99 107,274.74 1,292,831.73School Administrative Services 320,197.75 320,197.75Other Administrative Services 501,287.34 501,287.34Plant Operations and Maintenance 840,850.96 840,850.96Pupil Transportation 438,126.71 438,126.71Unallocated Benefits 2,017,592.33 2,017,592.33

Debt Service:Principal 190,000.00 190,000.00Interest Charges 206,225.04 206,225.04

Capital Outlay 88z385.01 88385.01

Total Expenditures 8z975z036.32 219z168.74 396z225.04 9z590z430.10

Excess (Deficiency) of Revenuesover Expenditures 2692398.39 0.96 2692399.35

Net Change in Fund Balances 269,398.39 0.96 269,399.35

Fund Balance-Beginning 12366z299.86 1.91 lz3662301.77

Fund Balance-Ending $ 1z6352698.25 $ $ 2.87 $ lz6352701.12

The accompanying Notes to Financial Statements are an integral part of this statement.

BETHLEHEM TOWNSHIP SCHOOL DISTRICTRECONCILIATION OF THE STATEMENT OF REVENUES, EXPENDITURES,

AND CHANGES IN FUND BALANCES OF GOVERNMENTAL FUNDSTO THE STATEMENT OF ACTIVITIESFOR THE YEAR ENDED JUNE 30. 2014

Total net change in fund balances - governmental funds (from B-2)

Amounts reported for governmental activities in the statementof activities (A-2) are different because:

Capital outlays are reported in governmental funds as expenditures. However, in the statement ofactivities, the cost of those assets is allocated over their estimated useful lives as depreciation expense.This is the amount by which depreciation exceeded capital outlays in the period.

Depreciation expenseCapital Outlays

Repayment of bond and lease obligation (long-term debt)principal is an expenditure in the governmental funds,but the repayment reduces long-term liabilities in the statement of net assets and is not reported in thestatement of activities.

In the statement of activities, the value of earned but unused compensated absences are accrued when it becomes,likely that these costs will be includable in employee termination payments, regardless of when due. In thegovernmental funds, compensated absence costs are reported in the accounting period in which they becomedue and payable. The net decrease in accrued compensated absences is an addition in the reconciliation. (+)

In the statement of activities, interest on long-term debt in the statement of activities is accrued,regardless of when due. In the governmental funds, interest is reported when due. The accruedinterest is a deduction in the reconciliation. (-)

Change in net assets of governmental activities

The accompanying Notes to Financial Statements are an integral part of this statement.

- 30-

Exhibit B-3

$ 269,399.35

(193,241.29)59,680.01 (133,561.28)

190,000.00

35,258.02

(4,388.75)

$ 356,707.34

PROPRIETARY FUNDS

- 31-

Exhibit B-4

BETHLEHEM TOWNSHIP SCHOOL DISTRICTSTATEMENT OF NET POSITION

PROPPRIETARY FUNDSJUNE 30, 2014

BUSINESS-TYPE TOTALACTIVITIES - ENTERPRISE

ENTERPRISE FUND FUNDFOOD ----~~-----

SERVICE TOTAL

ASSETSCurrent assets:

Cash and Cash EquivalentsAccounts Receivable (Net)Inventory

Total Assets

$ 1,080.65 $ 1,080.652,876.64 2,876.641,782.32 1,782.32

5,739.61 5,739.61

208,303.38 208,303.38(171,557.08) (171,557.08)

36,746.30 36,746.30

42,485.91 42,485.91

Total Current Assets

Noncurrent Assets:Furniture, Machinery & Equipment

Less Accumulated Depreciation

Total Noncurrent Assets

NET POSITIONInvested in Capital Assets Net of

Related DebtUnrestricted (Deficit)

36,746.305,739.61

36,746.305739.61

Total Net Position $ 42,485.91 $ ===4=2:l:::,4=85:::::.9=1=

The accompanying Notes to Financial Statements are an integral part of this statement.

