Embed Size (px)

Citation preview

RBC Capital Markets, LLCBulent Ozcan, CFA (Analyst)(212) [email protected]

Sector: Brokers, Asset Managers & Exchanges

OutperformNYSE: SCHW; USD 29.21

Price Target USD 38.00Scenario Analysis*

DownsideScenario

23.0020%

CurrentPrice

29.21

PriceTarget

38.0031%

UpsideScenario

44.0051%

*Implied Total Returns

Key StatisticsShares O/S (MM): 1,305.8Dividend: 0.24

Market Cap (MM): 38,142Yield: 0.8%Avg. Daily Volume: 7,146,679

RBC EstimatesFY Dec 2014A 2015E 2016E 2017EEPS, Rpt Diluted 0.95 1.10 1.58 1.82P/Rpt EPS 30.7x 26.6x 18.5x 16.0xEBITDA 2,314.0 2,665.4 3,725.6 4,307.6DPS 0.24 0.24 0.33 0.40Div Yield 0.8% 0.8% 1.1% 1.4%BVPS Basic 8.97 10.27 12.11 14.20P/BVPS 3.26x 2.84x 2.41x 2.06x

EPS, Rpt Diluted Q1 Q2 Q3 Q42014 0.24A 0.23A 0.24A 0.25A2015 0.26E 0.26E 0.27E 0.30E2016 0.39E 0.37E 0.39E 0.42EEBITDA2014 570.0A 569.0A 567.0A 608.0A2015 616.6E 652.0E 655.1E 741.7E2016 903.8E 895.7E 915.6E 1,010.4EAll values in USD unless otherwise noted.

March 26, 2015

The Charles Schwab CorporationInitiating at Outperform: With Ample Catalysts,Expect Strong Earnings GrowthOur view: Charles Schwab stands out as having the strongest franchiseamongst its peers. We believe that its diversified business model willallow the firm to capitalize on numerous secular tailwinds to generateasset growth. Furthermore, the firm is the most asset-sensitive and shouldbenefit disproportionately from higher interest rates. We expect EPS togrow at a CAGR of over 25% over the next three years.

Key points:Our in-depth study of the latest industry dynamics and our extensiveanalysis on the company's interest rate sensitivity leads us to believe thatthat The Charles Schwab Corporation is uniquely positioned to generatestrong earnings growth.

We expect numerous secular trends to contribute to top line expansion:

• Growth of independent RIAs: Schwab is the largest custodian forindependent RIAs. Our analysis indicates that wirehouse departures willaccelerate, with over $64 billion of assets likely to move this year. RIAassets under management are expected to reach $3.4 trillion in 2015.

• Growth of advice-based revenues: We estimate that valuations couldbenefit by $3 to $5 if the company were to increase the percentage ofretail clients' AUM that is receiving advice from 17% to 30%.

• Increase in popularity of ETFs: Passively managed products haveenjoyed increasing demand among investors. Schwab generatesrevenues through management fees, "program fees", and platform fees,among others. PwC expects that industry-wide ETF assets could doubleby 2020 and exceed $5 trillion.

• Introduction of the robo-advisor product: We believe that Schwabcould grow its assets by providing services to the general public whohave been unable to retain professional asset allocation advice.

Furthermore, we expect rising interest rates and cost control efforts tocontribute to margin expansion:

• Higher interest rates could boost earnings and margins: We expectrising interest rates to disproportionately benefit Schwab. We estimatethat a 50 basis points increase in interest rates could add $0.31 per shareto earnings.

• Expense saves could add incrementally to margin expansion: Effortssuch as relocating employees to low-cost locations and back officeefficiency improvements should contribute to margin expansion.

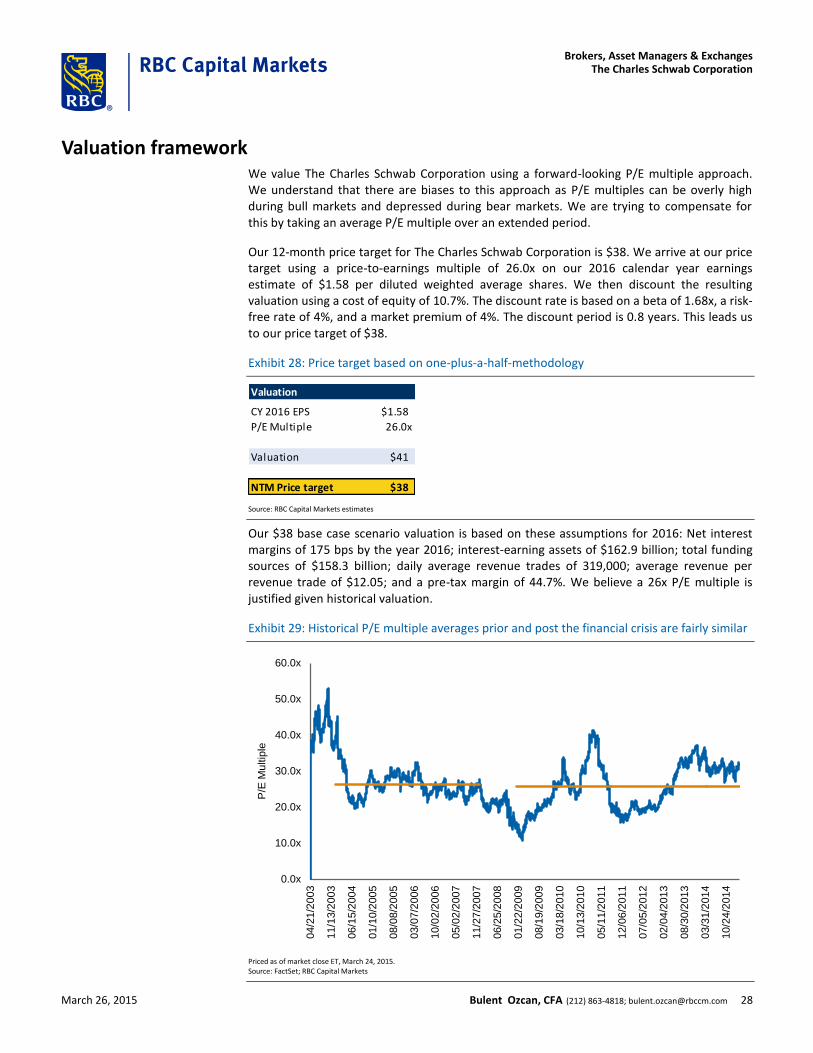

We are modeling pre-tax operating margins of 45% for 2016, up from 35%in 2014. Our above-consensus price target of $38 is based on a 26x P/Emultiple and 2016E EPS of $1.58.

Priced as of prior trading day's market close, EST (unless otherwise noted).For Required Conflicts Disclosures, see Page 47.

Target/Upside/Downside Scenarios

Exhibit 1: The Charles Schwab Corporation

150m

100m

50m

N2012

D J F M A M J J A S O N2013

D J F M A M J J A S O N2014

D J F2015

M

UPSIDE 44.00TARGET 38.00

CURRENT 29.21

DOWNSIDE 23.00

Mar 2016

423732

27

22

17

12

125 Weeks 02NOV12 - 25MAR15

SCHW Rel. S&P 500 COMPOSITE MA 40 weeks

Source: Bloomberg and RBC Capital Markets estimates for Upside/Downside/Target

Target price/base caseOur 12-month price target for SCHW is $38. We arrive at ourprice target using a price-to-earnings multiple of 26.0x on our2016 calendar year earnings estimate of $1.58 per dilutedweighted average shares. We then discount the resultingvaluation using a cost of equity of 10.7%.

Our base case scenario valuation is based on theseassumptions for 2016: Net interest margins of 175 basis pointsby 2016; interest-earning assets of $162.9 billion; total fundingsources of $158.3 billion; daily average revenue trades of319,000; average revenue per revenue trade of $12.05; and apre-tax margin of 44.7%.

Upside scenarioOur valuation is $44 based on 2016 EPS of $1.69 and a price-to-earnings multiple of 28.0x.

Our upside scenario valuation is based on these assumptionsfor 2016: Net interest margins of 189 basis points by 2016;interest- earning assets of $162.9 billion; total funding sourcesof $158.3 billion; daily average revenue trades of 321,000;average revenue per revenue trade of $12.05; and a pre-taxmargin of 46.3%.

Downside scenarioOur valuation is $23 based on 2016 EPS of $1.47 and a price-to-earnings multiple of 17.0x.

Our downside scenario valuation is based on theseassumptions for 2016: Net interest margins of 160 basis pointsby 2016; interest-earning assets of $162.9 billion; total fundingsources of $158.3 billion; a daily average revenue trades of317,000; average revenue per revenue trade of $12.05; and apre-tax margin of 43.1%.

Investment summaryWe are rating the shares of The Charles Schwab Corporationat Outperform, as we believe that the firm's diverse businessmodel allows it to capitalize on numerous opportunities togrow earnings.

Potential Catalysts• Growth of independent RIAs: Schwab is the largest

custodian to independent RIAs. Our analysis indicates thatwirehouse departures will accelerate, with over $64 billionof assets moving this year.

• Growth of advice-based revenues: We estimate thatvaluations could benefit by $3 to $5 if the company were toincrease percentage of retail clients' AUM that is receivingadvice from 17% to 30%.

• Increase in popularity of ETFs: Schwab generates revenuesthrough management fees, "program fees", and platformfees among others. PwC expects that industry-wide ETFassets could double by 2020 and exceed $5 trillion.

• Introduction of the robo-advisor product: We believe thatSchwab could grow its assets by providing services tothe general public, which has not been able to retainprofessional asset allocation advice.

