Embed Size (px)

Citation preview

T H E B O M B A Y C H A R T E R E D A C C O U N T A N T J O U R N A L

BC

AJ

VO

L. 52-A PA

RT 6 | S

EPTEM

BER

2020

SEPTEMBER 2020

VOL. 52-A PART 6

PAGES 156

PRICE: R100

THE FINANCE ACT, 2020

19DECODING GST: ROLE OF A STATUTORY AUDITOR VIS-À-VIS GST

84DATA-DRIVEN INTERNAL AUDIT – II: PRACTICAL CASE STUDIES

14‘COLLABORATE TO CONSOLIDATE’ – A GROWTH MODEL FOR PROFESSIONAL SERVICES FIRMS

11C U R I O S I T Y T O C R E AT I V I T Y

3BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

TAXATION ARTICLE: The Finance Act, 2020 | 19

REPORT: ROLE OF THE PROFESSIONAL IN A CHANGING TAX LANDSCAPE | 36 Direct Taxes

GLIMPSES OF SUPREME COURT RULINGS | 57 CONTROVERSIES: TAXATION OF RECEIPT BY RETIRING PARTNER | 67 IN THE HIGH COURTS: PART A: REPORTED DECISIONS 42 (i) Business expenditure – Disallowance – Sections 14A and 36(1)(iii) of ITA, 1961 –

Interest on borrowed capital – Finding that investment from interest-free funds available with assessee – Presumption that advances made out of interest-free funds available with assessee – Deletion of addition made u/s 14A justified;

(ii) Unexplained expenditure – Section 69C of ITA, 1961 – Suspicion that certain purchases were bogus based on information from sales tax authority – Neither independent inquiry conducted by A.O. nor due opportunity given to assessee – Deletion of addition by appellate authorities justified; A.Y. 2010-11 : | 47

43 Business expenditure – Deduction u/s 42(1)(a) of ITA, 1961 – Exploration and extraction of oil – Conditions precedent for deduction – Expenditure should be infructuous or abortive exploration expenses, and area should be surrendered prior to commencement of commercial production – Meaning of expression ‘surrender’ – Does not always connote voluntary surrender – Assessee entering into production sharing contract with Government of India and requesting for extension at end of contract period – Government refusing extension – Assessee entitled to deduction u/s 42(1)(a); A.Y. 2008-09 : | 47

44 Capital gains – Exemption u/s 54 of ITA, 1961 – Sale of residential house and purchase or construction of new residential house within stipulated time – Construction of new residential house need not begin after sale of original house; A.Y. 2012-13 : | 48

45 Capital gains – Transfer of bonus shares – Bonus shares in respect of shares held as stock-in-trade – No presumption that bonus shares constituted stock-in-trade – Tribunal justified in treating bonus shares as investments; A.Ys. 2006-07 to 2009-10 : | 49

46 Deemed income – Section 41(1) of ITA, 1961 – Remission or cessation of trading liability – Condition precedent for application of section 41(1) – Deduction must have been claimed for the liability – Gains on repurchase of debenture bonds – Not assessable u/s 41(1); | 49

47 Fringe benefits tax – Charge of tax – Section 115WA of ITA, 1961 – Condition precedent – Relationship of employer and employee – Free samples distributed to doctors by pharmaceutical company – Not fringe benefit – Amount spent not liable to fringe benefits tax; A.Y. 2006-07 : | 50

48 Income – Accrual of income – Mercantile system of accounting – Business of distribution of electricity to consumers – Surcharge levied on delayed payment of bills – Assessee liable to tax on receipt of such surcharge; A.Y. 2005-06 : | 50

49 Offences and prosecution – Sections 271(1)(c), 276C(2), 278B(3) of ITA, 1961 and Section 391 of Cr.P.C., 1973 – Wilful default in payment of penalty for concealment of income – Conviction of managing director and executive director of assessee by judicial magistrate – Appeal – Evidence – Documents to prove there was no wilful default left out to be marked due to inefficiency and inadvertence – Interest of justice – Appellate court has power to allow documents to be let in as additional evidence; A.Y. 2012-13 : | 51

50 Settlement of cases – Sections 245C(1) and 245D(4) of ITA, 1961 – Powers and duties of Settlement Commission – Application for settlement – Duty of Commission either to reject or proceed with application filed by assessee – Settlement Commission relegating assessee to A.O. – Not proper; A.Ys. 2008-09 to 2014-15 : | 51

51 Settlement of cases – Chapter XIX-A of ITA, 1961 – Powers of settlement commission – Application for settlement of case – Settlement commission cannot consider merits of case at that stage; A.Ys. 2015-16 to 2018-19 : | 52

In this issue . . .Namaskaar | 5 Editorial ‘Taxpayer Services: Message, Meaning and Means – 1/n | 7

From the President | 8

Continuous No. 727 Price Rs. 100 (For Members only)

CONTENTSTHE BOMBAY CHARTERED ACCOUNTANT JOURNAL

VOL. 52-A I PART 6 I SEPTEMBER 2020

Printed and published by Raman Jokhakar on behalf of Bombay Chartered Accountants’ Society, 7, Jolly Bhavan No. 2, New Marine

Lines, Mumbai-400020. Phone : 61377600 E-mail : [email protected]

Printed at Spenta Multimedia Pvt Ltd, Plot 15, 16 & 21/1, Village Chikloli, Morivali, MIDC, Ambernath (West), Dist. Thane.

JOURNAL COMMITTEE

QUOTE OF THE MONTHThe aim of education is

the knowledge, not of facts, but of values.

WILLIAM INGE

EDITORIAL BOARD Chairman & Editor I Raman Jokhakar

ConvenersJagdish Punjabi I Vinayak PaiPublisher I Raman JokhakarMembers of Editorial Board

Anil Sathe, Anup Shah, Ashok Dhere, Gautam Nayak, Kishor Karia, Sanjeev Pandit,

Sunil Gabhawalla

Suhas Paranjpe I Abhay MehtaMembers

Abbas Jaorawala | Bhadresh Doshi | Chandrashekhar Vaze | Chetan Shah | Gaurav

Shah | Jagdish Shah | Kinjal M. Shah | Mihir Sheth | Nitin Shingala | Parth Desai |

Puloma Dalal | Rajaram Ajgaonkar | Riddhi Lalan | Ritu Punjabi | Rutvik Sanghvi |

Shreyas Shah | Sonalee Godbole | Tarunkumar Singhal | Zubin Billimoria.

4 BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

were not in nature of royalty, whether under the Act or Article 12 of DTAA; fees for management services (such as sales support, financial advisory and human resources assistance) and fees for referral services did not satisfy the requirement of ‘make available’ under Article 12 of DTAA | 44

17 Article12 of the India-Ireland DTAA – Consideration received by the assessee from supply / distribution of its copyrighted software products was not chargeable to tax in India as royalty under Article 12 of India-Ireland DTAA | 45

18 Article 11(3)(c) of the India-Mauritius DTAA – Interest income earned from India by a Mauritian company engaged in the banking business is exempt under Article 11(3)(c) of the India-Mauritius DTAA; in terms of Circular No 789, TRC issued by Mauritius tax authority is valid proof of residence as well as beneficial ownership | 46

ACCOUNTANCY AND AUDIT ARTICLE: Data-Driven Internal Audit – II: Practical Case

Studies | 14 Ind AS/IGAAP – Interpretation & Practical Application | 78 FROM PUBLISHED ACCOUNTS | 110 FINANCIAL REPORTING DOSSIER | 129

CORPORATE AND OTHER LAWS SECURITIES LAWS: Disgorgement of Ill-Gotten Gains – A US Supreme

Court Judgment and a SEBI Committee Report | 101 ALLIED LAWS | 103 LAWS AND BUSINESS: Coparcenary Right of a Daughter in Father’s

HUF: Final Twist in The Tale? | 106 CORPORATE LAW CORNER | 113 RIGHT TO INFORMATION (r2i) | 122

PRACTICE MANAGEMENT ARTICLE: ‘Collaborate to Consolidate’ – A Growth Model for

Professional Services Firms | 11

NEWS AND VIEWS LIGHT ELEMENTS | 10

REGULATORY REFERENCER | 126 MISCELLANEA | 134 TECH MANTRA | 139 REPRESENTATION | 141 WHO CONTROVERSY: LACK OF GLOBAL LEADERSHIP IN

CORONA CRISIS | 143 SOCIETY NEWS | 148

Disclaimer The views expressed in this journal are the personal views of the contributors and the BCA Society does not necessarily concur with the same. The opinions expressed herein should not be construed as legal or professional advice. Neither the BCA Society, the publisher, the editor nor contributors are responsible for any decisions taken by readers on the basis of these views.

