Embed Size (px)

Citation preview

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Service Properties Trust

Q3 2019 Investor Presentation

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

This presentation contains statements that constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of

1995 and other securities laws. Also, whenever we use words such as “believe”, “expect”, “anticipate”, “intend”, “plan”, “estimate”, “will”, “may” and

negatives or derivatives of these or similar expressions, we are making forward-looking statements. These forward-looking statements are based upon

our present intent, beliefs or expectations, but forward-looking statements are not guaranteed to occur and may not occur. Forward-looking statements in

this presentation relate to various aspects of our business, including the performance of our operator or tenants and their ability to pay the contractual

amounts of returns or rents due to us, our sales and acquisitions of properties, our ability to compete for acquisitions effectively, our policies and plans

regarding investments, financings and dispositions, our ability to pay distributions to our shareholders and to sustain the amount of such distributions, our

ability to raise debt or equity capital, our ability to appropriately balance our use of debt and equity capital, our intent to make improvements to certain of

our properties and the success of our renovations, our ability to engage and retain qualified managers and tenants for our hotels and net lease properties

on satisfactory terms, the future availability of borrowings under our revolving credit facility, our ability to pay interest on and principal of our debt, our

credit ratings, our expectation that we benefit from our relationships with the RMR Group, Inc., or RMR, our qualification for taxation as a REIT, changes

in federal or state tax laws, and other matters.

Our actual results may differ materially from those contained in or implied by our forward-looking statements as a result of various factors, such as the

impact of conditions in the economy and the capital markets on us and our managers and tenants, competition within the real estate, hotel,

transportation, travel center and other industries in which our tenants operate, particularly in those markets in which our properties are located,

compliance with, and changes to applicable laws, regulations, rules and similar matters, limitations imposed on our business and our ability to satisfy

complex rules in order for us to maintain our qualification for taxation as a REIT for U.S. federal income tax purposes, acts of terrorism, outbreaks of so

called pandemics or other manmade or natural disasters beyond our control and actual and potential conflicts of interest with our related parties. Our

annual report on form 10-K for the year ended December 31, 2018 and our other filings with the Securities and Exchange Commission (SEC) identify

other important factors that could cause differences from our forward-looking statements. Our filings with the SEC are available on the SEC’s website at

www.SEC.gov. You should not place undue reliance upon our forward-looking statements. Except as required by law, we do not intend to update or

change any forward-looking statements as a result of new information, future events or otherwise.

Non-GAAP Financial Measures

This presentation contains Non-GAAP financial measures including, among others, “EBITDA” and “Adjusted EBITDA” in the exhibits section.

Reconciliation for those metrics to the most directly comparable financial measure calculated in accordance with U.S generally accepted accounting

principles (GAAP) are included herein.

Unless otherwise noted, all data presented is as of September 30, 2019.

Warning Concerning Forward -Looking Statements

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

SVC at a Glance: Port fol io Overview.

3

(1) As of and for the twelve months ended September 30, 2019.

(2) Please see page 23 for definitions of FFO and Normalized FFO available for common shareholders, a description of why SVC believes the presentation of these measures provides useful information to investors regarding its financial condition and

results of operations and a description of how it uses these measures.

Total Properties 1,274

• Hotels 328

• Net Lease Assets 946

Investment Value $12.6bn

Dividend Yield 8.4%

Normalized FFO

Payout Ratio (2) 56.8%

Key Metrics (1) Recent Developments

• Closed on $2.4bn net lease portfolio

acquisition.

• Raised $1.7bn of unsecured senior notes.

• Targeted asset sales of $800mn underway,

with 128 net lease properties sold or under

contract for proceeds of approximately

$500mn.

• Targeting $300mn of hotel sales, SVC is in the

process of selling or rebranding 22 hotels

managed by Wyndham and 30 Marriott hotels.

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Reasons to Own Service Propert ies Trust.

✓ CONSISTENT METHOD FOR CREATING VALUE AND STRATEGY FOR ACHIEVING

RESULTS.

✓ $12.6 BILLION INVESTED IN A DIVERSIFIED PORTFOLIO THAT PROVIDES MANY

AVENUES FOR GROWTH.

✓ UNIQUE STRUCTURE OF HOTEL AGREEMENTS PROVIDES STABLE CASH FLOWS

DESIGNED TO WITHSTAND RENOVATION DISRUPTION AND ECONOMIC DOWNTURNS.

✓ NECESSITY-BASED RETAIL ASSETS PROVIDE RELIABLE INCOME WITH LOW CAPEX

REQUIREMENTS UNDER TRIPLE NET LEASE STRUCTURE.

✓ INVESTMENT GRADE BALANCE SHEET.

✓ WELL COVERED DIVIDEND WITH PROVEN TRACK RECORD OF INCREASING RETURNS

TO SHAREHOLDERS.