• Higher interest rates could boost earnings and margins:We expect rising interest rates to disproportionately benefitSchwab. We estimate that a 50 basis points increase ininterest rates could add $0.31 per share to earnings.

• Expense saves could add incrementally to marginexpansion: Efforts such as relocating employees to low costlocations and back office efficiency improvements shouldcontribute to margin expansion.

Risks:• Prolonged period of low interest rates could lead to a decline

in net interest margins and earnings.• Unforeseen regulatory changes could impact growth and

profitability.• Increased competition could lead to balance sheet growth

below our expectation and earnings shortfall.• Losses from credit exposure could negatively impact

earnings.• Drop in consumer confidence and equity markets could

negatively impact trading revenues and fee-based earnings.

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 2

Key questions

Our view

1. Given Schwab’s size, can the company continue growing assets at a fast pace?

We believe that Schwab can continue to grow its balance sheet and add client assets at an attractive pace. We think that there are certain secular trends that could support our assertion. We expect that advisors could leave wirehouses at an accelerated rate, favoring open architecture. We expect demand for exchange traded funds (ETFs) to increase. We believe that Schwab should be able to gain traction with some of the new products it has been working on, such as ETF-based 401k plans or the firm’s “robo-advisor” that is going to be rolled out in 1Q/15 (see section on “innovative operator” beginning on page 5).

2. How should investors think about the firm’s interest rate sensitivity?

Schwab is by far the most asset-sensitive name among the discount brokers. About 75% of the assets are sensitive to movements in short-term rates. We estimate that the elimination of money market fee waivers alone could add about 16 cents to earnings. That is equal to 17% of the firm’s 2014 earnings per diluted share. Furthermore, Schwab earns a net interest margin on assets on its balance sheet. We would expect net interest margins to widen as interest rates move higher. We estimate this could add another $0.15 for a 50-bps move in rates. Thus, earnings could increase by over 30% for a 50-bps increase in interest rates. Furthermore, we would expect asset sensitivity to increase from recent changes enacted to sweep account thresholds. Schwab is now routing money coming to the broker–dealer onto its balance sheet at an increased rate. This decision is expected to add about $6 billion to Schwab’s balance sheet in 2015 alone. We believe an improving interest rate environment could significantly alter the value proposition. Our economists expect yield on the three-month treasury bill to increase from 0.04% in 2014, to 0.90% in 2015, and to further increase to 2.80% in 2016.

3. Are there any regulatory headwinds investors should be concerned about?

We believe that some of the most significant regulatory changes have already taken place. The SEC has provided new rules in respect to money market funds, which worked out in Schwab’s favor. The company has disclosed its expectation around the impact of the new Liquidity Coverage Ratio rules on its earnings—which is about half a penny per year.

4. How well does the company manage its balance sheet and its credit exposure?

We believe that the management team has been a good steward of capital. The ratio of non-performing assets to average loans and real estate owned has fluctuated around 50 basis points since 2009, peaking at 68 basis points in 2010. This ratio has declined further in 2014. As of December 31, 2014, outstanding mortgage and home equity loans were about $11 billion. We would not expect a sharp increase in default rates and thus see credit risk as not significant.

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 3

Table of contents

An innovative operator with multiple levers to generate asset growth, we expect strong top line growth .......................................................................................................... 5

Well positioned to take advantage of growth of independent RIAs ................................... 6

Advisory opportunity to deepen share of wallet; could add $3 to $5 to valuation ............ 9

Growth in usage of ETFs could boost asset growth at Schwab ......................................... 10

Robo-advisors could help the firm grow assets by focusing on an untapped market ...... 14

Concluding thoughts on ability to grow assets ................................................................. 15

We expect incremental contributions to earnings growth and margin expansion from rising interest rates and efforts to control costs ................................................................. 19

We expect rising interest rates to benefit Schwab’s earnings more than that of its peers ................................................................................................................................. 19

Expense saves could add to the bottom line and help expand margins ........................... 23

Where we could be wrong ................................................................................................. 27

Interest rate sensitivity could be a headwind, compressing net interest margins, if rates do not rise ................................................................................................................ 27

Given reliance on offices and infrastructure, required investments could lead to lower margins ................................................................................................................... 27

Schwab is under the supervision of a number of regulators putting the company at a disadvantage with respect to capital deployment ......................................................... 27

Valuation framework ......................................................................................................... 29

Risks and price target impediments ................................................................................... 31

Quick overview of Charles Schwab Corp. ............................................................................ 32

Revenue break-down ......................................................................................................... 35

Sources of revenue ........................................................................................................... 35

Business segments ............................................................................................................ 36

Products ............................................................................................................................. 38

Distribution ........................................................................................................................ 41

Competitors ....................................................................................................................... 42

History................................................................................................................................ 43

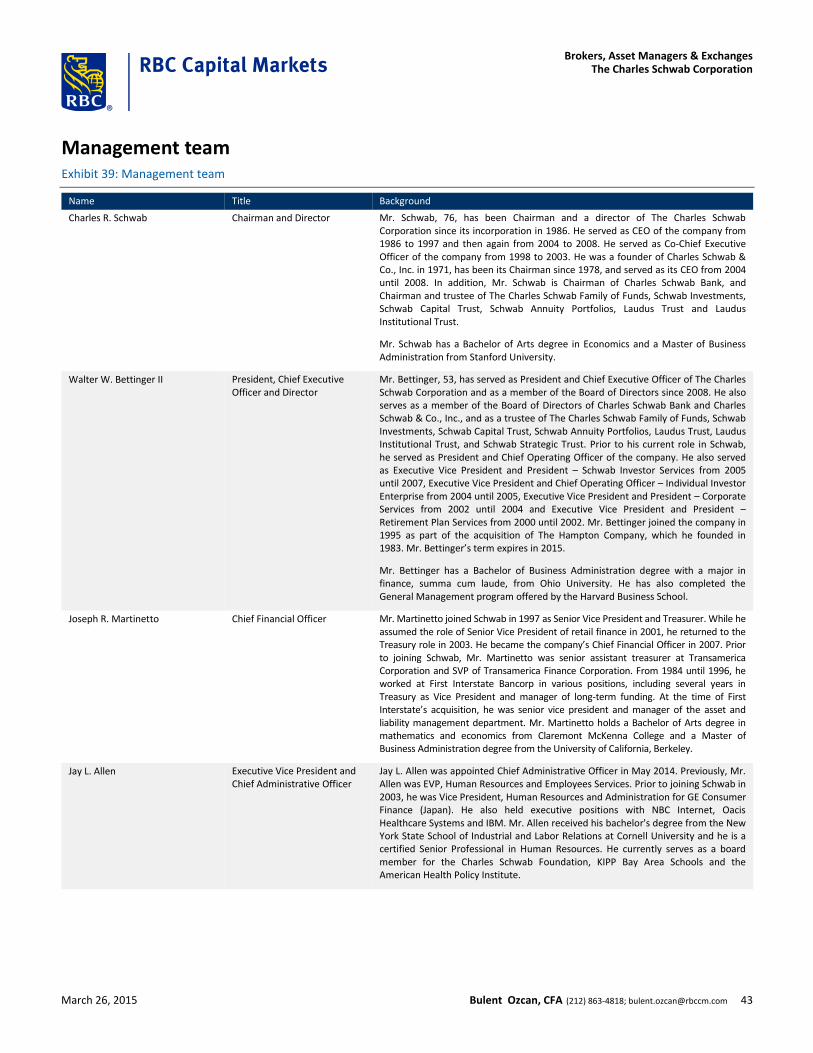

Management team ............................................................................................................. 44

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 4

An innovative operator with multiple levers to generate asset growth, we expect strong top line growth

Having built the most diverse business model among its peers, we believe that Schwab has multiple opportunities it can capitalize on to grow assets. Today, Schwab offers a full range of services, including wealth management, securities brokerage, banking, money management, and financial advisory services. It serves individual investors, as well as institutional clients. The firm has been an early adopter of technology and management seems comfortable with exploring new venues of revenues in order to remain relevant. While commissions were the main driver of earnings in the past, today, about half of the client assets are under some form of fee-based advisory relationship.

The table below compares the breadth of Schwab’s offerings versus those of its peers.

Exhibit 2: Charles Schwab offers a wide range of services and products

SCHW AMTD ETFC

Brokerage

Full range of investment products

Third-party research

In-house research

Mutual funds

Proprietary funds

Third-party funds

Exchange Traded Funds

Proprietary funds

Third-party funds

Advice - In-House

Investment advice

Tailored portfolio construction

Portfolio management

Separately managed accounts

Financial consultants 1,200 ~700 300

RIA relationships 7,000 ~5,000

Number of branches 325+ 105 30

Corporate services

Retirement plans (401k)

Equity compensation plans

Banking services

Full service bank

Trust

Custody services

Administrative trustee services

Source: Company reports, RBC Capital Markets

The firm has built a diversified business, offering more products and services than its peers do

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 5

Clearly, the distinction between services a traditional broker and Schwab can offer is not as clear-cut as it once was. Schwab continues to innovate and be an early adopter of products and technologies management deems worthwhile pursuing. This is exactly why we like the company: Management seems to have created a unique culture of innovation and adaptation, which we deem essential to succeed in a fast-paced industry.

Given Charles Schwab’s strong corporate culture, we would expect the firm to remain innovative and to pursue various opportunities to generate growth. Below are some of these potential opportunities. Please refer to our industry piece for a detailed discussion on current industry themes and drivers.

Well positioned to take advantage of growth of independent RIAs We view the independent RIA market as a meaningful venue of growth for Charles Schwab. We expect record advisor departures from wirehouses in 2015 and estimate that independent RIAs could control $3.4 trillion of assets by the end of this year. This provides multiple opportunities to grow revenues.

