Embed Size (px)

Citation preview

Sebastián Nieto Parra

Economist LAC Unit Development Centre

OECD

October 2015

INTEGRATING SECURITIES MARKETS TO BOOST COMPETITIVENESS

The Latin American Integrated Market – MILA DAY 2015

Contents

Key Challenge: Tackling the Middle Income Trap (MIT)1

Market Integration: a key asset to avoid the MIT2

Crucial role of Capital Markets3

Conditions and Benefits of Capital Markets Integration4

Contents

Key Challenge: Tackling the Middle Income Trap (MIT)

1

Market Integration: a key asset to avoid the MIT2

Crucial role of Capital Markets3

Conditions and Benefits of Capital Markets Integration4

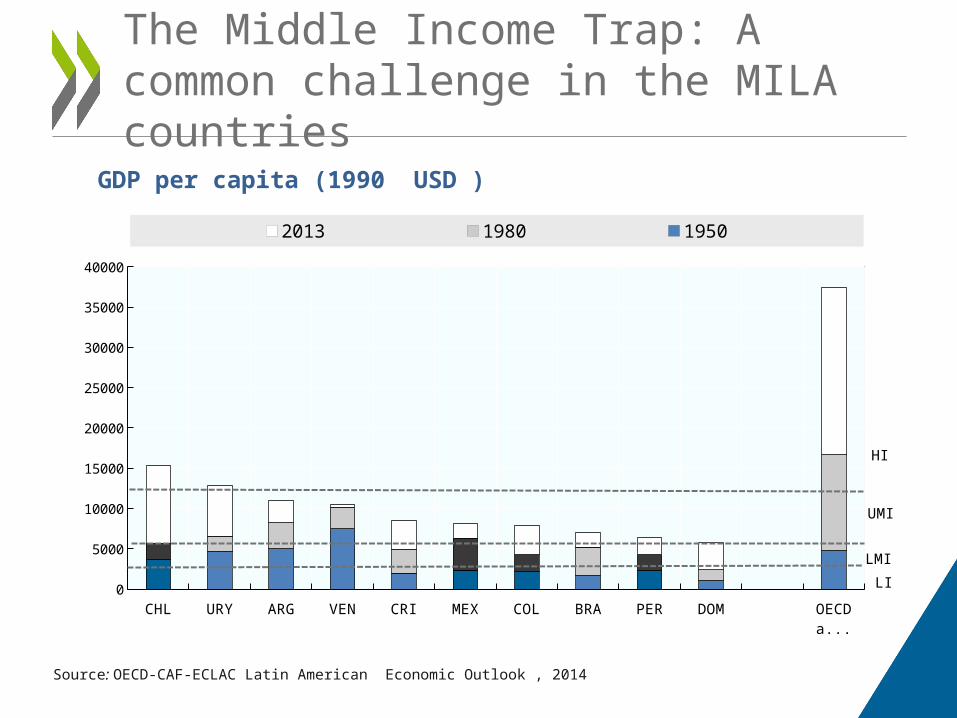

The Middle Income Trap: A common challenge in the MILA countries

Source: OECD-CAF-ECLAC Latin American Economic Outlook , 2014

GDP per capita (1990 USD )

CHL URY ARG VEN CRI MEX COL BRA PER DOM OECD average

0

5000

10000

15000

20000

25000

30000

35000

40000

2013 1980 1950

HI

UMI

LMI

LI

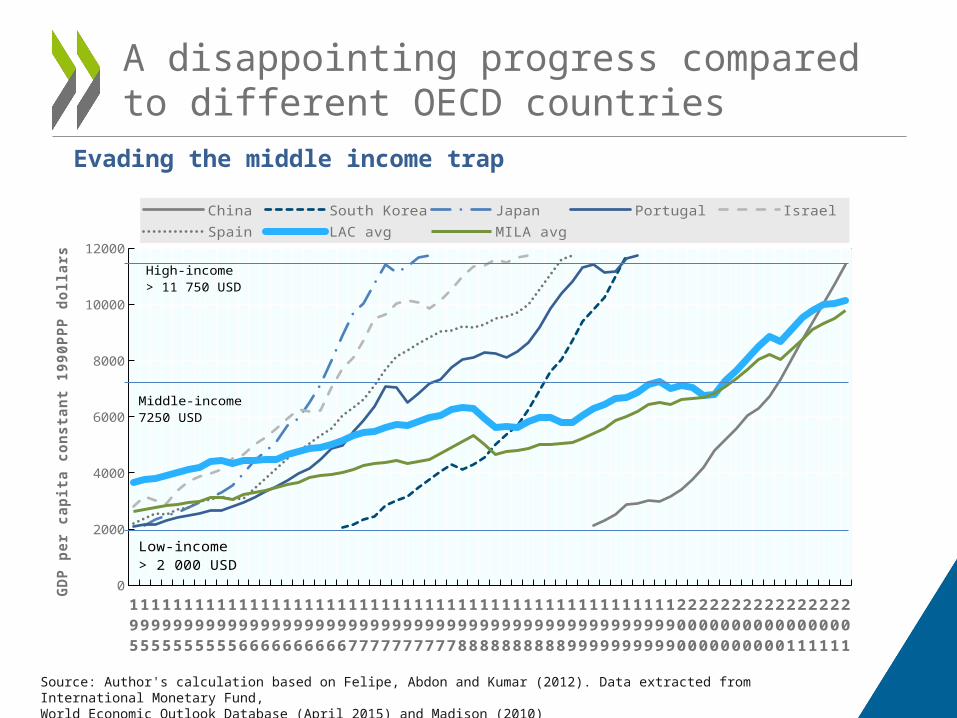

A disappointing progress compared to different OECD countries

Source: Author's calculation based on Felipe, Abdon and Kumar (2012). Data extracted from International Monetary Fund, World Economic Outlook Database (April 2015) and Madison (2010)

