Embed Size (px)

Citation preview

Chapter - 5

SECTOR-WISE AND BANK-WISE CREDIT DELIVERY

AND RECOVERY IN KOLLAM DISTRICT –

AN ANALYSIS

Location of Kollam District:-

Kollam is one of the 14 districts in Kerala State. It is located

between 9 o 28’ to8 o 45’ latitude and 76 o 28’ to 77 o 17’ north longitude. It

has a long history in trading with Chinese, Portuguese and the Dutch.

Portuguese and the Dutch established their trade centres in Kollam during

the beginning of 16th century and the British in 1795. Quilon was

recognized as an administrative unit by 1835 under Travancore state. In

1957, under the Kerala State Reorganisation Act of 1957 and further during

the formation of Alappuzha and later Pathanamthitta districts, it has to part

with Schenkotta to Tamil Nadu, six taluks to Alappuzha and Pathanamthitta

taluk to the newly formed district,viz, Pathanamthitta. Presently, the district

has only 2518 sq.km. It is bounded on the west by Arabian Sea, east by

Western Ghats bordering Tamil Nadu, south by Thiruvananthapuram; and,

shares border with Alappuzha and Pathanamthitta districts in north and

north east.

Topography and Physical Features:-

The district has low land, mid-land, mid upland and highland. Both

Karunagapally and Kollam taluks are in mid-land and low-land regions

respectively. About 10 per cent of the district”s geographical area is in

low-lands, 39 per cent is in mid-land and 28 per cent is in mid-upland; 18 per

cent of the area is in up-land and the remaining 5 per cent of the land is

highland category. Anchal taluk is largely under highland and up-land

96

category. The typical topography enriches its large backwater resources,

viz Ashtamudikayal, dense forest, reserve forest and the three lush rivers,

viz Kallada, Ithikkara and Achankovil rivers. Kulathupuzha Hills,

Achankovil Hills, Aryankavu Hills and Sabari Hills are the taller mountains

ranging from 1,500 m to 1,900 m separating the district from Tamil Nadu, on

the Western Ghats.

Climate:-

Climate of Kollam district is hot and humid. Summer season starts

from March and continues up to May. It is followed by South-West

Monsoon and stretched from June to September. October-November form

the retreating of monsoon and from December to February it is again

North-West Monsoon. The normal rainfall averages 2,742 mm and the

temperature ranges from 230 C to 360 C

Soil Structure

Sandy loam, laterite and forest soil dominate the district. The sandy

beaches at Chavara, Neendakara and Kovilthottam are rich in Monozite,

Ilmenite and Rutile. China clay is available at Kundara, Mulavana,

Chathannur and lime shells in Ashtamudy Lake. Bauxite is available in

Adichanallur and disseminated graphite in Punalur. The top soil is rich for

the cultivation of a variety of crops including plantation crops. This has

helped the farmers in developing homestead farming under rain-fed

conditions and based on family requirements using family labour.

Administrative Set up

The district for administrative convenience is divided into fiv taluks,

13 blocks, 104 villages, 71 grama panchayaths and one corporation and

two municipalities. Anchal, Anchalumoodu, Chadayamangalam,

Chittumala, Chavara, Ithikara, Karunagappally, Kottarakara, Mukhathala,

Ochira, Pathanapuram, Sasthmakotta and Vettikkavala are the 13 blocks.

97

Cultivators dominate Anchal, Chadayamangalam, Sasthamkotta,

Vettikavala and Kottarakara blocks.

Population:

As per Census 2001, the district is having a population of 25.84 lakh,

constituting 8 per cent of the state’s population. It has 5.9 lakh households;

of which 5 lakhs, 84 per cent, are in rural area. Literacy is worked out at 91

per cent and SC & ST population at approximately 12 per cent and 0.2 per

cent respectively. The household under Below Poverty Line (BPL) works

out to 8 per cent of the total household. Among the 25.84-lakh population,

cultivators total 57,000, Agricultural Labour 1,22,000, people engaged in

Allied sectors 92,000 and artisans 25,000. Similar to the state1 Kollam

district also has a sizable number of ageing population which adversely

affects its socio-economic development. The per capita income averages `

2,885 and share of Primary, Secondary and Tertiary Sectors in the state's

domestic product works out at 27 per cent, 24 per cent and 49 per cent

respectively.

Land Utilisation:-

Out of the total geographical area of 2.5 lakh hectares, area under

forest is 32 per cent and net sown area is 52 per cent and the cropping

intensity averages at 137 per cent during last few years.

Pattern of Land Holdings:-

The district has 5.5 lakh landholdings as per 1995-96 census.

Among them, 98 per cent of the holdings are below one hectare and they

share 79 per cent of the total area held under personal holdings. About

9,881 holdings are between one to two hectares, having 14 per cent of the

area and holdings above two hectares are 2,163 and they share about

98

seven per cent of the area. The pattern of holdings thus reflects the limited

scope for developing crop cultivation as the major economic activity for the

farm family to optimise their family income. This limitation resulted in

searching for alternate income sources and large level shift of the rural

youth to wage earners and migration.

Cropping Pattern:-

Coconut, rubber, tapioca, paddy, banana, pepper and cashew are

the important crops cultivated in the district. Homestead farming,

cultivation of paddy in wetland and cultivation of plantation crops, especially

rubber, are the systems followed.

The area under coconut and paddy, the major crops cultivated in

Kollam district, has a declining trend. Decreasing trend of coconut yield,

shortage of manpower for the regular maintenance of the coconut gardens

are serious threats the farmers face. Whereas, the area under rubber in

Kollam district recorded increasing trend. Regular returns and support

services from Rubber Board give hopes for farmers. Availability of subsidy

at ` 20,000 per hectare for new planting and ` 12,000 per hectare. for

replanting worked as incentives for faster switchover.

Irrigation

Majority of the cultivation in Kollam district is under rain-fed

conditions. Only 11 per cent of net area sown is under irrigation. Canals,

tanks, wells and others are the major sources of irrigation. The culture to

invest in irrigation is yet to pick up in the district. The groundwater

development in Kollam district as per the data available in 2004 is at 46 per

cent. Out of the 13 blocks in the district, in four blocks the groundwater

availability is at critical stage. The district has good scope for developing

lift irrigation projects2. The State Government also gives more importance

99

in development of minor irrigation in Kollam district.

Animal Wealth

The district has considerable good strength under livestock. It has

1.43 lakh milch-cows, 0.02 lakh milch buffaloes, 1.08 lakh goats, 0.11

plough animals and about 8.1 lakh poultry birds. The milch animals are of

improved genetic quality. However, development of commercial dairy units

are yet to pick up. Similarly, large commercial poultry units and stall-fed

goatery units are yet to emerge. The district has a good infrastructure

under Dairy3.

Fisheries

The district has 37 k.m. of coastline and 3,500 sq.k.m. continental

shelf. In addition to the above, it has three rivers, viz. Kallada, Ithikara and

Pallickkal and three large backwaters, viz. Kayamkulam, Ashtamudi and

Paravoor. About 53 fishing villages (27 under marine and 26 under inland)

are directly linked with fish capture and culture. Though Indo-Norwegian

project has introduced mechanised fishing, processing and marketing in

Neendakara as early as 1952-53, the fishery sector in the district under

capture, culture, processing and trading is yet to address its optimum

efficiency. The immense potential available under fish culture remains yet

to be exploited. Similarly, the value addition process under entire fish

produce is yet to be addressed.

Important Non-Farm Sector Activities

Handloom, coir, cashew processing, micro and small industries,

tourism etc. are the important sectors absorbing sizable number of

population. Under handloom sector, there are about 8,000 looms and

most of them are located at Chathannur, Veliyam Panchayath and outskirts

100

of Kollam Corporation. The activity provide employment opportunities for

more than 7,000 persons. Coir production has a concentration in Chavara,

Munroe Island and Karunagapally Panchayaths. The sector faces tough

competition from synthetic fibres and the coir co-operatives are relatively

weak to address timely required technology changes and product

diversification. Cashew processing has a concentration in Kottarakara,

Mukhathala, Sasthamkotta, Vettikkavala, Kundara and Kollam Corporation.

The sector employs nearly a lakh people and it has promising scope for

further value addition and brining out a variety of innovative and

market-friendly products.

Kollam district is having a good number of micro and small industries

based on wood, rubber, plastic, chemical, electrical, electronic, readymade

garments, leather, maintenance, fabrication, building construction, DTP

centres etc. The district is also having 276 industrial co-operatives. District

Industries Centre (DIC) provides hand-holding support to entrepreneurs

and also extends infrastructure facilities under mini industrial states located

at Perinad, Kareepra, Thevalakkara, Chavara and Sasthamkotta.

In addition to the mini industrial estates, larger industrial estates are

available at Umayanallur and Karunagapally. The estate located in

Mundakkal has 53 units. Small Industries Development Corporation

(SIDCO) is also planning to establish mini industrial estates in Thalavoor,

Pooyappally, Karavalur, Piravanthoor and Nilamel.

In order to strengthen the traditional sector, of late, Govt. of India is

extending support for cluster development programmes. Coir, bamboo,

khadi, straw-based picture making, wood lace work and dairy products are

the chosen sectors. Craftsmen/Farmers working in these sectors will get

hand-holding support to optimise their production and marketing efficiency.

These sectors also will receive need-based infrastructure and training

support. The identified sectors also will receive support system, especially

101

under Infrastructure Growth Pole Concepts, approximating ` 20 crore.

Mango, jackfruit, papaya and pineapple are cultivated in the district

and therefore, good scope is available for the production of canned fruits

and juice, making pickle, jam, candy, chips, etc.

Infrastructure Availability

Kollam district is having a fairly well developed infrastructure under

Railway (135 km), Surface Road (15,000 k.m.), Water Transport, services

of the Post Offices, telephone connections, availability of Educational (927

including 14 Prof: Colleges), and health providing agencies (9 Govt.

Hospitals & 64 PHCs), dispensaries ensuring animal health, agencies

engaged in extension services under Agriculture, Animal Husbandry, Dairy

Development, Fisheries Development, Poultry etc. There are also

satisfactory service providing agencies under skill up-gradation programme

and agencies extending hand hold services for marketing produce, products

and services.

Increasing involvement of the Banks in Agriculture and Rural

Development necessitated credit planning at various levels. Based on the

felt need, a study group led by Prof: Gadgil4 has recommended a

methodology in 1969 for the development of credit and banking plans in the

country. The study group felt district as the most viable unit of area to

begin with the credit planning as data/information required for the same are

readily available at the district level. Based on the suggestions and

subsequent recommendations made by Nariman Committee5, Reserve

Bank of India (RBI) had given the shape for Lead Bank Scheme (LBS) in

1969.

The LBS envisaged identifying a commercial bank having large

number of branch network in the district to shoulder lead bank

102

responsibilities. The lead bank was required to act as a group leader for

coordinating the efforts of all the credit agencies operating within the district

for branch expansion and meeting the credit needs of the rural economy6.

For firming up a user-friendly District Credit Plan (DCP), the lead bank was

required to carry out detailed studies within the district. In order to achieve

viable integration of the District Credit Plans with District Development

Plans, District Consultative Committee (DCC) was also set up in the district

to serve as a forum for consultation and coordination among the banks and

district development functionaries. Based on the experience gained, RBI

finalized the guidelines for preparation of DCP. Based on the matured

guidelines, the second round of DCPs were prepared during 1980-82. This

was followed by yearly allocation of the credit targets among various banks

within a district. This instrument was known as Annual Action Plans

(AAPs).

CRAFICARD7 had assessed the LBS and the preparation of DCP

and AAP in 1981 and recommended certain changes. Based on the

Committee’s recommendation, RBI issued new guidelines and 3rd round of

DCP for the period 1983-85 was prepared in accordance with revised

guidelines. In 1987, RBI issued fresh guidelines and the fourth round of

DCPs were prepared for a period of 3 years, 1988-90, beginning from

January 1988. From 1991 onwards Service Area Plans (SAPs) were also

introduced and this further helped in formulation of more meaningful DCPs

in the fifth round, 1991-92. As at the end of 1993, LBS covered almost all

the 453 districts prevailing in India at that time.

