Embed Size (px)

Citation preview

Applied Portfolio Management Analysts: Pascal Laucht, David-John Tiemens

Report Date: 5/6/2013

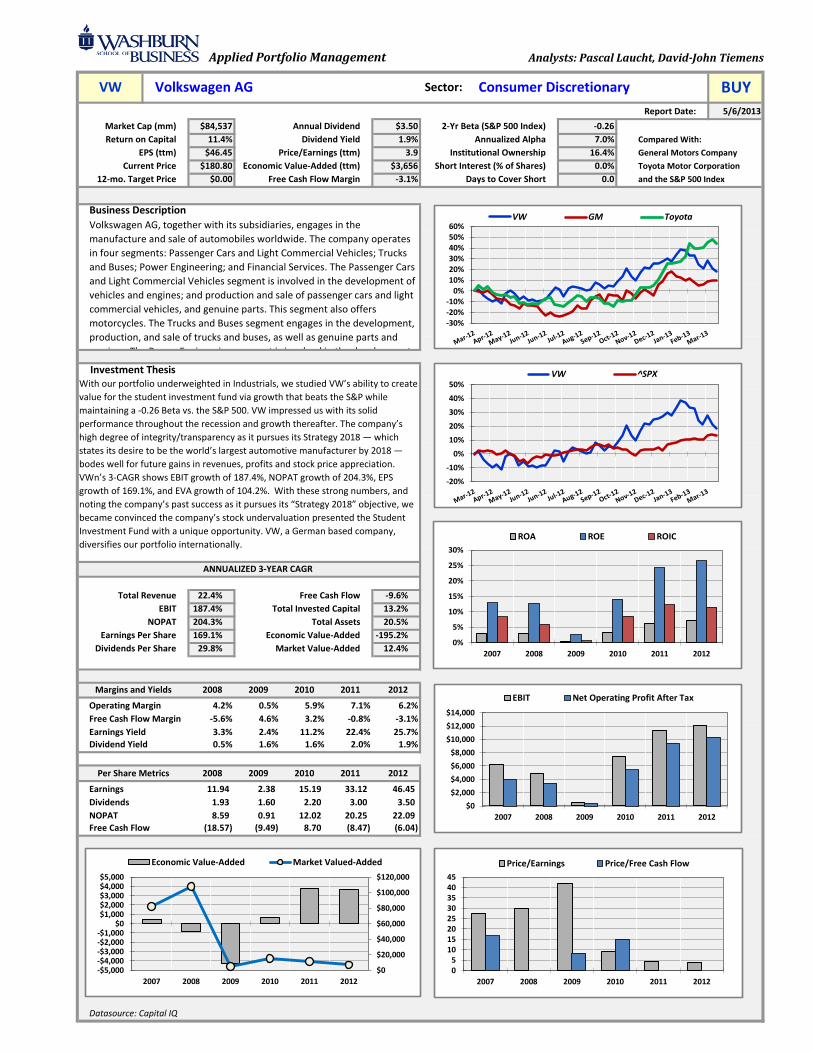

Market Cap (mm) $84,537 Annual Dividend $3.50 2-Yr Beta (S&P 500 Index) -0.26

Return on Capital 11.4% Dividend Yield 1.9% Annualized Alpha 7.0% Compared With:

EPS (ttm) $46.45 Price/Earnings (ttm) 3.9 Institutional Ownership 16.4% General Motors Company

Current Price $180.80 Economic Value-Added (ttm) $3,656 Short Interest (% of Shares) 0.0% Toyota Motor Corporation

12-mo. Target Price $0.00 Free Cash Flow Margin -3.1% Days to Cover Short 0.0 and the S&P 500 Index

Business Description

Total Revenue 22.4% Free Cash Flow -9.6%

EBIT 187.4% Total Invested Capital 13.2%

NOPAT 204.3% Total Assets 20.5%

Earnings Per Share 169.1% Economic Value-Added -195.2%

Dividends Per Share 29.8% Market Value-Added 12.4%

2008 2009 2010 2011 2012

4.2% 0.5% 5.9% 7.1% 6.2%

-5.6% 4.6% 3.2% -0.8% -3.1%

3.3% 2.4% 11.2% 22.4% 25.7%

0.5% 1.6% 1.6% 2.0% 1.9%

2008 2009 2010 2011 2012

11.94 2.38 15.19 33.12 46.45

1.93 1.60 2.20 3.00 3.50

8.59 0.91 12.02 20.25 22.09

(18.57) (9.49) 8.70 (8.47) (6.04)

Datasource: Capital IQ

Volkswagen AG Sector: Consumer Discretionary BUYVW

Volkswagen AG, together with its subsidiaries, engages in the

manufacture and sale of automobiles worldwide. The company operates

in four segments: Passenger Cars and Light Commercial Vehicles; Trucks

and Buses; Power Engineering; and Financial Services. The Passenger Cars

and Light Commercial Vehicles segment is involved in the development of

vehicles and engines; and production and sale of passenger cars and light

commercial vehicles, and genuine parts. This segment also offers

motorcycles. The Trucks and Buses segment engages in the development,

production, and sale of trucks and buses, as well as genuine parts and

services. The Power Engineering segment is involved in the development

Investment Thesis

ANNUALIZED 3-YEAR CAGR

With our portfolio underweighted in Industrials, we studied VW’s ability to create

value for the student investment fund via growth that beats the S&P while

maintaining a -0.26 Beta vs. the S&P 500. VW impressed us with its solid

performance throughout the recession and growth thereafter. The company’s

high degree of integrity/transparency as it pursues its Strategy 2018 — which

states its desire to be the world’s largest automotive manufacturer by 2018 —

bodes well for future gains in revenues, profits and stock price appreciation.

VWn’s 3-CAGR shows EBIT growth of 187.4%, NOPAT growth of 204.3%, EPS

growth of 169.1%, and EVA growth of 104.2%. With these strong numbers, and

noting the company’s past success as it pursues its “Strategy 2018” objective, we

became convinced the company’s stock undervaluation presented the Student

Investment Fund with a unique opportunity. VW, a German based company,

diversifies our portfolio internationally.

Margins and Yields

Operating Margin

Per Share Metrics

Earnings

NOPAT

Free Cash Flow

Dividends

Free Cash Flow Margin

Earnings Yield

Dividend Yield

-20%

-10%

0%

10%

20%

30%

40%

50%VW ^SPX

-30%-20%-10%

0%10%20%30%40%50%60%

VW GM Toyota

05

1015202530354045

2007 2008 2009 2010 2011 2012

Price/Earnings Price/Free Cash Flow

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2007 2008 2009 2010 2011 2012

EBIT Net Operating Profit After Tax

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

-$5,000-$4,000-$3,000-$2,000-$1,000

$0$1,000$2,000$3,000$4,000$5,000

2007 2008 2009 2010 2011 2012

Economic Value-Added Market Valued-Added

0%

5%

10%

15%

20%

25%

30%

2007 2008 2009 2010 2011 2012

ROA ROE ROIC

Please note that the company analyzed in this report is accurately named “The Volkswagen

Group.” However, the company is often described as, and/or is simply labeled “Volkswagen,”

“VW,” or “The Group.” These abbreviations for “The Volkswagen Group” will henceforth be

used interchangeably to describe the company.

Investment Thesis:

With our portfolio underweighted in Industrials, as analysts previously studying the automotive

industry, we became enticed as we studied VW’s ability to create value for the student

investment fund via growth that beats the S&P while maintaining a -0.26 Beta vs. the S&P 500

Looking deeper at the major players in the automotive industry, Volkswagen impressed us with

its solid performance throughout the recession and growth thereafter

The company’s high degree of integrity/transparency as it pursues its Strategy 2018 — which

states its desire to be the world’s largest automotive manufacturer by 2018 — bodes well for

future gains in revenues, profits and stock price appreciation

Volkswagen’s 3 year-CAGR shows EBIT growth of 187.4%, NOPAT growth of 204.3%, EPS growth

of 169.1%, and EVA growth of 104.2%. With these strong numbers, and noting the company’s

past success as it pursues its “Strategy 2018” objective, we became convinced the company’s

stock undervaluation presented the Student Investment Fund with a unique opportunity

Volkswagen, a German based company, diversifies our portfolio internationally

Highlights:

VW has a low Beta of -0.26, strong EVA growth of 104.2%, and a low P/E of 3.09

Calculating Intrinsic Value using conservative assumptions, we find that the company is

significantly undervalued by as much as 43.6% in 2012

The company is committed to growth and value creation, having publically instituted its “2018

Strategy,” which dictates the company to have unit sales of greater than 10 million and

operating margins of 8%. To date VW is manufacturing 9.2 million units and has a operating

margin slightly higher than 6%, so they remain on pace to meet all of the 2018 Strategy goals

VW’s ability to move into growth markets when opportunities arise (Asia in particular) even

during a recession, and the company's ability to maintain stable profit margins, have steadily

improved VW’s position in the market

Macroeconomic Analysis of the Automotive Industry:

The Automobile industry is slowly pulling itself out of the past recession, although overall industry

growth remains sluggish. The future of the industry is forecasted to grow at a slow yet stable pace.