Evading the middle income trap

1950

1951

1952

1953

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

0

2000

4000

6000

8000

10000

12000

China South Korea Japan Portugal Israel

Spain LAC avg MILA avg

GD

P p

er c

apit

a c

on

sta

nt

1990P

PP

doll

ars

High-income> 11 750 USD

Middle-income7250 USD

Low-income> 2 000 USD

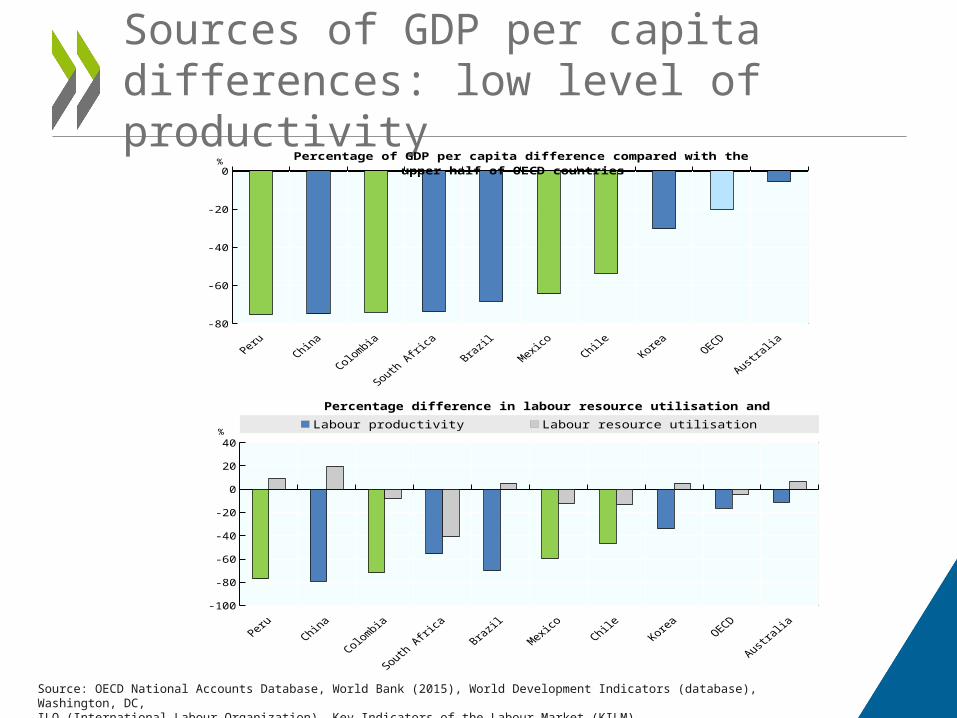

Sources of GDP per capita differences: low level of productivity

Peru China Colombia South Africa Brazil Mexico Chile Korea OECD Australia-80

-60

-40

-20

0

Percentage of GDP per capita difference compared with the upper half of OECD countries %

Source: OECD National Accounts Database, World Bank (2015), World Development Indicators (database), Washington, DC, ILO (International Labour Organization), Key Indicators of the Labour Market (KILM)

Peru China Colombia South Africa Brazil Mexico Chile Korea OECD Australia-100

-80

-60

-40

-20

0

20

40

Percentage difference in labour resource utilisation and labour productivity

Labour productivity Labour resource utilisation%

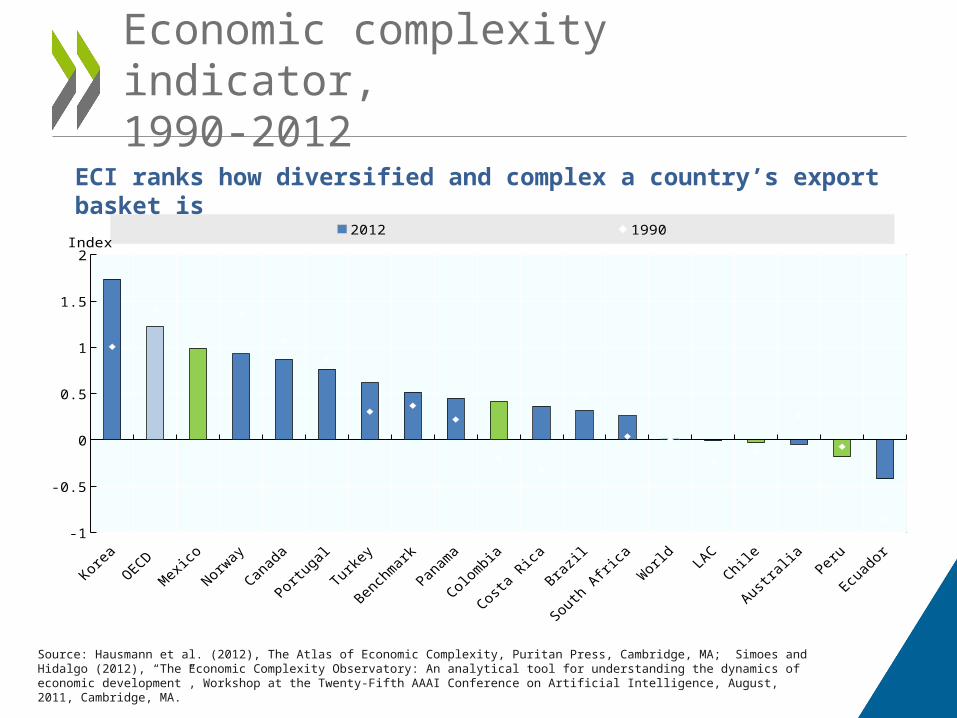

Economic complexity indicator, 1990-2012

Korea

OECD

Mexico

Norway

Canad

a

Portug

al

Turkey

Bench

mark

Panam

a

Colombia

Costa

RicaBraz

il

South

Africa

World

LAC

Chile

Austra

liaPeru

Ecuad

or-1

-0.5

0

0.5

1

1.5

2

2012 1990Index

ECI ranks how diversified and complex a country’s export basket is

Source: Hausmann et al. (2012), The Atlas of Economic Complexity, Puritan Press, Cambridge, MA; Simoes and Hidalgo (2012), “The Economic Complexity Observatory: An analytical tool for understanding the dynamics of economic development”, Workshop at the Twenty-Fifth AAAI Conference on Artificial Intelligence, August, 2011, Cambridge, MA.