For implementing the LBS, duties were assigned to i) Lead Bank ii)

Lead Bank Officer (LBO) appointed by the Lead Bank iii) District

Coordinators of the Non-Lead Bank iv) Lead District Officer (LDO) of RBI v)

Officers of NABARD entrusted with special duties of the District

Development Managers (DDMs) and posted at the respective district or

representatives of NABARD Regional Offices vi) District Consultative

103

Committee and its Standing Committee which supervise the scheme at the

district level vii) The District Level Review Committee which ensures

participation of non-officials in Credit Planning, viii) State Level Bankers’

Committee (SLBC) which coordinates the activities of financial institutions

at the state-level, and lastly, ix) State Level Coordination Committee which

coordinates the activities of financial institutions with those of the

Government Departments.

There are differences of opinion about the effects of LBS in achieving

its objectives of a well-balanced credit disbursements based on the credit

needs of the district. Agriculture Credit Review Committee (ACRC)8 had

viewed that though this scheme could create better awareness on the need

of credit planning, its implementing functionaries could not achieve much of

the scheme objectives. Absence of reliable data at the district and block

level, coupled with the poor coordination among the various development

agencies led to the poor implementation of the plans. To improve the

quality of the micro level credit programme, RBI has introduced Service

Area Approach based on the observations made by a team of the Chief

Executives of the Commercial Banks in 1987.

The Service Area Scheme introduced from April 1988 involved i)

Identification of the Service Area of each branch ii) Survey of the Service

Area to identify potential activities and the beneficiaries iii) Preparation of

credit plan on an annual basis iv) Coordination of the various development

agencies within the area and implementation of the plan; and, v) regular

monitoring of credit utilisation and timely recovery of the loan instalments.

This scheme also suffered from a number of operational problems

especially in regions with poor branch coverage. In such areas the

branches could not successfully cater to the credit requirements with the

available staff and poor transport facilities. Opening of new branches in

these areas was also felt difficult due to the non-availability of the required

104

support system. Thus, credit planning process in the country has

undergone considerable changes during the last decades. Highlighting

these limitations ACRC9 indicated that despite several blueprints evolved in

this regard, it has not made any serious effort at the level of implementation.

The committee viewed that for effective credit planning, it should be

backward-linked with developmental plans and forward-linked via credit

disbursement agencies with the borrowers.

The review committee felt that the District Development Plan should

be concerned with the targeting of output and investment both for private

and public functionaries unlike the national or state plans which have

concerned themselves only with planning of output and investment by

Central and State Government and Public Enterprises, leaving private

sector planning only to broad guidelines and indications.

After the formation of National Bank for Agriculture and Rural

Development (NABARD), the apex bank responsible for the development of

agriculture and rural areas felt the need for an in-depth planning process at

the micro-level. The bank introduced Potential Linked Credit Plan (PLP) in

1988. A new method of identifying the potential available in rural areas

with the help of Banks, Govt. Departments, Universities, Research Stations,

Commodity Development Boards, Service Providing Agencies,

Non-Government Agencies etc. was tried. Based on the existing potential,

exploitable potential during the plan period was identified and the cost and

the bank credit for the same were estimated along with the gap in

infrastructure and service sector support. For achieving the planned

programmes, banks were persuaded to meet the credit gap. Similarly, the

infrastructure and service providing agencies were also encouraged to meet

the needs during the planned period. The system is currently in operation

in all the 622 districts in Indian Union. RBI and the banking system

accepted PLP as the parent document for further credit planning process.

105

A well-integrated PLP with DCP and branch -wise allocation of the

credit targets enabled the branches to implement the programmes much

faster and more focussed. The system also helps the banking sector to

implement various priority sector-initiated development programmes of both

Central and State Governments. The availability of PLP during the

beginning of the year makes it convenient for banks and other sister

departments to make operational for the next financial year starting from 1st

April onwards. The regular review of DCP involving various banks and

representatives of development departments enabled smooth

implementation of the credit plans.

LBS Scheme in Kollam District

The Lead Bank Scheme (LBS) had its base on the need for ensuring

the smooth co-ordination of various institutional and development agencies

operating in the district. For this purpose, a coordinating agency consisting

of the Lead Bank, other Commercial Banks and Co-operative Banks,

representatives of various Development Departments at the district level,

representatives of apex level financial agencies such as RBI, NABARD and

SIDBI was formed. This was generally known as District Consultative

Committee (DCC). District Collector was designated as the Chairperson of

the forum in order to ensure the smooth functioning and to draw the required

inter- agency co-ordination for implementation of the various development

programmes of the district.

Constitution of the District Consultative Committee (DCC) was done

in all districts of Kerala right from the beginning of 1970. Along with the

function of Lead Bank Scheme and institution of DCCs, the Lead Bank was

also entrusted with the responsibility of preparation and implementation of

the Area Development Schemes within the district with special thrust on

priority sector and specific coverage programmes for socially and

106

economically weaker strata of the society.

Efforts of Lead Bank in their local area development through credit

business, met with different levels of success in the various districts during

the eighties. Implementation of DCPs was reviewed at the state-level

forums known as State Level Banker’s Committee (SLBCs). The SLBC

played an important role as inter-institutional forum for co-ordination and

joint implementation of various development programmes with the support

of bank credit. Though SLBC is basically a banker’s forum, State

Government representatives at higher level also participated with a view to

drawing inter- agency co-ordination for successful implementation of

development schemes/programmes. The SLBC meetings are generally

convened by the Lead Bank designated as Convener Bank.

In order to strengthen the Lead Bank Scheme, a State Level

Co-ordination Committee was also constituted during the mid-seventies in

Kerala. This forum co-ordinated the developmental programmes of banks

and drew support from State Government Departments. The forum also

reviewed the progress in implementation of special programmes. It also

sought legislative and administrative support from the State Government

based on specific requirements. The infrastructure and linkage facilities

required for increasing credit absorption is also highlighted and necessary

support ensured. The system during the last two decades got well

established in Kerala and the preparation of PLP, DCP and branch-wise

allocation, implementation and their reviews have become a regular

practice in Kerala and among her 14 districts.

Review of DCP in Kollam District

Kollam is a representative district of Kerala state. It has large

backwaters, dense forest, reserve forest, three rivers and large costalline.

It has border with state capital Thiruvananthapuram district, Alappuzha and

Pathanamthitta on the North and North-East. Arabian Sea is bounded on

107

the West and Western Ghats at the East bordering with Tamil Nadu. The

district has 26 lakh population, of which, nearly 18 per cent are urban and

remaining 72 per cent are rural. The SC and ST population comprises about

10 per cent and 1.5 per cent respectively. For administrative convenience,

the district is divided into fve Taluks, 13 Development Blocks and 71 Grama

Panchayaths. The headquarter Kollam is a Corporation and it has two

Municipalities. The district is having a fairly high rate of literacy rate at 92 per

cent. Primary sector contributes 27 per cent to the state economy and

secondary sector 24 per cent. The tertiary sector contributes the highest of

49 per cent. During the last three decades, contribution of agriculture

recorded a declining trend compared to the other two sectors. Smaller

size of land holdings (98 % below one hectare.) appeared to be the major

constraint.

The district has a fairly wellspread coverage of banks. It has 207

branches of Commercial Banks, 55 branches of District Central

Co-operative Bank (DCCB), 121 Primary Agriculture Co-operative Societies

(PACS) and four Primary Co-operative Agriculture and Rural Development

Banks (PCARDB). For credit planning purposes, NABARD prepares

Potential Linked Credit Plans (PLP) for each financial year. Through this

exercise the District Development Manager (DDM) posted at the district

prepares a list of tapable investments in the district with the assistance of

bank credit. This information is communicated to all the bank branches in

each block. Based on the available potential, the branches prepare their

Annual Credit Plans and these are further aggregated at the block level.

Subsequently, the block credit plans are aggregated at the district level and

state level. The process enable mapping of the potentials in a local area,

ensures bank credit facilities for their exploitation and also ensures

infrastructure and service support at local area, block and district levels.

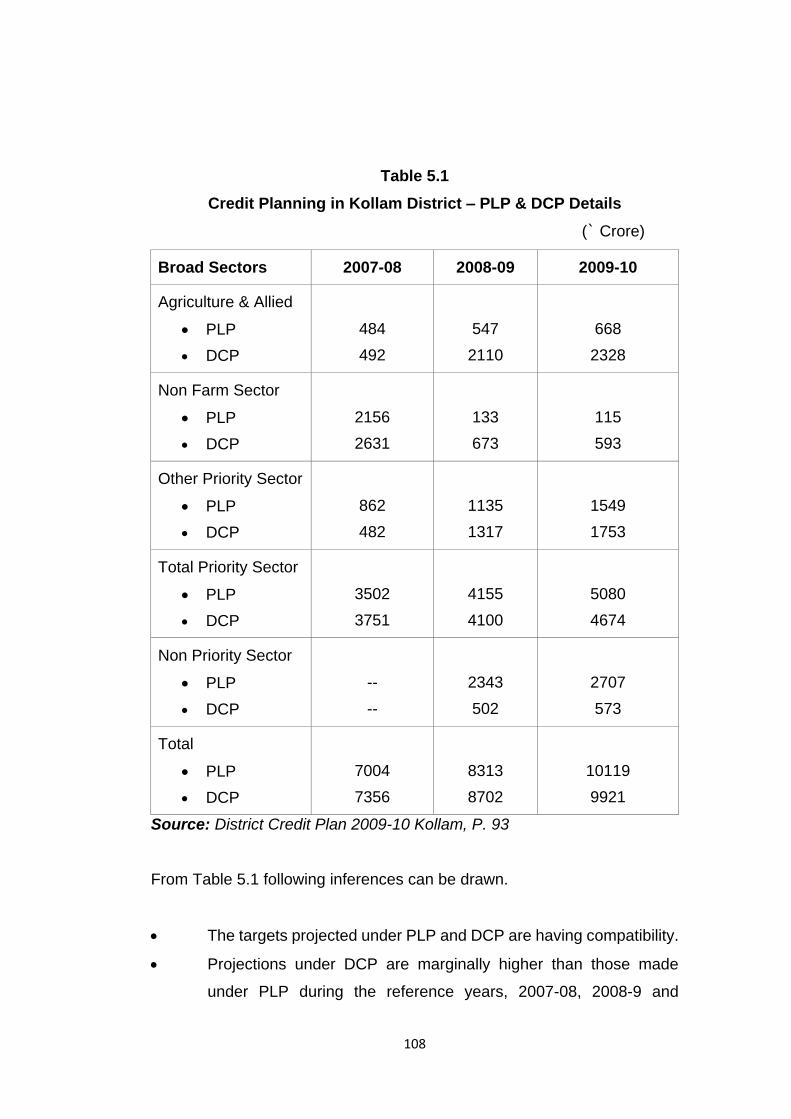

In order to have an idea on PLP projection viz-a-viz projections made

under DCP, the data regarding the latest 3 years is presented in Table 5.1

108

Table 5.1

Credit Planning in Kollam District – PLP & DCP Details

(` Crore)

Broad Sectors 2007-08 2008-09 2009-10

Agriculture & Allied

PLP

DCP

484

492

547

2110

668

2328

Non Farm Sector

PLP

DCP

2156

2631

133

673

115

593

Other Priority Sector

PLP

DCP

862

482

1135

1317

1549

1753

Total Priority Sector

PLP

DCP

3502

3751

4155

4100

5080

4674

Non Priority Sector

PLP

DCP

--

--

2343

502

2707

573

Total

PLP

DCP

7004

7356

8313

8702

10119

9921

Source: District Credit Plan 2009-10 Kollam, P. 93

From Table 5.1 following inferences can be drawn.

