Embed Size (px)

Citation preview

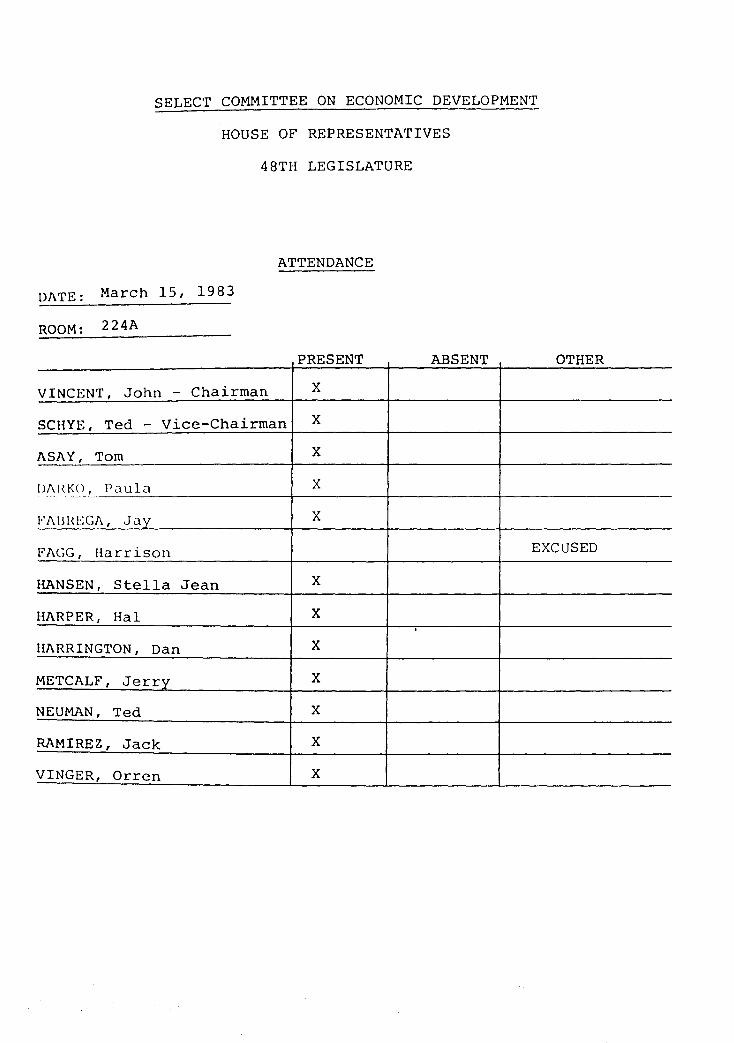

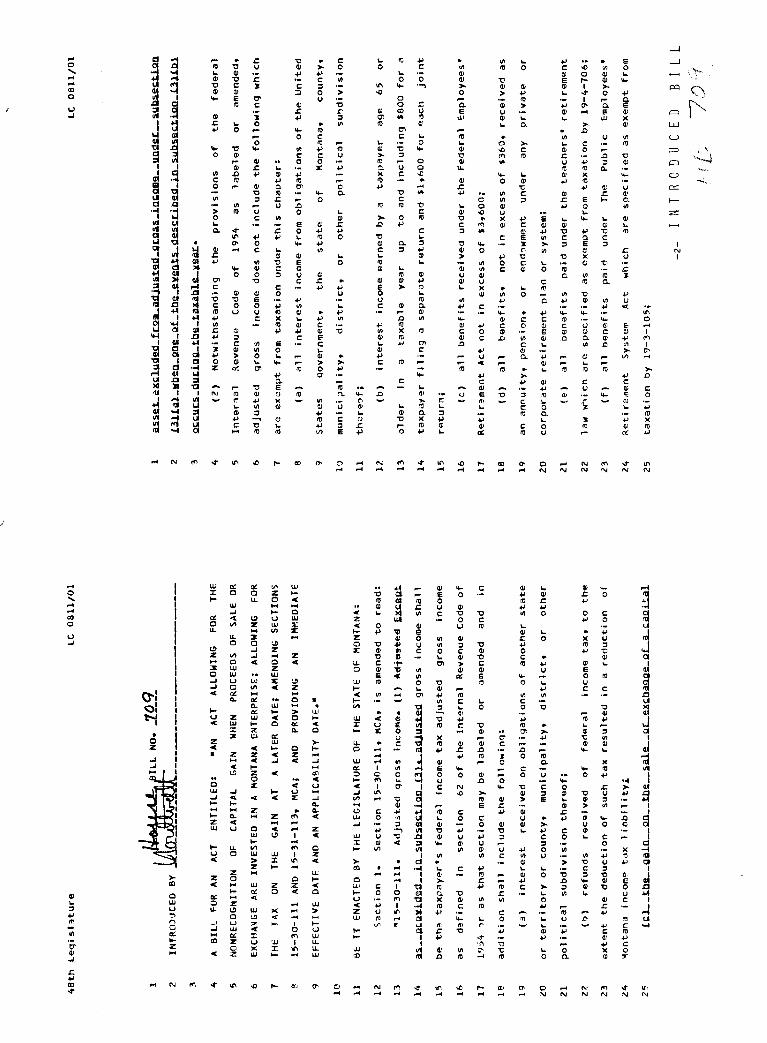

SELECT COMMITTEE ON ECONOMIC DEVELOPMENT

HOUSE OF REPRESENTATIVES

48TH LEGISLATURE

ATTENDANCE

DATE: March 15, 1983

ROOM: 224A

PRESENT

VINCENT, John - Chairman X

SCHYE, Ted - Vice-Chairman X

ASAY, Tom X

()i'\ l{ K~L,. Paula X

\o'ABHECA, Jay X

ABSENT OTHER

FAGG, Harrison EXCUSED

HANSEN, Stella Jean X

HARPER, Hal X

HARRINGTON, Dan X

METCALF, Jerry X

NEUMAN, Ted X

RAMIREZ, Jack X

VINGER, Orren X

MINUTES OF THE SELIX:.'T CC:M-{PlTEE 00 OCONCMIC DEVELOPMENT

March 15, 1983

The eleventh meeting of the Select Committee on Economic Development was called to order by Chairman, John Vincent at 10:24 p.m. in room 224A in the capitol Building, Helena, Ivbntana on March 15, 1983.

Roll call was taken and all rrembers were present with the exception of Representative Fagg who was excused.

QiAIRMAN VINCENT stated he would like to welcome everyone to the hearing and apologized for the lateness of the meeting. He commented due to the lateness of the hour, he would like the sponsors to save ~~eir detailed explanations of the bill for Executive Session, and let those who came to testify have rost of the tirre. The bills heard this evening will be in the following order: HB 709, SB 316, HB 865.

REPRESENTATIVE NORDIVEDr, Sponsor of HB 709, explained this bill is a mechanism that is rrore efficient than the venture capital corporation for bringing equity capital into Montana. This is a bill that if you sell a capital asset at a gain and within a certain period of time reinvest the capital in a Montana venture, your capital gain will be put off as long as it is invested in a Montana enterprise. He stated an example is demonstrated in Exhibit A.

CHAIRI'v1AN VINCENT asked for any Proponents to speak for HB 709, there being no Proponents, he asked for any OpFOnents.

OPPONENTS

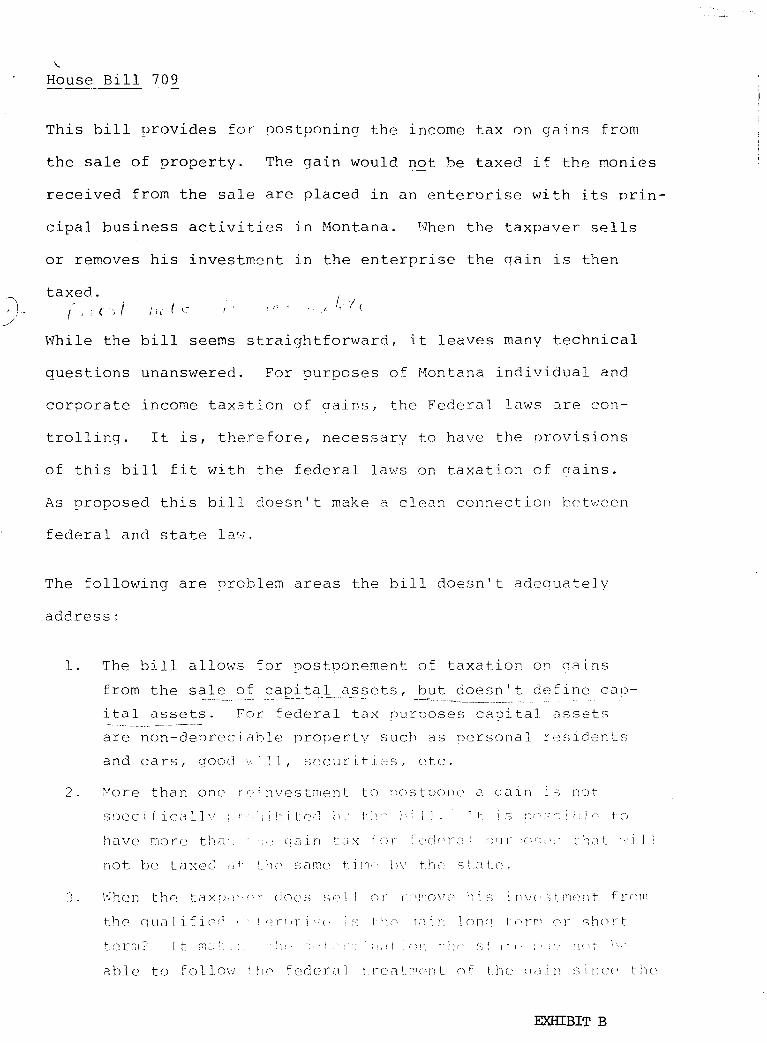

DAN BUCKS, Deputy Director of the Department of Revenue, explained while the bill seems straightforward, it leaves many technical questions unanswered. For purposes of Montana individual and corporate income taxation of gains, the federal laws are controlling. It is, therefore, necessary to have the provisions of this bill fit with the federal laws on taxation of gains. This ProFOsed bill doesn I t make a clean connection between federal and state law. He explained the six problems that the bill does not adequately address. See Exhibit B.

QiAIRMAN VINCENT asked if there were no further OpFOnents, would Representative Nordtvedt care to close.

REPRESENTATIVE NORDTVEDT stated he had intended to change the definition of the qualifying capital investments, because he believes 99% of the objections stated is to restrict this to equities. He felt this solves the difficulties with tracking with the dividend, etc. This is entirely different than an investment credit because this does not delay the payment of any taxes unless an act takes place. Unless a taxpayer roves an investment from out of state into the state, there is no benefit. He hoped to address same of the questions in rore detail later.

Page 2

CHAIRMAL~ VINCENT stated they would close the hearing on HB 709 and open the hearing on SB 316.

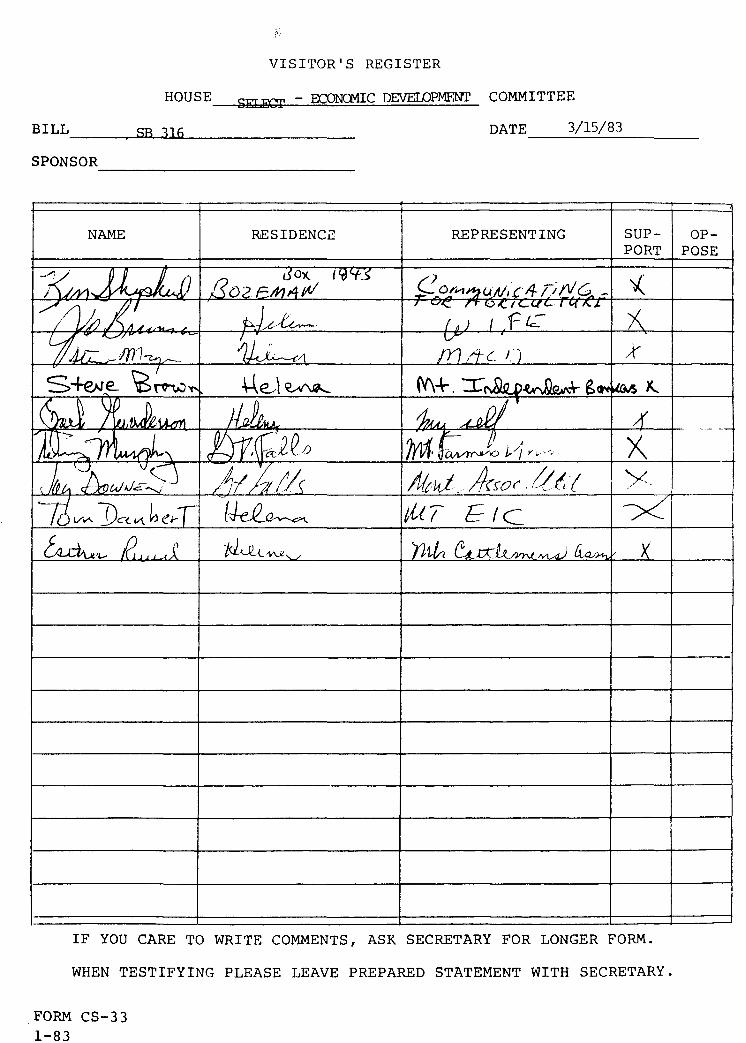

SENATOR TaVE, Sp:msor, explained this bill is the beginning farrrer IS

bill. He felt one of the areas that could have been rrore emphasized relating to the other bills before the committee is agriculture. He explained the mechanics of how SB 316 works. He commented this bill is patterned after the Iowa program that has been in operation for about 14 rronths. It is a bonding principal. There is CL"1 agriculture authority established and the agriculture authority then approves the sale of ronds. He stressed it works on a unique principal that is extrerrBly simple. His example explained a young farmer who wanted to rorraw $31,000 to build a pole bam. He went to the local bank, and the bank approved the loan for credit. The risk is with the bank, the state is not involved. The bank after approving the loan sent it up to the Iowa Agriculture Authori ty for their approval. After their approval, the loan is then sold at a bond for $31,000 to the sane bank. The bank buys the rond for that arrount, makes the rroney available which is then loaned to the farrrer. He explained that the bank in effect, has taken the agriculture loan out of the agriculture loan portifolio, and rroved it over to its municipal bond portifolio. When this happens two very important things happen. First the interest rate is substantially less. Secondly, not only is the interest lower, but the terms of the loan can be dealt with. He further explained the variable interest rate. He stated there are restrictions in the bill regarding who qualifies. He wanted to further explain the second provision to t~e bill that he felt was also very important.

This provision provides for a credit for retiring farmers who want to sell to a beginning farmer for less than 9%. All of the interest income or capital gains that would be received from that contract will be tax free from the Montana Individual Income Tax up to a maximum of $50,000. He felt this incentive might be enough to sell to a M:mtana individual rather than an out of state corporation. He asked the corrmittee to review Exhibit C, the StaterrBnt of Intent, and Exhibit D, a letter from Kenneth Siroky, Roy, M::mtana.

