Embed Size (px)

Citation preview

Update on Changes to Withholding & Grandfathered Obligations

Debbie Mercer-Miller, Director and U.S. Securities Country Manager, Citi

Nicole Tanguy, Director and Corporate Tax Counsel, Citi

IMPORTANT: This presentation does not constitute tax advice and is for information purposes only.

Final FATCA Regulations Training Session #1

June 2013

Securities & Fund Services

Table of Contents

1. What You Need to Know About Withholding 2

2. Tax Character and Sourcing of Payments 5

3. Special Issues by Type of Withholding Agent 11

4. Withholding Timeline 16

5. Exceptions to Withholding 19

6. Grandfathered Obligations 21

1 For information purposes only.

1. What You Need to Know About Withholding

Conditions For FATCA Withholding to Apply

FATCA withholding will apply if all of the following conditions are met:

The payment being made is a “withholdable payment”

The payment constitutes U.S. source income or relates to the disposition of a security that

may pay U.S. source income.

The withholding agent is an entity that is obligated to perform FATCA withholding

The account or payee is not FATCA compliant

The payment is made on or after the applicable effective date

The payment is not a type excepted from FATCA withholding

3 For information purposes only.

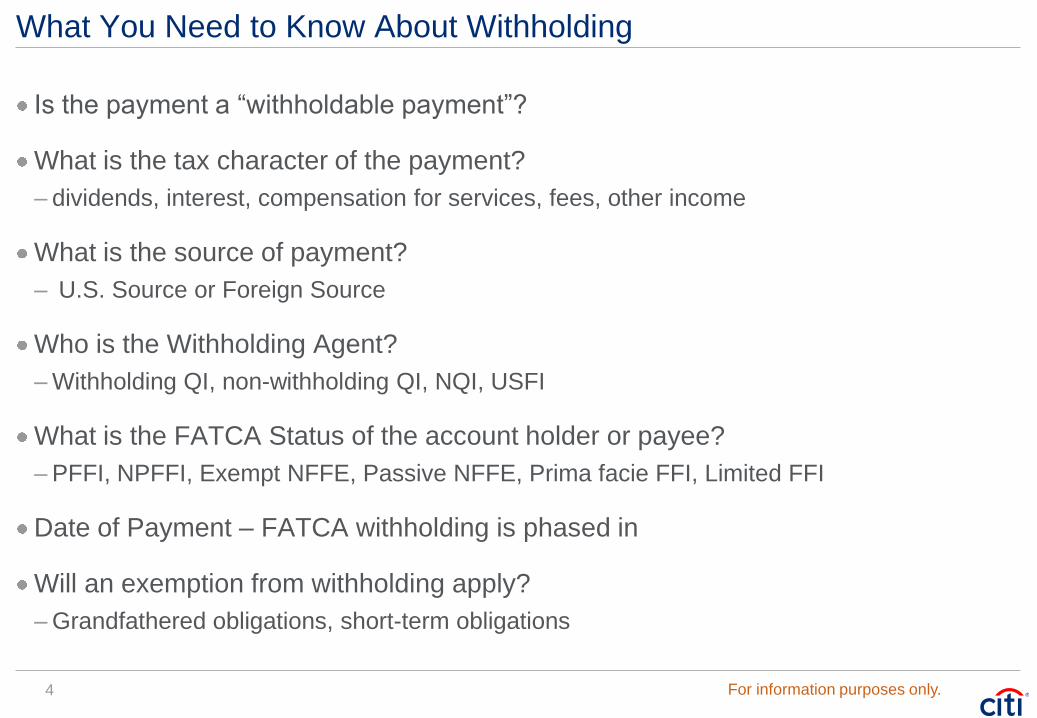

What You Need to Know About Withholding

Is the payment a “withholdable payment”?

What is the tax character of the payment?

– dividends, interest, compensation for services, fees, other income

What is the source of payment?

– U.S. Source or Foreign Source

Who is the Withholding Agent?

– Withholding QI, non-withholding QI, NQI, USFI

What is the FATCA Status of the account holder or payee?

– PFFI, NPFFI, Exempt NFFE, Passive NFFE, Prima facie FFI, Limited FFI

Date of Payment – FATCA withholding is phased in

Will an exemption from withholding apply?

– Grandfathered obligations, short-term obligations

4 For information purposes only.

2. Tax Character and Sourcing of Payments

What is a “Withholdable” Payment?

FATCA withholding will apply to certain types of “withholdable” payments:

U.S. source FDAP income (fixed or determinable, annual of periodic income):

– Interest (including interest on deposits in a foreign branch of a U.S. bank)

– Dividends

– Substitute or manufactured payment

– Original issue discount

Dividend equivalent payments:

– Substitute dividends paid under a securities loan or repo of a U.S. equity

– Payments under a swap pegged to dividends on a U.S. equity to the extent that they are dividend

equivalents under IRC section 871(m)

Gross Proceeds:

– Payments from the sale, redemption or other disposition of property that can pay U.S. source

dividends or interest

– But only if the sale or other disposition occurs after 2016

6

6 For information purposes only.

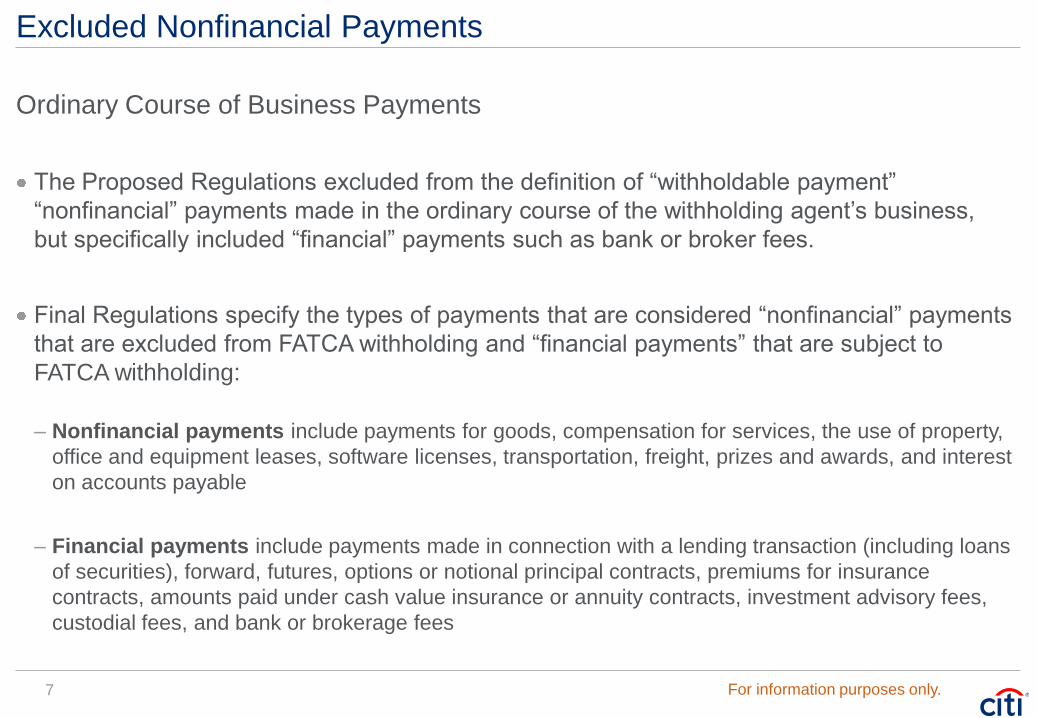

Excluded Nonfinancial Payments

Ordinary Course of Business Payments

The Proposed Regulations excluded from the definition of “withholdable payment”

“nonfinancial” payments made in the ordinary course of the withholding agent’s business,

but specifically included “financial” payments such as bank or broker fees.

Final Regulations specify the types of payments that are considered “nonfinancial” payments

that are excluded from FATCA withholding and “financial payments” that are subject to

FATCA withholding:

– Nonfinancial payments include payments for goods, compensation for services, the use of property,

office and equipment leases, software licenses, transportation, freight, prizes and awards, and interest

on accounts payable

– Financial payments include payments made in connection with a lending transaction (including loans

of securities), forward, futures, options or notional principal contracts, premiums for insurance

contracts, amounts paid under cash value insurance or annuity contracts, investment advisory fees,

custodial fees, and bank or brokerage fees

7 For information purposes only.

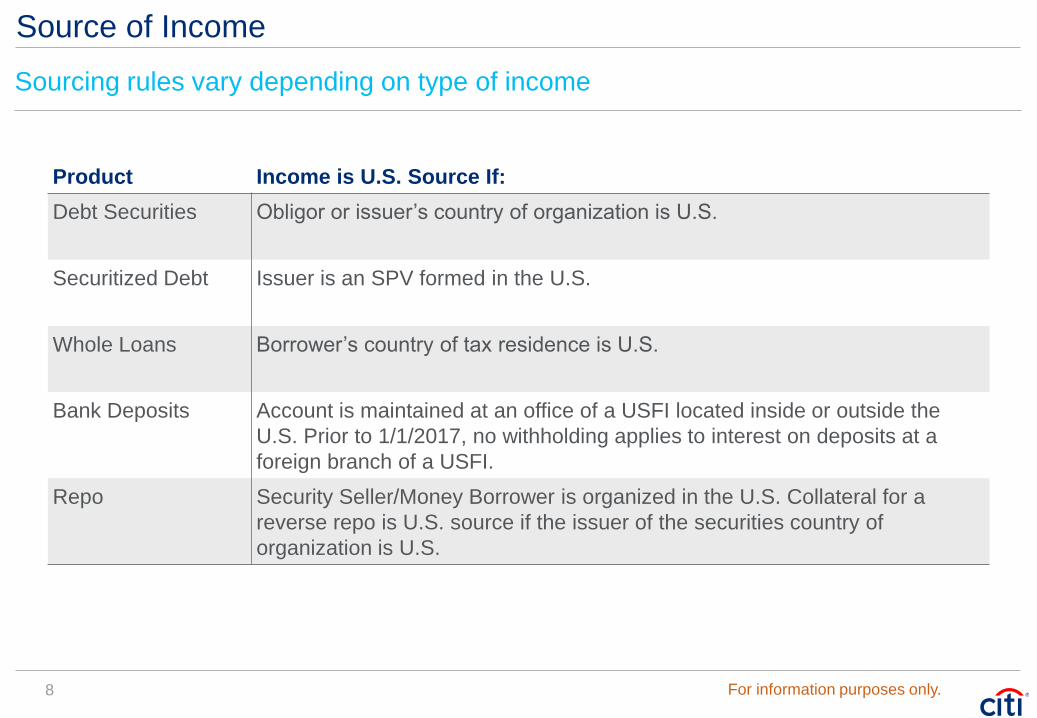

Source of Income

8

Product Income is U.S. Source If:

Debt Securities Obligor or issuer’s country of organization is U.S.

