Embed Size (px)

Citation preview

Monthly Canadian ABS Report

SEPTEMBER 2010

Securitization Servicer Report

Senior Vice PresidentStructured FinanceTel. +1 416 597 [email protected]

CONTACT INFORMATION

Scott Bridges

Vice President SurveillanceStructured FinanceTel. +1 416 597 [email protected]

Clara Vargas

Conventions used in this reportAll currency values are in Canadian Dollars unless otherwise specified.Percentage values may not add exactly to 100% due to rounding.Exchange rate: $1.00 US = $1.029 Canadian

Olga MironenkoFinancial AnalystStructured FinanceTel. +1 416 597 [email protected]

DBRS is a full-service credit rating agencyestablished in 1976. Privately owned and operatedwithout affiliation to any financial institution,DBRS is respected for its independent, third-partyevaluations of corporate and government issues,spanning North America, Europe and Asia.DBRSs extensive coverage of securitizations andstructured finance transactions solidifies ourstanding as a leading provider of comprehensive,in-depth credit analysis.

All DBRS ratings and research are available inhard-copy format and electronically on Bloombergand at DBRS.com, our lead delivery tool fororganized, Web-based, up-to-the-minuteinformation. We remain committed tocontinuously refining our expertise in the analysisof credit quality and are dedicated to maintainingobjective and credible opinions within the globalfinancial marketplace.

Monthly Canadian ABS Report

September 2010

Table of ContentsSummary 5

Market Summary 5Asset Composition and Market Share 9

Auto Loans 11Canadian Capital Auto Receivables Asset Trust II, 2006-1 11Canadian Capital Auto Receivables Asset Trust II, 2006-2 12Canadian Capital Auto Receivables Asset Trust II, 2007-1 13Canadian Capital Auto Receivables Asset Trust II, 2010-1 14Canadian Capital Auto Receivables Asset Trust III, 2010-1 15Ford Auto Securitization Trust 2009-R1 16Ford Auto Securitization Trust 2010-R1 17Ford Auto Securitization Trust 2010-R3 18

Auto Leases 19NIF-T, 2010-1 19

Fleet Leasing 20Fleet Leasing Receivables Trust, Series 2010-1 20

Floorplan Financing 21Canadian SWIFT Master Auto Receivables Trust, Series 2010-1 21CNH Capital Canada Wholesale Trust, 2009-1 22Ford Floorplan Auto Securitization Trust, 2006 23Ford Floorplan Auto Securitization Trust, 2010-F1 24Ford Floorplan Auto Securitization Trust, 2010-F2 25

Credit Cards 26Algonquin Credit Card Trust 26Broadway Credit Card Trust 28Canadian Credit Card Trust 30CARDS II Trust 32Eagle Credit Card Trust 34Glacier Credit Card Trust 36Gloucester Credit Card Trust 38Golden Credit Card Trust 40Master Credit Card Trust 42SCORE Trust 44

Lines of Credit 46Genesis Trust 46

Residential Mortgages 47Canada Mortgage Acceptance Corporation, 2006-C4 47Canada Mortgage Acceptance Corporation, 2006-C5 48Xceed Mortgage Trust, Series 2006-T1 49Xceed Mortgage Trust, Series 2007-T2 50

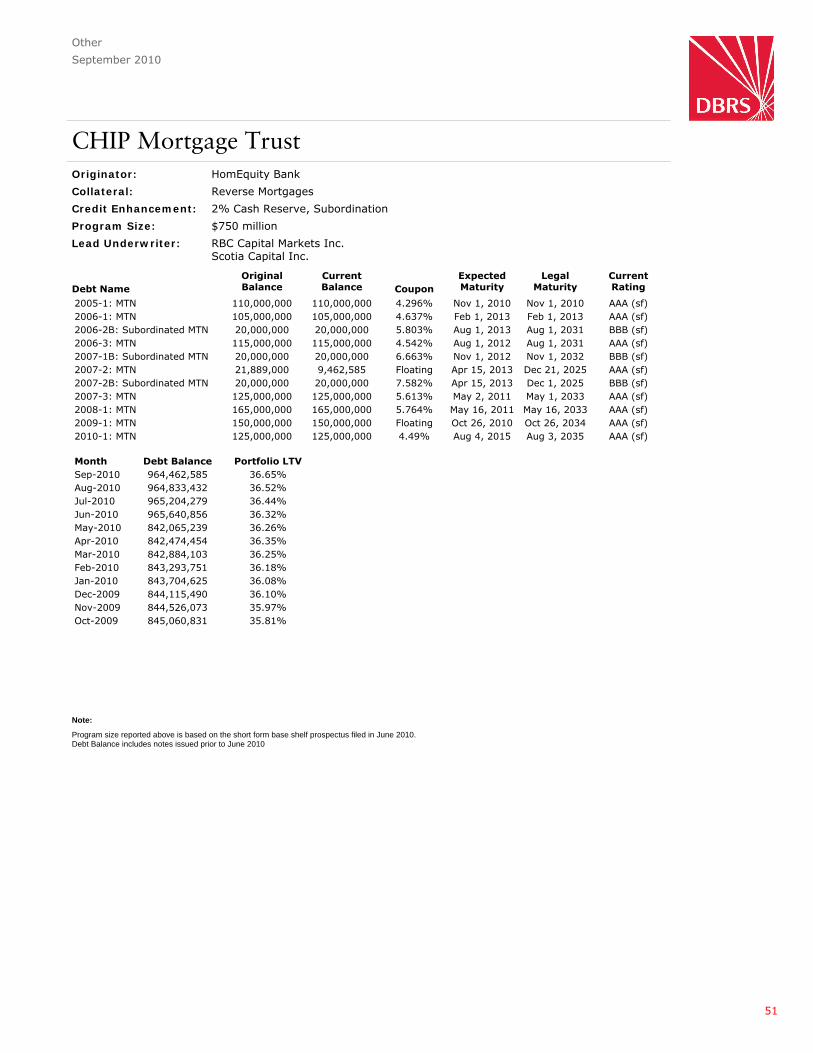

Other 51CHIP Mortgage Trust 51ASG Trust 52CBC Monetization Trust Notes 53

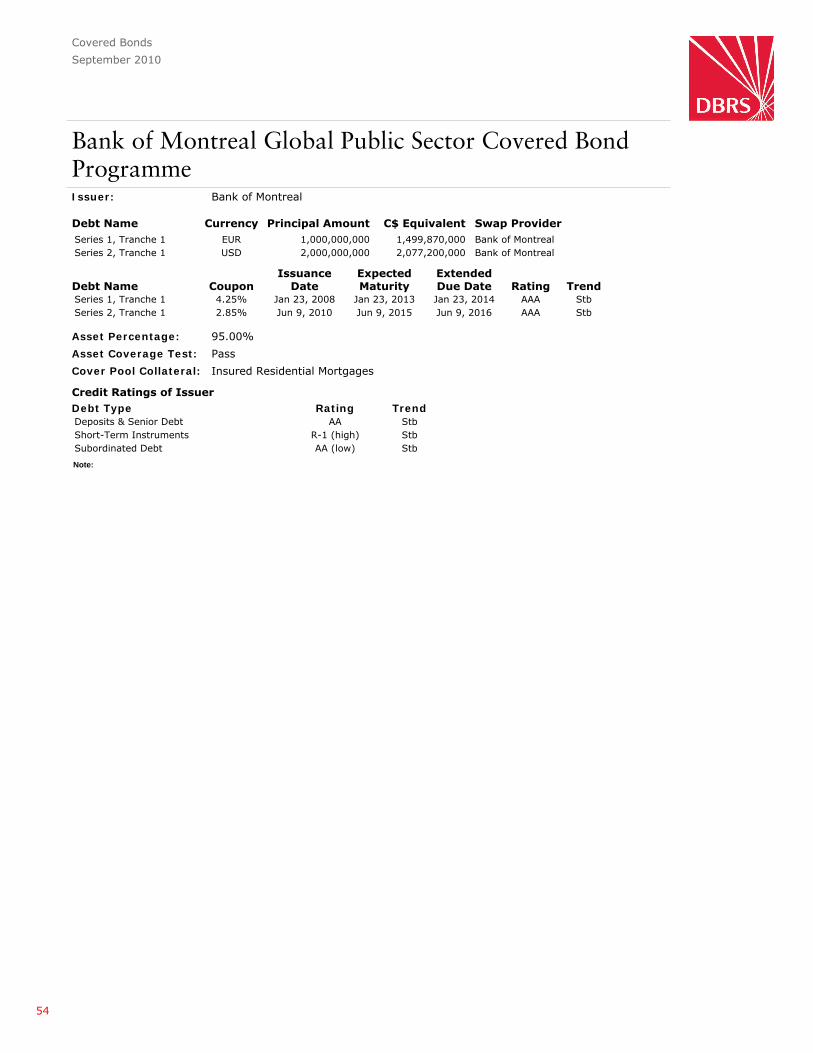

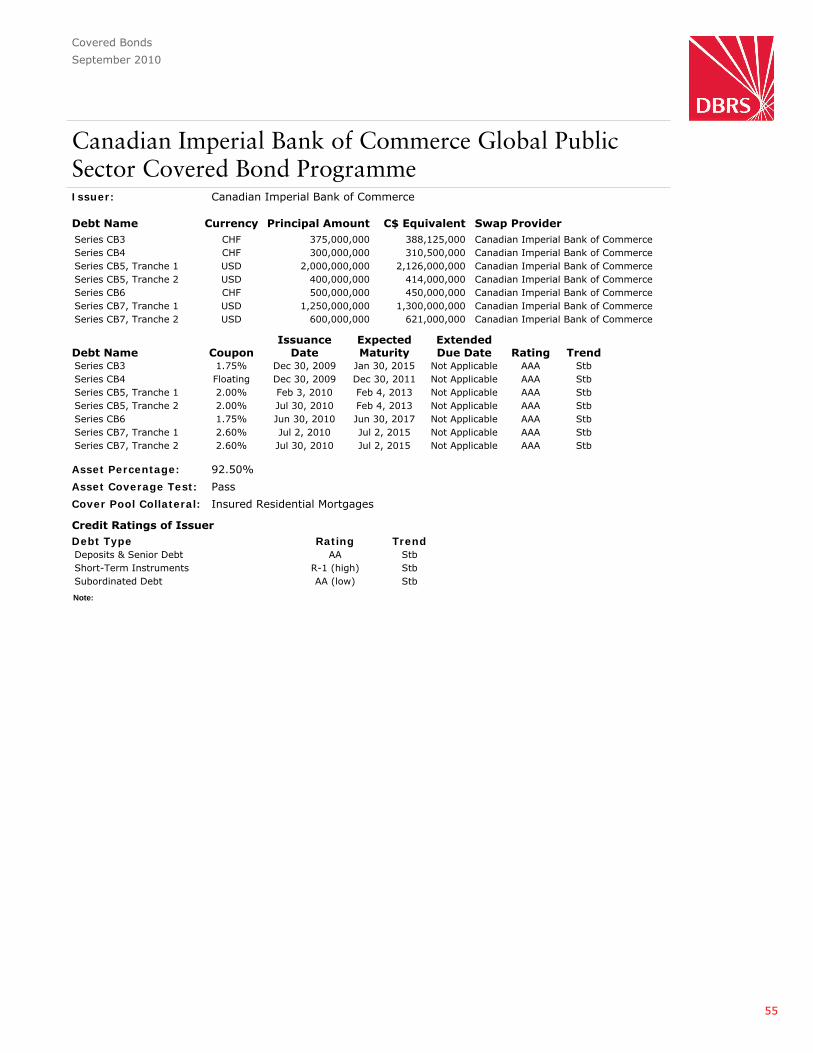

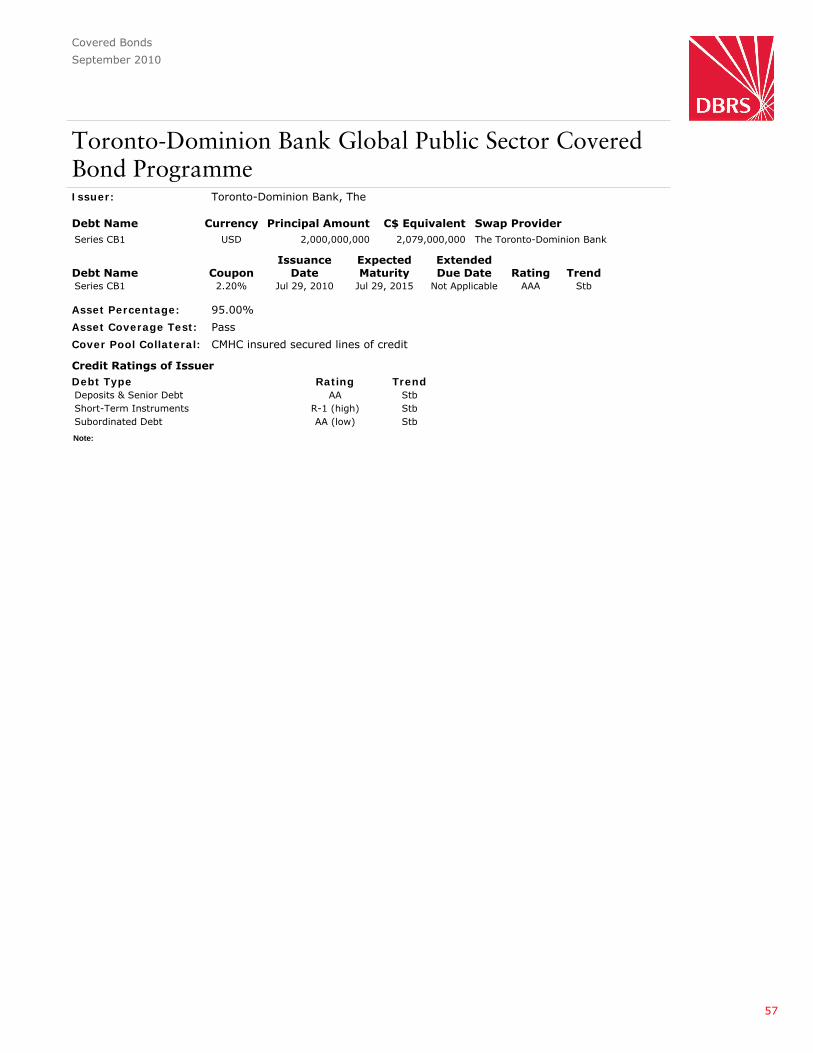

Covered Bonds 54Bank of Montreal Global Public Sector Covered Bond Programme 54Canadian Imperial Bank of Commerce Global Public Sector Covered Bond Programme 55

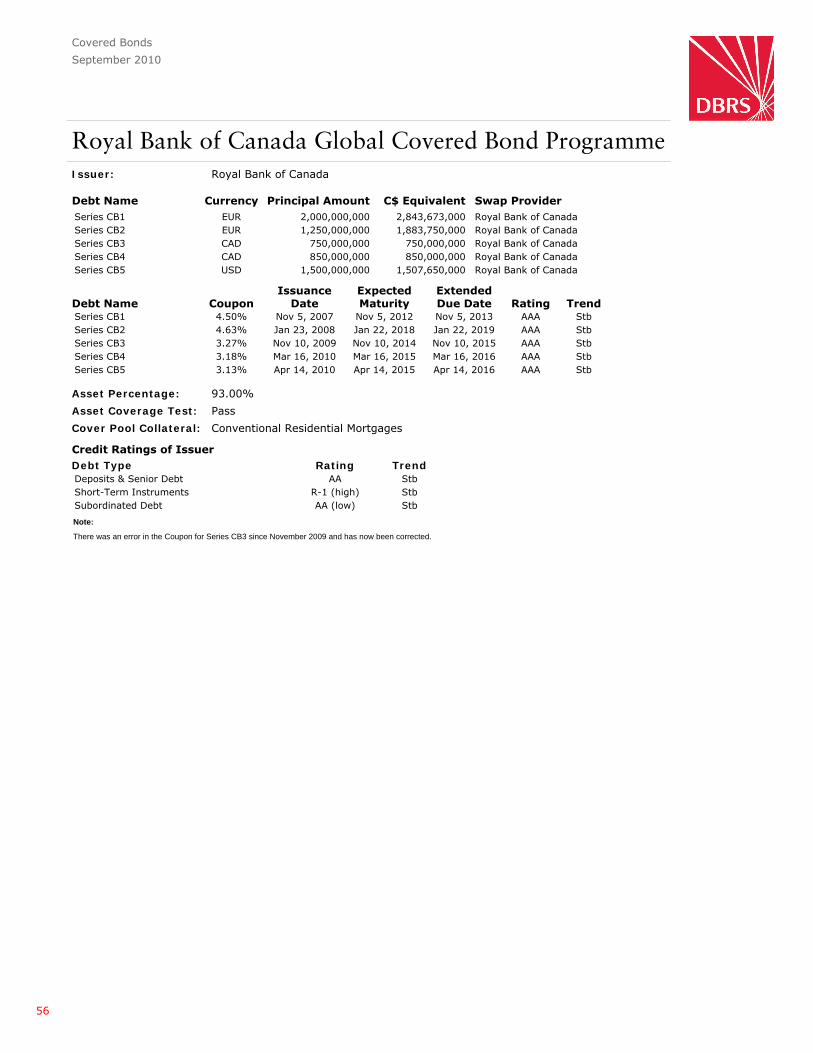

Royal Bank of Canada Global Covered Bond Programme 56Toronto-Dominion Bank Global Public Sector Covered Bond Programme 57

Appendix A: Asset Class Information 58

3

Monthly Canadian ABS Report

September 2010

Table of Contents (continued)Glossary 59

4

Market Summary

Monthly Canadian ABS Report

September 2010

Summary

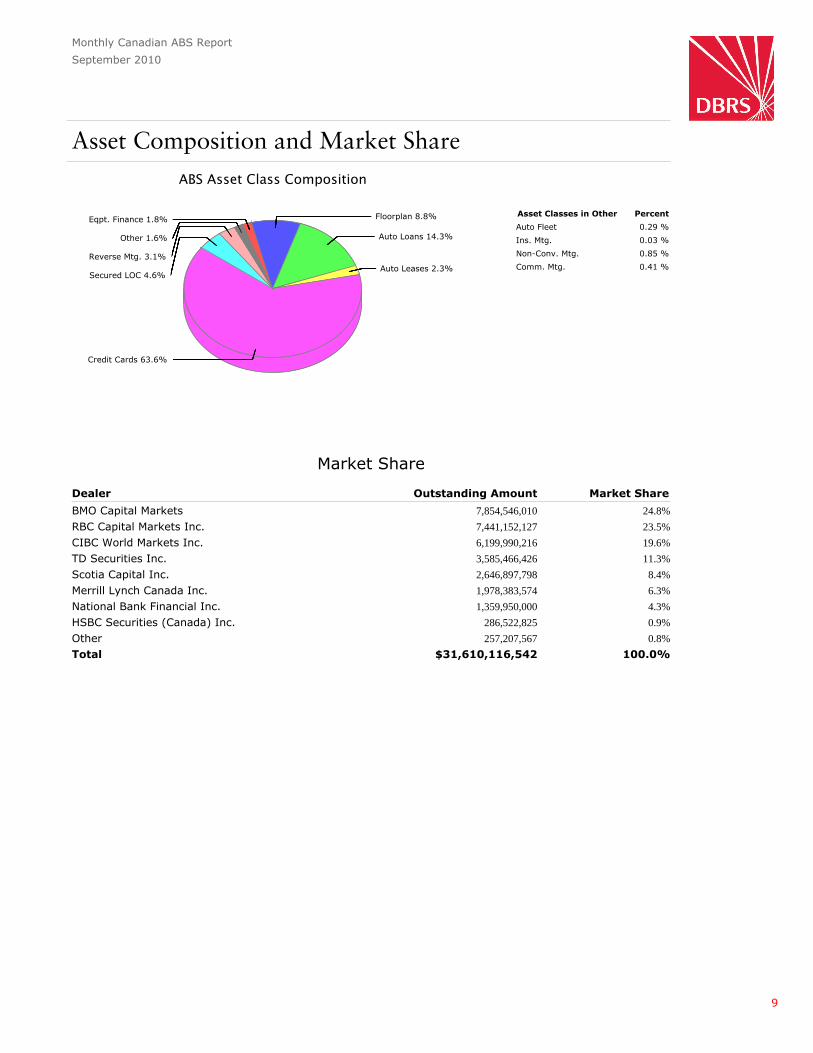

The year 2010 has seen the comeback of the Canadian ABS market, with 18 new issuances in thefirst three quarters of the year, totalling $10.7 billion, compared with six issuances for $3.9 billionduring the same period in 2009. Most of the activity has come from the auto industry, with eightnew transactions ($4.4 billion), followed by five credit card receivables ($3.7 billion), four floorplan($2.5 billion) and one reverse mortgage ($0.1 billion). From January to September 2009, the marketsaw only five new auto issuances and one transaction from the equipment finance industry.

Despite the higher activity in 2010, the volume from new issuances has been offset by maturitiesand normal runoff, resulting in a market size hovering near $31.6 billion.

Nonetheless, all the new transactions, combined with the attrition, have changed the shape of themarket, with increases in market share for the auto industry from 13.0% in December 2009 to16.9% in September 2010 and for floorplan transactions from 1.9% to 8.8%. Conversely, creditcard receivables have lost share in the market, despite the five large issuances seen this year, goingfrom 66.6% at the end of 2009 to 63.6% at the end of Q3 2010.

During September 2010, there was one new issuance from Ford Auto Securitization Trust 2010-R3and two full repayments - CARDS II Series 2005-3 and Canada Mortgage Acceptance Corporation,2005-C5, Class F - which resulted in an increase of $0.1 billion, or 0.3%, month over month. Thetotal outstanding amount in the Canadian ABS market stood at $31.6 billion as of September 30,2010.

On September 1, 2010, $285.4 million of delinquent, charged-off and low credit score accountswere removed from the custodial pool of Broadway Credit Card Trust in connection with the saleto Canadian Imperial Bank of Commerce (CIBC). This affected the reported performance of theTrust, reflected in zero credit losses, lower payment rate and low delinquencies for the month ofSeptember 2010. DBRS expects the performance to normalize in a few months.

Enhanced Monthly Canadian ABS Report

As part of DBRS's ongoing efforts to add transparency to the markets and commitment to provideenhanced disclosure, a new report, Enhanced Monthly Canadian ABS Report, has been produced inconjunction with the existing Monthly Canadian ABS Report.

5

Market Summary (continued)

Monthly Canadian ABS Report

September 2010

The Monthly Canadian ABS Report now has links that allow the user to go from the table ofcontents or from the individual transaction page to the corresponding Enhanced Monthly CanadianABS Report for that particular issuance.

The Enhanced Monthly Canadian ABS Report offers additional metrics, longer data series,definitions and charts that provide the user with both a numeric and a graphic presentation toallow a quick review of the overall performance and trends for each transaction as well asbenchmarking of transactions within an asset class.

For a limited period of time, the following select issuances will be available to the general public.Full access to the Enhanced Monthly Canadian ABS Report requires a subscription.

- Canada Mortgage Acceptance Corporation, 2006-C4- Canadian Capital Auto Receivables Asset Trust II, 2006-2- Fleet Leasing Receivables Trust, Series 2010-1- Ford Floorplan Auto Securitization Trust, 2006- Genesis Trust- Golden Credit Card Trust- NIF-T, 2010-1

Rating Actions

On September 1, 2010, DBRS noted that Fleet Leasing Receivables Trust issued Asset-BackedNotes, Series 2010-2, Class A and Class B on August 31, 2010. At this time, DBRS notes that thisissuance has no impact on the ratings of the classes of Asset-Backed Notes, Series 2010-1 issued bythe Trust on January 27, 2010.

On September 1, 2010, DBRS confirmed the ratings of Broadway Credit Card Trust with theclosing of the sale of $2.1 billion in MasterCard receivables from Citi Cards Canada Inc., the initialseller and servicer of the Trust, to Canadian Imperial Bank of Commerce, as discussed in the DBRSpress release dated June 15, 2010. The ratings for the outstanding notes issued by the Trust havebeen confirmed as follows:

- AAA (sf) for the Credit Card Receivables-Backed Class A Notes, Series 2004-2- "A" (sf) for the Credit Card Receivables-Backed Class B Notes, Series 2004-2- BBB (sf) for the Credit Card Receivables-Backed Class C Notes, Series 2004-2- AAA (sf) for the Credit Card Receivables-Backed Class A Notes, Series 2008-1- "A" (sf) for the Credit Card Receivables-Backed Class B Notes, Series 2008-1- BBB (sf) for the Credit Card Receivables-Backed Class C Notes, Series 2008-1- AAA (sf) for the Credit Card Receivables-Backed Class A Notes, Series 2008-2- "A" (sf) for the Credit Card Receivables-Backed Class B Notes, Series 2008-2- BBB (sf) for the Credit Card Receivables-Backed Class C Notes, Series 2008-2

On September 1, 2010, DBRS discontinued the ratings of the Variable Rate Credit CardReceivables-Backed Class A Notes, Series 2008-3, the Credit Card Receivables-Backed Class BNotes, Series 2008-3 and the Credit Card Receivables-Backed Class C Notes, Series 2008-3 issuedby Broadway Credit Card Trust as the Notes were fully repaid as of August 31, 2010.

On September 9, 2010, DBRS discontinued the rating of the Covered Bonds, Series CB1 issuedunder the Canadian Imperial Bank of Commerce (Global Public Sector Covered Bond Programme)as the Series was fully repaid on September 3, 2010.

6

Market Summary (continued)

Monthly Canadian ABS Report

September 2010

On September 15, 2010, DBRS assigned the following provisional ratings to Ford AutoSecuritization Trust 2010-R3 and finalized the ratings on September 28, 2010:

- AAA (sf) to the Asset-Backed Notes, Series 2010-R3, Class A-1 (the Class A-1 Notes)- AAA (sf) to the Asset-Backed Notes, Series 2010-R3, Class A-2 (the Class A-2 Notes)- AAA (sf) to the Asset-Backed Notes, Series 2010-R3, Class A-3 (the Class A-3 Notes)- AA (high) (sf) to the Asset -Backed Notes, Series 2010-R3, Class B (the Class B Notes)- A (high) (sf) to the Asset -Backed Notes, Series 2010-R3, Class C (the Class C Notes)- BBB (high) (sf) to the Asset -Backed Notes, Series 2010-R3, Class D (the Class D Notes)

On September 16, 2010, DBRS confirmed the rating of the Series 2008-1, Class A-2 Notes of CITCanada Equipment Receivables Trust, Series 2008-1 at AAA (sf).