While not entirely new, Schwab has been a custodian for 25 years, recent developments bode well for the company. Today, Schwab Advisor Services is the largest custodian, serving more than 7,000 independent registered investment advisors (RIAs) with $1 trillion of assets under their management (as of September 30, 2014). About 1,800 professionals provide custody, trading, and operations support. Their role is to help RIAs focus on their main objective, namely growing their business. A custodian holds the clients’ assets, but can also provide investment products, practice management solutions, back-office technology, and service support.

We believe that wirehouse departures will not only continue, but they can accelerate.

The RIA industry is growing very rapidly as more advisors are leaving the wirehouses either to retain more of the revenues they would otherwise have to share, because they like the open architecture firms such as Schwab can provide, or due to pressure by the wirehouses to eliminate less-profitable clients. Some advisors who have left the wirehouses complain that the push to move “upmarket” makes it less profitable for the advisor to serve mass-affluent clients. Merrill Lynch, for example, is implementing rules in 2015 that will negatively impact brokers’ payouts if they service a large number of affluent client households with under $250,000 in assets. Regulatory changes/scrutiny is also contributing to departures. Some advisors do not like the additional compliance and administrative burdens that come with being part of a wirehouse.

According to InvestmentNews, advisor-move activity is expected to pick up in 2015 should the economy continue to recover. Investment News projects that there will be an increase in the assets moving by an average of about 15%. Thus, assuming that the same ratio of advisors decide to leave the wirehouse channel as in 2014 to become independent (vs. moving to another wirehouse), there could be a record $64.3 billion of assets these advisors could take with them in 2015. The exhibit below shows. Assuming that Schwab’s market share of the RIA custody market is about 45%, as per Bernie Clark who is the executive vice president of Schwab Advisor Services, we calculate that the move by wirehouse advisors could add another $29b of new client assets.

We believe that breakaway brokers represent a very appealing opportunity, as Schwab is the largest custodian for independent RIAs

We estimate that breakaway brokers could add about $29 billion to Schwab’s net client assets in 2015

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 6

Exhibit 3: Wirehouse departures could accelerate in 2015 ($ in billion)

$27.1

$35.7

$62.6 $58.7

$55.9

$64.3

0%

10%

20%

30%

40%

50%

60%

70%

80%

$0

$10

$20

$30

$40

$50

$60

$70

$80

2010 2011 2012 2013 2014 2015E

Amount of Total AUM Leaving Wirehouses As % of Total AUM Moving

Source: InvestmentNews; RBC Capital Markets estimates

In addition, existing RIAs are growing their practices faster and adding assets, which helps discount brokers. RIA assets grew by 19.2% in 2013, following an increase of 15.5% in 2012, according to InvestmentNews. While some of the growth was attributable to movements in the markets, a larger portion of the growth seems to have been driven either by new assets that the RIAs did not manage before or by an increase in the assets provided by their existing clients. About 45% of the new assets were from new clients and another 16% were from existing clients in 2013. As a comparison, about 39% of new assets were from new clients and 22% of assets were from existing clients in 2012.

We estimate that the assets managed by RIAs were about $2 trillion by the end of 2012. Assuming a 19.2% growth in 2013, assets would have been around $2.4 trillion. Using the same assumptions for 2014 and 2015, we would expect RIA assets under management to be around $3.4 trillion by the end of 2015.

Exhibit 4: Assets managed by RIAs could reach $3.4 trillion by 2015 ($ in trillion)

$2.0

$2.4

$2.8

$3.4

$-

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

2012 2013 2014E 2015E

Source: InvestmentNews; RBC Capital Markets estimates

Is the 19.2% growth assumption reasonable? We believe so and think that this estimate could be somewhat conservative if we assume that the growth rate for all RIAs corresponds

Existing RIAs continue to grow their client assets, with over a third of these assets coming from new clients

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 7

to what the top 50 RIAs have been able to achieve. Data collected by InvestmentNews shows that the AUM grew at a CAGR of 23% over the past two years for the top 50 fee-only RIAs. While assets stood at $277.8 billion in 2012, that figure increased to nearly $416.9 billion by 2014.

Exhibit 5: Fee-only RIAs are managing more assets than a few years ago ($ in millions)

$277,767

$310,579

$416,855

$-

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

2012 2013 2014

Total AUM of the top 50 fee-only RIAs

Source: InvestmentNews; RBC Capital Markets

The increase in assets managed by RIAs could benefit the discount brokers as they act as custodians for them. The exhibit below shows a ranking by number of RIA clients. Schwab serves more independent RIAs than any of its competitors.

Exhibit 6: SCHW is the top custodian based on number of RIA relationships (2014)

($ in billion)

# of RIA

clients

RIA Assets in

Custody

Schwab Advisor Services 7,000 $1,081.0

TD Ameritrade Institutional 4,500 $300.0

Fidelity Institutional Wealth Services 2,948 n/a

Trade-PMR Inc. 1,525 n/a

Interactive Brokers 1,388 $150.0

Shareholders Service Group 1,255 n/a

Scottrade Advisor Services 1,100 n/a

Pershing Advisors Solutions 562 $106.4

Folio Institutional 325 n/a

Raymond James Investment Advisors Division 285 $100.0

LPL Financial LLC 282 $78.0

Source: InvestmentNews; RBC Capital Markets

Schwab, as the largest custodian for independent RIAs, stands to benefit from growth in RIA assets

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 8

Discount brokers do not usually charge custodian fees. Nonetheless, the firms can generate revenues as they are charging trading commissions, earning fees when an ETF is part of a customer’s model portfolio the company runs (advisory fees), and charging sales commissions. The ETF provider also pays a platform fee to be on the discount broker’s platform.

There is also room to grow by focusing on existing relationships. The firm’s share of wallet of its RIA assets is about 45% at this point and Schwab is keen to grow this. These RIAs are using multiple custodians. The firm should be able to get more of the assets by eliminating the need to have multiple custodians. There could be a benefit to the RIA to deal with one custodian, but the RIA has to be comfortable with the product offering, service, and counterparty risk. We believe that Schwab can address these concerns over time.

Advisory opportunity to deepen share of wallet; could add $3 to $5 to valuation We believe there is a significant opportunity to generate advice-based revenues from retail clients by increasing the share of wallet from currently 17% to the industry standard of 30%.

Currently, Schwab manages about $183 billion of retail client assets under an advisor relationship. Thus, only about 17% of the current retail clients’ AUM receive some sort of advice. This compares to about 30% to 35% for the wirehouses. Put differently, we believe there is an opportunity to gain some of the 83% of assets that are currently “self-directed”. Assuming that the firm manages to achieve the wirehouse-average of 30% of assets in an advisory relationship, we think there could be a significant opportunity to add to earnings and valuation.

Exhibit 7: Increasing the share of wallet to 30% could add $0.12 to $0.20 to earnings

Assumed incremental margins 35% 40% 45% 50% 55% 60%

Incremental EPS per diluted share @

18% share of wallet $0.01 $0.01 $0.01 $0.01 $0.01 $0.02

19% share of wallet $0.02 $0.02 $0.02 $0.03 $0.03 $0.03

20% share of wallet $0.03 $0.03 $0.03 $0.04 $0.04 $0.05

21% share of wallet $0.04 $0.04 $0.05 $0.05 $0.06 $0.06

22% share of wallet $0.04 $0.05 $0.06 $0.06 $0.07 $0.08

23% share of wallet $0.05 $0.06 $0.07 $0.08 $0.08 $0.09

24% share of wallet $0.06 $0.07 $0.08 $0.09 $0.10 $0.11

25% share of wallet $0.07 $0.08 $0.09 $0.10 $0.11 $0.12

26% share of wallet $0.08 $0.09 $0.10 $0.11 $0.13 $0.14

27% share of wallet $0.09 $0.10 $0.11 $0.13 $0.14 $0.15

28% share of wallet $0.10 $0.11 $0.13 $0.14 $0.15 $0.17

29% share of wallet $0.11 $0.12 $0.14 $0.15 $0.17 $0.18

30% share of wallet $0.12 $0.13 $0.15 $0.16 $0.18 $0.20

@ 50 bps management fees

Source: Company filings; RBC Capital Markets estimates

The above scenario assumes retail AUM of $1,077 billion. Furthermore, we are assuming a 38% tax rate. Applying a 25x P/E multiple on these earnings would add anywhere from $2.89 to $4.95 to valuations by our calculations—this excludes any organic growth.

Schwab can generate revenues in multiple ways when serving as a custodian: Management fees on funds and ETFs, commission revenues, and shelf space fees charged to fund manufacturers are just some examples

The firm could add about $3–$5 per share to its valuation by broadening its advisory relationship with clients from 17% to an industry average of 30%

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 9

Exhibit 8: At 30% share of wallet, valuations could improve between $3 to $5

Assumed incremental margins 35% 40% 45% 50% 55% 60%

Incremental EPS per diluted share @

18% share of wallet $0.22 $0.25 $0.29 $0.32 $0.35 $0.38

19% share of wallet $0.44 $0.51 $0.57 $0.63 $0.70 $0.76

20% share of wallet $0.67 $0.76 $0.86 $0.95 $1.05 $1.14

21% share of wallet $0.89 $1.02 $1.14 $1.27 $1.40 $1.52

22% share of wallet $1.11 $1.27 $1.43 $1.59 $1.74 $1.90

23% share of wallet $1.33 $1.52 $1.71 $1.90 $2.09 $2.28

24% share of wallet $1.55 $1.78 $2.00 $2.22 $2.44 $2.66

25% share of wallet $1.78 $2.03 $2.28 $2.54 $2.79 $3.05

26% share of wallet $2.00 $2.28 $2.57 $2.85 $3.14 $3.43

27% share of wallet $2.22 $2.54 $2.85 $3.17 $3.49 $3.81

28% share of wallet $2.44 $2.79 $3.14 $3.49 $3.84 $4.19

29% share of wallet $2.66 $3.05 $3.43 $3.81 $4.19 $4.57

30% share of wallet $2.89 $3.30 $3.71 $4.12 $4.54 $4.95

@ 50 bps management fees

Source: Company filings; RBC Capital Markets estimates

Growth in usage of ETFs could boost asset growth at Schwab We expect demand for ETFs to increase, providing Schwab with an opportunity to add to its assets under management and revenues. The company offers proprietary and third-party ETFs.

