Embed Size (px)

Citation preview

Assenagon Asset Management S.A.

Selective Dispersion Creating an affordable Long Volatility Exposure in an Equity Portfolio

Assenagon Asset Management S.A. 2

Contents

1. Single Stocks Volatilities versus Index Volatilities

2. Volatility Flows and their Impact on Correlation

3. How to invest in Dispersion?

4. From a Pair Trade to a Selective Dispersion Portfolio

– Pair Properties

– What about the Skew?

5. Dispersion Portfolio

– An Example

– Cost of Carry

6. A "small" Digression

7. Summary

Contacts

Disclaimer

Assenagon Asset Management S.A. 3

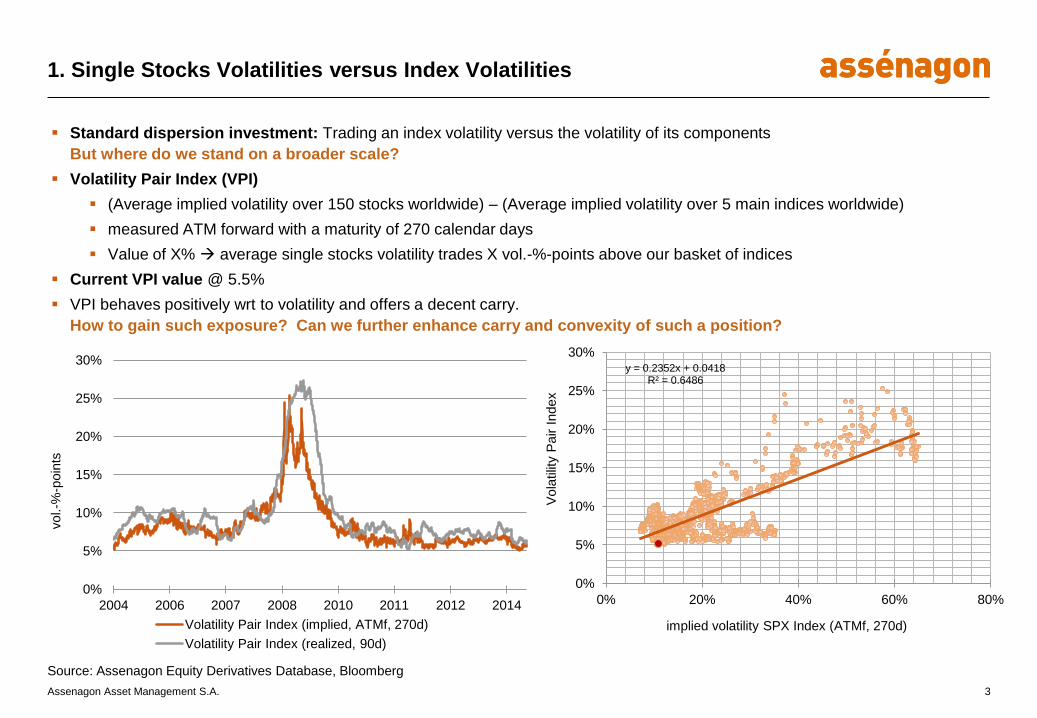

1. Single Stocks Volatilities versus Index Volatilities

Standard dispersion investment: Trading an index volatility versus the volatility of its components

But where do we stand on a broader scale?

Volatility Pair Index (VPI)

(Average implied volatility over 150 stocks worldwide) – (Average implied volatility over 5 main indices worldwide)

measured ATM forward with a maturity of 270 calendar days

Value of X% average single stocks volatility trades X vol.-%-points above our basket of indices

Current VPI value @ 5.5%

VPI behaves positively wrt to volatility and offers a decent carry.

How to gain such exposure? Can we further enhance carry and convexity of such a position?

Source: Assenagon Equity Derivatives Database, Bloomberg

0%

5%

10%

15%

20%

25%

30%

2004 2006 2007 2008 2010 2011 2012 2014

Volatility Pair Index (implied, ATMf, 270d)

Volatility Pair Index (realized, 90d)

vol.-%

-poin

ts

y = 0.2352x + 0.0418 R² = 0.6486

0%

5%

10%

15%

20%

25%

30%

0% 20% 40% 60% 80%

Vola

tilit

y P

air I

ndex

implied volatility SPX Index (ATMf, 270d)

