Embed Size (px)

Citation preview

Cash Management & eBanking January 2014

SEPA Country-Specific Information France

Contents

INTRODUCTION 3 END-DATE INFORMATION 3 IBAN CONVERSION SERVICE 4 SEPA PRODUCTS 4 SEPA CREDITOR IDENTIFIER (CI) 6 MANDATE INFORMATION 6 SEPA FORMATS 7

3

INTRODUCTION

This document provides an overview of country-specific information you need in order to successfully overcome the challenges of SEPA and achieve a seamless migration. Being properly informed and equipped with the necessary tools, you will be able to fully realise all the potential the new SEPA instruments will bring.

SEPA regulations apply to France and the following French territories: Guadeloupe, Guyana, Martinique, La Réunion, Saint Martin, Saint Barthélémy. Regulation 260/2012 does not apply to Mayotte, Saint Pierre et Miquelon, New Caledonia, French Polynesia and Wallis-and-Futuna. French Polynesia; New Caledonia and Wallis-and-Futuna will apply a special scheme called “SEPA COM PACIFIQUE”, starting from February 2014 onwards.

END-DATE INFORMATION

All national SEPA initiatives are coordinated by the National SEPA Committee which is co-headed by Banque de France and the French Banking Federation; Corporates are represented by the French Corporate Treasurer Association (AFTE). We expect the full national reachability to be ensured within the SEPA migration end-date which was agreed upon for 31 January 2014.

Regulation (EU) no. 260/2012 sets the end-dates for national payment schemes and SEPA migration schemes, as follows:

END-DATE INFORMATION

The end date was set for 31 January 2014 based on the EU regulation 260/2012. The amendment for an additional transition period until 31 July 2014 was approved by the EU authorities. The related impact on national products is linked to the end-date information. For more information please refer to the link below.*** National formats 31 January 2014 Domestic formats will not be accepted by banks after January 2014 Payment part of French “Virement Commercial” (VCom) has to migrate to SEPA Credit Transfer

“Niche products” 31 January 2016 (Products with less than 10% market share/country) “Titre Interbancaire de Paiement” (“TIP”)** “Télérèglement” (“TEP”)**

National products with a different migration date No decision has been taken yet regarding French “LCR”* valid until at least February 2016 IBAN-only national transactions 31 January 2014 IBAN-only cross-border transactions 31 January 2016

* ''TIP” and ''TEP” are typical French products, similar to domestic direct debit (''Prélèvement”). The difference between ''Prélèvement” and ''TIP” is that for ''TIP”, the debtor needs to authorise every transaction by signing and returning a paper that comes together with the invoice. In case of ''TEP”, the difference to a normal ''Prélèvement” is that with ''Télérèglement” the debtor indicates to his bank in advance the amount of the transaction, for every collection. ** ''LCR” – ''Lettre de Change Relevée” (for now out of the SEPA scope) *** http://www.ecb.europa.eu/paym/sepa/pdf/countries/fr_sepa_migration_fact_sheet.pdf?f46b124a40886a8b94cfe406e5c793ff

4

IBAN CONVERSION SERVICE

IBAN structure IBAN will replace RIB (Relevé d’Identité Bancaire) and identifies the account. In France, the IBAN is composed of 27 characters, structured as follows: Positions 1 – 2: ISO country code (FR for France); Positions 3 – 4: Check digits ( “76” in most cases when the account number is only composed of digits) Positions 5 – 9: Legacy code – Banque; Positions 10 – 14: Legacy code – Guichet, Positions 15 – 25: Account number (digits and/or letters); Positions 26 – 27: French check digits (clé RIB):

The IBAN calculation can be handled by the customer, given the procedure in place to derive IBAN from RIB, via a bank or an external provider.

