Embed Size (px)

Citation preview

1

Self-Funding and CIGNA Select Solutions

Brian HelmlyRogers Benefit Group

2

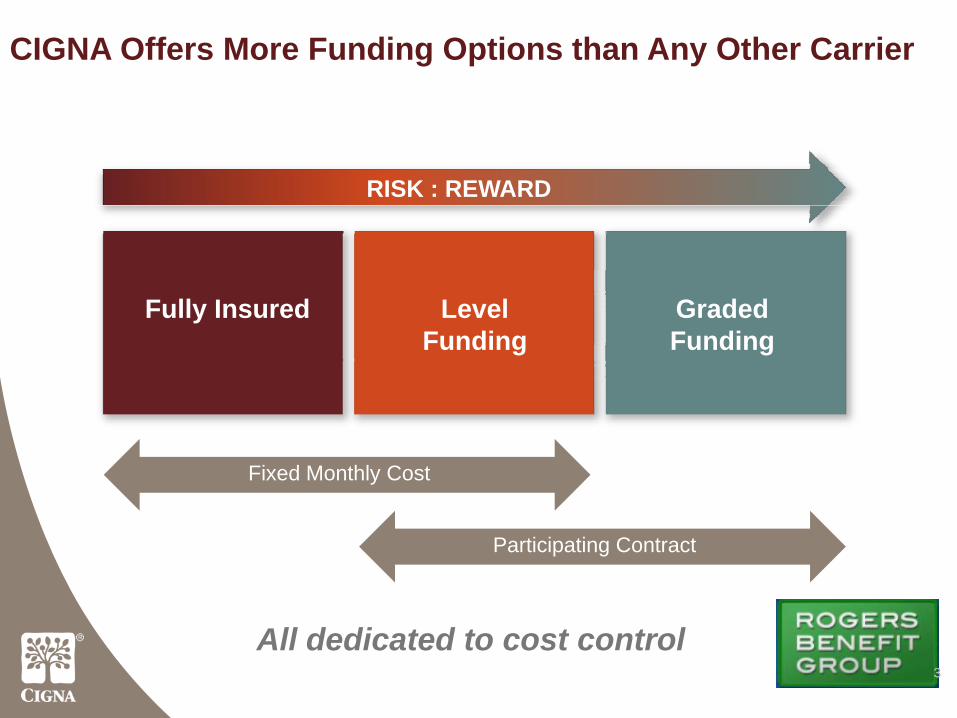

Innovative funding options

CIGNA offers more funding options for smaller companies than any other national health company.

A fully insured option Two self-funding options

33

CIGNA Offers More Funding Options than Any Other Carrier

All dedicated to cost control

RISK : REWARD

Fully Insured LevelFunding

GradedFunding

Fixed Monthly Cost

Participating Contract

4

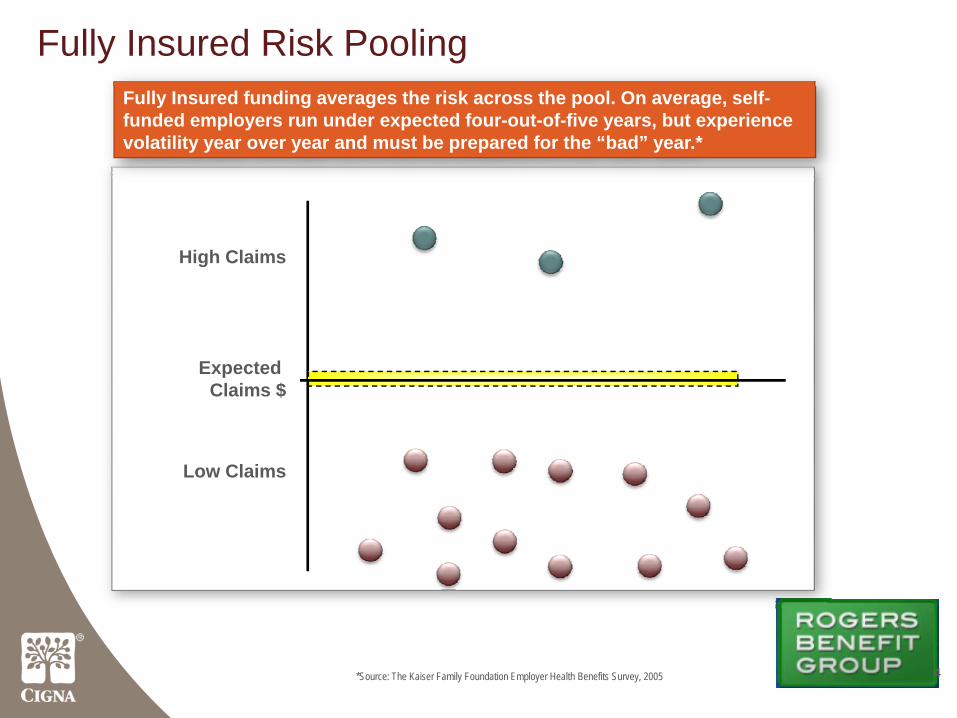

Fully Insured Risk Pooling

High Claims

Low Claims

Expected Claims $

*Source: The Kaiser Family Foundation Employer Health Benefits Survey, 2005 4

Fully Insured funding averages the risk across the pool. On average, self-funded employers run under expected four-out-of-five years, but experience volatility year over year and must be prepared for the “bad” year.*