Assenagon Asset Management S.A. 4

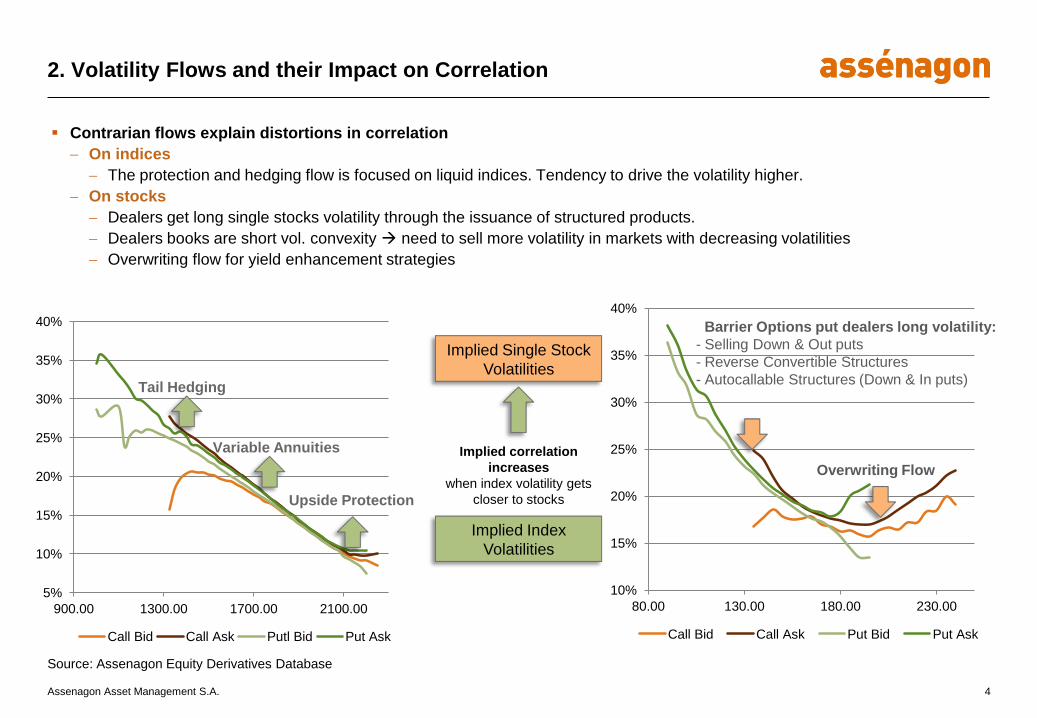

2. Volatility Flows and their Impact on Correlation

Contrarian flows explain distortions in correlation

On indices

The protection and hedging flow is focused on liquid indices. Tendency to drive the volatility higher.

On stocks

Dealers get long single stocks volatility through the issuance of structured products.

Dealers books are short vol. convexity need to sell more volatility in markets with decreasing volatilities

Overwriting flow for yield enhancement strategies

Source: Assenagon Equity Derivatives Database

Implied Single Stock

Volatilities

Implied Index

Volatilities

Implied correlation

increases

when index volatility gets

closer to stocks

5%

10%

15%

20%

25%

30%

35%

40%

900.00 1300.00 1700.00 2100.00

Call Bid Call Ask Putl Bid Put Ask

Upside Protection

Tail Hedging

Variable Annuities

10%

15%

20%

25%

30%

35%

40%

80.00 130.00 180.00 230.00

Call Bid Call Ask Put Bid Put Ask

Barrier Options put dealers long volatility:

- Selling Down & Out puts

- Reverse Convertible Structures

- Autocallable Structures (Down & In puts)