Securitized Debt Issuer is an SPV formed in the U.S.

Whole Loans Borrower’s country of tax residence is U.S.

Bank Deposits Account is maintained at an office of a USFI located inside or outside the

U.S. Prior to 1/1/2017, no withholding applies to interest on deposits at a

foreign branch of a USFI.

Repo Security Seller/Money Borrower is organized in the U.S. Collateral for a

reverse repo is U.S. source if the issuer of the securities country of

organization is U.S.

Sourcing rules vary depending on type of income

For information purposes only.

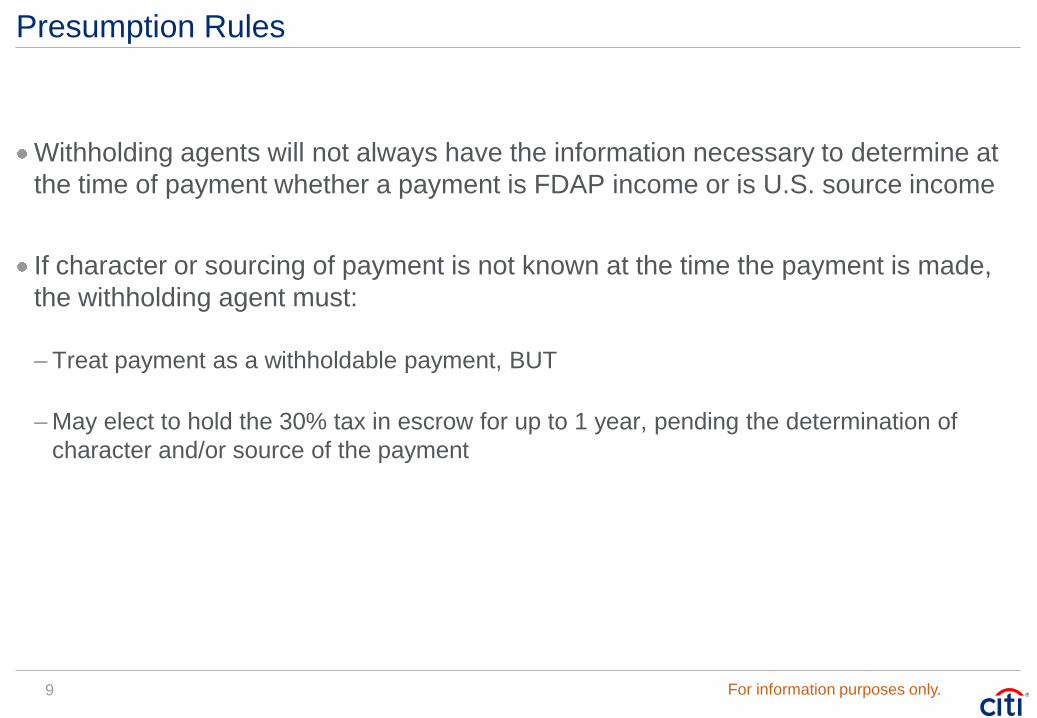

Presumption Rules

Withholding agents will not always have the information necessary to determine at

the time of payment whether a payment is FDAP income or is U.S. source income

If character or sourcing of payment is not known at the time the payment is made,

the withholding agent must:

– Treat payment as a withholdable payment, BUT

– May elect to hold the 30% tax in escrow for up to 1 year, pending the determination of

character and/or source of the payment

9 For information purposes only.

Changes from the Proposed Regulations

Withholding on gross proceeds is deferred until January 1, 2017

– New proposed regulations are expected to be published to address concerns about

withholding on gross proceed paid in a delivery vs. payment (DVP) transaction and

determining who is the payee

– Withholding agents may de-prioritize system development efforts related to payments of

gross proceeds

The IRS did not provide any guidance in the Final FATCA regulations on what is a

foreign pass-thru payment. However:

– The effective date for withholding on foreign pass-thru payments is January 1, 2017 at the

earliest, and

– USFIs are not required to withhold on foreign pass-thru payments

10 For information purposes only.

3. Special Issues by Type of Withholding Agent

Withholding Agents

FATCA withholding requirements are impacted by the type of withholding agent

– USFI, foreign branch of a USFI, Withholding QI, Non-withholding QI, NQI,

– A USFI is not required to withhold on payments made to individual accounts

– A QI that has not assumed primary withholding responsibility (i.e., a Non-withholding QI) or

an NQI can elect to be withheld upon by an upstream withholding agent

– A QI that has assumed primary withholding responsibility under Chapter 3 (i.e., a

Withholding QI) must actually perform withholding when required

– Citibank NA (CBNA) is a USFI

– A foreign branch of CBNA is obligated to perform withholding, unless it is a Non-withholding

QI that instructs an upstream withholding agent to withhold

– An NQI, NWP or NWT has a residual obligation to withhold if it knows or has reason to

know that an upstream withholding agent failed to withhold

The status of the legal entity that is making a payment will determine whether the

withholding agent is required to actually withhold or must instruct an upstream

withholding agent to perform withholding

12 For information purposes only.

Who is Subject to Withholding by USFIs?