PROPONENTS

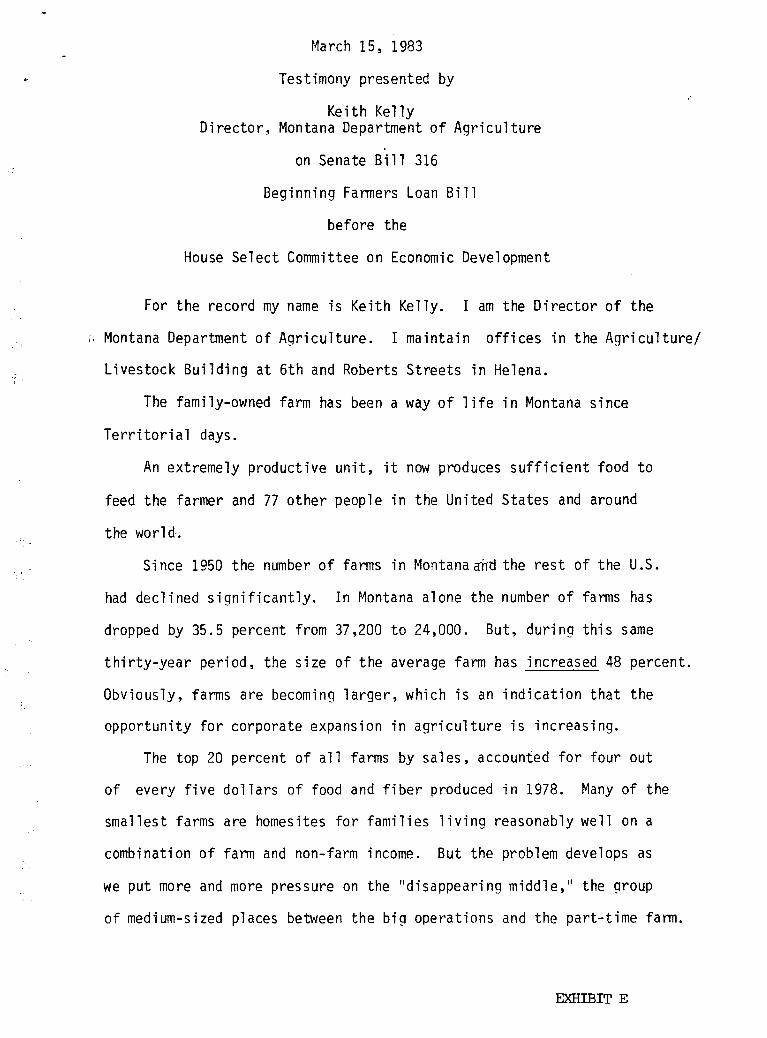

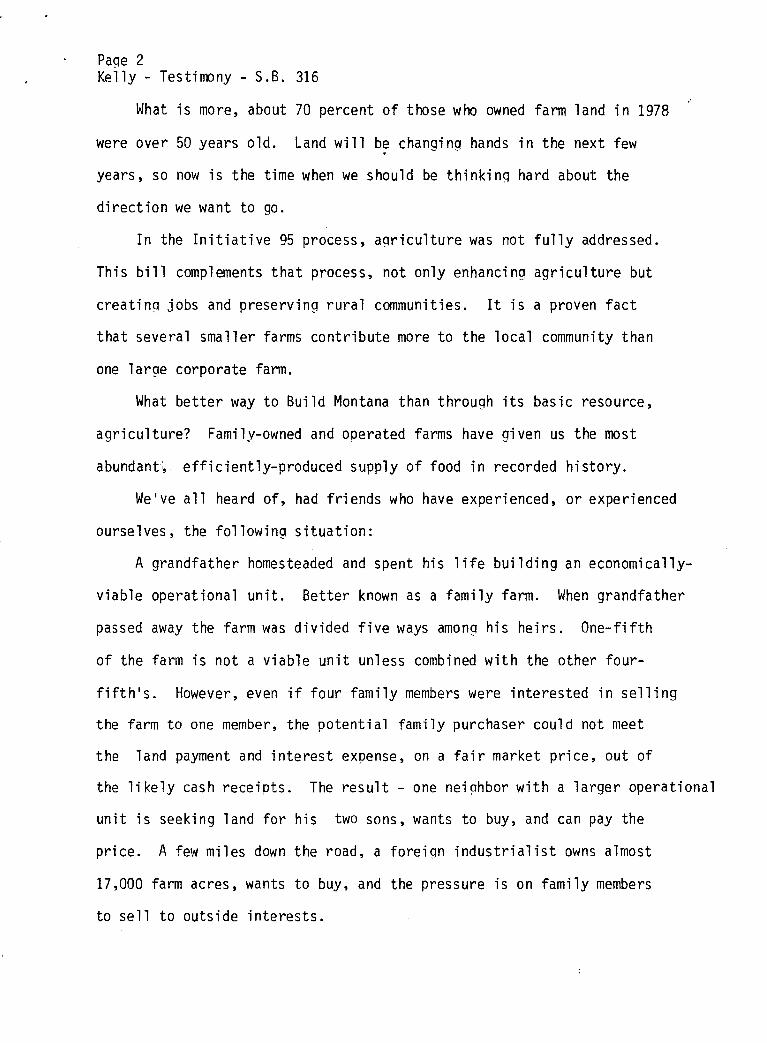

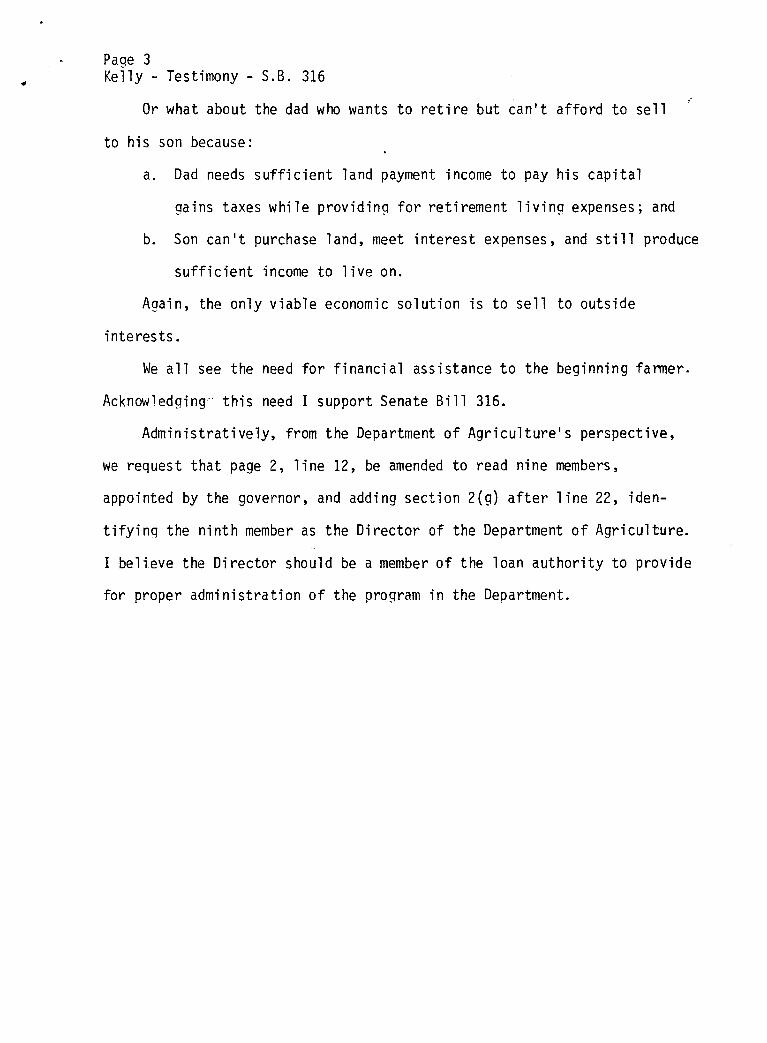

JACK GUNDERSON, Depart:rrent of Agriculture, stated their support of SB 316. He stated since 1950 the number of young fanns in M::>ntana and the rest of the U.S. has declined significantly. In M:>ntana alone, the number of farms has dropped by 35.5 percent fram 37,200 to 24,000, but during this sane thirty-year period, the size of the average farm has increased 48 percent. Obviously, fanns are becoming larger, which is an indication that the opportunity for corporate expansion in agriculture is increasing. He asked the comni ttee to review the testirrony fran Keith Kelly, Director of Montana Department of Agriculture for further oorrments. See Exhibit E. He asked the comnittee to tum to Exhibit E, page 3, regarding their one amendment to read nine members, appointed by the governor, and adding section 2(g) identifying the ninth member as the Director of the Department of Agriculture. He further stated he felt the last part of the bill was the most important.

Page 3

TERRY MURPHY, President of Famer' s Union, stated they have worked for a number of years for this type of bill and SB 316 is the most straightforward. He noted there is no fiscal impact on the state, it involves no state appropriation and will be self-supporting administratively.

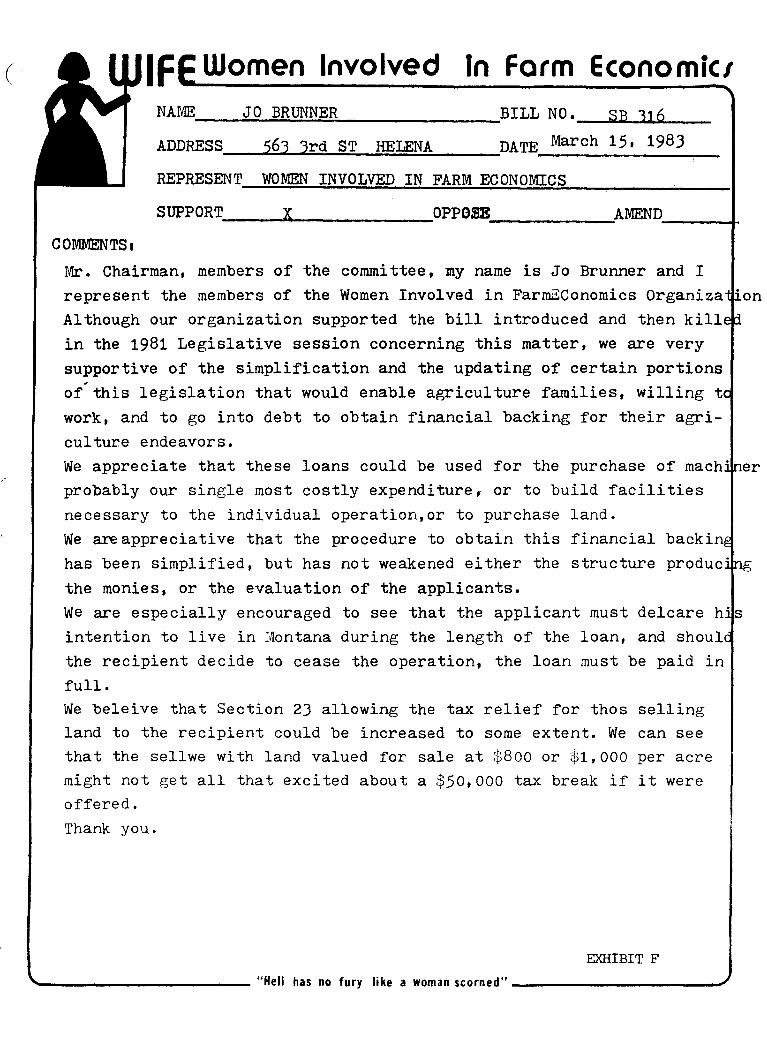

JO BRUNNER, Representing ~~ Involved in Farm Economics, stated their supp:Jrt of SB 316. She explained their organization supported the bill introduced by the '81 legislative session, and are very supp:Jrtive of the simplification and updating of certain portions to this bill. They appreciate that these loans could be used for the purchase of machinery, to build facilities, or to purchase land. They are especially encouraged to see the applicant must declare his intention to live in M:)ntana during the length of the loan. They believe that Section 23 allowing the tax relief for tmse selling land to the recipient could be increased, because they feel the $50,000 tax break might not be enough. See Exhibit F for further cormrents.

ESTHER RUEL, Representing M:)ntana Cattleman's Association, stated their support of SB 316. She noted she drove over 300 miles to testify for this bill tonight. She feels it is time that a bill such as this be supported.

STEVE MYER, Representing ~1Jntana Association of Conservation Districts, stated their sUpp:Jrt for SB 316.

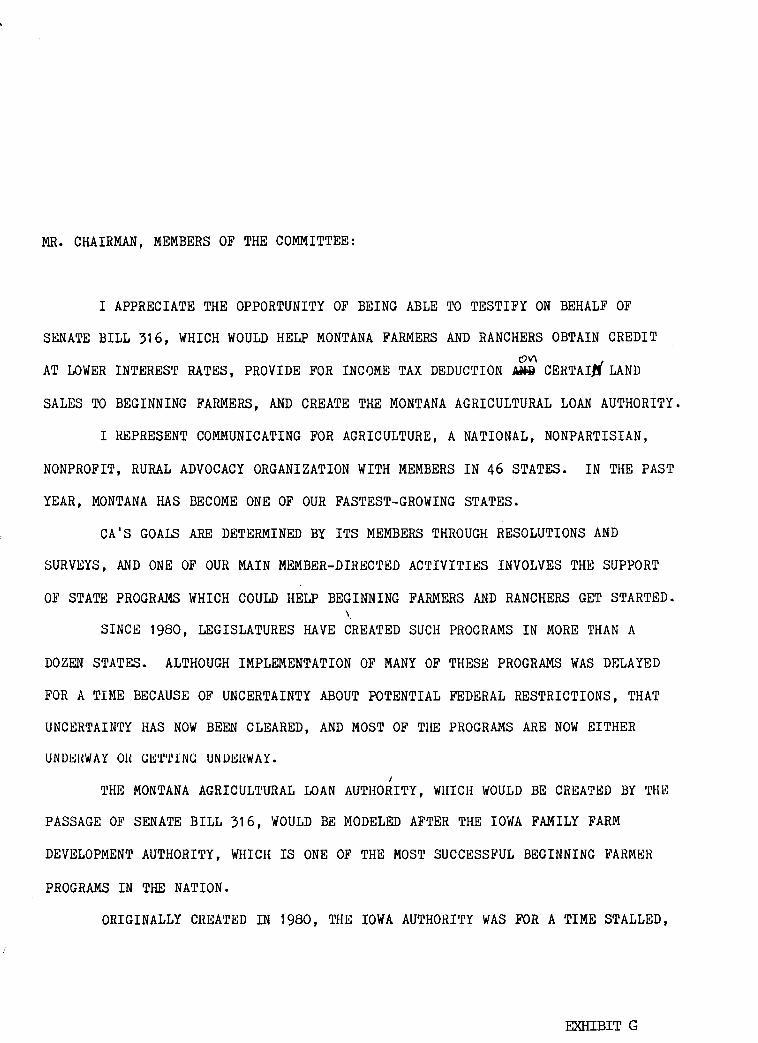

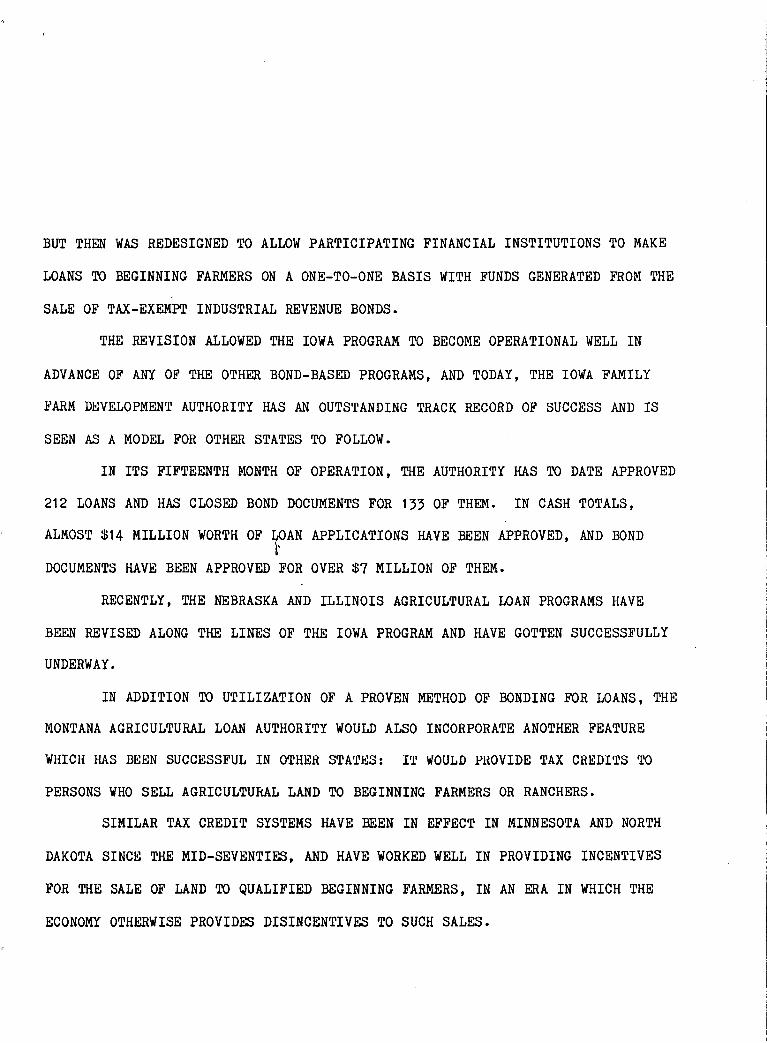

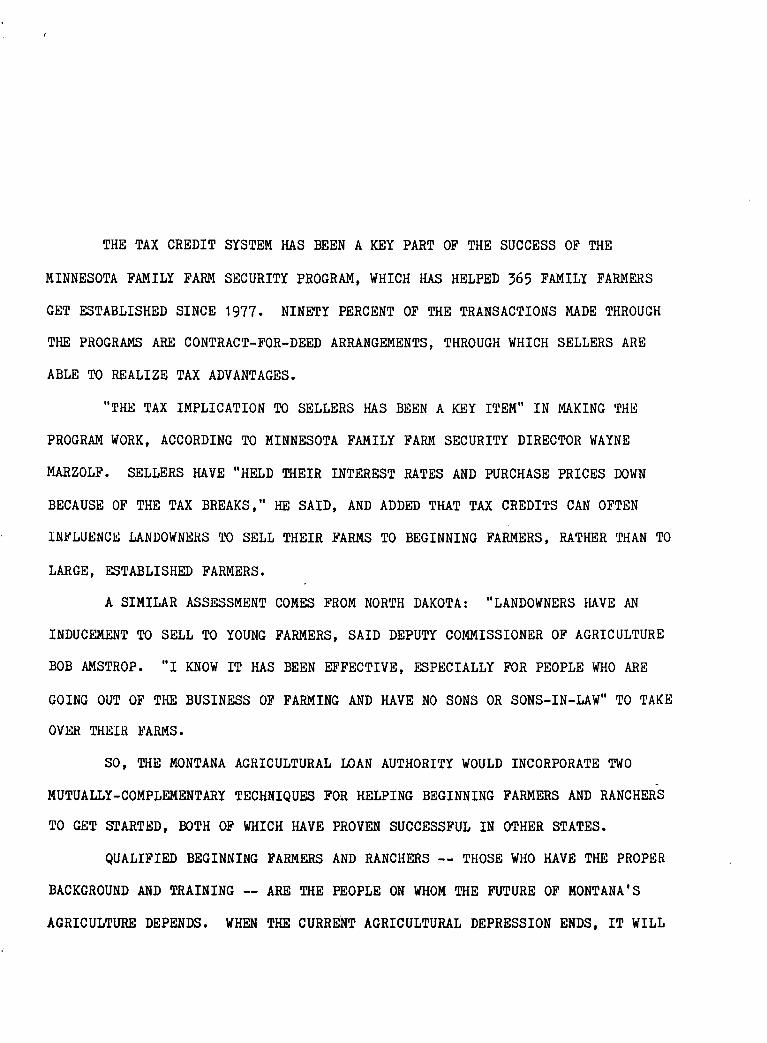

KEN SHEPHERD, Representing Corrmunicating for Agriculture, stated their sUPp:Jrt for SB 316. He asked the Comrrrrttee to review his testimony, see Exhibit G. He surmnarized one of t.~e rrost important items, is if we do not provide ways through which qualified beginning farmers and ranchers can successfully get started, we stand in danger of seeing our agricultural land acquired by large, nonagricultural corporations. These entities usually do not support local cammunities and businesses upon which the economy and vitality of the state depends, and they often abuse the land, rather than practice good conservation techniques. We urge you to approve SB 316 for the good of tbntana, and for the good of its agriculture and the good of its young people.

