Embed Size (px)

Citation preview

SDP Annual Conference

Charleston, SC September 20-23, 2016

The Society of Depreciation Professionals

extends its sincere appreciation to our

Gold Sponsors for their support of the

Annual Conference and Training

Alliance Consulting Group was formed by its Managing Partner, Dane Watson,

PE, CDP, in 2004 to provide depreciation, fixed asset and expert consulting

services for the full range of utilities in North America. Mr. Watson is actively

involved in the day-to-day operations of the business along with three senior

professionals – Dr. Karen Ponder, Rhonda Watts and Rebecca Richards as well

as other supporting staff. Alliance is dedicated to providing quality

depreciation consulting and fixed asset expert services. Their engineering and

accounting professionals have 100 years of combined experience around the utility industry, and have been employed in

the industry as utility employees and managers, auditors and consultants.

AUS Consultants has been delivering unsurpassed consulting services to the

utility industry for decades. Their expertise includes all aspects of the utility

regulatory and ratemaking arenas, as well as the valuation field. Because they

focus exclusively on the utility industry, they have developed deep industry

expertise and experience, which they pass on to their clients, providing first-rate

services and ensuring their clients’ success. Their consultants have decades of experience, are well respected throughout

the industry, and understand the key strategic issues faced by today’s utility professionals. All of their consultants are

utility experts and have advised vertically integrated utilities as well as utilities operating in the restructured industry.

AUS Consultants’ valuation expertise includes utility asset valuation, as well as the valuation of intellectual property and

intangible assets. AUS Consultants publishes two of the top utility reports in the industry: the AUS Monthly Utility

Report and the AUS Telephone Plant Index.

Founded in 1915, Gannett Fleming, is a global infrastructure firm that provides

planning, design, technology, and construction management services for a

diverse range of markets and disciplines. They have helped to shape

infrastructure and improve communities through transportation, environmental, water, energy, and facility-related

projects in more than 65 countries. The firm embraces sustainability and innovation for all activities, finding the best

solutions and the most efficient processes while being responsible stewards of the environment. Gannett Fleming

Valuation and Rate Consultants, LLC provides consulting services to investor-owned and publicly-owned utilities and

has successfully represented clients in public pricing policy and related matters before regulators and in courts of law.

Their team of engineers, accountants and analysts has a broad experience base to meet your needs and is skilled in using

computer-modeling techniques to customize studies and analysis. They combine the guiding traditional principles with

innovative approaches to provide an understandable product that can stand the test of scrutiny.

PowerPlan provides a fully integrated suite of asset-centric accounting, tax,

budgeting and regulatory software solutions. PowerPlan integrates asset data

across multiple departments and automates key workflows. By ensuring

everyone has visibility into detailed asset data at each phase of the asset lifecycle, you are able to make better decisions,

ultimately improving financial performance. The world’s most demanding asset-centric companies already trust

PowerPlan to manage more than $2.3 trillion in assets.

SDP Conference Materials

September 19-20, 2016

Section 1: Conference Schedule

Speaker Bios

Attendee List

Section 2: Electric Rate Ratemaking

Michael Gorman, Brubaker & Associates

Section 3: Tax and the Regulatory Impact

Matthew Kahn, conEdison, Inc.

Section 4: Cost Segregation Studies & Tangible Property Regulations

Ashley Sullivan & David Fabian, MS Consultants

Section 5: North American Utility Regulatory Trends

Derek Manville, PWC

Section 6: Making and Managing a Depreciation Study

John Wiedmayer, Gannett Fleming

Section 7: Results of Operations Modeling & Working Cash

Andy Strasner & David White, Utility Consulting Group

Section 8: Early Plant Retirement: Accounting Considerations

Cindy Leed & Melissa Abernathy, Duke Energy

Section 9: Accounting Update

John Lacey, California State University Long Beach

Materials as of 9/21/16

Click the section number to jump to that presentation.

Section 1 Click to jump back to Table of Contents

Sunday, September 18, 2016

SDP Conference Schedule

September 19-20, 2016

5:30-7:00 PM Welcome Reception Gold Ballroom

Monday, September 19, 2016

7:30-8:30 AM

8:30-8:45 AM

Registration and Breakfast

Welcome Remarks Rick Fisher, CDP

Carolina A

Carolina B

David Garrett

8:45-9:45 AM Regulation, Technological

Change & Capital Recovery:

Three Decades Later

Hon. Branko Terzic Carolina B

9:45-10:45 AM Electric Rate Ratemaking Michael Gorman Carolina B

10:45-11:00 AM Break

11:00 AM-12:00 PM Managing a Depreciation

Study

John Wiedmeyer Carolina B

12:00-1:30 PM Lunch and SDP Annual Meeting Carolina A

1:30-2:30 PM Tax Relief and the

Regulatory Impact

Matthew Kahn Carolina B

2:30-3:30 PM Cost Segregation Studies &

Tangible Property Regulations

Ashley Sullivan

David Fabian

Carolina B

3:30-3:45 PM Break

3:45-4:45 PM North American Utility

Regulatory Trends

Derek Manville Carolina B

5:30-7:00 PM Evening Reception

Continued on next page

- Off site The Macintosh479B King Street Charleston, SC 29403

Tuesday, September 20, 2016

7:45-8:30 AM

8:30-9:30 AM

Registration and Breakfast

Working Cash & Results Andy Strasner

Carolina A

Carolina B

of Operations Modeling Dave White

9:30-10:30 AM Early Plant Retirement

Accounting Considerations

Cynthia Lee Carolina B

10:30-10:45 AM Break

10:45-11:30 Accounting Updates John Lacey Carolina B

End of program

SDP Conference Speaker Biographies David Fabian, MS Consultants

David Fabian has 25+ years’ tax and accounting experience. He joined MS Consultants in 1999 and has

been personally involved in over 7,500 Cost Segregation projects in more than 30 states. David has

presented on a variety of topics including depreciation & cost segregation, energy modeling, tangible

property regs, & more. He also developed comprehensive in-house training and quality control

programs.

Michael Gorman, Brubaker & Associates Inc.

Mr. Gorman is a Managing Principal at BAI. He received Degrees of Bachelor of Science in Electrical

Engineering from Southern Illinois University at Carbondale and Master of Business Administration from

the University of Illinois at Springfield. Mr. Gorman has also done extensive graduate studies in Financial

Economics. He earned the designation Chartered Financial Analyst (CFA) from the CFA Institute.

Mr. Gorman has been in the consulting practice since 1990, and in the energy business since 1983. Mr.

Gorman was employed by the Illinois Commerce Commission and held positions including Director of

the Financial Analysis Department, Senior Analyst, Planning Analyst and Utility Engineer. Mr. Gorman

was also employed by Merrill Lynch as a Financial Consultant. In this position, he consulted on cash

management and investment strategies.

His responsibilities at BAI include project management, cost of capital studies, depreciation studies,

financial integrity studies, system resource planning studies alternative regulation plan/mechanisms cost

of studies, mechanisms, service, rate design, production cost evaluations, commodity risk management,

commodity procurement management, competitive supplier management and counterparty credit risk.

Cynthia (“Cindy”) S. Lee, Duke Energy Corporation

Cindy is the Director of Asset Accounting for Duke Energy Corporation, and has been at the Company

since 2002. She is a graduate of Rollins College with a Bachelor of Arts in Economics and a graduate of

The Johns Hopkins University with a Master of Business Administration. Cindy is a Certified Public

Accountant licensed in the state of North Carolina. As the Director of Asset Accounting, Cindy has

responsibility for the accounting functions for Duke Energy’s Asset Accounting function within the

Regulated Utilities business segment for each of the jurisdictions we operate (NC, SC, FL, OH, KY, IN).

She is also one of Duke Energy’s property accounting representatives with Edison Electric Institute, a

trade association of electric utility companies. Cindy lives in Charlotte with her husband Randy, and

daughter Derren.

Matthew Kahn, MST, Consolidated Edison, Inc.

Matthew Kahn is a Tax Manager with the New York Utility, Con Edison, Inc. As part of his role with the

company, Mr. Kahn is involved in the rate case process and oversees the preparation and review of

depreciation studies for the electric, gas, and steam businesses of the Utility. He holds a Bachelor’s

Degree in Accounting, and a Master’s Degree in Taxation, both from Bentley University. Mr. Kahn has

submitted testimony regarding depreciation and income tax accounting issues in the State of New York.

Derek Manville, PWC

Derek is a Director in PwC’s Advisory – Power & Utilities practice based in Atlanta, Georgia. Derek has

spent the last 10 years implementing complex business process and technology transformation

programs within the Utilities industry.

Derek’s relevant project experience including:

Merger Integration (Pre & Post-Merger)

Regulatory Strategy & Process Improvement

Financial Planning, Budgeting, & Forecasting

Financial Reporting (Internal & External)

Financial Chart of Accounts (CoA) Design

Derek leads PwC’s Advisory Regulatory process improvement offering – delivering regulatory

management process improvement and technology solutions to utilities clients. Derek graduated with

his Master of Business Administration (MBA) from Georgia Institute of Technology and a Bachelors of

Political Science from the Wright State University.

Andy Strasner, Manager, Utility Consulting Group LLC

Andy has over fifteen years of consulting experience serving various clients in the utility industry. His

experience includes project management, systems design and implementation, business requirements,

strategy development and business process reengineering. Prior to joining UCG, Andy was employed by

BearingPoint as a manager in the utility practice. He was also previously employed by Arthur Andersen

Business Consulting and served clients primarily in the utility industry. He holds a Bachelor’s degree in

Business-Economics and Accounting from the University of California at Santa Barbara.

Ashley Sullivan, MS Consultants

Ashley is a Quality Control Manager for Cost Segregation Studies at MS Consultants and joined the

company in 2013. She has over 12 years Cost Segregation experience. She heads up the Virginia office.

Ashley holds a Senior Cost Segregation Professional designation with ASCSP. She travels extensively

nationwide to meet with clients and discuss opportunities.

The Honorable Branko Terzic, Berkeley Research Group

Branko Terzic is a Managing Director at Berkeley Research Group (BRG) LLC and a Nonresident Senior

Fellow of the Atlantic Council’s Global Energy Center in Washington, DC. Dr. Terzic is a Founding

member of the Society of Depreciation Professionals (SDP) and was its first Vice President. In a speech

given at the 1986 Iowa State University Regulatory Conference, while in his last year as a Wisconsin PSC

Commissioner, Terzic called for the formation of the depreciation society.

Terzic’s service in government includes that of Commissioner on the U.S. Federal Energy Regulatory

Commission, Commissioner on the State of Wisconsin Public Service Commission and Chairman of the

State of Wisconsin Racing Board. In business prior to joining BRG, Terzic served as Executive Director of

the Deloitte Center for Energy Solutions; Global Regulatory Policy Leader for Deloitte & Touche LLP;

Chairman, President and CEO of Yankee Energy System, Inc.; Managing Director Arthur Andersen

Economic Consulting, Special Investigations Engineer at Wisconsin Electric Power Company and as a

management consultant. He has been a member of the National Petroleum Council and National Coal

Council and is a former Chairman of the United Nations Economic Commission for Europe (UN ECE) Ad

Hoc Group of Experts on Cleaner Electricity Production. A frequent speaker at industry forums and a

prolific writer Terzic currently appears regularly on CNN International and Fox Business channel. Terzic

was elected to the Energy Efficiency Forum Hall of Fame (2009) and was honored with the “Champion

Award” by The Women’s Council on Energy and Environment (2008) as well as other industry awards.

He is a faculty member of the Washington Campus consortium of 16 MBA schools, is a member of the

ASME, AEE, IAEE, Energy Bar Association and other organizations. Branko Terzic holds a BS in Energy

Engineering and was awarded an honorary Doctor of Sciences Engineering degree both from the

University of Wisconsin-Milwaukee.

Dave White, Utility Consulting Group LLC

Dave has over 25 years of experience serving numerous clients in the utility industry. He has been

involved in a wide range of consulting assignments covering regulatory, shared services, operations and

technology processes and systems. Prior to joining the management consulting firm Utility Consulting

Group LLC, Dave was employed by BearingPoint as a senior manager in their utility practice. He was also

a senior manager with Arthur Andersen Business Consulting, serving a number of utilities in North

America. Prior to Andersen, he was employed by Sargent & Lundy and managed cross-functional teams,

budgeted and scheduled projects, and counseled domestic and international clients on the procurement

of equipment and the design of electric substations. Dave holds a M.B.A from University of California at

Los Angeles, and a Bachelor of Science degree in Electrical Engineering from Northwestern University.