Payments of U.S. source FDAP income made to:

Non-participating FFIs and noncompliant NFFEs on or after 1/1/2014

– Undocumented new accounts

– Pre-existing accounts that are documented as NPFFIs

Prima facie FFIs who do not provide documentation of their FATCA status as of 7/1/2014

– Pre-existing accounts that

Are documented as QIs or NQIs, or

Are presumed or documented as foreign entities and are identified as financial institution based certain industry

classification (NAICS or SIC) codes

Participating FFIs (other than Withholding QIs) who elect to be withheld upon

Limited branches and affiliates

– Non-participating FFIs and branches that are members of a FATCA compliant affiliated group but are

prohibited by local law from complete compliance with FATCA

13 For information purposes only.

USFI Withholding on Individuals

USFIs have no FATCA obligation to withhold on individuals

Payments of U.S. source FDAP income to documented U.S. persons:

– Generally no withholding

– 28% backup withholding on U.S. non-exempt recipients, if:

No Form W-9 on file

Notification of Name/TIN mismatch

Notification by IRS that Citi must withhold due to payee underreporting

Payments of U.S. source FDAP income to documented Non-U.S. individuals:

– Withholding under Chapter 3 at 30% unless reduced by statute or treaty

Payments of U.S. source FDAP income to undocumented Non-U.S. individuals are

presumed U.S. resident individuals and are subject to 28% backup withholding

14 For information purposes only.

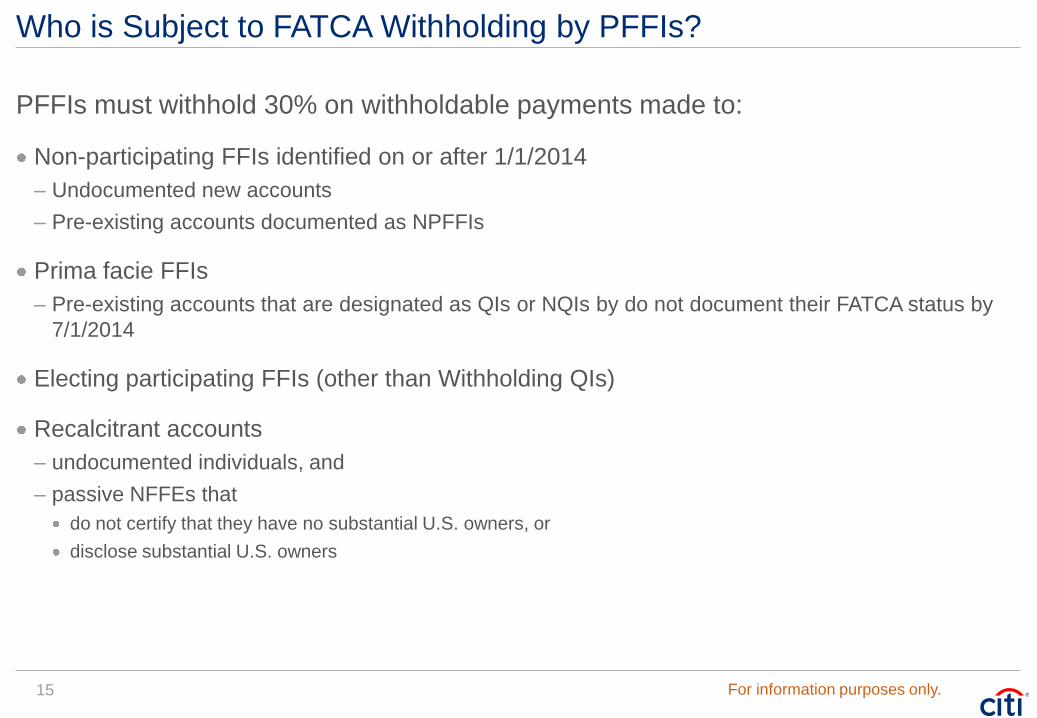

Who is Subject to FATCA Withholding by PFFIs?

