Embed Size (px)

Citation preview

Secrets of the Payments Processors

Chuck Phipps, CTP, AAP NetSpend

Dean Seifert Vantiv

Anita Stevenson Patterson, CTP Cox Enterprises

Travis Soto, CTP, AAP Merrick Bank

What are the Options?

• Credit

• Debit

• ACH

• Checks

• Wires

There are five primary payments types:

Our Focus is on electronic payments

What is a Payments System?

Payments Systems allow for the payment of funds in exchange for goods or services.

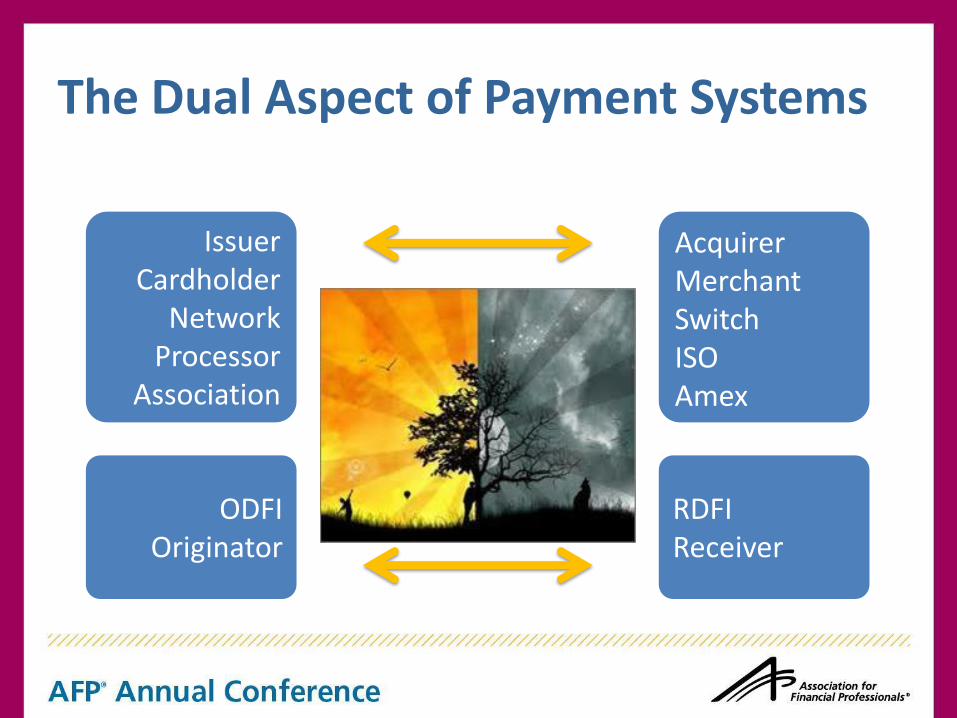

Issuer Cardholder

Network Processor

Association

Acquirer Merchant Switch ISO Amex RDFI Receiver

ODFI Originator

The Dual Aspect of Payment Systems

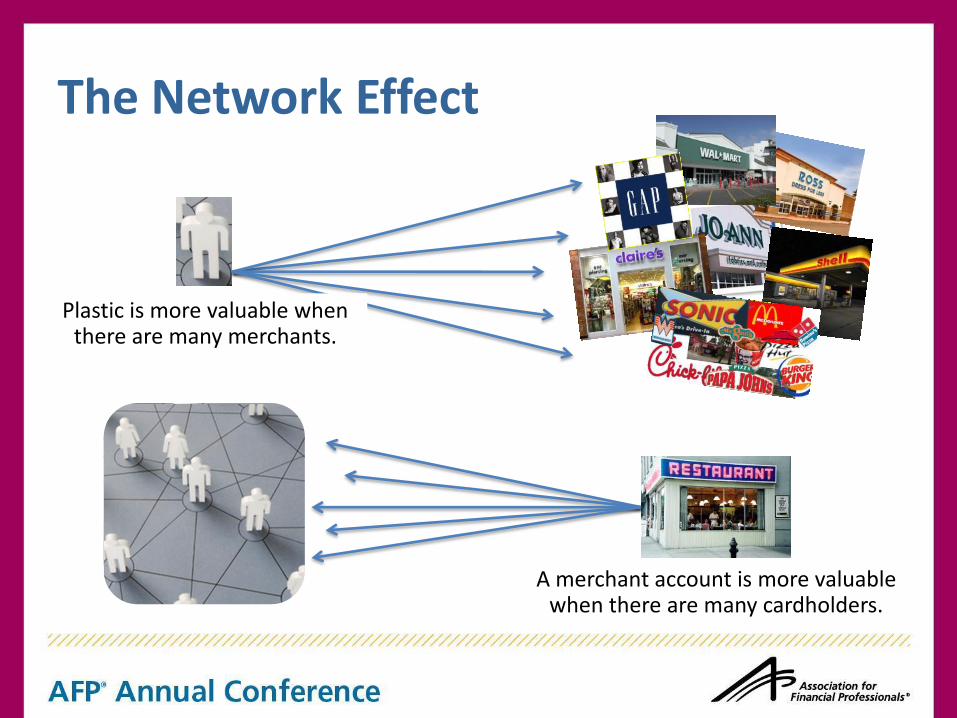

Plastic is more valuable when there are many merchants.

A merchant account is more valuable when there are many cardholders.

The Network Effect

Tools for Corporate Use

• Corporations use all payment types: − Checks − Cash − Wires − Credit cards − P-cards − ACH

• Corporate & ACH − Direct deposit of payroll − Daily Cash concentration − Payments to vendors & suppliers − Payments for federal & state taxes − Conversion of lockbox payments − Conversion of return items

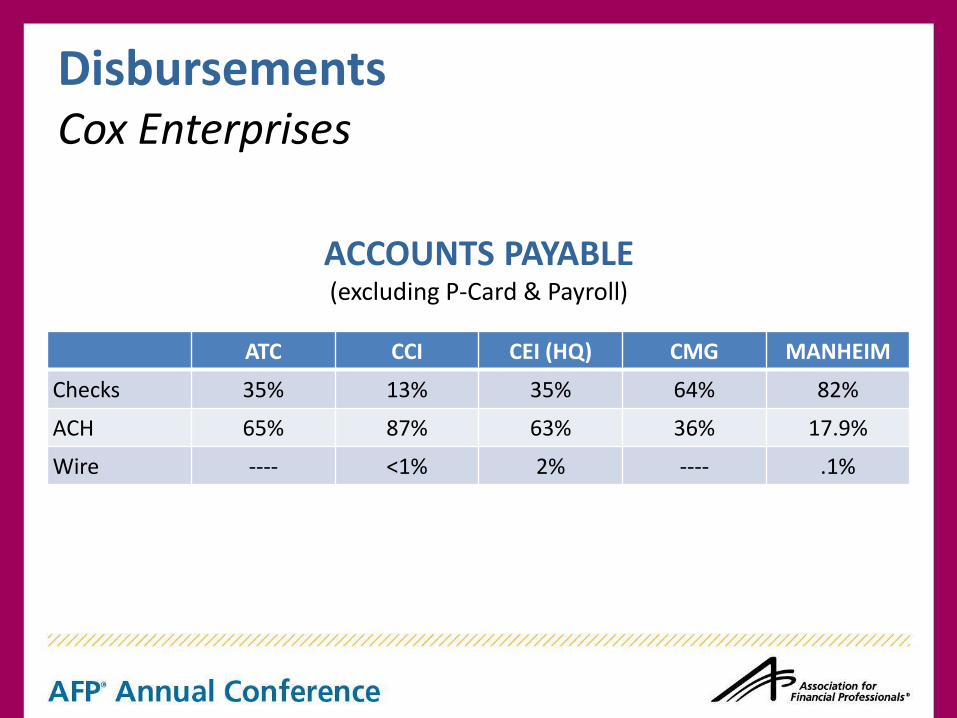

Disbursements Cox Enterprises

ATC CCI CEI (HQ) CMG MANHEIM

Checks 35% 13% 35% 64% 82%

ACH 65% 87% 63% 36% 17.9%

Wire ---- <1% 2% ---- .1%

ACCOUNTS PAYABLE (excluding P-Card & Payroll)