✓ STRONG MANAGEMENT PLATFORM AND AFFILIATE ADVANTAGES.

4

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

L a r g e ,

D i v e r s e

Po r t f o l i o

H o t e l m a n a g e m e n t

a g r e e m e n t s w i t h

a l i g n m e n t o f

i n t e r e s t s

T r i p l e n e t l e a s e

s t r u c t u r e p r o v i d e s

s t e a d y i n c o m e

s t re a m

I n v e s t m e n t g r a d e

b a l a n c e s h e e t

B i l l i o n d o l l a r

r e v o l v i n g c r e d i t

f a c i l i t y

S t r o n g a c c e s s t o

c a p i t a l m a r k e t s

ST R O N G

M AN AG EM E N T

PL AT F O R M

AN D AF F I L I AT E

AD V A N T A G ESSEC U R I T Y O F C AS H F L O W

O PPO R T U N I T I E S

F O R

G R O W T H

C AP A C I T Y T O

SU PPO R T

G R O W T H

T h e R M R G r o u p

…

T A

…

So n e s t a

Strategy for Achieving Results.

Ac q u i s i t i o n s

As s e t R e c yc l i n g

R e i n v e s t i n g t h r o u g h

r e n o v a t i o n s & c a p i t a l

i m p r o v e m e n t s

As s e t m a n a g e m e n t t o d r i v e o p e ra t i o n a l

i m p r o v e m e n t

5

D o w n s i d e

C a s h f l o w

Pr o t e c t i o n

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 20196

Portfol io Highl ights. (1)

($ in millions) Hotels

Net Lease

Assets Total

Properties 328 946 1,274

Keys / Square Feet 51,086 17.6 msf51,086/

17.6msf

States 40 45 48

Investments $6.9bn $5.8bn $12.6bn

Annual Minimum

Return/Rent$602mn $419mn $1,020bn

Annual Minimum

Returns and Rents

Coverage Ratio (3)

0.87x 2.27x 1.44x

Portfolio by Property Type (2)

Tenants by Industry (2)

(1) As of and for the twelve months ended September 30, 2019.

(2) Based on annualized minimum base returns and rents.

(3) See page 23 for our definition of coverage.

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

S V C ’s a s s e t s a r e l o c a t e d i n 4 8 s t a t e s , Wa s h i n g t o n D C , P u e r t o R i c o ,

a n d C a n a d a .

• SVC has invested $12.6 billion in its national real estate portfolio.

• SVC’s investments are located in various markets near demand generators.

• We believe geographic diversity creates mitigates market risk.

Data as of September 30, 2019.

Portfol io Highl ights: Geographical ly Diverse.

7

Annual Minimum Returns and Rents

Total

Property

Count

Hotel

Count

Net

Lease

Count

Total

($000s) % of Total

Hotel

($000s)

Hotel %

of Total

Net Lease

($000s)

Net Lease

% of Total

1 California 58 36 22 $ 112,984 11.1% $ 89,754 8.8% 23,230$ 2.3%

2 Texas 105 36 69 85,462 8.4% 50,863 5.0% 34,599 3.4%

3 Illinois 87 16 71 65,516 6.4% 34,741 3.4% 30,775 3.0%

4 Georgia 104 23 81 64,554 6.3% 42,352 4.2% 22,202 2.2%

5 Ohio 60 11 49 41,171 4.0% 13,474 1.3% 27,697 2.7%

6 Florida 68 14 54 41,041 4.0% 24,816 2.4% 16,224 1.6%

7 Arizona 44 15 29 37,443 3.7% 19,856 1.9% 17,587 1.7%

8 Massachusetts 15 14 1 33,732 3.3% 28,512 2.8% 5,221 0.5%

9 Pennsylvania 42 10 32 33,239 3.3% 17,799 1.7% 15,441 1.5%

10 New Jersey 20 15 5 32,752 3.2% 26,261 2.6% 6,492 0.6%

Top 10 603 190 413 $ 547,896 53.7% $ 348,428 34.1% 199,468$ 19.5%

Other 671 138 533 $ 472,580 46.3% $ 253,413 24.9% $ 219,167 21.5%

Total 1,274 328 946 1,020,476$ 100.0% 601,841$ 59.0% 418,635$ 41.0%

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Hotel Port fol io: Operated under a Diverse Group of Nat ional ly Recognized Brands.

8

• SVC’s 328 hotels are operated under

eight long-term agreements directly

with brand owners.

• 21 different hotel brands,

predominantly upper upscale and

upscale.

• Primarily extended stay and select

service hotels typically in near-urban

locations.

• Diversified hotel portfolio located in

40 states, Washington, D.C., Puerto

Rico and Canada.

