Embed Size (px)

Citation preview

Report Prepared by Connecticut Health Insurance Exchange

Report to the Board of Directors, Connecticut Health Insurance Exchange

Essential Health Benefits Selecting and Supplementing a Benchmark Plan in Connecticut

Recommendation of the Health Plan Benefits and Qualification Advisory Committee

Co-Chairpersons:

Anne Melissa Dowling Deputy Commissioner, Connecticut Insurance Department

Mark Espinosa, President, United Food and Commercial Worker’s Union 919

2

Abbreviations

ACA: Patient Protection and Affordable Care Act of 2010

ASD: Autism Spectrum Disorders

AV: Actuarial Value

Board: Connecticut Health Insurance Exchange Board of Directors

CID: Connecticut Insurance Department

CCIIO: Center for Consumer Information and Insurance Oversight

CMS: Center for Medicare and Medicaid Services

Committee: The Health Plan Benefits and Qualifications Advisory Committee

CPHHP: University of Connecticut’s Center for Public Health and Health Policy

EHB: Essential Health Benefits

Exchange: Connecticut Health Insurance Exchange

FEDVIP: Federal Employee Dental and Vision Insurance Program

HHS: Department of Health and Human Services

OMB: Connecticut’s Office of Management and Budget

PT/OT/ST: Physical Therapy/Occupational Therapy/Speech Therapy

PMPM: Per Member Per Month

QHP: Qualified Health Plan

Secretary: Secretary of the Department of Health and Human Services

Table of Contents

Abbreviations 2 I. Message from the Co-Chairpersons 4

II. Introduction 6 The Advisory Committee Process 6

III. Overview of the Essential Health Benefits 8 The Institute of Medicine Report: Balancing Costs and

Comprehensiveness 8 Essential Health Benefits Bulletin: The State Benchmark Approach 10 Treatment of State-Mandated Benefits 11

IV. Selection of the Connecticut’s Benchmark 14 Connecticut’s Ten Benchmark Options 14 Elimination of the “Plan E” and “Plan F”: State Mandates 15 Elimination of “Plan A” and “Plan C”: Lifetime Visitation Limits 16 EHB Selection: Balancing Comprehensiveness and Affordability 17

V. Supplemental Coverage 21 Prescription Drug 21 Pediatric Dental Care 22 Pediatric Vision Care 23 Habilitative Services 23

VI. Conclusion 24 VII. Exhibits 25

A. Committee Membership and Affiliation B. State Mandated Benefits and Mercer’s Assessment of EHB

Status C. Classification of State Mandated Benefits Under the ACA’s Ten

Categories of Care D. Summary Analysis of Benchmark Plans E. Detailed Analysis of Select Benchmark Plans F. Milliman Report: State Employees, State of Connecticut G. Comparison of Supplemental Options: Pediatric Dental Care

Tables and Figures Included: Figure 1. Process for Recommendation of EHB Benchmark 7 Table 1. Comparison of Select Rehabilitative Services in non-FEHBP EHB Benchmark Options 17 Figure 2. Utilization Rates for Rehabilitative Services in State Employee Health Plans 18 Table 1. Claims and Utilization Rate for Selected Rehabilitative Services in State Employee Health Plans 18

4

I. Message from the Co-Chairpersons

This Report to the Board of Directors of the Connecticut Health Insurance Exchange provides a detailed explanation regarding the process undertaken by the Health Plan Benefits and Qualifications Advisory Committee (Committee) in order to make a recommendation with regard to the selection of the essential health benefit (EHB) benefit package.

This important provision of the health care law is meant to ensure that all individuals and families are guaranteed a minimum level of coverage for certain health services considered “essential,” regardless of which health plan they choose.

The Affordable Care Act defines the “essential health benefits” as a series of ten broad benefit categories, with considerable discretion left to the Secretary of the U.S. Department of Health and Human Services (HHS) to further define the concept. In December 2011, HHS released guidance describing its intended approach for defining the scope of health services included in the essential health benefits package. Rather than create one federal definition, HHS gave each state the authority to define exactly what items and services will be included in its essential health benefits package for 2014 and 2015. This package must be based on a benchmark plan selected by the state.

All insurers operating in the individual and small-group markets, both inside and outside of the exchanges, must cover this standard package of benefits.

If a state’s benchmark plan does not cover one or more of the 10 categories of services that the essential health benefits is required to cover under the Affordable Care Act, a state will have to supplement its essential health benefits package with additional benefits from one of the other benchmark plan options. HHS provided additional guidance on how states will supplement a benchmark plan with coverage for habilitative services and pediatric dental and vision services, as these types of services are not traditionally offered in health plans today.

A state’s benchmark plan will play a significant role in defining the scope and amount of benefits offered in each of the 10 categories of services covered in a state’s essential health benefits package. As such, the recommendation of a benchmark is a balancing act between comprehensiveness and cost; the more inclusive the package, the higher the cost. No benefit designated as “essential” can be subject to an annual or lifetime dollar limit.

In making its recommendation, this Committee was directed to follow the statutory directives included in the Affordable Care Act and Public Act 11-53, the State legislation enabling the Exchange, as well as, the regulatory guidance that the Department of Health and Human Service is intending to propose.

After three months of extensive analysis and review the Health Plan Benefits and Qualifications Committee offers its recommendation to the Board of Directors of the Connecticut Health Insurance Exchange that the state of Connecticut’s EHB benchmark plan be defined by the benefits package included in the “Plan D” benchmark option, supplemented by: the prescription drug coverage included in “Plan C”; the dental care benefits included in Connecticut’s Children Health Insurance Program, Husky B, and; the benefits included in the vision plan in Federal Employee Dental/Vision Insurance Program with the largest national enrollment.

We wish to thank the members of the Committee for their dedication to our Committee’s process and their voluntary commitment in the service of the residents of Connecticut. We would also like to

5

thank everyone who offered perspectives for their invaluable contribution, including members of the public, committee members, the Consumer Outreach and Experience Advisory Committee.

On behalf of Exchange staff, we wish to extend appreciation to the carriers and the Office of the Comptroller for providing Exchange staff with the necessary health plan documentation and addressing follow-up inquries. Much of the analyses conducted by Exchange staff would not have been possible without the technical assistance and support provided by Scott Anderson, Assistant Director, in the Healthcare Policy and Benefits Service Division of the Office of the Comptroller, Mary Ellen Breault, Director, Life and Health Division in the Connecticut Insurance Department, and, Bob Carey, Principal at RLCarey Consulting.

We hope that the Board can utilize the recommendation presented in this Report to help define Connecticut’s essential health benefits. Please send any comments regarding this Committee’s recommendation and the supporting background information prepared by the Exchange to Grant Porter at: [email protected].

Thank you,

Anne Melissa Dowling

Mark Espinosa

6

II. Introduction

This Report to the Connecticut Health Insurance Exchange Board of Directors (Board), “Essential Health Benefits: Selecting and Supplementing a Benchmark Plan in Connecticut” (Report), reflects the recommendation of the Health Plan Benefits and Qualifications Advisory Committee (Committee) for the essential health benefits (EHB) package.

On March 23, 2010 the Patient Protection and Affordable Care Act of 2010 (ACA) was signed into law.1 The federal law requires all states, beginning in January 1, 2014, to participate in health insurance exchanges operated either by the state, the federal government, or through state-federal partnerships. On July 1, 2011 Governor Malloy signed into law Senate Bill 921 (Public Act 11-53), an Act Establishing the Connecticut Health Insurance Exchange (Act).2

The Act defines Connecticut’s Health Insurance Exchange (Exchange) as a quasi-governmental organization governed by a 14-member board of directors. Membership includes six ex officio members and eight members appointed by elected state officials. There are 12 voting members. The Act granted that the Exchange may establish advisory committees composed of a broad array of stakeholders to assist the Board in making decisions and/or recommendations on a variety of topics, including a study on the EHB as mandated in the Act.

The Health Plan Benefits and Qualifications Advisory Committee (Committee) was charged with making a formal recommendation on the state’s essential health benefit (EHB) package to the Board.

This Report to the Board, “Essential Health Benefits: Selecting and Supplementing a Benchmark Plan in Connecticut” (Report), provides justification in support of the benchmark option recommended by the Committee as the most appropriate in terms of health benefits and coverage to be made available for the residents of the State.

The Advisory Committee Process

The Board established four advisory committees to inform itself and the Exchange leadership on various topics related to healthcare reform. Among other subjects, the Committee was charged with examining the potential EHB benchmark options and offering its stakeholders’ perspectives on the functional implications of selecting an EHB benchmark from among the potential options available the Board.

To best inform the Committee and provide its members with neutral analyses of their options, the Exchange conferred with the Connecticut Insurance Department (CID), the Healthcare Policy and Benefit Services Division of the Office of the State Comptroller, the major insurance carriers selling plans in Connecticut’s small group market, the Center for Consumer Information and Insurance Oversight (CCIIO), and professional consulting firms, including Mercer and RLCarey Consulting.

The Exchange provided its analyses to the Consumer Outreach and Advisory Committee that independently considered the state’s EHB package. A voting member on that committee is a consumer advocate who serves on both committees and represented the consumer’s opinion to the Committee. The Committee’s recommendation represents a consensus with the opinion represented by the Consumer Outreach and Experience Advisory Committee. 1 H.R. 3590, The Patient Protection and Affordable Care Act of 2010 (P.L. 111-148). Internet: http://www.gpo.gov/fdsys/pkg/PLAW-111publ148 2 S. 921, An Act Establishing a State Health Insurance Exchange, 2011 (P.A. 11-53). Internet: http://www.cga.ct.gov/2011/ACT/PA/2011PA-00053-R00SB-00921-PA.htm (Accessed: July 15, 2012)

7

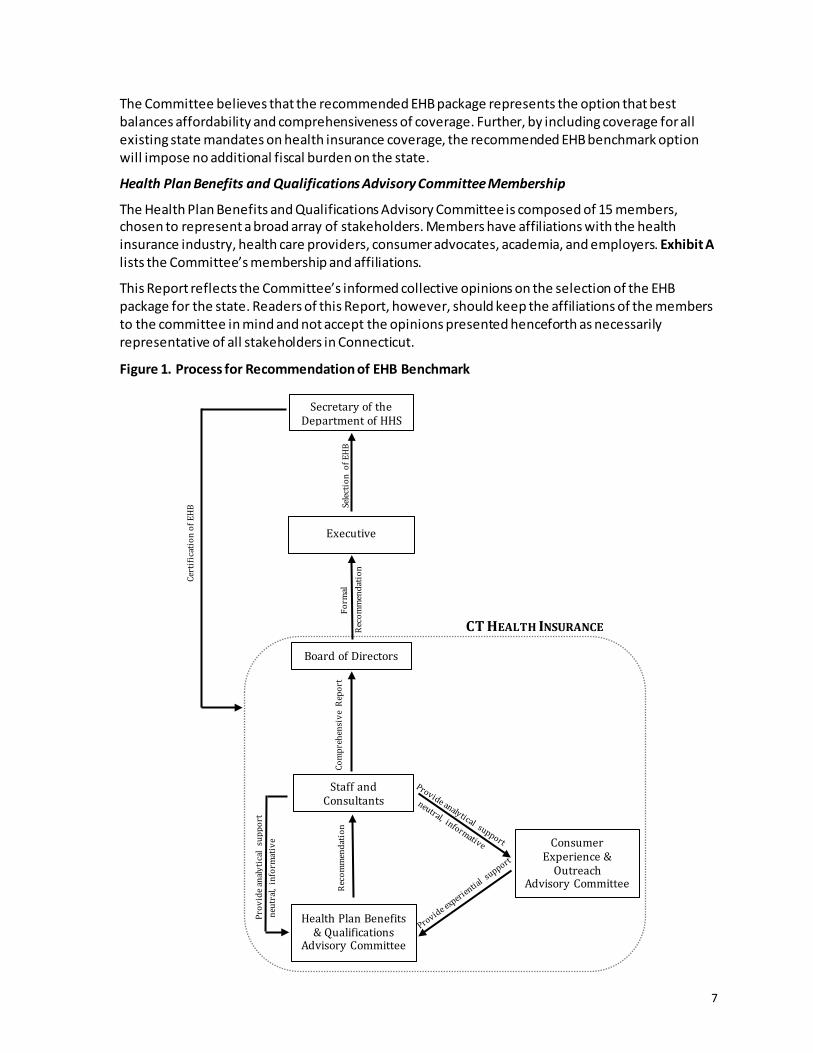

The Committee believes that the recommended EHB package represents the option that best balances affordability and comprehensiveness of coverage. Further, by including coverage for all existing state mandates on health insurance coverage, the recommended EHB benchmark option will impose no additional fiscal burden on the state.

Health Plan Benefits and Qualifications Advisory Committee Membership

The Health Plan Benefits and Qualifications Advisory Committee is composed of 15 members, chosen to represent a broad array of stakeholders. Members have affiliations with the health insurance industry, health care providers, consumer advocates, academia, and employers. Exhibit A lists the Committee’s membership and affiliations.

This Report reflects the Committee’s informed collective opinions on the selection of the EHB package for the state. Readers of this Report, however, should keep the affiliations of the members to the committee in mind and not accept the opinions presented henceforth as necessarily representative of all stakeholders in Connecticut.

Figure 1. Process for Recommendation of EHB Benchmark

Secretary of the Department of HHS

Executive

Com

preh

ensi

ve R

epor

t

Staff and Consultants

Health Plan Benefits & Qualifications

Advisory Committee

Consumer Experience &

Outreach Advisory Committee

Board of Directors

Reco

mm

enda

tion

Reco

mm

enda

tion

Form

al

Prov

ide a

naly

tical

supp

ort

ne

utra

l, in

form

ativ

e

Selec

tion

of E

HB

Cert

ifica

tion

of E

HB

CT HEALTH INSURANCE

8

III. Overview of the Essential Health Benefits

Section 1301 of the ACA requires that every non-grandfathered health insurance plan offered to an individual or small group, including, but not limited to, plans sold through the Connecticut Health Insurance Exchange (the Exchange), will need to be provide, at minimum, and among other requirements, the state’s essential health benefits (EHB) package. The EHB provides coverage for a specific level of preventive, diagnostic, and therapeutic services defined as “essential” by the Secretary of the Department of Health and Human Services (Secretary).

Nationally, more than 68 million people are estimated to obtain commercial insurance that will need to meet EHB requirements; in Connecticut, approximately 750,000 residents will be directly affected.3 The breadth of coverage underscores the importance that the EHB package reflects the needs and preferences of all residents.

The EHB is intended to be a meaningful and adequate standard that will ensure equitable coverage for all consumers carrying individual or small group coverage. It must include comprehensive coverage in at least the following 10 statutorily-defined benefit categories:

1) Ambulatory patient services, 2) Emergency services, 3) Hospitalization, 4) Maternity and newborn care, 5) Mental health and substance use disorder services, including behavioral health

treatment, 6) Prescription drugs, 7) Rehabilitative and habilitative services and devices, 8) Laboratory services, 9) Preventive4 and wellness services, and chronic disease management, and 10) Pediatric services, including oral and vision care.

Beyond the ten broad categories, however, the ACA leaves undefined the specific services that must be covered in the EHB.

Section 1302(b) gives the Secretary the discretionary authority to define the scope of coverage, provided that the EHB is consistent with a “typical employer plan” and includes meaningful coverage for each of the 10 statutorily-defined benefit categories.

The Institute of Medicine Report: Balancing Cost and Comprehensiveness

The ACA charged the Secretary with defining what the EHB package should include. To assist with this, the Secretary contracted with the Institute of Medicine (IOM) to recommend a process that would help the federal government define a process by which it would identify the benefits that should be included in the EHB, and update the benefits to take into account advances in science, gaps in access, and the effect of any benefit changes on cost. The task of the IOM was not to decide

3 Christine Eibner, Peter S. Hussey, and Federico Girosi. 2010. "The Effects of the Affordable Care Act on Workers' Health Insurance Coverage" New England Journal of Medicine. 4 With respect to defining preventive services, the benefits described in section 2713 of the PHS Act, as added by section 1001 of the Affordable Care Act, must be a part of the EHB.

9

what is covered in the EHB, but rather to propose a set of criteria and methods that should be used in deciding what benefits are most important for coverage. The IOM submitted its recommendations in a report entitled “Essential Health Benefits: Balancing Coverage and Cost” on October 7, 2011.5

In their Report, the IOM emphasized that HHS must consider both the breadth and cost of the benefit package. The EHB needs to be sufficiently inclusive to guarantee adequate access to essential services, but also be affordable so that as many people as possible can purchase the coverage.

The IOM recommended that the overall EHB must:

• be affordable for consumers, employers, and tax-payers; • maximize the number of people with insurance coverage; • protect the most vulnerable by addressing the particular needs of those populations; • encourage better care practices by promoting the right care to the right patient, in the right

setting, at the right time; • advance stewardship of resources by focusing on high-value services and reducing use of

low-value services, with “value” defined as outcomes relative to cost; • address the medical concerns of greatest importance to enrollees in EHB-related plans, as

identified through a public deliberative process; and • protect against the greatest financial risks due to catastrophic events or illnesses.

To address achieve these outcomes, the IOM maintained that the federal government should establish a general premium target for the EHB. Although pricing benefits is inherently imprecise and creates the potential for controversy, the IOM wished to emphasize the responsibility of policymakers to nonetheless consider costs.

While defining a precise premium target is neither within the Secretary’s statutory authority nor within the purview of the Committee’s recommendation, it is, as the IOM advises, the Exchange recognizes that it is a “fundamental reality” that if pricing is not taken into account when defining the EHB package, the benefits are likely to be defined too expansively.