JAY ~l, Representing M:)ntana Association of Utilities, feels this bill is exceptionally well drafted. They feel they could sell the same amount of kilowatt and telephone service to corporate interests, but they feel they owe a greater debt to the famers of M:)ntana, and they support t..l-J.is bill.

KEN KELLY, !.vbntana Dairyrren' s Association, stated they fully support this bill and urge the Corrmittee a 00 PASS on it.

Page 4

'Ia1 DAUBERI', Representing .r.bntana Environrrental Information Center, rose in support of SB 316.

JIM TPLNDY, Red Lodge, stated he is currently ranching and his family goes back to 1864. He stated they are in trouble and something needs to be done right away aOOut the little man. If the corporation comes in or the governrrent gets involved the prices will be very high. He stated how difficult it was to compete with the outside interest from F~t, etc. He stated they are willing to work with the $226 that the average farmer made last year, but they are slowly running out of tirre.

IARRY LELIa), Carbon County, stated in the area where he lives, in a 13 mile radius, there are 37 ranchers ana only 7 of these are under 30. He feels this bill will help the young rancher get started.

STEVE BRa~J, Representing Montana Independent Bankers ~ssociation, stated they fully support SB 316.

SENATOR 'lavE stated others in the house that supported this hill were SENATOR SEVERSON, REPRESENI'ATIVE TED NEUMAN, and Fred Brown, from N.F.O.

CHAIRMAN VINCENT stated since there were no further Proponents to SB 316, were there any Opponents. Being no Opponents, were there any questions from the committee.

SENATOR TaVE closed by stating the dedication of the witnesses show their dedication to this bill. He commented he would support the amendrrent proposed by Keith Kelley, and also he had no objection to restricting this to Montana residents. He wanted it noted that the banks of Iowa like this bill because it converts a loan from sorreone they know to a municipal bond loan, which is tax free for them. He explained this is not a panacea for beginning farmers, but is a small step to help them.

CHAIRMAN VINCENT stated they would close the hearing on SB 316, and open the hearing on HB 865.

REPRESENTATIVE FABREGA stated he was asked by Representative Fagg to introduce this bill, since he was not able to make it this evening. He explained that HB 865 is rreant to encourage new jobs in rv'bntana. He further explained the mechanics of the bill and the three incentives involved with the options of this bill.

PROPONENTS

DAVE C£SS, Representing Billings Chamber of Oommerce, expressed support for HB 865. He feels this bill is important because jobs have to be created in the local oommunity.

Page 5

OPPONENTS

DAN BUCKS, Department of Revenue, stated they have several administrative problems with this bill and most problems arise from Section 1 and Section 3. One problem is when a business shuts down in one part of the state and starts up in another credit is still being claimed. Also there is no definition of what a permanent full time position is in Montana or a new or expanding business is not defined. He stated there is another wage credit bill, SB 241, and these SaID2 problems were discussed in the Senate Taxation comnittee and arrendrrents were made to take care of some of these problems. His depar1::ment would pro[X)se that SB 241 is relevent to discussion here to provide for a limit of credit for $800 and be sunset after 2 years, so that data could be collected to determine what the fiscal effects are, and if these incentives really work or not to achieve the intended purpose.

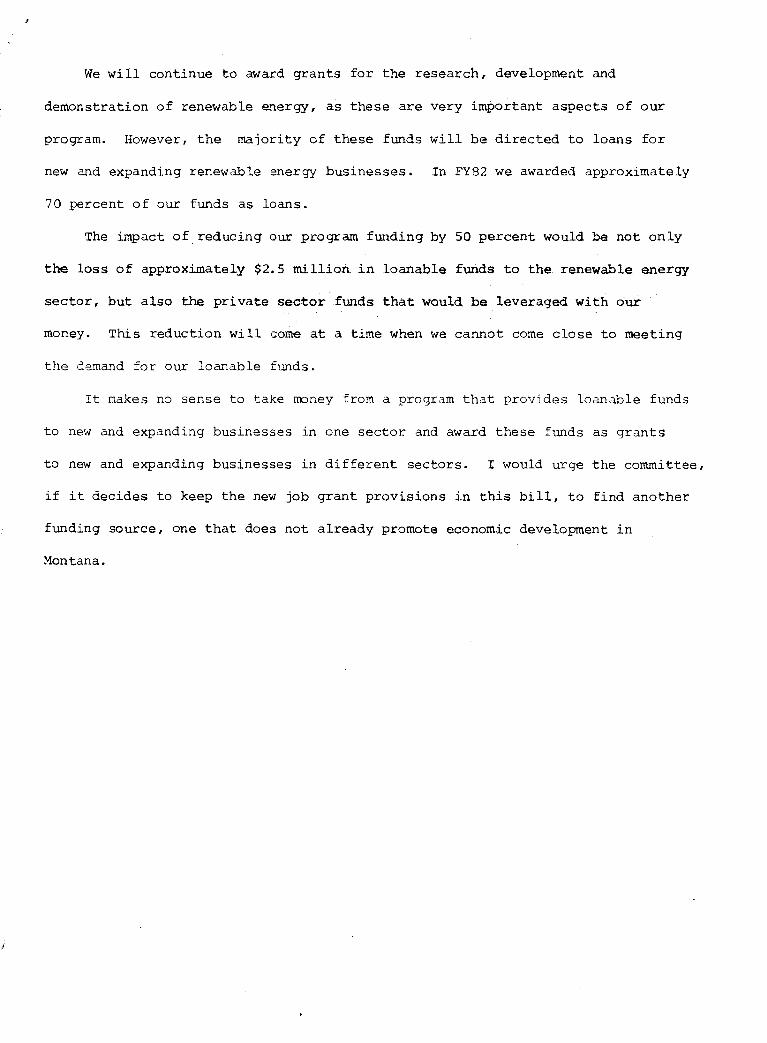

LEO BERRY, Director of the Department of Natural Resources and Conservation. He stated the department is not opposed to the concept of HB 865, but are opposed to the provision that takes one-half of the funds from the Al ternati ve Renewable Energy Sources Program and allocates t..'em to the Department of Cbmmerce for grants to businesses that create new jobs. See Exhibit H for further comments. He summarized that G,e impact of reducing our program funding by 50 percent v.Duld be not only the loss of approximately $2.5 million in loanable funds to the renewable energy sector, but also the private sector funds that \-Duld be leveraged with our money. This reduction will came at a time when we cannot come close to meeting the demand for our loanable funds.

JAMES MCNAIRY, Aero Alternative Energy Resources Organization, stated they also do not like the source of funds for the grant portion of HB 865. They agree with Mr. Berry I s reasons. They have problems concerning t.~e tax credi t portion of the bill. All businesses operating in Montana v.Duld be better off if markets existed to sell their products than tax credits existing for them to go into business. There is also no targeting set up for who gets the money. Also there is no carry over provision in the grant portion of this proposal. They find a problem with this, and a firm may not be able to take advantage of the grants.

REPRESENI'ATIVE FABRffiA closed by stating maybe the conmi ttee Vv'Ould like to ask Representative Fagg questions regarding the testimony given by the Opponents.

The meeting adjourned at 11:18 p.m.

{;Ji~i-Rfta!~ MIte ver Secretary

RESENTATIVE JOHN VIN::Et.:rr CHAIRMAN

VISITOR'S REGISTER

HOUSE SELECI' ECONaITC DEVELOPMENT. COMMITTEE

BILL ----------------------------lIB 865 DATE ____ 3/_J_5_1_83 ________ _

SPONSOR ---------------------------

NAME RESIDENCL REPRESENTING SUP- OP-PORT POSE

Be+ _W\~CX\ ~\\\;,,\'ll) ~~G 1'1rllK~ tmJQU V /~~~~;. it5::1P'

, ~~ {1~(;)/(/~~~' y

..0 <""

Q r; T

.. - -

- ". ---..

-

IF YOU CARE TO WRITE COr~ENTS, ASK SECRETARY FOR LONGER FORM.

WHEN TESTIFYING PLEASE LEAVE PREPARED STATEMENT WITH SECRETARY.

FORM CS-33 , n ...

VISITOR'S REGISTER

HOUSE SELOCT - ECCNMrC l)E:VELOPHENI' COMMITTEE

BILL HB 709 DATE 3/15/83 ------------------------------

SPONSOR --------------------------

NAME RESIDENC.2 REPRESENTING SUP-PORT

--IF YOU CARE TO WRITE COMMENTS, ASK SECRETARY FOR LONGER FORM.

WHEN TESTIFYING PLEASE LEAVE PREPARED STATEMENT WITH SECRETARY.

FORM CS-33 1-83

----..,

OP-POSE

--- --

I

VISITOR'S REGISTER

HOUSE £WECr - .ECON(lvUC DEVELOPMFNI' COMMITTEE

BILL ____ ~S~B~31~6 ______________ _ DATE 3/15/83 ----'----------SPONSOR -----------------------

NAME RESIDENCi:: REPRESENTING SUP- OPPORT POSE

v m A.. /'.

LLL.l

IF YOU CARE TO WRITE COr4MENTS, ASK SECRETARY FOR LONGER FORM.

WHEN TESTIFYING PLEASE LEAVE PREPARED STATEMENT WITH SECRETARY .

. FORM CS-33 1-83

.. ---

'< '<

48

th

leq

is1

3tu

re

lC

08

11

/01

1 ~~~_ NO

. _1.

~fd.

----------------

2 IN

TR

OH

CE

D

BY

3 4 A

BIL

L

FOR

A

N

AC

T E

NT

ITL

ED

: "A

N

AC

T A

LLO

WIN

G

FOR

TH

E

5 N

ON

RE

CO

GN

ITIO

N

OF

CA

PIT

_L

GA

IN

WH

EN

PRO

CE

ED

S O

F SA

LE

O

R

6 EXCHA~GE

AR

E IN

VE

ST

ED

IN

A

MO

NTA

NA

E

NT

ER

PR

ISE

; A

LLO

WIN

G

FOR

7 TH

E TA

X

ON

TH

E G

AIN

A

T A

LA

TER

D

AT

E;

AM

END

ING

S

EC

TIO

NS

8 1

5-3

0-1

11

A

ND

1

5-3

1-1

13

, M

CA

; A

ND

PR

OV

IDIN

G

AN

IM

ME

DIA

TE

9 E

FF

EC

TIV

E

DA

TE

AN

D

AN

AP

PL

ICA

BIL

ITY

D

AT

E.-

10

11

B

E IT

E

NA

CT

ED

SY

TH

E L

EG

ISL

AT

UR

E

OF

THE

STA

TE

O

F M

ON

TAN

A:

12

S

2cti

on

1

. S

ecti

on

1

5-3

0-1

11

, M

CA

, is

am

end

ed to

re

ad

:

13

"1

5-3

0-1

11

. A

dju

sted

q

ross

in

com

e.

(1) Adju~~e6 ~~eQ~

14

~ __

~la~igeg __

iu_subse~1LQo_ills-aQjus~d

gro

ss

inco

me

sh

all

15

b

e th~

tax

pay

er'

s

fed

era

l in

com

e ta

x

ad

juste

d

gro

ss

inco

me

16

as

defi

ned

in

secti

on

6

2 o

f th

e

Inte

rnal

Rev

enu

e C

od

e o

f

17

1

95

4 ,r

as

that

secti

on

m

ay

be

lab

ele

d

or

amen

ded

an

d

in

1'3

ad

dit

ion

sh

all

in

clu

de

the

foll

o"in

q:

19

(a

) in

tere

st

receiv

ed

o

n

ob

lig

ati

on

s

of

an

oth

er

sta

te

20

o

r te

rrit

ory

o

r co

un

ty,

mu

nic

ipali

ty,

dis

tric

t,

or

oth

er

21

p

oli

tical

SU

bd

ivis

ion

th

ere

of;

zz

(t»

re

fun

ds

receiv

ed

o

f fe

dera

l in

com

e ta

x.

to th

e

23

ex

ten

t th

e

ded

ucti

on

o

f su

ch

ta

x

resu

lted

in

a

red

ucti

on

o

f

24

~ontana

inco

me

tax

liabi1ity~

2"

L~1 __

~be-_ggln __

QO

__

1be _

_ sal2-_aL_exkbange_Qf-a_~an~1

1 2 3 4 5 6 7 8 9

10

11

12

13

14

15

16

11

18

19

20

21

22

23

24

25

LC

08

11

/01

asset_a~kludeg_fLQm_adjYsteg~LQSs-iakQ.2-_undeC __

su~~~a

illLal_~ben_Qae_Qf_1b2-e~eats-geskLlbeg_iD_SubsektiQD-LllLQ1

QkkUL5_QUCiDQ-tbe_taxgble-~eaL.