Generally speaking, the automotive industry is cyclical, and though we are forecasting a relatively slow

recovery, we expect it to not only reach pre-recession levels, but see further growth into the future. It is

important to note however, that Volkswagen has already grown past its pre-recession numbers.

More importantly to us with respect to VW, we note the company has not only seen strong post-

recession growth as it implements its Strategy 2018 directive (3 year revenue growth rate of 22%), it has

taken market share from those other automotive companies that have had to see considerable

contraction in light of the recessions negative impacts on those companies.

International Diversification:

VW is a German based company that has traditionally had a large presence in the Euro-Zone (which for

our purposes includes Russia). With the Euro-Zone’s macroeconomic woes for the past six years (which

include its automotive industry), many investors have been wary of the stock which has been reflected

in the company’s low P/E ratio and its low MVA.

However, the “story that is Volkswagen,” as already stated, is how the company has continued to grow

and generate profits in spite of this reality. This has not only transpired due to strong industry

fundamentals, much of this also comes as the end of the company’s incredible ability to position itself in

growth markets while trimming those segments with slow growth. This transformation of their revenue

diversification is displayed by the below figures showing The Group's portfolio movement outside of the

European market and into growth markets such as Asia and Oceana.

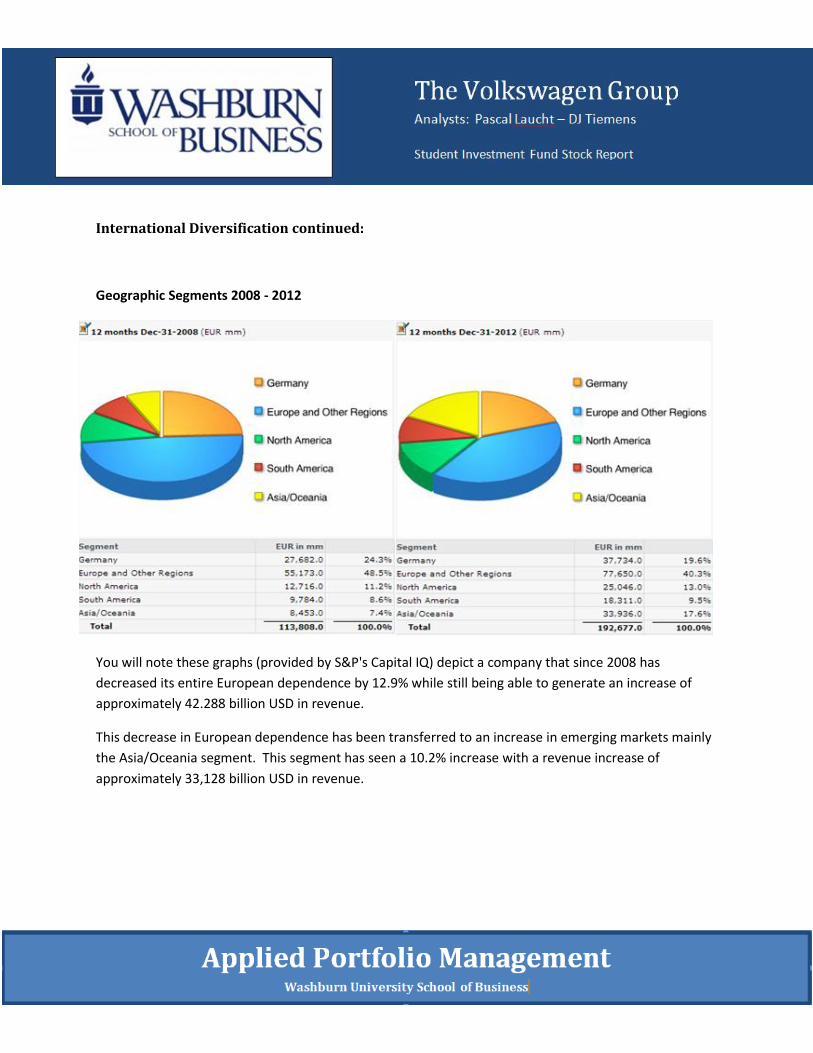

International Diversification continued:

Geographic Segments 2008 - 2012

You will note these graphs (provided by S&P's Capital IQ) depict a company that since 2008 has

decreased its entire European dependence by 12.9% while still being able to generate an increase of

approximately 42.288 billion USD in revenue.

This decrease in European dependence has been transferred to an increase in emerging markets mainly

the Asia/Oceania segment. This segment has seen a 10.2% increase with a revenue increase of

approximately 33,128 billion USD in revenue.

“Strategy 2018:”

A large part of understanding The Volkswagen Group's future value involves understanding its

commitment and the transparency that comes from its “Strategy 2018” vision statement. This strategy

states that the company intends to become the world’s most successful automaker by 2018.

This vision consists of four major initiatives (as taken from The VW’s 10-K):

Volkswagen intends to deploy intelligent innovations and technologies to become a world

leader in customer satisfaction and quality.

The goal is to increase unit sales to more than 10 million vehicles per year; in particular,

Volkswagen intends to capture an above-average share of the development of the major growth

markets.

Volkswagen intends to increase its return on sales before tax to at least 8% so as to ensure that

the Group’s solid financial position and ability to act are guaranteed even in difficult market

periods.

Volkswagen aims to become the top employer across all brands, companies and regions, which will allow the company to build a first-class team.

Continued on next page.

“Strategy 2018” continued:

To date, each of these matrixes has been positively impacted:

Measures 2008 2012

Customer Satisfaction Levels (base of 10) 8.32 8.67

Units Sales in Millions 5.80 9.30

Profit before Tax Margin 5.8% 13.2%

Employee approval rating 84% 90%

Financial Analysis:

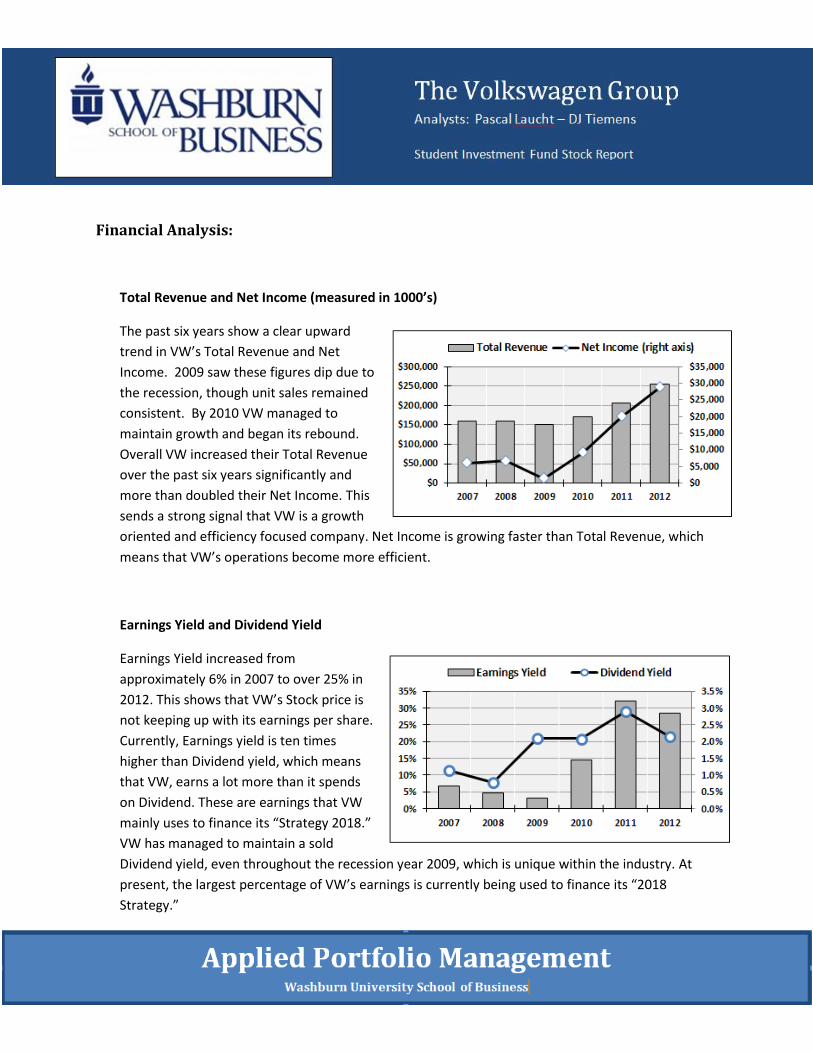

Total Revenue and Net Income (measured in 1000’s)

The past six years show a clear upward

trend in VW’s Total Revenue and Net

Income. 2009 saw these figures dip due to

the recession, though unit sales remained

consistent. By 2010 VW managed to

maintain growth and began its rebound.

