Embed Size (px)

Citation preview

SECOND QUARTER REPORT TO UNITHOLDERS FOR THE SIX MONTHS ENDED JUNE 30, 2008

W A J A X I N C O M E F U N D 2 0 0 8

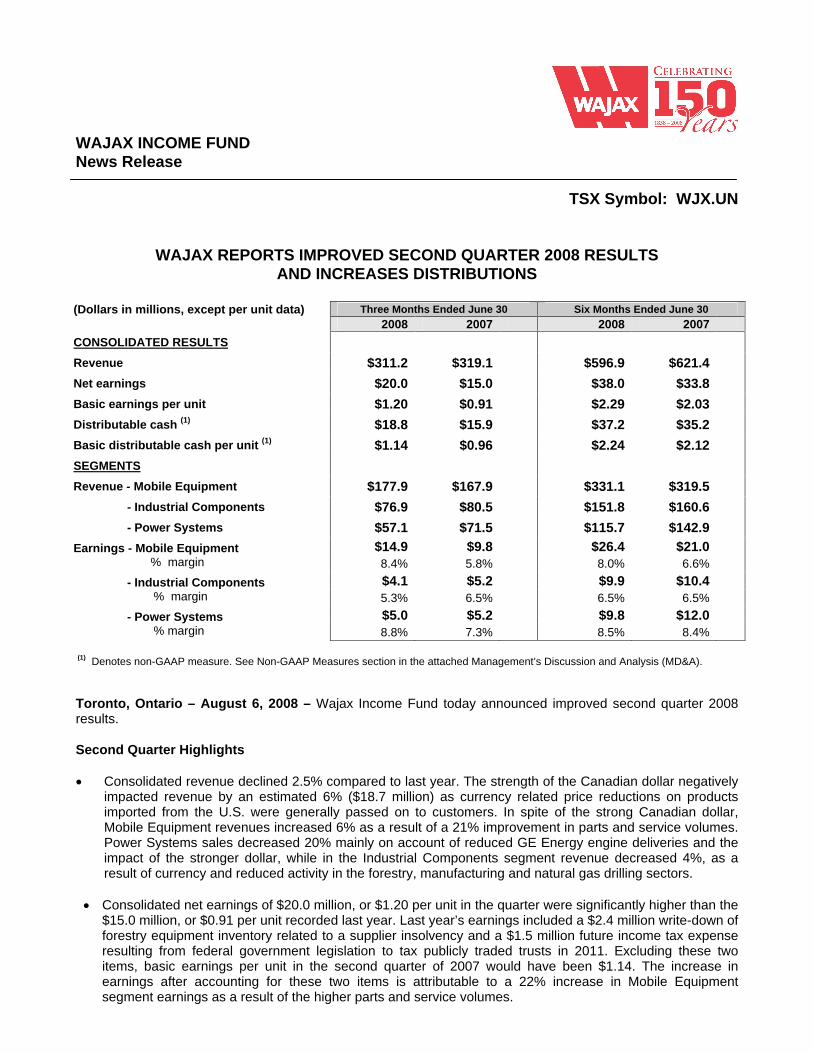

WAJAX INCOME FUND News Release

TSX Symbol: WJX.UN

WAJAX REPORTS IMPROVED SECOND QUARTER 2008 RESULTS AND INCREASES DISTRIBUTIONS

(Dollars in millions, except per unit data) Three Months Ended June 30 Six Months Ended June 30

2008 2007

2008 2007

CONSOLIDATED RESULTS

Revenue $311.2

$319.1

$596.9

$621.4

Net earnings $20.0

$15.0

$38.0

$33.8

Basic earnings per unit $1.20

$0.91

$2.29

$2.03

Distributable cash (1) $18.8

$15.9

$37.2

$35.2

Basic distributable cash per unit (1) $1.14

$0.96

$2.24

$2.12

SEGMENTS

Revenue - Mobile Equipment $177.9

$167.9

$331.1

$319.5

- Industrial Components $76.9

$80.5

$151.8

$160.6

- Power Systems $57.1

$71.5

$115.7

$142.9

Earnings - Mobile Equipment $14.9

$9.8

$26.4

$21.0

% margin 8.4% 5.8% 8.0% 6.6%

- Industrial Components $4.1

$5.2

$9.9

$10.4

% margin 5.3% 6.5% 6.5% 6.5%

- Power Systems $5.0

$5.2

$9.8

$12.0

% margin 8.8% 7.3% 8.5% 8.4%

(1) Denotes non-GAAP measure. See Non-GAAP Measures section in the attached Management’s Discussion and Analysis (MD&A).

Toronto, Ontario – August 6, 2008 – Wajax Income Fund today announced improved second quarter 2008 results.

Second Quarter Highlights

Consolidated revenue declined 2.5% compared to last year. The strength of the Canadian dollar negatively impacted revenue by an estimated 6% ($18.7 million) as currency related price reductions on products imported from the U.S. were generally passed on to customers. In spite of the strong Canadian dollar, Mobile Equipment revenues increased 6% as a result of a 21% improvement in parts and service volumes. Power Systems sales decreased 20% mainly on account of reduced GE Energy engine deliveries and the impact of the stronger dollar, while in the Industrial Components segment revenue decreased 4%, as a result of currency and reduced activity in the forestry, manufacturing and natural gas drilling sectors.

Consolidated net earnings of $20.0 million, or $1.20 per unit in the quarter were significantly higher than the $15.0 million, or $0.91 per unit recorded last year. Last year’s earnings included a $2.4 million write-down of forestry equipment inventory related to a supplier insolvency and a $1.5 million future income tax expense resulting from federal government legislation to tax publicly traded trusts in 2011. Excluding these two items, basic earnings per unit in the second quarter of 2007 would have been $1.14. The increase in earnings after accounting for these two items is attributable to a 22% increase in Mobile Equipment segment earnings as a result of the higher parts and service volumes.

Basic distributable cash (see Non-GAAP Measures section in the MD&A) of $1.14 per unit was higher than the $0.96 per unit recorded the previous year as a result of the higher Mobile Equipment segment earnings and the forestry equipment inventory write-down incurred last year.

The Fund announced a $0.01 per unit increase in monthly distributions for August, September and October to $0.35 per unit per month ($4.20 per unit annualized).

Commenting on the second quarter results and the outlook for the year, Neil Manning, President and CEO, stated “As we anticipated, strong market segments such as mining, including the oil sands, and infrastructure more than offset weaker areas of the Canadian economy. We are particularly pleased with the strength in Mobile Equipment parts and service sales as we benefit from servicing equipment sold in previous years. Looking forward, we continue to be concerned about the strength of several sectors of the Canadian economy, particularly manufacturing, forestry and residential construction. However, we anticipate a continuing benefit from strong sectors such as mining and infrastructure plus further growth in after-market support revenue. As well, management continues to be optimistic that an increase in natural gas drilling activity in western Canada may occur in the latter part of this year. As a result, we expect 2008 full year earnings to show improvement over the previous year.”

Wajax is a diversified income fund that has three core distribution businesses engaged in the sale and after-sales parts and service support of mobile equipment, industrial components and power systems, through a network of over 100 branches across Canada. Its customer base spans natural resources, construction, transportation, manufacturing, industrial processing and utilities.

Wajax will Webcast its Second Quarter Financial Results Conference Call. You are invited to listen to the live Webcast on Wednesday, August 6, 2008 at 1:30 p.m. ET. To access the Webcast, enter www.wajax.com

and click on the link for the Webcast on the Investor Relations page. The archived Webcast will be available at the above mentioned website within 24 hours after the conference call.

This news release contains forward-looking information. Please refer to the “Forward-Looking Statements” section in the accompanying Management Discussion and Analysis.

Management’s Discussion and Analysis – Q2 2008

The following management’s discussion and analysis (“MD&A”) discusses the consolidated financial condition and results of operations of Wajax Income Fund (the “Fund” or “Wajax”) for the quarter ended June 30, 2008. This MD&A should be read in conjunction with the information contained in the Unaudited Interim Consolidated Financial Statements and accompanying notes for the quarter-ended June 30, 2008, the annual Audited Consolidated Financial Statements and accompanying notes of the Fund for the year ended December 31, 2007 and the associated MD&A. Information contained in this MD&A is based on information available to management as of August 6, 2008.

Unless otherwise indicated, all financial information within this MD&A is in millions of dollars, except per unit data.

Responsibility of Management and the Board of Trustees

Management is responsible for the information disclosed in this MD&A and the Consolidated Financial Statements and accompanying notes, and has in place appropriate information systems, procedures and controls to ensure that information used internally by management and disclosed externally is materially complete and reliable. The Fund’s Board of Trustees has approved this MD&A and the interim Consolidated Financial Statements and accompanying notes. In addition, the Fund’s Audit Committee, on behalf of the Board of Trustees, provides an oversight role with respect to all public financial disclosures made by the Fund, and has reviewed this MD&A and the interim Consolidated Financial Statements and accompanying notes.

Disclosure Controls and Procedures and Internal Control over Financial Reporting

The Fund has designed disclosure controls and procedures to provide reasonable assurance that material information relating to the Fund is made known to the Chief Executive Officer and the Chief Financial Officer, particularly during the period in which the interim filings are being prepared. The Fund has designed internal controls over financial reporting to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with Canadian Generally Accepted Accounting Principles. There has been no change in the Fund’s internal control over financial reporting that occurred during the second quarter of fiscal 2008 that has materially affected, or is reasonably likely to materially affect, the Fund’s internal control over financial reporting.

Wajax Income Fund Overview

Wajax Income Fund is an unincorporated open-ended limited purpose trust established under the laws of the Province of Ontario pursuant to a declaration of trust dated April 27, 2005. The Fund was created to indirectly invest, on June 15, 2005, in substantially all of the assets and business formerly conducted by Wajax Limited.

The Fund intends to make monthly cash distributions, generally payable to unitholders of record on the last business day of each calendar month and to be paid on or about the 20th day of the following month. The Fund may make special cash and/or special non-cash distributions at the end of the year to ensure, as provided in the Fund’s Declaration of Trust, that the Fund’s total distributions for the year are equal to its taxable income for the year. Cash distributions are dependent on, among other things, the cash flow of the Fund.

Wajax has three core distribution businesses engaged in the sale and after-sales parts and service support of mobile equipment, power systems and industrial components, through a network of over 100 branches across Canada. Its customer base spans natural resources, construction, transportation, manufacturing, industrial processing and utilities.

The Fund’s strategy is to grow earnings in all segments through continuous improvement of operating margins and revenue growth while maintaining the Fund’s strong balance sheet. Revenue growth will be achieved through market share gains, new geographic territories and the addition of new complementary product lines either organically or through acquisitions.

Forward-Looking Information

This MD&A contains forward-looking statements. These statements relate to future events or future performance and reflect management’s current expectations and assumptions. Such forward-looking statements reflect management’s current beliefs and are based on information currently available to management of the Fund. A number of factors could cause actual events, performance or results to differ materially from the events, performance and results discussed in the forward-looking statements. These factors include and are not restricted to the risks identified in this MD&A. In addition these factors should be considered carefully and readers should not place undue reliance on the forward-looking statements. The forward-looking statements reflect management’s expectations as of the date hereof and the Fund does not assume any obligation to update or revise them to reflect new events or circumstances, except as required by law.

Consolidated Results

Three months ended June 30

Six months ended June 30

2008

2007

2008

2007

Revenue $311.2

$319.1 $596.9

$621.4

Gross profit Selling and administrative expenses

$71.7

$50.3

$67.3

$49.3

$139.3

$98.4

$136.8 $98.4

Earnings before interest and income taxes $21.4

$18.0

$40.9

$38.4

Interest expense $1.1

$1.3

$2.2

$2.7

Income tax expense $0.3

$1.6

$0.7

$1.9

Net earnings $20.0

$15.0

$38.0

$33.8

Distributable cash (1)

Cash distributions declared

Distributions paid - Monthly - Special

$18.8

$16.8

$16.6

-

$15.9

$15.9

$15.9

-

$37.2

$33.2

$33.0

$7.8

$35.2

$31.8

$31.8 $18.6

Earnings per unit - Basic - Diluted

$1.20

$1.19

$0.91

$0.90

$2.29

$2.27

$2.03

$2.02

Distributable cash per unit (1)

- Basic(2)

- Diluted

$1.14

$1.13

$0.96

$0.95

$2.24

$2.23

$2.12 $2.11

Cash distributions declared per unit (2) $1.01 $0.96 $2.00

$1.92

Distributions paid per unit (2)

- Monthly - Special

$1.00

-

$0.96

-

$1.99

$0.47

$1.92 $1.12

(1) Non-GAAP measure, see the Non-GAAP Measures and Distributable Cash sections. (2) Based on actual number of units outstanding on the relevant record date.