John F. Wiedmayer, CDP, Gannett Fleming, Inc.

John Wiedmayer is a Project Manager, Depreciation Studies for the Valuation and Rate Division of

Gannett Fleming, Inc. He has over 29 years of consulting experience and has conducted numerous

depreciation, valuation, and cost of service studies for clients in the electric, gas, railroad, telephone,

water, and wastewater industries.

John holds a B.A. from Lafayette College in Engineering and an M.B.A. from Penn State University. Mr.

Wiedmayer’s research paper for his M.B.A. was devoted to electric utility industry restructuring. He has

completed five week-long courses of depreciation training offered by Depreciation Programs, Inc. in

Grand Rapids, MI. He is a member of the National Society of Professional Engineers and the

Pennsylvania Society of Professional Engineers. Mr. Wiedmayer has provided expert testimony related

to depreciation in several states (MO, IL, NY, PA, KY, AZ, MD, and UT); in Nova Scotia, Newfoundland,

and Labrador; and before the FERC. John has served on the SDP Board and was SDP President in 2005.

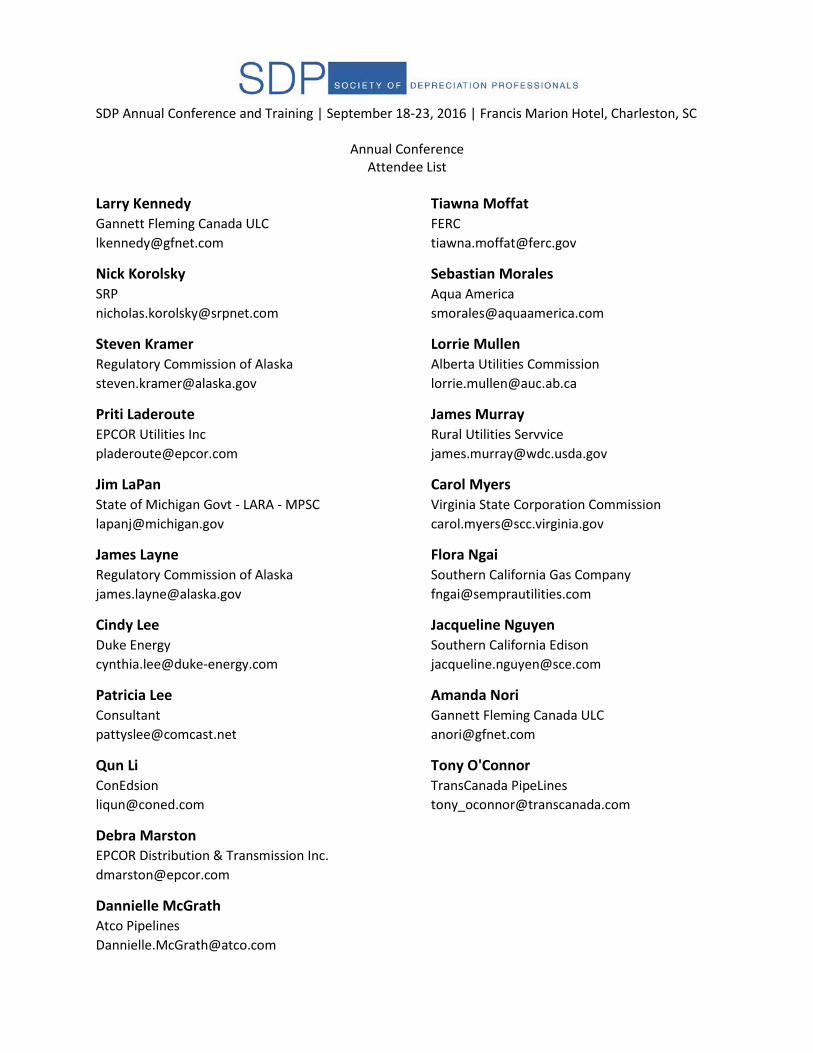

SDP Annual Conference and Training | September 18-23, 2016 | Francis Marion Hotel, Charleston, SC

Annual Conference Attendee List

Melissa Abernathy Duke Energy [email protected]

Ned Allis Gannett Fleming Valuation and Rate Consultants, LLC [email protected]

Brian Andrews Brubaker & Associates, Inc. [email protected]

Brian Bahr SouthWest Water Company [email protected]

Bryan Barnes PowerPlan Inc. [email protected]

Stephen Barreca BCRI Valuation Services [email protected]

Richard Bennett PowerPlan, Inc. [email protected]

Donna Bourne FortisAlberta [email protected]

Kiki Carlson Suburban Water Systems [email protected]

Jason Cash American Electric Power [email protected]

Michael Chalwell Consolidated Edison Company of New York, Inc. [email protected]

Richard Clarke Gannett Fleming Valuation and Rate Consultants, LLC [email protected]

Donald Clayton Tangibl LLC [email protected]

William Chris Colberg USDA Rural Utilities Service [email protected]

Ryan Cole CSX Transportation [email protected]

Corrado Costanzo TransCanada [email protected]

Karen Daly LG&E and KU Services [email protected]

Manoj Dandekar Baker Mckenzie Consulting LLC [email protected]

David Davis American Electric Power [email protected]

Amber DeLucenay TECO Energy - Peoples Gas [email protected]

SDP Annual Conference and Training | September 18-23, 2016 | Francis Marion Hotel, Charleston, SC

Annual Conference Attendee List

David Fabian MS Consultants, LLC [email protected]

Richard Fisher PowerPlan [email protected]

Sandra Funderburg Southern California Gas Company [email protected]

Ron Garner AR Public Service Commission [email protected]

David Garrett Garrett Group LLC [email protected]

Tammi Goldstein Pacific Gas and Electric Company [email protected]

Michael P. Gorman Brubaker & Associates, Inc. [email protected]

Tracy Greer SRP [email protected]

Chris Harris Virginia State Corporation Commission [email protected]

Marianella Hensley TECO Energy - Peoples Gas [email protected]

Wade Horigan Tangibl LLC [email protected]

Melissa Howard Gannett Fleming, Inc. [email protected]

Jeremy Hubert PA PUC [email protected]

Paul Hunt Southern California Edison [email protected]

Jerry Janow Gannett Fleming Canada ULC [email protected]

Susan Jensen Surface Transportation Board [email protected]

John Johnson Atmos Energy Corporation [email protected]

Frederick Johnston Gannett Fleming, Inc. [email protected]

Lance Kaufman Bardwell Consulting [email protected]

Robert Kelly SouthWest Water Company [email protected]

SDP Annual Conference and Training | September 18-23, 2016 | Francis Marion Hotel, Charleston, SC

Annual Conference Attendee List

Larry Kennedy Gannett Fleming Canada ULC [email protected]

Nick Korolsky SRP [email protected]

Steven Kramer Regulatory Commission of Alaska [email protected]

Priti Laderoute EPCOR Utilities Inc [email protected]

Jim LaPan State of Michigan Govt - LARA - MPSC [email protected]

James Layne Regulatory Commission of Alaska [email protected]

Cindy Lee Duke Energy [email protected]

Patricia Lee Consultant [email protected]

Qun Li ConEdsion [email protected]

Debra Marston EPCOR Distribution & Transmission Inc. [email protected]

Dannielle McGrath Atco Pipelines [email protected]

Tiawna Moffat FERC [email protected]

Sebastian Morales Aqua America [email protected]

Lorrie Mullen Alberta Utilities Commission [email protected]

James Murray Rural Utilities Servvice [email protected]

Carol Myers Virginia State Corporation Commission [email protected]

Flora Ngai Southern California Gas Company [email protected]

Jacqueline Nguyen Southern California Edison [email protected]

Amanda Nori Gannett Fleming Canada ULC [email protected]

Tony O'Connor TransCanada PipeLines [email protected]

SDP Annual Conference and Training | September 18-23, 2016 | Francis Marion Hotel, Charleston, SC

Annual Conference Attendee List

Michael Plunkett PowerPlan [email protected]

Karen Ponder Alliance Consulting Group [email protected]

Dixon Quong Atco Pipelines [email protected]

Joanna Richard Gannett Fleming Valuation and Rate Consultants, LLC [email protected]

Casey Robb State of Wyoming [email protected]

Earl Robinson AUS Consultants [email protected]

David Sheffer AUS Consultants [email protected]

Russell Shipe Brunswick EMC [email protected]

Aaron Smith PowerPlan, Inc. [email protected]

John Spanos Gannett Fleming Valuation and Rate Consultants, LLC [email protected]

Douglas Steiner Salt River Project [email protected]

Jack Stevens USDA/RUS [email protected]

Alla Strickland GDS Associates, Inc [email protected]

Ashley Sullivan MS Consultants, LLC [email protected]

Branko Terzic Berkeley Research Group LLC [email protected]

Crystal Turner ONE Gas [email protected]

Matthew Vanderbilt San Diego Gas & Electric [email protected]

Kevin Watkins Consumers Energy [email protected]

Dane Watson Alliance Consulting Group [email protected]

Brent Weber Anchorage Water & Wastewater Utility [email protected]

SDP Annual Conference and Training | September 18-23, 2016 | Francis Marion Hotel, Charleston, SC

Annual Conference Attendee List

Sean Welsh Virginia State Corporation Commission [email protected]

Kimber Wichmann Wyoming Dept of Environmental Quality [email protected]

John Wiedmayer Gannett Fleming Valuation and Rate Consulatants, LLC, Inc. [email protected]

Herb Wilson ONE Gas, Inc. [email protected]

Gerrilynn Wolfe AR Public Service Commission [email protected]

Valerie Yeager CSX Transportation [email protected]

David Young Southern California Edison [email protected]

Section 2 Click to jump back to Table of Contents

““Electric Rate Electric Rate Ratemaking”Ratemaking”presented by

Michael Gorman

September 19, 2016September 19, 2016

BRUBAKER & ASSOCIATES, INC.

Michael Gorman

16690 Swingley Ridge Rd., Suite 140P. O. Box 412000

Chesterfield, Missouri 63017636 898 6725

1

636-898-6725www.consultbai.com

Three Steps in theThree Steps in theRatemaking ProcessRatemaking ProcessRatemaking ProcessRatemaking Process

1) Utility Revenue

Requirements

1) Utility Revenue

RequirementsRequirements

2) Class Cost of Service

Requirements

2) Class Cost of Service COMMCOMMINDLTG

RES

)

3) R t D i

)

3) R t D i

INDOTHOTH

3) Rate Design3) Rate Design INDUSTRIAL

2

Utility Revenue Utility Revenue Utility Revenue Utility Revenue RequirementsRequirementsRequirementsRequirements

3

Test Year

12 Months12 Months12 Months12 Months

P FP FHistoricalHistoricalTest YearTest Year PeriodPeriod

RateRatePro FormaPro Forma

9 9 MonthsMonths_______________., future test year

4

., current test year

Historical Pro Forma Adjustments

Change Pro Forma Revenue Revenue Plant Depr. Normal Operating Revenue Proposedp p g p

Current Rates Additions Rates O&M Sales Results Adjustment Rates

I. RevenueSales Revenue $625,000 $5,000 $630,000 $23,500 3.7% $653,500

Miscellaneous Revenue $1,000 $1,000 $1,000

Total $626,000 $631,000 $654,500

II. Operating ExpensesOperation & Maintenace $439,300 $5,000 $444,300 $444,300

Depreciation $34,000 $4,281 $1,519 $39,800 $39,800

Other Taxes $25,029 $171 $25,200 $25,200

Income taxes:

Current $21 112 $21 112 8 225 $29 337 Current $21,112 $21,112 8,225 $29,337

Deferred $15,000 ($1,498) $13,502 $13,502

Total Operating Expense $534,441 $543,914 $552,139

III. Operating Income $91,559 $87,086 $102,361

IV. Rate BasePlant-In-Service $1,148,744 $171,256 $1,320,000 $1,320,000

Acc. Depr. $412,159 $2,141 $414,300 $414,300

Net Plant $736,585 $905,700 $905,700

Add:

CWIP $350,000 $140,800 $209,200 $209,200

Plant Held For Future Use $25,000 $6,700 $18,300 $18,300

Material & Supplies $75,000 $75,000 $75,000

Cash Working Capital $43,800 $43,800 $43,800

Less:

Acc Deferred Income Tax $101 251 $749 $102 000 $102 000Acc. Deferred Income Tax $101,251 $749 $102,000 $102,000

Rate Base $1,129,134 $1,150,000 $1,150,000

Rate Of Return 8.11% 7.57% 8.90%

Rate of ReturnWeightedWeighted

PercentPercent Cost Cost Cost Cost Type of CapitalType of Capital

LongLong--term debtterm debt 47 0047 00%% 7 007 00%% 3 293 29 %%LongLong--term debtterm debt 47.0047.00%% 7.007.00%% 3.293.29 %%

Preferred stockPreferred stock 6 006 00 7 257 25 0 440 44Preferred stockPreferred stock 6.006.00 7.257.25 0.440.44

Common equityCommon equity 47 0047 00 11 0011 00 5 175 17

TotalTotal 100.00100.00%% 8.908.90 %%

Common equityCommon equity 47.0047.00 11.0011.00 5.175.17

6

Class CostClass Cost LTGRESClass CostClass Cost

of Serviceof ServiceCOMMCOMMIND

LTG

OTHOTHof Serviceof Service

7

Customer ClassesCustomer Classes• Residential

• General Service (Commercial)

• Large Power (Industrial)

Lighting• Lighting

• OtherOther

Demand Size, Load Factor, Delivery Voltage

8

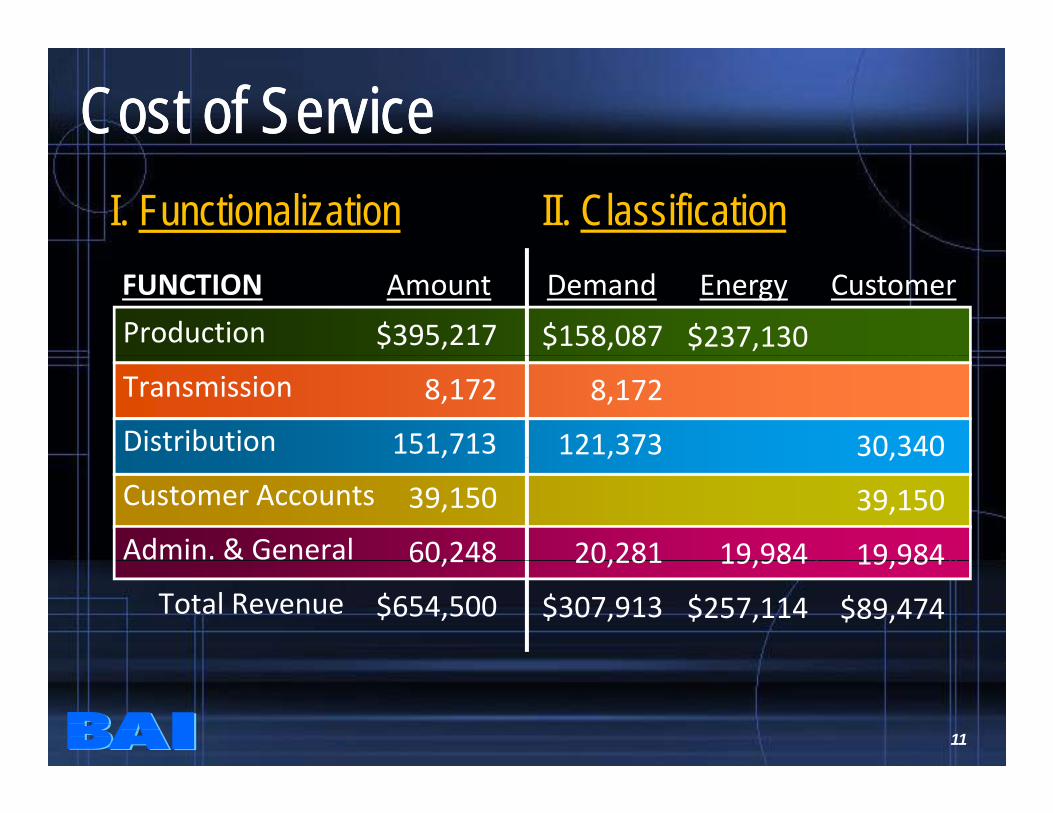

Step 1: FunctionalizationStep 1: Functionalization

AmountFUNCTION

ProductionProduction

TransmissionTransmission

$395,217

8 172TransmissionTransmission

DistributionDistribution

Customer AccountsCustomer Accounts

8,172

151,713

39 150Customer AccountsCustomer Accounts

Admin. & GeneralAdmin. & General

T t l RT t l R

39,150

60,248

$Total RevenueTotal Revenue $654,500

9

Step 2: ClassificationStep 2: Classification•• DemandDemand::

C t th t ith d dCosts that vary with demand

•• Energy:Energy:Costs that vary with energy provided

•• Customer:Customer:Costs related to customers served

•• DirectDirect AssignmentAssignment•• Direct Direct AssignmentAssignmentCosts attributable directly to a customer or

class

10

class

Cost of ServiceCost of ServiceII. ClassificationI. Functionalization

ProductionAmountFUNCTION

$395,217

Demand Energy Customer

$158,087 $237,130

Transmission

Distribution

8,172

151,713

8,172

121,373 30,340Customer Accounts

Admin. & General

,

39,150

60,248

,

20,281 19,984

,

39,150

19 984Total Revenue

60,248

$654,500

20,281

$307,913

19,984

$257,114

19,984

$89,474

11

TransmissionTransmission & Delivery of Electricity& Delivery of ElectricityTransmission

GENERATION GENERATION

Subtransmission

Distribution

DEMANDDEMAND

CUSTOMERCUSTOMER

KWKW

CUSTCUST##

DEMAND

CUSTOMER

KW

CUST#

Res.Com.C&I SecOther

DEMANDDEMAND

CUSTOMERCUSTOMER

KWKW

CUSTCUST##

DEMAND

CUSTOMER

KW

CUST#

Res.Com.C&I SecOther

DEMANDDEMAND

CUSTOMERCUSTOMER

KWKW

##

DEMAND

CUSTOMER

KW

#

Res.Com.C&I Sec

TRANS.

Industrial

12

CUSTCUST##

CUST# C&I Sec

Other

• Demand – Coincident (CP) vs.Non‐Coincident (NCP)Non Coincident (NCP)

• Based on class usage at generator, notat meter

13

Illustrative Example of Coincident vs.Illustrative Example of Coincident vs.NonNon Coincident DemandsCoincident DemandsNonNon--Coincident DemandsCoincident Demands

System PeakSystem Peak

NCPCP

man

d NCPCP

CP

NCP

Dem

RESRESCP

GSGS

INDINDNCP CP

CP

14TimeLTGLTG

Demand Loss FactorsGeneration / MeterDemand Available

100.00 kW GenerationGeneration

1.019 / 1.0001.019 / 1.000Trans/Sub CustomerTrans/Sub Customer

Transmission /Transmission /SubtransmissionSubtransmission98.11 kW

ters

ters

1.043 / 1.000 1.043 / 1.000 Primary CustomerPrimary Customer

95.88 kW PrimaryPrimaryMet

Met

1.071 / 1.000 1.071 / 1.000 Secondary CustomerSecondary Customer

93.34 kW SecondarySecondary

15

yy

Production / Transmission Allocation Production / Transmission Allocation MethodologiesMethodologies

d k ( )

MethodologiesMethodologies

• Coincident Peak (CP)

• Four Coincident Peak (4CP)• Four Coincident Peak (4CP)

• Average and Excess (A&E)g ( )

• Peak and Average (P&A)

16

Alternative 1Alternative 1C i id t P k D dC i id t P k D dCoincident Peak DemandCoincident Peak Demand

• Allocates demand on basis of each class’ demand at the time of the system peak

• Many variations are possible, i.e.,

– highest month in year (1CP)highest month in year (1CP)

– average of four highest months (4CP )

– maximum four summer month(s)maximum four summer month(s) (Sum 4CP)

17

CP Demand Allocation Factor Used for Production and Transmission Plant

GSGS IndInd

402402

LtgLtg

77

TotalTotalResRes

Coincident Coincident PeakPeak328328

1.07651.0765

402402

1.04611.0461

77

1.07711.0771

2,0412,041

1.07001.0700

1,3041,304

1.07711.0771

(MW) at Meter(MW) at Meter

Loss FactorLoss Factor

353353

16 16%16 16%

420420

19 23%19 23%

77

0 32%0 32%

2,1842,1841,4041,404CP at GenerationCP at Generation

All ti F tAll ti F t 16.16%16.16% 19.23%19.23% 0.32%0.32% 100%100%64.29%64.29%Allocation FactorAllocation Factor

18

Alternative 2Alternative 2F C i id t P k (4CP) D d F C i id t P k (4CP) D d Four Coincident Peak (4CP) Demand Four Coincident Peak (4CP) Demand

• Allocates demand to each class

based on the average of the fourbased on the average of the four

highest months for the system

19

Example:Example:Four Coincident Peak (4CP) DemandFour Coincident Peak (4CP) DemandFour Coincident Peak (4CP) DemandFour Coincident Peak (4CP) DemandMW at Generator Res GS Ind Ltg TotalMW at Generator Res GS Ind Ltg Total

1. Peak Month: October 1 404 353 420 7 2 184

Top Four Peak Months in Yearea o t Octobe 1,404 353 420 7 2,184

2. Peak Month: August 1,380 366 424 7 2,177

3. Peak Month: July 1,364 300 488 7 2,159

4. Peak Month: September 928 444 607 - 1,979

Four Month Average 1,269 365 484 5 2,1234CP Demand Factor 59.78% 17.18% 22.79% 0.25% 100.00%

20

Alternative 3Alternative 3A & E D dA & E D dAverage & Excess DemandAverage & Excess Demand

• Considers maximum demand

(NCP) of each class

• Considers energy use of each class

(l d f t )(load factor)

• Considers system peak loadConsiders system peak load

21

Average & Excess DemandAverage & Excess DemandSystem Peak in Jan = 2,185 MW

Excess Demand =NCP A g Demand

ExcessExcess== 918 MW918 MW NCP – Avg Demand 918 MW918 MW

Average = Average = 1,267 MW1,267 MW

Average Demand =

Energy / 8 760 hrs,,

J F M A M J J A S O N D

Energy / 8,760 hrs

22

Example:Example:Average & Excess DemandAverage & Excess DemandAverage & Excess DemandAverage & Excess DemandMW at Generator Res GS Ind Ltg TotalMW at Generator Res GS Ind Ltg Total

NCP 1,404 583 700 24 2,711Avg Demand (a) 532 230 493 12 1,267Class Excess Demand 872 353 207 12 1,444

System Excess 554 224 131 7 918 (c)System Excess Demand (b) 554 224 131 7 918 (c)

Average & Excess 1,086 454 625 20 2,185

(a) Energy at Generator / 8,760 hours

AED A.F. 49.72% 20.79% 28.59% 0.90% 100.00%

23

( ) gy(b) Allocated on the basis of Class Excess Demand(c) System Excess Demand = 1 CP – Avg Demand = 2,185 – 1,267

Alternative 4Alternative 4P k d A D dP k d A D dPeak and Average DemandPeak and Average Demand

• Allocates average demand on basis of

energy * (System L.F.)gy ( y )

• Allocates peak demand on basis of

l NCP d d * (1 S t L F )class NCP demand * (1-System L.F.)