PFFIs must withhold 30% on withholdable payments made to:

Non-participating FFIs identified on or after 1/1/2014

– Undocumented new accounts

– Pre-existing accounts documented as NPFFIs

Prima facie FFIs

– Pre-existing accounts that are designated as QIs or NQIs by do not document their FATCA status by

7/1/2014

Electing participating FFIs (other than Withholding QIs)

Recalcitrant accounts

– undocumented individuals, and

– passive NFFEs that

do not certify that they have no substantial U.S. owners, or

disclose substantial U.S. owners

15 For information purposes only.

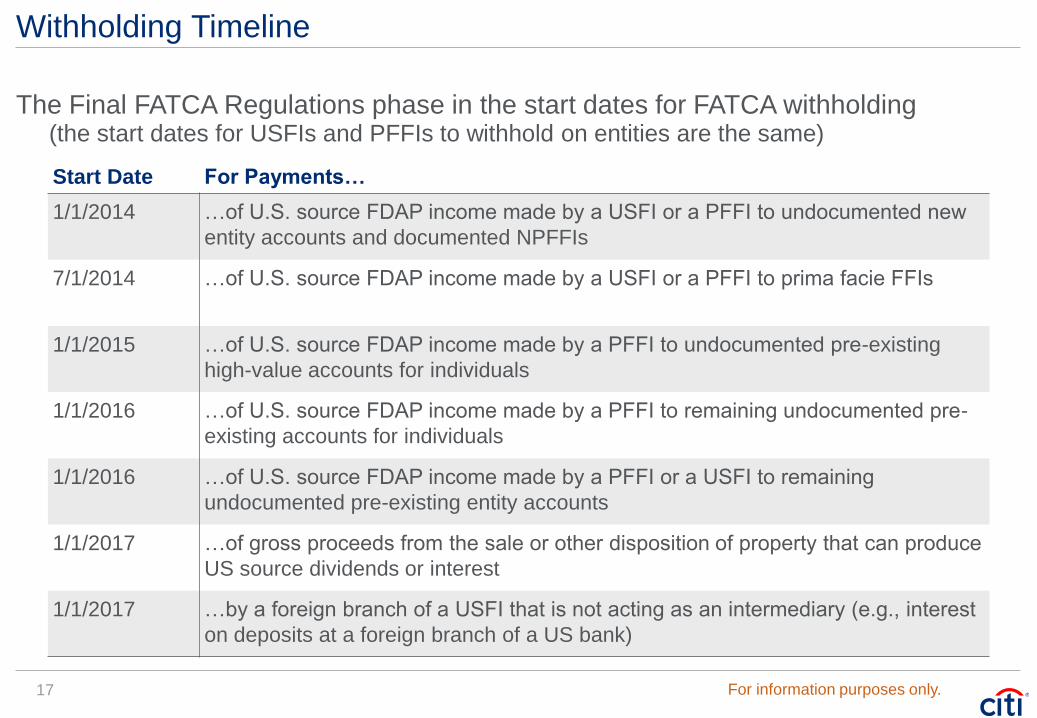

4. Withholding Timeline

Withholding Timeline

17

Start Date For Payments…

1/1/2014 …of U.S. source FDAP income made by a USFI or a PFFI to undocumented new

entity accounts and documented NPFFIs

7/1/2014 …of U.S. source FDAP income made by a USFI or a PFFI to prima facie FFIs

1/1/2015 …of U.S. source FDAP income made by a PFFI to undocumented pre-existing

high-value accounts for individuals

1/1/2016 …of U.S. source FDAP income made by a PFFI to remaining undocumented pre-

existing accounts for individuals

1/1/2016 …of U.S. source FDAP income made by a PFFI or a USFI to remaining

undocumented pre-existing entity accounts

1/1/2017 …of gross proceeds from the sale or other disposition of property that can produce

US source dividends or interest

1/1/2017 …by a foreign branch of a USFI that is not acting as an intermediary (e.g., interest

on deposits at a foreign branch of a US bank)

For information purposes only.

The Final FATCA Regulations phase in the start dates for FATCA withholding (the start dates for USFIs and PFFIs to withhold on entities are the same)

Changes in Circumstance

A change in circumstance is any change which will impact the FATCA status of an

account or payee.

– For example, the addition of U.S. indicia to an account or

– A change is the status of the payee as a U.S. or foreign person

Proposed Regulations provided a 90 day grace period to “cure” changes in

circumstance and avoid FATCA withholding in the interim

However, the Final Regulations change the end date of the grace period to the

earlier of 90th day after the change in circumstances or the date a withholdable

payment is made

– In effect there is no longer a grace period that protects accounts or payees from FATCA