On September 16, 2010, DBRS confirmed the rating of the Series 2009-1, Class A-2 Notes of CITCanada Equipment Receivables Trust II, Series 2009-1 at AAA (sf).

On September 17, 2010, DBRS confirmed the rating of the VPR Loans, Series 2006-1 issued byCanadian Capital Auto Receivables Asset Trust II at AAA (sf), with a Stable trend.

On September 17, 2010, DBRS confirmed the rating of the VPR Loans, Series 2006-2 (the VPRLoans) issued by Canadian Capital Auto Receivables Asset Trust II at AAA (sf), with a Stable trend.

On September 17, 2010, DBRS confirmed the rating of the VPR Loans, Series 2007-1 (the VPRLoans) issued by Canadian Capital Auto Receivables Asset Trust II, Series 2007-1 at AAA (sf), witha Stable trend.

On September 17, 2010, DBRS confirmed the following ratings of Ford Auto Securitization Trust2009-R1:

- AAA (sf) to the Asset-Backed Notes, Series 2009-R1, Class A-1- AAA (sf) to the Asset-Backed Notes, Series 2009-R1, Class A-2- AAA (sf) to the Asset-Backed Notes, Series 2009-R1, Class A-3

On September 17, 2010, DBRS confirmed the rating of the Asset-Backed Notes, Series 2009-R2issued by Ford Auto Securitization Trust 2009-R2 at AAA (sf).

On September 17, 2010, DBRS confirmed the following ratings of the Ford Auto SecuritizationTrust 2009-R3:

- AAA (sf) for the Asset-Backed Notes, Series 2009-R3, Class A-1- AAA (sf) for the Asset-Backed Notes, Series 2009-R3, Class A-2- AAA (sf) for the Asset-Backed Notes, Series 2009-R3, Class A-3

On September 21, 2010, DBRS discontinued the rating of the Covered Bonds, Series CB2 issuedunder the Canadian Imperial Bank of Commerce (Global Public Sector Covered Bond Programme)as the Series was fully repaid on September 16, 2010.

On September 24, 2010, DBRS discontinued the ratings of the Credit Card Receivables BackedFloating Rate Notes, Series 2005-3 issued by CARDS II Trust as the Notes were fully repaid onSeptember 23, 2010.

For more details regarding these rating actions, please refer to the press release on www.dbrs.com.7

Market Summary (continued)

Monthly Canadian ABS Report

September 2010

Subsequent Events

On October 5, 2010, DBRS noted that CNH Capital Canada Wholesale Trust entered into anagreement on September 24, 2010, whereby it issued asset-backed notes Series CW2010-1.

On October 15, 2010, DRBS discontinued the ratings of the Credit Card Receivables-BackedNotes, Series 2005-4 (the Notes) issued by CARDS II Trust as the Notes were fully repaid onOctober 15, 2010.

On October 19, 2010, DBRS discontinued the ratings of the Series 2005-1, Class A Notes, Class BNotes and Class C Notes issued by Algonquin Credit Card Trust as the Notes were fully repaid onOctober 15, 2010.

On October 19, 2010, DBRS assigned a rating of AAA to the Series CB8 covered bonds issuedunder the Canadian Imperial Bank of Commerce Global Public Sector Covered Bond Programme.The Series CB8 (AUD 750 million) covered bonds have a coupon rate of 5.75% and a maturity dateof December 19, 2013. All covered bonds issued under the Programme rank pari passu with eachother.

On October 21, 2010, DBRS assigned a provisional rating of AAA to the Covered Bonds, Series 2to be issued under the Bank of Nova Scotia (BNS) US$15 billion Global Public Sector CoveredBond Programme. The rating was finalized on October 29, 2010. As all covered bonds issued underthe Programme rank pari passu with each other, DBRS assigned a rating of AAA to the CoveredBonds, Series 1 issued on July 26, 2010, under the Programme. The Series 1 (US$2.5 billion)covered bonds have a coupon of 1.45% and a maturity date of July 26, 2013.

On October 22, 2010, DBRS discontinued the rating of the Class A-1 Senior Medium-Term Notes,Series 2009-1, issued by BMW Canada Auto Trust as the Notes were fully repaid as of September20, 2010.

On October 22, 2010, DBRS discontinued the rating of the Class A-1 Senior Medium-Term Notes,Series 2009-1 issued by NIF-T as the Notes were fully repaid as of March 23, 2010.

For more details regarding these rating actions, please refer to the press release on www.dbrs.com.

8

Asset Composition and Market Share

Monthly Canadian ABS Report

September 2010

Market ShareOutstanding AmountDealer

BMO Capital Markets 7,854,546,010 24.8%

RBC Capital Markets Inc. 7,441,152,127 23.5%

CIBC World Markets Inc. 6,199,990,216 19.6%

TD Securities Inc. 3,585,466,426 11.3%

Scotia Capital Inc. 2,646,897,798 8.4%

Merrill Lynch Canada Inc. 1,978,383,574 6.3%

National Bank Financial Inc. 1,359,950,000 4.3%

HSBC Securities (Canada) Inc. 286,522,825 0.9%

Other 257,207,567 0.8%

$31,610,116,542 100.0%Total

Asset Classes in Other Percent

Auto Fleet 0.29 %

Ins. Mtg. 0.03 %

Non-Conv. Mtg. 0.85 %

Comm. Mtg. 0.41 %

Market Share

9

Monthly Canadian ABS Report

September 2010

10 This page intentionally left blank.

Auto Loans

September 2010

Canadian Capital Auto Receivables Asset Trust II, 2006-1Originator: Ally Credit Canada Limited

Collateral: Portfolio of new subvented retail light truck and car loans from Ally

Credit Enhancement: Cash Reserve, Excess Spread, Overcollateralization, Subordination

Program Size: $1.1 billion

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Class A-1 190,000,000 0 4.171% Jan 17, 2007 Jul 17, 2012 DiscontinuedClass A-2 235,000,000 0 4.277% Jan 17, 2008 Jul 17, 2012 DiscontinuedClass A-3 255,000,000 0 4.393% Jan 17, 2009 Jul 17, 2012 DiscontinuedClass B 27,000,000 0 4.863% Jan 17, 2009 Jul 17, 2012 DiscontinuedVPR Loans 367,500,000 859,932 Floating Not Applicable Jul 17, 2012 AAA (sf)VPR Loans Class B 27,000,000 27,000,000 Floating Not Applicable Jul 12, 2012 Not Rated

Month Pool Balance Total Collections Net Loss RateDelinquency

Rate Reserve Ratio O/C RatioSep-2010 36,437,285 6,430,316 0.16% 0.23% 26.10% 30.79%Aug-2010 42,604,542 8,962,078 0.09% 0.29% 21.41% 25.21%Jul-2010 51,247,700 10,445,003 0.40% 0.17% 17.07% 20.10%Jun-2010 61,335,964 11,211,477 -0.40% 0.16% 13.81% 16.26%May-2010 72,079,866 11,995,371 0.26% 0.17% 11.47% 13.51%Apr-2010 83,569,982 12,743,376 0.40% 0.16% 9.71% 11.44%Mar-2010 95,743,917 15,535,804 0.15% 0.11% 8.36% 9.84%Feb-2010 110,491,801 12,191,136 0.31% 0.20% 7.15% 8.42%Jan-2010 122,042,250 12,839,404 -0.28% 0.20% 6.42% 7.56%Dec-2009 134,090,232 14,448,198 0.66% 0.19% 5.80% 6.83%Nov-2009 147,698,592 15,444,935 0.34% 0.13% 5.24% 6.17%Oct-2009 162,175,094 16,337,283 0.18% 0.20% 4.74% 5.58%

Month VPR LoansVPR Loans

Class BSep-2010 859,932 27,000,000Aug-2010 7,027,189 27,000,000Jul-2010 15,670,348 27,000,000Jun-2010 25,758,612 27,000,000May-2010 36,502,513 27,000,000Apr-2010 47,992,630 27,000,000Mar-2010 60,166,564 27,000,000Feb-2010 74,914,448 27,000,000Jan-2010 86,464,898 27,000,000Dec-2009 98,512,879 27,000,000Nov-2009 112,121,239 27,000,000Oct-2009 126,597,741 27,000,000

TD Securities Inc.Scotia Capital Inc.

11

Auto Loans

September 2010

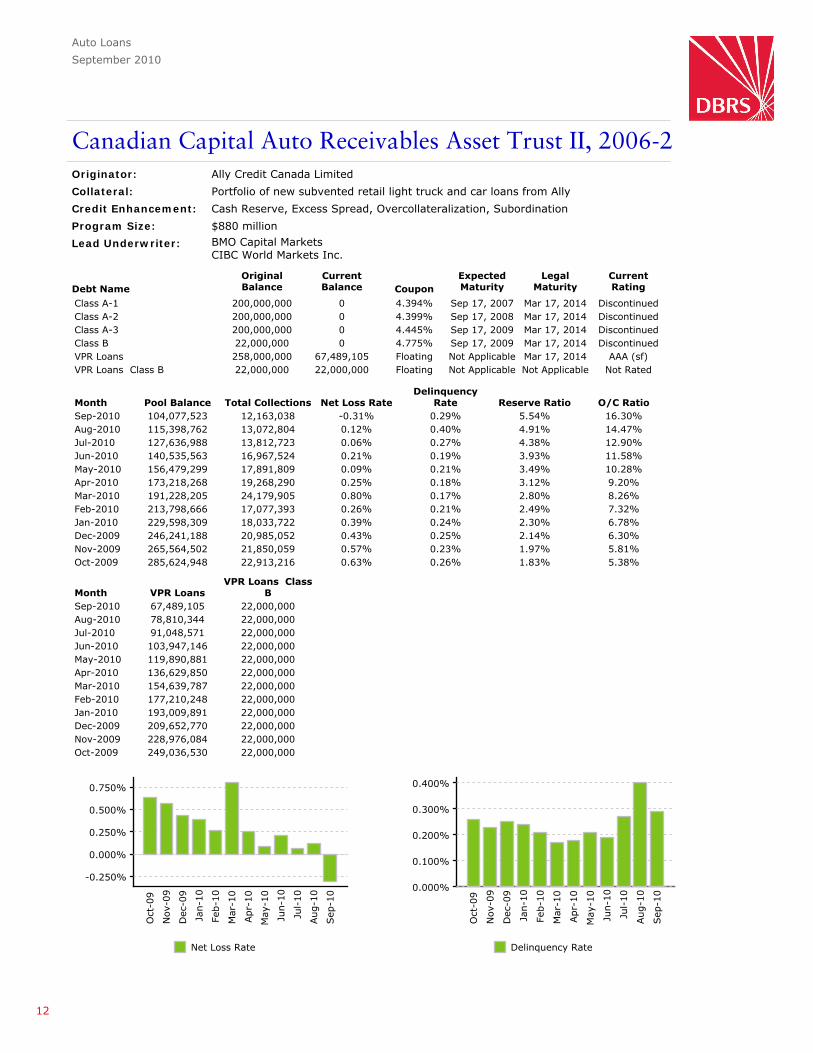

Canadian Capital Auto Receivables Asset Trust II, 2006-2Originator: Ally Credit Canada Limited

Collateral: Portfolio of new subvented retail light truck and car loans from Ally

Credit Enhancement: Cash Reserve, Excess Spread, Overcollateralization, Subordination

Program Size: $880 million

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Class A-1 200,000,000 0 4.394% Sep 17, 2007 Mar 17, 2014 DiscontinuedClass A-2 200,000,000 0 4.399% Sep 17, 2008 Mar 17, 2014 DiscontinuedClass A-3 200,000,000 0 4.445% Sep 17, 2009 Mar 17, 2014 DiscontinuedClass B 22,000,000 0 4.775% Sep 17, 2009 Mar 17, 2014 DiscontinuedVPR Loans 258,000,000 67,489,105 Floating Not Applicable Mar 17, 2014 AAA (sf)VPR Loans Class B 22,000,000 22,000,000 Floating Not Applicable Not Applicable Not Rated

Month Pool Balance Total Collections Net Loss RateDelinquency

Rate Reserve Ratio O/C RatioSep-2010 104,077,523 12,163,038 -0.31% 0.29% 5.54% 16.30%Aug-2010 115,398,762 13,072,804 0.12% 0.40% 4.91% 14.47%Jul-2010 127,636,988 13,812,723 0.06% 0.27% 4.38% 12.90%Jun-2010 140,535,563 16,967,524 0.21% 0.19% 3.93% 11.58%May-2010 156,479,299 17,891,809 0.09% 0.21% 3.49% 10.28%Apr-2010 173,218,268 19,268,290 0.25% 0.18% 3.12% 9.20%Mar-2010 191,228,205 24,179,905 0.80% 0.17% 2.80% 8.26%Feb-2010 213,798,666 17,077,393 0.26% 0.21% 2.49% 7.32%Jan-2010 229,598,309 18,033,722 0.39% 0.24% 2.30% 6.78%Dec-2009 246,241,188 20,985,052 0.43% 0.25% 2.14% 6.30%Nov-2009 265,564,502 21,850,059 0.57% 0.23% 1.97% 5.81%Oct-2009 285,624,948 22,913,216 0.63% 0.26% 1.83% 5.38%

Month VPR LoansVPR Loans Class

BSep-2010 67,489,105 22,000,000Aug-2010 78,810,344 22,000,000Jul-2010 91,048,571 22,000,000Jun-2010 103,947,146 22,000,000May-2010 119,890,881 22,000,000Apr-2010 136,629,850 22,000,000Mar-2010 154,639,787 22,000,000Feb-2010 177,210,248 22,000,000Jan-2010 193,009,891 22,000,000Dec-2009 209,652,770 22,000,000Nov-2009 228,976,084 22,000,000Oct-2009 249,036,530 22,000,000

BMO Capital MarketsCIBC World Markets Inc.

12

Auto Loans

September 2010

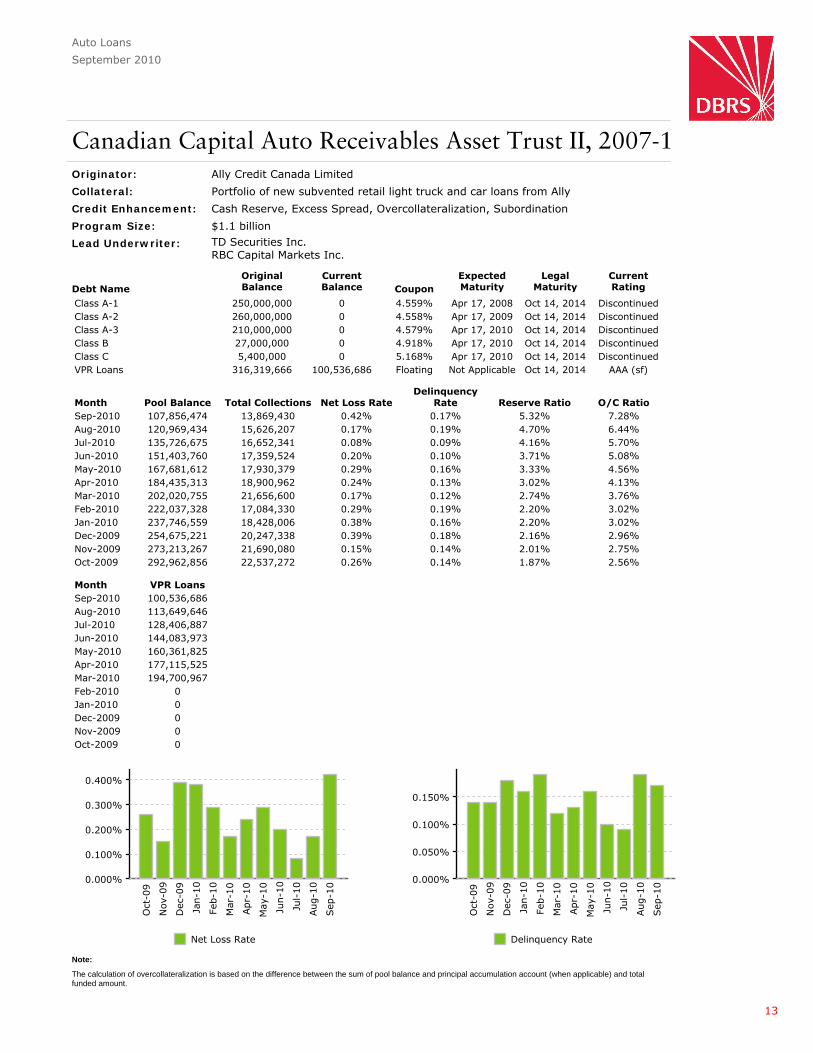

Canadian Capital Auto Receivables Asset Trust II, 2007-1Originator: Ally Credit Canada Limited

Collateral: Portfolio of new subvented retail light truck and car loans from Ally

Credit Enhancement: Cash Reserve, Excess Spread, Overcollateralization, Subordination

Program Size: $1.1 billion

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Class A-1 250,000,000 0 4.559% Apr 17, 2008 Oct 14, 2014 DiscontinuedClass A-2 260,000,000 0 4.558% Apr 17, 2009 Oct 14, 2014 DiscontinuedClass A-3 210,000,000 0 4.579% Apr 17, 2010 Oct 14, 2014 DiscontinuedClass B 27,000,000 0 4.918% Apr 17, 2010 Oct 14, 2014 DiscontinuedClass C 5,400,000 0 5.168% Apr 17, 2010 Oct 14, 2014 DiscontinuedVPR Loans 316,319,666 100,536,686 Floating Not Applicable Oct 14, 2014 AAA (sf)

Month Pool Balance Total Collections Net Loss RateDelinquency

Rate Reserve Ratio O/C RatioSep-2010 107,856,474 13,869,430 0.42% 0.17% 5.32% 7.28%Aug-2010 120,969,434 15,626,207 0.17% 0.19% 4.70% 6.44%Jul-2010 135,726,675 16,652,341 0.08% 0.09% 4.16% 5.70%Jun-2010 151,403,760 17,359,524 0.20% 0.10% 3.71% 5.08%May-2010 167,681,612 17,930,379 0.29% 0.16% 3.33% 4.56%Apr-2010 184,435,313 18,900,962 0.24% 0.13% 3.02% 4.13%Mar-2010 202,020,755 21,656,600 0.17% 0.12% 2.74% 3.76%Feb-2010 222,037,328 17,084,330 0.29% 0.19% 2.20% 3.02%Jan-2010 237,746,559 18,428,006 0.38% 0.16% 2.20% 3.02%Dec-2009 254,675,221 20,247,338 0.39% 0.18% 2.16% 2.96%Nov-2009 273,213,267 21,690,080 0.15% 0.14% 2.01% 2.75%Oct-2009 292,962,856 22,537,272 0.26% 0.14% 1.87% 2.56%

Month VPR LoansSep-2010 100,536,686Aug-2010 113,649,646Jul-2010 128,406,887Jun-2010 144,083,973May-2010 160,361,825Apr-2010 177,115,525Mar-2010 194,700,967Feb-2010 0Jan-2010 0Dec-2009 0Nov-2009 0Oct-2009 0

TD Securities Inc.RBC Capital Markets Inc.

The calculation of overcollateralization is based on the difference between the sum of pool balance and principal accumulation account (when applicable) and totalfunded amount.

Note:

13

Auto Loans

September 2010

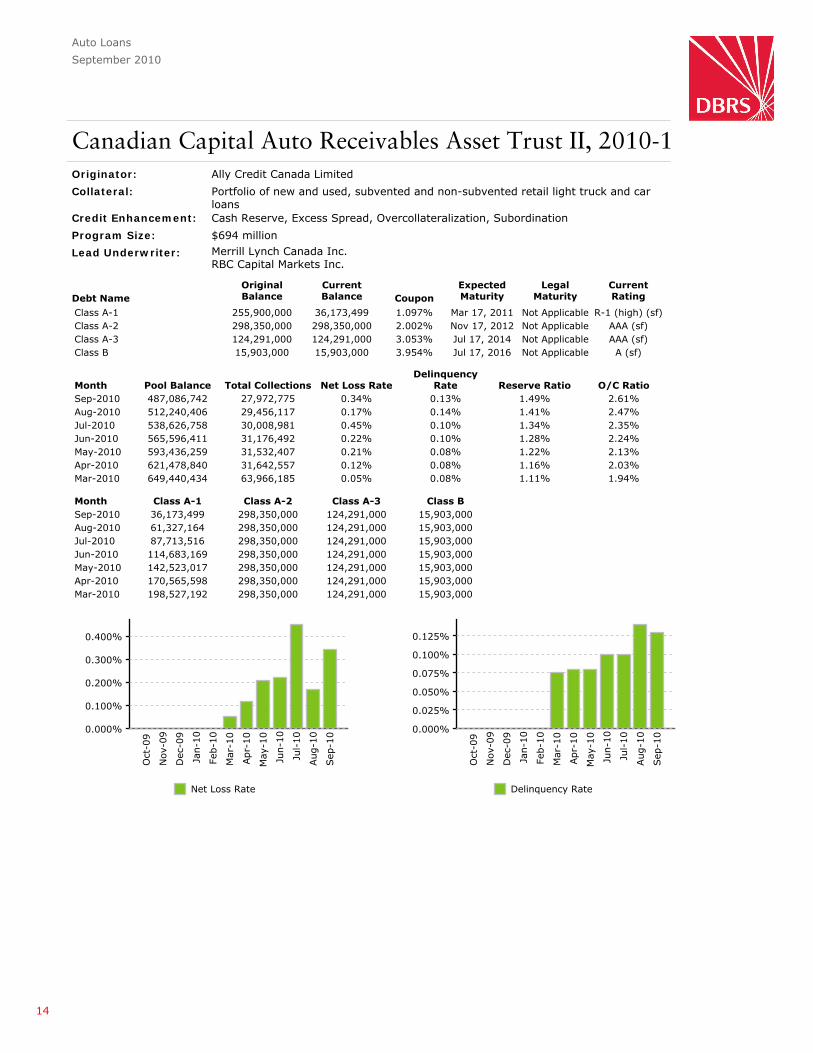

Canadian Capital Auto Receivables Asset Trust II, 2010-1Originator: Ally Credit Canada Limited

Collateral: Portfolio of new and used, subvented and non-subvented retail light truck and carloans

Credit Enhancement: Cash Reserve, Excess Spread, Overcollateralization, Subordination

Program Size: $694 million

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Class A-1 255,900,000 36,173,499 1.097% Mar 17, 2011 Not Applicable R-1 (high) (sf)Class A-2 298,350,000 298,350,000 2.002% Nov 17, 2012 Not Applicable AAA (sf)Class A-3 124,291,000 124,291,000 3.053% Jul 17, 2014 Not Applicable AAA (sf)Class B 15,903,000 15,903,000 3.954% Jul 17, 2016 Not Applicable A (sf)

Month Pool Balance Total Collections Net Loss RateDelinquency

Rate Reserve Ratio O/C RatioSep-2010 487,086,742 27,972,775 0.34% 0.13% 1.49% 2.61%Aug-2010 512,240,406 29,456,117 0.17% 0.14% 1.41% 2.47%Jul-2010 538,626,758 30,008,981 0.45% 0.10% 1.34% 2.35%Jun-2010 565,596,411 31,176,492 0.22% 0.10% 1.28% 2.24%May-2010 593,436,259 31,532,407 0.21% 0.08% 1.22% 2.13%Apr-2010 621,478,840 31,642,557 0.12% 0.08% 1.16% 2.03%Mar-2010 649,440,434 63,966,185 0.05% 0.08% 1.11% 1.94%

Month Class A-1 Class A-2 Class A-3 Class BSep-2010 36,173,499 298,350,000 124,291,000 15,903,000Aug-2010 61,327,164 298,350,000 124,291,000 15,903,000Jul-2010 87,713,516 298,350,000 124,291,000 15,903,000Jun-2010 114,683,169 298,350,000 124,291,000 15,903,000May-2010 142,523,017 298,350,000 124,291,000 15,903,000Apr-2010 170,565,598 298,350,000 124,291,000 15,903,000Mar-2010 198,527,192 298,350,000 124,291,000 15,903,000

Merrill Lynch Canada Inc.RBC Capital Markets Inc.