Total No. of Pages : 156 including Covers

Your feedback may be sent to

IN THE HIGH COURTS: PART B: UNREPORTED DECISIONS 9 Reopening – Capital gains arising on conversion of the land into

stock-in-trade – Closing stock has to be valued at cost or market price whichever is lower – No reason to believe income had escaped assessment – Reopening bad in law: Sections 45(2) and 147 of the Act | 53

TRIBUNAL NEWS: PART A: REPORTED DECISIONS 20 Section 50B read with sections 2(19), 2(42C) and 50 – Windmills of an

assessee, engaged in the business of aqua culture, export of frozen shrimp, sale of hatchery seed and wind-power generation, along with all the assets and liabilities, constitute an ‘undertaking’ for the purpose of slump sale | 40

21 Sections 28, 36(1)(iii) – In a case where since the date of incorporation the assessee has carried on substantial business activities such as raising loans, purchase of land, which was reflected as stock-in-trade in the books of accounts, and entering into development agreement, the assessee can be said to have not only set up but also commenced the business. Consequently, interest on loan taken from bank for purchase of land which was held as stock-in-trade is allowable as a deduction | 40

22 Sections 2(47), 28(i), 45 – Gains arising on transfer of development rights held as a business asset are chargeable to tax as ‘business income’ – Only that part of the consideration which accrued, as per terms of the agreement, would be taxable in the year of receipt | 41

TRIBUNAL NEWS: PART B: UNREPORTED DECISIONS 12 Section 254: Non-consideration of decision of jurisdictional High Court,

though not cited before the Tribunal at the time of hearing of appeal, constitutes a mistake apparent on record | 42

13 Section 35(1)(ii): Deduction claimed by an assessee in respect of donation given by acting upon a valid registration / approval granted to an institution cannot be disallowed if at a later point of time such registration is cancelled with retrospective effect | 42

14 Section 28: Share of profits paid to co-developer based on oral understanding not disallowable as the recipient had offered it to tax and there was no revenue loss and the transaction was tax-neutral | 43

Indirect Taxes

DECODING GST: Role of a Statutory Auditor Vis-À-Vis GST | 84 RECENT DEVELOPMENTS IN GST | 91 RECENT DECISIONS PART A: Service Tax | 93 RECENT DECISIONS PART C: Goods and Services Tax | 94

International Taxation INTERNATIONAL TAXATION: Taxability of a Project Office or Branch

Office of a Foreign Enterprise in India | 114 TRIBUNAL NEWS : PART C 16 Article 12 of India-Singapore DTAA; Section 9 of the Act – Provision for

IT infrastructure management and mailbox / website hosting services

672 (2020) 52-A BCAJ

5BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

673 (2020) 52-A BCAJ

attitudes, feelings and motivations. Our subconscious mind instinctively responds to harshly spoken words, expressions and physical gestures. But if we can control such reactions, we will not only emerge sharper but also as better, happier and more contented individuals.

I believe that despite the real world’s annoyances and

to overlook a negative reaction, thus ensuring a higher state of mind. On the physical level it is a well-established fact that our mental attitude does impinge on health! It is surely much easier for those who have deeply instilled these factors in their subconscious / spiritual level.

It is only by following what is dharma for our body and for our mind that we can strengthen our immune system

a clean lifestyle, a supportive attitude and spiritual endeavours will certainly boost our immune system. Our scriptures say that Dharma, grounding, withdrawal from materialistic activities and practices of Japa and Daan are internal preventive means.

While modern medicine does provide quick relief, debates continue about the side-effects and probable long-term harms of the same. But alternate medicine and cure undoubtedly educate us on how to keep the environment and ourselves naturally clean.

The spiritual immune system and the physical immune system are deeply interrelated. It is hard to separate one from the other and I believe that best results are obtained by working on health at both levels. We cannot possibly

develop the strength to handle them.

Even as the battle against the existing pandemic is being fought primarily by our healthcare workers, we can do our bit by limiting our exposure to the virus by staying indoors, maintaining required social distancing and following basic hygiene protocols to improve both physical and social immunity levels.

How can I emerge stronger through this devastating pandemic and become a real winner in a new and changed world? This is a question that must have certainly agitated everyone’s mind in these last few months.

So much has been written and discussed about the current situation. The actions that you take now and in

attitude towards life. And while the impact of this crisis will vary across regions, it will be no exaggeration to say that this time around the burden of destiny is real.

What is emerging from the competing demands and chaotic conditions is the paramount importance of being positive and doing the right thing at the right time. After all, anxiety and fear adversely affect the physiological systems that protect individuals from infection.

Let’s begin with immunity, the most desired condition that everyone wishes for. In today’s technical world the primary role of immunity is to recognise viruses and to obliterate them. Many good measures have been discussed and prescribed for improving immunity. These include a healthy diet, ample sleep, optimum hydration, regular exercise, minimising stress, meditation, yoga and pranayama, avoiding smoking and alcohol, etc. The most favoured therapy in vogue is the use of immunity-boosting supplements and foods.

If and when one gets infected, timely treatment is of paramount importance. However, healing involves not

body's immunity system. The same principle applies to our spiritual healing, too.

The Bhagavad Gita says that we should not fan our likes and our dislikes. If such thoughts develop in our minds, we should simply ignore them. But this is easier said than done.

We do strive to have a spiritual immune system. In general, such a system refers to our reactions to thoughts,

NAMASKAARNARAYAN PASARI

Chartered Accountant

NEED FOR IMMUNITY AND SPIRITUALITY IN PANDEMIC

6 BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

674 (2020) 52-A BCAJ

Available at leading law bookshops all over India or write to:

BHARAT LAW HOUSE PVT. LTD. T-1/95, Mangolpuri Industrial Area, Phase-I, New Delhi-110 083 Phones: 2791 0001-03

E-mail: [email protected] Website: www.bharatlaws.com Shop Online at: www.bharatlaws.com

Bharat's Budget Publications & Much More

DIRECT TAXES READY RECKONER

by Mahendra B. Gabhawala `

Bharat'sINCOME TAX ACT with Departmental Views

` Incorporating at proper places amendments made by

Finance Minister's Announcements/Press Release dated 13-5-2020 Finance Act, 2020

Taxation and Other Laws (Relaxation of Certain Provisions) Ordinance, 2020 Bharat's

`

Bharat's

`

Bharat's

`

by`

by`

by`

by`

by`

by`

by` by

`

by

`

by` by

by`

Bharat's

`

`by

`by

`

by

` with

withby

`

Sampath Iyengar's

Revised by

`

V.S. Wahi’s Treatise on COMPANIES ACT, 2013

Foreword by Justice D.K. JAIN, Former Judge, Supreme Court of India

with FREE Updates & Complimentary Bharat's Companies Act with Rules

7BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

675 (2020) 52-A BCAJ

EDITORIALA taxpayer is that rare citizen who creates value, earns income and parts with a portion of it as tax for nation-building. Just as it is the ‘legal’ obligation to pay tax, there is a much ‘higher moral social’ obligation upon the government to ensure that the taxpayer is treated as a valued patron and ensure that his taxes give him a bang for his buck.

Faceless Assessment and the Taxpayer’s Charter (TC) is an awakening and realisation of the above understanding. This move is what a wise government and sincere taxpayer would want. PM Modi spoke candidly about making the tax system and assuring the honest taxpayer of

Over the last few years, calibrated sequential changes were undertaken – the black money act, DeMo, post-DeMo amnesty scheme (GKY), the Benami Act, reduction of rates for corporates and individuals, increasing the threshold for the Department to litigate, dispute resolution Vivad se Vishwas scheme, E-assessments, etc.

its rightful place from posters in hallways to the statute book. The directional change is worthy of appreciation for what otherwise to many of us was a no-brainer. However,

Here are some thoughts on how this process can be made real and robust.