- 32-

Exhibit B-5

BETHLEHEM TOWNSHIP SCHOOL DISTRICTSTATEMENT OF REVENUES, EXPENSES, AND CHANGES IN NET POSITION

PROPRIETARY FUNDSFOR THE YEAR ENDED JUNE 30, 2014

BUSINESS-TYPEACTIVITIES -

ENTERPRISE FUNDFOOD

SERVICE

TOTALENTERPRISE

FUNDOperating Revenues:

Charges for Services:Daily Sales - Non-reimbursable Programs

Total Operating Revenues

Operating Income (Loss)

$ 80,626.80 $ 80,626.80

80,626.80 80,626.80

48,449.53 48,449.5334,532.56 34,532.565,299.51 5,299.51550.61 550.61

4,272.29 4,272.29223.09 223.09

1,642.70 1,642.709,000.00 9,000.008948.08 8,948.08

112918.37 112,918.37

{32,291.572 {32,291.572

Operating Expenses:Cost of SalesSalariesEmployee benefitsRepair and Maintenance ServicesAdministrative ExpensesMiscellaneous ExpensesTransportationManagement FeeDepreciation

Total Operating Expenses

Nonoperating Revenues (Expenses):State Sources:State School Lunch Program

Federal Sources:USDA CommoditiesNational School Lunch Program

Interest and Investment Revenue

Income (Loss) Before Transfers

1,095.87 1,095.87

6,114.82 6,114.8213,484.04 13,484.04

53.14 53.14

20747.87 20747.87

(11,543.70) (11,543.70)

(11,543.70) (11,543.70)

54029.61 54,029.61

$ 42485.91 $ 42,485.91

Total Nonoperating Revenues (Expenses)

Change in Net Position

Total Net Position-Beginning

Total Net Position-Ending

The accompanying Notes to Financial Statements are an integral part of this statement.- 33-