14

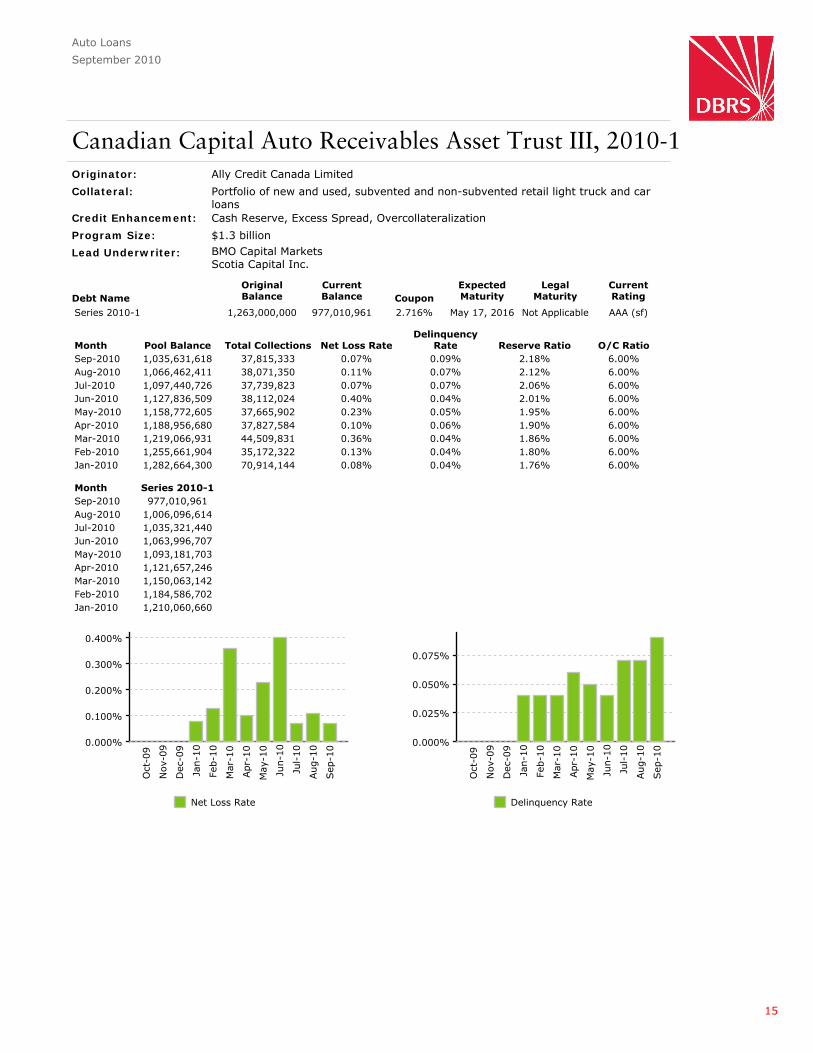

Auto Loans

September 2010

Canadian Capital Auto Receivables Asset Trust III, 2010-1Originator: Ally Credit Canada Limited

Collateral: Portfolio of new and used, subvented and non-subvented retail light truck and carloans

Credit Enhancement: Cash Reserve, Excess Spread, Overcollateralization

Program Size: $1.3 billion

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Series 2010-1 1,263,000,000 977,010,961 2.716% May 17, 2016 Not Applicable AAA (sf)

Month Pool Balance Total Collections Net Loss RateDelinquency

Rate Reserve Ratio O/C RatioSep-2010 1,035,631,618 37,815,333 0.07% 0.09% 2.18% 6.00%Aug-2010 1,066,462,411 38,071,350 0.11% 0.07% 2.12% 6.00%Jul-2010 1,097,440,726 37,739,823 0.07% 0.07% 2.06% 6.00%Jun-2010 1,127,836,509 38,112,024 0.40% 0.04% 2.01% 6.00%May-2010 1,158,772,605 37,665,902 0.23% 0.05% 1.95% 6.00%Apr-2010 1,188,956,680 37,827,584 0.10% 0.06% 1.90% 6.00%Mar-2010 1,219,066,931 44,509,831 0.36% 0.04% 1.86% 6.00%Feb-2010 1,255,661,904 35,172,322 0.13% 0.04% 1.80% 6.00%Jan-2010 1,282,664,300 70,914,144 0.08% 0.04% 1.76% 6.00%

Month Series 2010-1Sep-2010 977,010,961Aug-2010 1,006,096,614Jul-2010 1,035,321,440Jun-2010 1,063,996,707May-2010 1,093,181,703Apr-2010 1,121,657,246Mar-2010 1,150,063,142Feb-2010 1,184,586,702Jan-2010 1,210,060,660

BMO Capital MarketsScotia Capital Inc.

15

Auto Loans

September 2010

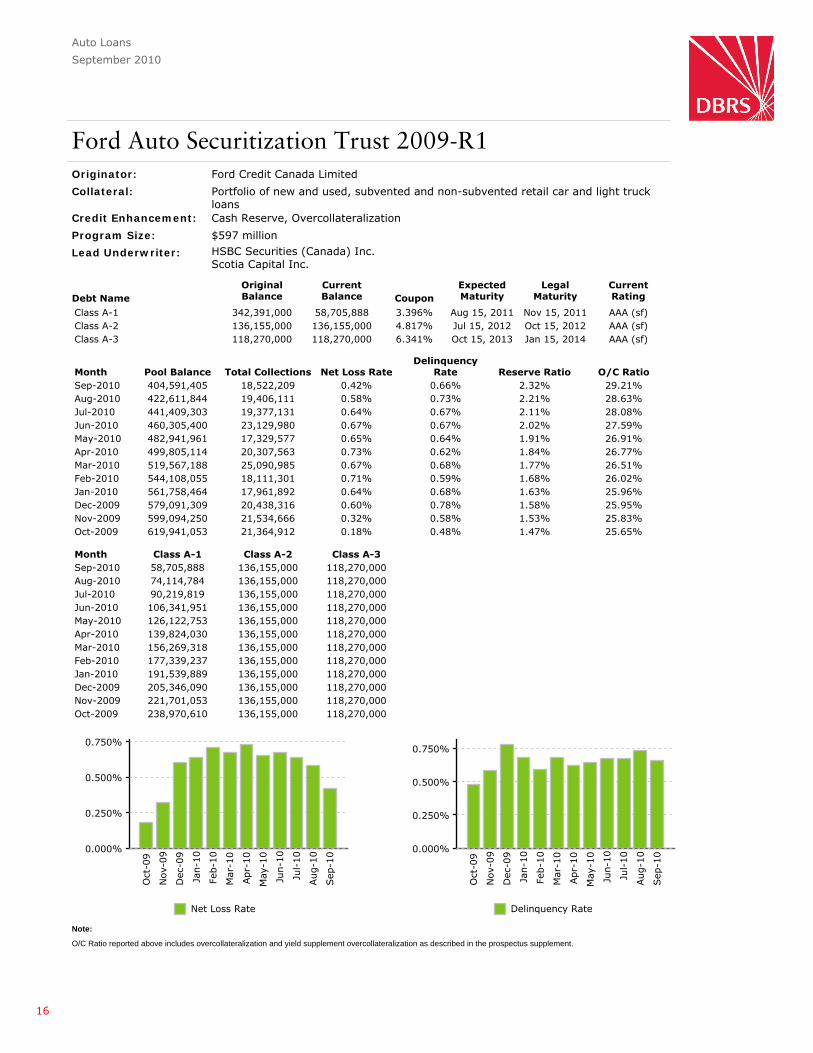

Ford Auto Securitization Trust 2009-R1Originator: Ford Credit Canada Limited

Collateral: Portfolio of new and used, subvented and non-subvented retail car and light truckloans

Credit Enhancement: Cash Reserve, Overcollateralization

Program Size: $597 million

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Class A-1 342,391,000 58,705,888 3.396% Aug 15, 2011 Nov 15, 2011 AAA (sf)Class A-2 136,155,000 136,155,000 4.817% Jul 15, 2012 Oct 15, 2012 AAA (sf)Class A-3 118,270,000 118,270,000 6.341% Oct 15, 2013 Jan 15, 2014 AAA (sf)

Month Pool Balance Total Collections Net Loss RateDelinquency

Rate Reserve Ratio O/C RatioSep-2010 404,591,405 18,522,209 0.42% 0.66% 2.32% 29.21%Aug-2010 422,611,844 19,406,111 0.58% 0.73% 2.21% 28.63%Jul-2010 441,409,303 19,377,131 0.64% 0.67% 2.11% 28.08%Jun-2010 460,305,400 23,129,980 0.67% 0.67% 2.02% 27.59%May-2010 482,941,961 17,329,577 0.65% 0.64% 1.91% 26.91%Apr-2010 499,805,114 20,307,563 0.73% 0.62% 1.84% 26.77%Mar-2010 519,567,188 25,090,985 0.67% 0.68% 1.77% 26.51%Feb-2010 544,108,055 18,111,301 0.71% 0.59% 1.68% 26.02%Jan-2010 561,758,464 17,961,892 0.64% 0.68% 1.63% 25.96%Dec-2009 579,091,309 20,438,316 0.60% 0.78% 1.58% 25.95%Nov-2009 599,094,250 21,534,666 0.32% 0.58% 1.53% 25.83%Oct-2009 619,941,053 21,364,912 0.18% 0.48% 1.47% 25.65%

Month Class A-1 Class A-2 Class A-3Sep-2010 58,705,888 136,155,000 118,270,000Aug-2010 74,114,784 136,155,000 118,270,000Jul-2010 90,219,819 136,155,000 118,270,000Jun-2010 106,341,951 136,155,000 118,270,000May-2010 126,122,753 136,155,000 118,270,000Apr-2010 139,824,030 136,155,000 118,270,000Mar-2010 156,269,318 136,155,000 118,270,000Feb-2010 177,339,237 136,155,000 118,270,000Jan-2010 191,539,889 136,155,000 118,270,000Dec-2009 205,346,090 136,155,000 118,270,000Nov-2009 221,701,053 136,155,000 118,270,000Oct-2009 238,970,610 136,155,000 118,270,000

HSBC Securities (Canada) Inc.Scotia Capital Inc.

O/C Ratio reported above includes overcollateralization and yield supplement overcollateralization as described in the prospectus supplement.

Note:

16

Auto Loans

September 2010

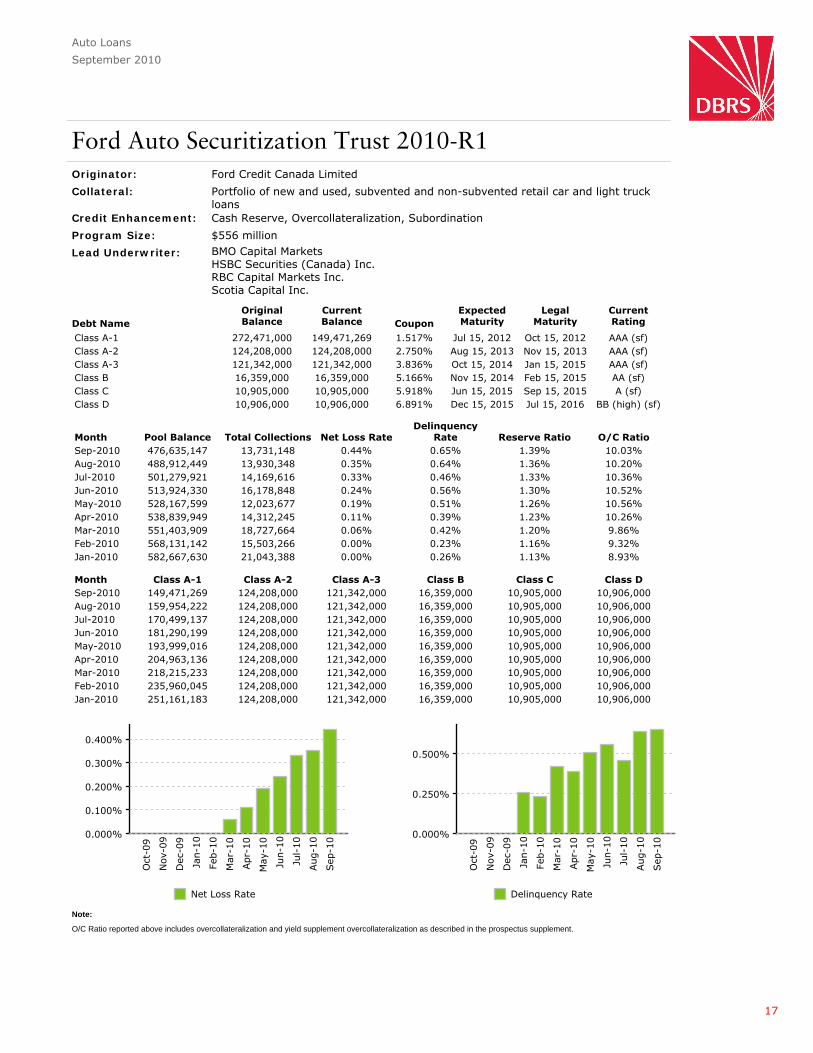

Ford Auto Securitization Trust 2010-R1Originator: Ford Credit Canada Limited

Collateral: Portfolio of new and used, subvented and non-subvented retail car and light truckloans

Credit Enhancement: Cash Reserve, Overcollateralization, Subordination

Program Size: $556 million

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Class A-1 272,471,000 149,471,269 1.517% Jul 15, 2012 Oct 15, 2012 AAA (sf)Class A-2 124,208,000 124,208,000 2.750% Aug 15, 2013 Nov 15, 2013 AAA (sf)Class A-3 121,342,000 121,342,000 3.836% Oct 15, 2014 Jan 15, 2015 AAA (sf)Class B 16,359,000 16,359,000 5.166% Nov 15, 2014 Feb 15, 2015 AA (sf)Class C 10,905,000 10,905,000 5.918% Jun 15, 2015 Sep 15, 2015 A (sf)Class D 10,906,000 10,906,000 6.891% Dec 15, 2015 Jul 15, 2016 BB (high) (sf)

Month Pool Balance Total Collections Net Loss RateDelinquency

Rate Reserve Ratio O/C RatioSep-2010 476,635,147 13,731,148 0.44% 0.65% 1.39% 10.03%Aug-2010 488,912,449 13,930,348 0.35% 0.64% 1.36% 10.20%Jul-2010 501,279,921 14,169,616 0.33% 0.46% 1.33% 10.36%Jun-2010 513,924,330 16,178,848 0.24% 0.56% 1.30% 10.52%May-2010 528,167,599 12,023,677 0.19% 0.51% 1.26% 10.56%Apr-2010 538,839,949 14,312,245 0.11% 0.39% 1.23% 10.26%Mar-2010 551,403,909 18,727,664 0.06% 0.42% 1.20% 9.86%Feb-2010 568,131,142 15,503,266 0.00% 0.23% 1.16% 9.32%Jan-2010 582,667,630 21,043,388 0.00% 0.26% 1.13% 8.93%

Month Class A-1 Class A-2 Class A-3 Class B Class C Class DSep-2010 149,471,269 124,208,000 121,342,000 16,359,000 10,905,000 10,906,000Aug-2010 159,954,222 124,208,000 121,342,000 16,359,000 10,905,000 10,906,000Jul-2010 170,499,137 124,208,000 121,342,000 16,359,000 10,905,000 10,906,000Jun-2010 181,290,199 124,208,000 121,342,000 16,359,000 10,905,000 10,906,000May-2010 193,999,016 124,208,000 121,342,000 16,359,000 10,905,000 10,906,000Apr-2010 204,963,136 124,208,000 121,342,000 16,359,000 10,905,000 10,906,000Mar-2010 218,215,233 124,208,000 121,342,000 16,359,000 10,905,000 10,906,000Feb-2010 235,960,045 124,208,000 121,342,000 16,359,000 10,905,000 10,906,000Jan-2010 251,161,183 124,208,000 121,342,000 16,359,000 10,905,000 10,906,000

BMO Capital MarketsHSBC Securities (Canada) Inc.RBC Capital Markets Inc.Scotia Capital Inc.

O/C Ratio reported above includes overcollateralization and yield supplement overcollateralization as described in the prospectus supplement.

Note:

17

Auto Loans

September 2010

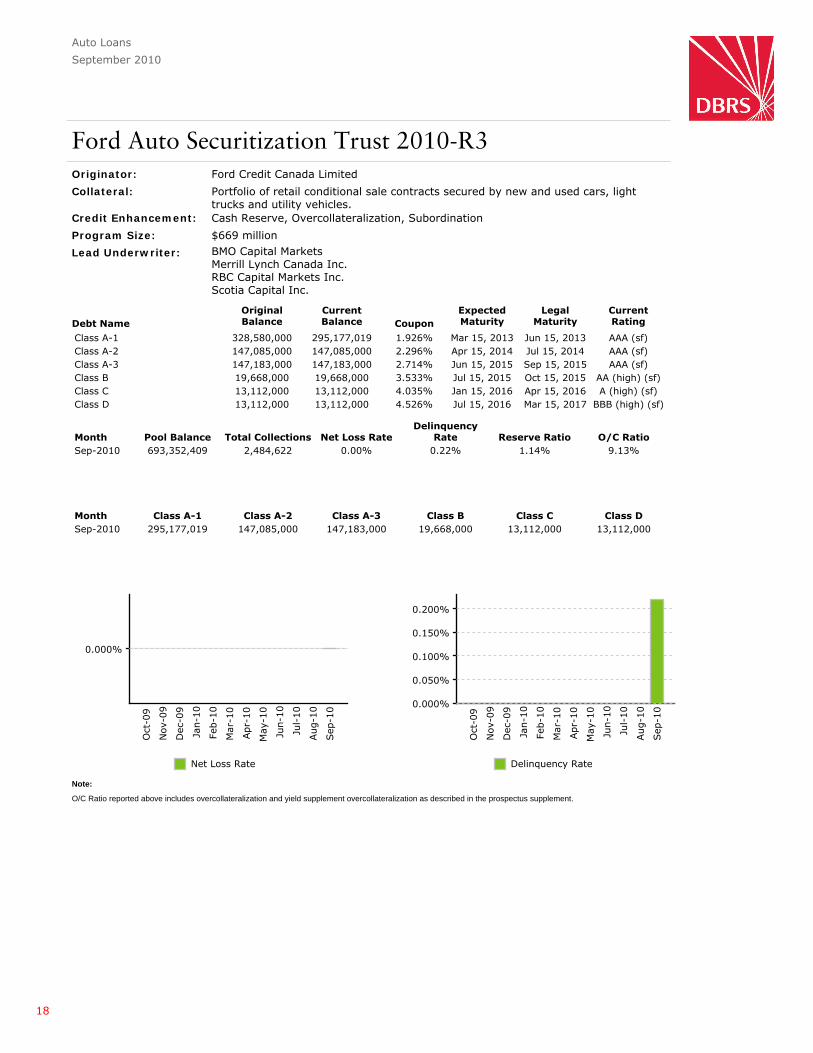

Ford Auto Securitization Trust 2010-R3Originator: Ford Credit Canada Limited

Collateral: Portfolio of retail conditional sale contracts secured by new and used cars, lighttrucks and utility vehicles.

Credit Enhancement: Cash Reserve, Overcollateralization, Subordination

Program Size: $669 million

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Class A-1 328,580,000 295,177,019 1.926% Mar 15, 2013 Jun 15, 2013 AAA (sf)Class A-2 147,085,000 147,085,000 2.296% Apr 15, 2014 Jul 15, 2014 AAA (sf)Class A-3 147,183,000 147,183,000 2.714% Jun 15, 2015 Sep 15, 2015 AAA (sf)Class B 19,668,000 19,668,000 3.533% Jul 15, 2015 Oct 15, 2015 AA (high) (sf)Class C 13,112,000 13,112,000 4.035% Jan 15, 2016 Apr 15, 2016 A (high) (sf)Class D 13,112,000 13,112,000 4.526% Jul 15, 2016 Mar 15, 2017 BBB (high) (sf)

Month Pool Balance Total Collections Net Loss RateDelinquency

Rate Reserve Ratio O/C RatioSep-2010 693,352,409 2,484,622 0.00% 0.22% 1.14% 9.13%

Month Class A-1 Class A-2 Class A-3 Class B Class C Class DSep-2010 295,177,019 147,085,000 147,183,000 19,668,000 13,112,000 13,112,000

BMO Capital MarketsMerrill Lynch Canada Inc.RBC Capital Markets Inc.Scotia Capital Inc.

O/C Ratio reported above includes overcollateralization and yield supplement overcollateralization as described in the prospectus supplement.

Note:

18

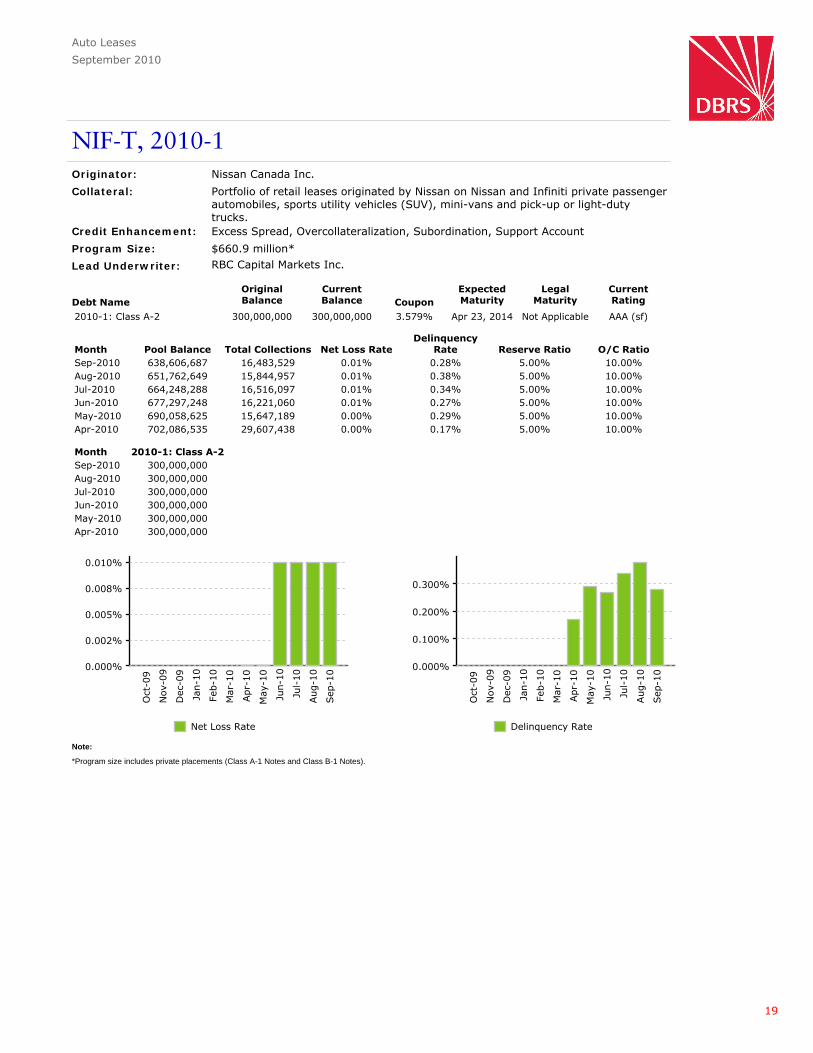

Auto Leases

September 2010

NIF-T, 2010-1Originator: Nissan Canada Inc.

Collateral: Portfolio of retail leases originated by Nissan on Nissan and Infiniti private passengerautomobiles, sports utility vehicles (SUV), mini-vans and pick-up or light-dutytrucks.

Credit Enhancement: Excess Spread, Overcollateralization, Subordination, Support Account

Program Size: $660.9 million*

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

2010-1: Class A-2 300,000,000 300,000,000 3.579% Apr 23, 2014 Not Applicable AAA (sf)

Month Pool Balance Total Collections Net Loss RateDelinquency

Rate Reserve Ratio O/C RatioSep-2010 638,606,687 16,483,529 0.01% 0.28% 5.00% 10.00%Aug-2010 651,762,649 15,844,957 0.01% 0.38% 5.00% 10.00%Jul-2010 664,248,288 16,516,097 0.01% 0.34% 5.00% 10.00%Jun-2010 677,297,248 16,221,060 0.01% 0.27% 5.00% 10.00%May-2010 690,058,625 15,647,189 0.00% 0.29% 5.00% 10.00%Apr-2010 702,086,535 29,607,438 0.00% 0.17% 5.00% 10.00%

Month 2010-1: Class A-2Sep-2010 300,000,000Aug-2010 300,000,000Jul-2010 300,000,000Jun-2010 300,000,000May-2010 300,000,000Apr-2010 300,000,000

RBC Capital Markets Inc.

*Program size includes private placements (Class A-1 Notes and Class B-1 Notes).

Note:

19

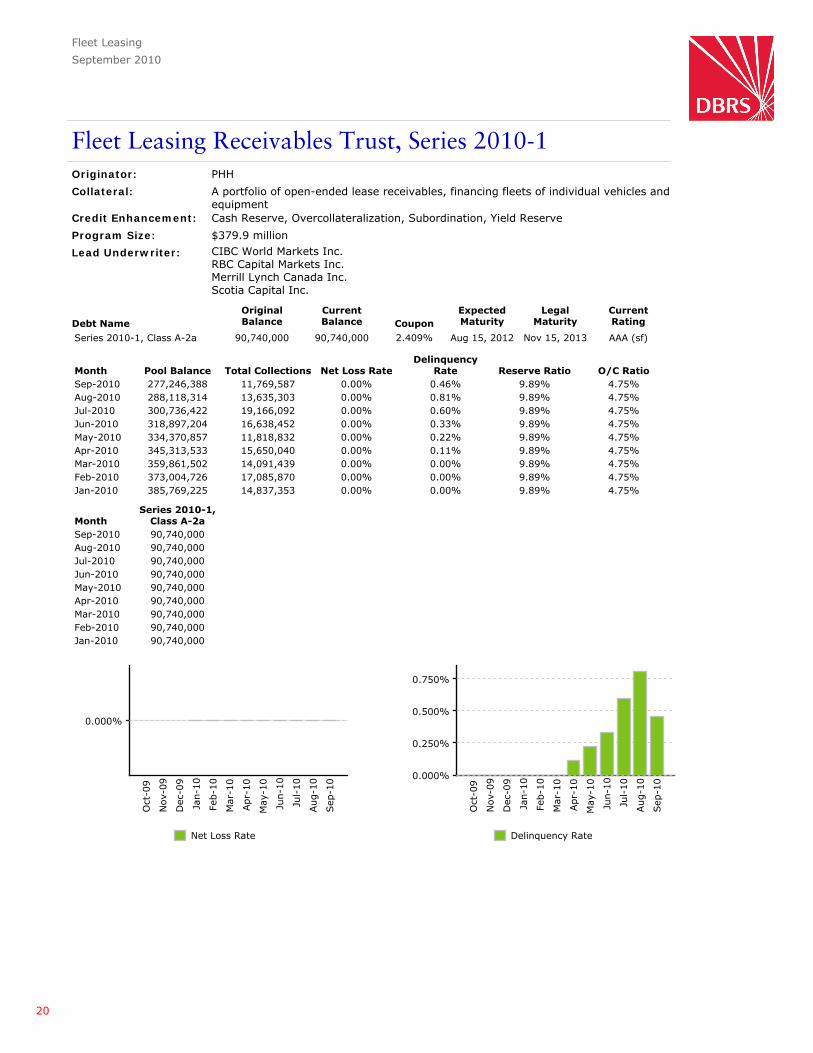

Fleet Leasing

September 2010

Fleet Leasing Receivables Trust, Series 2010-1Originator: PHH

Collateral: A portfolio of open-ended lease receivables, financing fleets of individual vehicles andequipment

Credit Enhancement: Cash Reserve, Overcollateralization, Subordination, Yield Reserve

Program Size: $379.9 million

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Series 2010-1, Class A-2a 90,740,000 90,740,000 2.409% Aug 15, 2012 Nov 15, 2013 AAA (sf)

Month Pool Balance Total Collections Net Loss RateDelinquency

Rate Reserve Ratio O/C RatioSep-2010 277,246,388 11,769,587 0.00% 0.46% 9.89% 4.75%Aug-2010 288,118,314 13,635,303 0.00% 0.81% 9.89% 4.75%Jul-2010 300,736,422 19,166,092 0.00% 0.60% 9.89% 4.75%Jun-2010 318,897,204 16,638,452 0.00% 0.33% 9.89% 4.75%May-2010 334,370,857 11,818,832 0.00% 0.22% 9.89% 4.75%Apr-2010 345,313,533 15,650,040 0.00% 0.11% 9.89% 4.75%Mar-2010 359,861,502 14,091,439 0.00% 0.00% 9.89% 4.75%Feb-2010 373,004,726 17,085,870 0.00% 0.00% 9.89% 4.75%Jan-2010 385,769,225 14,837,353 0.00% 0.00% 9.89% 4.75%

MonthSeries 2010-1,

Class A-2aSep-2010 90,740,000Aug-2010 90,740,000Jul-2010 90,740,000Jun-2010 90,740,000May-2010 90,740,000Apr-2010 90,740,000Mar-2010 90,740,000Feb-2010 90,740,000Jan-2010 90,740,000

CIBC World Markets Inc.RBC Capital Markets Inc.Merrill Lynch Canada Inc.Scotia Capital Inc.