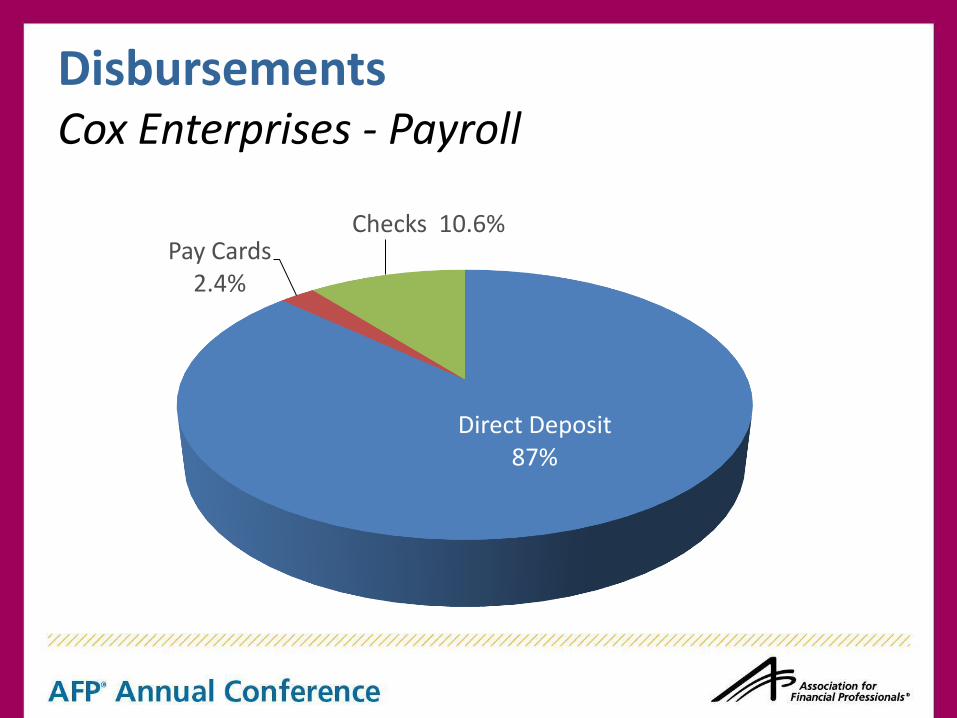

Disbursements Cox Enterprises - Payroll

Direct Deposit 87%

Pay Cards 2.4%

Checks 10.6%

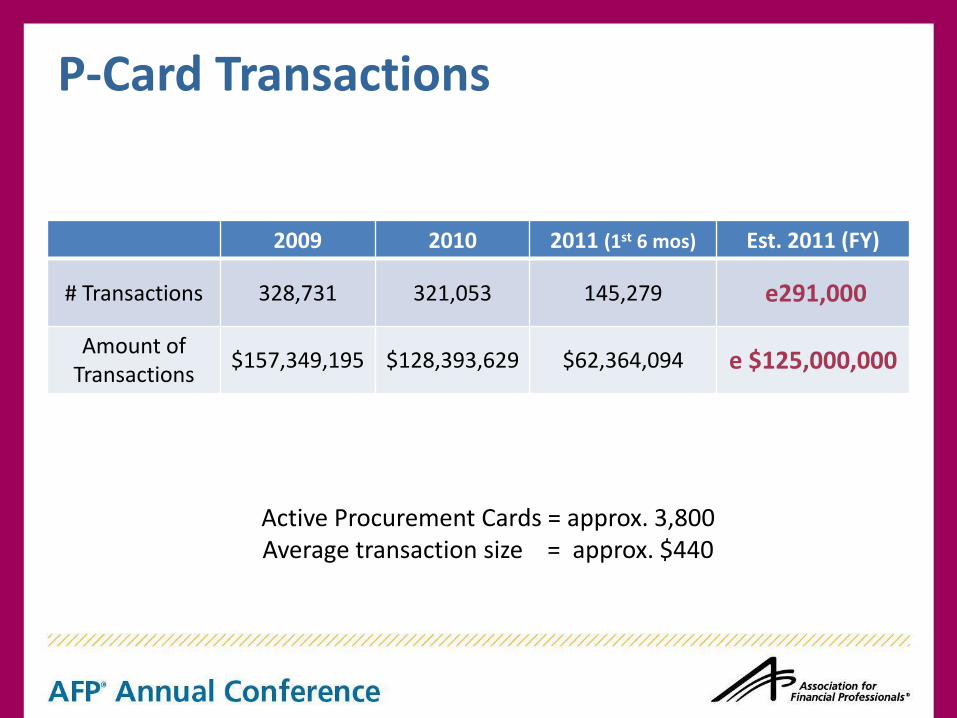

P-Card Transactions

2009 2010 2011 (1st 6 mos) Est. 2011 (FY)

# Transactions 328,731 321,053 145,279 e291,000

Amount of Transactions

$157,349,195 $128,393,629 $62,364,094 e $125,000,000

Active Procurement Cards = approx. 3,800 Average transaction size = approx. $440

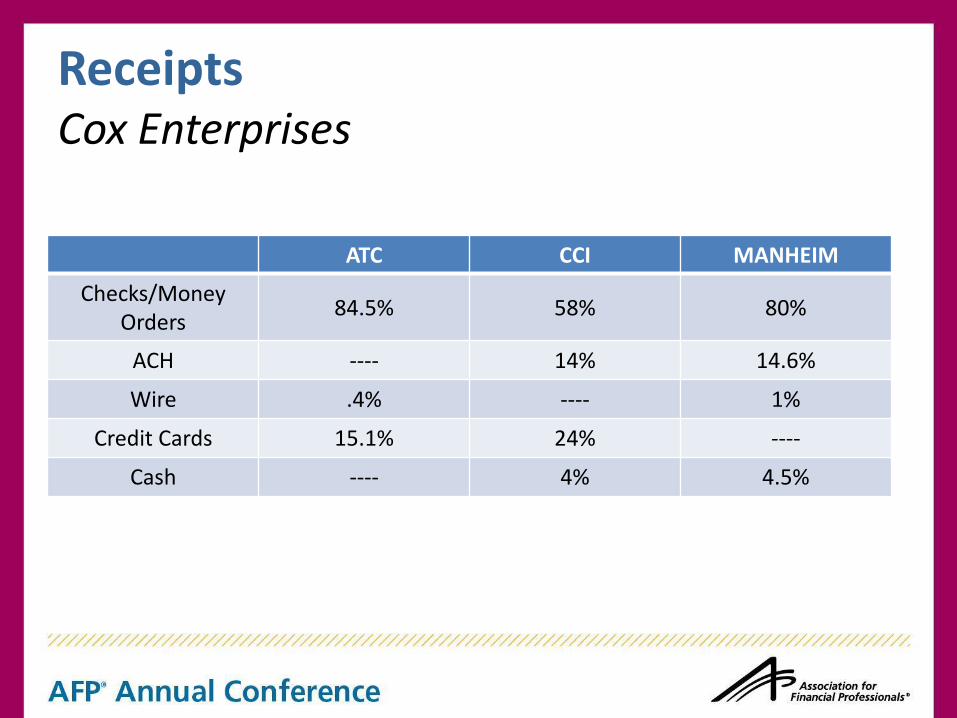

Receipts Cox Enterprises

ATC CCI MANHEIM

Checks/Money Orders

84.5% 58% 80%

ACH ---- 14% 14.6%

Wire .4% ---- 1%

Credit Cards 15.1% 24% ----

Cash ---- 4% 4.5%

Goals for Many Corporations

• 100% electronic payroll.

• Reduced reliance on paper items for A/P.

• Straight-thru processing.

• Improved verification of account numbers & account holders.

• Biller directory that identifies a corporation’s appropriate routing number & bank account for wires & ACH’s.

• More parity between consumer & corporate protections. – with ACH processing

• Data and dollars traveling together.

• More involvement in rule-making.

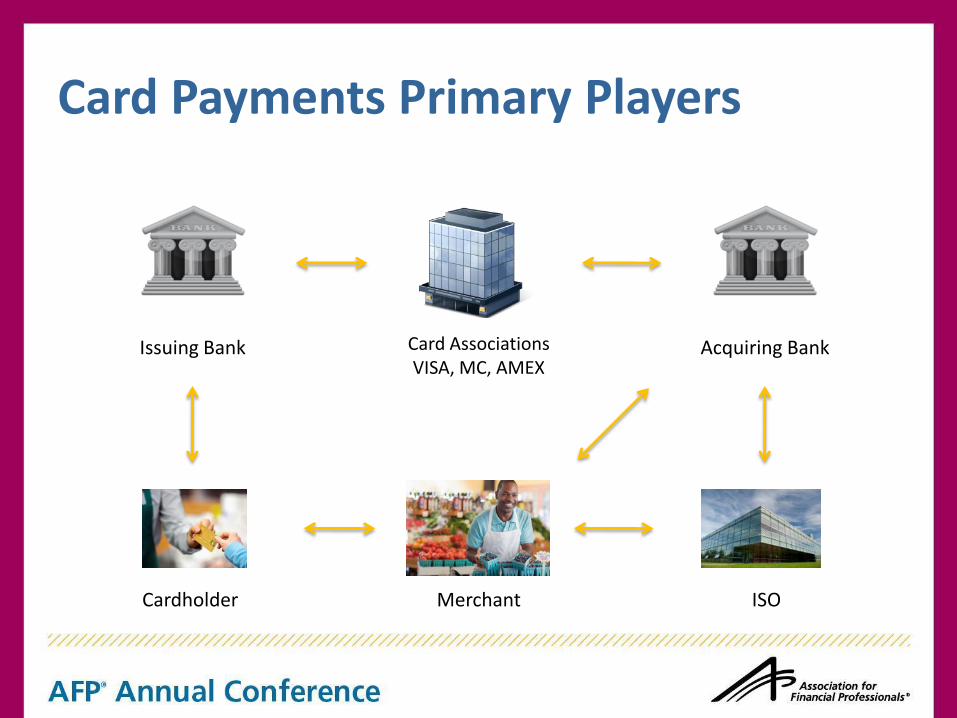

Card Payments Primary Players

Issuing Bank Acquiring Bank Card Associations VISA, MC, AMEX

Cardholder Merchant ISO

Card-Accepting Merchants Should understand:

• Discount Rate

• Interchange

• Early Termination Fee

• Monthly Minimums

• Mid-Qualified/Non-Qualified Fees

• PCI – Data Security

• Reserves

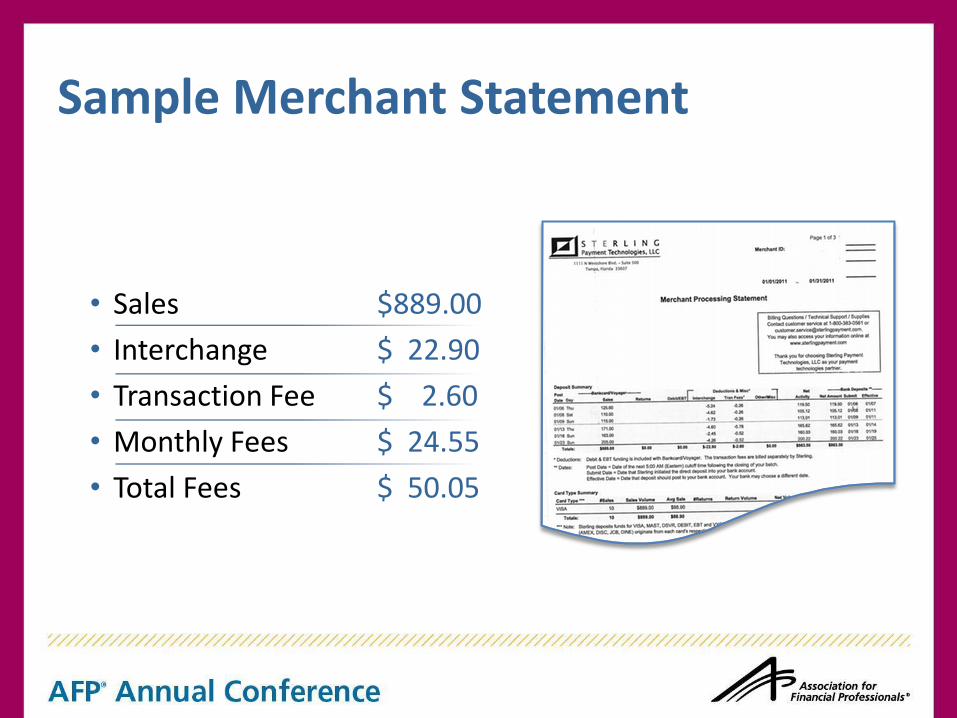

Sample Merchant Statement

• Sales $889.00

• Interchange $ 22.90

• Transaction Fee $ 2.60

• Monthly Fees $ 24.55

• Total Fees $ 50.05

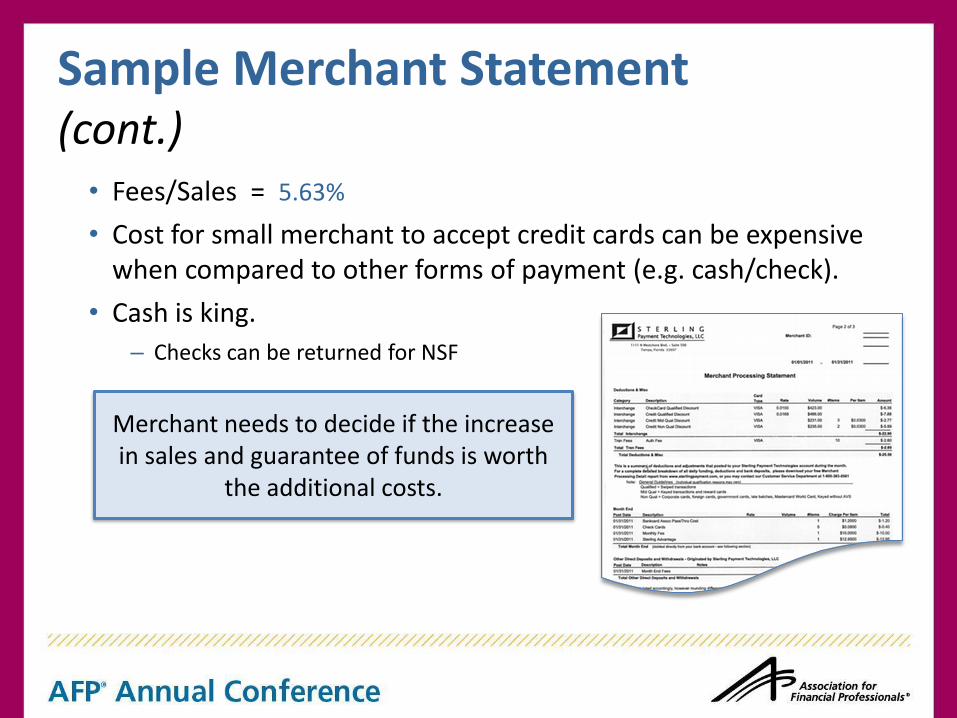

Sample Merchant Statement (cont.)

• Fees/Sales = 5.63%

• Cost for small merchant to accept credit cards can be expensive when compared to other forms of payment (e.g. cash/check).

• Cash is king.

– Checks can be returned for NSF

Merchant needs to decide if the increase in sales and guarantee of funds is worth

the additional costs.

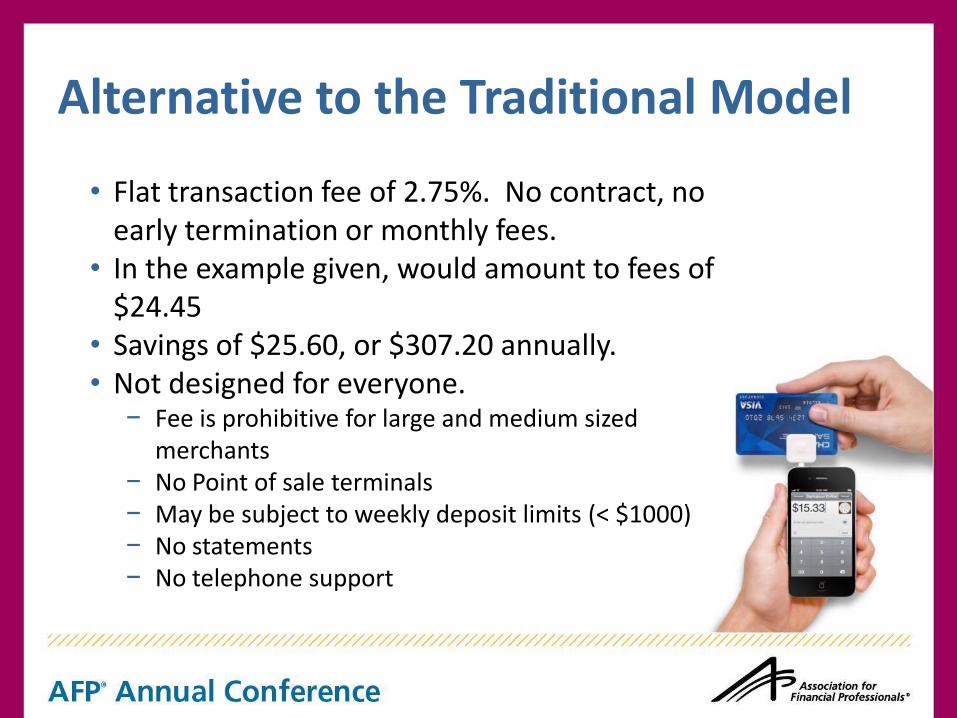

Alternative to the Traditional Model

• Flat transaction fee of 2.75%. No contract, no early termination or monthly fees.

• In the example given, would amount to fees of $24.45

• Savings of $25.60, or $307.20 annually. • Not designed for everyone.