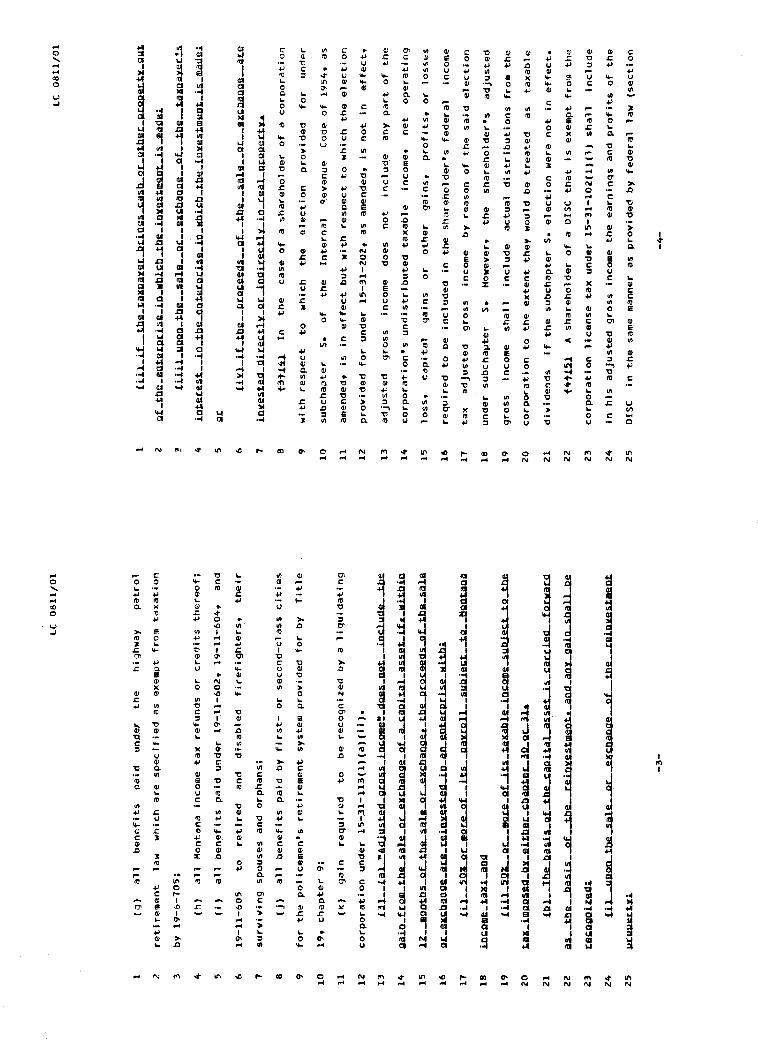

(2

)

No

twit

hst

an

din

g

the

pro

vis

ion

s

of

the

fed

era

l

Inte

rnal

Rev

enu

e C

od

e o

f 1

95

4

as

lab

ele

d

or

am

en

ded

,

ad

juste

d

gro

ss

inco

me

do

es

no

t in

clu

de th

e

foll

ow

ing

w

hic

h

are

ex

em

pt

fro

m

tax

ati

on

u

nd

er

this

ch

ap

ter:

(a)

all

in

tere

st

inco

me

fro

m o

bli

gati

on

s o

f th

e

Un

ited

Sta

tes

qo

vern

'1le

nt,

th

e

sta

te

of

Mo

nta

na,

co

un

ty,

mu

nic

i;>

a1

ity

, d

istr

ict,

o

r o

ther

po

liti

cal

su

hd

ivis

ion

there

e>

f;

(b)

inte

rest

inco

me

earn

ed

b

y

a ta

xp

ay

er

ag

e

65

o

r

old

er

In

a ta

xab

le

vear

up

to

an

d

inclu

din

g

$6

00

fo

r a

tax

pav

er

fili

ng

a

sep

ara

te

retu

rn

an

d

$1

,60

0

for

each

jo

int

retu

rn; (e)

all

b

en

efi

ts

receiv

ed

u

nd

er

the

Fed

era

l E

mp

loy

ees'

Reti

ram

en

t A

ct

no

t in

ex

cess

o

f $

3,6

00

;

(d)

all

b

en

efi

ts,

no

t in

ex

cess

o

f $

36

0,

receiv

ed

as

an

an

nu

ity

, p

en

sio

n,

or

en

d,w

men

t u

nrt

er

any

p

riv

ate

o

r

co

rpo

rate

re

tire

men

t p

lan

o

r sy

stem

;

Ie)

all

b

en

efi

ts

paid

u

nd

er

the te

ach

ers

' re

tire

men

t

la~ w~ich

are

sp

ecif

ied

as

ex

em

pt

fro

m ta

xati

on

b

y

19

-4-7

06

;

(f)

all

b

en

efi

ts

paid

u

nd

er

Th

e P

ub

lic

~mp1oyees'

Ret

i re

,nen

t S

yst

em

Act

w

h I c

h

are

sp

ec i

f i e

d

as

ex

em

pt

fro

m

tax

ati

on

b

y

19

-3-1

05

;

-2-

I N

T R

OD

U C

E D

B

IL

L

i·

Ie-

-; /j

~-l

/

'"

1 l 3 It

5 6 7 8 9 10

11

12

13

lit

15

16

17

18

19

20

21

22

23

24

25

LC

081.

.1/0

1

(g

)

all

b

en

efi

ts

paid

u

nd

er

the

hig

hw

ay

patr

ol

reti

rem

en

t la

w

wh

ich

are

sp

ecif

ied

as

exem~t

fro

m

tax

ati

on

by

1

9-6

-70

5;

(h)

all

M

on

tan

a in

com

e ta

x

refu

nd

s o

r cre

dit

s

there

of;

(i)

all

b

en

efi

ts

paid

u

nd

er

19

-11

-60

2.

19

-11

-60

4.

and

19

-11

-60

5

to

reti

red

an

d

dis

ab

led

fi

refi

gh

ters

. th

eir

su

rviv

ing

sp

ou

ses

and

o

rph

an

s;

(j)

all

b

en

efi

ts

paid

b

y fir

st-

or secc~d-class cit

ies

for

the

po

licem

en

's

reti

rem

en

t sy

stem

p

rov

ided

fo

r b

y

Tit

le

19

. c!t

ap

ter

9;

(k)

gain

re

qu

ired

to

b

e

reco

gn

ized

by

a

liq

uid

ati

ng

co

rpo

rati

on

u

nd

er

15

-31

-11

3(1

)(a)(

il).

Lll

__ La~Agju~~g_gLQ~_i~me~_~~_QQt-_ln~Ug~

gaiD_fCQu_tba-~ale_~ea~baage_af_a-~i~al_a~~t-if£_¥itbiD

lZ __

.gDtn~_Df-tbe-~aLA~c-ax~ang~_tbe_QLQ~ee~~f-~~le

Qc_e~baQge_ace_ceinx~ted_iD_4D-ent~QL~_wltbl

Lil

__ ~Q

I_gc_mgLe-a! _

_ it~_RaXLall __

~u~le~t_-tu--HgntaDa

iD~DIle._Ual~QI1

Lill_~Ql-_QC __

mQLe_Df-i~_taaable-iD~gme~ubl~tg-1be

ta~_imgD~eg_Qx_eitbec_~b~lQ_gC-lla

Lb

l __ lbe-ba5i~_af_tbe_~auiU1-a~~et-i~_~accie~_fQLwacg

U _

_ tbe._-ba!lU_-a!_-tbL-LelDl£ellmeob-ADg_auX-lJai~all~

Le~DgQi~ed.i.

Lil--"RlHL.tbe_~L~_~IS~nge_Qf_tbe._alD~meDt.

"t:lWect.~ ...

-3

-

1 2 ? 4 5 6 7 8 9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

LC

08

11

/01

Liil-if_tbe_t.aXQaxet:_bt:iDg~_~~D-gt:_gtbet:_RL2ReL~gut

gf_tbe._e.Qt.et:QLi~e_iQ-wbl~b_t.be_io~~t.meot-i~-mgdel

Lilil-"QQQ_1be_~ale __

DC __

e&~baQge __

DL _

_ t.be._Uaga~et:!~

iDt.

e.t:

e.~t

. __

iQ-1be_eDtet:QCue_io_.nl~b_t.be_lo~e.~t.meDt._i!l_madel

gt:

Lix

l_if

_t.b

e. __

Qt:~ee.d~ __

gf _

_ t.b

e __ ~ale __

gt: _

_ e&~baOQe_at:e

iDxe~t.e.d_dit:~tlx_gc-iQdlt:e~t.lx_iD_t:eal_gt:gge.ct.x.

t3tL

il

In

the

case

o

f a

share

ho

lder

of

a co

rpo

rati

on

wit

h

resp

ect

to

wh

ich

th

e

ele

cti

on

p

rov

ided

fo

r u

nd

er

sub

ch

ap

ter

S.

of

the

Inte

rnal

~evenue

Co

ae

of

19

54

. as

amen

ded

. is

in

eff

ect

bu

t w

ith

re

sp

ect

to

wh

ich

th

e ele

cti

on

pro

vid

ed

fo

r u

nd

er

15

-31

-20

2.

as

~mended,

is

no

t in

eff

ect.

ad

juste

d

gro

ss

inco

me

do

es

no

t in

clu

de

any

p

art

o

f th

e

co

rpo

rati

on

's u

nd

istr

ibu

ted

ta

xab

le

Inco

me.

n

et

op

era

tin

g

loss.

cap

ital

gain

s o

r o

ther

gain

s.

pro

fits

. o

r lo

sses

req

uir

ed

to

b

e in

clU

ded

in

th

e

sh

are

ho

lder'

s

fed

era

l in

com

e

tax

ad

juste

d

gro

ss

inco

me

by

re

aso

n

of

the

said

ele

cti

on

un

der

sub

ch

ap

ter

S.

Ho

wev

er.

the

sh

are

ho

lder'

s

ad

juste

d

gro

ss

inco

me

sh

all

in

clu

de

actu

al

dis

trib

uti

on

s

fro

m

the

co

rpo

rati

on

to

th

e ex

ten

t th

e V

w

ou

ld

be

treate

d

as

tax

ab

le

div

iden

ds

If th

e

sub

ch

ap

ter

S.

ele

cti

on

w

ere

no

t in

eff

ect.

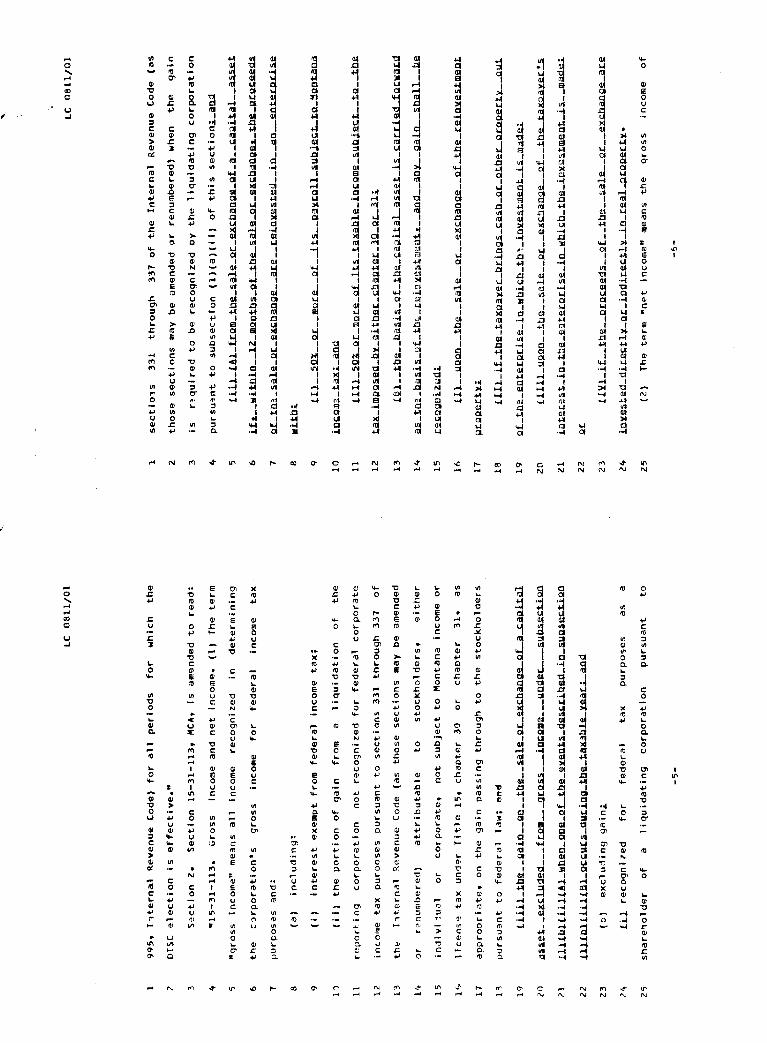

t~tL~l

A s

hare

ho

lder

of

a D

ISC

th

at

is

exem

pt fro~ th~

co

rpo

rati

on

li

cen

se ta

x u

nd

er

15

-31

-10

2(1

)(1

) sh

all

in

clU

de

in h

is

ad

juste

d

gro

ss

inco

me

the earn

ing

s an

d p

rofi

ts

of

the

DIS

C

in th

e

sam

e m

ann

er

as

pro

vid

ed

b

y fe

dera

l la

w

(secti

on

-4-

1 7 3 4 5 b 1 B

9 ID

11

12

13

1'.

15

1&

11

1~

19

2D

21

22

23

24

25

LC

08

11

/01

99

5,

r,t

ern

al

Rev

en

ue

Co

de)

for

all

p

eri

od

s

for

wh

ich

th

e

D!S

C ~lection

is effecti

ve."

Secti

on

2

. S

ecti

on

1

5-3

1-1

13

, M

CA

, is

a~ended to

re

ad

:

"1

5-3

1-1

13

. G

ross

in

com

e an

d n

et

inco

me.

(1)

Th

e te

rm

"g

ross

inco

me"

mean

s all

in

co

me

reco

gn

ized

in

d

ete

rmin

ing

the

~3rporation's

gro

ss

inco

me

for

fed

era

l in

co

me

tax

pu

rpo

ses

an

d:

(a)

inclu

din

g:

(i)

in

terest

ex

em

pt

fro

m

fed

era

l in

co

me ta

x;

(i i

) th

e p

ort

ion

o

f g

ain

fr

om

a

liq

uid

ati

on

o

f th

e

rep

ort

ing

co

rpo

rati

on

n

ot

reco

gn

ized

fo

r fe

dera

l co

rpo

rate

inco

me

tax

p

urp

oses

pu

rsu

an

t to

secti

on

s

33

1

thro

ug

h

33

1

of

the

Ilt

ern

al

Rev

en

ue

Co

de

{as

tho

se

secti

on

s

may

b

e

am

en

ded

or

r?n

um

bere

dj

att

rib

uta

ble

to

sto

ck

ho

lders

, eit

her

ind

ivi

jual

or

co

rpo

rate

, n

ot

su

bje

ct

to

Mo

nta

na

inco

me

or

licen

se ta

x und~r

Tit

le

15

, ch

ap

ter

30

o

r ch

ap

ter

31

, as

ap

pro

ori

ate

, o

n

the

gain

p

assin

g

thro

ug

h

to

the

sto

ck

ho

lders

pu

rsu

3n

t to

fe

dera

l la

w;

e~d

tiii

l_tb

a __

gai

D __

__ tb~ __

~ale_Qc_a~~baQ~_QI-a~aQLtgl

a~~et _

_ ~~~lUg~g _

__ tC

Qm

___

gCQ~ _

__ l~Qm~ _

__ u

ng

eC-_

_ ~uQse~tl2U

LIILbltlilLA1_~ben_gDe_Qt_tb~_~xeutS_ge~Libeg_1D-SUQs~tlQD

LllLblLlilL~l-QC~UC~-duciDg_tbe_ta~able_xeac&_aog

(b)

ex

clu

din

g

gain

&

Lil

re

co

gn

ized

fo

r fe

dera

l ta

x

pu

rpo

ses

as

a

share~older

of

a li

qu

idati

ng

co

rpo

rati

on

p

urs

uan

t to

-5-

1 2 3 4 5 6 1 B

9

10

11

12

13

14

15

16

11

18

19

20

21

22

23

24

25

" LC

08

11

/01

secti

o1

s

33

1

thro

ug

h

33

1

of

the

Inte

rnal

Rev

en

ue

Co

de

(as

tho

se

secti

on

s

may

b

e

am

en

ded

o

r re

nu

mb

ere

d)

wh

en

the

gain

is

r~quired

to

be

reco

gn

ized

b

y

the li

qu

idati

ng

co

rpo

rati

on

pursu~nt

to

su

bsecti

on

(l)

(a)(i

i)

of

this

section~_a~

Lill_LA1_tCQm_toe_~gle_Qc_eA~baD~_Qf_a _

_ ~a~ltal _

_ a~t

if£

__ w

itb

lD _

_ ll_mgDtb~_Qt_tbe_~gle_Qc_e~~bange£_tbe_~Q~eeQ~

Qt_tn~_~ale_Qc_e&kbaoge _

_ ~c

e _

_ ceiaxe~teg _

_ io

__

aa _

_ ~a~LQLi~

~itb~ L

!1 _

_ 22

1 __

Qc _

_ m

Qce

__

Qf_-1t~ _

_ ~a~£Qll-~ub!e~t-tQ-~QDtana

iD~gm~_t~~&_aag

Llll_221_QL_~QLe_Qf_lt~_ta~ble_iD~Qme_~~ble~t-_tQ_-the

ta~_imQQ~eg_bx_aitbec_~ba~tec_l2_Qc_lll

ial _

_ tb

e __

ba~i~_Qf_tbe_~a~ltal_a~~et_i~_~accl~fQc~aLQ

a~_to~_ba~i~_Qf_tb~_celQx~~tment£ _

_ aD

g __

an~ _

_ galD-_~ball _

_ ~

c~~QgDi~~g~

Lll

__ u

uan

__ tb

e __

~ale _

_ Q

c __ e~~baDge _

_ Qf_tbe_£eln~e~meot

~cQue[t~&

Llll~if_tbe_ta~uateL-b£log~-~a~b-QL-Qtbec-QLQ~ctt-~ut

gf_tba_eDteLucl~e_lo_~bl~b_tb~_iDxe~tment_i~_mag~

Lll

ll_

uQ

Qo

__ tb

e _

_ ~ale _

_ Q

c __

ex~baDge--Qf _

_ tbe_ta~atac!~

lotec~~t_1D_tbe_eutecnLi~e_in_~bi~b_tbe_iQ~e~tmeDt_1s__maa~

Q[

Ll~l_if _

_ tb

e __

QcQ~eos _

_ Q

f __ tb

e _

_ ~ale _

_ Qc _

_ ~khaQge~ce

iD~e~~ed_dice~tlt-Qc_1DdiLe~tlt-iD-£eal~cQ~eLtx·

(2)

Th

e tp

.rm

"n

pt

inco

me"

mea

ns

the

gro

ss

inco

me

of

-6

-

LC

08

11

/01

1 th

e

:~rporatlon

less

the

ded

ucti

on

s set

fort

h

in

15

-31

-11

4.