Revenue Revenue in the second quarter of 2008 decreased $7.9 million to $311.2 million from $319.1 million in 2007. The stronger Canadian dollar relative to the U.S. dollar had the effect of decreasing 2008 consolidated quarterly revenue by approximately $18.7 million, or 6%, as the Fund realized lower sales dollars per unit on U.S. sourced

products. Segment revenue increased 6% in Mobile Equipment while revenue fell 4% and 20% in Industrial Components and Power Systems, respectively. For the six months ended June 30, 2008, revenue decreased $24.5 million, or 4%.

Gross profit Gross profit in the second quarter of 2008 increased $4.4 million due to the positive impact of higher gross profit margins offset partially by the negative impact of lower revenues compared to last year. The gross profit margin percentage for the quarter increased to 23.0% in 2008 from 21.1% in 2007 due to a higher proportion of higher margin parts and service volumes, compared to last year, and a $2.4 million inventory write-down of forestry equipment in the Mobile Equipment segment related to a supplier insolvency in 2007. In addition, the gross profit margin was negatively affected by a reclassification of $0.5 million of selling and administrative expenses to cost of sales resulting from adoption of the new CICA Handbook Section 3031, Inventories, effective January 1, 2008 without restatement of 2007 results (“the new inventory accounting standard”). Excluding the impact of the new inventory accounting standard in 2008 and the forestry equipment inventory write-down in 2007, the gross profit percentage increased to 23.2% in the second quarter of 2008 compared to 21.8% in 2007.

For the six months ended June 30, 2008, gross profit increased $2.5 million compared to last year. Excluding the impact of the new inventory accounting standard in 2008 and the forestry equipment inventory write-down in 2007, the gross profit margin percentage increased to 23.7% in 2008 from 22.4% in 2007 compared to last year.

Selling and administrative expenses Selling and administrative expenses increased $1.0 million in the quarter due mainly to higher sales related costs in Mobile Equipment and increased corporate costs, offset partially by a reclassification of $0.7 million of overhead costs to cost of sales ($0.5 million) and inventory ($0.2 million), resulting from adoption of the new inventory accounting standard. Excluding the impact of adoption of the new inventory accounting standard, selling and administrative expenses as a percentage of revenue increased to 16.4% in 2008 from 15.4% in 2007.

For the six months ended June 30, 2008 selling and administrative expenses remained flat compared to last year. Increased personnel costs in Mobile Equipment and Industrial Components were offset mostly by a reclassification of $2.3 million of overhead costs to cost of sales ($2.0 million) and inventory ($0.3 million), resulting from adoption of the new inventory accounting standard. Excluding the impact of adoption of the new inventory accounting standard, selling and administrative expenses as a percentage of revenue increased to 16.9% in 2008 from 15.8% in 2007.

Interest expense Quarterly interest expense of $1.1 million decreased $0.2 million due mainly to lower interest rates compared to last year.

For the six months ended June 30, 2008, interest expense decreased $0.5 million compared to 2007 due primarily to lower interest rates and lower amortization of deferred financing costs.

Income tax expense The effective income tax rate of 1.6% for the quarter decreased from 9.7% the previous year due mainly to a $1.5 million future income tax expense adjustment made in 2007 to reflect temporary differences of the Fund that are estimated to reverse after 2010, tax effected at rates that will apply in the periods the differences are expected to reverse.

For the six months ended June 30, 2008 the effective tax rate decreased to 1.8% from 5.4% the previous year due mainly to a $1.5 million future income tax expense adjustment made in 2007 to reflect temporary differences of the Fund that are estimated to reverse after 2010, tax effected at rates that will apply in the periods the differences are expected to reverse.

The Fund’s effective income tax rate was lower than the Fund’s statutory income tax rate of 33.6% as the majority of the Fund’s income is not subject to tax in the Fund.

The Fund is a “mutual fund trust” as defined under the Income Tax Act (Canada) and is not currently taxable on its income to the extent that it is distributed to its unitholders. Pursuant to the terms of the Declaration of Trust, all income earned by the Fund is distributed to its unitholders. Accordingly, no provision for income taxes is required on income earned by the Fund that is distributed to its unitholders. The Fund’s corporate subsidiaries are subject to tax on their taxable income.

Under legislation enacted on June 22, 2007, the Fund as a publicly traded income trust will pay tax on its income distributed commencing in 2011 at a rate that is substantially equivalent to the general corporate income tax rate. The Fund may become taxable on its distributions prior to 2011 if its equity capital grows beyond certain dollar limits measured by reference to the Fund’s market capitalization on October 31, 2006. The Fund has not exceeded its growth limits at June 30, 2008.

On July 14, 2008, the Department of Finance released draft rules designed to permit income funds to “convert” into public corporations without triggering adverse tax consequences to the income fund and its unitholders. The Fund is currently evaluating the draft rules which provide for alternative methods whereby an income fund can convert to a public corporation. As long as the Fund continues to benefit from the efficient distribution of its taxable income to unitholders and continues to meet the limitations on growth in equity, the current expectation is that the Fund will delay conversion to a corporate structure until January 1, 2011. The Fund will continue to monitor this position on the timing of conversion to a corporation taking into account the factors described above and other capital market considerations.

Net earnings Quarterly net earnings of $20.0 million, or $1.20 per unit, increased $5.0 million from $15.0 million, or $0.91 per unit in 2007. The positive impact of higher gross profit margins, the $2.4 million write-down of forestry equipment inventory in 2007, lower income tax expenses and interest costs were partially offset by the negative impact of lower volumes and higher selling and administrative costs compared to last year. (Net earnings include $0.2 million of income after tax resulting from adoption of the new inventory accounting standard. Please see Changes in Accounting Policy – Inventories section of this MD&A for further details.)

For the six months ended June 30, 2008 net earnings of $38.0 million, or $2.29 per unit, increased $4.2 million from $33.8 million, or $2.03 per unit, in 2007. (Net earnings include $0.3 million of income after tax resulting from adoption of the new inventory accounting standard. Please see Changes in Accounting Policy – Inventories section of this MD&A for further details.)

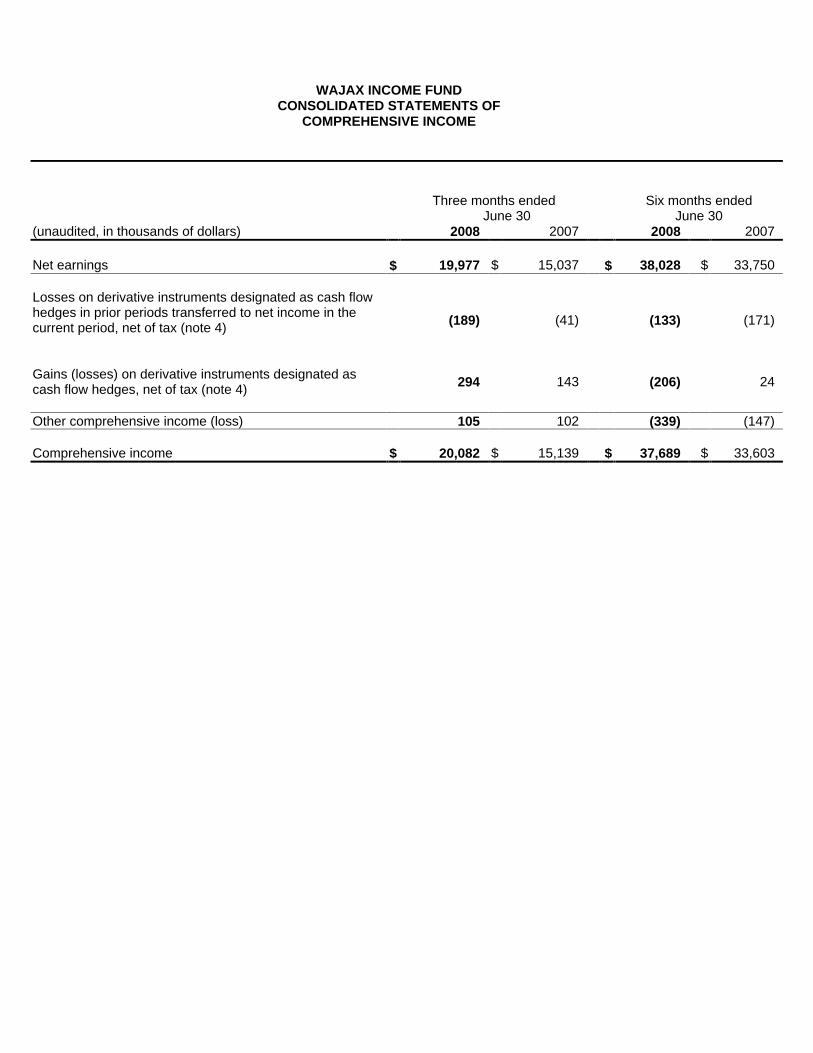

Comprehensive income Comprehensive income for the quarter of $20.1 million increased $5.0 million from $15.1 million the previous year due to a $5.0 million increase in net earnings. For the six months ended June 30, 2008, comprehensive income of $37.7 million increased $4.1 million from $33.6 million the previous year due to a $4.2 million increase in net earnings offset partially by a $0.2 million increase in other comprehensive loss to $0.3 million in 2008 from $0.1 million in 2007.

Funded net debt Funded debt net of cash (“funded net debt”) of $88.2 million decreased $6.5 million compared to March 31, 2008 as second quarter cash flows from operations of $23.5 million and a decrease in non-cash working capital of $4.8 million more than offset cash distributions of $16.6 million and capital spending of $5.0 million.

Compared to June 30, 2007 funded net debt increased $1.5 million. The Fund’s quarter-end debt-to-equity ratio of 0.43:1 at June 30, 2008 decreased from last quarter’s ratio of 0.47:1 and remains the same as last year’s ratio of 0.43:1.