− Fee is prohibitive for large and medium sized merchants

− No Point of sale terminals − May be subject to weekly deposit limits (< $1000) − No statements − No telephone support

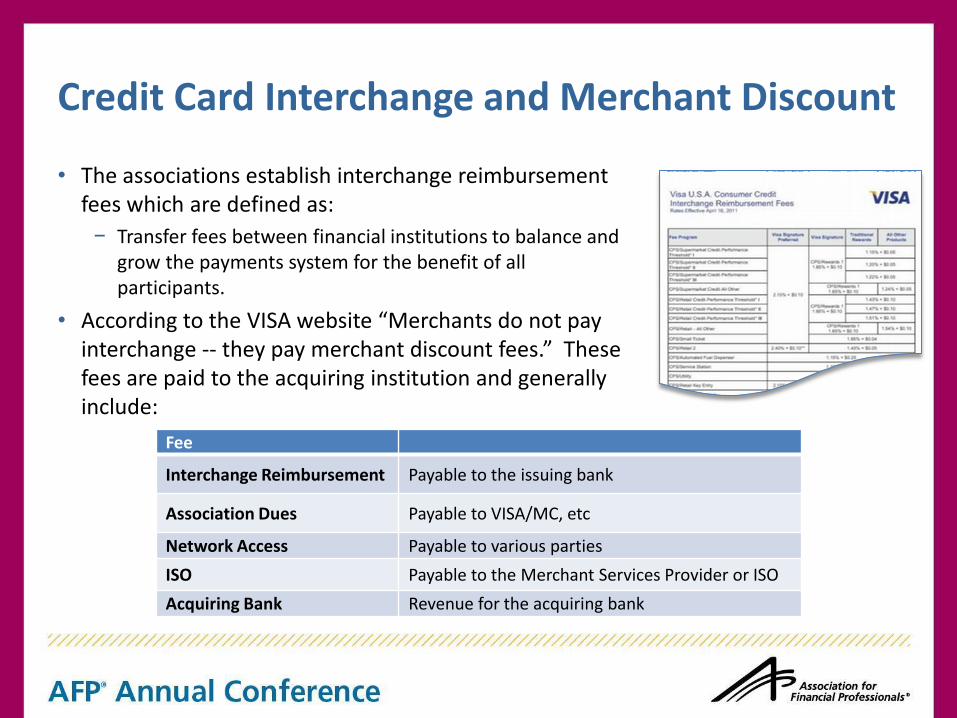

Credit Card Interchange and Merchant Discount

• The associations establish interchange reimbursement fees which are defined as:

− Transfer fees between financial institutions to balance and grow the payments system for the benefit of all participants.

• According to the VISA website “Merchants do not pay interchange -- they pay merchant discount fees.” These fees are paid to the acquiring institution and generally include:

Fee

Interchange Reimbursement Payable to the issuing bank

Association Dues Payable to VISA/MC, etc

Network Access Payable to various parties

ISO Payable to the Merchant Services Provider or ISO

Acquiring Bank Revenue for the acquiring bank

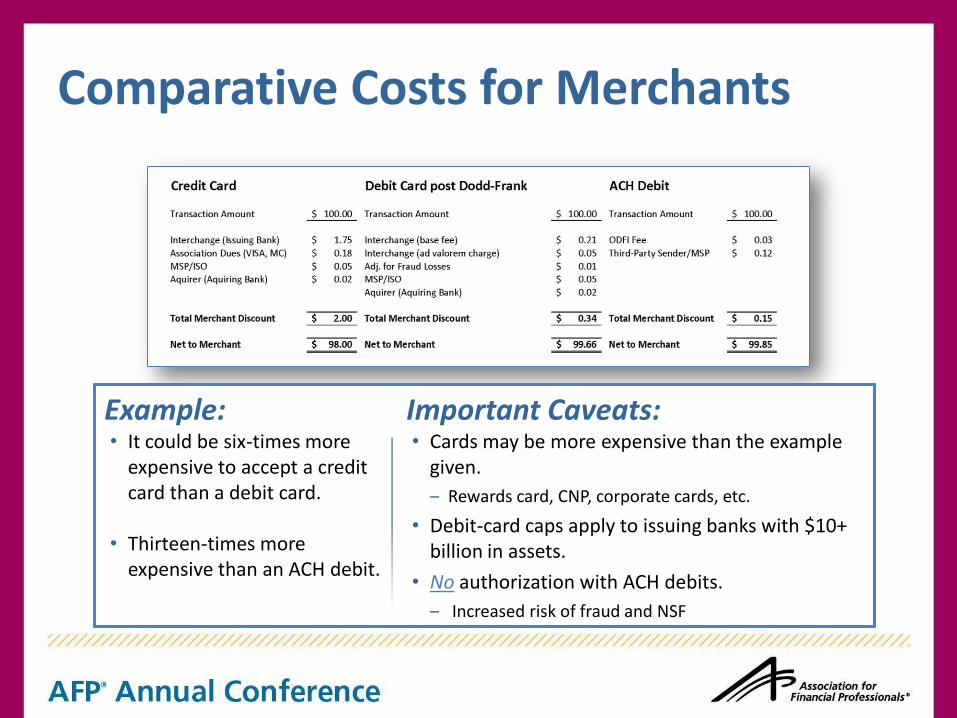

Comparative Costs for Merchants

Example: • It could be six-times more

expensive to accept a credit card than a debit card.

• Thirteen-times more

expensive than an ACH debit.

Important Caveats: • Cards may be more expensive than the example

given.

– Rewards card, CNP, corporate cards, etc.

• Debit-card caps apply to issuing banks with $10+ billion in assets.

• No authorization with ACH debits.

– Increased risk of fraud and NSF

Merchant’s response

• With the reduction in interchange from Dodd-Frank, retailers are: − Trying to steer consumers toward using debit cards.

− This has been happening for years, but the savings are now greater.

Bank’s response But consumers still have a choice.

• Issuers continue to innovate. – And make up for lost revenue tied to debit card transactions.

• Wells Fargo is testing a $3-monthly debit card fee. B of A implementing a $5-monthly debit card fee.

• Issuers no longer offering rewards tied to debit cards.

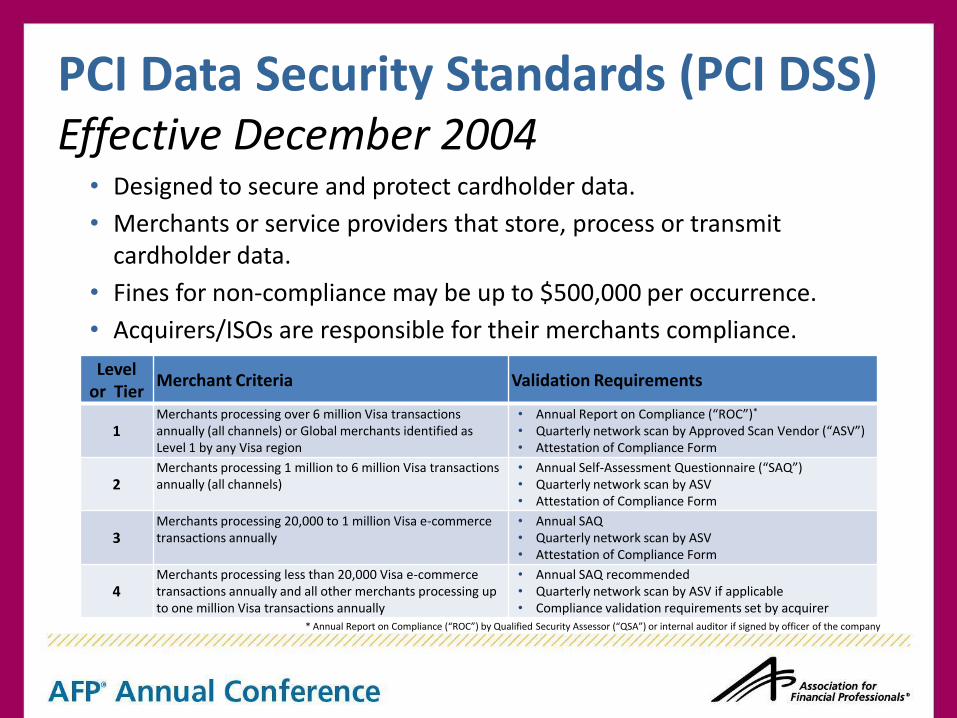

PCI Data Security Standards (PCI DSS) Effective December 2004

• Designed to secure and protect cardholder data.

• Merchants or service providers that store, process or transmit cardholder data.

• Fines for non-compliance may be up to $500,000 per occurrence.