2 3

(3

)

1 i c

en

se

No

co

rpo

rati

on

tax

u

nle

ss

is

exem

pt

sp

ecif

icall

y

fro

m

the

co

rpo

rati

on

pro

vid

ed

fo

r u

nd

er

4 1

5-3

1-1

01

(3)

or

15

-31

-10

2.

Any

co

rpo

rati

on

n

ot

sUb

ject

to

or

5 li

ab

le

for

fed

era

l in

com

e ta

x

bu

t n

ot

exem

pt

fro

m

the

6 co

rpo

rati

on

li

cen

se

tax

u

nd

er

15

-31

-10

1(3

) o

r 1

5-3

1-1

02

7 sh

all

co

mp

ute

g

ross

inco

me

for

co

rpo

rati

on

li

cen

se

tax

~

purpos~s

in

the

sam

e m

ann

er

as

a co

rpo

rati

on

th

at

is

su

bje

ct

9 to

o

r li

ab

le

for

fed

era

l in

com

e ta

x

acco

rdin

g

to th

e

10

p

rov

isio

ns

for

dete

rmin

ing

g

ross

in

com

e in

th

e

fed

era

l

11

Inte

rnal

Rev

enu

e C

od

e in

eff

ect

for

the

tax

ab

le

year.

-

12

~f~_SftIlOti&

Secti

on

3

. E

ffecti

ve

date

13

ap

pli

cab

ilit

y d

ate

. T

his

act

is

eff

ecti

ve

on

p

ass

ag

e

and

14

ap

pro

val

and

ap

ol

ies

to

tax

ab

le

years

b

eg

inn

ing

aft

er

15

D

ecem

ber

3

1,

19

82

.

-En

d-

-7-

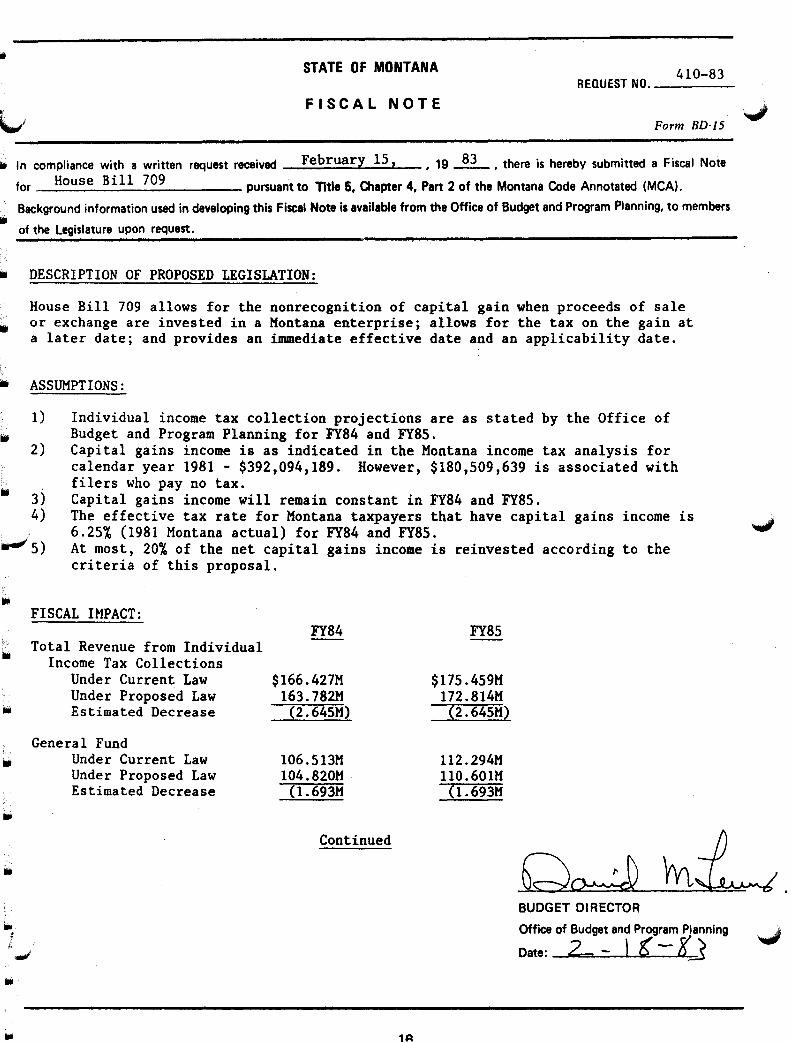

.. STATE OF MONTANA 410-83 REQUEST NO. ____ _

FISCAL NOTE Form BD·15

III In compliance with a written request received February 15, , 19 ~ , there is hereby submitted a Fiscal Note

.. III

..

III

iii

for House Bill 709 pursuant to Title 6, Olapter 4, Part 2 of the Montana Code Annotated (MCA). Background information used in developing this Fiscal Note is available from the Office of Budget and Program Planning, to members of the legislature upon request.

DESCRIPTION OF PROPOSED LEGISLATION:

House Bill 709 allows for the nonrecognition of capital gain when proceeds of sale or exchang~ are invested in a Montana enterprise; allows for the tax on the gain at a later date; and provides an immediate effective date and an applicability date.

ASSUMPTIONS:

1)

2)

3) 4)

Individual income tax collection projections are as stated by the Office of Budget and Program Planning for FY84 and FY85. Capital gains income is as indicated in the Montana income tax analysis for calendar year 1981 - $392,094,189. However, $180,509,639 is associated with filers who pay no tax. Capital gains income will remain constant in FY84 and FY85. The effective tax rate for Montana taxpayers that have capital gains income is ~

~·5) 6.25% (1981 Montana actual) for FY84 and FY85. At most, 20% of the net capital gains income is reinvested according to the criteria of this proposal.

lit

IiII

.. :

..

FISCAL IMPACT:

Total Revenue from Individual Income Tax Collections

Under Current Law Under Proposed Law Estimated Decrease

General Fund Under Current Law Under Proposed Law Estimated Decrease

FY84

$166.427M 163.782M

(2.645M)

106.513M 104.820M

(1.693M

Continued

1R

FY85

$175.459M 172.814M

(2.645M)

112.294M llO.601M

(l.693M

BUDGET DIRECTOR Office of Budget and Program Planning

Date: 2 - I t - 8'.J

2

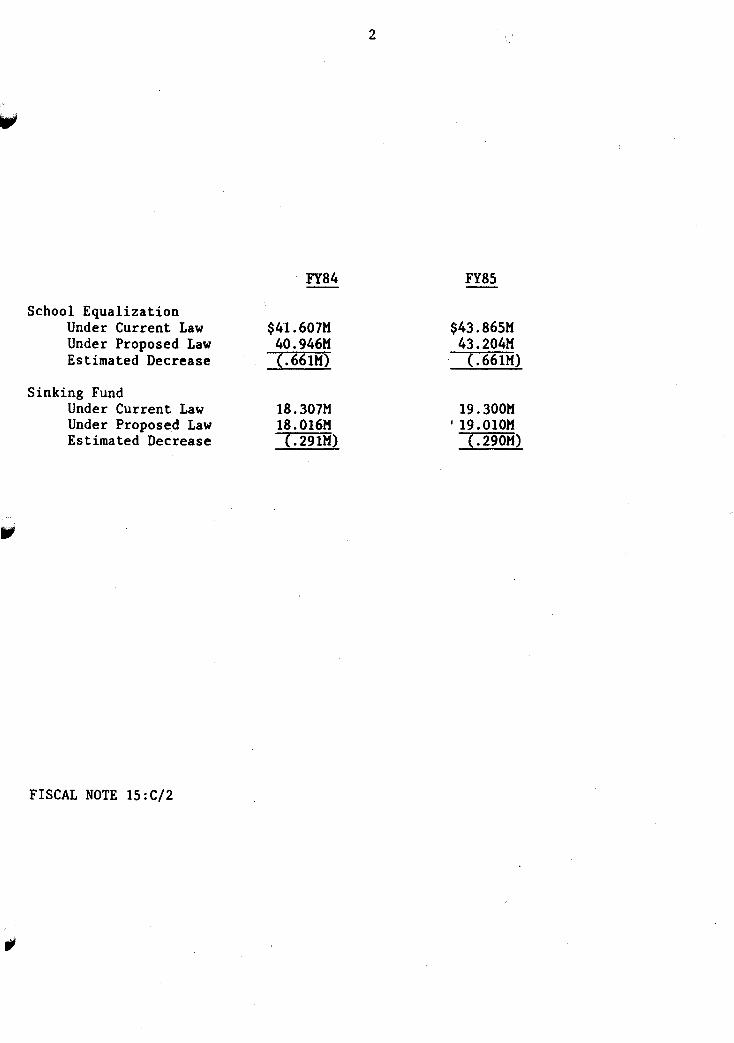

FY84 FY85

School Equalization Under Current Law $41.607M $43. 865M Under Proposed Law 40.946M 43.204M Estimated Decrease (.66IM) L661M)

Sinking Fund Under Current Law 18.307M 19.300M Under Proposed Law 18.016M I 19.010M Estimated Decrease (.29IM) (.290M)

FISCAL NOTE 15:C/2

,

48

th

Leq

lsla

ture

LC

lZ

53

/01

1 Z

3 It

5 6 1 8 9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

~

BY ~ -

BIL

L

NO

. J!

M

-------~------

--

INTR

OO

UC

ED

A B

ILL

FOR

AN

ACT

E

NT

ITL

ED

: -A

N

ACT

TO

STIM

ULA

TE

ECO

NO

MIC

DEV

ELO

PMEN

T IN

M

ONTA

NA

BY

PRO

VID

ING

EC

ON

OM

IC

INC

EN

TIV

ES

FOR

NEW

Oc

t EX

PAN

DIN

G

BU

SIN

ESS

ES

CR

EATI

NG

"'lE

W

J08

S

IN

ItON

lAN

A;

AM

END

I:IIG

SE

CTI

ON

1

5-3

5-1

08

, M

CA;

AND

PRO

VID

ING

AN

APP

LIC

AB

ILIT

Y

DA

TE

.-

BE

IT

ENA

CTED

BY

TH

E LE

GIS

LATU

RE

OF

THE

STA

TE

OF

MO

NTA

NA

:

MfW-SftIlD~a

Secti

on

1

. P

urp

ose

--

new

jo

b

defi

ned

.

(I)

Th

e p

urp

ose

o

f [s

ecti

on

s

1 th

rou

gh

7]

is

to

en

co

ura

ge

the cre

ati

on

o

f ne

w

job

s In

M

on

tan

a w

ith

ou

t ad

vers

ely

aff

ecti

ng

th

e sta

te's

re

ven

ues.

(Z)

Fo

r p

urp

ose

s o

f [s

ecti

on

s

1 th

rou

qh

1

J,

Mne

w

job

-

Mea

ns

a p

erm

an

en

t full-tl~

po

sit

ion

tn

M

on

tan

a th

at

was

n

ot

in ex

iste

nce

on

[t

he eff

ecti

ve d

ate

o

f th

is act]

an

d th

at

is

cre

ate

d

becau

se o

f a

new

o

r ex

pan

ded

b

usi

ness

.

~~W_SftIlO~a

Secti

on

2

. F

inan

cia

l In

cen

tiv

es

for

job

cre

ati

on

. A

n in

div

idu

al,

co

rpo

rati

on

, p

art

ners

hip

, o

r s.a

ll

bu

sin

ess

co

rpo

rati

on

, as

defi

ned

In

1

5-3

1-2

01

, th

at

sta

rts

a

new

b

usi

ness

o

r ex

pan

ds

an ex

isti

ng

b

usi

ness

m

ay

ch

oo

se

fro

m

the

foll

ow

ing

fi

nan

cia

l In

cen

tiv

es

for

cre

ati

ng

ne

w job~:

(1)

a ta

x cre

dit

as

pro

vid

ed

in

[s

ecti

on

3

];

(21

a

gra

nt

as

pro

vid

ed

in

fs

ectl

on

6

J;

or

1 2 3 4 5 6 7 8 9

10

11

12

n 14

1')

16

17

18

19

ZO

21

22

23

24

25

LC

lZ5

3/0

1

(3)

an

In

tere

st

pay

Men

t o

ffset

as

pro

vid

ed

In

[s

ecti

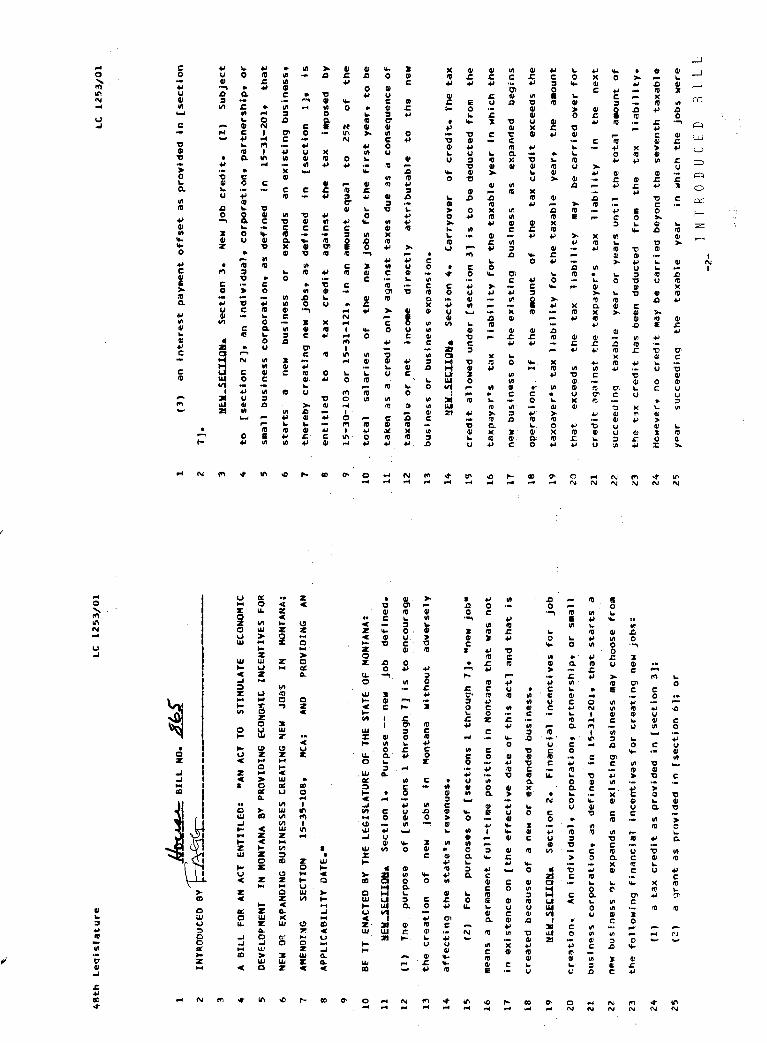

on

7].

~~W_SftIlQ~a

Secti

on

3

. N

ew

job

cre

dit

. (1

) S

ub

ject

to

[secti

on

2

],

an

Ind

ivid

ual.

co

rpo

rati

on

. p

art

ners

hip

. o

r

small

~uslness

co

rpo

rati

on

. as

defi

ned

In

1

5-3

1-2

01

. th

at

sta

rts

a ne

w

bu

sin

ess

o

r ex

pan

ds

an ex

isti

ng

b

usin

ess.

there

by

cr,

atl

ng

ne

w jo

bs,

as

defi

ned

In

[s

ecti

on

1

].

is

en

titl

ed

to

a

tax

cre

dit

ag

ain

st

the

tax

I.

po

sed

b

y

15

-30

-10

3 o

r 1

5-3

1-1

21

. in

an

am

ou

nt

eq

ual

to

Z5~

of

the

tota

l sala

ries

of

the

new

jo

bs

for

the fir

st

year.

to

b

e

tak

en

as

a cre

dit

o

nly

ag

ain

st

tax

es

du

e as

a co

nse

qu

en

ce o

f

tax

ab

le o

r n

et

Inco

.e

dir

ectl

y

att

rib

uta

ble

to

th

e

new

bu

sin

ess

o

r b

usi

ness

ex

pan

sio

n.

~~W_SftllDHa

Secti

on

4

. C

arr

yo

ver

of

cred

it.

Th

e ta

x

cre

dit

all

ow

ed

u

nd

er

[secti

on

3

] is

to

b

e d

ed

ucte

d

fro

m

the

tax

pay

er'

s

tax

li

ab

ilit

y fo

r th

e ta

xab

le

ye

ar

In

wh

ich

th

e

new

b

usi

ness

o

r th

e ex

isti

ng

b

usi

ness

as

ex

pan

ded

b

eg

ins

operation~_

If

the

a.o

un

t o

f th

e

tax

cre

dit

ex

ceed

s th

e

tax

oav

er"

s ta

x li

ab

ilit

y fo

r th

e ta

xab

le

year.

th

e

amo

un

t

that

exce~ds

the

tax

li

ab

ilit

y

may

b

e carr

ied

o

ver

for

cre

dit

ag

ain

st

the ta

xp

ay

er'

s

tax

li

ab

ilit

y

In

the

nex

t

succeed

ing

ta

xab

le

year

or

years

u

nti

l th

e to

tal

amo

un

t o

f

the

t3X

cre

dit

h

as

bee

n

ded

ucte

d

fro

m

the

tax

li

ab

ilit

y.

