Embed Size (px)

Citation preview

Sector note

Egyptian Telecom SectorTelecoms | Egypt MENA research

A yield game Real penetration of 95% implies limited subscriber growth going forward,

mainly driven by an increase in dual/triple SIMs and a young population A relatively high telecom spending to GDP implies low revenue growth for

the sector (2011–14e CAGR of 2.8%), making it no longer a growth story

We remain Overweight on TE (TP EGP21.1/share, 2010e FCF and dividend yield of 16.6% and 8.1%) and Neutral on Mobinil (TP EGP179.6/share)

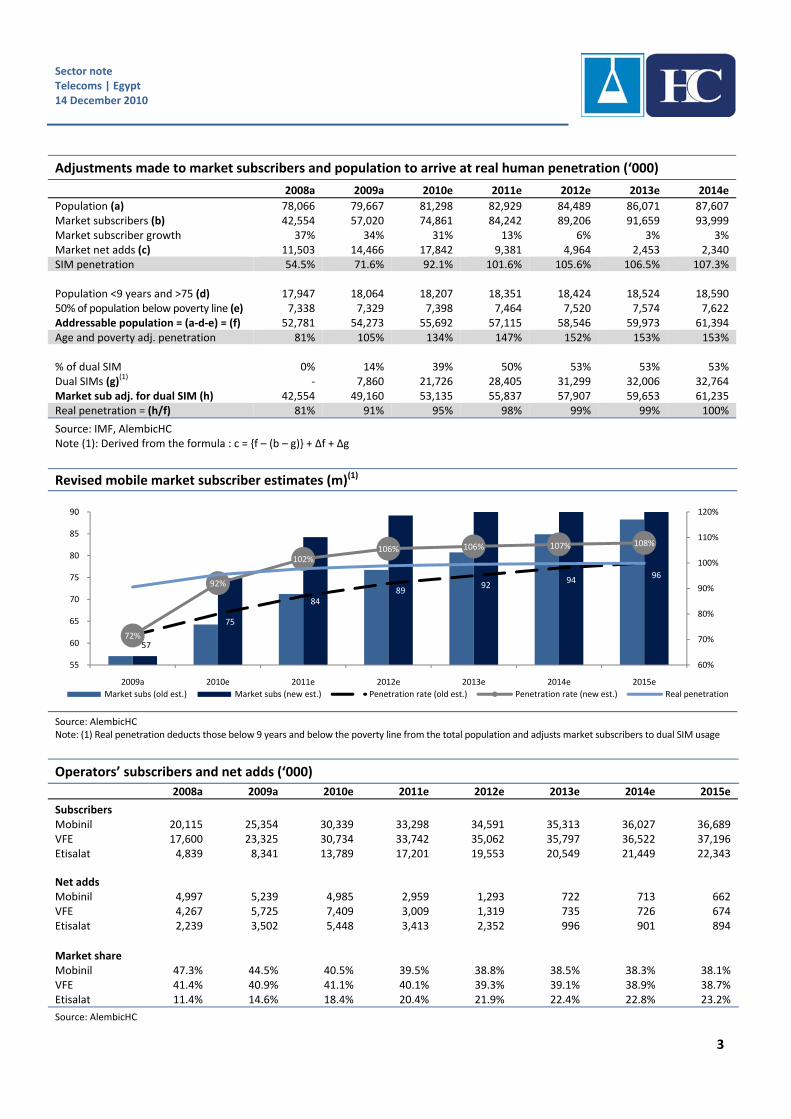

The penetration rate in Egypt is higher than it seems as real penetration is expected to reach 95% by the end of 2010e. We forecast an addressable population of 55.7m (adjusted for age and income distribution) versus a total population of 81.3m. Based on our calculations, we estimate dual SIMs stand at 39% of the total subscriber base, which implies 53.1m human subscribers versus reported subscribers of 74.9m. Accordingly, we expect limited subscriber growth, with a 2011–14e CAGR of 5.9% mainly driven by dual/triple SIMs (reaching 53% by 2012e) and new additions (1.4m per year) from the youth segment (21% of the population). We expect ARPU dilution to continue on the back of price cuts into 2011e as operators fight for subscribers. Blended ARPU is expected to dilute at a 4.5% 2011–14e CAGR, offsetting market subscriber growth. Accordingly, we expect Telecom Egypt (TE), Mobinil, and Vodafone Egypt’s (VFE) revenue to grow at a 2011–14e CAGR below 2.7%. Our revenue growth estimates are supported by Egypt’s relatively high telecom spending to GDP (3.3%) compared to other emerging and developed markets. We believe the Egyptian telecom story suits value investors, as such TE remains our top pick. We reiterate our Overweight rating on TE (TP EGP 21.1/share) a defensive stock with a high yield. We expect dividend yields of 8.1% for 2010e and 8.7% for 2011e, supported by strong cash flow generation (FCF yield of 16.6% and 11.2%) and a solid balance sheet (TE’s cash balance is expected to reach 17% of total assets in 2013e). Our cash flow assumptions take into account an MVNO license fee (EGP550m) in 2011e, related annual CAPEX of EGP150m onwards and further broadband expansion. TE is cheap on multiples, trading at a 10% discount to peers on 2011e PE and 36% on adjusted EV/EBITDA. We maintain our Neutral rating on Mobinil (TP EGP179.6/share) as we expect FCF yield and net profit growth to come under pressure given expected high CAPEX and margin compression due to competition. We expect a dividend yield of 4.3% for 2010e and 5.8% for 2011e (payout ratio of 50% and 70%). Upside risks to our valuation are lower ARPU dilution and Orascom Telecom exercising its put option, thereby forcing France Telecom to launch a mandatory tender offer to minorities at EGP221.7/share.

Mobinil Neutral

Target price (EGP) 179.6Current price (EGP) 166.7Potential return 7.7%Bloomberg EMOB EYReuters EMOB.CAMCap (USDbn) 2.9Daily volume (USDm) 2.6

All prices as of 12 December 2010

14 December 2010

Karim Khadr Analyst

+971 4 293 5381 karim.khadr@hc‐si.com

Sarah Shabayek Analyst

+971 4 293 5389 sarah.shabayek@hc‐si.com

Disclaimer: See page 40

Telecom Egypt Overweight

Target price (EGP) 21.1Current price (EGP) 17.6Potential return 20.0%Bloomberg ETEL EYReuters ETEL.CAMCap (USDbn) 5.2Daily volume (USDm) 3.9

Sector note Telecoms | Egypt 14 December 2010

2

Muted growth outlook

Limited subscriber growth as real penetration is expected to reach 95% in 2010e, dual/triple SIMs to drive 2011–12e growth, the young to remain long‐term drivers

Continuing ARPU dilution (2011–14e CAGR of ‐5%) as operators are subscriber acquisition oriented

Relatively high telecom spending to GDP indicates growth at par with real GDP, albeit at a lower rate in the short term due to competition, 2011–14e CAGR of 2.8%

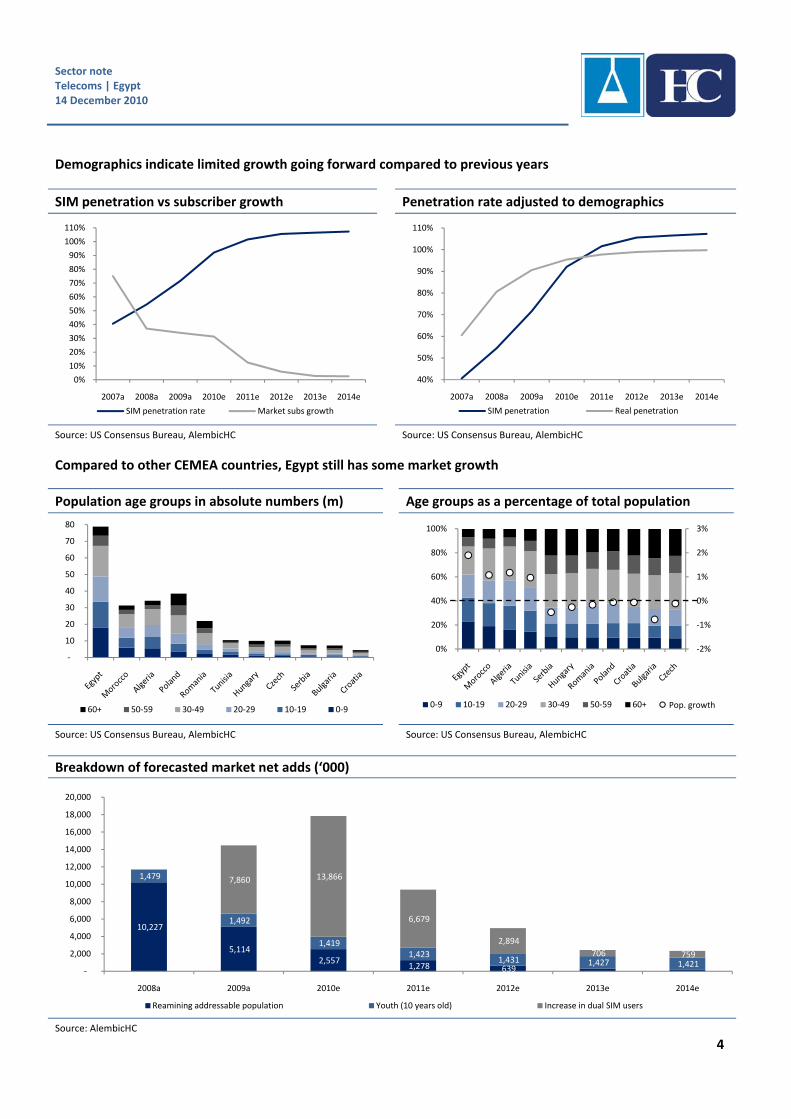

Real penetration of 95% in 2010e Egypt’s penetration rate is higher than it seems since the addressable market is considerably smaller than Egypt’s population (55.7m versus 81.3m). We calculated the penetration rate by taking into account age and income distribution and subtracting those below 9 years of age, those above 75, and half of those under the poverty line (to avoid double counting). Dual SIM users are expected to represent 39% of total subscribers (supported by Mobinil and TE’s management guidance of c35%) leading to human subscribers of 53.1m versus reported market subscribers of 74.9m. Dual/triple SIMs to drive growth in 2011e and 2012e We believe price competition in the mobile sector ensures some short‐term growth as it stimulates dual and even triple SIMs. Mobinil is back in the game fighting for its market share, and VFE changed its strategy from focusing on value‐added propositions to subscriber acquisitions. The fight on market leadership and Etisalat’s efforts to further increase its market share ensure that competition remains in the market and that the percentage of dual SIMs could increase to 50% in 2011e and 53% in 2012e from 39% in 2010e. We believe the pricing environment will stabilize by 2012e and therefore going forward headline prices should remain unchanged. The on‐net/off‐net price differential should be maintained and therefore subscribers would have no incentive to purchase another SIM or drop one they own. New additions of 1.4m/annum from the youth segment to continue to drive growth in the long term Some growth should still take place driven by those below 9 years of age. The Egyptian population’s growth rate is c1.9% (most CEMEA countries are experiencing negative growth), and a significant part of the population is under the age of 9 (21% of the total population). New subscribers are expected to be the main source of market growth (c1.4m new subscribers per year). We increased our estimates for market subscribers in 2010e and 2011e to reflect continuing intense competition but lowered the rate by which subscribers grow in the long run to reflect market maturity.

Sector note Telecoms | Egypt 14 December 2010

3

Adjustments made to market subscribers and population to arrive at real human penetration (‘000)

2008a 2009a 2010e 2011e 2012e 2013e 2014e

Population (a) 78,066 79,667 81,298 82,929 84,489 86,071 87,607 Market subscribers (b) 42,554 57,020 74,861 84,242 89,206 91,659 93,999 Market subscriber growth 37% 34% 31% 13% 6% 3% 3% Market net adds (c) 11,503 14,466 17,842 9,381 4,964 2,453 2,340 SIM penetration 54.5% 71.6% 92.1% 101.6% 105.6% 106.5% 107.3% Population <9 years and >75 (d) 17,947 18,064 18,207 18,351 18,424 18,524 18,590 50% of population below poverty line (e) 7,338 7,329 7,398 7,464 7,520 7,574 7,622 Addressable population = (a‐d‐e) = (f) 52,781 54,273 55,692 57,115 58,546 59,973 61,394 Age and poverty adj. penetration 81% 105% 134% 147% 152% 153% 153% % of dual SIM 0% 14% 39% 50% 53% 53% 53% Dual SIMs (g)(1) ‐ 7,860 21,726 28,405 31,299 32,006 32,764 Market sub adj. for dual SIM (h) 42,554 49,160 53,135 55,837 57,907 59,653 61,235 Real penetration = (h/f) 81% 91% 95% 98% 99% 99% 100%

Source: IMF, AlembicHC Note (1): Derived from the formula : c = {f – (b – g)} + Δf + Δg

Revised mobile market subscriber estimates (m)(1)

Source: AlembicHC Note: (1) Real penetration deducts those below 9 years and below the poverty line from the total population and adjusts market subscribers to dual SIM usage

Operators’ subscribers and net adds (‘000)

2008a 2009a 2010e 2011e 2012e 2013e 2014e 2015e

Subscribers Mobinil 20,115 25,354 30,339 33,298 34,591 35,313 36,027 36,689 VFE 17,600 23,325 30,734 33,742 35,062 35,797 36,522 37,196 Etisalat 4,839 8,341 13,789 17,201 19,553 20,549 21,449 22,343 Net adds Mobinil 4,997 5,239 4,985 2,959 1,293 722 713 662 VFE 4,267 5,725 7,409 3,009 1,319 735 726 674 Etisalat 2,239 3,502 5,448 3,413 2,352 996 901 894

Market share Mobinil 47.3% 44.5% 40.5% 39.5% 38.8% 38.5% 38.3% 38.1% VFE 41.4% 40.9% 41.1% 40.1% 39.3% 39.1% 38.9% 38.7% Etisalat 11.4% 14.6% 18.4% 20.4% 21.9% 22.4% 22.8% 23.2%

Source: AlembicHC

57

75

8489

9294

96

72%

92%

102%106% 106% 107% 108%

60%

70%

80%

90%

100%

110%

120%

55

60

65

70

75

80

85

90

2009a 2010e 2011e 2012e 2013e 2014e 2015e

Market subs (old est.) Market subs (new est.) Penetration rate (old est.) Penetration rate (new est.) Real penetration

Sector note Telecoms | Egypt 14 December 2010

4

Demographics indicate limited growth going forward compared to previous years

SIM penetration vs subscriber growth Penetration rate adjusted to demographics

Source: US Consensus Bureau, AlembicHC Source: US Consensus Bureau, AlembicHC

Compared to other CEMEA countries, Egypt still has some market growth

Population age groups in absolute numbers (m) Age groups as a percentage of total population

Source: US Consensus Bureau, AlembicHC Source: US Consensus Bureau, AlembicHC

Breakdown of forecasted market net adds (‘000)

Source: AlembicHC

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

2007a 2008a 2009a 2010e 2011e 2012e 2013e 2014e

SIM penetration rate Market subs growth

40%

50%

60%

70%

80%

90%

100%

110%

2007a 2008a 2009a 2010e 2011e 2012e 2013e 2014e

SIM penetration Real penetration

‐

10

20

30

40

50

60

70

80

60+ 50‐59 30‐49 20‐29 10‐19 0‐9

‐2%

‐1%

0%

1%

2%

3%

0%

20%

40%

60%

80%

100%

0‐9 10‐19 20‐29 30‐49 50‐59 60+ pop. growth

10,227

5,114 2,557

1,278 639

1,479

1,492

1,419 1,423

1,431 1,427 1,421

7,860 13,866

6,679

2,894

706 759

‐

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2008a 2009a 2010e 2011e 2012e 2013e 2014e

Reamining addressable population Youth (10 years old) Increase in dual SIM users

Pop. growth

Sector note Telecoms | Egypt 14 December 2010

5

ARPU to dilute by a 2011–14e CAGR of 5% New subscribers are younger than 9 years or hold another SIM We believe ARPU dilution will continue as long as market volatility persists, which is expected to end in 2012e. The fact that real penetration is expected to reach 95% by the end of 2010e means that every additional subscriber should be harder to add since he/she would either be less than 9 years old, already subscribed to another operator, or one of the few remaining from the addressable population. We believe the existing fierce competition (based on our calculation for incremental ARPU) is eroding value, suggesting that existing subscribers for Mobinil and VFE are spending less.

Incremental ARPU Calculation (EGP)(1) ARPU forecast (EGP)

Source: Mobinil, VG, TE, AlembicHC Note: (1) Negative incremental ARPU means that existing subscribers are spending less

Source: Mobinil, VG, TE, AlembicHC

Tariff plans mirror operator strategies, all targeting subscriber acquisitions There are 3 main tariff plans in the Egyptian market apart from the recently introduced per second billing. The plans say much about the strategies of the different operators. Mobinil’s plans speak of its recent change of strategy in 3Q10. Previously focusing on enhancing usage with plans characterized by a higher first‐minute rate, call set‐up and subscription fees, Mobinil has clearly signaled its return to the subscriber acquisition war with its newest offer, Bedoun Sheroot (Without Conditions), introduced on 21 October to match VFE and Etisalat’s flat rate on off‐net (19pt) and offering a lower on‐net minute rate (14pt).