• Acquirers/ISOs are responsible for their merchants compliance. Level

or Tier Merchant Criteria Validation Requirements

1 Merchants processing over 6 million Visa transactions annually (all channels) or Global merchants identified as Level 1 by any Visa region

• Annual Report on Compliance (“ROC”)*

• Quarterly network scan by Approved Scan Vendor (“ASV”) • Attestation of Compliance Form

2 Merchants processing 1 million to 6 million Visa transactions annually (all channels)

• Annual Self-Assessment Questionnaire (“SAQ”) • Quarterly network scan by ASV • Attestation of Compliance Form

3 Merchants processing 20,000 to 1 million Visa e-commerce transactions annually

• Annual SAQ • Quarterly network scan by ASV • Attestation of Compliance Form

4 Merchants processing less than 20,000 Visa e-commerce transactions annually and all other merchants processing up to one million Visa transactions annually

• Annual SAQ recommended • Quarterly network scan by ASV if applicable • Compliance validation requirements set by acquirer

* Annual Report on Compliance (“ROC”) by Qualified Security Assessor (“QSA”) or internal auditor if signed by officer of the company

1

2

3

4

5

6

Payment Lifecycle

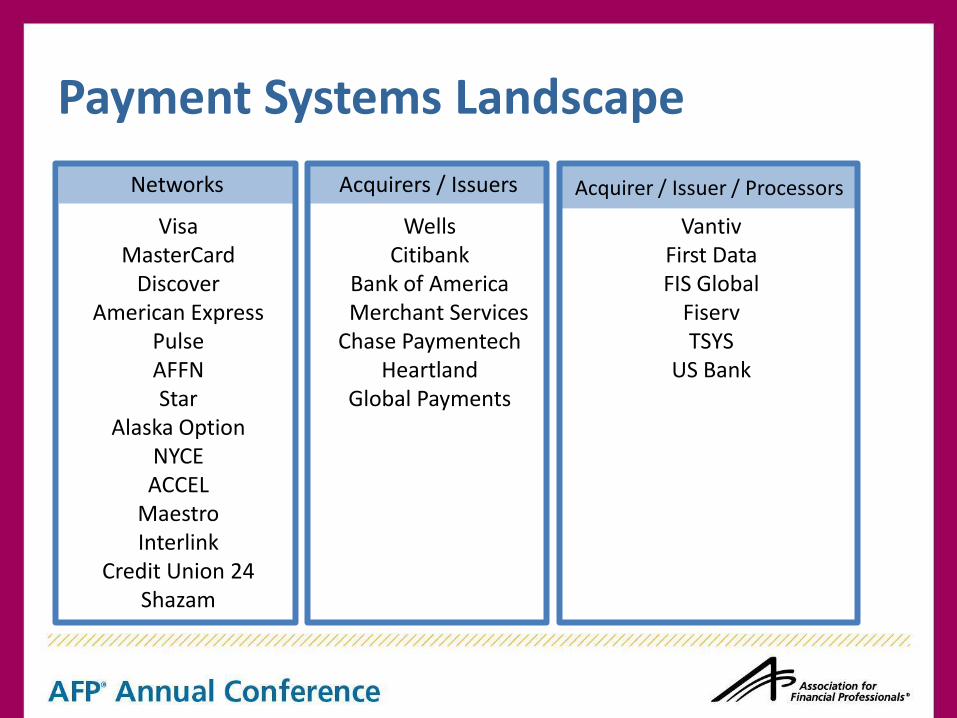

Networks

Visa MasterCard

Discover American Express

Pulse AFFN Star

Alaska Option NYCE ACCEL

Maestro Interlink

Credit Union 24 Shazam

Acquirers / Issuers

Wells Citibank

Bank of America Merchant Services

Chase Paymentech Heartland

Global Payments

Acquirer / Issuer / Processors

Vantiv First Data FIS Global

Fiserv TSYS

US Bank

Payment Systems Landscape

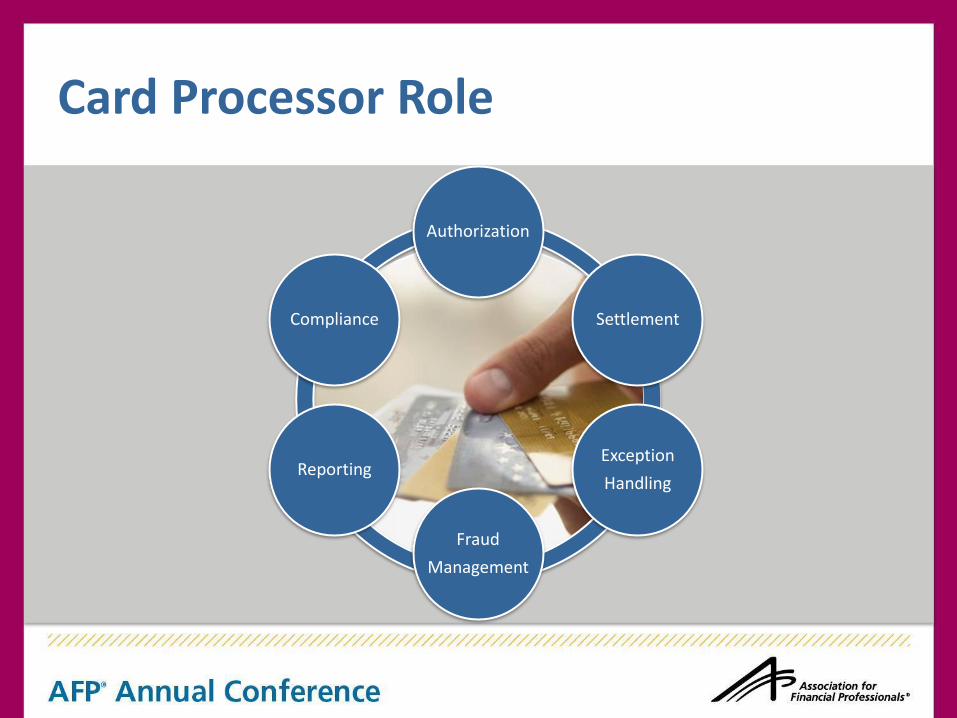

Card Processor Role

Settlement

Exception

Handling

Fraud

Management