Overwriting Flow

Assenagon Asset Management S.A. 5

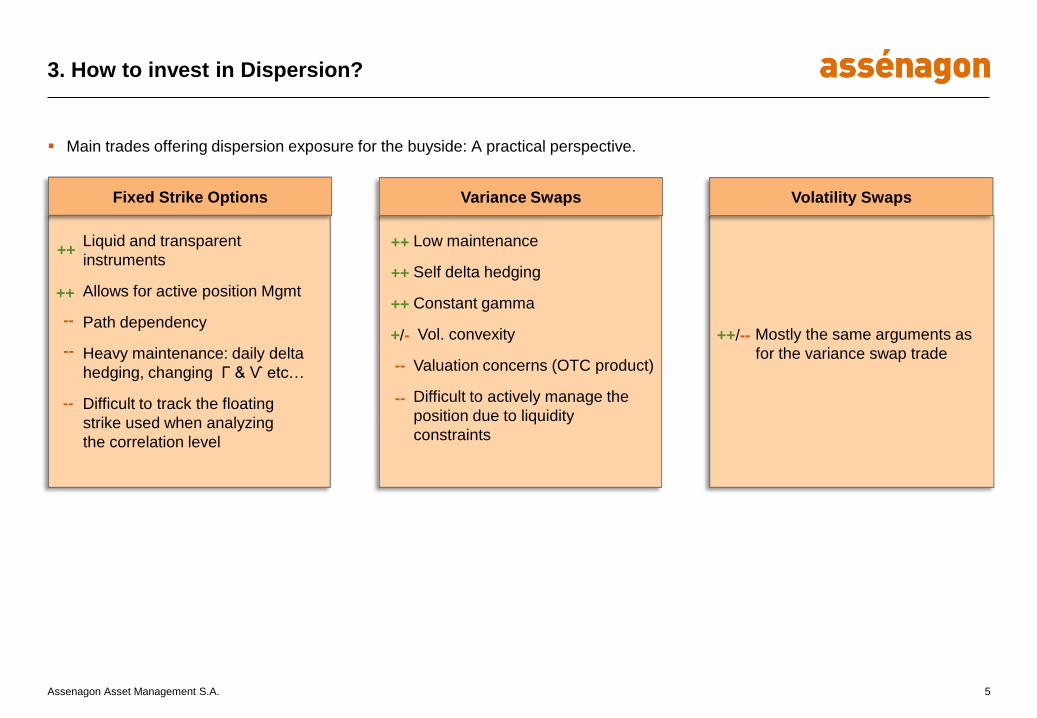

3. How to invest in Dispersion?

Main trades offering dispersion exposure for the buyside: A practical perspective.

Liquid and transparent

instruments

Allows for active position Mgmt

Path dependency

Heavy maintenance: daily delta

hedging, changing Γ & Ѵ etc…

Difficult to track the floating

strike used when analyzing

the correlation level

Mostly the same arguments as

for the variance swap trade

Fixed Strike Options Volatility Swaps

--

--

--

++ Low maintenance

Self delta hedging

Constant gamma

Vol. convexity

Valuation concerns (OTC product)

Difficult to actively manage the

position due to liquidity

constraints

Variance Swaps

++

++

++

--

--

++/-- +/-

++

Assenagon Asset Management S.A. 6

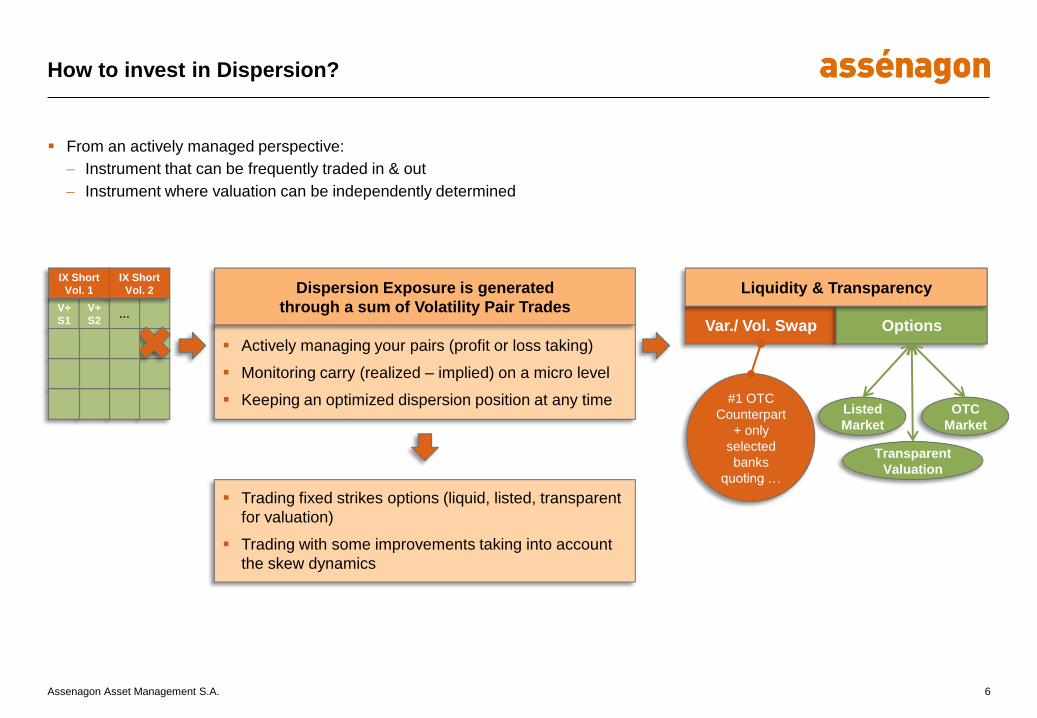

How to invest in Dispersion?

Actively managing your pairs (profit or loss taking)

Monitoring carry (realized – implied) on a micro level

Keeping an optimized dispersion position at any time

Dispersion Exposure is generated

through a sum of Volatility Pair Trades

Trading fixed strikes options (liquid, listed, transparent

for valuation)

Trading with some improvements taking into account

the skew dynamics

Var./ Vol. Swap Options

Liquidity & Transparency

#1 OTC

Counterpart

+ only

selected

banks

quoting …

Listed

Market

OTC

Market

Transparent

Valuation

… V+

S2

V+

S1

IX Short

Vol. 2

IX Short

Vol. 1

From an actively managed perspective:

Instrument that can be frequently traded in & out

Instrument where valuation can be independently determined

Assenagon Asset Management S.A. 7

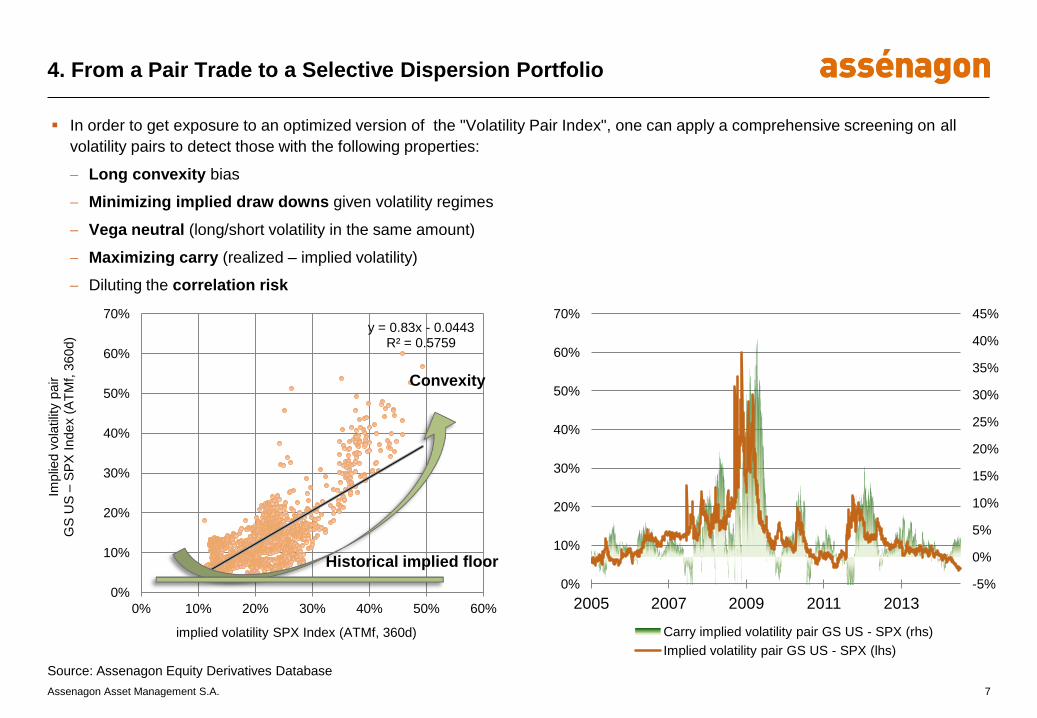

4. From a Pair Trade to a Selective Dispersion Portfolio

In order to get exposure to an optimized version of the "Volatility Pair Index", one can apply a comprehensive screening on all

volatility pairs to detect those with the following properties:

Long convexity bias

Minimizing implied draw downs given volatility regimes

Vega neutral (long/short volatility in the same amount)

Maximizing carry (realized – implied volatility)

Diluting the correlation risk

Source: Assenagon Equity Derivatives Database

y = 0.83x - 0.0443 R² = 0.5759

0%

10%

20%

30%

40%

50%

60%

70%

0% 10% 20% 30% 40% 50% 60%

Implie

d v

ola

tilit

y p

air

GS

US

– S

PX

Index (

AT

Mf,

360d)

implied volatility SPX Index (ATMf, 360d)

Convexity

Historical implied floor

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0%

10%

20%

30%

40%

50%

60%

70%

2005 2007 2009 2011 2013

Carry implied volatility pair GS US - SPX (rhs)

Implied volatility pair GS US - SPX (lhs)