As such, balancing the competing goals of comprehensiveness of coverage and costs, and accepting the tradeoffs inherent in such deliberations, was a major concern for the Committee.

The IOM also recommended a transitional period, during which time HHS could grant the states some allowance to amend the initial EHB package to better reflect the typical small employer plan sold within the state; therefore minimizing the disruption of local health care delivery systems. The IOM recommended as a model for the EHB the benefits typically offered through plans sold in the small employer market because such plans are generally less generous than large employer plan benefits.

Notwithstanding specific recommendation that the state’s be delegated some discretionary authority to revise the EHB, the IOM’s general recommendations remained premised upon the assumption that the federal government would be defining a comprehensive and conclusive standard for the EHB.

5 Institute of Medicine. 2011. “Essential Health Benefits: Balancing Coverage and Cost.” Internet: http://www.iom.edu/EHB.

10

Essential Health Benefits Bulletin: The Benchmark Approach

On December 16, 2011 the Center for Consumer Information and Insurance Oversight (CCIIO) issued its Essential Health Benefits Bulletin (Bulletin).6 While the Bulletin is not binding guidance, it does outline the regulatory approach that HHS “intends to propose” to define the EHB.

The bulletin did not adopt the IOM’s recommended approach that was premised on the identification of a national health benefits package with state flexibility. Instead, the Bulletin provides for a “transitional period” for 2014 and 2015 that allows states to establish a state-specific EHB that reflects the benefits included in a “typical employer plan” offered in a state. This approach accommodates existing state mandates and any local market peculiarities. Federal subsidies will be adjusted to reflect the variability among the different state benchmark plans.

The Bulletin outlines a “benchmark approach” for states to follow to define the EHB. Under this approach, states would choose one of the following benchmark health insurance plans, based on first quarter 2012 enrollment:

• Largest plan by enrollment in any of the three largest small group products in state’s small group market

• Any of the three largest state benefit plans by enrollment • Any of the three largest national Federal Employee Health Benefit Program (FEHBP) plan

options by enrollment • Largest insured commercial non-Medicaid HMO operating in state

If a state does not select a benchmark plan, the Secretary intends to propose that the default benchmark will be the small group plan with the largest enrollment in the state.

Shortly after the release of the Bulletin, HHS released additional complementary guidance in the form of an FAQ7 to further describe the Bulletin’s proposed process. The FAQ reiterates that the only options for a state’s EHB are the ten benchmark plans, supplemented if necessary and in accordance with the guidelines set forth in the Bulletin. Any benefits provided through a rider to the policy are excluded from the benefits package of the benchmark for the purpose of defining the EHB. Further, the state cannot cherry-pick benefits or limits/exclusions across the plans, except in specific circumstances where the selected benchmark is lacking meaningful coverage in a required category.

The scope of benefits, and any limits thereof, included in the selected benchmark will become the state’s EHB package.

If a benchmark plan is missing coverage in one or more of the ten statutory categories, or if coverage is offered only through the purchase of riders, the state must supplement the benchmark by reference to another benchmark plan that includes coverage of services in the missing categories. If none of the benchmarks offer sufficiently comprehensive coverage of particular categories of benefits, the Bulletin describes specific rules to ensure meaningful benefits in those categories.

In Connecticut, no benchmark option offers comprehensive coverage for pediatric dental care, pediatric vision care, and habilitative services. Only a few include prescription drug coverage as part of its base policy.

6 Center for Consumer Information and Insurance Oversight. 12/16/2011. “Essential Health Benefits Bulletin.” Internet: http://cciio.cms.gov/resources/fi les/Files2/12162011/essential_health_benefits_bulletin.pdf. 7 Center for Medicare and Medicaid Services. 2/16/2011. “Frequently Asked Questions on Essential Health Benefits Bulletin” Internet: http://cciio.cms.gov/resources/fi les/Files2/02172012/ehb-faq-508.pdf

11

Carrier Flexibility

The Bulletin expressly indicates that issuers will retain some flexibility in benefit design. Specifically, the Bulletin proposes that a carrier would only be required to offer benefits that are “substantially equal” to the state benchmark. Carriers would be able to “adjust benefits, including both the specific services covered and any quantitative limits provided they continue to offer coverage for all 10 statutory EHB categories.” HHS intends that the “substantially equal” equivalency standard will mirror that applied to CHIP plans.

A Two-Year Transitional Period

The benchmark approach outlined in the Bulletin is intended to establish a state-specific EHB for plan years 2014 and 2015. It is important to note that this is a transitional period and that the HHS intends to assess the benchmark approach and develop a process for defining the EHB that likely will exclude some state mandates for years 2016 and beyond.

The Bulletin suggests that states will be expected to coordinate between their mandates and any forthcoming EHB standard defined by HHS. This transitional period will allow states to determine which of their mandates fall within the EHB, thereby allowing them to identify those additional mandates whose costs would need to be defrayed by the state should the state continue to require them as part of any QHP sold through a state Exchange.

Treatment of State-Mandated Benefits

There is nothing in neither the ACA nor Public Act 11-53 establishing the Exchange that preempt state laws “mandating” coverage of specific benefits and provider services. However, section 1311(d)(3)(B) of the ACA requires that if a mandated benefit was to be not-included in the Secretary’s final EHB package, the state would need to defray (either to the individual or to the health plan on behalf of the individual) any additional costs associated with providing that benefit to Exchange enrollees.

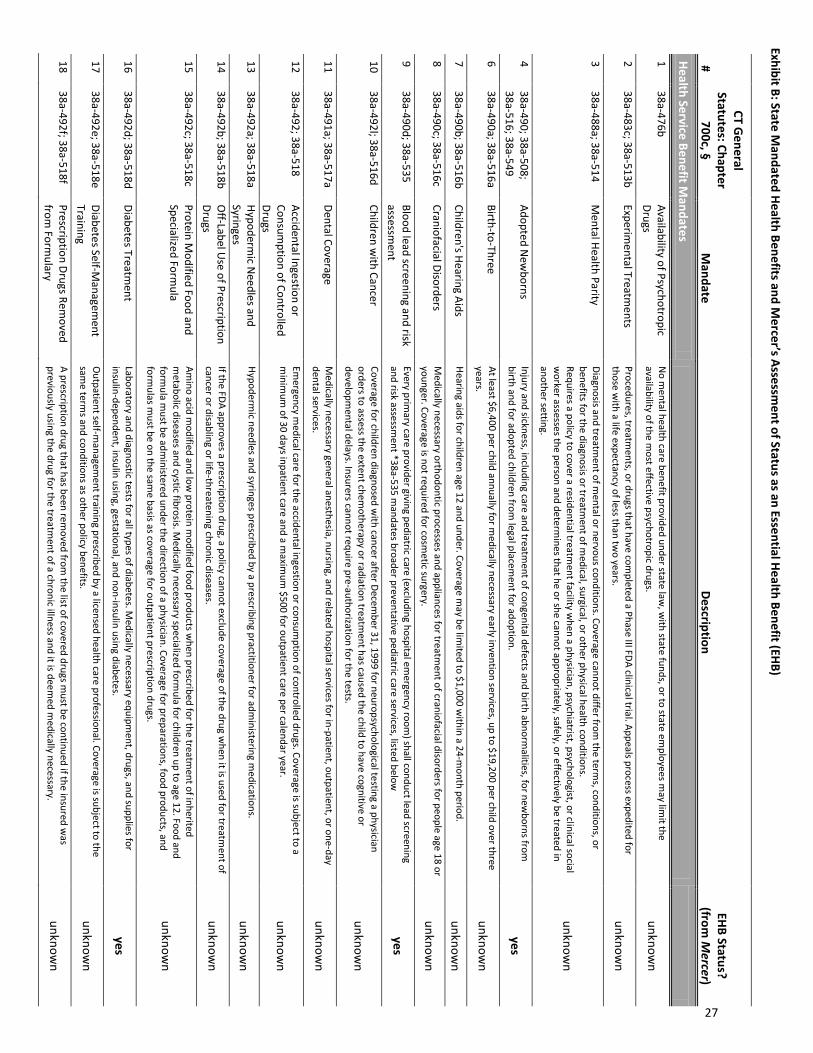

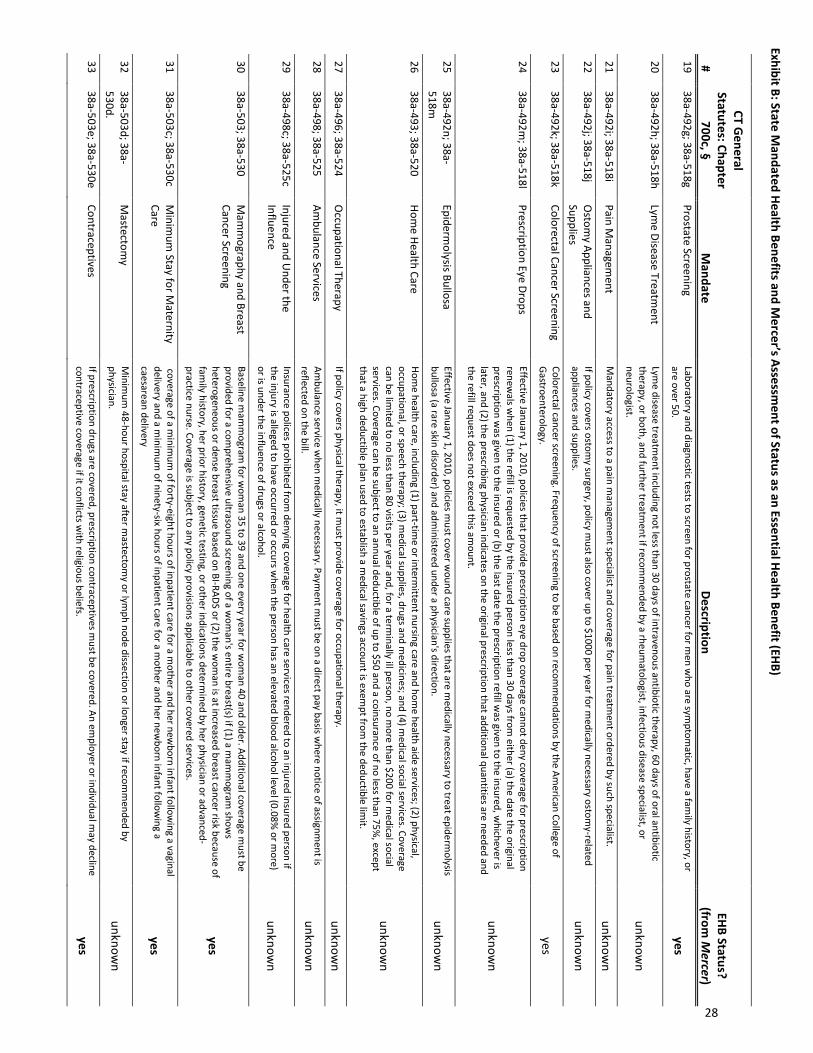

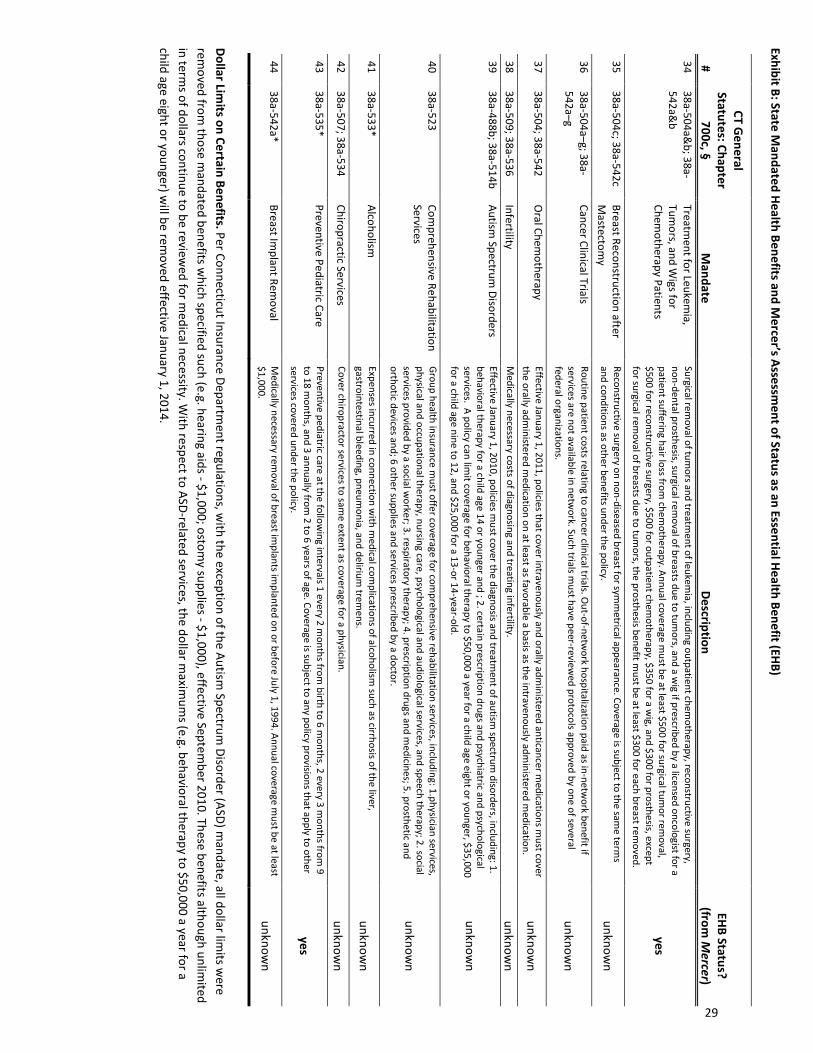

Connecticut is among the 90th percentile of states in terms of the number of health mandates. And so while it is the Committee’s perspective that all state mandates should be viewed as “essential,” in anticipation of the potential fiscal liability resulting from the state retaining mandates that exceed the EHB, section 14a of the Exchange’s establishing Act requires the state to “prepare an analysis of the cost impact on the state and a cost-benefit analysis of the essential health benefits package.”

Mercer Report

In 2011, Connecticut’s Office of Policy and Management (OPB) contracted with Mercer to produce a report on the impact of the ACA in Connecticut. Their scope of work included an analysis of the fiscal impact of the EHB.

To assess whether or not each of the state’s mandates would likely be covered as part of the EHB, Mercer employed the general guidance for defining an EHB as outlined in the IOM Report. Mercer concluded that as many as three-quarters of the benefits that Connecticut mandates could exceed what the federal government requires.

Of the mandates that Mercer identified in the group policy market, it noted only nine as ”essential.” Those include coverage of newborn infants, diabetes testing and treatment, prostate and colorectal cancer screening, mammography and breast ultrasounds, prescription contraceptives, and the cancer, tumors and leukemia benefit.