• No excess demand

• Combines for composite allocation

24

Peak Peak & & Average Average DemandDemandSystem Peak in Jan = 2,185 MW

Peak Demands

Average = Average =

Peak Demands =

Monthly Class NCP MW

Peak Peak = = 2 1852 185 MWMW

1,267 MW1,267 MWAverage Demand =

Energy / 8,760 hrs2,185 2,185 MWMW

J F M A M J J A S O N D

gy

25

Example:Example:Peak Peak & & Average Average DemandDemandPeak Peak & & Average Average DemandDemandMW at Generator Res GS Ind Ltg TotalMW at Generator Res GS Ind Ltg Total

NCP 1,404 583 700 24 2,711

System Annual LF = 58%

NCP

Avg. DemandFactor (a)

,

51.79%

532

41.99%

21.50%

230

18.15%

25.82%

493

38.91%

0.89%

12

0.95%

,

100.00%

1,267

100.00%

(1-LF) * Pk DemandLF * Avg. Demand

21.75%

24.35%

9.03%

10.53%

10.84%

22.57%

0.37%

0.55%

42.00%

58.00%

(a) Energy at Generator / 8,760 hours

Peak & Average A.F. 46.10% 19.56% 33.41% 0.92% 100.00%

g

26

( ) gy

Summary:Summary:Demand Allocation FactorsDemand Allocation FactorsDemand Allocation FactorsDemand Allocation Factors

MW at Generator Res GS Ind Ltg Total

64.29% 16.16% 19.23% 0.32% 100.00%CP Factor 64.29% 16.16% 19.23% 0.32% 100.00%CP Factor

4CP Factor 59.78% 17.18% 22.79% 0.25% 100.00%

A & E Factor 49.72% 20.79% 28.59% 0.90% 100.00%

Peak & Average A.F. 46.10% 19.56% 33.41% 0.92% 100.00%

27

Production Energy at GenerationProduction Energy at Generationgygy

Energy ChargeSeasonalSeasonal––SeasonalSeasonal

––TimeTime--ofof--DayDay

28

Energy Loss FactorsGeneration / MeterEnergy Available

100.00 kWh GenerationGeneration

T i i /T i i /1.019 / 1.0001.019 / 1.000Trans/Sub CustomerTrans/Sub Customer

Transmission /Transmission /SubtransmissionSubtransmission98.11 kWh

ters

ters

1.043 / 1.000 1.043 / 1.000 Primary CustomerPrimary Customer

95.88 kWh PrimaryPrimaryMet

Met

1.071 / 1.000 1.071 / 1.000 Secondary CustomerSecondary Customer

93.34 kWh SecondarySecondary

29

yy

Energy AllocationsS l C V i iSeasonal Cost Variation

Summer Months

Peak (6.0¢)Peak (6.0¢)

Cycling (3.5¢)Cycling (3.5¢)

Base (2 5¢)Base (2 5¢)

J J FF M M A A M M J J J J A A SS O O N N D D

Base (2.5¢)Base (2.5¢)

30

Energy AllocationsOff-Peak Energy Cost

Peak BaseBaseCycle Cycle

90%90%10%10%

Cyclingyy

Peak Peak TotalTotal

0%0%100%100%

BaseTotal Cost = 3.3¢/kW

Off‐Peak Hours1 2 3 4 5 6 19 20 21 22 23 24

On-Peak Energy CostBaseBaseCycleCyclePeakPeak

50%50%30%30%20%20%

Peak

C li PeakPeakTotalTotal

20%20%100%100%

Cycling

Total Cost = Base 4.1¢/kW

7 8 9 10 11 12 13 14 15 16 17 18

On‐Peak Hours 31

Example:Example:Annual Energy Allocation FactorsAnnual Energy Allocation Factors

ResRes GSGS IndInd LtgLtg

MWh SalesMWh Sales 4,350,0004,350,000 1,880,0001,880,000 4,170,0004,170,000 100,000100,000

Loss FactorLoss Factor 1.07141.0714 1.07021.0702 1.03601.0360 1.07271.0727

MWh MWh Gen.Gen. 4,660,6134,660,613 2,011,9782,011,978 4,320,1354,320,135 107,274107,274

Energy A.FEnergy A.F.. 41.99%41.99% 18.13%18.13% 38.92%38.92% 0.97%0.97%

32

Example:Example:“TOU” Energy Allocation FactorsTOU Energy Allocation Factors

ResRes GSGS IndInd LtgLtg

OnOn--Pk MWh*Pk MWh*1,508,9841,508,984 2,160,0682,160,068 21,45521,4553,728,4903,728,490

OnOn Pk MWhPk MWh

OffOff--Pk MWh*Pk MWh*

Generation

G ti

OnOn--Pk A.FPk A.F 50.26%50.26% 20.34%20.34% 29.12%29.12% 0.29%0.29%

932,123932,123 502,995502,995 2,160,0682,160,068 85,81985,819Generation

OffOff--Pk A.FPk A.F.. 25.32%25.32% 13.66%13.66% 58.68%58.68% 2.33%2.33%

*MWH@ Generator

33

*MWH @ Generator

Annual Production Capacity and Energy Costs by Rate Class under Various Allocation MethodsRate Class under Various Allocation Methods

$125.75

$250$140

CP D d

s $93.10

$107.63 $200

$100

$120 CP DemandA & E DemandPeak & Average 4CP DemandEnergy

Cap

acity

Cos

ts

nerg

y C

osts

$72.38 $72.38 $72.38

$55.98

$87.60

$67.31

$76.95

$85.78

$150

$60

$80

$/M

WhS

($KW)

nergy

C En

$55.98$51.92

$50

$100

$40

$60

$0$0

$20

RES GS INDRES GS IND

34

Capacity Costs / PricesCapacity Costs / PricesR C t / M k t L dR C t / M k t L dResource Costs / Market LoadsResource Costs / Market Loads

Capacity Energy*

I. Utility Resource

C bi d C l $12 65 $25 31

Capacity Energy $/kW $/MWh

Combined Cycle

Combustion Turbine

$12.65

$9.80

$25.31

$46.55

II. Market Price

PJM / MISOSingle price needed

for peak loadfor peak load

*Gas $3 50 / Dth and variable O&M at $15 20 (CT) and $6 55 (CC) per MWh

35

Gas $3.50 / Dth and variable O&M at $15.20 (CT) and $6.55 (CC) per MWh

NN i id t d di id t d d•• NonNon--coincident demandcoincident demand

•• Equipment needed for deliveryEquipment needed for delivery•• Equipment needed for deliveryEquipment needed for delivery

voltagevoltage

–– Subtransmission voltageSubtransmission voltage

–– Primary voltagePrimary voltagePrimary voltagePrimary voltage

–– Secondary voltageSecondary voltage

36

Illustrative Example of Coincident vs.Illustrative Example of Coincident vs.NonNon Coincident DemandsCoincident DemandsNonNon--Coincident DemandsCoincident Demands

System PeakSystem Peak

NCPCP

man

d NCPCP

CP

NCP

Dem

RESRESCP

GSGS

INDINDNCP CP

CP

37TimeLTGLTG

Distribution Classification

•Minimum Distribution System /yZero Intercept

C t i d t t t– Costs incurred to connect customerto system unrelated to demand orusageusage

•Demand Costs – Non-Load

38

Distribution SystemDemand Available

100.00 kW GenerationGeneration

Transmission /Transmission /SubtransmissionSubtransmission98.11 kW

ters

ters

95.88 kW PrimaryPrimaryMet

Met

93.34 kW SecondarySecondary

39

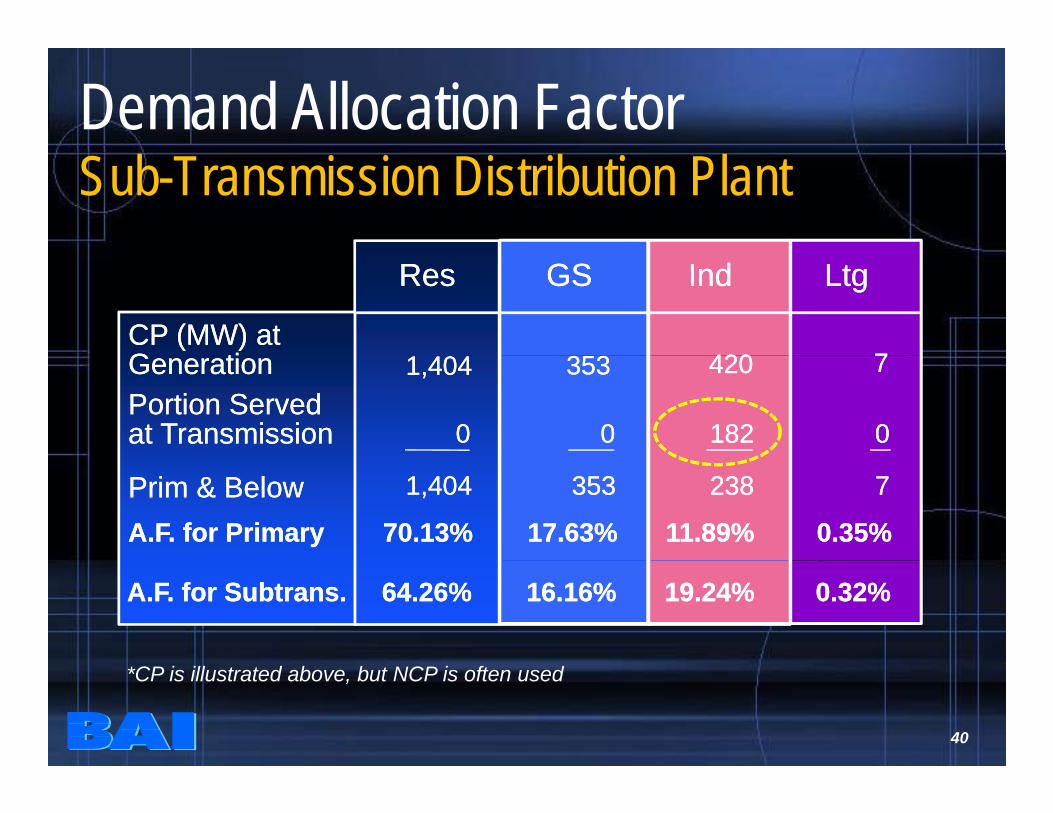

Demand Allocation FactorSub-Transmission Distribution Plant

CP (MW) atCP (MW) atG tiG ti 3 33 3 420420 77

ResRes GSGS IndInd LtgLtg

GenerationGeneration 1,4041,404

Portion Portion ServedServedat Transmissionat Transmission 00

353353

00

420420

182182

77

00

Prim & BelowPrim & Below 1,4041,404

A.F. for PrimaryA.F. for Primary 70.13%70.13%

353353

17.63%17.63%

238238

11.89%11.89%

77

0.35%0.35%

A.F. for Subtrans.A.F. for Subtrans. 64.26%64.26% 16.16%16.16% 19.24%19.24% 0.32%0.32%