• Majority of minimum hotel returns and

rents secured by security deposits or

corporate guarantees.

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Airport15% Interstate

1%

Resort4%

Small Metro1%

Suburban68%

Urban11%

Marriott, $1,843

InterContinental, $2,267

Sonesta, $1,763

Wyndham, $399

$299

Hotel Chain Scale

(by # of units) (1)

Luxury3%

Midscale23%

Upper Midscale6%

Upper Upscale

4%

Upscale64%Extended Stay

56%

Full Service15%

Select Service29%

Hotel Service Level

(by # of units) (1)

(1) Data as of September 30, 2019.

(2) Represents historical cost of properties plus capital improvements funded by SVC less impairment writedowns, if any, and excludes capital improvements made from FF&E reserves funded from hotel operations which do not result in

increases in minimum returns or rents.

Hotel Location Segment

(by # of units) (1)

Hotel Managers

(by investment $ in millions) (1),(2)

• SVC’s targets are select service hotels

in near-urban locat ions, as wel l as ful l

service hotels in urban markets to

expand our brand owner relat ionships.

Radisson

Hyatt,

$302

Hotel Port fol io: Our Strategy Provides Flexibi l i ty in Regard to Asset Mix.

9

Chain Scale

Acquisitions

since 2015 % Mix

Luxury 1 2%

Upper Upscale 7 17%

Upscale 32 78%

Upper Midscale 1 2%

Midscale 0 0%

Total 41 100%

Service Level

Acquisitions

since 2015 % Mix

Full Service 15 37%

Extended Stay 26 63%

Select Service 0 0%

Total 41 100%

Location Segment

Acquisitions

since 2015 % Mix

Suburban 27 66%

Urban 12 29%

Airport 1 2%

Resort 1 2%

Interstate 0 0%

Small Metro 0 0%

Total 41 100%

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

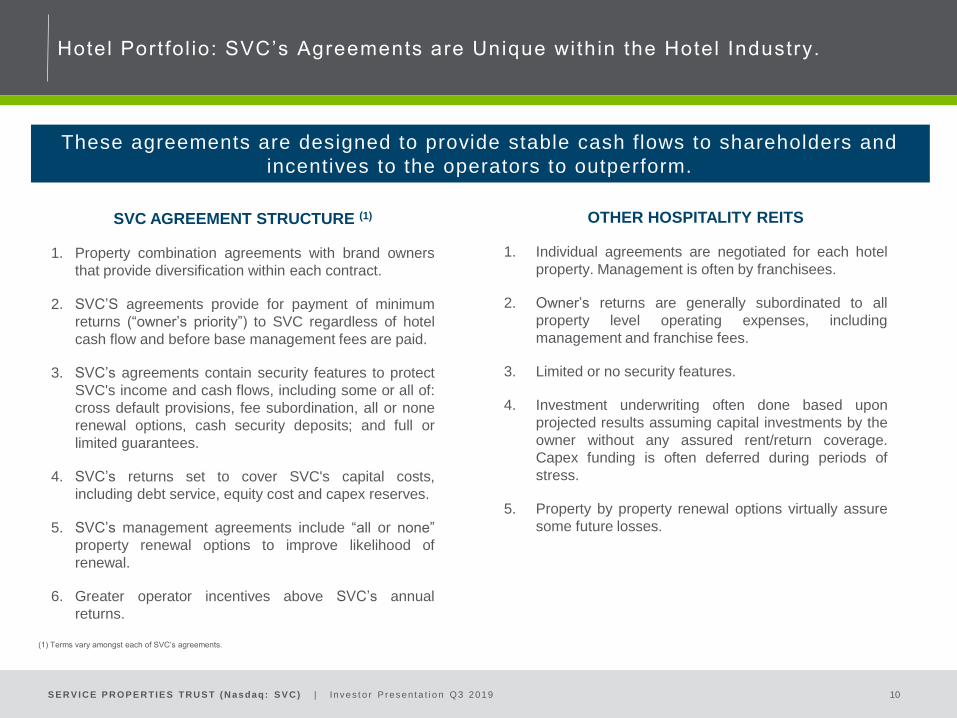

Hotel Port fol io: SVC’s Agreements are Unique within the Hotel Industry.

10

SVC AGREEMENT STRUCTURE (1)

1. Property combination agreements with brand owners

that provide diversification within each contract.

2. SVC’S agreements provide for payment of minimum

returns (“owner’s priority”) to SVC regardless of hotel

cash flow and before base management fees are paid.

3. SVC’s agreements contain security features to protect

SVC's income and cash flows, including some or all of:

cross default provisions, fee subordination, all or none

renewal options, cash security deposits; and full or

limited guarantees.

4. SVC’s returns set to cover SVC's capital costs,

including debt service, equity cost and capex reserves.