20

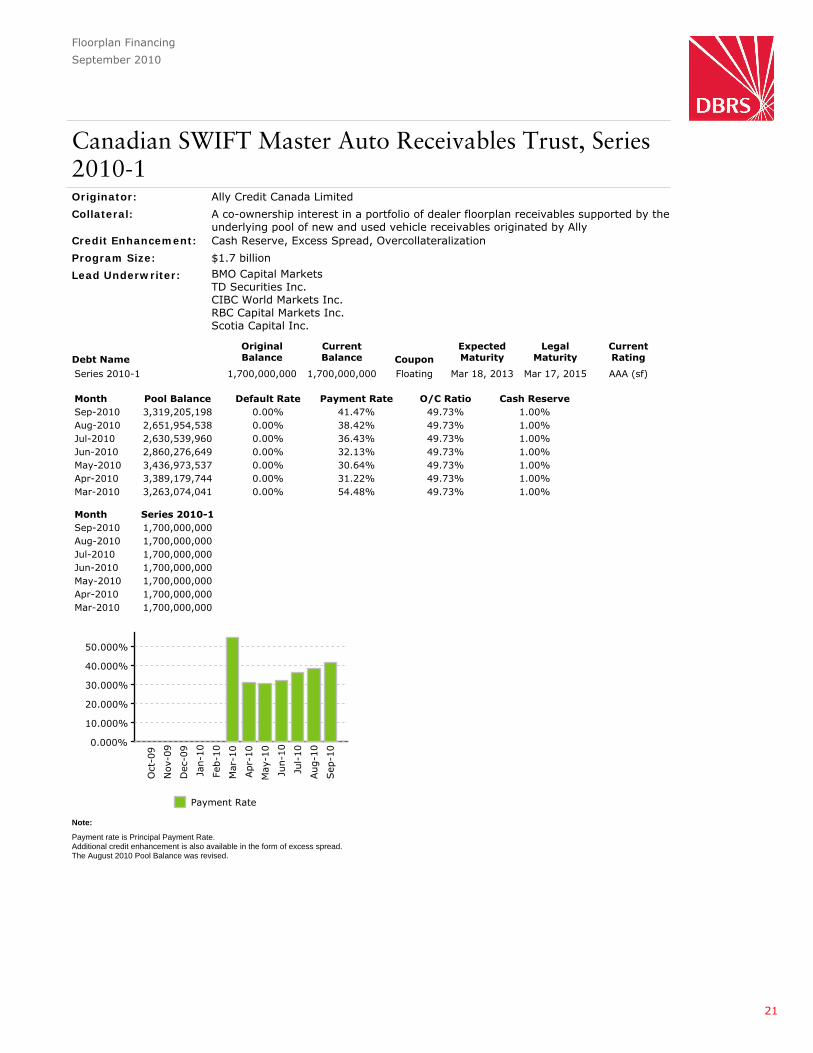

Floorplan Financing

September 2010

Canadian SWIFT Master Auto Receivables Trust, Series2010-1Originator: Ally Credit Canada Limited

Collateral: A co-ownership interest in a portfolio of dealer floorplan receivables supported by theunderlying pool of new and used vehicle receivables originated by Ally

Credit Enhancement: Cash Reserve, Excess Spread, Overcollateralization

Program Size: $1.7 billion

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Series 2010-1 1,700,000,000 1,700,000,000 Floating Mar 18, 2013 Mar 17, 2015 AAA (sf)

Month Pool Balance Default Rate Payment Rate O/C Ratio Cash ReserveSep-2010 3,319,205,198 0.00% 41.47% 49.73% 1.00%Aug-2010 2,651,954,538 0.00% 38.42% 49.73% 1.00%Jul-2010 2,630,539,960 0.00% 36.43% 49.73% 1.00%Jun-2010 2,860,276,649 0.00% 32.13% 49.73% 1.00%May-2010 3,436,973,537 0.00% 30.64% 49.73% 1.00%Apr-2010 3,389,179,744 0.00% 31.22% 49.73% 1.00%Mar-2010 3,263,074,041 0.00% 54.48% 49.73% 1.00%

Month Series 2010-1Sep-2010 1,700,000,000Aug-2010 1,700,000,000Jul-2010 1,700,000,000Jun-2010 1,700,000,000May-2010 1,700,000,000Apr-2010 1,700,000,000Mar-2010 1,700,000,000

BMO Capital MarketsTD Securities Inc.CIBC World Markets Inc.RBC Capital Markets Inc.Scotia Capital Inc.

Payment rate is Principal Payment Rate.Additional credit enhancement is also available in the form of excess spread.The August 2010 Pool Balance was revised.

Note:

21

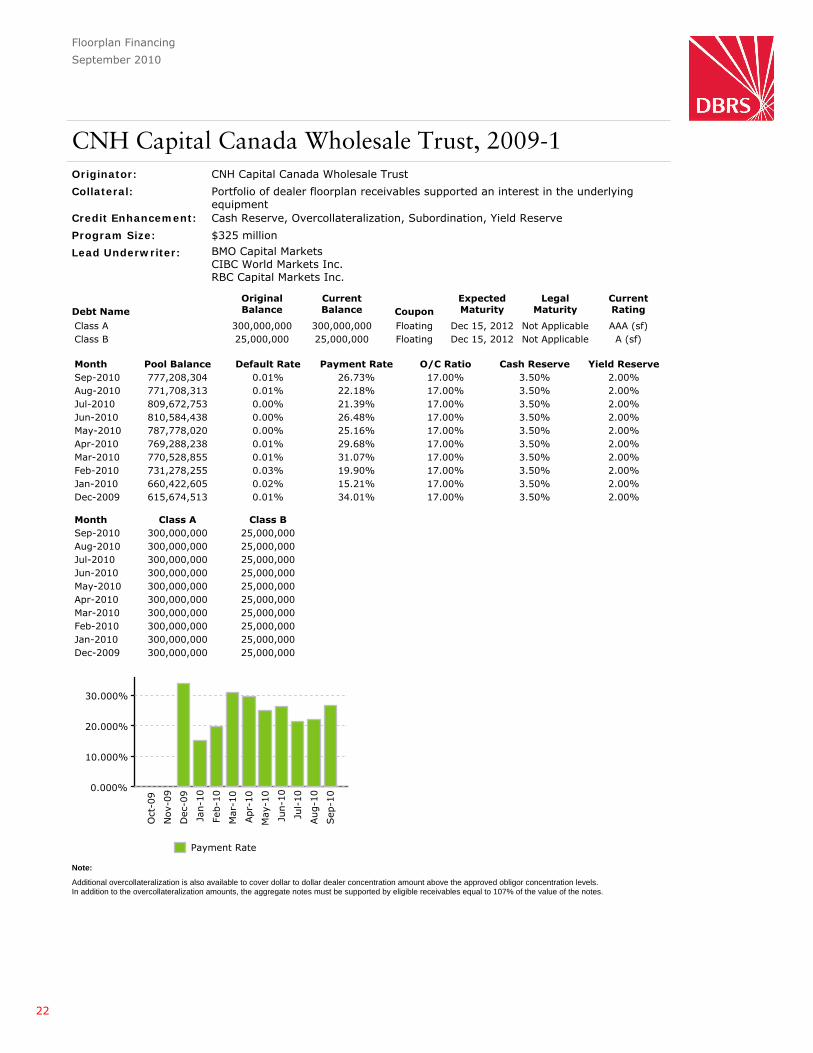

Floorplan Financing

September 2010

CNH Capital Canada Wholesale Trust, 2009-1Originator: CNH Capital Canada Wholesale Trust

Collateral: Portfolio of dealer floorplan receivables supported an interest in the underlyingequipment

Credit Enhancement: Cash Reserve, Overcollateralization, Subordination, Yield Reserve

Program Size: $325 million

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Class A 300,000,000 300,000,000 Floating Dec 15, 2012 Not Applicable AAA (sf)Class B 25,000,000 25,000,000 Floating Dec 15, 2012 Not Applicable A (sf)

Month Pool Balance Default Rate Payment Rate O/C Ratio Cash Reserve Yield ReserveSep-2010 777,208,304 0.01% 26.73% 17.00% 3.50% 2.00%Aug-2010 771,708,313 0.01% 22.18% 17.00% 3.50% 2.00%Jul-2010 809,672,753 0.00% 21.39% 17.00% 3.50% 2.00%Jun-2010 810,584,438 0.00% 26.48% 17.00% 3.50% 2.00%May-2010 787,778,020 0.00% 25.16% 17.00% 3.50% 2.00%Apr-2010 769,288,238 0.01% 29.68% 17.00% 3.50% 2.00%Mar-2010 770,528,855 0.01% 31.07% 17.00% 3.50% 2.00%Feb-2010 731,278,255 0.03% 19.90% 17.00% 3.50% 2.00%Jan-2010 660,422,605 0.02% 15.21% 17.00% 3.50% 2.00%Dec-2009 615,674,513 0.01% 34.01% 17.00% 3.50% 2.00%

Month Class A Class BSep-2010 300,000,000 25,000,000Aug-2010 300,000,000 25,000,000Jul-2010 300,000,000 25,000,000Jun-2010 300,000,000 25,000,000May-2010 300,000,000 25,000,000Apr-2010 300,000,000 25,000,000Mar-2010 300,000,000 25,000,000Feb-2010 300,000,000 25,000,000Jan-2010 300,000,000 25,000,000Dec-2009 300,000,000 25,000,000

BMO Capital MarketsCIBC World Markets Inc.RBC Capital Markets Inc.

Additional overcollateralization is also available to cover dollar to dollar dealer concentration amount above the approved obligor concentration levels.In addition to the overcollateralization amounts, the aggregate notes must be supported by eligible receivables equal to 107% of the value of the notes.

Note:

22

Floorplan Financing

September 2010

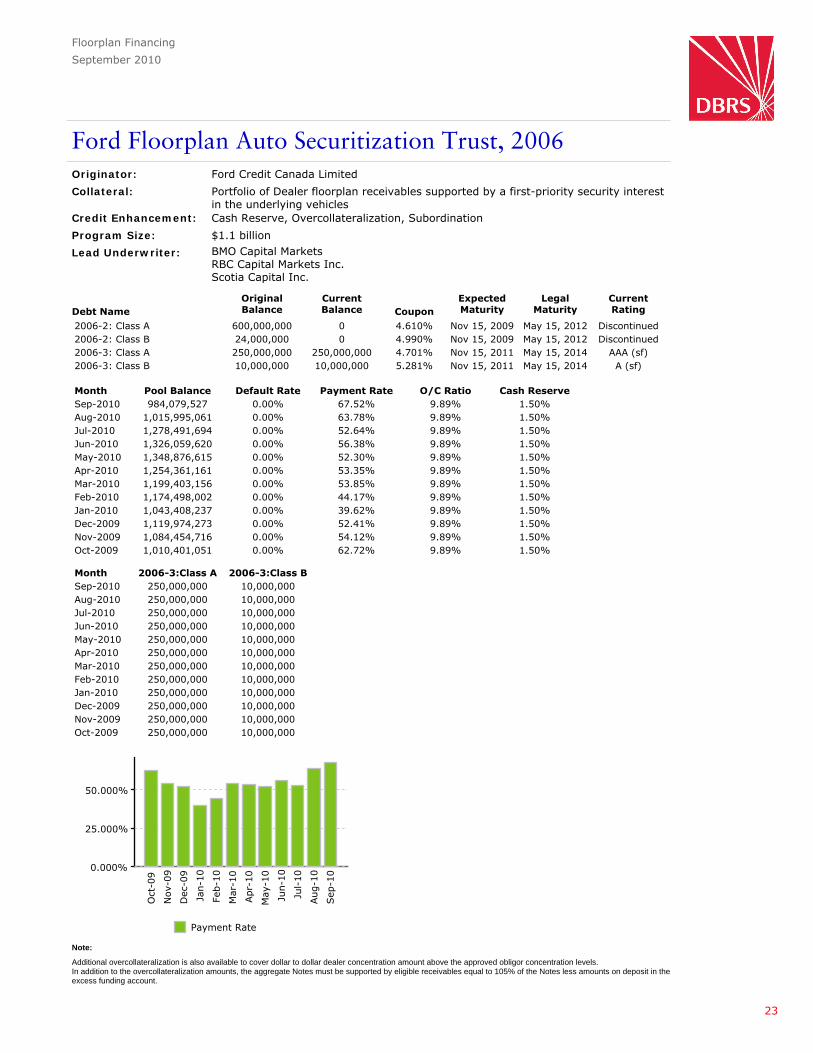

Ford Floorplan Auto Securitization Trust, 2006Originator: Ford Credit Canada Limited

Collateral: Portfolio of Dealer floorplan receivables supported by a first-priority security interestin the underlying vehicles

Credit Enhancement: Cash Reserve, Overcollateralization, Subordination

Program Size: $1.1 billion

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

2006-2: Class A 600,000,000 0 4.610% Nov 15, 2009 May 15, 2012 Discontinued2006-2: Class B 24,000,000 0 4.990% Nov 15, 2009 May 15, 2012 Discontinued2006-3: Class A 250,000,000 250,000,000 4.701% Nov 15, 2011 May 15, 2014 AAA (sf)2006-3: Class B 10,000,000 10,000,000 5.281% Nov 15, 2011 May 15, 2014 A (sf)

Month Pool Balance Default Rate Payment Rate O/C Ratio Cash ReserveSep-2010 984,079,527 0.00% 67.52% 9.89% 1.50%Aug-2010 1,015,995,061 0.00% 63.78% 9.89% 1.50%Jul-2010 1,278,491,694 0.00% 52.64% 9.89% 1.50%Jun-2010 1,326,059,620 0.00% 56.38% 9.89% 1.50%May-2010 1,348,876,615 0.00% 52.30% 9.89% 1.50%Apr-2010 1,254,361,161 0.00% 53.35% 9.89% 1.50%Mar-2010 1,199,403,156 0.00% 53.85% 9.89% 1.50%Feb-2010 1,174,498,002 0.00% 44.17% 9.89% 1.50%Jan-2010 1,043,408,237 0.00% 39.62% 9.89% 1.50%Dec-2009 1,119,974,273 0.00% 52.41% 9.89% 1.50%Nov-2009 1,084,454,716 0.00% 54.12% 9.89% 1.50%Oct-2009 1,010,401,051 0.00% 62.72% 9.89% 1.50%

Month 2006-3:Class A 2006-3:Class BSep-2010 250,000,000 10,000,000Aug-2010 250,000,000 10,000,000Jul-2010 250,000,000 10,000,000Jun-2010 250,000,000 10,000,000May-2010 250,000,000 10,000,000Apr-2010 250,000,000 10,000,000Mar-2010 250,000,000 10,000,000Feb-2010 250,000,000 10,000,000Jan-2010 250,000,000 10,000,000Dec-2009 250,000,000 10,000,000Nov-2009 250,000,000 10,000,000Oct-2009 250,000,000 10,000,000

BMO Capital MarketsRBC Capital Markets Inc.Scotia Capital Inc.

Additional overcollateralization is also available to cover dollar to dollar dealer concentration amount above the approved obligor concentration levels.In addition to the overcollateralization amounts, the aggregate Notes must be supported by eligible receivables equal to 105% of the Notes less amounts on deposit in theexcess funding account.

Note:

23

Floorplan Financing

September 2010

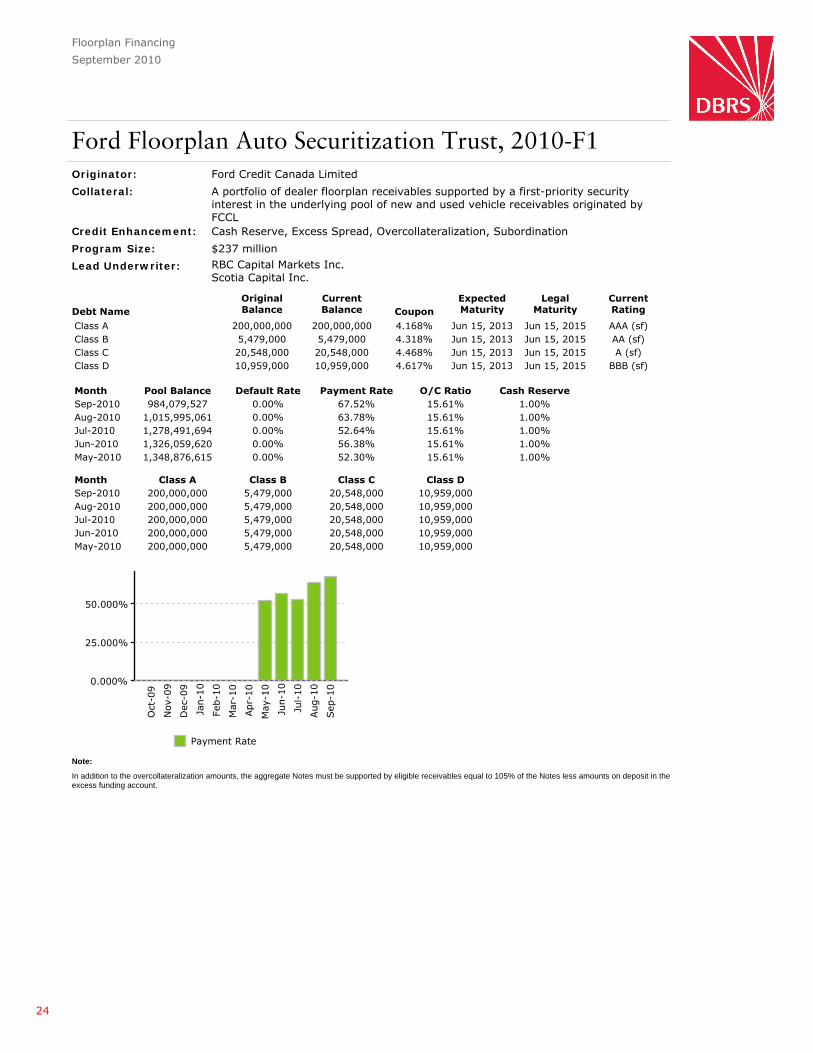

Ford Floorplan Auto Securitization Trust, 2010-F1Originator: Ford Credit Canada Limited

Collateral: A portfolio of dealer floorplan receivables supported by a first-priority securityinterest in the underlying pool of new and used vehicle receivables originated byFCCL

Credit Enhancement: Cash Reserve, Excess Spread, Overcollateralization, Subordination

Program Size: $237 million

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Class A 200,000,000 200,000,000 4.168% Jun 15, 2013 Jun 15, 2015 AAA (sf)Class B 5,479,000 5,479,000 4.318% Jun 15, 2013 Jun 15, 2015 AA (sf)Class C 20,548,000 20,548,000 4.468% Jun 15, 2013 Jun 15, 2015 A (sf)Class D 10,959,000 10,959,000 4.617% Jun 15, 2013 Jun 15, 2015 BBB (sf)

Month Pool Balance Default Rate Payment Rate O/C Ratio Cash ReserveSep-2010 984,079,527 0.00% 67.52% 15.61% 1.00%Aug-2010 1,015,995,061 0.00% 63.78% 15.61% 1.00%Jul-2010 1,278,491,694 0.00% 52.64% 15.61% 1.00%Jun-2010 1,326,059,620 0.00% 56.38% 15.61% 1.00%May-2010 1,348,876,615 0.00% 52.30% 15.61% 1.00%

Month Class A Class B Class C Class DSep-2010 200,000,000 5,479,000 20,548,000 10,959,000Aug-2010 200,000,000 5,479,000 20,548,000 10,959,000Jul-2010 200,000,000 5,479,000 20,548,000 10,959,000Jun-2010 200,000,000 5,479,000 20,548,000 10,959,000May-2010 200,000,000 5,479,000 20,548,000 10,959,000

RBC Capital Markets Inc.Scotia Capital Inc.

In addition to the overcollateralization amounts, the aggregate Notes must be supported by eligible receivables equal to 105% of the Notes less amounts on deposit in theexcess funding account.

Note:

24

Floorplan Financing

September 2010

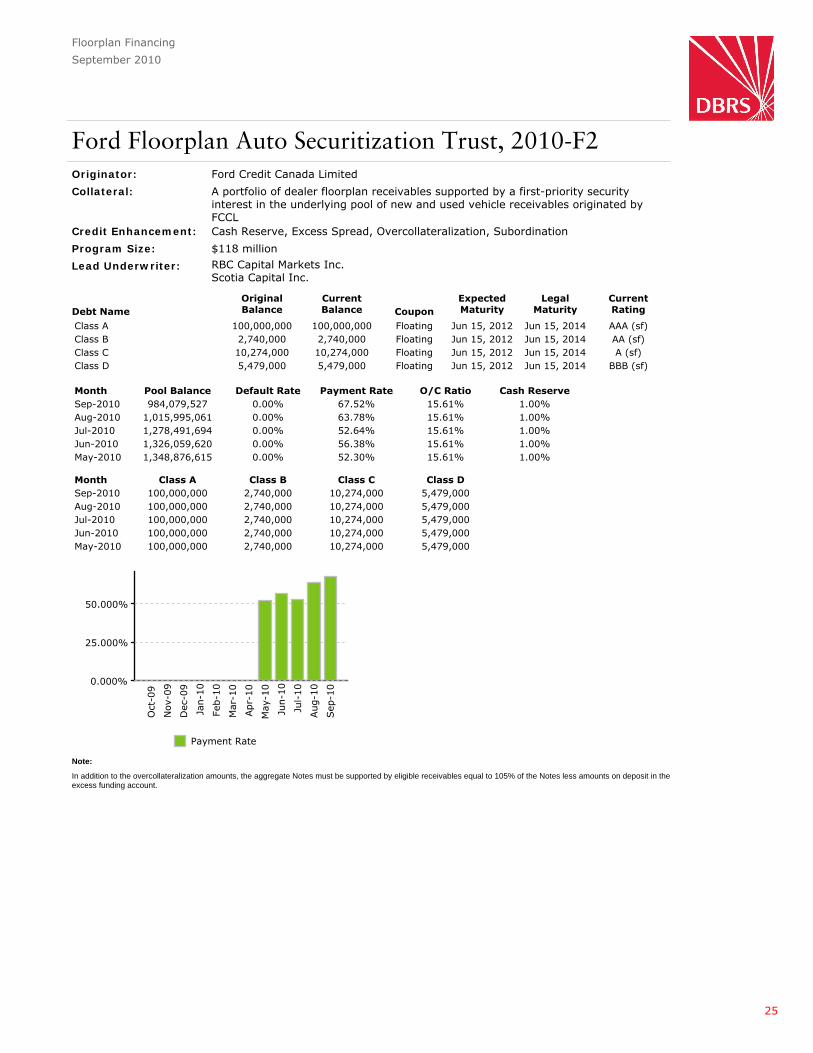

Ford Floorplan Auto Securitization Trust, 2010-F2Originator: Ford Credit Canada Limited

Collateral: A portfolio of dealer floorplan receivables supported by a first-priority securityinterest in the underlying pool of new and used vehicle receivables originated byFCCL

Credit Enhancement: Cash Reserve, Excess Spread, Overcollateralization, Subordination

Program Size: $118 million

Lead Underwriter:

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Class A 100,000,000 100,000,000 Floating Jun 15, 2012 Jun 15, 2014 AAA (sf)Class B 2,740,000 2,740,000 Floating Jun 15, 2012 Jun 15, 2014 AA (sf)Class C 10,274,000 10,274,000 Floating Jun 15, 2012 Jun 15, 2014 A (sf)Class D 5,479,000 5,479,000 Floating Jun 15, 2012 Jun 15, 2014 BBB (sf)

Month Pool Balance Default Rate Payment Rate O/C Ratio Cash ReserveSep-2010 984,079,527 0.00% 67.52% 15.61% 1.00%Aug-2010 1,015,995,061 0.00% 63.78% 15.61% 1.00%Jul-2010 1,278,491,694 0.00% 52.64% 15.61% 1.00%Jun-2010 1,326,059,620 0.00% 56.38% 15.61% 1.00%May-2010 1,348,876,615 0.00% 52.30% 15.61% 1.00%

Month Class A Class B Class C Class DSep-2010 100,000,000 2,740,000 10,274,000 5,479,000Aug-2010 100,000,000 2,740,000 10,274,000 5,479,000Jul-2010 100,000,000 2,740,000 10,274,000 5,479,000Jun-2010 100,000,000 2,740,000 10,274,000 5,479,000May-2010 100,000,000 2,740,000 10,274,000 5,479,000

RBC Capital Markets Inc.Scotia Capital Inc.

In addition to the overcollateralization amounts, the aggregate Notes must be supported by eligible receivables equal to 105% of the Notes less amounts on deposit in theexcess funding account.