40

*CP is illustrated above, but NCP is often used

Demand Allocation FactorSecondary Distribution Plant

ResRes GSGS IndInd LtgLtg

NCPNCP DemandDemandNCP NCP DemandDemand

Secondary Secondary

(MW)(MW) 1,3041,304 526526 121121 2323

NCP NCP A.F.A.F. 66.06%66.06% 26.65%26.65% 6.13%6.13% 1.17%1.17%

41

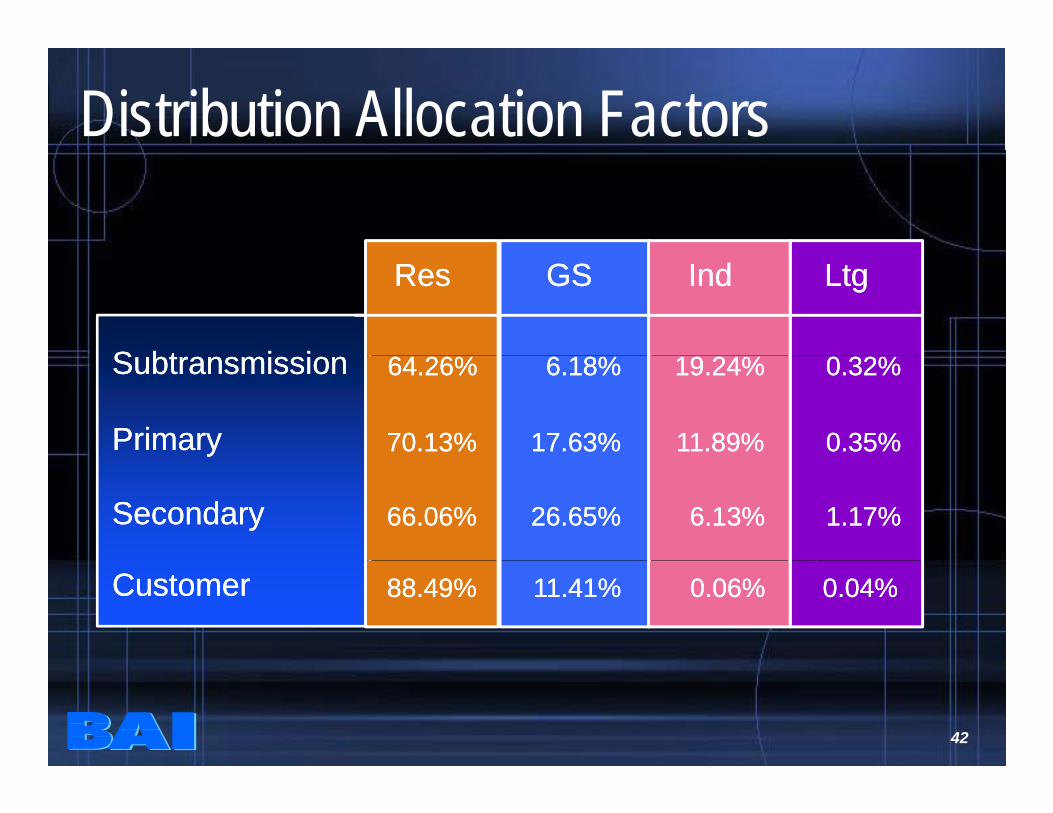

Distribution Allocation Factors

ResRes GSGS IndInd LtgLtg

S bt i iS bt i iSubtransmissionSubtransmission

PrimaryPrimary 70.13%70.13% 17.63%17.63% 11.89%11.89% 0.35%0.35%

64.26%64.26% 6.18%6.18% 19.24%19.24% 0.32%0.32%

SecondarySecondary 66.06%66.06% 26.65%26.65% 6.13%6.13% 1.17%1.17%

CustomerCustomer 88.49%88.49% 11.41%11.41% 0.06%0.06% 0.04%0.04%

42

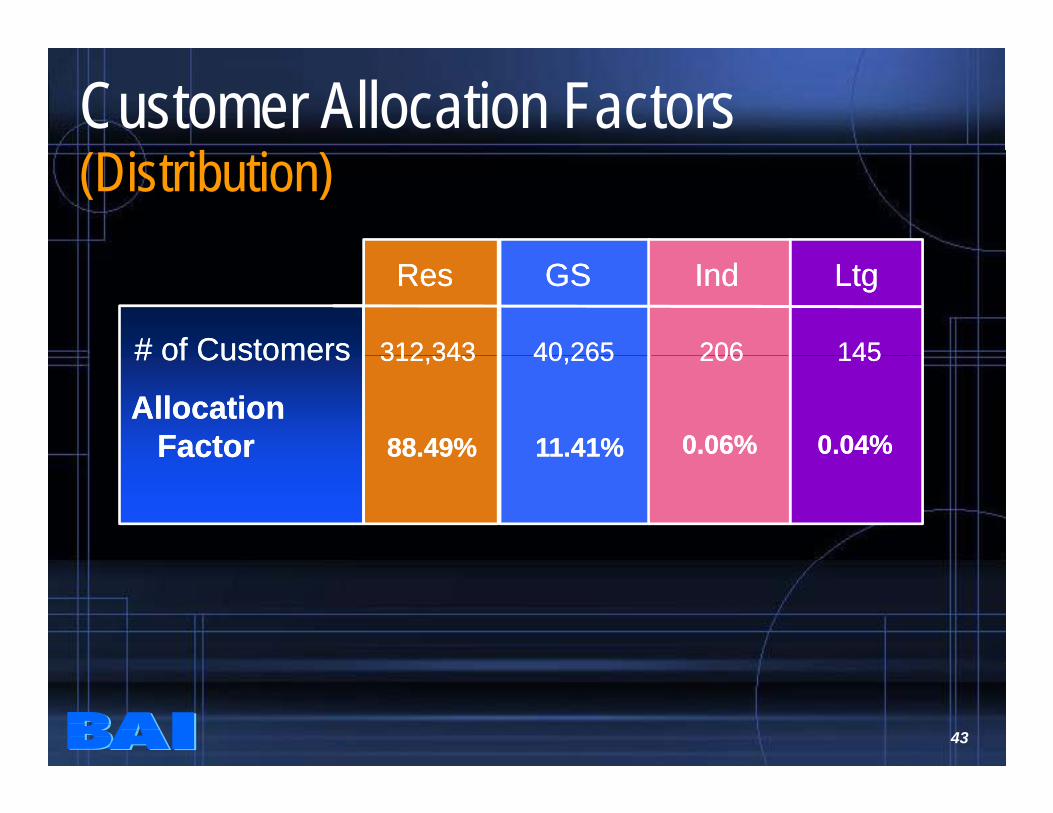

Customer Allocation Factors(Distribution)

# of Customers# of Customers

ResRes GSGS IndInd LtgLtg

312 343312 343 40 26540 265 206206 145145# of Customers# of Customers 312,343312,343 40,26540,265 206206 145145

AllocationAllocationFactorFactor 88.49%88.49% 11.41%11.41% 0.06%0.06% 0.04%0.04%

43

Weighted Customer Allocation FactorsMeters/Services

Cost of MeterCost of Meter

ResRes GSGS IndInd LtgLtg

$180$180 $185$185 $69 030$69 030 $180$180Cost of MeterCost of Meter

Relative to Relative to

ResidentialResidential

$180$180 $185$185 $69,030$69,030 $180$180

$180$180 $180$180 $180$180 $180$180ResidentialResidential

WeightWeight 1.0001.000 1.0281.028 383.5383.5 1.0001.000

$180$180 $180$180 $180$180 $180$180

44

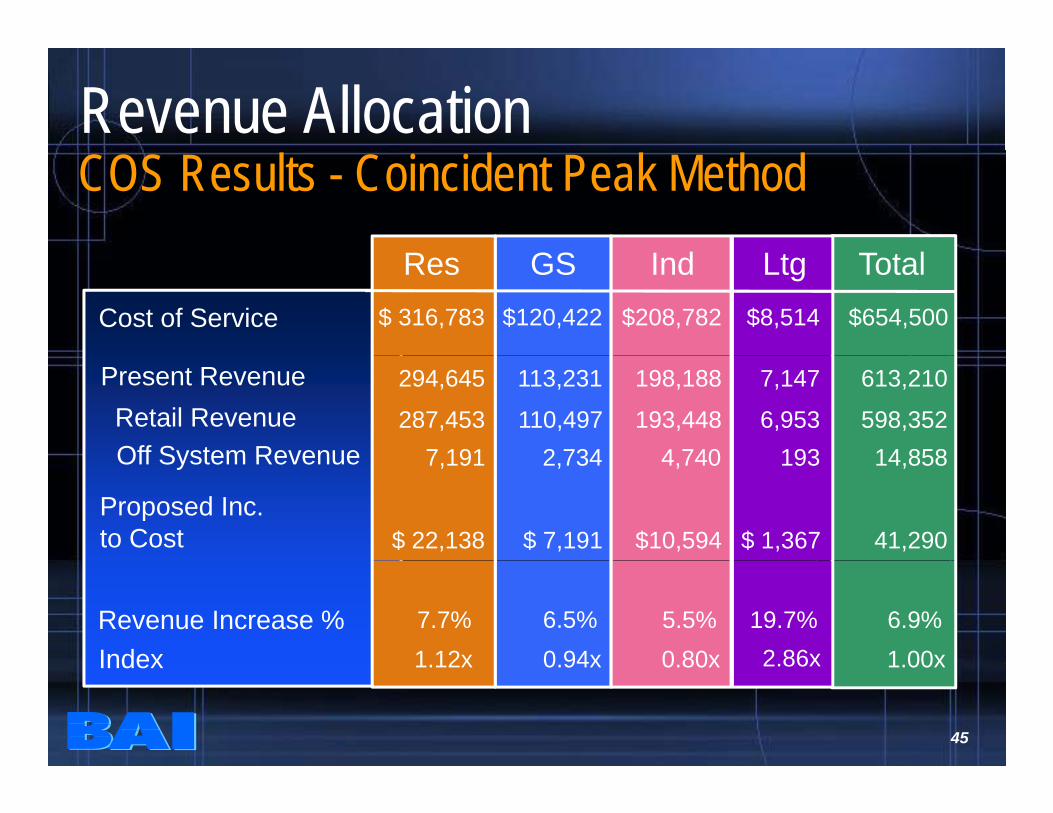

Revenue Allocation

R GS I d Lt T t l

COS Results - Coincident Peak MethodRes GS Ind Ltg Total

Cost of Service $654,500$208,782 $8,514$ 316,783 $120,422

Retail Revenue

Off System Revenue

598,352

14 858

Present Revenue 613,210

193,448

4 740

198,188

6,953

193

7,147

287,453

7 191

294,645

110,497

2 734

113,231

Off System Revenue

Proposed Inc.

to Cost

14,8584,740

$10,594

193

$ 1,367

7,191

$ 22,138 41,290

2,734

$ 7,191

Revenue Increase % 6.9%5.5% 19.7%7.7% 6.5%

Index 1 12x 0 94x 0 80x 2 86x 1 00x

45

Index 1.12x 0.94x 0.80x 2.86x 1.00x

Revenue Allocation

R GS I d Lt T t l

COS Results SummaryRes GS Ind Ltg Total

Coin. Peak Method6 9%6 9%5 5%5 5% 19 7%19 7%7 7%7 7% 6 5%6 5%R I % 6.9%6.9%5.5%5.5% 19.7%19.7%7.7%7.7% 6.5%6.5%Revenue Increase %

Index 1.12x 0.94x 0.80x 2.86x 1.00x

Avg. & Excess Methodg6.9%6.9%7.6%7.6% 19.2%19.2%6.4%6.4% 5.7%5.7%Revenue Increase %

Index 0.93x 0.83x 1.10x 2.78x 1.00x

Avg. & Peak Method6.9%6.9%8.5%8.5% 19.7%19.7%5.7%5.7% 6.4%6.4%Revenue Increase %

Index 0.83x 0.93x 1.23x 2.85x 1.00x

46

R t D iR t D iRate DesignRate Design INDUSTRIAL

47

Rate Design –Sub-Trans Primary Secondary

I. FUNCTIONAL COSTSProduction / Transmission

Capacity $200 $100 $50E $180 $95 $48

Industrial Energy $180 $95 $48

Distribution Subtransmission $50 $20 $10 Primary $20 $15Secondary $5 Secondary $5

II. COSTSTotal Prod/Trans Costs

Capacity $200 $100 $50 Energy $180 $95 $48gy

Total Distribution Costs $50 $40 $30

III. BILLING UNITSCP Demand 40.0 19.4 9.4Non-CP Demand 45.0 29.6 17.1Metered kWh 7.2 3.7 1.8

IV. CAPACITY RATESProd/Trans Demand ($/kW) $5.00 $5.15 $5.32

48

Distribution Demand ($/kW) $1.11 $1.35 $1.75

Energy Rate ($/MWh) $25.00 $25.68 $26.09

49

Section 3 Click to jump back to Table of Contents

1

Tax Relief and the Regulatory Impact

Society of Depreciation Professionals

September 19, 2016

Agenda

Tax terminology

Income taxes on the income statement

Recent trends in tax legislation

Bonus depreciation Tangible property regulations Tax repairs

Five-year growth in deferred tax liability balances

Impact of deferred income taxes on rate regulated business

2

2

Tax Terms: Permanent Differences

3

US GAAP does not define the term permanent difference

APB 11 (superseded by FAS 109 and ASC 740) definedpermanent differences as:

Differences between taxable income and pretax accounting (book) income arising from transactions that, under applicable tax laws and regulations, will not be offset by corresponding differences or “turn around” in other periods

In layperson’s terms, a permanent difference is an item thatappears on the income statement or the tax return, but not onboth

Example: Lobbying costs are “deducted” in GAAP, not for taxes ESOP dividends have no “deduction” in GAAP, but do for taxes

Tax Terms: Temporary Differences

Temporary differences that will result in taxable amounts in futureyears when the related asset or liability is recovered or settled arereferred to as taxable temporary differences

The future tax effect of a taxable temporary difference is recordedon the balance sheet as a deferred tax liability

Example: Depreciation on plant assets

4

3

Tax Terms: Temporary Differences continued… Temporary differences that will result in deductible amounts in

future years are referred to as deductible temporary differences

The future tax effect of a deductible temporary difference isrecorded on the balance sheet as a deferred tax asset

Example:

Accrued pension costs that are tax deductible when paid

5

Income Taxes on the Income Statement

6

Record deferred income taxes for temporary differencesbetween GAAP and tax

No deferred income taxes for permanent differences betweenGAAP and tax

Permanent differences impact the Company’s effective tax rate

Temporary differences have NO IMPACT on effective tax rate

4

Income Taxes on the Income Statement

Matching concept in accounting

Temporary differences between financial statements and tax returns should be accounted for as deferred income taxes

7

Because of higher temporary differences in recent years, CEI has paid minimal federal income taxes since 2009.