5

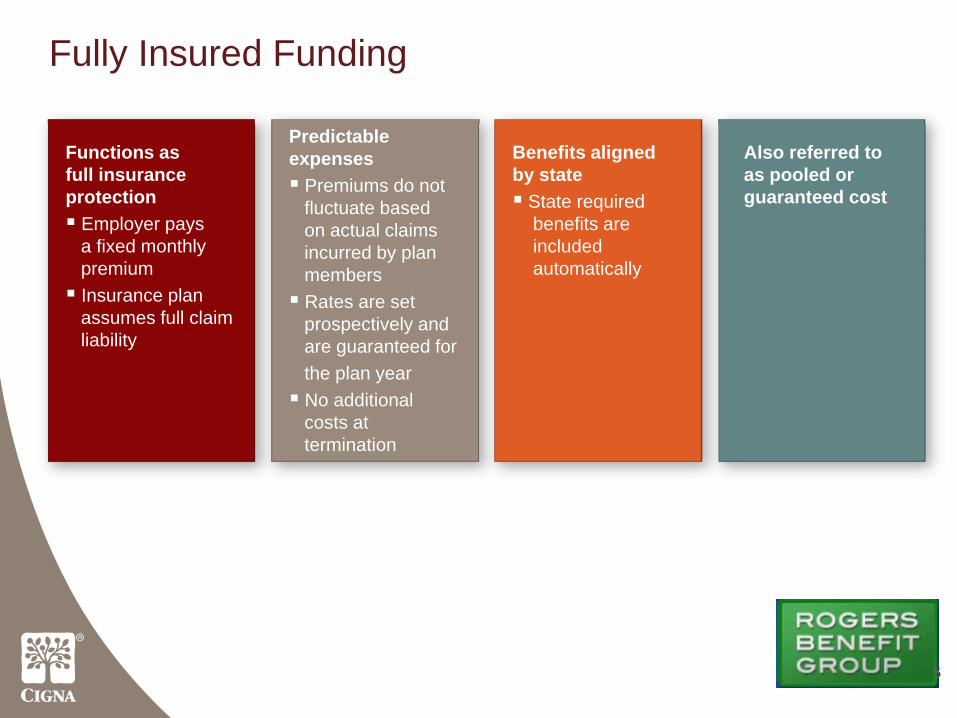

Fully Insured Funding

Functions as full insurance protection

Employer pays a fixed monthlypremiumInsurance plan assumes full claimliability

5

Predictableexpenses

Premiums do not fluctuate based on actual claims incurred by plan membersRates are set prospectively and are guaranteed forthe plan year No additional costs attermination

Benefits aligned by state

State required benefits are included automatically

Also referred to as pooled orguaranteed cost

6

CIGNA Fully Insured Product Overview51 (or more) ELIGIBLE and Minimum of 50% PARTICIPATION

7

Simplicity and predictability

Fully insured funding is ideal for companies looking for the financial protection that comes from knowing their annual health care expenses.With a fully insured option, companies:

A fully insured option

Can easily budget with a single, set premium amount due each month.Get full protection for covered claims, regardless of how high claims go during the year.Enjoy features that are straightforward and easy to understand.Gain financial advantages in claims risk by being combined with a large group of smaller employer clients.

Innovative funding options

8

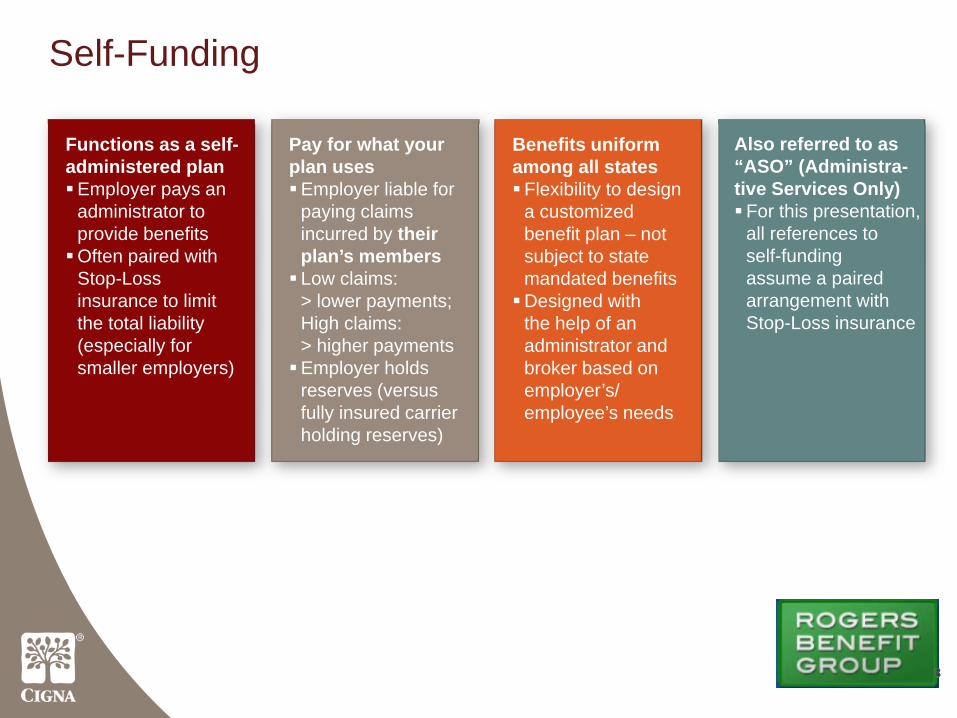

Self-Funding

8

Functions as a self-administered plan

Employer pays an administrator to provide benefitsOften paired with Stop-Loss insurance to limit the total liability (especially for smaller employers)

