Embed Size (px)

Citation preview

1

Selecting your Business Structure

Disadvantaged Business Enterprise (DBE) Supportive Services Program

The contents of this training course reflect the views of the author who is responsible for the facts and accuracy of the data presented herein. The contents do not necessarily reflect the official views or policies of the State of California or the Federal Highway Administration. This course outline does not constitute a standard, specification, or regulation.

2

Disclaimer

The information contained in this presentation has been prepared by GCAP Services as a service to the California

Department of Transportation and is not intended to constitute legal advice. GCAP has used reasonable efforts in collecting, preparing, and providing this information, but does

not guarantee the accuracy, completeness, adequacy, or currency of the information contained in this presentation. The publication and distribution of this presentation are not

intended to create, and receipt does not constitute, an attorney-client relationship.

Agenda

❖ Choice of Legal Entity❖ Key factors in selecting

your entity

❖ Types of legal entities

❖ Specific factors related to each business entity:

❖ Formation

❖ Limitations

❖ Tax and other filings

❖ Liability

2

Key factors in selecting your entity

❖Liability

❖Ownership

❖Filing requirements, fees, & formalities

❖Taxes

Types of Legal Entities

❖Sole Proprietorship

❖Corporation♦ C-Corp or S-Corp

❖Partnership♦ General or Limited

❖Limited Liability Company (LLC)

Sole Proprietorship

❖Business owned by one person

❖Unlimited liability (protect yourself with insurance)

❖Taxed as an individual at ordinary income rate

3

7

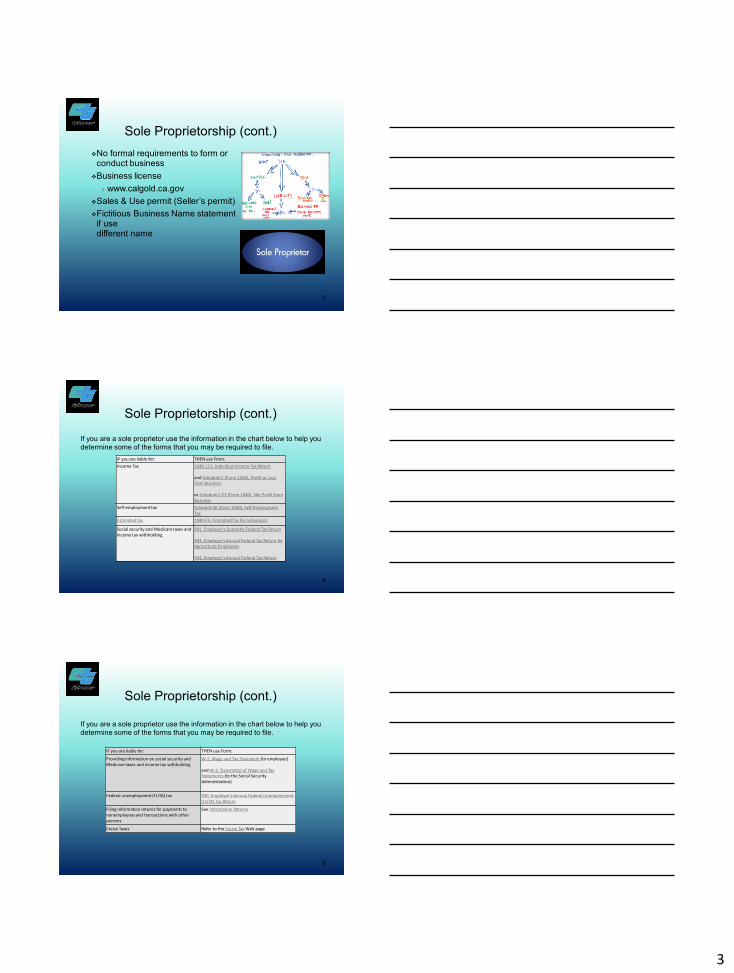

Sole Proprietorship (cont.)

