Embed Size (px)

Citation preview

Session 42 PD, Public and Private Disability Insurance: Past, Present, and Future

Moderator:

Ali Zaker-Shahrak, FSA, MAAA, Ph.D.

Presenters: Stephen Goss, ASA, MAAA

Doug Vrooman, FSA, MAAA

Social Security Disability Insurance: Benefits, Actuarial Status, Future

Stephen C. Goss, Chief Actuary, Social Security Administration

Society of Actuaries 2016 Health Meeting: Session 42 June 15, 2016

2

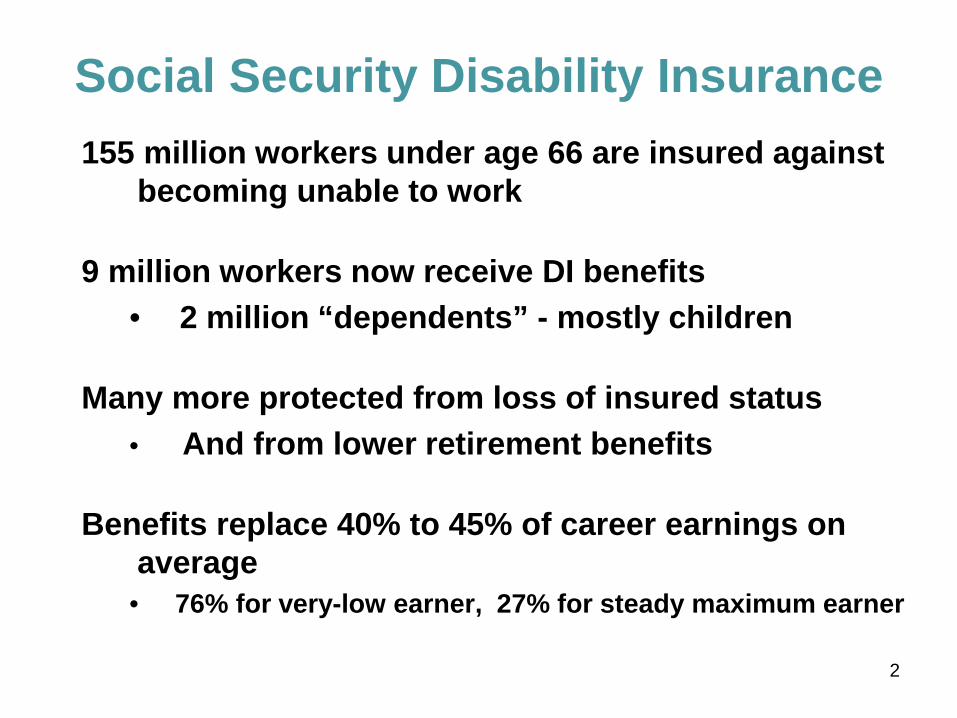

Social Security Disability Insurance155 million workers under age 66 are insured against

becoming unable to work

9 million workers now receive DI benefits• 2 million “dependents” - mostly children

Many more protected from loss of insured status• And from lower retirement benefits