Pay for what yourplan uses

Employer liable for paying claims incurred by their plan’s membersLow claims: > lower payments; High claims: > higher paymentsEmployer holds reserves (versus fully insured carrier holding reserves)

Benefits uniformamong all states

Flexibility to design a customized benefit plan – not subject to state mandated benefitsDesigned with the help of an administrator and broker based on employer’s/ employee’s needs

Also referred to as“ASO” (Administra-tive Services Only)

For this presentation, all references to self-funding assume a paired arrangement with Stop-Loss insurance

9

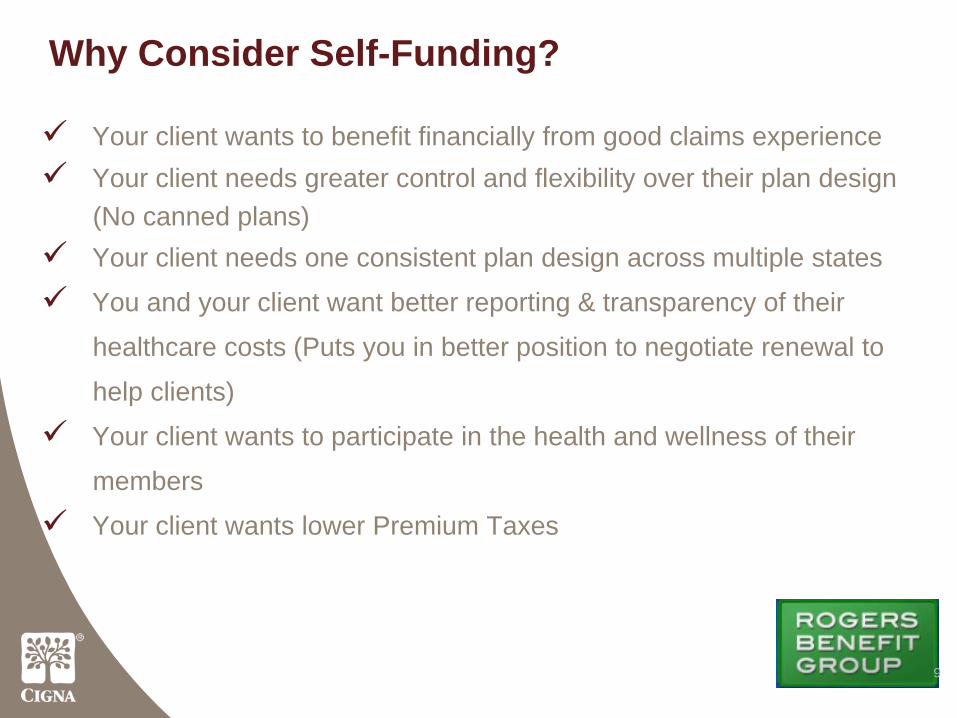

Why Consider Self-Funding?

Your client wants to benefit financially from good claims experienceYour client needs greater control and flexibility over their plan design (No canned plans)Your client needs one consistent plan design across multiple states

You and your client want better reporting & transparency of their

healthcare costs (Puts you in better position to negotiate renewal to

help clients)