SEPA PRODUCTS

The following payment/collection schemes are going to be affected by the SEPA migration and discontinued after 31 January 2014: Domestic credit transfers, including salary payments, will have to be migrated to SCT; Domestic Virement Commercial (VCom) will have to be migrated to SCT for the payment part; Cross-border credit transfers – when the beneficiary is located within the SEPA area and the currency is EUR – are going to

be replaced by SCT; The domestic collection scheme called “Prélèvement” (“Prélèvement Accéléré” included), will have to be migrated to SDD

Core or SDD B2B.

While designing the SEPA migration approach, companies should get complete and exact knowledge of the differences in the required data. Related main aspects are summarised below:

SEPA Credit Transfer

COMPARISON – FRENCH DOMESTIC CREDIT TRANSFER VS. SEPA CREDIT TRANSFER

Criteria Domestic Credit Transfer SEPA Credit Transfer Coverage area Only for domestic payments For domestic and cross-border payments

within the SEPA area

IBAN/BIC Only Relevé d’Identité Bancaire (RIB) required IBAN/BIC* of the beneficiary required Transactions N/A SHARED fees only

EUR currency No maximum limit

Processing time** 1 day guaranteed since 2012 1 day guaranteed since 2012 Execution date Debit: At execution date

Credit: D+1 Debit: At execution date Credit: D+1

Central Bank reporting N/A N/A

* BIC mandatory for domestic payments only until 31 January 2014. BIC mandatory only for cross-border payments until 31 January 2016 ** Working days

5

Additional optional services SCT Reversal, as a mechanism that allows the reversal of wrongly sent SCT transactions, can be applied only to the correction of technical errors made by banks. The types of errors are strictly limited to: duplicate sending, technical problems resulting in erroneous bank coordinates of the beneficiaries (BIC or IBAN) or erroneous amounts. The amount of the Reversal has to be strictly identical to the amount of the original transaction.

SEPA Direct Debits SDD does not allow per se any type of mandate management, but will require a bilateral exchange of documents between creditor and debtor, without involving banks. Mandates can't be activated on the initiative of the debtor’s bank but only on the initiative of the creditor. Notifications of mandate modification or cancellation are sent to the beneficiary by the debtor.

SDD scheme supports the following data set which includes the mandate-related information: IBAN and BIC of the payer’s payment account to be debited for the collection; Unique Creditor Identifier – which replaces the NNE (“Numéro National Emetteur”); Date of signing the mandate.

COMPARISON – DOMESTIC DIRECT DEBITS VS. SEPA DIRECT DEBITS

Criteria Prélèvement Prélèvement Accéléré SDD Core SDD B2B Allowance of SDD collection

No Local format does not contain all necessary data to allow SDD

Yes

Region Only domestic Only domestic SEPA area SEPA area Format CFONB160 CFONB160 XML ISO20022 pain.008 XML ISO20022 pain.008 Sequence type N/A N/A Recurrent/One-off Recurrent/One-off Eligible debtor Consumer and non-

consumer Consumer and non-consumer

Consumer and non-consumer

Non-consumer only*

Intra banking submission D-4 D-2 D-5 (First/One-off) D-2 (Recurrent)

D-1 (all)

Mandate management Debtor Mandate Flow Debtor Mandate Flow SDD is based on the Creditor Mandate Flow Model: Creditor is fully responsible for the mandate storage and management.

SDD is based on the Creditor Mandate Flow Model: creditor is fully responsible for the mandate storage and management.

Refunds Unconditional refund right within 8 weeks, following the date of debit 13 months for an unauthorised transaction

Unconditional refund right within 8 weeks, following the date of debit 13 months for an unauthorised transaction

Unconditional refund right within 8 weeks, following the date of debit 13 months for an unauthorised transaction

No refund for an authorised transaction 13 months for an unauthorised transaction

Latest date for Bank return

D+5 D+2 D+5 D+2

IBAN and BIC IBAN of the debtor’s account and BIC of the debtor’s bank are not required RIB only

IBAN of the debtor’s account and BIC of the debtor’s bank are not required RIB only

IBAN of the debtor’s account and BIC* *of the debtor’s bank are required

IBAN of the debtor’s account and BIC** of the debtor’s bank are required

Mandate checking Mandates are maintained by the debtors’ bank and checked against collection order

Mandates are maintained by the debtors’ bank and checked against collection order

No preliminary check of the mandate by the debtor bank

Mandate must be stored at debtor’s bank before the first collection and checked by the debtor bank

* In France, micro-enterprises are seen as businesses and can therefore be declared debtors for B2B SDD mandates; ** BIC mandatory only for domestic payments until 31 January 2014. BIC mandatory only for cross-border payments until 31 January 2016.