Note:

25

Credit Cards

September 2010

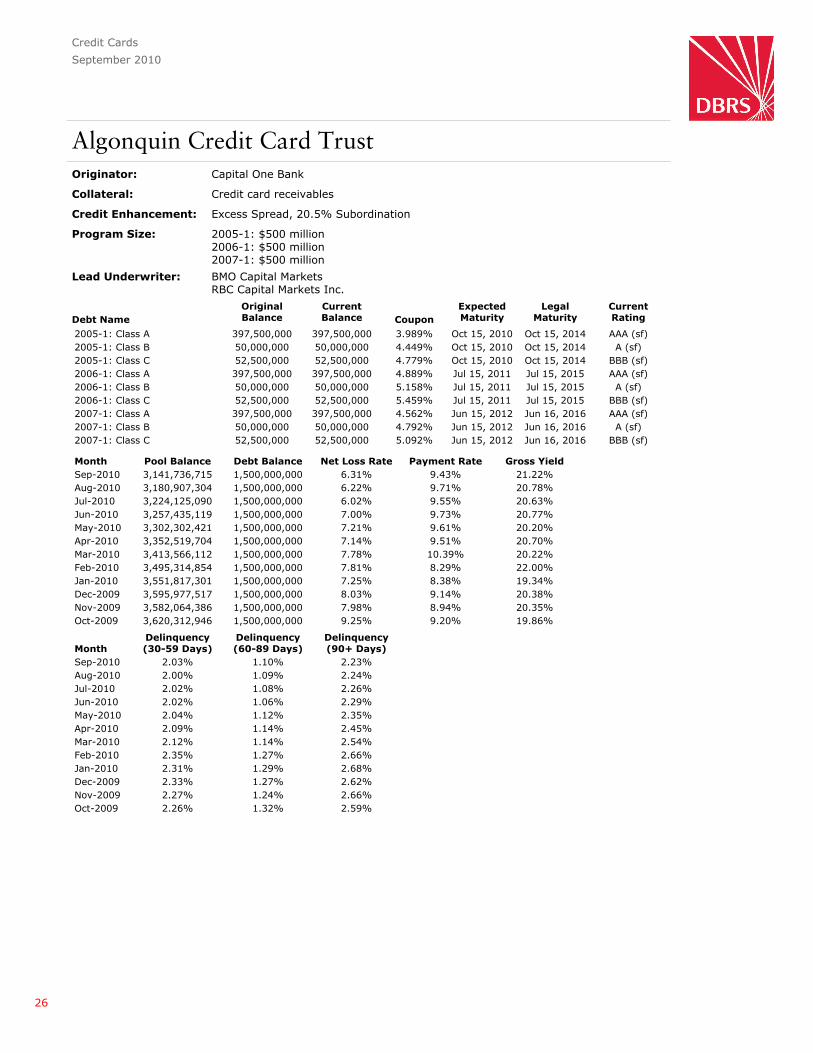

Algonquin Credit Card TrustOriginator: Capital One Bank

Collateral: Credit card receivables

Credit Enhancement: Excess Spread, 20.5% Subordination

Program Size: 2005-1: $500 million2006-1: $500 million2007-1: $500 million

Lead Underwriter: BMO Capital MarketsRBC Capital Markets Inc.

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

2005-1: Class A 397,500,000 397,500,000 3.989% Oct 15, 2010 Oct 15, 2014 AAA (sf)2005-1: Class B 50,000,000 50,000,000 4.449% Oct 15, 2010 Oct 15, 2014 A (sf)2005-1: Class C 52,500,000 52,500,000 4.779% Oct 15, 2010 Oct 15, 2014 BBB (sf)2006-1: Class A 397,500,000 397,500,000 4.889% Jul 15, 2011 Jul 15, 2015 AAA (sf)2006-1: Class B 50,000,000 50,000,000 5.158% Jul 15, 2011 Jul 15, 2015 A (sf)2006-1: Class C 52,500,000 52,500,000 5.459% Jul 15, 2011 Jul 15, 2015 BBB (sf)2007-1: Class A 397,500,000 397,500,000 4.562% Jun 15, 2012 Jun 16, 2016 AAA (sf)2007-1: Class B 50,000,000 50,000,000 4.792% Jun 15, 2012 Jun 16, 2016 A (sf)2007-1: Class C 52,500,000 52,500,000 5.092% Jun 15, 2012 Jun 16, 2016 BBB (sf)

Month Pool Balance Debt Balance Net Loss Rate Payment Rate Gross YieldSep-2010 3,141,736,715 1,500,000,000 6.31% 9.43% 21.22%Aug-2010 3,180,907,304 1,500,000,000 6.22% 9.71% 20.78%Jul-2010 3,224,125,090 1,500,000,000 6.02% 9.55% 20.63%Jun-2010 3,257,435,119 1,500,000,000 7.00% 9.73% 20.77%May-2010 3,302,302,421 1,500,000,000 7.21% 9.61% 20.20%Apr-2010 3,352,519,704 1,500,000,000 7.14% 9.51% 20.70%Mar-2010 3,413,566,112 1,500,000,000 7.78% 10.39% 20.22%Feb-2010 3,495,314,854 1,500,000,000 7.81% 8.29% 22.00%Jan-2010 3,551,817,301 1,500,000,000 7.25% 8.38% 19.34%Dec-2009 3,595,977,517 1,500,000,000 8.03% 9.14% 20.38%Nov-2009 3,582,064,386 1,500,000,000 7.98% 8.94% 20.35%Oct-2009 3,620,312,946 1,500,000,000 9.25% 9.20% 19.86%

MonthDelinquency(30-59 Days)

Delinquency(60-89 Days)

Delinquency(90+ Days)

Sep-2010 2.03% 1.10% 2.23%Aug-2010 2.00% 1.09% 2.24%Jul-2010 2.02% 1.08% 2.26%Jun-2010 2.02% 1.06% 2.29%May-2010 2.04% 1.12% 2.35%Apr-2010 2.09% 1.14% 2.45%Mar-2010 2.12% 1.14% 2.54%Feb-2010 2.35% 1.27% 2.66%Jan-2010 2.31% 1.29% 2.68%Dec-2009 2.33% 1.27% 2.62%Nov-2009 2.27% 1.24% 2.66%Oct-2009 2.26% 1.32% 2.59%

26

Credit Cards

September 2010

Algonquin Credit Card Trust (continued)

Payment rate is Principal Payment Rate.Credit enhancement indicates the credit support to AAA rated notes only.

Note:

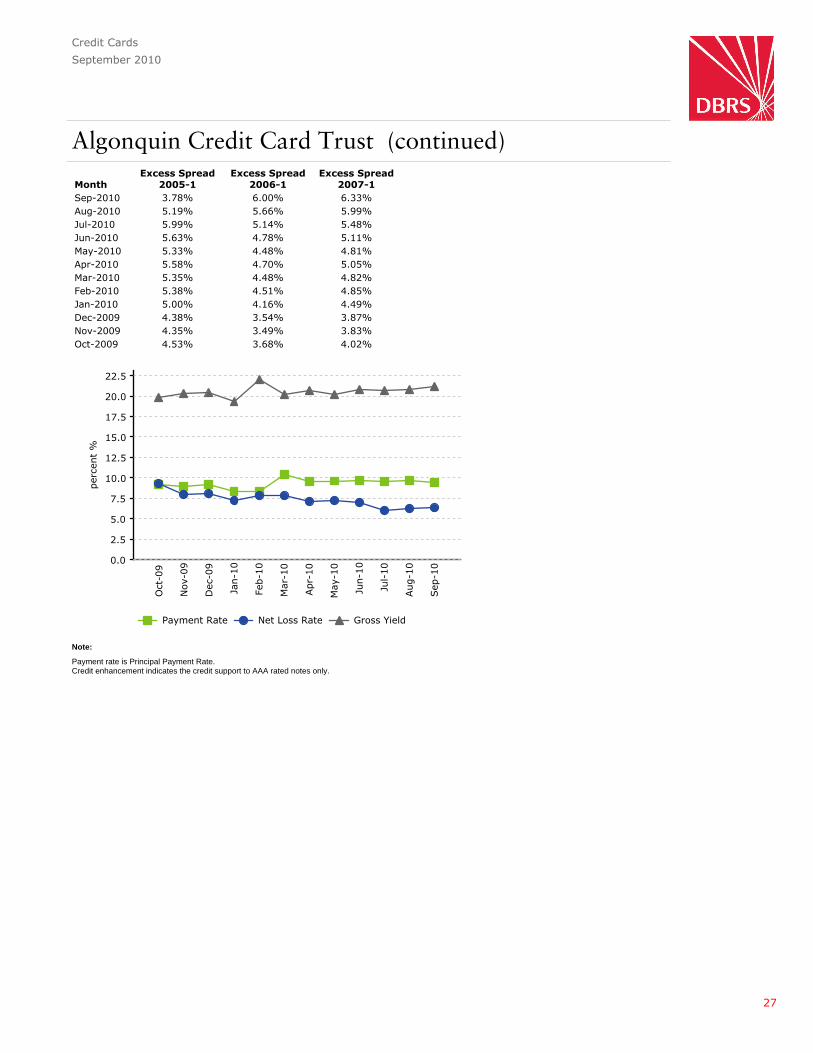

MonthExcess Spread

2005-1Excess Spread

2006-1Excess Spread

2007-1Sep-2010 3.78% 6.00% 6.33%Aug-2010 5.19% 5.66% 5.99%Jul-2010 5.99% 5.14% 5.48%Jun-2010 5.63% 4.78% 5.11%May-2010 5.33% 4.48% 4.81%Apr-2010 5.58% 4.70% 5.05%Mar-2010 5.35% 4.48% 4.82%Feb-2010 5.38% 4.51% 4.85%Jan-2010 5.00% 4.16% 4.49%Dec-2009 4.38% 3.54% 3.87%Nov-2009 4.35% 3.49% 3.83%Oct-2009 4.53% 3.68% 4.02%

27

Credit Cards

September 2010

Broadway Credit Card TrustOriginator: Citi Cards Canada Inc.

Collateral: Credit card receivables

Credit Enhancement: 1.5% Cash Reserve, Excess Spread, 14% / 17% Subordination

Program Size: 2004-2: $398 million2008-1: $583 million2008-2: $278 million

Lead Underwriter: TD Securities Inc.Merrill Lynch Canada Inc.

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

2004-2: Class A 350,000,000 350,000,000 4.804% Mar 17, 2014 Mar 17, 2017 AAA (sf)2004-2: Class B 31,818,182 31,818,182 5.434% Mar 17, 2014 Mar 17, 2017 A (sf)2004-2: Class C 15,909,091 15,909,091 5.884% Mar 17, 2014 Mar 17, 2017 BBB (sf)2004-2: Enhancement Notes 23,942,150 23,942,150 Not Available Mar 17, 2017 Mar 17, 2017 Not Rated2008-1: Class A 525,000,000 525,000,000 5.234% Jun 17, 2011 Jun 17, 2014 AAA (sf)2008-1: Class B 29,167,000 29,167,000 6.084% Jun 17, 2011 Jun 17, 2014 A (sf)2008-1: Class C 29,167,000 29,167,000 7.143% Jun 17, 2011 Jun 17, 2014 BBB (sf)2008-1: Enhancement Notes 27,123,928 27,123,928 Not Available Mar 17, 2017 Mar 17, 2017 Not Rated2008-2: Class A 250,000,000 250,000,000 5.449% Jun 17, 2013 Jun 17, 2016 AAA (sf)2008-2: Class B 13,889,000 13,889,000 6.439% Jun 17, 2013 Jun 17, 2016 A (sf)2008-2: Class C 13,889,000 13,889,000 7.659% Jun 17, 2013 Jun 17, 2016 BBB (sf)2008-2: Enhancement Notes 12,916,251 12,916,251 Not Available Mar 17, 2017 Mar 17, 2017 Not Rated

Month Pool Balance Debt Balance Net Loss Rate Payment Rate Gross YieldSep-2010 1,759,016,543 1,322,821,602 -0.04% 14.33% 21.06%Aug-2010 2,027,317,854 1,322,821,602 11.02% 18.56% 22.81%Jul-2010 2,061,894,249 1,925,194,869 10.45% 17.53% 22.43%Jun-2010 2,099,724,162 1,925,194,869 11.38% 17.25% 22.67%May-2010 2,143,563,637 1,925,194,869 9.55% 15.95% 20.67%Apr-2010 2,178,612,746 1,925,194,869 10.93% 16.33% 22.37%Mar-2010 2,206,907,417 1,925,194,869 12.01% 16.19% 22.82%Feb-2010 2,245,250,591 1,925,194,869 10.57% 15.19% 19.50%Jan-2010 2,308,542,006 1,925,194,869 11.52% 16.26% 22.32%Dec-2009 2,357,028,914 1,925,194,869 9.89% 15.40% 20.46%Nov-2009 2,352,575,359 1,925,194,869 11.22% 15.04% 21.25%Oct-2009 2,374,933,967 1,925,194,869 9.62% 16.76% 21.58%

MonthDelinquency(30-59 Days)

Delinquency(60-89 Days)

Delinquency(90+ Days)

Sep-2010 1.13% 0.00% 0.00%Aug-2010 2.25% 1.44% 2.85%Jul-2010 2.21% 1.41% 2.80%Jun-2010 2.27% 1.35% 2.80%May-2010 2.07% 1.32% 2.79%Apr-2010 2.09% 1.44% 2.77%Mar-2010 2.35% 1.42% 2.84%Feb-2010 2.20% 1.43% 2.76%Jan-2010 2.06% 1.34% 2.71%Dec-2009 2.04% 1.33% 2.65%Nov-2009 2.10% 1.32% 2.73%Oct-2009 2.04% 1.36% 2.73%

28

Credit Cards

September 2010

Broadway Credit Card Trust (continued)

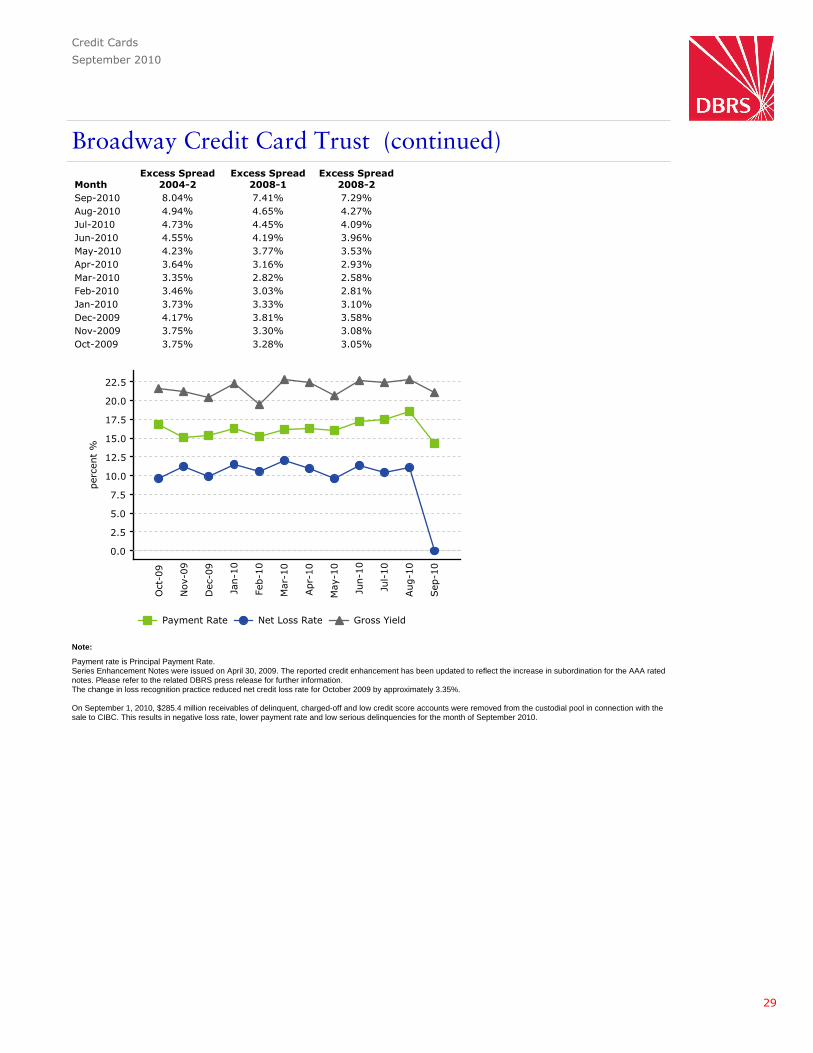

Payment rate is Principal Payment Rate.Series Enhancement Notes were issued on April 30, 2009. The reported credit enhancement has been updated to reflect the increase in subordination for the AAA ratednotes. Please refer to the related DBRS press release for further information.The change in loss recognition practice reduced net credit loss rate for October 2009 by approximately 3.35%.

On September 1, 2010, $285.4 million receivables of delinquent, charged-off and low credit score accounts were removed from the custodial pool in connection with thesale to CIBC. This results in negative loss rate, lower payment rate and low serious delinquencies for the month of September 2010.

Note:

MonthExcess Spread

2004-2Excess Spread

2008-1Excess Spread

2008-2Sep-2010 8.04% 7.41% 7.29%Aug-2010 4.94% 4.65% 4.27%Jul-2010 4.73% 4.45% 4.09%Jun-2010 4.55% 4.19% 3.96%May-2010 4.23% 3.77% 3.53%Apr-2010 3.64% 3.16% 2.93%Mar-2010 3.35% 2.82% 2.58%Feb-2010 3.46% 3.03% 2.81%Jan-2010 3.73% 3.33% 3.10%Dec-2009 4.17% 3.81% 3.58%Nov-2009 3.75% 3.30% 3.08%Oct-2009 3.75% 3.28% 3.05%

29

Credit Cards

September 2010

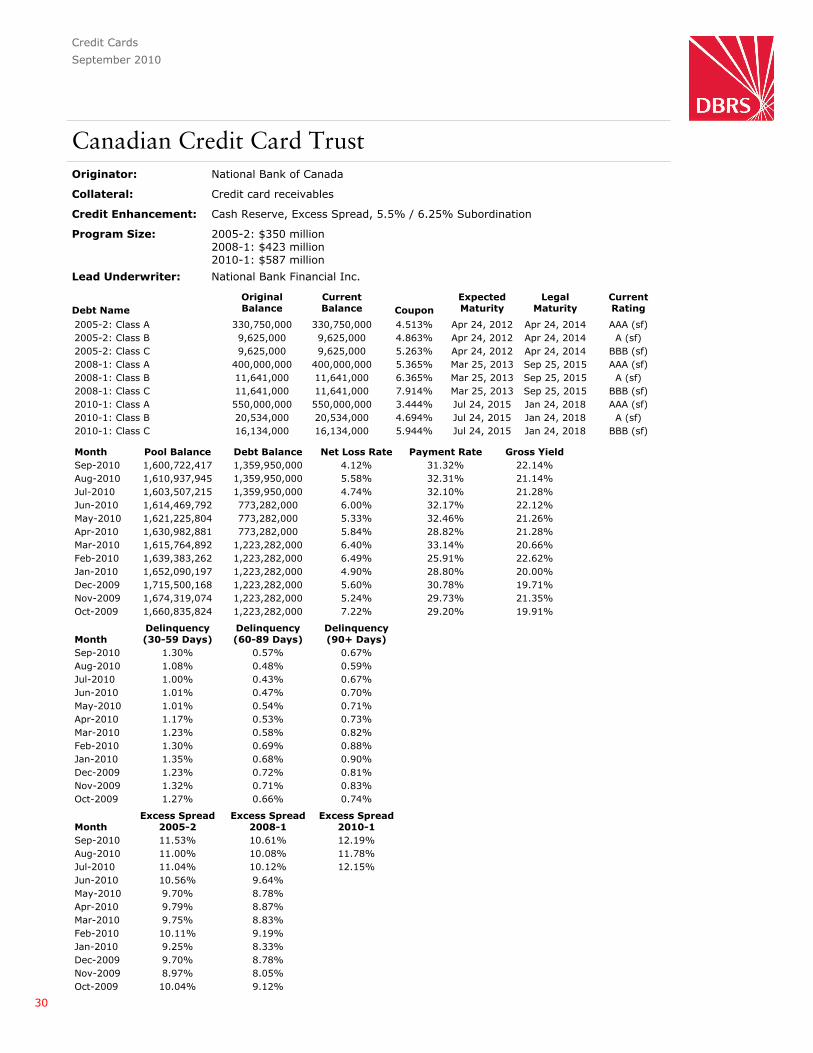

Canadian Credit Card TrustOriginator: National Bank of Canada

Collateral: Credit card receivables

Credit Enhancement: Cash Reserve, Excess Spread, 5.5% / 6.25% Subordination

Program Size: 2005-2: $350 million2008-1: $423 million2010-1: $587 million

Lead Underwriter: National Bank Financial Inc.

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

2005-2: Class A 330,750,000 330,750,000 4.513% Apr 24, 2012 Apr 24, 2014 AAA (sf)2005-2: Class B 9,625,000 9,625,000 4.863% Apr 24, 2012 Apr 24, 2014 A (sf)2005-2: Class C 9,625,000 9,625,000 5.263% Apr 24, 2012 Apr 24, 2014 BBB (sf)2008-1: Class A 400,000,000 400,000,000 5.365% Mar 25, 2013 Sep 25, 2015 AAA (sf)2008-1: Class B 11,641,000 11,641,000 6.365% Mar 25, 2013 Sep 25, 2015 A (sf)2008-1: Class C 11,641,000 11,641,000 7.914% Mar 25, 2013 Sep 25, 2015 BBB (sf)2010-1: Class A 550,000,000 550,000,000 3.444% Jul 24, 2015 Jan 24, 2018 AAA (sf)2010-1: Class B 20,534,000 20,534,000 4.694% Jul 24, 2015 Jan 24, 2018 A (sf)2010-1: Class C 16,134,000 16,134,000 5.944% Jul 24, 2015 Jan 24, 2018 BBB (sf)

Month Pool Balance Debt Balance Net Loss Rate Payment Rate Gross YieldSep-2010 1,600,722,417 1,359,950,000 4.12% 31.32% 22.14%Aug-2010 1,610,937,945 1,359,950,000 5.58% 32.31% 21.14%Jul-2010 1,603,507,215 1,359,950,000 4.74% 32.10% 21.28%Jun-2010 1,614,469,792 773,282,000 6.00% 32.17% 22.12%May-2010 1,621,225,804 773,282,000 5.33% 32.46% 21.26%Apr-2010 1,630,982,881 773,282,000 5.84% 28.82% 21.28%Mar-2010 1,615,764,892 1,223,282,000 6.40% 33.14% 20.66%Feb-2010 1,639,383,262 1,223,282,000 6.49% 25.91% 22.62%Jan-2010 1,652,090,197 1,223,282,000 4.90% 28.80% 20.00%Dec-2009 1,715,500,168 1,223,282,000 5.60% 30.78% 19.71%Nov-2009 1,674,319,074 1,223,282,000 5.24% 29.73% 21.35%Oct-2009 1,660,835,824 1,223,282,000 7.22% 29.20% 19.91%

MonthDelinquency(30-59 Days)

Delinquency(60-89 Days)

Delinquency(90+ Days)

Sep-2010 1.30% 0.57% 0.67%Aug-2010 1.08% 0.48% 0.59%Jul-2010 1.00% 0.43% 0.67%Jun-2010 1.01% 0.47% 0.70%May-2010 1.01% 0.54% 0.71%Apr-2010 1.17% 0.53% 0.73%Mar-2010 1.23% 0.58% 0.82%Feb-2010 1.30% 0.69% 0.88%Jan-2010 1.35% 0.68% 0.90%Dec-2009 1.23% 0.72% 0.81%Nov-2009 1.32% 0.71% 0.83%Oct-2009 1.27% 0.66% 0.74%

MonthExcess Spread

2005-2Excess Spread

2008-1Excess Spread

2010-1Sep-2010 11.53% 10.61% 12.19%Aug-2010 11.00% 10.08% 11.78%Jul-2010 11.04% 10.12% 12.15%Jun-2010 10.56% 9.64%May-2010 9.70% 8.78%Apr-2010 9.79% 8.87%Mar-2010 9.75% 8.83%Feb-2010 10.11% 9.19%Jan-2010 9.25% 8.33%Dec-2009 9.70% 8.78%Nov-2009 8.97% 8.05%Oct-2009 10.04% 9.12%

30

Credit Cards

September 2010

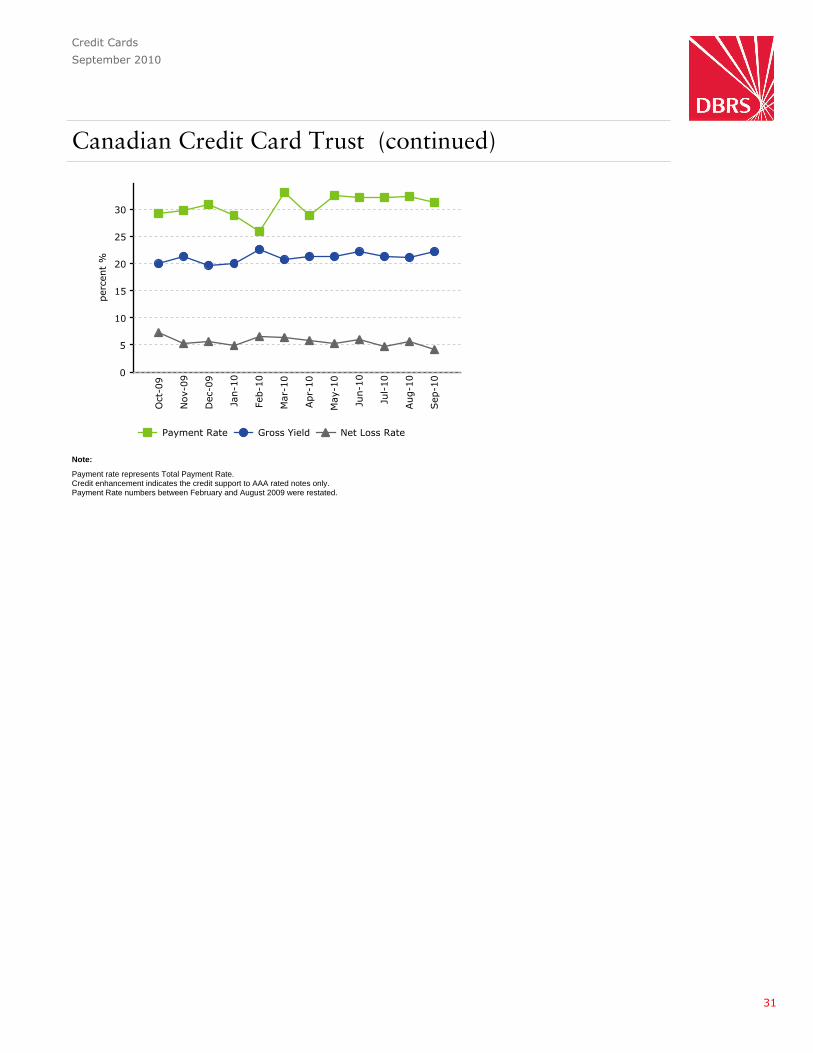

Canadian Credit Card Trust (continued)

Payment rate represents Total Payment Rate.Credit enhancement indicates the credit support to AAA rated notes only.Payment Rate numbers between February and August 2009 were restated.