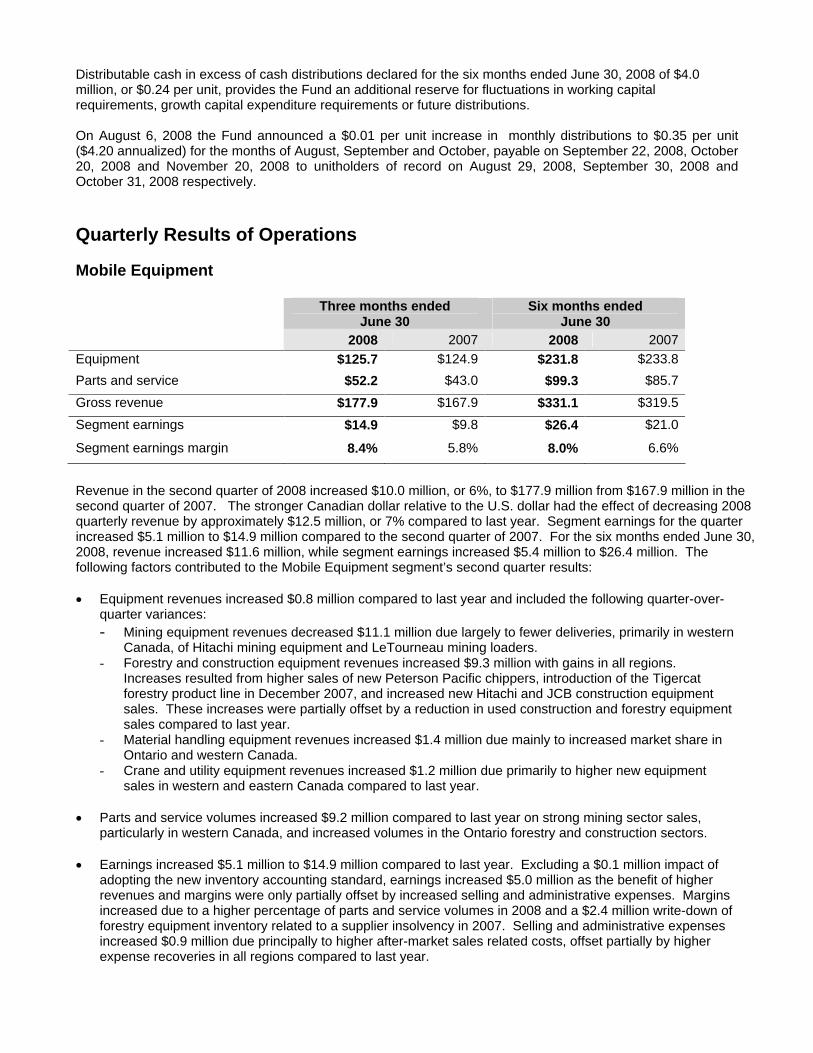

Distributable cash (see Non-GAAP Measures section) and distributions For the quarter ended June 30, 2008 distributable cash was $18.8 million, or $1.14 per unit, compared to $15.9 million, or $0.96 per unit, the previous year. The $2.9 million increase in distributable cash is due primarily to higher cash flows from operations before changes in non-cash working capital compared to last year. For the same period cash distributions declared were $1.01 per unit (2007 - $0.96 per unit).

Distributable cash in excess of cash distributions declared for the three months ended June 30, 2008 of $2.0 million, or $0.13 per unit, provides the Fund an additional reserve for fluctuations in working capital requirements, growth capital expenditure requirements or future distributions. For the six months ended June 30, 2008 distributable cash was $37.2 million, or $2.24 per unit, compared to $35.2 million, or $2.12 per unit, the previous year. The $2.0 million increase in distributable cash is due primarily to lower accruals for mid-term incentives partially offset by higher maintenance capital expenditures compared to last year. For the same period cash distributions declared were $2.00 per unit (2007 - $1.92 per unit).

Distributable cash in excess of cash distributions declared for the six months ended June 30, 2008 of $4.0 million, or $0.24 per unit, provides the Fund an additional reserve for fluctuations in working capital requirements, growth capital expenditure requirements or future distributions.

On August 6, 2008 the Fund announced a $0.01 per unit increase in monthly distributions to $0.35 per unit ($4.20 annualized) for the months of August, September and October, payable on September 22, 2008, October 20, 2008 and November 20, 2008 to unitholders of record on August 29, 2008, September 30, 2008 and October 31, 2008 respectively.

Quarterly Results of Operations

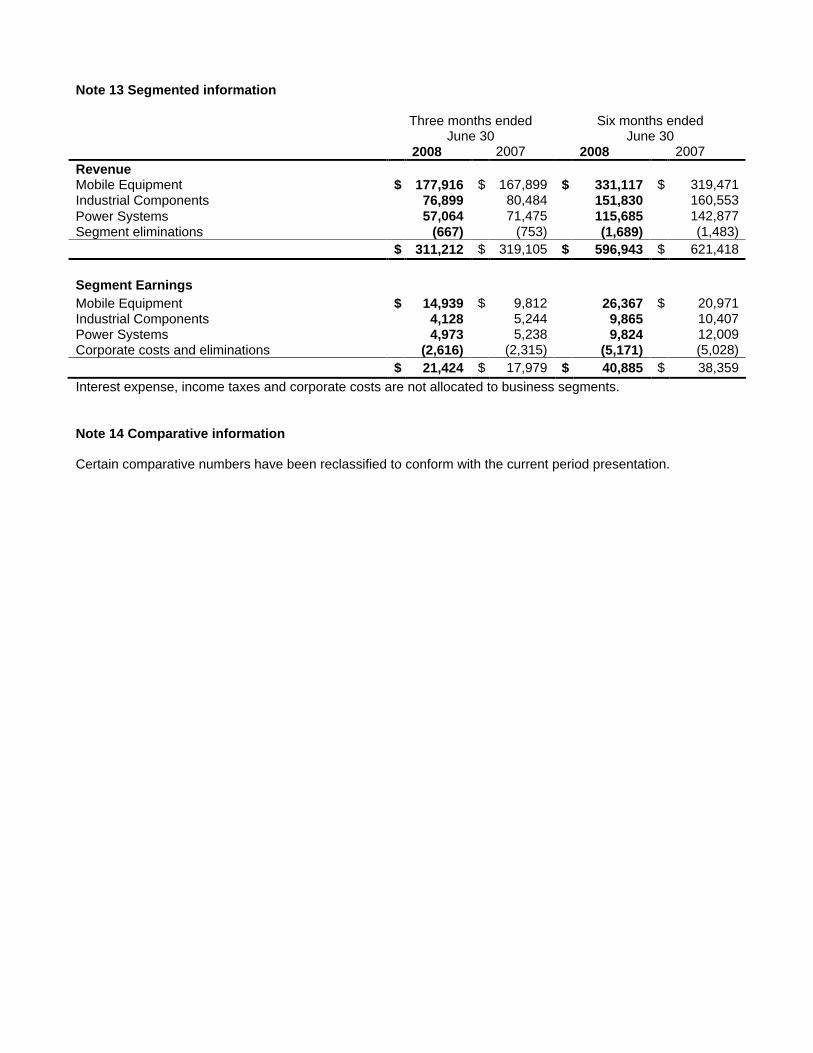

Mobile Equipment

Three months ended June 30

Six months ended June 30

2008

2007

2008

2007

Equipment $125.7

$124.9

$231.8

$233.8

Parts and service $52.2

$43.0

$99.3

$85.7

Gross revenue $177.9

$167.9

$331.1

$319.5

Segment earnings $14.9

$9.8

$26.4

$21.0

Segment earnings margin 8.4%

5.8%

8.0%

6.6%

Revenue in the second quarter of 2008 increased $10.0 million, or 6%, to $177.9 million from $167.9 million in the second quarter of 2007. The stronger Canadian dollar relative to the U.S. dollar had the effect of decreasing 2008 quarterly revenue by approximately $12.5 million, or 7% compared to last year. Segment earnings for the quarter increased $5.1 million to $14.9 million compared to the second quarter of 2007. For the six months ended June 30, 2008, revenue increased $11.6 million, while segment earnings increased $5.4 million to $26.4 million. The following factors contributed to the Mobile Equipment segment’s second quarter results:

Equipment revenues increased $0.8 million compared to last year and included the following quarter-over-quarter variances: - Mining equipment revenues decreased $11.1 million due largely to fewer deliveries, primarily in western

Canada, of Hitachi mining equipment and LeTourneau mining loaders. - Forestry and construction equipment revenues increased $9.3 million with gains in all regions.

Increases resulted from higher sales of new Peterson Pacific chippers, introduction of the Tigercat forestry product line in December 2007, and increased new Hitachi and JCB construction equipment sales. These increases were partially offset by a reduction in used construction and forestry equipment sales compared to last year.

- Material handling equipment revenues increased $1.4 million due mainly to increased market share in Ontario and western Canada.

- Crane and utility equipment revenues increased $1.2 million due primarily to higher new equipment sales in western and eastern Canada compared to last year.

Parts and service volumes increased $9.2 million compared to last year on strong mining sector sales, particularly in western Canada, and increased volumes in the Ontario forestry and construction sectors.

Earnings increased $5.1 million to $14.9 million compared to last year. Excluding a $0.1 million impact of adopting the new inventory accounting standard, earnings increased $5.0 million as the benefit of higher revenues and margins were only partially offset by increased selling and administrative expenses. Margins increased due to a higher percentage of parts and service volumes in 2008 and a $2.4 million write-down of forestry equipment inventory related to a supplier insolvency in 2007. Selling and administrative expenses increased $0.9 million due principally to higher after-market sales related costs, offset partially by higher expense recoveries in all regions compared to last year.

Industrial Components – Kinecor

Three months ended June 30

Six months ended June 30

2008

2007

2008

2007

Gross revenue $76.9

$80.5

$151.8

$160.6

Segment earnings $4.1

$5.2

$9.9

$10.4

Segment earnings margin 5.3%

6.5%

6.5%

6.5%

Revenue at Kinecor of $76.9 million decreased 4%, or $3.6 million from $80.5 million in the second quarter of 2007. The stronger Canadian dollar relative to the U.S. dollar had the effect of decreasing 2008 quarterly revenue by approximately $2.8 million, or 3% compared to last year. Segment earnings decreased $1.1 million to $4.1 million, compared to $5.2 million the previous year. For the six months ended June 30, 2008, revenue declined $8.8 million, while segment earnings decreased $0.5 million to $9.9 million compared to the same period last year. The following factors contributed to the segment’s second quarter results:

Bearings and power transmission parts sales decreased $1.0 million compared to last year, as decreased volumes in the forestry sector in eastern Canada and Ontario more than offset increased sales to manufacturing based customers across all regions.

Fluid power parts and service revenue declined $2.6 million primarily as a result of reduced natural gas drilling activity in western Canada, lower sales to transportation and manufacturing based customers, and reduced forestry sector sales compared to last year. Offsetting these revenue declines were gains made to utilities & government, metal processing and mining sector customers.

Segment earnings decreased $1.1 million to $4.1 million compared to last year, as the negative impact of lower volumes and higher selling and administrative expenses more than offset higher margins. Margins increased due to a modification of pricing strategies and a reduction in lower margin forestry sector volumes compared to last year. Selling and administrative expenses increased $0.8 million compared to last year due mainly to higher personnel related costs and consulting costs associated with the new computer system conversion.

The new computer system, currently being implemented in Kinecor, will provide additional functionality and capacity which will accommodate the segment’s future growth. The system will be implemented into Kinecor’s operations across Canada in four stages during 2008 and the first half of 2009.

Power Systems

Three months ended

June 30 Six months ended

June 30 2008

2007

2008

2007

Equipment $23.0

$37.8

$46.9

$74.2

Parts and service $34.1

$33.7

$68.8

$68.7

Gross revenue $57.1

$71.5

$115.7

$142.9

Segment earnings $5.0

$5.2

$9.8

$12.0

Segment earnings margin 8.8%

7.3%

8.5%

8.4%

Revenue in the second quarter decreased 20%, or $14.4 million, to $57.1 million compared to $71.5 million in 2007. The stronger Canadian dollar relative to the U.S. dollar had the effect of decreasing 2008 quarterly revenue by approximately $3.4 million, or 5% compared to last year. Segment earnings decreased $0.2 million

to $5.0 million in the quarter compared to the previous year. For the six months ended June 30, 2008, revenue decreased $27.2 million, or 19%, to $115.7 million, while earnings decreased $2.2 million to $9.8 million compared to $12.0 million in 2007. The following factors impacted quarterly revenues and earnings:

Revenue at Waterous Power Systems (“Waterous”) in western Canada was down $1.9 million compared to last year as a decline in equipment sales of $2.8 million, attributable to reduced natural gas drilling activity, was partially offset by a $0.9 million increase in parts and service revenues.

Revenue at the eastern Canada operation, DDACE Power Systems (“DDACE”) decreased $12.5 million compared to 2007. Equipment sales decreased $11.9 million, due principally to lower GE Energy engine deliveries. Parts and service revenues decreased $0.6 million compared to last year.

Segment earnings decreased $0.2 million to $5.0 million compared to last year as the negative impact of lower volumes was almost entirely mitigated by higher margins and a reduction in selling and administrative expenses compared to last year. Margins increased due primarily to a higher proportion of higher margin parts and service revenues and improved margins on DDACE new equipment and generator set sales compared to last year.