We expect exchange traded funds (ETFs) to continue to gain market share. A recently published study by PricewaterhouseCoopers (ETF 2020 – Preparing for a new horizon) suggests that global ETF assets could grow from $2.6 trillion in 2014 to $5 trillion by 2020. Our own research shows that a majority of active managers were not able to beat their benchmark in 11 out of 13 years under review. We think that ETFs will become increasingly popular and that Schwab should benefit from this trend in multiple ways:

It offers its own proprietary ETFs;

Schwab earns a “program fee” of up to $250,000 for each ETF on its platform that participates in ETF OneSource;

It also earns an annual asset fee of up to 15 basis points on the total ETF asset purchased by customers; and

The firm earns trading commissions when a client buys/sells ETFs that are not on the OneSource platform.

Schwab has a number of proprietary ETFs across three core asset classes (domestic equities, international equities, and bonds). It offers these products in two different flavors: market-cap index ETFs and fundamental index ETFs. These products are offered commission free, but the company generates revenues through management fees. As the exhibit below shows, Schwab’s ETFs are very competitively priced.

PwC expects the ETF market to double in size by 2020 and our research supports this as active managers continue to lag their benchmarks

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 10

Exhibit 9: Schwab’s ETFs are very competitively priced (2014)

Strategy Schwab Vanguard iShares

Multi-cap core 4 bps 5 bps 15 bps

Large-cap core 4 bps 9 bps 7 bps

Large-cap growth 7 bps 9 bps 15 bps

Large-cap value 7 bps 9 bps 18 bps

Equity income 7 bps 10 bps 12 bps

Mid-cap core 7 bps 9 bps 14 bps

Small-cap core 8 bps 9 bps 14 bps

Real estate 7 bps 10 bps 35 bps

Core bond 6 bps 8 bps 8 bps

Inflation protected bond 7 bps 10 bps 10 bps

Short-term US Treasury 8 bps n/a 15 bps

General US Treasury 10 bps 12 bps 15 bps

Source: Company reports; RBC Capital Markets

In addition, Schwab offers a product called Schwab ETF OneSource. This platform allows the firm’s customers to trade about 200 exchange traded funds from 13 providers commission free. The exhibit below compares Schwab’s offering versus its peers.

Exhibit 10: Schwab has the broadest ETF selection among peers (2014)

Schwab E*TRADE AMTD Fidelity

Commission free ETFs 198 108 101 76

# of ETF providers 13 3 9 2

Morningstar categories covered 64 37 44 51

Source: Company reports; RBC Capital Markets

As active managers underperform their benchmark, we would expect Schwab to be a beneficiary of increased demand for passive strategies We would expect continued growth in the usage of exchange traded funds and indexed funds. As we have outlined in our industry note, we are continuing to see a majority of active asset managers underperform their benchmark. Performance in 2014 seems to have gotten worse, not better.

Exhibit 11: Active managers continued to underperform in 2014

ALL US open-ended funds

Nov-13 Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14# of funds beating benchmark 2550 2598 2522 2599 2524 2457 2318 2530 2416 2397 2315 2213 2083# of funds with data 5904 5959 5964 5968 5972 5977 5979 5985 5987 5989 5995 5996 5995% of funds beating benchmark 43.2% 43.6% 42.3% 43.5% 42.3% 41.1% 38.8% 42.3% 40.4% 40.0% 38.6% 36.9% 34.7%

ALL US open-ended FIXED INCOME funds

Nov-13 Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14# of funds beating benchmark 545 528 466 473 484 463 464 582 592 601 589 509 453# of funds with data 1023 1033 1034 1035 1036 1036 1036 1036 1038 1038 1040 1041 1039% of funds beating benchmark 53.3% 51.1% 45.1% 45.7% 46.7% 44.7% 44.8% 56.2% 57.0% 57.9% 56.6% 48.9% 43.6%

ALL US open-ended EQUITY funds

Nov-13 Dec-13 Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14# of funds beating benchmark 1555 1608 1620 1672 1609 1567 1398 1366 1207 1098 1043 1039 979# of funds with data 3174 3197 3200 3202 3204 3208 3210 3215 3215 3216 3217 3217 3219% of funds beating benchmark 49.0% 50.3% 50.6% 52.2% 50.2% 48.8% 43.6% 42.5% 37.5% 34.1% 32.4% 32.3% 30.4%

Note: 1-year returns ending in the month. Benchmark used is the primary prospectus benchmark for each fund. Actively managed US mutual funds, ex-index funds. Fund returns exclude sales charges, but include management, administrative, and 12b-1 fees. Source: Morningstar, RBC Capital Markets

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 11

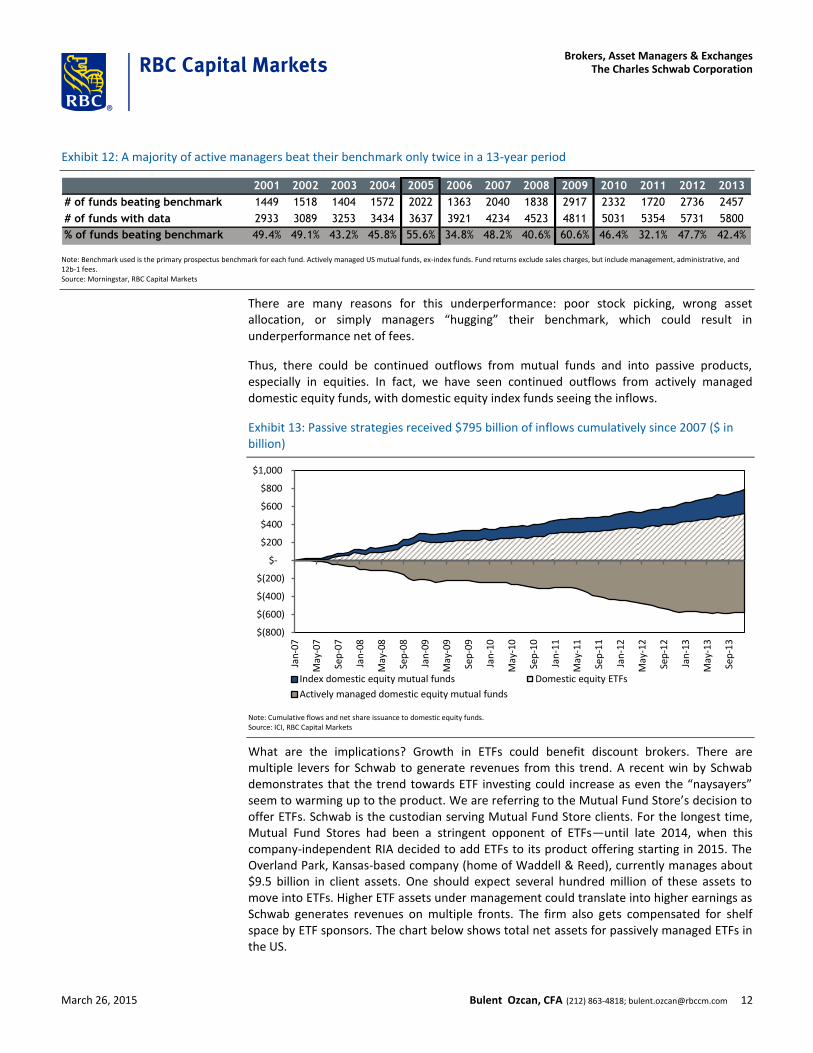

Exhibit 12: A majority of active managers beat their benchmark only twice in a 13-year period

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

# of funds beating benchmark 1449 1518 1404 1572 2022 1363 2040 1838 2917 2332 1720 2736 2457

# of funds with data 2933 3089 3253 3434 3637 3921 4234 4523 4811 5031 5354 5731 5800

% of funds beating benchmark 49.4% 49.1% 43.2% 45.8% 55.6% 34.8% 48.2% 40.6% 60.6% 46.4% 32.1% 47.7% 42.4%

Note: Benchmark used is the primary prospectus benchmark for each fund. Actively managed US mutual funds, ex-index funds. Fund returns exclude sales charges, but include management, administrative, and 12b-1 fees. Source: Morningstar, RBC Capital Markets

There are many reasons for this underperformance: poor stock picking, wrong asset allocation, or simply managers “hugging” their benchmark, which could result in underperformance net of fees.

Thus, there could be continued outflows from mutual funds and into passive products, especially in equities. In fact, we have seen continued outflows from actively managed domestic equity funds, with domestic equity index funds seeing the inflows.