5. SVC’s management agreements include “all or none”

property renewal options to improve likelihood of

renewal.

6. Greater operator incentives above SVC’s annual

returns.

OTHER HOSPITALITY REITS

1. Individual agreements are negotiated for each hotel

property. Management is often by franchisees.

2. Owner’s returns are generally subordinated to all

property level operating expenses, including

management and franchise fees.

3. Limited or no security features.

4. Investment underwriting often done based upon

projected results assuming capital investments by the

owner without any assured rent/return coverage.

Capex funding is often deferred during periods of

stress.

5. Property by property renewal options virtually assure

some future losses.

These agreements are designed to provide stable cash flows to shareholders and

incentives to the operators to outperform.

(1) Terms vary amongst each of SVC’s agreements.

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Net Lease Port fol io: High -Qual i ty Service & Necessity Based Assets.

11

Net Lease Portfolio Statistics (1)

946 $419mm

Properties Annual Contractual Rent

17.6mm 11.3 Years

Rentable Square Feet Weighted Average Lease Term

98% 2.27x(2)

Occupancy W.A. FCCR

Diverse Geographical Footprint (3)

(1) Data as of and for the twelve months ended September 30, 2019.

(2) See page 23 for our definition of coverage.

(3) By annual minimum rent.

% of Rent (1)<1% 8.5%

6%

9%

5%

7% 5% 7%

<1%

<1%

<1%

<1%

<1%

<1%

<1%

<1%

<1%

<1%

<1%

<1%

<1%

1%

1%

2%

2%

1%

1%1%

1%1%

4%

4%

4%

3%

3%

3%

3%

3%

2%

2%

2%

2%

2%

2%

2%

2%2%

23 Industries | 163 Brands

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Net Lease Port fol io: Rel iable Income Stream and Low Capex Requirements.

12

Well-Laddered Lease Expirations (2)

(1) As of September 30, 2019.

(2) By annual minimum rent.

92%of Leases Have

Contractual Increases

or Percentage Rent

Lease Structures (1)

0% 2% 2% 3% 1% 3% 3% 4% 6%

76%

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028+

60%

19%

14%

8%

Percentage Rent

CPI

Fixed/Scheduled

Flat

$419mm

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Net Lease Port fol io: Tenants & Industr ies that Benef i t f rom Strong Demand Drivers.

13

(1) By annual minimum rent.

(2) Leases subject to full or partial corporate guarantees.

(3) As of and for the twelve months ended September 30, 2019. See page 23 for our definition of coverage.

Tenants by Brand (1)Tenants by Industry (1)

Brand

% of

Annualized

Cash Rent Coverage (3)

Travel Centers of America (2) 40.1% 1.95x

Petro Stopping Centers (2) 18.7% 1.62x

AMC Theaters (2) 18.7% 1.36x

The Great Escape 2.6% 4.12x

Crème de la Crème (2) 1.7% 1.84x

Goodrich Quality Theaters 1.4% 1.48x

Life Time Fitness (2) 1.3% 3.56x

Casual Male 1.3% 1.24x

Buehler's Fresh Foods 1.2% 2.22x

CarMax 1.2% 2.51x

Other 11.8% 3.15x

100% 2.27x

Travel Centers, 59%

Restaurants - Quick Service, 6%

Movie Theaters, 6%

Restaurants - Casual Dining, 5%

Health & Fitness, 3%

Miscellaneous Retail, 2%

Medical/Other Office, 2%

Auto Parts & Service, 2%

Grocery, 2%

Automotive Dealers, 2% Other, 11%

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Balance Sheet Overview as of September 30, 2019.

14

(1) Net debt means total debt less cash and cash equivalents as of the date reported.

(2) See page 23 for the calculation of EBITDA, EBITDAre and Adjusted EBITDAre, and a reconciliation of net income (loss) determined in accordance with GAAP to these amounts.

(3) We completed the SMTA transaction on September 20, 2019. For purpose of calculating coverage ratios for the three months ended September 30, 2019, we included our pro forma estimates of the annualized Adjusted EBITDAre we expect to be

generated from the SMTA portfolio.

Well Laddered Debt Maturities

Book Capitalization

Leverage/Coverage Ratios

Net Debt (1) / Total Gross Assets 51.8%

Net Debt (1) / Gross Book Value of Real Estate Assets 56.0%

Adjusted EBITDAre (2) (3) / Interest Expense 4.0x

Net Debt(1) / Annualized Adjusted EBITDAre (2) (3) 6.6x

Investment Grade Balance Sheet

Unsecured Floating Rate Debt 13%

Unsecured Fixed Rate Debt 58%

Shareholder’s Equity 29%

• No secured debt.

• Unsecured senior notes: $5.4 billion.