Benefits replace 40% to 45% of career earnings on average

• 76% for very-low earner, 27% for steady maximum earner

3

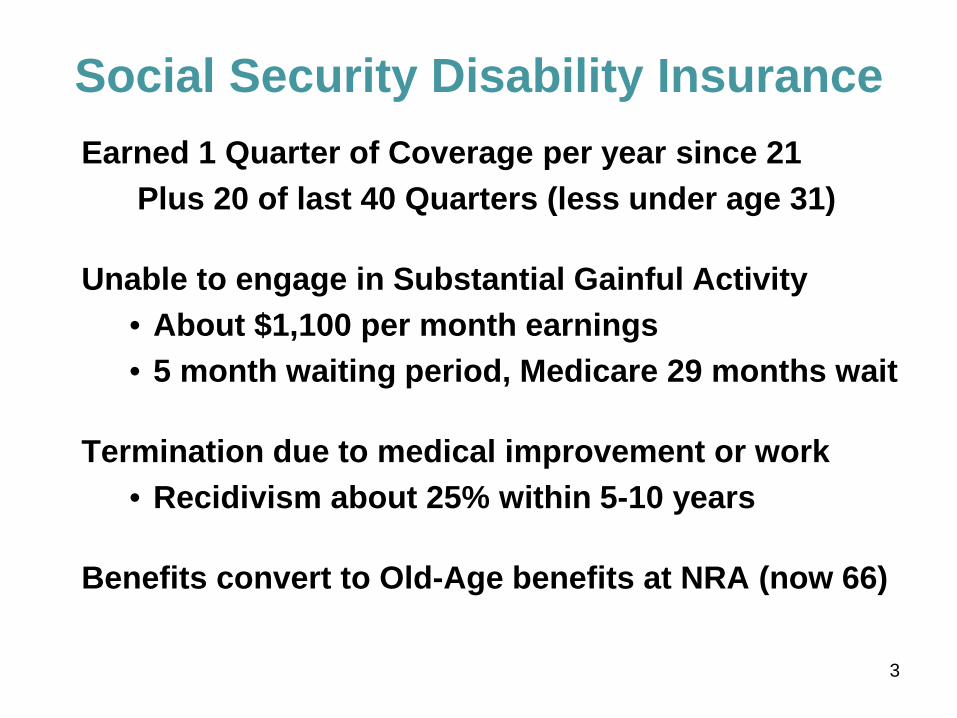

Social Security Disability InsuranceEarned 1 Quarter of Coverage per year since 21

Plus 20 of last 40 Quarters (less under age 31)

Unable to engage in Substantial Gainful Activity• About $1,100 per month earnings• 5 month waiting period, Medicare 29 months wait

Termination due to medical improvement or work• Recidivism about 25% within 5-10 years

Benefits convert to Old-Age benefits at NRA (now 66)

4

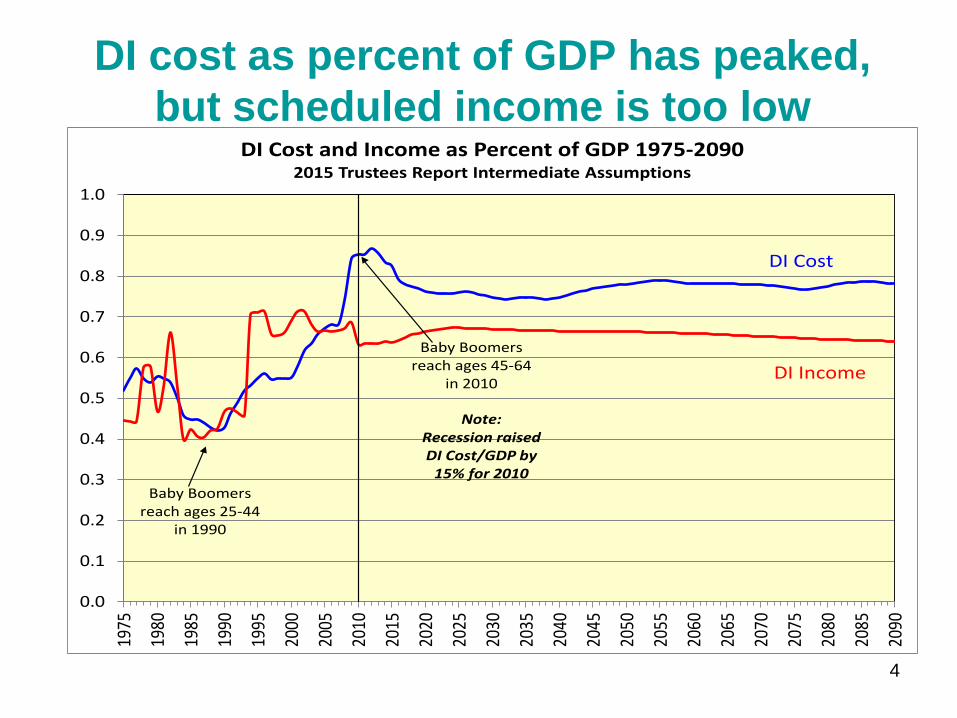

DI cost as percent of GDP has peaked, but scheduled income is too low

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

2055

2060

2065

2070

2075

2080

2085

2090

DI Cost and Income as Percent of GDP 1975-20902015 Trustees Report Intermediate Assumptions