12

Mercer classified the EHB status of the other mandates as “unknown”; although it suggested that many of the mandates that it classified as ‘”unknown,” “have very strong, rational arguments as to why they might be covered as an EHB.” (p. 208)

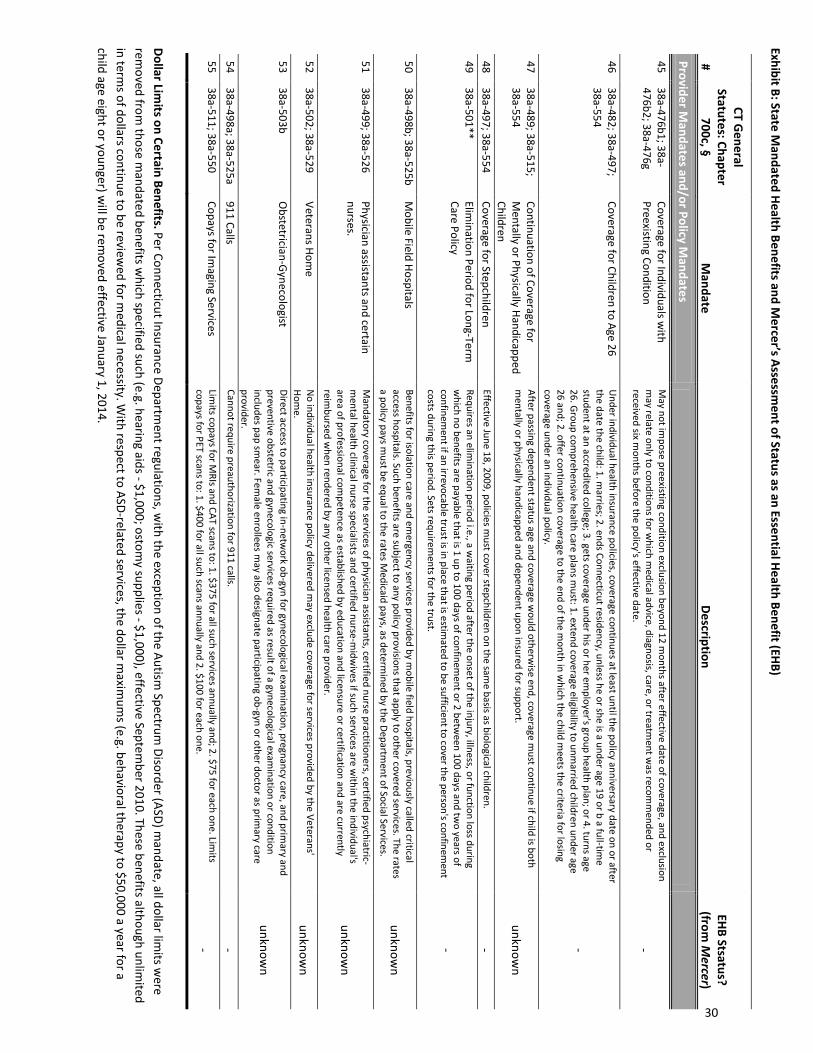

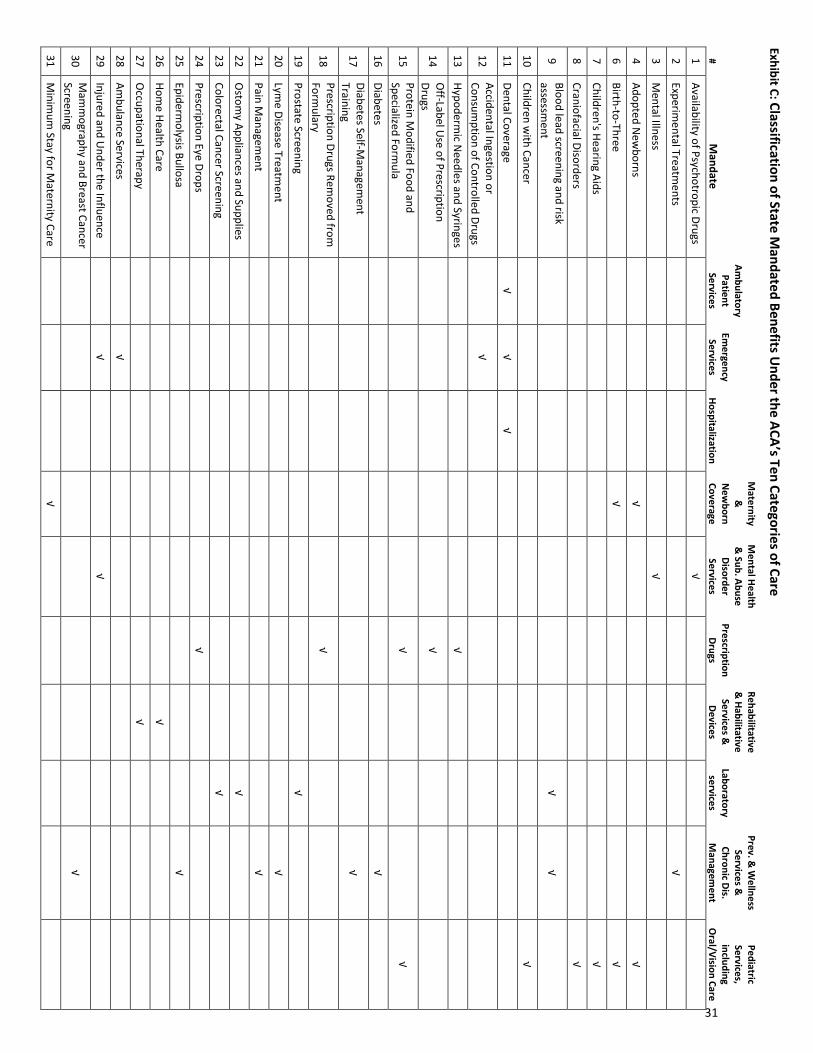

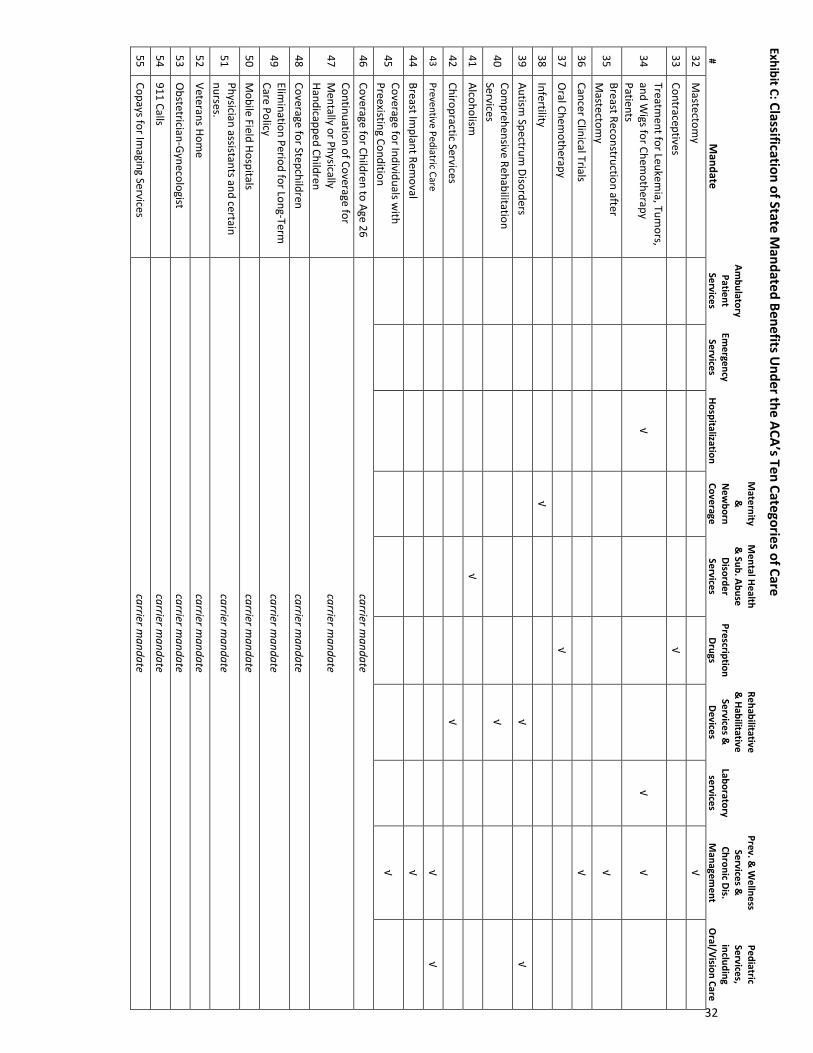

Exhibit B summarizes each of Connecticut’s mandates and presents Mercer’s assessment as to whether or not the mandate can be classified with some certainty as an EHB. Exhibit C classifies the state mandates among the 10 categories of care.

Mercer subsequently projected the cost impact of the state mandates on insurance premiums, based on actuarial estimates provided by University of Connecticut’s Center for Public Health and Health Policy.8 A rough approximation of the aggregate fiscal impact to the state for including all the unknown state mandates could be approximated using the University of Connecticut’s estimated per member per month (PMPM) cost of the mandates.

Impact of the Bulletin on Coverage of State Mandates

The proposed benchmark approach outlined in the Bulletin provides a means by which a state can have all of its mandates governing group plans included in the EHB package at no cost to the state’s budget. Whether the coverage for an existing state benefit mandate will be included in the EHBs will depend on the benchmark plan the state selects.

The benchmark options include health plans in the states’ small group market. These options are generally regulated by the state and would therefore be subject to any state mandate applicable to the small group market. If a state selected one of these options as its benchmark, those mandates would be included in the state’s EHB.

Among the ten potential benchmark options in Connecticut, all of the fully-insured small group plans and state employee health plans include every state mandate—either by law, in the case of the small group plans, or by union negotiation, in the case of the state employee plans. This means that if any one of these benchmark options is selected to define the state’s EHB package, the state will incur no fiscal burden for requiring QHPs to continue to provide coverage for all existing state mandates.

If, however, the state selects as its EHB benchmark option one of the three largest FEHBP plans that are not subject to any state mandates, the state will need to reimburse the marginal costs associated with any mandate that is not covered by the selected FEHBP plan.

To avoid this situation and any potential fiscal obligations or administrative burdens that would surely ensue from selecting a benchmark option that did not provide coverage for all state mandates, the Committee, early in its process of selecting an EHB benchmark, removed from further consideration any of the three FEHBP plans.

8 In 2009, the Connecticut passed a law, Public Act 09-179, requiring the Insurance Department to contract with the University of Connecticut’s Center for Public Health and Health Policy (CPHHP) to evaluate any prospective mandated health benefits that the General Assembly’s Insurance and Real Estate Committee plans to introduce each legislative session. The law also required that there be a retrospective review of all statutorily mandated health benefits existing on or effective July 1, 2009. Mercer was able to offer a rough approximation of the potential cost to the state for supplementing the EHB employed by using the Per Member Per Month (PMPM) cost of each mandate, as calculated by the CPHHP.

13

EHB Preemption of Limits on State Mandates

The ACA does not permit annual or lifetime dollar limits on the EHB. Therefore, if a benefit included in the selected EHB benchmark plan has a dollar limit, that benefit will be incorporated into the EHB definition without the dollar limit. This includes state mandates that may have statutorily-defined dollar limits. Per the Connecticut Insurance Department’s issue approval process, with the exception of the Autism Spectrum Disorder (ASD) mandate, all dollar limits have been removed from those mandated benefits which specified such (e.g. hearing aids - $1,000; ostomy supplies - $1,000), effective September 2010. With respect to ASD-related services, the dollar maximums (e.g. the allowance of $50,000/year toward behavioral therapy for a child age eight or younger) will be removed effective January 1, 2014. As with any benefit, these mandated benefits although unlimited in terms of dollars continue to be reviewed for medical necessity.

14

IV. Selection of Connecticut’s Benchmark

The benchmark approach described in the Bulletin intends to propose that the EHB benchmark options will be drawn from insurance policies that are already offered and that are popular in each state. This should minimize the need for insurers to make changes and allow small employers to continue coverage that is similar to what they already offer. The small group plan benchmark options are already approved by the Connecticut Insurance Department and are therefore familiar to regulators and should be more readily adaptable to any new requirements.

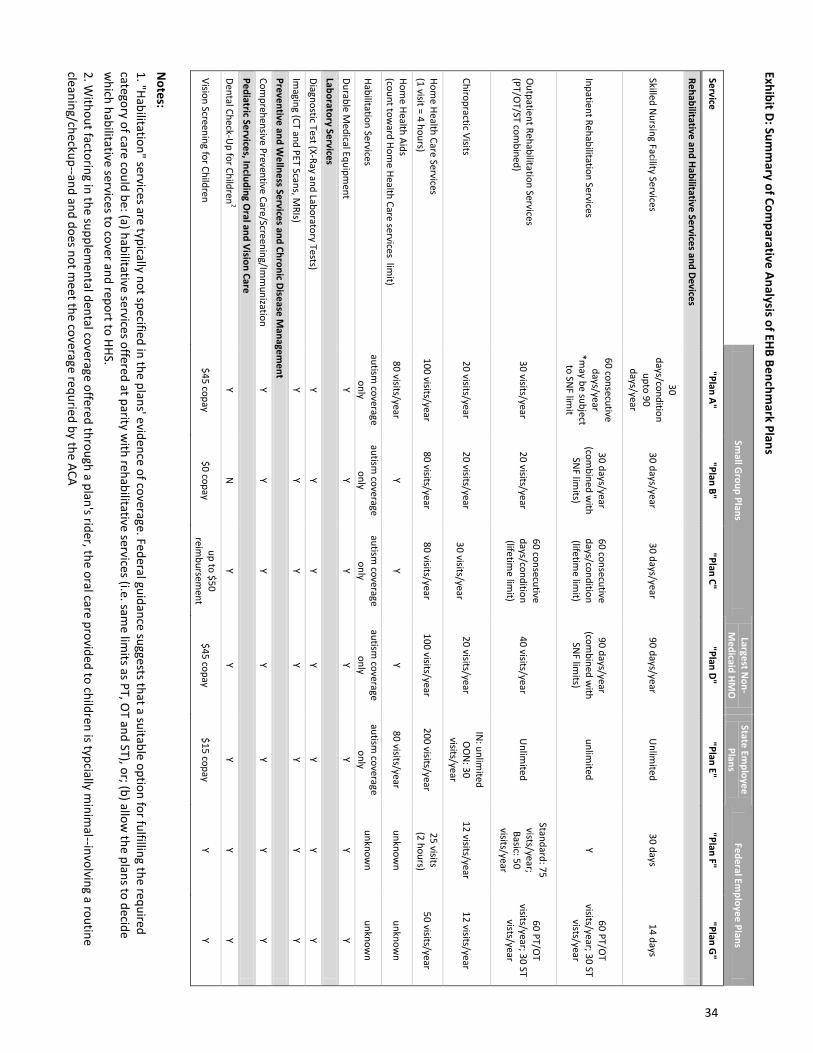

Connecticut’s Ten Benchmark Options

The ten potential EHB benchmark plans that apply to Connecticut, as defined by guidance in the Bulletin, are the benefits package included in:

• The largest plan in the three largest small group products (Source: CMS, CCIIO): o Anthem Blue Cross Blue Shield BlueCare Health Maintenance Organization (HMO), o Aetna Qualfied Point-of-Service (POS), and; o Oxford Preferred Provider Organization (PPO).

• The three largest FEHBP plans (Source: U.S. OPM): o FEHBP Blue Cross Blue Shield Standard Option; o FEHBP Blue Cross Blue Shield Basic Option, and; o FEHBP Government Employees Health Association (GEHA) Standard Option.

• The three largest state employee plans (Source: State of Connecticut, Office of the State Comptroller):

o Anthem State BlueCare Point-of-Enrollment (POE); o Anthem State BlueCare POS plan, and; o Oxford HMO Select Point of Enrollment (POE).

• The largest non-Medicaid HMO plan (Source: CMS, CCIIO): o ConnectiCare HMO

If Connecticut fails to make a recommendation, HHS will define the State’s EHB by the benefits package of the largest plan in the largest small group product, the Anthem Blue Cross Blue Shield BlueCare HMO.

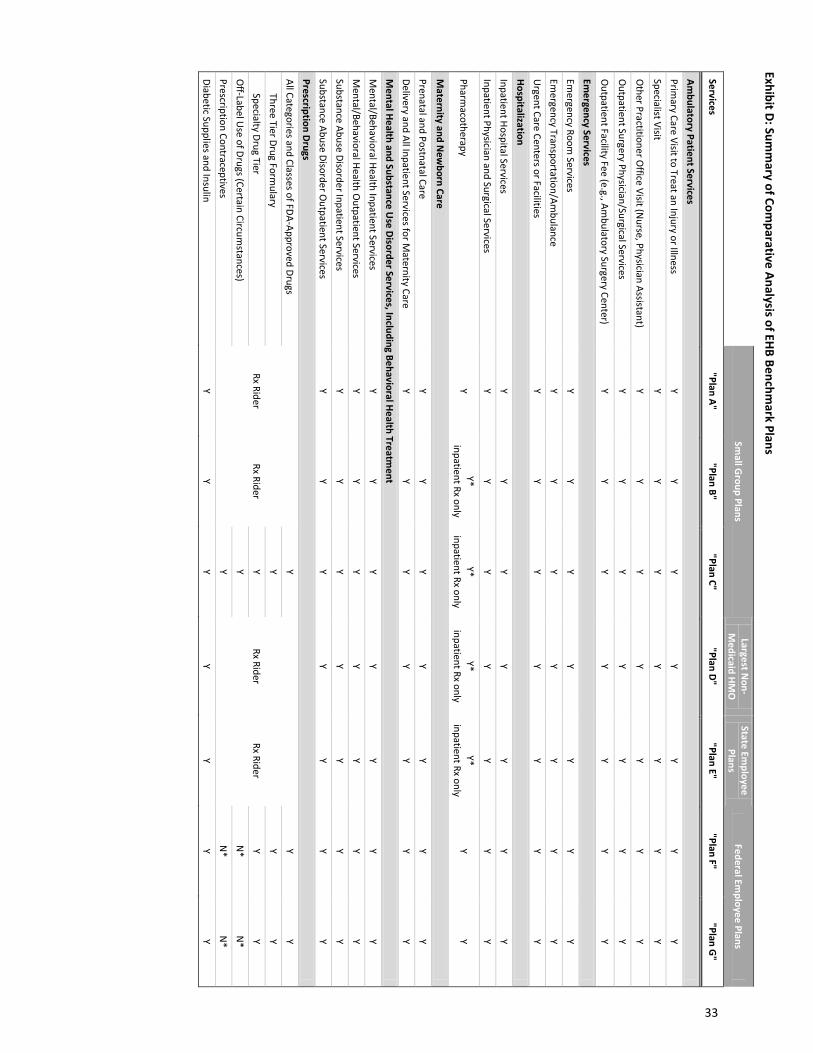

Despite the ten distinct benchmark options, for their subsequent analyses, the Exchange approached them as seven distinct choices.

The Blue Cross Blue Shield Standard Option and Basic Option are the same from the perspective of the plan’s covered benefits: the two plans differ only with respect to the plans’ cost sharing arrangements and their provider networks that for the purpose of defining the EHB are irrelevant distinctions. So, the two plans are treated collectively.

Additionally, all health plans offered to Connecticut state employees cover the same benefits, and so the Exchange treated the three state employee plans as equivalent for the purposes of their subsequent analyses.

It is worth emphasizing that while the Committee is recommending a specifc health plan sold as the benchmark option, it is recommending the benefits described in the plan, not the plan itself. The recommendation of the Committee reflects no endorsement of a specific carrier. The carrier is irrelevant.