Note:

31

Credit Cards

September 2010

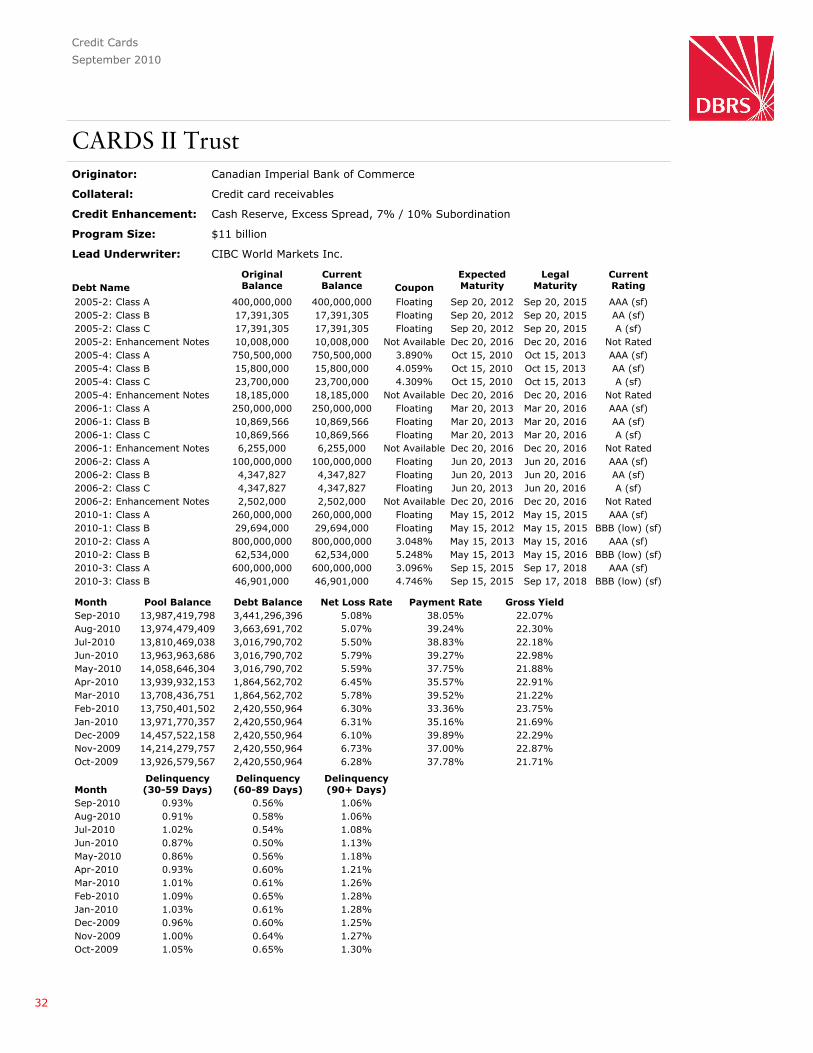

CARDS II TrustOriginator: Canadian Imperial Bank of Commerce

Collateral: Credit card receivables

Credit Enhancement: Cash Reserve, Excess Spread, 7% / 10% Subordination

Program Size: $11 billion

Lead Underwriter: CIBC World Markets Inc.

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

2005-2: Class A 400,000,000 400,000,000 Floating Sep 20, 2012 Sep 20, 2015 AAA (sf)2005-2: Class B 17,391,305 17,391,305 Floating Sep 20, 2012 Sep 20, 2015 AA (sf)2005-2: Class C 17,391,305 17,391,305 Floating Sep 20, 2012 Sep 20, 2015 A (sf)2005-2: Enhancement Notes 10,008,000 10,008,000 Not Available Dec 20, 2016 Dec 20, 2016 Not Rated2005-4: Class A 750,500,000 750,500,000 3.890% Oct 15, 2010 Oct 15, 2013 AAA (sf)2005-4: Class B 15,800,000 15,800,000 4.059% Oct 15, 2010 Oct 15, 2013 AA (sf)2005-4: Class C 23,700,000 23,700,000 4.309% Oct 15, 2010 Oct 15, 2013 A (sf)2005-4: Enhancement Notes 18,185,000 18,185,000 Not Available Dec 20, 2016 Dec 20, 2016 Not Rated2006-1: Class A 250,000,000 250,000,000 Floating Mar 20, 2013 Mar 20, 2016 AAA (sf)2006-1: Class B 10,869,566 10,869,566 Floating Mar 20, 2013 Mar 20, 2016 AA (sf)2006-1: Class C 10,869,566 10,869,566 Floating Mar 20, 2013 Mar 20, 2016 A (sf)2006-1: Enhancement Notes 6,255,000 6,255,000 Not Available Dec 20, 2016 Dec 20, 2016 Not Rated2006-2: Class A 100,000,000 100,000,000 Floating Jun 20, 2013 Jun 20, 2016 AAA (sf)2006-2: Class B 4,347,827 4,347,827 Floating Jun 20, 2013 Jun 20, 2016 AA (sf)2006-2: Class C 4,347,827 4,347,827 Floating Jun 20, 2013 Jun 20, 2016 A (sf)2006-2: Enhancement Notes 2,502,000 2,502,000 Not Available Dec 20, 2016 Dec 20, 2016 Not Rated2010-1: Class A 260,000,000 260,000,000 Floating May 15, 2012 May 15, 2015 AAA (sf)2010-1: Class B 29,694,000 29,694,000 Floating May 15, 2012 May 15, 2015 BBB (low) (sf)2010-2: Class A 800,000,000 800,000,000 3.048% May 15, 2013 May 15, 2016 AAA (sf)2010-2: Class B 62,534,000 62,534,000 5.248% May 15, 2013 May 15, 2016 BBB (low) (sf)2010-3: Class A 600,000,000 600,000,000 3.096% Sep 15, 2015 Sep 17, 2018 AAA (sf)2010-3: Class B 46,901,000 46,901,000 4.746% Sep 15, 2015 Sep 17, 2018 BBB (low) (sf)

Month Pool Balance Debt Balance Net Loss Rate Payment Rate Gross YieldSep-2010 13,987,419,798 3,441,296,396 5.08% 38.05% 22.07%Aug-2010 13,974,479,409 3,663,691,702 5.07% 39.24% 22.30%Jul-2010 13,810,469,038 3,016,790,702 5.50% 38.83% 22.18%Jun-2010 13,963,963,686 3,016,790,702 5.79% 39.27% 22.98%May-2010 14,058,646,304 3,016,790,702 5.59% 37.75% 21.88%Apr-2010 13,939,932,153 1,864,562,702 6.45% 35.57% 22.91%Mar-2010 13,708,436,751 1,864,562,702 5.78% 39.52% 21.22%Feb-2010 13,750,401,502 2,420,550,964 6.30% 33.36% 23.75%Jan-2010 13,971,770,357 2,420,550,964 6.31% 35.16% 21.69%Dec-2009 14,457,522,158 2,420,550,964 6.10% 39.89% 22.29%Nov-2009 14,214,279,757 2,420,550,964 6.73% 37.00% 22.87%Oct-2009 13,926,579,567 2,420,550,964 6.28% 37.78% 21.71%

MonthDelinquency(30-59 Days)

Delinquency(60-89 Days)

Delinquency(90+ Days)

Sep-2010 0.93% 0.56% 1.06%Aug-2010 0.91% 0.58% 1.06%Jul-2010 1.02% 0.54% 1.08%Jun-2010 0.87% 0.50% 1.13%May-2010 0.86% 0.56% 1.18%Apr-2010 0.93% 0.60% 1.21%Mar-2010 1.01% 0.61% 1.26%Feb-2010 1.09% 0.65% 1.28%Jan-2010 1.03% 0.61% 1.28%Dec-2009 0.96% 0.60% 1.25%Nov-2009 1.00% 0.64% 1.27%Oct-2009 1.05% 0.65% 1.30%

32

Credit Cards

September 2010

CARDS II Trust (continued)

Payment rate represents Total Payment Rate.Delinquency Rate buckets are 31-60 days, 61-90 days and 91+ days.Series Enhancement Notes were issued on July 21, 2009. The reported credit enhancement has been updated to reflect the increase in subordination for the AAA ratednotes. Please refer to the related DBRS press release for further information.As of June 25, 2009, Pool Interchange Amount, a component of Gross Yield, includes all interchange generated by the receivables, compared to a previously cappedpercentage.

Note:

MonthExcess Spread

2005-2Excess Spread

2005-4Excess Spread

2006-1Excess Spread

2006-2Excess Spread

2010-1Excess Spread

2010-2Sep-2010 14.00% 0.99% 14.01% 14.04% 13.45% 11.80%Aug-2010 14.21% 3.14% 14.21% 14.24% 13.62% 11.85%Jul-2010 14.02% 5.34% 14.03% 14.06% 13.81% 12.38%Jun-2010 13.80% 6.90% 13.81% 13.84% 13.90% 12.67%May-2010 13.45% 8.20% 13.46% 13.49% 14.29% 13.63%Apr-2010 13.40% 9.35% 13.40% 13.43%Mar-2010 13.32% 10.01% 13.33% 13.36%Feb-2010 13.52% 10.20% 13.53% 13.56%Jan-2010 13.34% 9.95% 13.35% 13.38%Dec-2009 13.31% 9.92% 13.32% 13.35%Nov-2009 13.26% 9.91% 13.27% 13.30%Oct-2009 13.26% 9.88% 13.27% 13.30%

MonthExcess Spread

2010-3Sep-2010 13.10%Aug-2010 14.64%Jul-2010Jun-2010May-2010Apr-2010Mar-2010Feb-2010Jan-2010Dec-2009Nov-2009Oct-2009

33

Credit Cards

September 2010

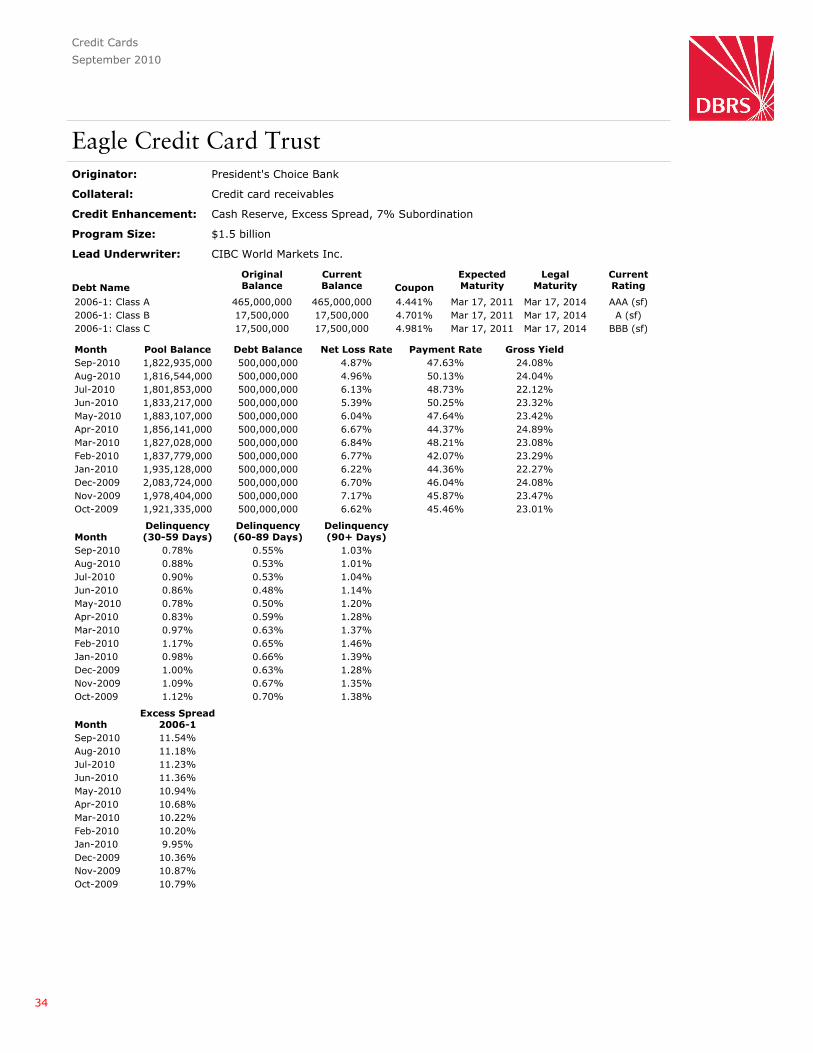

Eagle Credit Card TrustOriginator: President's Choice Bank

Collateral: Credit card receivables

Credit Enhancement: Cash Reserve, Excess Spread, 7% Subordination

Program Size: $1.5 billion

Lead Underwriter: CIBC World Markets Inc.

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

2006-1: Class A 465,000,000 465,000,000 4.441% Mar 17, 2011 Mar 17, 2014 AAA (sf)2006-1: Class B 17,500,000 17,500,000 4.701% Mar 17, 2011 Mar 17, 2014 A (sf)2006-1: Class C 17,500,000 17,500,000 4.981% Mar 17, 2011 Mar 17, 2014 BBB (sf)

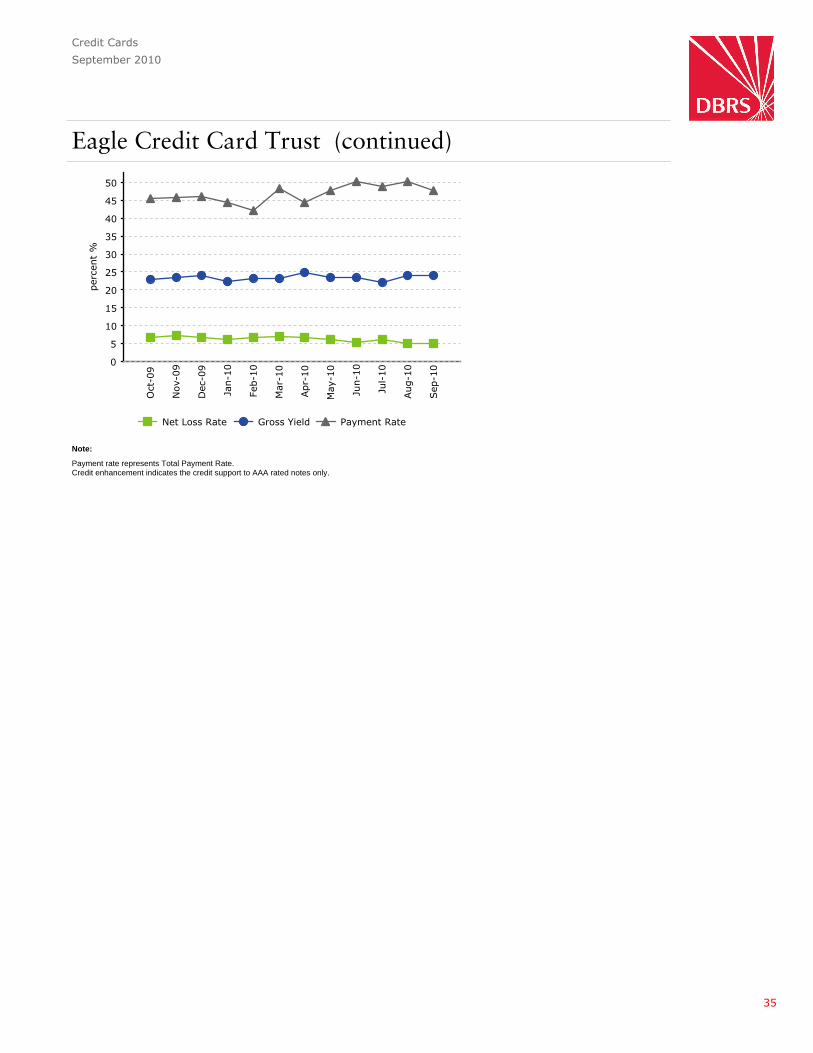

Month Pool Balance Debt Balance Net Loss Rate Payment Rate Gross YieldSep-2010 1,822,935,000 500,000,000 4.87% 47.63% 24.08%Aug-2010 1,816,544,000 500,000,000 4.96% 50.13% 24.04%Jul-2010 1,801,853,000 500,000,000 6.13% 48.73% 22.12%Jun-2010 1,833,217,000 500,000,000 5.39% 50.25% 23.32%May-2010 1,883,107,000 500,000,000 6.04% 47.64% 23.42%Apr-2010 1,856,141,000 500,000,000 6.67% 44.37% 24.89%Mar-2010 1,827,028,000 500,000,000 6.84% 48.21% 23.08%Feb-2010 1,837,779,000 500,000,000 6.77% 42.07% 23.29%Jan-2010 1,935,128,000 500,000,000 6.22% 44.36% 22.27%Dec-2009 2,083,724,000 500,000,000 6.70% 46.04% 24.08%Nov-2009 1,978,404,000 500,000,000 7.17% 45.87% 23.47%Oct-2009 1,921,335,000 500,000,000 6.62% 45.46% 23.01%

MonthDelinquency(30-59 Days)

Delinquency(60-89 Days)

Delinquency(90+ Days)

Sep-2010 0.78% 0.55% 1.03%Aug-2010 0.88% 0.53% 1.01%Jul-2010 0.90% 0.53% 1.04%Jun-2010 0.86% 0.48% 1.14%May-2010 0.78% 0.50% 1.20%Apr-2010 0.83% 0.59% 1.28%Mar-2010 0.97% 0.63% 1.37%Feb-2010 1.17% 0.65% 1.46%Jan-2010 0.98% 0.66% 1.39%Dec-2009 1.00% 0.63% 1.28%Nov-2009 1.09% 0.67% 1.35%Oct-2009 1.12% 0.70% 1.38%

MonthExcess Spread

2006-1Sep-2010 11.54%Aug-2010 11.18%Jul-2010 11.23%Jun-2010 11.36%May-2010 10.94%Apr-2010 10.68%Mar-2010 10.22%Feb-2010 10.20%Jan-2010 9.95%Dec-2009 10.36%Nov-2009 10.87%Oct-2009 10.79%

34

Credit Cards

September 2010

Eagle Credit Card Trust (continued)

Payment rate represents Total Payment Rate.Credit enhancement indicates the credit support to AAA rated notes only.

Note:

35

Credit Cards

September 2010

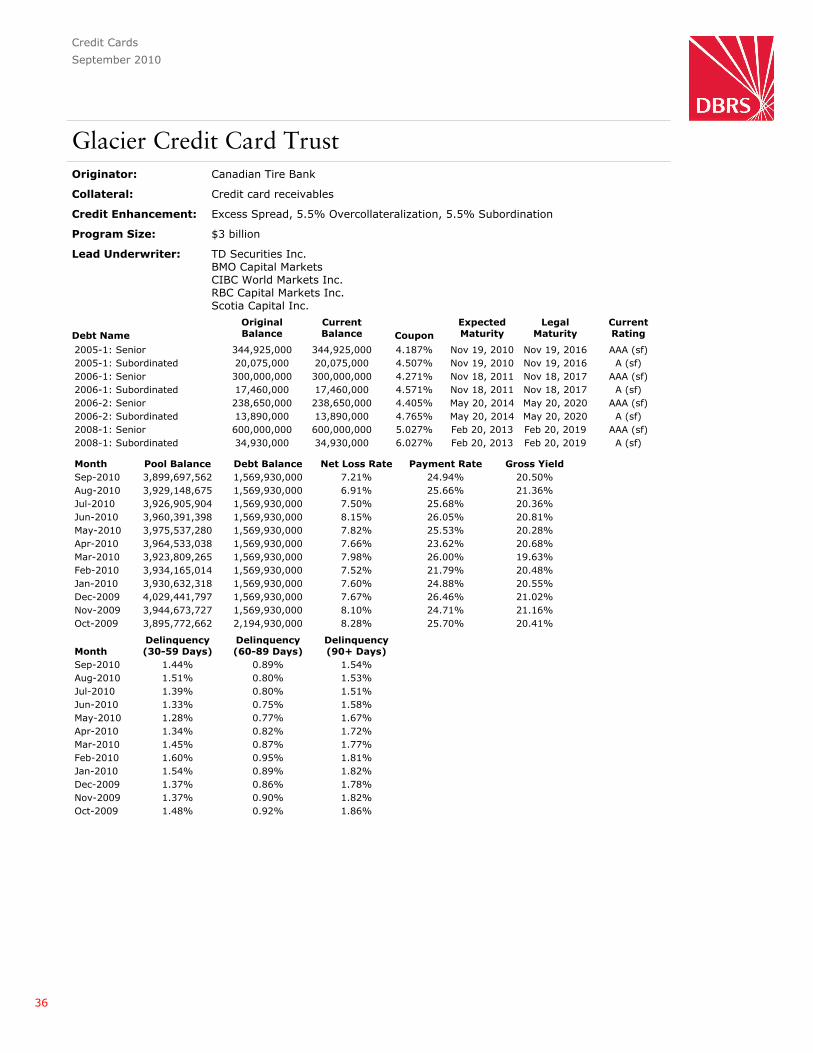

Glacier Credit Card TrustOriginator: Canadian Tire Bank

Collateral: Credit card receivables

Credit Enhancement: Excess Spread, 5.5% Overcollateralization, 5.5% Subordination

Program Size: $3 billion

Lead Underwriter: TD Securities Inc.BMO Capital MarketsCIBC World Markets Inc.RBC Capital Markets Inc.Scotia Capital Inc.

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

2005-1: Senior 344,925,000 344,925,000 4.187% Nov 19, 2010 Nov 19, 2016 AAA (sf)2005-1: Subordinated 20,075,000 20,075,000 4.507% Nov 19, 2010 Nov 19, 2016 A (sf)2006-1: Senior 300,000,000 300,000,000 4.271% Nov 18, 2011 Nov 18, 2017 AAA (sf)2006-1: Subordinated 17,460,000 17,460,000 4.571% Nov 18, 2011 Nov 18, 2017 A (sf)2006-2: Senior 238,650,000 238,650,000 4.405% May 20, 2014 May 20, 2020 AAA (sf)2006-2: Subordinated 13,890,000 13,890,000 4.765% May 20, 2014 May 20, 2020 A (sf)2008-1: Senior 600,000,000 600,000,000 5.027% Feb 20, 2013 Feb 20, 2019 AAA (sf)2008-1: Subordinated 34,930,000 34,930,000 6.027% Feb 20, 2013 Feb 20, 2019 A (sf)

Month Pool Balance Debt Balance Net Loss Rate Payment Rate Gross YieldSep-2010 3,899,697,562 1,569,930,000 7.21% 24.94% 20.50%Aug-2010 3,929,148,675 1,569,930,000 6.91% 25.66% 21.36%Jul-2010 3,926,905,904 1,569,930,000 7.50% 25.68% 20.36%Jun-2010 3,960,391,398 1,569,930,000 8.15% 26.05% 20.81%May-2010 3,975,537,280 1,569,930,000 7.82% 25.53% 20.28%Apr-2010 3,964,533,038 1,569,930,000 7.66% 23.62% 20.68%Mar-2010 3,923,809,265 1,569,930,000 7.98% 26.00% 19.63%Feb-2010 3,934,165,014 1,569,930,000 7.52% 21.79% 20.48%Jan-2010 3,930,632,318 1,569,930,000 7.60% 24.88% 20.55%Dec-2009 4,029,441,797 1,569,930,000 7.67% 26.46% 21.02%Nov-2009 3,944,673,727 1,569,930,000 8.10% 24.71% 21.16%Oct-2009 3,895,772,662 2,194,930,000 8.28% 25.70% 20.41%

MonthDelinquency(30-59 Days)

Delinquency(60-89 Days)

Delinquency(90+ Days)

Sep-2010 1.44% 0.89% 1.54%Aug-2010 1.51% 0.80% 1.53%Jul-2010 1.39% 0.80% 1.51%Jun-2010 1.33% 0.75% 1.58%May-2010 1.28% 0.77% 1.67%Apr-2010 1.34% 0.82% 1.72%Mar-2010 1.45% 0.87% 1.77%Feb-2010 1.60% 0.95% 1.81%Jan-2010 1.54% 0.89% 1.82%Dec-2009 1.37% 0.86% 1.78%Nov-2009 1.37% 0.90% 1.82%Oct-2009 1.48% 0.92% 1.86%

36

Credit Cards

September 2010

Glacier Credit Card Trust (continued)

Series 1997-1 (ABCP) is reported in the Monthly Canadian ABCP Report. Series 1997-1 is not entitled to interchange.Payment rate represents Total Payment Rate.Delinquency Rate buckets are 31-60 days, 61-90 days and 91+ daysCredit enhancement indicates the credit support to AAA rated notes only.