We have serious consequence

taxpayers. For a law to be fair, we need equivalent

and ‘jehadism’ (all for lack of a vocabulary which needs to be evolved) on the Tax Department depending on the

TAXPAYER SERVICES: MESSAGE, MEANING AND MEANS – 1/n

intensity of their actions that eventually get turned down at subsequent levels of appeal.

monetarily and otherwise. An assessee should be compensated for the hassle that she has to go through.

Another example is of prosecution, which if proved excessive or overruled, the ITO must face the music for irresponsible behaviour that resulted in agony, cost and loss of reputation.

The taxpayer should be able to take grounds of calling the order ‘perverse’, ‘excessive’, or ‘illegal’ (all for lack of a vocabulary which needs to be evolved) and should be able to claim reverse penalty on the Department if he wins. Grounds such as

and that would give the taxpayer equal ‘power’ to call the bluff of the ITO.

Setting targets should be made illegal. The vocabulary, mentality and methods that follow a ‘target regime’ create bias against a fair, respectful and reasonable assessment. The TC is perhaps one of the best news of the year. The change deserves our support, encouragement and positivity. At the same time, as the title of this Editorial

.

Raman JokhakarEditor

8 BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

676 (2020) 52-A BCAJ

Many things have happened all around us in the recent past. On 20th August, the BCAS along with the BCA Foundation hosted the Fifth Narayan Varma Memorial digital event jointly with other organisations. Everything happened virtually in the true spirit of ‘the show must go on’ and following the positive attitude of the Late In the panel discussion

psychologist and a Covid survivor CA professional who shared their thoughts and experiences. As per tradition, the BCA Foundation recognised the social contributions of its CA nominee Sanjay Hegde and felicitated him.

This year, the volunteers of the BCAS and the BCA Foundation could not visit Dharampur for the annual tree plantation programme. This initiative was started

now gone on to over 300 trees. We started with seven volunteers visiting the place and now it is over 40 with a

th August we arranged the tree plantation event via a digital meeting with the trustees of the Sarvodaya Parivar Trust with video presentations of the Dharampur site. We followed ‘Work from Home’ here, too, in an innovative manner with our ‘BCAS Green Warriors’. We felicitated the volunteers who planted trees in and around their localities and carried out tree plantation this year although they were working from home.

In the West, tech companies have surged past every other industry in this digital transformation regime

most famous equity benchmark, the Dow Jones Industrial Average of USA, replaced the world's biggest company of the last decade, viz., Exxon Mobile Corp., from the

steady challenges faced by commodity companies

economies, too.

‘Retire from your job, but never retire your mind.’ These are golden words. Retirement is a stage of life that could be a new beginning with new initiatives on the family front, the social front, or in one’s personal space which might have been missed during the days of one’s employment.

The person who plans his retirement years in advance –

prudent and wise.

th August, on the occasion of India's 74th

(MSD) bid adieu to international cricket and thus called

was, as we know him well, done in his normally cool, silent style, with very few words.

‘Looking at you as just a sportsperson would be an injustice. The correct way to assess your impact is as a phenomenon! Rising from humble beginnings in a small town, you burst onto the national scene, made a name for yourself and, most importantly, made India proud,’ – this is how the Hon. Prime Minister, Mr. Narendra Modi, wished the hero of the Word Cup. How aptly the person and the situation are portrayed in these few words. All Indians would always be proud of MSD and he would be an inspiration to the next generation. I wish and hope that post-retirement he would take up and initiate the setting up of a training academy to create more MSDs for Indian cricket.

Recently, the Reserve Bank of India (RBI) published its th June, 2020). On

a review of the report and certain comments therein, I, as an accounting professional, observed three key perspectives – accountants, auditors and economics / investment.

The accountant's perspectiveRBI’s lower income and higher provisions resulted in the transfer of lesser surplus to the government. It fell to Rs.

The auditor's perspective

FROM THE PRESIDENTMy Dear Members,

9BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

677 (2020) 52-A BCAJ

but progressive and innovative. The report narrates in detail the various measures initiated by RBI including progressive reductions in the Repo rate and the various windows to infuse additional liquidity to lead the economy onto the path of growth.

Come September and let it bring changes much awaited and longed for. May I close this page by requesting you to visit our site bcasonline.org for extremely relevant and innovative events in the month of September, 2020, such as M&A – Master Class, Brand Building by professional

BCAS Global social media handle for the events missed, if any.

Best Regards,

CA Suhas ParanjpePresident

though low-value online cybercrimes arising out of net transactions are a cause of worry, too.

Economic / investment perspectiveThe moratorium for loan repayments with the infusion of more than Rs. 3 lakh-crore guarantees by the Central Government has boosted the morale of the MSME sector where banks have started disbursing funds to help the sector recover from the adverse impact of the pandemic and migrant labour.

The sharp cut in corporate tax announced in September,

and build up cash and other current asset balances rather than a fresh CAPEX cycle. This resulted in a weakness in private investment demand and capital expenditure in the economy.

monetary policies cannot be traditional and book-bound

10 BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

The profession was basically rendering a very specialised service to businessmen and many government / private organisations. Under the law then prevailing, it was mandatory for many organisations to avail their professional services.

The persons belonging to that profession were under the impression that the profession was important and indispensable. But the reality was that had it not been legally incumbent, nobody would have willingly gone for their services. The payment to those professionals was always considered as unproductive and was at the bottom of the list of priorities with the users of their services. It was common that the fees of these professionals were kept unpaid for up to three or even four years.

But all of a sudden, the ‘Governors’ of the profession, with a laudable objective to protect the profession, declared that if your fees are unpaid for two consecutive years by a client, you should discontinue your services to that client.

The ‘Governors’ said it would be unethical to render service to that client who owes you so much. There was a big hue and cry against this decision. But the ‘Governors’ said the client cannot escape because no other service provider can accept his work unless the previous person’s fees are paid.

So, the previous professional lost the work. He could not get any other work since all the clients had avoided payments to their respective professionals. The mandatory service could not be rendered by anybody to anybody!

All clients became defaulters under the laws concerned.

businesses were closed.

The government realised the gravity of the situation, so it brought an amnesty scheme. The mandatory compliance was waived. Clients found it more economical to pay the money under amnesty rather than paying fees to the professionals.

This is an article that ‘appeared’ in the daily ‘Futurology’ in the year 2050. The title of the article was ‘Extinct Profession’. It was to mark the Silver Jubilee of the death

‘Overlaw’ in an unknown ocean. The following are some excerpts from the said article:

There has always been a policy in the business that the big players get some work done by small players by offering them a seemingly lucrative business volume. Small players get excited, especially if they are new entrants in the business. Their costing is fully monitored by the big players. After a couple of years of a smooth relationship, the big start delaying the payments. The poor small ones don’t mind it initially. The big ones place larger orders with some small advances.

Again, they withhold the payments. They paint a rosy future before the small players. The poor fellows have no choice.

The small go to a banker and raise funds on the ‘merit’ that they have orders from large corporates. The bankers oblige. Their meters of interest and EMI start ticking. But the small ones cannot function smoothly.

Gradually, the small players see the death of their own businesses. The big ones are scratch-free. They have a hundred reasons for not paying – from ‘quality defects’ to ‘belated deliveries’.

continues forever… Government makes laws against

implementation.

Here is a story where an entire profession in the country had to be closed down 25 years ago. Had the profession survived, it would have celebrated its centenary year in the current year 2050. Continued on Page 90

LIGHT ELEMENTSChartered Accountant

EXTINCT PROFESSION

11BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

‘COLLABORATE TO CONSOLIDATE’ – A GROWTH MODEL FOR PROFESSIONAL SERVICES FIRMS

In today’s times, when the market is seeking lower cost alternatives in every spend and the otherwise not-to-

is increasingly being questioned by CFOs and business owners, with ever-increasing need for specialist advice, the refrain is to come together with like-minded professionals.

prerequisite for professions to grow. It is a huge challenge

changed the rules of the game and advanced the time for these discussions. If you are not growing consistently, there is a case for a relook. If you haven’t thought through

so.

This article is an attempt to provide some ideas and

and work together for their common growth.

thought, analysis and a sustained positive outlook. The mindset of growth has to be foremost for any consolidation to be productive and value accretive. And to start this

good way to proceed.