Ho

wev

er.

no

cre

dit

M

ay

be carr

ied

b

eyo

nd

th

e

sev

en

th ta

xab

le

year

succeed

inq

th

e

tax

ab

le

year

in

wh

ich

th

e

job

s w

ere

N T

RO

D U

C E

D

B I

LL

-2

-

1 2 3 • 5 6 7 8 9 10

11

12

13

14

15

16

11

18

19

20

21

22

23

24

25

lC

12

53

/01

cre"t.~d.

~EW_SEtIlQ~&

Secti

on

5

. E

xclu

sio

n

of

oth

e ...

tax

incen

tiv

es.

If

a ta

x

c ... e

dit

Is

cla

ille

d

un

de

... [s

ectl

.on

. 3

).

no

oth

e...

ta

x

c ... e

dit

m

ay

be

cla

imed

in

... e

lati

on

to

th

e

saM

e

job

-cre

ati

ng

b

usin

ess.

HfW_SEtIl~&

Secti

on

6

. G

... an

ts

fo ...

job

c

... eati

on

•. (1

)

Su

bje

ct

to

[secti

on

2

].

an

Ind

ivid

ual.

co

... p

o ... ati

on

.

pa

... tn

e ... sh

lp.

or

sMal~

bu

sin

ess

cQ ...

po

... atl

on

. as

defi

ned

In

15

-31

-20

1.

that

sta

rts

a

new

b

usin

ess

0'" e

xp

an

ds

an.

ex

i.st

lng

bu

sin

ess

Is

en

titl

ed

to

a

Sl.

00

0

g ... an

t fo

... each

ne

w jo

b.

c ... eate

d.

(2)

Th

e g

... an

t M

ay

no

t b

e cla

imed

fo

r m

o ... e

th

an

1

00

ne

w

job

s.

an

d

the to

tal

g ... a

nt

may

n

ot

ex

ceed

th

e ~ount

of

tax

ab

le

Inco

me

dl

... ectl

y att

rib

uta

ble

to

th

e

new

b

usin

ess

or

bu

sin

ess

ex

pan

sio

n.

(3)

Th

e g

... an

ts

Mu

st

be ad

mln

iste

... ed

b

y th

e

dep

a ... ta

en

t

of

com

me .

.. ce

an

d

a ... e

p

ay

ab

le

f ...

oM

co

al

sev

e ...

an

ce ta

x

fun

ds

all

ocate

d to

th

e

dep

a ...

tmen

t fo

... th

at

pu

... p

ose

.

~EH_SEtIlg&a

Secti

on

7

. In

te ... e

st

off

set.

S

ub

ject

to

[secti

on

2J

. an

In

div

idu

al.

co

rpo

... ati

on

. p

art

ne ... sh

ip.

0'"

small

b

usin

ess co

rpo

rati

on

th

at

sta

... ts

a ne

w

bu

sin

ess

0

...

ex

pan

ds

an

ex

isti

ng

b

usin

ess

Is e

nti

tled

to

an

o

ffset

of

on

e-f

ou

... th

In

te ... est

po

int

for

ev

e ...

y 1

0

new

jo

bs

cre

ate

d.

up

to

a m

axim

um

of

4 In

te ... est

po

ints

. ag

ain

st

any

fi

nan

cin

g

ob

tain

ed

f

... om

th

e sta

te fo

... p

... o

jects

q

uali

fyin

g

and

fi

nan

ced

-3-

.1 2 3 ,. 5' 6 7 8 9

10

11

12

.

13

14

15

16

17

18

19

20

21

22

23

z.

25

LC

12

53

/01

un

der

[LC

ll

lt8

] •.

Secti

on

8

. S

ecti

on

1

5-3

5-1

08

. M

CA

. Is

am

end

ed

to

read

:

15

-35

-10

8.

(Eff

ecti

ve

Ju

ly

1.

19

83

) D

isp

osa

l o

f

sev

e ...

an

ce

tax

es.

Seve~ance

tax

es

co

llecte

d

unde

...

the

pro

vis

ion

s o

f th

is

ch

ap

te ...

are

all

ocate

d as

foll

ow

s:

(1)

To

th

e

t ... u

st

fun

d

c ... eate

d

by

A

... ti

cle

IX

, se~tion

,,5

. o

f th

e

Ho

nt.

an

a.c

on

s.tl

tutl

on

, Z5~

of

tota

l co

llecti

on

s

a

yea ...

. A

fter

Dec

emb

e ...

31

. 1

91

9.

50~

of

co

al

sev

era

nce

tax

co

llecti

on

s

a ...

e all

ocate

d to

th

is

t ... u

st

fun

d.

Th

e t

... u

st

fun

d

mo

ney

s sh

all

b

e

dep

osi

ted

in

17

-6-:

2J3

J5)

and

In

vest

ed

b

y

the

.p~ovided

by

la

ve

the

fun

d

esta

bll

sh

e9

u

n d

e ...

bo

ard

o

f in

vesta

en

ts

as

(Z)

Co

al

sev

e ... a

nce

tax

co

llecti

on

s

... em

aln

lnq

aft

e ...

all

ocati

on

to

th

e

all

ocate

d

In

the

bala

nce:

t ... u

st

fun

d

unde

...

su

bsecti

on

(1

) a

... e

foll

ow

ing

p

erc

en

tag

es

of,

the

... em

aln

lng

Ca)

to

th

e

co

un

ty

in

wh

ich

co

al

Is

min

ed

. 2~

of

the

sev

e ... an

ce

tax

p

aid

o

n

the

co

al

min

ed

In th

at

co

un

ty u

nti

l

Jan

ua ...

y 1

. 1

98

0.

fo ...

su

ch

p

u ... o

ose

s as

the

go

ve

... n

ing

b

od

y

of

the

co

un

ty

may

d

ete

....

lne;

(D)

Z l/Z~

un

til

Dec

embe

...

31

. 1

97

9.

an

d th

e ... eaft

e ...

~-~f~ '-Ll~l

to th

e ea ..

.. a

... k

ed

... ev

en

ue

fun

d

to th

e

c ... ed

it o

f

the

31

te ... n

at

I ve

en

e ...

gy

... ese

a ...

ch

d

ev

elo

pll

len

t an

d

deM

On

st ...

ati

on

acco

un

t;

(el

26

1/2~ u

nti

l Ju

ly 1

. 1

97

9.

and

th

ere

aft

e ...

37

1

/2*

-4

-

1 2 3 4

·5

6 1 6 q

1.0

11

12

13

14

15

16

11

18

19

LC

12

53

/01

to

the

ear.

ark

ed

re

ven

ue

fun

d

to th

e cre

dit

o

f th

e

local

imp

act

and

ed

ucati

on

tr

ust

fun

d

acco

un

t;

(d)

for

each

o

f th

e

2 fi

scal

years

fo

llo

win

g

Jun

e

30

.

19

71

. 1

3*

to

th

e ear.

ark

ed

re

ven

ue

fun

d

to th

e cre

dit

o

f th

e

r.o

al ~rea

hig

hw

ay

i.p

rov

em

en

t acco

un

t;

(el

10

*

to

the

earm

ark

ed

re

ven

ue

fun

d

for

sta

te

eq

uali

zati

on

aid

to

p

ub

lic sc

ho

ols

o

f th

e s

tate

;

(f) l'

to th

e

earm

ark

ed

re

ven

ue

fun

d to

th

e cre

dit

o

f

the

co

un

ty

lan

d

pla

nn

ing

acco

un

t;

(gl

.1 1

/4'

to

the

Sin

kin

g

fun

d to

th

e cre

dit

o

f th

e

ren

ew

ab

le

reso

urc

e

dev

elo

pft

nt

bo

nd

acco

un

t;

(h)

5'

to th

e

ean

lla.

rked

re

ven

ue

fun

d

to

the cre

d i

t o

f

a tr

ust

fun

d

for

the

pu

rpo

se

of

par~s

acq

uis

itio

n o

r

manage~ent,

pro

tecti

on

o

f w

ork

s o

f art

In th

e sta

te cap

ito

l,

and

o

ther

cu

ltu

ral

and

aesth

eti

c

PfO

jectS

. In

cDm

e fr

OID

th

is

tru

st

fun

d

sh

all

b

e

ap

pro

pri

ate

d as

foll

ow

s:

(i)

1

/3 fo

r p

rote

cti

on

o

f w

ork

s o

f art

in

th

e

sta

te

cap

ito

l an

d

oth

er

cu

ltu

ral

and

aesth

eti

c p

roje

cts

; an

d

(I I

, 2

/3

for

the

acq

uis

itio

n

of

sit

es

and

are

as

20

d

escri

bed

in

2

3-1

-10

2

an

d t~e o

pera

tio

n

and

.a

inte

nan

ce

of

21

sit

es

so

acq

uir

ed

;

22

!i,

l'

to th

e

earm

ark

ed

re

ven

ue

fun

d to

th

e cre

dit

o

f

23

th

e sta

te

lib

rary

co

mm

issi

on

fo

r th

e

pu

rpo

ses

of

pro

vid

ing

24

b

asic

li

bra

ry

serv

ices

for

the

reS

iden

ts

of

all

co

un

ties

25

.throucr~

lib

rary

fe

dera

tio

ns

and

fo

r p

aym

ent

of

the co

sts

o

f

-5-

1 2 3 It

5 6 1 8 q

10

11

12

13

lit

15

16

1'1

LC

12

53

/01

part

iCip

ati

ng

in

re

gio

nal

an

d n

ati

on

al

netw

ork

ing

;

(J)

1/2

o

f l'

to

the

earm

ark

ed

re

ven

ue

fun

d

for

co

nserv

ati

on

d

istr

icts

;

(k)

1 1

/4'

to th

e sin

kin

g fu

nd

to

th

e

cre

dit

o

f th

e

wate

r d

ev

elo

pm

en

t sin~ing

acco

un

t;

lll __

~_li~l_1g-tb~_~aL~-LeKeQuc-fund-t~~~

gf _

_ tb~ _

_ deQa~tment_~f _

_ ~gmme~~-fQL_~LPQ~Gi-.akiQg Q~

jg~s-a~aQts_AS_Q~gxlded-1Q_L~1LgQ-6J4

t.tL

ml

all

o

ther

rev

en

ues

fro

. se

vera

nce

tax

es

co

llecte

d

un

der

the

pro

vis

ion

s

of

this

ch

ap

ter

to th

e cre

dit

of

the

qen

era

l fu

nd

o

f th

e sta

te.-

~EH_SftIlO~&

Secti

on

q

. C

oo

rdin

ati

on

In

str

ucti

on

. If

81

11

N

o.

[LC

11~8J

Is

no

t p

ass

ed

b

y

the

48

th

leg

isla

ture

an

d

ap

pro

ved

b

y

the

go

vern

or.

secti

on

7

an

d

su

bsecti

on

3

of

secti

on

2

are

v

oid

.

~EW_SE~IID~&

Secti

on

1

0.

Ap

pli

cab

ilit

y.

Th

is

act

is

ap

pli

cab

le

for

tax

y

ears

b

eg

inn

ing

afte

r

Dec

emb

er

31

. 1

98

3.

-En

d-

-6

-

..

..

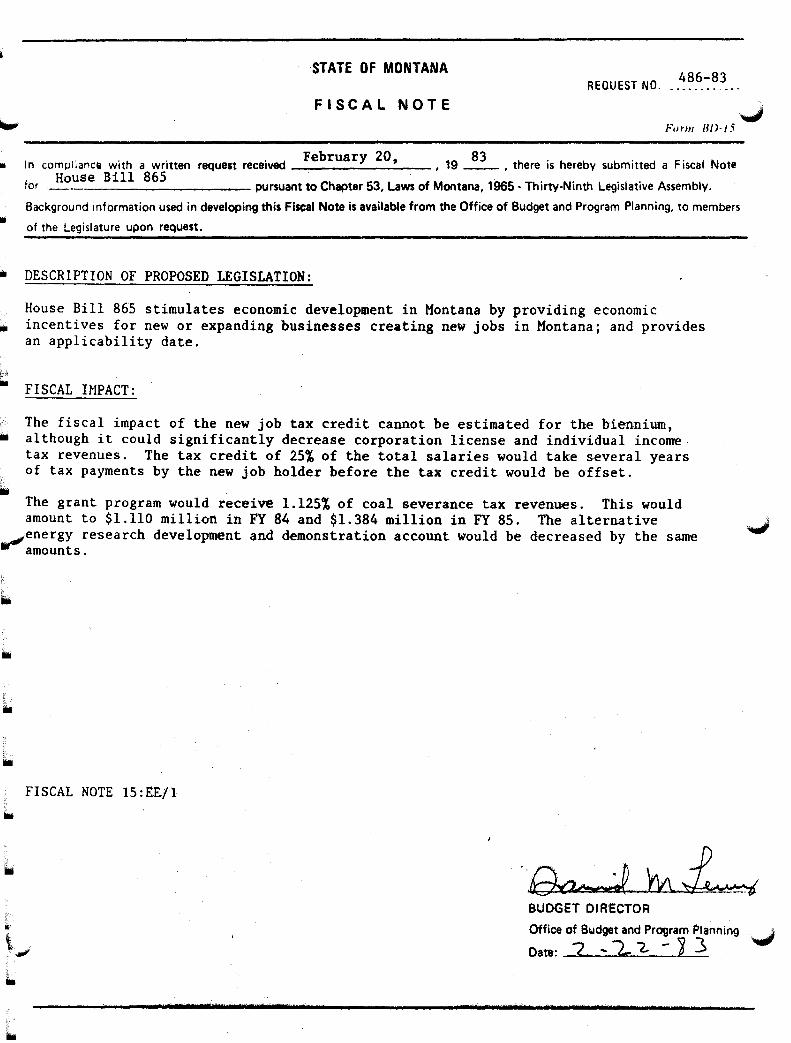

-STATE OF MONTANA REQUEST NO.

486-83

FISCAL NOTE ..., Forni H/)'15

February 20, 83 In compliance with a written request received , 19 __ , there is hereby submitted a Fiscal Note

for House Bill 865 pursuant to Chapter 53, Laws of Montana, 1965 - Thirty-Ninth legislative Assembly.

Background information used in developing this Fiscal Note is available from the Office of Budget and Program Planning, to members

of the Legislature upon request.

DESCRIPTION OF PROPOSED LEGISLATION:

House Bill 865 stimulates economic development in Montana by providing economic incentives for new or expanding businesses creating new jobs in Montana; and provides an applicability date.

FISCAL IMPACT:

The fiscal impact of the new job tax credit cannot be estimated for the biennium, although it could significantly decrease corporation license and individual income· tax revenues. The tax credit of 25% of the total salaries would take several years of tax payments by the new job holder before the tax credit would be offset .

The grant program would receive 1.125% of coal severance tax revenues. This would amount to $1.110 million in FY 84 and $1.384 million in FY 85. The alternative """"

~energy research development and demonstration account would be decreased by the same amounts.

FISCAL NOTE 15:EE/1

,dee 1 1 '

BUDGET DI R'ECTOR

Office of Bwdget and Program Planning

Date: 2 ... 2. "'2, - U

-

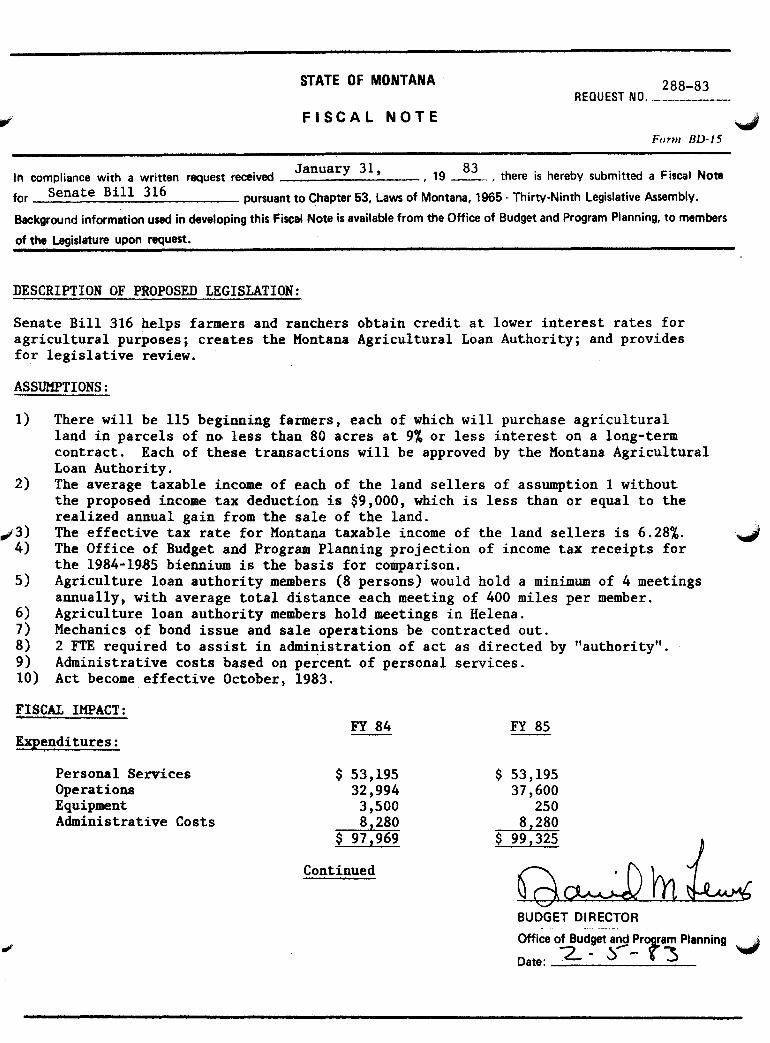

STATE OF MONTANA 288-83 REQUEST NO.