• Unsecured term loan: $400 million, July 2023 maturity.

• Revolving credit facility:

• $1 billion ($790 million outstanding).

• July 2022 maturity plus two six-month extensions.

• No derivatives, off-balance sheet liabilities, or material

adverse change clauses or ratings triggers.

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

13%

58%

29%

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

(1) 2015 period excludes a $0.20 per share non-cash distribution of The RMR Group, or, RMR common stock to SVC shareholders.

(2) Based on actual 2019 dividend and LTM normalized FFO for the period ended September 30, 2019.

Proven track record of returns to shareholders even during market downturns.

Our Cash Flow Payout Strategy Al lows for a Secure, Wel l -Covered Dividend.

15

$1.80 $1.80 $1.82

$1.89

$1.95

$1.99

$2.03

$2.07

$2.11

$2.15

20%

30%

40%

50%

60%

70%

80%

90%

100%

$1.20

$1.30

$1.40

$1.50

$1.60

$1.70

$1.80

$1.90

$2.00

$2.10

$2.20

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Dividends Paid Per Share Normalized FFO Dividend Payout Ratio

(1) (2)

Dividend Paid Per Share and Normalized FFO Dividend Payout Ratio

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

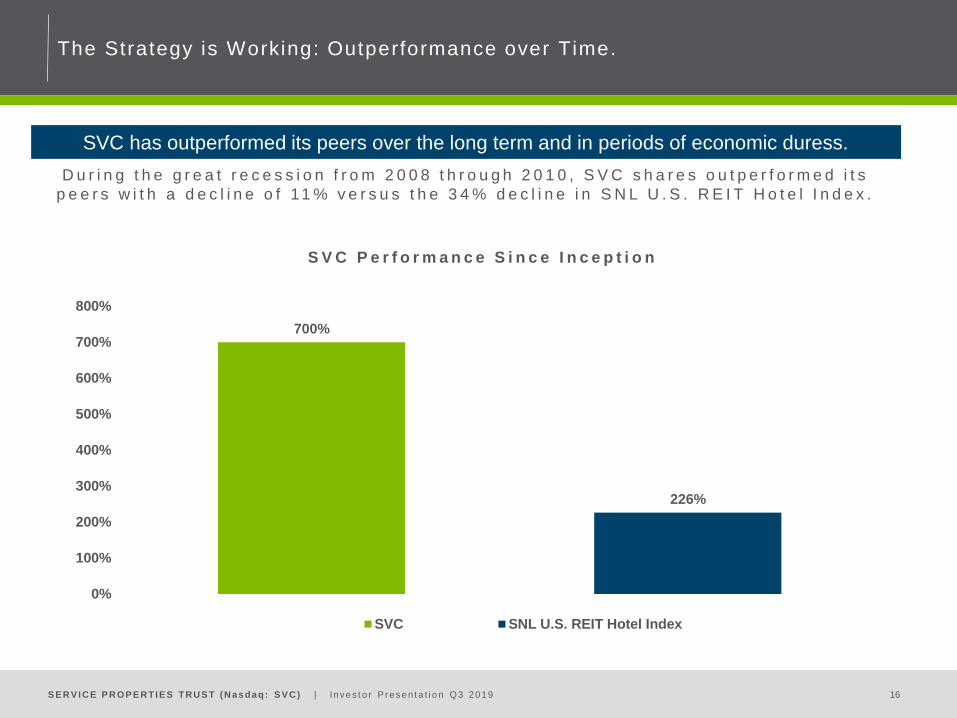

The Strategy is Working: Outperformance over Time.

16

700%

226%

0%

100%

200%

300%

400%

500%

600%

700%

800%

SVC SNL U.S. REIT Hotel Index

D u r i n g t h e g r e a t r e c e s s i o n f r o m 2 0 0 8 t h r o u g h 2 0 1 0 , S V C s h a r e s o u t p e r f o r m e d i t s

p e e r s w i t h a d e c l i n e o f 11 % v e r s u s t h e 3 4 % d e c l i n e i n S N L U . S . R E I T H o t e l I n d e x .

SVC has outperformed its peers over the long term and in periods of economic duress.

S V C P e r f o r m a n c e S i n c e I n c e p t i o n

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Financial

Services:

Real Estate

Services:

Business

Services:

AccountingAcquisitions/

DispositionsAdministration

Capital MarketsAsset

ManagementHuman Resources

Compliance/ AuditConstruction/

Development

Information

Technology (IT)

Finance/ Planning Engineering Investor Relations

Treasury Leasing Marketing

TaxProperty

Management

Legal/

Risk Management

RMR’s Operations Include:

$32.8 Billion in AUM

Approximately 600 CRE

Professionals

More than 30 Offices

Throughout the U.S.Over

50,000 Employees

Over 2,200

Properties

$12 Billion in

Annual Revenues

Combined RMR

Managed Companies:

Office Industrial Medical OfficeSenior Living

Hotel /Net Lease

Travel Centers

Senior Living OfficeHotels Securities REIT

CRE Mortgages

T h e R M R G r o u p

E q u i t y R E I T S O p e r a t i n g C o m p a n i e s O t h e r U n i t s

Strong Management Platform and Aff i l iate Advantages.