❖No formal requirements to form or conduct business

❖Business license

♦ www.calgold.ca.gov

❖Sales & Use permit (Seller’s permit)

❖Fictitious Business Name statement if use different name

8

IF you are liable for: THEN use Form:

Income Tax 1040, U.S. Individual Income Tax Return

and Schedule C (Form 1040), Profit or Loss from Business

or Schedule C-EZ (Form 1040), Net Profit from Business

Self-employment tax Schedule SE (Form 1040), Self-Employment Tax

Estimated tax 1040-ES, Estimated Tax for Individuals

Social security and Medicare taxes and income tax withholding

941, Employer's Quarterly Federal Tax Return

943, Employer's Annual Federal Tax Return for Agricultural Employees

944, Employer's Annual Federal Tax Return

If you are a sole proprietor use the information in the chart below to help you

determine some of the forms that you may be required to file.

Sole Proprietorship (cont.)

9

IF you are liable for: THEN use Form:

Providing information on social security and Medicare taxes and income tax withholding

W-2, Wage and Tax Statement (to employee)

and W-3, Transmittal of Wage and Tax Statements (to the Social Security Administration)

Federal unemployment (FUTA) tax 940, Employer's Annual Federal Unemployment (FUTA) Tax Return

Filing information returns for payments to nonemployees and transactions with other persons

See Information Returns

Excise Taxes Refer to the Excise Tax Web page

If you are a sole proprietor use the information in the chart below to help you

determine some of the forms that you may be required to file.

Sole Proprietorship (cont.)

4

10

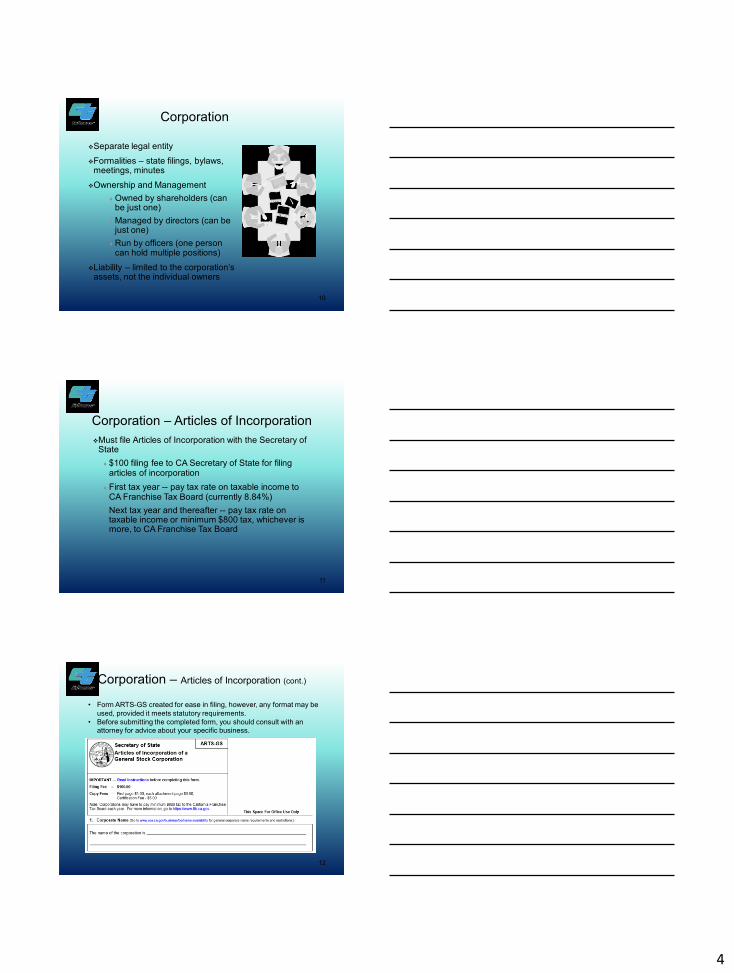

Corporation

❖Separate legal entity

❖Formalities – state filings, bylaws, meetings, minutes

❖Ownership and Management

♦ Owned by shareholders (can be just one)

♦ Managed by directors (can be just one)

♦ Run by officers (one person can hold multiple positions)

❖Liability – limited to the corporation’s assets, not the individual owners

11

Corporation – Articles of Incorporation

❖Must file Articles of Incorporation with the Secretary of State

♦ $100 filing fee to CA Secretary of State for filing articles of incorporation

♦ First tax year -- pay tax rate on taxable income to CA Franchise Tax Board (currently 8.84%)

♦ Next tax year and thereafter -- pay tax rate on taxable income or minimum $800 tax, whichever is more, to CA Franchise Tax Board

12

Corporation – Articles of Incorporation (cont.)