37

2814

‐5

46

33

7

1

(10)

0

10

20

30

40

50

2007a 2008a 2009a 2010e

Mobinil VFE

‐14%

‐15%

‐21%‐10% ‐5% ‐1% 0%

‐12%

‐22%

‐24%

‐14%‐5% ‐1% 1%

20

25

30

35

40

45

50

55

60

65

70

75

2007a 2008a 2009a 2010e 2011e 2012e 2013e 2014e

Mobinil VFE

Sector note Telecoms | Egypt 14 December 2010

6

Current prepaid tariff plans

Mobinil Vodafone Etisalat

A) Flat Rate

Al Masry Bedoun Sheroot Kol El Masryeen Kol El Nas

On‐net rates

19pt 19pt

First 2 minutes 18pt 14pt

Starting the third minute 8pt

Off‐net rates

First minute 28pt 19pt

Starting the second minute 18pt

Analysis:

Encourages usage beyond Third min. (on net), Second min. (off net)

NA NA

Targeted ARPU(1) EGP13.2/month NA NA Cheapest on‐net rate

B) Preferred on‐net numbers

Ahsan Nas Hakawy Friends Yes

Number of preferred numbers 4 3 3 Preferred number rate 5pt(2) 5pt(2) 5pt On‐net rate 20pt 20pt 15pt Off‐net rate 30pt 30pt 25pt

Analysis:

Encourages usage beyond 3 minutes/day 3 minutes/day NA Targeted ARPU(1) EGP18.0/Month EGP18.0/month NA Cheapest rate

C) Targeting areas outside Greater Cairo Baladna Hakawy Regional Mohafazat

Rates for customers outside Greater Cairo On net 8pt 14pt

15pt Off net 14pt 24pt Rates for customers inside Greater Cairo On net 22pt 19pt

20pt Off net 35pt 24pt Call set up fee 11pt NA NA

Analysis:

Encourages usage beyond First minute of the call NA NA Targeted ARPU(1) EGP8.1/month NA NA Cheapest on net outside Greater Cairo Cheapest off net outside Greater Cairo Cheapest on net inside Greater Cairo Cheapest off net inside Greater Cairo

Source: Mobinil, VFE, Etisalat Egypt Note: (1) Assuming usage is enhanced beyond targeted minutes and multiplied by 30 (2) VFE and Mobinil: Customers can make calls to preferred numbers for free (12am–6pm for no more than 120 minutes/day) on the condition that they use three charged minutes per day

Sector note Telecoms | Egypt 14 December 2010

7

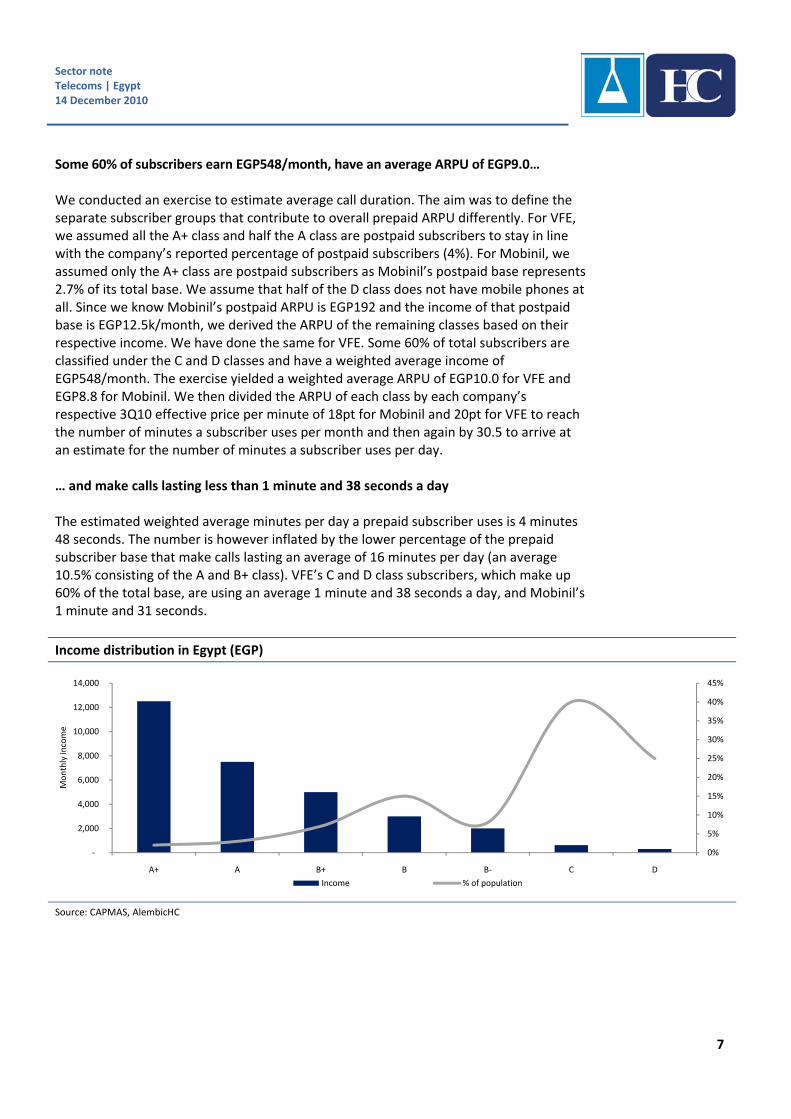

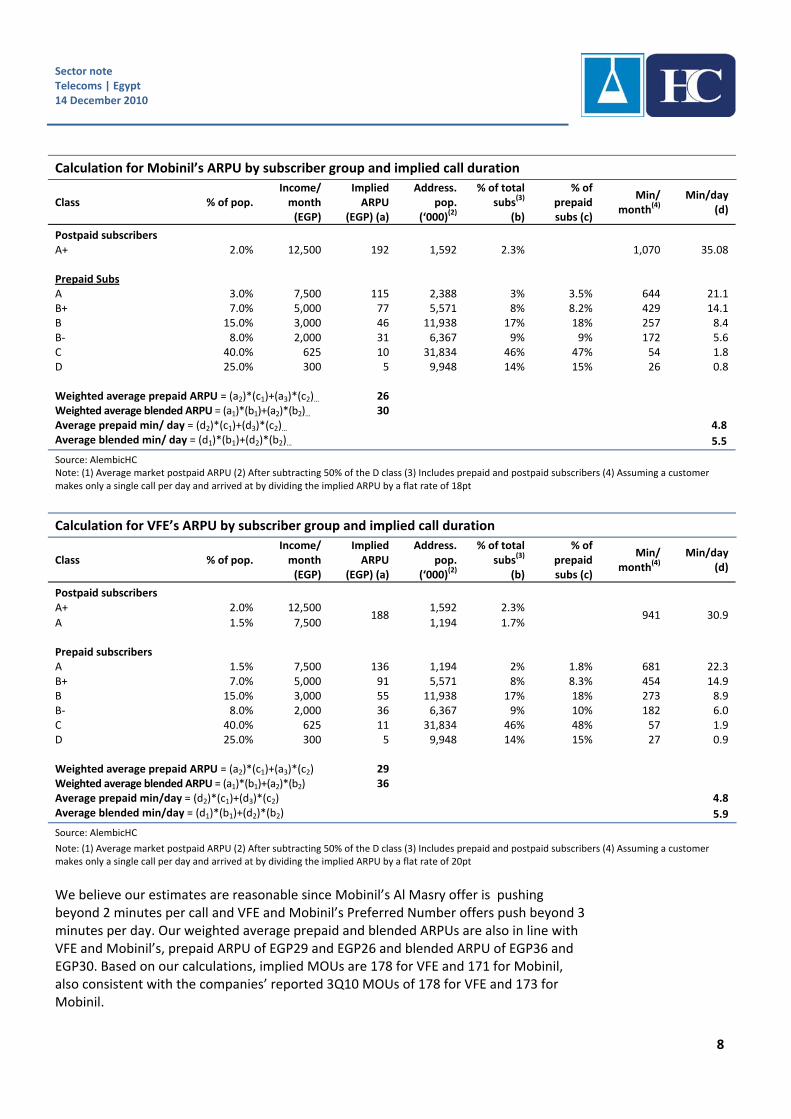

Some 60% of subscribers earn EGP548/month, have an average ARPU of EGP9.0… We conducted an exercise to estimate average call duration. The aim was to define the separate subscriber groups that contribute to overall prepaid ARPU differently. For VFE, we assumed all the A+ class and half the A class are postpaid subscribers to stay in line with the company’s reported percentage of postpaid subscribers (4%). For Mobinil, we assumed only the A+ class are postpaid subscribers as Mobinil’s postpaid base represents 2.7% of its total base. We assume that half of the D class does not have mobile phones at all. Since we know Mobinil’s postpaid ARPU is EGP192 and the income of that postpaid base is EGP12.5k/month, we derived the ARPU of the remaining classes based on their respective income. We have done the same for VFE. Some 60% of total subscribers are classified under the C and D classes and have a weighted average income of EGP548/month. The exercise yielded a weighted average ARPU of EGP10.0 for VFE and EGP8.8 for Mobinil. We then divided the ARPU of each class by each company’s respective 3Q10 effective price per minute of 18pt for Mobinil and 20pt for VFE to reach the number of minutes a subscriber uses per month and then again by 30.5 to arrive at an estimate for the number of minutes a subscriber uses per day. … and make calls lasting less than 1 minute and 38 seconds a day The estimated weighted average minutes per day a prepaid subscriber uses is 4 minutes 48 seconds. The number is however inflated by the lower percentage of the prepaid subscriber base that make calls lasting an average of 16 minutes per day (an average 10.5% consisting of the A and B+ class). VFE’s C and D class subscribers, which make up 60% of the total base, are using an average 1 minute and 38 seconds a day, and Mobinil’s 1 minute and 31 seconds.

Income distribution in Egypt (EGP)

Source: CAPMAS, AlembicHC

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

‐

2,000

4,000

6,000

8,000

10,000

12,000

14,000

A+ A B+ B B‐ C D

Monthly income

Income % of population

Sector note Telecoms | Egypt 14 December 2010

8

Calculation for Mobinil’s ARPU by subscriber group and implied call duration

Class % of pop. Income/ month (EGP)

Implied ARPU

(EGP) (a)

Address. pop.

(‘000)(2)

% of total subs(3)

(b)

% of prepaid subs (c)

Min/ month

(4) Min/day

(d)

Postpaid subscribers A+ 2.0% 12,500 192 1,592 2.3% 1,070 35.08 Prepaid Subs A 3.0% 7,500 115 2,388 3% 3.5% 644 21.1 B+ 7.0% 5,000 77 5,571 8% 8.2% 429 14.1 B 15.0% 3,000 46 11,938 17% 18% 257 8.4 B‐ 8.0% 2,000 31 6,367 9% 9% 172 5.6 C 40.0% 625 10 31,834 46% 47% 54 1.8 D 25.0% 300 5 9,948 14% 15% 26 0.8 Weighted average prepaid ARPU = (a2)*(c1)+(a3)*(c2)… 26 Weighted average blended ARPU = (a1)*(b1)+(a2)*(b2)… 30 Average prepaid min/ day = (d2)*(c1)+(d3)*(c2)… 4.8 Average blended min/ day = (d1)*(b1)+(d2)*(b2)… 5.5

Source: AlembicHC Note: (1) Average market postpaid ARPU (2) After subtracting 50% of the D class (3) Includes prepaid and postpaid subscribers (4) Assuming a customer makes only a single call per day and arrived at by dividing the implied ARPU by a flat rate of 18pt

Calculation for VFE’s ARPU by subscriber group and implied call duration

Class % of pop. Income/ month (EGP)

Implied ARPU

(EGP) (a)

Address. pop.

(‘000)(2)

% of total subs

(3)

(b)

% of prepaid subs (c)

Min/ month

(4) Min/day

(d)

Postpaid subscribers A+ 2.0% 12,500

188 1,592 2.3%

941 30.9 A 1.5% 7,500 1,194 1.7% Prepaid subscribers A 1.5% 7,500 136 1,194 2% 1.8% 681 22.3 B+ 7.0% 5,000 91 5,571 8% 8.3% 454 14.9 B 15.0% 3,000 55 11,938 17% 18% 273 8.9 B‐ 8.0% 2,000 36 6,367 9% 10% 182 6.0 C 40.0% 625 11 31,834 46% 48% 57 1.9 D 25.0% 300 5 9,948 14% 15% 27 0.9 Weighted average prepaid ARPU = (a2)*(c1)+(a3)*(c2) 29 Weighted average blended ARPU = (a1)*(b1)+(a2)*(b2) 36 Average prepaid min/day = (d2)*(c1)+(d3)*(c2) 4.8 Average blended min/day = (d1)*(b1)+(d2)*(b2) 5.9

Source: AlembicHC

Note: (1) Average market postpaid ARPU (2) After subtracting 50% of the D class (3) Includes prepaid and postpaid subscribers (4) Assuming a customer makes only a single call per day and arrived at by dividing the implied ARPU by a flat rate of 20pt

We believe our estimates are reasonable since Mobinil’s Al Masry offer is pushing beyond 2 minutes per call and VFE and Mobinil’s Preferred Number offers push beyond 3 minutes per day. Our weighted average prepaid and blended ARPUs are also in line with VFE and Mobinil’s, prepaid ARPU of EGP29 and EGP26 and blended ARPU of EGP36 and EGP30. Based on our calculations, implied MOUs are 178 for VFE and 171 for Mobinil, also consistent with the companies’ reported 3Q10 MOUs of 178 for VFE and 173 for Mobinil.

Sector note Telecoms | Egypt 14 December 2010

9

ARPU call duration among subscriber groups for Mobinil(1)

Source: IMF, AlembicHC

Note: (1) Assuming subscribers make a single call per day

ARPU call duration among subscriber groups for VFE(1)

Source: IMF, AlembicHC

Note: (1) Assuming subscribers make a single call per day

Mobinil targeting net additions by cutting its off‐net rate with Bedoun Sheroot Mobinil’s newest tariff plan cannibalizes its older plan, Al Masry, offering the lowest on‐net minute rate in Egypt of 8pt (see page 6 for tariff plans). With Bedoun Sheroot, a 2 minute call costs 28pt and a 3 minute call costs 42pt. With Al Masry, a 2 minute call costs 36pt and a 3 minute call costs 44pt. Bedoun Sheroot is cheaper for those making calls less than 4 minutes, yet more expensive for calls longer than that. Since we calculated that 60% of Mobinil’s subscribers make calls lasting less than 1 minute and 31 seconds per day, we believe once customers migrate to the plan it will be ARPU dilutive for Mobinil unless subscribers make calls longer than 4 minutes. We find this unlikely since Mobinil tried to push beyond the second minute with Al Masry, which seems to have failed, causing the company to offer a plan that cannibalizes its previous one. The new plan offers a lower off‐net rate of 19pt, matching VFE and Etisalat’s flat rates. While this actually stimulates cross‐net usage, it will compress margins due to interconnect costs.

2%

3%

8%

17%9%

46%14%

(50)

‐

50

100

150

200

250

(2) ‐ 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34

ARPU (EG

P)

Call duration (minutes) % of Total Subs

4%

2%

8%

17%9%

46%14%

(50)

‐

50

100

150

200

250

(2) ‐ 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34

ARPU (EG

P)

Call duration (minutes) Series1

Weighted avg. ARPU = EGP8

Calc. prepaid ARPU = EGP26

Calc. blended ARPU = EGP30

% of total subscribers

Weighted avg. ARPU = EGP10

Calc. prepaid ARPU = EGP29

Calc. blended ARPU = EGP36

% of total subscribers

Sector note Telecoms | Egypt 14 December 2010

10

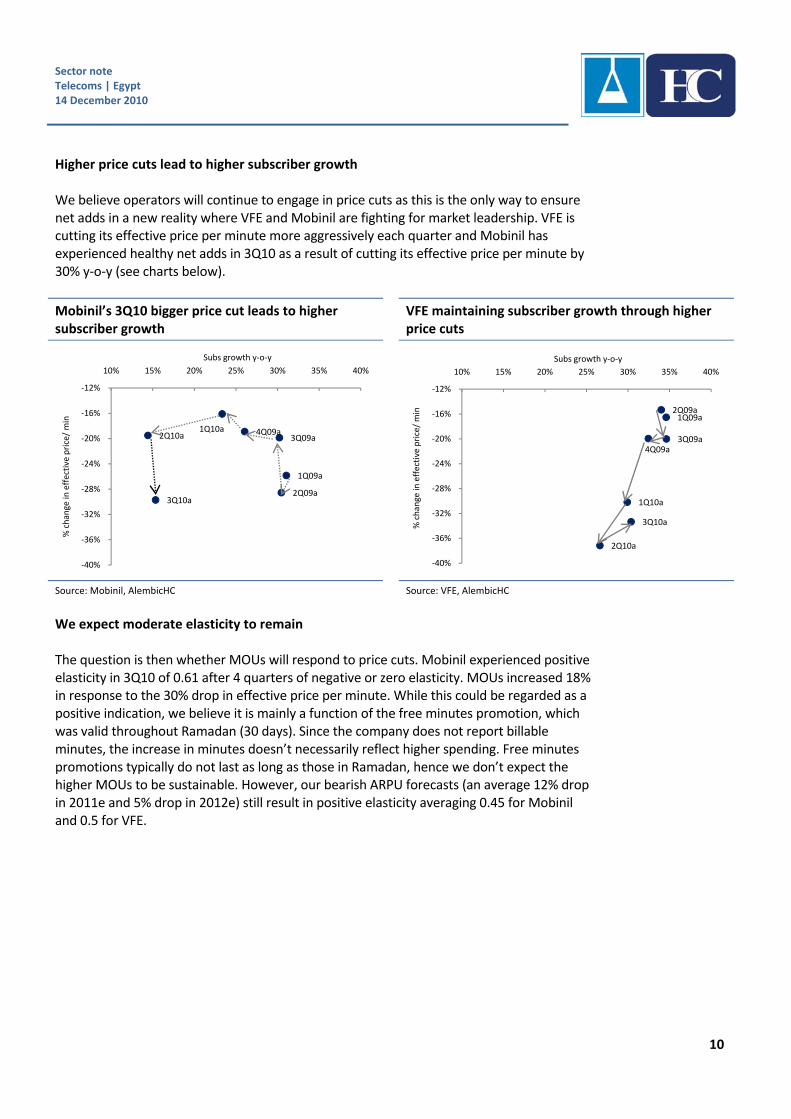

Higher price cuts lead to higher subscriber growth We believe operators will continue to engage in price cuts as this is the only way to ensure net adds in a new reality where VFE and Mobinil are fighting for market leadership. VFE is cutting its effective price per minute more aggressively each quarter and Mobinil has experienced healthy net adds in 3Q10 as a result of cutting its effective price per minute by 30% y‐o‐y (see charts below).

Mobinil’s 3Q10 bigger price cut leads to higher subscriber growth

VFE maintaining subscriber growth through higher price cuts

Source: Mobinil, AlembicHC Source: VFE, AlembicHC

We expect moderate elasticity to remain The question is then whether MOUs will respond to price cuts. Mobinil experienced positive elasticity in 3Q10 of 0.61 after 4 quarters of negative or zero elasticity. MOUs increased 18% in response to the 30% drop in effective price per minute. While this could be regarded as a positive indication, we believe it is mainly a function of the free minutes promotion, which was valid throughout Ramadan (30 days). Since the company does not report billable minutes, the increase in minutes doesn’t necessarily reflect higher spending. Free minutes promotions typically do not last as long as those in Ramadan, hence we don’t expect the higher MOUs to be sustainable. However, our bearish ARPU forecasts (an average 12% drop in 2011e and 5% drop in 2012e) still result in positive elasticity averaging 0.45 for Mobinil and 0.5 for VFE.