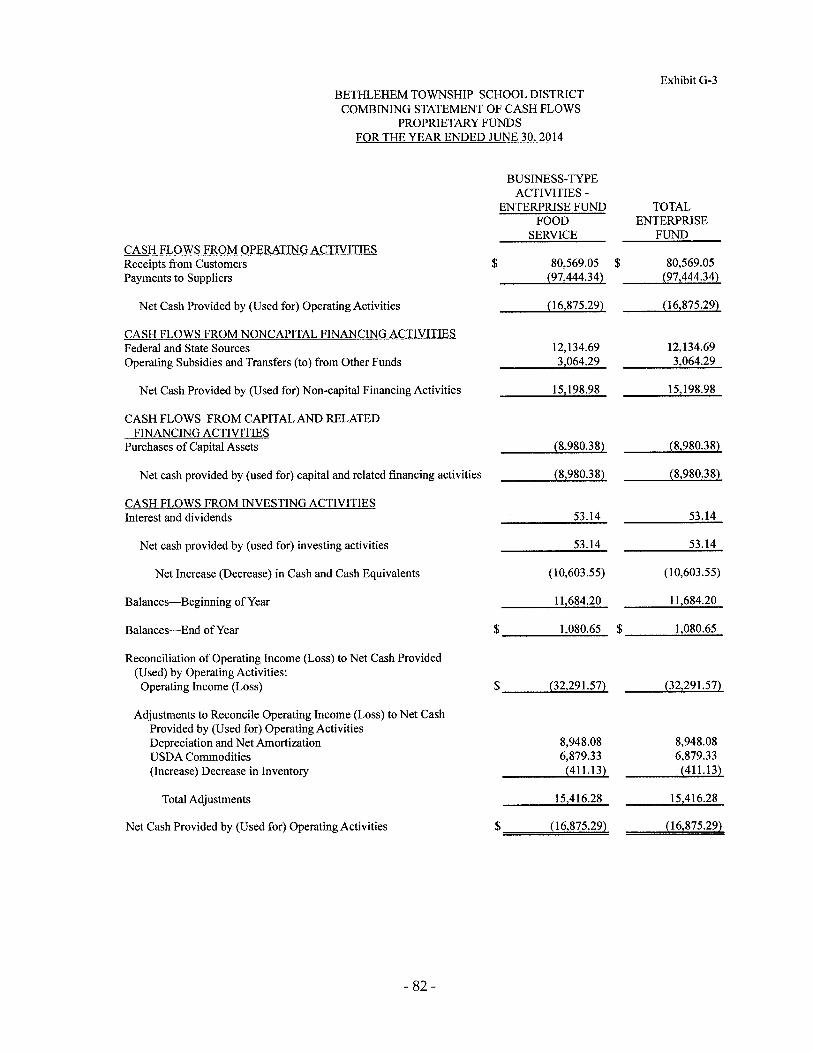

Exhibit B-6BETHLEHEM TOWNSHIP SCHOOL DISTRICT

STATEMENT OF CASH FLOWSPROPRIETARY FUNDS

FOR THE YEAR ENDED JUNE 30. 2014

Net Cash Provided by (Used for) Operating Activities

BUSINESS-TYPEACTIVITIES -

ENTERPRISE FUND TOTALFOOD ENTERPRISE

SERVICE FUND

$ 80,569.05 $ 80,569.05(97,444.34) (97,444.34)

(16,875.29) (16,875.29)

12,134.69 12,134.693064.29 3,064.29

15 198.98 15:198.98

CASH FLOWS FROM OPERATING ACTIVITIESReceipts from CustomersPayments to Suppliers

CASH FLOWS FROM NONCAPITAL FINANCING ACTIVITIESFederal and State SourcesOperating Subsidies and Transfers (to) from Other Funds

Net Cash Provided by (Used for) Non-capital Financing Activities

CASH FLOWS FROM CAPITALAND RELATEDFINANCING ACTIVITIES

Purchases of Capital Assets (8:980.38) (8:980.38)

(8:980.38) (8:980.38)

53.14 53.14

53.14 53.14

(10,603.55) (10,603.55)

11:684.20 11:684.20

1080.65 $ 1:080.65

Net cash provided by (used for) capital and related financing activitie ~;...;;;..;;=.;;;",-

CASH FLOWS FROM INVESTING ACTIVITIESInterest and dividends

Net cash provided by (used for) investing activities

Net Increase (Decrease) in Cash and Cash Equivalents

Balances-Beginning of Year

Balances-End of Year $ ---:==;_

Reconciliation of Operating Income (Loss) to Net Cash Provided(Used] by Operating Activities:Operating Income (Loss) $ (32:291.57) (32:291.57)

Adjustments to Reconcile Operating Income (Loss) to Net CashProvided by (Used for) Operating ActivitiesDepreciation and Net Amortization 8,948.08 8,948.08USDA Commodities 6,879.33 6,879.33(Increase) Decrease in Inventory (411.13) (411.13)

Total Adjustments 15:416.28 15:416.28

Net Cash Provided by (Used for) Operating Activities $ {16z875.29} {16z875.29}

The accompanying Notes to Financial Statements are an integral part of this statement.

- 34-

FIDUCIARY FUNDS

- 35-

Exhibit - B- 7

BETHLEHEM TOWNSHIP SCHOOL DISTRICTSTATEMENT OF FIDUCIARY NET POSITION

JUNE 30,2014

AgencyFunds

ExpendableTrust Funds

Employee BenefitTrust Fund TOTALS

ASSETS

Cash and Cash Equivalents $ 132,980.75 $ __ ____;1;.o.;8;.;;;.5;;;..;;3.=89_$ 134,834.64

132,980.75 $ 1,853.89 $ 134,834.64Total Assets $

LIABILITIES

Liabilities:Interfund Accounts PayableAccounts PayablePayroll Deductions and WitholdingsStudent Activity reserves

$ 136.74 $ 13.32 $ 150.06

113,311.9819,532.03

113,311.9819,532.03

Total Liabilities $ ==1=:3:::::2i:::,9:::80::::.7:::5= 13.32 132,994.07-------NET POSITION

Reserved for:Unemployment Compensation Insurance 1 840.57 1,840.57

1,840.57 $==1=,8=4=0.=57=Total Net Position $

The accompanying Notes to Financial Statements are an integral part of this statement.