Overall VW increased their Total Revenue

over the past six years significantly and

more than doubled their Net Income. This

sends a strong signal that VW is a growth

oriented and efficiency focused company. Net Income is growing faster than Total Revenue, which

means that VW’s operations become more efficient.

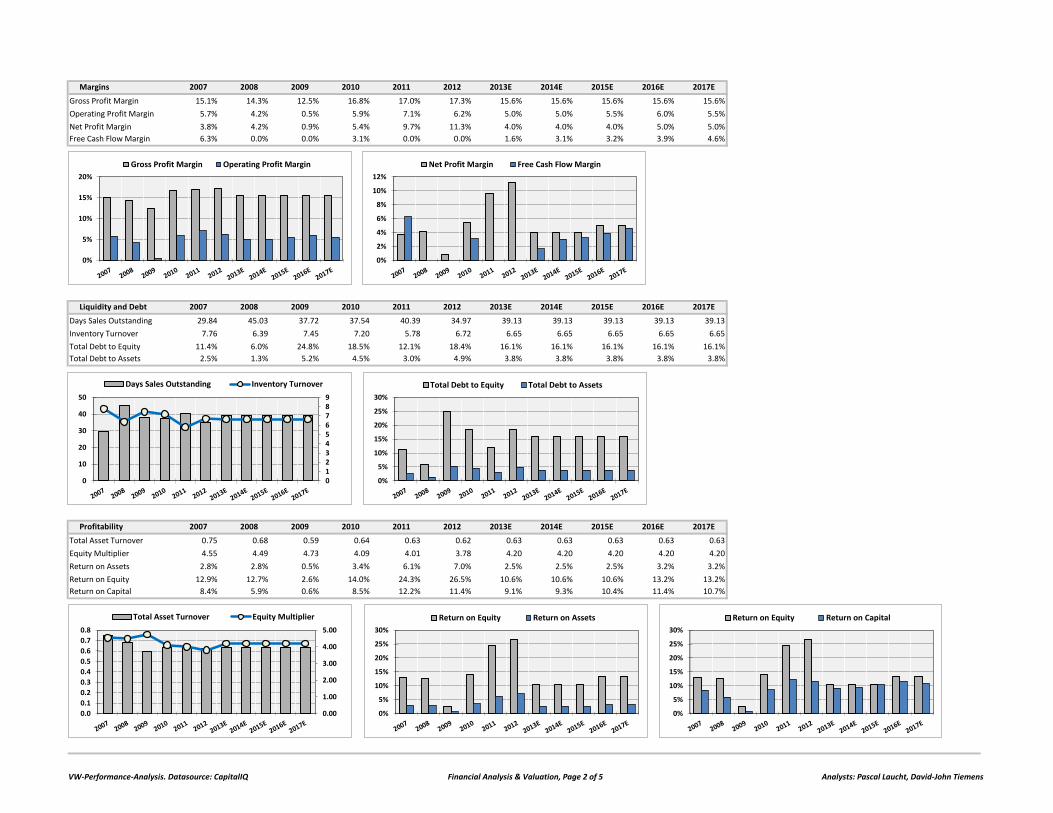

Earnings Yield and Dividend Yield

Earnings Yield increased from

approximately 6% in 2007 to over 25% in

2012. This shows that VW’s Stock price is

not keeping up with its earnings per share.

Currently, Earnings yield is ten times

higher than Dividend yield, which means

that VW, earns a lot more than it spends

on Dividend. These are earnings that VW

mainly uses to finance its “Strategy 2018.”

VW has managed to maintain a sold

Dividend yield, even throughout the recession year 2009, which is unique within the industry. At

present, the largest percentage of VW’s earnings is currently being used to finance its “2018

Strategy.”

05

1015202530354045

2007 2008 2009 2010 2011 2012

Price/Earnings Price/Free Cash Flow

0%

5%

10%

15%

20%

25%

30%

2007 2008 2009 2010 2011 2012

ROA ROE ROIC

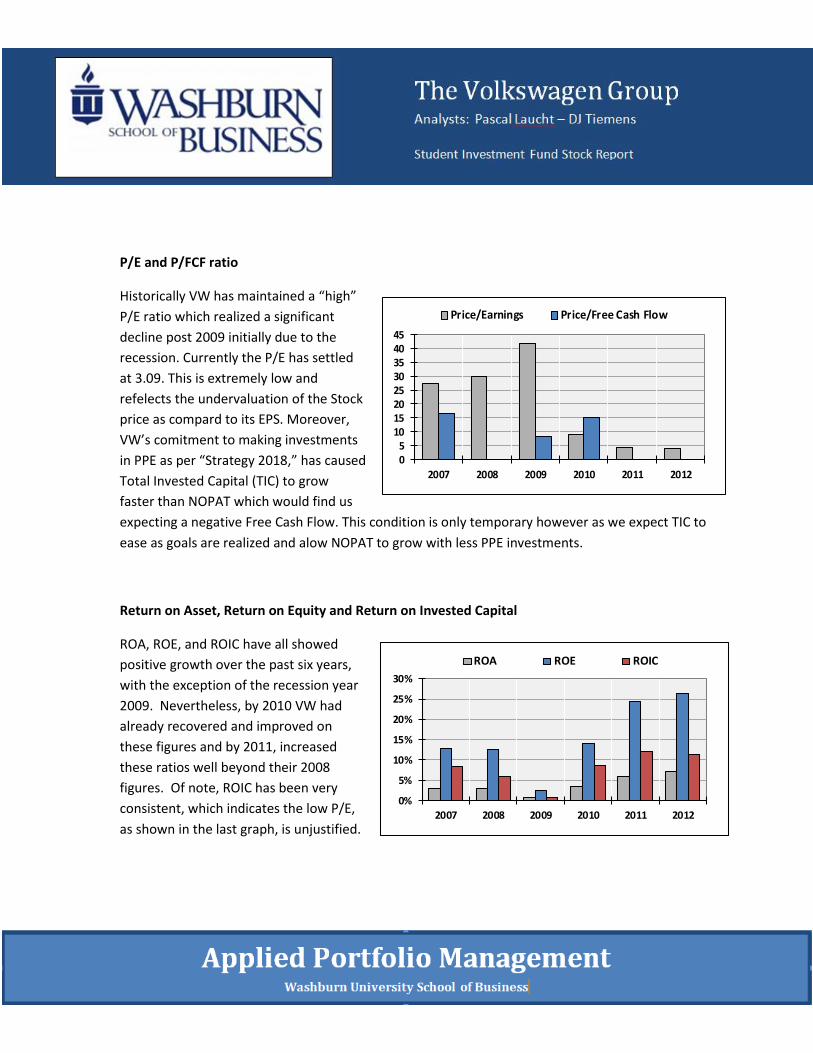

P/E and P/FCF ratio

Historically VW has maintained a “high”

P/E ratio which realized a significant

decline post 2009 initially due to the

recession. Currently the P/E has settled

at 3.09. This is extremely low and

refelects the undervaluation of the Stock

price as compard to its EPS. Moreover,

VW’s comitment to making investments

in PPE as per “Strategy 2018,” has caused

Total Invested Capital (TIC) to grow

faster than NOPAT which would find us

expecting a negative Free Cash Flow. This condition is only temporary however as we expect TIC to

ease as goals are realized and alow NOPAT to grow with less PPE investments.

Return on Asset, Return on Equity and Return on Invested Capital

ROA, ROE, and ROIC have all showed

positive growth over the past six years,

with the exception of the recession year

2009. Nevertheless, by 2010 VW had

already recovered and improved on

these figures and by 2011, increased

these ratios well beyond their 2008

figures. Of note, ROIC has been very

consistent, which indicates the low P/E,

as shown in the last graph, is unjustified.