17

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

RMR base management fee tied to SVC share

price performance.

• Consists of an annual fee based on generally 50 bps

multiplied by the lower of:

(1) SVC’s historical cost of real estate, or

(2) SVC’s total market capitalization.

• There is no incentive for RMR to complete any

transaction that could reduce share price.

RMR incentive fees contingent on total

shareholder return(1) outperformance.

• Equal to 12% of value generated by SVC in excess of

the benchmark index total returns (SNL US Hotel REIT

Index) per share over a three year period, subject to a

cap (1.5% of equity market cap).

• Absolute dollar outperformance must be positive to

receive an incentive fee: it can’t be negative but better

than the index.

• Shareholders keep 100% of benchmark returns and

88% of returns in excess of the benchmark.

Alignment of Interests

If total market cap exceeds historical cost of real estate,

base fee is paid on assets.

If total market cap is less than historical cost of real

estate, base fee fluctuates with share price.

Incentive fee structure keeps RMR focused on increasing

total shareholder return.

Members of RMR senior management are substantial

holders of SVC stock, some subject to long term lock up

agreements.

SVC shareholders have visibility into publicly traded

RMR.

SVC benefits from RMR’s national footprint and

economies of scale of $32.8 billion platform.

(1) To determine final share price in SVC’s Total Return calculation, the business management agreement requires that the highest ten day share price average within the last 30 trading

days of the measurement period be used. In the past, this and other less significant factors have resulted in differences between SNL’s calculation of SVC’s total return percentage and

the total return percentage computed under the agreement.

The RMR Group LLC and Shareholder Al ignment.

18

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Long Island

Newton (Boston)

Los

Angeles

San Diego

Baltimore / Annapolis

Honolulu(2)

Washington D.C.(3)

Albuquerque

Austin(2)

Minneapolis

Chicago(2)

Atlanta(2)

Indianapolis

ColumbiaPhoenix

Denver

Dallas

Kansas

City(2)

PhiladelphiaSacramento

Houston

Richmond(2)

Seattle

San Jose

Ontario,

Canada

Puerto Rico

Norfolk

SVC Benefits from The RMR Group’s Integration and Management Capabilities.

• The RMR Group currently manages over $32.8 billion in assets.

• Operating platform includes 30 offices throughout the U.S. with over 600 commercial real estate professionals.

• Provides national, regional and local market leasing, asset management and property management expertise.

• Net lease portfolio and ongoing management is expected to be easily integrated.

The RMR Group has a Nat ional, Vert ical ly - Integrated Operat ing Platform.

19

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Appendix

20

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Calculat ion of EBITDA, EBITDAre and Adjusted EBITDAre. (1)

( In thousands )

21

(1)

(2)

(3)

(4)

(5)

We recorded a $159,535 gain on sale of real estate in the three months ended March 31, 2019, in connection with the sales of 20 travel centers.

Amounts represent the equity compensation awarded to our trustees, our officers and certain other employees of RMR LLC.

We recorded a loss of $8,451 on early extinguishment of debt in the three months ended September 30, 2019 related to the termination of a term loan commitment we arranged in connection with the SMTA transaction.

We also recorded a $160 loss on early extinguishment of debt in the three months ended June 30, 2018 in connection with the amendment of our revolving credit facility and term loan.

Unrealized gains and losses on equity securities, net represent the adjustment required to adjust the carrying value of our investments in RMR Inc. and TA common shares to their fair value as of the end of the period.

We sold our shares of RMR Inc. in July 2019.

Please see page 23 for definitions of EBITDA, EBITDAre and Adjusted EBITDAre and a description of why we believe the presentation of these measures provide useful information to investors.

$ 40,074 $ 8,782 $ 225,787 $ (108,860) $ 117,099 $ 274,643 $ 294,594

Interest expense 52,375 49,601 49,766 49,624 49,308 151,742 145,589

Income tax expense (benefit) 467 (260) 1,059 (754) 707 1,266 1,949

Depreciation and amortization 103,160 99,196 99,365 102,769 101,007 301,721 300,308

196,076 157,319 375,977 42,779 268,121 729,372 742,440

Gain on sale of real estate (2) — — (159,535) — — (159,535) —

196,076 157,319 216,442 42,779 268,121 569,837 742,440

General and administrative expense paid in common shares (3) 1,068 865 436 909 1,008 2,369 2,278

Loss on early extinguishment of debt (4) 8,451 — — — — 8,451 160

Unrealized gains and losses on equity securities, net (5) 3,950 60,788 (20,977) 106,085 (43,453) 43,761 (89,348)

$ 209,545 $ 218,972 $ 195,901 $ 149,773 $ 225,676 $ 624,418 $ 655,530

(1)

(2)

(3)

(4)

(5)

We recorded a $159,535 gain on sale of real estate in the three months ended March 31, 2019, in connection with the sales of 20 travel centers.