Baby Boomers reach ages 45-64

in 2010

Baby Boomers reach ages 25-44

in 1990

Note: Recession raisedDI Cost/GDP by

15% for 2010

DI Cost

DI Income

5

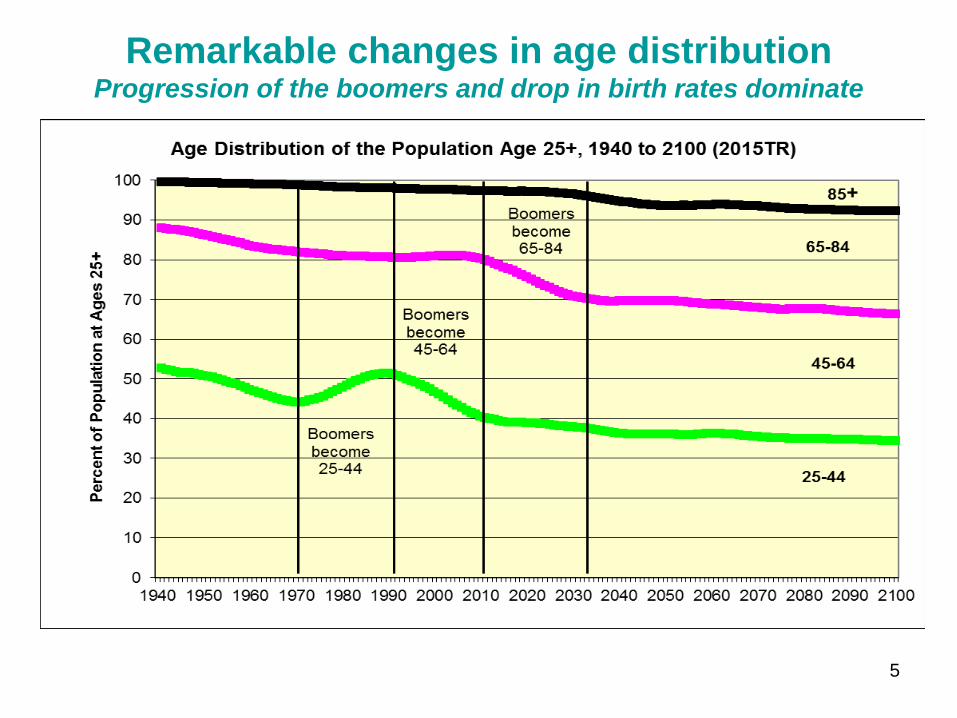

Remarkable changes in age distributionProgression of the boomers and drop in birth rates dominate