15

To emphasize this distinction, the subsequent analyses substitutes an identifier for each of the plans, as follows:

• Small Group/Largest non-Medicaid HMO Plans: o Small Group “Plan A” Anthem Blue Cross Blue Shield HMO o Small Group “Plan B” Aetna Qualified POS o Small Group “Plan C” Oxford PPO o HMO “Plan D” ConnectiCare HMO

• Connecticut State Employee Plans: o State Employee “Plan E” Anthem State POE

• Federal Employee Health Benefit Program Plans: o FEHBP “Plan F” FEHBP BCBS Standard/Basic Option o FEHBP “Plan G” FEHBP GEHA Standard Option

The default EHB benchmark option is “Plan A”.

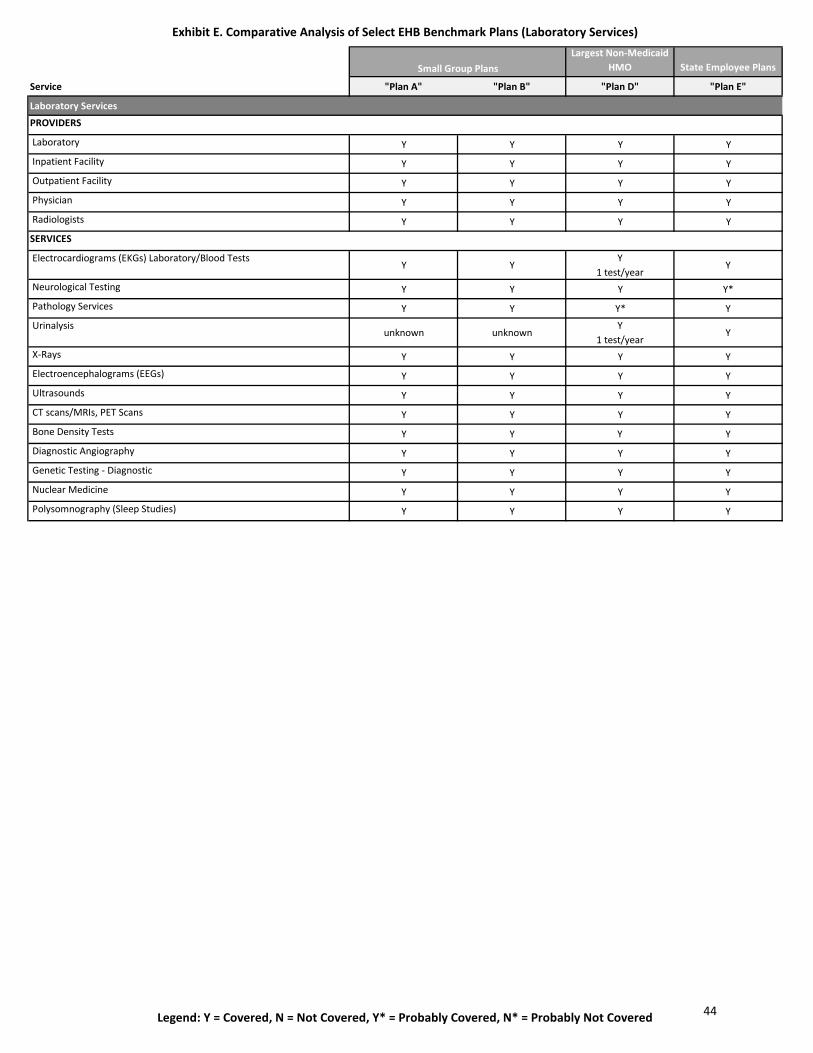

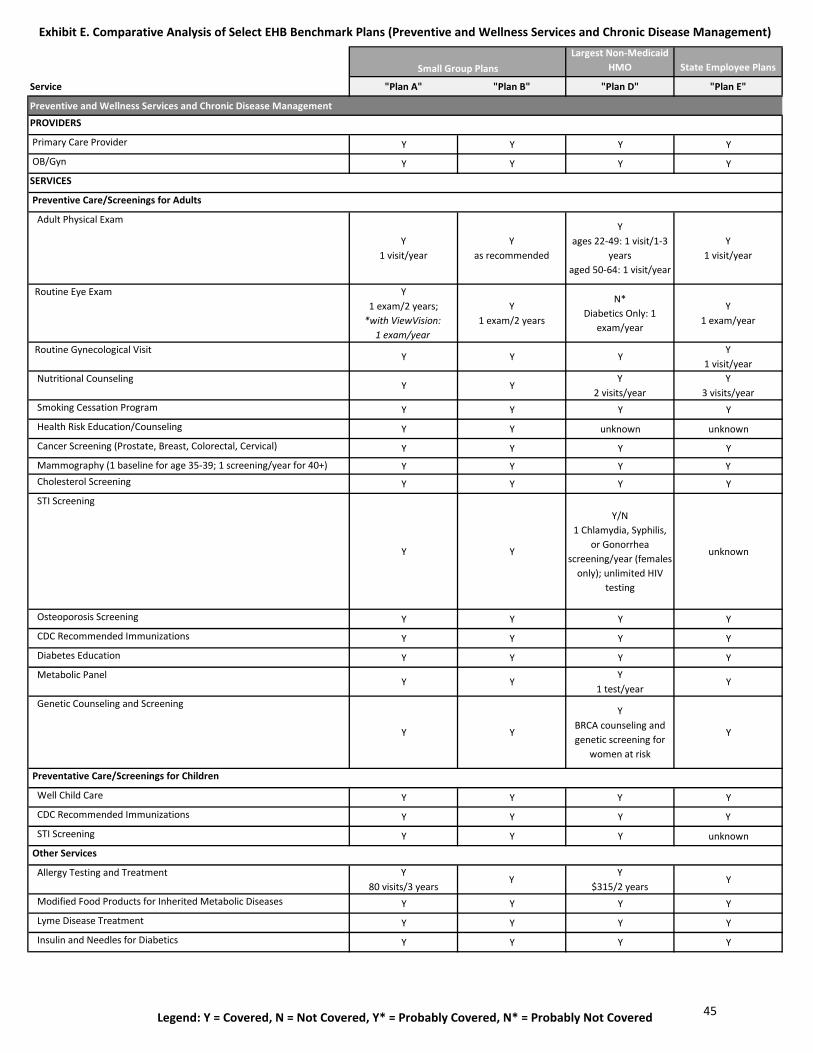

The preliminary survey of the small group plans, the largest non-Medicaid HMO, the state employee plans, and the federal employee plans by the Exchange suggests that the plans in Connecticut do not differ significantly in the range of services and items covered. This observation accords with the Institute of Medicine’s conclusion that the primary type of variation in health insurance products relates not to the covered benefits, but to cost sharing provisions of the product (deductibles, copayments, and coinsurance).

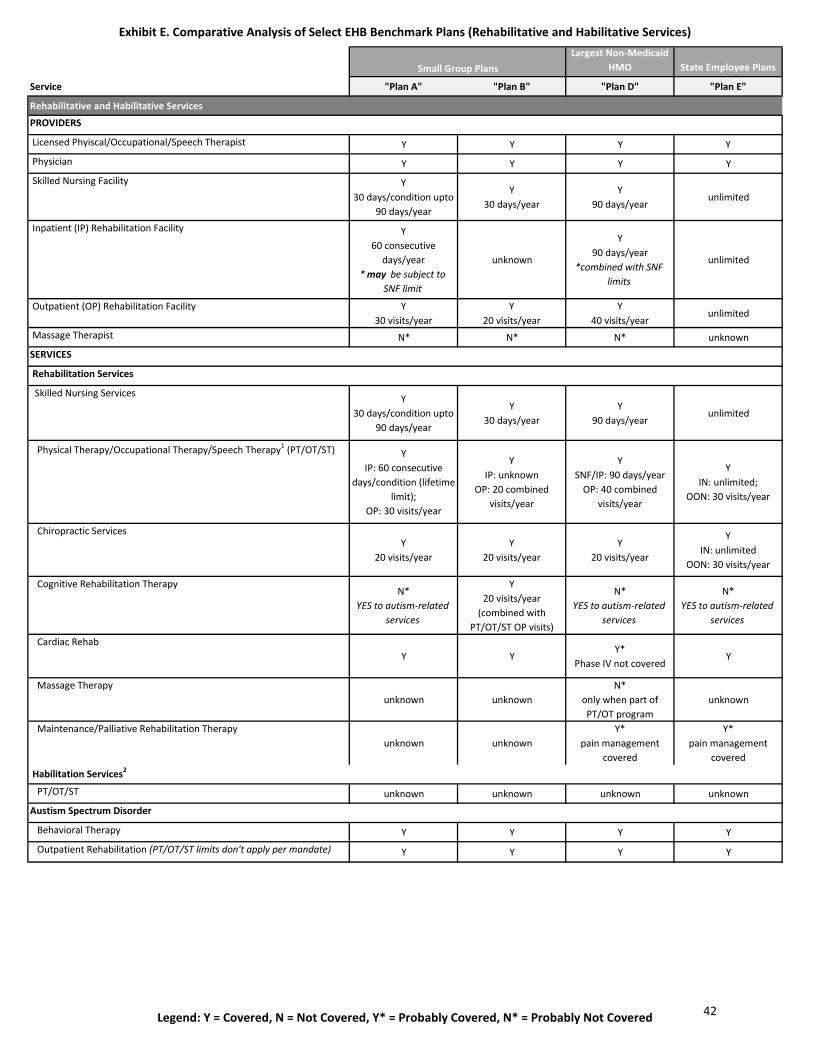

The most meaningful variation is the durational limits imposed on certain rehabilitative services, such as outpatient PT/OT/ST, chiropractic services, and skilled nursing services.

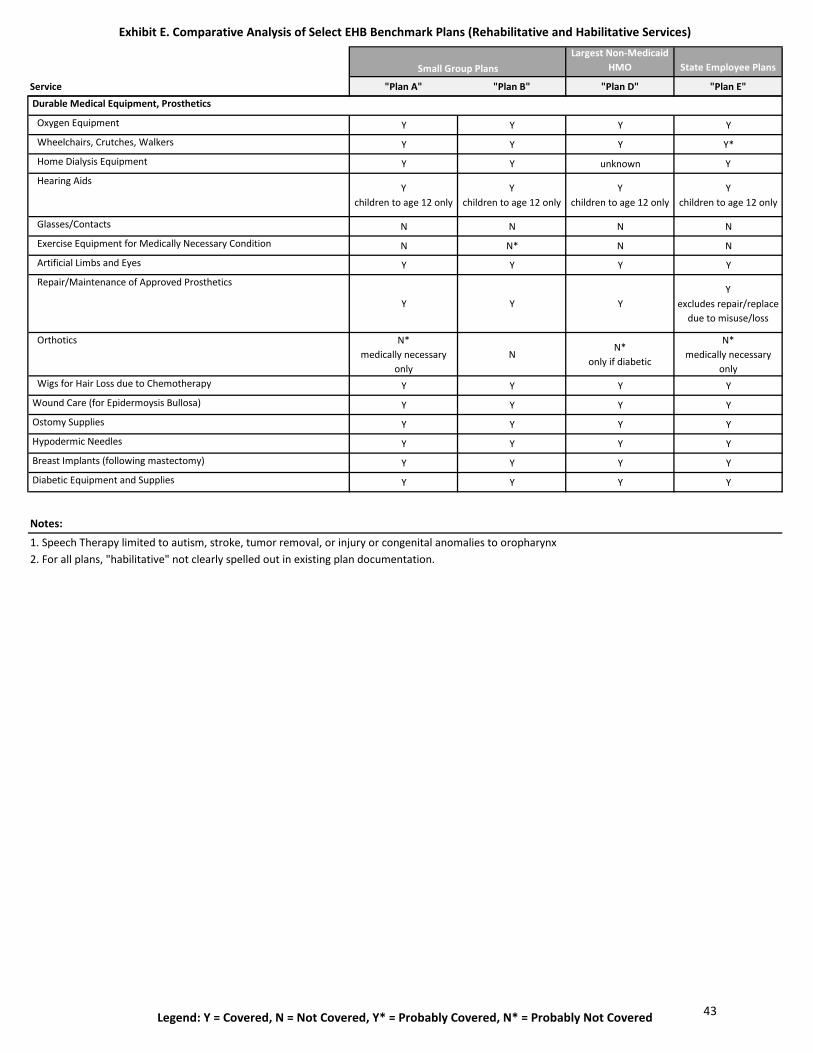

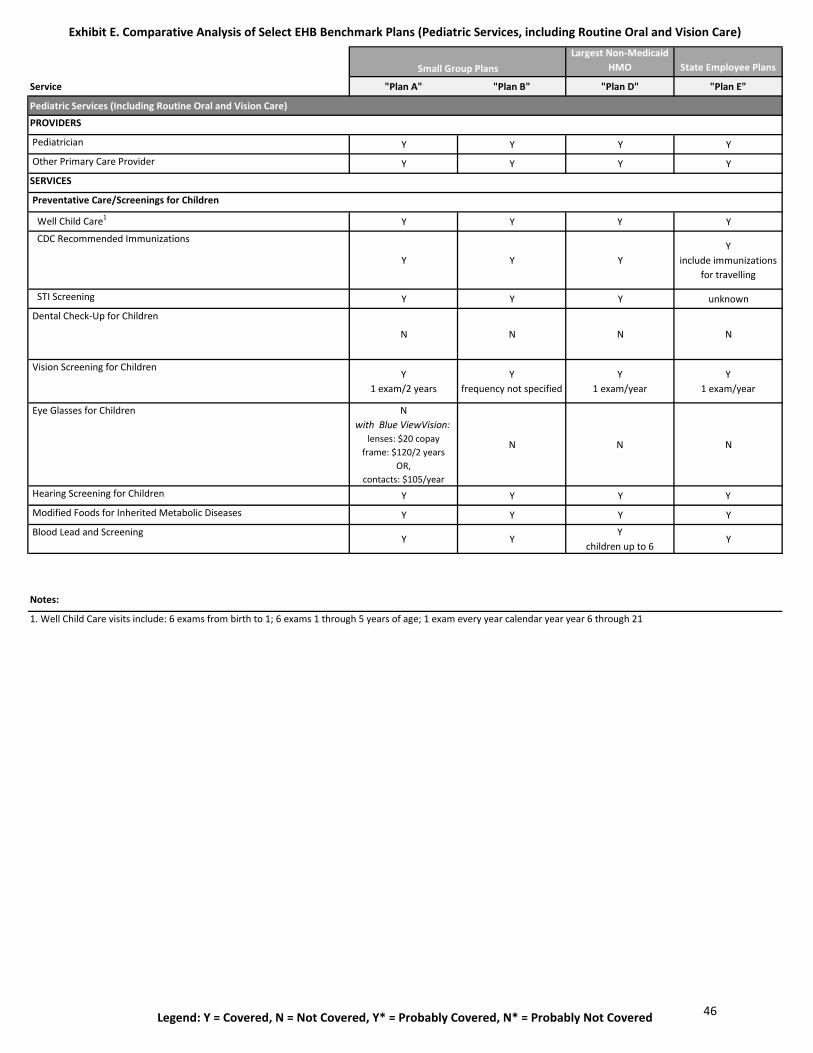

None of the benchmarks provide sufficiently comprehensive coverage for routine pediatric dental care, pediatric vision care, or habilitative services.

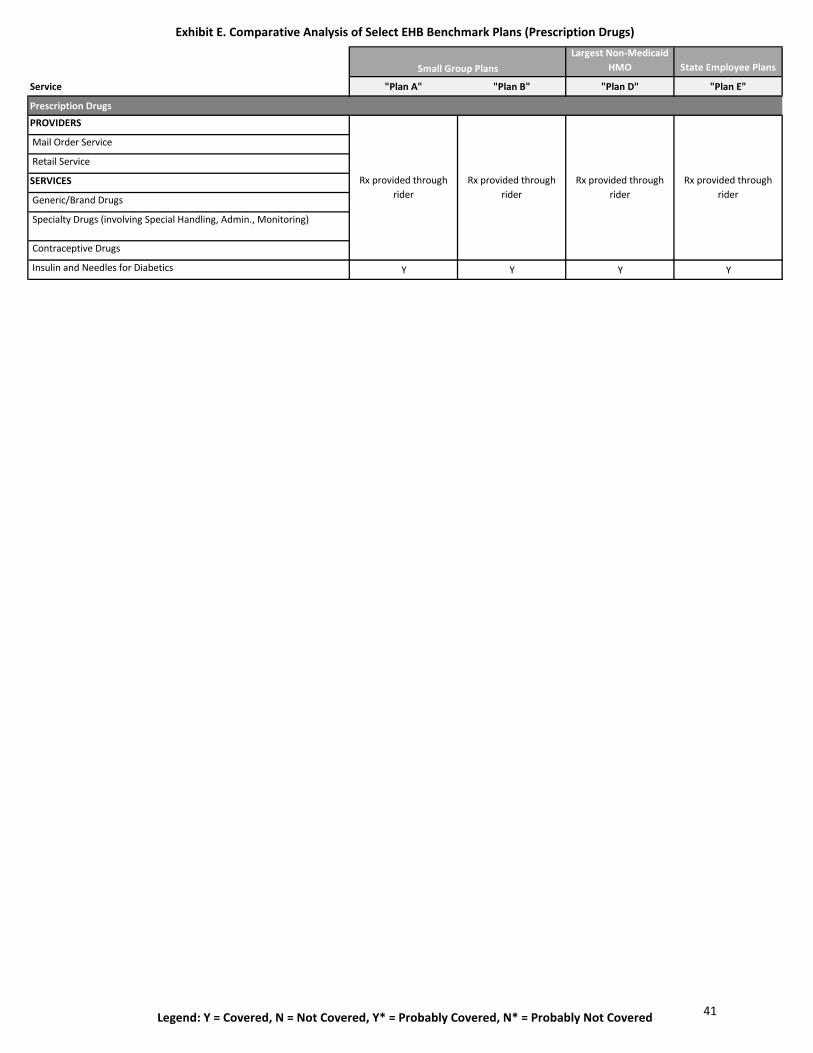

With respect to prescription drug coverage, only the small group “Plan C” and federal plans, “Plan F” and “Plan G,” include coverage as part of their plan. The other benchmarks typically offer prescription drugs through a rider, but this reflects a separate contract that HHS has indicated will be excluded from the benefit offerings of the benchmark plan.