Exhibit 13: Passive strategies received $795 billion of inflows cumulatively since 2007 ($ in billion)

$(800)

$(600)

$(400)

$(200)

$-

$200

$400

$600

$800

$1,000

Jan

-07

May

-07

Sep

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Sep

-13

Index domestic equity mutual funds Domestic equity ETFs

Actively managed domestic equity mutual funds

Note: Cumulative flows and net share issuance to domestic equity funds. Source: ICI, RBC Capital Markets

What are the implications? Growth in ETFs could benefit discount brokers. There are multiple levers for Schwab to generate revenues from this trend. A recent win by Schwab demonstrates that the trend towards ETF investing could increase as even the “naysayers” seem to warming up to the product. We are referring to the Mutual Fund Store’s decision to offer ETFs. Schwab is the custodian serving Mutual Fund Store clients. For the longest time, Mutual Fund Stores had been a stringent opponent of ETFs—until late 2014, when this company-independent RIA decided to add ETFs to its product offering starting in 2015. The Overland Park, Kansas-based company (home of Waddell & Reed), currently manages about $9.5 billion in client assets. One should expect several hundred million of these assets to move into ETFs. Higher ETF assets under management could translate into higher earnings as Schwab generates revenues on multiple fronts. The firm also gets compensated for shelf space by ETF sponsors. The chart below shows total net assets for passively managed ETFs in the US.

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 12

Exhibit 14: ETF assets under management have grown at a CAGR of 22.7% since 2005

276 382

547 465

686

886 934

1,201

1,474

1,735

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

AU

M (

$B

)

Passively Managed, Long-term ETF AUM

Source: Morningstar; RBC Capital Markets

Consider this: While assets under management have grown at a compounded growth rate of 22.7% since 2005, assets for actively managed US open-ended funds have grown at a rate of 8.5% for the same time period. As of the end of 2014, ETFs composed about 15% of the combined assets. We believe there is further growth momentum.

There has been an increase in exposure to ETFs and there is further growth potential among existing users. Schwab’s 2014 ETF Investor Study found that ETFs make up only about 18% of the assets of investors who hold them in their portfolios. As a comparison, a 2008 study found that while 80% of RIAs owned ETFs, the average exposure to ETFs was only 10%. As for the future, about half of all investors think that ETFs will be a larger portion of their total portfolio. And an earlier study done by Schwab in 2013 (Independent Advisor Outlook Study – Fall 2013) concluded that 55% of the RIAs think that future client investment interest will focus on low-cost index funds and ETFs. We think the writing is on the wall.

Despite the company’s size and its diverse product offerings, Schwab continues to introduce new products to capitalize on the ETF opportunity. For instance, the company launched Schwab Index Advantage 401(k) plans in 2012. This product combines internal and external, low-cost index funds with third-party investment advice services. Two years later, in 2014, the company built upon this platform and introduced a second version of this product using ETFs only. This is yet another example of a disruptive product that the company launched. Certainly, there are intense discussions among pension consultants whether having an ETF in a 401(k) plan makes sense as there is potential for tracking error and no need for intraday liquidity. Some think that employers will not add ETFs to their 401k offering if the consultants do not recommend those. After all, revenue-sharing helps to pay for the costs of operating a pension plan. ETFs would not provide such arrangements or not to the same degree as actively managed mutual funds, i.e., there is less of an incentive for pension consultants to include ETFs in a pension plan. This is the kind of idea that could once again change the status quo. Certainly, others have introduced similar products. TD Ameritrade’s product gives plan participants the choice between mutual funds and ETFs. However, given Schwab’s marketing power and its ability to cut fees, we would expect increased demand for a low-cost retirement product offering. Assuming an employee works and saves over the next 40 years, a reduction in fund expenses could significantly boost returns.

The firm has come a long way despite entering the ETF space late. Schwab introduced its first ETFs in 2009 and had $200 million of assets under management (AUM) as of December 2009.

Schwab continues to introduce products most industry participants would consider disruptive – such as ETF-based 401k plans and a “robo-advisor”

Despite recent growth, we estimate that ETFs comprise about 15% of total retail assets in the US. We believe there is room for growth

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 13

The industry had about $690 billion of AUM at that point. Today, Schwab manages about $27 billion of assets in its proprietary exchange traded funds. This shows the power of distribution, especially since its competitors have been claiming that their ETFs would not sell as they did not have the liquidity needed to succeed. The 401k industry is about $3.2 trillion in size and Schwab has a 3.1% market share. Close to 100% of the assets are currently in the company’s traditional 401k plans. There is certainly an opportunity for growth, despite the firm’s limited target market of plans with $20m to $1 billion of plan assets.

Robo-advisors could help the firm grow assets by focusing on an untapped market We view the robo-advisor product as an opportunity to tap a new market: We believe that Schwab could grow its assets by providing services to the general public who have been unable to retain professional asset allocation advice.

Another product that could significantly alter the current landscape are robo-advisors. Robo-advisors are online portfolio management tools that help determine an optimum asset allocation strategy relying on algorithms and Modern Portfolio Theory. We believe that this product will allow Schwab to target a new client base that it had not previously, namely parts of the mass market and the middle market. Schwab believes that this is a $400 billion market. We believe that this could be a conservative assumption given that households with investable assets of less than $500,000 hold combined assets of $7 trillion. We view this opportunity as an option and do not incorporate associated earnings into our model.

We are optimistic about this product as early surveys point to a high uptake rate. Charles Schwab provided some context during its 2015 Winter Business Update. About 83% of the company’s retail assets are currently self-directed. Management stated that it has been to 15 branches since the beginning of this year and that there is significant interest in Schwab’s robo-advisor. About half of the financial consultants management met with stated that they have won clients from competing firms in anticipation of enrolling in Schwab’s robo-advisor called “Schwab Intelligent Portfolios” (SIP).

Schwab is currently introducing SIP to its retail clients, and will roll out to RIAs shortly thereafter. It offers a number of exchange traded funds to customers to construct their portfolios. This product will be an RIA offering (RIA advisory account vs. brokerage account), meaning that it will be a fiduciary-based product. In fact, management stated that only one of the ETFs it offers on Schwab ETF OneSource passes the screen to be on this platform.

The firm will not charge advisory fees, trading commissions, or account-servicing fees. However, the firm will earn fund-management fees on Schwab’s proprietary ETFs, platform revenues from ETF providers, and will be able to earn a yield on cash balances held by clients. The ultimate goal is to attract new clients outside its core baby boomer base, namely, Generation X and Millennial clients. This product is important, as it should allow the firm to move “down-market”, targeting less-affluent clients.

Sure, Schwab is not the first firm to offer this technology. However, we would expect an increased adoption rate among consumers once Charles Schwab puts its marketing machine into gear. We would expect Schwab to surpass competitors in terms of AUM given the firm’s relationship with over 7,000 independent RIAs who manage about $2.4 trillion in assets.

We believe that the impact of technology on financial advisors could be similar to that of exchange traded funds on active managers. Will robo-advisors put human advisors out of work? We do not believe so, but they will have to work harder to retain assets if they are

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 14

targeting the mass-affluent segment. There could also be fee pressure unless human advisors can demonstrate that they are providing genuine value-added services. However, advisors who are merely in the asset gathering business could lose assets as investors could use Schwab’s robo-advisor to construct an auto-balancing portfolio based on their individual risk profile and investment horizon. We believe some advisors will have to rethink their approach and refocus on providing value-added advice. Based on Schwab’s Independent Advisor Outlook Study, which was given to 720 advisors and published June 2014, 56% of the advisors responded that they believe robo-advisors can supplement their current offer/help grow their business. The remaining 44% see robo-advisors as a threat to their business.

Concluding thoughts on ability to grow assets We do not believe that Charles Schwab’s ability to grow assets is constrained by the firm’s size. In fact, we would expect strong growth given secular tailwinds.

A key question on investors’ minds is whether the firm will be able to grow assets as it is already the largest discount broker by a wide margin. Our answer would be yes and, as we stated at the beginning of this note, it all comes down to the company’s culture. We believe that the company has demonstrated, over time, that it is willing to explore new opportunities and navigate uncharted waters in pursuit of profit. The organization is constantly evolving and innovation remains a key driver of the firm’s success. Charles Schwab seems to have a very good understanding of consumer behavior and market dynamics – and is willing to adapt to these changes in order to capitalize on the opportunity set. However, management is not taking a “risk it all” approach. It is content with being an early adopter, as demonstrated above, if the long-term growth opportunity justifies the investment. We think the company’s culture reflects this, and believe that it provides the appropriate mix of entrepreneurial spirit and risk management.