Your client wants to participate in the health and wellness of their

members

Your client wants lower Premium Taxes

10

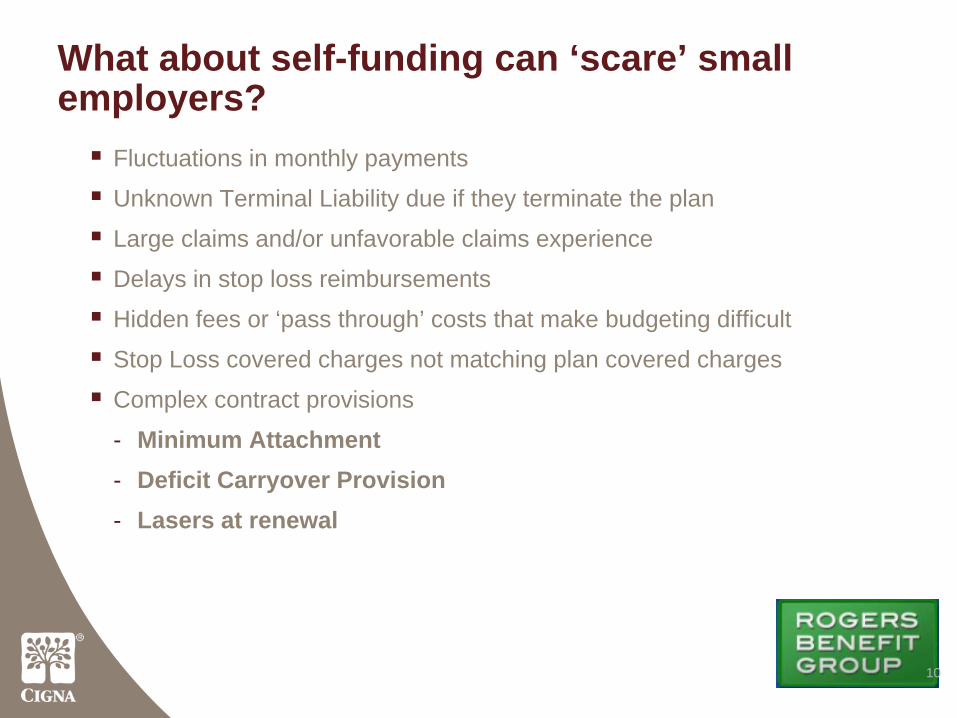

What about self-funding can ‘scare’ small employers?

Fluctuations in monthly payments

Unknown Terminal Liability due if they terminate the plan

Large claims and/or unfavorable claims experience

Delays in stop loss reimbursements

Hidden fees or ‘pass through’ costs that make budgeting difficult

Stop Loss covered charges not matching plan covered charges

Complex contract provisions

- Minimum Attachment - Deficit Carryover Provision- Lasers at renewal

11

CIGNA Level Funding Product25 (or more) ENROLLED

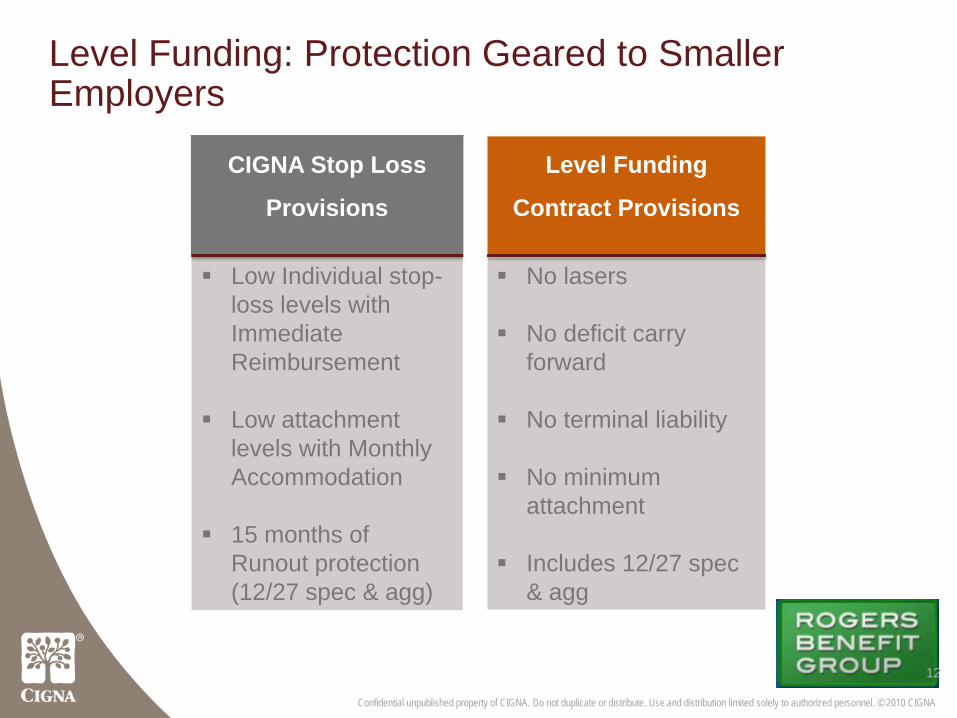

Level Funding: Protection Geared to Smaller Employers

CIGNA Stop Loss

Provisions

Low Individual stop-loss levels with Immediate Reimbursement

Low attachment levels with Monthly Accommodation

15 months of Runout protection (12/27 spec & agg)

Level Funding

Contract Provisions

No lasers

No deficit carry forward

No terminal liability

No minimum attachment

Includes 12/27 spec & agg

Confidential unpublished property of CIGNA. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2010 CIGNA

