Embed Size (px)

Citation preview

Enriching the

Ecosystem

SECTION 1

• OVERVIEWSECTION 2

• PERFORMANCE OVERVIEWSECTION 3

• DIVIDENDS

A P R E S E N T A T I O N B Y

9 - 1 0 J U N E 2 0 1 4

INVEST MALAYSIA 2014 MANDARIN ORIENTAL HOTEL, KUALA LUMPUR

Enriching the

Ecosystem

SECTION 1

• OVERVIEWSECTION 2

• PERFORMANCE OVERVIEWSECTION 3

• DIVIDENDSSECTION 4

• CORPORATE GOVERNANCESECTION 5

• OUTLOOK & MEDIA CONVERGENCE

A P R E S E N T A T I O N B Y

9 - 1 0 J U N E 2 0 1 4

INVEST MALAYSIA 2014 MANDARIN ORIENTAL HOTEL, KUALA LUMPUR

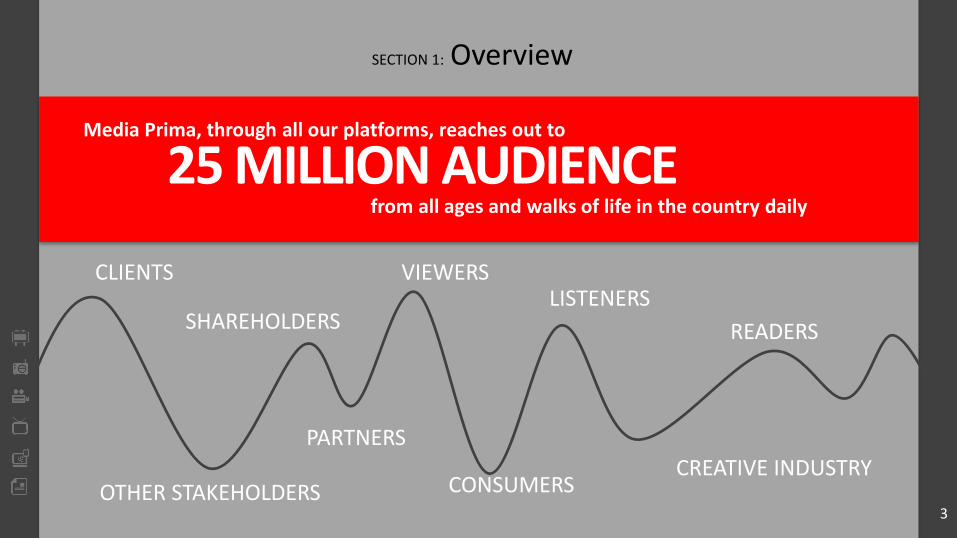

SECTION 1: Overview

Media Prima, through all our platforms, reaches out to

25 MILLION AUDIENCE from all ages and walks of life in the country daily

CLIENTS

READERS

LISTENERSVIEWERS

OTHER STAKEHOLDERS

PARTNERS

SHAREHOLDERS

CREATIVE INDUSTRYCONSUMERS

3

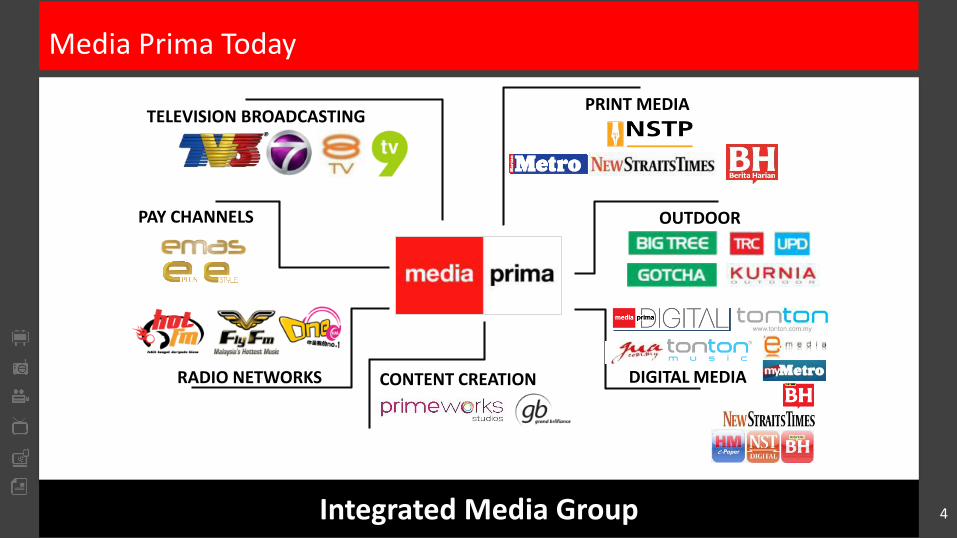

Integrated Media Group

Media Prima Today

TELEVISION BROADCASTING

RADIO NETWORKS

PRINT MEDIA

OUTDOOR

DIGITAL MEDIACONTENT CREATION

PAY CHANNELS

4

SECTION 2: Performance Review

5

Media Prima Today

Television Broadcasting Print Media Outdoor Media Radio Content Creation Digital

98%100%

100%

100%

100%

100%

100%

100%

100%

100%

100%

100%

80%

100% 100%

Fact sheet as at 31 December 2013

Issued and paid-up share capital

Shareholders funds

Total assets Cash Group borrowings

PDS Ratings (RAM)

RM1,100.5m RM1,656.4m RM2,606.7m RM618.4m RM498.4m AA2/P1(CP/MTN)

6

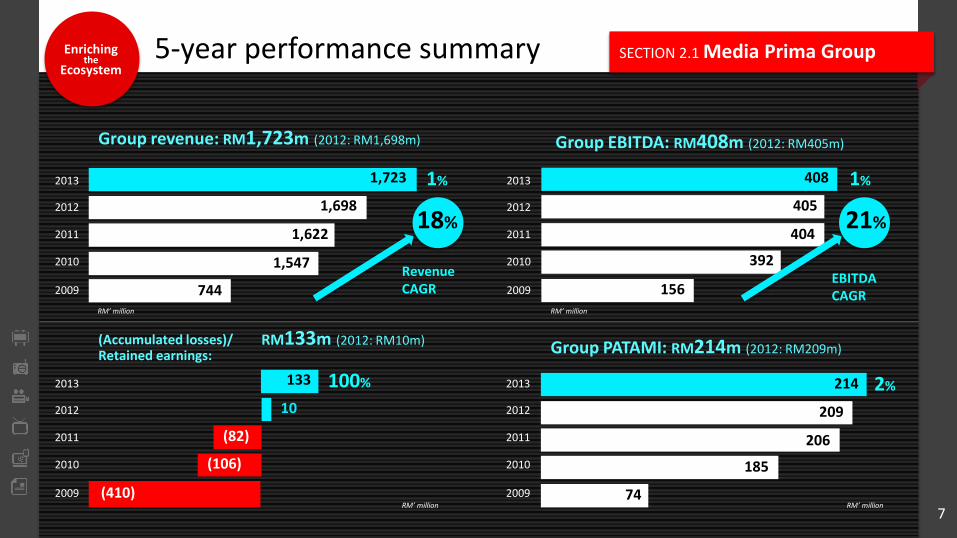

SECTION 2.1 Media Prima Group5-year performance summary

RM133m (2012: RM10m)

1%1,723

RM’ million

1,698

1,622

1,547

744

Group EBITDA: RM408m (2012: RM405m)

408

405

404

392

156

Group PATAMI: RM214m (2012: RM209m)

214

209

206

185

74

2013

2012

2011

2010

2009

2013

2012

2011

2010

2009

Group revenue: RM1,723m (2012: RM1,698m)

(Accumulated losses)/Retained earnings:

2013

2012

2011

2010

2009

SECTION 2.1 Media Prima Group

2013

2012

2011

2010

2009

133

(82)

(106)

(410)

10

1%

2%100%

RM’ million

RM’ million RM’ million

Enriching the

Ecosystem

EBITDA CAGR

Revenue CAGR

18% 21%

7

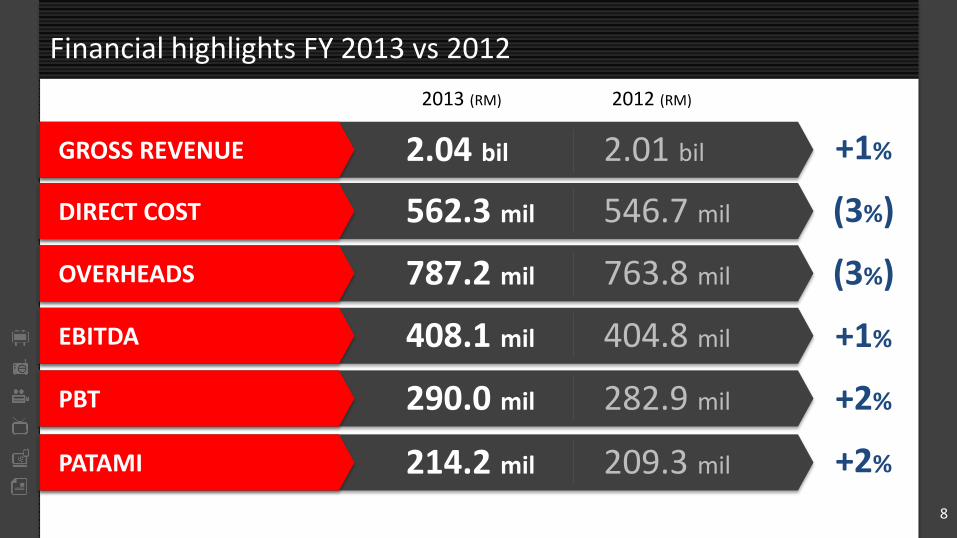

Financial highlights FY 2013 vs 2012

+1%

(3%)

(3%)

+1%

+2%

+2%

2012 (RM)2013 (RM)