6

SEPA CREDITOR IDENTIFIER (CI)

CI for France (and French territories in scope) CI (“Identifiant Créancier SEPA” ) format consists of 13 characters structured as follows: Positions 1 – 2: ISO country code (FR for France); Positions 3 – 4: Check digits; Positions 5 – 7: Creditor Business Code (to be assigned by creditor, by default “ZZZ”); Positions 8 – 13: NNE (“Numéro National d’Emetteur”).

Currently, a company requesting a NNE in France will automatically receive the SEPA CI with its NNE.

How to obtain a SEPA Creditor Identifier Banque de France manages the SEPA CI Register.

Only creditors with an account registered at the Payment Service Provider (PSP) in France may ask for a French CI. The request must be introduced by the creditor to his bank which, in turn, will make the request to the Banque de France. CI is transmitted by Banque de France to the requesting PSP which relays the information to the Creditor.

When requesting a SEPA CI from his bank, the creditor must also submit an “Extrait Kbis” (extract from the Trade Register) at least 3 months in advance. This document can be requested from a “Greffe du Tribunal de Commerce” (physically or online via infogreffe.fr).

MANDATE INFORMATION

Mandate migration All existing Prélèvement mandates remain valid for SDD Core SDD without requiring a new signature from your counterparties. For SDD B2B a new mandate is necessary.

The creditor must inform the debtor about the migration to SDD and provide the following information: the chosen migration date, its SCI and the Unique Mandate Reference of the migrated authorisation(s).

New mandates Any new mandate can be paper-based or electronic, but it must be signed by the Debtor. There is no definite norm for the new mandate but some information is compulsory. Mandates are identified by a unique couple of Mandate Reference + CI.

For B2B Mandates, the Debtor must inform his bank and provide the characteristics of the new mandate.