The targets projected under PLP and DCP are having compatibility.

Projections under DCP are marginally higher than those made

under PLP during the reference years, 2007-08, 2008-9 and

109

2009-10.

Among the broad sectors, viz. Agriculture & Allied, NFS and Other

Priority Sector, the variation in projection is observed larger in the

case of Agriculture & Allied Sector, followed by Non-Farm Sector.

Limitations caused in data compilation in both the agencies can be

one of the reasons for wide variation. This is relatively more

reflected in the data available during the year 2007-08 in the case of

NFS and Other Priority Sector.

More careful treatment of the data by the Lead Bank and NABARD

is required for better compatibility.

Credit Flow in Kollam District

On successful preparation of the Credit Plans at branch level, block

level and at the district level, the banking sector implements the credit

programmes on a regular basis. The same is also reviewed regularly by

the controlling banks and various review forums at block level and district

level. The banks also are required to implement various development

programmes such as Swarna Jayanthi Gram Swarozgar Yojana (SGSY),

Swarna Jayanthi Shahari Rozgar Yojana (SJSRY), Prime Minister’s

Employment Generation Programme (PMEGP) etc. In addition to the

above, various development departments of both State and Central

Governments also seek active co-operation of the banking sector for

implementation of specific programmes initiated under both Farm and Non-

Farm Sector. Project initiated by Department of Agriculture, Horticulture

Mission, NFS Activities supported by KVIC and KVIB etc. are examples.

In the following write up an attempt is made to review the credit flow

in Kollam district under the broad sectors, against their planned programme

and actual achievements. At the initial stage, in order to have an overall

assessment, the analysis is carried out among the broad sectors, viz. Farm

Sector, Non-Farm Sector and Other Priority Sector. The results are

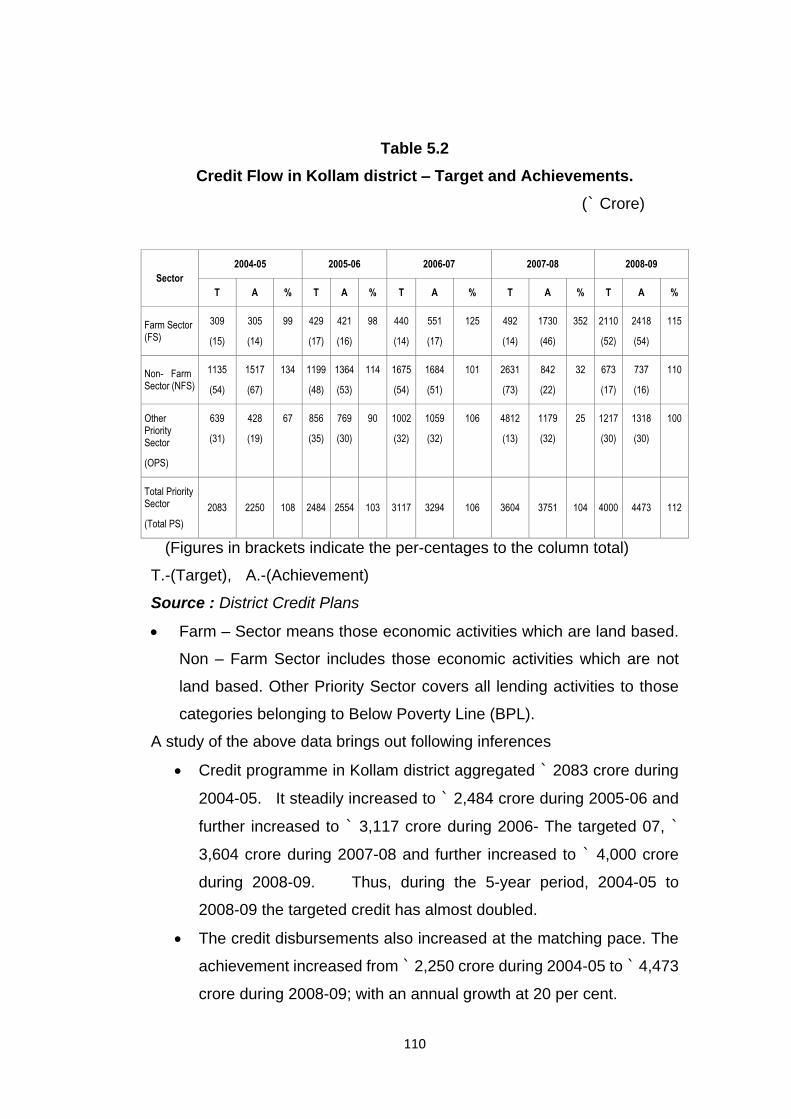

tabulated in Table 5.2.

110

Table 5.2

Credit Flow in Kollam district – Target and Achievements.

(` Crore)

Sector

2004-05 2005-06 2006-07 2007-08 2008-09

T A % T A % T A % T A % T A %

Farm Sector (FS)

309

(15)

305

(14)

99 429

(17)

421

(16)

98 440

(14)

551

(17)

125 492

(14)

1730

(46)

352 2110

(52)

2418

(54)

115

Non- Farm Sector (NFS)

1135

(54)

1517

(67)

134 1199

(48)

1364

(53)

114 1675

(54)

1684

(51)

101 2631

(73)

842

(22)

32 673

(17)

737

(16)

110

Other Priority Sector

(OPS)

639

(31)

428

(19)

67 856

(35)

769

(30)

90 1002

(32)

1059

(32)

106 4812

(13)

1179

(32)

25 1217

(30)

1318

(30)

100

Total Priority Sector

(Total PS)

2083 2250 108 2484 2554 103 3117 3294 106 3604 3751 104 4000 4473 112

(Figures in brackets indicate the per-centages to the column total)

T.-(Target), A.-(Achievement)

Source : District Credit Plans

Farm – Sector means those economic activities which are land based.

Non – Farm Sector includes those economic activities which are not

land based. Other Priority Sector covers all lending activities to those

categories belonging to Below Poverty Line (BPL).

A study of the above data brings out following inferences

Credit programme in Kollam district aggregated ` 2083 crore during

2004-05. It steadily increased to ` 2,484 crore during 2005-06 and

further increased to ` 3,117 crore during 2006- The targeted 07, `

3,604 crore during 2007-08 and further increased to ` 4,000 crore

during 2008-09. Thus, during the 5-year period, 2004-05 to

2008-09 the targeted credit has almost doubled.

The credit disbursements also increased at the matching pace. The

achievement increased from ` 2,250 crore during 2004-05 to ` 4,473

crore during 2008-09; with an annual growth at 20 per cent.

111

During the 5-year reference period, in all the years the target was

achieved. The rate of achievement was 108 per cent during

2004-05 and it was the highest in 2008-09 at 112 per cent. Among

the three broad sectors, the achievement under Farm Sector and

Non- Farm Sector was at 99 per cent and 134 per cent respectively;

while the achievement under Other Priority Sector lagged behind at

67 per cent during the year 2004-05. This trend marginally

improved during the year 2005-06 and the achievement under Other

Priority Sector recorded at 90 per cent of the target and further rose

to 106 per cent during 2006-07 but drastically decreased to 25per

cent during 2007-08 and during 2008-09 the targeted credit was

achieved at 108 per cent.

In the case of Non-Farm Sector, the targeted credit was unable to

achieve in the year 2007-08 and the rest of the years it was achieved.

The achievement of the targeted credit might have been influenced

by many factors such as market demand for credit during the

reference year, incentives extended, initiatives made by the credit

agencies and the pattern of allocation of the credit targets. During

the year 2004-05, 54 per cent of the allocation was made under NFS

followed by 31 per cent under OPS and the remaining 15 per cent

under Farm Sector. Almost the same trend continued during the

period 2005-06 and 2006-07. During 2007-08, the allocation under

NFS was as high as 73 per cent. However, during 2008-09 the

allocation was drastically reduced to 16 per cent and the allocation

under Farm Sector increased to 53 per cent and OPS 30 per cent.

The relatively higher allocation under NFS during 2005-06, 2006-07

and 2007-08 reflected the higher priority given to this sector.

Further, based on the national policy, more importance was given to

the allocation under Agriculture Sector based on the national needs.

Similar policy implementation was also observed in Gujarat10 where

people’s participation was encouraged by the Govt. of Gujrat through

“Krishi Mahotsav” or “Rath” sort of festivities to enthuse the public for

112

productive utilization of the institutional credit.

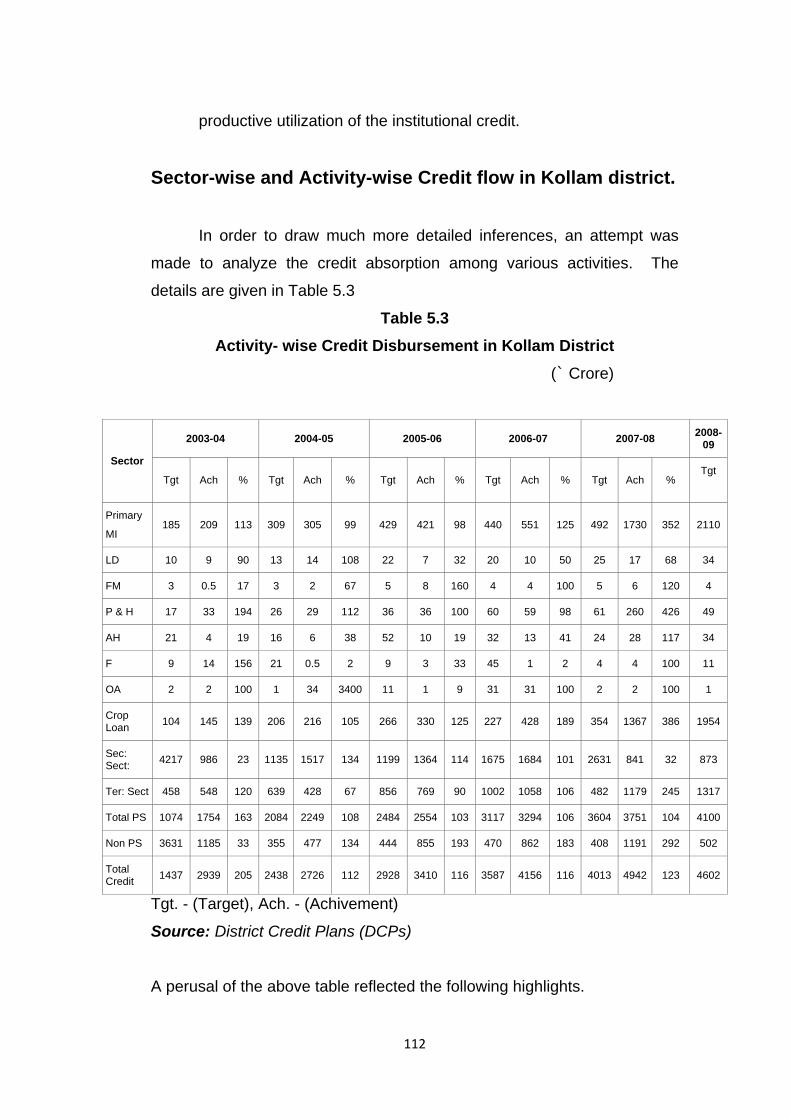

Sector-wise and Activity-wise Credit flow in Kollam district.