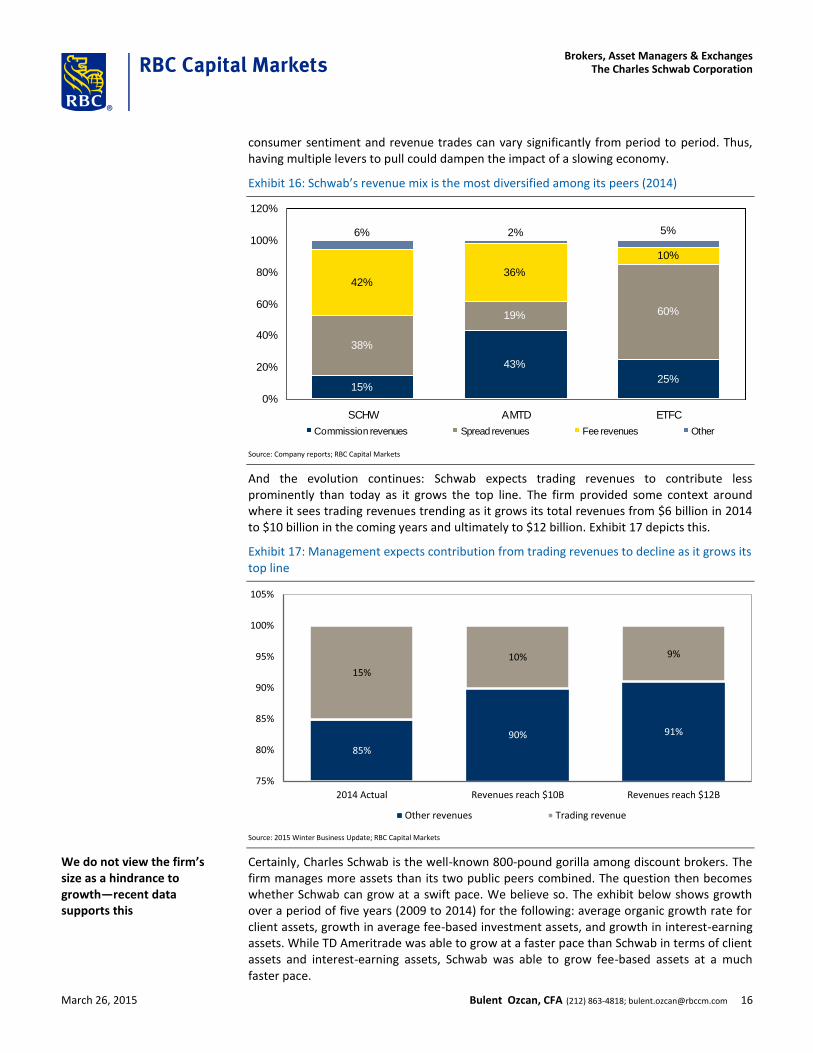

The exhibit below shows the evolution of Schwab in pursuit of opportunities. While trading contributed to total revenues to the tune of 40% a decade ago, commissions comprise only about 15% of total revenues today.

Exhibit 15: Today, Schwab is less dependent on commission revenues than ever

39% 40%

15%

49%

21%

38%

7%

27% 42%

12%

6%4%

0%

20%

40%

60%

80%

100%

120%

1990 2000 2014

Commission revenues Interest revenues Asset management Other

Source: Company filings; RBC Capital Markets

An added benefit of this evolution is that the firm’s diversified revenue mix should provide added downside protection versus its peers. Trading is highly dependent on volatility and

We like the fact that Schwab continues to explore a multitude of opportunities to find catalysts of growth—the firm’s change in revenue mix reflects this effort

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 15

consumer sentiment and revenue trades can vary significantly from period to period. Thus, having multiple levers to pull could dampen the impact of a slowing economy.

Exhibit 16: Schwab’s revenue mix is the most diversified among its peers (2014)

15%

43%

25%

38%

19% 60%

42%36%

10%

2% 5%6%

0%

20%

40%

60%

80%

100%

120%

SCHW AMTD ETFC

Commission revenues Spread revenues Fee revenues Other

Source: Company reports; RBC Capital Markets

And the evolution continues: Schwab expects trading revenues to contribute less prominently than today as it grows the top line. The firm provided some context around where it sees trading revenues trending as it grows its total revenues from $6 billion in 2014 to $10 billion in the coming years and ultimately to $12 billion. Exhibit 17 depicts this.

Exhibit 17: Management expects contribution from trading revenues to decline as it grows its top line

85%

90% 91%

15%

10% 9%

75%

80%

85%

90%

95%

100%

105%

2014 Actual Revenues reach $10B Revenues reach $12B

Other revenues Trading revenue

Source: 2015 Winter Business Update; RBC Capital Markets

Certainly, Charles Schwab is the well-known 800-pound gorilla among discount brokers. The firm manages more assets than its two public peers combined. The question then becomes whether Schwab can grow at a swift pace. We believe so. The exhibit below shows growth over a period of five years (2009 to 2014) for the following: average organic growth rate for client assets, growth in average fee-based investment assets, and growth in interest-earning assets. While TD Ameritrade was able to grow at a faster pace than Schwab in terms of client assets and interest-earning assets, Schwab was able to grow fee-based assets at a much faster pace.

We do not view the firm’s size as a hindrance to growth—recent data supports this

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 16

Exhibit 18: Schwab’s five-year compound annual growth rate versus peers (2009 to 2014)

5%

11%

5%

24%

20%

n/m

16% 17%

-2%-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

SCHW AMTD ETFC

Client assets organic growth Avg. fee based investment balances Avg. Interest rate sensitive assets

Source: Company filings; RBC Capital Markets

What are our expectations for asset growth? We remain optimistic that the firm will continue to grow its balance sheet smartly. Management provided some guidance during its Interim Business Update in October 2014. It expects to add about $12–$15 billion to its interest-earning assets in 2015. Investors were provided with a breakdown of these new assets: $6bn will be due to organic growth of money funds; $3bn–5bn will be added from changing sweep account thresholds for advisors, and $3–4bn will be in potential bulk transfers. Our 2015 earnings estimate incorporates asset growth at the lower end of this guidance, leaving room for a positive surprise. As for 2016, we are assuming that total interest-earning assets could grow by about $13 billion as interest rates rise. The main drivers of asset growth are innovative products that meet clients’ needs and distribution, in our view. Schwab has both. Going back to our ETF example, Schwab did not have a presence in the market in 2009. Today, the firm is a top 8 ETF provider.

However, there are also other initiatives that can add to balance sheet growth. The firm is optimizing how it uses its balance sheet. Schwab recently announced changes to its sweep account option and is now routing more of the new cash from clients onto their balance sheet, as opposed to the broker–dealer business. Previously, if an advisor had client assets of over $100,000, any cash held by the client would qualify to be invested in money market funds. The hurdle rate for retail clients was $500,000, as a comparison. Schwab has raised the limit to use money market funds as a sweep option to $500,000 for clients of its independent advisors. Consequently, the firm expects to direct more cash onto its balance sheet where it currently earns a yield of 160 bps, versus 12 bps on money market funds. The yield of 160 bps could grow to over 300 bps in a normal rate environment. The yield on money market funds is about 55 bps in a normal rate environment.

The firm has raised the threshold for the bank sweep default from advisor services to $500k a month ($1.5bn a quarter), so that it syncs with the retail services. Clearly, the sweep assets that can be invested on its balance sheet are one of the most profitable cash products, with Schwab earning about 145 bps above what it could at the broker–dealer. However, there will be some limitations to growth, as Schwab would have to hold additional capital to support the balance sheet. As a reminder, there are no capital charges for money market funds as these are segregated assets.

As for the future, we expect growth to be driven by smarter usage of its balance sheet, increased cross selling, and introduction of new products

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 17

We expect incremental contributions to earnings growth and margin expansion from rising interest rates and efforts to control costs

We expect rising interest rates to benefit Schwab’s earnings more than that of its peers Schwab is by far the most asset sensitive of the discount brokers. We estimate a 50 bps increase in short term rates could add about $0.31 to earnings per share (33% accretive based on 2014 EPS).

Our Chief US Economist, Tom Porcelli, holds a constructive view on the economy and expects the first Fed hike as early as June. Specifically, he expects the three-month treasury rate to be 90 basis points by the end of 2015 and to increase to 280 basis points by 2016. Likewise, he believes that the rate on the two-year Treasury note could increase from 66 basis points as of the end of 2014 to 200 basis points by the end of 2015 and further to 320 basis points by 2016.

Our Head of US Rate Strategy, Michael Cloherty, holds a similar view and expects rate increases in the near term. More importantly, he expects rate increases to happen gradually over time for the following reasons: First, the Fed needs to learn to use its new tools in an utterly changed regulatory environment. The Fed will be treading carefully in order not to negatively impact the economic recovery. Second, the massive volatility we saw on October 15, 2014 suggests the market will not be able to handle rapid tightening, and as the Fed can't move rapidly without shocking the markets, it will need to start tightening its monetary policy well before inflation appears.

We would be buyers of Schwab under this premise. Our analysis demonstrates that the firm’s earnings are the most sensitive to movements in short-term rates and should benefit disproportionately from rising rates.

To be precise, about 75% of the firm’s assets are sensitive to movements in short-term rates. One of the key drivers of this interest rate sensitivity is money market funds. Charles Schwab is the only discount broker that offers proprietary money market funds to its clients. In fact, Charles Schwab is the seventh largest money market mutual fund manager in the US. As of 4Q/14, the firm was managing close to $168 billion of money market funds. While this exposure has been a hindrance to earnings growth in the current low interest rate environment, we expect the company’s shares to outperform its peers in a rising rate environment.

Consider this: Instead of earning a normalized fee of 58 basis points (bps) on its money market fund assets, the company was able to earn an effective fee rate of only 13 bps during the most recent quarter. Like other money market fund managers, Charles Schwab voluntarily “waived fees” to ensure that investors were not earning a negative yield on the funds. These money market fund fee waivers are material. The exhibit below shows the amount of money market fund waivers over time. The past year stands out with $751 million of revenues that were lost as Schwab reduced its management fees to ensure clients would not experience negative returns on their cash balances.

Our Chief US Economist and our Head of US Rate Strategy both expect the Fed to start tightening its monetary policy at a measured pace this year

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 18

Exhibit 19: Money market fund fee waivers have been increasing since 2009 ($ in millions)

$224

$433

$568 $587

$674

$751

$-

$100

$200

$300

$400

$500

$600

$700

$800

2009 2010 2011 2012 2013 2014

Source: Company filings; RBC Capital Markets

Should short-term interest rates rise, we could see a significant uptick in earnings at Schwab. Unlike asset managers who have been “sharing the pain” with distributors when interest rates declined, Schwab had to absorb the impact of money market fee waivers dollar-for-dollar. Thus, when interest rates start increasing, Schwab should be able to experience accelerated earnings growth relative to asset managers such as Federated Investors (ticker: FII) that will now have to share the incremental management fee revenues with their distributors as interest rates rise. Schwab is the only discount broker among its peers providing proprietary money market funds.

