Embed Size (px)

Citation preview

SEAFOOD INDUSTRY

INDUSTRY DEFINITION

Aquaculture is the controlled production by man of vegetable and animal organisms which spend at least some of their life cycle in a water environment. These organisms, which include �sh, mollusks and crustaceans, provide a range of business opportunities and are a nutritional alternative. The activity helps the recovery of diminishing natural populations.Wild-capture �shing is the extraction of aquatic organisms from continental waters in their natural state or subjected to development activities.

THE SEAFOOD INDUSTRY IN MEXICO

* Source: Secretariat of Agriculture, Livestock, Rural Development, Fisheries and Food (SAGARPA), National Commission of Aquaculture and Fishing (CONAPESCA).** Source: INEGI. Mexican System of National Accounts.

Mexico's enormous potential in the �sheries sector lies in its 11,592 kilometers of coastline, of which 76% are on the Paci�c coast and 24% on the Gulf of Mexico, the Caribbean coast and islands. Its continental shelf is approximately 394,000 km², being larger in the Gulf of Mexico. It also has 12,500 km² of coastal lagoons and estuaries and 6,500 km² of inland waters such as lakes, lagoons, reservoirs, and rivers.

Fishing, hunting and capture accounted for 1.7% of Mexico's agricultural GDP in 2013**. In 2014, the volume of �shery production in live weight was 1,751 thousand tons, a growth of 0.3% compared to the previous year. Of the total production volume, 81.4% was capture �shing and the remaining 18.6% aquaculture. The total production value was US$1,812 million.

Aquaculture �sh production in 2014 reached a value of US$776.1 million, the main species produced through this activity according to volume were: mojarra with a share of 37%, shrimp 27%, and oyster 14%.

Aquaculture Capture

284

285

271

263

254

246

325

1,462

1,483

1,349

1,398

1,433

1,501

1,426

2008 2009 2010 2011 2012 2013 2014

Graph 1. Volume of Fishery Production in Mexico(thousands of tonnes.) 2008-2014*

The value of aquaculture production in 2014 was US$776.1 million, where the main species according to volume obtained were: mojarra with a 37% share, shrimp 27%, and oysters 14%.

Source: INEGI. Mexican System of National Accounts.

Product Millions ofUS dollars

Table 1. Fishery Production, 2014

Shrimp

Mojarra

Tuna

Octopus

Trout

Lobster

Guachinango

Sardine

Carp

Crab

Robalo

Others

Total

700.4

158.4

157.2

80.7

65.9

48.1

41.4

37.1

35.7

32.3

30.3

424.5

1,812.0

Sinaloa (43%), Sonora (26%) and Tamaulipas (7%)

Jalisco (21%), Chiapas (18%) and Michoacán (12%)

Sinaloa (38%), BC (38%), Colima (11%) and Chiapas (10%)

Yucatán (71%) and Campeche (22%)

Michoacán (39%), Edo México (28%) and Puebla (17%)

BCS (47%), BC (23%) and Yucatán(11%)

Jalisco (14%), BCS (11%), Michoacán (10%), Tabasco (9%)

and Oaxaca (9%)

Sonora (45%), Sinaloa (19%), BCS (18%) and BC (18%)

Jalisco (23%), Edo México (22%), and Hidalgo (15%)

Sinaloa (41%), Sonora (20%), Veracruz (13%), Campeche

(11%) and Tamaulipas (9%)

Campeche (22%), Veracruz (21%), Tabasco (16%) and

Nayarit (14%)

Main producers

THE SEAFOOD INDUSTRY IN MEXICO

Source: CONAPESCA, SAGARPA.

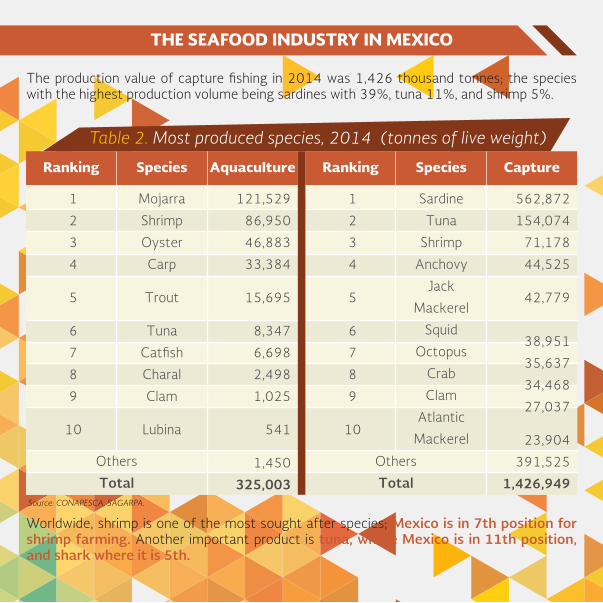

The production value of capture �shing in 2014 was 1,426 thousand tonnes; the species with the highest production volume being sardines with 39%, tuna 11%, and shrimp 5%.