In order to draw much more detailed inferences, an attempt was

made to analyze the credit absorption among various activities. The

details are given in Table 5.3

Table 5.3

Activity- wise Credit Disbursement in Kollam District

(` Crore)

Sector

2003-04 2004-05 2005-06 2006-07 2007-08 2008-

09

Tgt Ach % Tgt Ach % Tgt Ach % Tgt Ach % Tgt Ach % Tgt

Primary

MI 185 209 113 309 305 99 429 421 98 440 551 125 492 1730 352 2110

LD 10 9 90 13 14 108 22 7 32 20 10 50 25 17 68 34

FM 3 0.5 17 3 2 67 5 8 160 4 4 100 5 6 120 4

P & H 17 33 194 26 29 112 36 36 100 60 59 98 61 260 426 49

AH 21 4 19 16 6 38 52 10 19 32 13 41 24 28 117 34

F 9 14 156 21 0.5 2 9 3 33 45 1 2 4 4 100 11

OA 2 2 100 1 34 3400 11 1 9 31 31 100 2 2 100 1

Crop Loan

104 145 139 206 216 105 266 330 125 227 428 189 354 1367 386 1954

Sec: Sect:

4217 986 23 1135 1517 134 1199 1364 114 1675 1684 101 2631 841 32 873

Ter: Sect 458 548 120 639 428 67 856 769 90 1002 1058 106 482 1179 245 1317

Total PS 1074 1754 163 2084 2249 108 2484 2554 103 3117 3294 106 3604 3751 104 4100

Non PS 3631 1185 33 355 477 134 444 855 193 470 862 183 408 1191 292 502

Total Credit

1437 2939 205 2438 2726 112 2928 3410 116 3587 4156 116 4013 4942 123 4602

Tgt. - (Target), Ach. - (Achivement)

Source: District Credit Plans (DCPs)

A perusal of the above table reflected the following highlights.

113

Minor Irrigation (MI), Land Development (LD), Farm Mechanization

(FM), Plantation and Horticulture (P&H), Fisheries (F) and Other

Activities (OA) were the important sub sectors which absorbed

sizable quantum of credit during the reference period under the

study.

Minor Irrigation

Under Primary Sector, MI allocation was increased from ` 185 crore

during 2003-04 to ` 309 crore during 2004-05 and further increased

to ` 429 crore and 440 crore during 2005-06 and 2006-07

respectively. In the year 2007-08 the allocation was at ` 492 crore

and the achievement was at ` 1,730 crore, 352 per cent of the target.

Considering this fact the allocation during 2008-09 was kept at a high

level of ` 2,110 crore. The credit disbursement under MI was also

satisfactory during the reference period and it recorded large

achievement potential from the year 2006-07 onwards.

Land Development

Owing to the limited potential under LD the credit allocation under

this activity ranged from ` 10 crore during 2003-04 to ` 25 crore

during 2007-08 and further the target was kept at ` 34 crore during

2008-09. The achievement under this sector fell short of the targets

during the year 2003-04 at 90 per cent, 34 per cent during 2005-06,

50 percent during 2006-07 and 68 per cent during 2007-08. Thus

except during the year 2004-05 when the achievement was at 108

per cent, during all the years the target could not be achieved.

Farm Mechanisation

The small size of landholding was one of the limiting factors for credit

114

absorption under Farm Mechanisation (FM). The targets envisaged

under this sector ranged from ` 3 crore during 2003-04 and ` 5 crore

during 2007-08. The achievement under the sector also was less

attractive in most of the years except during 2005-06 and 2007-08,

both the years the target was achieved. During 2003-04 and

2004-05 the achievement was only at 17 per cent and 67 per cent of

the targets.

Plantation and Horticulture

The credit allocation under Plantation and Horticulture (P & H)

ranged from ` 17 crore during 2003-04 to ` 61 crore during 2007-08.

During the earlier reference of the period the targets were achieved

at 194 per cent during 2003-04 and at 116 per cent during 2004-05.

However, during 2006-07 the target marginally fell short at 98 per

cent. However, it picked up during 2007-08 at 426 per cent.

Animal Husbandry

Under Animal Husbandry (AH) the achievement was much lower

compared to the credit allocation. In spite of a larger size of rural

area in Kollam district and availability of the required infrastructure for

dairy development the credit allocation ranged from ` 21 crore during

2003-04 to ` 52 crore during 2005-06. Subsequently during

2006-07 and 2007-08 the credit allocations were at ` 32 crore

and ` 24 crore respectively. In most of the years the targets were

not achieved. The achievements were as low as 19 per cent during

2003-04 and 2005-06. The highest achievement was recorded at

117 per cent during 2007-08. During this year, as against the

targeted ` 24 crore the achievement recorded ` 28 crore.

115

Fisheries

Under fisheries sector, the targeted credit ranged from ` 9 crore

during 2003-04 to ` 45 crore during 2006-07. The pattern of

allocation records inconsistencies. During 2004-05 the allocation

was ` 21 crore whereas during 2005-06 it was kept at ` 9 crore and

further increased to ` 45 crore during 2006-07; and, the target was

kept at very low at ̀ 4 crore during 2007-08. The achievements also

recorded erratic trends. It was at 156 per cent during 2003-04 and as

low as two per cent during 2004-05 and 2006-07. Inspite of a long

coastline and a developed fishing harbour at Sakthikulangara and a

large area of backwater and different fish varieties having potential

for their culture, value addition and trade, the credit absorption under

this sector remained poor in Kollam district.

Other Activities

Under Other Activities the credit targets increased from ` 2 crore

to ` 11 crore during 2003-04 and 2005-06; and ` 31 crore during

2006-07 and further a very low allocation at ` 2 crore was made

during 2007-08. The credit disbursement during the year 2003-04

under this sector was ` 2 crore only. It increased to ` 34 crore

during 2004-05, and subsequentlyfel down to ` 31 crore during

2006-07. During 2004-05 and 2007-08 the achievements were

reported at a very low level of ` 1 crore and ` 2 crore respectively.

Crop Loan

The targeted credit programme under Crop Loan during the

reference period, 2003-04 to 2007-08, reflected unusual

inconsistency. During 2003-04 the target was kept at ` 104 crore;

during 2004-05 it was ` 206 crore and during 2005-06 the target was

116

further increased to ` 266 crore. Thus, a steady increasing trend

reflected during the 3 years. However, during 2006-07 the target

was kept at ` 227 crore and then further increased to ` 354 crore

during 2007-08. However, the achievement during these 2 years

exceeded the target and registered 186 per cent and 386 per cent

respectively. Further, the target during 2008-09 was kept at ` 1,954

crore. The reason for keeping a lower target compared to the

previous year especially when the achievements were made need

further probing. It appears that there are missing links in

professionalism in fixing credit target, especially under Crop Loan.

All the 5-year period the credit disbursement under Crop Loan in

Kollam district was more than the targeted allocations. The

achievement ranged from 105 per cent during 2004-05 to as high as

386 per cent during 2007-08. During this year as against the target

of ` 354 crore the achievement stood at ` 1,367 crore. The pattern

of disbursement warrants indepth studies on credit allocation and

end utilisation.

Secondary Sector

Under Secondary Sector, the credit allocation reflected larger

inconsistencies inspite of the existence of PLP, block level and

district level monitoring committees and District Industries Centre

(DIC), a department exclusively to take care of the development

activities under the Secondary Sector. The targeted credit under

this sector during 2003-04 was as high as ̀ 4,217 crore of which only

` 986 crore was disbursed and the disbursement worked out only at

23 per cent. Considering the low level of achievement the target

during 2004-05 was kept at ` 1,135 crore and the achievement was

at ` 1,517 crore, at 134 per cent. The target during 2005-06 and

2006-07 was further kept at ` 1,199 crore and ` 1,675 crore

respectively. The achievement during this two years worked out to

117

114 per cent and 101 per cent respectively. During the year

2007-08, as against the allocated target of ` 2,631 crore. The

achievement was only at ` 841 crore, at 32 per cent. This might

have compelled for a smaller allocation of the target under this sector

during 2008-09 at ` 873 crore. Thus the analysis clearly brings out

the fact that the credit allocation under Secondary Sector in Kollam

district need much more scientific analysis for assessing the effective

demand of credit.

Tertiary Sector

Both credit allocation and utilisation trends under Tertiary Sector

reflected less attractive trends in Kollam district during the reference

period. In spite of the increasing contribution of Tertiary Sector in

the district’s economy, the credit allocation under this sector ranged

from ` 458 crore during 2003-04 to ` 1,317 crore during 2008-09.

The trends in allocation reflected a steady increase during the first 4

years. However, during 2007-08 the allocation was only 46 per cent

of the earlier achievement during 2006-07. However, the

achievement during the year was at ̀ 1,179 crore, 245 per cent of the

targeted programme at ` 482 crore.

Priority Sector - Total

The Priority Sector achievement totalled ` 1,754 crore during

2003-04 and gone up to ` 3,751 crore during 2007-08. The annual

increase worked out to 23 per cent. The achievement under Priority

Sector was highest at 163 per cent during the year 2003-04 and it

was at the lowest at 103 per cent during 2005-06.

Non-Priority Sector - Total

The credit allocation under Non-Priority Sector also reflected

118

inconsistencies, perhaps due to the changes happened in data

aggregation. The target under the sector during 2003-04 was kept

at ` 3,631 crore. The same was kept at ` 355 crore during 2004-05

and marginally increased to ` 444 crore , ` 470 crore and ` 408 crore

during the subsequent years 2005-06, 2006-07, 2007-08

respectively. The target during 2008-09 is kept at `502 crore.

Except during the year 2003-04 the achievement during the

subsequent years were at 134 per cent, 193 per cent, 183 per cent

and 292 per cent respectively.

Total Credit

The total credit disbursement in Kollam district recorded at ` 2,939

crore during 2003-04. During the subsequent year, 2004-05 the

total credit disbursement marginally declined to ` 2,726 crore.

During the year 2005-06 the credit disbursement totalled ` 3,410

crore and increased to ̀ 4,156 crore during 2006-07 and further to ̀

4,942 crore during 2007-08. Thus, the credit absorption in Kollam

district during the reference period, 2003-04 to 2007-08, has

increased only at 17 per cent per annum. The achievement fell

short of the general ambition to double the institutional credit at 5

year interval.

The above highlights enable to draw the following inferences.

The credit planning process at the branch level, the block level and

the district level need much more careful and scientific approach to

contain the exploitable potential under each sector. Though a

regular exercise is being attempted to contain the aspirations

envisaged under the PLP, a perusal of the time series data even for a

short interval of 5- year period reflected avoidable limitations.

The allocations under subsectors such as MI, LD, FM, PH, AH and

fisheries deserve much more realistic approach to contain the

119

potential which can be addressed in each of these sectors. For this

purpose a deliberate attempt to increase the effective demand for

credit by the true entrepreneurs is needed. This is a larger subject

and can be addressed only through collective efforts of all the

development departments, local forums of farmers, investors under

Dairy, Fishery, PH, AH, MI and LD.

Along with credit planning and implementation, empowerment of the

prospective entrepreneurs is a subject which is lagging in the district.

Proper awareness among the leadership in local-self governments,

local forums, local functionaries of the Government and bankers

along with the handholding of the market operators can change the

scenario and change the present negligible status of bank credit on

National Domestic Product (NDP) as observed by Kuldip and

Seema11.

Review of Govt. Sponsored Schemes in Kollam District

Under poverty alleviation for employment generation and

empowerment of specific target groups both the Government of India and

State Government implemented a series of development

schemes/programmes with the help of banks. Swarnajayanthi Gram

Swarozgar Yojana (SGSY), Swarna Jayanthi Shahari Rozgar Yojana

(SJSRY), Prime Minister’s Rozgar Yojana (PMRY), USEP, DWCRA etc. are

the major programmes. An attempt is made below to study the extent of

achievement under these programmes with the support of institutional

credit.