Income Taxes on the Income StatementExample

8

GAAP TaxPre-Tax Income 9,000$ 9,000$

Permanent Differences Lobbying Costs 1,000 1,000

Temporary Differences Depreciation (5,000) Pension Accrual 1,000

Taxable Income 10,000$ 6,000$ Tax Rate 40% 40%

Current Tax Expense 2,400 Deferred Tax Expense 1,600 Total Tax Expense 4,000$ 4,000$

Effective Tax Rate

Tax Expense 4,000$ Pre-Tax Income 9,000$

= 44%

Deferred Income Tax Expense

increases Cost of Service

The Deferred Tax Liability reduces

Rate Base

5

Tax legislation: Bonus Depreciation

• Recent trends in extenders

• 2016 – 2019 Phase-Out

– 2016 = 50%

– 2017 = 50%

– 2018 = 40%

– 2019 = 30%

– 2020 = Bonus %’s expire…

• Or do they?

9

Impacts of Bonus Depreciation

• Pros

– Cash Tax Savings

– Lowers requirements to seek external funding for strategicinvestments

• Cons

– Carrying Charges (vs. borrowing rates)

– Renewable Tax Credits (Realization/Monetization)

10

6

Tangible Property Regulations

• Reg. Sec. 1.162-3: Materials and Supplies

• Reg. Sec. 1.263(a)-1: Capital Expenditures in general

• Reg. Sec. 1.263(a)-2: Amounts paid to acquire or producetangible property

• Reg. Sec. 1.263(a)-3: Amounts paid to improve tangibleproperty

• Reg. Sec. 1.168(i)-7: Accounting for MACRS property

• Reg. Sec. 1.168(i)-8: Dispositions of MACRS property

11

Tangible Property Regulations

• Rev. Proc. 2014-16

− Materials and supplies

− Acquisition costs

− Improvements/repairs

• Rev. Proc. 2014-54

− Disposition of MACRS assets

12

In addition, the following revenue procedures provide implementation guidance for taxpayers:

7

Tangible Property Regulations Effective Dates

• Mandatory for tax years beginning on or after1/1/2014

• Accounting Method Changes (Form 3115) will berequired

− Changes are automatic changes

13

Tangible Property –Materials and Supplies• Definition of Materials and Supplies

(Reg. Sec. 1.162-3)− A unit of property < $200, or

− A unit of property used or consumed in 12 months orless, or

− Replacement parts, tools, or other items acquired to maintain or improve tangible property, or

− Fuel, lubricants, water and similar items consumed in 12 months or less, or

− Identified as materials and supplies in other IRS guidance

14

8

Materials and Supplies Types and Timing of Deductions• Incidentals (no record of consumption or physical

inventory) are deducted when acquired (Reg. Sec. 1.162-3(a)(1) and (2))

• Non-incidentals (including emergency spare parts) are deducted when consumed (Reg. Sec. 1.162-3(a)(1))

• Rotable spare parts and temporary spare parts are deducted when disposed (Reg. Sec. 1.162-3(a)(3))

• Taxpayer may elect to capitalize and depreciate rotable and temporary spare parts (Reg. Sec. 1.162-3(d)(3))

15

Materials and Supplies Types and Timing of Deductions

• Con Edison elected to depreciate these parts

• Form 3115 not required

• Con Edison is deducting non-incidental materials and supplies as they are removed from inventory

• Company filed accounting method change to deduct non-incidental parts when removed from inventory and consumed in a project

• Tax deduction for 2014 was approximately $100 million

16

9

De Minimis Safe HarborReg. Sec. 1.263(a)(1)(f)

• Annual election to follow book expense policy

− No more than $5,000 per invoice or item

− Written book policy must be in place at beginning of2014

− Con Edison did not elect to adopt safe harbor

− Book policy is to capitalize all materials and suppliesassigned to capital projects

17

Costs incurred to facilitate acquisitions of real or personal property-Reg. Sec. 1.263(a)-2(f)(2)(ii)• Inherently facilitative costs must be capitalized

a) Transporting the property (for example, shipping fees and movingcosts);

b) Securing an appraisal or determining the value or price of property;

c) Negotiating the terms or structure of the acquisition and obtainingtax advice on the acquisition;

d) Application fees, bidding costs, or similar expenses;

e) Preparing and reviewing the documents that effectuate theacquisition of the property (for example, preparing the bid, offer,sales contract, or purchase agreement);

f) Examining and evaluating the title of property;18

10

Costs incurred to facilitate acquisitions of real or personal property-Reg. Sec. 1.263(a)-2(f)(2)(ii)• Inherently facilitative costs must be capitalized (cont’d)

g) Obtaining regulatory approval of the acquisition or securing permitsrelated to the acquisition, including application fees;

h) Conveying property between the parties, including sales andtransfer taxes, and title registration costs;

i) Finders’ fees or broker’s commissions, including contingency fees(defined in paragraph (f)(3)(iii) of this section);

j) Architectural, geological, survey, engineering, environmental, orinspection services pertaining to particular properties; or

k) Services provided by a qualified intermediary or other facilitator ofan exchange under section 1031

19

Costs incurred to facilitate acquisitions of real or personal property-Reg. Sec. 1.263(a)-2(f)(2)(ii)

• Employee compensation and overhead costs aretreated as non-facilitative costs

− Some costs are capitalized as mixed service costs

− Investigatory costs for real estate are tax deductible

• Con Edison currently compliant with this regulation

20

11

Tangible property – improvementsReg. Sec. 1.263(a)-3• Most capitalize amounts paid to improve a unit of property

− Results in a betterment to the unit of property Corrects a pre-existing material condition or defect Results in a material addition Results in a material increase in capacity, strength, quality or output 23 examples in Reg. Sec. 1.263(a)-3(j)(3)

− Restores a unit of property Replaces a component for which a loss is claimed Repairs damage related to claimed casualty loss Replaces component for which tax basis adjusted in gain or loss

transaction Repairs unit of property to ordinarily efficient operating condition Rebuilds unit of property to “like new” condition at the end of its class life Replaces major component or substantial structural part of a unit of

property 31 examples in Reg. Sec. 1.263(a)-3(k)(7) 21

Tangible property – improvementsReg. Sec. 1.263(a)-3• Most capitalize amounts paid to improve a unit of property (cont’d)

− Adopts a unit of property to a new or different use New use inconsistent with intended use when originally placed in

service 7 examples in Reg. Sec. 1.263(a)-3(l)(3)

• What is a unit of property? - Reg. Sec. 1.263(a)- 3(e)(3)(i)− General rule: All components of property that are functionally

interdependent comprise a single unit of property

− Functional interdependence means the placing in service of onecomponent is dependent on the placing in service of another component

• Unit of property for network assets – Reg. Sec. 1.263(a)-3e(3)(iii)− Refers taxpayer to other guidance− Con Edison follows Rev. Proc. 2011-43 22

12

Tangible property – improvementsReg. Sec. 1.263(a)-3• Improvements to buildings and structural components. Reg. Sec.

1.263(a)- 3(e)(2)− Each of the following structural components of a building is separate from

the building structure, and the improvement rules must be applied separately to each component

• Con Edison filed a Form 3115 to elect application of this Reg. − No Sec. 481 adjustment was required 23

HVACMotors, compressors, boilers, chillers, pipes,

ducts

PlumbingPipes, drains, sinks,

bathtubs, toilets, water/sewer equipment

ElectricalWiring, outlets, junction boxes, lighting fixtures

Fire Protection/Alarm

Sprinklers, computer controls, fire

doors/escapes

SecurityDoor locks, security cameras, security

lighting, alarm system

ElevatorAll building elevators

GasPipes and equipment used to distribute gas

EscalatorAll building escalators

OtherRoof, walls, foundation,

windows, doors

Reg. Sec. 1.263(a)- 3(e)(2)(B)

Tangible property – repairs safe harborsReg. Sec. 1.263(a)-3(i)(l)(i) and (ii)• Routine maintenance safe harbor for plant assets -

Reg. Sec. 1.263(a)- 3(i)(l)(i) and (ii)

− Routine maintenance expenses are deductible if taxpayer can reasonably expect to perform the activity more than once during property’s class life

− Must incur cost to keep asset in its ordinary and efficient operating condition as a result of taxpayer’s use

− Routine maintenance does not apply if expense constitutes a betterment to a unit of property

− Routine maintenance does not apply to most restorations where the taxpayer reported a gain or loss on the sale or exchange of a component part

− Routine maintenance does not apply where the taxpayer claims a casualty loss on a component part

24

13

Tangible property – repairs safe harborsReg. Sec. 1.263(a)-3(i)(l)(i) and (ii)

•Routine maintenance safe harbor for buildings− Same rule as mentioned above except that taxpayer

must reasonably expect to perform the activity more than once during a 10 year period beginning on the date the building is placed in service

•Con Edison filed an accounting method change toadopt routine maintenance rules− No Sec. 481 adjustment was required

25

Tangible property regulations –depreciation and dispositionsReg. Sec. 1.168(i)-8• General Asset Accounts (GAA)

− Establish GAAs with assets of similar depreciation methods,recovery periods, conventions

Depreciated as one asset

No loss recognized upon the disposition of one asset in the accounts

Amounts realized on disposition are recognized as ordinary income

• Con Edison not electing GAA

• Dispositions (not in GAA)− Generally, dispositions do not include partial dispositions (e.g.

structural components of a building)

− May not claim both a repair and a loss on disposition on same asset

26

14

Tangible property regulations –depreciation and dispositionsReg. Sec. 1.168(i)-8

• Dispositions (put in GAA) (cont’d)− For electric transmission and distribution assets, Con Edison claims

repair deductions

− For repaired assets, Con Edison adds back to taxable income bookretirement costs

− Optional election to recognize partial dispositions

For buildings, gas, and steam assets, Con Edison will make partialdisposition gain or loss election

Will capitalize improvements and report gain or loss on retiredcomponent

27

Con Edison 2014 Action Steps needed to comply with Tangible Property Regs.1. Calculate and claim tax deprecation on rotable spare

parts

2. File Form 3115 to change accounting method to deductnon-incidental parts acquired in 2014

− No Sec. 481(a) adjustment required

3. File Form 3115 to adopt units of property for buildingsand structural components

− No Sec. 481(a) adjustment required

4. File Form 3115 to adopt routine maintenance safe harborfor plant assets and for buildings

5. File an annual election to recognize partial dispositionson components of buildings and structural components

28

15

Tax Repairs: Regulations Timeline

• In 2004, Treasury opened a reg project

– Proposed regs 2006

– Re-proposed regs 2008

– Temporary regs 2011

– Final regs 2013

• Effective 2014 (optional early adopt)

– Critical to regs to CEI

• 2011-43 (Electric T&D)

• 2013-24 (Generation)

Tax Repairs: Points of consideration

• UOP

• Establishing thresholds

• Historical books and records and the 481(a)

• FIN 48

• Rate Base

16

Tax Repairs: Network Assets and Industry Guidance

“In the case of network assets, the unit of property isdetermined by the taxpayer’s particular facts andcircumstances except as otherwise provided in publishedguidance. For these purposes, the functionalinterdependence standard is not determinative.”

