Embed Size (px)

DESCRIPTION

Fin ppt

Citation preview

FMT2 – Session 2

Pradeepta SethiTAPMI

Stock repurchases

¢ Buying own stock back from stockholders.¢ Distributing cash to existing shareholders.¢ Reduction in the cash balance.¢ Reduces the book value of equity.¢ Reduces the number of shares outstanding.¢ Profit per share increases.¢ Once repurchased, the shares become treasury

stock.

Why repurchase stock?¢ Investor tax argument

¢ Leverage hypothesis

¢ Uncertainty about the ability to continue generating thesecash flows in future periods

¢ A repurchase is a signal that stock is underpriced.¢ Executive compensation is often affected by share buybacks.

¢ Increasing insider control in firms.

¢ Supporting stock prices when they are declining.

¢ Allow to maintain flexibility for future periods.

Share Repurchase Methods

Buy in the Open Market

• Use brokers to buy shares.

• Method provides flexibility for the company.

Fixed Price Tender Offer

• Specify the number of shares and the share price.

• Buy pro rata if oversubscribed.

Dutch Auction Tender Offer

• Specify the number of shares and the range of prices.

• Shareholders determine the number of shares they will sell back and specify the price within the range.

DirectNegotiation

• Negotiate with a specific shareholder.

• Method may be used to prevent “activist” shareholder from getting on board.

SEBI regulations¢ No offer of buy-back for 15% or more of the paid up capital

and free reserves of the company shall be made from theopen market.

¢ Shall not make any offer of buy-back within a period of oneyear reckoned from the date of closure of the preceding offerof buy-back.

¢ Put 25% of the amount earmarked for buyback in an escrowaccount and to complete their share purchase offer within sixmonths.

¢ Companies to purchase at least 50% of the offer size, failingwhich they will have to forfeit 2.5% of the total amountearmarked.

Advantages of stock repurchases

¢ Stockholders can tender or not.¢ Helps avoid setting a high dividend that cannot be

maintained.¢ Repurchased stock can be used in takeovers or

resold to raise cash as needed.¢ Income received is capital gains rather than higher-

taxed dividends.¢ Stockholders may take as a positive signal--

management thinks stock is undervalued.

Disadvantages of stock repurchases

¢ May be viewed as a negative signal (firm has poorinvestment opportunities).

¢ Could attract penalties if repurchases were primarilyto avoid taxes on dividends.

¢ Selling stockholders may not be well informed,hence be treated unfairly.

¢ Firm may have to bid up price to completepurchase, thus paying too much for its own stock.

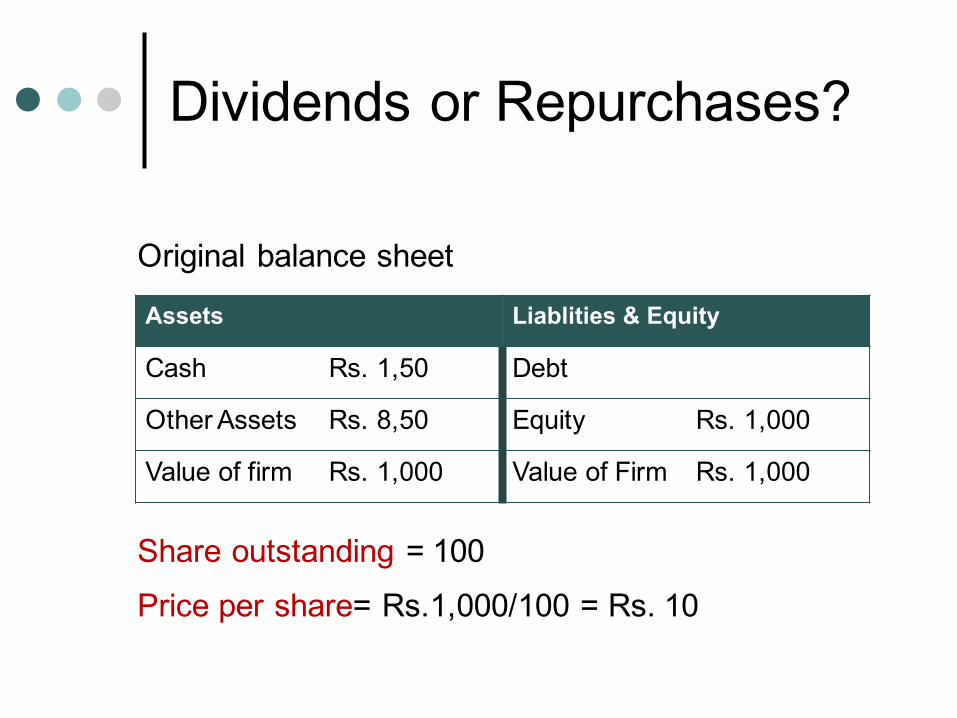

Dividends or Repurchases?