Contents

Key Challenge: Tackling the Middle Income Trap (MIT)1

Market Integration: a key asset to avoid the MIT2

Crucial role of Capital Markets3

Conditions and Benefits of Capital Markets Integration4

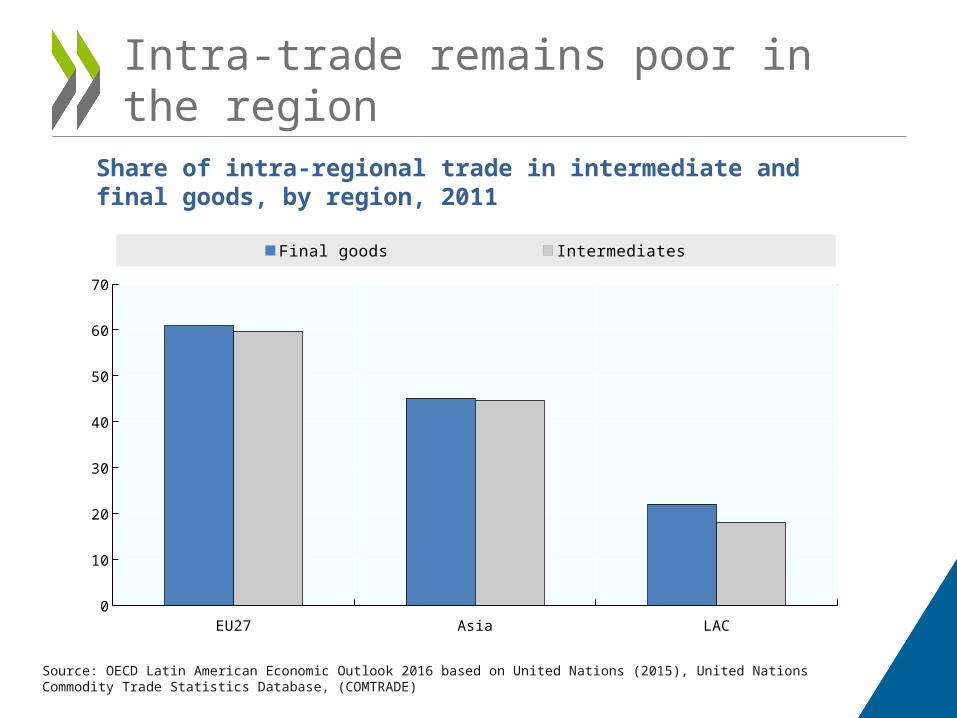

Intra-trade remains poor in the region

Share of intra-regional trade in intermediate and final goods, by region, 2011

EU27 Asia LAC0

10

20

30

40

50

60

70

Final goods Intermediates

Source: OECD Latin American Economic Outlook 2016 based on United Nations (2015), United Nations Commodity Trade Statistics Database, (COMTRADE)

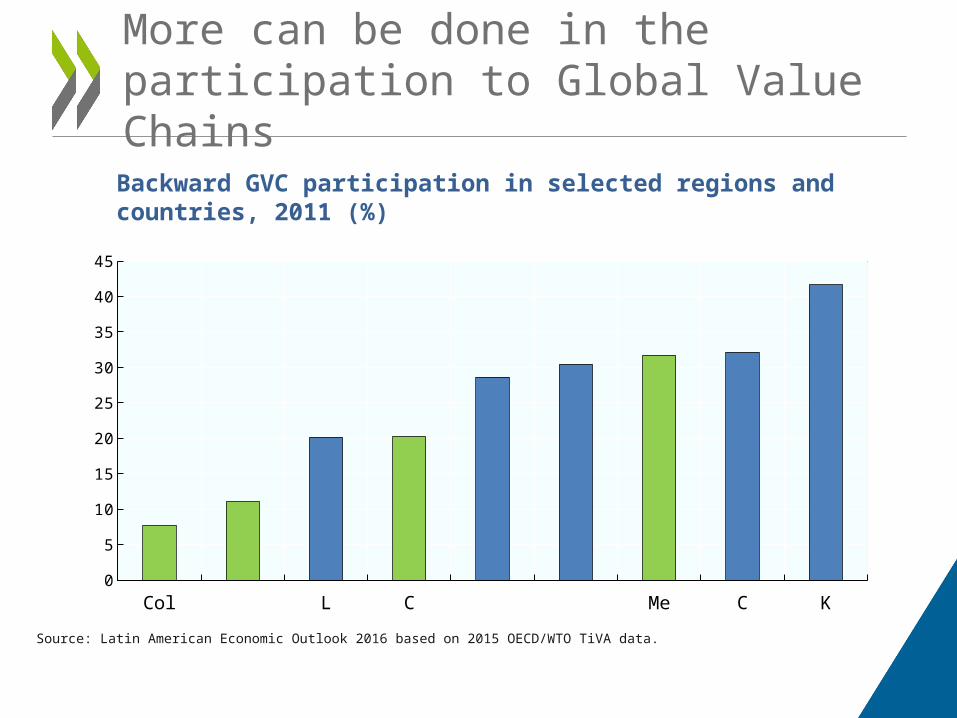

More can be done in the participation to Global Value Chains

Colombia Peru LAC 6 Chile EU27 Asia Mexico China Korea0

5

10

15

20

25

30

35

40

45

Backward GVC participation in selected regions and countries, 2011 (%)

Source: Latin American Economic Outlook 2016 based on 2015 OECD/WTO TiVA data.

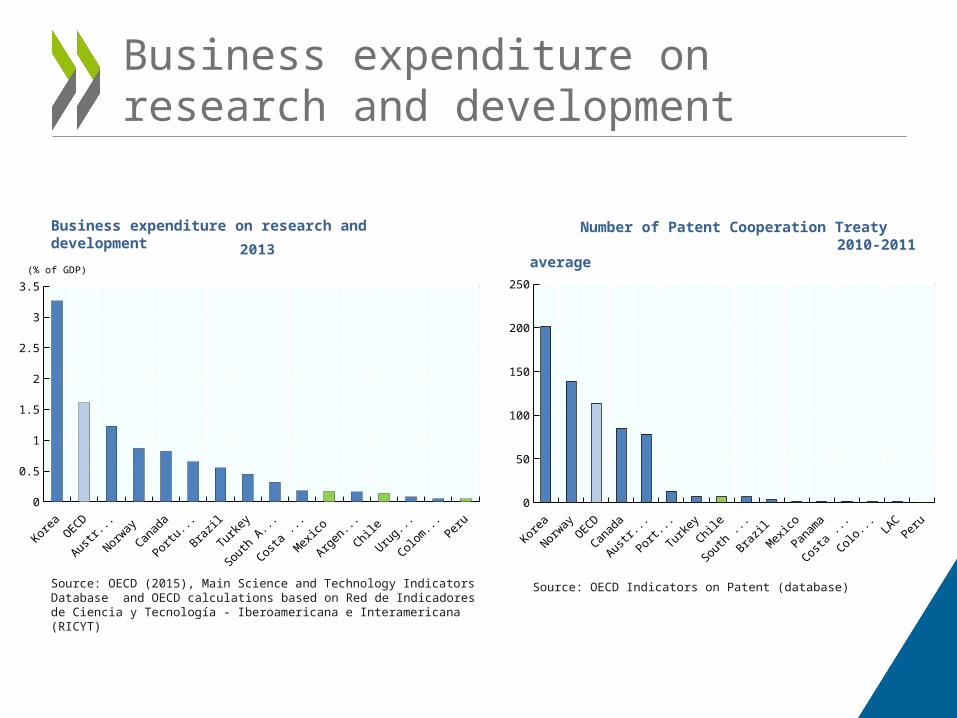

Business expenditure on research and development

Korea

OECD

Australi

a

Norway

Canada

Portuga

l Braz

il

Turkey

South A

frica

Costa R

ica

Mexico

Argentin

aChile

Uruguay

Colombia

Peru

0

0.5

1

1.5

2

2.5

3

3.5

2013(% of GDP)

Korea

Norway

OECDCana

da

Australi

a

Portuga

l

Turkey

Chile

South A

frica

Brazil

Mexico

Panama

Costa R

ica

Colombia LA

CPeru

0

50

100

150

200

250

Number of Patent Cooperation Treaty 2010-2011 average

Source: OECD Indicators on Patent (database)

Business expenditure on research and development

Source: OECD (2015), Main Science and Technology Indicators Database and OECD calculations based on Red de Indicadores de Ciencia y Tecnología - Iberoamericana e Interamericana (RICYT)