withholding while new or additional documentation is collected

18 For information purposes only.

5. Exceptions to Withholding

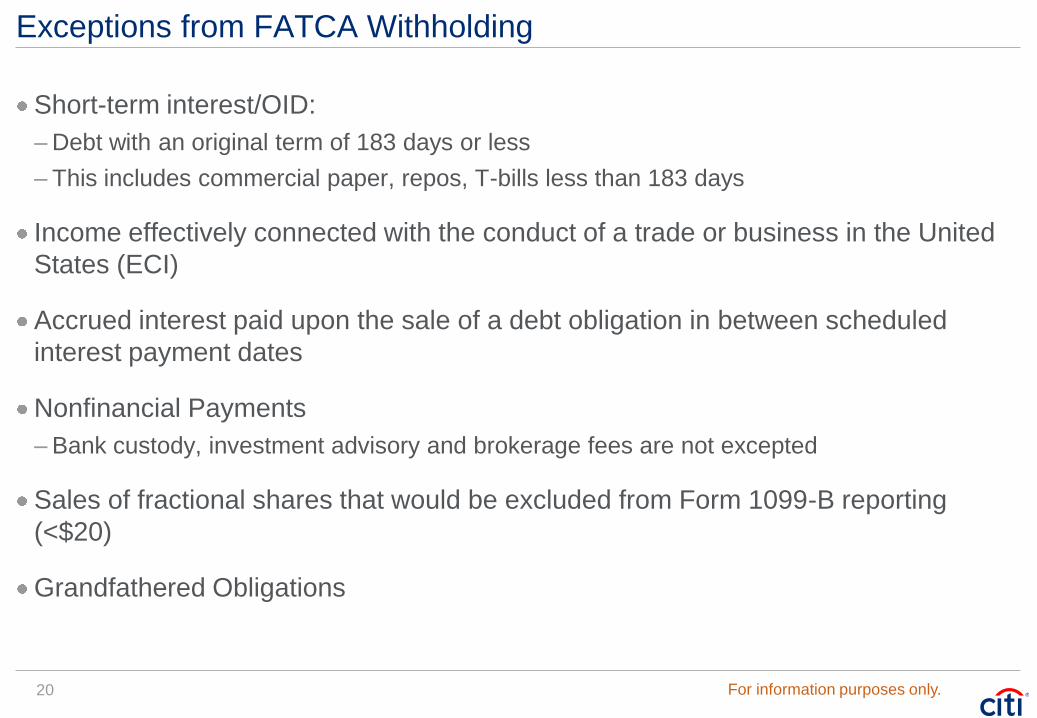

Exceptions from FATCA Withholding

Short-term interest/OID:

– Debt with an original term of 183 days or less

– This includes commercial paper, repos, T-bills less than 183 days

Income effectively connected with the conduct of a trade or business in the United

States (ECI)

Accrued interest paid upon the sale of a debt obligation in between scheduled

interest payment dates

Nonfinancial Payments

– Bank custody, investment advisory and brokerage fees are not excepted

Sales of fractional shares that would be excluded from Form 1099-B reporting

(<$20)

Grandfathered Obligations

20 For information purposes only.

6. Grandfathering

Impact on Grandfathered Obligations – Expanded Scope

The Final Regulations expand the scope of the grandfathering rules

Moved the date for treating outstanding obligations that pay or could pay U.S. source FDAP

income (“U.S. obligations”) as grandfathered from 1/1/2013 to 1/1/2014

Means U.S. obligations issued or entered into in 2013 are grandfathered

Any obligation that gives rise to a dividend equivalent payment under IRC section 871(m) is

grandfathered if the obligation is entered into on/before the day that is 6 months after the

date on which such obligations are treated as giving rise to dividend equivalent payments

– Applies to certain total return swaps over U.S. stocks

22 For information purposes only.

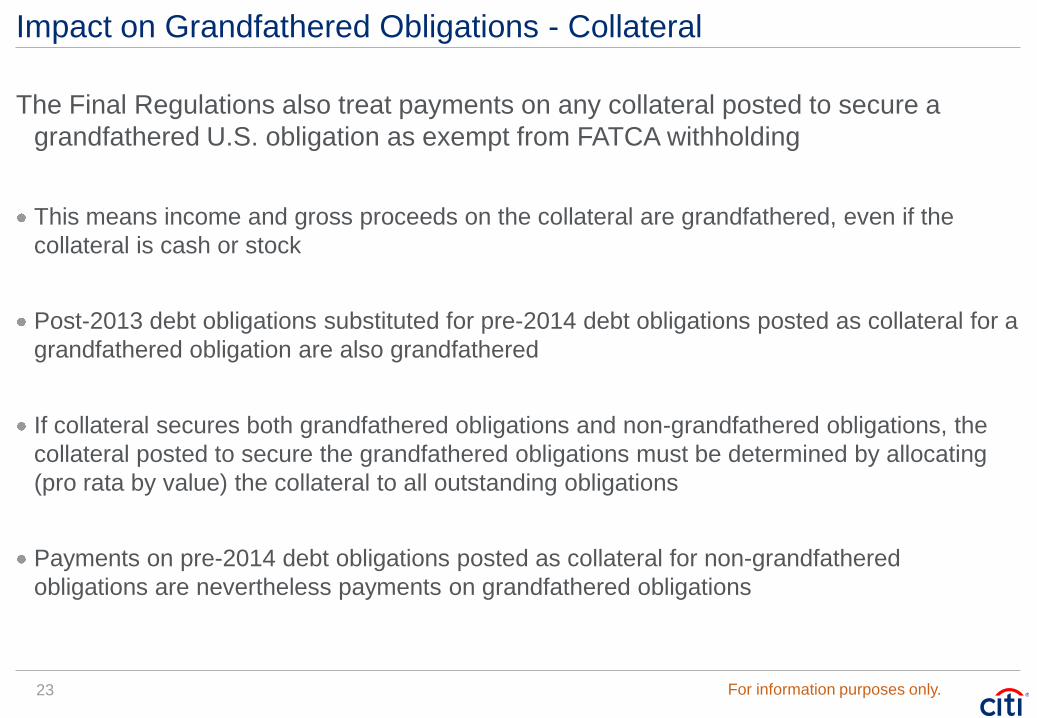

The Final Regulations also treat payments on any collateral posted to secure a

grandfathered U.S. obligation as exempt from FATCA withholding

This means income and gross proceeds on the collateral are grandfathered, even if the

collateral is cash or stock

Post-2013 debt obligations substituted for pre-2014 debt obligations posted as collateral for a

grandfathered obligation are also grandfathered

If collateral secures both grandfathered obligations and non-grandfathered obligations, the

collateral posted to secure the grandfathered obligations must be determined by allocating