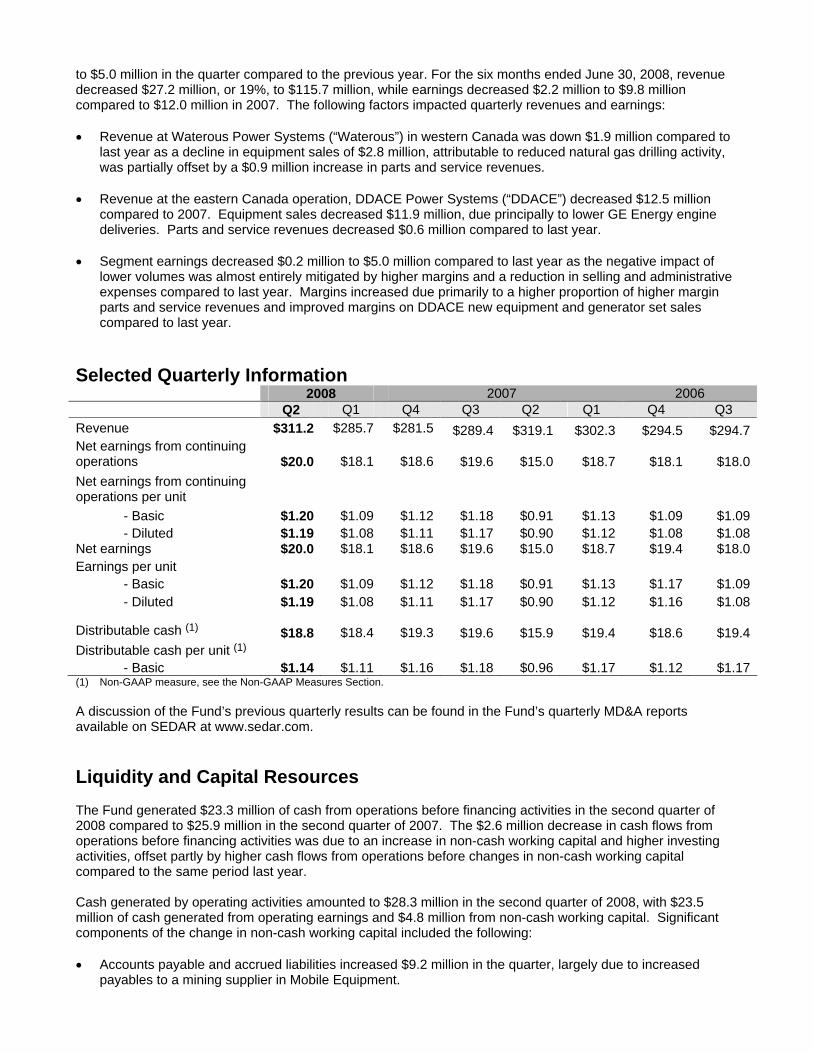

Selected Quarterly Information

2008 2007 2006

Q2 Q1 Q4 Q3 Q2 Q1 Q4 Q3 Revenue $311.2

$285.7

$281.5

$289.4

$319.1

$302.3

$294.5

$294.7

Net earnings from continuing operations

$20.0

$18.1

$18.6

$19.6

$15.0

$18.7

$18.1

$18.0

Net earnings from continuing operations per unit

- Basic $1.20

$1.09

$1.12

$1.18

$0.91

$1.13

$1.09

$1.09

- Diluted $1.19

$1.08

$1.11

$1.17

$0.90

$1.12

$1.08

$1.08

Net earnings $20.0

$18.1

$18.6

$19.6

$15.0

$18.7

$19.4

$18.0

Earnings per unit - Basic $1.20

$1.09

$1.12

$1.18

$0.91

$1.13

$1.17

$1.09

- Diluted $1.19

$1.08

$1.11

$1.17

$0.90

$1.12

$1.16

$1.08

Distributable cash (1)

$18.8

$18.4

$19.3

$19.6

$15.9

$19.4

$18.6

$19.4

Distributable cash per unit (1)

- Basic $1.14

$1.11

$1.16

$1.18

$0.96

$1.17

$1.12

$1.17

(1) Non-GAAP measure, see the Non-GAAP Measures Section.

A discussion of the Fund’s previous quarterly results can be found in the Fund’s quarterly MD&A reports available on SEDAR at www.sedar.com.

Liquidity and Capital Resources

The Fund generated $23.3 million of cash from operations before financing activities in the second quarter of 2008 compared to $25.9 million in the second quarter of 2007. The $2.6 million decrease in cash flows from operations before financing activities was due to an increase in non-cash working capital and higher investing activities, offset partly by higher cash flows from operations before changes in non-cash working capital compared to the same period last year.

Cash generated by operating activities amounted to $28.3 million in the second quarter of 2008, with $23.5 million of cash generated from operating earnings and $4.8 million from non-cash working capital. Significant components of the change in non-cash working capital included the following:

Accounts payable and accrued liabilities increased $9.2 million in the quarter, largely due to increased payables to a mining supplier in Mobile Equipment.

Inventory increased $8.4 million, reflecting higher inventory levels in all business segments including higher levels of JCB equipment, due in part to the Greer acquisition in the first quarter of 2008, and Tigercat forestry equipment due to the introduction of the line in December 2007.

Accounts receivable declined $6.1 million resulting from improved collections in Power Systems compared to the last quarter.

Prepaid expenses increased $2.1 million as a result of an increase in the amount of deposits with suppliers.

During the quarter the Fund invested a net amount of $5.0 million. The investing activities included $2.2 million of lift truck rental fleet additions, net of disposals, $2.4 million of other various capital asset additions (including $1.3 million relating to Kinecor’s new computer system), net of disposals, and a $0.3 million post closing adjustment related to the acquisition of Baytec Fluid Power Limited in March 2006.

Funded net debt decreased $6.5 million compared to March 31, 2008 as second quarter cash flows from operations of $23.5 million and a decrease in non-cash working capital of $4.8 million more than offset cash distributions of $16.6 million and capital spending of $5.0 million. Compared to June 30, 2007 funded net debt increased $1.5 million. The Fund’s quarter-end debt-to-equity ratio of 0.43:1 at June 30, 2008 decreased from last quarter’s ratio of 0.47:1 and remains the same as last year’s ratio of 0.43:1. At June 30, 2008 the Fund had borrowed $89.2 million and issued $4.0 million of letters of credit for a total utilization of $93.2 million of its $175 million bank credit facility and had no utilization of its $15 million equipment financing facility.

The Fund’s $175 million bank credit facility along with its $15 million equipment financing demand facility should be sufficient to meet the Fund’s short-term working capital, maintenance capital and growth capital requirements. In the long-term the Fund may be required to access the equity or debt markets in order to fund significant acquisitions and growth related working capital and capital expenditures requirements.

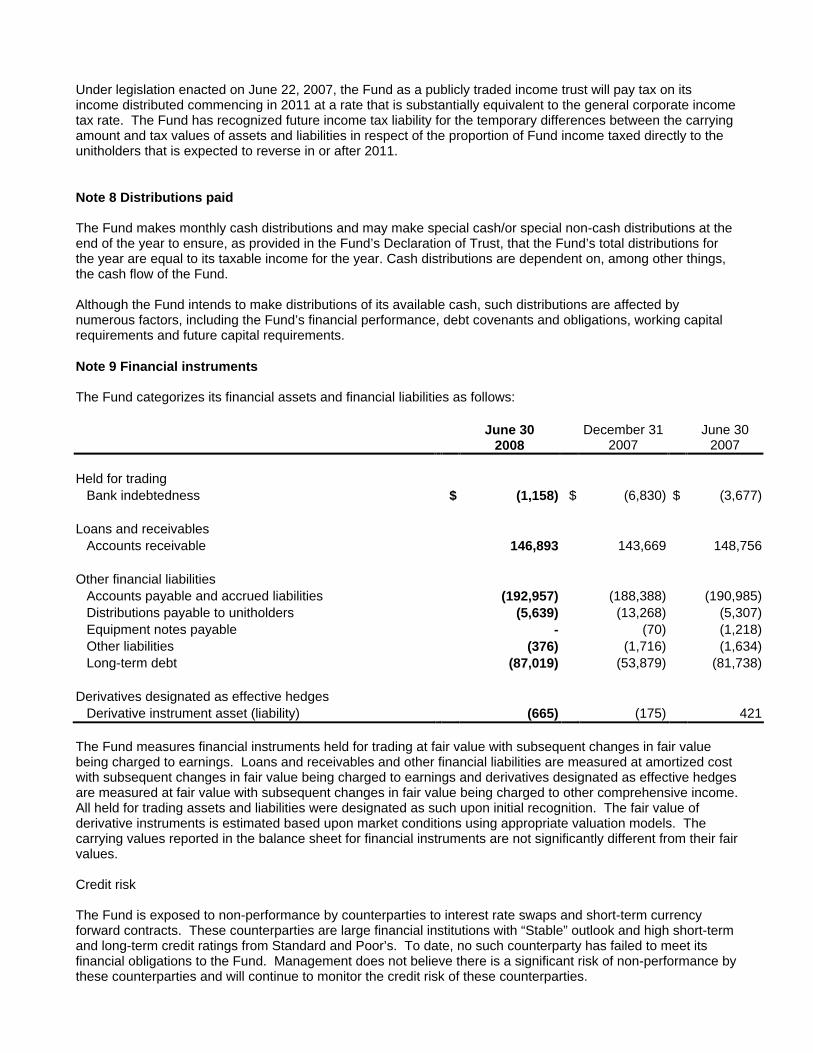

Financial Instruments

The Fund uses derivative financial instruments in the management of its foreign currency and interest rate exposures. The Fund’s policy is not to utilize derivative financial instruments for trading or speculative purposes. Significant derivative financial instrument transactions and those outstanding at the end of the quarter were as follows:

On June 7, 2008 the delayed interest rate swap (entered into on May 9, 2007 with two of its lenders) became effective such that in total the interest rate on the $30 million non-revolving term portion of the bank credit facility is effectively fixed at 4.60% plus applicable margins until expiry of the facility on December 31, 2011. Margins depend on the Fund’s Leverage Ratio and range between 0.75% and 2.50%.

The Fund enters into short-term currency forward contracts to fix the cost of certain inbound inventory and to hedge certain foreign currency-denominated sales to, or receivables from, customers as part of its normal course of business. As at June 30, 2008, the Fund had contracts outstanding to buy US$15.2 million and €0.2 million (June 30, 2007 – to buy US$7.0 million and €1.3 million). These include contracts expiring between July 2008 and October 2009, with U.S. dollar rates ranging from 0.9880 to 1.0300 and Euro dollar rates ranging from 1.4934 to 1.5711.

Contractual Obligations

There have been no material changes to contractual obligations since December 31, 2007.

Off Balance Sheet Financing

The Mobile Equipment segment had $51.3 million of consigned inventory on-hand from a major manufacturer as at June 30, 2008 compared to $60.9 million the previous year. In the normal course of business, Wajax receives inventory on consignment from this manufacturer which is generally sold to customers or purchased by Wajax. This consigned inventory is not included in the Fund’s inventory as the manufacturer retains title to the goods.

The Fund’s off balance sheet financing arrangements with Wajax Finance (a “private label” financing operation of CIT Financial Ltd.) include operating lease contracts in relation to the Fund’s long-term lift truck rental fleet in the Mobile Equipment segment. At June 30, 2008, the non-discounted operating lease commitment for the rental fleet was $10.9 million (June 30, 2007 - $15.8 million).

Non-GAAP Measures

To supplement the consolidated financial statements, the Fund uses non-GAAP financial measures that do not have standardized meaning prescribed by Canadian GAAP and are therefore unlikely to be comparable to similar measures used by other entities.