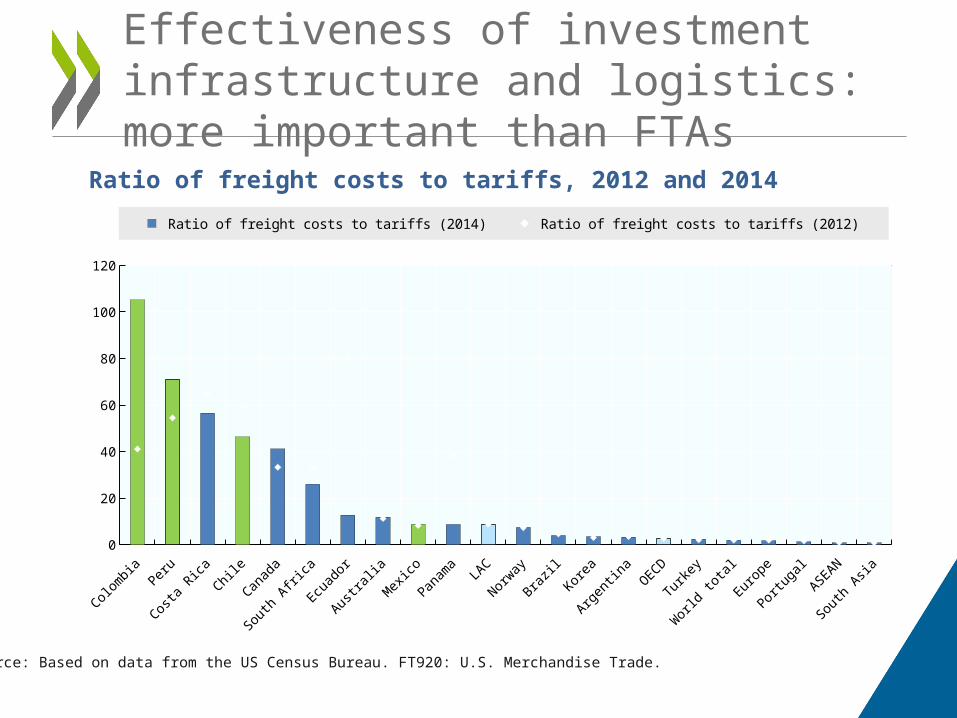

Effectiveness of investment infrastructure and logistics: more important than FTAs

Ratio of freight costs to tariffs, 2012 and 2014

Source: Based on data from the US Census Bureau. FT920: U.S. Merchandise Trade.

Colombia Peru

Costa R

ica Chile

Canad

a

South

Africa

Ecuado

r

Austral

iaMexi

co

Panam

aLA

C

Norway

Brazil

Korea

Argentin

aOECD

Turkey

World t

otal

Europe

Portug

al

ASEAN

South

Asia0

20

40

60

80

100

120

Ratio of freight costs to tariffs (2014) Ratio of freight costs to tariffs (2012)

Contents

Key Challenge: Tackling the Middle Income Trap (MIT)1

Market Integration: a key asset to avoid the MIT2

Crucial role of Capital Markets3

Conditions and Benefits of Capital Markets Integration4

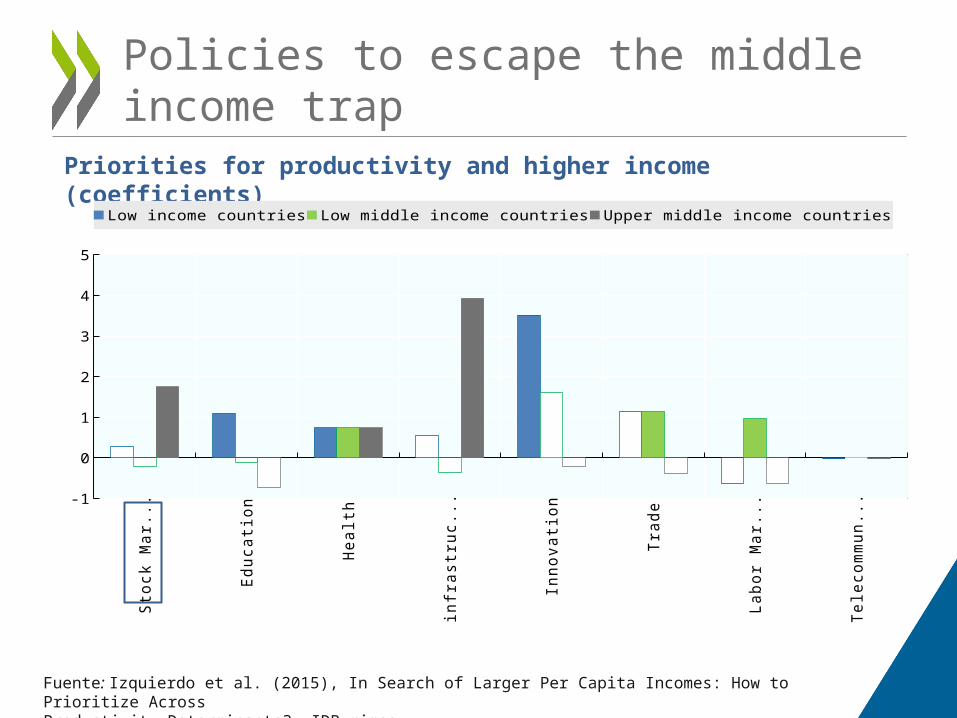

Priorities for productivity and higher income (coefficients)

Fuente: Izquierdo et al. (2015), In Search of Larger Per Capita Incomes: How to Prioritize Across Productivity Determinants?, IDB mimeo.