Reporting

Compliance

Authorization

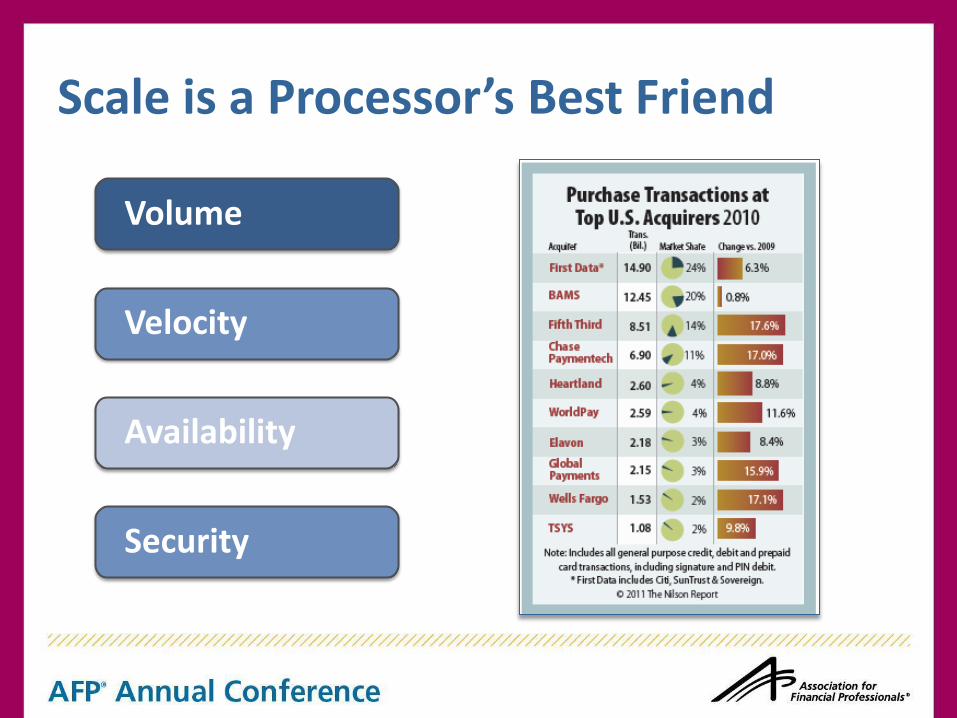

Volume

Velocity

Availability

Security

Scale is a Processor’s Best Friend

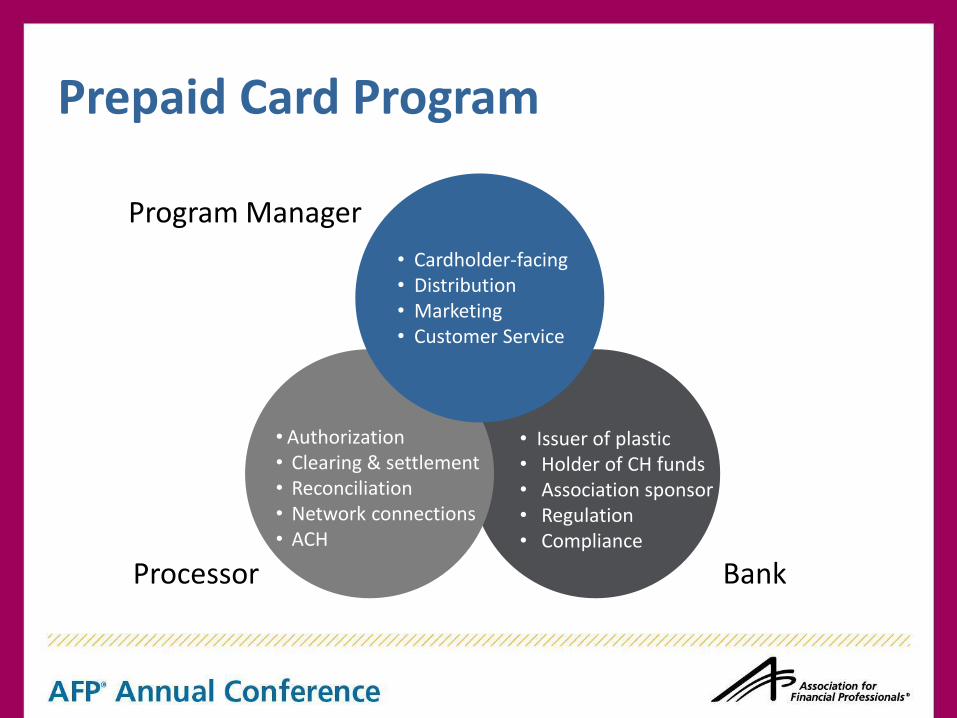

Prepaid

One Account-Holder per separate account

One pooled account for many Account-Holders

The difference between Debit and Prepaid

Debit

Processor

Program Manager

Bank

• Issuer of plastic • Holder of CH funds • Association sponsor • Regulation • Compliance

• Authorization • Clearing & settlement • Reconciliation • Network connections • ACH

Prepaid Card Program

• Cardholder-facing • Distribution • Marketing • Customer Service

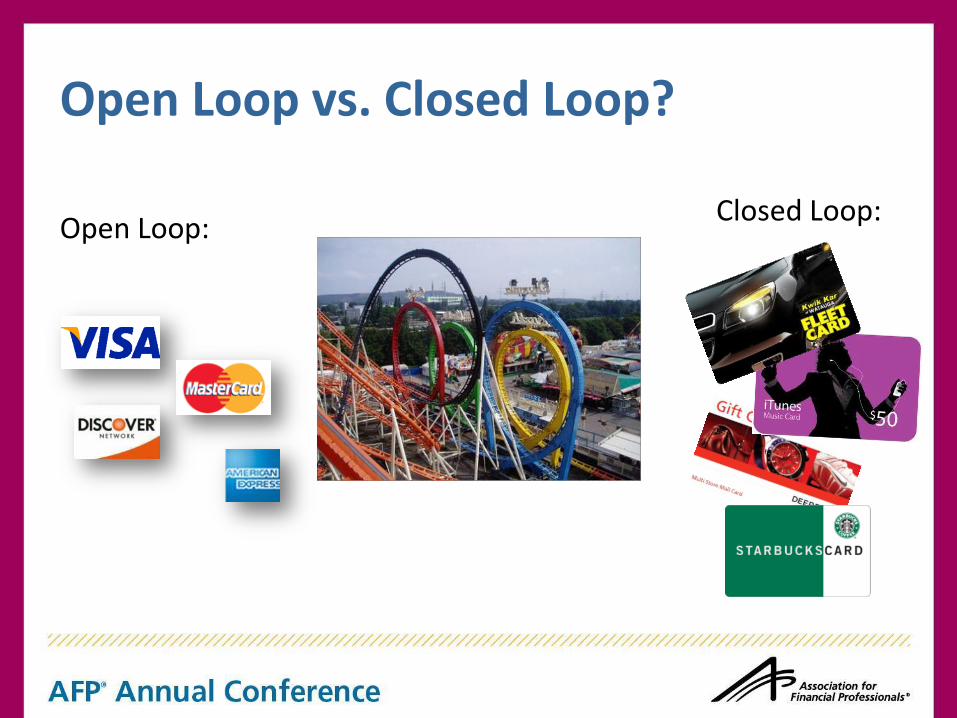

Open Loop:

Open Loop vs. Closed Loop?

Closed Loop:

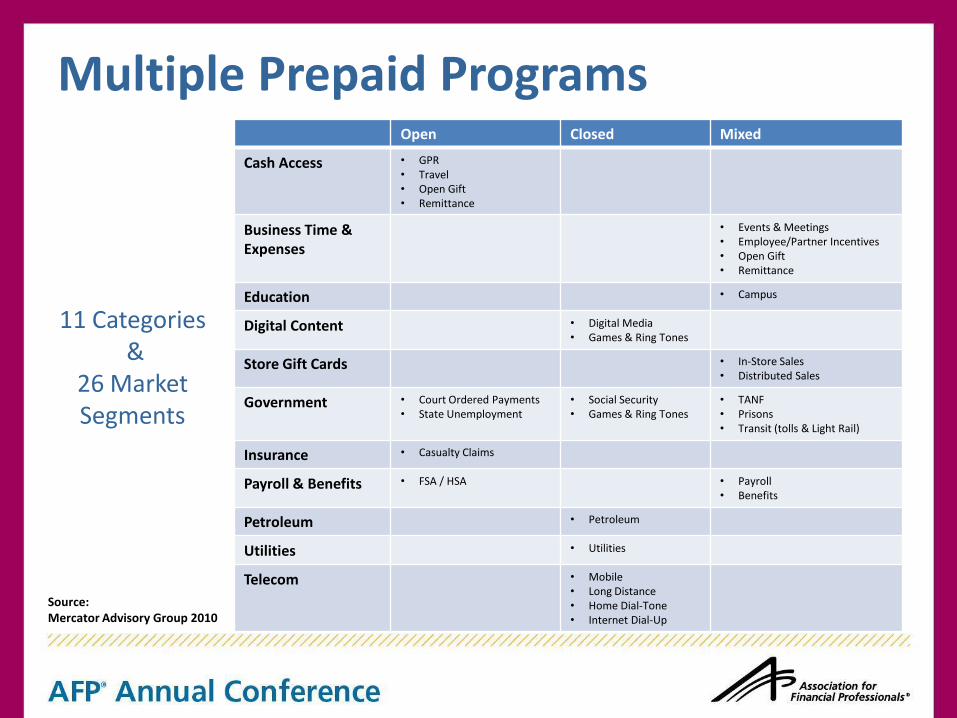

Multiple Prepaid Programs Open Closed Mixed

Cash Access • GPR • Travel • Open Gift • Remittance

Business Time & Expenses

• Events & Meetings • Employee/Partner Incentives • Open Gift • Remittance

Education • Campus

Digital Content • Digital Media

• Games & Ring Tones

Store Gift Cards • In-Store Sales

• Distributed Sales

Government • Court Ordered Payments • State Unemployment

• Social Security • Games & Ring Tones

• TANF • Prisons • Transit (tolls & Light Rail)

Insurance • Casualty Claims

Payroll & Benefits • FSA / HSA • Payroll • Benefits

Petroleum • Petroleum

Utilities • Utilities

Telecom • Mobile

• Long Distance • Home Dial-Tone • Internet Dial-Up

Source: Mercator Advisory Group 2010

11 Categories &

26 Market Segments

• Implementation took less time than expected.

• Mandated electronic payroll vs. optional?

• Employee adoption was key.

• Program management vs. processing management?

• Direct Deposit adoption near 90%.