• Form ARTS-GS created for ease in filing, however, any format may be

used, provided it meets statutory requirements.

• Before submitting the completed form, you should consult with an

attorney for advice about your specific business.

5

13

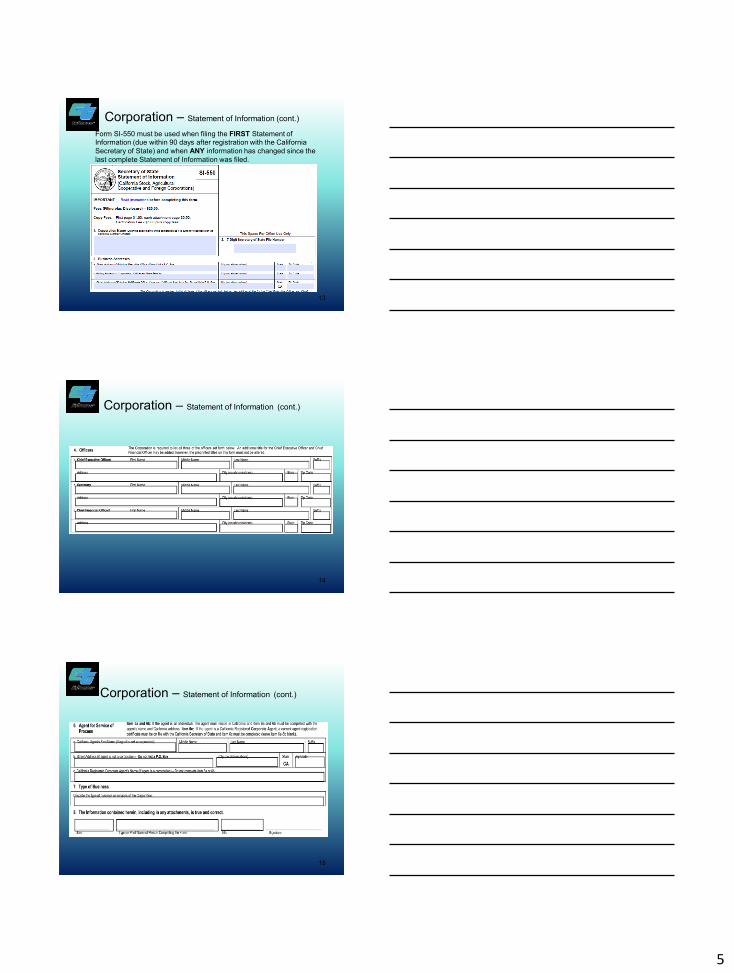

Corporation – Statement of Information (cont.)

Form SI-550 must be used when filing the FIRST Statement of

Information (due within 90 days after registration with the California

Secretary of State) and when ANY information has changed since the

last complete Statement of Information was filed.

14

Corporation – Statement of Information (cont.)

15

Corporation – Statement of Information (cont.)

6

16

Corporation (cont.)

❖Must qualify in other states where it does business

❖Formalities: separate bank accounts, meeting minutes, articles of incorporation, stock certificates, tax return, etc.

Corporate Taxation – C-Corporation

❖Taxed as a separate entity

❖Tax based upon corporation’s net income

❖Profits distributed to its owners -- two levels of tax:

♦ Corporation taxed on income

♦ Then shareholders and employees taxed on income and dividends

18

If you are a C corporation or an S corporation then you may be liable for...

Use Form... Separate Instructions...