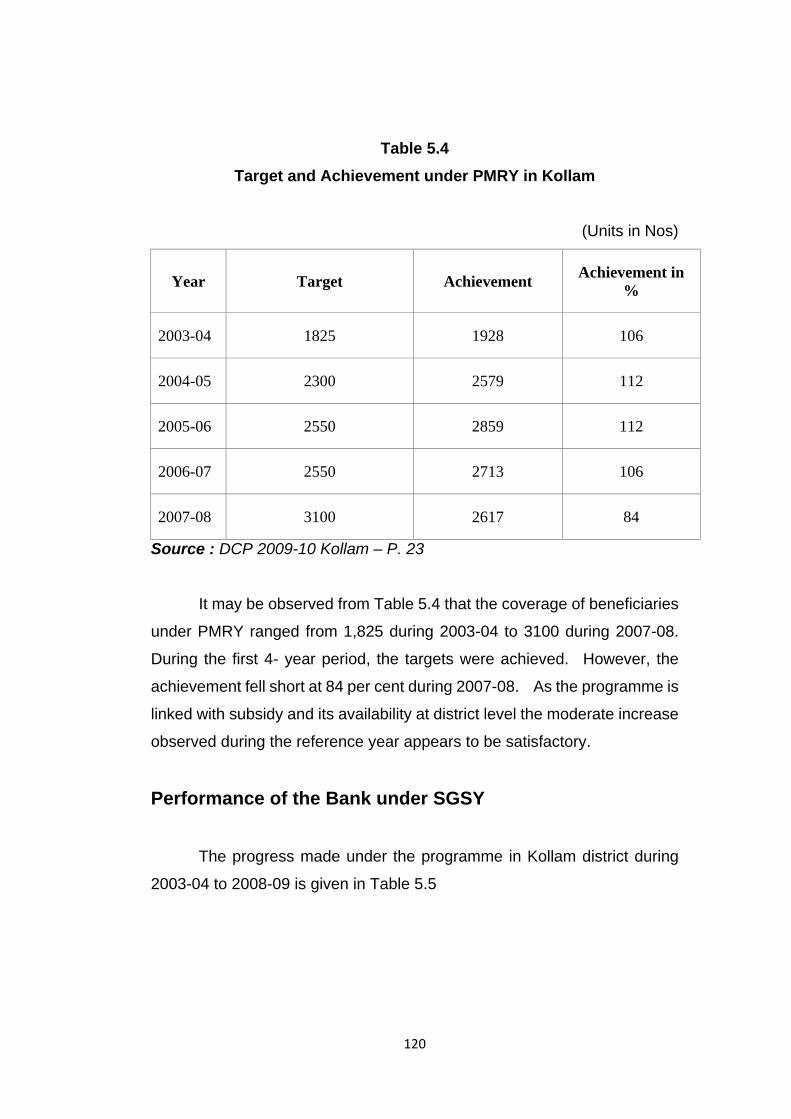

Performance of the Bank under PMRY

The Target vis-a-vis achievement made under this programme

during the last 5 year period, 2003-04 to 2007-08 is given in Table 5.4

120

Table 5.4

Target and Achievement under PMRY in Kollam

(Units in Nos)

Year Target Achievement Achievement in

%

2003-04 1825 1928 106

2004-05 2300 2579 112

2005-06 2550 2859 112

2006-07 2550 2713 106

2007-08 3100 2617 84

Source : DCP 2009-10 Kollam – P. 23

It may be observed from Table 5.4 that the coverage of beneficiaries

under PMRY ranged from 1,825 during 2003-04 to 3100 during 2007-08.

During the first 4- year period, the targets were achieved. However, the

achievement fell short at 84 per cent during 2007-08. As the programme is

linked with subsidy and its availability at district level the moderate increase

observed during the reference year appears to be satisfactory.

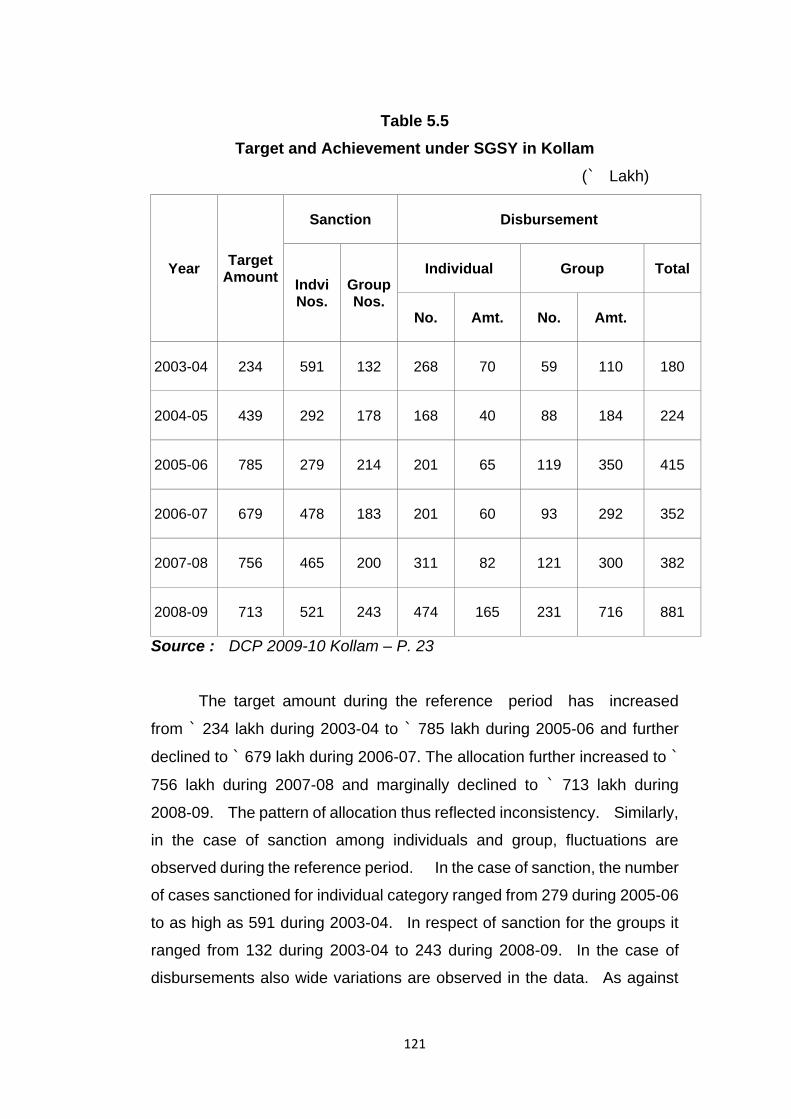

Performance of the Bank under SGSY

The progress made under the programme in Kollam district during

2003-04 to 2008-09 is given in Table 5.5

121

Table 5.5

Target and Achievement under SGSY in Kollam

(` Lakh)

Year Target

Amount

Sanction Disbursement

Indvi Nos.

Group Nos.

Individual Group Total

No. Amt. No. Amt.

2003-04 234 591 132 268 70 59 110 180

2004-05 439 292 178 168 40 88 184 224

2005-06 785 279 214 201 65 119 350 415

2006-07 679 478 183 201 60 93 292 352

2007-08 756 465 200 311 82 121 300 382

2008-09 713 521 243 474 165 231 716 881

Source : DCP 2009-10 Kollam – P. 23

The target amount during the reference period has increased

from ` 234 lakh during 2003-04 to ` 785 lakh during 2005-06 and further

declined to ` 679 lakh during 2006-07. The allocation further increased to `

756 lakh during 2007-08 and marginally declined to ` 713 lakh during

2008-09. The pattern of allocation thus reflected inconsistency. Similarly,

in the case of sanction among individuals and group, fluctuations are

observed during the reference period. In the case of sanction, the number

of cases sanctioned for individual category ranged from 279 during 2005-06

to as high as 591 during 2003-04. In respect of sanction for the groups it

ranged from 132 during 2003-04 to 243 during 2008-09. In the case of

disbursements also wide variations are observed in the data. As against

122

the sanction of 591 under individual during 2003-04 only 268 cases of

disbursements were made. Similarly, during the same year out of the 132

cases sanctioned under groups, in 59 cases only the loan amount was

disbursed. Similar trends are observed during all the years covered under

the study. In the case of overall disbursement and increase is recorded

during the year 2003-04. The disbursement under SGSY totalled ` 180

lakh during 2003-04. It has gone up to ` 881 lakh during the year 2008-09.

However, yearly fluctuations were also observed especially during 2006-07.

The pattern of loan sanction and disbursement under SGSY in

Kollam district do not reflect a steady increasing trend. It depends more on

the initiatives of the programme implementing functionaries during the

respective years. The wide variations in sanction and disbursement

reflected the limited skill and professionalism of the programme

implementing agencies and the inadequate zeal of the identified

beneficiaries. There is large scope for the programme implementing

functionaries for the right identification of promising entrepreneurs under

SGSY. Wider awareness programmes coupled with need-based training

and handholding may result in minimizing the existing gap between

sanction and disbursement.

Performance of the Bank under SJSRY

Under Swarna Jayanthi Shahari Rozgar Yojana (SJSRY), Urban Self

Employment Programme (USEP) and Development of Women and

Children in Rural Area (DWCRA) were the two major development

programmes in which banks have participated in Kollam district.

Involvement of the banks in implementing these two programmes during

2003-04 and 2007-08 is given in Table 5.5

123

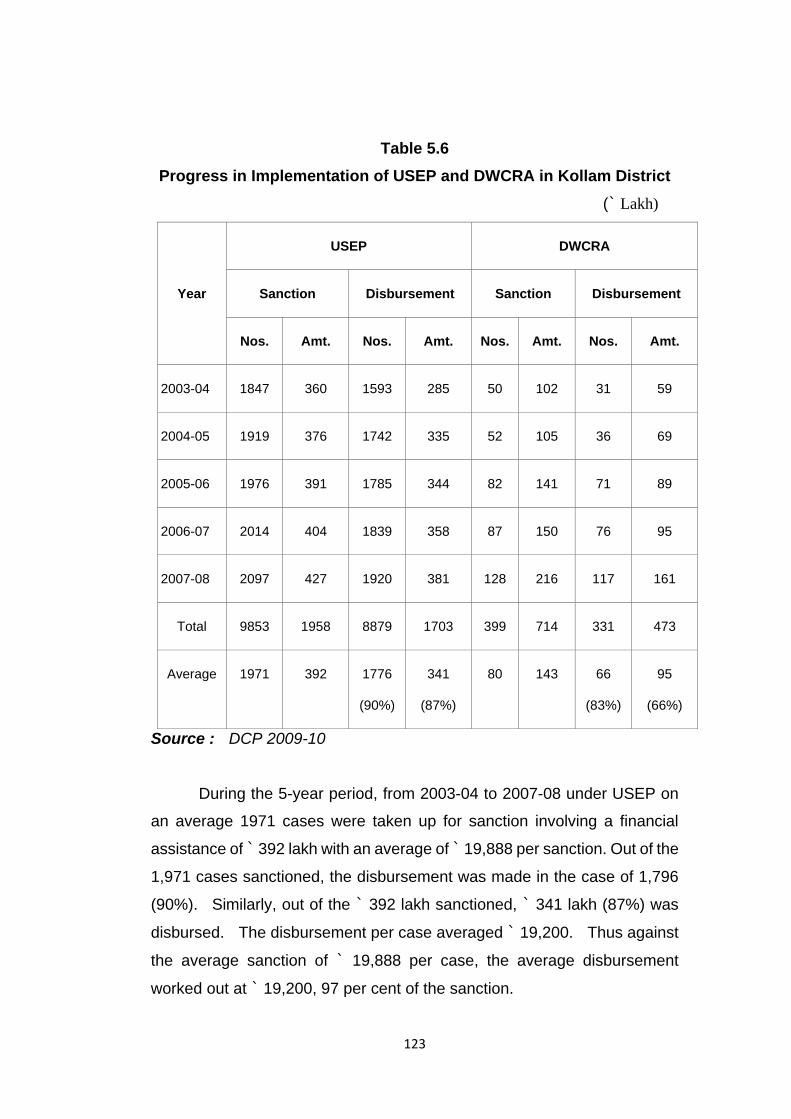

Table 5.6

Progress in Implementation of USEP and DWCRA in Kollam District

(` Lakh)

Year

USEP DWCRA

Sanction Disbursement Sanction Disbursement

Nos. Amt. Nos. Amt. Nos. Amt. Nos. Amt.