(I) PREREQUISITES OF CONSOLIDATION

(i) MindsetIt is of paramount importance that the mindset to collaborate, consolidate and grow is clear and positive. Having a positive, open mindset means that one is willing

Consolidation doesn't only have to be by merger. One can consolidate mindsets, expertise, people, teams, functions,

accounts, administration and various other aspects which

and adaptable to change and growth.

(II) GETTING STARTEDIt is also not lost on any of us that coming together for a common client or referred client may be a good way to get started.

For example:When there is a referred client, where a professional refers some matter to another professional, although the other professional will be the primary service provider, the referring professional should contribute actively by providing the background knowledge on the basis of his / her experience and the relationship aspects of dealing

from the referring partner’s experience and expertise.

engaging, powerful, organised and delivered in a properly thought through manner, then you have the right prerequisites for a successful consolidation.

The thesis is that enthusiastic collaboration is a vital ingredient and a prerequisite for sustained, organised

will pursue the above with a lot of enthusiasm and momentum once a road-map is given and a framework is created.

(III) MODELS OF CONSOLIDATION

VAIBHAV MANEKChartered Accountant

Referral

Preferred Partner

Associate

Network

Merger

12 BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

(A) Referral modelThis is a simple, ‘start with’ model. ABC & Co has a client to whom it is providing audit and tax services. The client needs MIS services. Given that ABC & Co is an auditor, it

may no longer be independent. So, ABC contacts XYZ & Co and refers the client’s MIS work. XYZ delivers and invoices fees.

XYZ will in turn ensure that it will not pitch for any other services to the client. If the client comes for any other work, it will get referred back to ABC. This is an unwritten code that is based on trust.

If this is done well, trust develops and this lays the ground

ABC will not work with XYZ in the future. That itself is a good deterrent in this model.

The code of conduct and rules of professional engagement may prohibit payment of referral fees and this needs to be respected.

(B) Preferred partner modelThis is an extension of the referral model, where ABC and

with. If ever there is work coming to ABC which it cannot

Conversely, XYZ will refer work to ABC for any engagement where it needs help / support. In this model again, it is a very clear way of supporting each other in such a way

There could be exceptions where XYZ is not able to service a client of ABC, in which case ABC is obviously

common association and agree to abide by the principles and rules of working under a larger umbrella. The associate

need to change its constitution nor its key areas of work.

referral model and the preferred partner model with more formalised meetings, exchange of knowledge, use of resources, common marketing collaterals and a greater

speed of response and alignment.

years and has proved to be a very credible alternative

biggest difference is that members are free to continue their own brands and they have far more independence in what they choose to do or not to do, including the choice

and choice of sharing of information.

Effectively, there are no compulsions and there are no

territory and is free to conduct or practice any service area without any pre-approval or without worrying about a centrally administered bureaucratic process.

The main disadvantage of an associate model is that it

can choose not to fall in line citing whatever compulsions

(D) Network modelA network model is one of the best ways to grow

global network or a national or regional network, using a common brand, using common tools and having signed a

leadership, a common partner pool and, most importantly, a common identity.

Indeed, over a century it has been proven that the network model has the ability to grow the fastest and to become the largest amongst all prevalent models of collaborations

In a network, the biggest consideration is giving up one’s

the international brand or the national or regional brand

marketing collaterals and service delivery are under the

a foreign brand. In such cases, the network pushes for

rules.

common rules of engagement. Conduct of shared work, sharing of knowledge, territorial restrictions, respect for

wide dissemination of developments and a governance

13BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

structure where partners align with the central leadership

Whilst there are several perceived disadvantages such as loss of one’s own brand, the associated loss of identity and integration into common practices which one may take some time to evolve, understand and add up to, the network model has stood the test of time. It has proven and validated the concept of ‘collaborate to grow manifold’ and critics have accepted the formal network models.

bank account. Effectively, one is ‘all in’. That means it is

There are no real silos, there are no individual mindsets, nor any individual practices.

belief that as long as one is contributing to his or her best abilities, the larger collective will grow. As a partner, I am

In a merger situation, the rules of the game are very different and may appear overwhelming to start with. One should get into a merger only after detailed due diligence and after a few years of working together with one of the

be made, there are positions to be gone away from and yet there's the harmony and beauty of the collective.

A partner may not need to be spending time on areas outside of his or her core focus. What it does is provide partners with adequate time to build, consolidate and grow. Focus on service areas, with administrative or functional work percolating down to the teams, is a positive outcome.

(IV) ROAD-MAP FOR CONSOLIDATION

Having looked at the various models of consolidation, it is now time to look at the execution road-map for consolidation:

USP is critical.

(ii) The objective of the collaboration should be very

working with the best minds, professional growth, sharing of knowledge, newer geographies, recognition of the changing market place and demands of the client? Clarity on the objective is very critical. Often, in the haste of coming together, the main objective is forgotten. That’s to be avoided at all costs.

particular area, the automatic next step will be to have

intensely and with the purpose of achieving a target of

with. These one or two partners have the responsibility of ensuring that the objectives of the collaboration are

(iv) One of the better ways to start is by working together on actual projects. That normally provides a

provides an easy and operational way to get to know the

baby steps is important.

(v) Once some early success is seen, the foremost assumption that all partners are aligned for collective growth will be tested. It will be hard for partners to sit

challenging. Keep moving forward to a point where trust is created and enhanced. Each model should be given adequate chance to work and succeed. At some point,

model.

have to be at it. It’s a constant effort. Take small steps but keep moving forward. It won’t get done overnight. But achieving small successes will pave the way for larger integration. If all cylinders are aligned, the practices will

model.

CONCLUSIONIt is no longer okay to continue the status quo. During

Perhaps, it is time to understand and introspect. It is time to move forward from working as disaggregated practices. It is time to work together. It is time to consolidate

14 BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

DATA-DRIVEN INTERNAL AUDIT – IIPRACTICAL CASE STUDIES

BACKGROUNDInternal auditors are effective in their delivery of professional services only by conducting value-added services. Important value drivers for management are:- cost savings / optimisation,- prevention or detection of frauds,- compliance with procedures and regulations.

These can only be achieved in today’s day and age by adoption of technology for all stages in the life-cycle of the internal audit. It may necessitate getting the data from multiple sources, analysing huge quanta of data,

of data in intelligent form to various stakeholders for action to be taken for improvement/s.

Let’s add the fact that we are moving to remote auditing, again a necessity in today’s circumstances and which would most probably become the new normal in times to come. Remote auditing is already being practised by many organisations where internal auditors carry out internal auditing for global, geographically-spread entities from their internal audit teams based out of India.

In our earlier article (Pages 11-13; BCAJ, August, 2020), we have discussed the necessity of adopting a data-driven

audit, basically explaining ‘why’. Now, we are offering the methodology to be adopted for making it happen, in other words, ‘how’ to do it.

Using what you know(1) DETERMINE WHETHER DATA ANALYTICS IS APPROPRIATE FOR THE AUDIT

judged from the audit objectives and the expected problems, as well as from the data volume, the number

should be given to the usefulness of additional analysis over what is currently provided by the system and whether any special factors apply, such as fraud detection

and investigation, Value for Money audits (in obtaining performance statistics) and special projects.

(2) CONSIDER AUDIT OBJECTIVES AND WHERE DATA ANALYTICS CAN BE USEDData Analytics can be used in different areas with different goals and objectives. Data Analytics is generally used to validate the accuracy and the integrity of data, to display data in different ways and to generate analysis that would otherwise not be available. It can also be helpful in identifying unusual or strange items, testing the validity of items by cross-checking them against other information, or re-performing calculations.

Although Data Analytics allows you to increase your coverage by investigating a large number of items

may still want to extract and analyse a portion of the database by using the sampling tasks within. You could examine a subset of the population (a sample), to predict

a particular event or attribute occurs in the population as a whole.

The quality of the data, your knowledge of the database and your experience will contribute to the success of Data Analytics processes. With time you will be able to increase or widen the scope of investigations (for example, conducting tests which cannot be done manually) to

that you never thought were feasible.

It is also not unusual that far more exceptional items

than other methods and that these may require follow-up time. However, the use of Data Analytics may replace other tests and save time overall. Clearly, the cost of using the Data Analytics Tool must be balanced against

Case Study 1 – General Ledger – What is our Audit Objective?