More info: Tom Hunt, CTP. Big Change, AFP Exchange, April-2011. p. 33

Pay Card Case Study

Payment Network Operating Costs

Stay on target:

• Transaction

• Event

• License

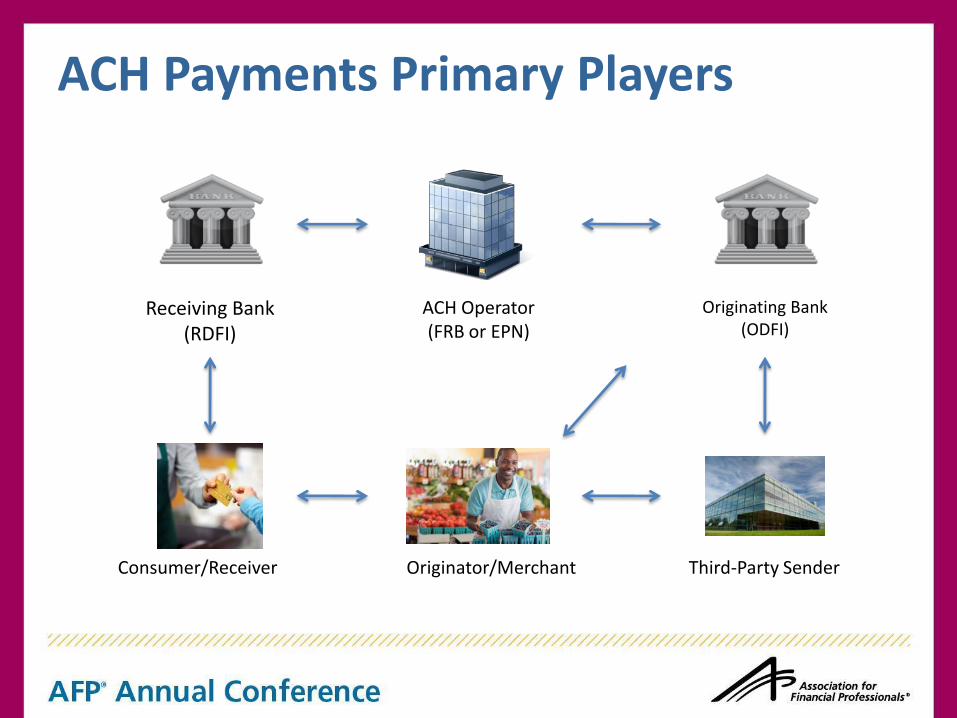

ACH Payments Primary Players

ACH Operator (FRB or EPN)

Receiving Bank (RDFI)

Originating Bank (ODFI)

Consumer/Receiver Originator/Merchant Third-Party Sender

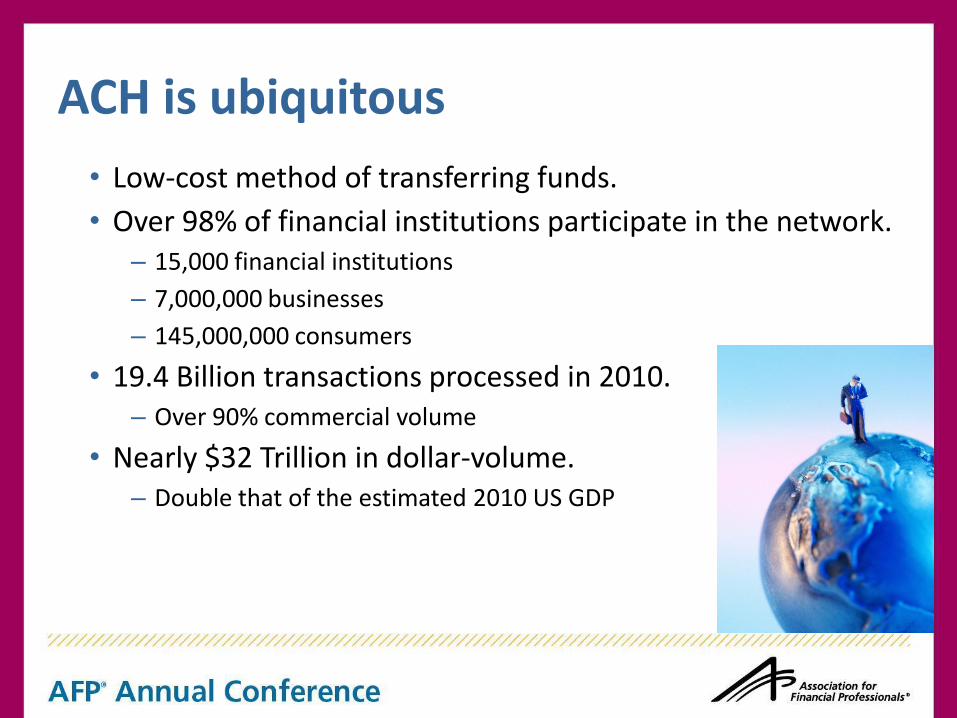

ACH is ubiquitous

• Low-cost method of transferring funds.

• Over 98% of financial institutions participate in the network. – 15,000 financial institutions

– 7,000,000 businesses

– 145,000,000 consumers

• 19.4 Billion transactions processed in 2010. – Over 90% commercial volume

• Nearly $32 Trillion in dollar-volume. – Double that of the estimated 2010 US GDP

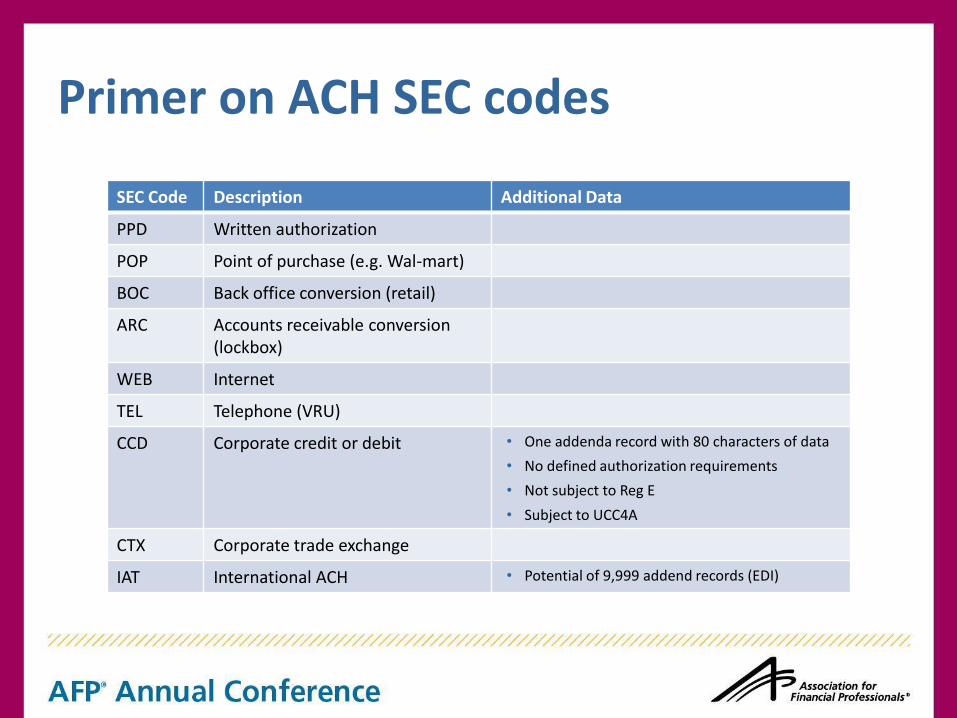

Primer on ACH SEC codes

SEC Code Description Additional Data

PPD Written authorization

POP Point of purchase (e.g. Wal-mart)

BOC Back office conversion (retail)

ARC Accounts receivable conversion (lockbox)

WEB Internet

TEL Telephone (VRU)

CCD Corporate credit or debit • One addenda record with 80 characters of data

• No defined authorization requirements

• Not subject to Reg E

• Subject to UCC4A

CTX Corporate trade exchange

IAT International ACH • Potential of 9,999 addend records (EDI)

Merchants who use ACH Should understand:

• Who the players are... – Originator, ODFI, Operator, RDFI, Receiver, et al.

• NACHA rules, Reg. E and UCC4A – Rules, rules, and more rules...

• ACH credit vs. debit – Push vs. pull

• Batch vs. real-time – No real time authorization or guarantee of good funds

• Standard Entry Class Codes (SECs) – ACH warranties are based on the transaction type (SEC)

• Authorization requirements – Differ depending on the SEC code used

– Requirement to maintain copies of the authorization for 2 years

Merchants who use ACH Should also understand:

• Settlement and delivery timeframes – Credits: delivered to ACH operator one-to-two days prior to settlement date.

• Credits settle to the RDFI at 8:30am on the settlement date

– Debits: delivered to ACH operator the day before settlement. • Debits Settle to the RDFI at 11:00am on the settlement date

• Risk of Return – Again, no real-time authorization or guarantee of funds – Compliance with NOCs

• Reserves – There is risk in ACH processing

• The ODFI warrants its Originator’s transactions • ODFI is responsible for their Originator’s compliance • KYC applies

• Data Security Rules

Merchants should keep an eye on these ACH topics:

• Secure Vault Payments (SVP)

– SVP offers the Immediate Authorization of an ACH credit transaction with guaranteed payment for on-line payments and e-commerce transactions.

• Expedited Processing and Settlement (EPS)

– Would allow entries to be processed and settled on the same day.

– Preserves the existing processing and settlement windows.

• Current schedules have not changed in 35 years

– Ability for the ACH network to improve product offerings.

• Market demand • Customer expectations

– Proposed effective date of March 15, 2013

Regulatory Landscape?

Complex and Shifting

State Networks

Federal

Will 2012 be the Year of Chip & Pin?

• Mandate vs. Liability Shift

• Contact vs. Contactless

• Market Momentum & NFC

Standards

• Standards plural of stand ard (noun) 1. Something considered by an authority or by general consent

as a basis of comparison; an approved model.

2. An object that is regarded as the usual or most common size or form, of its kind: We stock the deluxe models as well as the standards.