12

13

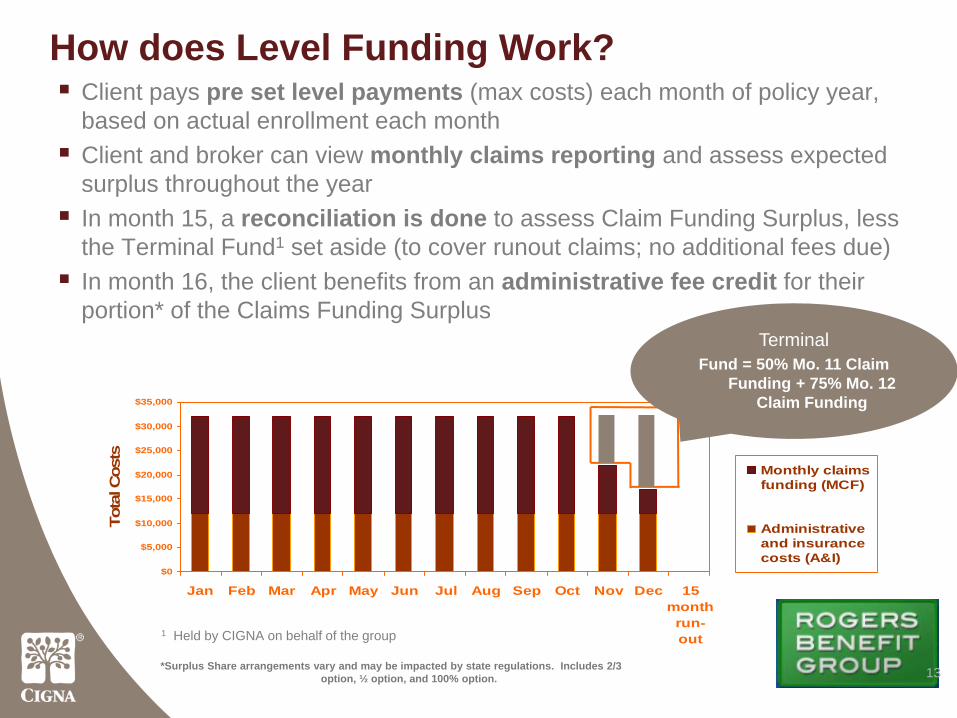

How does Level Funding Work?

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 15month

run-out

Tota

l Cos

ts

Monthly claimsfunding (MCF)

Administrativeand insurancecosts (A&I)

1 Held by CIGNA on behalf of the group

Client pays pre set level payments (max costs) each month of policy year, based on actual enrollment each month Client and broker can view monthly claims reporting and assess expected surplus throughout the yearIn month 15, a reconciliation is done to assess Claim Funding Surplus, less the Terminal Fund1 set aside (to cover runout claims; no additional fees due)In month 16, the client benefits from an administrative fee credit for their portion* of the Claims Funding Surplus

*Surplus Share arrangements vary and may be impacted by state regulations. Includes 2/3 option, ½ option, and 100% option.

TerminalFund = 50% Mo. 11 Claim

Funding + 75% Mo. 12 Claim Funding

14

Who Are the Ideal Candidates?

1 What employers want from health insurers in 2010: Better information, more value, Pricewaterhouse Coopers’ Health Research Institute, January 2010

Level FundingThe “losers” under Obama Care (Young, healthy, favorable industry)

Wants to benefit from good claims experience

Needs greater control and flexibility

Needs consistent plan across multiple markets

Wants better reporting & transparency

Wants to participate in the health and wellness of their members

Wants lower Premium Taxes

Is accustomed to fully insured Needs predictable paymentsNeeds low pooling level

15

CIGNA Graded Funding Product25 (or more) ENROLLED

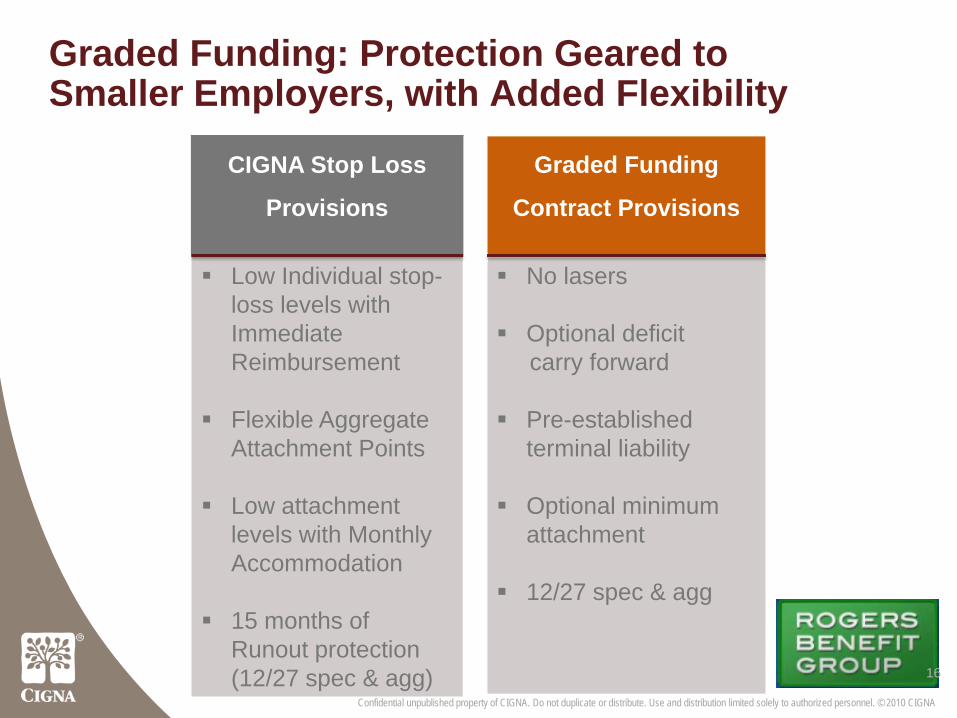

Graded Funding: Protection Geared to Smaller Employers, with Added Flexibility

CIGNA Stop Loss

Provisions

Low Individual stop-loss levels with Immediate Reimbursement

Flexible Aggregate Attachment Points

Low attachment levels with Monthly Accommodation

15 months of Runout protection (12/27 spec & agg)