1Q09a

2Q09a

3Q09a4Q09a1Q10a

2Q10a

3Q10a

‐40%

‐36%

‐32%

‐28%

‐24%

‐20%

‐16%

‐12%

10% 15% 20% 25% 30% 35% 40%

% change in

effective price/ min

Subs growth y‐o‐y

1Q09a2Q09a

3Q09a4Q09a

1Q10a

2Q10a

3Q10a

‐40%

‐36%

‐32%

‐28%

‐24%

‐20%

‐16%

‐12%

10% 15% 20% 25% 30% 35% 40%

% change in

effective price/ min

Subs growth y‐o‐y

Sector note Telecoms | Egypt 14 December 2010

11

Mobinil: Usage vs effective price/minute Vodafone: Usage vs effective price/minute

Source: Mobinil, AlembicHC Source: VFE, AlembicHC

Mobinil and VFE’s forecasted (4Q10e–4Q11e) MOUs, effective price/minute (EGP), and elasticity

Mobinil VFE

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11

MOUs 141 159 173 161 165 167 188 168 159 179 178 172 181 201 200 192 Ef. price/min 0.22 0.19 0.18 0.18 0.16 0.16 0.14 0.15 0.24 0.20 0.20 0.20 0.17 0.16 0.15 0.16 Elasticity ‐0.21 ‐0.23 0.61 0.63 0.67 0.28 0.41 0.25 0.31 0.60 0.51 0.51 0.48 0.51 0.51 0.51

Source: Mobinil, Vodafone Group, AlembicHC

Tariffs to drop as SIM penetration increases

Egypt’s mobile tariffs are relatively high compared to other emerging markets. We carried out an exercise using ITU ICT basket data and concluded that Egypt’s tariff basket as measured by ITU is 23% higher than it should be compared to other countries. The mobile tariff basket represents the price of standard monthly usage in USD for 25 outgoing calls per month (on net, off net, and to a fixed line, and for peak, off‐peak, and weekends according to predetermined ratios) and 30 SMS messages. The basket is based on 2H09 prepaid tariffs since they represent the dominant payment method. The basket is then divided by GNI per capita to ensure comparability between countries. We use the chart below only as an indication for tariff trend.

Relative mobile tariff baskets (USD) vs penetration rates for emerging markets

Source: ITU, AlembicHC

‐40%

‐30%

‐20%

‐10%

0%

10%

20%

30%

Mar‐09

Jun‐09

Sep‐09

Dec‐09

Mar‐10

Jun‐10

Sep‐10

Dec‐10

Mar‐11

Jun‐11

Sep‐11

Dec‐11

Change in usage y‐o‐y Change in effective price/ min y‐o‐y

‐40%

‐30%

‐20%

‐10%

0%

10%

20%

30%

Mar‐09

Jun‐09

Sep‐09

Dec‐09

Mar‐10

Jun‐10

Sep‐10

Dec‐10

Mar‐11

Jun‐11

Sep‐11

Dec‐11

% Change in effective price/ min y‐o‐y % Change in usage y‐o‐y

Bahrain

Brazil

ChileChina

Colombia

Czech Repupblic

Egypt in 2009a

HungaryIndiaIndonesia

IsraelKoreaMalaysia

Mexico

Peru

Philippines

Poland Russia

Slovenia

South Africa

Thailand

Turkey

2010e 2011e2012e

0

1

2

3

4

5

6

40% 60% 80% 100% 120% 140% 160% 180% 200%

ITU basket/ GNI

Sector note Telecoms | Egypt 14 December 2010

12

Our exercise implies an inverse relationship between penetration rates and tariffs, which is consistent with lower incremental ARPU as a result of acquiring more lower‐income subscribers. Applying our forecasted penetration rate for Egypt of 92% in 2010e, 102% in 2011e, and 106% in 2012e yields a basket/GNI per capita of 1.9%, 1.8%, and 1.7% respectively, implying a drop of 8% in 2011e and 4% in 2012e. VFE and Etisalat launched per second billing, Mobinil not competing

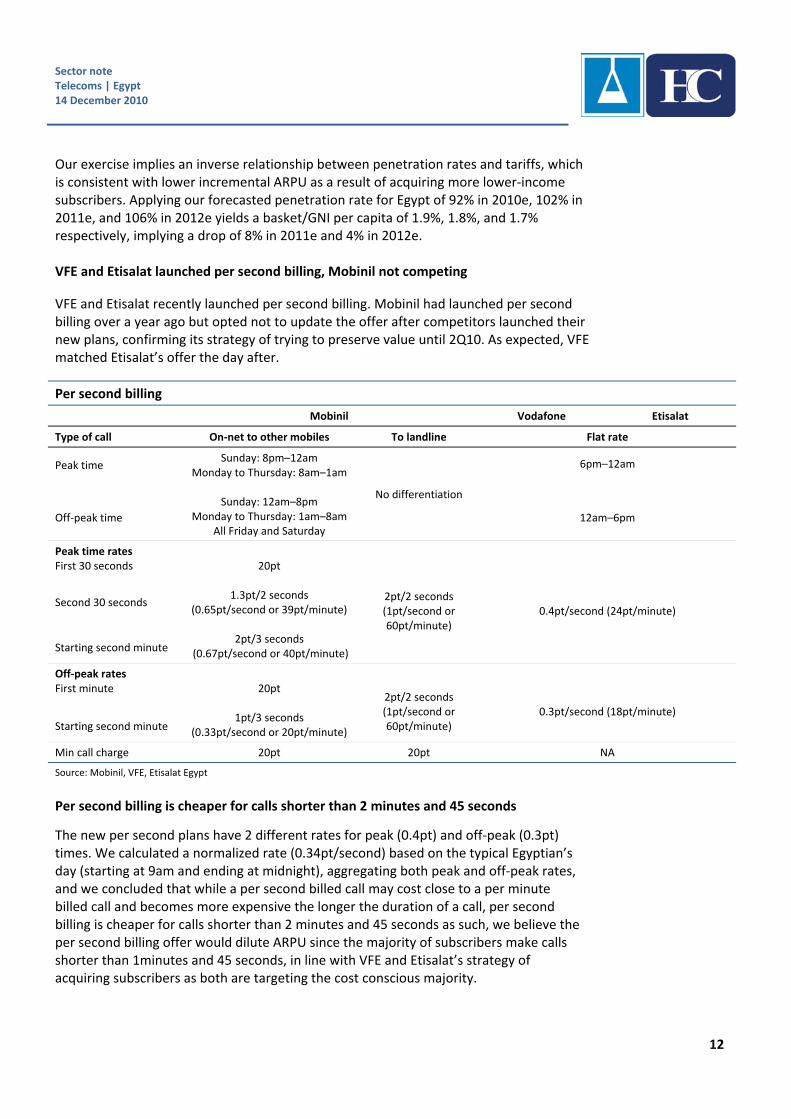

VFE and Etisalat recently launched per second billing. Mobinil had launched per second billing over a year ago but opted not to update the offer after competitors launched their new plans, confirming its strategy of trying to preserve value until 2Q10. As expected, VFE matched Etisalat’s offer the day after.

Per second billing

Mobinil Vodafone Etisalat

Type of call On‐net to other mobiles To landline Flat rate

Peak time Sunday: 8pm–12am

Monday to Thursday: 8am–1am

No differentiation

6pm–12am

Off‐peak time

Sunday: 12am–8pm Monday to Thursday: 1am–8am

All Friday and Saturday 12am–6pm

Peak time rates First 30 seconds 20pt

2pt/2 seconds (1pt/second or 60pt/minute)

0.4pt/second (24pt/minute)

Second 30 seconds 1.3pt/2 seconds

(0.65pt/second or 39pt/minute)

Starting second minute 2pt/3 seconds

(0.67pt/second or 40pt/minute)

Off‐peak rates First minute 20pt

2pt/2 seconds (1pt/second or 60pt/minute)

0.3pt/second (18pt/minute)

Starting second minute 1pt/3 seconds

(0.33pt/second or 20pt/minute)

Min call charge 20pt 20pt NA

Source: Mobinil, VFE, Etisalat Egypt

Per second billing is cheaper for calls shorter than 2 minutes and 45 seconds

The new per second plans have 2 different rates for peak (0.4pt) and off‐peak (0.3pt) times. We calculated a normalized rate (0.34pt/second) based on the typical Egyptian’s day (starting at 9am and ending at midnight), aggregating both peak and off‐peak rates, and we concluded that while a per second billed call may cost close to a per minute billed call and becomes more expensive the longer the duration of a call, per second billing is cheaper for calls shorter than 2 minutes and 45 seconds as such, we believe the per second billing offer would dilute ARPU since the majority of subscribers make calls shorter than 1minutes and 45 seconds, in line with VFE and Etisalat’s strategy of acquiring subscribers as both are targeting the cost conscious majority.

Sector note Telecoms | Egypt 14 December 2010

13

VFE and Etisalat’s per‐second billing for a 20 minute call

Source: Mobinil, VFE, Etisalat Egypt, AlembicHC Note: (1) Assumes a day constitutes 9 off‐peak and 7 peak hours

VFE and Etisalat’s per‐second billing for a 5 minute call

Source: Mobinil, VFE, Etisalat Egypt, AlembicHC Note: (1) Assumes a day constitutes 9 off‐peak and 7 peak hours

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

Call cost (EG

P)

Call duration (min)

Per‐second peak rate Per‐second off peak rate Per‐second normalized rate (1) Minute rate

0

20

40

60

80

100

120

1 2 3 4 5

Call cost (pt)

Call duration (min)

Per‐second peak rate Per‐second off peak rate Per‐second normalized rate (1) Minute rate

Peak rate starts becoming more expensive

Before this point the normalized rate is always cheaper

Sector note Telecoms | Egypt 14 December 2010

14

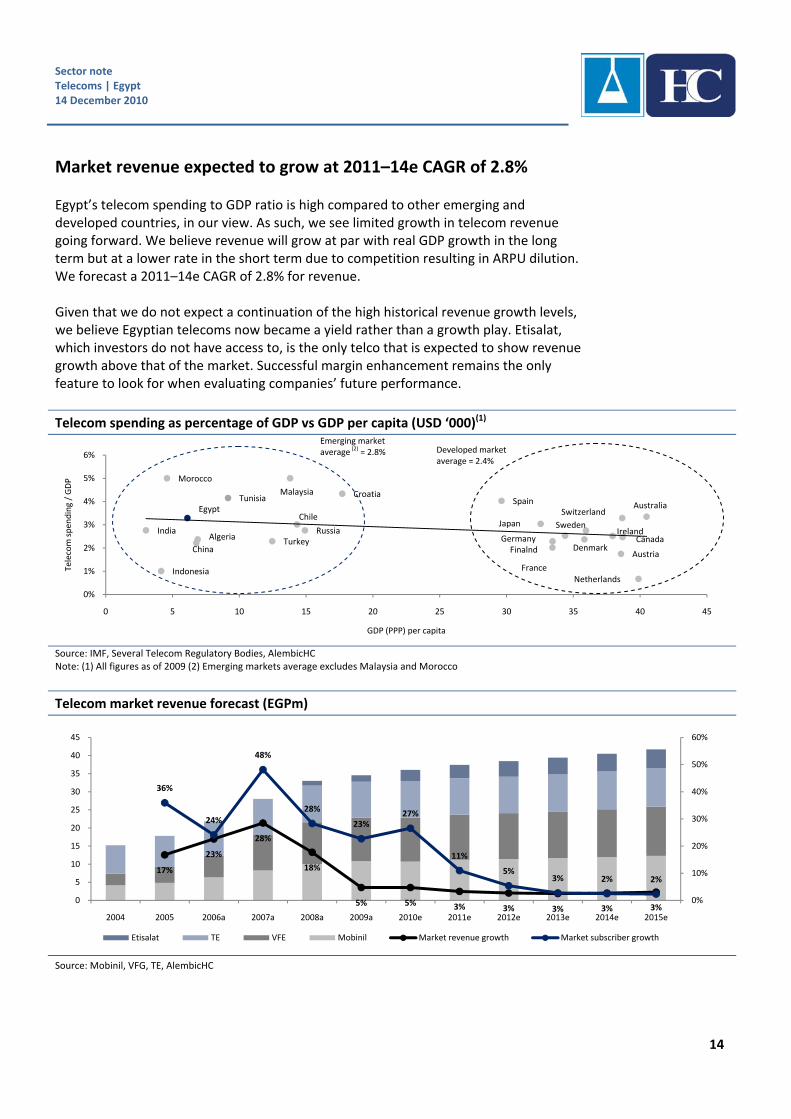

Market revenue expected to grow at 2011–14e CAGR of 2.8% Egypt’s telecom spending to GDP ratio is high compared to other emerging and developed countries, in our view. As such, we see limited growth in telecom revenue going forward. We believe revenue will grow at par with real GDP growth in the long term but at a lower rate in the short term due to competition resulting in ARPU dilution. We forecast a 2011–14e CAGR of 2.8% for revenue. Given that we do not expect a continuation of the high historical revenue growth levels, we believe Egyptian telecoms now became a yield rather than a growth play. Etisalat, which investors do not have access to, is the only telco that is expected to show revenue growth above that of the market. Successful margin enhancement remains the only feature to look for when evaluating companies’ future performance.

Telecom spending as percentage of GDP vs GDP per capita (USD ‘000)(1)

Source: IMF, Several Telecom Regulatory Bodies, AlembicHC Note: (1) All figures as of 2009 (2) Emerging markets average excludes Malaysia and Morocco

Telecom market revenue forecast (EGPm)

Source: Mobinil, VFG, TE, AlembicHC

Egypt

India

China

Indonesia

Chile

Turkey

Malaysia

Russia

Morocco

Algeria

Tunisia CroatiaAustralia

FinalndCanada

Ireland

Netherlands

Sweden

France

SwitzerlandJapan

Austria

Germany

Spain

Denmark

0%

1%

2%

3%

4%

5%

6%

0 5 10 15 20 25 30 35 40 45

Telecom spen

ding / GDP

GDP (PPP) per capita

17%

23%

28%

18%

5% 5% 3% 3% 3% 3% 3%

36%

24%

48%

28%

23%27%

11%

5%3% 2% 2%

0%

10%

20%

30%

40%

50%

60%

0

5

10

15

20

25

30

35

40

45

2004 2005 2006a 2007a 2008a 2009a 2010e 2011e 2012e 2013e 2014e 2015e

Etisalat TE VFE Mobinil Market revenue growth Market subscriber growth

Emerging market average (2) = 2.8% Developed market

average = 2.4%

Mobinil Telecoms | Egypt 14 December 2010

15

Mobinil

Subscriber growth at a high price Mobinil’s return to the subscriber acquisition game comes at the expense of

profitability, subscribers forecast to grow at a 2011–14e CAGR of 4.4%

Reconsider Mobinil by the end of next year, EPS expected to drop 30% y‐o‐y in 4Q10e and to remain flat in 2011e, while we forecast a dividend yield of 4.3% in 2010e and 5.8% in 2011e

We cut our TP 17% to EGP179.6/share and maintain our Neutral recommendation Limited subscriber growth going forward We believe subscriber growth should be limited going forward (2011–14e CAGR of 4.4%) given our expectations of limited market growth (real penetration of 95% in 2010e). ARPU dilution is expected to continue (2011–14e CAGR of ‐4%) as Mobinil is back in the subscriber acquisition fight, with operators competing for existing subscribers leading to increasing dual SIMs. The full consolidation of LINKdotNET will take place in 2011e and as such we expect revenue growth of 5.0% versus only 2.4% for the mobile segment. Profitability is expected to come under pressure until pricing stabilizes in 2012e. We forecast a 2011–14e CAGR of 2.7% for revenue and 3.0% for EBITDA. Operational pressures in 2010e and high expected CAPEX in 2011e lead to lower yields Mobinil’s EPS is expected to drop 30% in 2010e as a result of margin compression. Improvement in revenue is not expected to filter through to the bottom line in 2011e due to 11% higher interest cost leading to a flat EPS. FCF is expected to be negative in 2010e as a result of EBITDA dropping 15% and license payments, while 2011e FCF is expected to be pressured by increased CAPEX. We therefore assume a 50% dividend payout for 2010e, a yield of 4.3%, and expect the payout to increase to 70% in 2011e due to lower operational pressures, which would result in a 5.8% yield.

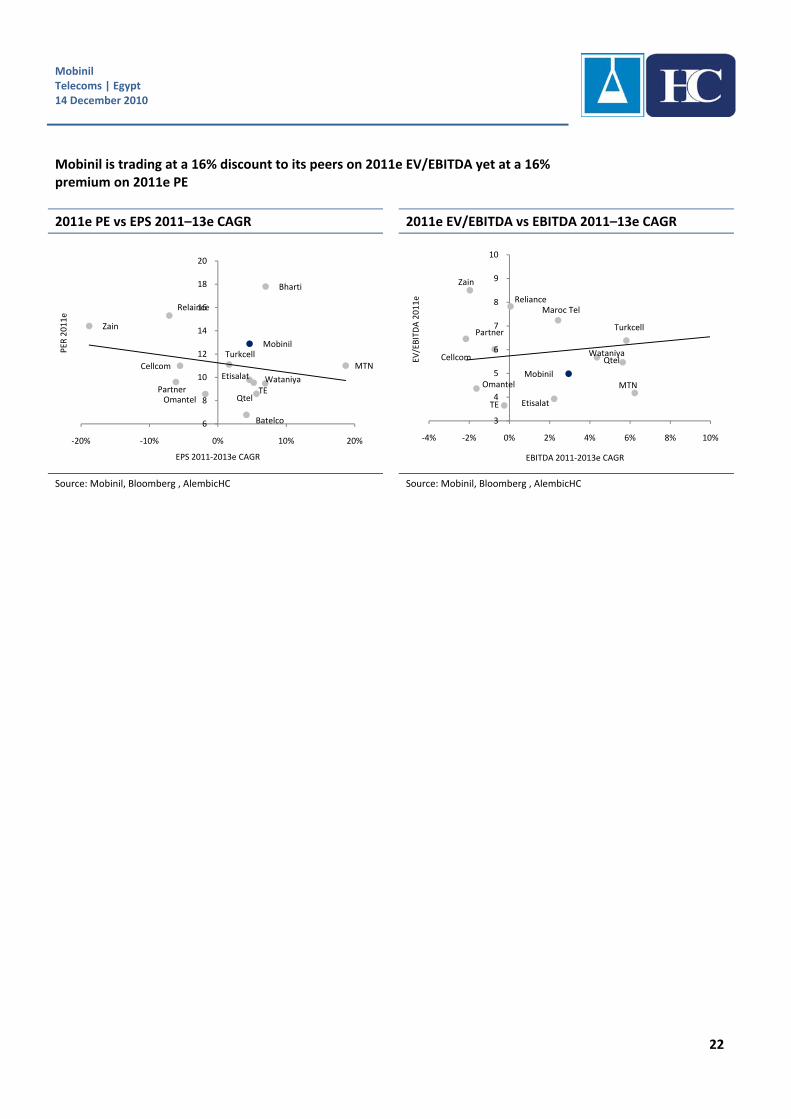

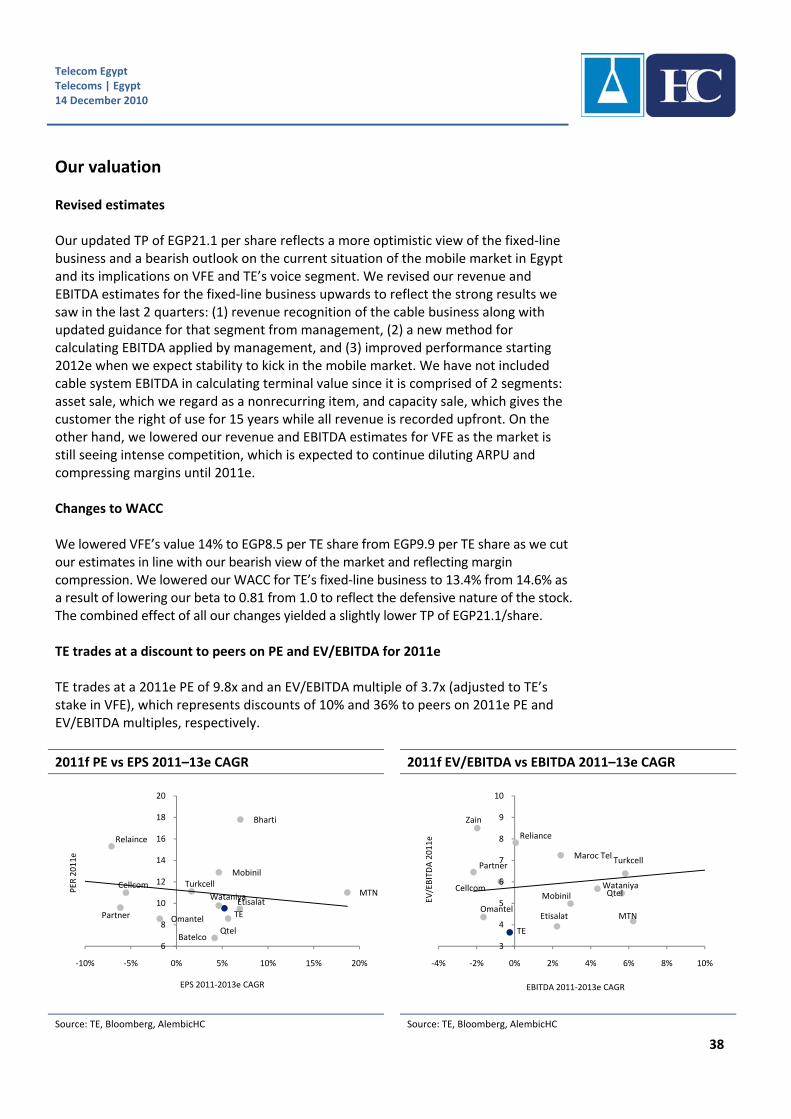

Paradigm shift confirmed Our view on Mobinil in our previous note Signs of a paradigm shift (29 April 2010) has been confirmed by 2Q10 and 3Q10. We cut our TP to reflect slower market growth, delaying market stability to 2012e, factoring in margin compression and higher interest expense. The stock is trading at a 16% premium on 2011e PE although it trades at a 16% discount to peers on 2011e EV/EBITDA. We still don’t view the discount as sufficiently attractive.