Worldwide, shrimp is one of the most sought after species; Mexico is in 7th position for shrimp farming. Another important product is tuna, where Mexico is in 11th position, and shark where it is 5th.

THE SEAFOOD INDUSTRY IN MEXICO

CaptureSpeciesRanking

Table 2. Most produced species, 2014 (tonnes of live weight)

562,872

154,074

71,178

44,525

42,779

38,951

35,637

34,468

27,037

23,904

391,525

1,426,949

Sardine

Tuna

Shrimp

Anchovy

Jack

Mackerel

Squid

Octopus

Crab

Clam

Atlantic

Mackerel

1

2

3

4

5

6

7

8

9

10

Others

Total

AquacultureSpeciesRanking

121,529

86,950

46,883

33,384

15,695

8,347

6,698

2,498

1,025

541

1,450

325,003

Mojarra

Shrimp

Oyster

Carp

Trout

Tuna

Cat�sh

Charal

Clam

Lubina

1

2

3

4

5

6

7

8

9

10

Others

Total

There are more than 2,400 commercial �sh farms in Mexico and around 800 self-consumption units. Among the states with the highest number of production centers are Veracruz with more than 600, which produce mainly tilapia. Shrimp farms are more common in Sinaloa, with more than 300 and Sonora with more than 130, which make a signi�cant contribution to the supply of aquaculture foods.While there is certainly huge development potential for farmed shrimp production, in Mexico the greatest potential lies in the production of marine �n�sh and bivalve mollusks (oysters, clams and mussels).

EMPLOYMENT

In 2013, the �shing sector in Mexico employed 272,533 people, Sinaloa being the state with the highest number with a 17% share, followed by Veracruz with 15%, Tabasco 6.7%, Jalisco 5.4%, Sonora 5.3% and Michoacán 5.1%.

PROCESSING AND INDUSTRIALIZATION

20.4%

SHRIMP

22.8%

TUNA FISHMEAL

14.9%

The products with the highest percentage share of the fishing industry were:

AQUACULTURE PRODUCTION

12.6%

SARDINES & MACKEREL

Graph 2. Products with the highest percentage share

PROCESSING AND INDUSTRIALIZATION

Species %Share per species, 2011

Table 3. Fishing industry production in net weight by species, 2013

Tuna

Shrimp

Fishmeal

Sardines and mackerel

Squid

Full scale

Octopus

Fish oil

Shark

Crab

Lobster

Other

22.8%

20.4%

14.9%

12.6%

6.0%

5.0%

4.1%

3.7%

2.4%

2.2%

0.6%

5.1%

116,280

104,096

75,749

64,365

30,729

25,548

21,062

18,937

12,122

11,134

3,035

26,046

Production in net weight, (tons)

Note: Statistical Yearbook of Aquaculture and Fisheries 2013, CONAPESCA.

In 2013, the production volume in net weight of the main industrialization processes was 509,103 tons. The growth of production obtained through canned processes between 2007 and 2013 is particularly noteworthy with an average annual growth rate of 9.8%.

Mexico has almost 300 plants that process different �sh and shell�sh, including lobster, oysters, tuna, clams, squid, sardines, shrimp, and octopus.

Source: CONAPESCA Latest update: 21-10-2013.

BajaCalifornia 40

B.C.S. 14Yucatán 30

Jalisco 16

Colima 2

State of Mexico 1

Puebla 1

Oaxaca 2

Chiapas 9Campeche 24

Quintana Roo 4

Tlaxcala 1Queretaro 1

Veracruz 4Tabasco 4

Sonora 62

Tamaulipas 8San Luis Potosí 1

Guanajuato 5

Sonora 32

CONSUMPTION

Source: Statistical Yearbook of Aquaculture and Fisheries, 2013.

In 2013, of total �shing production, 37.4% was for indirect human consumption: national reduction plants transformed mainly sardines into �shmeal and �sh oil; 0.6% of production is classed as industrial use, algae, kelp, and some shells being its main exponents; the remaining 61.9% of production goes directly for human consumption.