Note:

MonthExcess Spread

2005-1Excess Spread

2006-1Excess Spread

2006-2Excess Spread

2008-1Sep-2010 11.59% 9.21% 9.08% 8.42%Aug-2010 9.08% 9.01% 8.87% 8.22%Jul-2010 8.44% 8.35% 8.21% 7.56%Jun-2010 8.54% 8.44% 8.31% 7.65%May-2010 8.20% 8.10% 7.97% 7.31%Apr-2010 8.35% 8.26% 8.13% 7.46%Mar-2010 8.25% 8.16% 8.03% 7.37%Feb-2010 8.87% 8.79% 8.65% 7.99%Jan-2010 8.93% 8.85% 8.71% 8.06%Dec-2009 8.77% 8.69% 8.55% 7.90%Nov-2009 8.43% 8.34% 8.21% 7.55%Oct-2009 8.37% 8.28% 8.15% 7.49%

37

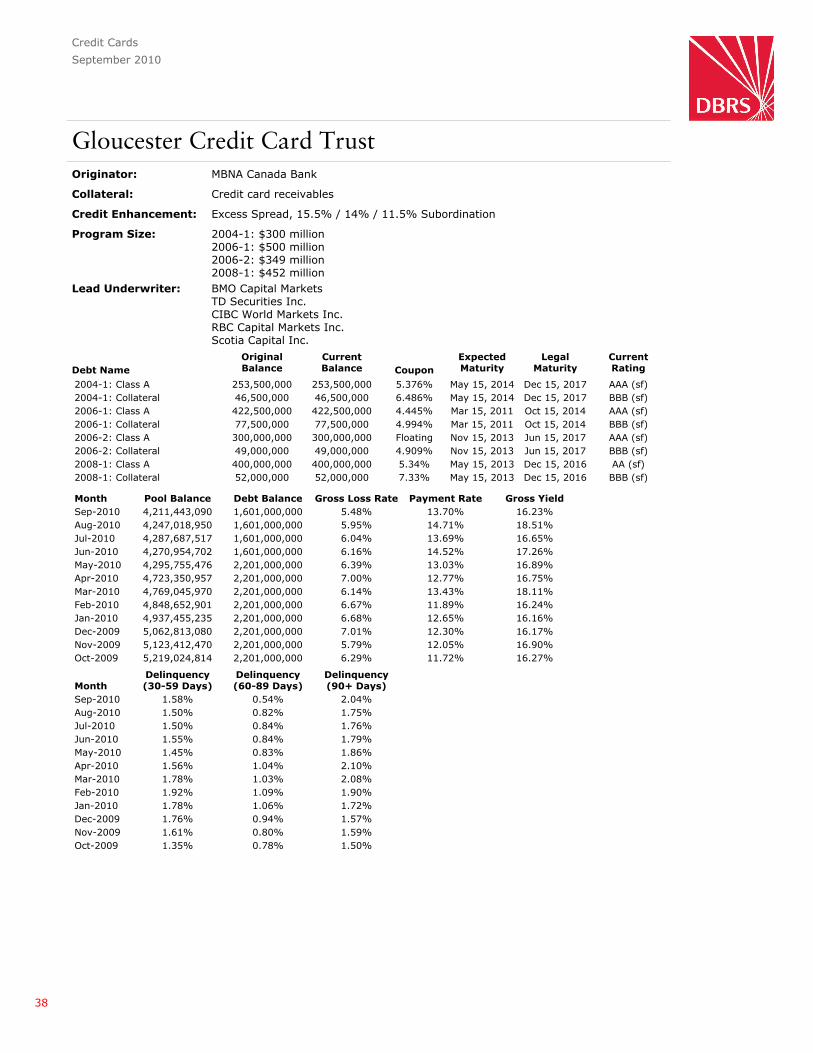

Credit Cards

September 2010

Gloucester Credit Card TrustOriginator: MBNA Canada Bank

Collateral: Credit card receivables

Credit Enhancement: Excess Spread, 15.5% / 14% / 11.5% Subordination

Program Size: 2004-1: $300 million2006-1: $500 million2006-2: $349 million2008-1: $452 million

Lead Underwriter: BMO Capital MarketsTD Securities Inc.CIBC World Markets Inc.RBC Capital Markets Inc.Scotia Capital Inc.

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

2004-1: Class A 253,500,000 253,500,000 5.376% May 15, 2014 Dec 15, 2017 AAA (sf)2004-1: Collateral 46,500,000 46,500,000 6.486% May 15, 2014 Dec 15, 2017 BBB (sf)2006-1: Class A 422,500,000 422,500,000 4.445% Mar 15, 2011 Oct 15, 2014 AAA (sf)2006-1: Collateral 77,500,000 77,500,000 4.994% Mar 15, 2011 Oct 15, 2014 BBB (sf)2006-2: Class A 300,000,000 300,000,000 Floating Nov 15, 2013 Jun 15, 2017 AAA (sf)2006-2: Collateral 49,000,000 49,000,000 4.909% Nov 15, 2013 Jun 15, 2017 BBB (sf)2008-1: Class A 400,000,000 400,000,000 5.34% May 15, 2013 Dec 15, 2016 AA (sf)2008-1: Collateral 52,000,000 52,000,000 7.33% May 15, 2013 Dec 15, 2016 BBB (sf)

Month Pool Balance Debt Balance Gross Loss Rate Payment Rate Gross YieldSep-2010 4,211,443,090 1,601,000,000 5.48% 13.70% 16.23%Aug-2010 4,247,018,950 1,601,000,000 5.95% 14.71% 18.51%Jul-2010 4,287,687,517 1,601,000,000 6.04% 13.69% 16.65%Jun-2010 4,270,954,702 1,601,000,000 6.16% 14.52% 17.26%May-2010 4,295,755,476 2,201,000,000 6.39% 13.03% 16.89%Apr-2010 4,723,350,957 2,201,000,000 7.00% 12.77% 16.75%Mar-2010 4,769,045,970 2,201,000,000 6.14% 13.43% 18.11%Feb-2010 4,848,652,901 2,201,000,000 6.67% 11.89% 16.24%Jan-2010 4,937,455,235 2,201,000,000 6.68% 12.65% 16.16%Dec-2009 5,062,813,080 2,201,000,000 7.01% 12.30% 16.17%Nov-2009 5,123,412,470 2,201,000,000 5.79% 12.05% 16.90%Oct-2009 5,219,024,814 2,201,000,000 6.29% 11.72% 16.27%

MonthDelinquency(30-59 Days)

Delinquency(60-89 Days)

Delinquency(90+ Days)

Sep-2010 1.58% 0.54% 2.04%Aug-2010 1.50% 0.82% 1.75%Jul-2010 1.50% 0.84% 1.76%Jun-2010 1.55% 0.84% 1.79%May-2010 1.45% 0.83% 1.86%Apr-2010 1.56% 1.04% 2.10%Mar-2010 1.78% 1.03% 2.08%Feb-2010 1.92% 1.09% 1.90%Jan-2010 1.78% 1.06% 1.72%Dec-2009 1.76% 0.94% 1.57%Nov-2009 1.61% 0.80% 1.59%Oct-2009 1.35% 0.78% 1.50%

38

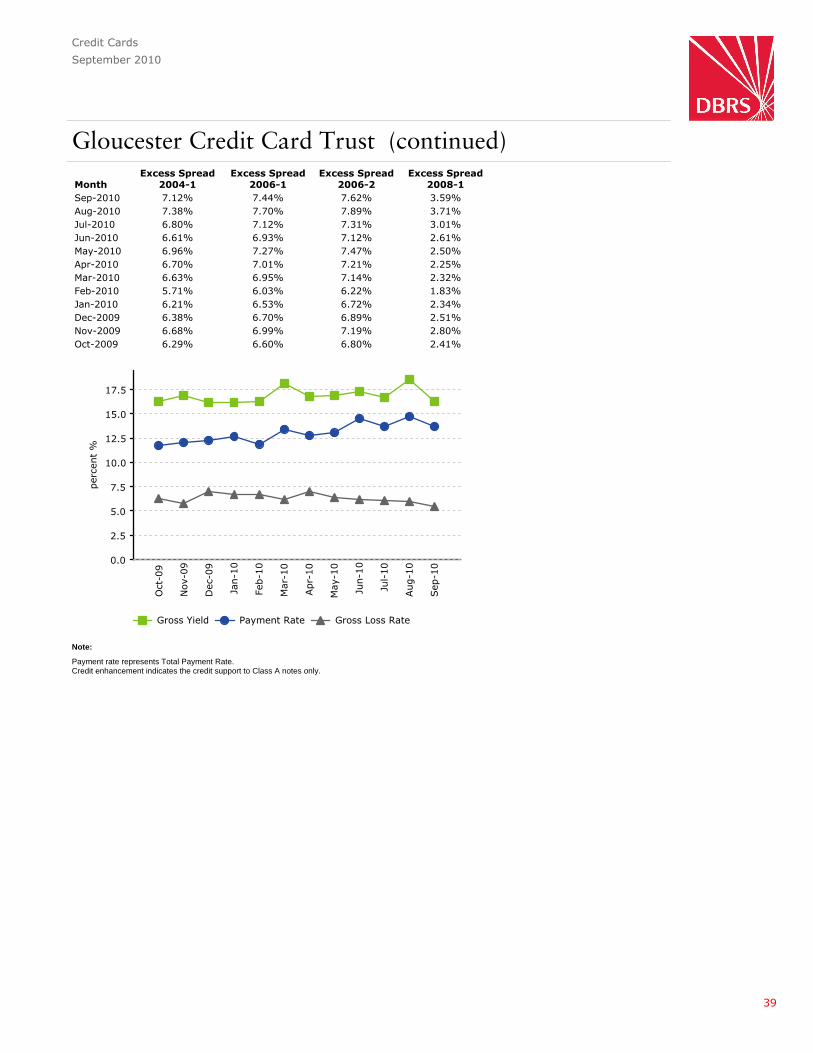

Credit Cards

September 2010

Gloucester Credit Card Trust (continued)

Payment rate represents Total Payment Rate.Credit enhancement indicates the credit support to Class A notes only.

Note:

MonthExcess Spread

2004-1Excess Spread

2006-1Excess Spread

2006-2Excess Spread

2008-1Sep-2010 7.12% 7.44% 7.62% 3.59%Aug-2010 7.38% 7.70% 7.89% 3.71%Jul-2010 6.80% 7.12% 7.31% 3.01%Jun-2010 6.61% 6.93% 7.12% 2.61%May-2010 6.96% 7.27% 7.47% 2.50%Apr-2010 6.70% 7.01% 7.21% 2.25%Mar-2010 6.63% 6.95% 7.14% 2.32%Feb-2010 5.71% 6.03% 6.22% 1.83%Jan-2010 6.21% 6.53% 6.72% 2.34%Dec-2009 6.38% 6.70% 6.89% 2.51%Nov-2009 6.68% 6.99% 7.19% 2.80%Oct-2009 6.29% 6.60% 6.80% 2.41%

39

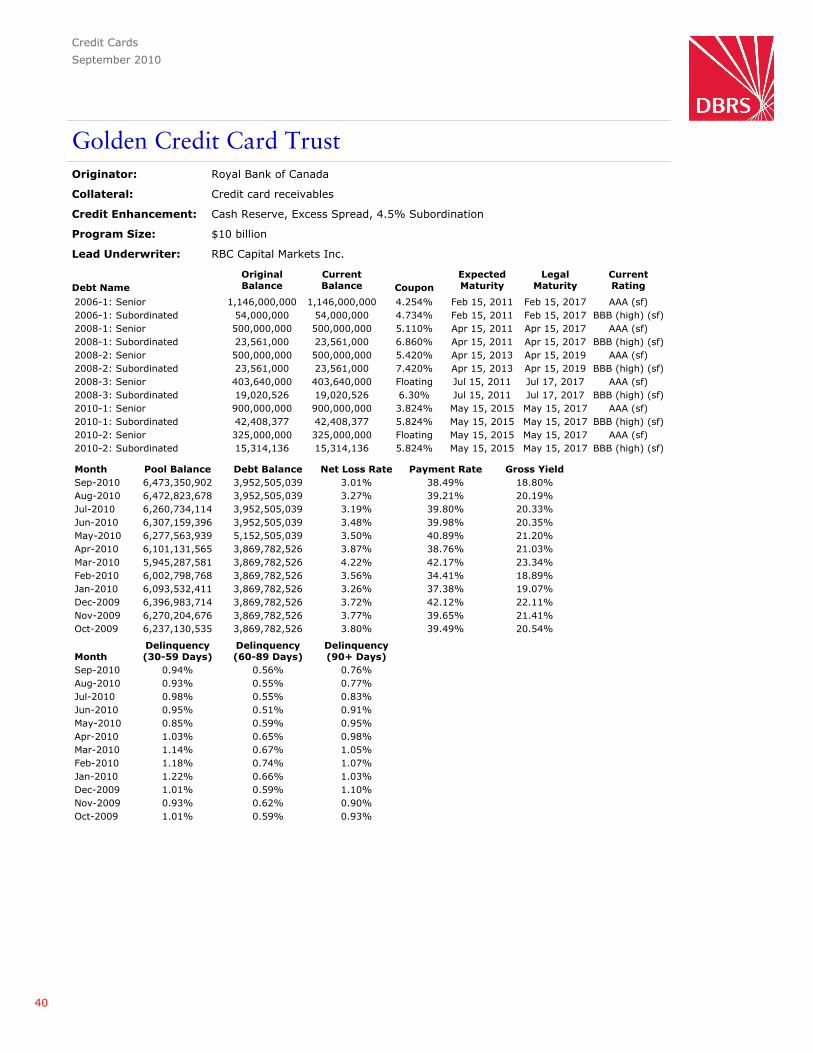

Credit Cards

September 2010

Golden Credit Card TrustOriginator: Royal Bank of Canada

Collateral: Credit card receivables

Credit Enhancement: Cash Reserve, Excess Spread, 4.5% Subordination

Program Size: $10 billion

Lead Underwriter: RBC Capital Markets Inc.

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

2006-1: Senior 1,146,000,000 1,146,000,000 4.254% Feb 15, 2011 Feb 15, 2017 AAA (sf)2006-1: Subordinated 54,000,000 54,000,000 4.734% Feb 15, 2011 Feb 15, 2017 BBB (high) (sf)2008-1: Senior 500,000,000 500,000,000 5.110% Apr 15, 2011 Apr 15, 2017 AAA (sf)2008-1: Subordinated 23,561,000 23,561,000 6.860% Apr 15, 2011 Apr 15, 2017 BBB (high) (sf)2008-2: Senior 500,000,000 500,000,000 5.420% Apr 15, 2013 Apr 15, 2019 AAA (sf)2008-2: Subordinated 23,561,000 23,561,000 7.420% Apr 15, 2013 Apr 15, 2019 BBB (high) (sf)2008-3: Senior 403,640,000 403,640,000 Floating Jul 15, 2011 Jul 17, 2017 AAA (sf)2008-3: Subordinated 19,020,526 19,020,526 6.30% Jul 15, 2011 Jul 17, 2017 BBB (high) (sf)2010-1: Senior 900,000,000 900,000,000 3.824% May 15, 2015 May 15, 2017 AAA (sf)2010-1: Subordinated 42,408,377 42,408,377 5.824% May 15, 2015 May 15, 2017 BBB (high) (sf)2010-2: Senior 325,000,000 325,000,000 Floating May 15, 2015 May 15, 2017 AAA (sf)2010-2: Subordinated 15,314,136 15,314,136 5.824% May 15, 2015 May 15, 2017 BBB (high) (sf)

Month Pool Balance Debt Balance Net Loss Rate Payment Rate Gross YieldSep-2010 6,473,350,902 3,952,505,039 3.01% 38.49% 18.80%Aug-2010 6,472,823,678 3,952,505,039 3.27% 39.21% 20.19%Jul-2010 6,260,734,114 3,952,505,039 3.19% 39.80% 20.33%Jun-2010 6,307,159,396 3,952,505,039 3.48% 39.98% 20.35%May-2010 6,277,563,939 5,152,505,039 3.50% 40.89% 21.20%Apr-2010 6,101,131,565 3,869,782,526 3.87% 38.76% 21.03%Mar-2010 5,945,287,581 3,869,782,526 4.22% 42.17% 23.34%Feb-2010 6,002,798,768 3,869,782,526 3.56% 34.41% 18.89%Jan-2010 6,093,532,411 3,869,782,526 3.26% 37.38% 19.07%Dec-2009 6,396,983,714 3,869,782,526 3.72% 42.12% 22.11%Nov-2009 6,270,204,676 3,869,782,526 3.77% 39.65% 21.41%Oct-2009 6,237,130,535 3,869,782,526 3.80% 39.49% 20.54%

MonthDelinquency(30-59 Days)

Delinquency(60-89 Days)

Delinquency(90+ Days)

Sep-2010 0.94% 0.56% 0.76%Aug-2010 0.93% 0.55% 0.77%Jul-2010 0.98% 0.55% 0.83%Jun-2010 0.95% 0.51% 0.91%May-2010 0.85% 0.59% 0.95%Apr-2010 1.03% 0.65% 0.98%Mar-2010 1.14% 0.67% 1.05%Feb-2010 1.18% 0.74% 1.07%Jan-2010 1.22% 0.66% 1.03%Dec-2009 1.01% 0.59% 1.10%Nov-2009 0.93% 0.62% 0.90%Oct-2009 1.01% 0.59% 0.93%

40

Credit Cards

September 2010

Golden Credit Card Trust (continued)

Gross Yield included interchange effective the month of October 2009.Payment rate is Total Payment Rate.The Series 2008-3 Senior Note balance is USD$ 400,000,000, which is equivalent to CAD$ 403,640,000 based on the currency swap agreement. Historical debtbalances have been updated accordingly.Delinquency Rate buckets are 31-60 days, 61-90 days and 91+ days.Credit enhancement indicates the credit support to AAA rated notes only.Net Loss Rate, Payment Rate and Gross Yield numbers between April and August 2009 were restated.

Note:

MonthExcess Spread

2006-1Excess Spread

2008-1Excess Spread

2008-2Excess Spread

2008-3Excess Spread

2010-1Excess Spread

2010-2Sep-2010 13.75% 11.33% 10.96% 11.58% 12.49% 12.60%Aug-2010 13.38% 11.69% 11.32% 11.93% 12.85% 12.97%Jul-2010 12.90% 11.95% 11.59% 12.20% 13.11% 13.21%Jun-2010 12.91% 11.96% 11.59% 12.20%May-2010 13.66% 12.71% 12.34% 12.95%Apr-2010 12.87% 11.92% 11.56% 12.17%Mar-2010 12.42% 11.47% 11.11% 11.72%Feb-2010 12.19% 11.24% 10.87% 11.48%Jan-2010 12.95% 12.00% 11.64% 12.25%Dec-2009 13.27% 12.32% 11.95% 12.56%Nov-2009 10.33% 9.38% 9.01% 9.62%Oct-2009 7.86% 6.54% 6.54% 7.15%

41

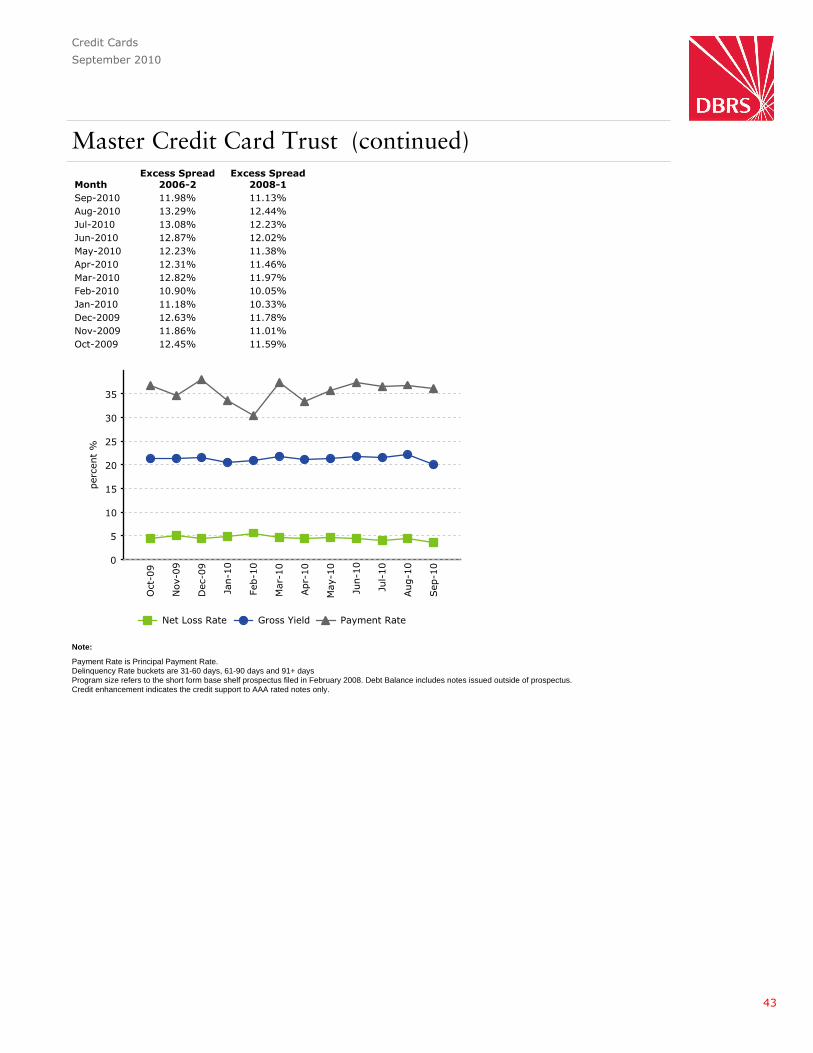

Credit Cards

September 2010

Master Credit Card TrustOriginator: Bank of Montreal

Collateral: Credit card receivables

Credit Enhancement: Cash Reserve, Excess Spread, 4.5% Subordination

Program Size: $3 billion

Lead Underwriter: BMO Capital Markets

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

2006-2: Class A 955,000,000 955,000,000 4.444% Nov 21, 2011 May 21, 2013 AAA (sf)2006-2: Class B 22,500,000 22,500,000 4.594% Nov 21, 2011 May 21, 2013 A (sf)2006-2: Class C 22,500,000 22,500,000 4.744% Nov 21, 2011 May 21, 2013 BBB (sf)2006-3: Class A 231,250,000 231,250,000 Floating Nov 21, 2011 May 21, 2013 AAA (sf)2006-3: Class B 9,375,000 9,375,000 Floating Nov 21, 2011 May 21, 2013 A (sf)2006-3: Class C 9,375,000 9,375,000 Floating Nov 21, 2011 May 21, 2013 BBB (sf)2008-1: Class A 525,000,000 525,000,000 5.237% May 21, 2013 Nov 21, 2014 AAA (sf)2008-1: Class B 12,370,000 12,370,000 6.237% May 21, 2013 Nov 21, 2014 A (sf)2008-1: Class C 12,370,000 12,370,000 7.237% May 21, 2013 Nov 21, 2014 BBB (sf)2008-2: Class A 1,000,000,000 1,000,000,000 5.297% Aug 21, 2012 Feb 21, 2014 AAA (sf)2008-2: Class B 23,565,000 23,565,000 6.297% Aug 21, 2012 Feb 21, 2014 A (sf)2008-2: Class C 23,565,000 23,565,000 7.297% Aug 21, 2012 Feb 21, 2014 BBB (sf)2008-3: Class A 1,000,000,000 1,000,000,000 Floating Nov 21, 2012 May 21, 2014 AAA (sf)2008-3: Class B 40,550,000 40,550,000 Floating Nov 21, 2012 May 21, 2014 A (sf)2008-3: Class C 40,550,000 40,550,000 Floating Nov 21, 2012 May 21, 2014 BBB (sf)2008-4: Class A 500,000,000 500,000,000 Floating Nov 21, 2013 May 21, 2015 AAA (sf)2008-4: Class B 20,275,000 20,275,000 Floating Nov 21, 2013 May 21, 2015 A (sf)2008-4: Class C 20,275,000 20,275,000 Floating Nov 21, 2013 May 21, 2015 BBB (sf)

Month Pool Balance Debt Balance Net Loss Rate Payment Rate Gross YieldSep-2010 7,273,809,909 4,468,520,000 3.54% 36.23% 19.98%Aug-2010 7,251,572,952 4,468,520,000 4.37% 36.87% 22.12%Jul-2010 7,271,774,326 4,468,520,000 4.01% 36.47% 21.55%Jun-2010 7,191,165,452 4,468,520,000 4.40% 37.31% 21.73%May-2010 7,193,157,292 4,468,520,000 4.58% 35.76% 21.27%Apr-2010 7,244,208,155 4,468,520,000 4.38% 33.47% 21.15%Mar-2010 6,976,661,857 4,468,520,000 4.58% 37.46% 21.86%Feb-2010 7,137,189,317 4,468,520,000 5.61% 30.35% 20.97%Jan-2010 7,222,046,901 4,468,520,000 4.95% 33.60% 20.59%Dec-2009 7,505,184,487 4,468,520,000 4.40% 37.99% 21.49%Nov-2009 7,212,474,054 4,468,520,000 5.10% 34.62% 21.42%Oct-2009 7,139,109,673 4,718,520,000 4.36% 36.79% 21.26%

MonthDelinquency(30-59 Days)

Delinquency(60-89 Days)

Delinquency(90+ Days)

Sep-2010 1.31% 0.72% 1.13%Aug-2010 1.27% 0.63% 1.13%Jul-2010 1.17% 0.62% 1.13%Jun-2010 1.11% 0.60% 1.15%May-2010 1.12% 0.67% 1.17%Apr-2010 1.19% 0.62% 1.18%Mar-2010 1.24% 0.69% 1.26%Feb-2010 1.39% 0.75% 1.27%Jan-2010 1.38% 0.69% 1.24%Dec-2009 1.19% 0.63% 1.19%Nov-2009 1.16% 0.66% 1.25%Oct-2009 1.24% 0.70% 1.28%

42

Credit Cards

September 2010

Master Credit Card Trust (continued)

Payment Rate is Principal Payment Rate.Delinquency Rate buckets are 31-60 days, 61-90 days and 91+ daysProgram size refers to the short form base shelf prospectus filed in February 2008. Debt Balance includes notes issued outside of prospectus.Credit enhancement indicates the credit support to AAA rated notes only.