Mobinil Telecoms | Egypt 14 December 2010

16

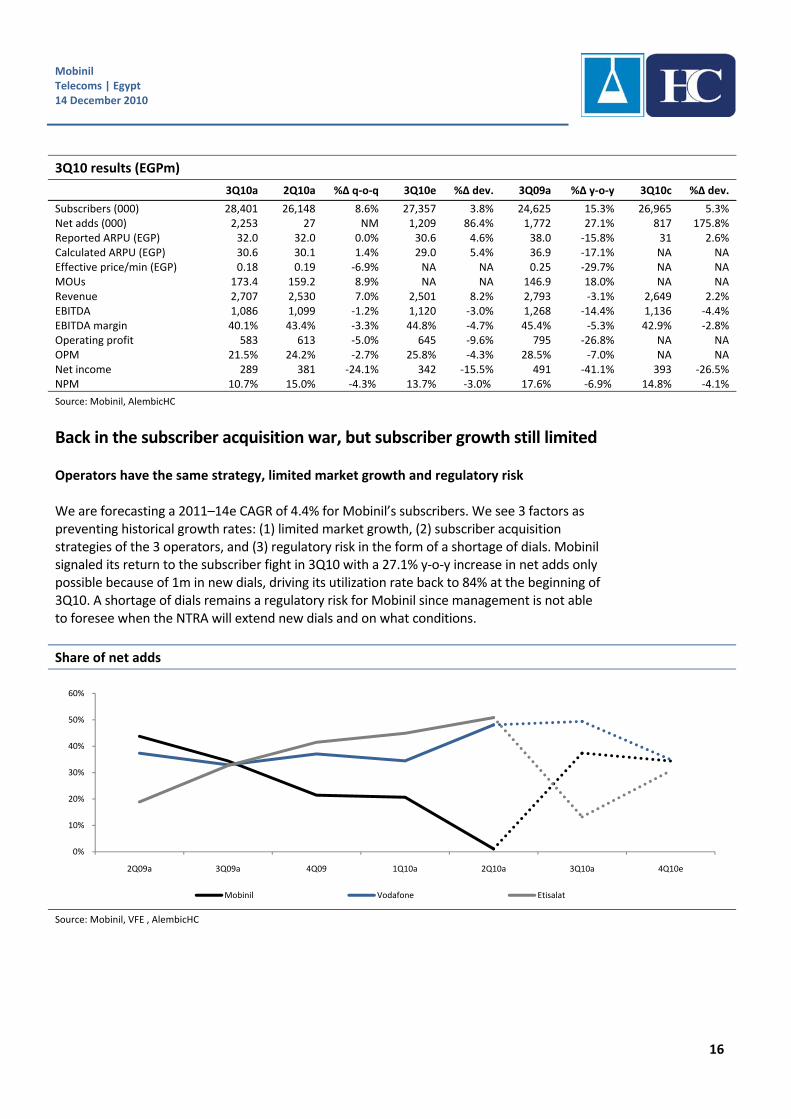

3Q10 results (EGPm)

3Q10a 2Q10a %Δ q‐o‐q 3Q10e %Δ dev. 3Q09a %∆ y‐o‐y 3Q10c %Δ dev.

Subscribers (000) 28,401 26,148 8.6% 27,357 3.8% 24,625 15.3% 26,965 5.3% Net adds (000) 2,253 27 NM 1,209 86.4% 1,772 27.1% 817 175.8% Reported ARPU (EGP) 32.0 32.0 0.0% 30.6 4.6% 38.0 ‐15.8% 31 2.6% Calculated ARPU (EGP) 30.6 30.1 1.4% 29.0 5.4% 36.9 ‐17.1% NA NA Effective price/min (EGP) 0.18 0.19 ‐6.9% NA NA 0.25 ‐29.7% NA NA MOUs 173.4 159.2 8.9% NA NA 146.9 18.0% NA NA Revenue 2,707 2,530 7.0% 2,501 8.2% 2,793 ‐3.1% 2,649 2.2% EBITDA 1,086 1,099 ‐1.2% 1,120 ‐3.0% 1,268 ‐14.4% 1,136 ‐4.4% EBITDA margin 40.1% 43.4% ‐3.3% 44.8% ‐4.7% 45.4% ‐5.3% 42.9% ‐2.8% Operating profit 583 613 ‐5.0% 645 ‐9.6% 795 ‐26.8% NA NA OPM 21.5% 24.2% ‐2.7% 25.8% ‐4.3% 28.5% ‐7.0% NA NA Net income 289 381 ‐24.1% 342 ‐15.5% 491 ‐41.1% 393 ‐26.5% NPM 10.7% 15.0% ‐4.3% 13.7% ‐3.0% 17.6% ‐6.9% 14.8% ‐4.1%

Source: Mobinil, AlembicHC

Back in the subscriber acquisition war, but subscriber growth still limited Operators have the same strategy, limited market growth and regulatory risk We are forecasting a 2011–14e CAGR of 4.4% for Mobinil’s subscribers. We see 3 factors as preventing historical growth rates: (1) limited market growth, (2) subscriber acquisition strategies of the 3 operators, and (3) regulatory risk in the form of a shortage of dials. Mobinil signaled its return to the subscriber fight in 3Q10 with a 27.1% y‐o‐y increase in net adds only possible because of 1m in new dials, driving its utilization rate back to 84% at the beginning of 3Q10. A shortage of dials remains a regulatory risk for Mobinil since management is not able to foresee when the NTRA will extend new dials and on what conditions.

Share of net adds

Source: Mobinil, VFE , AlembicHC

0%

10%

20%

30%

40%

50%

60%

2Q09a 3Q09a 4Q09 1Q10a 2Q10a 3Q10a 4Q10e

Mobinil Vodafone Etisalat

Mobinil Telecoms | Egypt 14 December 2010

17

Operational efficiency to determine the success of operators in the short term

We believe Mobinil and VFE will most probably lose market share to Etisalat equally in the long term as we believe Mobinil and VFE should reach about the same utilization rate (89%, 90%) and would therefore put both in the same competitive position. It will be a matter of which operator has the operational efficiency to manage its existing dials, recycle old dials in a timely manner, make use of special algorithms, and manage dials allocated to roaming partners. Mobinil was able to increase its operational efficiency in 3Q10 – in 1Q10 it had the same utilization rate and added only 767,000 subscribers. We expect the company to add another 1.9m in 4Q10e with the activation of 1m dials in October and an additional 2m to activate this year. This way of looking at the market puts VFE in the lead but only slightly with a market share just 0.5% higher than Mobinil.

Market share and subscriber growth (quarterly) Market share and subscriber growth (annual)

Source: Mobinil press releases, AlembicHC Source: Mobinil press releases, AlembicHC

ARPU dilution driven by collective acquisition strategy and increase in dual SIMs in light of market maturity

Subscriber growth remains the source of revenue growth in Egypt as usage does not respond well to moderate price cuts. This was demonstrated by Mobinil in 1H10 when it cut its effective price per minute more cautiously and, as a result, saw 2 quarters of inelasticity. Realizing that usage only responds to aggressive cuts and having more dials on hand, Mobinil cut its effective price per minute 29.7% y‐o‐y in 3Q10, up from an average 18.6% in the previous year, and was consequently able to stimulate usage (MOUs increased an impressive 18% y‐o‐y). Its Bedoun Sheroot offer also indicates that it plans to continue competing on pricing. VFE on the other hand has been experiencing 3 quarters of positive elasticity as it is increasing its price cut each quarter. We believe that at current market maturity level, operators will continue cutting prices as they vie for each others’ subscribers. The increase in dual SIMs is going to put additional pressure on ARPU as subscribers divide their spending wallet on different operators.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2Q09a 3Q09a 4Q09 1Q10a 2Q10a 3Q10a 4Q10e

Marke share Utilization rate Subs growth y‐o‐y

0%

10%

20%

30%

40%

50%

60%

70%

2007a 2008a 2009a 2010e 2011e 2012e 2013e 2014e

Marke share Subs growth (y‐o‐y)

Mobinil Telecoms | Egypt 14 December 2010

18

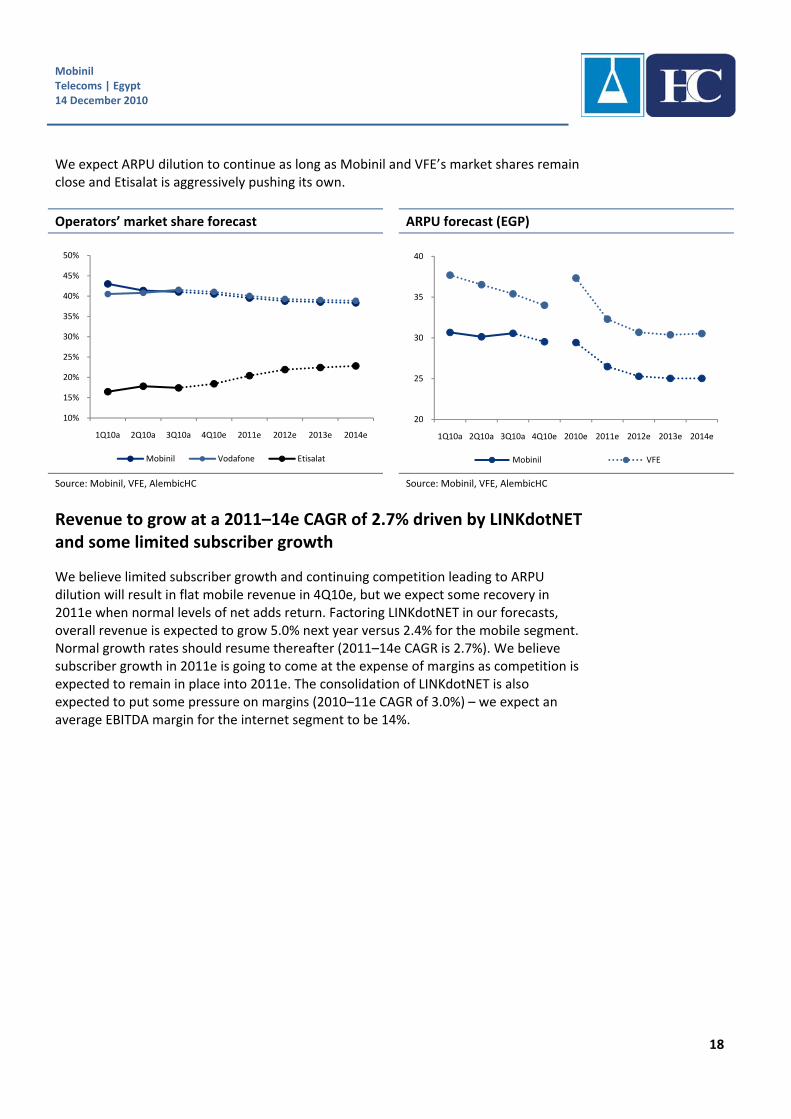

We expect ARPU dilution to continue as long as Mobinil and VFE’s market shares remain close and Etisalat is aggressively pushing its own.

Operators’ market share forecast ARPU forecast (EGP)

Source: Mobinil, VFE, AlembicHC Source: Mobinil, VFE, AlembicHC

Revenue to grow at a 2011–14e CAGR of 2.7% driven by LINKdotNET and some limited subscriber growth

We believe limited subscriber growth and continuing competition leading to ARPU dilution will result in flat mobile revenue in 4Q10e, but we expect some recovery in 2011e when normal levels of net adds return. Factoring LINKdotNET in our forecasts, overall revenue is expected to grow 5.0% next year versus 2.4% for the mobile segment. Normal growth rates should resume thereafter (2011–14e CAGR is 2.7%). We believe subscriber growth in 2011e is going to come at the expense of margins as competition is expected to remain in place into 2011e. The consolidation of LINKdotNET is also expected to put some pressure on margins (2010–11e CAGR of 3.0%) – we expect an average EBITDA margin for the internet segment to be 14%.

10%

15%

20%

25%

30%

35%

40%

45%

50%

1Q10a 2Q10a 3Q10a 4Q10e 2011e 2012e 2013e 2014e

Mobinil Vodafone Etisalat

20

25

30

35

40

1Q10a 2Q10a 3Q10a 4Q10e 2010e 2011e 2012e 2013e 2014e

Mobinil VFE

Mobinil Telecoms | Egypt 14 December 2010

19

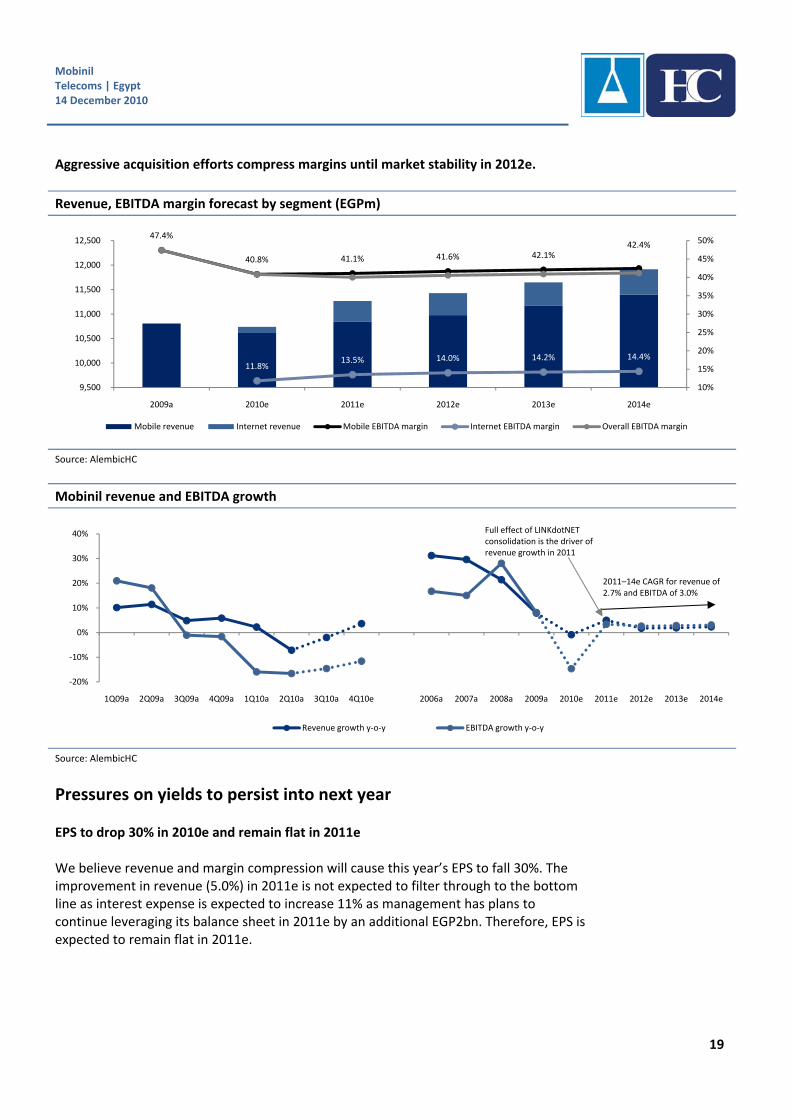

Aggressive acquisition efforts compress margins until market stability in 2012e.

Revenue, EBITDA margin forecast by segment (EGPm)

Source: AlembicHC

Mobinil revenue and EBITDA growth

Source: AlembicHC

Pressures on yields to persist into next year EPS to drop 30% in 2010e and remain flat in 2011e We believe revenue and margin compression will cause this year’s EPS to fall 30%. The improvement in revenue (5.0%) in 2011e is not expected to filter through to the bottom line as interest expense is expected to increase 11% as management has plans to continue leveraging its balance sheet in 2011e by an additional EGP2bn. Therefore, EPS is expected to remain flat in 2011e.