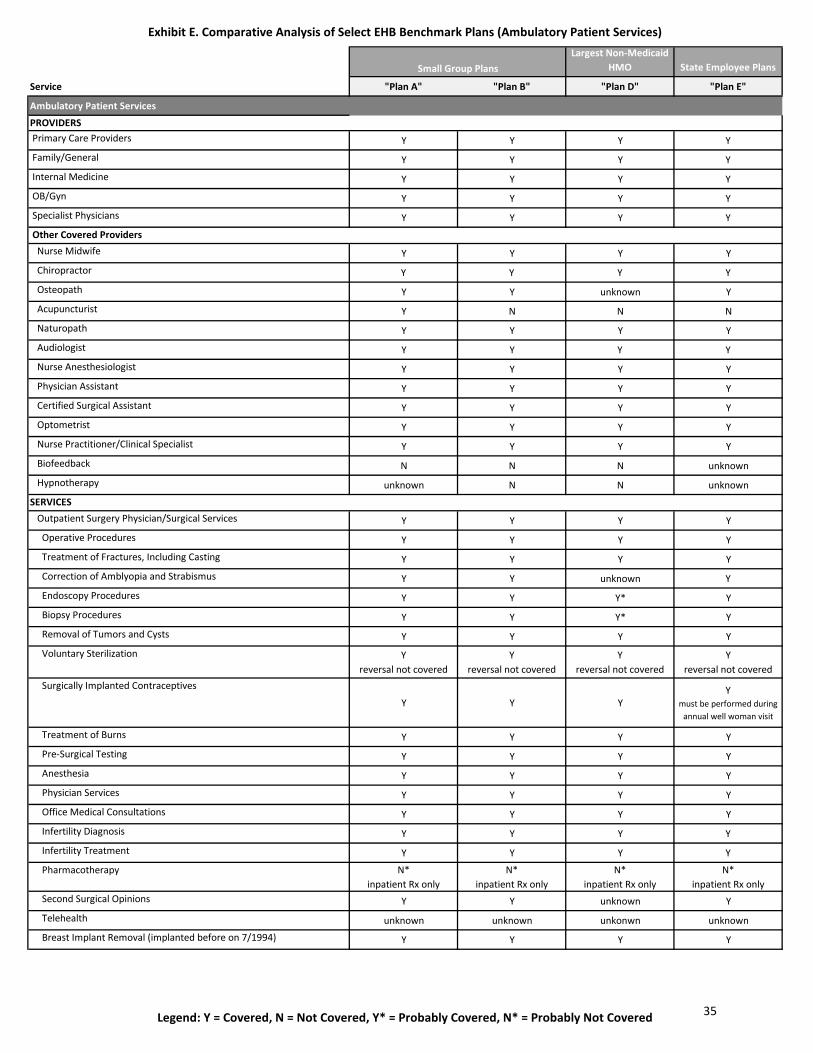

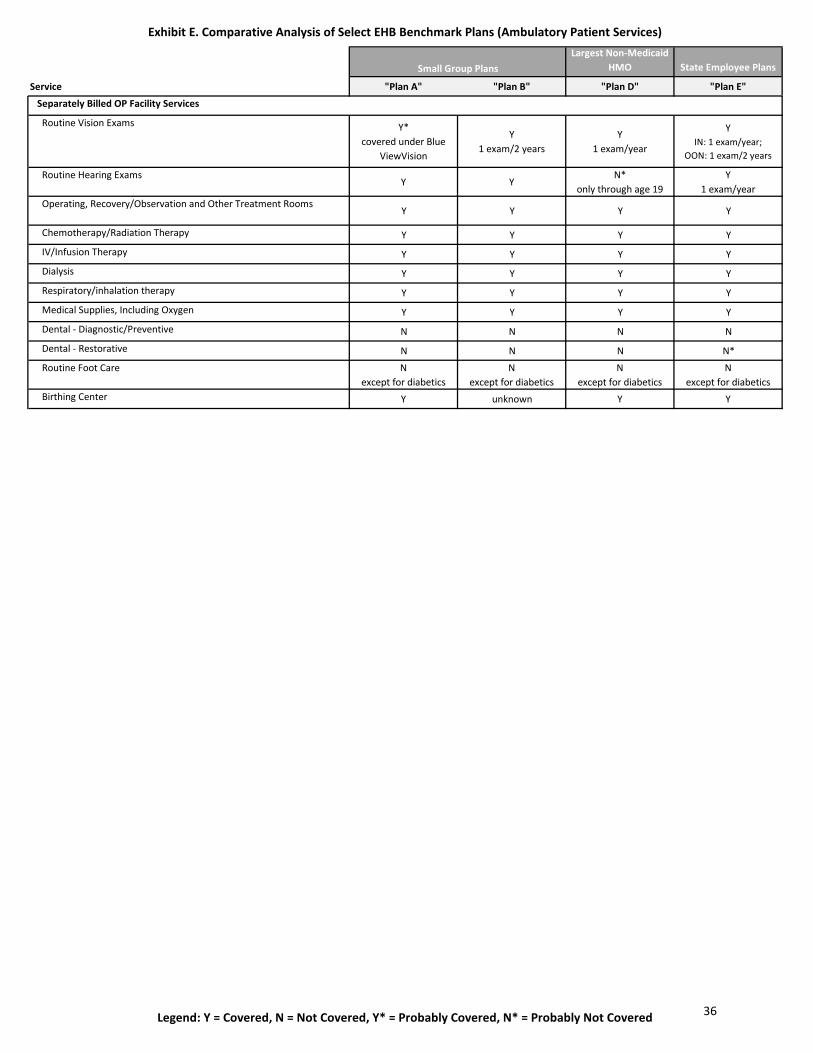

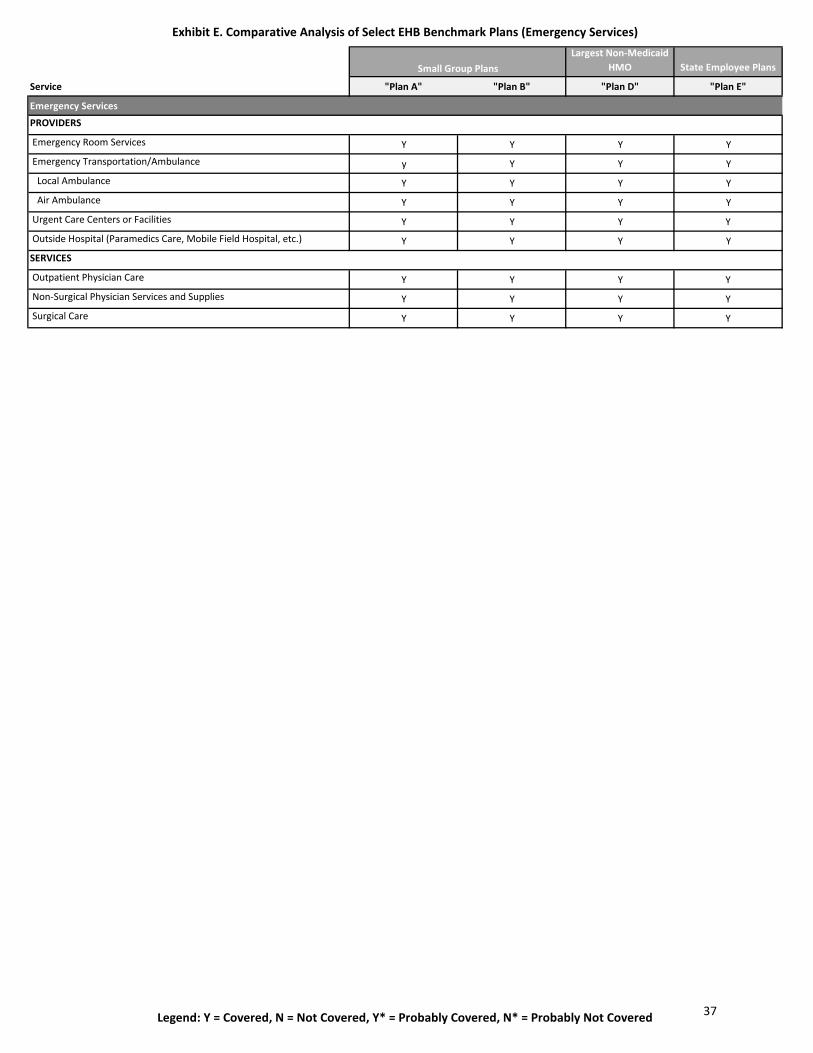

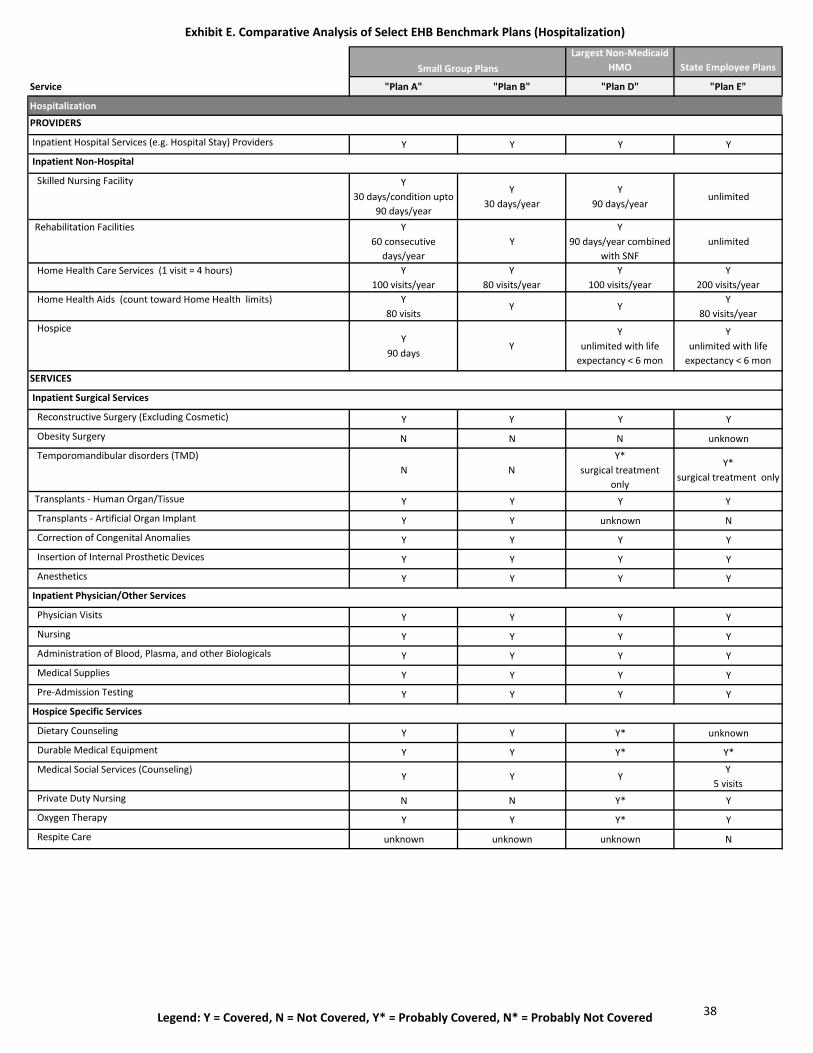

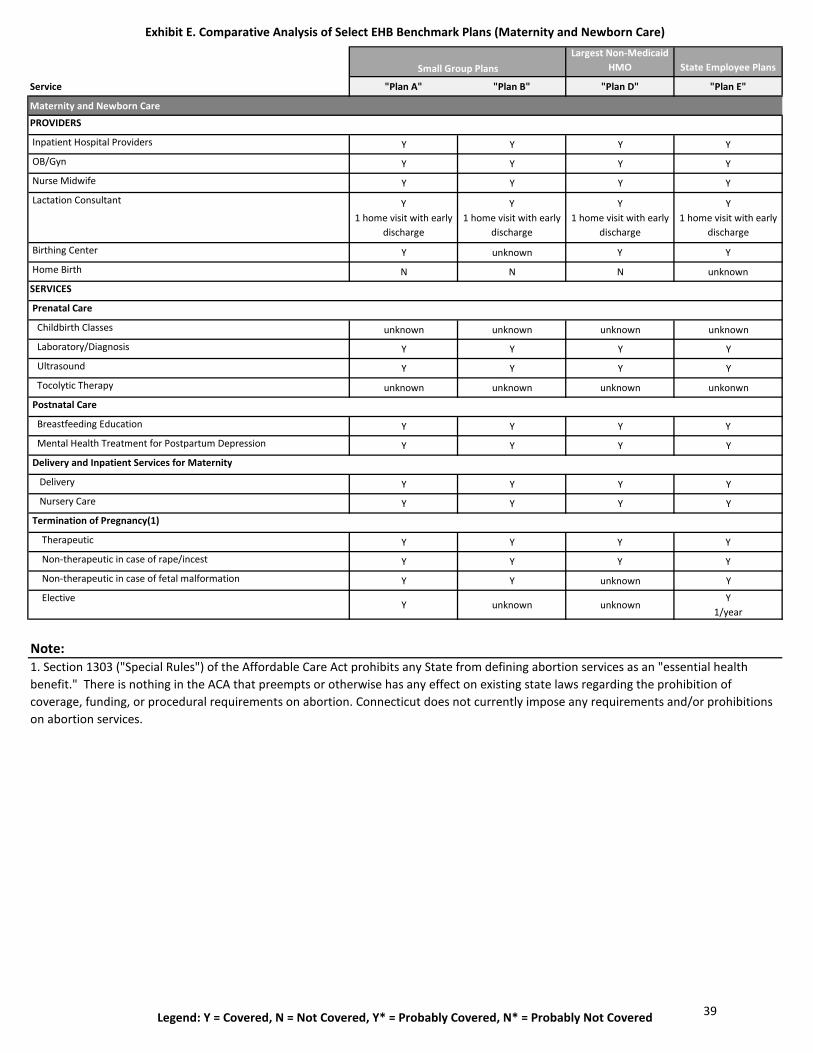

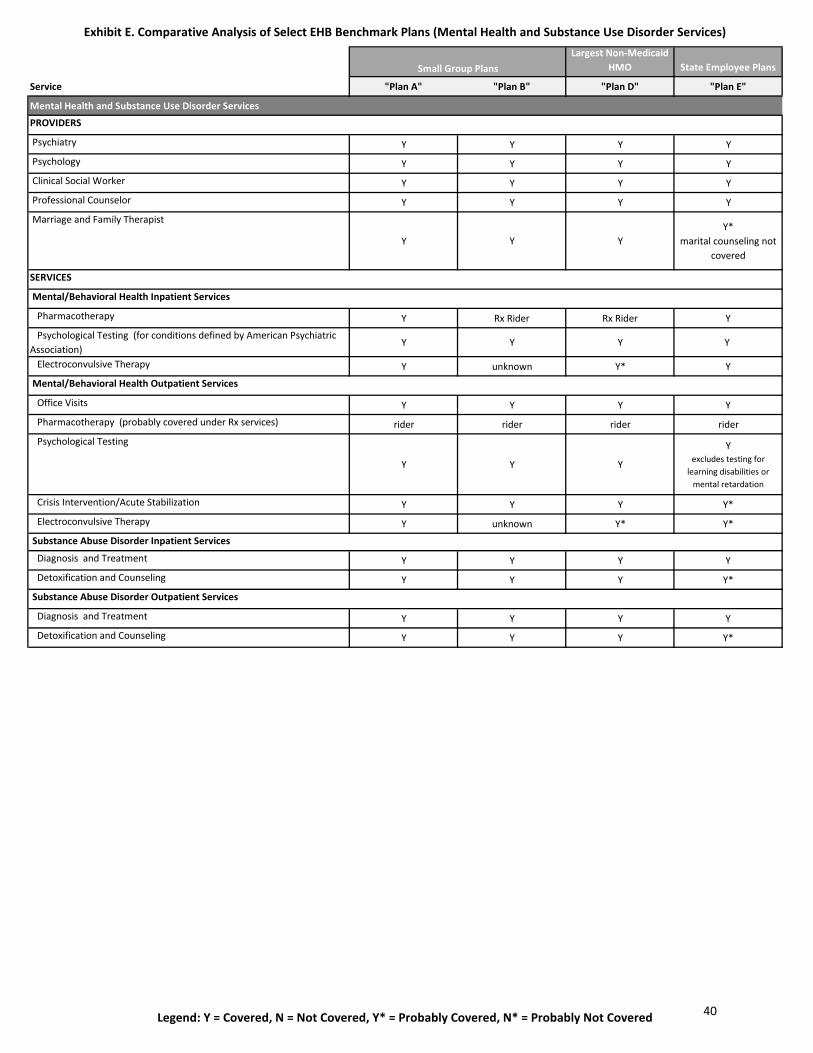

Exhibit E provides a summary analysis of the seven distinct benchmark options. Exchange staff reviewed the carrier’s documentation, including the specific evidence of coverage for each of the benchmark options and their response to a survey of the carriers conducted by the Connecticut Insurance Department in December 2011. The staff’s initial review of the plans prompted inquiries for additional information on certain benefits, exclusions and any limits.