- 36-

Exhibit - B-8

BETHLEHEM TOWNSHIP SCHOOL DISTRICTSTATEMENT OF CHANGES IN FIDUCIARY NET POSITION

FIDUCIARY FUNDSFOR THE YEAR ENDED JUNE 30, 2014

ExpendableTrust Funds

Employee BenefitTrust Fund Totals

ADDITIONS:Deductions from Employees' Salaries $ 8692.40 $ 8,692.40

Total Additions 8692.40 8692.40

DEDUCTIONS:Eligible Benefits 12991.51 12991.51

Total Deductions 12,991.51 12,991.51

Change in Net Position (4,299.11) (4,299.11)

Net Position - Beginning 6 139.38 6 139.38

Net Position - Ending $ 1,840.27 $ 1,840.27

The accompanying Notes to Financial Statements are an integral part of this statement.

- 37-

TOWNSHIP OF BETHLEHEM SCHOOL DISTRICTCOUNTY OFBHUNTERDON, NEW JERSEY

NOTES TO FINANCIAL STATEMENTSJUNE 30, 2014

NOTE 10 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Ao Description of Government-Wide Financial Statements

The government-wide financial statements (i.e., the statement of net position and the statement ofactivities) of the Board of Education (Board) of the Township of bethlehem School District (District)report information on all of the nonfiduciary activities of the primary government only. All fiduciaryactivities are reported only in the fund financial statements. Governmental activities, which normally aresupported by taxes, intergovernmental revenues, and other nonexchange transactions, are reportedseparately from business-type activities, which rely to a significant extent on fees and charges to externalcustomers for support. The District is not financially accountable for any legally separate componentunits, and no component units have been included in the government-wide financial statements.

Bo Reporting Entity:

The Township of Bethlehem School District is a Type II district located in the County of Hunterdon,State of New Jersey. As a Type II district, the School District functions independently through a Board ofEducation. The board is comprised of seven members elected to three-year terms. The purpose of thedistrict is to educate students in grades K-8. High school students (grades 9-12) are enrolled in the NorthHunterdon- Vorhees Regional High School District. The Township of Bethlehem School District had andaily enrollment of 451 students in grades K through 8 at the close of the 2013-2014 school year.

The primary criterion for including activities within the District's reporting entity, as set forth in Section2100 of the GASB Codification of Governmental Accounting and Financial Reporting Standards, iswhether:

~ the organization is legally separate (can sue or be sued in their own name)~ the District holds the corporate powers of the organization~ the District appoints a voting majority of the organization's board~ the District is able to impose its will on the organization~ the organization has the potential to impose a financial benefit/burden on the District~ there is a fiscal dependency by the organization on the District

Based on the aforementioned criteria, the District has no component units. Furthermore, the District is notincludable in any other reporting entity on the basis of such criteria.

Co Basis of Presentation - Government-Wide Financial Statements

While separate government-ide and fund financial statements are presented, they are interrelated. Thegovernmental activities column incorporates data from governmental funds and internal service funds,while business-type activities incorporate data from the government's enterprise funds. Separate financialstatements are provided for governmental funds, proprietary funds and fiduciary funds, even though thelatter are excluded from the government-wide financial statements. As a general rule, the effect ofinterfund activity has been eliminated from the government-wide financial statements.

- 38-

NOTES TO FINANCIAL STATEMENTS

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D)

D. Basis of Presentation - Fnnd Financial Statements

The fund financial statements provide information about the District's funds, including its fiduciaryfunds. Separate statements for each category - governmental, proprietary and fiduciary - are presented.The emphasis of fund financial statements is on major governmental and enterprise funds, with eachdisplayed in a separate column. Any remaining governmental and enterprise funds are aggregated andreported as nonmajor funds. Major individual governmental and enterprise funds are reported as separatecolumns in the fund financial statements.