(pro rata by value) the collateral to all outstanding obligations

Payments on pre-2014 debt obligations posted as collateral for non-grandfathered

obligations are nevertheless payments on grandfathered obligations

Impact on Grandfathered Obligations - Collateral

23 For information purposes only.

Impact on Grandfathered Obligations

Pay Foreign Pass-thru Payments

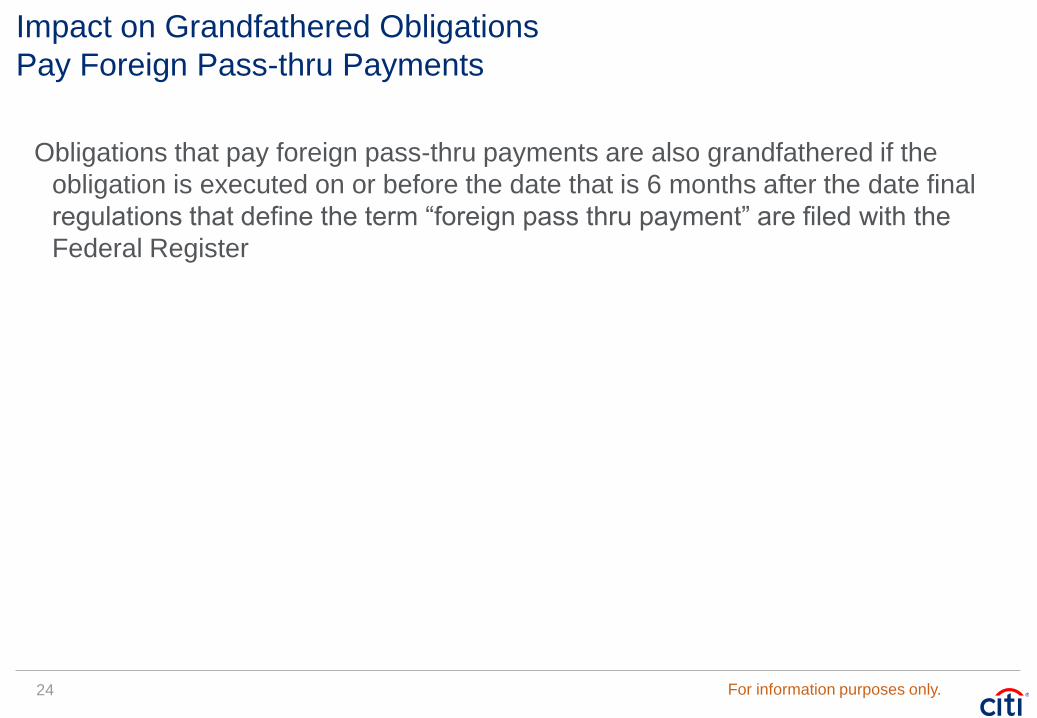

Obligations that pay foreign pass-thru payments are also grandfathered if the

obligation is executed on or before the date that is 6 months after the date final

regulations that define the term “foreign pass thru payment” are filed with the

Federal Register

24 For information purposes only.

Material Modifications

A grandfathered obligation will lose its status if there is a material modification of its

terms

– Examples of material modifications include a change in:

The yield of a debt instrument by more than the greater of 25 basis point or 5% of the annual yield

The timing of payments on a debt instrument that results in a material deferral of scheduled

payments

The obligor or security underlying a debt instrument

The nature of the obligation that causes it not to be a debt instrument

FATCA withholding will be required on payments made after the date the material

modification occurs

Citi is working to establish procedures to monitor grandfathered obligations for

material modifications

25 For information purposes only.

Determination of Grandfathered Status

The Final Regulations clarify how a withholding agent can determine grandfathered

status

Withholding agents may:

– Absent actual knowledge, rely upon a written statement of the issuer to determine whether the

obligation meets the requirements for grandfathering

The issuer (or an agent of the issuer) will be deemed to have actual knowledge

– Treat a modification as material only if the withholding agent knows or has reason to know the

modification is material

A withholding agent will have reason to know if it receives such a disclosure from the issuer of the

obligation

26 For information purposes only.

Citi believes that sustainability is good business practice. We work closely with our clients, peer financial institutions, NGOs and other partners to finance solutions to climate change, develop industry standards, reduce our own environmental

footprint, and engage with stakeholders to advance shared learning and solutions. Highlights of Citi’s unique role in promoting sustainability include: (a) releasing in 2007 a Climate Change Position Statement, the first US financial institution to do

so; (b) targeting $50 billion over 10 years to address global climate change: includes significant increases in investment and financing of renewable energy, clean technology, and other carbon-emission reduction activities; (c) committing to an

absolute reduction in GHG emissions of all Citi owned and leased properties around the world by 10% by 2011; (d) purchasing more than 234,000 MWh of carbon neutral power for our operations over the last three years; (e) establishing in

2008 the Carbon Principles; a framework for banks and their U.S. power clients to evaluate and address carbon risks in the financing of electric power projects; (f) producing equity research related to climate issues that helps to inform investors

on risks and opportunities associated with the issue; and (g) engaging with a broad range of stakeholders on the issue of climate change to help advance understanding and solutions.