Assets Liablities & Equity

Cash Rs. 1,50 Debt

Other Assets Rs. 8,50 Equity Rs. 1,000

Value of firm Rs. 1,000 Value of Firm Rs. 1,000

Original balance sheet

Share outstanding = 100

Price per share= Rs.1,000/100 = Rs. 10

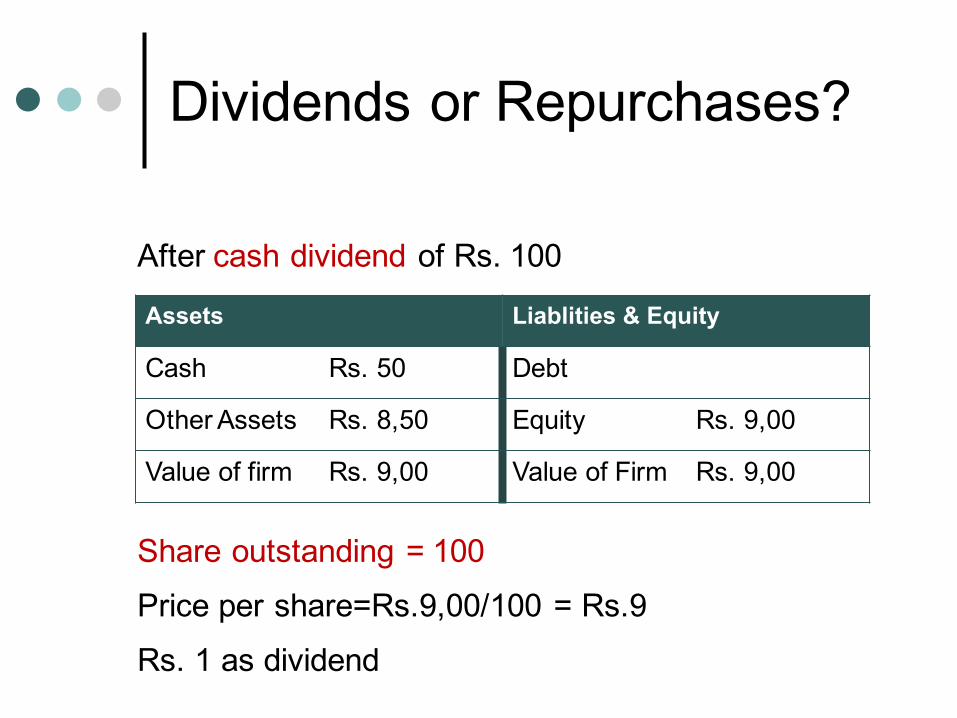

Dividends or Repurchases?

Assets Liablities & Equity

Cash Rs. 50 Debt

Other Assets Rs. 8,50 Equity Rs. 9,00

Value of firm Rs. 9,00 Value of Firm Rs. 9,00

After cash dividend of Rs. 100

Share outstanding = 100

Price per share=Rs.9,00/100 = Rs.9

Rs. 1 as dividend

Dividends or Repurchases?

Assets Liablities & Equity

Cash Rs. 50 Debt

Other Assets Rs. 8,50 Equity Rs. 9,00

Value of firm Rs. 9,00 Value of Firm Rs. 9,00

After stock repurchase of Rs. 100

At Rs. 10/- share, we could buy 100/10=10 shares

Shares outstanding= 100-10 =90

Price per share=Rs.9,00/90 = Rs.10

Share repurchase and Earnings Per Share

The Happy New Year Corporation is planning a Rs100lakh share repurchase. Its current stock price is Rs 25 pershare, and there are 16 lakh shares outstanding prior tothe repurchase. Earnings per share without therepurchase would be Rs. 3 per share. What is theearnings per share under each of these two scenarios?

Scenario 1: Use idle cash on hand.Scenario 2: Borrow funds at after-tax rate of 7%.

Share repurchase and Earnings Per Share

¢ Scenario 1:l Net income = Rs.3 × Rs16 lakhs = Rs. 48 lakhsl EPS Scenario 1 = Rs.48 lakhs ÷ (16 lakhs – 4

lakhs) = Rs.4 per share¢ Scenario 2:

l Net income = Rs.3 × 16 lakhs – (0.07 × Rs.100 lakhs) = Rs.41 lakhs

l EPS Scenario 2 = Rs.41 lakhs ÷ (16 lakhs – 4 lakhs) = Rs.3.41 per share

Share repurchase and Earnings Per Share

¢ After-tax borrowing rate = 7%¢ Earnings yield = Rs.3 ÷ Rs. 25 = 12%¢ After-tax borrowing rate < Earnings yield¢ Whether EPS é, ê or ó:

• If the after-tax borrowing rate = earnings yield, EPSunchanged from buyback financed with debt.

• If the after-tax borrowing rate < earnings yield, EPSincreases.

• If the after-tax borrowing rate > earnings yield, EPSdecreases.

Dividends or Repurchases?¢ If…

l The tax consequences of dividends and capital gains are the same and

l The information content of cash dividends and stock repurchases is the same,

¢ Then the effects of cash dividends and repurchases on shareholder value will be the same.

¢ Both cash dividends and stock repurchases:l Reduce assets by the amount of the dividend or

repurchase.l Reduce equity by the amount of the dividend or

repurchase.l Provide investors with the same cash flow.

Choosing between dividends & repurchases

¢ Sustainability and stability of excess cash flow.

¢ Stockholder tax preferences

¢ Predictability of future investment needs

¢ Undervaluation of the stock

¢ Management compensation

Dividend Policy Survey 2004

Dividend Policy Survey 2004

Summary of views about payout policy

![핵심인재양성을위한솔루션 · Session 2: 긍정적삶을위한롤플레잉게임 [오프라인] 학습원정대 Session 1: 체험학습현장 Session 2: 미션수행 Session](https://img.pdfslide.net/doc/110x75/5fea8bdf34892c266d2fd149/oeoee-session-2-eoeoeeoeeeoe.jpg)

![CRM Session 2[2]](https://img.pdfslide.net/doc/110x75/577cce6e1a28ab9e788e0e28/crm-session-22.jpg)