2013

Indirecthuman consumption

Directhuman consumption

Industrial use 0.6%

61.9%37.4%

Graph 3. Fishery production, 2013

Categories % Share2014

Growth 2013-2014

Table 4. Market volume of fresh products in Mexico, 2014

Crustaceans

Fish

Mollusks and cephalopods

Fish and seafood

14%

69%

17%

100%

1.8%

2.3%

1.2%

2.0%

1.9%

2.1%

1.2%

1.9%

CAGR2014-2019

89.4

449

109.5

647.9

Volume 2014(Thousands of tons)

Categories % Share 2014 CAGR (2014-2019)

Table 5. Market value of processed products in Mexico, 2014

Crustaceans

Fish

Mollusks and cephalopods

Fish and seafood

81%

4%

15%

100%

0.9%

1.6%

1.5%

1.0%

1,068

57

193

1,318

Value 2014(millions of US dollars)

Mexico is the second largest market for fresh �sh and sea products in Latin America, recording a volume of 648,000 tons in 2014 and is expected to grow at a CAGR of 2% between 2014 and 2019 to reach 713,000 tons.

MARKET SIZE

Source: Euromonitor.

The HIGHEST SELLINGFRESH PRODUCE SEGMENT in MEXICO is FISH,

with a 69% MARKET SHARE.

MARKET SIZE

The market value of processed �sh and �shery products in Mexico in 2014 was US$1,318 million, canned and preserved products being the highest selling. Refrigerated and frozen products are expected to grow at an annual rate of 1.5% between 2014 and 2019.

Companies in Mexico with biggest market share in the canned and preserved seafood market are Grupo Herdez, Pescados Industrializados and Marindustrias with a combined share of 46%.

Source: ProMéxico based on Euromonitor.

Brand Company % Share

Herdez

Dolores

Tuny

Nair

Calmex

Calvo

El Vigilante

Mazatún

Guaymex

Yavaros

Herdez SA de CV, Grupo

Pescados Industrializados SA de CV

Marindustrias SA de CV

Herdez SA de CV, Grupo

Pando, Grupo SA de CV

Grupo Calvo SA

Justo López Valcárcel SA

Pescados Industrializados SA de CV

Productos Pesqueros de Guaymas SA de CV

Pando, Grupo SA de CV

Others

Total

17.1

16.2

13.1

5.3

4.2

3.6

2.6

2.5

2.3

1.5

31.6

100

Table 6. Main companies and brands in the canned and preserved seafood market of México, 2014

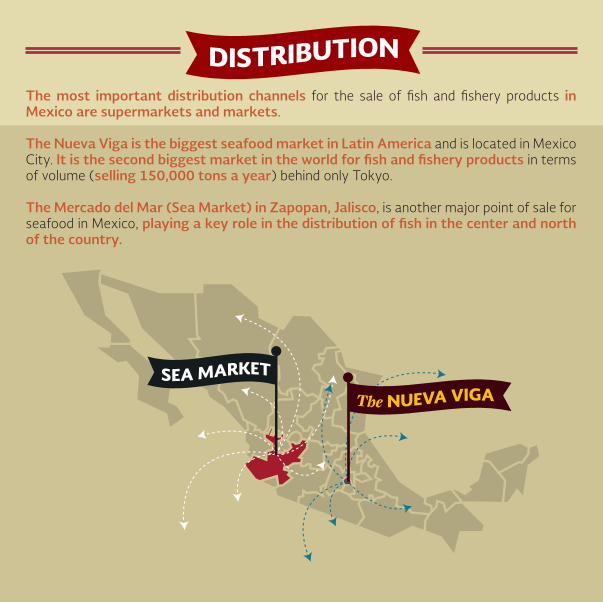

The most important distribution channels for the sale of �sh and �shery products in Mexico are supermarkets and markets.

The Nueva Viga is the biggest seafood market in Latin America and is located in Mexico City. It is the second biggest market in the world for �sh and �shery products in terms of volume (selling 150,000 tons a year) behind only Tokyo.

The Mercado del Mar (Sea Market) in Zapopan, Jalisco, is another major point of sale for seafood in Mexico, playing a key role in the distribution of �sh in the center and north of the country.