2.04 bilGROSS REVENUE 2.01 bil

562.3 milDIRECT COST 546.7 mil

787.2 milOVERHEADS 763.8 mil

408.1 milEBITDA 404.8 mil

290.0 milPBT 282.9 mil

214.2 milPATAMI 209.3 mil

8

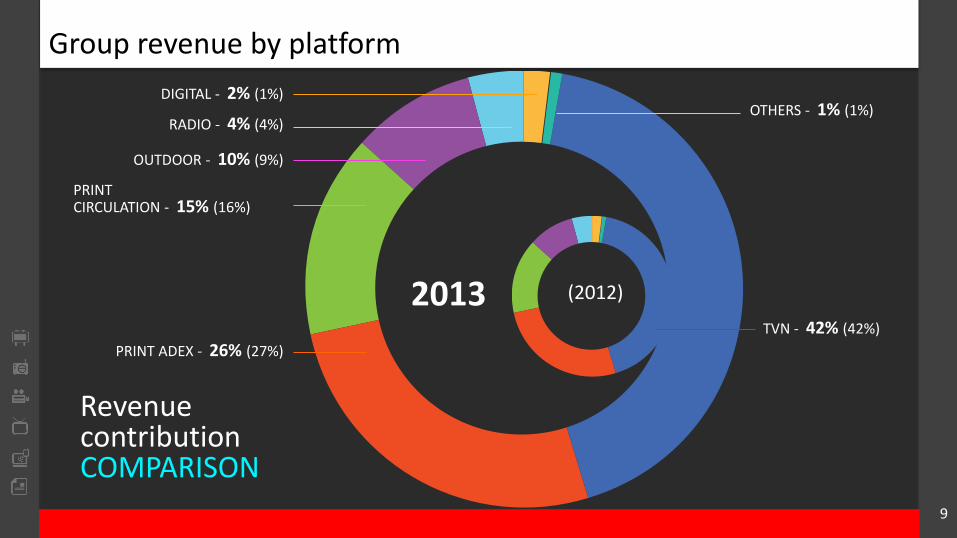

Group revenue by platform

(2012)2013

RevenuecontributionCOMPARISON

DIGITAL - 2% (1%)

RADIO - 4% (4%)

OUTDOOR - 10% (9%)

PRINTCIRCULATION - 15% (16%)

PRINT ADEX - 26% (27%)

OTHERS - 1% (1%)

TVN - 42% (42%)

9

SECTION 2.2: TV networks

10

Segmentation of our TV channels

Progressive Malay dominance

MASS MARKET

INSPIRASI HIDUPKU - Family orientated programmes, and cultural proximity content

FMCGs, communications, services & transportation brands

TAR

GET

AU

DIE

NC

EP

OSI

TIO

NIN

GA

DV

ERTI

SER

S

25-45 YRS OLD URBANITES, kids & mass Chinese

MY FEEL GOOD CHANNEL –Television as an escapade

Urban middle to high class image products and lifestyle brands

15-24 YRS OLD URBANITES, Mass Chinese

WE ARE DIFFERENT –Tastemaker, energetic and differentiation in content

MASS MARKET, Young semi-urban & rural Malays

DEKAT DI HATI- A mixture of drama, real-life & current affairs

FMCGs, non-traditional brands and government

Young urban, sports, energy drink, fashion brands. Chinese viewers with interest in health & wealth

11

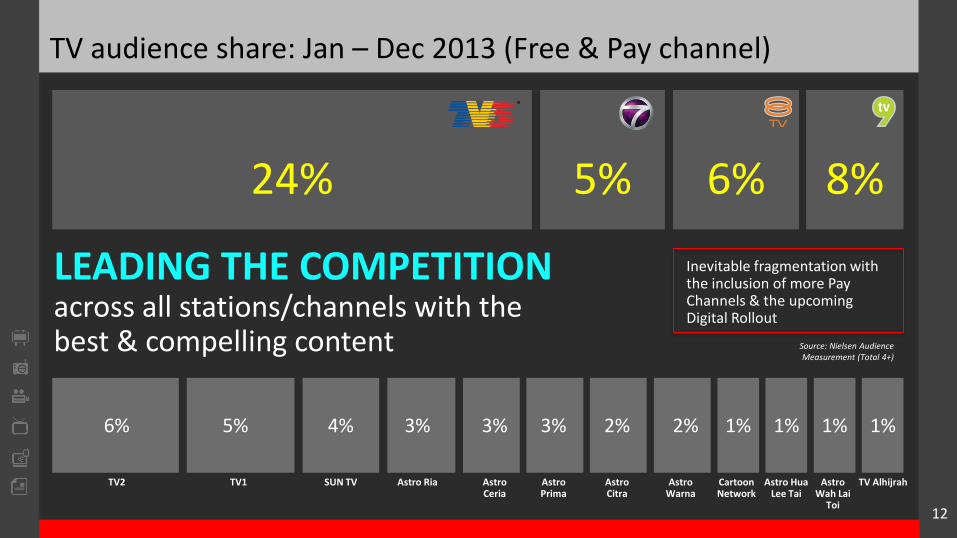

LEADING THE COMPETITIONacross all stations/channels with the best & compelling content

6% 5% 4% 3% 3% 3% 2% 2% 1% 1% 1% 1%

TV2 TV1 SUN TV Astro Ria AstroCeria

AstroPrima

AstroCitra

AstroWarna

CartoonNetwork

Astro HuaLee Tai

AstroWah Lai

Toi

TV Alhijrah

Inevitable fragmentation with the inclusion of more Pay Channels & the upcoming Digital Rollout

Source: Nielsen Audience Measurement (Total 4+)

8%6%5%24%

TV audience share: Jan – Dec 2013 (Free & Pay channel)

12

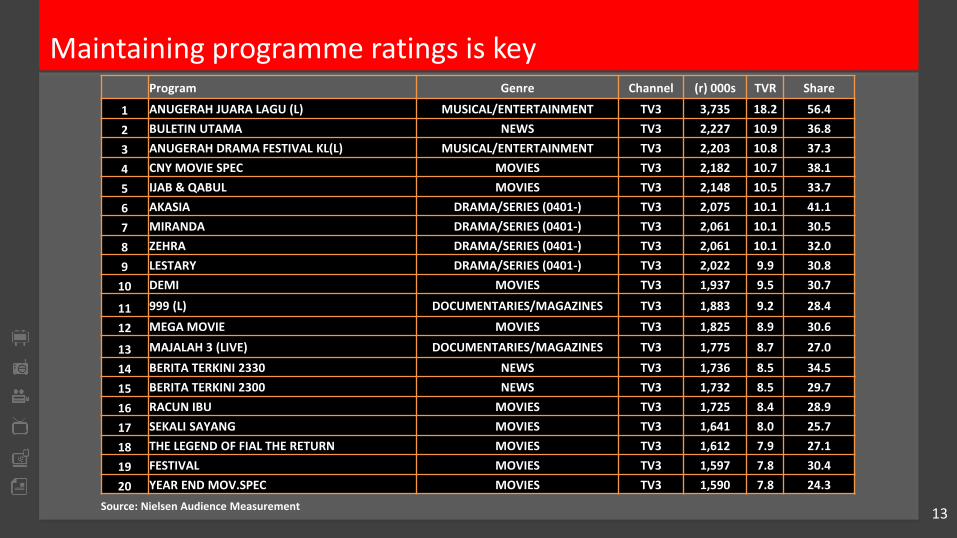

Program Genre Channel (r) 000s TVR Share

1 ANUGERAH JUARA LAGU (L) MUSICAL/ENTERTAINMENT TV3 3,735 18.2 56.4

2 BULETIN UTAMA NEWS TV3 2,227 10.9 36.8

3 ANUGERAH DRAMA FESTIVAL KL(L) MUSICAL/ENTERTAINMENT TV3 2,203 10.8 37.3

4 CNY MOVIE SPEC MOVIES TV3 2,182 10.7 38.1

5 IJAB & QABUL MOVIES TV3 2,148 10.5 33.7

6 AKASIA DRAMA/SERIES (0401-) TV3 2,075 10.1 41.1

7 MIRANDA DRAMA/SERIES (0401-) TV3 2,061 10.1 30.5

8 ZEHRA DRAMA/SERIES (0401-) TV3 2,061 10.1 32.0

9 LESTARY DRAMA/SERIES (0401-) TV3 2,022 9.9 30.8

10 DEMI MOVIES TV3 1,937 9.5 30.7

11 999 (L) DOCUMENTARIES/MAGAZINES TV3 1,883 9.2 28.4

12 MEGA MOVIE MOVIES TV3 1,825 8.9 30.6

13 MAJALAH 3 (LIVE) DOCUMENTARIES/MAGAZINES TV3 1,775 8.7 27.0

14 BERITA TERKINI 2330 NEWS TV3 1,736 8.5 34.5

15 BERITA TERKINI 2300 NEWS TV3 1,732 8.5 29.7

16 RACUN IBU MOVIES TV3 1,725 8.4 28.9

17 SEKALI SAYANG MOVIES TV3 1,641 8.0 25.7

18 THE LEGEND OF FIAL THE RETURN MOVIES TV3 1,612 7.9 27.1

19 FESTIVAL MOVIES TV3 1,597 7.8 30.4

20 YEAR END MOV.SPEC MOVIES TV3 1,590 7.8 24.3

Source: Nielsen Audience Measurement

Maintaining programme ratings is key

13

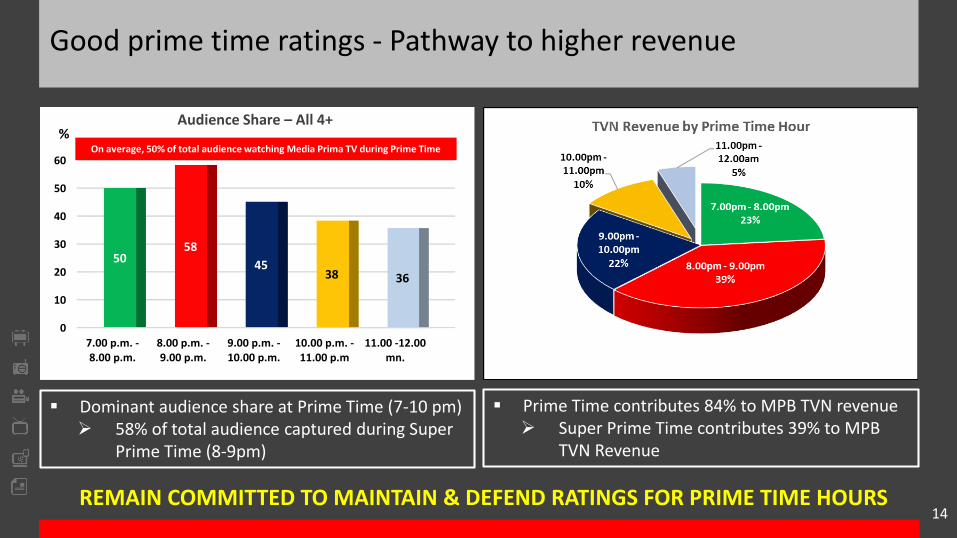

Good prime time ratings - Pathway to higher revenue

Dominant audience share at Prime Time (7-10 pm) 58% of total audience captured during Super

Prime Time (8-9pm)

REMAIN COMMITTED TO MAINTAIN & DEFEND RATINGS FOR PRIME TIME HOURS

0

10

20

30

40

50

60

7.00 p.m. -8.00 p.m.