Assuming interest rates rise to pre-financial crisis levels allowing Schwab to earn 58 bps on its money market mutual funds, a 38% tax rate, and no growth in money market fund AUM, we calculate incremental earnings of $0.16 per diluted shares. This estimate is based on an assumption that about 60% of money market fund assets would not have to waive fees, Schwab keeps 25% of the incremental revenues for growth initiatives and invests the capital back into the business. Furthermore, we are using our 2015 projected diluted weighted average share count of 1,327 million shares. As a reference point, Schwab earned $0.95 per diluted share in 2014. Thus, we estimate a rise in interest rates would be accretive to the tune of 17% based on 2014 earnings.

The current rate environment is certainly unusual given historical patterns and not sustainable over the long run, in our view. The exhibit below alludes to this and shows the effective federal funds rate over time. As a reference, this rate was around 5% in 2006 and 2007.

EPS could increase by 16 cents if 60% of money market fund assets were not to waive fees with higher rates

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 19

Exhibit 20: Monetary easing has resulted in record low federal fund rates

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

19

55

19

58

19

61

19

64

19

67

19

70

19

73

19

76

19

79

19

82

19

85

19

88

19

91

19

94

19

97

20

00

20

03

20

06

20

09

20

12

Source: Board of Governors of the Federal Reserve System; RBC Capital Markets

We estimate that a rise of 45 bps in the federal funds rate should result in the elimination of 60 percent of fee waivers.

Money market fund waivers impact asset management and administration fee revenues. However, this is not the only component of revenues that could be positively impacted by rising rates. Net interest revenues contribute to a significant portion of revenues. Broker–dealers are putting clients’ cash to work in a similar fashion to a bank. Discount brokers earn a yield on these “interest-earning assets”. In its 10k filings, the company provided the results of a simulation of changes in interest rates and the impact on net interest revenue. The exhibit below assumes a 100-bps gradual increase/decrease in market interest rates relative to Schwab’s market rates forecast over a 12-month period (base case).

Exhibit 21: Impact on net interest revenue from rising interest rates seems meaningful

11.1% 11.0%

-4.2% -4.5%

-9%

-4%

1%

6%

11%

16%

Sep 30, 2014 Dec 31, 2013

Increase of 100 bps Decrease of 100 bps

Source: Company filings; RBC Capital Markets

We can only assume what the base case assumption is for the firm. Thus, we do not view the sensitivity provided by the firm in its annual filings as useful.

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 20

Our approach to determine Schwab’s interest rate sensitivity Charles Schwab has provided some data points, which we used to come up with our interest rate sensitivity. The company disclosed that a 100-bps increase in rates will add about 60 bps to net interest margins. A further 100-bps increase will add another 60 bps. Assuming average interest-bearing assets of $142.5 billion, the first 100-bps increase would add $855 million of incremental net interest revenue, while a 200-bps increase would add about $1.7 billion of incremental revenue. There seems to be a linear relationship. Hence, if we assume a 50-bps increase in interest rates, net interest revenues could add about $0.32 per diluted share—again, we are using our projected share count of 1,327 million shares. Were we to assume that 75% of this amount flows through to shareholders and a 38% tax rate, we calculate earnings could increase by $0.15 on top of the $0.16 from recouping 60% of money market fund fee waivers. Thus, earnings could pick up by $0.31.

We believe that the impact on earnings from a 50-bps increase will be driven by elimination of money market fund fee waivers and expansion of net interest revenues. Thereafter, net interest revenue will be the main driver of earnings expansion. We show this below.

Exhibit 22: Elimination of fee waivers could meaningfully add to EPS

Assumed marginsMoney Market Funds 70% 75% 80% 85% 90%

2014 Fee waivers ($MM) $751 $751 $751 $751 $751Recovery percentage 60% 60% 60% 60% 60%Fee rate 13bps 13bps 13bps 13bps 13bpsNormalized rate 58bps 58bps 58bps 58bps 58bpsDelta 45bps 45bps 45bps 45bps 45bps

Incremental revenues for 50 bps increase

in rates $451 $451 $451 $451 $451Tax rate 38% 38% 38% 38% 38%Share count (2015E) 1,327 1,327 1,327 1,327 1,327

EPS Impact $0.15 $0.16 $0.17 $0.18 $0.19

Source: Company reports; RBC Capital Markets estimates

The exhibit below shows impact on earnings using various margin and changes in interest rate assumptions:

Elimination of fee waivers could add $0.16 to earnings per diluted share, assuming that the company retains 25% of revenues for growth initiatives

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 21

Exhibit 23: Impact on EPS due to margin expansion

Assumed margins

Net interest revenue 70% 75% 80% 85% 90%

Average interest-earnings assets ($B) $142.5 $142.5 $142.5 $142.5 $142.5

Incremental revenues ($MM) - 50 bps $427.5 $427.5 $427.5 $427.5 $427.5

Incremental revenues ($MM) - 100 bps $854.9 $854.9 $854.9 $854.9 $854.9

Incremental revenues ($MM) - 200 bps $1,709.9 $1,709.9 $1,709.9 $1,709.9 $1,709.9

Tax rate 38% 38% 38% 38% 38%

Share count (2015E) 1,327 1,327 1,327 1,327 1,327

EPS Impact - 50 bps $0.14 $0.15 $0.16 $0.17 $0.18

EPS Impact - 100 bps $0.28 $0.30 $0.32 $0.34 $0.36

EPS Impact - 200 bps $0.56 $0.60 $0.64 $0.68 $0.72

Source: Company reports; RBC Capital Markets estimates

While there are a number of assumptions in our analysis, the main point should not be missed. Rising interest rates will have a significant impact on earnings. Thus, assuming no growth, we estimate elimination of fee waivers and higher net interest revenues could add about $0.31 to earnings. Put differently, 2014 earnings per share could have been 30%-plus higher in a more benign interest rate environment.

The company provided an updated earnings-sensitivity to movements in the Federal Funds rate in February 2015, which seems consistent with our analysis. Management expects the first 100-bps increase to add about $1.6 billion to revenues. It expects a further 100-bps increase to add an incremental $800 million to revenues. Thus, revenues could rise by $2.4 billion for a 200-bps move in the Federal Funds rate without any asset growth. Based on this model, earnings could move about $0.28 for a 50-bps increase in rates, were we to assume a margin of 75%, a 38% tax rate and 1,327 million diluted shares outstanding. While this figure seems slightly more conservative than our own calculation, one should not ignore that $0.28 would still be 29% accretive to 2014 earnings.

Expense saves could add to the bottom line and help expand margins Controlling expenses will continue to remain a priority at Schwab with its clients benefitting in the form of lower fees. Expense savings should lead to increased investments in new products, revenue growth and better margins.

Another driver of margin expansion and earnings growth could be expense saves. We believe that the current efforts to control costs in combination with an increase in revenues could bear fruit over coming years. While the company does not provide specific guidance on the dollar amount of expense saves, it discloses certain efforts. A recent one of these efforts would be the relocation of employees from higher cost locations such as San Francisco to lower cost markets such as Denver, Austin and El Paso. Management indicated that this is a multi-year effort. The goal is to relocate about half of the 2,400 employees that are currently working out of the San Francisco office. There are first signs that the management is moving forward with its plan. The past year’s margins were compressed as the company is altering its geographic footprint. Schwab took a severance charge of $68 million in 3Q/14.

A 50-bps move in short-term rates could add $0.15 to earnings per share; however, should rates move by 200 basis points, investors could see an increase of $0.60 in EPS—assuming 75% incremental margins

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 22

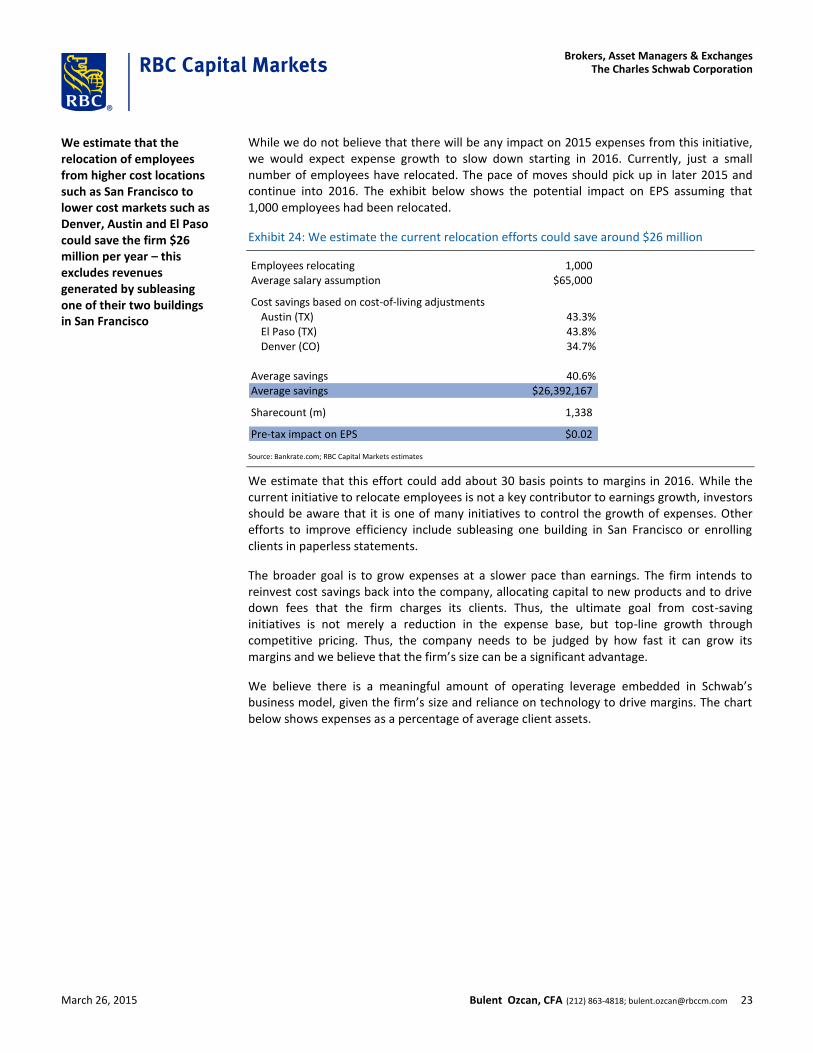

While we do not believe that there will be any impact on 2015 expenses from this initiative, we would expect expense growth to slow down starting in 2016. Currently, just a small number of employees have relocated. The pace of moves should pick up in later 2015 and continue into 2016. The exhibit below shows the potential impact on EPS assuming that 1,000 employees had been relocated.