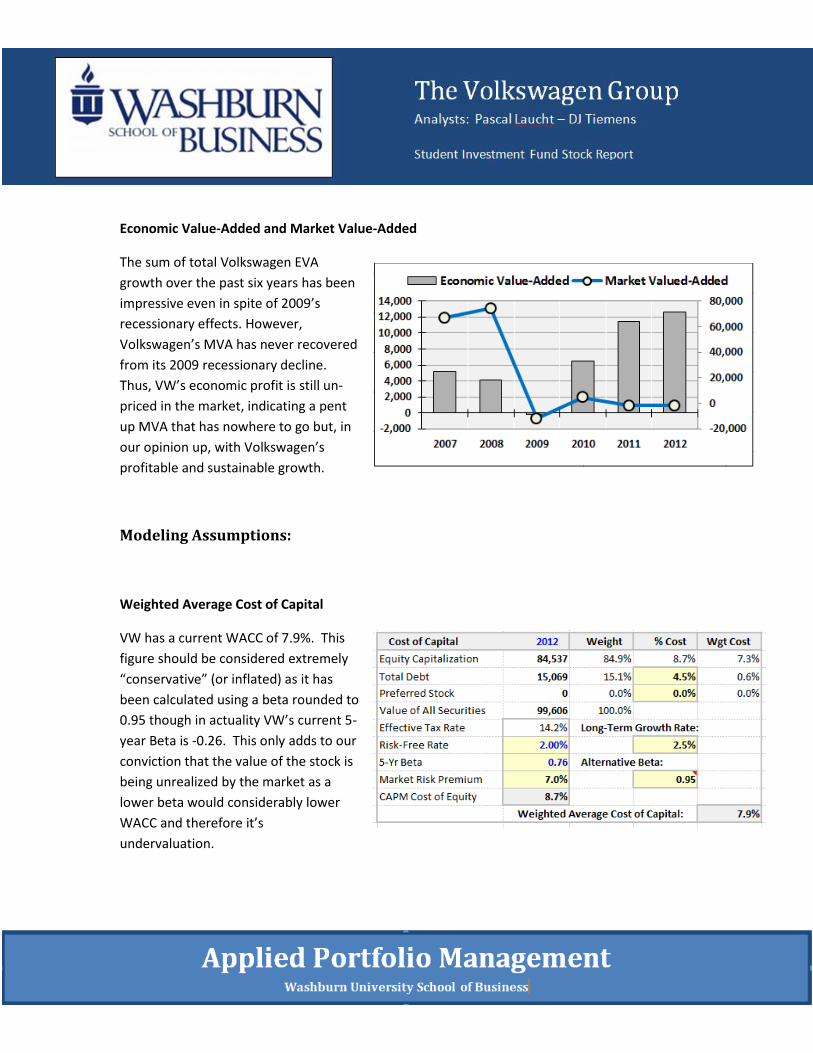

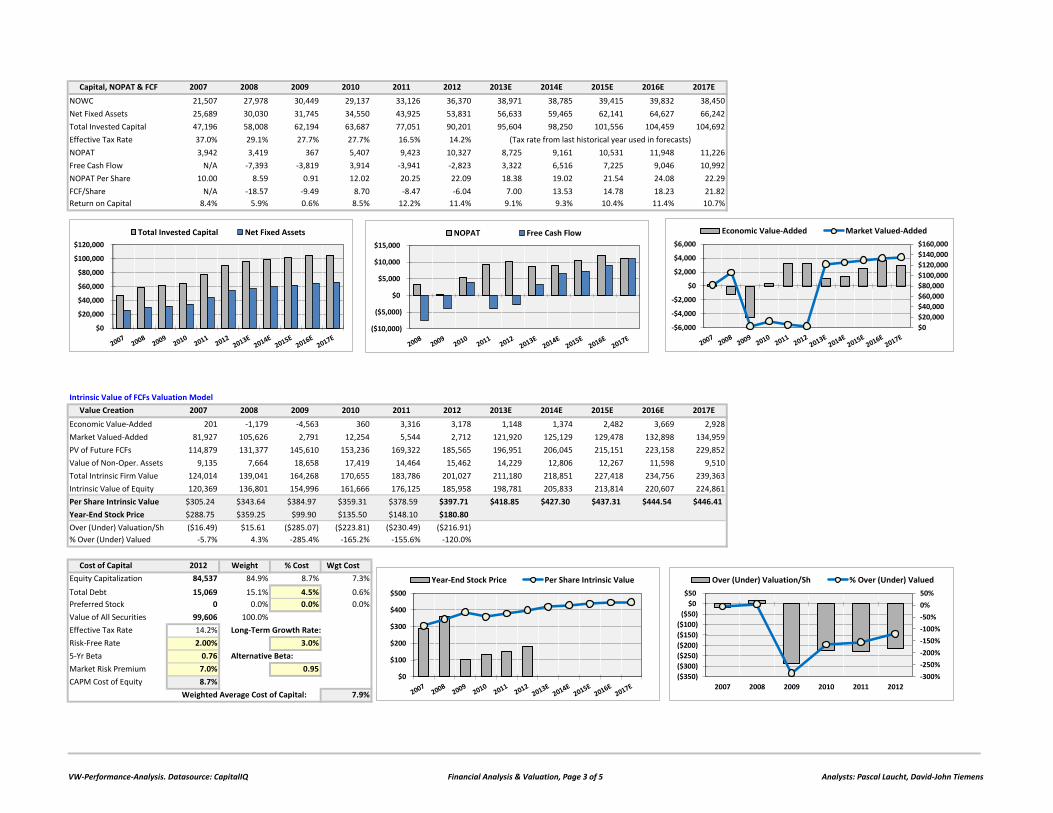

Economic Value-Added and Market Value-Added

The sum of total Volkswagen EVA

growth over the past six years has been

impressive even in spite of 2009’s

recessionary effects. However,

Volkswagen’s MVA has never recovered

from its 2009 recessionary decline.

Thus, VW’s economic profit is still un-

priced in the market, indicating a pent

up MVA that has nowhere to go but, in

our opinion up, with Volkswagen’s

profitable and sustainable growth.

Modeling Assumptions:

Weighted Average Cost of Capital

VW has a current WACC of 7.9%. This

figure should be considered extremely

“conservative” (or inflated) as it has

been calculated using a beta rounded to

0.95 though in actuality VW’s current 5-

year Beta is -0.26. This only adds to our

conviction that the value of the stock is

being unrealized by the market as a

lower beta would considerably lower

WACC and therefore it’s

undervaluation.

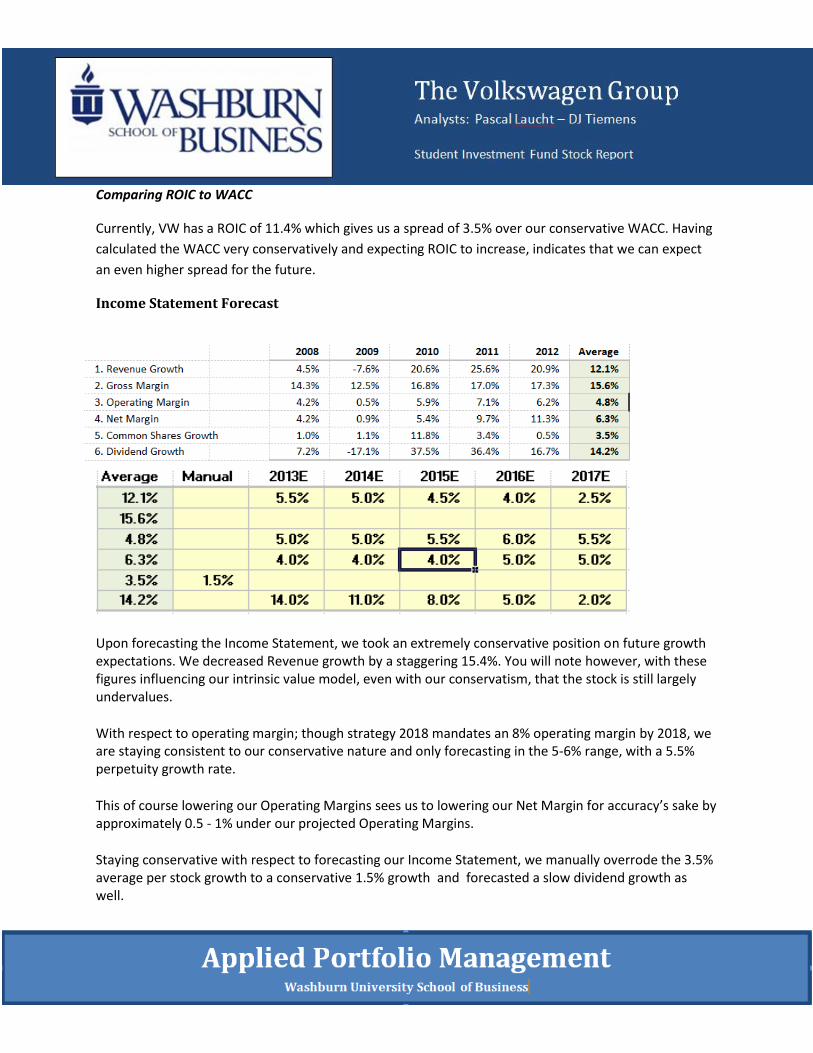

Comparing ROIC to WACC

Currently, VW has a ROIC of 11.4% which gives us a spread of 3.5% over our conservative WACC. Having

calculated the WACC very conservatively and expecting ROIC to increase, indicates that we can expect

an even higher spread for the future.