Citi works with its clients in greenhouse gas intensive industries to evaluate emerging risks from climate change and, where appropriate, to mitigate those risks.

© 2013 Citibank, N.A. All rights reserved. Citi and Citi and Arc Design are trademarks and service marks of Citigroup Inc. or its affiliates and are used and registered throughout the world.

IRS Circular 230 Disclosure: Citigroup Inc. and its affiliates do not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended or written to be used, and cannot be used or relied upon, by

you for the purpose of avoiding any tax penalties and (ii) may have been written in connection with the "promotion or marketing" of any transaction contemplated hereby ("Transaction"). Accordingly, you should seek advice

based on your particular circumstances from an independent tax advisor.

In any instance where distribution of this communication is subject to the rules of the US Commodity Futures Trading Commission (“CFTC”), this communication constitutes an invitation to consider entering into a derivatives

transaction under U.S. CFTC Regulations §§ 1.71 and 23.605, where applicable, but is not a binding offer to buy/sell any financial instrument.

However, this is not a recommendation to enter into any swap with any counterparty or a recommendation of a trading strategy involving a swap. Prior to recommending a swap or a trading strategy involving a swap to you,

Citigroup would need to undertake diligence in order to have a reasonable basis to believe that the recommended swap or swap trading strategy is suitable for you, obtain written representations from you that you are

exercising independent judgment in evaluating any such recommendation, and make certain disclosures to you. Furthermore, nothing in this pitch book is, or should be construed to be, an offer to enter into a swap.

Any terms set forth herein are intended for discussion purposes only and are subject to the final terms as set forth in separate definitive written agreements. This presentation is not a commitment to lend, syndicate a financing, underwrite or

purchase securities, or commit capital nor does it obligate us to enter into such a commitment, nor are we acting as a fiduciary to you. By accepting this presentation, subject to applicable law or regulation, you agree to keep confidential the

information contained herein and the existence of and proposed terms for any Transaction.

Prior to entering into any Transaction, you should determine, without reliance upon us or our affiliates, the economic risks and merits (and independently determine that you are able to assume these risks) as well as the legal, tax and accounting

characterizations and consequences of any such Transaction. In this regard, by accepting this presentation, you acknowledge that (a) we are not in the business of providing (and you are not relying on us for) legal, tax or accounting advice, (b)

there may be legal, tax or accounting risks associated with any Transaction, (c) you should receive (and rely on) separate and qualified legal, tax and accounting advice and (d) you should apprise senior management in your organization as to

such legal, tax and accounting advice (and any risks associated with any Transaction) and our disclaimer as to these matters. By acceptance of these materials, you and we hereby agree that from the commencement of discussions with

respect to any Transaction, and notwithstanding any other provision in this presentation, we hereby confirm that no participant in any Transaction shall be limited from disclosing the U.S. tax treatment or U.S. tax structure of such Transaction.

We are required to obtain, verify and record certain information that identifies each entity that enters into a formal business relationship with us. We will ask for your complete name, street address, and taxpayer ID number. We may also

request corporate formation documents, or other forms of identification, to verify information provided.

Any prices or levels contained herein are preliminary and indicative only and do not represent bids or offers. These indications are provided solely for your information and consideration, are subject to change at any time without notice and are

not intended as a solicitation with respect to the purchase or sale of any instrument. The information contained in this presentation may include results of analyses from a quantitative model which represent potential future events that may or

may not be realized, and is not a complete analysis of every material fact representing any product. Any estimates included herein constitute our judgment as of the date hereof and are subject to change without any notice. We and/or our

affiliates may make a market in these instruments for our customers and for our own account. Accordingly, we may have a position in any such instrument at any time.

Although this material may contain publicly available information about Citi corporate bond research, fixed income strategy or economic and market analysis, Citi policy (i) prohibits employees from offering, directly or indirectly, a favorable or

negative research opinion or offering to change an opinion as consideration or inducement for the receipt of business or for compensation; and (ii) prohibits analysts from being compensated for specific recommendations or views contained in

research reports. So as to reduce the potential for conflicts of interest, as well as to reduce any appearance of conflicts of interest, Citi has enacted policies and procedures designed to limit communications between its investment banking and

research personnel to specifically prescribed circumstances.

![Working Effectively with Citi - DoD Travel [Read-Only]securities.citibank.com/transactionservices/home/card...Working Effectively with Citi DoD Travel Card Judi Latham Citi® Commercial](https://img.pdfslide.net/doc/110x75/5abae90e7f8b9af27d8c2dbe/working-effectively-with-citi-dod-travel-read-only-effectively-with-citi-dod.jpg)