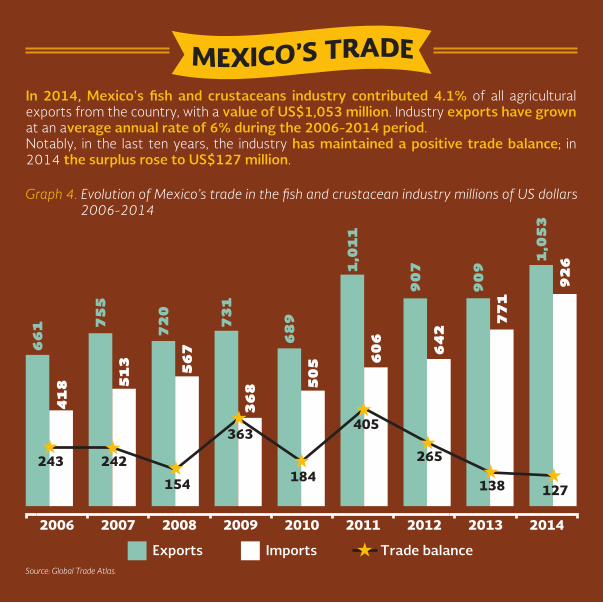

In 2014, Mexico's �sh and crustaceans industry contributed 4.1% of all agricultural exports from the country, with a value of US$1,053 million. Industry exports have grown at an average annual rate of 6% during the 2006-2014 period.Notably, in the last ten years, the industry has maintained a positive trade balance; in 2014 the surplus rose to US$127 million.

Source: Global Trade Atlas.

66

1 75

5

72

0

73

1

68

9

1,0

11

90

7

90

9

1,0

53

41

8 51

3 56

7

36

8 50

5 60

6

64

2

77

1

92

6

243 242

154

363

184

405

265

138 127

2006 2007 2008 2009 2010 2011 2012 2013 2014

Exports Imports Trade balance

Graph 4. Evolution of Mexico’s trade in the �sh and crustacean industry millions of US dollars 2006-2014

In 2014, 63.4% of Mexican �sh and crustacean exports went to the United States, followed by Hong Kong with a share of 8.3%, Japan 8.3%, Spain 6.9%, and Vietnam with 3.9%. Exports to South Korea have grown considerably at a rate of 132% compared with 2013.

MEXICO’S TRADE

Source: Global Trade Atlas.

Table 7. Destination of �sh and crustacean exports from Mexico, 2014

Country % Share 2014 Growth 2013-2014

United States

Hong Kong

Japan

Spain

Vietnam

Italy

South Korea

Malaysia

China

Canada

Others

Total

63.4%

8.3%

8.3%

6.9%

3.9%

2.9%

0.8%

0.8%

0.7%

0.6%

3.3%

100.0%

16.0%

-3.5%

15.3%

48.8%

54.7%

85.2%

132.5%

-9.9%

-69.0%

10.3%

11.3%

15.9%

668

88

88

73

41

30

9

8

7

7

34

1,053

Value 2014(millions of US dollars)

VOLUME of FISH PRODUCTION in MEXICO(thousands of tons)

2008-2014

1,462 1,4831,349

1,398 1,4331,501 1,426

284 285 271 263 254 246 325

Aquaculture Capture �sheries

Source: Secretariat of Agriculture, Livestock, Rural Development, Fisheries and Food (SAGARPA),

National Commission of Aquaculture and Fisheries (CONAPESCA).

2008 2009 2010 2011 2012 2013 2014

EXPORT SUPPLY

Table 8.1 Export supply of the �sh and crustacean industry in Mexico, 2014

HS Code

% Share

% Growth 2013-2014

Main export destinations and % share

DescriptionExports(millions ofUS dollars)

0306

0303

0302

0307

0304

Crustaceans

(except preserved)

Frozen �sh (excluding �llets)

Fresh or chilled �sh

(except �llets)

Mollusks

(except preserved)

Fresh, refrigerated or frozen

�llets and other �sh meat

461

132

131

114

79

43.8%

12.5%

12.4%

10.8%

7.5%

17%

23%

6%

-3%

32%

U.S.A. 84.2%, Hong Kong

9.1%, Vietnam 3.8%, Japan

0.9% and France 0.8%.

Spain 33.5%, Japan 28.1%,

U.S.A. 10.6%, Malaysia

5.5% and Vietnam 4.9%

U.S.A. 64.3%, Japan

31.7%, Canada 3.3%,

United Kingdom 0.3% and

South Korea 0.3%

U.S.A. 25.3%, Italia 23.9%,

Hong Kong 15.6%, Spain

14.6%, and Vietnam 7.9%

U.S.A. 82.1%, Spain 13.2%,

Hong Kong 1.7%, Japan

1.4% and China 0.7%Source: Global Trade Atlas.