Chartered Accountants

15BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

to the General Ledger is a common way of committing

appropriateness of journal entries recorded in the General Ledger.

The objectives may include testing for risk or unusual transactions such as:• Journals with no description,• Journals not balancing,• Journals containing keywords,• Journals posted by unauthorised users,• Journals posted just below approval limits,• Journals posted to suspense or contra accounts.

Case Study 2 – Accounts Receivable – What is our Audit Objective?Accounts Receivable is one of the largest assets of a

assurance that the amounts stated are accurate and reasonable.

The objectives may include:• Identify large and / or unusual credit notes raised in the review period,

year,• Isolate customers with balances over their credit limit,• Filter out related party transactions and balances,• Generate duplicates and gaps in the sales invoice numbers,• Match after-date collections to year-end open items / balances.

Preparing data for analysis(3) DETERMINE DATA REQUIRED AND ARRANGE DOWNLOAD WITH PREPARATIONData download is the most technical stage in the process, often requiring assistance and co-operation from Information Technology (IT). Before downloading or analysing the data, it is necessary to identify the required data. Data may be required from more than

the user understands the availability and the details of the databases. You may also have to examine the

relationships between databases and tables.

In determining what data is required, it may be easier

Therefore, it may be better to be selective, ignoring blank

needed. At the same time, key information should not be omitted.

Case Study 1 – General Ledger – Planning – What Data is Required?The Auditor needs to obtain a full General Ledger transactions history for the audit year after all the year-end (period-end) postings have been completed by the client. To carry out a completeness test on the General Ledger transactions, the ‘Final’ Closing Trial Balances at the current and previous year-ends are required. Where possible,

the export of the Trial Balance, this will give assurance over

from the Accounting Software or ERP system.

General ledger initial check for preparing the dataField Statistics can be used to verify the completeness and accuracy of data like incorrect totals, unusual trends, missing values and incorrect date periods in the General Ledger. This pre-check in the data preparation stage allows the Auditor a greater chance of identifying any issues that will cause invalid test results. Comparing difference in totals obtained from the client for the Transaction Totals in the General Ledger with the Field Statistics should be

Analytic tests.

Case Study 2 – Accounts Receivable – Planning – What Data is Required?The Auditor should requisition the ‘AR Customer-wise open items at the year-end’ data. This data provides more details than a simple list of balances because often an Auditor wants to test a sample of unpaid invoices rather than testing the whole customer balance. Further, the Auditor should obtain the ‘Accounts Receivable Transactions’ during the year to analyse customer receipts in the year, to test for likely recoverability. Apart from this, more detailed Data Analytics can be performed on the sales invoices and credit notes, as well as cut-off analysis.

Accounts receivable initial check for preparing the dataField Statistics can be used to verify the completeness and accuracy of data like incorrect totals, unusual trends, missing values and incorrect date periods in the Accounts Receivable (AR) ledger. This pre-check in the data

16 BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

Interpretation of Results – Any gaps in invoicing sequences require further investigation to ensure that revenue has been correctly allocated, as well as to check for improper revenue recognition which can be accomplished by manipulating income records, causing material misstatement.

Discovering patterns, outliers, trends using pre-built analytic intelligenceThe Discover task provides insights through patterns, duplicates, trends and outliers by mapping data to high-

Analytic Intelligence.

• Identify trends, patterns, segmental performance and outliers automatically.• Intuitive auto-generation of dashboards that can then be

(5) REVIEW AND HOUSEKEEPINGAs with any software application, all work done in Data Analytic Tools must be reviewed. Review procedures are often compliance-based, verifying that the documentation is complete and that reconciliations have been carried out.

preparation stage offers the Auditor a better chance of identifying any issues that could cause invalid test results. Comparing difference in totals obtained from the client for the AR Debit Credit Totals with the Field Statistics should

the Analytic tests.

Validating data(4) USE ANALYTIC TASKSCase Study 1 – General Ledger – Highlighting Key Words within Journal Entry Descriptions

– To isolate and extract any manual journal entries using key words or unusual journal descriptions. These can include, but not be limited to, ‘adjustment, cancel, missing, suspense’.

– Apply a search command on the manual

unusual descriptions by using a text search command.

Interpretation of Results – Records shown when using the above criteria would display records which have description narratives that include key terms such as ‘adjustment’, ‘cancel’, ‘suspense’ and ‘missing’, and may require further investigation.

When determining which manual journal entries to select for testing, and also what description should be tested,

misstated through a variety of fraudulent journal entries and adjustments, including:• Writing off liabilities to income,• Adjustments to reserves and allowances (understated or overstated),• False sales reversed after year-end and out-of-period

will need to tailor the said search to the type of manual journal entry that the Auditor is aiming to test.

Case Study 2 – Accounts Receivable – Detecting suppression of Sales

– To test for gaps in invoicing sequences which may indicate unrecorded sales and / or deleted invoices.

– Gap Detection is used to detect gaps in data. These could be gaps within purely numeric or alpha-numeric sequential reference numbers, or these could be gaps within a sequence of dates. Perform a Gap Detection

17BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

The actual history logs from each analytical activity should also be reviewed.

Backup of all the project folders must be done meticulously and regularly.

Clear operating instructions with full details on how to

documented for each project and kept easily accessible for the Audit Teams who will take up the project in the ensuing review period. If necessary, logic diagrams with

appropriate explanatory comments should be placed

could pick up the project in the following year.

CONCLUSIONBy embedding data analytics in every stage of the audit process and mining the vast (and growing) repositories of data available (both internal and external), Auditors can deliver unprecedented real-time insight, as well as enhanced levels of assurance to management and audit committees.

Businesses are faced with unprecedented complexity, volatility and uncertainty. Key stakeholders can’t wait for Auditor’s analysis of historical data. They must be alerted to issues at once and be assured of repetitive monitoring of key risks. Data Analytics empowers Audit to deliver, as well as to serve the business more proactively in audit planning, scoping and risk assessments, and by monitoring key risk indicators closely and concurrently. Auditor’s use of data analytics in every phase of the audit can help management and the audit committee make the right decision at the right time.

18 BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

For more details, write to us at [email protected] or call us on our

Toll Free Nos. Airtel: 1800-102-8177, BSNL: 1800-180-7126 (Mon - Fri, 8:30 am to 5 pm)

Now Available on www.lexisnexis.in

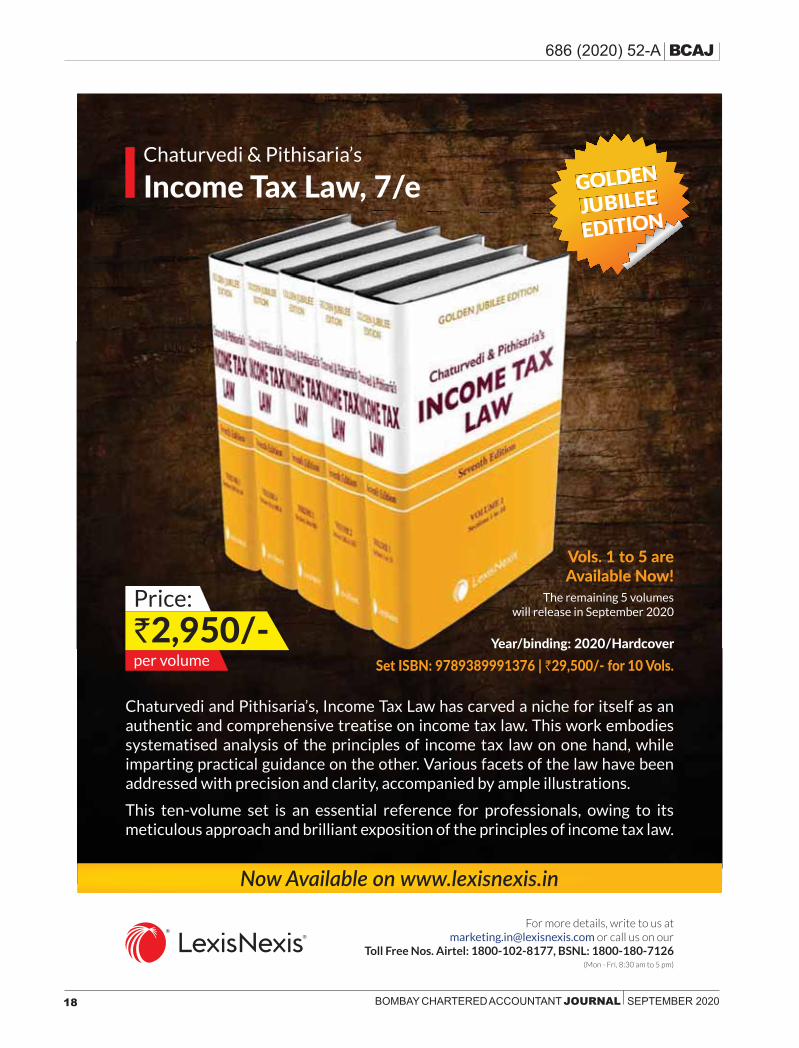

GOLDEN

JUBILEE

EDITION

Chaturvedi and Pithisaria’s, Income Tax Law has carved a niche for itself as an authentic and comprehensive treatise on income tax law. This work embodies systematised analysis of the principles of income tax law on one hand, while imparting practical guidance on the other. Various facets of the law have been addressed with precision and clarity, accompanied by ample illustrations.