“Distributable cash” and “Distributable cash per unit” are not recognized measures under GAAP, and the method of calculation adopted by the Fund may differ from methods used by other entities. Accordingly, “Distributable cash” and “Distributable cash per unit” as presented may not be comparable to similar measures presented by other entities. The Fund believes that “Distributable cash” and “Distributable cash per unit” are useful financial metrics as they represent the key determination of cash flow available for distribution to unitholders. “Distributable cash” and “Distributable cash per unit” should not be construed as an alternative to net earnings as determined by GAAP. Distributable cash is calculated as cash flows from operating activities from continuing operations adjusted for changes in non-cash working capital, less maintenance capital expenditures and amortization of deferred financing costs. Changes in non-cash working capital are excluded from distributable cash as the Fund currently has a $175 million bank credit facility which is available for use to fund general corporate requirements including working capital requirements, subject to borrowing capacity restrictions dependent on the level of the Fund’s inventories on-hand and outstanding trade accounts receivable, and a $15 million demand inventory equipment financing facility with a non-bank lender. In addition, the Fund will periodically finance equipment inventory on a non-interest bearing basis through Wajax Finance, a “private label” financing operation of CIT Financial Ltd. See the Distributable Cash section below for the method of calculating the Fund’s “Distributable cash”.

“Maintenance capital expenditures” is not a recognized measure under GAAP, and the method of calculation adopted by the Fund may differ from methods used by other entities. The Fund believes that “Maintenance capital expenditures” represents cash expenditures required to maintain normal operations. “Maintenance capital expenditures” exclude business acquisitions and land and building additions as they are considered to be expenditures that are not required to maintain normal operations. See the Distributable Cash and Estimated Distributable Cash sections below for the method of calculating “Maintenance capital expenditures”.

“Standardized distributable cash” and “Standardized distributable cash per unit” are not recognized measures under GAAP. However, “Standardized distributable cash” has been calculated following the guidance provided in the CICA publication: Standardized Distributable Cash in Income Trusts and Other Flow-Through Entities: Guidance on Preparation and Disclosure. While the Fund has followed the principles of this guidance, the Fund has made assumptions and judgments in determining how such guidance is to be applied. In this respect, the Fund’s calculation may differ from similar calculations done by other entities. See the Standardized Distributable Cash and Reconciliation to Distributable Cash section for the method of calculating the Fund’s “Standardized distributable cash”.

“EBIT” is not a recognized measure under GAAP, and has been calculated as earnings before, interest and taxes and may differ from methods used by other entities.

Distributions

The Fund intends to make monthly cash distributions, generally payable to unitholders of record on the last business day of each calendar month and to be paid on or about the 20th day of the following month. The Fund may make special cash and/or special non-cash distributions at the end of the year to ensure, as provided in the Fund’s Declaration of Trust, that the Fund’s total distributions for the year are equal to its taxable income for the year.

Distributions are based on distributable cash (see Non-GAAP Measures and Distributable Cash sections) and dependent on, among other things, the cash flow generated from operations before changes in non-cash working capital and after providing for maintenance capital expenditures (see Non-GAAP Measures section) and any amount that the Trustees may reasonably consider to be necessary to provide for the payment of costs or other obligations that have been or are reasonably expected to be incurred by the Fund. See Distributable Cash section below.

Cash distributions to unitholders were declared as follows:

Record Date Payment Date Per Unit Amount April 30, 2008 May 20, 2008 $0.33 $5.5 May 30, 2008 June 20, 2008 0.34 5.6 June 30, 2008 July 21, 2008 0.34 5.6

Three months ended June 30, 2008 $1.01 $16.8

(1) See Distributable Cash section below

Cash distributions paid by the Fund during the quarter were funded from cash generated by the Fund’s operations before changes in non-cash working capital and the Fund’s bank credit facilities.

On May 7, 2008 the Fund announced a $0.01 per unit increase in monthly distributions to $0.34 per unit ($4.08 annualized) for the months of May, June and July, payable on June 20, 2008, July 21, 2008 and August 20, 2008 to unitholders of record on May 30, 2008, June 30, 2008 and July 31, 2008 respectively.

On August 6, 2008 the Fund announced a $0.01 per unit increase in monthly distributions to $0.35 per unit ($4.20 annualized) for the months of August, September and October, payable on September 22, 2008, October 20, 2008 and November 20, 2008 to unitholders of record on August 29, 2008, September 30, 2008 and October 31, 2008 respectively.

Unitholder tax information relating to 2007 distributions is available on the Fund’s website at www.wajax.com.

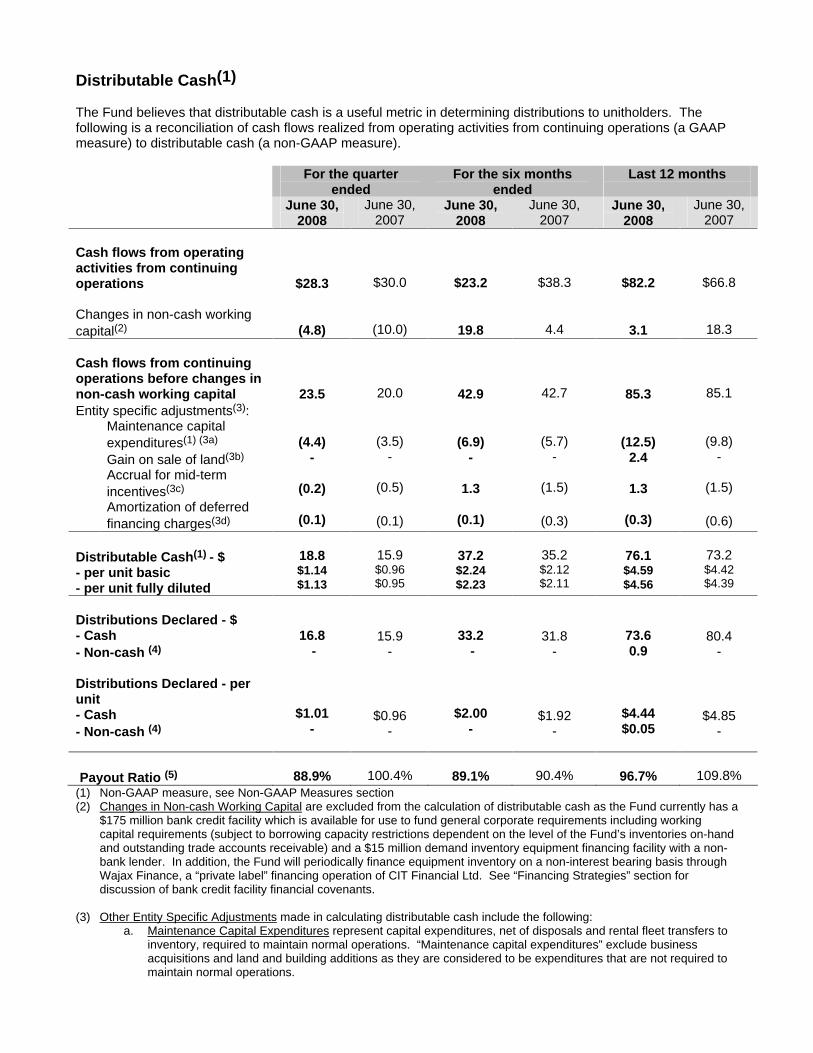

Distributable Cash(1)

The Fund believes that distributable cash is a useful metric in determining distributions to unitholders. The following is a reconciliation of cash flows realized from operating activities from continuing operations (a GAAP measure) to distributable cash (a non-GAAP measure).

For the quarter ended

For the six months ended

Last 12 months

June 30,

2008 June 30,

2007 June 30,

2008 June 30,

2007 June 30,

2008 June 30,

2007

Cash flows from operating activities from continuing operations $28.3 $30.0 $23.2 $38.3 $82.2 $66.8

Changes in non-cash working capital(2) (4.8) (10.0) 19.8 4.4 3.1 18.3

Cash flows from continuing operations before changes in non-cash working capital 23.5 20.0 42.9 42.7 85.3 85.1 Entity specific adjustments(3):

Maintenance capital expenditures(1) (3a)

Gain on sale of land(3b)

Accrual for mid-term incentives(3c)

Amortization of deferred financing charges(3d)

(4.4) -

(0.2)

(0.1)

(3.5) -

(0.5)

(0.1)

(6.9) -

1.3

(0.1)

(5.7) -

(1.5)

(0.3)

(12.5) 2.4

1.3

(0.3)

(9.8) -

(1.5)

(0.6)

Distributable Cash(1) - $ - per unit basic - per unit fully diluted

18.8 $1.14 $1.13

15.9 $0.96 $0.95

37.2 $2.24 $2.23

35.2 $2.12 $2.11

76.1 $4.59 $4.56

73.2 $4.42 $4.39

Distributions Declared - $ - Cash - Non-cash (4)

Distributions Declared - per unit - Cash - Non-cash (4)

16.8 -

$1.01 -

15.9 -

$0.96 -

33.2 -

$2.00 -

31.8 -

$1.92 -

73.6 0.9

$4.44 $0.05

80.4 -

$4.85 -

Payout Ratio (5) 88.9% 100.4% 89.1% 90.4% 96.7% 109.8% (1) Non-GAAP measure, see Non-GAAP Measures section (2) Changes in Non-cash Working Capital are excluded from the calculation of distributable cash as the Fund currently has a

$175 million bank credit facility which is available for use to fund general corporate requirements including working capital requirements (subject to borrowing capacity restrictions dependent on the level of the Fund’s inventories on-hand and outstanding trade accounts receivable) and a $15 million demand inventory equipment financing facility with a non-bank lender. In addition, the Fund will periodically finance equipment inventory on a non-interest bearing basis through Wajax Finance, a “private label” financing operation of CIT Financial Ltd. See “Financing Strategies” section for discussion of bank credit facility financial covenants.

(3) Other Entity Specific Adjustments made in calculating distributable cash include the following: a. Maintenance Capital Expenditures represent capital expenditures, net of disposals and rental fleet transfers to

inventory, required to maintain normal operations. “Maintenance capital expenditures” exclude business acquisitions and land and building additions as they are considered to be expenditures that are not required to maintain normal operations.

b. Gain on Sale of Land: during the third quarter of 2007, the Fund excluded proceeds from the sale of land

previously held for development, up to the cost amount, of $3.1 million as the cost was excluded from the distributable cash when it was originally acquired.

c. Accruals for Mid-Term Incentives: Changes in accruals for mid-term incentives are added back in determining cash flows from operating activities as they were treated as long-term liabilities effective January 1, 2007. These accruals are deducted in calculating distributable cash as the Fund believes it provides unitholders with a better indication of annual compensation costs and provides consistency with prior years.

d. Amortization of Deferred Financing Costs is a deduction in calculating distributable cash based on the amount included in the operating activities section of the statement of cash flow (in the years following the financing transaction) allocated over the term of the financing. The Fund believes this treatment provides a better indication of annual financing costs.

(4) See Distributions section. (5) Payout Ratio is equal to distributions declared as a percentage of distributable cash.

For the quarter ended June 30, 2008 distributable cash was $18.8 million, or $1.14 per unit, compared to $15.9 million, or $0.96 per unit, the previous year. The $2.9 million increase in distributable cash is due primarily to higher cash flows from operations before changes in non-cash working capital compared to last year. Distributions declared for the quarter ended June 30, 2008 were $1.01 per unit (2007 - $0.96 per unit). Distributable cash in excess of cash distributions declared for the three months ended June 30, 2008 of $2.0 million, or $0.13 per unit, provides the Fund an additional reserve for fluctuations in working capital requirements, growth capital expenditure requirements or future distributions.

For the six months ended June 30, 2008 distributable cash was $37.2 million, or $2.24 per unit, compared to $35.2 million, or $2.12 per unit, the previous year. The $2.0 million increase in distributable cash is due primarily to lower accruals for mid-term incentives partially offset by higher maintenance capital expenditures compared to last year. For the same period, distributions declared were $2.00 per unit (2007 - $1.92 per unit). Distributable cash in excess of cash distributions declared for the six months ended June 30, 2008 of $4.0 million, or $0.24 per unit, provides the Fund an additional reserve for fluctuations in working capital requirements, growth capital expenditure requirements or future distributions.