2003-04 1847 360 1593 285 50 102 31 59

2004-05 1919 376 1742 335 52 105 36 69

2005-06 1976 391 1785 344 82 141 71 89

2006-07 2014 404 1839 358 87 150 76 95

2007-08 2097 427 1920 381 128 216 117 161

Total 9853 1958 8879 1703 399 714 331 473

Average 1971 392 1776

(90%)

341

(87%)

80 143 66

(83%)

95

(66%)

Source : DCP 2009-10

During the 5-year period, from 2003-04 to 2007-08 under USEP on

an average 1971 cases were taken up for sanction involving a financial

assistance of ̀ 392 lakh with an average of ̀ 19,888 per sanction. Out of the

1,971 cases sanctioned, the disbursement was made in the case of 1,796

(90%). Similarly, out of the ` 392 lakh sanctioned, ` 341 lakh (87%) was

disbursed. The disbursement per case averaged ` 19,200. Thus against

the average sanction of ` 19,888 per case, the average disbursement

worked out at ` 19,200, 97 per cent of the sanction.

124

The per year sanction and disbursement under USEP over the years

2003-04 to 2007-08 recorded steady increasing trend. The number of

cases sanctioned increased from 1,847 during 2003-04 to 2097 during

2007-08. During the same period, the sanction amount also recorded

steady increase from ` 360 lakh to ` 427 lakh . In accordance with the

sanction the disbursement under USEP also steadily increased from 1,593

during 2003-04 to 1,920 during 2007-08. In the case of disbursement also

steady increase was recorded during the period. The disbursement under

USEP rose from ` 285 lakh during 2003-04 to ` 381 lakh during 2007-08.

The above analysis indicates that the banks in Kollam district have

actively participated in implementing Urban Self Employment Programme

during the reference period 2003-04 to 2007-08. The participation

recorded steady increasing trends in both sanction and disbursement. In

the case of sanction, the partner agencies could achieve a steady

increasing trend in extending the programme to an increasing number of the

needy.

Performance of the Bank under DWCRA

Banks participation in implementing the programme, Development of

Women and Children in Rural Area, in Kollam district during the period

2003-04 and 2007-08 is given in Table 5.6 As under USEP, the

performance under DWCRA also recorded increasing trends under both

sanction and disbursements. During the reference period, on an average

as against the targeted 80 cases per annum, the banks could assist 66

cases and the achievement worked out at 83 per cent. Similarly, as

against the targeted sanction of ` 143 lakh per annum the actual

disbursement work out ` 95 lakh, at 66 per cent. The per account sanction

and disbursement worked out to ` 55,882 and ` 1,42,900 respectively.

Thus, as against the sanction, the per account disbursement worked out to

125

039 per cent only. The analysis thus indicate that there is a large scope for

increasing the quantum of financial assistance extended to the beneficiaries

under DWCRA. A more careful and scientific approach is warranted from

all the programme implementing functionaries.

Broad Sector-wise and Agency-wise Ground Level Credit

Flow

Sector-wise Credit Flow

In order to study the Ground Level Credit flow (GLC) in Kollam

district, an attempt has been made to analyze credit flow from 2004-05 to

2008-09. The analysis is carried out for the broad sectors like Crop Loan

(ST), Term Loan, both Medium Term (MT) and Long Term (LT), Non -Farm

Sector (NFS) and Other Priority Sector (OPS). The agencies are classified

as Commercial Banks (CBs), State Co-operative Bank (SCB), State

Co-operative Agriculture and Rural Development Bank (SCARDB) and

Regional Rural Bank (RRB). To appreciate the credit delivery system, a

simple average of 5- year period is worked out and the results are presented

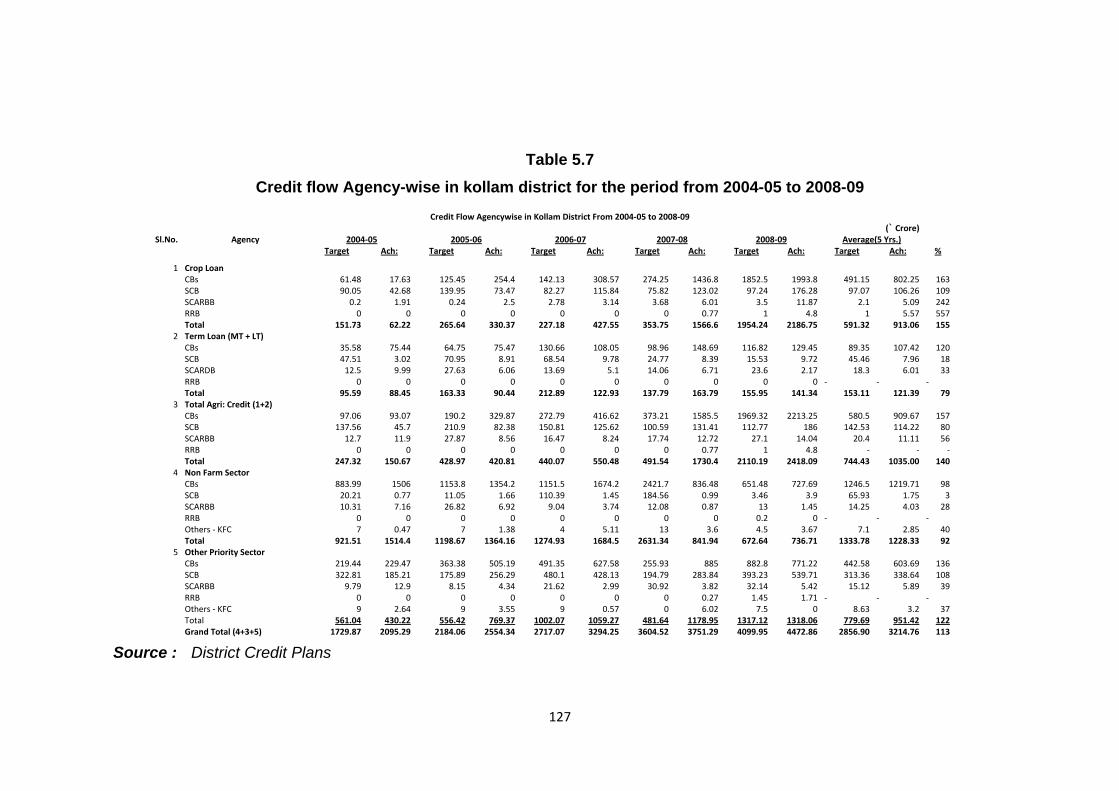

in table 5.7

127

Table 5.7

Credit flow Agency-wise in kollam district for the period from 2004-05 to 2008-09

Credit Flow Agencywise in Kollam District From 2004-05 to 2008-09

(` Crore)

Sl.No. Agency 2004-05 2005-06 2006-07 2007-08 2008-09 Average(5 Yrs.)

Target Ach: Target Ach: Target Ach: Target Ach: Target Ach: Target Ach: %

1 Crop Loan

CBs 61.48 17.63 125.45 254.4 142.13 308.57 274.25 1436.8 1852.5 1993.8 491.15 802.25 163

SCB 90.05 42.68 139.95 73.47 82.27 115.84 75.82 123.02 97.24 176.28 97.07 106.26 109

SCARBB 0.2 1.91 0.24 2.5 2.78 3.14 3.68 6.01 3.5 11.87 2.1 5.09 242

RRB 0 0 0 0 0 0 0 0.77 1 4.8 1 5.57 557

Total 151.73 62.22 265.64 330.37 227.18 427.55 353.75 1566.6 1954.24 2186.75 591.32 913.06 155 2 Term Loan (MT + LT)

CBs 35.58 75.44 64.75 75.47 130.66 108.05 98.96 148.69 116.82 129.45 89.35 107.42 120

SCB 47.51 3.02 70.95 8.91 68.54 9.78 24.77 8.39 15.53 9.72 45.46 7.96 18

SCARDB 12.5 9.99 27.63 6.06 13.69 5.1 14.06 6.71 23.6 2.17 18.3 6.01 33

RRB 0 0 0 0 0 0 0 0 0 0 - - -

Total 95.59 88.45 163.33 90.44 212.89 122.93 137.79 163.79 155.95 141.34 153.11 121.39 79 3 Total Agri: Credit (1+2)

CBs 97.06 93.07 190.2 329.87 272.79 416.62 373.21 1585.5 1969.32 2213.25 580.5 909.67 157

SCB 137.56 45.7 210.9 82.38 150.81 125.62 100.59 131.41 112.77 186 142.53 114.22 80

SCARBB 12.7 11.9 27.87 8.56 16.47 8.24 17.74 12.72 27.1 14.04 20.4 11.11 56

RRB 0 0 0 0 0 0 0 0.77 1 4.8 - - -

Total 247.32 150.67 428.97 420.81 440.07 550.48 491.54 1730.4 2110.19 2418.09 744.43 1035.00 140 4 Non Farm Sector

CBs 883.99 1506 1153.8 1354.2 1151.5 1674.2 2421.7 836.48 651.48 727.69 1246.5 1219.71 98

SCB 20.21 0.77 11.05 1.66 110.39 1.45 184.56 0.99 3.46 3.9 65.93 1.75 3

SCARBB 10.31 7.16 26.82 6.92 9.04 3.74 12.08 0.87 13 1.45 14.25 4.03 28

RRB 0 0 0 0 0 0 0 0 0.2 0 - - -

Others - KFC 7 0.47 7 1.38 4 5.11 13 3.6 4.5 3.67 7.1 2.85 40

Total 921.51 1514.4 1198.67 1364.16 1274.93 1684.5 2631.34 841.94 672.64 736.71 1333.78 1228.33 92

5 Other Priority Sector

CBs 219.44 229.47 363.38 505.19 491.35 627.58 255.93 885 882.8 771.22 442.58 603.69 136

SCB 322.81 185.21 175.89 256.29 480.1 428.13 194.79 283.84 393.23 539.71 313.36 338.64 108

SCARBB 9.79 12.9 8.15 4.34 21.62 2.99 30.92 3.82 32.14 5.42 15.12 5.89 39

RRB 0 0 0 0 0 0 0 0.27 1.45 1.71 - - -

Others - KFC 9 2.64 9 3.55 9 0.57 0 6.02 7.5 0 8.63 3.2 37

Total 561.04 430.22 556.42 769.37 1002.07 1059.27 481.64 1178.95 1317.12 1318.06 779.69 951.42 122

Grand Total (4+3+5) 1729.87 2095.29 2184.06 2554.34 2717.07 3294.25 3604.52 3751.29 4099.95 4472.86 2856.90 3214.76 113

Source : District Credit Plans

128

It may be seen from table 5.7 that the average GLC during 2004-05

and 2008-09 was targeted at ` 2,856.9 crore. As against the target, the

actual credit flow averaged ` 3,214.74 crore and the achievement worked

out at 113 per cent. Under Crop Loan, as against the targeted ` 590.32

crore, the achievement averaged at ` 913.60 crore and it worked out at 155

per cent. When compared to the GLC under Crop Loan, the credit flow

under medium term and long term investment purposes was targeted at a

low amount of ` 153.11 crore per annum during the last 5-year reference

period. As against this target, the achievement averaged ` 121.39 crore,

79 per cent of the target. Thus, compared to the flow of credit under Crop

Loan, both credit target and achievements for capital formation process

under agriculture was at a low pace in Kollam district during the reference

period. This subject draws serious concern from the policy-makers to

further strengthen agriculture sector in the district.