8.00 p.m. -9.00 p.m.

9.00 p.m. -10.00 p.m.

10.00 p.m. -11.00 p.m

11.00 -12.00mn.

5058

4538 36

Audience Share – All 4+%

Prime Time contributes 84% to MPB TVN revenue Super Prime Time contributes 39% to MPB

TVN Revenue

On average, 50% of total audience watching Media Prima TV during Prime Time

14

SECTION 2.3: Print media

15

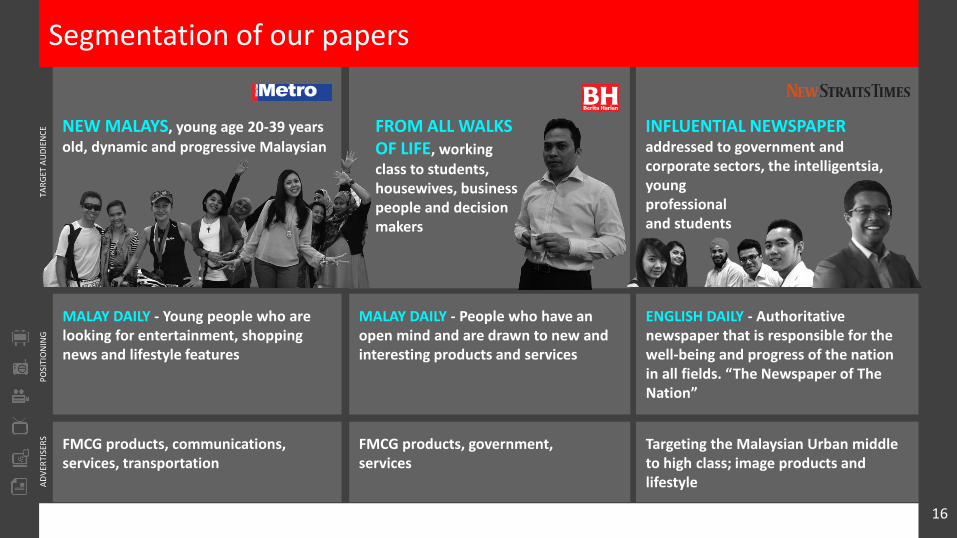

Segmentation of our papers

NEW MALAYS, young age 20-39 years old, dynamic and progressive Malaysian

MALAY DAILY - Young people who are looking for entertainment, shopping news and lifestyle features

FMCG products, communications, services, transportation

TAR

GET

AU

DIE

NC

EP

OSI

TIO

NIN

GA

DV

ERTI

SER

S

FROM ALL WALKS OF LIFE, working class to students, housewives, business people and decision makers

MALAY DAILY - People who have an open mind and are drawn to new and interesting products and services

FMCG products, government, services

INFLUENTIAL NEWSPAPER addressed to government and corporate sectors, the intelligentsia, young professional and students

ENGLISH DAILY - Authoritative newspaper that is responsible for the well-being and progress of the nation in all fields. “The Newspaper of The Nation”

Targeting the Malaysian Urban middle to high class; image products and lifestyle

16

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2009 2010 2011 2012 2013

RM

'00

0

English Malay Chinese Tamil

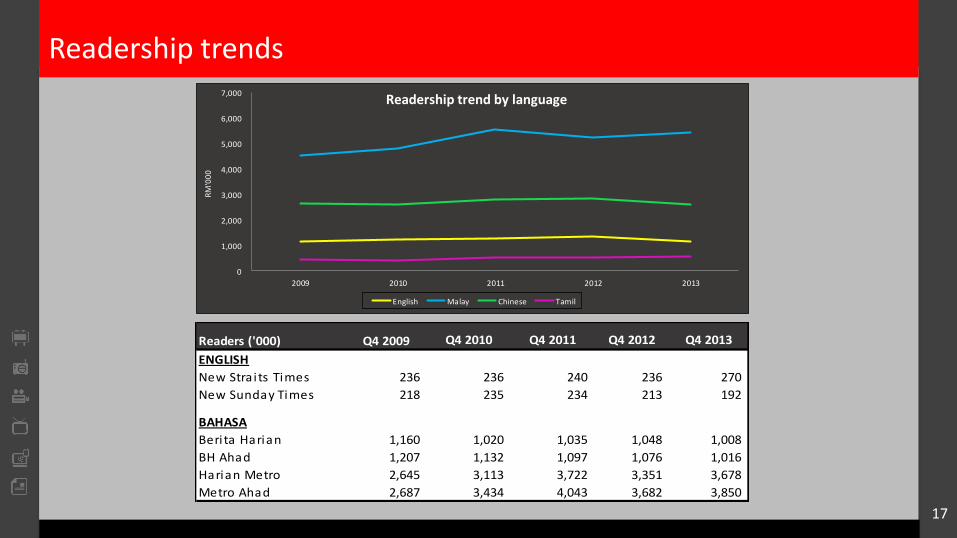

Readers ('000) Q4 2009 Q4 2010 Q4 2011 Q4 2012 Q4 2013

ENGLISH

New Stra i ts Times 236 236 240 236 270

New Sunday Times 218 235 234 213 192

BAHASA

Berita Harian 1,160 1,020 1,035 1,048 1,008

BH Ahad 1,207 1,132 1,097 1,076 1,016

Harian Metro 2,645 3,113 3,722 3,351 3,678

Metro Ahad 2,687 3,434 4,043 3,682 3,850

Readership trend by language

Readership trends

17

18

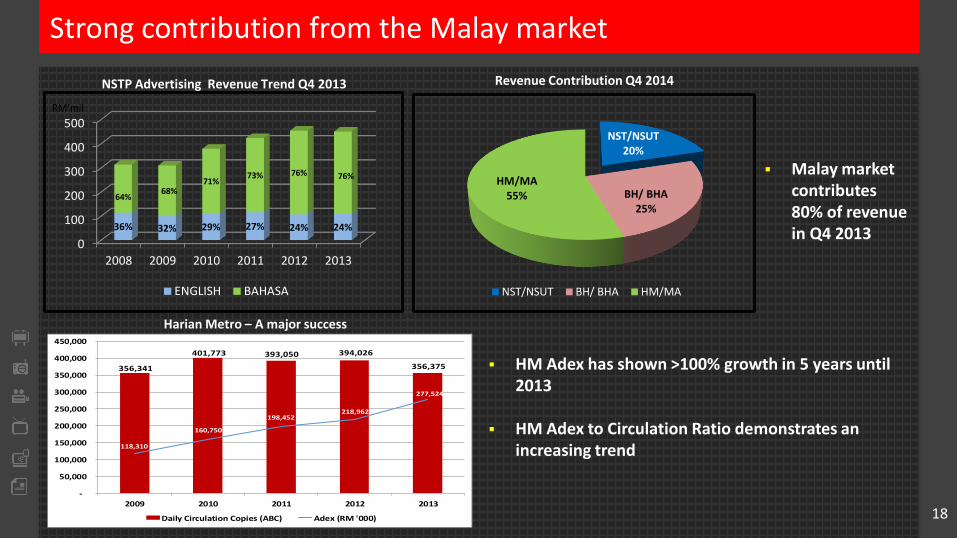

NST/NSUT20%

BH/ BHA25%

HM/MA55%

NST/NSUT BH/ BHA HM/MA

NSTP Advertising Revenue Trend Q4 2013 Revenue Contribution Q4 2014

0

100

200

300

400

500

2008 2009 2010 2011 2012 2013

36% 32% 29% 27% 24% 24%

64%68%

71%73% 76% 76%

ENGLISH BAHASA

356,341

401,773 393,050 394,026

356,375

118,310

160,750

198,452 218,962

277,524

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2009 2010 2011 2012 2013

Daily Circulation Copies (ABC) Adex (RM '000)

HM Adex has shown >100% growth in 5 years until 2013

HM Adex to Circulation Ratio demonstrates an increasing trend

Malay market contributes 80% of revenue in Q4 2013

Harian Metro – A major success

Strong contribution from the Malay market

18

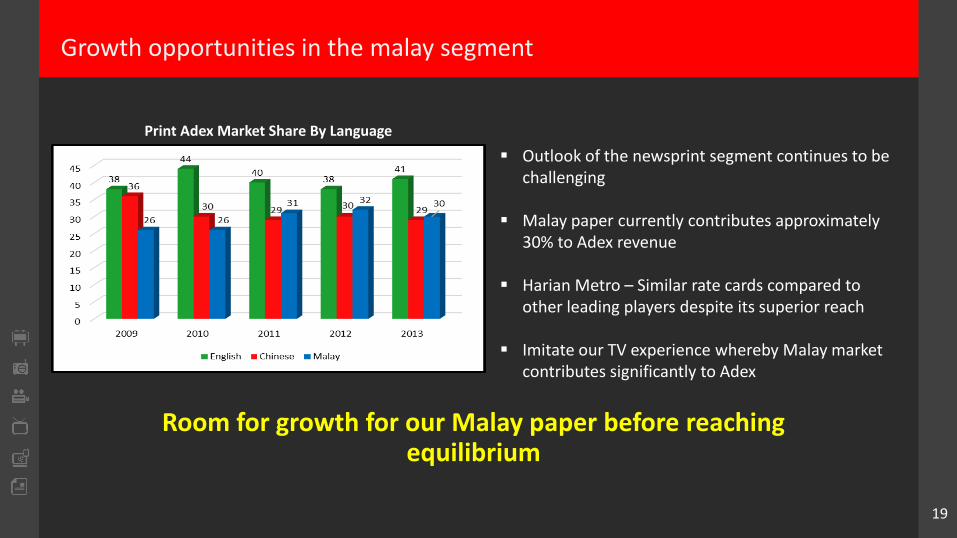

Growth opportunities in the malay segment

Outlook of the newsprint segment continues to be challenging

Malay paper currently contributes approximately 30% to Adex revenue

Harian Metro – Similar rate cards compared to other leading players despite its superior reach