Amounts represent the equity compensation awarded to our trustees, our officers and certain other employees of RMR LLC.

We recorded a loss of $8,451 on early extinguishment of debt in the three months ended September 30, 2019 related to the termination of a term loan commitment we arranged in connection with the SMTA transaction. We

also recorded a $160 loss on early extinguishment of debt in the three months ended June 30, 2018 in connection with the amendment of our revolving credit facility and term loan.

Unrealized gains and losses on equity securities, net represent the adjustment required to adjust the carrying value of our investments in RMR Inc. and TA common shares to their fair value as of the end of the period. We

sold our shares of RMR Inc. in July 2019.

Please see page 23 for definitions of EBITDA, EBITDAre and Adjusted EBITDAre and a description of why we believe the presentation of these measures provide useful information to investors.

Add (Less):

Adjusted EBITDAre

Net income (loss)

Add (Less):

EBITDA

Less:

EBITDAre

For the Three Months Ended For the Nine Months Ended

9/30/2019 6/30/2019 3/31/2019 12/31/2018 9/30/2018 2019 2018

CALCULATION OF EBITDA, EBITDAre AND ADJUSTED EBITDAre (1)

(in thousands)

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Calculat ion of Funds From Operat ions (FFO) and Normal ized FFO. (1)

( In thousands )

22

$ 40,074 $ 8,782 $ 225,787 $ (108,860) $ 117,099 $ 274,643 $ 294,594

Depreciation and amortization 103,160 99,196 99,365 102,769 101,007 301,721 300,308

Gain on sale of real estate (2) — — (159,535) — — (159,535) —

Unrealized gains and losses on equity

securities, net (3) 3,950 60,788 (20,977) 106,085 (43,453) 43,761 (89,348)

147,184 168,766 144,640 99,994 174,653 460,590 505,554

Loss on early extinguishment of debt (4) 8,451 — — — — 8,451 160

$ 155,635 $ 168,766 $ 144,640 $ 99,994 $ 174,653 $ 469,041 $ 505,714

164,321 164,284 164,278 164,278 164,232 164,294 164,212

164,348 164,326 164,322 164,278 164,274 164,332 164,242

$ 0.24 $ 0.05 $ 1.37 $ (0.66) $ 0.71 $ 1.67 $ 1.79

$ 0.90 $ 1.03 $ 0.88 $ 0.61 $ 1.06 $ 2.80 $ 3.08

$ 0.95 $ 1.03 $ 0.88 $ 0.61 $ 1.06 $ 2.85 $ 3.08

(1)

(2)

(3)

(4)

CALCULATION OF FFO AND NORMALIZED FFO (1)

(amounts in thousands, except share data)

For the Three Months Ended For the Nine Months Ended

9/30/2019 6/30/2019 3/31/2019 12/31/2018 9/30/2018 2019 2018

Net income (loss)

Add

FFO

Add:

Normalized FFO

Weighted average shares outstanding (basic)

Weighted average shares outstanding (diluted)

We recorded a loss of $8,451 on early extinguishment of debt in the three months ended September 30, 2019 related to the termination of a term loan commitment we arranged in

connection with the SMTA transaction. We also recorded a $160 loss on early extinguishment of debt in the three months ended June 30, 2018 in connection with the amendment of our

revolving credit facility and term loan.

Net income (loss)

FFO

Normalized FFO

Basic and diluted per share common share

Please see page 23 for definitions of FFO and Normalized FFO, a description of why we believe the presentation of these measures provides useful information to investors regarding

our financial condition and results of operations and a description of how we use these measures.

We recorded a $159,535 gain on sale of real estate in the three months ended March 31, 2019 in connection with the sales of 20 travel centers.

Unrealized gains and losses on equity securities, net represent the adjustment required to adjust the carrying value of our investments in RMR Inc. and TA common shares to their fair

value as of the end of the period. We sold our shares of RMR Inc. in July 2019. (1)

(2)

(3)

(4) We recorded a loss of $8,451 on early extinguishment of debt in the three months ended September 30, 2019 related to the termination of a term loan commitment we arranged in

connection with the SMTA transaction. We also recorded a $160 loss on early extinguishment of debt in the three months ended June 30, 2018 in connection with the amendment of our

revolving credit facility and term loan.