Policies to escape the middle income trapS

tock

Mar

kets

Edu

catio

n

Hea

lth

infra

stru

ctur

e

Inno

vatio

n

Trad

e

Labo

r Mar

kets

Tele

com

mun

icat

ion-1

0

1

2

3

4

5

Low income countries Low middle income countries Upper middle income countries

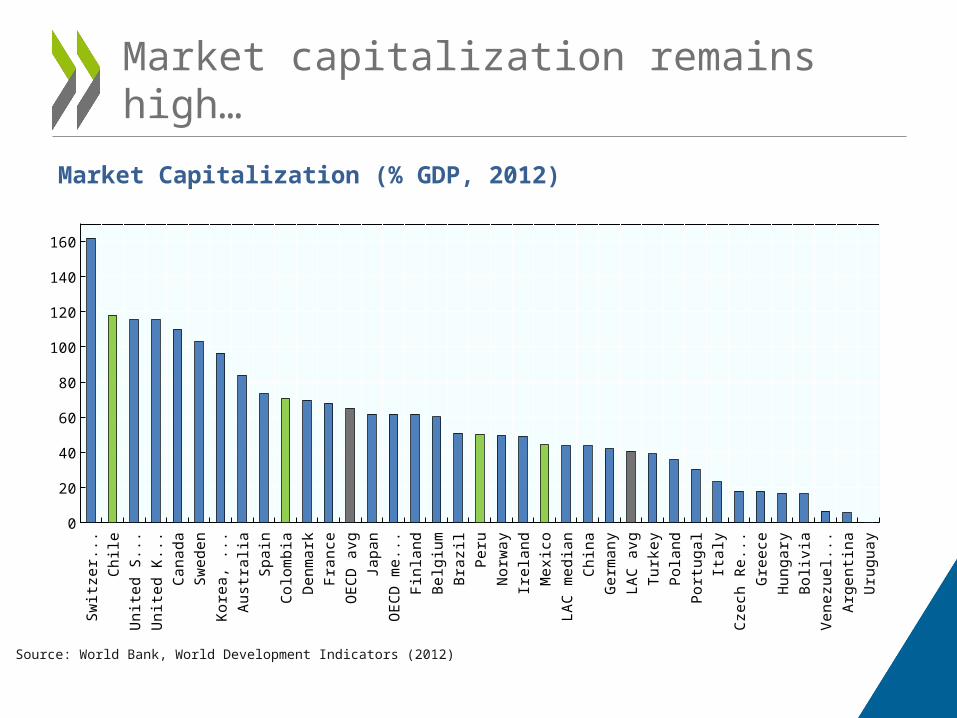

Market Capitalization (% GDP, 2012)

Source: World Bank, World Development Indicators (2012)

Switz

erla

ndC

hile

Uni

ted

Stat

esU

nite

d Ki

ngdo

mC

anad

aSw

eden

Kore

a, R

ep.

Aust

ralia

Spai

nC

olom

bia

Den

mar

kFr

ance

OEC

D a

vgJa

pan

OEC

D m

edia

nFi

nlan

dBe

lgiu

mBr

azil

Peru

Nor

way

Irela

ndM

exic

oLA

C m

edia

nC

hina

Ger

man

yLA

C a

vgTu

rkey

Pola

ndPo

rtuga

lIta

lyC

zech

Rep

ublic

Gre

ece

Hun

gary

Boliv

iaVe

nezu

ela,

RB

Arge

ntin

aU

rugu

ay

0

20

40

60

80

100

120

140

160

Market capitalization remains high…

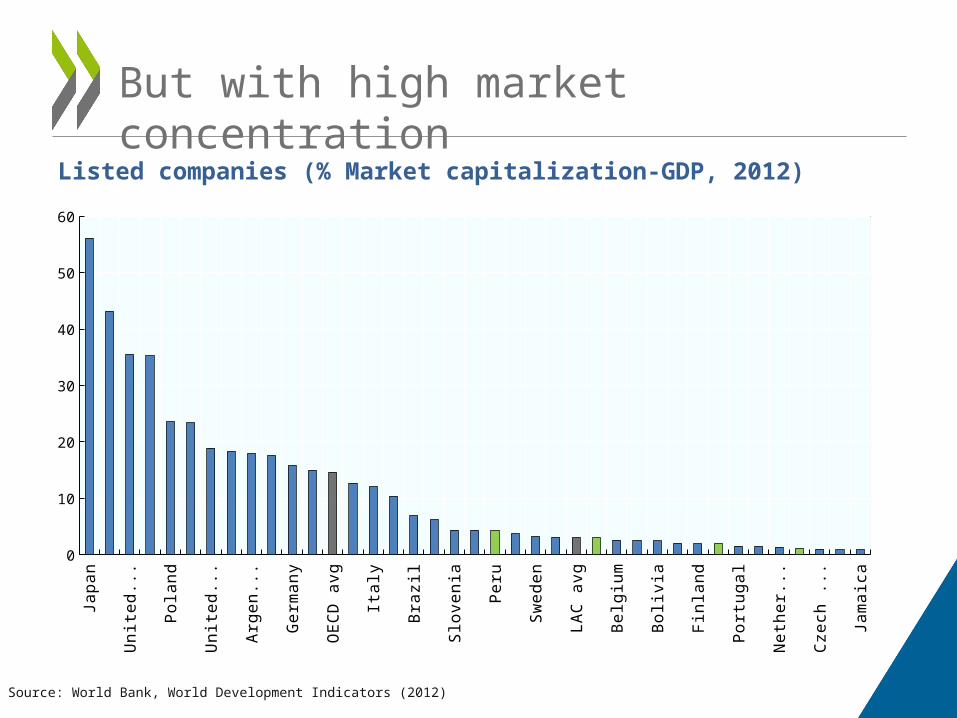

Listed companies (% Market capitalization-GDP, 2012)

Source: World Bank, World Development Indicators (2012)

Japa

nSp

ain

Unite

d St

ates

Cana

daPo

land

Aust

ralia

Unite

d Ki

n...

Kore

a, R

ep.