3. A rule or principle that is used as a basis for judgment: They tried to establish standards for a new philosophical approach.

Standards

• We have too many standards. − Multiple organizations making up

“standards”

− There are so many that they are just suggestions

• Even the standards aren’t standard.

• What are we to follow? − Adoption is complex

− Some solutions are proprietary

− Lack of flexibility and interoperability

How do we get there? Electronic Payments Processes

• Have a limited selection of standards from which to choose.

• Involve corporate practitioners in the decision process.

• Ensure solutions for all. – Small

– Medium

– Large corporations

Thank You

• Questions?

• Follow-up discussions?

Chuck Phipps CTP, AAP EFT Processing Manager

512-539-5987 [email protected]

Anita Stevenson Patterson CTP Director of Treasury Services

678-645-4840 [email protected]

Travis Soto CTP, AAP VP –Treasurer

801-545-6619 [email protected]

Dean Seifert Senior VP – Product Strategy

303-601-6057 [email protected]

Contact Information

Resources and Additional Reading Contardi, James. Processors: Connecting the Dots for Payments Growth?

Lydian Journal, March-2011. http://www.pymnts.com/assets/Lydian_Journal/LydianJournalMarchBusiness1.pdf

Herbst-Murphy, Susan. Getting Down to Business: Commercial Cards in Business-to-Business Payments. Federal Reserve Bank of Philadelphia, Mar 2011. http://www.philadelphiafed.org/payment-cards-center/publications/discussion-papers/2011/D-2011-Commercial-Cards.pdf

Apfel, Ira. 5 Questions about Global Commercial Cards. AFP, Feb 2011. http://www.afponline.org/pub/res/news/5_Questions_about_Global_Commercial_Cards.html

Gibbons, Randy. Payments Innovation Takes Flight at Southwest Airlines. Pymnts.com/Briefing Room, Apr 2011. http://www.pymnts.com/payments-innovation-takes-flight-at-southwest-airlines

McCormack, Scott. How TSYS Prepaid is Reinventing Corporate Payments. Pymnts.com/Briefing Room, Apr 2011. http://www.pymnts.com/How-TSYS-Prepaid-is-Reinventing-Corporate-Payments-Transcript/

Visa Announces Plans to Accelerate Chip Migration and Adoption of Mobile Payments. Aug 2011 http://broadcast01p.visabroadcasts.com/xfm/?39697/1/dd4fa0859105b432fd8e5eba143f1980/16780800

Payment Cards. AFP Exchange. April-2011, p. 24.

Tom Hunt, CTP. Big Change: Why Retailer Big Lots Implemented a Pay Card Solution. AFP Exchange, Apr 2011, p. 33.

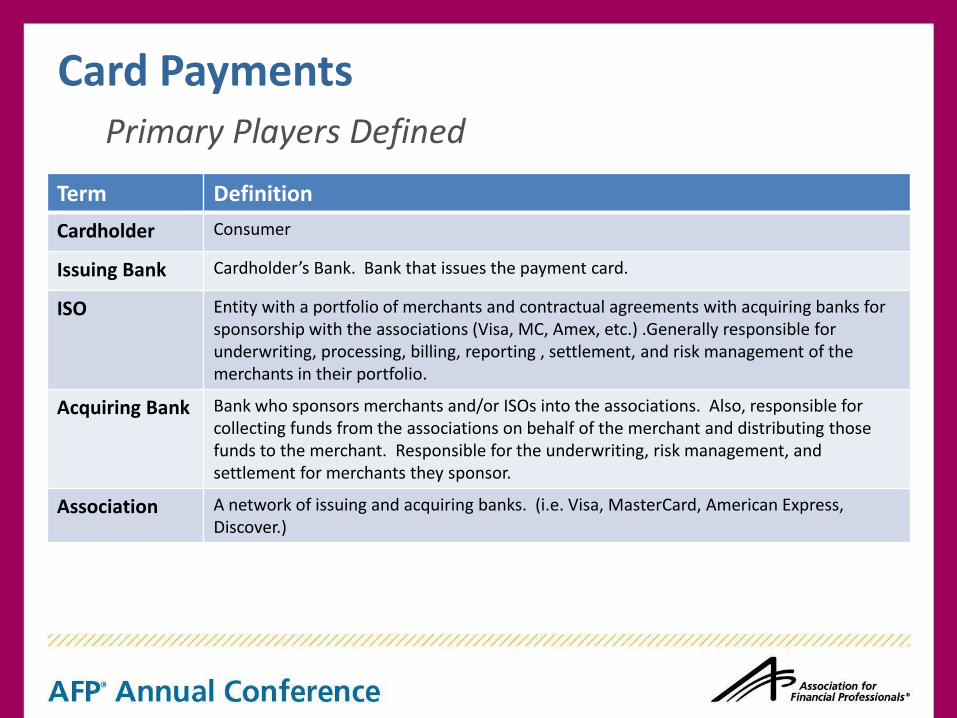

Card Payments Primary Players Defined

Term Definition

Cardholder Consumer

Issuing Bank Cardholder’s Bank. Bank that issues the payment card.

ISO Entity with a portfolio of merchants and contractual agreements with acquiring banks for sponsorship with the associations (Visa, MC, Amex, etc.) .Generally responsible for underwriting, processing, billing, reporting , settlement, and risk management of the merchants in their portfolio.

Acquiring Bank Bank who sponsors merchants and/or ISOs into the associations. Also, responsible for collecting funds from the associations on behalf of the merchant and distributing those funds to the merchant. Responsible for the underwriting, risk management, and settlement for merchants they sponsor.

Association A network of issuing and acquiring banks. (i.e. Visa, MasterCard, American Express, Discover.)

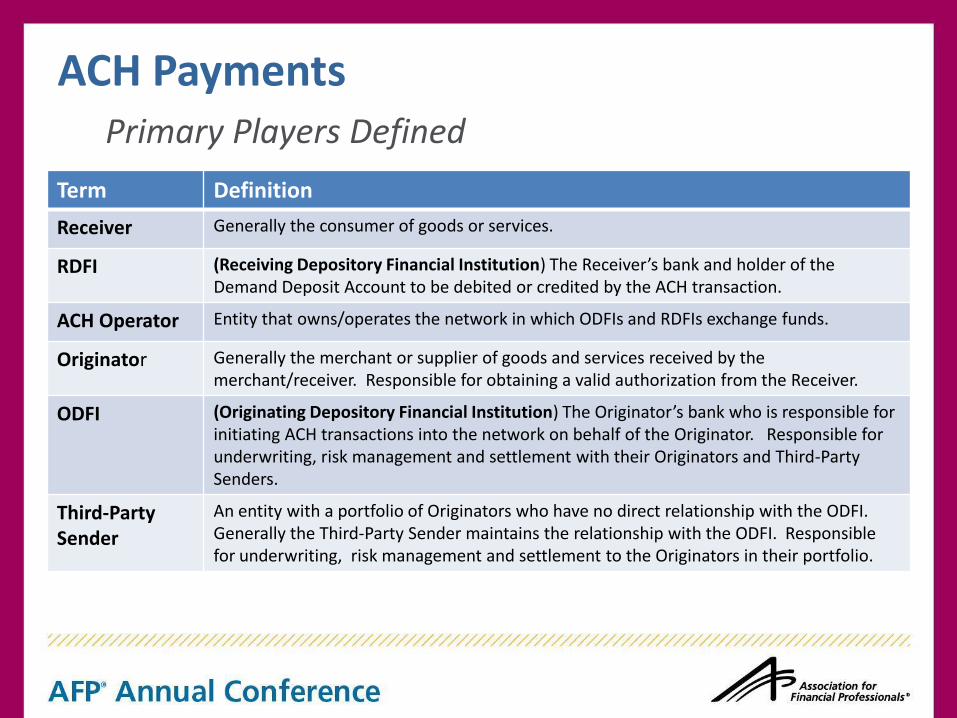

ACH Payments Primary Players Defined

Term Definition

Receiver Generally the consumer of goods or services.

RDFI (Receiving Depository Financial Institution) The Receiver’s bank and holder of the Demand Deposit Account to be debited or credited by the ACH transaction.

ACH Operator Entity that owns/operates the network in which ODFIs and RDFIs exchange funds.

Originator Generally the merchant or supplier of goods and services received by the merchant/receiver. Responsible for obtaining a valid authorization from the Receiver.

ODFI (Originating Depository Financial Institution) The Originator’s bank who is responsible for initiating ACH transactions into the network on behalf of the Originator. Responsible for underwriting, risk management and settlement with their Originators and Third-Party Senders.

Third-Party Sender

An entity with a portfolio of Originators who have no direct relationship with the ODFI. Generally the Third-Party Sender maintains the relationship with the ODFI. Responsible for underwriting, risk management and settlement to the Originators in their portfolio.