For the twelve months ended June 30, 2008 distributable cash was $76.1 million, or $4.59 per unit, compared to $73.2 million, or $4.42 per unit. The $2.9 million increase was due primarily to lower accruals for mid-term incentives compared to last year. For the same period, cash distributions declared were $4.44 per unit (2007 - $4.85 per unit) and included monthly cash distributions totaling $3.97 per unit (2007 - $3.73 per unit) plus a special cash distribution of $0.47 per unit declared in December 2007 ($1.12 per unit declared December 2006). In addition, a special non-cash distribution was declared December 31, 2007 equal to $0.05 per unit in order to distribute the Fund’s non-taxable portion of its capital gains for the year. The special cash distributions were declared to ensure, as provided by the Fund’s Declaration of Trust, the Fund’s total distributions for the fiscal year were equal to the Fund’s taxable income for such year.

For the three months ended June 30, 2008, the payout ratio of cash distributions based on distributable cash was 89%, compared to 100% the previous year.

For the six months ended June 30, 2008, the payout ratio of cash distributions based on distributable cash was 89%, compared to 90% the previous year.

For the twelve months ended June 30, 2008, the payout ratio of cash distributions based on distributable cash was 97% (2007 - 110%). Excluding the special cash distribution of $0.47 per unit (2007 - $1.12 per unit), the payout ratio was 87% (2007 - 84%).

The following shows the relationship between distributions and cash flows from operating activities, net income and distributable cash.

($millions)

For the quarter ended June 30, 2008

For the six months ended June 30, 2008

For the year ended

December 31, 2007

For the year ended

December 31, 2006

A. Cash flows from operating activities(1) $28.3 $23.2 $97.3 $56.2

B. Net earnings (1) 20.0 38.0 72.0 71.5

C. Distributable cash (2) 18.8 37.2 74.1 74.0

D. Cash distributions declared 16.8 33.2 72.3 73.5

E. Excess (shortfall) of cash flows from operating activities over cash distributions declared (A – D) 11.5 (10.0) 25.0 (17.3)

F. Excess (shortfall) of net earnings over cash distributions declared (B – D) 3.2 4.8 (0.3) (2.0)

G. Excess of distributable cash over cash distributions declared (C – D)

2.0 4.0 1.8 0.5

(1) Based on continuing operations. (2) Non-GAAP measure, see Non-GAAP Measures section.

Significant variances between cash distributions declared by the Fund and cash flows from operating activities, net earnings and distributable cash include the following:

For the quarter ended June 30, 2008, the $11.5 million excess of cash flows from operating activities over cash distributions declared is comprised of a reduction in non-cash working capital of $4.8 million, maintenance capital expenditures, net of disposals, of $4.4 million, other entity specific adjustments totaling $0.3 million and the $2.0 million excess of distributable cash over cash distributions declared. The $2.0 million reserve provides the Fund an additional reserve for fluctuations in working capital requirements, growth capital expenditure requirements for future distributions.

For the six months ended June 30, 2008, the $10.0 million shortfall of cash flows from operating activities over cash distributions declared is due primarily to an increase in non-cash working capital of $19.8 million and other entity specific adjustments totaling $1.1 million, less maintenance capital expenditures, net of disposals, of $6.9 million and the $4.0 million excess of distributable cash over cash distributions declared. The shortfall was funded through the Fund’s bank credit facilities

For the twelve months ended December 31, 2007, the $25.0 million excess of cash flows from operating activities over cash distributions declared is due primarily to a reduction in non-cash working capital of $12.2 million and maintenance capital expenditures, net of disposals, of $11.3 million, less the $2.4 million gain on sale of land, plus a $3.9 million reserve. The $3.9 million provides the Fund an additional reserve for fluctuations in working capital requirements, growth capital expenditure requirements or future distributions.

For the year ended December 31, 2006 the $17.3 million excess of cash distributions declared over cash flows from operating activities was due to a $28.9 million increase in non-cash working capital less capital expenditures, net of disposals, of $10.4 million. The shortfall was funded through the Fund’s bank credit facilities.

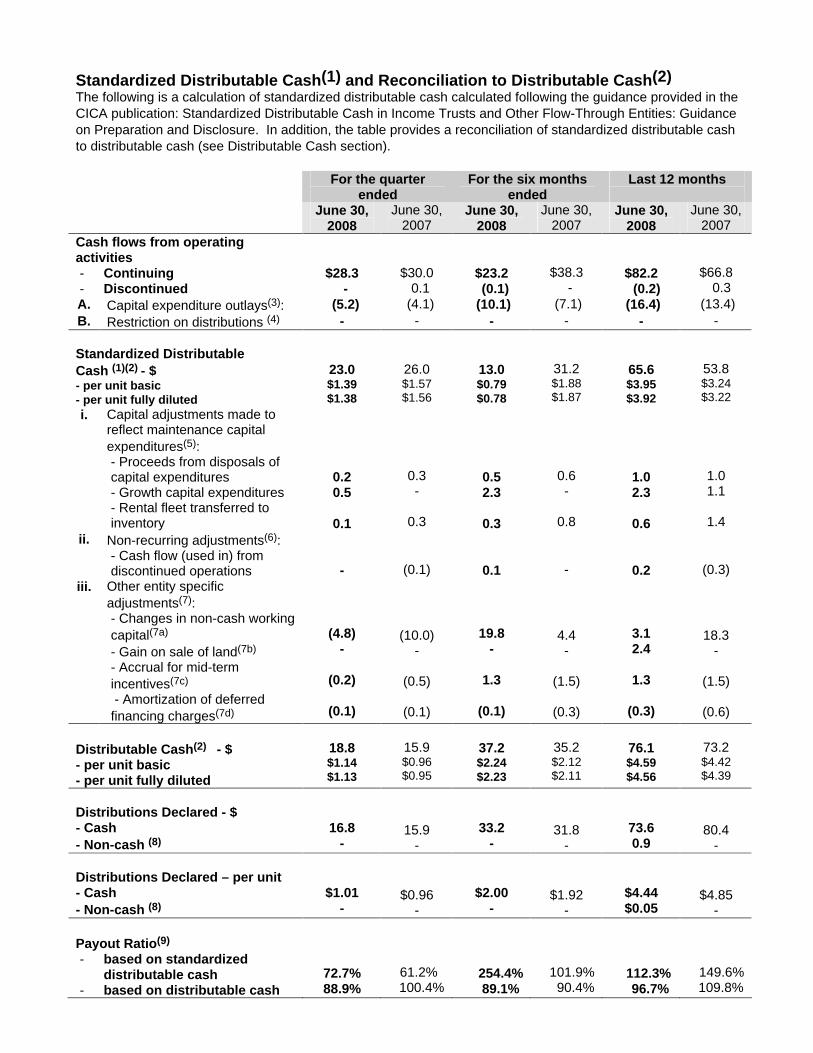

Standardized Distributable Cash(1) and Reconciliation to Distributable Cash(2) The following is a calculation of standardized distributable cash calculated following the guidance provided in the CICA publication: Standardized Distributable Cash in Income Trusts and Other Flow-Through Entities: Guidance on Preparation and Disclosure. In addition, the table provides a reconciliation of standardized distributable cash to distributable cash (see Distributable Cash section).

For the quarter ended

For the six months ended

Last 12 months

June 30,

2008 June 30,

2007 June 30,

2008 June 30,

2007 June 30,

2008 June 30,

2007 Cash flows from operating activities - Continuing - Discontinued

$28.3 -

$30.0 0.1

$23.2 (0.1)

$38.3 -

$82.2 (0.2)

$66.8 0.3

A. Capital expenditure outlays(3): (5.2) (4.1) (10.1) (7.1) (16.4) (13.4) B. Restriction on distributions (4) - - - - - -

Standardized Distributable Cash (1)(2) - $ - per unit basic - per unit fully diluted

23.0 $1.39 $1.38

26.0 $1.57 $1.56

13.0 $0.79 $0.78

31.2 $1.88 $1.87

65.6 $3.95 $3.92

53.8 $3.24 $3.22

i. Capital adjustments made to reflect maintenance capital expenditures(5): - Proceeds from disposals of capital expenditures - Growth capital expenditures - Rental fleet transferred to inventory

0.2 0.5

0.1

0.3 -

0.3

0.5 2.3

0.3

0.6 -

0.8

1.0 2.3

0.6

1.0 1.1

1.4 ii. Non-recurring adjustments(6):

- Cash flow (used in) from discontinued operations - (0.1) 0.1 - 0.2 (0.3)

iii. Other entity specific adjustments(7): - Changes in non-cash working capital(7a)

- Gain on sale of land(7b)

- Accrual for mid-term incentives(7c)

- Amortization of deferred financing charges(7d)

(4.8) -

(0.2)

(0.1)

(10.0) -

(0.5)

(0.1)

19.8 -

1.3

(0.1)

4.4 -

(1.5)

(0.3)

3.1 2.4

1.3

(0.3)

18.3 -

(1.5)

(0.6)

Distributable Cash(2) - $ - per unit basic - per unit fully diluted

18.8 $1.14 $1.13

15.9 $0.96 $0.95

37.2 $2.24 $2.23

35.2 $2.12 $2.11

76.1 $4.59 $4.56

73.2 $4.42 $4.39

Distributions Declared - $ - Cash - Non-cash (8)

16.8 -

15.9 -

33.2 -

31.8 -

73.6 0.9

80.4 -

Distributions Declared – per unit - Cash - Non-cash (8)

$1.01 -

$0.96 -

$2.00 -

$1.92 -

$4.44 $0.05

$4.85 -

Payout Ratio(9)

- based on standardized distributable cash

- based on distributable cash 72.7% 88.9%

61.2% 100.4%

254.4%

89.1% 101.9% 90.4%

112.3% 96.7%

149.6% 109.8%

(1) Standardized distributable cash is a non-GAAP measure calculated following the guidance provided in the CICA

publication: Standardized Distributable Cash in Income Trusts and Other Flow-Through Entities: Guidance on Preparation and Disclosure.

(2) Non-GAAP measure, see Non-GAAP Measures section. (3) Capital expenditure outlays include both maintenance capital expenditure outlays and growth capital expenditure

outlays deducted in calculating standardized distributable cash. See Productivity Capacity and Productivity Capacity Management section.

(4) There are currently no restrictions on distributions arising from compliance with financial covenants. See Financing Strategies section.

(5) Capital adjustments are made to adjust capital expenditure outlays (deducted in computing standardized distributable cash) to reflect maintenance capital expenditures, net of disposals, as a deduction in computing distributable cash. These adjustments include: the exclusion of growth capital, the inclusion of proceeds from the disposal of capital expenditures and rental fleet transferred to inventory. See Non-GAAP Measures and Productivity Capacity and Productivity Capacity Management sections for calculation of maintenance capital expenditures.

(6) Non-recurring adjustments include the exclusion of cash flows (used in) from discontinued operations in calculating distributable cash as they are not a reflection of the Fund’s expected future cash flows.

(7) Other Entity Specific Adjustments made in calculating distributable cash include the following: a. Changes in Non-cash Working Capital see Distributable Cash section. b. Gain on Sale of Land see Distributable Cash section. c. Accruals for Mid-Term Incentives see Distributable Cash section. d. Amortization of Deferred Financing Costs see Distributable Cash section.

(8) See Distributions section. (9) Payout ratio is equal to distributions declared as a percentage of distributable cash.