6

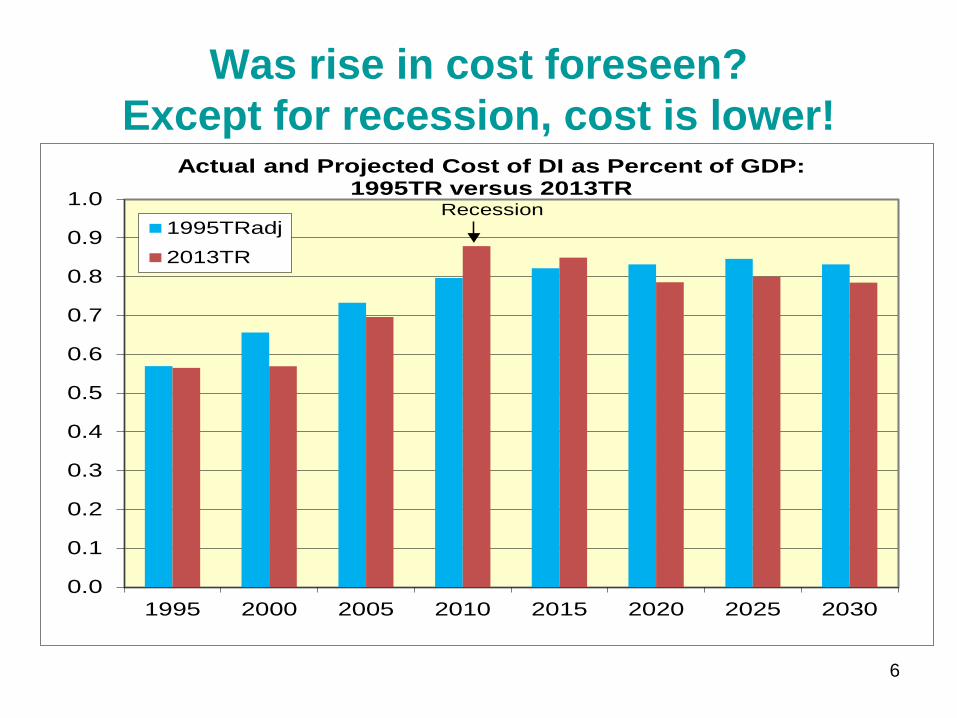

Was rise in cost foreseen?Except for recession, cost is lower!