Income Statement Forecast

Upon forecasting the Income Statement, we took an extremely conservative position on future growth expectations. We decreased Revenue growth by a staggering 15.4%. You will note however, with these figures influencing our intrinsic value model, even with our conservatism, that the stock is still largely undervalues.

With respect to operating margin; though strategy 2018 mandates an 8% operating margin by 2018, we are staying consistent to our conservative nature and only forecasting in the 5-6% range, with a 5.5% perpetuity growth rate.

This of course lowering our Operating Margins sees us to lowering our Net Margin for accuracy’s sake by approximately 0.5 - 1% under our projected Operating Margins.

Staying conservative with respect to forecasting our Income Statement, we manually overrode the 3.5% average per stock growth to a conservative 1.5% growth and forecasted a slow dividend growth as well.

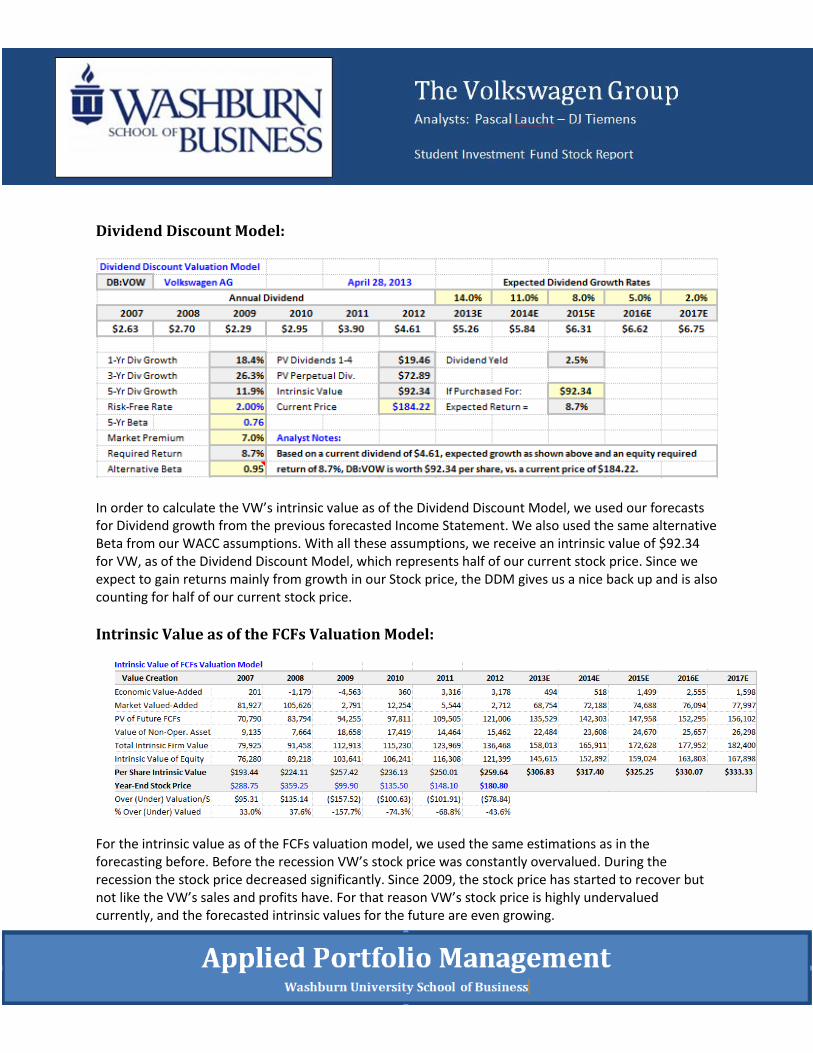

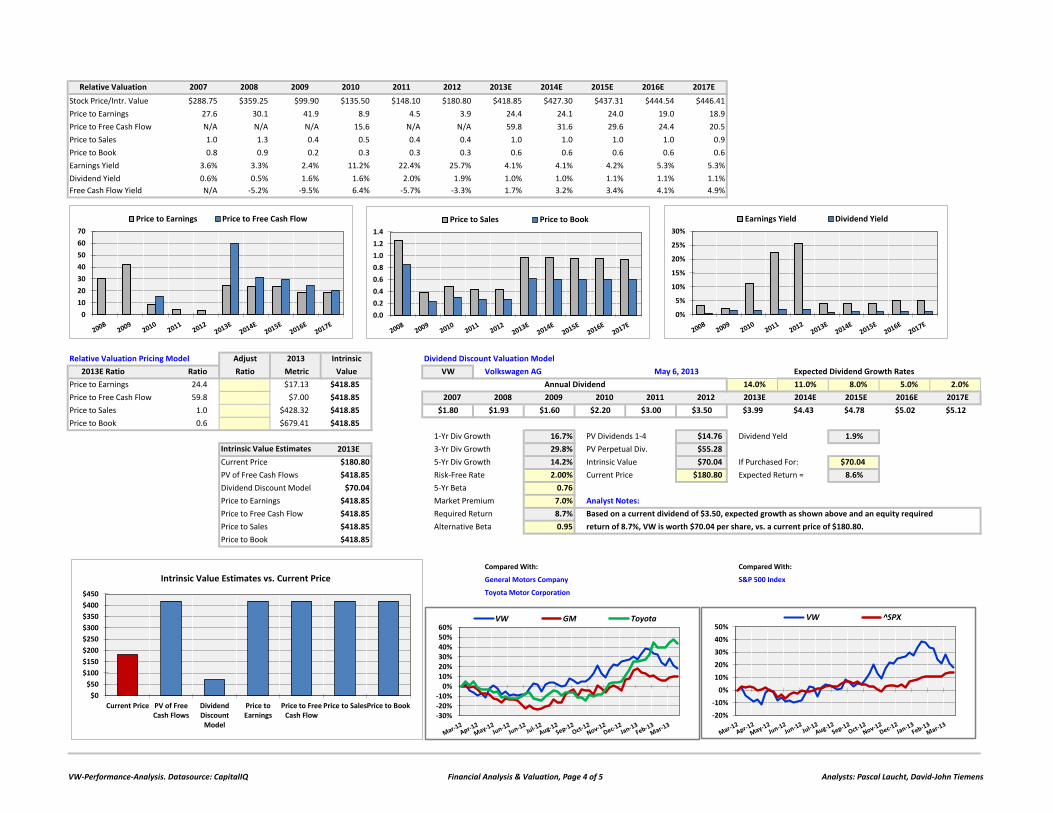

Dividend Discount Model:

In order to calculate the VW’s intrinsic value as of the Dividend Discount Model, we used our forecasts for Dividend growth from the previous forecasted Income Statement. We also used the same alternative Beta from our WACC assumptions. With all these assumptions, we receive an intrinsic value of $92.34 for VW, as of the Dividend Discount Model, which represents half of our current stock price. Since we expect to gain returns mainly from growth in our Stock price, the DDM gives us a nice back up and is also counting for half of our current stock price.

Intrinsic Value as of the FCFs Valuation Model:

For the intrinsic value as of the FCFs valuation model, we used the same estimations as in the forecasting before. Before the recession VW’s stock price was constantly overvalued. During the recession the stock price decreased significantly. Since 2009, the stock price has started to recover but not like the VW’s sales and profits have. For that reason VW’s stock price is highly undervalued currently, and the forecasted intrinsic values for the future are even growing.

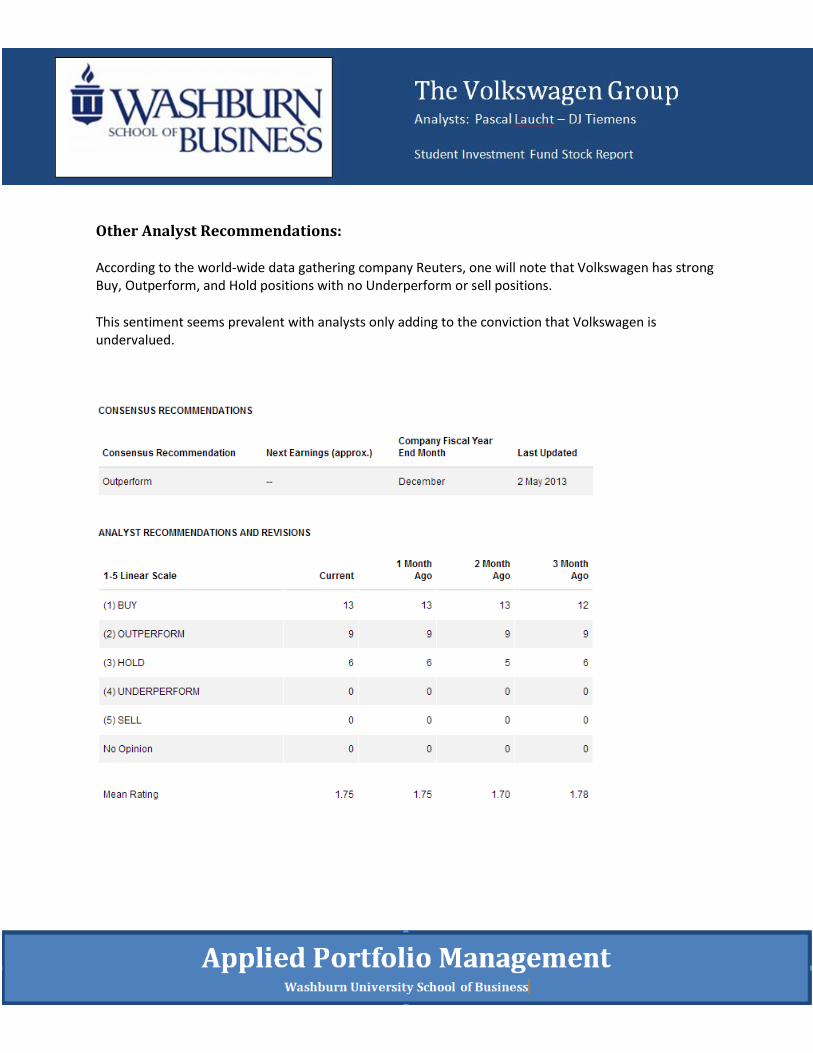

Other Analyst Recommendations:

According to the world-wide data gathering company Reuters, one will note that Volkswagen has strong Buy, Outperform, and Hold positions with no Underperform or sell positions.

This sentiment seems prevalent with analysts only adding to the conviction that Volkswagen is undervalued.

Recommendation/Summary:

From the Intrinsic value estimates we can see

that VW’s current stock price is undervalued in

every category, except the dividend discount

model (we expect no value(s) for Price to Future

Cash Flows as described previously). VW has a

very low dividend yield of slightly less than 2%,

which does not even cover the risk-free rate, but

the intrinsic value of the dividend discount model

is still accounting for a large portion of the stock.

This again, shows that VW is undervalued.

Ultimately we believe Volkswagen stock is grossly undervalued even when we forecast with reduced

growth rates of 15.4% over 2012 figures, and increase the beta from -0.26 to .0.95. We believe that this

is in large part due to the fear of investing in an automotive stock based out of the “Euro-Zone.”

Though these concerns are not to be taken lightly, upon investigation, conservative analysis, neither of

the authors can substantiate these concerns knowing of Volkswagen’s incredible past performance and

ability to historically combat what has proven to be, catastrophic recessions to others in the industry.

Moreover, bolstered by the knowledge that Volkswagen is actively becoming an even more world-wide

diversified company as we write this, only bolster our position more-so.

We are also encouraged noting that as Volkswagen moves ahead, it will ultimately be reducing its

current rate of investment in capital which has been necessary to reach the growth rates set out by its

2018 Strategy; as these growth rates in terms of unit sales have nearly been reached already in 2012.

Thus, we expect that ROIC will begin to realize gains unseen to date. Moreover, VW’s luxury auto’s

which produce the company’s largest profits have also seen an incredible resurgence as evidenced by

Porsche’s unit sales increases since 2009 (approximate unit growth of 1400 units in 2009 to over 3800 in

2012), which will all lead to the company’s stock realizing gains as the market reacts to these figures.

Therefore we recommend a buy position on The Volkswagen Groups stock with an eye on what we

believe will be its inevitable long-term growth.

Investment Thesis:

With our portfolio underweighted in Industrials, as analysts previously studying the automotive

industry, we became enticed as we studied VW’s ability to possibly create value for the portfolio

via growth that beats the S&P and still maintain a -0.26 Beta vs. the S&P 500

Looking deeper at the major players in the automotive industry, Volkswagen impressed us with

its solid performance throughout the recession and growth thereafter

The company’s high degree of integrity/transparency as it pursues its Strategy 2018 — which

states its desire to be the world’s largest automotive manufacturer by 2018 — bodes well for

future gains in revenues, profits and stock price appreciation

Volkswagen’s 3-CAGR shows EBIT growth of 187.4%, NOPAT growth of 204.3%, EPS growth of

169.1%, and EVA growth of 104.2%. With these strong numbers, and noting the company’s past

success as it pursues its “Strategy 2018” objective, we became convinced the company’s stock

undervaluation presented the Student Investment Fund with a unique opportunity

Volkswagen, a German based company, diversifies our portfolio internationally

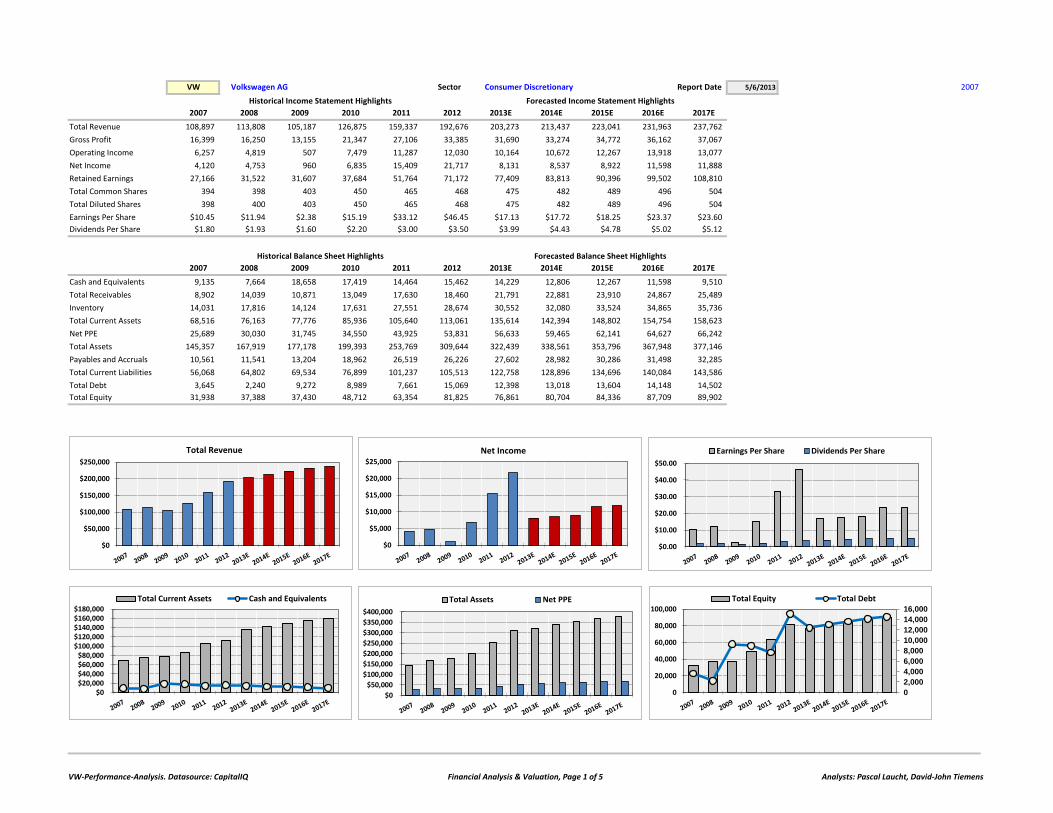

VW Volkswagen AG Sector Consumer Discretionary Report Date 5/6/2013 2007

2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

Total Revenue 108,897 113,808 105,187 126,875 159,337 192,676 203,273 213,437 223,041 231,963 237,762

Gross Profit 16,399 16,250 13,155 21,347 27,106 33,385 31,690 33,274 34,772 36,162 37,067

Operating Income 6,257 4,819 507 7,479 11,287 12,030 10,164 10,672 12,267 13,918 13,077

Net Income 4,120 4,753 960 6,835 15,409 21,717 8,131 8,537 8,922 11,598 11,888

Retained Earnings 27,166 31,522 31,607 37,684 51,764 71,172 77,409 83,813 90,396 99,502 108,810

Total Common Shares 394 398 403 450 465 468 475 482 489 496 504

Total Diluted Shares 398 400 403 450 465 468 475 482 489 496 504

Earnings Per Share $10.45 $11.94 $2.38 $15.19 $33.12 $46.45 $17.13 $17.72 $18.25 $23.37 $23.60

Dividends Per Share $1.80 $1.93 $1.60 $2.20 $3.00 $3.50 $3.99 $4.43 $4.78 $5.02 $5.12

2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

Cash and Equivalents 9,135 7,664 18,658 17,419 14,464 15,462 14,229 12,806 12,267 11,598 9,510

Total Receivables 8,902 14,039 10,871 13,049 17,630 18,460 21,791 22,881 23,910 24,867 25,489

Inventory 14,031 17,816 14,124 17,631 27,551 28,674 30,552 32,080 33,524 34,865 35,736

Total Current Assets 68,516 76,163 77,776 85,936 105,640 113,061 135,614 142,394 148,802 154,754 158,623