Imitate our TV experience whereby Malay market contributes significantly to Adex

Room for growth for our Malay paper before reaching equilibrium

Print Adex Market Share By Language

19

THE SHARPER READThe only English daily that recorded growth in readership compared to 2012 (Source: Nielsen Media Index)

Focus on news, analysis, commentaries, op-eds, and lettersPage 1 with stronger visual elements 20

Daily pullouts

now combined into

BH AHAD

A NEW LOOK

21

More infographics

22

TASTE

5-DAYS AD CAMPAIGN

Selling creative solutions – 5D

TOUCH

SOUND

SMELL

SIGHT

23

SECTION 2.4: Radio networks

24

#Others - Inclusive of Media Prima Berhad, Alternate Records and Primeworks Studios

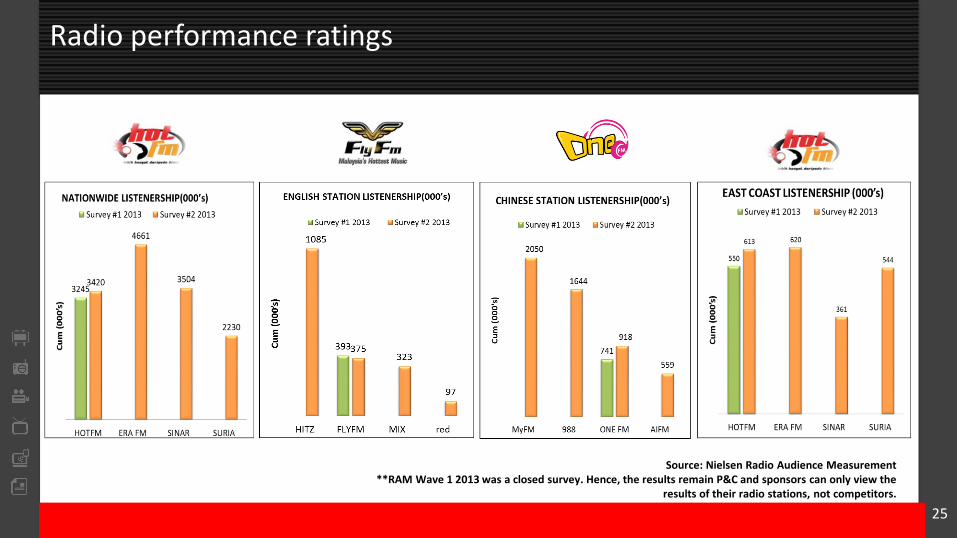

Radio performance ratings

Source: Nielsen Radio Audience Measurement**RAM Wave 1 2013 was a closed survey. Hence, the results remain P&C and sponsors can only view the

results of their radio stations, not competitors.

25

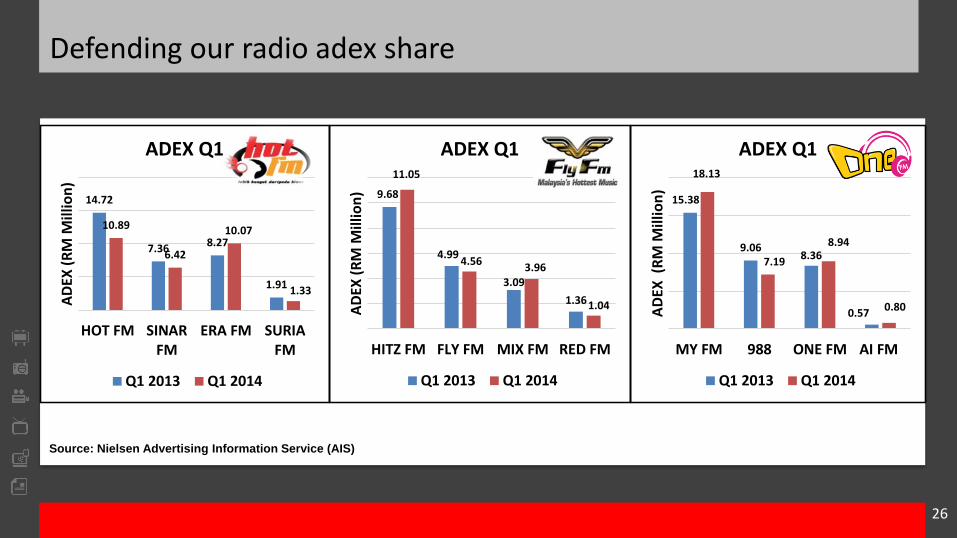

Defending our radio adex share

9.68

4.99

3.09

1.36

11.05

4.563.96

1.04

HITZ FM FLY FM MIX FM RED FMA

DEX

(R

M M

illio

n)

ADEX Q1

Q1 2013 Q1 2014

15.38

9.068.36

0.57

18.13

7.19

8.94

0.80

MY FM 988 ONE FM AI FM

AD

EX (

RM

Mill

ion

)

ADEX Q1

Q1 2013 Q1 2014

14.72

7.368.27

1.91

10.89

6.42

10.07

1.33

HOT FM SINARFM

ERA FM SURIAFM

AD

EX (

RM

Mill

ion

)

ADEX Q1

Q1 2013 Q1 2014

Source: Nielsen Advertising Information Service (AIS)

26

Largest online & social media presence in the country

2.4millionFANS

Source: Nielsen Audience Measurement (Total 4+)

1.1milionFOLLOWERS

67,000FOLLOWERS

Hot FM: 390,506

Fly FM: 142,581

One FM: 177,330

(no comparison as we are the only radio stations that have the official accounts)

FACEBOOK TWITTER INSTAGRAM

1. Hot FM 1,844,372 1,067,318 52,238

2. Era FM 855,523 165,339 40,314

3. Suria FM 244,711 68,909 4,519

4. Sinar FM 173,378 24,311 5,621

Facebook Twitter Instagram Weibo

1. One FM 439,924 6,777 6,701 10,008

2. My FM 357,014 6,760 6828 9,925

3. 988 157,783 2,516 895 9,173

FACEBOOK TWITTER INSTAGRAM

1. Hitz FM 769,361 202,839 12,447

2. Fly FM 169,696 93,385 8,132

3. Red FM 56,005 13,804 938

27

Regional radio: INVESTING FOR GROWTH

CLOSE TO 70% RADIO REACH

Source: Nielsen Radio Audience Measurement

• Hot FM Kelate & Hot FM T’ganu were launched in January 2012 to build new regional revenue

• Untapped Adex in the East Coast

• Can be catalyst for regionalization of stations

28

SECTION 2.4: Outdoor media

29

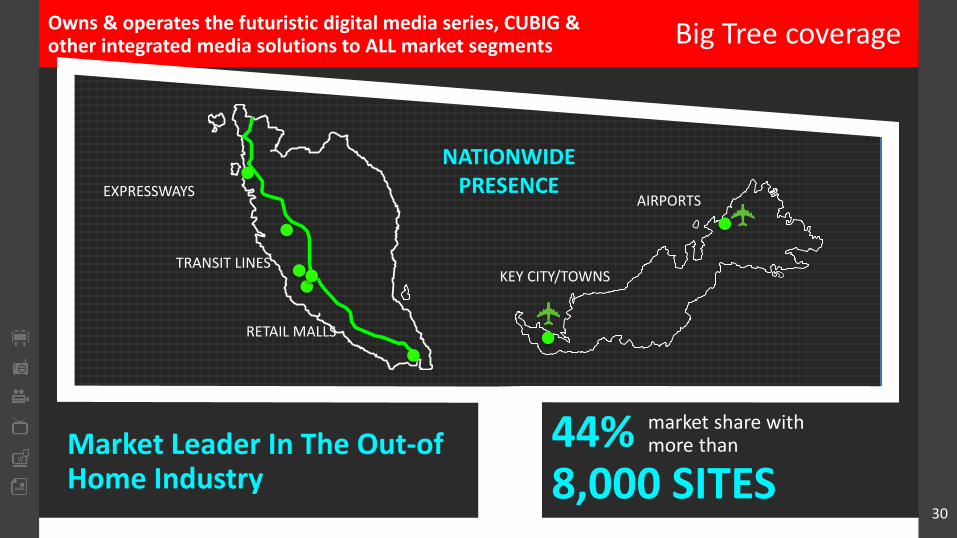

Big Tree coverage

NATIONWIDEPRESENCEEXPRESSWAYS

TRANSIT LINES

AIRPORTS

KEY CITY/TOWNS

RETAIL MALLS

Market Leader In The Out-of Home Industry

44% 8,000 SITES

market share with more than

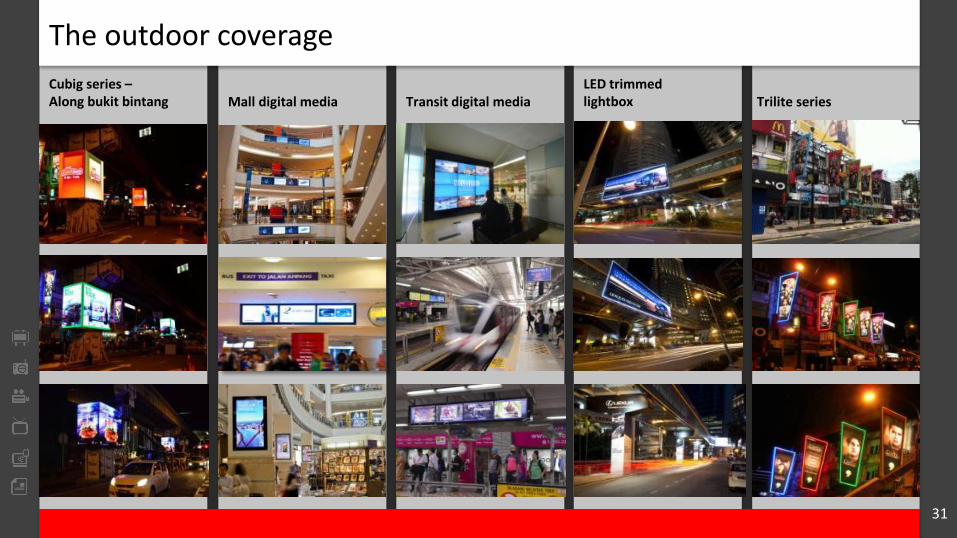

30

Owns & operates the futuristic digital media series, CUBIG & other integrated media solutions to ALL market segments