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

1995 2000 2005 2010 2015 2020 2025 2030

Actual and Projected Cost of DI as Percent of GDP: 1995TR versus 2013TR

1995TRadj2013TR

Recession

7

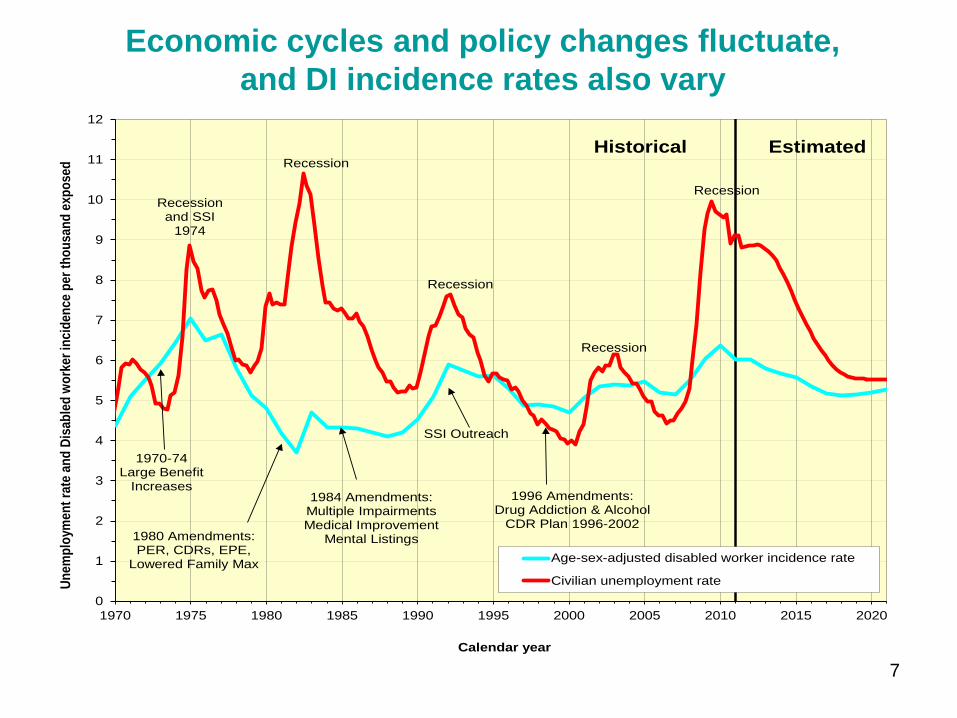

Economic cycles and policy changes fluctuate, and DI incidence rates also vary

0

1

2

3

4

5

6

7

8

9

10

11

12

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Unem

ploy

men

t rat

e an

d Di

sabl

ed w

orke

r inc

iden

ce p

er th

ousa

nd e

xpos

ed

Calendar year

Age-sex-adjusted disabled worker incidence rate

Civilian unemployment rate

Historical Estimated

Recession and SSI

1974

Recession

Recession

Recession

1980 Amendments: PER, CDRs, EPE,

Lowered Family Max

1984 Amendments: Multiple Impairments Medical Improvement

Mental Listings

1996 Amendments: Drug Addiction & Alcohol

CDR Plan 1996-2002

SSI Outreach

1970-74 Large Benefit

Increases

Recession

8

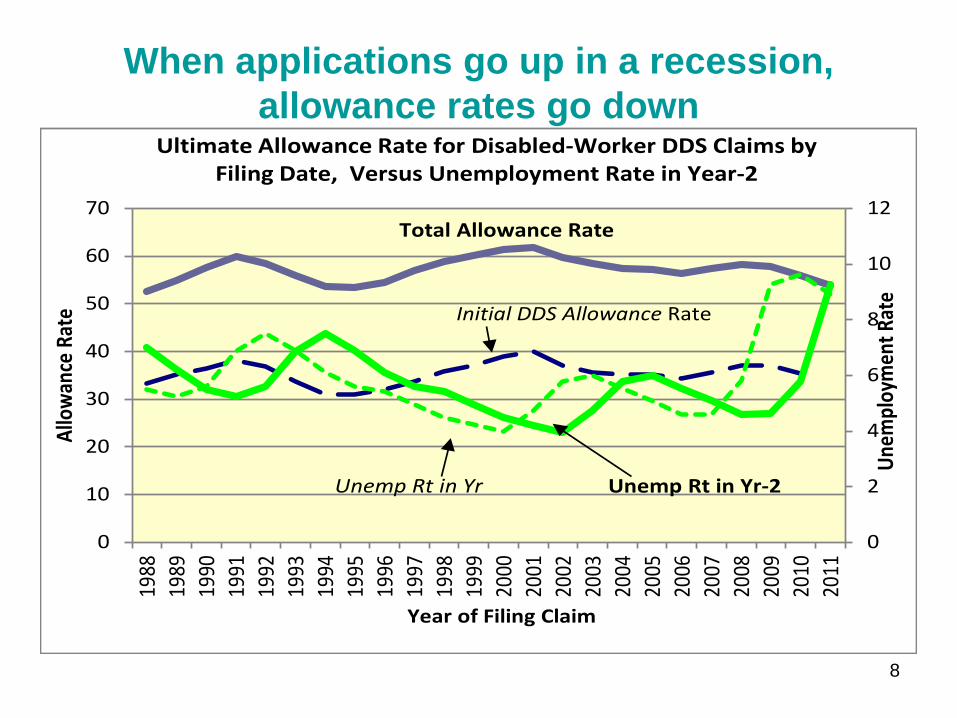

When applications go up in a recession, allowance rates go down

0

2

4

6

8

10

12

0

10

20

30

40

50

60

70

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Unem

ploy

men

t Rat

e

Allo

wan

ce R

ate

Year of Filing Claim

Ultimate Allowance Rate for Disabled-Worker DDS Claims by Filing Date, Versus Unemployment Rate in Year-2