Please see page 23 for definitions of FFO and Normalized FFO, a description of why we believe the presentation of these measures provides useful information to investors regarding

our financial condition and results of operations and a description of how we use these measures.

We recorded a $159,535 gain on sale of real estate in the three months ended March 31, 2019 in connection with the sales of 20 travel centers.

Unrealized gains and losses on equity securities, net represent the adjustment required to adjust the carrying value of our investments in RMR Inc. and TA common shares to their fair

value as of the end of the period. We sold our shares of RMR Inc. in July 2019.

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

NON-GAAP FINANCIAL MEASURES

We present certain “non-GAAP financial measures” within the meaning of applicable Securities and Exchange Commission, or SEC, rules, including EBITDA, EBITDAre, Adjusted

EBITDAre, FFO and Normalized FFO. These measures do not represent cash generated by operating activities in accordance with GAAP and should not be considered alternatives to net

income (loss) as indicators of our operating performance or as measures of our liquidity. These measures should be considered in conjunction with net income (loss) as presented in our

condensed consolidated statements of income. We consider these non-GAAP measures to be appropriate supplemental measures of operating performance for a REIT, along with net

income (loss). We believe these measures provide useful information to investors because by excluding the effects of certain historical amounts, such as depreciation and amortization

expense, they may facilitate a comparison of our operating performance between periods and with other REITs.

EBITDA, EBITDAre AND ADJUSTED EBITDAre

We calculate earnings before interest, taxes, depreciation and amortization, or EBITDA, EBITDA for real estate, or EBITDAre, and Adjusted EBITDAre as shown on page 21. EBITDAre is

calculated on the basis defined by The National Association of Real Estate Investment Trusts, or Nareit, which is EBITDA, excluding gains and losses on the sale of real estate, loss on

impairment of real estate assets, if any, as well as certain other adjustments currently not applicable to us. In calculating Adjusted EBITDAre, we adjust for the items shown on page 21 and

include business management incentive fees only in the fourth quarter versus the quarter when they are recognized as expense in accordance with GAAP due to their quarterly volatility

not necessarily being indicative of our core operating performance and the uncertainty as to whether any such business management incentive fees will be payable when all contingencies

for determining such fees are known at the end of the calendar year. Other real estate companies and REITs may calculate EBITDA, EBITDAre and Adjusted EBITDAre differently than we

do.

FFO AND NORMALIZED FFO

We calculate funds from operations, or FFO, and Normalized FFO as shown on page 22. FFO is calculated on the basis defined by Nareit, which is net income (loss), calculated in

accordance with GAAP, excluding any gain or loss on sale of properties and loss on impairment of real estate assets, if any, plus real estate depreciation and amortization, less any

unrealized gains and losses on equity securities, as well as certain other adjustments currently not applicable to us. In calculating Normalized FFO, we adjust for the item shown on page

22 and include business management incentive fees, if any, only in the fourth quarter versus the quarter when they are recognized as expense in accordance with GAAP due to their

quarterly volatility not necessarily being indicative of our core operating performance and the uncertainty as to whether any such business management incentive fees will be payable when

all contingencies for determining such fees are known at the end of the calendar year. FFO and Normalized FFO are among the factors considered by our Board of Trustees when

determining the amount of distributions to our shareholders. Other factors include, but are not limited to, requirements to maintain our qualification for taxation as a REIT, limitations in our

credit agreement and public debt covenants, the availability to us of debt and equity capital, our distribution rate as a percentage of the trading price of our common shares, or dividend

yield, and to the dividend yield of other REITs, our expectation of our future capital requirements and operating performance and our expected needs for and availability of cash to pay our

obligations. Other real estate companies and REITs may calculate FFO and Normalized FFO differently than we do.

COVERAGE

We define hotel coverage as total hotel revenues minus all hotel expenses and FF&E reserve escrows which are not subordinated to minimum returns due to SVC divided by the minimum

returns or rents due to SVC.

We define net lease coverage as annual property level adjusted earnings before interest, taxes, depreciation, amortization and rent, or EBITDAR, divided by the annual minimum rent due

to us weighted by the minimum rent of the property to total minimum rents of the net lease portfolio. The annual property level adjusted EBITDAR is determined based on the most recent

operating statements, if any, furnished by the tenant. Operating statements furnished by the tenant often are unaudited and, in certain cases, may not have been prepared in accordance

with GAAP and are not independently verified by us. Properties that do not report operating information are excluded from the coverage calculations.

Non-GAAP Financial Measures Def ini t ions.

23

S E RV ICE P ROP E RTIE S TRUS T (Nasdaq: S V C) | Inves t o r P resen ta t i o n Q3 2019

Service Properties Trust

Q3 2019 Investor Presentation