The District reports the following major governmental funds:

General Fund - The General Fund is the general operating fund of the District. It is used to account forall financial resources except those required to be accounted for in another fund. Included are certainexpenditures for vehicles and movable instructional or noninstructional equipment which are classified inthe Capital Outlay sub fund.

As required by the New Jersey State Department of Education, the District includes budgeted CapitalOutlay in this fund. Generally accepted accounting principles as they pertain to governmental entitiesstate that General Fund resources may be used to directly finance capital outlays for long-livedimprovements as long as the resources in such cases are derived exclusively from unrestricted revenues.

Resources for budgeted capital outlay purposes are normally derived from State of New Jersey Aid,district taxes and appropriated fund balance. Expenditures are those that result in the acquisition of oradditions to fixed assets for land, existing buildings, improvements of grounds, construction of buildings,additions to or remodeling of buildings and the purchase of built-in equipment. These resources can betransferred from and to Current Expense by board resolution.

Special Revenue Fund - The Special Revenue Fund is used to account for the proceeds of specificrevenue from State and Federal Government, (other than major capital projects, Debt Service or theEnterprise Funds) and local appropriations that are legally restricted to expenditures for specifiedpurposes.

Capital Projects Fund - The Capital Projects Fund is used to account for all financial resources to beused for the acquisition or construction of major capital facilities (other than those financed byProprietary Funds). The financial resources are derived from temporary notes or serial bonds that arespecifically authorized by the voters as a separate question on the ballot either during the annual electionor at a special election. State Aid in the form of Economic Development Authority Grants under EFCF Aare also financial resources of this fund

Debt Service Fund - The Debt Service Fund is used to account for the accumulation of resources for, andthe payment of principal and interest on bonds issued to finance major property acquisition, constructionand improvement programs.

Permanent Fund - The Permanent Fund is used to report resources that are legally restricted to theextent that only earnings, and not principal, may be used for purposes that support the District's programs.

- 39-

NOTES TO FINANCIAL STATEMENTS

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D)

D. Basis of Presentation - Fund Financial Statements (Cont'd.)

The District reports the following major enterprise funds:

Food Service Fund - The Food Service Fund is used to account fore the activities of the cafeteria operations of theDistrict.

The District also reports the following fiduciary fund types:

Agency Fund - The Agency Fund is used to account for assets held by the District in a trustee capacityor as an agent for individuals, private organizations, other governments and/or other funds. Agency fundsare custodial in nature and do not involve measurement of results of operations. Agency funds includepayroll and student activities funds.

Employee Benefit Trust (Flexible Spending) - Employee Benefit Trust should be used to reportresources that are required to be held in trust for members and beneficiaries of employee benefit plans.

Private Purpose Scholarship Trust - The Private Purpose Scholarship Trust should be used to report alltrust arrangements under which principal and/or income benefit individuals, private organizations or othergovernments.

During the course of its normal operations, the District will have activity between funds (interfundactivity) for various purposes. Any residual interfund balances at year end are reported as interfundaccounts receivable/payable. While these balances are reported in fund financial statements, certaineliminations are made in the preparation of the government-wide financial statements. Balances betweenfunds included within governmental activities (the governmental and internal service funds) areeliminated so that only the net amount is included as internal balances in the governmental activitiescolumn. Similarly, any interfund balances between business-type (enterprise) funds are eliminated so thatonly the net amount is included as internal balances in the business-type activities columns.

Further, interfund activity may occur during the year involving transfers of resources between funds. Infund financial statements, these amounts are reported at gross amounts as transfers in/out. In thepreparation of the government-wide financial statements, transfers between funds included asgovernmental activities are eliminated so that only net amounts of resources transferred ferom or to thegovernmental activities are reported. A similar treatment is afforded transfers of resources betweenenterprise funds for the preparation of business-type activity financial statements.