Exhibit F presents a detailed analysis of the small group plan, “Plan B,” the HMO plan, “Plan D” and the state employee plan, “Plan G.”

The following section goes through the process by which the Committee winnowed the choices before it and came to its final recommendation.

Elimination of the FEHBP Plans, “Plan E” and “Plan F”: Exclusion of Certain State Mandates

As discussed in the section on state mandates, the Committee excluded from consideration the FEHBP plans. The primary rationale for their elimination was the exclusion of certain State-mandated benefits

16

in the benchmark plan. The EHB would not preempt Connecticut law and so the State would need to supplement the EHB with any missing mandate and finance any cost associated thereof.

As neither FEHBP plan, “Plan F” and“Plan G,” differed remarkably from the other benchmark options—that is aside from lacking certain state mandates that would nevertheless be included in Connecticut’s EHB—there is no apparent off-setting advantage to selecting a benchmark plan that would impose unnecessary costs on the state. If “Plan F” and “Plan G” could be characterized as having a slightly more restrictive benefits packages (and therefore potentially more affordable) than some of the alternative benchmark options, the variation is not consistent—fewer skilled nursing facility days, fewer chiropractic visists, but more PT/OT visits.

Some members of the Committee raised the argument that selecting one of the slightly more restrictive FEHBP plan designs could avoid unnecessary revisions to the state’s EHB in the future if HHS revisits, as its has indicated it intends to do so, the benchmark approach and its treatment of State benefit mandates for plan years starting in 2016.

The Committee acknowledges that the benefits included in a FEHBP benchmark plan will likely become the basis for a federally-defined EHB; although, there is no guarantee that this hypothetical EHB would exactly resemble a FEHBP plan. Other than the IOM’s report—while the best arbiter of how the Secretary might approach defining the EHB is not a federal regulation—there is no explicit guidance describing how the Secretary will interpret the charge that the scope of the EHB shall equal the scope of benefits provided under a typical employer plan.

Elimination of Small Group Plans, “Plan A” and “Plan C”: Lifetime Visitation Limits

The Committee—along with the Consumer Outreach and Experience Advisory Committee—expressed concern over the lifetime durational limits included in “Plan C.” According to the plan’s evidence of coverage, inpatient/outpatient rehabilitation care is limited to 60 consecutive days/visits per condition: meaning an individual could get up to 60 days of inpatient services followed by 60 visits for outpatient services for each condition. These are lifetime—not annual—durational limits. For each condition the individual will initiate a new 60 day/60 visit limit. For the purposes of the rehabilitation coverage, “per condition” means the disease or injury causing the need for the therapy.

It should be emphasized that none of the benchmark options cover rehabilitative services on a long-term basis and so irrespective of a plan’s contracted durational limits, most benefits have implicit lifetime limits on the number of allowed visits. However, if an individual were to suffer a illness or injury requiring intensive rehabilitation over a number of years an explicit lifetime durational limit could be financially catastrophic.

Two reforms attributed to requirements of the ACA make the inclusion of a lifetime durational limit on a medically-necessary service unnattractive to the EHB.

First, the inclusion of people with pre-existing conditions will likely increase demand for certain services, including rehabilitative services.

Second, because the rehabilitative benefit, and presumably any limits thereof, may be used to define a plan’s habilitative benefits, a lifetime limit could diminish the value of the new benefit. Without any utilization data there is no reference point for suggesting the appropriateness of a lifetime durational limit. Further, it is unclear how the provision of habilitative services will be affected by the typical restrictions against providing long-term care and so the Committee does not want to prematurely restrict necessary treatments.

17

Similar to “Plan C,” “Plan A” includes a lifetime durational limit and so it is similarly not recommended.

EHB Selection: Balancing Comprehensiveness and Affordability

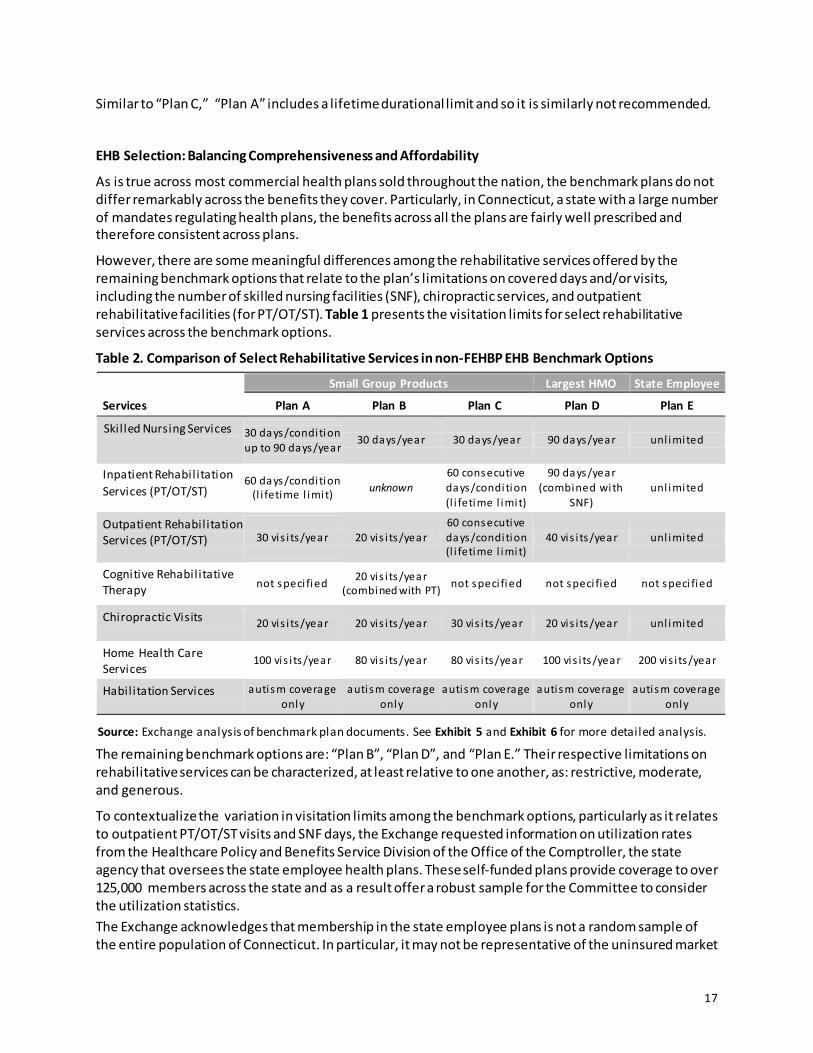

As is true across most commercial health plans sold throughout the nation, the benchmark plans do not differ remarkably across the benefits they cover. Particularly, in Connecticut, a state with a large number of mandates regulating health plans, the benefits across all the plans are fairly well prescribed and therefore consistent across plans.

However, there are some meaningful differences among the rehabilitative services offered by the remaining benchmark options that relate to the plan’s limitations on covered days and/or visits, including the number of skilled nursing facilities (SNF), chiropractic services, and outpatient rehabilitative facilities (for PT/OT/ST). Table 1 presents the visitation limits for select rehabilitative services across the benchmark options.

Table 2. Comparison of Select Rehabilitative Services in non-FEHBP EHB Benchmark Options

The remaining benchmark options are: “Plan B”, “Plan D”, and “Plan E.” Their respective limitations on rehabilitative services can be characterized, at least relative to one another, as: restrictive, moderate, and generous.

To contextualize the variation in visitation limits among the benchmark options, particularly as it relates to outpatient PT/OT/ST visits and SNF days, the Exchange requested information on utilization rates from the Healthcare Policy and Benefits Service Division of the Office of the Comptroller, the state agency that oversees the state employee health plans. These self-funded plans provide coverage to over 125,000 members across the state and as a result offer a robust sample for the Committee to consider the utilization statistics. The Exchange acknowledges that membership in the state employee plans is not a random sample of the entire population of Connecticut. In particular, it may not be representative of the uninsured market

Small Group Products Largest HMO State Employee

Services Plan A Plan B Plan C Plan D Plan E

Skil led Nursing Services 30 days/condition up to 90 days/year

30 days/year 30 days/year 90 days/year unl imited

Inpatient Rehabilitation Services (PT/OT/ST)

60 days/condition (l i fetime l imit) unknown

60 consecutive days/condition (l i fetime l imit)

90 days/year (combined with

SNF) unl imited

Outpatient Rehabilitation Services (PT/OT/ST) 30 vis i ts/year 20 vis i ts/year

60 consecutive days/condition (l i fetime l imit)

40 vis i ts/year unl imited

Cognitive Rehabilitative Therapy not speci fied 20 vis i ts/year

(combined with PT) not speci fied not speci fied not speci fied

Chiropractic Visits 20 vis i ts/year 20 vis i ts/year 30 vis i ts/year 20 vis i ts/year unl imited

Home Health Care Services

100 vis i ts/year 80 vis i ts/year 80 vis i ts/year 100 vis i ts/year 200 vis i ts/year

Habil itation Services autism coverage only

autism coverage only

autism coverage only

autism coverage only

autism coverage only

Source: Exchange analysis of benchmark plan documents. See Exhibit 5 and Exhibit 6 for more detailed analysis.

18

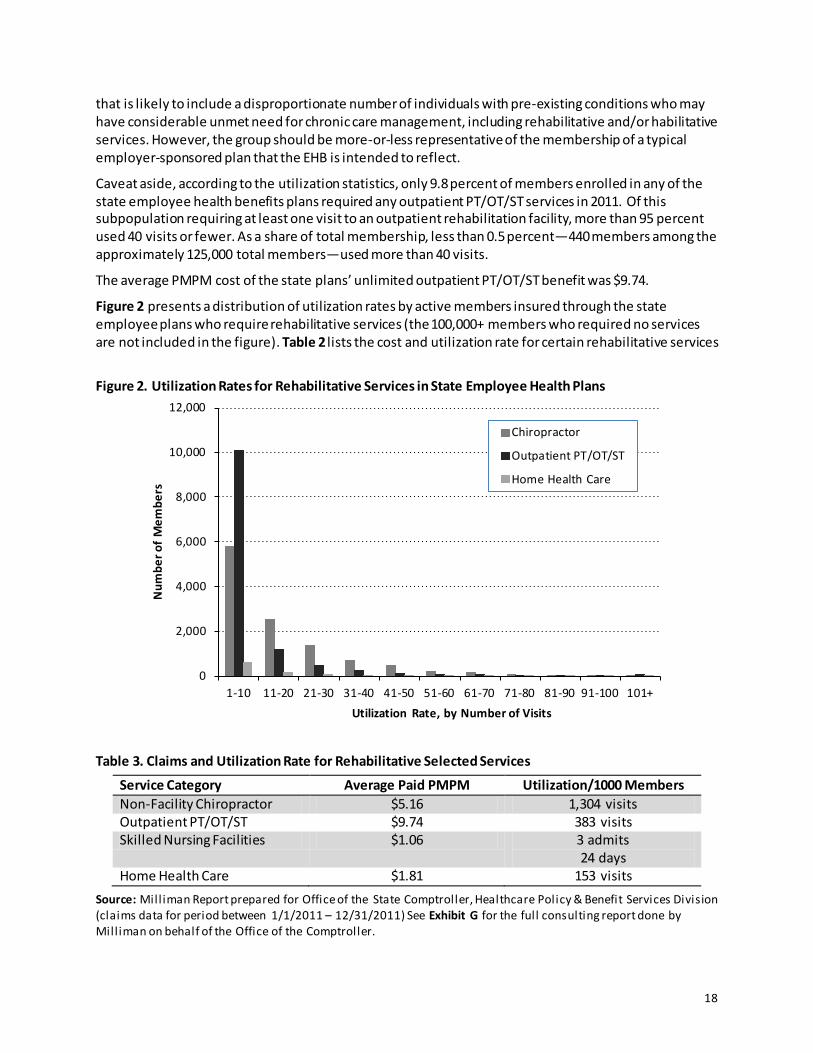

that is likely to include a disproportionate number of individuals with pre-existing conditions who may have considerable unmet need for chronic care management, including rehabilitative and/or habilitative services. However, the group should be more-or-less representative of the membership of a typical employer-sponsored plan that the EHB is intended to reflect.

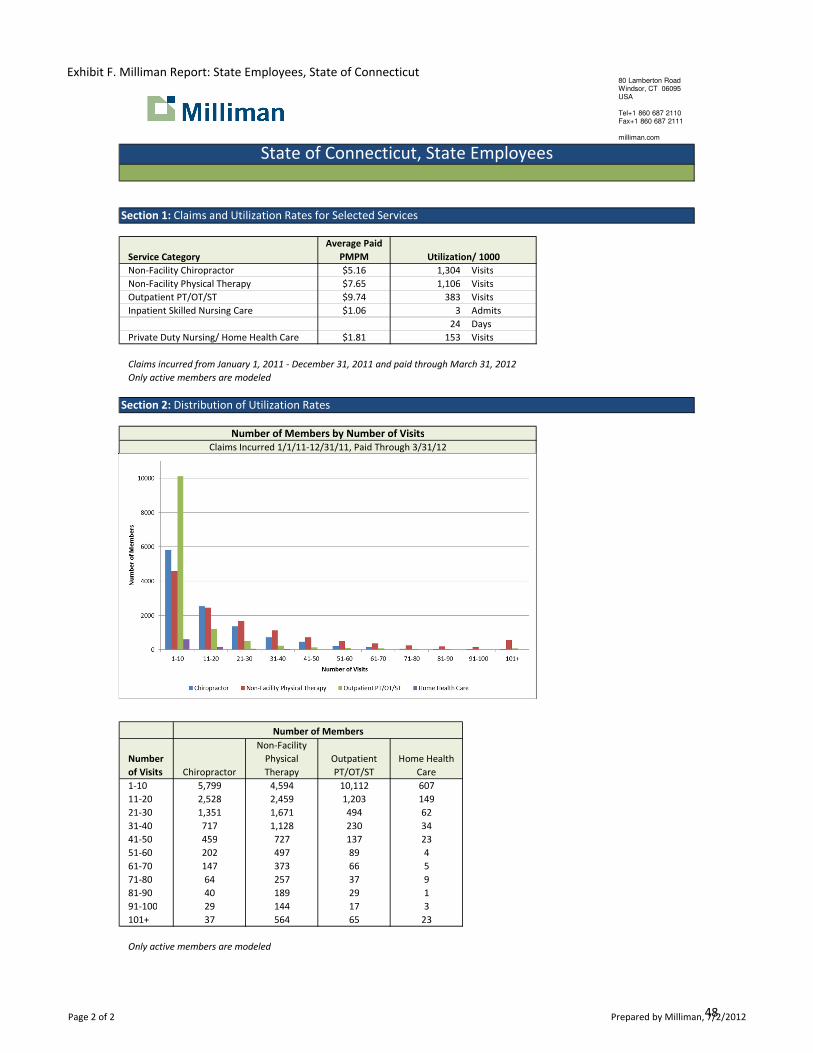

Caveat aside, according to the utilization statistics, only 9.8 percent of members enrolled in any of the state employee health benefits plans required any outpatient PT/OT/ST services in 2011. Of this subpopulation requiring at least one visit to an outpatient rehabilitation facility, more than 95 percent used 40 visits or fewer. As a share of total membership, less than 0.5 percent—440 members among the approximately 125,000 total members—used more than 40 visits.

The average PMPM cost of the state plans’ unlimited outpatient PT/OT/ST benefit was $9.74.

Figure 2 presents a distribution of utilization rates by active members insured through the state employee plans who require rehabilitative services (the 100,000+ members who required no services are not included in the figure). Table 2 lists the cost and utilization rate for certain rehabilitative services

Figure 2. Utilization Rates for Rehabilitative Services in State Employee Health Plans

Table 3. Claims and Utilization Rate for Rehabilitative Selected Services

Service Category Average Paid PMPM Utilization/1000 Members Non-Facility Chiropractor $5.16 1,304 visits Outpatient PT/OT/ST $9.74 383 visits Skilled Nursing Facilities $1.06 3 admits

24 days Home Health Care $1.81 153 visits

Source: Mill iman Report prepared for Office of the State Comptroller, Healthcare Policy & Benefit Services Division (claims data for period between 1/1/2011 – 12/31/2011) See Exhibit G for the full consulting report done by Mill iman on behalf of the Office of the Comptroller.

0

2,000

4,000

6,000

8,000

10,000

12,000

1-10 11-20 21-30 31-40 41-50 51-60 61-70 71-80 81-90 91-100 101+

Num

ber o

f Mem

bers

Utilization Rate, by Number of Visits

Chiropractor

Outpatient PT/OT/ST

Home Health Care

19

Elimination of “Plan E”: Too Generous

The state employee plan, “Plan G,” is not recommended because defining the State’s minimum standard with a health plan that has unlimited visit and day limits for certain rehabilitative services is too generous a standard for the entire market. From an affordability perspective, the Committee believes it would be irresponsbile for the State to select the most generous benchmark as its minimum standard for benefits, as that could potentially spur inflation in premium rates.

Even though the vast majority of the insured use fewer than 20 or 40 outpatient PT/OT/ST visits/year, there is still value to having a visit limit.