Assenagon Asset Management S.A. 8

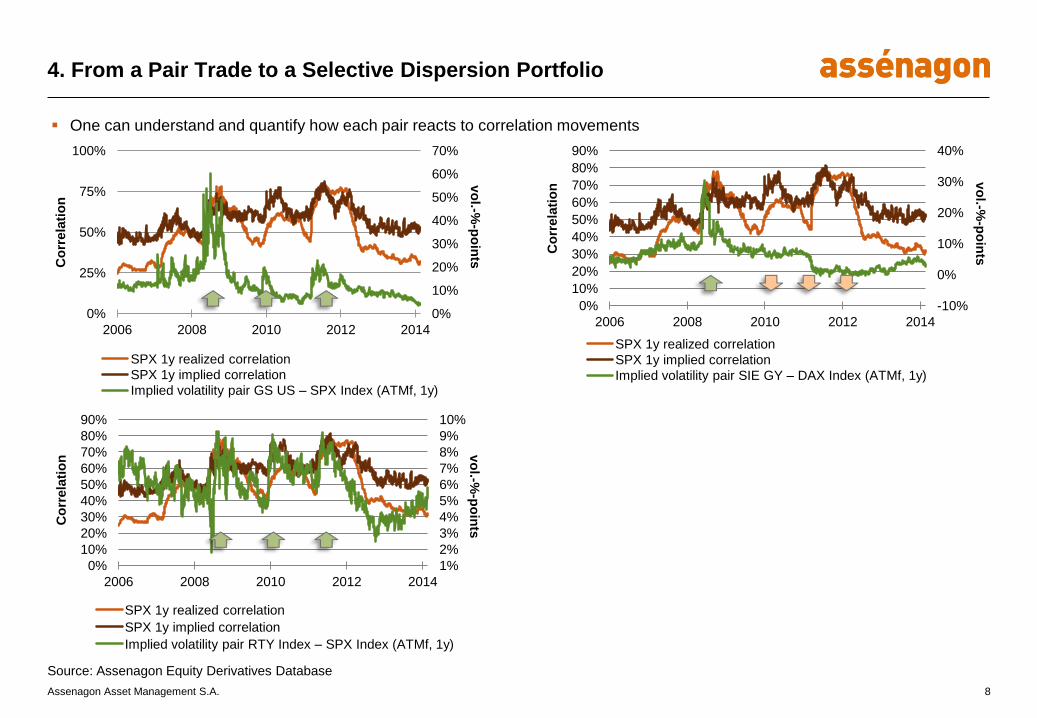

4. From a Pair Trade to a Selective Dispersion Portfolio

One can understand and quantify how each pair reacts to correlation movements

0%

10%

20%

30%

40%

50%

60%

70%

0%

25%

50%

75%

100%

2006 2008 2010 2012 2014

vo

l.-%-p

oin

ts C

orr

ela

tio

n

SPX 1y realized correlation

SPX 1y implied correlation

Implied volatility pair GS US – SPX Index (ATMf, 1y)

-10%

0%

10%

20%

30%

40%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2006 2008 2010 2012 2014

vo

l.-%-p

oin

ts

Co

rrela

tio

n

SPX 1y realized correlation

SPX 1y implied correlation

Implied volatility pair SIE GY – DAX Index (ATMf, 1y)

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2006 2008 2010 2012 2014

vo

l.-%-p

oin

ts

Co

rrela

tio

n

SPX 1y realized correlation

SPX 1y implied correlation

Implied volatility pair RTY Index – SPX Index (ATMf, 1y)

Source: Assenagon Equity Derivatives Database

Assenagon Asset Management S.A. 9

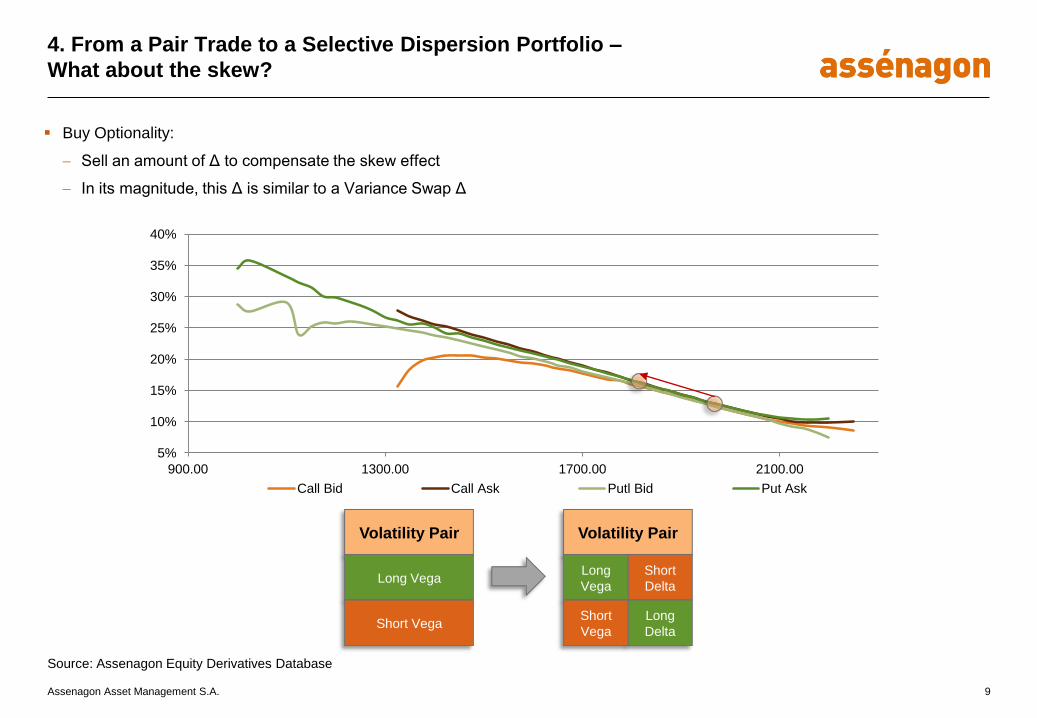

4. From a Pair Trade to a Selective Dispersion Portfolio –

What about the skew?