E. Measurement Focus and Basis of Accounting

The accounting and financial reporting treatment applied is determined by its measurement focus andbasis of accounting. Measurement focus indicates the type of resources being measured, such as currentfinancial resources or economic resources. The basis of accounting refers to the timing of transactions orevents for recognition in the financial statements.

The government-wide financial statements are reported using the economic resources measurement focusand the accrual basis of accounting. Revenues are recorded when earned and expenses are recorded whena liability is incurred, regardless of the timing of the related cash flows. Property taxes are recognized asrevenues in the fiscal period that the taxes are levied by the municipality(s) within which the District isdomiciled. Ad Valorem (Property) Taxes are susceptible to accrual and under New Jersey State Statute amunicipality is required to remit to its school district the entire balance of taxes in the amount voted uponor certified, prior to the end of the school year. The District recognizes the entire approved tax levy as

- 40-

NOTES TO FINANCIAL STATEMENTS

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D)

E. Measurement Focus and Basis of Accounting (Cont'd.)

revenue in the fiscal period for which they were levied. The District is entitled to receive moneys underan established payment schedule and any unpaid amount is considered to be an "accounts receivable".Grants and similar items are recognized as revenue as soon as all eligibility requirements imposed by theprovider have been met. State categorical aid revenues are recognized as District revenue during the fiscalperiod in which they are appropriated.

The governmental funds financial statements are reported using the current financial resourcesmeasurement focus and the modified accrual basis of accounting. Revenue is recognized when it becomesmeasurable and available. "Measurable" means the amount of the transaction can be determined and"available" means collectible within the current period or soon enough thereafter to be used to payliabilities of the current period. For this purpose, the District considers revenues to be available if theyare collected within 60 days of the end of the current fiscal period. Expenditures are generally recordedwhen a liability is incurred, as under accrual basis accounting. Exceptions to this general rule includedebt service, for which interest and principal expenditures in the Debt Service Fund are recognized ontheir due dates, and expenditures relating to compensated absences, claims and judgments, which arerecorded in the period when payment becomes due. General capital asset acquisitions are recorded asexpenditures in the governmental funds and are not capitalized. The issuance of long-term debt for capitalpurposes and capital lease obligations incurred to acquire general capital assets are reported as "otherfinancing sources".

The District records the entire approved tax levy as revenue (accrued) at the start of the fiscal year, sincethe revenue is both measurable and available. Entitlements are recorded as revenue when all eligibilityrequirements, including timing of funding appropriations, are met, subject to the 60-day availabilityrequirement for collection. Interest and tuition revenues are considered susceptible to accrual and havebeen recognized as revenues of the current fiscal period, subject to availability. Expenditure driven grantrevenues are recorded as qualifying expenditures are incurred and all other eligibility requirements havebeen met, subject to availability requirements. All other revenue items are considered measurable andavailable only when cash is received by the District.

The District's proprietary funds, employee benefit trust fund and private purpose scholarship trust fundsare reported using the economic resources measurement focus and the accrual basis of accounting. Theagency fund has no measurement focus but utilizes the accrual basis of accounting for reporting its assetsand liabilities.