Income Tax 1120, U.S. Corporation Income Tax Return (PDF)

Instructions for Form 1120 U.S. Corporation Income Tax Return(PDF)

Estimated tax 1120-W, Estimated Tax for Corporations (PDF)

Instructions for Form 1120-W(PDF)

•Employment taxes Social security and Medicare taxes and income tax withholding•Federal unemployment (FUTA) tax

941, Employer's Quarterly Federal Tax Return (PDF) or 943, Employer's Annual Federal Tax Return for Agricultural Employees (PDF) (for farm employees)

940, Employer's Annual Federal Unemployment (FUTA) Tax return(PDF)

Instructions for Form 941 (PDF) Instructions for Form 943 (PDF)

Instructions for Form 940 (PDF)

Excise Taxes Refer to the Excise Tax Web page

Corporations

Corporation (cont.)

7

19

❖No federal income tax – single tax level

❖Owners (shareholders) pay taxes individually on the profits when earned

❖Owners (shareholders) can also deduct losses on their personal income tax returns

❖Still pay state taxes -- currently 1.5% for S-corporation

Corporate Taxation – S-Corporation

20

S-Corporation (cont.)

❖ Requirements:

♦ limited to 100 shareholders

♦ corporation, partnership or trust cannot own shares

♦ shareholders cannot be nonresident aliens (for tax purposes)

❖ Additional filing requirement with the Internal Revenue Service and CA Franchise Tax Board

21

Chart 1 - S Corporation

If you are an S corporation then you may be liable for...

Use Form...Separate Instructions...

Income Tax 1120S (PDF) 1120S Sch. K-1 (PDF) Instructions for Form 1120S (PDF) Instructions for Form 1120S Sch. K-1(PDF)

Estimated tax 1120-W (PDF) (corporation only) and 8109

Instructions for Form 1120-W (PDF)

Employment taxes:•Social security and Medicare taxes and income tax withholding•Federal unemployment (FUTA) tax•Depositing employment taxes

941 (PDF) ( 943 (PDF) for farm employees)940 (PDF)8109

Instructions for Form 941 Employers QUARTERLY Federal Tax Return (PDF)Instructions for Form 943 Employers Annual Federal Tax Return for Agricultural Employees(PDF)Instructions for Form 940 Employers Annual Federal Unemployment (FUTA) Tax Return(PDF)

Excise Taxes Refer to the Excise Tax Web page

S-Corporation (cont.)

Chart 1 - S Corporation - file 1120S

8

22

Chart 2 - S Corporation Shareholders

If you are an S corporation shareholder then you may be liable for...

Use Form...

Separate Instructions...

Income Tax 1040 and Schedule E (PDF) and other forms referenced on the shareholder's Schedule K-1

Instructions for Schedule E (Form 1040)Supplemental Income and Loss(PDF)

Estimated tax 1040-ES (PDF)

Chart 2 - S Corporation Shareholders – file 1040 and Schedule E

S-Corporation (cont.)

23

Partnerships

• There are two types of partnerships• General

• Limited

• The partners will decide the structure of the organization and the distribution of profits and losses. A formal, written partnership agreement is advisable.

• A separate bank account should be established to run the operations.

• A partnership allows more than one owner, unlike a sole proprietorship.

• The cost to form a partnership is generally less expensive than forming a corporation.

24

Partnerships (Cont.)

• The items of income, deductions, and credits flow through from the partnership to each partner’s California Schedule K-1, Partner’s Share of Income, Deductions, Credits, and distributive shares of property, payroll, and sales.

• Each partner is responsible for paying taxes on their distributive share.

• In a general partnership, each partner is personally liable for all business debts and lawsuits.

• A partnership exists as long as the partners agree it will and as long as there are at least two partners, one of whom is a general partner.

• Partnerships do not pay income tax, however, limited partnerships are subject to the annual tax of $800.

9

25

General Partnership

❖ A business conducted by at least 2 people

❖ Each partner has unlimited liability for debts and obligations of the business

❖ Partnership does not pay federal income tax

♦ Each individual partner files returns

♦ Maximum flexibility in allocating profits and losses, e.g., cash paying partner can deduct all the losses

General Partnership (cont.)