Buy Optionality:

Sell an amount of Δ to compensate the skew effect

In its magnitude, this Δ is similar to a Variance Swap Δ

Source: Assenagon Equity Derivatives Database

Volatility Pair

Short

Delta

Long

Delta

Long

Vega

Short

Vega

Volatility Pair

Long Vega

Short Vega

5%

10%

15%

20%

25%

30%

35%

40%

900.00 1300.00 1700.00 2100.00

Call Bid Call Ask Putl Bid Put Ask

Assenagon Asset Management S.A. 10

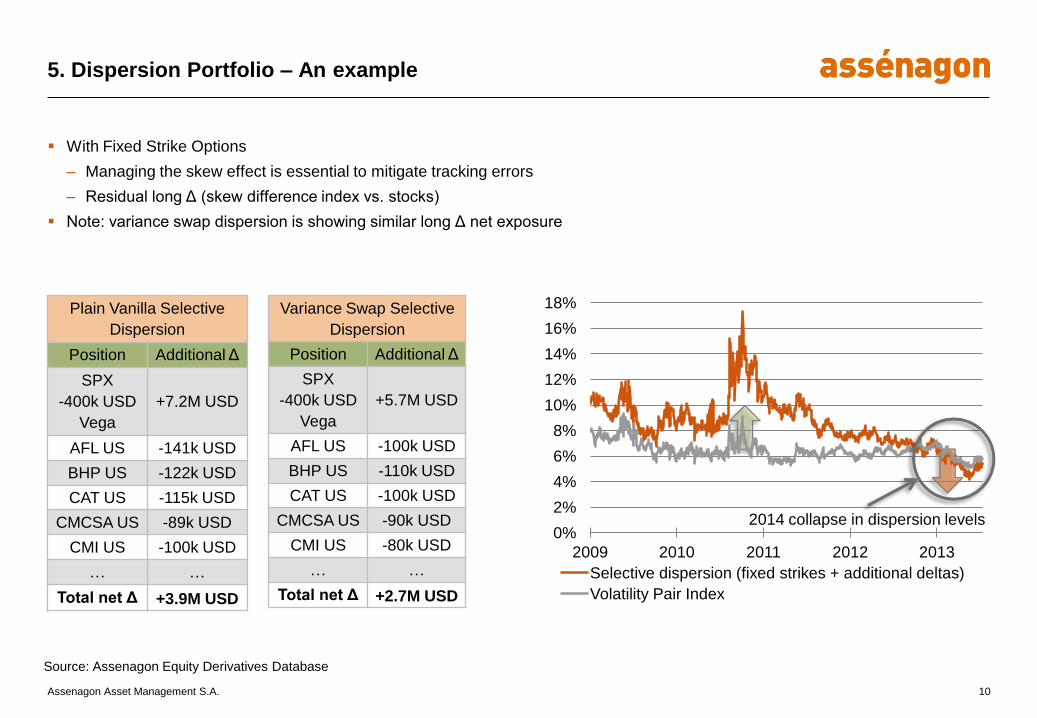

5. Dispersion Portfolio – An example

With Fixed Strike Options

– Managing the skew effect is essential to mitigate tracking errors

– Residual long Δ (skew difference index vs. stocks)

Note: variance swap dispersion is showing similar long Δ net exposure

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2009 2010 2011 2012 2013

Selective dispersion (fixed strikes + additional deltas)