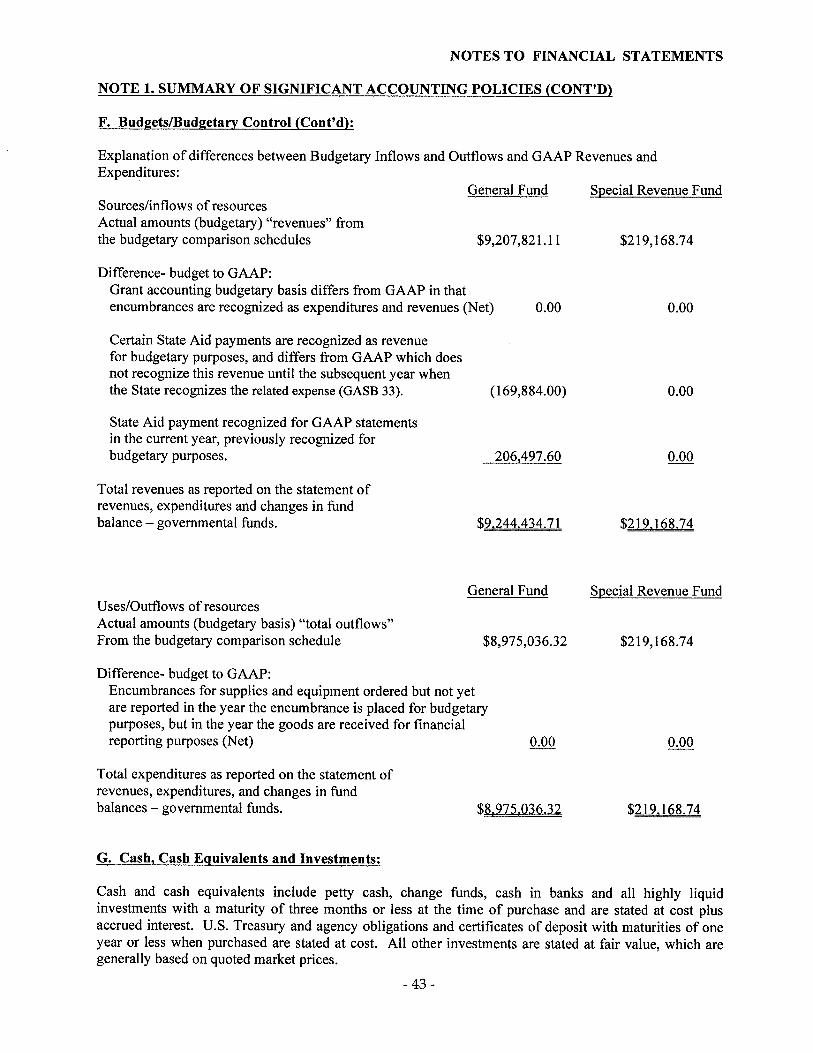

F. Budgets/Budgetary Control:

Annual budgets are adopted for the general, special revenue and debt service funds using a regulatorybasis of accounting which differs from generally accepted accounting principles in one material respect;Budgetary revenues for certain nonexchange state aid transactions are recognized for budgetary purposesin the fiscal period prior to the period in which the state recognizes expenditures/expenses. The amountsof the adjustments needed to reconcile the budgetary basis to the GAAP based fund financial statementsis set forth in the explanation of differences schedules which follow.

- 41-

NOTES TO FINANCIAL STATEMENTS

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONT'D)

F. Budgets/Budgetary Control: (Cont'd.)

Annual appropriated budgets are prepared in the spring of each year for the general, special revenue, anddebt service funds. The budgets are submitted to the county office for approval. Pursuant to changes inthe Local District School Budget Law, statutorily conforming base budgets of Districts with annualschool elections held in November (The District has chosen this option) are no longer required to bepresented to the voters for approval on the third Tuesday in April. Budgets are prepared using themodified accrual basis of accounting, except for the special revenue fund as described later. The legallevel of budgetary control is established at line item accounts within each fund. Line item accounts aredefined as the lowest (most specific) level of detail as established pursuant to the minimum chart ofaccounts referenced in N.J.A.C. 6:20-2A.2(m)1. Transfers of appropriations may be made by SchoolBoard resolution at any time during the fiscal year. New Jersey statutes place limits on the Board's abilityto increase budgeted expenditures through the appropriation of previously undesignated fund balance andrequires the District to obtain additional approvals when budgetary transfers, measured using theadvertised budgetary account totals rather than line-item totals, exceed certain thresholds. The Board ofEducation did not make any supplemental budgetary appropriations during the fiscal year that requiredadditional approvals from oversight agencies.