Arge

ntin

aUr

ugua

yG

erm

any

Gre

ece

OEC

D av

gFr

ance

Italy

Turk

eyBr

azil

Vene

zuel

a, R

BSl

oven

iaO

ECD

med

ian

Peru

Norw

aySw

eden

Hung

ary

LAC

avg

Mex

ico

Belg

ium

Denm

ark

Boliv

iaLA

C m

edia

nFi

nlan

dCh

ilePo

rtuga

lSw

itzer

land

Neth

erla

nds

Colo

mbi

aCz

ech

Repu

...Ire

land

Jam

aica

0

10

20

30

40

50

60

But with high market concentration

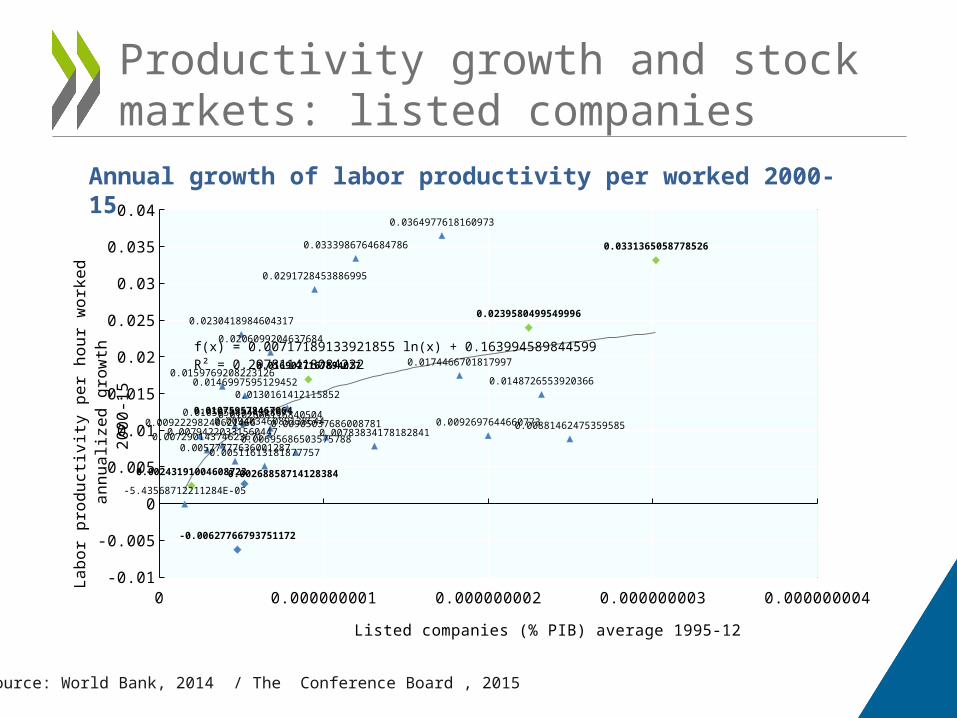

Annual growth of labor productivity per worked 2000-15

Source: World Bank, 2014 / The Conference Board , 2015

0 5E-10 0.000000001 0.0000000015 0.000000002 0.0000000025 0.000000003 0.0000000035-0.01

-0.005

0

0.005

0.01

0.015

0.02

0.025

0.03

0.035

0.040.0364977618160973

0.0333986764684786 0.0331365058778526

0.0291728453886995

0.02395804995499960.0230418984604317

0.0206099204637684

0.01744667018179970.01690271678940270.0159769208223126

0.01487265539203660.01469975951294520.0130161412115852

0.0107595784670640.01058506944918670.01026661168405040.00940346089138644 0.00926976446607730.00922298240621466 0.00905037686008781 0.00881462475359585

0.00794220331560447 0.007838341781828410.00729014374623671 0.006956865035757880.005777776360012870.00511613181877757

0.002688587141283840.00243191004608723

-5.43568712211284E-05

-0.00627766793751172

f(x) = 0.00717189133921856 ln(x) + 0.163994589844599R² = 0.297811418084232

Listed companies (% PIB) average 1995-12

Labo

r pro

duct

ivity

per

hou

r wor

ked

ann

ualiz

ed g

rowt

h 20

00-1

5Productivity growth and stock markets: listed companies

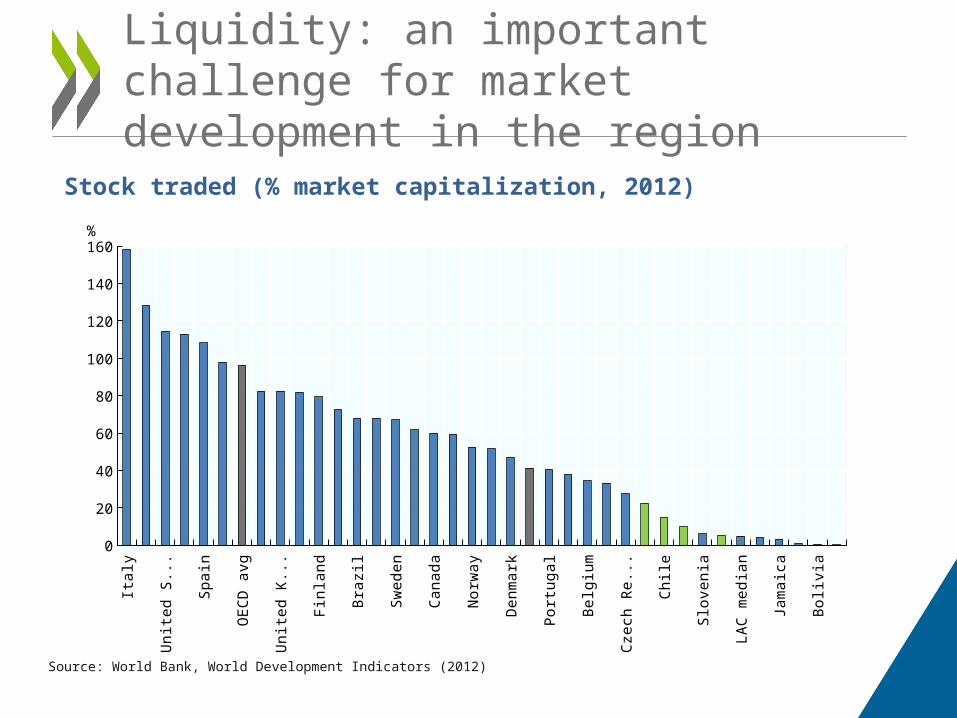

Stock traded (% market capitalization, 2012)

Italy

Kore

a, R

ep.

Uni

ted

Stat

esTu

rkey

Spai

nJa

pan

OEC

D a

vgG

erm

any

Uni

ted

King

dom

Aust

ralia

Finl

and

OEC

D m

edia

nBr

azil

Net

herla

nds

Swed

enFr

ance

Can

ada

Switz

erla

ndN

orw

ayH

unga

ryD

enm

ark

LAC

avg

Portu

gal

Pola

ndBe

lgiu

mG

reec

eC

zech

Rep

ublic

Mex

ico

Chi

leC

olom

bia

Slov

enia

Peru

LAC

med

ian

Arge

ntin

aJa

mai

caU

rugu

ayBo

livia

Vene

zuel

a

0

20

40

60

80

100

120

140

160%

Source: World Bank, World Development Indicators (2012)

Liquidity: an important challenge for market development in the region

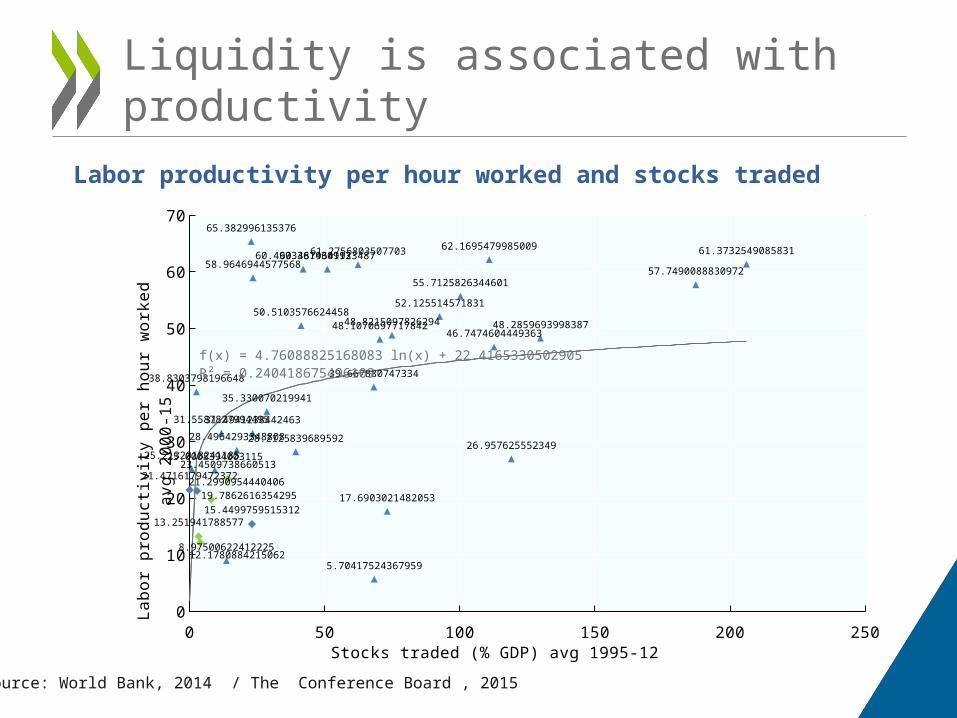

Liquidity is associated with productivity

Source: World Bank, 2014 / The Conference Board , 2015

Labor productivity per hour worked and stocks traded

0 50 100 150 200 2500

10

20

30

40

50

60

7065.382996135376

62.1695479985009 61.373254908583161.275680350770360.499336143091360.487964192348758.9646944577568