Graded Funding

Contract Provisions

No lasers

Optional deficit carry forward

Pre-established terminal liability

Optional minimum attachment

12/27 spec & agg

Confidential unpublished property of CIGNA. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2010 CIGNA

16

17

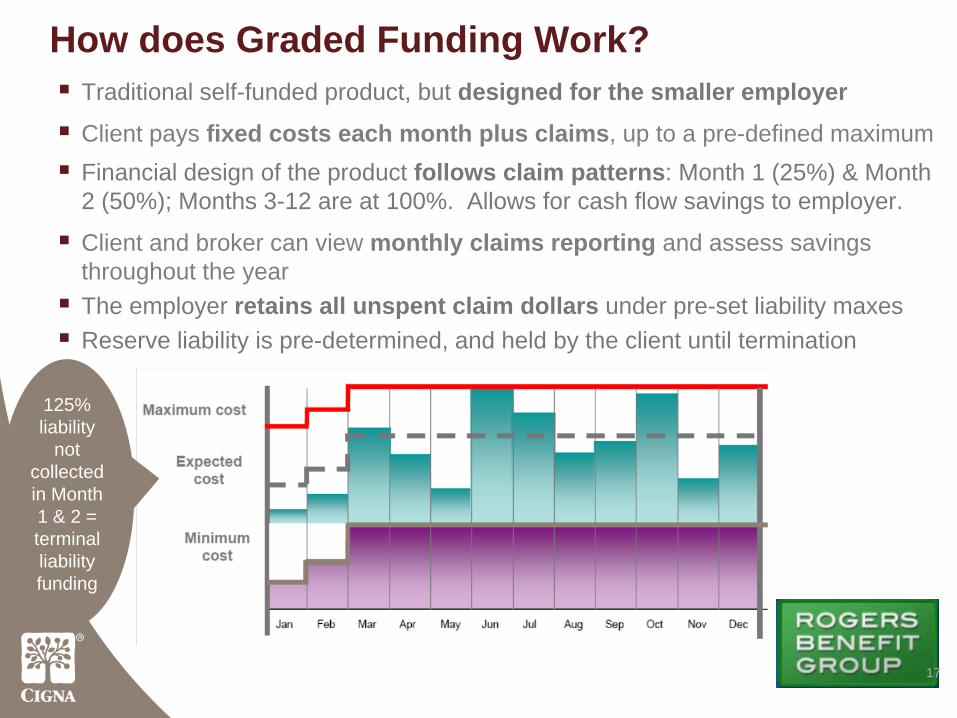

How does Graded Funding Work?Traditional self-funded product, but designed for the smaller employer

Client pays fixed costs each month plus claims, up to a pre-defined maximumFinancial design of the product follows claim patterns: Month 1 (25%) & Month 2 (50%); Months 3-12 are at 100%. Allows for cash flow savings to employer.

Client and broker can view monthly claims reporting and assess savings throughout the year The employer retains all unspent claim dollars under pre-set liability maxesReserve liability is pre-determined, and held by the client until termination

125% liability

not collected in Month 1 & 2 = terminal liability funding

18

Who Are the Ideal Candidates?Graded Funding

The “losers” under Obama Care (healthy, young, favorable industry)

Wants to benefit from good claims experience

Needs greater control and flexibility

Clients seeking cash flow advantage

Needs consistent plan across multiple markets

Wants better reporting & transparency

Wants to participate in the health and wellness of their members

Wants lower Premium Taxes

Wants to retain ALL unspent claim dollarsIs comfortable with variations in monthly cost, and like the benefit of cash flow

19

Self-Funded CIGNA vs TPA

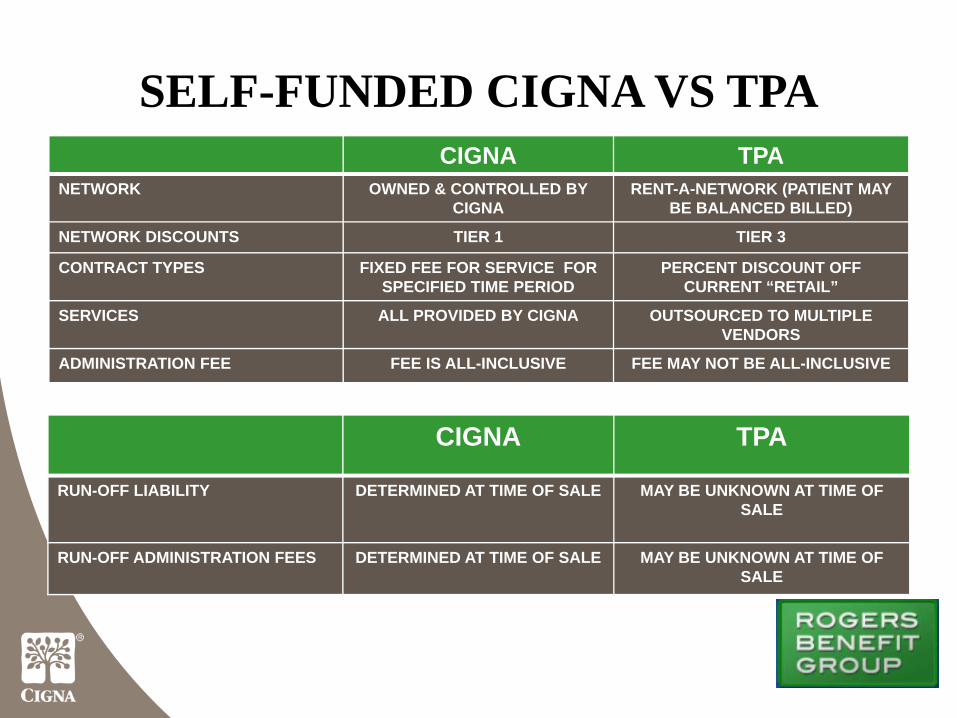

SELF-FUNDED CIGNA VS TPACIGNA TPA

NETWORK OWNED & CONTROLLED BY CIGNA

RENT-A-NETWORK (PATIENT MAY BE BALANCED BILLED)