47.4%

40.8% 41.1% 41.6% 42.1%42.4%

11.8%13.5% 14.0% 14.2% 14.4%

10%

15%

20%

25%

30%

35%

40%

45%

50%

9,500

10,000

10,500

11,000

11,500

12,000

12,500

2009a 2010e 2011e 2012e 2013e 2014e

Mobile revenue Internet revenue Mobile EBITDA margin Internet EBITDA margin Overall EBITDA margin

‐20%

‐10%

0%

10%

20%

30%

40%

1Q09a 2Q09a 3Q09a 4Q09a 1Q10a 2Q10a 3Q10a 4Q10e 2006a 2007a 2008a 2009a 2010e 2011e 2012e 2013e 2014e

Revenue growth y‐o‐y EBITDA growth y‐o‐y

Full effect of LINKdotNET consolidation is the driver of revenue growth in 2011

2011–14e CAGR for revenue of 2.7% and EBITDA of 3.0%

Mobinil Telecoms | Egypt 14 December 2010

20

Debt accumulation until 2011e will put additional pressure on the bottom line (EGPm)

Source: Mobinil, AlembicHC

EPS (EGP) and EPS growth

Source: Mobinil, AlembicHC

Unattractive FCF and dividend yield in 2010e and 2011e FCF is expected to be negative this year given our forecast of 15% drop in EBITDA along with EGP1.85bn in license payments (of which EGP1.1bn expected to be made in 4Q10e). FCF in 2011e is expected to be pressured (FCF yield of 3.0%) by additional CAPEX (20% of sales versus 16% in 2010e) as we expect normal levels of CAPEX to resume after the company saved on CAPEX in 2010e to be able to make license payments and purchase LINKdotNET. As such, we assumed a dividend payout of 50% for 2010e (in line with 2009), leading to a dividend yield of 4.3%, and expect the payout to increase to 70% in 2011e as operational pressures recede, which will however still result in a 5.8% yield. We believe investors should consider Mobinil again by the end of next year when we expect operational recovery, and according to our estimates FCF yield reaches 9.6%, with dividend yield of 6.6% by 2012e.

25% 25%

22%

17%

24% 25%

32%

25%

6%5%

20%

22%

26%

30%28%

24%

20%

0%

5%

10%

15%

20%

25%

30%

35%

0

2,000

4,000

6,000

8,000

10,000

12,000

1Q08a 2Q08a 3Q08a 4Q08a 1Q10a 2Q10a 3Q10a 4Q10e 2006a 2007a 2008a 2009a 2010e 2011e 2012e 2013e 2014e

Total deb

t

Total debt Interest expense as % of EBIT

12%

5% 5%

‐30%

‐2%

6%10% 10%

‐35%

‐25%

‐15%

‐5%

5%

15%

25%

35%

0

2

4

6

8

10

12

14

16

18

20

2007a 2008a 2009a 2010e 2011e 2012e 2013e 2014e

EPS EPS growth

Exceptionally high due to USD60m of forex losses

Mobinil Telecoms | Egypt 14 December 2010

21

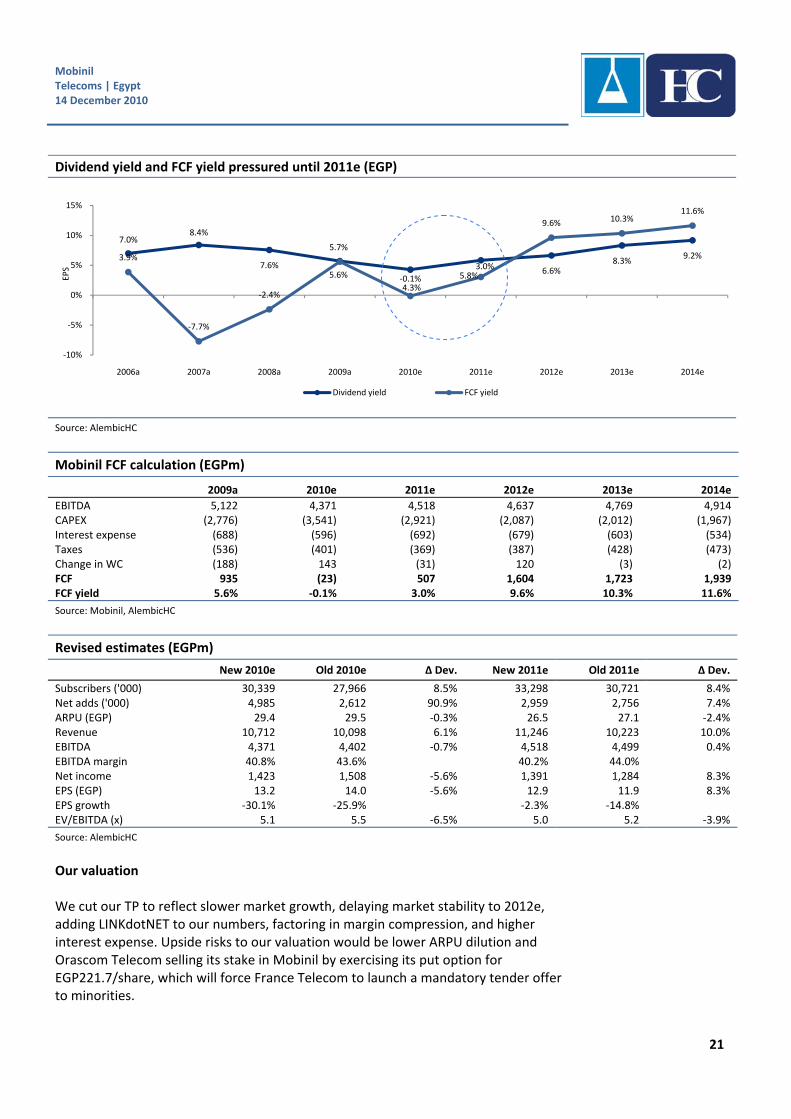

Dividend yield and FCF yield pressured until 2011e (EGP)

Source: AlembicHC

Mobinil FCF calculation (EGPm)

2009a 2010e 2011e 2012e 2013e 2014e

EBITDA 5,122 4,371 4,518 4,637 4,769 4,914 CAPEX (2,776) (3,541) (2,921) (2,087) (2,012) (1,967) Interest expense (688) (596) (692) (679) (603) (534) Taxes (536) (401) (369) (387) (428) (473) Change in WC (188) 143 (31) 120 (3) (2) FCF 935 (23) 507 1,604 1,723 1,939 FCF yield 5.6% ‐0.1% 3.0% 9.6% 10.3% 11.6%

Source: Mobinil, AlembicHC

Revised estimates (EGPm)

New 2010e Old 2010e ∆ Dev. New 2011e Old 2011e ∆ Dev.

Subscribers ('000) 30,339 27,966 8.5% 33,298 30,721 8.4% Net adds ('000) 4,985 2,612 90.9% 2,959 2,756 7.4% ARPU (EGP) 29.4 29.5 ‐0.3% 26.5 27.1 ‐2.4% Revenue 10,712 10,098 6.1% 11,246 10,223 10.0% EBITDA 4,371 4,402 ‐0.7% 4,518 4,499 0.4% EBITDA margin 40.8% 43.6% 40.2% 44.0% Net income 1,423 1,508 ‐5.6% 1,391 1,284 8.3% EPS (EGP) 13.2 14.0 ‐5.6% 12.9 11.9 8.3% EPS growth ‐30.1% ‐25.9% ‐2.3% ‐14.8% EV/EBITDA (x) 5.1 5.5 ‐6.5% 5.0 5.2 ‐3.9%

Source: AlembicHC

Our valuation We cut our TP to reflect slower market growth, delaying market stability to 2012e, adding LINKdotNET to our numbers, factoring in margin compression, and higher interest expense. Upside risks to our valuation would be lower ARPU dilution and Orascom Telecom selling its stake in Mobinil by exercising its put option for EGP221.7/share, which will force France Telecom to launch a mandatory tender offer to minorities.

7.0%8.4%

7.6%

5.7%

4.3%

5.8%6.6%

8.3%9.2%3.9%

‐7.7%

‐2.4%

5.6% ‐0.1%

3.0%

9.6% 10.3%11.6%

‐10%

‐5%

0%

5%

10%

15%

2006a 2007a 2008a 2009a 2010e 2011e 2012e 2013e 2014e

EPS

Dividend yield FCF yield

Mobinil Telecoms | Egypt 14 December 2010

22

Mobinil is trading at a 16% discount to its peers on 2011e EV/EBITDA yet at a 16% premium on 2011e PE

2011e PE vs EPS 2011–13e CAGR 2011e EV/EBITDA vs EBITDA 2011–13e CAGR

Source: Mobinil, Bloomberg , AlembicHC Source: Mobinil, Bloomberg , AlembicHC

TE

Zain

Wataniya

Qtel

MTN

Bharti

Mobinil

Batelco

Omantel

Relaince

Partner

Cellcom

Turkcell

Etisalat

6

8

10

12

14

16

18

20

‐20% ‐10% 0% 10% 20%

PER

2011e

EPS 2011‐2013e CAGR

TE

Maroc Tel

Zain

WataniyaQtel

MTN Mobinil

Omantel

Reliance

Cellcom

PartnerTurkcell

Etisalat

3

4

5

6

7

8

9

10

‐4% ‐2% 0% 2% 4% 6% 8% 10%

EV/EBITDA 2011e

EBITDA 2011‐2013e CAGR

Mobinil Telecoms | Egypt 14 December 2010

23

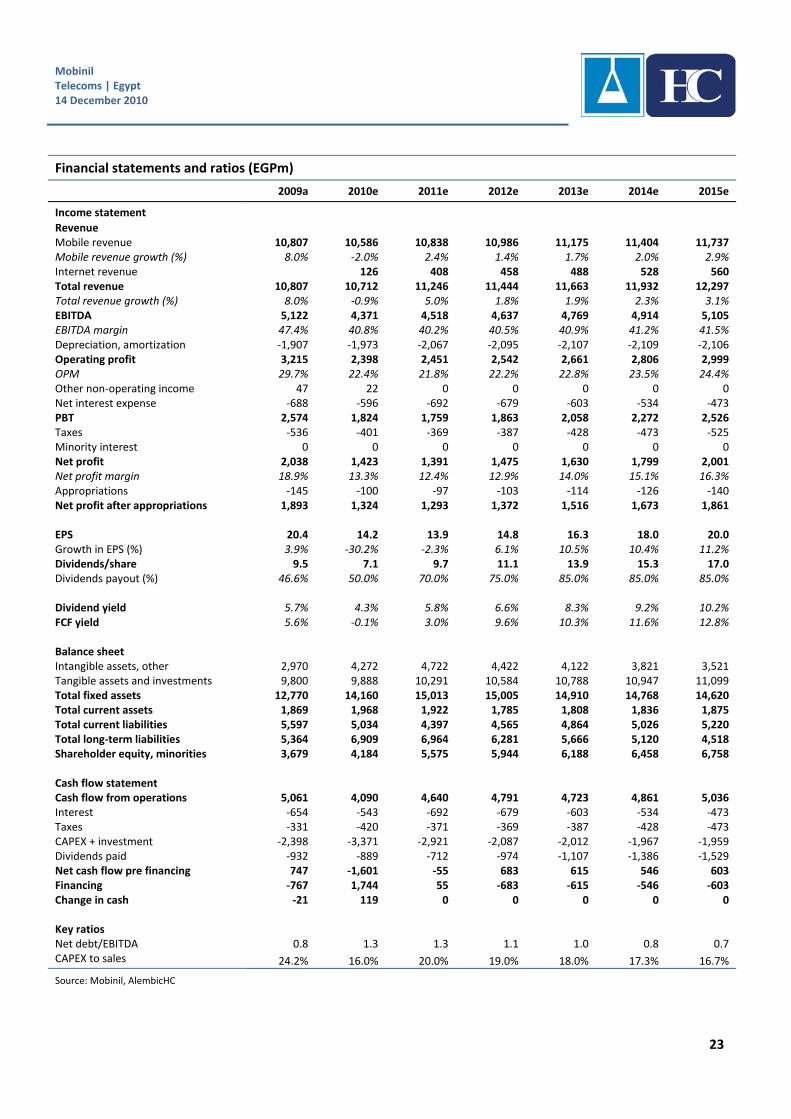

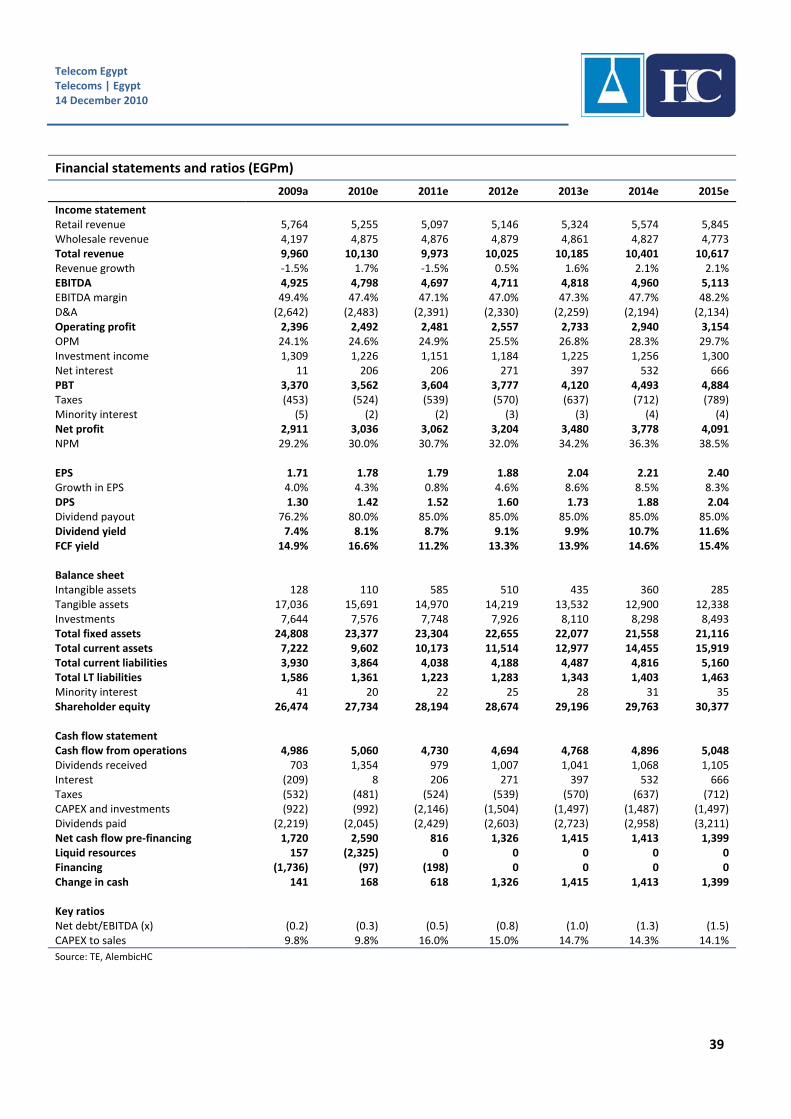

Financial statements and ratios (EGPm)

2009a 2010e 2011e 2012e 2013e 2014e 2015e

Income statement Revenue Mobile revenue 10,807 10,586 10,838 10,986 11,175 11,404 11,737 Mobile revenue growth (%) 8.0% ‐2.0% 2.4% 1.4% 1.7% 2.0% 2.9% Internet revenue 126 408 458 488 528 560 Total revenue 10,807 10,712 11,246 11,444 11,663 11,932 12,297 Total revenue growth (%) 8.0% ‐0.9% 5.0% 1.8% 1.9% 2.3% 3.1% EBITDA 5,122 4,371 4,518 4,637 4,769 4,914 5,105 EBITDA margin 47.4% 40.8% 40.2% 40.5% 40.9% 41.2% 41.5% Depreciation, amortization ‐1,907 ‐1,973 ‐2,067 ‐2,095 ‐2,107 ‐2,109 ‐2,106 Operating profit 3,215 2,398 2,451 2,542 2,661 2,806 2,999 OPM 29.7% 22.4% 21.8% 22.2% 22.8% 23.5% 24.4% Other non‐operating income 47 22 0 0 0 0 0 Net interest expense ‐688 ‐596 ‐692 ‐679 ‐603 ‐534 ‐473 PBT 2,574 1,824 1,759 1,863 2,058 2,272 2,526 Taxes ‐536 ‐401 ‐369 ‐387 ‐428 ‐473 ‐525 Minority interest 0 0 0 0 0 0 0 Net profit 2,038 1,423 1,391 1,475 1,630 1,799 2,001 Net profit margin 18.9% 13.3% 12.4% 12.9% 14.0% 15.1% 16.3% Appropriations ‐145 ‐100 ‐97 ‐103 ‐114 ‐126 ‐140 Net profit after appropriations 1,893 1,324 1,293 1,372 1,516 1,673 1,861 EPS 20.4 14.2 13.9 14.8 16.3 18.0 20.0 Growth in EPS (%) 3.9% ‐30.2% ‐2.3% 6.1% 10.5% 10.4% 11.2% Dividends/share 9.5 7.1 9.7 11.1 13.9 15.3 17.0 Dividends payout (%) 46.6% 50.0% 70.0% 75.0% 85.0% 85.0% 85.0% Dividend yield 5.7% 4.3% 5.8% 6.6% 8.3% 9.2% 10.2% FCF yield 5.6% ‐0.1% 3.0% 9.6% 10.3% 11.6% 12.8% Balance sheet Intangible assets, other 2,970 4,272 4,722 4,422 4,122 3,821 3,521 Tangible assets and investments 9,800 9,888 10,291 10,584 10,788 10,947 11,099 Total fixed assets 12,770 14,160 15,013 15,005 14,910 14,768 14,620 Total current assets 1,869 1,968 1,922 1,785 1,808 1,836 1,875 Total current liabilities 5,597 5,034 4,397 4,565 4,864 5,026 5,220 Total long‐term liabilities 5,364 6,909 6,964 6,281 5,666 5,120 4,518 Shareholder equity, minorities 3,679 4,184 5,575 5,944 6,188 6,458 6,758 Cash flow statement Cash flow from operations 5,061 4,090 4,640 4,791 4,723 4,861 5,036 Interest ‐654 ‐543 ‐692 ‐679 ‐603 ‐534 ‐473 Taxes ‐331 ‐420 ‐371 ‐369 ‐387 ‐428 ‐473 CAPEX + investment ‐2,398 ‐3,371 ‐2,921 ‐2,087 ‐2,012 ‐1,967 ‐1,959 Dividends paid ‐932 ‐889 ‐712 ‐974 ‐1,107 ‐1,386 ‐1,529 Net cash flow pre financing 747 ‐1,601 ‐55 683 615 546 603 Financing ‐767 1,744 55 ‐683 ‐615 ‐546 ‐603 Change in cash ‐21 119 0 0 0 0 0 Key ratios Net debt/EBITDA 0.8 1.3 1.3 1.1 1.0 0.8 0.7 CAPEX to sales 24.2% 16.0% 20.0% 19.0% 18.0% 17.3% 16.7%

Source: Mobinil, AlembicHC

Telecom Egypt Telecoms | Egypt 14 December 2010

24

Telecom Egypt

Strong yields

Revenue expected to remain flat in the medium term due to wholesale, but TE still offers high FCF and dividend yield of 16.6% and 8.1% expected in 2010e

In our view, concerns about interconnect dispute and MVNO are minimal

Reiterate Overweight view and lower TP 2.0% to EGP21.1/share

We forecast a flat top line growth

On the retail front, broadband revenue (2011–14e CAGR of 18.5%) is expected to offset the drop in voice and access (CAGR of ‐3.1%). Domestic wholesale is expected to grow at a CAGR of 5.6%, offsetting the drop in international revenue (CAGR of ‐2.4%) now that Etisalat also has an international gateway. We expect the EBITDA margin to remain volatile as TE recognizes different types of cable revenue. We expect continued pressure due to competition with mobile operators until stability kicks in 2012e, but EBITDA is expected to follow its normal trend going forward with a 2011–14e CAGR of 0.8%.