EXPORT SUPPLY

Table 8.2 Export supply of the �sh and crustacean industry in Mexico, 2014

HS Code

% Share

% Growth 2013-2014

Main export destinations and % share

DescriptionExports(millions ofUS dollars)

1605

0308

1604

0305

Prepared or preserved

crustaceans, mollusks and

other aquatic invertebrates

Aquatic invertebrates

(except preserved)

Prepared or preserved �sh,

caviar and caviar substitutes

Fish, dried, salted or in brine;

smoked �sh, �ours, meals

and pellets of �sh

65

35

28

8

6.2%

3.3%

2.7%

0.7%

4%

223%

45%

-29%

U.S.A. 66.7%, Hong Kong

21%, Singapore 5.2%,

South Korea 3.5% and

Japan 1%

U.S.A. 59.8%, Vietnam

22.3%, Hong Kong 16.3%,

Thailand 0.9% and

Singapore 0.5%

U.S.A. 83.9%, Costa Rica

10.9%, Puerto Rico 2.4%,

Spain 1.1% and Panama

0.7%

Hong Kong 87.4%, China

6.3%, U.S.A. 4.4%, Cuba

1.9% and Vietnam 0.01%

Source: Global Trade Atlas.

EXPORT SUPPLY

Table 8.3 Export supply of the �sh and crustacean industry in Mexico, 2014

HS Code

% Share

% Growth 2013-2014

Main export destinations and % share

DescriptionExports(millions ofUS dollars)

0301 Live �sh

Total

1

1,053

0.1%

100%

-48%

16%

U.S.A. 51.1%, South Korea

44.3%, Japan 3.2%,

Honduras 1% and Panama

0.2%

The most exported products are crustaceans like shrimp, lobster and crab, with a 44% share of total industry exports, followed by frozen �sh 13%, fresh �sh with 12%, mollusks 11%, and �llets and other �sh meat with an 8% share. The export of aquatic invertebrates showed considerable annual growth of 223%.

The number of export companies in Mexico in 2014 was around of 500. About 63% of export companies are located in the states of Sinaloa, Sonora, Baja California y Yucatán.

Source: Global Trade Atlas.

In 2014, 63.4% of Mexican �sh and crustacean exports went to the United States, followed by Hong Kong with a share of 8.3%, Japan 8.3%, Spain 6.9%, and Vietnam with 3.9%. Exports to South Korea have grown considerably at a rate of 132% compared with 2013.

In July 2013, Chiapas governor announced Malpaso Aquaculture Park project expansion, which aims to attract FDI in�ows over US$30mn in order to produce 70 thousand tonnes of tilapia annually for the next 5 years.

FOREIGN DIRECT INVESTMENT

Source: Ministry of Economy.

In the PERIOD from 1999 to 2014,THE INDUSTRY REGISTERED

US$2.8 MILLION of FDI.

NAICS Code Description

Table 9. FDI in�ows in the seafood products industry

11251

11411

31171

Aquaculture

Fisheries

Seafood Product Preparation and Packaging

Total

0.03

1.0

1.7

2.8

Value 2014(millions of US dollars)

On April 22, 2014, the WTO announced its �nal ruling in favor of Mexico in the dispute over the restrictive effects caused by "dolphin-safe" labeling on Mexican tuna exports to the United States market. The Mexican government recognized the WTO's decision which con�rms that the �shing methods used by the Mexican �eet comply with the highest international standards for the protection of species like dolphins.

The method employed by the Mexican tuna �eet is regulated by the Agreement on the International Dolphin Conservation Program recognized by the United Nations Food and Agriculture Organization (FAO) as having the highest sustainability, and which protects dolphins and tuna resources by avoiding the capture of juvenile tuna to ensure future supply.

FAO �gures for 2012 ranked Mexico 16th for world capture �shery production, representing 1.8% of the total. Despite Mexico's world ranking, its position is less favorable when the focus is on industrialization, a sign that with the raw material produced in the country, there is ample opportunity to invest in seafood processing and thereby increase value-added production.

Furthermore, the aquaculture industry in Mexico is in a stage of development and growth and therefore affords important investment opportunities: the cultivation of mollusks like oysters, shrimp, white �sh, tilapia, and others, for example. In particular there are species with potential for expansion such as abalone, clams, lobster, and shrimp.Exports can be increased through the introduction of Mexican products to the fast growing markets of Europe, Asia, and Russia, through key distribution channels like supermarkets.

MEXICO MEETS INTERNATIONAL STANDARDS