Cubig series –Along bukit bintang Mall digital media Transit digital media

LED trimmed lightbox Trilite series

The outdoor coverage

31

Creativity – Selling innovative solutions

32

Enhanced media formats – Distinct competitive edges

SECTION 2.4: Digital media

33

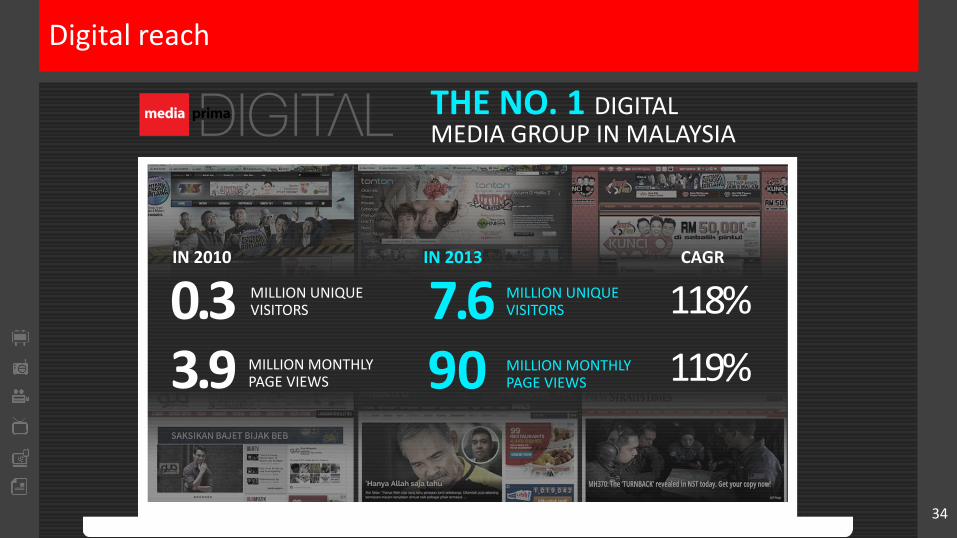

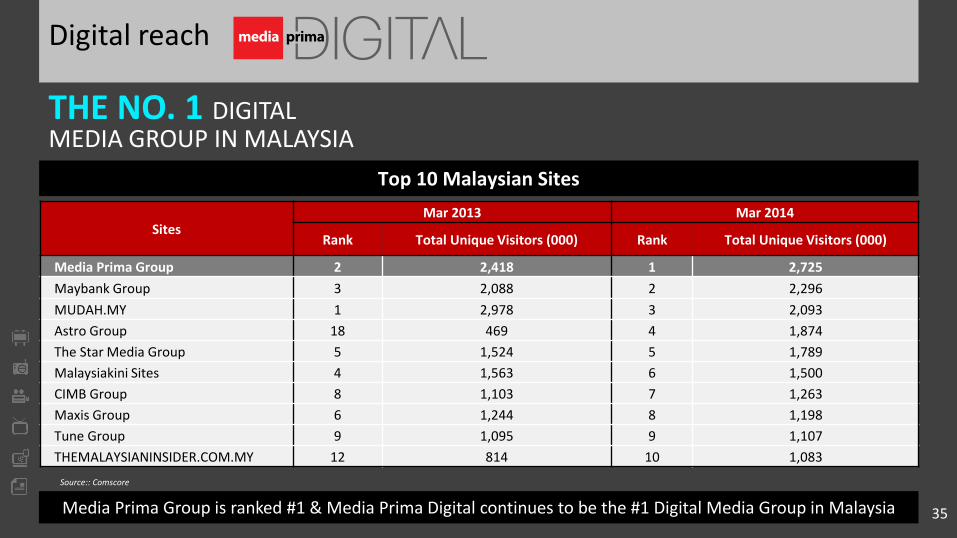

THE NO. 1 DIGITAL MEDIA GROUP IN MALAYSIA

7.6 MILLION UNIQUE VISITORS

90 MILLION MONTHLY PAGE VIEWS3.9 MILLION MONTHLY

PAGE VIEWS

IN 2010 IN 2013

MILLION UNIQUE VISITORS0.3 118%

CAGR

119%

34

Digital reach

Digital reach

THE NO. 1 DIGITAL MEDIA GROUP IN MALAYSIA

Top 10 Malaysian Sites

Media Prima Group is ranked #1 & Media Prima Digital continues to be the #1 Digital Media Group in Malaysia

Source: comScore Key Measures

SitesMar 2013 Mar 2014

Rank Total Unique Visitors (000) Rank Total Unique Visitors (000)

Media Prima Group 2 2,418 1 2,725

Maybank Group 3 2,088 2 2,296

MUDAH.MY 1 2,978 3 2,093

Astro Group 18 469 4 1,874

The Star Media Group 5 1,524 5 1,789

Malaysiakini Sites 4 1,563 6 1,500

CIMB Group 8 1,103 7 1,263

Maxis Group 6 1,244 8 1,198

Tune Group 9 1,095 9 1,107

THEMALAYSIANINSIDER.COM.MY 12 814 10 1,083

Source:: Comscore

35

Tonton’s growth

201320122011

PAGE VIEWS

UNIQUE VISITORS

VIDEO VIEWS22.8 29.0

48.0

17.2

25.7

53.2

73.9

119.8

245.2

28%65%

50%107%

62%

105%

TONTON’S 2011 TO 2013 GROWTH CHART

Source:: Omniture Site Catalyst

mill

ion

REGISTERED USERSm

illio

n

1.92.6

3.5

35%

37%

mill

ion

mill

ion

36

REVENUE

mill

ion 18.5

25.1

33.8

35%

36%

201320122011

MEDIA PRIMA DIGITAL’S 2011 TO 2013 GROWTH CHART

TONTON PREMIUM

48 HOURS BEFORE TV

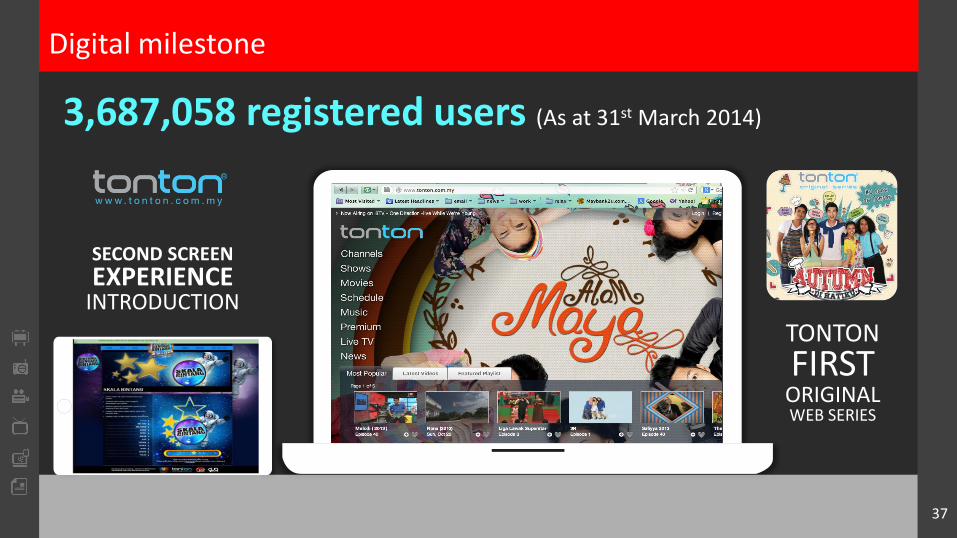

SECOND SCREEN EXPERIENCE

INTRODUCTION

TONTON

FIRST ORIGINALWEB SERIES

3,687,058 registered users (As at 31st March 2014)

Digital milestone

37

SECTION 2.5: Content creation

38

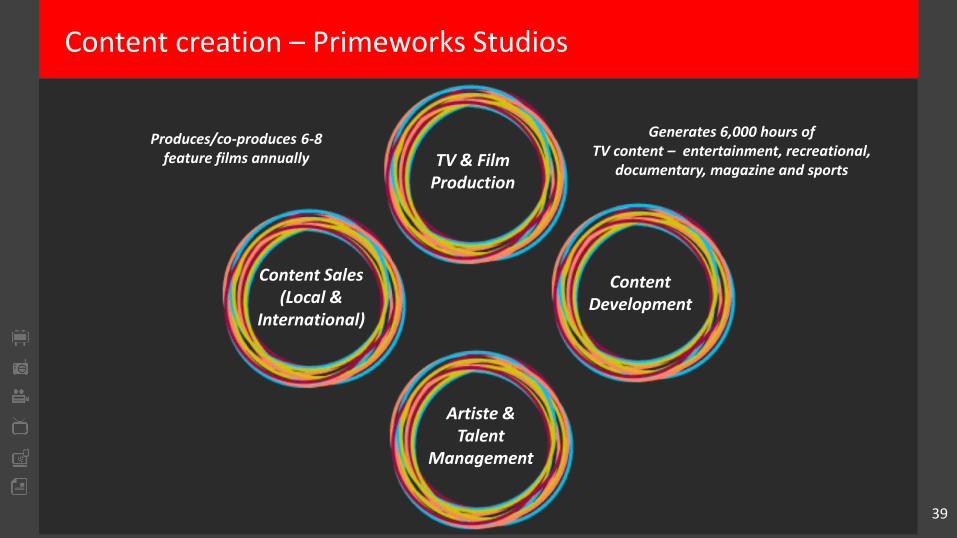

Content creation – Primeworks Studios

39

TV & Film Production

Content Development

Artiste & Talent

Management

Content Sales (Local &

International)