❖No formal requirements

❖Partnership Agreement

♦ Can override partnership laws(e.g., agreement may permit business to continue even if one partner leaves through a buyout)

27

General Partnership (cont)

Chart 1 – Partnership filing Form 1065

10

28

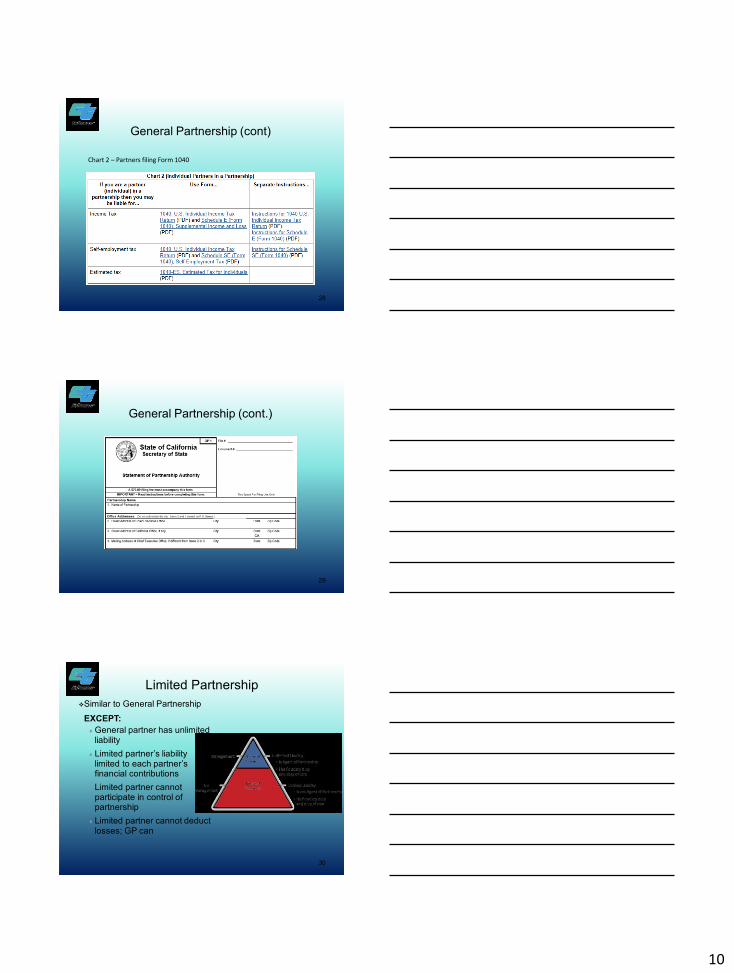

General Partnership (cont)

Chart 2 – Partners filing Form 1040

29

General Partnership (cont.)

30

Limited Partnership

❖Similar to General Partnership

EXCEPT:

♦ General partner has unlimited liability

♦ Limited partner’s liability limited to each partner’s financial contributions

♦ Limited partner cannot participate in control of partnership

♦ Limited partner cannot deduct losses; GP can

11

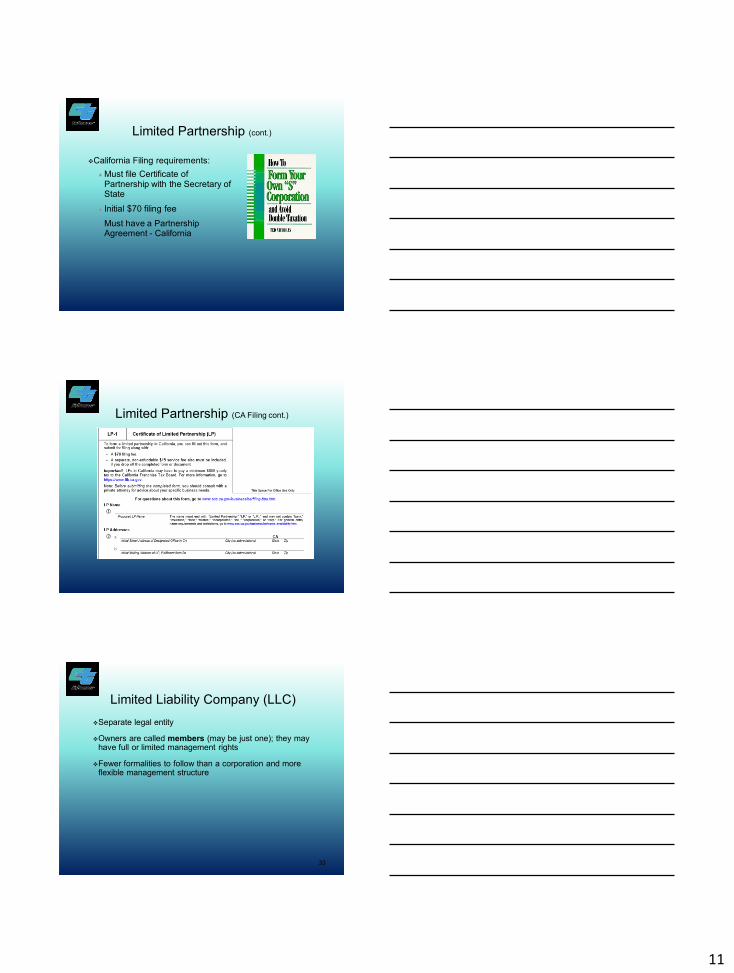

Limited Partnership (cont.)

❖California Filing requirements:

♦ Must file Certificate of Partnership with the Secretary of State

♦ Initial $70 filing fee

♦ Must have a Partnership Agreement - California

Limited Partnership (CA Filing cont.)

33

Limited Liability Company (LLC)

❖Separate legal entity

❖Owners are called members (may be just one); they may have full or limited management rights

❖Fewer formalities to follow than a corporation and more flexible management structure

12

34

LLC – Key Factors

• An LLC is a hybrid business entity that can be treated as a partnership, but it has the limited liability protection under civil law.

• An LLC is formed by filing "articles of organization" with the California Secretary of State prior to conducting business. An out-of-state LLC that conducts business in California should register with the Secretary of State.

• Forming an LLC is simpler and faster than forming and maintaining a civil law corporation.

• Either before or after filing its articles of organization, the LLC members must enter into a verbal or written operating agreement. A formal, written agreement is advisable.

• An LLC is typically managed by its members, unless the members agree to have a manager handle the LLC’s business affairs

35

LLC – Key Factors

• If the LLC has more than one owner, it will be treated as a partnership (subject to Subchapter K), unless it elected to be treated as a corporation. The items of income, deductions, and credits flow through from the LLC to each member’s California Schedule K-1, Members’ Share of Income, Deductions, Credits, etc., and distributive shares of property, payroll, and sales.

• Each member is responsible for paying taxes on their distributive share. If the LLC has a single member, it will be treated as a disregarded entity, and it will be treated as a sole proprietorship or a division of its owner, unless it elects to be taxable as a corporation.

• A husband and wife owning an LLC may elect to be treated as a partnership or a disregarded entity.

• If the LLC elected to be taxed as a corporation, it is subject to corporation tax law and filing requirements.

• In general, all the owners (members) are shielded from individual liability for debts and obligations of the LLC.

• LLCs do not issue stock and are not required to hold annual meetings or keep written minutes, which a corporation must do in order to preserve the liability shield for its owners.

36

LLC – Key Factors

• A husband and wife owning an LLC may elect to be treated as a partnership or a disregarded entity.

• If the LLC elected to be taxed as a corporation, it is subject to corporation tax law and filing requirements.

• In general, all the owners (members) are shielded from individual liability for debts and obligations of the LLC.

• LLCs do not issue stock and are not required to hold annual meetings or keep written minutes, which a corporation must do in order to preserve the liability shield for its owners.

13

37

Limited Liability Company (cont.)

Why form an LLC?

❖No limit on the number or types of members e.g., a corporation or another LLC may be a member

❖Liability limited to the LLC’s assets -- not the individual owner(s)

38

Limited Liability Company (cont.)

❖ LLC may elect not to pay federal income tax

❖ Each individual member files tax returns

❖ Maximum flexibility for allocating profits and losses

i.e., there’s no requirement that profits and losses be

divided according to the percentage of ownership. For

example, the cash paying member can deduct all the

losses.

39

Limited Liability Company (cont.)