NETWORK DISCOUNTS TIER 1 TIER 3

CONTRACT TYPES FIXED FEE FOR SERVICE FOR SPECIFIED TIME PERIOD

PERCENT DISCOUNT OFF CURRENT “RETAIL”

SERVICES ALL PROVIDED BY CIGNA OUTSOURCED TO MULTIPLE VENDORS

ADMINISTRATION FEE FEE IS ALL-INCLUSIVE FEE MAY NOT BE ALL-INCLUSIVE

CIGNA TPA

RUN-OFF LIABILITY DETERMINED AT TIME OF SALE MAY BE UNKNOWN AT TIME OF SALE

RUN-OFF ADMINISTRATION FEES DETERMINED AT TIME OF SALE MAY BE UNKNOWN AT TIME OF SALE

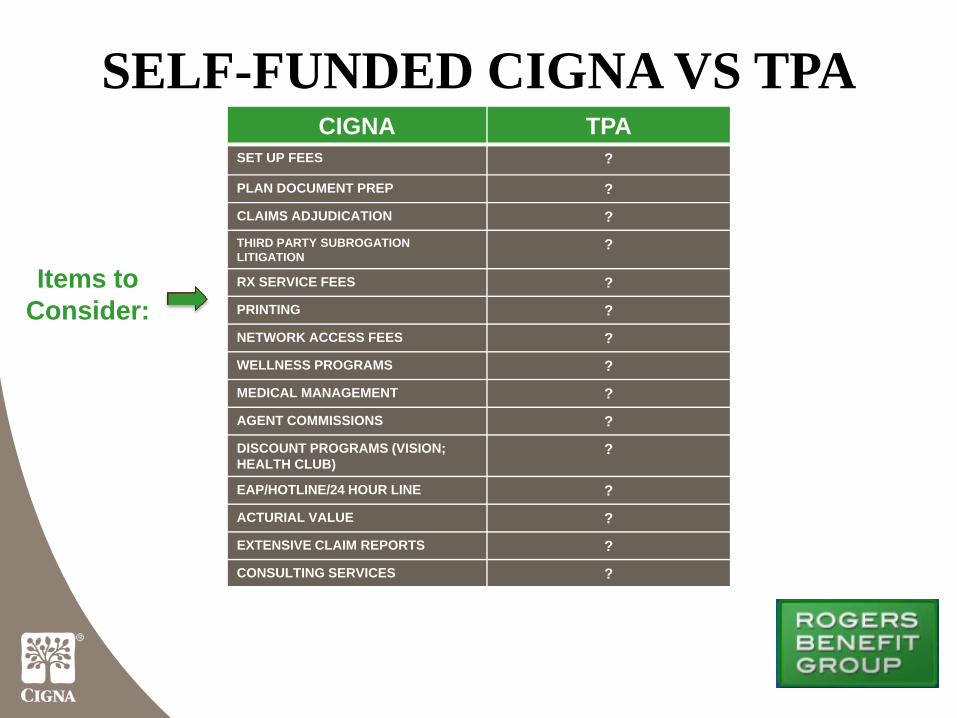

SELF-FUNDED CIGNA VS TPACIGNA TPA

SET UP FEES ?

PLAN DOCUMENT PREP ?

CLAIMS ADJUDICATION ?THIRD PARTY SUBROGATION LITIGATION

?

RX SERVICE FEES ?

PRINTING ?

NETWORK ACCESS FEES ?

WELLNESS PROGRAMS ?

MEDICAL MANAGEMENT ?

AGENT COMMISSIONS ?

DISCOUNT PROGRAMS (VISION;HEALTH CLUB)

?

EAP/HOTLINE/24 HOUR LINE ?

ACTURIAL VALUE ?

EXTENSIVE CLAIM REPORTS ?

CONSULTING SERVICES ?