57.749008883097255.7125826344601

52.12551457183150.5103576624458

48.8215097826294 48.285969399838748.107069771784246.7474604449363

39.66788074733438.8303798196648

35.330070219941

31.558782799449531.4941238442463

28.496429334880828.212583968959226.9576255523491

25.213201824118525.000839400311523.4509738660513

21.471617947237221.299095444040619.7862616354295 17.6903021482053

15.449975951531213.251941788577

12.17808842150628.97500622412225

5.70417524367959

f(x) = 4.76088825168084 ln(x) + 22.4165330502905R² = 0.24041867549611

Stocks traded (% GDP) avg 1995-12

Labo

r pro

duct

ivity

per

hou

r wor

ked

avg

2000

-15

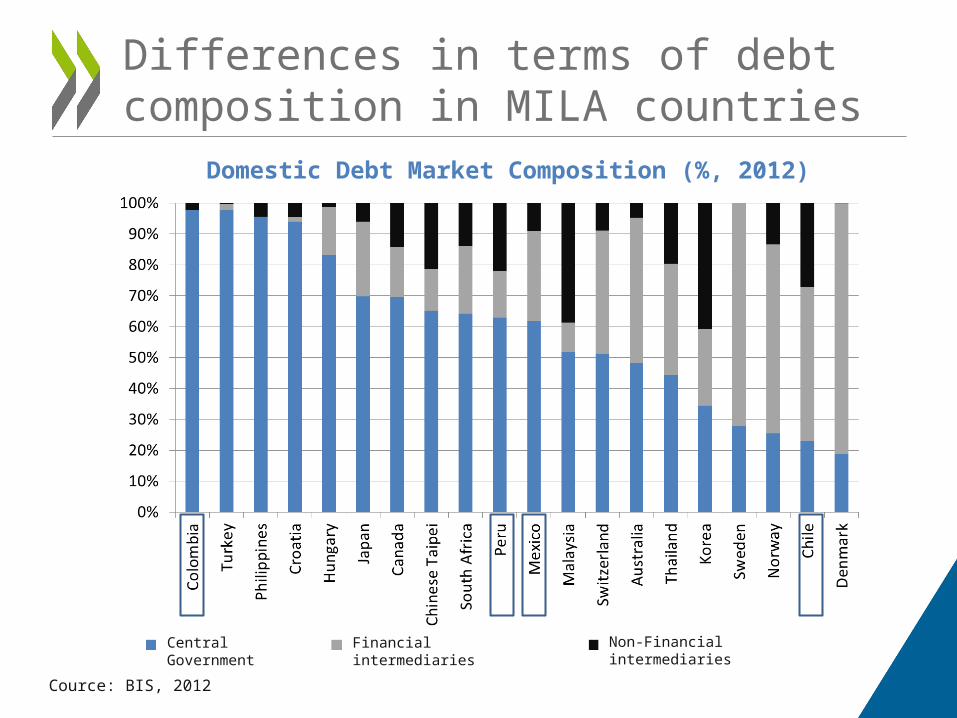

Differences in terms of debt composition in MILA countries

Domestic Debt Market Composition (%, 2012)

Cource: BIS, 2012

Central Government

Financial intermediaries Non-Financial intermediaries

Contents

Key Challenge: Tackling the Middle Income Trap (MIT)1

Market Integration: a key asset to avoid the MIT2

Crucial role of Capital Markets3

Conditions and Benefits of Capital Markets Integration

4

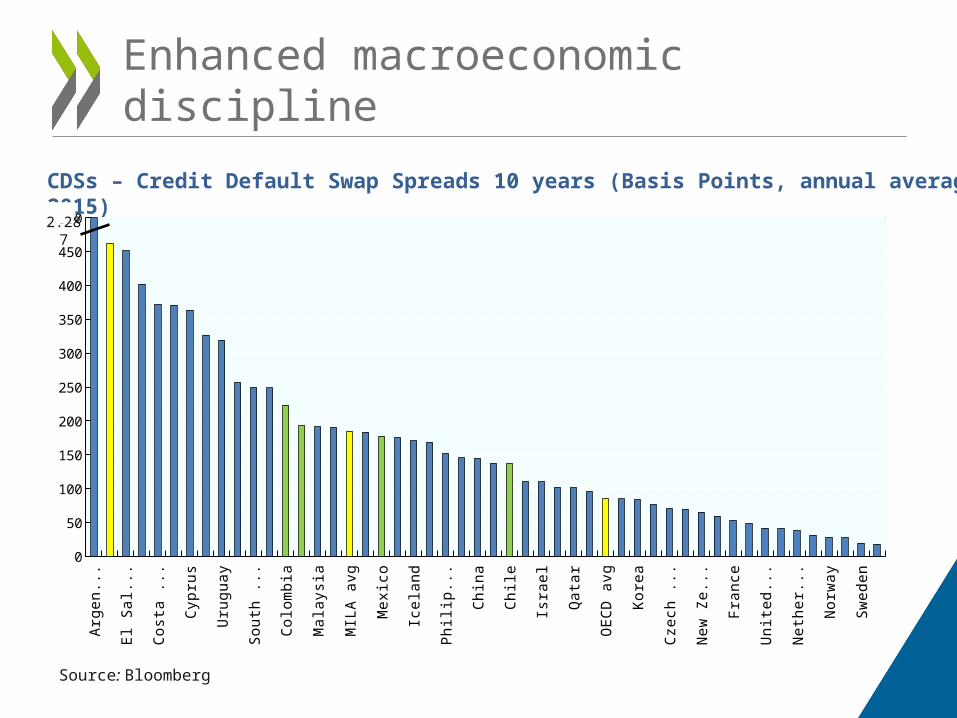

CDSs – Credit Default Swap Spreads 10 years (Basis Points, annual average 2015)

Enhanced macroeconomic discipline

Source: Bloomberg

Arge

ntin

aLA

C a

vgEl

Sal

vado

rD

omin

ican

r...

Cos

ta R

ica

Rus

sia

Cyp

rus

Gua

tem

ala

Uru

guay

Indo

nesi

aSo

uth

Afric

aTu

rkey

Col

ombi

aPe

ruM

alay

sia

Pana

ma

MIL

A av

gPo

rtuga

lM

exic

oH

unga

ryIc

elan

dTh

aila

ndPh

ilipp

ines

Slov

enia

Chi

na Italy

Chi

leSp

ain

Isra

elPo

land

Qat

arSi

ngap

ore

OEC

D a

vgSl

ovak

Rep

u...