This ten-volume set is an essential reference for professionals, owing to its meticulous approach and brilliant exposition of the principles of income tax law.

Price:

`2,950/- per volume

Year/binding: 2020/HardcoverSet ISBN: 9789389991376 | `29,500/- for 10 Vols.

Vols. 1 to 5 are Available Now!

The remaining 5 volumes will release in September 2020

Chaturvedi & Pithisaria’s

Income Tax Law, 7/e

19BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

THE FINANCE ACT, 2020

1. BACKGROUND

st

February, 2020. The Finance Bill, 2020, presented along with the Budget with certain amendments suggested by the Finance Minister on the basis of discussions with the stakeholders, was passed by the Parliament without any discussion on 23rd March, 2020. It received the assent of the President on 27th March, 2020. The Finance Act, 2020 was passed by both the Houses of Parliament without any discussion in view of the recent lockdown due to the coronavirus pandemic which has affected India and the whole world.

relating to the Direct Taxes, can be summarised as under:(i) In line with the reduction in rates of Income-tax for certain domestic companies which forgo certain deductions and tax incentives introduced last year, the Finance Act, 2020 provides for revised slabs of Income-tax rates for Individuals and HUFs who do not claim certain deductions and tax incentives.(ii) Dividend Distribution Tax, hitherto payable by companies and Mutual Funds and consequent exemption on dividend received by shareholders and unitholders,

st April, 2020. Consequently, the exemption in respect of dividend receipt enjoyed by the shareholders and unitholders of Mutual Funds has been withdrawn.(iii) The compliance burden of Charitable Trusts and Institutions has been increased.(iv) The Finance Minister has recognised the need for

st April, 2020 to provide that CBDT shall adopt and declare the Taxpayer’s Charter. CBDT will issue guidelines for

the Tax Department.(v) One important measure announced by the Finance Minister this year relates to the Disputed Income-tax Settlement Scheme. ‘The Direct Tax Vivad Se Vishwas Bill, 2020’ was introduced by her and was passed by

th March, 2020. This Scheme has been

introduced with a view to reduce litigation. It is stated

various appellate authorities. The assessees can avail

getting waiver of penalty, interest and fee.

amendments made in the Income-tax Act by the Finance Act, 2020.

2. RATES OF TAXES

the case of a domestic company, the rate of tax is the

company having total turnover or gross receipts of less

requirement was with reference to total turnover or gross

2.2 The rates for Surcharge on tax applicable in A.Y. 2020-

st April, 2020 is now taxable in the hands of the shareholder. Earlier, the company was required to pay Dividend Distribution Tax (DDT) and the shareholder was not liable to pay any tax.

will be liable to tax in the hands of the shareholder. In order to provide relief in the rate of Surcharge to Individual, HUF, AOP, etc. having total income exceeding Rs. 2 crores, it

Income-tax on dividend income included in the total income.

and Surcharge shall continue as in the earlier year.

3. REDUCTION IN TAX RATES FOR INDIVIDUALS AND HUFs

Chartered Accountants

20 BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

the company does not claim certain deductions and tax incentives. In respect of newly-formed manufacturing

st

incentives were not claimed.

has been inserted in the Income-tax Act with effect from

Individuals and HUFs if the assessee does not claim certain deductions and tax incentives. For claiming this concession in tax rates, the assessee will have to exercise the option in the prescribed manner. The reduced tax rates are as under:

Income (Rupees in lakhs) Existing rate Reduced rate (section

115BAC)1 2.50 L Nil Nil2 2.50 to 5.00 L 5% 5%3 5.00 to 7.50 L 20% 10%4 7.50 to 10.00 L 20% 15%5 10.00 to 12.50 L 30% 20%6 12.50 to 15.00 L 30% 25%7 Above 15.00 L 30% 30%

chargeable. It may be noted that there is no separate higher threshold for senior and very senior citizens in the above concessional tax rate scheme.

tax rates, the assessee will have to forgo the deductions

with special allowances granted to employees other than

th June, 2020.

Out of the above, some of the allowances as may be

cases, deduction for professional tax, etc., available to salaried employees, (viii) 24(b) – Interest on borrowing

depreciation, (x) 32AD – Investment in new plant and

Deposits in tea, coffee and rubber development account,

expenditure on Agricultural Extension Project, (xvi) 57(iia) – Standard deduction for Family Pension, (xvii) Chapter VIA – All deductions under Chapter VIA – excluding

dealing with deduction in respect of certain income of International Financial Services Centre.

(investment in PPF A/c, LIP payments or investments

forward loss from house property against income from other heads, (ixx) Section 32 – Depreciation u/s 32 [other

manner, (xx) No exemption or deduction for allowances or perquisites allowable under any other law can be claimed, (xxi) provisions of Alternate Minimum Tax and credit under

3.4 As stated above, the assessee will have to exercise the option in the prescribed manner where an Individual or HUF has no business income, this option can be

words, the option can be exercised every year in the prescribed manner.

3.5 If the Individual or HUF has income from business

once exercised shall apply to that year and all subsequent years. Such an assessee can withdraw the option at any time in a subsequent year and, thereafter, it will not be possible to exercise the option at any time so long as the said assessee has income from business or profession.

3.6 It may be noted that the above option for concession in tax rates will not be available to AOP, BOI, etc. The existing slab rates will continue to apply to them. Further,

21BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

Alternative Minimum Tax and credit for such tax will not

3.7 Considering the above conditions, it is possible that very few assessees will exercise this option for lower tax rates. If deductions for PPF contribution, LIP, etc., u/s

this concession in tax rates to Individuals and HUFs will not be attractive.

4. TAXATION OF DIVIDENDSst March, 2020, domestic companies declaring

/ distributing dividend to shareholders were required to

Fund while distributing income on its units at varying

that the shareholder receiving dividend from a domestic company or a unitholder receiving income from an M.F. will not be required to pay any tax on such dividend income and income received from an M.F. in respect of

an assessee, other than a domestic company and Public

plus applicable Surcharge and Cess if the total dividend

4.2 Now, after about two decades, the system of levying st

domestic companies / M.F.s are now made inoperative.

st April, 2020.

4.3 In view of the above, any dividend declared by a domestic company or income distributed by an M.F.,

st April, 2020 will be taxable in the hands of the shareholder / unitholder at the rate applicable to the assessee. In the case of a non-resident assessee it will

which will include limit on tax rate for dividend income and tax credit in home country as provided in the applicable tax treaty.

4.4 Section 57 has been amended to provide that

expenditure by way of interest paid on monies borrowed for investment in shares and units of M.F.s will be allowed to be deducted from Dividend Income or Income from

Dividend Income or Income from units of M.F.s. No other deduction will be allowed from such income.

domestic company whose gross total income includes dividend from any other (i) domestic company, (ii) foreign company, or (iii) a business trust. The deduction under this section will be allowed to the extent of dividend distributed by such company on or before the due date. For this purpose ‘Due Date’ means the date one month

company, Rs. 50 lakhs from a foreign company and Rs. st

st

th

income from units of M.F.s.