FISCAL NOTE Form 8D-15

January 31, 83 In compliance with a written request received , 19 __ , there is hereby submitted a Fiscal Note for Senate Bill 316 pursuant to Chapter 53, Laws of Montana, 1965 -Thirty-Ninth Legislative Assembly. Background information used in developing this Fiscal Note is available from the Office of Budget and Program Planning, to members of the Legislature upon request.

DESCRIPTION OF PROPOSED LEGISLATION:

Senate Bill 316 helps farmers and ranchers obtain credit at lower interest rates for agricultural purposes; creates the Montana Agricultural Loan Authority; and provides for legislative review.

ASSUMPTIONS:

1)

2)

",·3) 4)

5)

6) 7) 8) 9) 10)

There will be 115 beginning farmers, each of which will purchase agricultural land in parcels of nG less than 80 acres at 9% or less interest on a long-term contract. Each of these transactions will be approved by the Montana Agricultural Loan Authority. The average taxable income of each of the land sellers of assumption 1 without the proposed income tax deduction is $9,000, which is less than or equal to the realized annual gain from the sale of the land. The effective ta~ rate for Montana taxable income of the land sellers is 6.28%. The Office of Budget and Program Planning projection of income tax receipts for the 1984-1985 biennium is the basis for comparison. Agriculture loan authority members (8 persons) would hold a minimum of 4 meetings annually, with average total distance each meeting of 400 miles per member. Agriculture loan authority members hold meetings in Helena. Mechanics of bond issue and sale operations be contracted out. 2 FTE required to assist in administration of act as directed by "authority". Administrative costs based on percent of personal services. Act become effective October, 1983.

FISCAL IMPACT:

Expenditures:

Personal Services Operations Equipment Administrative Costs

FY 84

$ 53,195 32,994 3,500 8,280

$ 97,969

Continued

FY 85

$ 53,195 37,600

250 8,280

$9G~lliL BUDGET DIRECTOR

Office of Budget a~ PrOj!am Planning -..,; Date: 2 - 0 - " ':5

II'

-2-

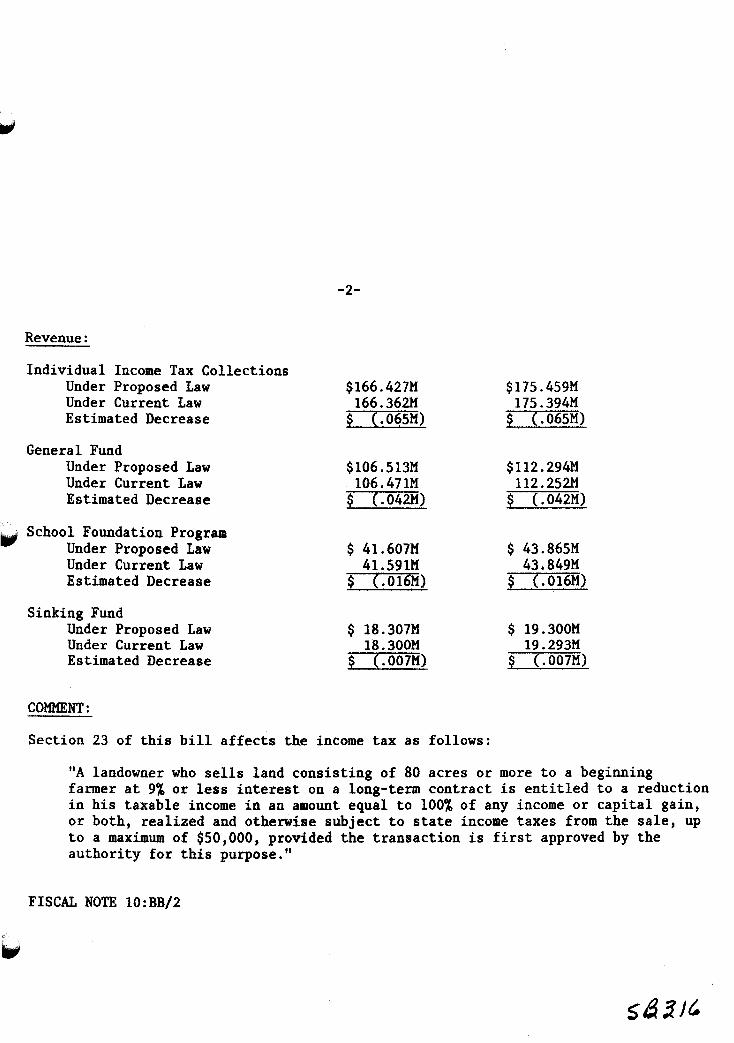

Revenue:

Individual Income Tax Collections Under Proposed Law $166.427M Under CUrrent Law 166.362M Estimated Decrease $ ~.0~5M)

General Fund Under Proposed Law $106.513M Under Current Law 106.471M Estimated Decrease $ ~.042M)

School Foundation Program Under Proposed Law $ 41.607M Under Current Law 41. 591M Estimated Decrease $ COIE)M)

Sinking Fund Under Proposed Law $ 18.307M Under Current Law 18.300M Estimated Decrease $ L007M)

COMMENT:

Section 23 of this bill affects the income tax as follows:

$175.459M 175.394M

$ (.065M)

$112.294M 112.252M

$ (.042M)

$ 43.865M 43.849M

$ L016M)

$ 19.300M 19.293M

§ (.OO7M)

"A landowner who sells land consisting of 80 acres or more to a beginning farmer at 9% or less interest on a long-term contract is entitled to a reduction in his taxable income in an amount equal to 100% of any income or capital gain, or both, realized and otherwise subject to state income taxes from the sale, up to a maximum of $50,000, provided the transaction is first approved by the authority for this purpose."

FISCAL NOTE 10:BB/2

.. -

-.. -

,.-.

b ~J -,-~4-cA:> sdl. -r~

bu.~ HT C,orf. A sdQ kT C'O .... r. A

hu.~ \)~ ?o~-l

c)~V~~6~t

bl.\ (s t--\,-~ r,

s~ f-A-T ~r,

tl Z sJ q,,~

Z.S'tU~b

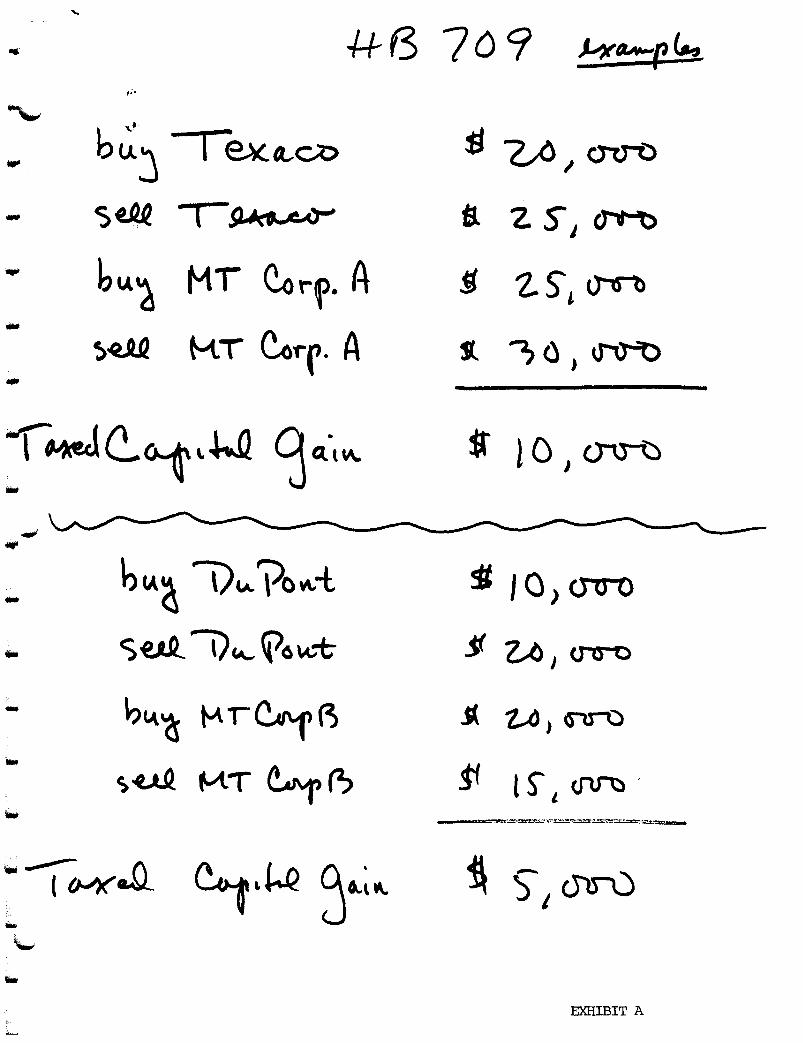

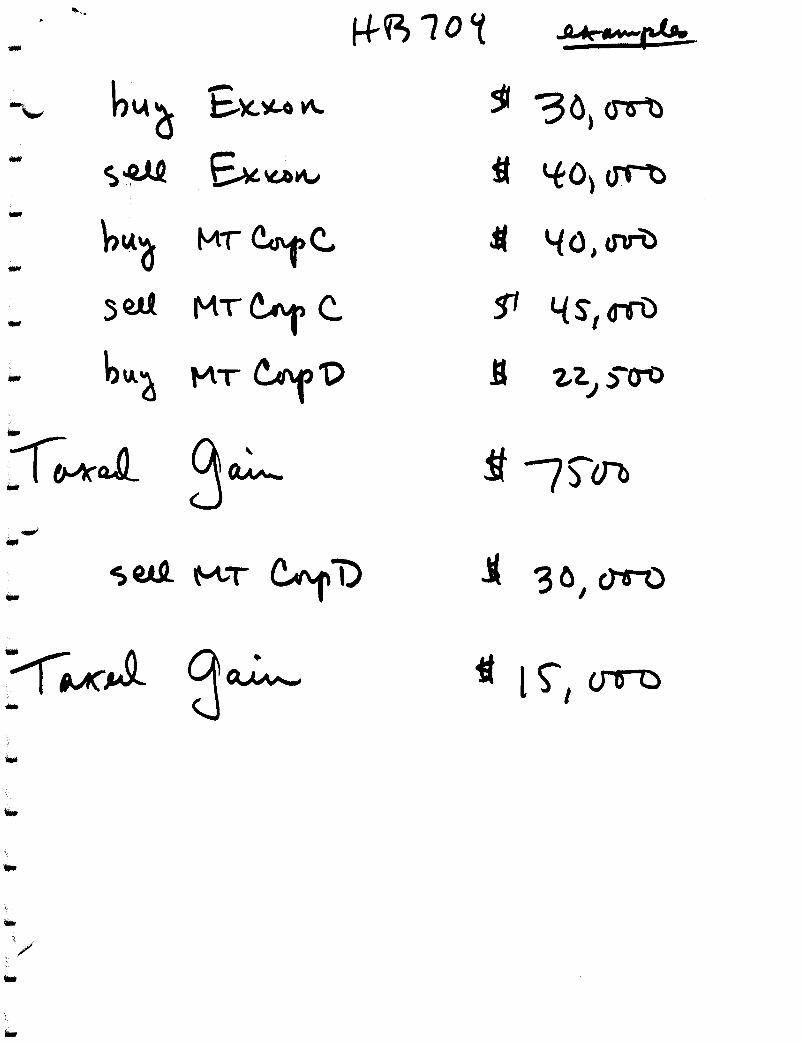

EXHIBIT A

"'" ~r, 10~ ~fc~~ -

-'-' 6"'6 ---. c.)(.~ V\.. ~ 30, <rot)

- s~ ~~~ ~ \fo) crr~ -

\'14~ tv\T ~c. ~ '-l () I crrl> -sell MT~C. $1 L{SI a-ro

.. bu.d t-'\T ~'D '2,,) ,)'0-0

...

. /

"-House Bill 709

This bill provides for rostponin~ the income tax on gains from

the sale of property. The gain would not be taxed if the monies

received from the sale are placed in an enterprise with its prin-

cipal business activities ln Montana. Nhen the taxpaver sells

or removes his investment in the enterprise the qain is then

taxed. I ,~( ; i

While the bill seems straightforward, it leaves many technical

questions unanswered. For purposes of Montana individual and

corporate income taxation of gains, the Federal laws are con-

trolling. It is, therefore, necessary to have the provisions

of this bill fit with the federal laws on taxation of qains.

As proposed this bill doesn't make a clean connection between

federal and state law.

The following are nroblem areas the bill doesn't adeauately

address:

1. The bill allows for postnonement of taxation on qalnS

from the sale of capital assets, but doesn't define can-~_._---".-._.- ---_ . .::.... __ . __ .- _. --

ital assets. For federal tax purooses caoital assets

are non-depreciahle proper tv such as nersonal residents

and cars, Good ~i~l, securities, etc.

2. ~~ore than one rnll1Vec:~tment to nost-oon(' a qaln is not

sllecificcill"

have morc, th,li.

not be taxceJ «1 :~110 same tiPlr' hv t'le:' sLlt(~.

I t- l'll!'