Kore

aEs

toni

aC

zech

Rep

u...

Irela

ndN

ew Z

eala

ndBe

lgiu

mFr

ance

Japa

nU

nite

d Ki

n...

Finl

and

Net

herla

nds

Aust

riaN

orw

ayD

enm

ark

Swed

enG

erm

any

0

50

100

150

200

250

300

350

400

450

5002.287

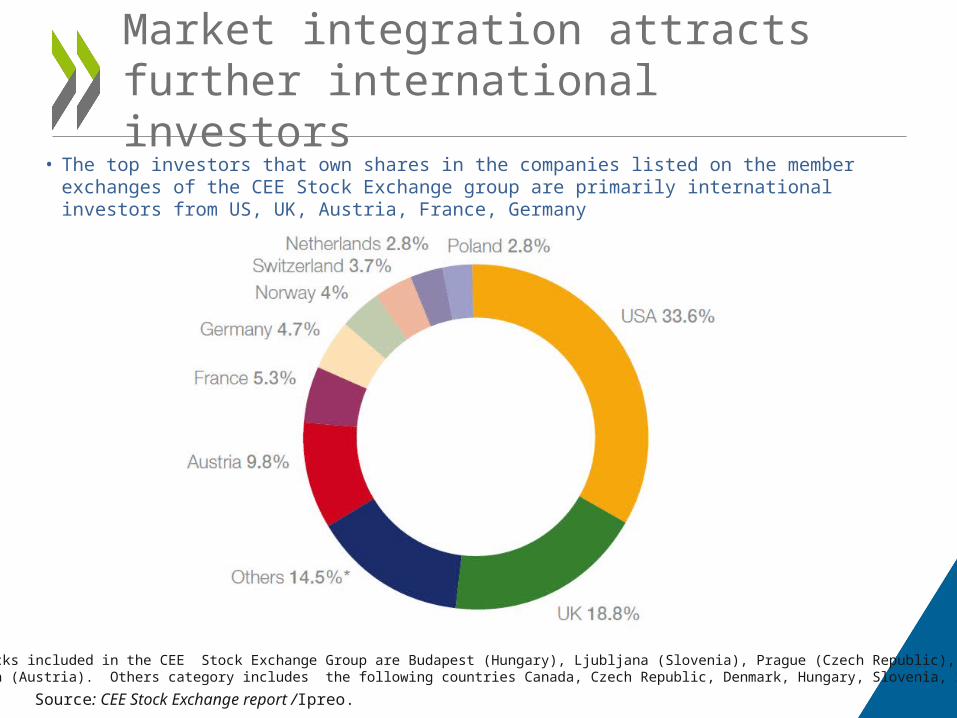

Market integration attracts further international investors

• The top investors that own shares in the companies listed on the member exchanges of the CEE Stock Exchange group are primarily international investors from US, UK, Austria, France, Germany

Source: CEE Stock Exchange report /Ipreo.

Note: Stocks included in the CEE Stock Exchange Group are Budapest (Hungary), Ljubljana (Slovenia), Prague (Czech Republic), and Vienna (Austria). Others category includes the following countries Canada, Czech Republic, Denmark, Hungary, Slovenia, Sweden

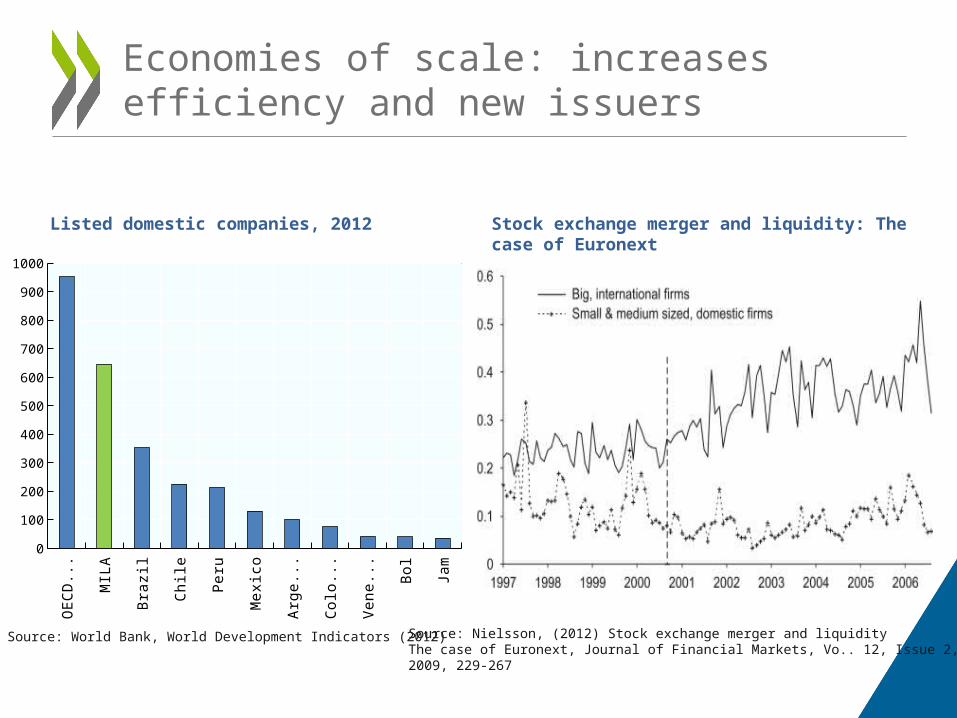

Economies of scale: increases efficiency and new issuers

Listed domestic companies, 2012

Source: World Bank, World Development Indicators (2012)

OEC

D...

MIL

A

Braz

il

Chi

le

Peru

Mex

ico

Arge

ntin

a

Col

ombi

a

Vene

z...

Boliv

ia

Jam

aica

0

100

200

300

400

500

600

700

800

900

1000

Stock exchange merger and liquidity: The case of Euronext

Source: Nielsson, (2012) Stock exchange merger and liquidityThe case of Euronext, Journal of Financial Markets, Vo.. 12, Issue 2, 2009, 229-267

Conclusions

- Pacific Alliance countries have a common challenge: to boost productivity and competitiveness

To tackle the Middle Income Trap.

- A key actor to facilitate improvements in these areas: Capital Markets.

- In particular MILA: to increase the number of listed companies, the liquidity, and to attract new investors.

- A key pillar: credibility of macroeconomic policies.

- OECD supports regional integration in Latam and in particular close work/collaboration with MILA/Pacific Alliance countries: - Chile and Mexico: OECD members- Colombia: Accession Process to join the OECD- Peru: OECD Country Programme

Sebastián Nieto Parra

Development Centre

OECD

October 2015

INTEGRATING SECURITIES MARKETS TO BOOST COMPETITIVENESS

The Latin American Integrated Market – MILA DAY 2015