The credit target planned under Total Agri-Credit including Crop

Loan and loans under Medium- Term (MT) and Long- Term (LT) averaged

` 743.43 crore during the reference period. As against this target the

achievement averaged ` 1,035 crore per annum during the reference

period. The percentage of achievement worked out at 140. Thus, it may

be observed that the targets under Crop Loan, Term Loan and Total Agri

Credit were achieved during the reference period from 2004-05 to 2008-09.

During the same period the credit flow per annum under Non- Farm

Sector (NFS) averaged ` 1,333.78 crore and the achievement averaged `

1,228.33 crore, at 92 per cent. During the reference period the targeted

credit under NFS ranged from ` 921.51 crore during 2004-05 and it was

kept at a low level of ` 672.64 crore during 2008-09. The data reflects a

lowering of the credit target under NFS from the year 2008-09. The

achievement which stood at ` 1,514.40 crore during 2004-05

marginally fell to ` 1,364.16 crore during 2005-06 and subsequently

129

increased to ` 1,684.50 crore during 2006-07 and further decreased to

` 841.94 crore during 2007-08 and thereafter decreased to ` 736.71 crore

during the year 2008-09. The reason for lower allocation of target under

NFS and the corresponding declining trend in achievement of the loan

disbursement under the sector is worth probing. Looking at the increasing

share of Secondary and Tertiary Sectors in the district economy, the lower

level of credit disbursements under NFS appears to be a mismatch.

As against the average targeted credit of ` 779.69 crore per annum

during the reference period, the achievement averaged ` 951.42 crore, at

122 per cent. A perusal of the credit target and achievement under OPS

reflects an increasing trend till 2006-07 and further a declining trend in the

target during 2007-08. The credit target under OPS was kept at ` 561.04

crore during 2004-05 and it was marginally decreased to ` 556.42 crore

during 2005-06 and further increased to ` 1,002.07 crore and subsequently

the target was kept at Rs 481.64 crore during 2007-08 and further kept at a

higher level of ` 1,317.12 crore during the year 2008-09. However, the

disbursement under OPS records an increasing trend from ` 430.22 crore

from 2004-05 to ` 769.37 crore, ` 1,059.27 crore, ` 1,178.95 crore

and ` 1,318.06 crore during the year 2005-06, 2006-07, 2007-08 and

2008-09 respectively.

Out of the average annual credit disbursement of ` 3,214.76 crore

the credit flow under Crop Loans averaged ` 913.60 crore per annum, 28

per cent of the credit disbursement. In the case of the average

disbursement under Term Loan at ` 121.39 crore constituting only 4 per

cent of the GLC, the pattern of credit flow for capital formation appears to be

at a very low level. In the case of the total credit flow under agriculture, the

actual disbursement for capital formation in agriculture constituted only 12

per cent of the credit. The pattern of the credit disbursement under capital

formation also reflected a marginal increasing trend. It was at ` 88.45

crore during 2004-05 and recorded a marginal increase of ` 90.44 crore

130

during 2005-06 and further rose to ` 122.93 crore during 2006-07, ` 163.79

crore during 2007-08 and further declined to ` 141.34 crore during 2008-09.

From the data it appears that there was a relatively poor demand and

disbursement of credit for capital formation process under agriculture during

the reference period in Kollam district.

The allocated credit under NFS during the reference period averaged

` 1,333.78 crore, constituting 41 per cent of the annual credit target. The

achievement during the period averaged ̀ 1,228.33 crore, 38 per cent of the

average credit disbursements. Thus, there was a fall in achievement of the

target under NFS. The pattern of disbursement under NFS during the

period reflects inconsistent trends. The credit disbursement which was `

1,514.40 crore during 2004-05 declined to ` 1,364.16 crore during 2005-06

and marginally increased to ` 1,684.50 crore during 2006-07 and further

declined to ` 841.94 crore during 2007-08 and the disbursement further

decreased to ` 736.71 crore during 2008-09. During the same reference

period fixation of the targets also reflected illogical trends from the year

2007-08. The target which was kept at ` 1,274.93 crore during 2006-07

was increased to 2,631.34 crore during 2007-08 and drastically reduced to ̀

672.64 crore during 2008-09. The logic of such a sizable reduction in the

allocation of the credit target under NFS in a developing district economy

warrants careful planning process.

Both credit planning and credit disbursements under Other Priority

Sector (OPS) reflected increasing trends. The average disbursements per

annum consisting of ̀ 951.42 crore constituted 30 per cent of the total credit

disbursement. The actual disbursement under OPS increased from `

430.22 crore during 2004-05 to ` 769.37 crore during 2005-06 and further

increased to ` 1,059.27 crore in 2006-07, ` 1,178.95 crore during 2007-08

and further rose to ` 1,318.06 crore during 2008-09. Thus, the

disbursement under OPS recorded a steady increasing trend. The liberal

credit facilities followed by the banks under this sector appear to be the

131

reason for the steady increase.

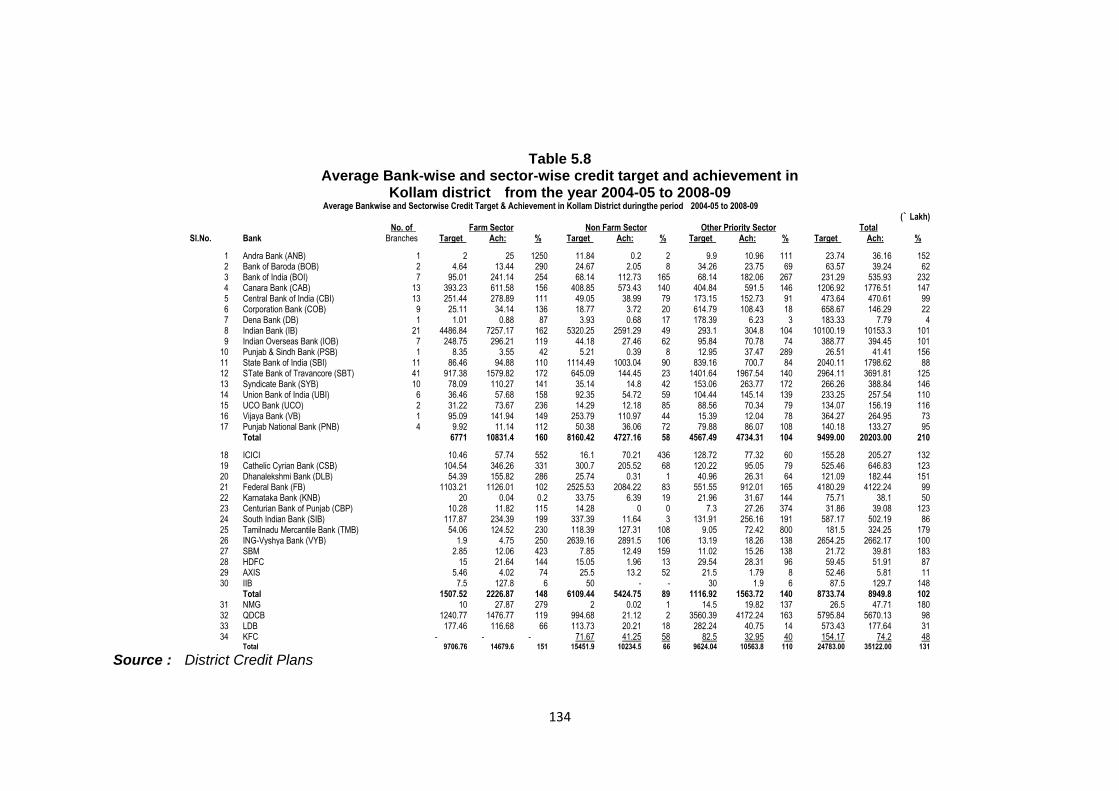

Agency-wise Credit Flow

Out of the average annual credit disbursement at ` 3,214.76 crore

during the period from 2004-05 to 2008-09, the credit disbursed by

Commercial Banks (CBs) totalled ` 2,733.06 crore, 85 per cent. Thus

Commercial Banks played a major role in the disbursement of GLC in

Kollam district during the reference year 2004-05 and 2008-09. Out of the

per annum average Crop Loan disbursement at ` 913.60 crore, ` 802.25

crore, 87 per cent was disbursed by CBs. Similarly, out of the average

credit disbursement of ` 121.39 crore under Term Loan, ` 107.42 crore, 88

per cent was disbursed by CBs. In the case of NFS out of the total

disbursement of ` 1,228.33 crore, ` 1,219.71 crore, 99 per cent was

disbursed by CBs. Under Other Priority Sector (OPS) out of the total

disbursement of ` 951.42 crore, ` 603.69 crore, 63 per cent was disbursed

by Commercial Banks. Thus it is revealed that in all the four major sectors,

viz Crop Loan, Term Loan, NFS and OPS, Commercial Banks played an

important role in the credit delivery system in Kollam district. Thus the

hyposis that the flow of credit under agriculture sector was ensured by

banks under co-operative sectors compared to Commercial Banks is

rejected as the Commercial Banks played a major role in credit delivery.

In the case of loan disbursements under Crop Loan, Commercial

Banks played an increasing role in Kollam district. The credit

disbursement by CBs rose from ` 17.63 crore during 2004-05 in Kollam

district to ` 1,993.80 crore during 2008-09. Thus there is a significant

increase in the credit delivery system under Crop Loan by CBs. Whereas,

in the case of the loan disbursements under Term Loan, i.e. the loans

stipulated for capital formation process recorded an increase from ` 75.44

crore during 2004-05 to ` 129.45 crore during 2008-09, a marginal increase

under an important sector. The disbursements under NFS by Commercial

132

Banks in Kollam district also reflected a mixed trend. The disbursement

which were ranging from ` 1,506 crore in 2004-05 and ` 1,674.20 crore

during 2006-07 recorded declining trend in 2007-08 and during 2008-09.

The disbursement under NFS during these years was as less as ` 836.48

crore and ` 727.69 crore respectively.

Followed by Commercial Banks, State Co-operative Bank (SCB)

played a major role in disbursement of Crop Loan in Kollam district during

the year. Out of the total Crop Loan disbursement of ` 913.60 crore per

annum `106.26 crore, 12 per cent, was disbursed by SCB. In the case of

loan disbursement under Term Loan for capital formation under agriculture,

SCB played an insignificant role by disbursing on an average only ` 7.96

crore (7%) out of the total credit disbursement of ` 121.39 crore per annum

during the reference period in Kollam district. In spite of the co-operative

nature of the bank it could play only a minor role in credit disbursements

under Term Loan as well as under Non-Farm Sector. However, under

Other Priority Sector the bank could disburse on an average ` 338.64 crore

per annum during the reference period. This constituted 36 per cent of the

total credit disbursement per annum under OPS in Kollam district.

The role played by State Co-operative Agriculture and Rural

Development Bank (SCARDB) was minimal at ` 5.09 crore per annum

constituting only 0.6 per cent of the credit disbursement under Crop Loan.

In the case of the loan disbursement under Term Loan, the banks

disbursement averaged ` 6.01 crore per annum constituting only 5 per cent

of the total credit disbursement under the sector for capital formation

process. The bank which is supposed to play a major role in strengthening

the agriculture sector through capital formation process could play only an

insignificant role. The policy planners of the State Government who control

the bank should empower it to deliver its responsibilities. Such credit

institutions professional capacity to address the local requirement and

compete with other credit institutions generally reflects the capability of the

133

management system. The bank also could play only minor roles in the

case of credit delivery under NFS and OPS. The average disbursement

made by the bank per annum under NFS and OPS worked out at ` 4.03

crore and ` 5.89 crore respectively.

In Kollam district, RRB has also played only a small role in the case

of credit delivery under Crop Loan. The bank could not make any impact

on credit delivery under Term Loan, NFS and OPS. RRBs credit delivery

under Crop Loan also was insignificant to highlight.