Produces/co-produces 6-8 feature films annually

Generates 6,000 hours of TV content – entertainment, recreational,

documentary, magazine and sports

40

41

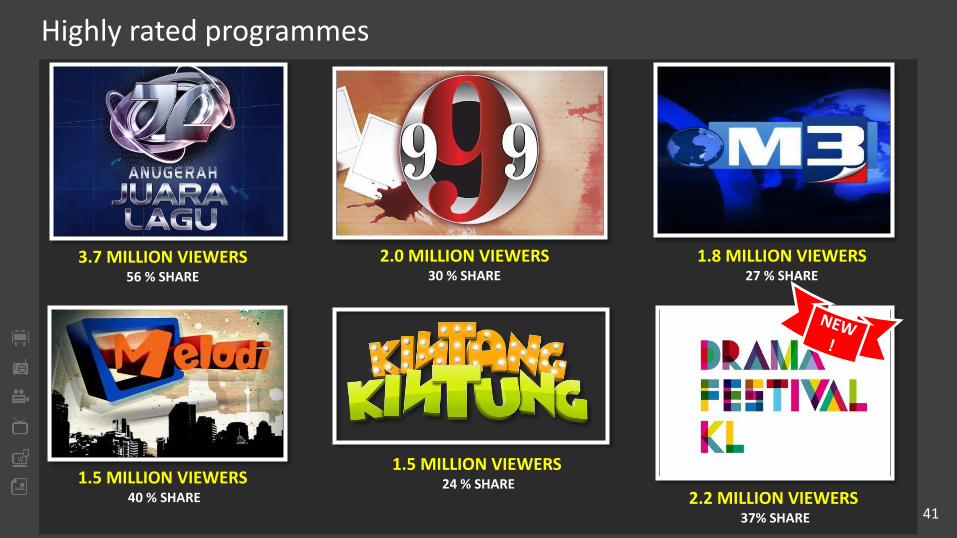

Highly rated programmes

1.5 MILLION VIEWERS24 % SHARE

2.0 MILLION VIEWERS30 % SHARE

3.7 MILLION VIEWERS56 % SHARE

1.8 MILLION VIEWERS27 % SHARE

1.5 MILLION VIEWERS40 % SHARE 2.2 MILLION VIEWERS

37% SHARE

42

AWARD WINNING MOVIES

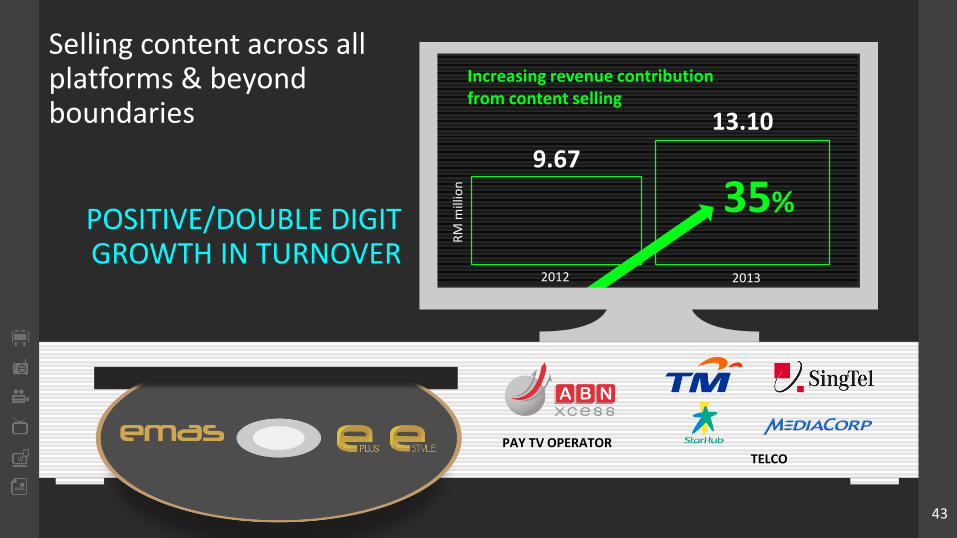

Selling content across all platforms & beyond boundaries

PAY TV OPERATORSelling content to

TELCO

POSITIVE/DOUBLE DIGIT GROWTH IN TURNOVER

13.10

35%

9.67

RM

mill

ion

2012 2013

Increasing revenue contribution from content selling

43

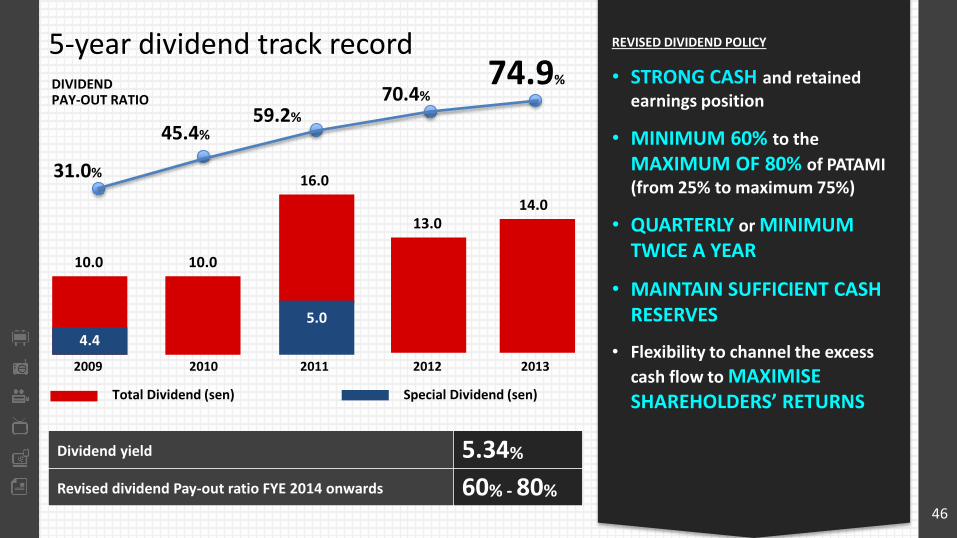

SECTION 3: Dividend

44

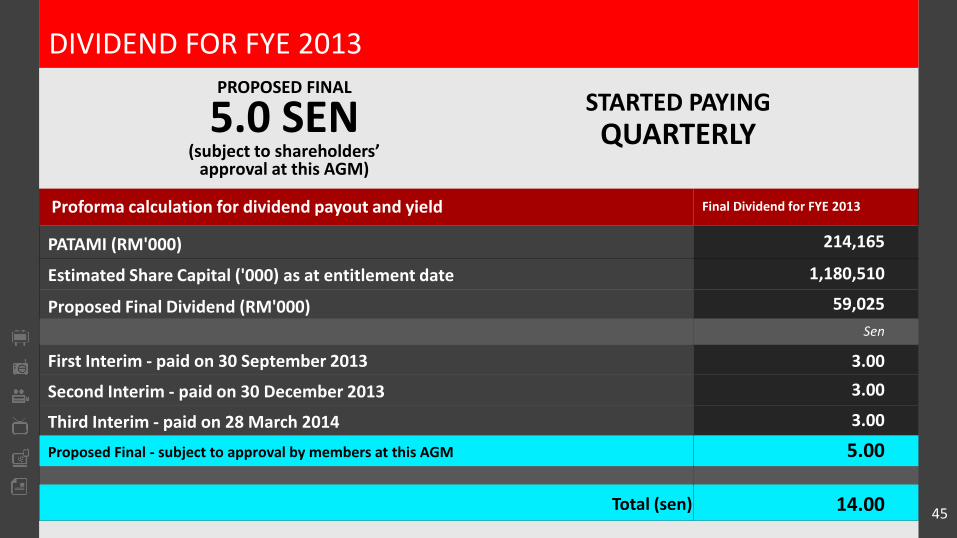

STARTED PAYING

QUARTERLY

Proforma calculation for dividend payout and yield Final Dividend for FYE 2013

PATAMI (RM'000) 214,165

Estimated Share Capital ('000) as at entitlement date 1,180,510

Proposed Final Dividend (RM'000) 59,025

Sen

First Interim - paid on 30 September 2013 3.00

Second Interim - paid on 30 December 2013 3.00

Third Interim - paid on 28 March 2014 3.00

Proposed Final - subject to approval by members at this AGM 5.00

Total (sen) 14.00

DIVIDEND FOR FYE 2013PROPOSED FINAL

5.0 SEN (subject to shareholders’

approval at this AGM)

45

REVISED DIVIDEND POLICY

• STRONG CASH and retained earnings position

• MINIMUM 60% to the

MAXIMUM OF 80% of PATAMI (from 25% to maximum 75%)

• QUARTERLY or MINIMUM TWICE A YEAR

• MAINTAIN SUFFICIENT CASH RESERVES

• Flexibility to channel the excess

cash flow to MAXIMISE SHAREHOLDERS’ RETURNS

10.0 10.0

16.0

13.014.0

2009 2010 2011 2012 2013

Total Dividend (sen) Special Dividend (sen)

DIVIDEND PAY-OUT RATIO

31.0%

45.4%59.2%

70.4%74.9%

5-year dividend track record

Dividend yield 5.34%

Revised dividend Pay-out ratio FYE 2014 onwards 60% - 80%

4.4

5.0

46

SECTION 4: Corporate Governance

47

MPB BOARD OF DIRECTORS AS AT

31 DECEMBER 2013

Commitment towards good corporate governance

70%

20%

10%

Non-Independent Non-Executive

Executive

Independent Non-Executive

The Board has ten (10) members of which two (2) are Executive Directors and eight (8) are Non-Executive Directors.