❖Must file Articles of Organization with the Secretary of State

• $70 initial filing fee

• $800 annual tax due to CA Franchise Tax Board

• first year tax of $800 payable within first 3 months of organization

• also subject to an annual fee to CA Franchise Tax Board based on LLC’s gross income

14

40

Limited Liability Company (cont.)

41

Limited Liability Company (cont.)

❖Formalities: Must also have an Operating Agreement and maintain separate bank accounts, BUT no meetings or minutes are required

Key factors in selecting your entity

❖ Liability

❖ Taxes

❖ Filing requirements, fees, and formalities

❖ www.ss.ca.gov

(Business Portal)

15

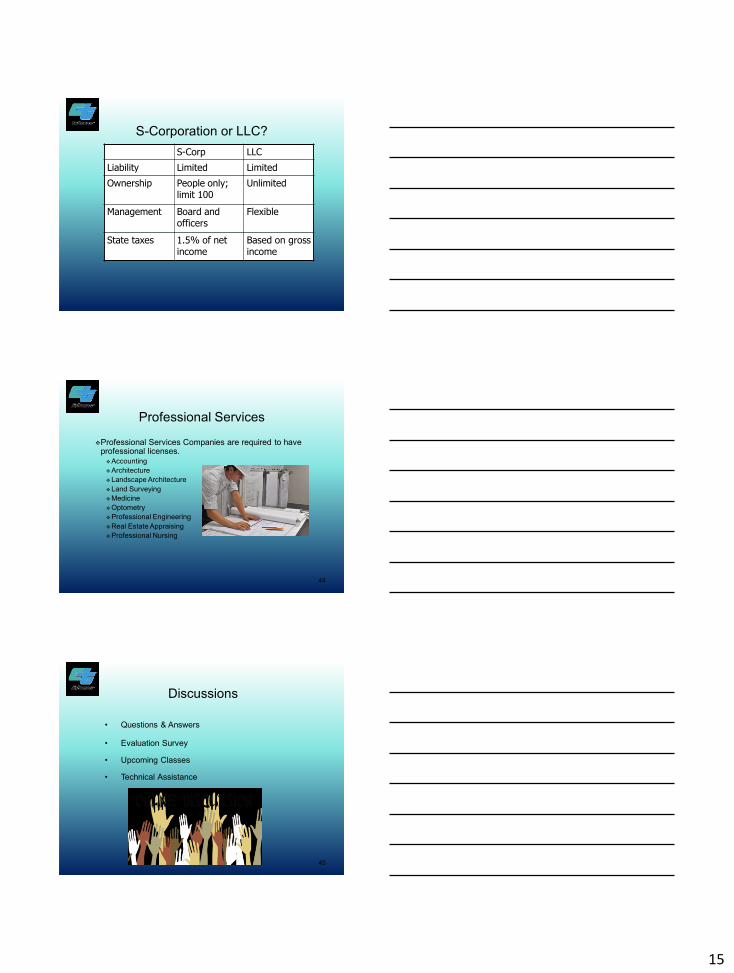

S-Corporation or LLC?

S-Corp LLC

Liability Limited Limited

Ownership People only; limit 100

Unlimited

Management Board and officers

Flexible

State taxes 1.5% of net income

Based on gross income

44

Professional Services

❖Professional Services Companies are required to have professional licenses.❖Accounting

❖Architecture

❖Landscape Architecture

❖Land Surveying

❖Medicine

❖Optometry

❖Professional Engineering

❖Real Estate Appraising

❖Professional Nursing

45

Discussions

• Questions & Answers

• Evaluation Survey

• Upcoming Classes

• Technical Assistance

16

46

Thank you!

➢ Questions & Answers

➢ Evaluation Survey – Link will be emailed to you after this class

➢ Upcoming Classes – Register today!➢Check www.dbe-advantage.com

➢Emails will be sent to you soon

47

Business Development Program

➢ Business Plan Development

➢ One-on-One Mentoring

➢ Free Technical Assistance

➢ Certificate upon Completion of Program

➢ Teaming/Partnering

➢ Access to Recorded Webinars

➢ Access to Valuable Business

Resources

➢ Custom Level Bid Matching

For more information:

➢ Visit: www.dbe-advantage.com

➢ Email: [email protected]