Evidence from Medicare demonstrates the potentially adverse effect on health care spending that can result from shifting from a defined benefit to an unlimited benefit. While there are certainly other causal factors at work and Medicare’s fee-for-service model may encourage greater utilization than compared to the HMO model that is typical in the Connecticut market, the elimination of a defined spending cap on Medicare’s rehabilitative benefit had an undeniably precipitous correlation with an increase in overall spending, and without any apparent corresponding improvement in overall health outcomes. For example, a steady and significant increase in Medicare spending immediately followed the lifting of an expenditure cap on rehabilitation therapy in 1999: between 2000 and 2004, total Medicare spending on outpatient rehabilitative services more than doubled; between 2004 to 2008 the volume of services increased by an average annual rate of 7.5 percent per beneficiary; and from 2008 to 2009, annual per beneficiary growth increased to 11.2 percent. (Medpac, various reports)

The selection of the benefits package represented by “Plan G,” with its unlimited visits would effectively impose a new mandate on all carriers and consumers in the state that the Committee feels is neither necessary nor equitable.

Elimination of “Plan B”: Too Restrictive

The Committee believes that the 30 day/year limit on skilled nursing facilities (SNF) and the 20 combined visits/year for outpatient rehabilitation services is too restrictive a benefit. The limitations could be financially catastrophic for those few individuals requiring the care.

As the Committee justified the elimination “Plan A” and “Plan C” (with their lifetime limits), two reforms attributed to requirements of the ACA make the inclusion of an overly restrictive limit on a medically-necessary service unnattractive: (1) the inclusion of people with pre-existing conditions, and; (2) uncertainty over how the habilitative services benefit will be implemented by the carriers.

A Committee member countered the elimination of “Plan B” by arguing that the EHB is only a minimum standard for the state. Irrespective of the visitation limits included in the EHB, carriers can continue to offer a more generous benefits packages. And as is represented by the current market, they will likely continue to differentiate themselves on their rehabilitative services. For the same reasons used to justify not selecting a Benchmark with an unlimited rehabilitative services benefit, the state should not impose any undo requirements on the carriers, whether or not the selected benchmark is considered “moderate” from a comparative perspective.

However, the ACA’s prohibition against insurers denying coverage to individuals with a pre-existing condition greatly expands the threat that risk selection poses. Insurers are likely be more cautious with deviating from their competitors in terms of their plans’ benefit limits for fear of attracting sicker individuals–the carriers are more likely to compete on quality of service, not its quantity.

For these reasons, the Committee concluded that “Plan B’s” rehabilitative service benefit sets too low a precedent for the EHB.

20

Selection of “Plan D”

As a minimal standard, the Committee recognizes that the 40 combined visit/year limit on outpatient PT/OT/ST visits and 90 days/year of skilled nursing services included in “Plan D” is equitable and sufficiently comprehensive for nearly every resident in the state.

“Plan D” imposes a limit of 20 visits/year on chiropractic visits, the same as the other small group product benchmarks. While the State offers unlimited benefits, the 20 visit/year limit seems more aligned with a “typical employer plan.”

Some members voiced concern over the potential cost of requiring every QHP to insure up to 90 days/year of SNF services. While this benefit should not be mistaken for long-term nursing home care,9 extended SNF services can still be extremely costly.

Fortunately, utilization of short-term SNF services among the non-elderly and non-disabled population is extremely limited:10 based on utilization and reimbursement data from the state employee plans (that have an unlimited in-network SNF benefit), the utilization rate of SNF services averaged just 3 admissions/1,000 members, with an average of 8 days per admission. The average PMPM cost of the state plans’ unlimited SNF benefit was $1.06.

As such, the effective premium differential between a 30 day/year (as in “Plan B”) and a 90 day/year limit (as in “Plan D”), while certainly not be 0, should be close to immaterial.

Although the Committee understands that imposing any limits will mean that some individuals will potentially face unanticipated out-of-pocket expenses that could be considered catastrophic for some, it believe the limits included in “Plan D” strike a proper balance. While more generous than “Plan B” and therefore potentially more costly, the higher utilization limits should be viewed as relatively cheap protection against the costs of catastrophic injury or illness.

EHB Benchmark Recommendation:

“Plan D”

9 As with all the benchmark options, SNF services include only short-term skil led nursing and intense rehabil itation services to beneficiaries, typically after a stay in an acute care hospital. Examples of SNF patients include those recovering from surgical procedures, such as hip and knee replacements, or from medical conditions, such as stroke and pneumonia. While most SNFs are part of nursing homes that furnish long-term care, the SNF provisions do not cover long-term care or strictly custodial care. 10 As a point of comparison, among Medicare fee-for-service members, util ization of SNF services was an average of 72 admissions per 1000 members; with each admit averaging 27.3 days (Medpac, 2011).

21

V. Supplemental Coverage

The benchmark package defined by “Plan D” needs to be augmented with supplemental coverage to provide sufficiently comprehensive care across each of the ten categories of care. Those categories that require supplementation include:

• Prescription Drugs • Pediatric Dental Care 11 • Pediatric Vision Care • Habilitative Services

With the exception of prescription drug coverage, which, while often included as a rider, is generally part of most major medical health insurance plans and reflected in the plans’ base premium, the other supplemental benefits are not typically included in any existing employer-sponsored plan.

The Exchange proposes the following supplemental benefits for the fulfillment of the requirement that the EHB package provides coverage across all ten categories of care.

Prescription Drug Coverage

The potential benchmark options for prescription drug coverage are:

• “Plan C” • “Plan F” • “Plan G”

With respect to coverage for prescription drugs, the Bulletin notes that HHS intends to propose that “If a benchmark plan offers a drug in a certain category or class, all plans must offer at least one drug in that same category or class, even though the specific drugs on the formulary may vary.” The plans’ exact formularies and their cost-sharing arrangments (i.e. drug tiers) may differ, but these are irrelevant differences for the purpose of defining the EHB benchmark.

On behalf of the Exchange, RLCarey Consulting worked with a pharmacy benefits consultant to evaluate the categories and classes of drugs covered by the prescription drug formularies included in the base medical benefit of “Plan C” and “Plan F” (a FEHBP benchmark options). The purpose of this assessment was to determine whether “Plan C” differed from a FEHBP plan, in any respect, with regard to the categories and classes of drugs covered.

The review of formularies concluded that both plans cover the same categories or classes of drugs.

For example, the Oxford PPO plan covers a medication called Alfuzosin, which is in a class of drugs called alpha blockers used for BPH. This drug is one of the few not listed in the FEHBP formulary. However, the FEHBP Rx plan covers Doxazosin, which is also an alpha blocker used for BPH.

The selection of either as the benchmark prescription drug plan for the EHB benchmark will have the same effect with regard to the categories or classes of drugs that must be covered by all QHP sold in

11 While Connecticut has a state mandate that requires all individual and small group plans to include coverage for general anesthesia, nursing and related hospital services provided in conjunction with in-patient, outpatient or one-day dental services that are deemed medically necessary, the benefit does not include routine dental care (section 38-491a and section 38-517a of Chapter 700c).

22

the individual and small group markets in 2014. Both formularies are equivalent in terms of the categories or classes of drugs that they cover.

Connecticut Prescription Drug Mandates

An area where the prescription drug benefits included in “Plan C” differ from that included in any of the FEHBPP plans is with respect to state mandates.

Chapter 700c of the Connecticut statutes includes two mandates affecting prescription drugs:

• Section 38a-503e: guaranteed coverage of prescription contraceptives for women, and; • Section 38a-518b: coverage of the off-label use of FDA-approved prescription drugs for

treatment of cancer, chronic diseases.

First, and consistent with recent federal regulations issued by HHS, all small group drug plans sold in the State must provide for the coverage of FDA-approved prescription contraceptives. Prescription contraceptives are included for the FEHBP plans. And so, from the perspective of this state mandate the benchmark options do not differ.

Second, and relevant to a discussion of the differences among the prescription drug options, Connecticut mandates that any group drug plan cover the off-label use of FDA-approved prescription drugs for the treatment of certain types of cancer or disabling or life-threatening chronic diseases. The off-label use of drugs is considered experimental/investigational by many payers and typically not covered by insurance products. Both FEHBP plans exclude experimental and/or investigational services. While these plans offer expanded drug benefits for treatment of cancer, neither explicitly defines the off-label use of drugs as a covered benefit in their certificates of coverage.

The selection of a benchmark does not preempt state law. Therefore, given that the plans are otherwise equal, the Committee recommends the prescription drug benefit included in “Plan C” as it covers the State mandate for the off-label coverage of drugs.

Supplemental Prescription Drug Coverage Recommendation:

“Plan C”

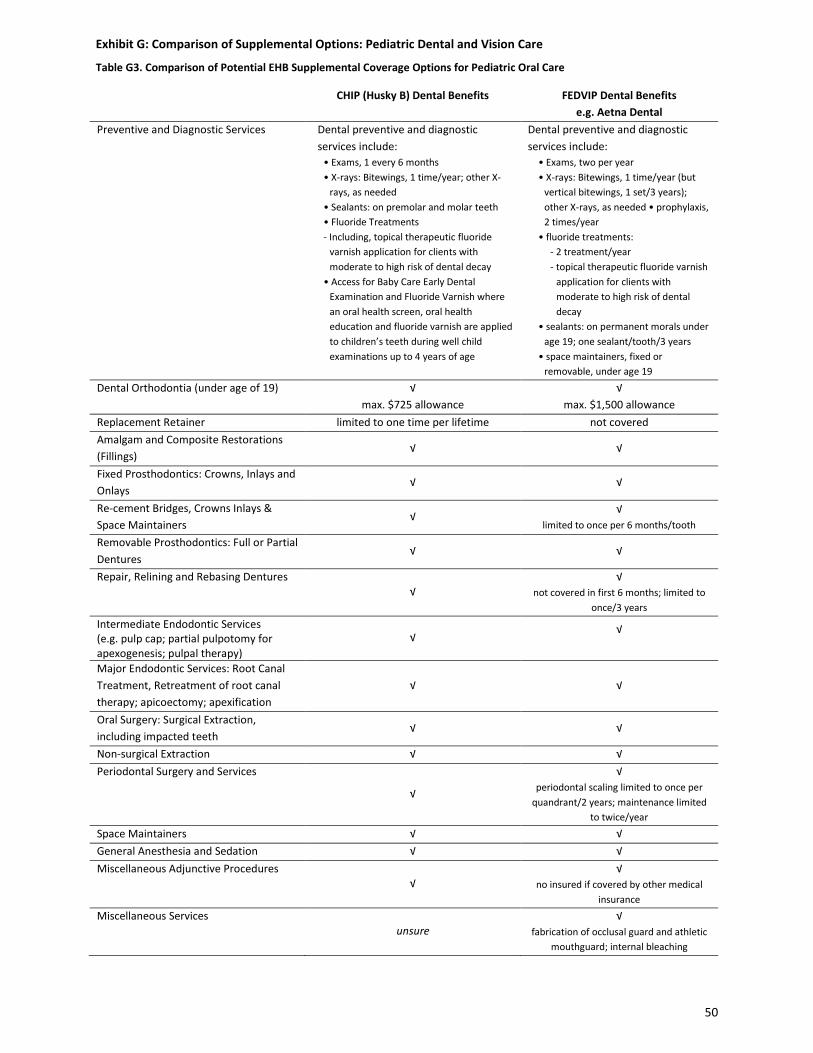

Pediatric Dental Care Coverage

Coverage of dental and vision care services are typically provided through a mix of comprehensive health coverage plans and stand-alone coverage separate from the major medical coverage.

With respect to pediatric oral care, the February FAQ issued by the federal government, provided some additional guidance. The FAQ indicated that the states could—subject to a final rule—supplement the selected benchmark plan with benefits from either:

• the Federal Employees Dental and Vision Insurance Program (FEDVIP) dental plan with the largest national enrollment; or

• the State’s separate Children’s Health Insurance Program (CHIP), Husky B

Both the state’s CHIP and the FEDVIP dental plans cover preventive and basic dental services such as cleanings and fillings, as well as advanced dental services such as root canals, crowns and medically necessary orthodontia. The December Bulletin clarifies, “We intend to propose the EHB definition would not include non-medically necessary orthodontic benefits.” (p. 11)

23

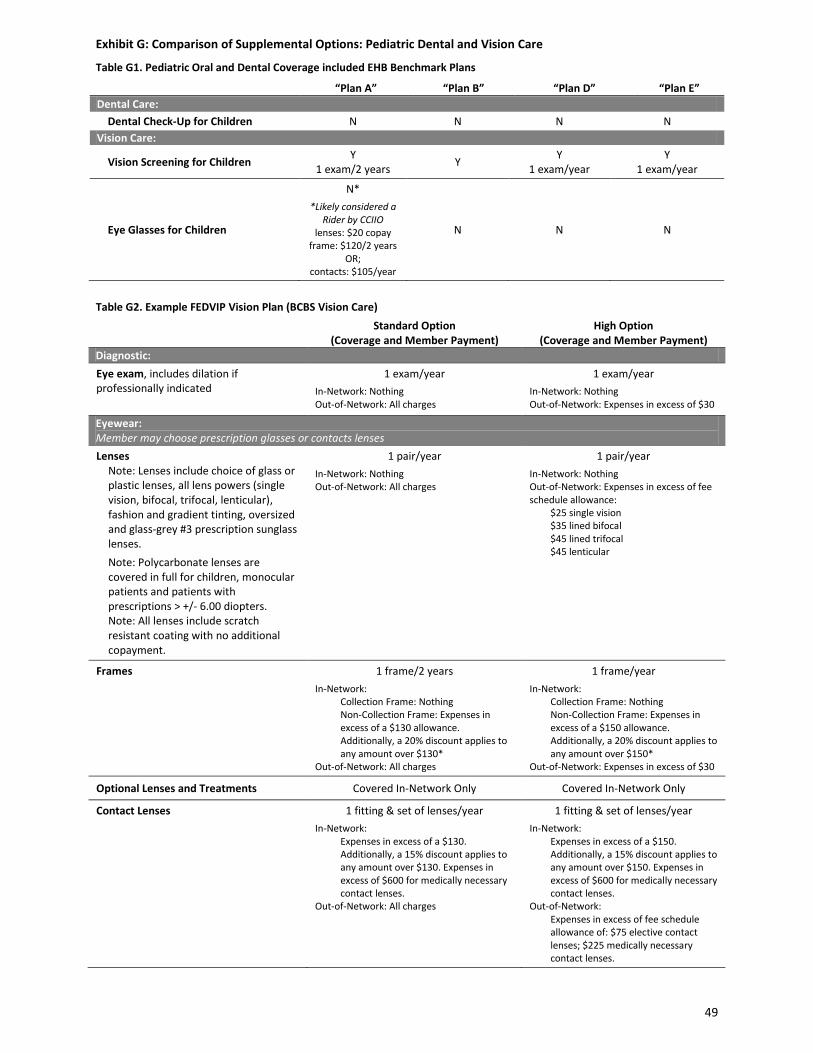

Exhibit G includes a table comparing Connecticut’s current Husky B dental benefits and, as an example of the FEDVIP dental benefits, Aetna’s Nationwide Dental Plan.

There are no meaningful differences in coverage of benefits. Nonetheless a decision must be rendered. The Committee recommends the dental care benefits provided by the state’s Children Health Insurance Program (CHIP), Husky B.

Supplemental Pediatric Dental Care Recommendation:

“CHIP-Husky B”

Pediatric Vision Care Coverage

Most of the benchmark options include annual or bi-annual vision screening for members—adults and children. This benefit will continue to be part of the EHB.

However, none of the plans include an allowance for prescription eyeware or contacts and as such, this benefit is insufficiently comprehensive for children.

Given the absence of any alternative for pediatric vision care, the state’s essential health benefit package will be supplemented by the appropriate benefits included in the largest Federal Employee Dental and Vision Insurance Program (FEDVIP).

Supplemental Pediatric Vision Care Coverage:

Nation’s largest “FEDVIP” plan, by enrollment

Habilitative Services

To meet the ACA requirement that the EHB must provide for coverage for all the statutory categories of care, the benchmark must be augmented with a meaningful habilitative care benefit.

There is no generally accepted definition of habilitative services among health plans, and in general, health insurance plans do not identify habilitative services as a distinct group of services. In Connecticut, the autism spectrum disorder mandate (section 38a-514b of chapter 700c) is a likley habilitative care benefit; but this coverage is insufficiently comprehensive for the EHB.

Given the paucity of best-practices, the Bulletin discusses a transitional approach for habilitative services that references the two alternative options that HHS is considering proposing:

• A plan would be required to offer the same services for habilitative needs as it offers for rehabilitative needs and offer them at parity.

• A plan would decide which habilitative services to cover and report the coverage to HHS.

Under either approach, a QHP will be required to offer at least some habilitative benefit.

The Committee has no recommendation.

Supplemental Habilitative Services Coverage:

Carrier’s decision

24

VI. Conclusion

In summary, the Committee recommends to the Board that the state should give strong consideration to an EHB defined by the health benefits included in “Plan D,” supplemented with the dental care benefits provided by CHIP (Husky B), the vision care benefits provided by the largest FEDVIP plan, and the prescription drug benefits included in “Plan C.” The plans will be accorded flexibility to design its habilitative service benefits.