Net PPE 25,689 30,030 31,745 34,550 43,925 53,831 56,633 59,465 62,141 64,627 66,242

Total Assets 145,357 167,919 177,178 199,393 253,769 309,644 322,439 338,561 353,796 367,948 377,146

Payables and Accruals 10,561 11,541 13,204 18,962 26,519 26,226 27,602 28,982 30,286 31,498 32,285

Total Current Liabilities 56,068 64,802 69,534 76,899 101,237 105,513 122,758 128,896 134,696 140,084 143,586

Total Debt 3,645 2,240 9,272 8,989 7,661 15,069 12,398 13,018 13,604 14,148 14,502

Total Equity 31,938 37,388 37,430 48,712 63,354 81,825 76,861 80,704 84,336 87,709 89,902

Historical Income Statement Highlights Forecasted Income Statement Highlights

Historical Balance Sheet Highlights Forecasted Balance Sheet Highlights

$0

$50,000

$100,000

$150,000

$200,000

$250,000

Total Revenue

$0

$5,000

$10,000

$15,000

$20,000

$25,000

Net Income

$0$20,000$40,000$60,000$80,000

$100,000$120,000$140,000$160,000$180,000

Total Current Assets Cash and Equivalents

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

0

20,000

40,000

60,000

80,000

100,000

Total Equity Total Debt

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

Earnings Per Share Dividends Per Share

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

Total Assets Net PPE

VW-Performance-Analysis. Datasource: CapitalIQ Financial Analysis & Valuation, Page 1 of 5 Analysts: Pascal Laucht, David-John Tiemens

Margins 2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

Gross Profit Margin 15.1% 14.3% 12.5% 16.8% 17.0% 17.3% 15.6% 15.6% 15.6% 15.6% 15.6%

Operating Profit Margin 5.7% 4.2% 0.5% 5.9% 7.1% 6.2% 5.0% 5.0% 5.5% 6.0% 5.5%

Net Profit Margin 3.8% 4.2% 0.9% 5.4% 9.7% 11.3% 4.0% 4.0% 4.0% 5.0% 5.0%

Free Cash Flow Margin 6.3% 0.0% 0.0% 3.1% 0.0% 0.0% 1.6% 3.1% 3.2% 3.9% 4.6%

Liquidity and Debt 2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

Days Sales Outstanding 29.84 45.03 37.72 37.54 40.39 34.97 39.13 39.13 39.13 39.13 39.13

Inventory Turnover 7.76 6.39 7.45 7.20 5.78 6.72 6.65 6.65 6.65 6.65 6.65

Total Debt to Equity 11.4% 6.0% 24.8% 18.5% 12.1% 18.4% 16.1% 16.1% 16.1% 16.1% 16.1%

Total Debt to Assets 2.5% 1.3% 5.2% 4.5% 3.0% 4.9% 3.8% 3.8% 3.8% 3.8% 3.8%

Profitability 2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

Total Asset Turnover 0.75 0.68 0.59 0.64 0.63 0.62 0.63 0.63 0.63 0.63 0.63

Equity Multiplier 4.55 4.49 4.73 4.09 4.01 3.78 4.20 4.20 4.20 4.20 4.20

Return on Assets 2.8% 2.8% 0.5% 3.4% 6.1% 7.0% 2.5% 2.5% 2.5% 3.2% 3.2%

Return on Equity 12.9% 12.7% 2.6% 14.0% 24.3% 26.5% 10.6% 10.6% 10.6% 13.2% 13.2%

Return on Capital 8.4% 5.9% 0.6% 8.5% 12.2% 11.4% 9.1% 9.3% 10.4% 11.4% 10.7%

0.00

1.00

2.00

3.00

4.00

5.00

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Total Asset Turnover Equity Multiplier

0123456789

0

10

20

30

40

50

Days Sales Outstanding Inventory Turnover

0%

5%

10%

15%

20%

Gross Profit Margin Operating Profit Margin

0%

2%

4%

6%

8%

10%

12%

Net Profit Margin Free Cash Flow Margin

0%

5%

10%

15%

20%

25%

30%

Total Debt to Equity Total Debt to Assets

0%

5%

10%

15%

20%

25%

30%

Return on Equity Return on Assets

0%

5%

10%

15%

20%

25%

30%

Return on Equity Return on Capital

VW-Performance-Analysis. Datasource: CapitalIQ Financial Analysis & Valuation, Page 2 of 5 Analysts: Pascal Laucht, David-John Tiemens

Capital, NOPAT & FCF 2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

NOWC 21,507 27,978 30,449 29,137 33,126 36,370 38,971 38,785 39,415 39,832 38,450

Net Fixed Assets 25,689 30,030 31,745 34,550 43,925 53,831 56,633 59,465 62,141 64,627 66,242

Total Invested Capital 47,196 58,008 62,194 63,687 77,051 90,201 95,604 98,250 101,556 104,459 104,692

Effective Tax Rate 37.0% 29.1% 27.7% 27.7% 16.5% 14.2%

NOPAT 3,942 3,419 367 5,407 9,423 10,327 8,725 9,161 10,531 11,948 11,226

Free Cash Flow N/A -7,393 -3,819 3,914 -3,941 -2,823 3,322 6,516 7,225 9,046 10,992

NOPAT Per Share 10.00 8.59 0.91 12.02 20.25 22.09 18.38 19.02 21.54 24.08 22.29

FCF/Share N/A -18.57 -9.49 8.70 -8.47 -6.04 7.00 13.53 14.78 18.23 21.82

Return on Capital 8.4% 5.9% 0.6% 8.5% 12.2% 11.4% 9.1% 9.3% 10.4% 11.4% 10.7%

Intrinsic Value of FCFs Valuation Model

Value Creation 2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

Economic Value-Added 201 -1,179 -4,563 360 3,316 3,178 1,148 1,374 2,482 3,669 2,928

Market Valued-Added 81,927 105,626 2,791 12,254 5,544 2,712 121,920 125,129 129,478 132,898 134,959

PV of Future FCFs 114,879 131,377 145,610 153,236 169,322 185,565 196,951 206,045 215,151 223,158 229,852

Value of Non-Oper. Assets 9,135 7,664 18,658 17,419 14,464 15,462 14,229 12,806 12,267 11,598 9,510

Total Intrinsic Firm Value 124,014 139,041 164,268 170,655 183,786 201,027 211,180 218,851 227,418 234,756 239,363

Intrinsic Value of Equity 120,369 136,801 154,996 161,666 176,125 185,958 198,781 205,833 213,814 220,607 224,861

Per Share Intrinsic Value $305.24 $343.64 $384.97 $359.31 $378.59 $397.71 $418.85 $427.30 $437.31 $444.54 $446.41

Year-End Stock Price $288.75 $359.25 $99.90 $135.50 $148.10 $180.80

Over (Under) Valuation/Sh ($16.49) $15.61 ($285.07) ($223.81) ($230.49) ($216.91)

% Over (Under) Valued -5.7% 4.3% -285.4% -165.2% -155.6% -120.0%

Cost of Capital 2012 Weight % Cost Wgt Cost

Equity Capitalization 84,537 84.9% 8.7% 7.3%

Total Debt 15,069 15.1% 4.5% 0.6%

Preferred Stock 0 0.0% 0.0% 0.0%

Value of All Securities 99,606 100.0%

Effective Tax Rate 14.2% Long-Term Growth Rate:

Risk-Free Rate 2.00% 3.0%

5-Yr Beta 0.76 Alternative Beta:

Market Risk Premium 7.0% 0.95

CAPM Cost of Equity 8.7%

7.9%

(Tax rate from last historical year used in forecasts)

Weighted Average Cost of Capital:

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

-$6,000

-$4,000

-$2,000

$0

$2,000

$4,000

$6,000

Economic Value-Added Market Valued-Added

$0

$100

$200

$300

$400

$500

Year-End Stock Price Per Share Intrinsic Value

-300%

-250%

-200%

-150%

-100%

-50%

0%

50%

($350)

($300)

($250)

($200)

($150)

($100)

($50)

$0

$50

2007 2008 2009 2010 2011 2012

Over (Under) Valuation/Sh % Over (Under) Valued

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

Total Invested Capital Net Fixed Assets

($10,000)

($5,000)

$0

$5,000

$10,000

$15,000

NOPAT Free Cash Flow

VW-Performance-Analysis. Datasource: CapitalIQ Financial Analysis & Valuation, Page 3 of 5 Analysts: Pascal Laucht, David-John Tiemens

Relative Valuation 2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

Stock Price/Intr. Value $288.75 $359.25 $99.90 $135.50 $148.10 $180.80 $418.85 $427.30 $437.31 $444.54 $446.41