4.6 In order to provide some relief to Individuals, HUFs, AOP, BOI, etc., a concession in the rate of Surcharge has been provided in respect of dividend income. In case of such assessees, the rate of Surcharge on income

It is now provided that if the income of such assessee exceeds Rs. 2 crores, the rate of Surcharge shall not

Dividend Income included in the total income. From the wording of this concession given to Dividend Income, it appears that this concession will not apply to the income from units of M.F.s received by the assessee.

4.7 Since the income from dividend on shares is now

shareholder will be deducted at source. In the case of a non-resident shareholder, the TDS will be at the rate

distributed to a resident unitholder. In the case of a non-

22 BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

not required to be deducted at source from interest paid by a quoted company to its debenture-holders if the said debentures are held in demat form. This concession is

shares or units of M.F.s held in demat form. Therefore, the provisions for TDS will apply in respect of shares or units of M.F.s held in demat form.

5. TAX DEDUCTION AND COLLECTION AT SOURCE

Sections 191 and 192: Both these sections are

sweat equity shares (ESOP) allotted to any employee by the employer as a perquisite. The value of ESOP is the fair market value on the date on which the option is exercised as reduced by the actual payment made by the employee. When the shares are subsequently sold, any gain on such sale is taxable as capital gain. The employer has to deduct tax at source on such perquisite at the time

In order to ease the burden of startups, the amendments in these two sections provide that a company which

assessment year, or (ii) from the date of sale of such ESOP shares by the employee, or (iii) from the date on

ceases to be an employee of the company, whichever is earlier. For this purpose, the tax rates in force in the

allotted or transferred are to be considered. By this amendment, the liability of the employee to pay tax on such perquisite and deduction of tax on the same is deferred as stated above. Consequential amendments

5.2 Sections 194, 194K and 194LBA:

st April, 2020. These sections now provide as under:

resident shareholder by a company exceeds Rs. 5,000 in

at source. In the case of a non-resident shareholder, the

distributed by an M.F. to a resident unitholder and such

M.F. In the case of a non-resident unitholder, the rate of

in respect of income distributed by a Business Trust to a resident unitholder, being dividend received or receivable from a Special Purpose Vehicle, the tax shall be deducted

5.3 Section 196C:income by way of interest or dividends in respect of Bonds or GDRs purchased by a non-resident in foreign

st April, 2020. Under

the dividend paid to the non-resident.

5.4 Section 196D: This section deals with TDS from income in respect of securities held by an FII. Amendment

st April, 2020 now provides that dividend paid to an FII or FPI will be subject to TDS at the

5.5 Section 194A: This section deals with TDS from interest income. This section is amended effective from

st April, 2020. At present, a co-operative society is not required to deduct tax at source on interest payment in the following cases:(i) Interest payment by a co-operative society (other than a Co-operative Bank) to its members.(ii) Interest payment by a co-operative society to any other co-operative society.(iii) Interest payment on deposits with a Primary Agricultural Credit Society or Primary Credit Society or a Co-operative Land Mortgage Bank.(iv) Interest payment on deposits (other than time deposits) with a co-operative society (other than societies mentioned in iii above) engaged in the business of banking.

st April, 2020, the above exemptions have been

deduct tax at source in all the above cases at the rates in

23BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

(a) The total sales, gross receipts or turnover of the co-operative society exceeds Rs. 50 crores during the

(b) The amount of interest, or the aggregate of the

year, is more than Rs. 50,000 in case the payee is a senior citizen (aged 60 years or more) or more than Rs. 40,000 in other cases.

5.6 Section 194C: This section is amended effective from st

section to include manufacturing or supplying a product

by using material purchased from such customer. Now, this term ‘Work’ will also include material purchased from the associate of such customer. For this purpose, the

5.7 Section 194J: This section is amended effective from st April, 2020. The rate of TDS has been reduced to

services. The rate of TDS from professional fees will

Section 194LC: This section is amended effective st April, 2020. The eligibility of borrowing under

the loan agreement or by issue of long-term bonds for concessional rate of TDS under this section has now been extended from 30th June, 2020 to 30th June, 2023. Further,

interest on monies borrowed by an Indian company from a source outside India by issue of long-term Bonds or

st April, 2020 and 30th June, 2023, which are listed on a recognised stock exchange in any International Financial Services Centre.

in other cases).

Section 194LD: This section is amended effective st April, 2020. This amendment is made to cover

st th June, 2023

Rupee-Denominated Bonds of an Indian company or

st April, 2020 and 30th June, 2023 will also be covered under the provisions of this section. The rate for

Section 194N:st

respect of cash withdrawn by any account holder from

accounts in different branches of the bank, total cash withdrawals in all these accounts will be considered for this purpose. This TDS provision applied to all persons,

engaged in business or profession, as also to all persons maintaining bank accounts for personal purposes. Under this section there will be no TDS on cash withdrawn up

Now, the above section has been replaced by a new st July, 2020. This new

section provides as under:

st July, 2020, if the account holder in the

the three assessment years relevant to the three previous

(ii) The Central Government has been authorised to notify, in consultation with RBI, that in the case of any account holder the above provisions may not apply or tax may be

(iii) This section does not apply to cash withdrawals by

banking correspondent, white label ATM operators and

Government in consultation with RBI if such person

reduced rates or at Nil rate.(iv) This provision is made in order to discourage cash withdrawals from banks and promote digital economy.

assessee. If the amount of this TDS is not treated as

24 BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

income of the assessee, credit for tax deducted at source

read with Rule 37BA. If such credit is not given, this will be an additional tax burden on the assessee.

Section 194-O and 206AA:st April, 2020. Existing

section 206AA has been amended from the same date.

to E-commerce operators. The effect of this provision is as under:

(a) ‘E-commerce operator’ is a person who owns, operates or manages digital or electronic facility or platform for electronic commerce, and (b) ‘E-commerce participant’ is a person resident in India selling goods or providing services or both, including digital products, through digital or electronic facility or platform for electronic commerce. For this purpose the services will include fees for professional services and fees for technical services.(ii) An E-commerce operator facilitating sale of goods or provision of services of an E-commerce participant, through its digital electronic facility or platform, is now

the payment of gross amount of sales or services or both to the E-commerce participant. Such TDS is to be deducted from the amount paid by the purchaser of goods or recipient of services directly to the E-commerce participant / E-commerce operator.(iii) No tax is required to be deducted if the payment is made to an E-commerce participant who is an Individual

than Rs. 5 lakhs and the E-commerce participant has furnished PAN or Aadhaar Card Number.(iv) Further, in the case of an E-commerce operator who is required to deduct tax at source as stated in (ii) above or in a case stated in (iii) above, there will be no obligation to deduct tax under any provisions of Chapter XVII-B in respect of the above transactions. However, this exemption will not apply to any amount received by an E-commerce operator for hosting advertisements or providing any other services which are not in connection with sale of goods or services.(v) If the E-commerce participant does not furnish PAN or Aadhaar Card Number, the rate for TDS u/s 206AA will

section 206AA.(vi) It is also provided that CBDT, with the approval of the Central Government, may issue guidelines for the

Section 206C: This section dealing with collection of st

October, 2020. Hitherto, this provision for TCS applied in

seller is required to collect tax from the buyer of certain

st October, 2020 extends the net of TCS u/s

(i) An authorised dealer, who is authorised by RBI to deal in foreign exchange or foreign security, receiving Rs.

remittance out of India under the Liberalised Remittance

the person remitting such amount. Thus, LRS remittance

this TCS. If the remitter does not provide PAN or Aadhaar

(ii) In the above case, if the remittance in excess of Rs. 7 lakhs is by a person who is remitting the foreign exchange

If the remitter does not furnish PAN or Aadhaar Card

(iii) The seller of an overseas tour programme package, who receives any amount from a buyer of such package,

noted that the TCS provision will apply in this case even if the amount is less than Rs. 7 lakhs. If the buyer does not provide PAN or Aadhaar Card Number, the rate for TCS

(iv) It may be noted that the above provisions for TCS do not apply in the following cases:

(a) An amount in respect of which the sum has been collected by the seller.(b) If the buyer is liable to deduct tax at source under the provisions of the Act. This will mean that for remittance for professional fees, commission, fees for technical services, etc. from which tax is to be deducted at source, this section will not apply.(c) If the remitter is the Central Government, State Government, an Embassy, High Commission, a Legation, a Commission, a Consulate, the Trade Representation of a Foreign State, a Local Authority or any person in respect of whom the Central Government has issued a

st October, 2020 provides that a seller of goods is liable to

from the buyer of goods, other than goods covered by

25BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

apply only in respect of the consideration in excess of Rs.