The Independent Non-Executive Directors make up 70% of the Board membership.

Size of the Board is optimum given the scope and size of the Group.

Size of the Board is sufficient to provide for effective decision-making with a substantial degree of independence from the Management.

All of the Group’s operating companies have separate and independent boards.

48

SECTION 5: Outlook & Media Convergence

49

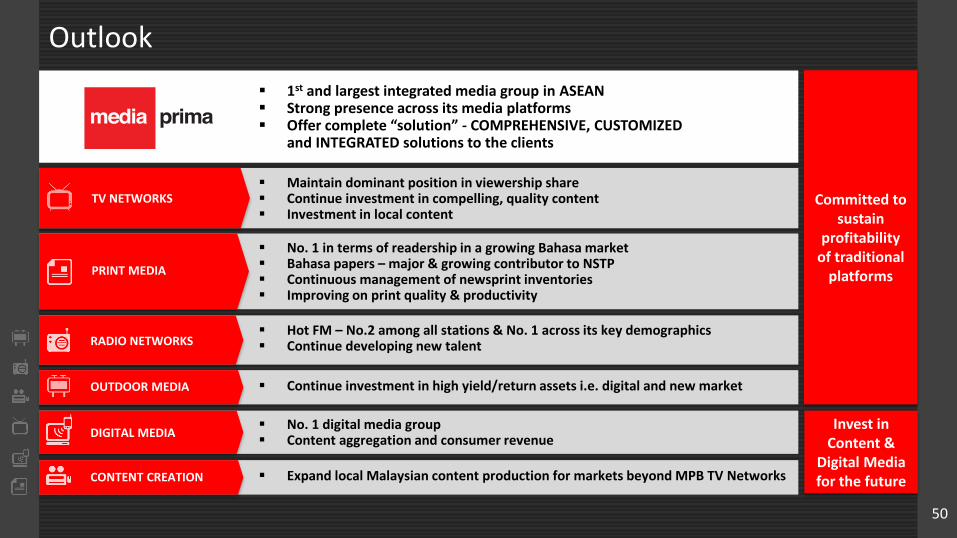

Outlook

TV NETWORKS

PRINT MEDIA

RADIO NETWORKS

OUTDOOR MEDIA

DIGITAL MEDIA

CONTENT CREATION

Maintain dominant position in viewership share Continue investment in compelling, quality content Investment in local content

1st and largest integrated media group in ASEAN Strong presence across its media platforms Offer complete “solution” - COMPREHENSIVE, CUSTOMIZED

and INTEGRATED solutions to the clients

No. 1 in terms of readership in a growing Bahasa market Bahasa papers – major & growing contributor to NSTP Continuous management of newsprint inventories Improving on print quality & productivity

Hot FM – No.2 among all stations & No. 1 across its key demographics Continue developing new talent

Continue investment in high yield/return assets i.e. digital and new market

No. 1 digital media group Content aggregation and consumer revenue

Expand local Malaysian content production for markets beyond MPB TV Networks

50

Committed to sustain

profitability of traditional

platforms

Invest in Content &

Digital Media for the future

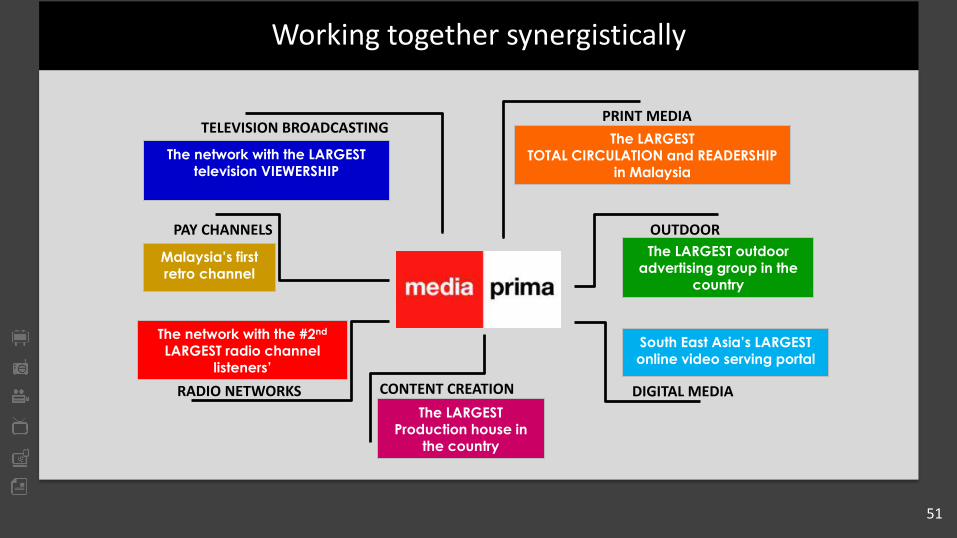

Working together synergistically

TELEVISION BROADCASTING

RADIO NETWORKS

PRINT MEDIA

OUTDOOR

DIGITAL MEDIA

PAY CHANNELS

CONTENT CREATION

The network with the LARGEST television VIEWERSHIP

The LARGEST TOTAL CIRCULATION and READERSHIP

in Malaysia

The LARGEST Production house in

the country

South East Asia’s LARGEST online video serving portal

The LARGEST outdoor advertising group in the

country

The network with the #2nd

LARGEST radio channel listeners’