Bank/Agency-wise Credit Flow

In order to study the bank-wise credit flow during the period 2004-05

and 2008-09 an attempt has been made to work out the average targeted

credits and corresponding achievements during the period under the broad

head, Farm Sector, Non- Farm Sector and Other Priority Sector. For this

purpose the data is collected from various District Credit Plans. The

results are given in table 5.8

134

Table 5.8 Average Bank-wise and sector-wise credit target and achievement in

Kollam district from the year 2004-05 to 2008-09 Average Bankwise and Sectorwise Credit Target & Achievement in Kollam District duringthe period 2004-05 to 2008-09

(` Lakh)

No. of Farm Sector Non Farm Sector Other Priority Sector Total

Sl.No. Bank Branches Target Ach: % Target Ach: % Target Ach: % Target Ach: %

1 Andra Bank (ANB) 1 2 25 1250 11.84 0.2 2 9.9 10.96 111 23.74 36.16 152 2 Bank of Baroda (BOB) 2 4.64 13.44 290 24.67 2.05 8 34.26 23.75 69 63.57 39.24 62 3 Bank of India (BOI) 7 95.01 241.14 254 68.14 112.73 165 68.14 182.06 267 231.29 535.93 232 4 Canara Bank (CAB) 13 393.23 611.58 156 408.85 573.43 140 404.84 591.5 146 1206.92 1776.51 147 5 Central Bank of India (CBI) 13 251.44 278.89 111 49.05 38.99 79 173.15 152.73 91 473.64 470.61 99 6 Corporation Bank (COB) 9 25.11 34.14 136 18.77 3.72 20 614.79 108.43 18 658.67 146.29 22 7 Dena Bank (DB) 1 1.01 0.88 87 3.93 0.68 17 178.39 6.23 3 183.33 7.79 4 8 Indian Bank (IB) 21 4486.84 7257.17 162 5320.25 2591.29 49 293.1 304.8 104 10100.19 10153.3 101 9 Indian Overseas Bank (IOB) 7 248.75 296.21 119 44.18 27.46 62 95.84 70.78 74 388.77 394.45 101

10 Punjab & Sindh Bank (PSB) 1 8.35 3.55 42 5.21 0.39 8 12.95 37.47 289 26.51 41.41 156 11 State Bank of India (SBI) 11 86.46 94.88 110 1114.49 1003.04 90 839.16 700.7 84 2040.11 1798.62 88 12 STate Bank of Travancore (SBT) 41 917.38 1579.82 172 645.09 144.45 23 1401.64 1967.54 140 2964.11 3691.81 125 13 Syndicate Bank (SYB) 10 78.09 110.27 141 35.14 14.8 42 153.06 263.77 172 266.26 388.84 146 14 Union Bank of India (UBI) 6 36.46 57.68 158 92.35 54.72 59 104.44 145.14 139 233.25 257.54 110 15 UCO Bank (UCO) 2 31.22 73.67 236 14.29 12.18 85 88.56 70.34 79 134.07 156.19 116 16 Vijaya Bank (VB) 1 95.09 141.94 149 253.79 110.97 44 15.39 12.04 78 364.27 264.95 73 17 Punjab National Bank (PNB) 4 9.92 11.14 112 50.38 36.06 72 79.88 86.07 108 140.18 133.27 95

Total

6771 10831.4 160 8160.42 4727.16 58 4567.49 4734.31 104 9499.00 20203.00 210

18 ICICI

10.46 57.74 552 16.1 70.21 436 128.72 77.32 60 155.28 205.27 132 19 Cathelic Cyrian Bank (CSB) 104.54 346.26 331 300.7 205.52 68 120.22 95.05 79 525.46 646.83 123 20 Dhanalekshmi Bank (DLB) 54.39 155.82 286 25.74 0.31 1 40.96 26.31 64 121.09 182.44 151 21 Federal Bank (FB) 1103.21 1126.01 102 2525.53 2084.22 83 551.55 912.01 165 4180.29 4122.24 99 22 Karnataka Bank (KNB) 20 0.04 0.2 33.75 6.39 19 21.96 31.67 144 75.71 38.1 50 23 Centurian Bank of Punjab (CBP) 10.28 11.82 115 14.28 0 0 7.3 27.26 374 31.86 39.08 123 24 South Indian Bank (SIB) 117.87 234.39 199 337.39 11.64 3 131.91 256.16 191 587.17 502.19 86 25 Tamilnadu Mercantile Bank (TMB) 54.06 124.52 230 118.39 127.31 108 9.05 72.42 800 181.5 324.25 179 26 ING-Vyshya Bank (VYB) 1.9 4.75 250 2639.16 2891.5 106 13.19 18.26 138 2654.25 2662.17 100 27 SBM

2.85 12.06 423 7.85 12.49 159 11.02 15.26 138 21.72 39.81 183

28 HDFC

15 21.64 144 15.05 1.96 13 29.54 28.31 96 59.45 51.91 87 29 AXIS

5.46 4.02 74 25.5 13.2 52 21.5 1.79 8 52.46 5.81 11

30 IIB

7.5 127.8 6 50 - - 30 1.9 6 87.5 129.7 148

Total

1507.52 2226.87 148 6109.44 5424.75 89 1116.92 1563.72 140 8733.74 8949.8 102

31 NMG

10 27.87 279 2 0.02 1 14.5 19.82 137 26.5 47.71 180 32 QDCB

1240.77 1476.77 119 994.68 21.12 2 3560.39 4172.24 163 5795.84 5670.13 98

33 LDB

177.46 116.68 66 113.73 20.21 18 282.24 40.75 14 573.43 177.64 31 34 KFC

- - - 71.67 41.25 58 82.5 32.95 40 154.17 74.2 48

Total

9706.76 14679.6 151 15451.9 10234.5 66 9624.04 10563.8 110 24783.00 35122.00 131

Source : District Credit Plans

135

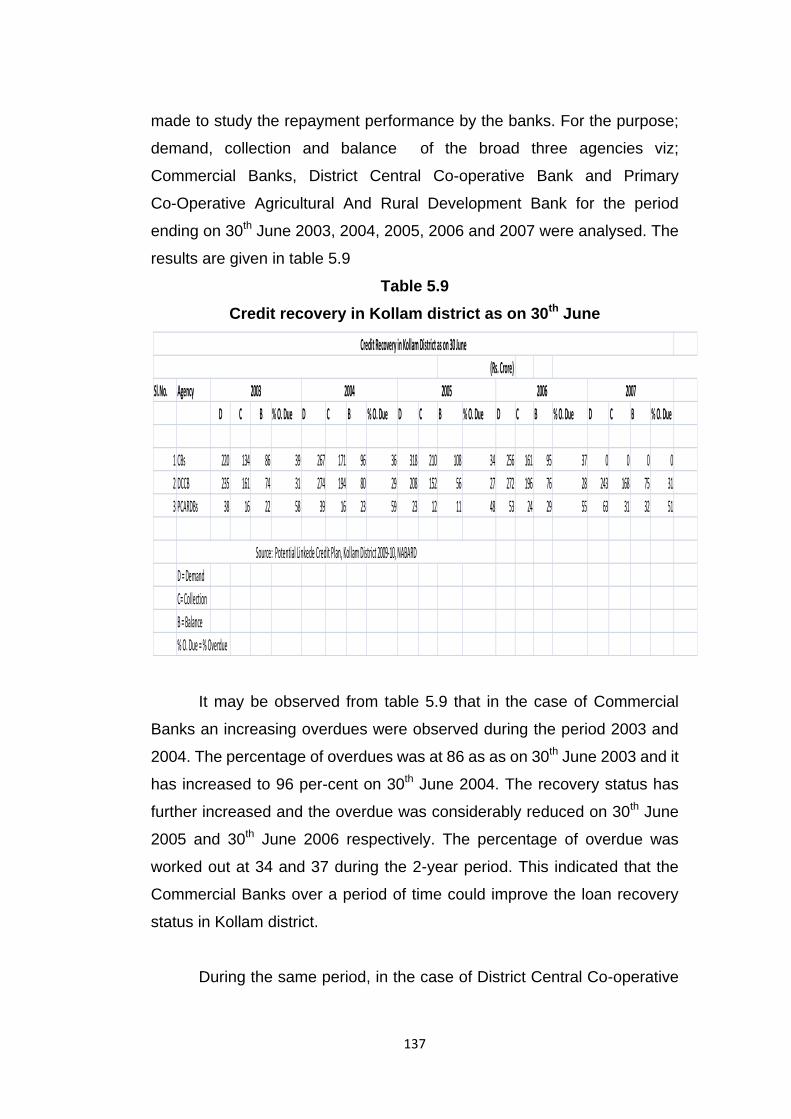

Out of the major Commercial Banks, around 30 agencies

participated in the credit delivery in Kollam district along with the RRB, North

Malabar Grameen Bank (NMG), Quilon District Co-operative Bank (QDCB),

the SCARDB and Kerala Financial Corporation (KFC). As may be seen

from the table 5.8 that among the major Commercial Banks, State Bank of

Travancore (SBT) was having 41 branches in the district followed by Indian

Bank (IB) 21 branches, Canara Bank (CAB) and Central Bank of India (CBI)

13 branches each, State Bank of India (SBI) 11 branches, Syndicate Bank

(SYB) 10 branches and Corporation Bank (COB) nine branches. The

remaining banks had branches ranging from one to seven as indicated in

the table 5.8.

The data in table 5.8 reflected regular target allocation among all the

financial institutions in Kollam district. The allocation of the target had a

direct relation with the number of branches that bank is having in the district.

Among the nationalised banks State Bank of Travancore (SBT) having 41

branches in Kollam district had the maximum credit allocation followed by

State Bank of India, Canara Bank and Corporation Bank. Other

nationalised banks were having relatively lesser target allocation.

Among the private sector banks, Federal Bank (FB) had relatively

larger credit allocation followed by ING Vysya Bank, Catholic Syrian Bank

and ICICI Bank. New banks like HDFC, AXIS, IIB, Karnataka Bank etc.

had a nominal credit allocation only. Most of these banks are having one

or two branches located at the commercial centre in Kollam Corporation.

These banks’ involvement in rural credit disbursements are yet to pick up.

Quilon District Co-operative Bank and SCARDB actively participated

in the credit delivery system in Kollam district. However, SCARDBs credit

disbursement was at a low level of 31 per cent of the credit target only. The

role played by Financial Corporation was also much below the expected

136

level. Their credit disbursements were around 48 per cent of the targeted

credit during the reference period. The North Malabar Grameen Bank

functioning in the district also played insignificant role in the rural credit

delivery. Though they had achieved the targeted credit, the quantum of

achievement was insignificant at ` 48 lakh per annum during the reference

period 2004-05 and 2008-09.

Among the broad sectors viz. Farm Sector, Non- Farm Sector and

other Priority Sector, the average targeted credit under Non- Farm Sector

was the highest at 47 per cent followed by the credit targets under Other

Priority Sector at 27 per cent and remaining 26 per cent was targeted under

Farm Sector. Though the credit targets were achieved at 101 per cent of

the target during the reference period, the achievement of the targets under

Non- Farm Sector often fell below the targets and it averaged at 66 per cent

during the 5-year period under the study. The achievement under Farm

Sector was relatively higher at 151 per cent compared to the other two

sectors. Govt. of India’s consistent thrust on increasing the rural credit flow

under agriculture appears to be the reason for the higher achievements.

The above analysis thus highlights the fact that there is larger scope

for financial institutions in Kollam district to further augment the rural credit

delivery. Though 34 agencies are participating in the delivery system,

except four major Commercial Banks, a couple of private banks and the

branches of Quilon District Central Co-operative Banks, a larger number of

the banks participation is on a nominal basis. Often these banks are also

given a smaller credit target for achievement based on their own earlier

trends in credit disbursements. This results in a continuous lower level of

credit allocation and disbursements. Thus there is a need to review the

whole exercise of credit allocation based on realistic potential and keeping