If the buyer is liable to deduct tax at source from the seller on the goods purchased and made such deduction, this provision for TCS will not apply.

not apply in the following cases:

(a) If the buyer is the Central Government, State Government, an Embassy, a High Commission, Legation, Commission, Consulate, the Trade Representation of a Foreign State, a Local Authority, a person importing goods into India or any other person as the Central Government may notify.(b) If the seller is a person whose sales, turnover or gross

(vii) The CBDT, with the approval of the Central Government, may issue guidelines for removing any

provisions.

Obligation to Deduct Tax at Source: Hitherto, the obligation to comply with the provisions of sections

Individuals or HUFs whose total sales or gross receipts or turnover from business or profession exceeded the

st April, 2020, to provide that the above TDS provisions will apply to an individual or HUF whose total sales or gross receipts or turnover

case of business or Rs. 50 lakhs in the case of profession. Thus, every Individual or HUF carrying on business will have to comply with the above TDS provisions even if he is not liable to get his accounts audited u/s 44AB.

General:(i) From the above amendments it is evident that the net for TDS and TCS has now been widened and even transactions which do not result in income are now covered under these provisions. Individuals and HUFs carrying on business and not covered by Tax Audit u/s 44AB will now be covered by the TDS and TCS provision. In particular, persons remitting foreign exchange exceeding Rs. 7 lakhs under LRS of RBI will have to pay tax u/s 206C. This tax

will be considered as payment of tax by the remitter u/s 206C(4) and he can claim credit for such tax u/s 206C(4)

(ii) It may be noted that the Government has issued a th May, 2020 giving certain relief during

th May, 2020 st

of TDS / TCS from payments or receipts from residents. This concession is not in respect of TDS from salaries or TDS from non-residents and TDS / TCS under sections 260AA or 206CC.

6. EXEMPTIONS AND DEDUCTIONS This is a new clause providing for

exemption of income from dividend, interest or long-term capital gain arising from investment made in India by a

st st March, 2024. The investment may be in the form of a debt,

means a wholly-owned subsidiary of Abu Dhabi Investment Authority which complies with the various conditions of the Explanation given in the section. For claiming the above

for at least three years. Further, the investment should be in (a) a Business Trust, (b) an Infrastructure Company as

I or Category II Alternative Investment Fund regulated

companies as referred to in (a), (b) or (c) above.

If exemption under this section is granted in any year, the same shall be withdrawn in any subsequent year when

section in a subsequent year. It is also provided in the

implementation of this section, CBDT, with the approval of the Central Government, may issue guidelines for

6.2 st April, 2020. It provides for exemption in respect of any income of Indian Strategic Petroleum Reserves Ltd., as a result of arrangement for replenishment of crude oil stored in its storage facility in pursuance of directions of the Central Government.

6.3 This section was added by the

26 BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

an Individual from a Financial Institution for acquiring a residential house. One of the conditions in the section is that the loan should be sanctioned during the period

st st March, 2020. This period is now st

6.4 This section deals with certain

Till now, this deduction was allowed even if amounts

st June, 2020 and the above

6.5 This section deals with deduction in

be claimed for three consecutive assessment years out of seven years from the year of incorporation. By amendment of this section, the outer limit of seven years has been increased to ten years.

is provided that the total turnover of the business of the startup claiming deduction under this section should not exceed Rs. 25 crores. This limit is now increased to Rs.

6.6 This section deals with deduction

present, for claiming deduction under this section one of the conditions is that the housing project should be approved by the Competent Authority during the period

st st March, 2020. This period is st

6.7 Filing Tax Audit Report:

Audit Report u/s 44AB along with the return of income.

st April,

7. CHARITABLE TRUSTSAt present, a University, Educational Institution, Hospital or other Medical Institution claiming exemption u/s

from the designated authority (Principal Commissioner or a Commissioner of Income-tax). The procedure for this is

is operative until cancelled by the designated authority. For other Charitable Trusts the procedure for registration

continues until it is cancelled by the designated authority. The Charitable Trusts and other Institutions are entitled

This approval is valid until cancelled by the Designated

donor to the Charitable Trust or other Institutions can claim deduction in the computation of his income for the

of Trusts. These provisions are discussed below.

New procedure for registration:st October,

amended and a similar procedure, as stated in section

Trusts and other Institutions registered under sections

Therefore, all Trusts / Institutions claiming exemption

(ii) Existing Charitable Trusts, Educational Institutions, Hospitals, etc., will have to apply for fresh registration u/s

st December, 2020. The designated authority will grant

from the end of the month in which the application is made. Six months before the expiry of the above period of

to the designated authority for renewal of registration

has to be passed by the designated authority within six months from the end of the month when the application for renewal is made.

(iii) For new Charitable Trusts, Educational Institutions,

27BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

Hospitals, etc., the following procedure is to be followed:(a) The application for registration in the prescribed form should be made to the designated authority at least one month prior to the commencement of the previous year relevant to the assessment year for which the registration is sought.(b) In such a case, the designated authority will grant provisional registration for a period of three assessment years. The order for provisional registration is to be passed by the designated authority within one month from the last date of the month in which the application for registration is made.(c) Where such provisional registration is granted for three years, the Trust / Institutions will have to apply for renewal of registration at least six months prior to expiry of the period of the provisional registration or within six months of commencement of its activities, whichever is earlier. In this case, the designated authority has to pass the order within six months from the end of the month in which the application is made. In such a case, renewal of

inoperative from the date on which the Trust is st October, 2020,

whichever is later. In such a case the Trust can apply for

months prior to the commencement of the assessment year for which the registration is sought. The designated authority will have to pass the order within six months from the end of the month in which the application is made.

conditions of registration, application should be made to the designated authority within 30 days from the date of

(vi) Where the application for registration, renewal of registration is made as stated above, the designated authority has power to call for such documents or information from the Trust / Institutions or make such inquiry in order to satisfy itself about (a) the genuineness of the Trust / Institutions, and (b) the compliance with requirements of any other applicable law for achieving the objects of the Trust or Institution. After satisfying himself,

years or reject the application for registration after giving a hearing to the trustees. If the application is rejected,

Tribunal within 60 days. The designated authority also has power to cancel the registration of any Trust or Institutions

st October, 2020 will be considered as applications made under the new

7.2. Corpus donation:(i) Hitherto, a corpus donation given by an Educational

to a similar institution claiming exemption under that section, was not considered as application of income

st April, 2020, a corpus donation given by such an Institution to a Charitable Trust registered u/s

a corpus donation given by a Charitable Trust to another

st

April, 2020, to provide that a corpus donation given by a

and to Educational Institutions or a Hospital registered u/s

st April, 2020, to provide that any corpus donation received by an Educational Institution or a Hospital claiming exemption under that section will not be considered as its income. At

this provision.

7.3. A proviso st October,

it is cancelled. Now, this provision is deleted and a new

as under:

it will have to make a fresh application in the prescribed

st December, 2020. In such a

has to pass the order within three months from the last date of the month in which the application is made.

have to be made at least six months before the date of

28 BOMBAY CHARTERED ACCOUNTANT JOURNAL SEPTEMBER 2020

BCAJ

to pass the order within six months from the last date of the month in which the application is made.

the commencement of the previous year relevant to the assessment year for which the approval is sought. In such a case, the designated authority will give provisional approval for three years. The designated authority has to pass the order within one month from the last date of the month in which the application is made.(iv) In a case where provisional approval is given, application for renewal will have to be made at least six months prior to the expiry of the period of provisional approval, or within six months of the commencement of the activities by the Trust / Institution, whichever is earlier. In this case the designated authority has to pass the order within six months from the last date of the month in which the application is made.

In cases of renewal of approval as stated in (ii) and (iv) above, the designated authority shall call for such documents or information or make such inquiries as he thinks necessary in order to satisfy himself that the activities of the Trust / Institution are genuine and that

can reject the application after giving a hearing to the

7.4. Clauses (viii) and (ix) st October, 2020 to

tax Authority particulars of all donors in the prescribed form within the prescribed time. The Trust / Institution has

donor about the donations received by it. The donor will