VFE to continue cutting prices

We expect VFE to continue cutting prices aggressively to maintain its market leadership position, which we believe will lead to considerable ARPU dilution (2011–14e CAGR of ‐4.9%). Compared to Mobinil, VFE might seem better poised, but we expect revenue and EBITDA to see increasing pressure compared to historical levels. We expect revenue to remain flat in 2010e and EBITDA to drop 4.7%. We believe revenue will grow at a 2011–14e CAGR of 2.3% and EBITDA 2.5%. We lower our TP for VFE to EGP8.5 per TE share based on revised estimates in line with our bearish view on the market and reflecting margin compression as a result of competition. Two concerns with minimal downside risk

On the interconnect dispute, we believe that if the old regime is restored it will bring down the EBITDA margin to 45.4% from 47.1% in 2011e and to 46.2% from 48.2% in 2015e, push the dividend yield down to 8.3% from 8.7%, and dilute our TP by 3.9% to EGP20.3. The other concern is the Mobile Virtual Network Operator (MVNO) setup, which we believe TE will take as a short‐term solution to penetrate the mobile market, which is also its cheapest option. TE’s plans to establish a full MVNO would require a level of investment (already factored in our numbers), which we believe would have a minimal effect on its dividend distribution although we did not forecast any potential upside in our model.

We cut our TP 2.0% to EGP21.1/share and maintain Overweight

We lower our TP 2.0% to EGP21.1/share and maintain our Overweight rating on the stock due to (1) TE’s strong balance sheet (cash balance to rise from 8% in 2010e to 24% of total assets in 2015e), (2) a sustainable high FCF yield averaging 14.2%, (3) an EPS 2011–14e CAGR of 5.6% fuelled by higher EBITDA and interest income, and (4) an expected dividend yield of 8.1% in 2010e and 8.7% in 2011e. We believe that dividend distribution can increase further given the strong cash accumulation. The stock trades at a 36% and 10% discount to peers on 2011e EV/EBITDA and PE, respectively.

Telecom Egypt Telecoms | Egypt 14 December 2010

25

Revenue expected to remain flat in the medium term

Retail revenue to remain under pressure (2010–14e CAGR of 1.5%) saved by the data segment (CAGR of 18.5%)

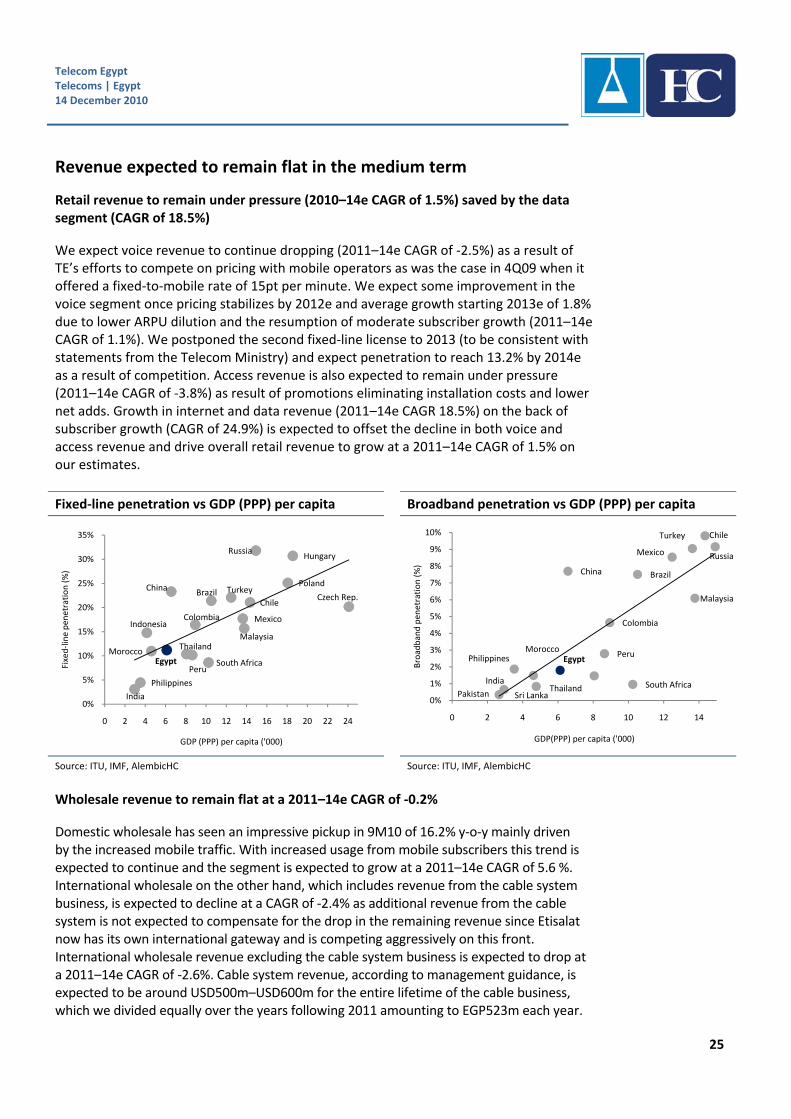

We expect voice revenue to continue dropping (2011–14e CAGR of ‐2.5%) as a result of TE’s efforts to compete on pricing with mobile operators as was the case in 4Q09 when it offered a fixed‐to‐mobile rate of 15pt per minute. We expect some improvement in the voice segment once pricing stabilizes by 2012e and average growth starting 2013e of 1.8% due to lower ARPU dilution and the resumption of moderate subscriber growth (2011–14e CAGR of 1.1%). We postponed the second fixed‐line license to 2013 (to be consistent with statements from the Telecom Ministry) and expect penetration to reach 13.2% by 2014e as a result of competition. Access revenue is also expected to remain under pressure (2011–14e CAGR of ‐3.8%) as result of promotions eliminating installation costs and lower net adds. Growth in internet and data revenue (2011–14e CAGR 18.5%) on the back of subscriber growth (CAGR of 24.9%) is expected to offset the decline in both voice and access revenue and drive overall retail revenue to grow at a 2011–14e CAGR of 1.5% on our estimates.

Fixed‐line penetration vs GDP (PPP) per capita Broadband penetration vs GDP (PPP) per capita

Source: ITU, IMF, AlembicHC Source: ITU, IMF, AlembicHC

Wholesale revenue to remain flat at a 2011–14e CAGR of ‐0.2%

Domestic wholesale has seen an impressive pickup in 9M10 of 16.2% y‐o‐y mainly driven by the increased mobile traffic. With increased usage from mobile subscribers this trend is expected to continue and the segment is expected to grow at a 2011–14e CAGR of 5.6 %. International wholesale on the other hand, which includes revenue from the cable system business, is expected to decline at a CAGR of ‐2.4% as additional revenue from the cable system is not expected to compensate for the drop in the remaining revenue since Etisalat now has its own international gateway and is competing aggressively on this front. International wholesale revenue excluding the cable system business is expected to drop at a 2011–14e CAGR of ‐2.6%. Cable system revenue, according to management guidance, is expected to be around USD500m–USD600m for the entire lifetime of the cable business, which we divided equally over the years following 2011 amounting to EGP523m each year.

India

Philippines

South AfricaPeru

ThailandMorocco

Egypt

Indonesia

Malaysia

Colombia Mexico

Czech Rep.Chile

Brazil TurkeyChina Poland

HungaryRussia

0%

5%

10%

15%

20%

25%

30%

35%

0 2 4 6 8 10 12 14 16 18 20 22 24

Fixed‐line pen

etration (%)

GDP (PPP) per capita ('000)

India

PhilippinesMorocco

Egypt

China

Thailand

Peru

Colombia

South Africa

Brazil

Turkey

Mexico

Malaysia

Chile

Russia

Sri LankaPakistan0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0 2 4 6 8 10 12 14

Broadband pen

etration (%)

GDP(PPP) per capita ('000)

Telecom Egypt Telecoms | Egypt 14 December 2010

26

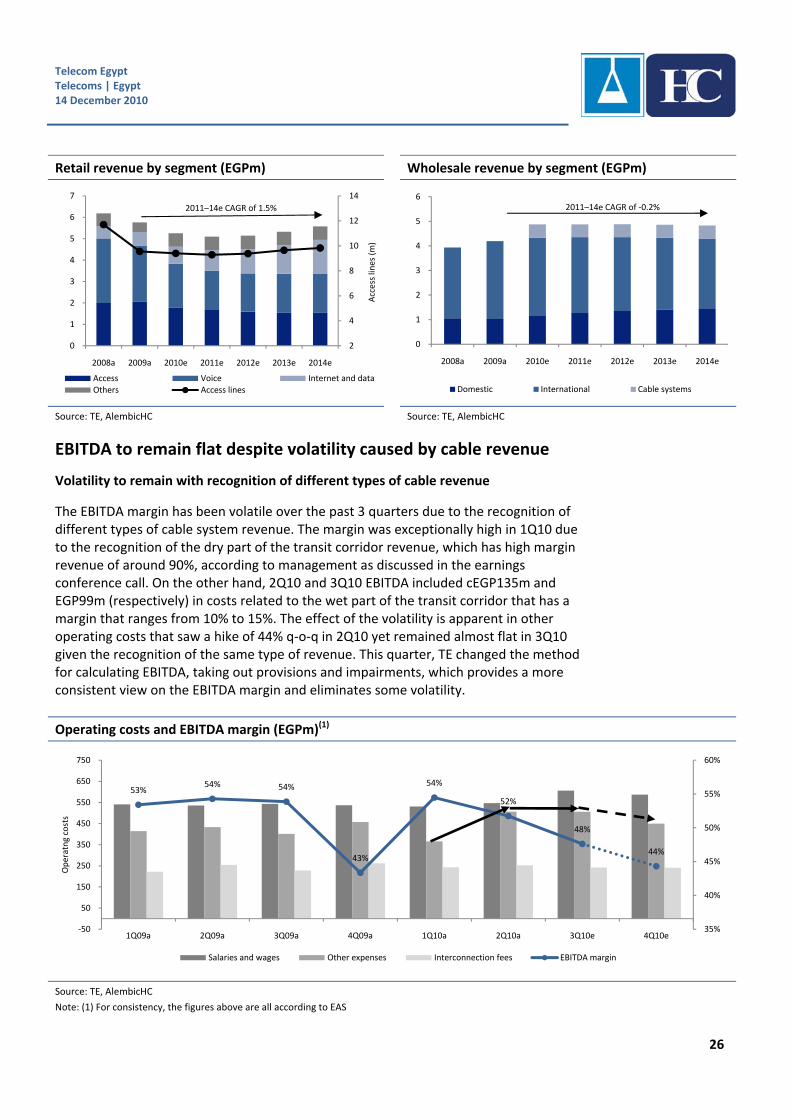

Retail revenue by segment (EGPm) Wholesale revenue by segment (EGPm)

Source: TE, AlembicHC Source: TE, AlembicHC

EBITDA to remain flat despite volatility caused by cable revenue

Volatility to remain with recognition of different types of cable revenue

The EBITDA margin has been volatile over the past 3 quarters due to the recognition of different types of cable system revenue. The margin was exceptionally high in 1Q10 due to the recognition of the dry part of the transit corridor revenue, which has high margin revenue of around 90%, according to management as discussed in the earnings conference call. On the other hand, 2Q10 and 3Q10 EBITDA included cEGP135m and EGP99m (respectively) in costs related to the wet part of the transit corridor that has a margin that ranges from 10% to 15%. The effect of the volatility is apparent in other operating costs that saw a hike of 44% q‐o‐q in 2Q10 yet remained almost flat in 3Q10 given the recognition of the same type of revenue. This quarter, TE changed the method for calculating EBITDA, taking out provisions and impairments, which provides a more consistent view on the EBITDA margin and eliminates some volatility.

Operating costs and EBITDA margin (EGPm)(1)

Source: TE, AlembicHC

Note: (1) For consistency, the figures above are all according to EAS

2

4

6

8

10

12

14

0

1

2

3

4

5

6

7

2008a 2009a 2010e 2011e 2012e 2013e 2014eAccess lines (m)

Access Voice Internet and dataOthers Access lines

0

1

2

3

4

5

6

2008a 2009a 2010e 2011e 2012e 2013e 2014e

Domestic International Cable systems

53%54% 54%

43%

54%

52%

48%

44%

35%

40%

45%

50%

55%

60%

‐50

50

150

250

350

450

550

650

750

1Q09a 2Q09a 3Q09a 4Q09a 1Q10a 2Q10a 3Q10e 4Q10e

Operatng costs

Salaries and wages Other expenses Interconnection fees EBITDA margin

2011–14e CAGR of 1.5% 2011–14e CAGR of ‐0.2%

Telecom Egypt Telecoms | Egypt 14 December 2010

27

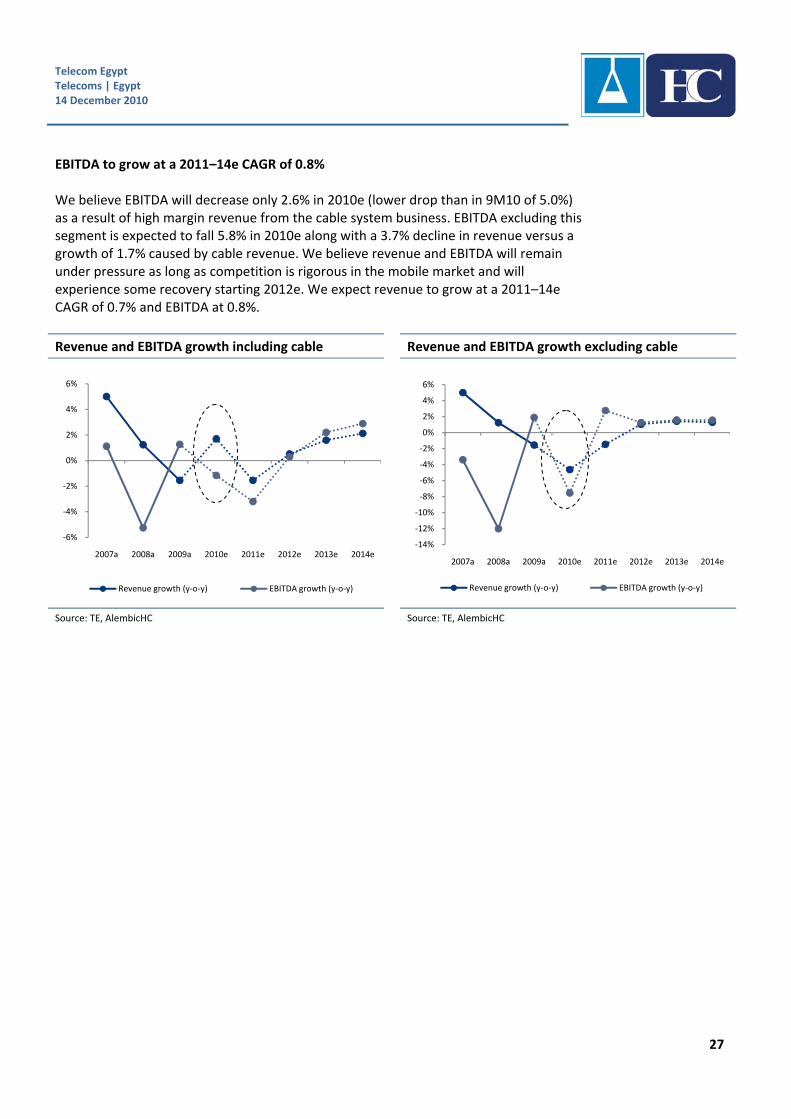

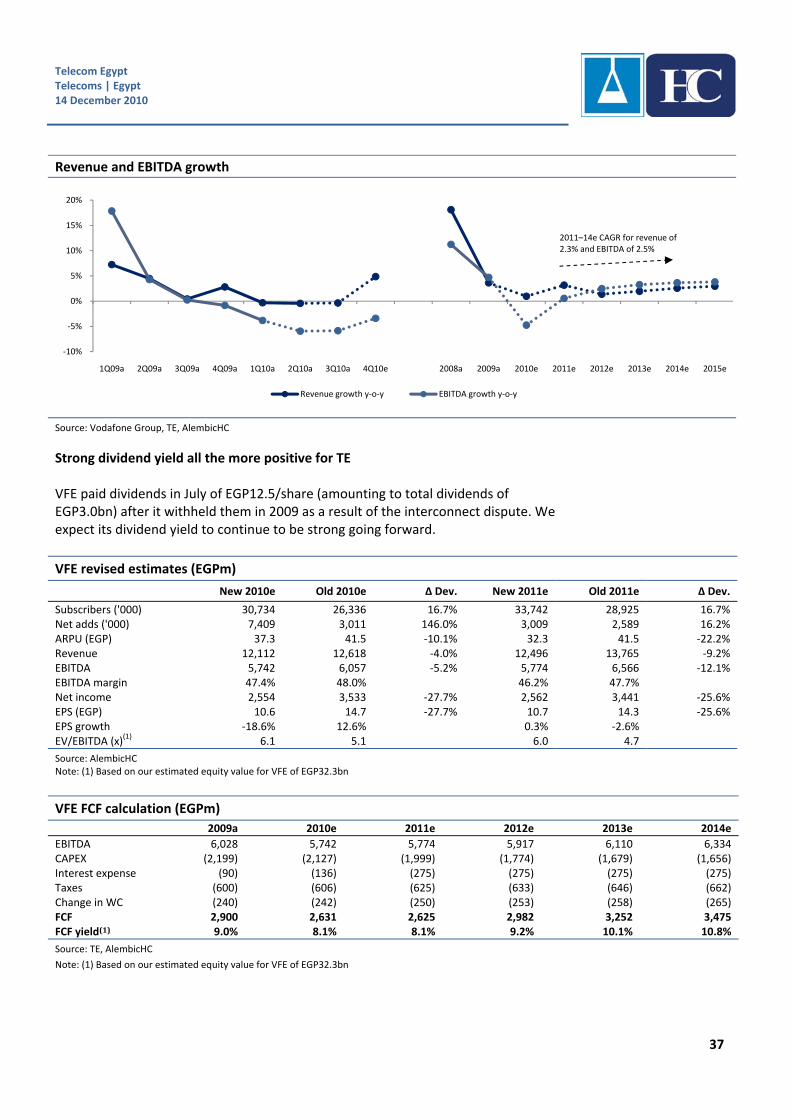

EBITDA to grow at a 2011–14e CAGR of 0.8% We believe EBITDA will decrease only 2.6% in 2010e (lower drop than in 9M10 of 5.0%) as a result of high margin revenue from the cable system business. EBITDA excluding this segment is expected to fall 5.8% in 2010e along with a 3.7% decline in revenue versus a growth of 1.7% caused by cable revenue. We believe revenue and EBITDA will remain under pressure as long as competition is rigorous in the mobile market and will experience some recovery starting 2012e. We expect revenue to grow at a 2011–14e CAGR of 0.7% and EBITDA at 0.8%.