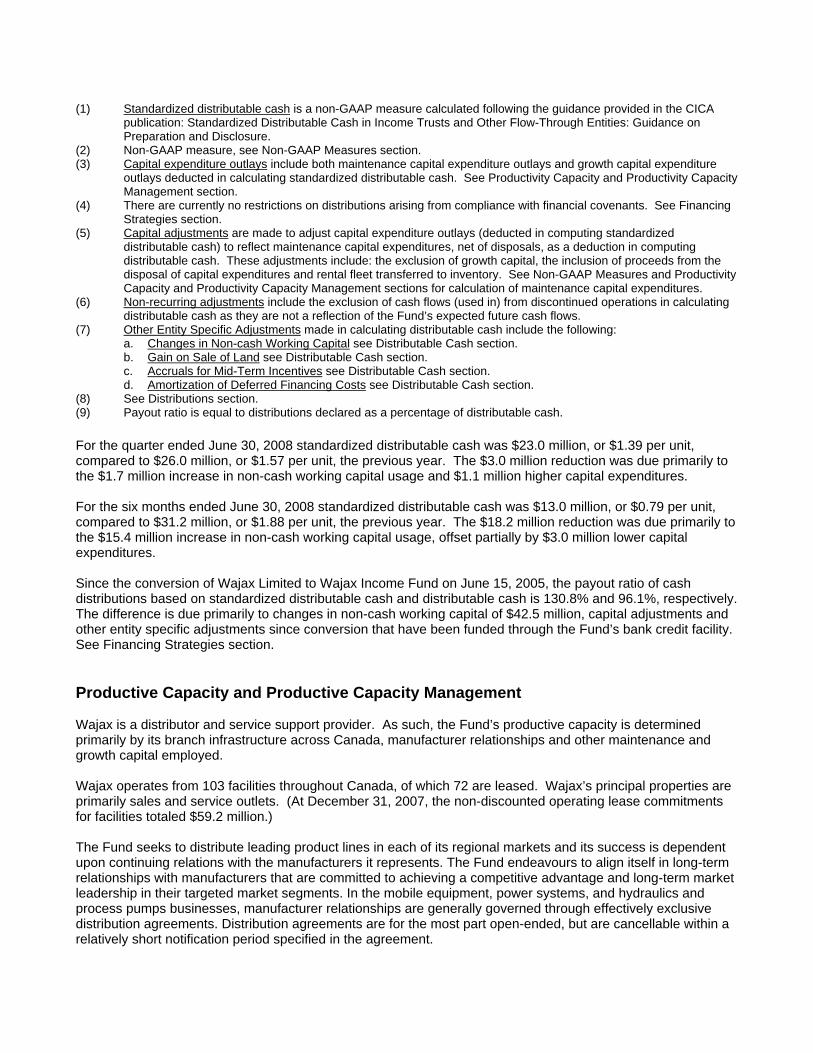

For the quarter ended June 30, 2008 standardized distributable cash was $23.0 million, or $1.39 per unit, compared to $26.0 million, or $1.57 per unit, the previous year. The $3.0 million reduction was due primarily to the $1.7 million increase in non-cash working capital usage and $1.1 million higher capital expenditures.

For the six months ended June 30, 2008 standardized distributable cash was $13.0 million, or $0.79 per unit, compared to $31.2 million, or $1.88 per unit, the previous year. The $18.2 million reduction was due primarily to the $15.4 million increase in non-cash working capital usage, offset partially by $3.0 million lower capital expenditures.

Since the conversion of Wajax Limited to Wajax Income Fund on June 15, 2005, the payout ratio of cash distributions based on standardized distributable cash and distributable cash is 130.8% and 96.1%, respectively. The difference is due primarily to changes in non-cash working capital of $42.5 million, capital adjustments and other entity specific adjustments since conversion that have been funded through the Fund’s bank credit facility. See Financing Strategies section.

Productive Capacity and Productive Capacity Management

Wajax is a distributor and service support provider. As such, the Fund’s productive capacity is determined primarily by its branch infrastructure across Canada, manufacturer relationships and other maintenance and growth capital employed.

Wajax operates from 103 facilities throughout Canada, of which 72 are leased. Wajax’s principal properties are primarily sales and service outlets. (At December 31, 2007, the non-discounted operating lease commitments for facilities totaled $59.2 million.)

The Fund seeks to distribute leading product lines in each of its regional markets and its success is dependent upon continuing relations with the manufacturers it represents. The Fund endeavours to align itself in long-term relationships with manufacturers that are committed to achieving a competitive advantage and long-term market leadership in their targeted market segments. In the mobile equipment, power systems, and hydraulics and process pumps businesses, manufacturer relationships are generally governed through effectively exclusive distribution agreements. Distribution agreements are for the most part open-ended, but are cancellable within a relatively short notification period specified in the agreement.

Maintenance capital employed includes rental fleet primarily in the Mobile Equipment segment, which will vary with market demand, and other capital which is employed primarily to support and maintain the branch network operations.

In addition, the Fund enters into off balance sheet financing arrangements including operating lease contracts entered into for the long-term lift truck rental fleet in Mobile Equipment with Wajax Finance, vehicles and other equipment. (At December 31, 2007, the non-discounted operating lease commitments for rental fleet totaled $13.1 million, vehicles $0.6 million and other equipment $1.6 million.)

Growth capital expenditures include acquisitions of land and building that are not required to maintain normal operations.

For the seven year period from 2000 to 2007, average annual maintenance capital expenditures, net of proceeds from disposals, (including rental fleet but excluding discontinued operations and an ERP computer system abandoned in 2002), were $8.9 million. The annual maintenance capital expenditures varied between $3.4 million and $12.0 million during the period. Management’s expectation for future annual maintenance capital expenditures is between $8 million and $14 million.

Financing Strategies

The Fund’s $175 million bank credit facility along with the $15 million demand inventory equipment financing facility should be sufficient to meet the Fund’s short-term working capital, maintenance capital and growth capital requirements.

In the long-term the Fund may be required to access the equity or debt markets or reduce distributions in order to fund significant acquisitions and growth related working capital and capital expenditures.

The Fund’s short-term working capital requirements can swing widely quarter-to-quarter due to timing of large inventory purchases and/or sales and changes in market activity. In general, as Wajax experiences growth, there is a need for additional working capital as was the case in 2006 and in the first quarter of 2008. Conversely, as Wajax experiences economic slowdowns working capital reduces, reflecting the lower activity levels. This can result in standardized distributable cash increasing in years of declining activity and decreasing in years of growth. Fluctuations in working capital are generally funded by, or used to repay, the bank credit facilities. Therefore, for the reasons noted the Fund adjusts for changes in non-cash working capital in calculating distributable cash in periods where the Fund has capacity under its credit facility to fund the changes in non-cash working capital.

The bank credit facility contains covenants that could restrict the ability of the Fund to make cash distributions, if (i) an event of default exists or would exist as a result of a cash distribution, and (ii) the leverage ratio (Debt to EBITDA) is greater than 3.0. If the leverage ratio is less than or equal to 3.0, then the aggregate cash distributions by the borrowers in each fiscal quarter may not exceed 115% of distributable cash for the trailing four fiscal quarters. Notwithstanding the restrictions relating to the leverage ratio, a special cash distribution in the first quarter of each fiscal year is permitted in an amount not to exceed the amount by which distributable cash for the preceding fiscal year exceeds declared cash distributions for the preceding fiscal year plus any excess cumulative distributable cash over cash distributions of prior years. In addition, borrowing capacity under the bank credit facility is dependent on the level of the Fund’s inventories on-hand and outstanding trade accounts receivables. For further detail, the Fund’s bank credit facility is available on SEDAR at www.sedar.com.

Unit Capital

The trust units of the Fund issued are included in unitholders’ equity on the balance sheet as follows:

Issued and fully paid Trust Units as at June 30, 2008

Number Amount Balance at the beginning of quarter Rights exercised

16,585,206 -

$104.9

-

Balance at end of quarter

16,585,206

$104.9

The Fund has two unit rights plans that issue rights to the participants which are settled by issuing Wajax Income Fund units: the Wajax Unit Ownership Plan in which certain members of management participate and the Trustees’ Deferred Unit Plan. Compensation expense is determined based upon the fair value of the rights when issued and recognized over the vesting period. The Fund recorded compensation cost of $559 thousand for the quarter (2007 - $302 thousand) and $1,024 thousand for the year to date (2007 - $620 thousand) in respect of these plans.

Critical Accounting Estimates

Critical accounting estimates used by the Fund’s management are discussed in detail in the MD&A for the year ended December 31, 2007 which can be found on SEDAR at www.sedar.com.

Changes in Accounting Policy

The following is a summary of the relevant Canadian Institute of Chartered Accountants (“CICA”) Handbook revisions that were adopted by the Fund on January 1, 2008.

Capital Disclosures CICA Handbook Section 1535, Capital Disclosures, establishes standards for disclosure of information regarding an entity’s capital and how it is managed. It requires disclosure of an entity’s objectives, policies and processes for managing capital. In addition, disclosures are to be included whether companies have complied with externally imposed capital requirements and the consequences of any non-compliance. This standard has no impact on the recognition and measurement of amounts included in the financial statements.

Inventories CICA Handbook Section 3031, Inventories, changes the standards for the measurement and disclosure of inventories. The measurement changes include the elimination of the last in first out method, the requirement to measure inventories at the lower of cost and net realizable value, the allocation of overhead based on normal capacity, the use of the specific cost method for inventories that are not ordinarily interchangeable or goods and services produced for specific purposes, the requirement for an entity to use a consistent cost formula for inventory of a similar nature and use, and the reversal of previous write-downs to net realizable value when there is a subsequent increase in the value of inventories. The Fund retrospectively adopted the new inventory requirements without restatement. It reassessed the method whereby it was allocating service department overhead to cost of conversion resulting in an increase in the carrying value of work in process inventory of $0.7 million and an adjustment of $0.6 million (net of tax of $0.1 million) which was recorded directly to opening accumulated retained earnings. Disclosures of inventories have also been enhanced. Inventory policies, carrying amounts, amounts recognized as an expense, write-downs and the reversals of write-downs are required to be disclosed.

Financial Instruments – Disclosures and Financial Instruments - Presentation CICA Handbook Sections 3862 and 3863 increase the emphasis on the risks associated with both recognized and unrecognized financial instruments and how those risks are managed. The new presentation standards carry forward the former presentation requirements. The above standard has no impact on the recognition and measurement of amounts included in the financial statements.

Goodwill and Intangible Assets In February 2008, the CICA issued Handbook Section 3064, Goodwill and Intangible Assets, replacing Section 3062, Goodwill and Other Intangible Assets, and Section 3450, Research and Development Costs. New Section 3064 provides new guidelines for recognition, measurement, presentation and disclosure of goodwill and intangible assets. The Section also issued amendments to Section 1000, Financial Statement Concepts. These changes are effective for fiscal years beginning on or after October 1, 2008, with earlier adoption encouraged. Collectively, these changes bring Canadian practice closer to International Financial Reporting Standards and U.S. GAAP by eliminating the practice of recognizing as assets a variety of startup, pre-production and similar costs that do not meet the definition and recognition criteria of an asset. The Fund has decided to early adopt CICA 3064. Adoption of this standard has no impact on the recognition and measurement of amounts included in the financial statements and no additional disclosure is necessary.

The following is a summary of new standards which will impact the Fund:

In February 2008, The Canadian Accounting Standards Board confirmed that the use of International Financial Reporting Standards (IFRS) will be required in Canada for publicly accountable profit oriented enterprises for fiscal years beginning on or after January 1, 2011. The Fund will be required to report using IFRS beginning January 1, 2011. IFRS uses a conceptual framework similar to current Canadian GAAP, but there are significant differences in recognition, measurement and disclosures.

We are currently in the process of evaluating the potential impact of IFRS on our consolidated financial statements. Our project will consist of four phases: awareness, assessment, design and implementation. We have substantially completed the awareness phase. During the assessment phase, which we anticipate to have substantially completed by the end of 2008, we will determine major recognition, measurement and reporting differences and assess impacts on business process and information systems. Subsequently, the design phase will involve selection of accounting policies where choices exist and development of appropriate disclosures. We will then implement the revised accounting policies based on the choices made, change business processes and information systems and execute training and communications programs.

Risks and Uncertainties

As with most businesses, the Fund is subject to a number of marketplace and industry related risks and uncertainties which could have a material impact on operating results. The Fund attempts to minimize many of these risks through diversification of core businesses and through the geographic diversity of its operations. There are however, a number of risks that deserve particular comment which are discussed in detail in the MD&A for the year ended December 31, 2007 which can be found on SEDAR at www.sedar.com. For the period January 1, 2008 to August 6, 2008 there have been no material changes to the business of the Fund that require an update to the discussion of the applicable risks discussed in the MD&A for the year ended December 31, 2007.