EXHIBIT B

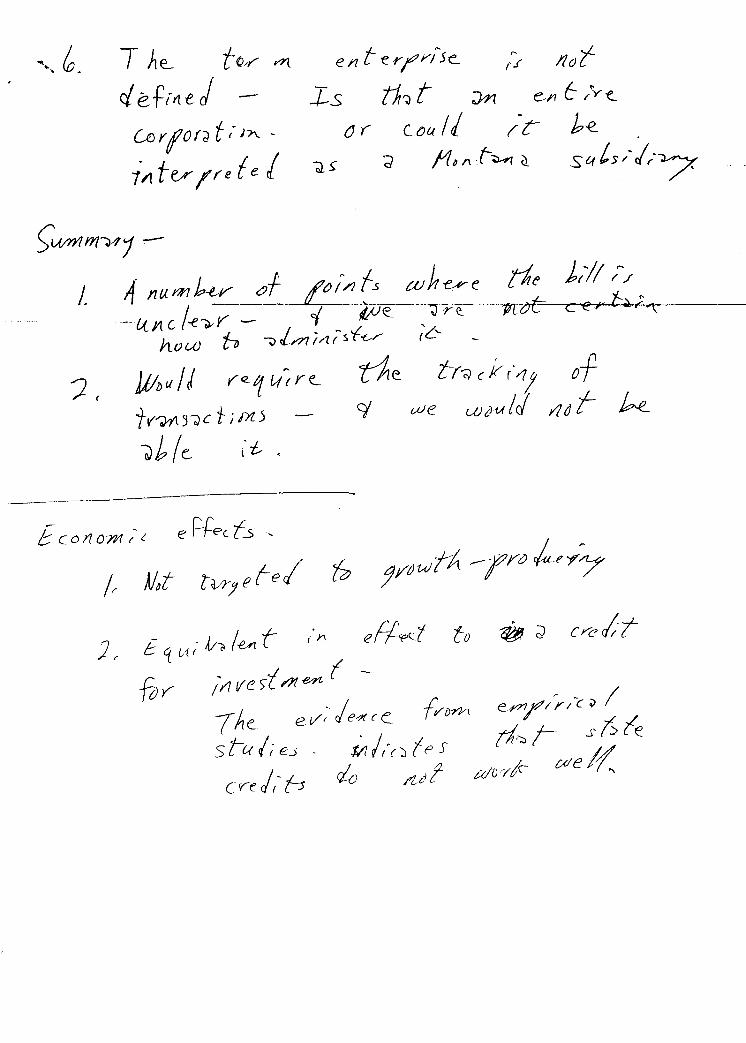

T he.... to/- rl't en t e y r' yt5 e..

cL efttlej - -1-5 tJ,~ t J,n

Co y f 0 f"d t ;)'" -1'" te/' Ire te !

or Cou 1/

5:wmm,";)41-J. ~. nv.mW CJf ~;.d5 aJht!A'e tie 1,;/1 (.I

_ (;{Jt1 c /-e~V _ ~·--;;U~-----'J-r~-.--1rro"E=' c er 't-:.;" how h "-,) rlm;/1. (-s i't--' ;t:>

)j;lJ Ii / , r e 1 w; y ~

IV";h1 S --;) c t ; ;n )

t"f';J c K r-1f of we UJJulJ Ylo r k

-0;1, If:.- (t, ~

6 c () J1 om I' ( e f--t:ec. f.s,

/. AU lWJefel (;, rdwtll ~t'N /a~.;/

7A~ ei/; je4(c~ f~{)rh st-u/;e3 - iz//(':Jips eve dr' h cia /1-d f

el'71,rt'rl-C:~ I ti~;-" J,~/e

u/Vylc- Cd e J(

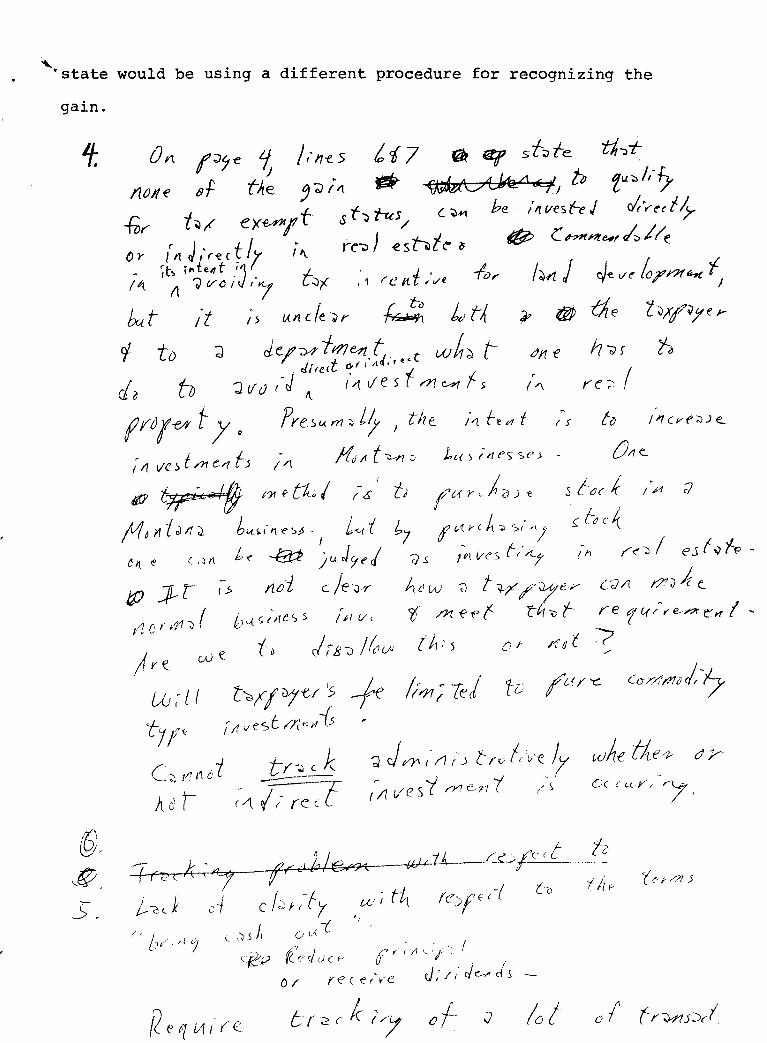

"-·state would be using a different procedure for recognizing the

gain.

011 f;J'jt: 1; I/"nes ~{7 fk lil1 st7J"t-e ti-;d-nOl{e of the J";;};/l .. ·wfdc/l~;/I4.J to fl.l~k~

fOr t.,r e XM"f t $ t, tus / ( ~ be /. ves t-el 01. ',ed I;,.. 01" (fl J,'nut/r i", re-;;» €shie ~ ~ cnH;7(e,r~/(e (" ;r~ i'~':~ /J 'I' t~f ,1 re ,tt ;v' -I~Y hrl j ~e ,,-fol''''''' 1/

/t ;5 Lutc/e~r ~ l)t~ ;p (jj thE' t~l'r~ye;-

d de.l'7J4fl?1~.t" ,t w/'"d t tJ/1.(! h';) 'h direct Orl AQ"e

cia to 'J(jtJ(-J r\ ,·/(vesfrn&11f.s /'\ re~(

f YO /-U t 1 Q Pre Sv. rr/":J LI; I tile /'1 f:-~ t4 f (5' to

;/IVc~t/11e;?f5 (/l )1dlft~7:- )..,t-o r"/lt"SSe'j UI'/e.. rP t~6.#f} I?fPt/tJI /6' h (tArl-JO)t .st{)('k /pr d

/'1dnf;Jl1~ bv..f.,·ttt"-;'P., i'<-fi /:'7 fl-1.Hh-;;O'":;,(·;1) (fcJck

tit (! (,:))1 f,-( ~ jl,(J;t~j -;;)5 '~ll/(," tr'~ I~h ,re"~! eJfv'/-p-

ftJ]tt (-.> t1.oi cje~f I..ow '0 tv-//7~tr CJ/l t77J4~ r1.(:(.11~( ~)vl..c.(-M.S5 /I/V, t /J1.."f'Pf 'tk-v'i- re 11-{;"€.-#rE"'I'fI,

wet i> cI '( g J I fc) 1../': tk' 5 0 r /1 dr.? Ir(!. UJ (- / f t~r/~-el ';; -r

( 11 vest ,7le:.A {s tll~

-f (2 C • \ I i.ec k d

1,"/ .... )1'< , ,{ 1

/.J ",I k / e '9"1;

'J J t/)1 (' :' r"J tr~ f,.1i'e.. ~ (/, VI? S i r?1 e/l1 t /',>

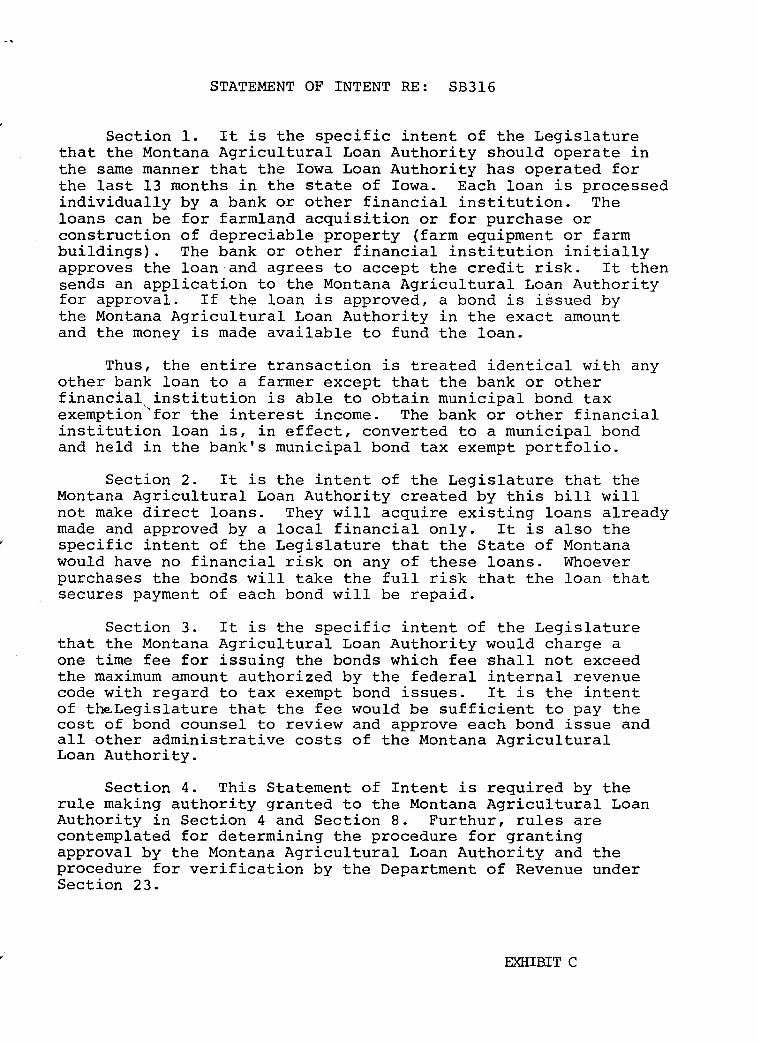

STATEMENT OF INTENT RE: SB3l6

Section 1. It is the specific intent of the Legislature that the Montana Agricultural Loan Authority should operate in the same manner that the Iowa Loan Authority has operated for the last 13 months in the state of Iowa. Each loan is processed individually by a bank or other financial institution. The loans can be for farmland acquisition or for purchase or construction of depreciable property (farm equipment or farm buildings). The bank or other financial institution initially approves the loan and agrees to accept the credit risk. It then sends an application to the Montana Agricultural Loan Authority for approval. If the loan is approved, a bond is issued by the Montana Agricultural Loan Authority in the exact amount and the money is made available to fund the loan.

Thus, the entire transaction is treated identical with any other bank loan to a farmer except that the bank or other financial, institution is able to obtain municipal bond tax exemption'for the interest income. The bank or other financial institution loan is, in effect, converted to a municipal bond and held in the bank's municipal bond tax exempt portfolio.

Section 2. It is the intent of the Legislature that the Montana Agricultural Loan Authority created by this bill will not make direct loans. They will acquire existing loans already made and approved by a local financial only. It is also the specific intent of the Legislature that the State of Montana would have no financial risk on any of these loans. Whoever purchases the bonds will take the full risk that the loan that secures payment of each bond will be repaid.

Section 3. It is the specific intent of the Legislature that the Montana Agricultural Loan Authority would charge a one time fee for issuing the bonds which fee shall not exceed the maximum amount authorized by the federal internal revenue code with regard to tax exempt bond issues. It is the intent of t~Legislature that the fee would be sufficient to pay the cost of bond counsel to review and approve each bond issue and all other administrative costs of the Montana Agricultural Loan Authority.

Section 4. This Statement of Intent is required by the rule making authority granted to the Montana Agricultural Loan Authority in Section 4 and Section 8. Furthur, rules are contemplated for determining the procedure for granting approval by the Montana Agricultural Loan Authority and the procedure for verification by the Department of Revenue under Section 23.

EXHIBIT C

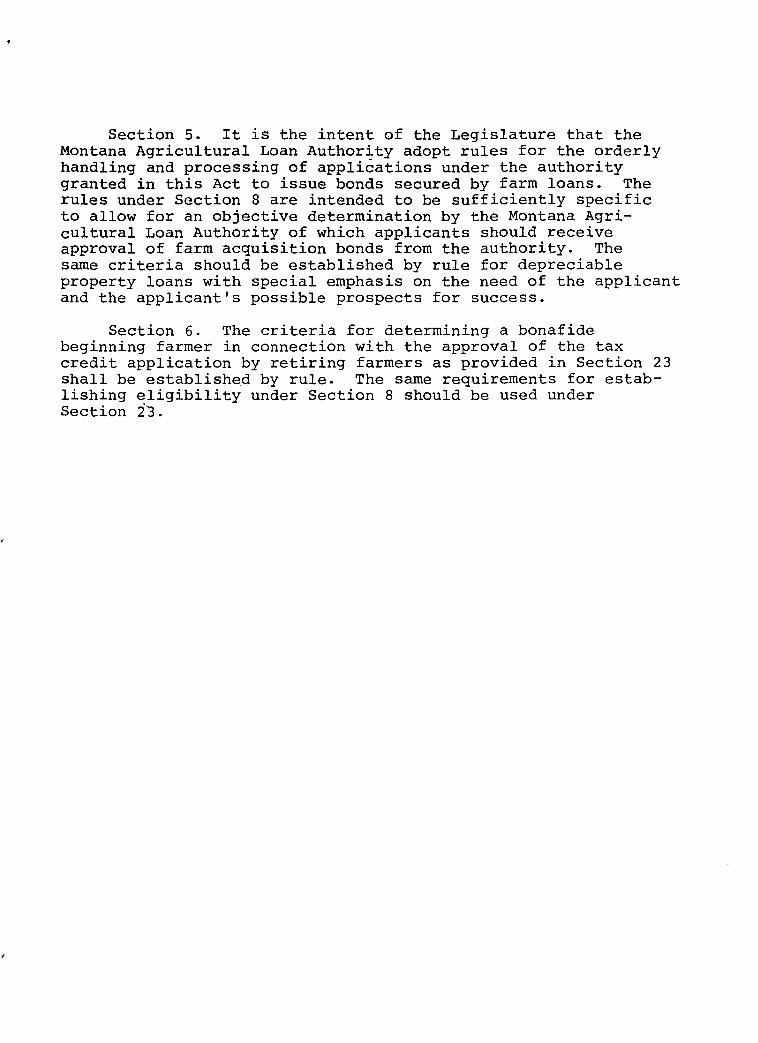

Section 5. It is the intent of the Legislature that the Montana Agricultural Loan Authority adopt rules for the orderly handling and processing of applications under the authority granted in this Act to issue bonds secured by farm loans. The rules under Section 8 are intended to be sufficiently specific to allow for an objective determination by the Montana Agricultural Loan Authority of which applicants should receive approval of farm acquisition bonds from the authority. The same criteria should be established by rule for depreciable property loans with special emphasis on the need of the applicant and the applicant's possible prospects for success.

Section 6. The criteria for determining a bonafide beginning farmer in connection with the approval of the tax credit application by retiring farmers as provided in Section 23 shall be established by rule. The same requirements for establishing eligibility under Section 8 should be used under Section iJ.

•

..

..

..

..

..

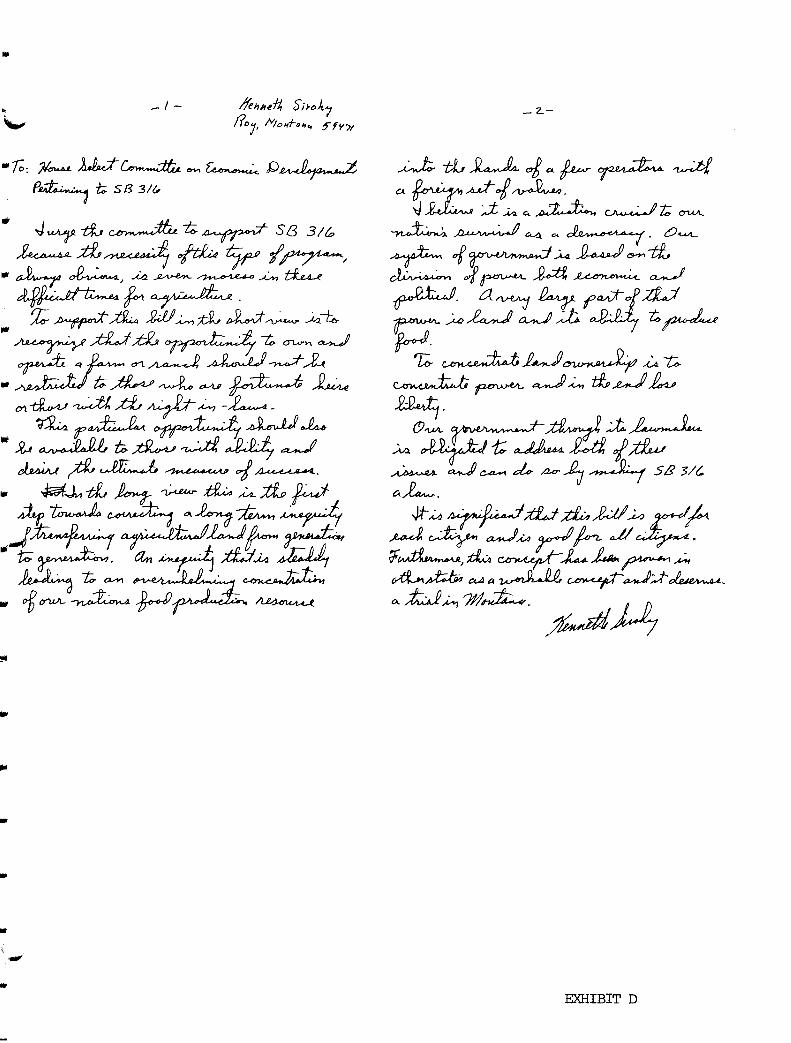

_1- IlehMfit S;;t:>kt 110y, /VtO"f-a"4 5"fY)1

_ 2.-

EXHIBIT D

Ma rch 15, 1983

Testimony presented by

Keith Kelly Director, Montana Department of Agriculture

on Senate Bill 316