Volatility Pair Index

Source: Assenagon Equity Derivatives Database

2014 collapse in dispersion levels

Plain Vanilla Selective

Dispersion

Position Additional Δ

SPX

-400k USD

Vega

+7.2M USD

AFL US -141k USD

BHP US -122k USD

CAT US -115k USD

CMCSA US -89k USD

CMI US -100k USD

… …

Total net Δ +3.9M USD

Variance Swap Selective

Dispersion

Position Additional Δ

SPX

-400k USD

Vega

+5.7M USD

AFL US -100k USD

BHP US -110k USD

CAT US -100k USD

CMCSA US -90k USD

CMI US -80k USD

… …

Total net Δ +2.7M USD

Assenagon Asset Management S.A. 11

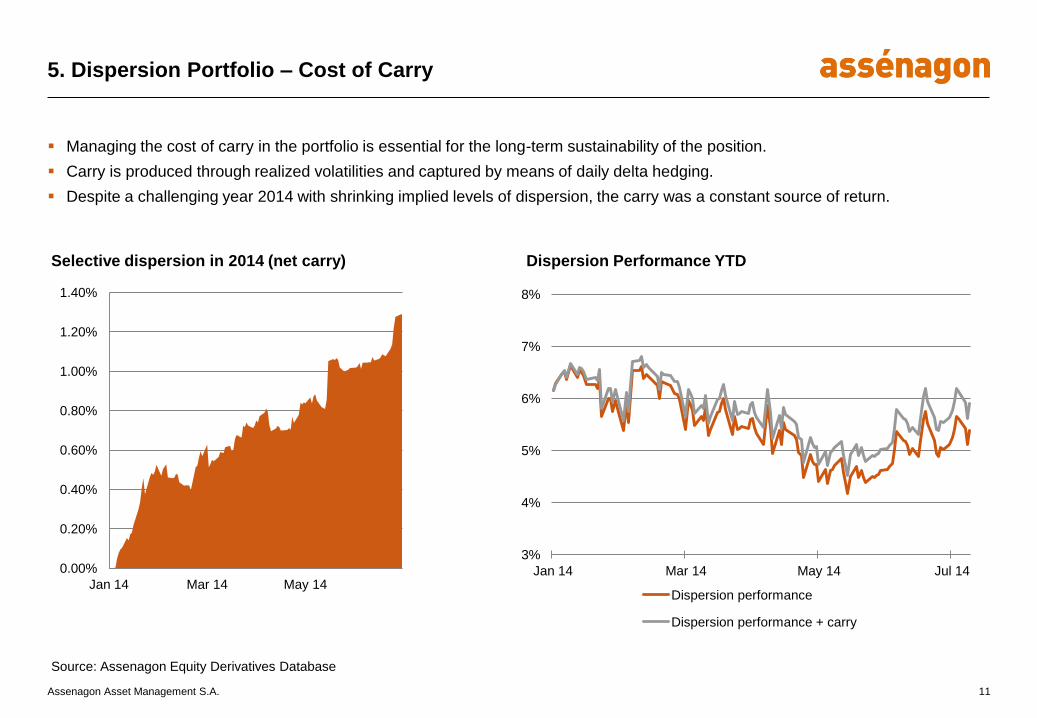

5. Dispersion Portfolio – Cost of Carry

Managing the cost of carry in the portfolio is essential for the long-term sustainability of the position.

Carry is produced through realized volatilities and captured by means of daily delta hedging.

Despite a challenging year 2014 with shrinking implied levels of dispersion, the carry was a constant source of return.

Source: Assenagon Equity Derivatives Database

Selective dispersion in 2014 (net carry) Dispersion Performance YTD

3%

4%

5%

6%

7%

8%

Jan 14 Mar 14 May 14 Jul 14

Dispersion performance

Dispersion performance + carry

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

Jan 14 Mar 14 May 14

Assenagon Asset Management S.A. 12

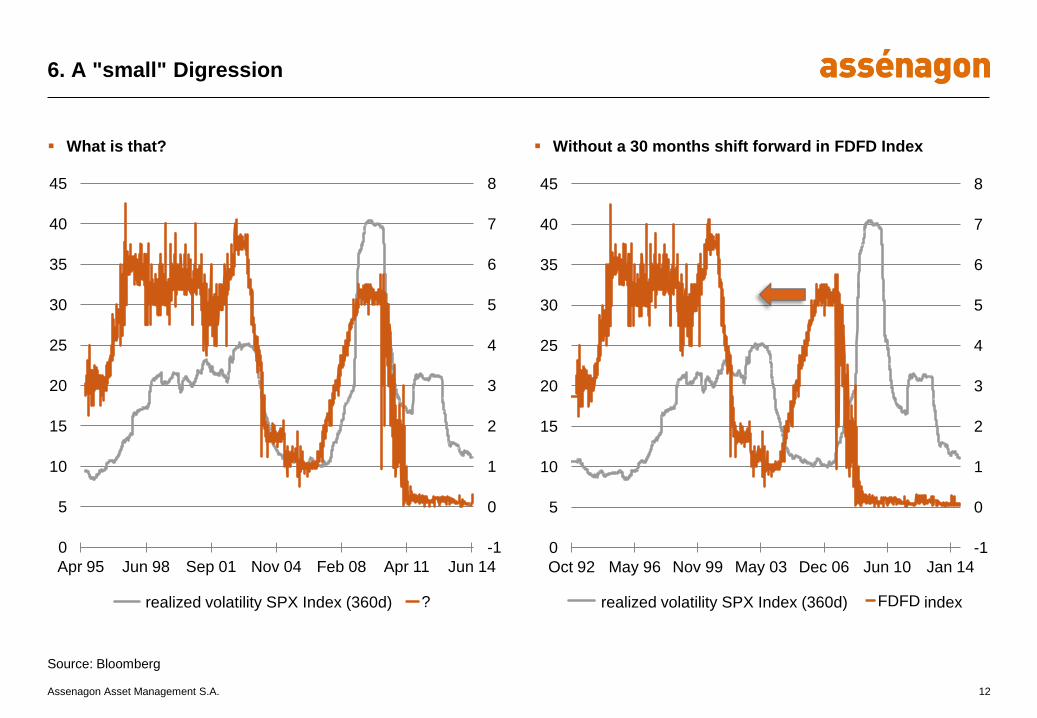

6. A "small" Digression

What is that? Without a 30 months shift forward in FDFD Index

Source: Bloomberg

-1

0

1

2

3

4

5

6

7

8

0

5

10

15

20

25

30

35

40

45

Apr 95 Jun 98 Sep 01 Nov 04 Feb 08 Apr 11 Jun 14

SPX 360 Days Realized Volatility ?