Malaysia’s first retro channel

51

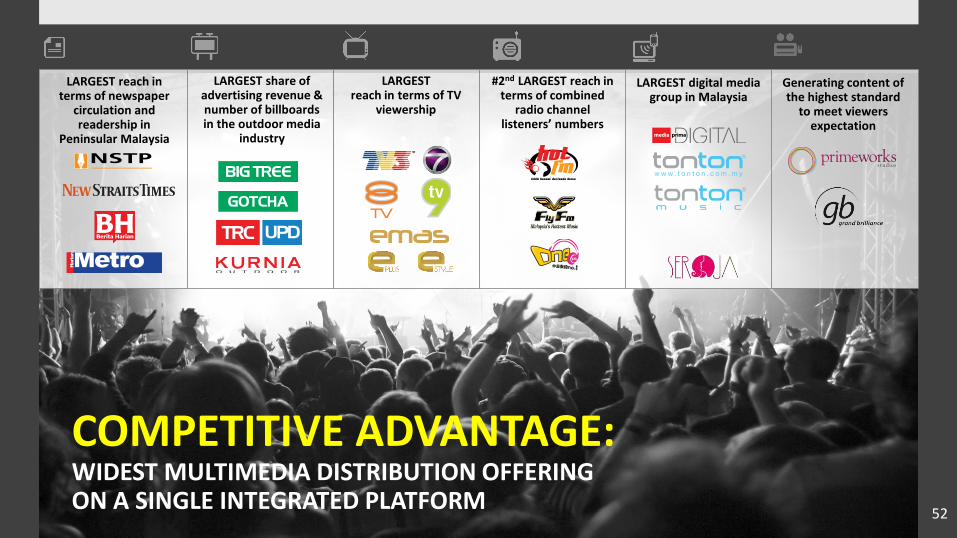

COMPETITIVE ADVANTAGE:WIDEST MULTIMEDIA DISTRIBUTION OFFERING ON A SINGLE INTEGRATED PLATFORM

LARGEST share of advertising revenue & number of billboards in the outdoor media

industry

LARGEST reach in terms of TV

viewership

#2nd LARGEST reach in terms of combined

radio channel listeners’ numbers

LARGEST reach in terms of newspaper

circulation and readership in

Peninsular Malaysia

Generating content of the highest standard

to meet viewers expectation

LARGEST digital media group in Malaysia

52

53

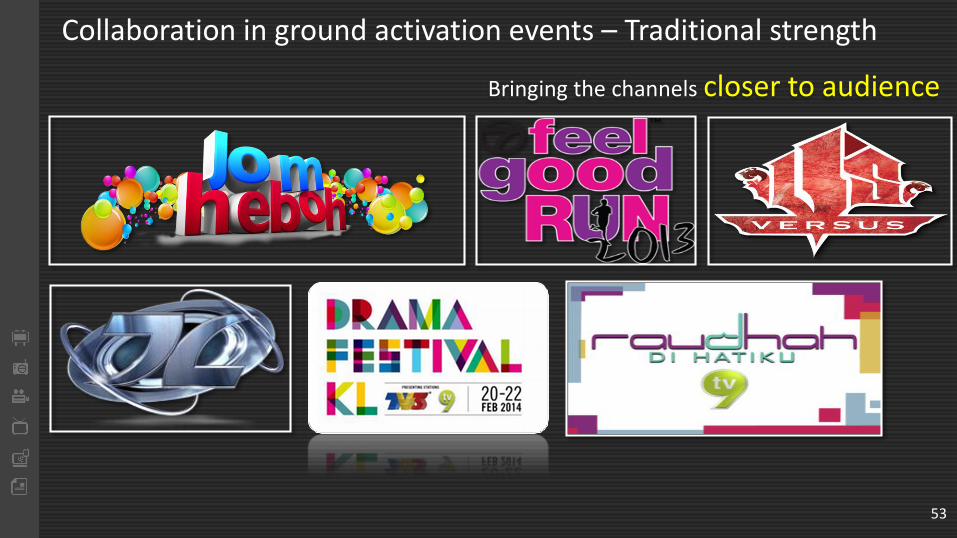

Collaboration in ground activation events – Traditional strength

Bringing the channels closer to audience

54

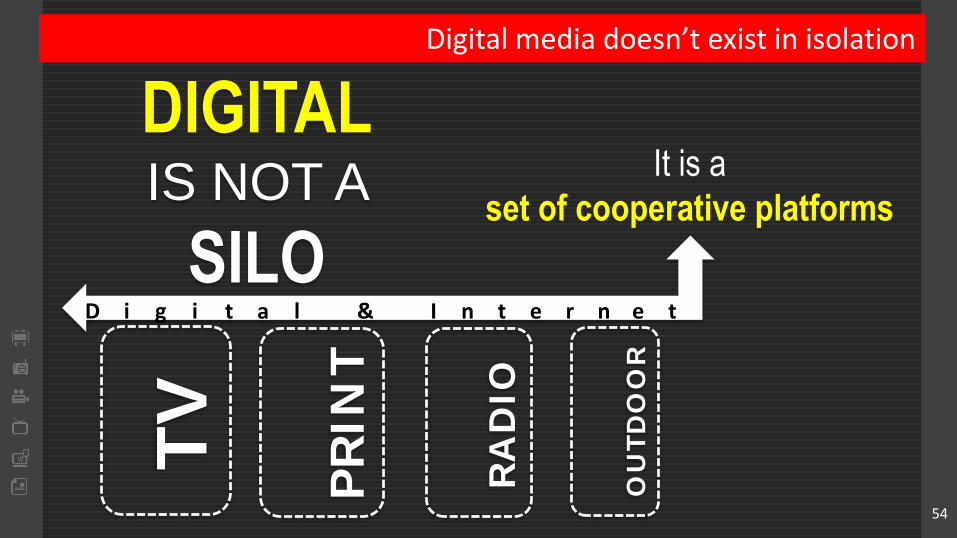

DIGITALIS NOT A

SILOT

V

PR

INT

RA

DIO

OU

TD

OO

R

It is a

set of cooperative platforms

D i g i t a l & I n t e r n e t

Digital media doesn’t exist in isolation

Pakatan accepts GE13 results, let’s talk unity “immediately”Why I’ll be

voting in the coming GE13

Stricter rules imposed on PKR election candidates

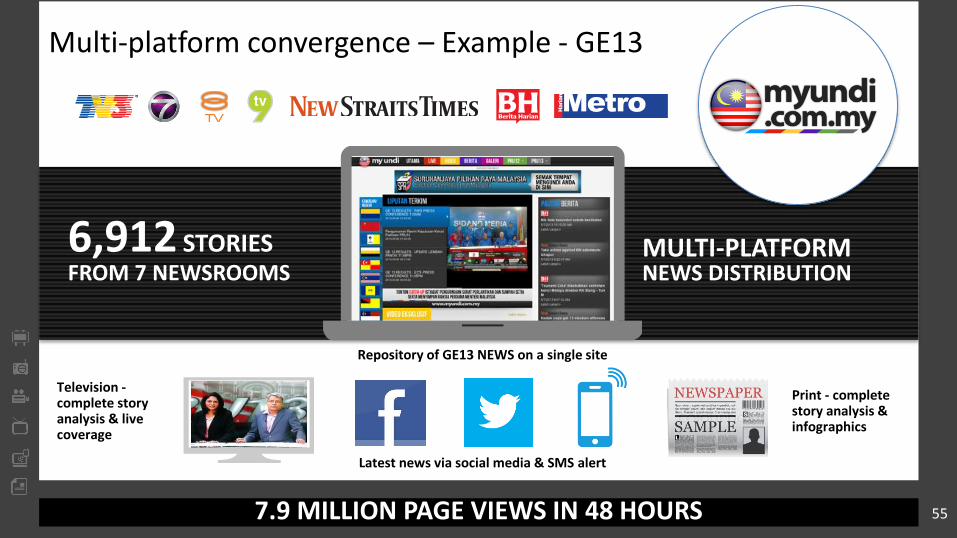

Multi-platform convergence – Example - GE13

6,912 STORIESFROM 7 NEWSROOMS

MULTI-PLATFORMNEWS DISTRIBUTION

Television -complete story analysis & live coverage

Latest news via social media & SMS alert

7.9 MILLION PAGE VIEWS IN 48 HOURS

Print - complete story analysis & infographics

Repository of GE13 NEWS on a single site

55

56

Cross media collaboration – Project Metro

PROJECTMETRO

Reality TV showIn search of a new face in the entertainment industry

Successfully broadcasted over 8 episodes

Cross media collaboration

<

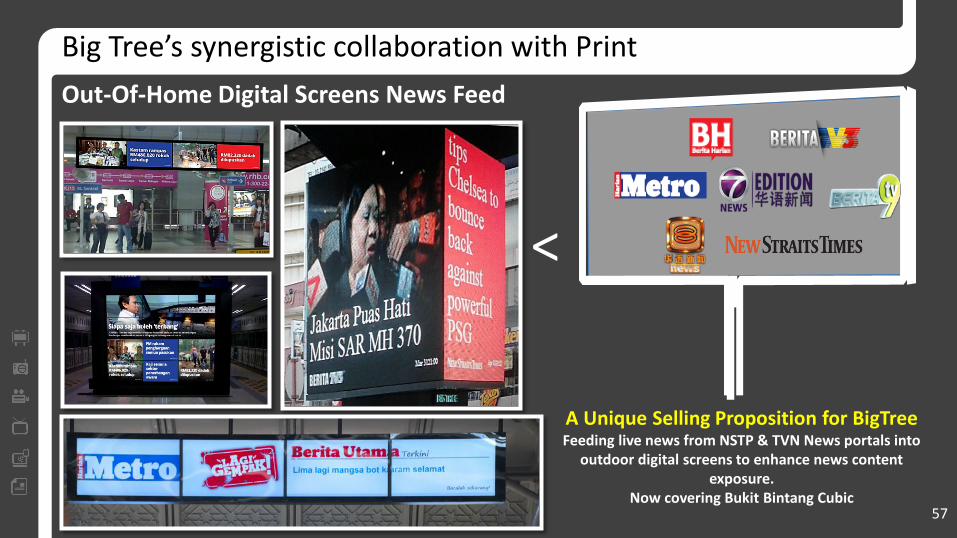

Out-Of-Home Digital Screens News Feed

Big Tree’s synergistic collaboration with Print

57

A Unique Selling Proposition for BigTreeFeeding live news from NSTP & TVN News portals into

outdoor digital screens to enhance news content exposure.

Now covering Bukit Bintang Cubic

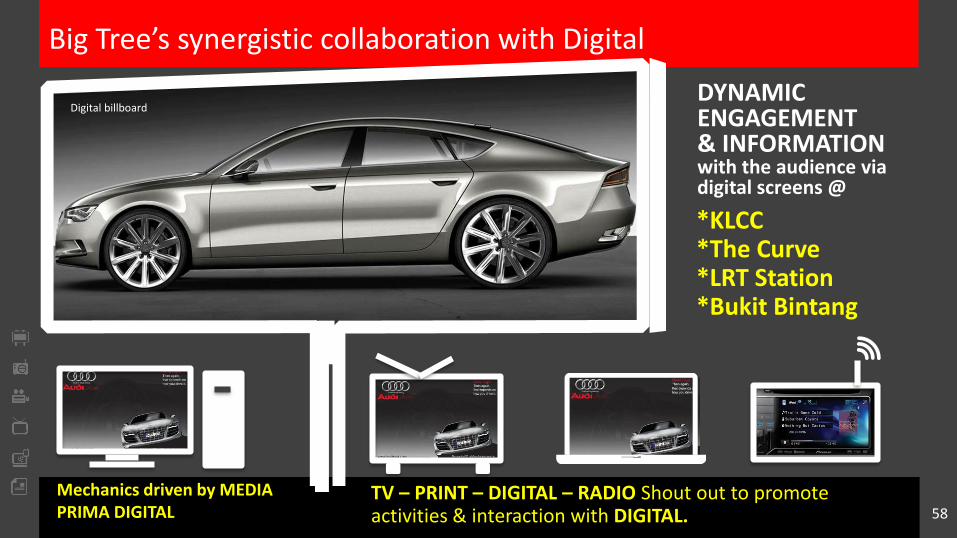

Big Tree’s synergistic collaboration with Digital

TV – PRINT – DIGITAL – RADIO Shout out to promote activities & interaction with DIGITAL.

Digital billboardDYNAMIC ENGAGEMENT& INFORMATION with the audience via digital screens @

*KLCC*The Curve *LRT Station*Bukit Bintang

Mechanics driven by MEDIA PRIMA DIGITAL 58

Relevant content to local market

Relationship with local music label

MUSICAL EVENT

Experience in producing iconic music events.

ACCESS TO LOCAL & INDIE

CONTENTMULTIPLATFORM

REACHAccess to Malaysia’s leading TV, Radio & Print brand – AJL, ABPBH

Access to celebrity/personality

Access to popular program HotFM am crew, AJL, MuzikMuzik & more

EXCLUSIVE ACCESS

1st MUSIC PORTAL IN THE COUNTRY TO OFFER A FREE MOBILE STREAMING SERVICE.

1st MUSIC PORTAL TO HAVE A FULLY INTEGRATED DIGITAL MUSIC SERVICE

OPPORTUNITY TO EXPAND ADVERTISING AVENUES

59

Brand extensions for Hot FM, Fly FM, & one FM

Radio’s synergistic collaboration with Digital

117,804Page views

in 7 days

46,939Page views within

48 hrs of AJL

Note: This presentation may contain forward-looking statements which are based on MPB's current expectations, forecasts and assumptions based on management's good faithexpectations and belief concerning future developments. In some cases forward-looking statements may be identified by forward-looking words like “would”, “intend”, “hope”,“will”, “may”, “should”, “expect”, “anticipate”, “believe”, “estimate”, “predict”, “continue”, or similar words. Forward-looking statements involve risks and uncertainties whichcould cause actual outcomes and results to differ materially from MPB's expectations, forecasts and assumptions. We caution that these forward-looking statements are notstatements of historical facts and are subject to risks and uncertainties not in the control of MPB, including, without limitation, economic, competitive, governmental, regulatory,technological and other factors that may affect MPB's operations. Unless otherwise required by law, MPB disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events, or otherwise. Although we believe the expectations reflected in forward-looking statements arereasonable we cannot guarantee future results, levels of activity, performance or achievements.

THANK YOU

For more information, visitwww.mediaprima.com.my

orwww.mediaprima.com.my/investorcenter/feedbackcomments

for inquiries, suggestions & comments

60