Revenue and EBITDA growth including cable Revenue and EBITDA growth excluding cable

Source: TE, AlembicHC Source: TE, AlembicHC

‐6%

‐4%

‐2%

0%

2%

4%

6%

2007a 2008a 2009a 2010e 2011e 2012e 2013e 2014e

Revenue growth (y‐o‐y) EBITDA growth (y‐o‐y)

‐14%

‐12%

‐10%

‐8%

‐6%

‐4%

‐2%

0%

2%

4%

6%

2007a 2008a 2009a 2010e 2011e 2012e 2013e 2014e

Revenue growth (y‐o‐y) EBITDA growth (y‐o‐y)

Telecom Egypt Telecoms | Egypt 14 December 2010

28

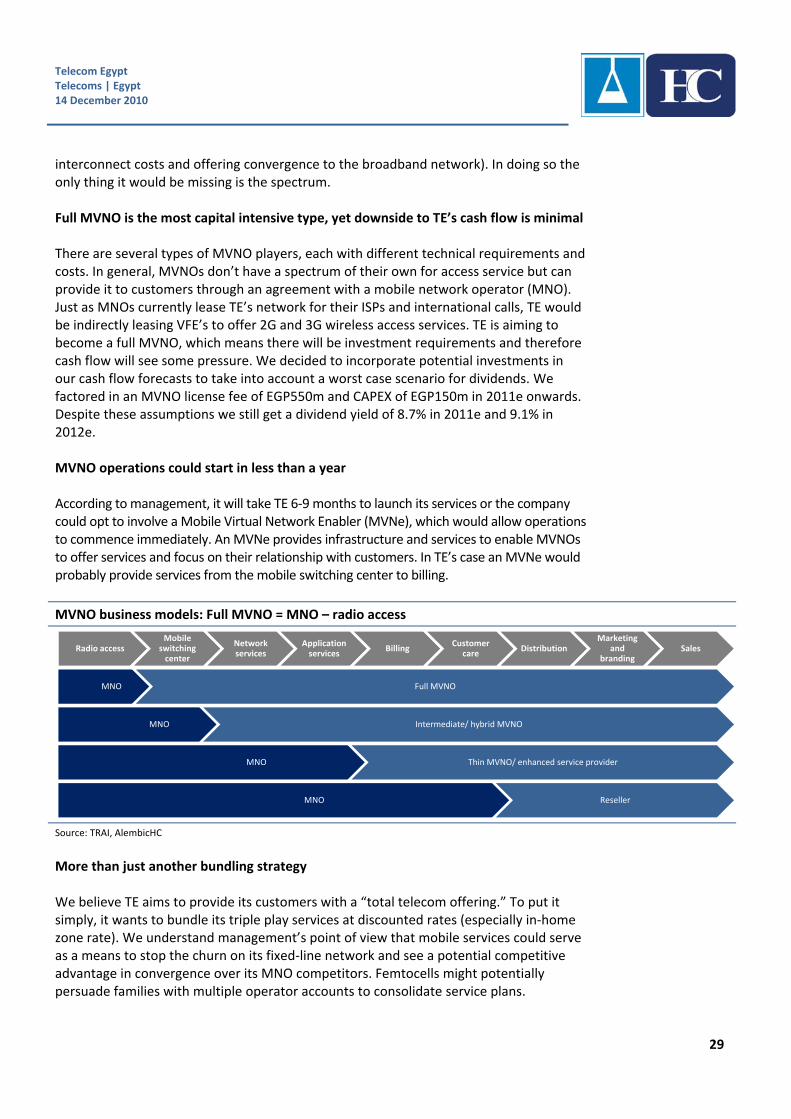

More than a traditional MVNO: Differentiation through convergence Entering the mobile market through an MVNO setup is a first stage The Telecom Ministry decided to postpone offering a fourth mobile license beyond 2013 and discussions between TE and VG to purchase the latter’s stake in VFE were not concluded, meaning that TE’s only option to venture into the mobile space would be buying Egypt’s first MVNO license. TE is currently studying the viability of being a virtual mobile operator and is expected to reach a final decision by 1Q11. We believe TE will continue to eye VG’s stake in VFE or bid for Egypt’s fourth (4G) mobile license therefore the MVNO setup would provide TE with a short term solution (the cheapest as well) to access Egypt’s mobile market. We previously argued in favor of fixed‐to‐mobile convergence (FMC) In our last note Not a doomsday scenario (6 April 2010) we argued in favor of a fourth mobile license as we are confident in the opportunities FMC can offer. TE’s MVNO venture will still play on convergence but with an alternative technology deploying femtocells. Femtocells are small cellular base stations (very similar to Wi‐Fi routers) that allow a customer to connect to the broadband network once indoors and be charged lower rates in line with the fixed‐line rate. In essence, TE will be able to compete with mobile operators by utilizing femtocells to capture mobile users when at home (60% of voice and 70% of data usage occurs indoors) and divert their mobile originated voice and data calls to the fixed‐line network, like with VoIP. The femtocell value proposition Femtocells offer customers six main benefits: (1) improved in‐home mobile coverage, (2) enhancing video and audio downloading, (3) cheaper in‐home call/ data rates, (4) higher mobile internet speed, (5) improved phone battery life (especially for Wi‐Fi users), and (6) various value‐added services, of which the most appealing would be allowing customers to have a virtual home number, meaning they would require only one handset instead of two. As such, we see more to the story than the traditional minute reseller as we believe in the value proposition convergence could offer. Reasoning behind TE and VFE’s willingness to agree on an MVNO setup TE is likely to opt for an MVNO setup on VFE’s network since TE would probably receive a better wholesale price than from mobile operators. VFE’s CEO already expressed his willingness to the Egyptian press. We believe VFE would benefit from (1) delaying the issuance of a fourth mobile license in the market and ensuring that they get a share of the forth entrant’s revenue and (2) delaying TE’s acquisition talks regarding VG’s stake in VFE. Full MVNO: Relative independence of MNO and various synergies TE plans to launch a full (also called heavy) MVNO to capitalize on the synergies it can extract from its fixed‐line business including a large distribution network in all Egyptian governorates, a customer service call center, experienced employees in various functional areas, an international gateway, and the fixed‐line infrastructure (saving on

Telecom Egypt Telecoms | Egypt 14 December 2010

29

interconnect costs and offering convergence to the broadband network). In doing so the only thing it would be missing is the spectrum. Full MVNO is the most capital intensive type, yet downside to TE’s cash flow is minimal There are several types of MVNO players, each with different technical requirements and costs. In general, MVNOs don’t have a spectrum of their own for access service but can provide it to customers through an agreement with a mobile network operator (MNO). Just as MNOs currently lease TE’s network for their ISPs and international calls, TE would be indirectly leasing VFE’s to offer 2G and 3G wireless access services. TE is aiming to become a full MVNO, which means there will be investment requirements and therefore cash flow will see some pressure. We decided to incorporate potential investments in our cash flow forecasts to take into account a worst case scenario for dividends. We factored in an MVNO license fee of EGP550m and CAPEX of EGP150m in 2011e onwards. Despite these assumptions we still get a dividend yield of 8.7% in 2011e and 9.1% in 2012e. MVNO operations could start in less than a year According to management, it will take TE 6‐9 months to launch its services or the company could opt to involve a Mobile Virtual Network Enabler (MVNe), which would allow operations to commence immediately. An MVNe provides infrastructure and services to enable MVNOs to offer services and focus on their relationship with customers. In TE’s case an MVNe would probably provide services from the mobile switching center to billing.

MVNO business models: Full MVNO = MNO – radio access

Source: TRAI, AlembicHC

More than just another bundling strategy We believe TE aims to provide its customers with a “total telecom offering.” To put it simply, it wants to bundle its triple play services at discounted rates (especially in‐home zone rate). We understand management’s point of view that mobile services could serve as a means to stop the churn on its fixed‐line network and see a potential competitive advantage in convergence over its MNO competitors. Femtocells might potentially persuade families with multiple operator accounts to consolidate service plans.

Radio accessMobile switching center

Network services

Application services

BillingCustomer

careDistribution

Marketing and

brandingSales

MNO Full MVNO

MNO Intermediate/ hybrid MVNO

MNO Thin MVNO/ enhanced service provider

MNO Reseller

Telecom Egypt Telecoms | Egypt 14 December 2010

30

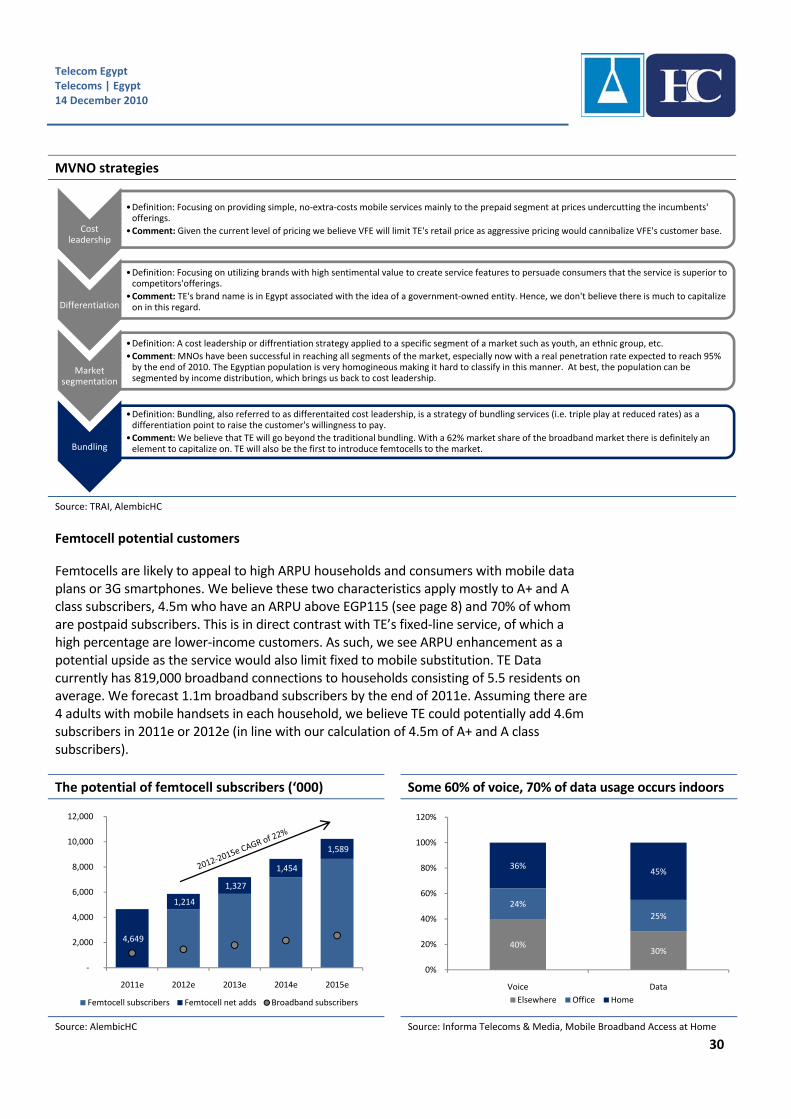

MVNO strategies

Source: TRAI, AlembicHC

Femtocell potential customers

Femtocells are likely to appeal to high ARPU households and consumers with mobile data plans or 3G smartphones. We believe these two characteristics apply mostly to A+ and A class subscribers, 4.5m who have an ARPU above EGP115 (see page 8) and 70% of whom are postpaid subscribers. This is in direct contrast with TE’s fixed‐line service, of which a high percentage are lower‐income customers. As such, we see ARPU enhancement as a potential upside as the service would also limit fixed to mobile substitution. TE Data currently has 819,000 broadband connections to households consisting of 5.5 residents on average. We forecast 1.1m broadband subscribers by the end of 2011e. Assuming there are 4 adults with mobile handsets in each household, we believe TE could potentially add 4.6m subscribers in 2011e or 2012e (in line with our calculation of 4.5m of A+ and A class subscribers).

The potential of femtocell subscribers (‘000) Some 60% of voice, 70% of data usage occurs indoors

Source: AlembicHC Source: Informa Telecoms & Media, Mobile Broadband Access at Home

Cost leadership

•Definition: Focusing on providing simple, no‐extra‐costs mobile services mainly to the prepaid segment at prices undercutting the incumbents' offerings.

•Comment: Given the current level of pricing we believe VFE will limit TE's retail price as aggressive pricing would cannibalize VFE's customer base.

Differentiation

•Definition: Focusing on utilizing brands with high sentimental value to create service features to persuade consumers that the service is superior to competitors'offerings.

•Comment: TE's brand name is in Egypt associated with the idea of a government‐owned entity. Hence, we don't believe there is much to capitalize on in this regard.

Market segmentation

•Definition: A cost leadership or diffrentiation strategy applied to a specific segment of a market such as youth, an ethnic group, etc.

•Comment: MNOs have been successful in reaching all segments of the market, especially now with a real penetration rate expected to reach 95% by the end of 2010. The Egyptian population is very homogineous making it hard to classify in this manner. At best, the population can be segmented by income distribution, which brings us back to cost leadership.

Bundling

•Definition: Bundling, also referred to as differentaited cost leadership, is a strategy of bundling services (i.e. triple play at reduced rates) as a differentiation point to raise the customer's willingness to pay.

•Comment: We believe that TE will go beyond the traditional bundling. With a 62% market share of the broadband market there is definitely an element to capitalize on. TE will also be the first to introduce femtocells to the market.

4,649

1,214

1,327

1,454

1,589

‐

2,000

4,000

6,000

8,000

10,000

12,000

2011e 2012e 2013e 2014e 2015e

Femtocell subscribers Femtocell net adds Broadband subscribers

40%30%

24%

25%

36%45%

0%

20%

40%

60%

80%

100%

120%

Voice Data

Elsewhere Office Home

Telecom Egypt Telecoms | Egypt 14 December 2010

31

Concerns surrounding the MVNO endeavor While we believe in the opportunities the service has to offer, its implementation and customer appeal remain questionable. The technology is new, and although 17 operators in 11 countries have already adopted it, subscriber numbers are not disclosed and marketing initiatives have not been aggressive. The only exception to this has been Vodafone UK, which has slashed femtocell prices 70% since their launch in 2009 and rebranded the service to Sure Signal in an attempt to market it for areas with limited coverage. Pricing is also a potential issue since a femtocell’s selling price is cUSD200, and operators are still testing retail pricing schemes to offset the cost of service and equipment while stimulating adoption. Pricing ranges from a complete subsidy (KDDI and Softbank in Japan) to monthly installments (ranging from USD9 to USD32). Our bearish outlook on the mobile market is based on real penetration reaching 95% in 2010e, which indicates that there is no room for another market entrant, and means high churn for other operators if the service gains customer appeal. Therefore, we chose not to reflect any upside potential in our model but only the worst case scenario (CAPEX cash out flows) on dividend distribution. MVNO setup with VFE is a double‐edged sword for TE Cannibalizing VFE’s market share would affect its revenue, which will eventually reflect on TE’s investment income booked from VFE. On the other hand, VFE would be adding a new revenue segment that would reflect positively on TE’s investment income. Whether these 2 phenomena would offset each other and how they will eventually affect investment income from VFE (an important element to TE’s bottom line) is uncertain in our view as it will be dependent on the wholesale agreement and the MVNO’s rate of success.

Telecom Egypt Telecoms | Egypt 14 December 2010

32

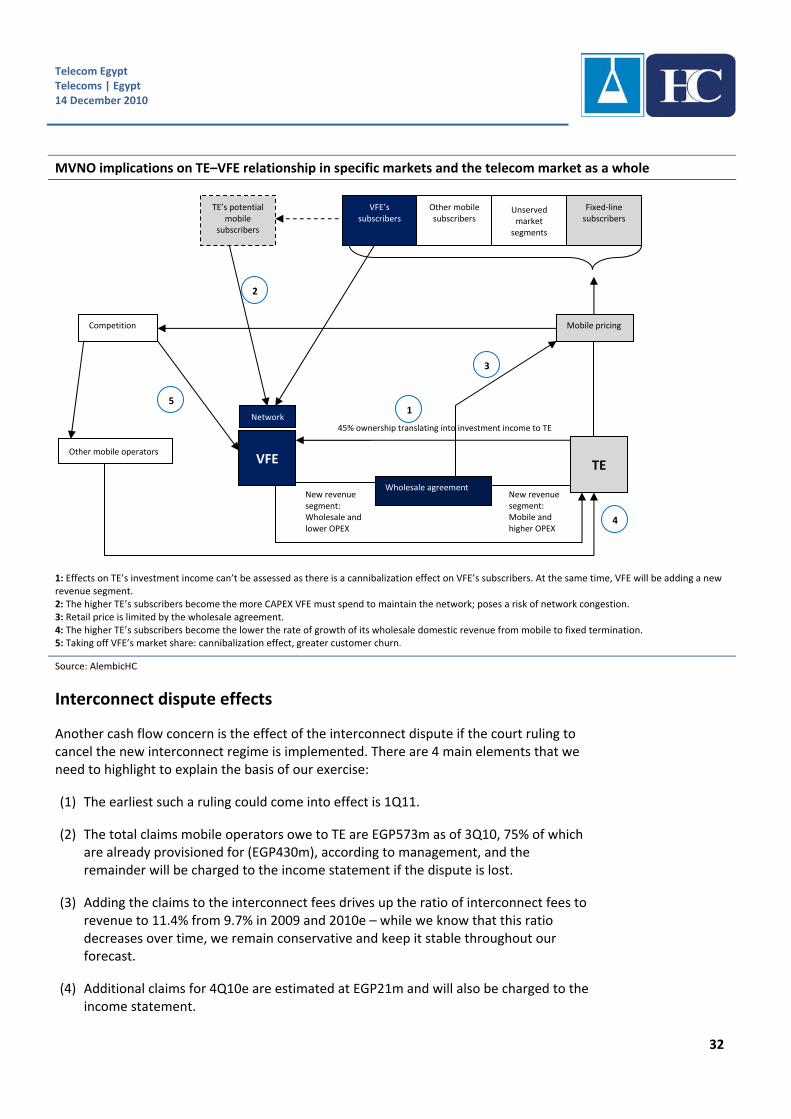

MVNO implications on TE–VFE relationship in specific markets and the telecom market as a whole

1: Effects on TE’s investment income can’t be assessed as there is a cannibalization effect on VFE’s subscribers. At the same time, VFE will be adding a new revenue segment. 2: The higher TE’s subscribers become the more CAPEX VFE must spend to maintain the network; poses a risk of network congestion. 3: Retail price is limited by the wholesale agreement. 4: The higher TE’s subscribers become the lower the rate of growth of its wholesale domestic revenue from mobile to fixed termination. 5: Taking off VFE’s market share: cannibalization effect, greater customer churn.

Source: AlembicHC

Interconnect dispute effects

Another cash flow concern is the effect of the interconnect dispute if the court ruling to cancel the new interconnect regime is implemented. There are 4 main elements that we need to highlight to explain the basis of our exercise:

(1) The earliest such a ruling could come into effect is 1Q11.