Note:

MonthExcess Spread

2006-2Excess Spread

2008-1Sep-2010 11.98% 11.13%Aug-2010 13.29% 12.44%Jul-2010 13.08% 12.23%Jun-2010 12.87% 12.02%May-2010 12.23% 11.38%Apr-2010 12.31% 11.46%Mar-2010 12.82% 11.97%Feb-2010 10.90% 10.05%Jan-2010 11.18% 10.33%Dec-2009 12.63% 11.78%Nov-2009 11.86% 11.01%Oct-2009 12.45% 11.59%

43

Credit Cards

September 2010

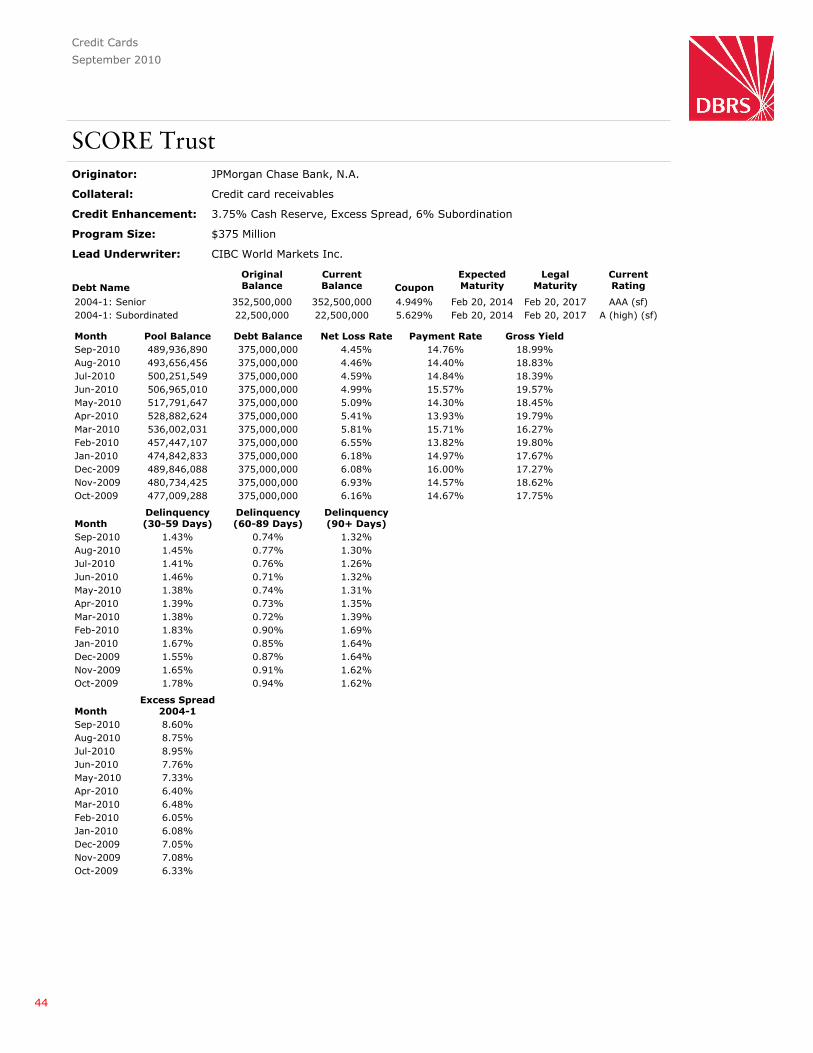

SCORE TrustOriginator: JPMorgan Chase Bank, N.A.

Collateral: Credit card receivables

Credit Enhancement: 3.75% Cash Reserve, Excess Spread, 6% Subordination

Program Size: $375 Million

Lead Underwriter: CIBC World Markets Inc.

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

2004-1: Senior 352,500,000 352,500,000 4.949% Feb 20, 2014 Feb 20, 2017 AAA (sf)2004-1: Subordinated 22,500,000 22,500,000 5.629% Feb 20, 2014 Feb 20, 2017 A (high) (sf)

Month Pool Balance Debt Balance Net Loss Rate Payment Rate Gross YieldSep-2010 489,936,890 375,000,000 4.45% 14.76% 18.99%Aug-2010 493,656,456 375,000,000 4.46% 14.40% 18.83%Jul-2010 500,251,549 375,000,000 4.59% 14.84% 18.39%Jun-2010 506,965,010 375,000,000 4.99% 15.57% 19.57%May-2010 517,791,647 375,000,000 5.09% 14.30% 18.45%Apr-2010 528,882,624 375,000,000 5.41% 13.93% 19.79%Mar-2010 536,002,031 375,000,000 5.81% 15.71% 16.27%Feb-2010 457,447,107 375,000,000 6.55% 13.82% 19.80%Jan-2010 474,842,833 375,000,000 6.18% 14.97% 17.67%Dec-2009 489,846,088 375,000,000 6.08% 16.00% 17.27%Nov-2009 480,734,425 375,000,000 6.93% 14.57% 18.62%Oct-2009 477,009,288 375,000,000 6.16% 14.67% 17.75%

MonthDelinquency(30-59 Days)

Delinquency(60-89 Days)

Delinquency(90+ Days)

Sep-2010 1.43% 0.74% 1.32%Aug-2010 1.45% 0.77% 1.30%Jul-2010 1.41% 0.76% 1.26%Jun-2010 1.46% 0.71% 1.32%May-2010 1.38% 0.74% 1.31%Apr-2010 1.39% 0.73% 1.35%Mar-2010 1.38% 0.72% 1.39%Feb-2010 1.83% 0.90% 1.69%Jan-2010 1.67% 0.85% 1.64%Dec-2009 1.55% 0.87% 1.64%Nov-2009 1.65% 0.91% 1.62%Oct-2009 1.78% 0.94% 1.62%

MonthExcess Spread

2004-1Sep-2010 8.60%Aug-2010 8.75%Jul-2010 8.95%Jun-2010 7.76%May-2010 7.33%Apr-2010 6.40%Mar-2010 6.48%Feb-2010 6.05%Jan-2010 6.08%Dec-2009 7.05%Nov-2009 7.08%Oct-2009 6.33%

44

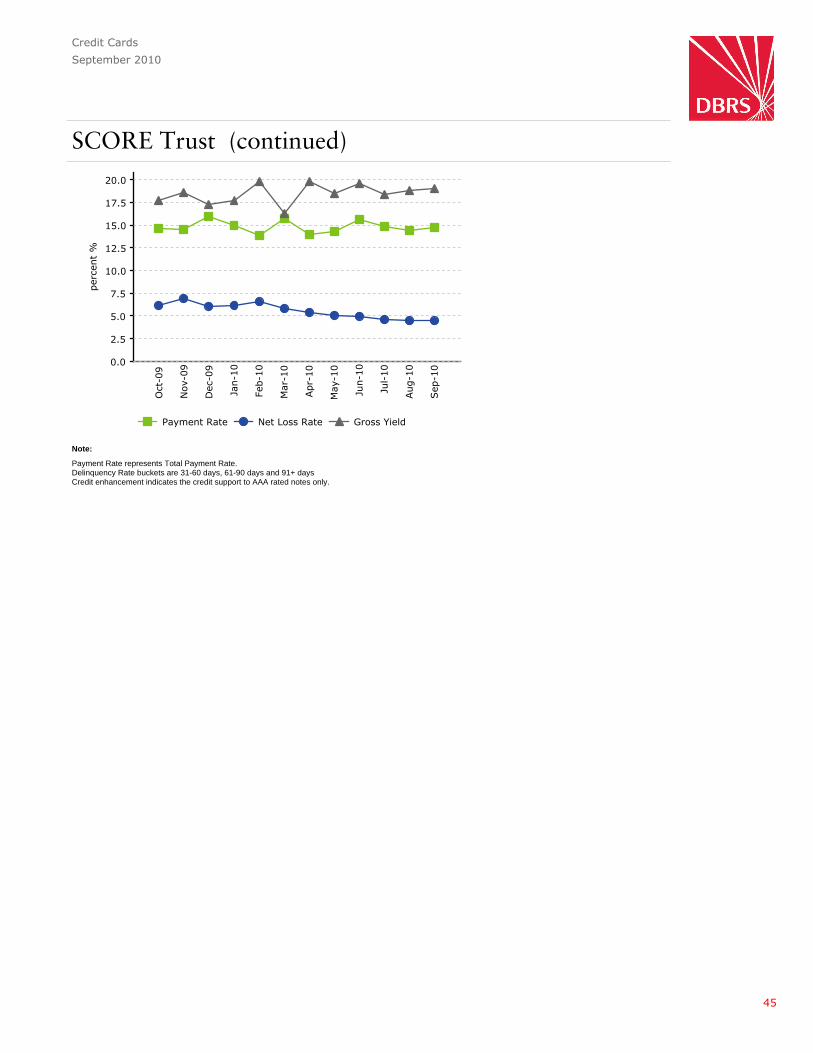

Credit Cards

September 2010

SCORE Trust (continued)

Payment Rate represents Total Payment Rate.Delinquency Rate buckets are 31-60 days, 61-90 days and 91+ daysCredit enhancement indicates the credit support to AAA rated notes only.

Note:

45

Lines of Credit

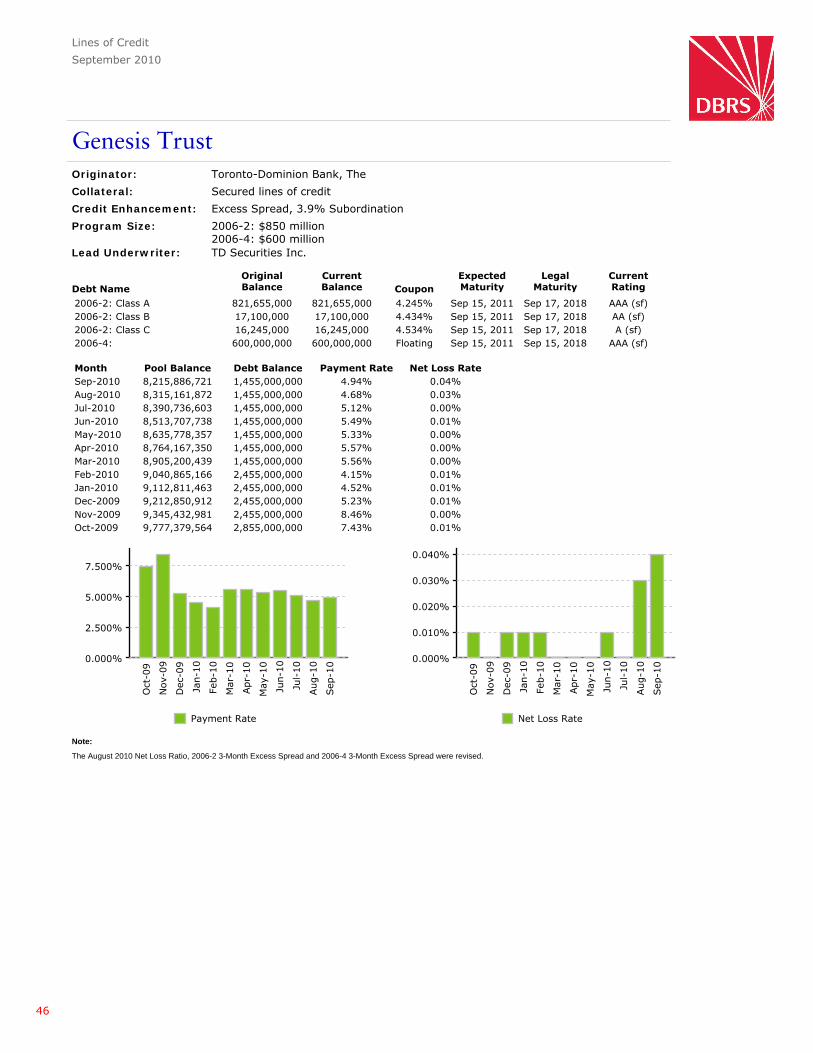

September 2010

Genesis TrustOriginator: Toronto-Dominion Bank, The

Collateral: Secured lines of credit

Credit Enhancement: Excess Spread, 3.9% Subordination

Program Size: 2006-2: $850 million2006-4: $600 million

Lead Underwriter: TD Securities Inc.

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

2006-2: Class A 821,655,000 821,655,000 4.245% Sep 15, 2011 Sep 17, 2018 AAA (sf)2006-2: Class B 17,100,000 17,100,000 4.434% Sep 15, 2011 Sep 17, 2018 AA (sf)2006-2: Class C 16,245,000 16,245,000 4.534% Sep 15, 2011 Sep 17, 2018 A (sf)2006-4: 600,000,000 600,000,000 Floating Sep 15, 2011 Sep 15, 2018 AAA (sf)

Month Pool Balance Debt Balance Payment Rate Net Loss RateSep-2010 8,215,886,721 1,455,000,000 4.94% 0.04%Aug-2010 8,315,161,872 1,455,000,000 4.68% 0.03%Jul-2010 8,390,736,603 1,455,000,000 5.12% 0.00%Jun-2010 8,513,707,738 1,455,000,000 5.49% 0.01%May-2010 8,635,778,357 1,455,000,000 5.33% 0.00%Apr-2010 8,764,167,350 1,455,000,000 5.57% 0.00%Mar-2010 8,905,200,439 1,455,000,000 5.56% 0.00%Feb-2010 9,040,865,166 2,455,000,000 4.15% 0.01%Jan-2010 9,112,811,463 2,455,000,000 4.52% 0.01%Dec-2009 9,212,850,912 2,455,000,000 5.23% 0.01%Nov-2009 9,345,432,981 2,455,000,000 8.46% 0.00%Oct-2009 9,777,379,564 2,855,000,000 7.43% 0.01%

The August 2010 Net Loss Ratio, 2006-2 3-Month Excess Spread and 2006-4 3-Month Excess Spread were revised.

Note:

46

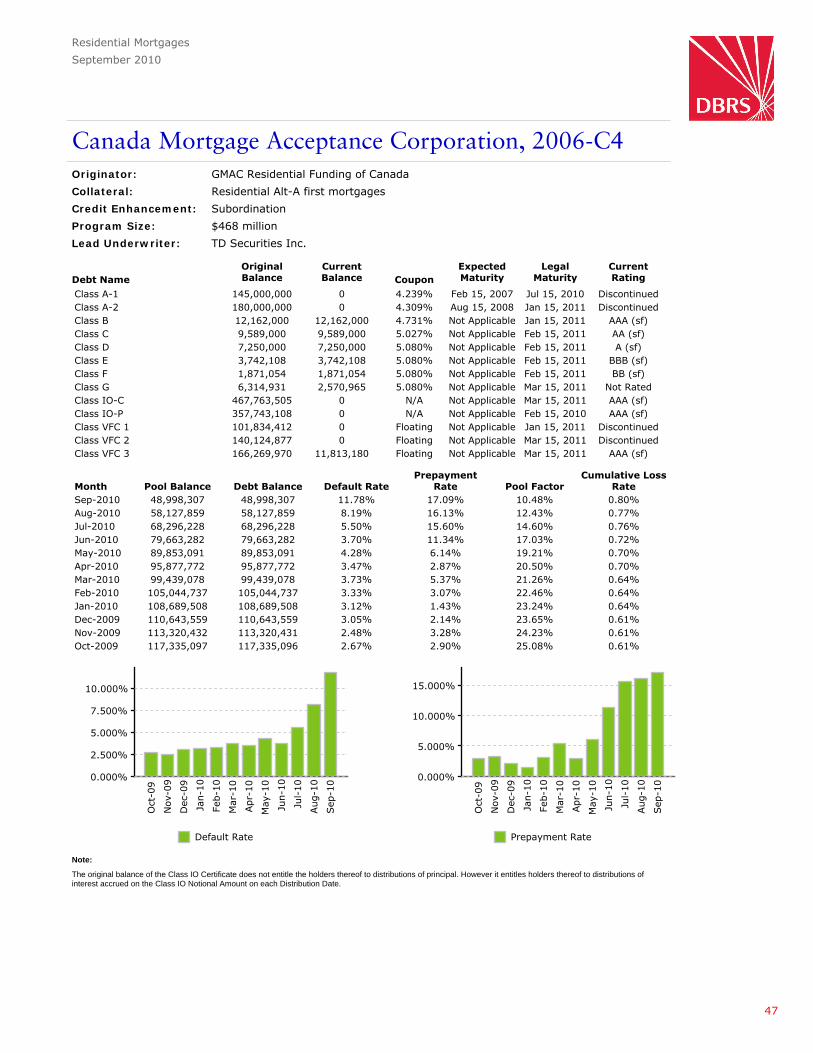

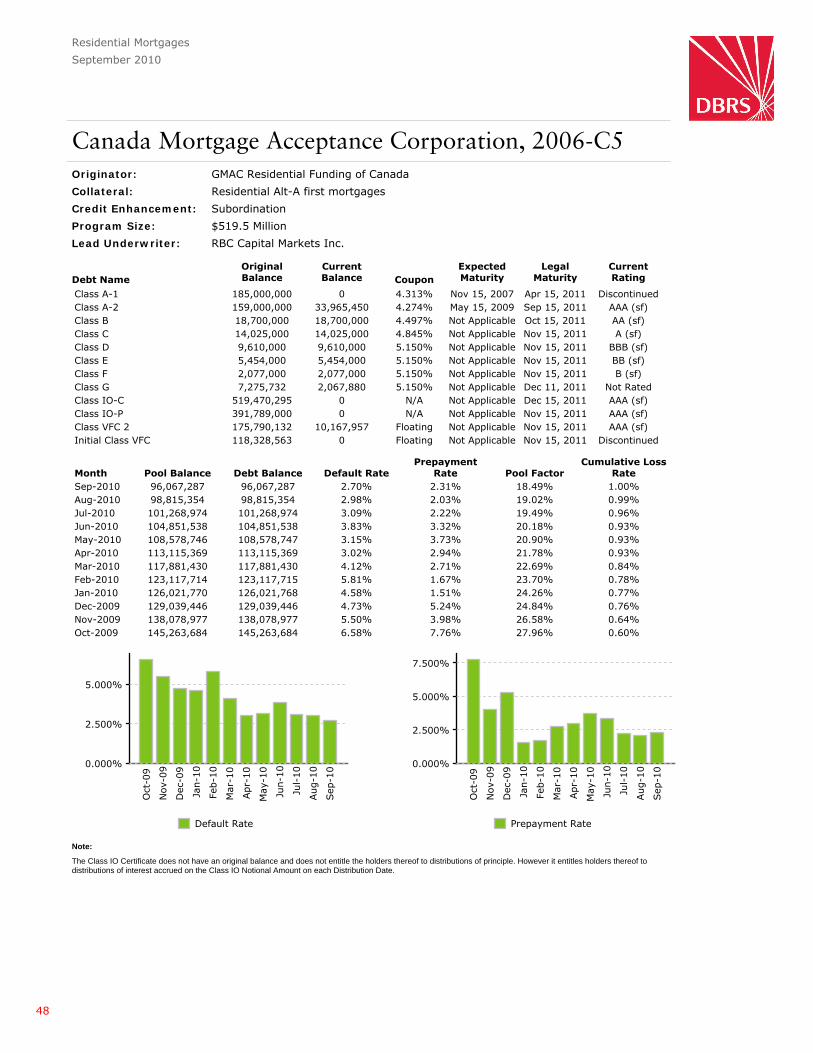

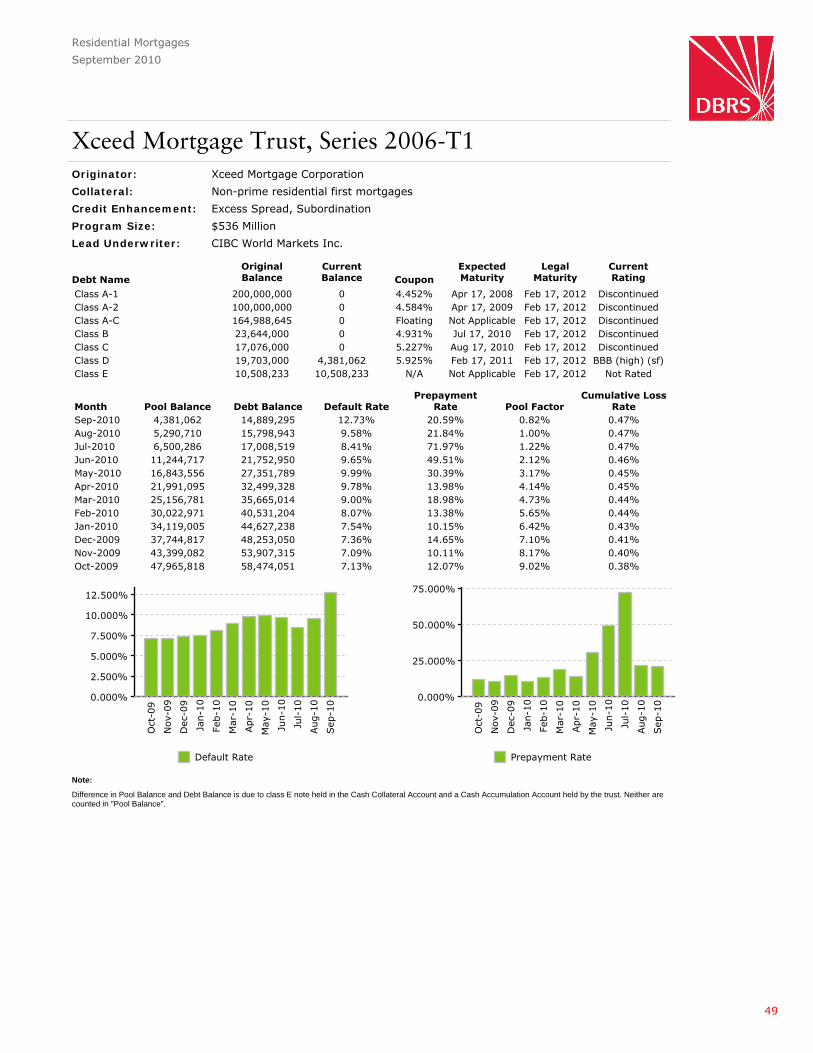

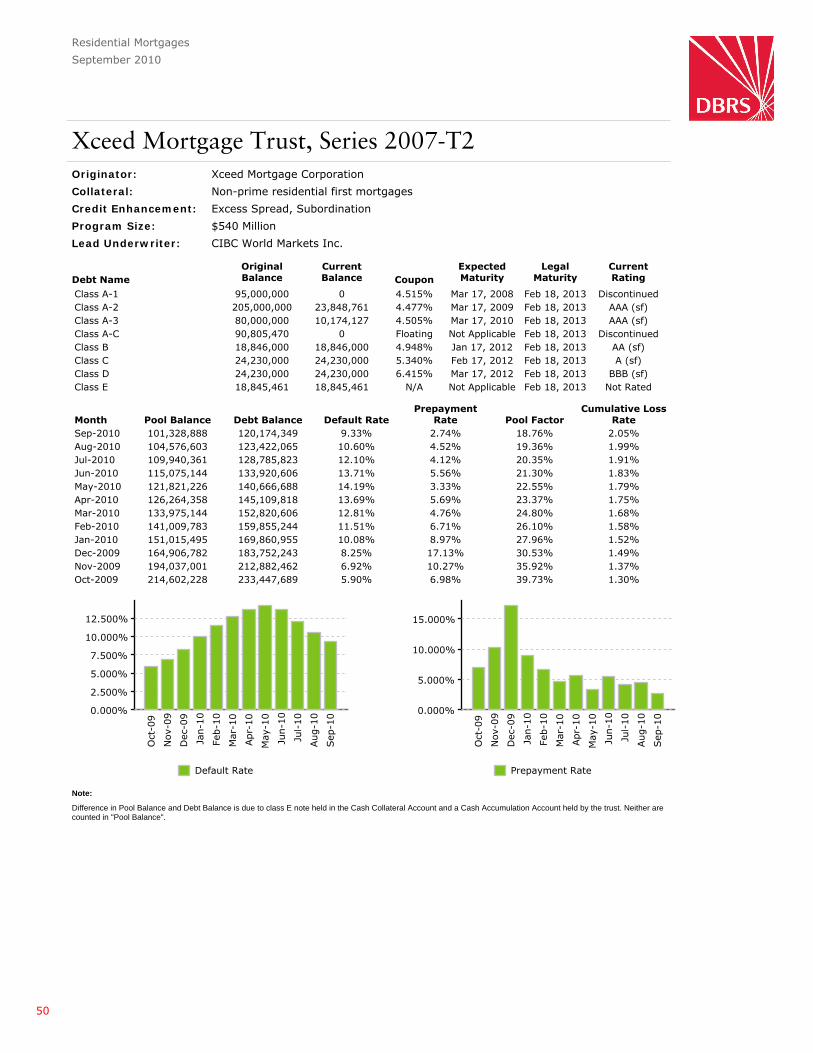

Residential Mortgages

September 2010

Canada Mortgage Acceptance Corporation, 2006-C4Originator: GMAC Residential Funding of Canada

Collateral: Residential Alt-A first mortgages

Credit Enhancement: Subordination

Program Size: $468 million

Lead Underwriter: TD Securities Inc.

Debt NameOriginalBalance

CurrentBalance Coupon

ExpectedMaturity

LegalMaturity

CurrentRating

Class A-1 145,000,000 0 4.239% Feb 15, 2007 Jul 15, 2010 DiscontinuedClass A-2 180,000,000 0 4.309% Aug 15, 2008 Jan 15, 2011 DiscontinuedClass B 12,162,000 12,162,000 4.731% Not Applicable Jan 15, 2011 AAA (sf)Class C 9,589,000 9,589,000 5.027% Not Applicable Feb 15, 2011 AA (sf)Class D 7,250,000 7,250,000 5.080% Not Applicable Feb 15, 2011 A (sf)Class E 3,742,108 3,742,108 5.080% Not Applicable Feb 15, 2011 BBB (sf)Class F 1,871,054 1,871,054 5.080% Not Applicable Feb 15, 2011 BB (sf)Class G 6,314,931 2,570,965 5.080% Not Applicable Mar 15, 2011 Not RatedClass IO-C 467,763,505 0 N/A Not Applicable Mar 15, 2011 AAA (sf)Class IO-P 357,743,108 0 N/A Not Applicable Feb 15, 2010 AAA (sf)Class VFC 1 101,834,412 0 Floating Not Applicable Jan 15, 2011 DiscontinuedClass VFC 2 140,124,877 0 Floating Not Applicable Mar 15, 2011 DiscontinuedClass VFC 3 166,269,970 11,813,180 Floating Not Applicable Mar 15, 2011 AAA (sf)

Month Pool Balance Debt Balance Default RatePrepayment

Rate Pool FactorCumulative Loss