Tax Repairs: Electric T&D

• Rev. Proc. 2011-43

– August 19, 2011

• Elective safe harbor

• Defined UOPs

– Linear

– Non-linear

• Thresholds

– 10%

– Aggregation rules

17

Tax Repairs: Generation

• Rev. Proc. 2013-24

– April 30, 2013

• Defined UOPs

• Defined major components

– Did not address portion of a major component

• Automatic change

• Permits extrapolation

Tax Repairs: Gas T&D

• UOPs

– Transmission

• Hydraulic subsystem (pipe between compressors)

• Same pressure

– Distribution

• None – simplified procedure

– Non-linear

• Detailed listing

• Major components

• Threshold

– Transmission – 10%

– Distribution - 4 miles

18

Tax Repairs: Gas T&D

• Per se capital

– Customer Expansion

– System Expansion

– Add cathodic protection where none existed

• Aggregation

– Same hydraulic subsystem (T) or zip code (D)

– Document (PUC order or project authorization)

• Identifies UOPs or locations for replacements

• Identifies total cost or amount of pipe and

• Describes replacements w/in 5 years

Five-Year Growth:CEI Accumulated Deferred Tax Summary2009 vs. 2014

36

Dec. 31, 2009 Dec. 31, 2014 Increase

(millions) (millions) (millions)

Accumulated deferred income tax liability $ 4,239 $ 6,676 $ 2,437

Deferred tax liability future income tax 1,317 2,275 958

Accumulated deferred Investment Tax Credits 66 125 59

Total deferred tax liability per Form 10‐K $ 5,622 $ 9,076 $ 3,454

Five‐year increase 61%

Major contributors to the increase is primarily plant-related:• Accelerated tax depreciation (method and life)• Bonus depreciation• Repairs

19

Impact of Deferred Income Taxes on Rate Regulated Business Deferred income taxes decreased the revenue requirement in the

latest rate cases as follows:

37

CECONY* O&R***2015 2016 2016

Rate Base Amounts per Rate Orders Electric Gas Steam Electric** Gas Steam Electric Gas(millions)Net utility plant $ 20,659 $ 4,754 $1,861 $ 21,692 $ 5,155 $ 1,901 $ 957 $ 498 Working capital 816 93 91 890 97 95 46 22Regulatory assets and liabilities 202 47 (34) (90) 61 (18) (32) (22)Accumulated deferred income taxes (3,564) (1,031) (371) (4,211) (1,077) (374) (208) (132)

Total Rate Base $ 18,113 $ 3,863 $1,547 $ 18,281 $ 4,236 $ 1,604 $ 763 $ 366

Pre-tax rate of return 9.98% 10.06% 10.06% 9.70% 10.14% 10.14% 9.89% 9.89%

Accumulated deferred income taxes reduced rate base by: $ (3,564) $ (1,031) $ (371) $ (4,211) $ (1,077) $ (374) $(208) $(132)

Decrease in revenue requirement $ (355) $ (103) $ (37) $ (408) $ (109) $ (38) $ (20) $ (13)

* Per Joint Proposal for cases 13-E-0030, 13-G-0031, and 13-S-0032** Per one-year extension Joint Proposal

*** Per Joint Proposal for cases 14-E-0493 and 14-G-0494

Section 4 Click to jump back to Table of Contents

9/16/2016

1

Cost Segregation Studies, Updates on the Tangible Property Regulations,

Depreciation, & The PATH Act

© MS Consultants, LLC 2016

Cost Segregation Studies & Tangible Property Regulations

David A. FabianDirector, MS Consultants LLC

Office: 716‐633‐9840Cell : 716‐573‐9378Fax : 716‐633‐9469

© MS Consultants, LLC 2016

9/16/2016

2

David A. Fabian• 25+ years’ tax and accounting experience

• Joined MS Consultants in 1999

• Personally involved in over 7,500 Cost Segregation projects in more than 30 states

• Presented on a variety of topics including depreciation & cost segregation, energy modeling, tangible property regs, & more

• Developed comprehensive in-house training and quality control programs

© MS Consultants, LLC 2016

Ashley SullivanManager, MS Consultants LLC

Office: 757‐821‐3020Cell : 757‐705‐6264Fax : 716‐250‐6605

© MS Consultants, LLC 2016

9/16/2016

3

Ashley Sullivan• Over 12 years Cost Segregation experience

• Joined MS Consultants in 2013

• Heads up our Virginia office

• Senior Cost Segregation Professional designation with ASCSP

• Travels extensively nationwide to meet with clients and discuss opportunities

• Quality Control Manager for Cost Segregation Studies

© MS Consultants, LLC 2016

MS Consultants, LLC• We have completed over 12,000 studies nationwide.

• We’re made up of tax, construction, and engineering professionals.

• Years of experience:– Cost Segregation Studies since 1996– §179D certifications since 2006– §45L certification since 2008– Tangible Property Regulation analyses since 2008

© MS Consultants, LLC 2016

9/16/2016

4

What is a Cost Segregation Study?

• IRS approved method to acceleratedepreciation of specific assets

• Allocates a portion of “39 and 27.5 year”property into 5, 7, and 15 year property

• IRS Tax codes §1245 and §1250

Why perform a Cost Segregation Study?

• Taxpayers under‐depreciate their assets, because…

• Rules are very complex• Properly segregating a property is a complex

process, requiring the right combination of know‐how:o Tax expertise and familiarity with prior tax litigationo Engineering and construction knowledge

9/16/2016

5

Cost Segregation Example

Client purchases a building for $5,000,000 in 2013, and has taken depreciation over 39 years.

Example: Medium-Size Office Building

9/16/2016

6

Example:Office Building - Acquisition

100,000500,000750,000

3,650,000

$325,950 $763,369 $437,419$258,710

$258,710

$366,266

$5,000,000

Example:Office Building – New Construction

100,000500,000750,000

3,650,000

$325,950 $1,175,656 $849,706$426,381

$426,381

$446,653

$5,000,000

9/16/2016

7

Real Property: 27.5 or 39 Year(Structural Components)

• HVAC units • Ceramic tile floors• Exterior doors• Windows• Interior plumbing• Siding• Concrete flatwork & foundations• Roof

HVAC Units

Ceramic Tile

Siding

Concrete flatwork& foundations

Exterior Doors & Windows

Roofs

Interior Plumbing

Where does the money come from?

9/16/2016

8

15-year Property(Land Improvements)

• Removable site improvements• Certain Site utilities & drainage• Fencing & gates• Paving & Striping• Landscaping• & More

Where does the money come from?

Paving

Sidewalks, Stepsand Curbing

Retaining Walls

Site Lighting

Trees, Landscapingand Irrigation

Grid Striping andPavement Symbols

Flagpoles

Benches and otherOutdoor equipment

15-year PropertyLand Improvements

& More

9/16/2016

9

Other 5- & 7-year Property(Personal Property)

• Specialty plumbing & electric• Decorative wall coverings• Carpet and other removable flooring• Decorative lighting• Trim, cabinetry & millwork• Window treatments• & More

Where does the money come from?

Decorative Trim

Decorative andaccent lighting

Window Treatments

Decorative wood panels, wallpaperAnd other wallcoverings

Specialty electricand plumbing

Carpet andremovable flooring

5-year Property–Personal Property

& Much, Much More

9/16/2016

10

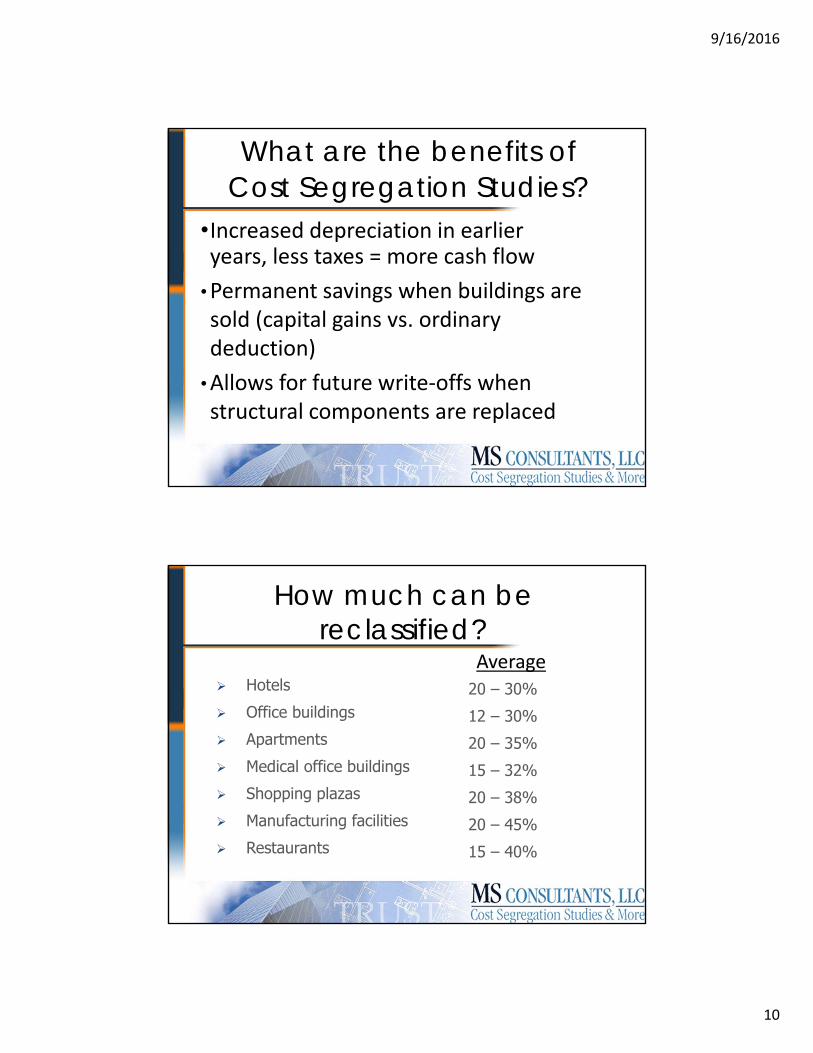

What are the benefits of Cost Segregation Studies?

•Increased depreciation in earlieryears, less taxes = more cash flow

•Permanent savings when buildings aresold (capital gains vs. ordinarydeduction)

•Allows for future write‐offs whenstructural components are replaced

How much can be reclassified?

Average Hotels Office buildings Apartments Medical office buildings Shopping plazas Manufacturing facilities Restaurants

20 – 30%12 – 30%20 – 35%15 – 32%20 – 38%20 – 45%15 – 40%

9/16/2016

11

What buildings are eligible?

• New buildings under construction• Existing buildings undergoing renovations

and/or additions• Purchases of existing properties• Buildings purchased or constructed since

1987• Inherited buildings

Types of Cost Segregation Studies Performed

Airport Hangars Apartment Buildings Automobile Dealerships Automobile Service

Centers Banks Casual & Fine Dining

Restaurants Daycare Centers Department Stores Distribution Centers

Fast Food (QuickService) Restaurants

Fitness Centers Flex Industrial Gas Stations Golf Resorts Grocery Stores Healthcare Centers High Rise Buildings Hospitals Hotels

Laboratory Facilities Manufacturing &

Processing Facilities Marinas Nursing Homes Office Buildings Retail Plazas Senior Assisted

Living Facilities Truck Terminals Warehouses ALL BUILDINGS

9/16/2016

12

Updates on TPRs, Depreciation, & PATH Act

MS Consultants, LLC

Updates – Top 10• TPR Today• Form 3115 Changes• De Minimis• Bonus Depreciation• 15 year Qs• QIP• Section 179 & 179 on Real Estate• Repairs & Dispositions• Recent Rev Procs• Section 179D / 45L

9/16/2016

13

TPR - Updates

• Taxpayers willing to pay for services• Many taxpayers took advantage of opportunities for large tax savings

• But some taxpayers and practitioners ignored the rules (only 500k‐600k 3115’s filed)

• Most of the provisions in the TPR’s can be utilized in 2015 and forward

TPR - Updates

• Rev‐Proc 2015‐56 Safe Harbor for betterment, restoration and adaptation tests (75/25)

• New de minimis amount ‐ Notice 2015‐82• Rev‐Proc 2016‐29 – Automatic Change Updates

• New Form 3115 Application for Change in Accounting method

© MS Consultants, LLC 2016

9/16/2016

14

Common 3115 filings

• They are automatic if assigned a methodnumber – also no filing fee

• Fix bonus election problems (CHANGE #7)• Write‐off prior improperly capitalized repairs(CHANGE #184)

• CHANGE #196 for late PAD – Expired 2014

© MS Consultants, LLC 2016

Common 3115 filings

• Write‐off replaced structural componentscurrently being depreciated (CHANGE #205)

• Write‐off replaced non‐structural componentscurrently being depreciated (CHANGE #206)

• Write‐off current or future removal costsassociated with an improvement (CHANGE #21)

© MS Consultants, LLC 2016

9/16/2016

15

3115 Updates for 2015

• File one signed original with timely filed return• Send one signed original to Kentucky (previouslywas Utah)

• 12 spaces for concurrent designated changenumbers (previously was one line)

• New instructions caution not to rely only on theinstructions, must go to website to determine ifthere has been any newly published guidance

© MS Consultants, LLC 2016

De minimis

• Rules• Updates

© MS Consultants, LLC 2016

9/16/2016

16

De minimis Expensing Rule-1.263(a)-1(f)

– Definition:– Useful life less than 12 months

» OR

– Property costing less than certain dollar amount» AND

– Must be expensed on books/financial statements

© MS Consultants, LLC 2016

De minimis Expensing Rule-1.263(a)-1(f)

• 3 Thresholds:–Applicable Financial Statements‐(AFS)‐$5,000

–No written policy, if consistently applied ‐$2,500 (raised from $500) – Effective01/01/16….or earlier.