Price to Earnings 27.6 30.1 41.9 8.9 4.5 3.9 24.4 24.1 24.0 19.0 18.9

Price to Free Cash Flow N/A N/A N/A 15.6 N/A N/A 59.8 31.6 29.6 24.4 20.5

Price to Sales 1.0 1.3 0.4 0.5 0.4 0.4 1.0 1.0 1.0 1.0 0.9

Price to Book 0.8 0.9 0.2 0.3 0.3 0.3 0.6 0.6 0.6 0.6 0.6

Earnings Yield 3.6% 3.3% 2.4% 11.2% 22.4% 25.7% 4.1% 4.1% 4.2% 5.3% 5.3%

Dividend Yield 0.6% 0.5% 1.6% 1.6% 2.0% 1.9% 1.0% 1.0% 1.1% 1.1% 1.1%

Free Cash Flow Yield N/A -5.2% -9.5% 6.4% -5.7% -3.3% 1.7% 3.2% 3.4% 4.1% 4.9%

Relative Valuation Pricing Model Adjust 2013 Intrinsic Dividend Discount Valuation Model

2013E Ratio Ratio Ratio Metric Value VW Volkswagen AG

Price to Earnings 24.4 $17.13 $418.85 14.0% 11.0% 8.0% 5.0% 2.0%

Price to Free Cash Flow 59.8 $7.00 $418.85 2007 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

Price to Sales 1.0 $428.32 $418.85 $1.80 $1.93 $1.60 $2.20 $3.00 $3.50 $3.99 $4.43 $4.78 $5.02 $5.12

Price to Book 0.6 $679.41 $418.85

1-Yr Div Growth 16.7% PV Dividends 1-4 $14.76 Dividend Yeld 1.9%

2013E 3-Yr Div Growth 29.8% PV Perpetual Div. $55.28

Current Price $180.80 5-Yr Div Growth 14.2% Intrinsic Value $70.04 If Purchased For: $70.04

PV of Free Cash Flows $418.85 Risk-Free Rate 2.00% Current Price $180.80 Expected Return = 8.6%

Dividend Discount Model $70.04 5-Yr Beta 0.76 ($70.04) $3.99 $4.43 $4.78 $82.06 $77.03

Price to Earnings $418.85 Market Premium 7.0% Analyst Notes:

Price to Free Cash Flow $418.85 Required Return 8.7% Based on a current dividend of $3.50, expected growth as shown above and an equity required

Price to Sales $418.85 Alternative Beta 0.95 return of 8.7%, VW is worth $70.04 per share, vs. a current price of $180.80.

Price to Book $418.85

Compared With: Compared With:

General Motors Company S&P 500 Index

Toyota Motor Corporation

Expected Dividend Growth Rates

Intrinsic Value Estimates vs. Current Price

May 6, 2013

Annual Dividend

0

10

20

30

40

50

60

70

Price to Earnings Price to Free Cash Flow

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Price to Sales Price to Book

0%

5%

10%

15%

20%

25%

30%

Earnings Yield Dividend Yield

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

Current Price PV of FreeCash Flows

DividendDiscount

Model

Price toEarnings

Price to FreeCash Flow

Price to SalesPrice to Book

Intrinsic Value Estimates vs. Current Price

-30%-20%-10%

0%10%20%30%40%50%60%

VW GM Toyota

-20%

-10%

0%

10%

20%

30%

40%

50%VW ^SPX

VW-Performance-Analysis. Datasource: CapitalIQ Financial Analysis & Valuation, Page 4 of 5 Analysts: Pascal Laucht, David-John Tiemens

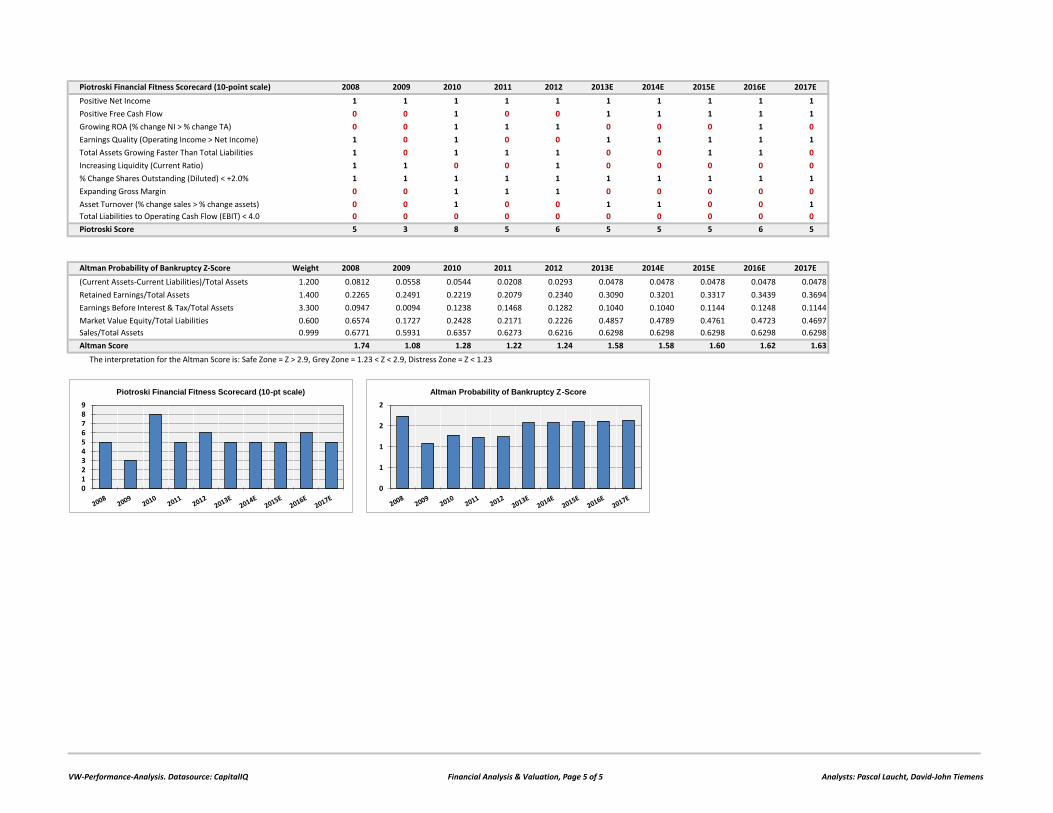

Piotroski Financial Fitness Scorecard (10-point scale) 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

Positive Net Income 1 1 1 1 1 1 1 1 1 1

Positive Free Cash Flow 0 0 1 0 0 1 1 1 1 1

Growing ROA (% change NI > % change TA) 0 0 1 1 1 0 0 0 1 0

Earnings Quality (Operating Income > Net Income) 1 0 1 0 0 1 1 1 1 1

Total Assets Growing Faster Than Total Liabilities 1 0 1 1 1 0 0 1 1 0

Increasing Liquidity (Current Ratio) 1 1 0 0 1 0 0 0 0 0

% Change Shares Outstanding (Diluted) < +2.0% 1 1 1 1 1 1 1 1 1 1

Expanding Gross Margin 0 0 1 1 1 0 0 0 0 0

Asset Turnover (% change sales > % change assets) 0 0 1 0 0 1 1 0 0 1

Total Liabilities to Operating Cash Flow (EBIT) < 4.0 0 0 0 0 0 0 0 0 0 0

Piotroski Score 5 3 8 5 6 5 5 5 6 5

Altman Probability of Bankruptcy Z-Score Weight 2008 2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E

(Current Assets-Current Liabilities)/Total Assets 1.200 0.0812 0.0558 0.0544 0.0208 0.0293 0.0478 0.0478 0.0478 0.0478 0.0478

Retained Earnings/Total Assets 1.400 0.2265 0.2491 0.2219 0.2079 0.2340 0.3090 0.3201 0.3317 0.3439 0.3694

Earnings Before Interest & Tax/Total Assets 3.300 0.0947 0.0094 0.1238 0.1468 0.1282 0.1040 0.1040 0.1144 0.1248 0.1144

Market Value Equity/Total Liabilities 0.600 0.6574 0.1727 0.2428 0.2171 0.2226 0.4857 0.4789 0.4761 0.4723 0.4697

Sales/Total Assets 0.999 0.6771 0.5931 0.6357 0.6273 0.6216 0.6298 0.6298 0.6298 0.6298 0.6298

Altman Score 1.74 1.08 1.28 1.22 1.24 1.58 1.58 1.60 1.62 1.63

The interpretation for the Altman Score is: Safe Zone = Z > 2.9, Grey Zone = 1.23 < Z < 2.9, Distress Zone = Z < 1.23

0123456789

Piotroski Financial Fitness Scorecard (10-pt scale)

0

1

1

2

2

Altman Probability of Bankruptcy Z-Score

VW-Performance-Analysis. Datasource: CapitalIQ Financial Analysis & Valuation, Page 5 of 5 Analysts: Pascal Laucht, David-John Tiemens