7

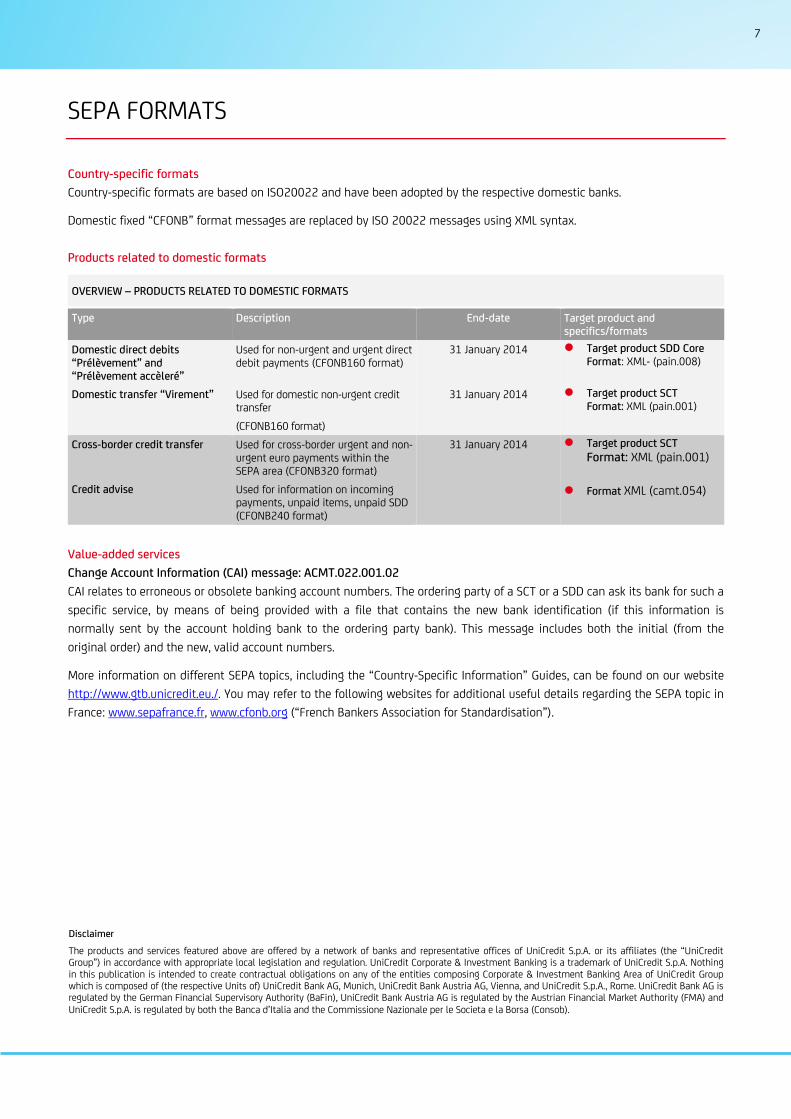

SEPA FORMATS

Country-specific formats Country-specific formats are based on ISO20022 and have been adopted by the respective domestic banks.

Domestic fixed “CFONB” format messages are replaced by ISO 20022 messages using XML syntax.

Products related to domestic formats

OVERVIEW – PRODUCTS RELATED TO DOMESTIC FORMATS

Type Description End-date Target product and specifics/formats

Domestic direct debits “Prélèvement” and “Prélèvement accèleré”

Used for non-urgent and urgent direct debit payments (CFONB160 format)

31 January 2014 Target product SDD Core Format: XML- (pain.008)

Domestic transfer “Virement” Used for domestic non-urgent credit transfer (CFONB160 format)

31 January 2014 Target product SCT Format: XML (pain.001)

Cross-border credit transfer Used for cross-border urgent and non-urgent euro payments within the SEPA area (CFONB320 format)

31 January 2014 Target product SCT Format: XML (pain.001)

Credit advise Used for information on incoming payments, unpaid items, unpaid SDD (CFONB240 format)

Format XML (camt.054)

Value-added services Change Account Information (CAI) message: ACMT.022.001.02 CAI relates to erroneous or obsolete banking account numbers. The ordering party of a SCT or a SDD can ask its bank for such a specific service, by means of being provided with a file that contains the new bank identification (if this information is normally sent by the account holding bank to the ordering party bank). This message includes both the initial (from the original order) and the new, valid account numbers.

More information on different SEPA topics, including the “Country-Specific Information” Guides, can be found on our website http://www.gtb.unicredit.eu./. You may refer to the following websites for additional useful details regarding the SEPA topic in France: www.sepafrance.fr, www.cfonb.org (“French Bankers Association for Standardisation”).

Disclaimer The products and services featured above are offered by a network of banks and representative offices of UniCredit S.p.A. or its affiliates (the “UniCredit Group”) in accordance with appropriate local legislation and regulation. UniCredit Corporate & Investment Banking is a trademark of UniCredit S.p.A. Nothing in this publication is intended to create contractual obligations on any of the entities composing Corporate & Investment Banking Area of UniCredit Group which is composed of (the respective Units of) UniCredit Bank AG, Munich, UniCredit Bank Austria AG, Vienna, and UniCredit S.p.A., Rome. UniCredit Bank AG is regulated by the German Financial Supervisory Authority (BaFin), UniCredit Bank Austria AG is regulated by the Austrian Financial Market Authority (FMA) and UniCredit S.p.A. is regulated by both the Banca d’Italia and the Commissione Nazionale per le Societa e la Borsa (Consob).

8

UniCredit Bank AG Corporate & Investment Banking www.unicredit.eu Cash Management & eBanking Am Tucherpark 1 D-80538 Munich