–Do nothing ‐$200

© MS Consultants, LLC 2016

9/16/2016

17

De minimis Expensing Rule-1.263(a)-1(f)

• Written Capitalization Policy

• For tax years beginning _________, and forward, (Name of Business) elects to treat as an expense for both book and income tax purposes property with a cost of $____________ or less, including items that have a useful life of 12 months or less. It is (Name of Business’s) intention that this election complies with the IRS Section 1.263(a)‐1(f) de minimis safe harbor election.

© MS Consultants, LLC 2016

De minimis Expensing Rule-1.263(a)-1(f)

• A taxpayer can elect to apply the de minimis rule in one year and not the next

• The de minimis safe harbor is elected annually by including a statement on the taxpayer’s tax return (including extensions) for the year elected

© MS Consultants, LLC 2016

9/16/2016

18

Safe Harbor Election• Statement must be attached annually to a timelyfiled (including extensions) income tax return

• Statement must be titled “Section 1.263(a)‐1(f)de minimis safe harbor election” and contain thefollowing information:– Taxpayer’s name– Taxpayer’s address– Taxpayer identification number– Statement that the taxpayer is making the de minimissafe harbor election under Section 1.263(a)‐1(f)

© MS Consultants, LLC 2016

Tax tips

• Elect de minimis annually• Have all clients set up capitalization policiesand include in permanent tax file

• Obtain separate invoices for shippinginstallation etc. to keep below thresholds

© MS Consultants, LLC 2016

9/16/2016

19

• Bonus Depreciation rules:– 50% deduction (currently)– Must be a new Unit of Property– Original use of the Unit of Property must beginwith the taxpayer

– Must have a depreciable life less than 20 years• Personal property, land improvements• Importance of Cost Segregation Studies

– Can elect out by recovery class© MS Consultants, LLC 2016

• Bonus has been extended thru 2019• 2015 = 50%• 2016 = 50%• 2017 = 50%• 2018 = 40%• 2019 = 30%• This will allow for more effective tax planning

© MS Consultants, LLC 2016

9/16/2016

20

• The Act retroactively extends and makes permanentthe 15 year straight line depreciation option for:

• Qualified Leasehold Improvement Property (QLI)• Qualified Restaurant Property (QRP)• Qualified Retail Improvement Property (QRIP)

© MS Consultants, LLC 2016

Qualified Leasehold Improvement Property

– QLI property includes• Code Sec. 1250 property

– The improvement is made "under or pursuant toa lease”

– The portion of the building is to be occupiedexclusively by the lessee

– The improvement is placed in service more than3 years after the date the building was firstplaced in‐service

9/16/2016

21

Qualified Leasehold Improvement Property

– QLI property DOES include:

• Plumbing and electrical systems• Drywall• Ceramic tile• Lighting fixtures• Acoustic ceiling tiles• & more

Qualified Leasehold Improvement Property

– QLI property DOES NOT include:

• enlargement of the building• any elevator or escalator• any structural component benefiting acommon area

• the internal structural framework of thebuilding

9/16/2016

22

Qualified Leasehold Improvement Property

• Qualified Leasehold Improvements

– 09/11/01 – 10/22/04 – 39 year QLI qualifies for Bonus

– 10/23/04 – 12/31/04 – 15 year QLI qualifies for Bonus– 01/01/05 – 12/31/07 – 15 year QLI – NO Bonus– 01/01/08 – 12/31/13 – 15 year QLI qualifies for Bonus– 01/01/14 – permanent – 15 yr QLI qualifies for Bonus

© MS Consultants, LLC 2016

Qualified Restaurant Property– QRP includes:

–An improvement to a building, if more than50% of the building's square footage isdevoted to preparation of, and seating foron‐premises consumption of, preparedmeals.

–Can be related party

9/16/2016

23

Qualified Restaurant Property– QRP includes:

– Interior Improvements only ‐ 2004‐2008– Interior and exterior, including all 1250property – 2009‐current

–No 3year rule, meaning QRP is applicable fora newly constructed restaurant – 2009‐current

Qualified Restaurant Property

• Qualified Restaurant Property

– 10/23/04 – 12/31/07 – 15 year QRP – NO Bonus– 01/01/08 – 12/31/08 – 15 year QRP qualifies for Bonus– 01/01/09 – 12/31/13 – 15 year QRP – NO Bonus– 01/01/14 – permanent – 15 year QRP – NO Bonus

– Rev Proc. 2011‐26 – QRP is bonus eligible if meets the“dual characteristic” test of QLI

© MS Consultants, LLC 2016

9/16/2016

24

Qualified Retail Improvement Property

– QRIP

–open to the general public and is used in theretail trade or business of selling tangiblepersonal property to the general public,

–placed in service more than 3 years after thedate the building was first placed in service.

–made by the owner of that improvement willbe qualified retail improvement property

Qualified Retail Improvement Property

• Qualified Retail Improvement Property

– 01/01/09 – 12/31/13 – 15 year QRIP – NO Bonus

– 01/01/14 – permanent – 15 year QRIP – NO Bonus

– Rev Proc. 2011‐26 – QRIP is bonus eligible if meets the“dual characteristic” test of QLI

© MS Consultants, LLC 2016

9/16/2016

25

Qualified ImprovementProperty

• New “Q” on the block – effective 01/01/16

– Similar to QLI• Bonus eligible• Can be 15‐yr SL

– Also can be 39‐yr with BONUS– No in service requirement pursuant to a lease

• Eligible for your own building

– No 3 year old requirement• Improvements still have to be done after building is PIS

© MS Consultants, LLC 2016

Qualified ImprovementProperty

• New “Q” on the block

– Example• An internal improvement (structural component) thatbenefits a common area does not qualify for a 15‐yrrecovery period in the case of a leased buildingproperty or a retail building. HOWEVER, QI propertydoes not contain this restriction. Therefore, such aninternal improvement to a common area maynevertheless qualify for bonus depreciation as qualifiedimprovement property.

© MS Consultants, LLC 2016

9/16/2016

26

Qualified ImprovementProperty

• QLI, QRP, QRIP all have been made permanentwith the PATH act

• QIP has been introduced as part of the Bonusdepreciation extensions. Will QIP expire atthe end of 2019?

• Enhanced section 179 deduction was madepermanent

• Maximum deduction set at $500,000• Phase‐out threshold set at $2,000,000• For tax years after 2015, the amounts will beindexed for inflation– 2016 = $500,000 on $2,010,000

© MS Consultants, LLC 2016

9/16/2016

27

• An eligible Unit of Property has to be “New toYou”. So it can be “used” property, unlikeBonus eligible property must be new

• Must be used at least 50% for business in thefirst year it is placed in service

• Tangible personal property• Section 179 cannot create a loss

– Carryforwards are available© MS Consultants, LLC 2016

Section 179 Planning– Taxpayer is allowed $500,000 (total)

• Includes any 179 expense on 1245 personalproperty (up to $500,000)

• Includes any 179 expense on 1250 (QLI, QRP, orQRIP) real property (up to $500,000 for 2016 &forward)

– Overall purchases limited to $2,000,000

9/16/2016

28

Section 179 Planning– Limitations:

• Can elect personal property only• If taxpayer elects both (PP & QP), a proportionate amount must be taken

– Example ahead• Husband and wife are treated as one taxpayer with regard to the maximum dollar limit

• Only available to your aggregate taxable income derived from the active conduct of any trade or business during the taxable year

Section 179 PlanningFor taxable years beginning in 2015, the provision extends the limitation on carryovers and the maximum amount available with respect to qualified real property of $250,000.

The provision removes the limitation related to the amount of section 179 property that may be attributable to qualified real property for taxable years beginning after 2015.

9/16/2016

29

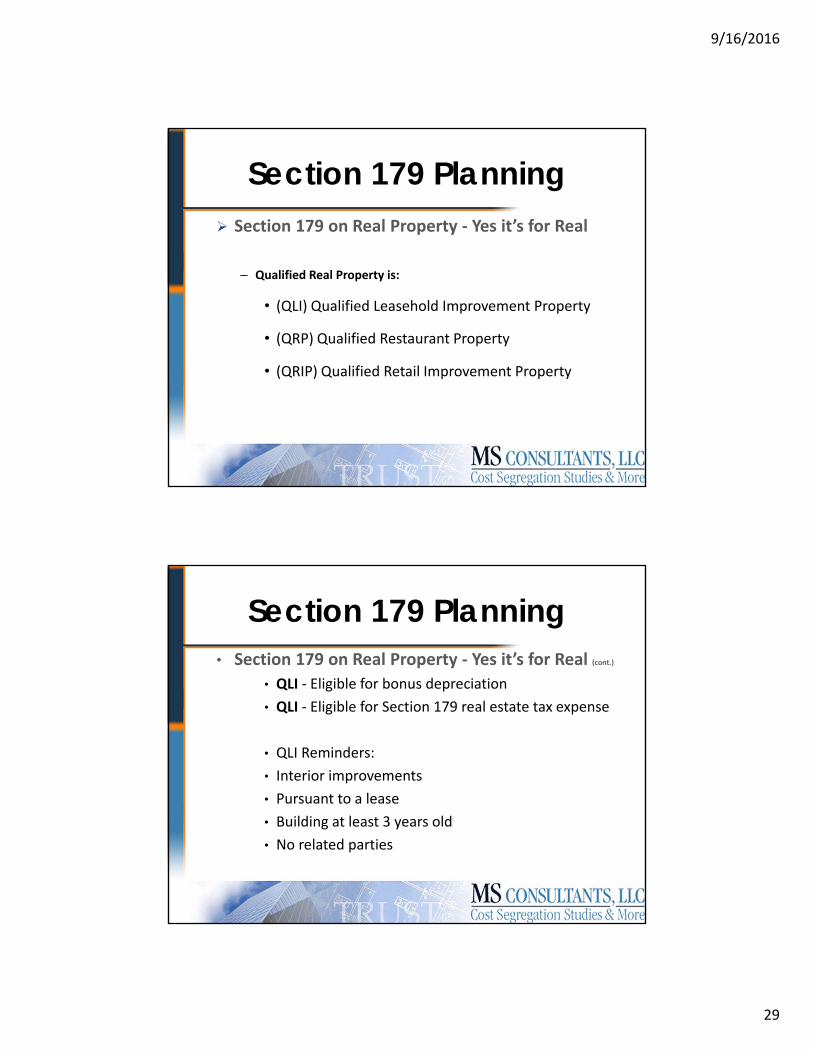

Section 179 Planning Section 179 on Real Property ‐ Yes it’s for Real

– Qualified Real Property is:

• (QLI) Qualified Leasehold Improvement Property

• (QRP) Qualified Restaurant Property

• (QRIP) Qualified Retail Improvement Property

Section 179 Planning• Section 179 on Real Property ‐ Yes it’s for Real (cont.)