Outlook

As expected, strong market segments such as mining, including the oil sands, and infrastructure more than offset weaker areas of the Canadian economy in the quarter. Strong Mobile Equipment parts and service sales benefited from servicing equipment sold in previous years. Looking forward, management continues to be concerned about the strength of several sectors of the Canadian economy, particularly manufacturing, forestry and residential construction. However, management anticipates a continuing benefit from strong sectors such as mining and infrastructure plus further growth in after-market support revenue. As well, management continues to be optimistic that an increase in natural gas drilling activity in western Canada may occur in the latter part of this year. As a result, management expects 2008 full year earnings to show improvement over the previous year.

Additional information, including the Fund’s Annual Report and Annual Information Form, are available on SEDAR at www.sedar.com.

WAJAX INCOME FUND

Unaudited Consolidated Financial Statements

For the six months ended June 30, 2008

Notice required under National Instrument 51-102, “Continuous Disclosure Obligations” Part 4.3(3) (a):

The attached consolidated financial statements have been prepared by Management of Wajax Income Fund and have not been reviewed by the Fund’s auditors.

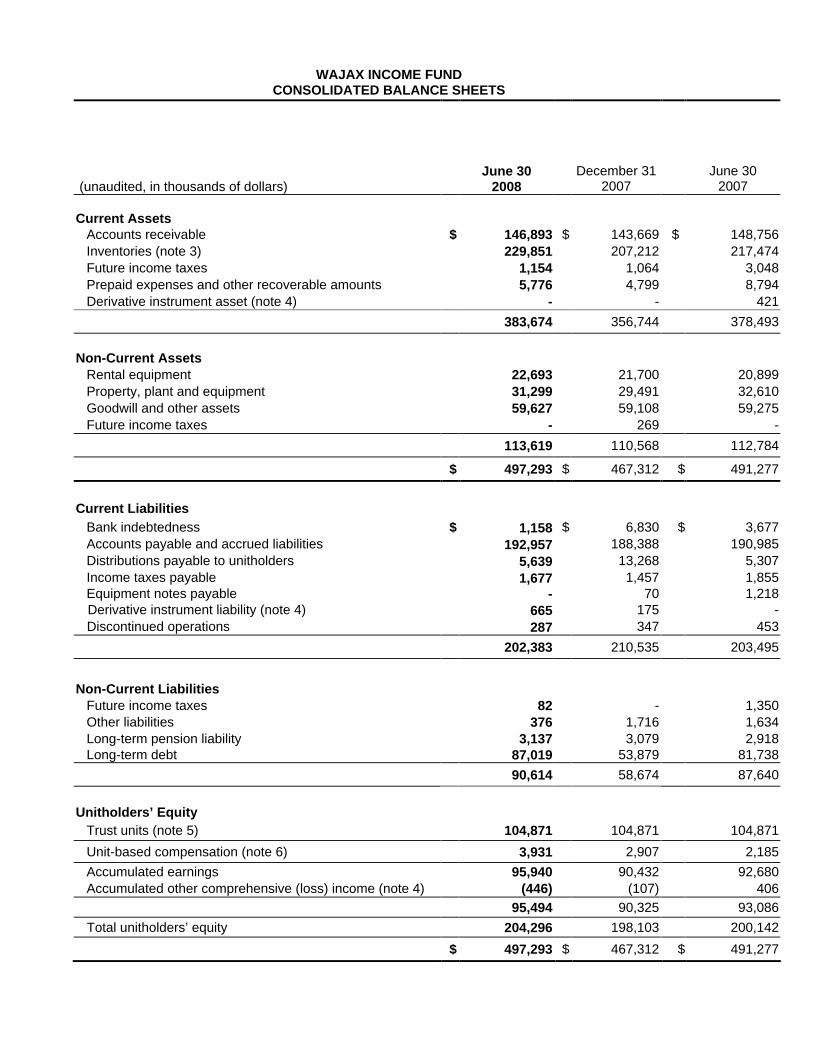

WAJAX INCOME FUND

CONSOLIDATED BALANCE SHEETS

(unaudited, in thousands of dollars)

June 30

2008

December 31

2007

June 30 2007

Current Assets

Accounts receivable $

146,893

$

143,669

$

148,756

Inventories (note 3)

229,851

207,212

217,474

Future income taxes

1,154

1,064

3,048

Prepaid expenses and other recoverable amounts

5,776

4,799

8,794

Derivative instrument asset (note 4)

-

-

421

383,674

356,744

378,493

Non-Current Assets

Rental equipment

22,693

21,700

20,899

Property, plant and equipment

31,299

29,491

32,610

Goodwill and other assets

59,627

59,108

59,275

Future income taxes

-

269

-

113,619

110,568

112,784

$

497,293

$

467,312

$ 491,277

Current Liabilities

Bank indebtedness $

1,158

$

6,830

$ 3,677

Accounts payable and accrued liabilities

192,957

188,388

190,985

Distributions payable to unitholders

5,639

13,268

5,307

Income taxes payable

1,677

1,457

1,855

Equipment notes payable

-

70

1,218

Derivative instrument liability (note 4)

665

175

-

Discontinued operations

287

347

453

202,383

210,535

203,495

Non-Current Liabilities

Future income taxes

82

-

1,350

Other liabilities

376

1,716

1,634

Long-term pension liability

3,137

3,079

2,918

Long-term debt

87,019

53,879

81,738

90,614

58,674

87,640

Unitholders’ Equity

Trust units (note 5)

104,871

104,871

104,871

Unit-based compensation (note 6)

3,931

2,907

2,185

Accumulated earnings

95,940

90,432

92,680

Accumulated other comprehensive (loss) income (note 4)

(446)

(107)

406

95,494

90,325

93,086

Total unitholders’ equity

204,296

198,103

200,142

$

497,293

$

467,312

$ 491,277

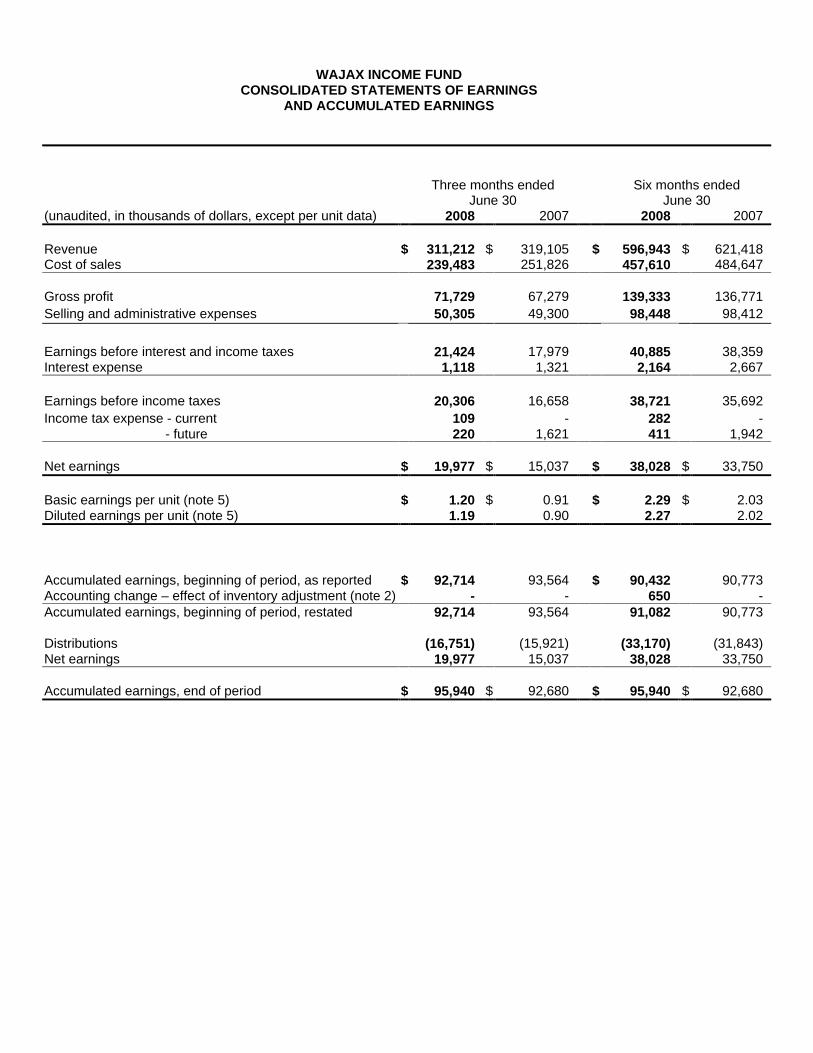

WAJAX INCOME FUND

CONSOLIDATED STATEMENTS OF EARNINGS AND ACCUMULATED EARNINGS

Three months ended

June 30

Six months ended

June 30 (unaudited, in thousands of dollars, except per unit data)

2008

2007

2008

2007

Revenue Cost of sales

$

311,212 239,483

$

319,105 251,826

$

596,943 457,610

$

621,418 484,647

Gross profit

71,729

67,279

139,333

136,771 Selling and administrative expenses

50,305

49,300

98,448

98,412

Earnings before interest and income taxes

21,424

17,979

40,885

38,359 Interest expense

1,118

1,321

2,164

2,667

Earnings before income taxes

20,306

16,658

38,721

35,692 Income tax expense - current

109

-

282

- - future

220

1,621

411

1,942

Net earnings $

19,977 $

15,037

$

38,028 $

33,750

Basic earnings per unit (note 5) $

1.20 $

0.91

$

2.29 $

2.03 Diluted earnings per unit (note 5)

1.19

0.90

2.27

2.02

Accumulated earnings, beginning of period, as reported $

92,714

93,564

$

90,432

90,773 Accounting change – effect of inventory adjustment (note 2)

-

-

650

- Accumulated earnings, beginning of period, restated

92,714

93,564

91,082

90,773

Distributions

(16,751)

(15,921)

(33,170)

(31,843) Net earnings

19,977

15,037

38,028

33,750

Accumulated earnings, end of period $

95,940 $

92,680

$

95,940 $

92,680

WAJAX INCOME FUND

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

Three months ended

June 30

Six months ended

June 30 (unaudited, in thousands of dollars)

2008

2007

2008 2007

Net earnings $

19,977 $

15,037

$

38,028 $

33,750

Losses on derivative instruments designated as cash flow hedges in prior periods transferred to net income in the current period, net of tax (note 4)

(189)

(41)

(133)

(171)

Gains (losses) on derivative instruments designated as cash flow hedges, net of tax (note 4)

294

143

(206)

24

Other comprehensive income (loss)

105

102

(339)

(147)

Comprehensive income $

20,082 $

15,139

$

37,689 $

33,603

WAJAX INCOME FUND

CONSOLIDATED STATEMENTS OF CASH FLOWS

Three months ended June 30

(unaudited, in thousands of dollars)

2008

2007

OPERATING ACTIVITIES

Net earnings from continuing operations $

19,977

$

15,037

Items not affecting cash flows:

Amortization

- Rental equipment

1,274

1,127

- Property, plant and equipment

1,025

1,108

- Intangible assets

103

71

- Deferred financing costs

70

70

Pension expense, net of payments

29

45

Long-term portion of mid-term incentive plan expense

177

547

Non-cash rental expense

12

12

Unit-based compensation expense (note 6)

559

302

Future income taxes

220

1,621

Cash flows from continuing operations before changes in non-cash working capital

23,446

19,940

Changes in non-cash working capital

Accounts receivable

6,106

(4,689)

Inventories

(8,404)

4,229

Prepaid expenses and other recoverable amounts

(2,059)

922

Accounts payable and accrued liabilities

9,188

9,495

Income taxes payable

(16)

46

Unrealized gain in derivative instrument

-

53

4,815

10,056

Cash flows from operating activities from continuing operations

28,261

29,996

INVESTING ACTIVITIES

Rental equipment additions

(2,433)

(3,132)

Proceeds on disposal of rental equipment

192

256

Property, plant and equipment additions

(2,437)

(957)

Proceeds on disposal of property, plant and equipment

5

43

Acquisition of business (note 10)

(323)

(322)

(4,996)

(4,112)

Cash flows from continuing operations before financing activities

23,265

25,884