EHB Recommendation:

Benchmark Option – “Plan D”

Prescription Drugs – “Plan C”

Pediatric Dental Care – CHIP-Husky B

Pediatric Vision Care – FEDVIP Vision Plan

Habilitative Care – Carrier’s Decision

25

VII. Exhibits

The following supporting documents are included:

A. Committee Membership and Affiliation B. State Mandated Benefits and Mercer’s Assessment of EHB Status C. Classification of State Mandated Benefits Under the ACA’s Ten Categories of Care D. Summary Analysis of Benchmark Plans E. Detailed Analysis of Select Benchmark Plans F. Milliman Report: State Employees, State of Connecticut G. Comparison of Supplemental Options: Pediatric Dental Care

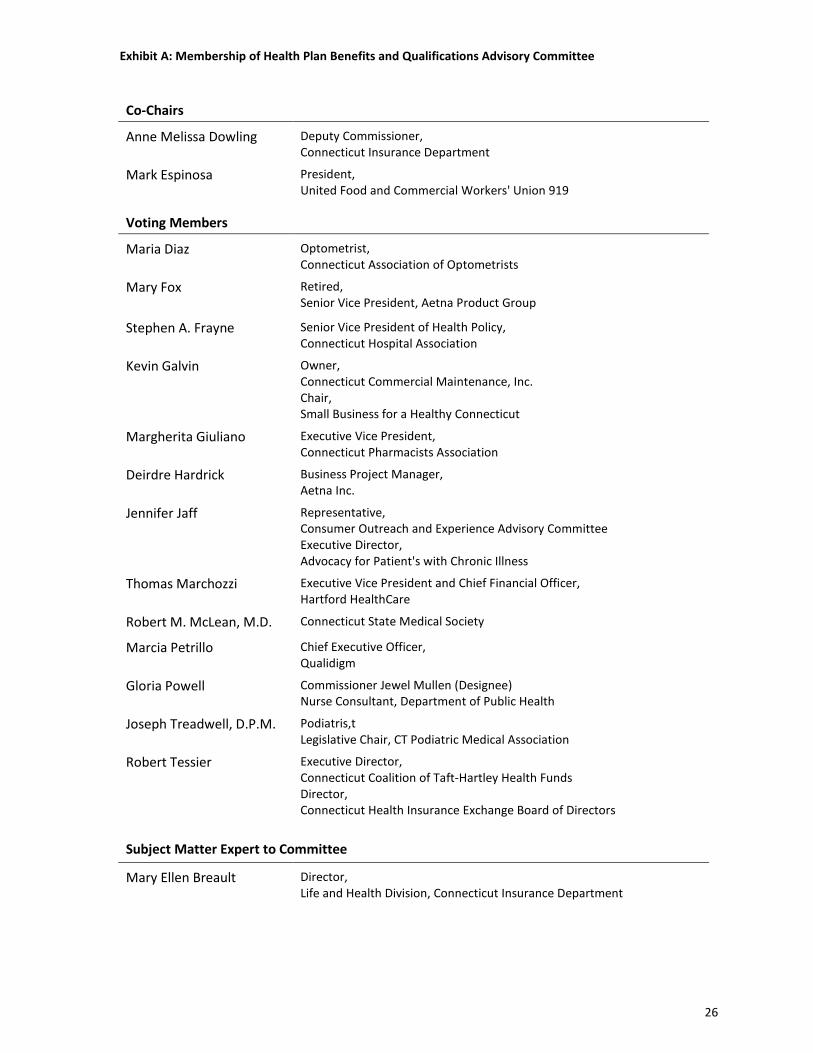

Exhibit A: Membership of Health Plan Benefits and Qualifications Advisory Committee

Co-Chairs

Anne Melissa Dowling Deputy Commissioner, Connecticut Insurance Department

Mark Espinosa President, United Food and Commercial Workers' Union 919

Voting Members

Maria Diaz Optometrist, Connecticut Association of Optometrists

Mary Fox Retired, Senior Vice President, Aetna Product Group

Stephen A. Frayne Senior Vice President of Health Policy, Connecticut Hospital Association

Kevin Galvin Owner, Connecticut Commercial Maintenance, Inc. Chair, Small Business for a Healthy Connecticut

Margherita Giuliano Executive Vice President, Connecticut Pharmacists Association

Deirdre Hardrick Business Project Manager, Aetna Inc.

Jennifer Jaff Representative, Consumer Outreach and Experience Advisory Committee Executive Director, Advocacy for Patient's with Chronic Illness

Thomas Marchozzi Executive Vice President and Chief Financial Officer, Hartford HealthCare

Robert M. McLean, M.D. Connecticut State Medical Society

Marcia Petrillo Chief Executive Officer, Qualidigm

Gloria Powell Commissioner Jewel Mullen (Designee) Nurse Consultant, Department of Public Health

Joseph Treadwell, D.P.M. Podiatris,t Legislative Chair, CT Podiatric Medical Association

Robert Tessier Executive Director, Connecticut Coalition of Taft-Hartley Health Funds Director, Connecticut Health Insurance Exchange Board of Directors

Subject Matter Expert to Committee

Mary Ellen Breault Director, Life and Health Division, Connecticut Insurance Department

26

Exhibit B: State Mandated Health Benefits and M

ercer’s Assessment of Status as an Essential Health Benefit (EHB)

#

CT General

Statutes: Chapter 700c, §

Mandate

Description EHB Status?

(from M

ercer)

Health Service Benefit Mandates

1 38a-476b

Availability of Psychotropic Drugs

No m

ental health care benefit provided under state law, w

ith state funds, or to state employees m

ay limit the

availability of the most effective psychotropic drugs.

unknown

2 38a-483c; 38a-513b

Experimental Treatm

ents Procedures, treatm

ents, or drugs that have completed a Phase III FDA clinical trial. Appeals process expedited for

those with a life expectancy of less than tw

o years. unknow

n

3 38a-488a; 38a-514

Mental Health Parity

Diagnosis and treatment of m

ental or nervous conditions. Coverage cannot differ from the term

s, conditions, or benefits for the diagnosis or treatm

ent of medical, surgical, or other physical health conditions.

Requires a policy to cover a residential treatment facility w

hen a physician, psychiatrist, psychologist, or clinical social w

orker assesses the person and determines that he or she cannot appropriately, safely, or effectively be treated in

another setting.

unknown

4 38a-490; 38a-508; 38a-516; 38a-549

Adopted New

borns Injury and sickness, including care and treatm

ent of congenital defects and birth abnormalities, for new

borns from

birth and for adopted children from legal placem

ent for adoption. yes

6 38a-490a; 38a-516a

Birth-to-Three At least $6,400 per child annually for m

edically necessary early invention services, up to $19,200 per child over three years.

unknown

7 38a-490b; 38a-516b

Children's Hearing Aids Hearing aids for children age 12 and under. Coverage m

ay be limited to $1,000 w

ithin a 24-month period.

unknown

8 38a-490c; 38a-516c

Craniofacial Disorders M

edically necessary orthodontic processes and appliances for treatment of craniofacial disorders for people age 18 or

younger. Coverage is not required for cosmetic surgery.

unknown

9 38a-490d; 38a-535

Blood lead screening and risk assessm

ent Every prim

ary care provider giving pediatric care (excluding hospital emergency room

) shall conduct lead screening and risk assessm

ent *38a-535 mandates broader preventative pediatric care services, listed below

yes

10 38a-492l; 38a-516d

Children with Cancer

Coverage for children diagnosed with cancer after Decem

ber 31, 1999 for neuropsychological testing a physician orders to assess the extent chem

otherapy or radiation treatment has caused the child to have cognitive or

developmental delays. Insurers cannot require pre-authorization for the tests.

unknown

11 38a-491a; 38a-517a

Dental Coverage M

edically necessary general anesthesia, nursing, and related hospital services for in-patient, outpatient, or one-day dental services.

unknown

12 38a-492; 38a-518

Accidental Ingestion or Consum

ption of Controlled Drugs

Emergency m

edical care for the accidental ingestion or consumption of controlled drugs. Coverage is subject to a

minim

um of 30 days inpatient care and a m

aximum

$500 for outpatient care per calendar year. unknow

n

13 38a-492a; 38a-518a

Hypodermic N

eedles and Syringes

Hypodermic needles and syringes prescribed by a prescribing practitioner for adm

inistering medications.

unknown

14 38a-492b; 38a-518b

Off-Label U

se of Prescription Drugs

If the FDA approves a prescription drug, a policy cannot exclude coverage of the drug when it is used for treatm

ent of cancer or disabling or life-threatening chronic diseases.

unknown

15 38a-492c; 38a-518c

Protein Modified Food and

Specialized Formula

Amino acid m

odified and low protein m

odified food products when prescribed for the treatm

ent of inherited m

etabolic diseases and cystic fibrosis. Medically necessary specialized form

ula for children up to age 12. Food and form

ula must be adm

inistered under the direction of a physician. Coverage for preparations, food products, and form

ulas must be on the sam

e basis as coverage for outpatient prescription drugs. unknow

n

16 38a-492d; 38a-518d

Diabetes Treatment

Laboratory and diagnostic tests for all types of diabetes. Medically necessary equipm

ent, drugs, and supplies for insulin-dependent, insulin using, gestational, and non-insulin using diabetes.

yes

17 38a-492e; 38a-518e

Diabetes Self-Managem

ent Training

Outpatient self-m

anagement training prescribed by a licensed health care professional. Coverage is subject to the

same term

s and conditions as other policy benefits. unknow

n

18 38a-492f; 38a-518f

Prescription Drugs Removed

from Form

ulary A prescription drug that has been rem

oved from the list of covered drugs m

ust be continued if the insured was

previously using the drug for the treatment of a chronic illness and it is deem

ed medically necessary.

unknown

27

Exhibit B: State Mandated Health Benefits and M

ercer’s Assessment of Status as an Essential Health Benefit (EHB)

#

CT General

Statutes: Chapter 700c, §

Mandate

Description EHB Status?

(from M

ercer) 19

38a-492g; 38a-518g Prostate Screening

Laboratory and diagnostic tests to screen for prostate cancer for men w

ho are symptom

atic, have a family history, or

are over 50. yes

20 38a-492h; 38a-518h

Lyme Disease Treatm

ent Lym

e disease treatment including not less than 30 days of intravenous antibiotic therapy, 60 days of oral antibiotic

therapy, or both, and further treatment if recom

mended by a rheum

atologist, infectious disease specialist, or neurologist.

unknown

21 38a-492i; 38a-518i

Pain Managem

ent M

andatory access to a pain managem

ent specialist and coverage for pain treatment ordered by such specialist.

unknown

22 38a-492j; 38a-518j

Ostom

y Appliances and Supplies

If policy covers ostomy surgery, policy m

ust also cover up to $1000 per year for medically necessary ostom

y-related appliances and supplies.

unknown

23 38a-492k; 38a-518k

Colorectal Cancer Screening Colorectal cancer screening. Frequency of screening to be based on recom

mendations by the Am

erican College of Gastroenterology.

yes

24 38a-492m

; 38a-518l Prescription Eye Drops

Effective January 1, 2010, policies that provide prescription eye drop coverage cannot deny coverage for prescription renew

als when (1) the refill is requested by the insured person less than 30 days from

either (a) the date the original prescription w

as given to the insured or (b) the last date the prescription refill was given to the insured, w

hichever is later, and (2) the prescribing physician indicates on the original prescription that additional quantities are needed and the refill request does not exceed this am

ount.

unknown

25 38a-492n; 38a-518m

Epiderm

olysis Bullosa Effective January 1, 2010, policies m

ust cover wound care supplies that are m

edically necessary to treat epidermolysis

bullosa (a rare skin disorder) and administered under a physician's direction.

unknown

26 38a-493; 38a-520

Home Health Care

Home health care, including (1) part-tim

e or intermittent nursing care and hom

e health aide services; (2) physical, occupational, or speech therapy; (3) m

edical supplies, drugs and medicines; and (4) m

edical social services. Coverage can be lim

ited to no less than 80 visits per year and, for a terminally ill person, no m

ore than $200 for medical social

services. Coverage can be subject to an annual deductible of up to $50 and a coinsurance of no less than 75%, except

that a high deductible plan used to establish a medical savings account is exem

pt from the deductible lim

it.

unknown

27 38a-496; 38a-524

Occupational Therapy

If policy covers physical therapy, it must provide coverage for occupational therapy.

unknown

28 38a-498; 38a-525

Ambulance Services

Ambulance service w

hen medically necessary. Paym

ent must be on a direct pay basis w

here notice of assignment is

reflected on the bill. unknow

n

29 38a-498c; 38a-525c

Injured and Under the

Influence Insurance polices prohibited from

denying coverage for health care services rendered to an injured insured person if the injury is alleged to have occurred or occurs w

hen the person has an elevated blood alcohol level (0.08% or m

ore) or is under the influence of drugs or alcohol.

unknown

30 38a-503; 38a-530

Mam

mography and Breast

Cancer Screening Baseline m

amm

ogram for w

oman 35 to 39 and one every year for w

oman 40 and older. Additional coverage m

ust be provided for a com

prehensive ultrasound screening of a wom

an's entire breast(s) if (1) a mam

mogram

shows

heterogeneous or dense breast tissue based on BI-RADS or (2) the wom

an is at increased breast cancer risk because of fam

ily history, her prior history, genetic testing, or other indications determined by her physician or advanced-

practice nurse. Coverage is subject to any policy provisions applicable to other covered services.

yes

31 38a-503c; 38a-530c

Minim

um Stay for M

aternity Care

coverage of a minim

um of forty-eight hours of inpatient care for a m

other and her newborn infant follow

ing a vaginal delivery and a m

inimum

of ninety-six hours of inpatient care for a mother and her new

born infant following a

caesarean delivery yes

32 38a-503d; 38a-530d.

Mastectom

y M

inimum

48-hour hospital stay after mastectom

y or lymph node dissection or longer stay if recom

mended by

physician. unknow

n

33 38a-503e; 38a-530e

Contraceptives If prescription drugs are covered, prescription contraceptives m

ust be covered. An employer or individual m

ay decline contraceptive coverage if it conflicts w

ith religious beliefs. yes

28

Exhibit B: State Mandated Health Benefits and M

ercer’s Assessment of Status as an Essential Health Benefit (EHB)

#

CT General

Statutes: Chapter 700c, §

Mandate

Description EHB Status?

(from M

ercer) 34

38a-504a&b; 38a-

542a&b

Treatment for Leukem

ia, Tum

ors, and Wigs for

Chemotherapy Patients

Surgical removal of tum

ors and treatment of leukem

ia, including outpatient chemotherapy, reconstructive surgery,

non-dental prosthesis, surgical removal of breasts due to tum

ors, and a wig if prescribed by a licensed oncologist for a

patient suffering hair loss from chem

otherapy. Annual coverage must be at least $500 for surgical tum

or removal,

$500 for reconstructive surgery, $500 for outpatient chemotherapy, $350 for a w

ig, and $300 for prosthesis, except for surgical rem

oval of breasts due to tumors, the prosthesis benefit m

ust be at least $300 for each breast removed.

yes

35 38a-504c; 38a-542c

Breast Reconstruction after M

astectomy

Reconstructive surgery on non-diseased breast for symm

etrical appearance. Coverage is subject to the same term

s and conditions as other benefits under the policy.

unknown

36 38a-504a–g; 38a-542a–g

Cancer Clinical Trials Routine patient costs relating to cancer clinical trials. O

ut-of-network hospitalization paid as in-netw

ork benefit if services are not available in netw

ork. Such trials must have peer-review

ed protocols approved by one of several federal organizations.

unknown

37 38a-504; 38a-542

Oral Chem

otherapy Effective January 1, 2011, policies that cover intravenously and orally adm

inistered anticancer medications m

ust cover the orally adm

inistered medication on at least as favorable a basis as the intravenously adm

inistered medication.

unknown

38 38a-509; 38a-536

Infertility M

edically necessary costs of diagnosing and treating infertility. unknow

n 39

38a-488b; 38a-514b Autism

Spectrum Disorders

Effective January 1, 2010, policies must cover the diagnosis and treatm

ent of autism spectrum

disorders, including: 1. behavioral therapy for a child age 14 or younger and ; 2. certain prescription drugs and psychiatric and psychological services. A policy can lim

it coverage for behavioral therapy to $50,000 a year for a child age eight or younger, $35,000 for a child age nine to 12, and $25,000 for a 13-or 14-year-old.

unknown

40 38a-523

Comprehensive Rehabilitation

Services Group health insurance m

ust offer coverage for comprehensive rehabilitation services, including: 1.physician services,

physical and occupational therapy, nursing care, psychological and audiological services, and speech therapy; 2. social services provided by a social w

orker; 3. respiratory therapy; 4. prescription drugs and medicines; 5. prosthetic and

orthotic devices and; 6 other supplies and services prescribed by a doctor. unknow

n

41 38a-533*

Alcoholism

Expenses incurred in connection with m

edical complications of alcoholism

such as cirrhosis of the liver, gastrointestinal bleeding, pneum

onia, and delirium trem

ens. unknow

n

42 38a-507; 38a-534

Chiropractic Services Cover chiropractor services to sam

e extent as coverage for a physician. unknow

n 43

38a-535* Preventive Pediatric Care

Preventive pediatric care at the following intervals 1 every 2 m

onths from birth to 6 m

onths, 2 every 3 months from

9 to 18 m

onths, and 3 annually from 2 to 6 years of age. Coverage is subject to any policy provisions that apply to other

services covered under the policy. yes

44 38a-542a*

Breast Implant Rem

oval M

edically necessary removal of breast im

plants implanted on or before July 1, 1994. Annual coverage m

ust be at least $1,000.

unknown

Dollar Limits on Certain Benefits. Per Connecticut Insurance Departm

ent regulations, with the exception of the Autism

Spectrum Disorder (ASD) m

andate, all dollar limits w

ere rem

oved from those m