-1

0

1

2

3

4

5

6

7

8

0

5

10

15

20

25

30

35

40

45

Oct 92 May 96 Nov 99 May 03 Dec 06 Jun 10 Jan 14

SPX 360 Days Realized Volatility FDFD Index realized volatility SPX Index (360d) realized volatility SPX Index (360d) index

Assenagon Asset Management S.A. 13

7. Summary

Trading dispersion can offer both long volatility and positive carry

Current dispersion levels are very attractive compared to recent years

Practical implementation can be tricky and cumbersome (but not impossible)

Ensuring liquidity in the dispersion portfolio is crucial

Assenagon Asset Management S.A. 14

Contacts

Customer Coverage

Hans Günther Bonk

Phone +49 89 519966-410

Michael Huber

Phone +49 89 519966-452

Matthias Kunze

Phone +49 89 519966-421

Michael van Riesen

Phone +49 89 519966-419

Ronald Siebel

Phone +49 89 519966-420

Marcus Steudner

Phone +49 89 519966-451

Scan for App

Sales Operations

Simone Alanne

Phone +49 89 519966-460

Carina Herz

Phone +49 89 519966-462

Senior Advisor

Christian Maria Kreuser

Phone +49 89 519966-378

Chief Economist

Dr. Martin W. Hüfner

Phone +49 89 519966-150

Imprint

Assenagon Asset Management S.A.

Aerogolf Center

1B, Heienhaff

1736 Senningerberg, Luxemburg

Assenagon Asset Management S.A.

Zweigniederlassung München

Prannerstraße 8

80333 München, Deutschland

Assenagon Schweiz GmbH

Paradeplatz 4

8001 Zürich, Schweiz

Assenagon Client Service GmbH

Prannerstraße 8

80333 München, Deutschland

www.assenagon.com

Assenagon Asset Management S.A. 15

Disclaimer

All information contained in this document is based on carefully selected sources which are considered to be reliable. However, Assenagon S.A., Luxembourg, Assenagon Asset Management S.A.,

Luxembourg and its branch offices as well as Assenagon Schweiz GmbH, Assenagon Client Service GmbH, Munich and Assenagon GmbH, Munich (hereinafter collectively referred to as "Assenagon

Group") cannot guarantee the correctness, completeness or accuracy of the information. Any liability or warranty arising from this document is therefore completely excluded, and the Assenagon

Group assumes no responsibility for, among other things, the completeness, correctness, timeliness and availability of the information, despite having compiled it with due care.

The information in this presentation on fund products, securities and financial services was examined only for compliance with Luxembourg and German law. In some jurisdictions, the dissemination

of such information may be subject to legal restrictions. The preceding information is thus not intended for natural or legal persons who have their residence or registered office in a jurisdiction that

restricts dissemination of information of this type. Natural or legal persons who have their residence or registered office in a foreign jurisdiction should seek information on such restrictions and

observe them accordingly.

In particular, the information contained in this document is not intended for citizens of the UK or the USA nor is it designed for such purpose.

This document is neither a public offer to sell nor a solicitation of an offer to buy securities, fund units or other financial instruments. An investment decision regarding any securities, fund units or other

financial instruments should be made on the basis of the relevant sales documents (e.g. prospectus and key investor information, available in German from the head office of Assenagon Asset

Management S.A. or at www.assenagon.com), but under no circumstances on the basis of this presentation. All opinions expressed in this presentation are based on the assessment of the

Assenagon Group at the time it was published, regardless of when you receive the information, and are subject to change without prior notice. The Assenagon Group thus expressly reserves the right

to change any opinions expressed in the presentation at any time and without prior notice. The content of this presentation may also be unsuitable or inapplicable for certain investors. It is simply

provided by the company as information for use at your own discretion and is no substitute for individual advice.

The value and return of the fund products, securities and financial services presented may decrease and increase, and in some cases investors may not receive back the full amount they invested.

Past performance is no indicator of future performance. The performance of fund products is calculated using the BVI method; simulations are based on historical returns. Front loads and individual

costs such as fees, commissions and other charges are not accounted for in this presentation, and would have a negative impact on performance were they to be included.

The Assenagon Group may have published other documents that contradict the information contained in this presentation or that come to other conclusions. These publications may reflect other

assumptions, statements of opinion and analysis methods. Past performance is neither an indicator nor a guarantee of future performance. Future performance is neither explicitly nor implicitly

guaranteed or promised.

The content of this document is protected and may not be copied, published, adopted or used for other purposes in any form whatsoever without the prior written permission of the Assenagon Group.

This document is only intended to be used by the persons at whom it is directed. It may neither be used by other persons nor made accessible to other persons by means of publication or

dissemination.

The tax information in this presentation is not intended to provide or replace binding tax advice, and does not claim to cover all tax aspects that may be relevant in connection with the acquisition,

holding or sale of fund units. The information is not exhaustive, nor does it take into account the individual circumstances affecting certain investors or groups of investors. It cannot replace advice

from a tax advisor based on your specific case.

12 August 2014