(2) The total claims mobile operators owe to TE are EGP573m as of 3Q10, 75% of which are already provisioned for (EGP430m), according to management, and the remainder will be charged to the income statement if the dispute is lost.

(3) Adding the claims to the interconnect fees drives up the ratio of interconnect fees to revenue to 11.4% from 9.7% in 2009 and 2010e – while we know that this ratio decreases over time, we remain conservative and keep it stable throughout our forecast.

(4) Additional claims for 4Q10e are estimated at EGP21m and will also be charged to the income statement.

VFE TE Other mobile operators

Unserved market segments

Fixed‐line subscribers

VFE’s subscribers

Other mobile subscribers

TE’s potential mobile

subscribers

Wholesale agreement

45% ownership translating into investment income to TE

Mobile pricing Competition

Network

New revenue segment: Mobile and higher OPEX

New revenue segment: Wholesale and lower OPEX

5

2

3

1

4

Telecom Egypt Telecoms | Egypt 14 December 2010

33

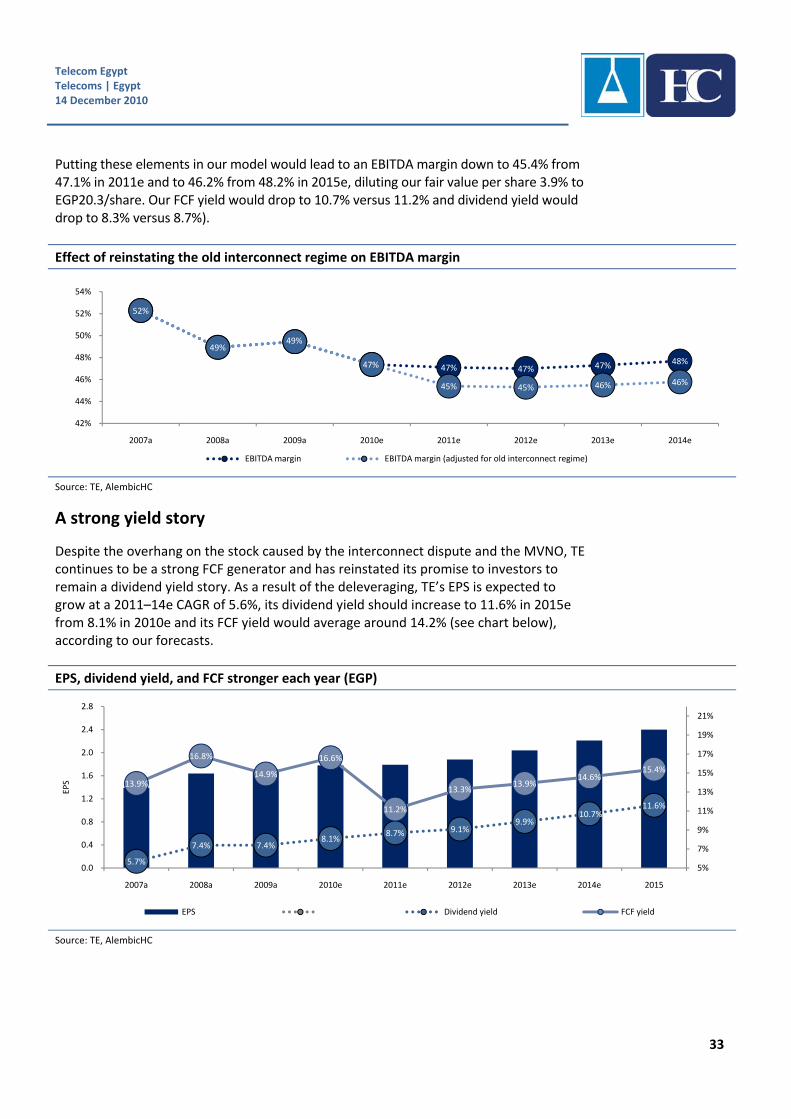

Putting these elements in our model would lead to an EBITDA margin down to 45.4% from 47.1% in 2011e and to 46.2% from 48.2% in 2015e, diluting our fair value per share 3.9% to EGP20.3/share. Our FCF yield would drop to 10.7% versus 11.2% and dividend yield would drop to 8.3% versus 8.7%).

Effect of reinstating the old interconnect regime on EBITDA margin

Source: TE, AlembicHC

A strong yield story

Despite the overhang on the stock caused by the interconnect dispute and the MVNO, TE continues to be a strong FCF generator and has reinstated its promise to investors to remain a dividend yield story. As a result of the deleveraging, TE’s EPS is expected to grow at a 2011–14e CAGR of 5.6%, its dividend yield should increase to 11.6% in 2015e from 8.1% in 2010e and its FCF yield would average around 14.2% (see chart below), according to our forecasts.

EPS, dividend yield, and FCF stronger each year (EGP)

Source: TE, AlembicHC

47% 47% 47% 48%

52%

49%49%

47%

45% 45% 46% 46%

42%

44%

46%

48%

50%

52%

54%

2007a 2008a 2009a 2010e 2011e 2012e 2013e 2014e

EBITDA margin EBITDA margin (adjusted for old interconnect regime)

5.7%

7.4% 7.4%8.1%

8.7% 9.1%9.9%

10.7%11.6%

13.9%

16.8%

14.9%

16.6%

11.2%

13.3%13.9%

14.6%15.4%

5%

7%

9%

11%

13%

15%

17%

19%

21%

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2.8

2007a 2008a 2009a 2010e 2011e 2012e 2013e 2014e 2015

EPS

EPS Dividend yield FCF yield

Telecom Egypt Telecoms | Egypt 14 December 2010

34

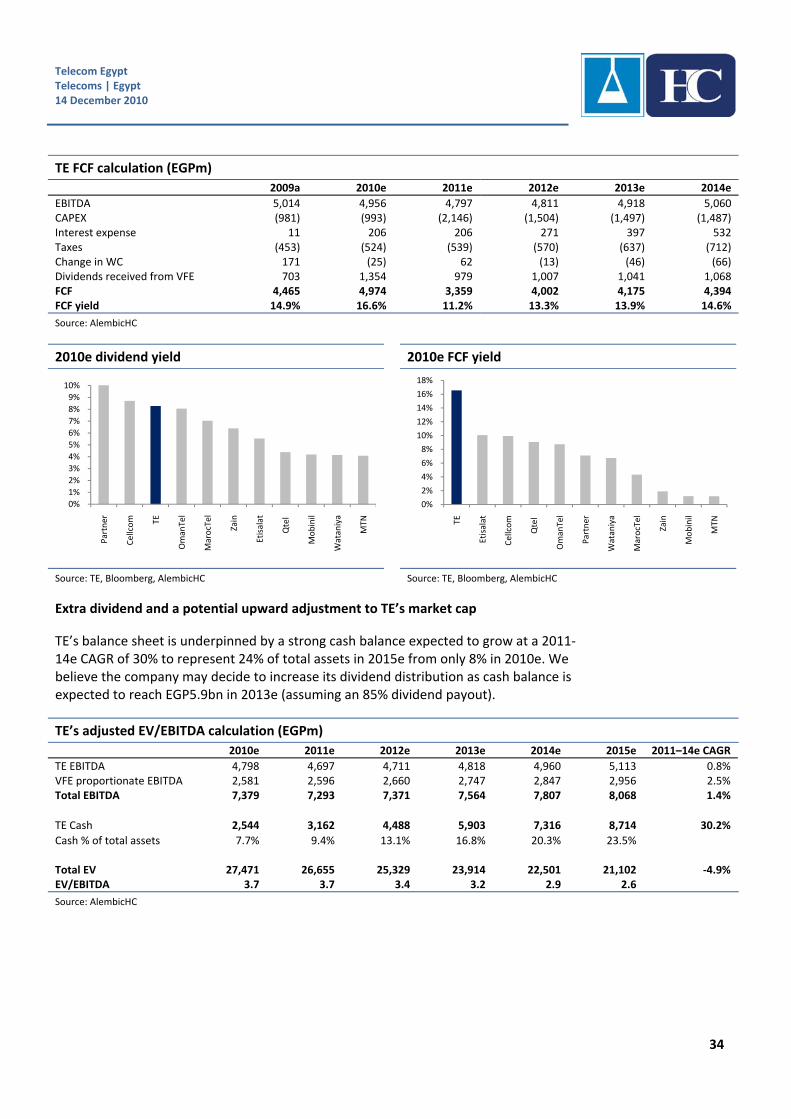

TE FCF calculation (EGPm)

2009a 2010e 2011e 2012e 2013e 2014e

EBITDA 5,014 4,956 4,797 4,811 4,918 5,060 CAPEX (981) (993) (2,146) (1,504) (1,497) (1,487) Interest expense 11 206 206 271 397 532 Taxes (453) (524) (539) (570) (637) (712) Change in WC 171 (25) 62 (13) (46) (66) Dividends received from VFE 703 1,354 979 1,007 1,041 1,068 FCF 4,465 4,974 3,359 4,002 4,175 4,394 FCF yield 14.9% 16.6% 11.2% 13.3% 13.9% 14.6%

Source: AlembicHC

2010e dividend yield 2010e FCF yield

Source: TE, Bloomberg, AlembicHC Source: TE, Bloomberg, AlembicHC

Extra dividend and a potential upward adjustment to TE’s market cap

TE’s balance sheet is underpinned by a strong cash balance expected to grow at a 2011‐14e CAGR of 30% to represent 24% of total assets in 2015e from only 8% in 2010e. We believe the company may decide to increase its dividend distribution as cash balance is expected to reach EGP5.9bn in 2013e (assuming an 85% dividend payout).

TE’s adjusted EV/EBITDA calculation (EGPm)

2010e 2011e 2012e 2013e 2014e 2015e 2011–14e CAGR

TE EBITDA 4,798 4,697 4,711 4,818 4,960 5,113 0.8% VFE proportionate EBITDA 2,581 2,596 2,660 2,747 2,847 2,956 2.5% Total EBITDA 7,379 7,293 7,371 7,564 7,807 8,068 1.4%

TE Cash 2,544 3,162 4,488 5,903 7,316 8,714 30.2%

Cash % of total assets 7.7% 9.4% 13.1% 16.8% 20.3% 23.5% Total EV 27,471 26,655 25,329 23,914 22,501 21,102 ‐4.9% EV/EBITDA 3.7 3.7 3.4 3.2 2.9 2.6

Source: AlembicHC

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Partner

Cellcom TE

OmanTel

MarocTel

Zain

Etisalat

Qtel

Mobinil

Wataniya

MTN

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

TE

Etisalat

Cellcom

Qtel

OmanTel

Partner

Wataniya

MarocTel

Zain

Mobinil

MTN

Telecom Egypt Telecoms | Egypt 14 December 2010

35

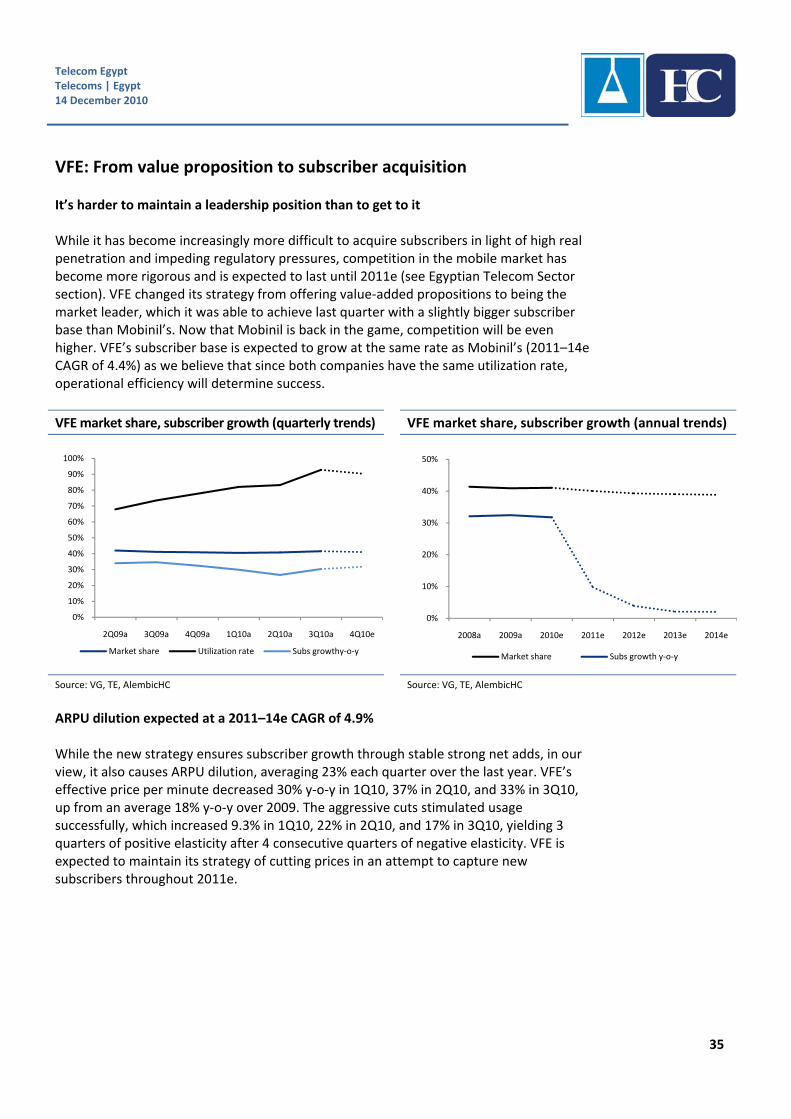

VFE: From value proposition to subscriber acquisition It’s harder to maintain a leadership position than to get to it While it has become increasingly more difficult to acquire subscribers in light of high real penetration and impeding regulatory pressures, competition in the mobile market has become more rigorous and is expected to last until 2011e (see Egyptian Telecom Sector section). VFE changed its strategy from offering value‐added propositions to being the market leader, which it was able to achieve last quarter with a slightly bigger subscriber base than Mobinil’s. Now that Mobinil is back in the game, competition will be even higher. VFE’s subscriber base is expected to grow at the same rate as Mobinil’s (2011–14e CAGR of 4.4%) as we believe that since both companies have the same utilization rate, operational efficiency will determine success.

VFE market share, subscriber growth (quarterly trends) VFE market share, subscriber growth (annual trends)

Source: VG, TE, AlembicHC Source: VG, TE, AlembicHC

ARPU dilution expected at a 2011–14e CAGR of 4.9% While the new strategy ensures subscriber growth through stable strong net adds, in our view, it also causes ARPU dilution, averaging 23% each quarter over the last year. VFE’s effective price per minute decreased 30% y‐o‐y in 1Q10, 37% in 2Q10, and 33% in 3Q10, up from an average 18% y‐o‐y over 2009. The aggressive cuts stimulated usage successfully, which increased 9.3% in 1Q10, 22% in 2Q10, and 17% in 3Q10, yielding 3 quarters of positive elasticity after 4 consecutive quarters of negative elasticity. VFE is expected to maintain its strategy of cutting prices in an attempt to capture new subscribers throughout 2011e.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2Q09a 3Q09a 4Q09a 1Q10a 2Q10a 3Q10a 4Q10e

Market share Utilization rate Subs growthy‐o‐y

0%

10%

20%

30%

40%

50%

2008a 2009a 2010e 2011e 2012e 2013e 2014e

Market share Subs growth y‐o‐y

Telecom Egypt Telecoms | Egypt 14 December 2010

36

VFE usage vs effective price per minute VFE net adds vs % change in ARPU

Source: VG, AlembicHC Source: VG, AlembicHC

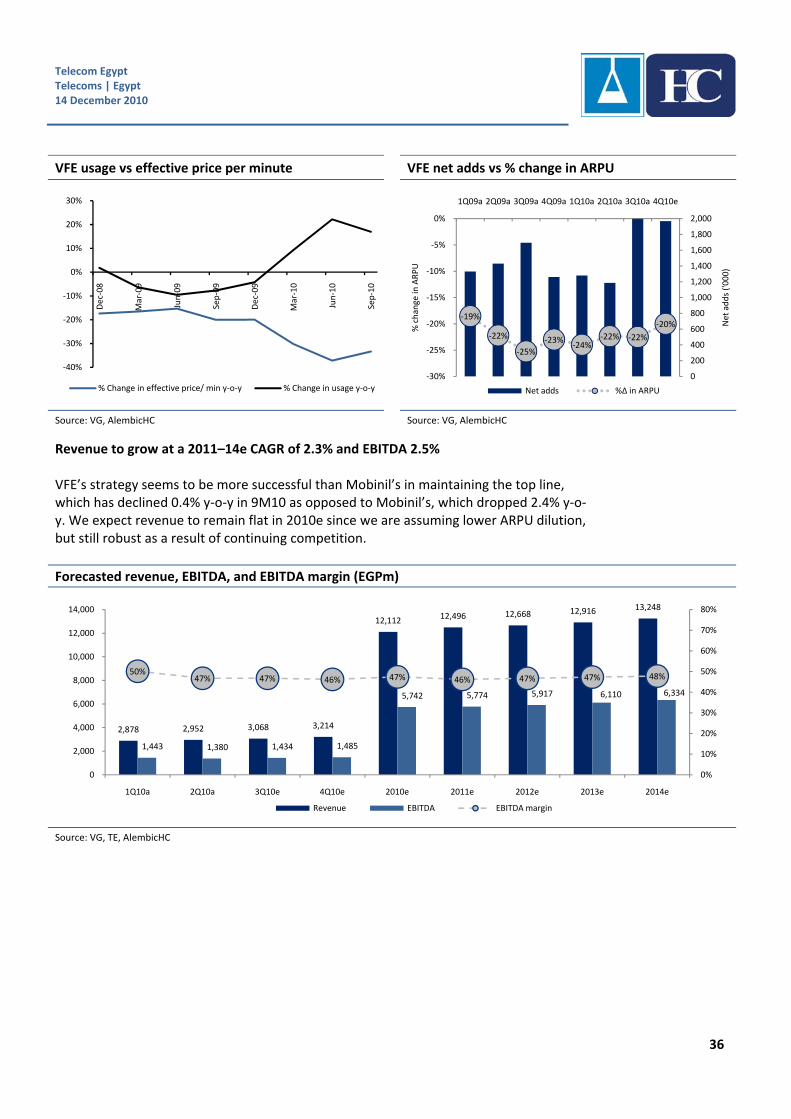

Revenue to grow at a 2011–14e CAGR of 2.3% and EBITDA 2.5% VFE’s strategy seems to be more successful than Mobinil’s in maintaining the top line, which has declined 0.4% y‐o‐y in 9M10 as opposed to Mobinil’s, which dropped 2.4% y‐o‐y. We expect revenue to remain flat in 2010e since we are assuming lower ARPU dilution, but still robust as a result of continuing competition.

Forecasted revenue, EBITDA, and EBITDA margin (EGPm)

Source: VG, TE, AlembicHC

‐40%

‐30%

‐20%

‐10%

0%

10%

20%

30%

Dec‐08

Mar‐09