Items to Consider:

22

Requirements for Quoting

23

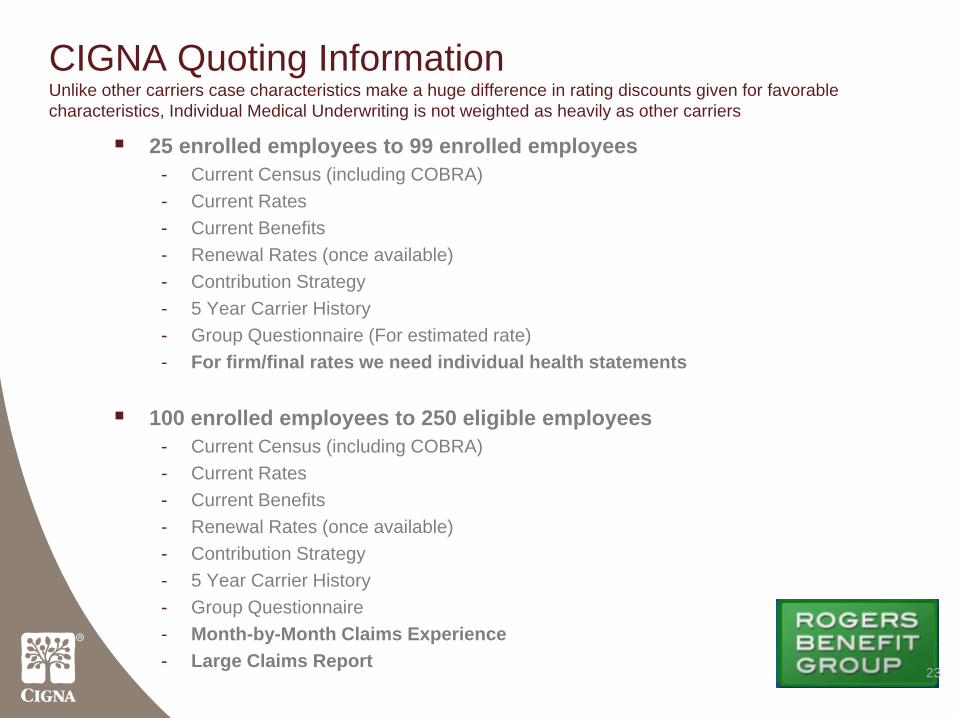

CIGNA Quoting InformationUnlike other carriers case characteristics make a huge difference in rating discounts given for favorable characteristics, Individual Medical Underwriting is not weighted as heavily as other carriers

25 enrolled employees to 99 enrolled employees- Current Census (including COBRA)- Current Rates- Current Benefits- Renewal Rates (once available)- Contribution Strategy - 5 Year Carrier History- Group Questionnaire (For estimated rate)- For firm/final rates we need individual health statements

100 enrolled employees to 250 eligible employees- Current Census (including COBRA)- Current Rates- Current Benefits- Renewal Rates (once available)- Contribution Strategy- 5 Year Carrier History- Group Questionnaire - Month-by-Month Claims Experience- Large Claims Report

Confidential unpublished property of CIGNA. Do not duplicate or distribute. Use and distribution limited solely to authorized personnel. © 2010 CIGNA

24

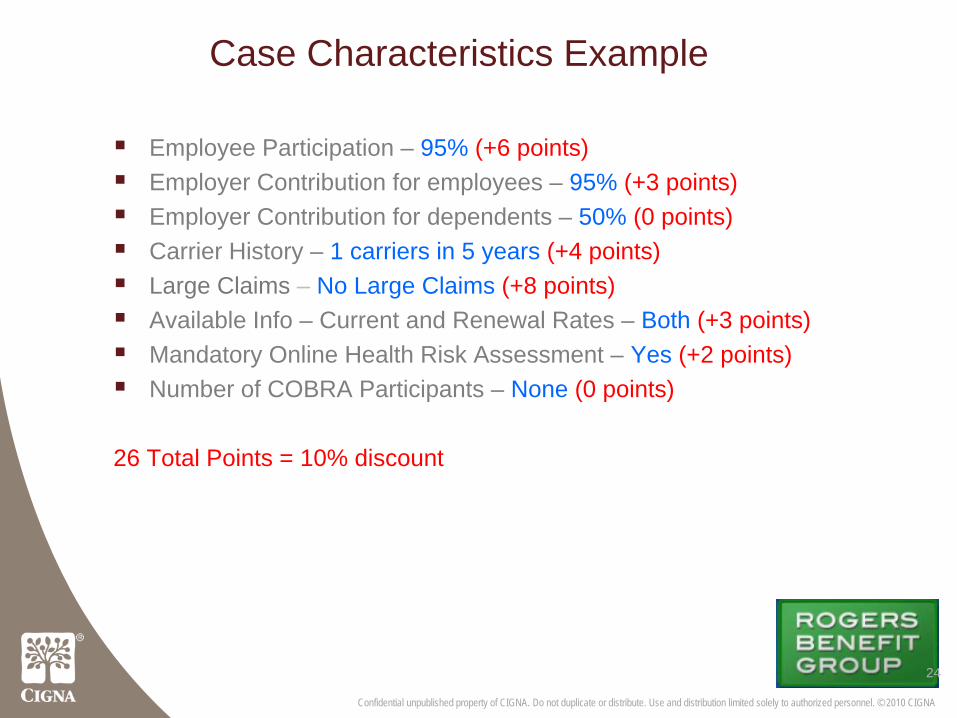

Case Characteristics Example

Employee Participation – 95% (+6 points)Employer Contribution for employees – 95% (+3 points)Employer Contribution for dependents – 50% (0 points)Carrier History – 1 carriers in 5 years (+4 points)Large Claims – No Large Claims (+8 points)Available Info – Current and Renewal Rates – Both (+3 points)Mandatory Online Health Risk Assessment – Yes (+2 points)Number of COBRA Participants – None (0 points)

26 Total Points = 10% discount