Exhibit 24: We estimate the current relocation efforts could save around $26 million

Employees relocating 1,000 Average salary assumption $65,000

Cost savings based on cost-of-living adjustmentsAustin (TX) 43.3%El Paso (TX) 43.8%Denver (CO) 34.7%

Average savings 40.6%Average savings $26,392,167

Sharecount (m) 1,338

Pre-tax impact on EPS $0.02

Source: Bankrate.com; RBC Capital Markets estimates

We estimate that this effort could add about 30 basis points to margins in 2016. While the current initiative to relocate employees is not a key contributor to earnings growth, investors should be aware that it is one of many initiatives to control the growth of expenses. Other efforts to improve efficiency include subleasing one building in San Francisco or enrolling clients in paperless statements.

The broader goal is to grow expenses at a slower pace than earnings. The firm intends to reinvest cost savings back into the company, allocating capital to new products and to drive down fees that the firm charges its clients. Thus, the ultimate goal from cost-saving initiatives is not merely a reduction in the expense base, but top-line growth through competitive pricing. Thus, the company needs to be judged by how fast it can grow its margins and we believe that the firm’s size can be a significant advantage.

We believe there is a meaningful amount of operating leverage embedded in Schwab’s business model, given the firm’s size and reliance on technology to drive margins. The chart below shows expenses as a percentage of average client assets.

We estimate that the relocation of employees from higher cost locations such as San Francisco to lower cost markets such as Denver, Austin and El Paso could save the firm $26 million per year – this excludes revenues generated by subleasing one of their two buildings in San Francisco

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 23

Exhibit 25: Schwab’s cost base appears to be the lowest among peers

0.64%0.58%

0.55%

0.33%

0.18%

0.60%0.56%

0.41%

0.29%

0.17%

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

0.7%

MS BoA ETFC AMTD SCHW

2013 2014

Source: Company filings; RBC Capital Markets

Given our expectation of increasing interest rates, balance sheet growth, and efforts to control costs, we would expect a significant improvement in the company’s pre-tax margins over the next three years. We are showing our estimates below.

Exhibit 26: Schwab’s margins have been expanding constantly, with further improvement projected

30%

18%

30% 30%31%

35%37%

45%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2009 2010 2011 2012 2013 2014 2015E 2016E

Source: Company reports; RBC Capital Markets estimates

How has Schwab done historically in controlling expenses? We have analyzed expenses as a percentage of ending client assets over time and have found that Schwab was able to control expenses beginning in 2010. The exhibit below depicts this. For our model, we are assuming that expenses as a percentage of ending client assets will not decline further in arriving at our earnings estimates. One could argue that this is a conservative assumption. However, we are expecting pre-tax operating margins to expand north of 40% despite the conservatism over the next two years.

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 24

Exhibit 27: Schwab is benefiting from economies of scale as it is growing assets (expenses as % of ending client assets)

0.21%0.22%

0.20%

0.18%0.17% 0.16% 0.16% 0.16%

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

2009 2010 2011 2012 2013 2014 2015E 2016E

Note: Calculated using simple averages; figures differ from expense ratios provided by the companies in Exhibit 25 Source: Company filings; RBC Capital Markets estimates

The firm disclosed during its recent Business Update meeting that while assets have grown by 75% over the last five years, expenses have increased by 35% only. The key takeaway would be that Charles Schwab is more efficient than wirehouses and its peers. Thus, we would expect asset growth to add incrementally more to the bottom line versus peers.

Charles Schwab provided some guidance for 2015 during its Business Update meeting in February. The firm wants the gap between revenue and expense growth to be at least 150 basis points. Could there be some conservatism in this figure? We believe so. Management had set a goal of growing revenues by 300 to 500 basis points faster than expenses. The firm ended the year with a gap of 580 basis points.

While there are a number of short-term catalysts that could lead to strong performance, we believe that Charles Schwab has created a strong franchise that could bode well for asset growth. The following section will cover these growth opportunities.

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 25

Where we could be wrong

Interest rate sensitivity could be a headwind, compressing net interest margins, if rates do not rise We consider Schwab to be the most asset sensitive discount broker. Our investment thesis is based on our expectation that interest rates rise. This perspective is based on our house view that the Federal Reserve Bank could raise interest in mid-year. However, it is difficult to predict with certainty what might/could expire in the current year. There are certain global developments to consider.

Investors view the US dollar as a safe haven. Geopolitical and economic difficulties abroad could lead to capital influx into the US, offsetting any efforts undertaken by the Board of Governors of the Federal Reserve System to raise interest rates. Lower interest rates would mean continued fee waivers on money market funds and thus lower revenues than we expect.

Absent of a meaningful revenue growth, it would be difficult for Schwab to expand margins as the cost-cutting efforts are really reducing expenses. These efforts are geared towards reducing the pace of expense growth.

Given reliance on offices and infrastructure, higher than expected investments could lead to lower margins Another “drag” on earnings could be increased investments in infrastructure. Unlike its peers, Schwab relies extensively on its branch offices. There are currently over 300 branch offices and our discussions with the company indicate that this number could increase as interest rates rise. Their market research indicates that affluent clients are more likely to use branches in a higher rate environment. We assume that this could be driven by perceived wealth as rising rates point to a stronger economy and higher stock market valuations.

Assuming we are right with our expectation that interest rates do indeed rise, the company could incur additional expenses not factored into our model. Put differently, margin expansion at Schwab could fall below our estimate as the company expands its branch offices.

Schwab is under the supervision of a number of regulators putting the company at a disadvantage with respect to capital deployment Given the company’s size and business model, Schwab is under the supervision of a number of regulators. The Charles Schwab Corporation (CSC) is a savings and loan holding company and Schwab Bank is a federal savings banks. While CSC is regulated by the Federal Reserve Bank, Schwab Bank is regulated by the Office of the Comptroller of the Currency. Schwab’s principal broker–dealers are members of FINRA and are also regulated by the Commodities Futures Trading Commission. Furthermore, Dodd-Franks created the Consumer Financial Protection Bureau, which could negatively impact the range of products offered and the profitability of products sold by Schwab.

As one can see, a number of regulators control how the company conducts its business and ultimately determine how much capital Schwab can return to its shareholders in the form of dividends and share buybacks. This is in stark contrast to TD Ameritrade, which operates under a “capital light model” and under less regulatory scrutiny.

The Charles Schwab CorporationBrokers, Asset Managers & Exchanges

March 26, 2015 Bulent Ozcan, CFA (212) 863-4818; [email protected] 26

Given the size of Schwab Bank, with a balance sheet of $105.6 billion, the firm has to comply with rules that don’t apply to its peers. An example of this would be a quantitative liquidity requirement consistent with the liquidity coverage ratio (LCR) standard established by Basel III. The LCR ratio compares the ratio of high-quality liquid assets that the firm needs to hold to potential cash outflows under certain scenarios. While LCR applies to all international banks, Schwab has to comply with a modified LCR approach as mandated by the federal reserve bank. Schwab will be required to be fully compliant by January 1, 2017. The company disclosed that compliance would impact annual returns by less than half a penny. However, there are still some uncertainties around how the rules will apply to the brokerage business. There are also other considerations to take into account as the company becomes compliant with Basel III rules. Here are some excerpts from the company’s 2013 10K filing:

Revise required minimum risk-based and leverage capital requirements by (1) establishing a new minimum Common Equity Tier 1 Risk Based Capital Ratio of 4.5%; (2) raising minimum Tier 1 Risk Based Capital Ratio from 4% to 6%; (3) maintaining the minimum Total Risk Based Capital Ratio of 8%; and (4) maintaining a minimum Tier 1 Leverage Ratio of 4%

Add a requirement to maintain a minimum capital conservation buffer, composed of common equity Tier 1 capital, of 2.5% of risk-weighted assets, which means that banking organizations, on a fully phased-in basis no later than January 1, 2019, must maintain a Common Equity Tier 1 Risk Based Capital Ratio greater than 7% and Tier 1 Risk Based Capital Ratio greater than 8.5% and a Total Risk based Capital Ratio greater than 10.5%

Change the definition of capital categories for insured depository to be considered “well capitalized”, Schwab Bank must have a Common Equity Tier 1 Risk Based Capital Ratio of at least 6.5%, a Tier 1 Risk Based Capital Ratio of at least 8%, a Total Risk Based Capital Ratio of at least 10% and a Tier 1 Leverage Ratio of at least 5%.

The new minimum regulatory capital ratios and changes to the calculation of risk-weighted assets are effective beginning January 1, 2015. The required minimum capital conservation buffer will be phased in incrementally, starting at 0.625% on January 1, 2016 and increasing to 1.25% on January 1, 2017, 1.875% on January 1, 2018, and 2.5% on January 1, 2019