Total Allowance Rate

Unemp Rt in Yr Unemp Rt in Yr-2

Initial DDS Allowance Rate

9

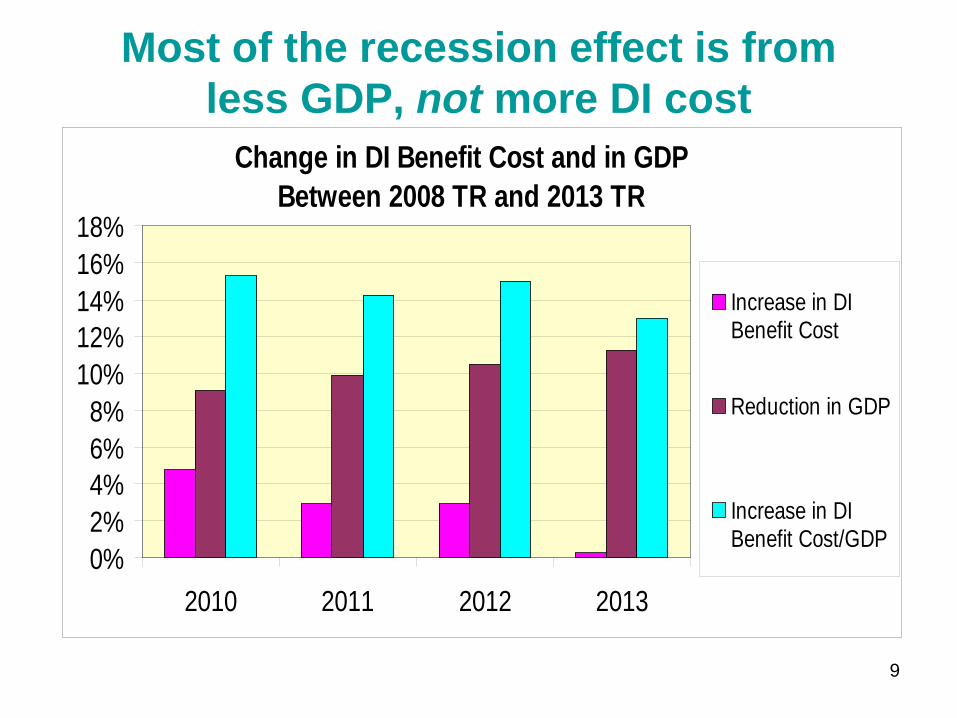

Most of the recession effect is from less GDP, not more DI cost

Change in DI Benefit Cost and in GDP Between 2008 TR and 2013 TR

0%2%4%6%8%

10%12%14%16%18%

2010 2011 2012 2013

Increase in DIBenefit Cost

Reduction in GDP

Increase in DIBenefit Cost/GDP

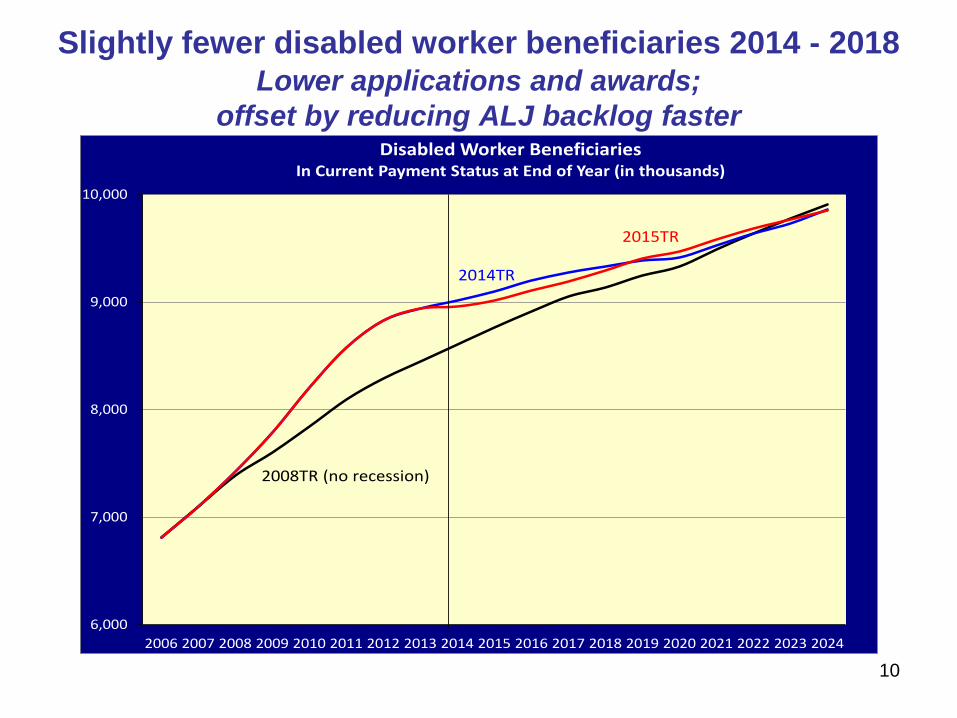

Slightly fewer disabled worker beneficiaries 2014 - 2018Lower applications and awards;

offset by reducing ALJ backlog faster

6,000

7,000

8,000

9,000

10,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Disabled Worker BeneficiariesIn Current Payment Status at End of Year (in thousands)

2008TR (no recession)

2015TR

2014TR

10

11

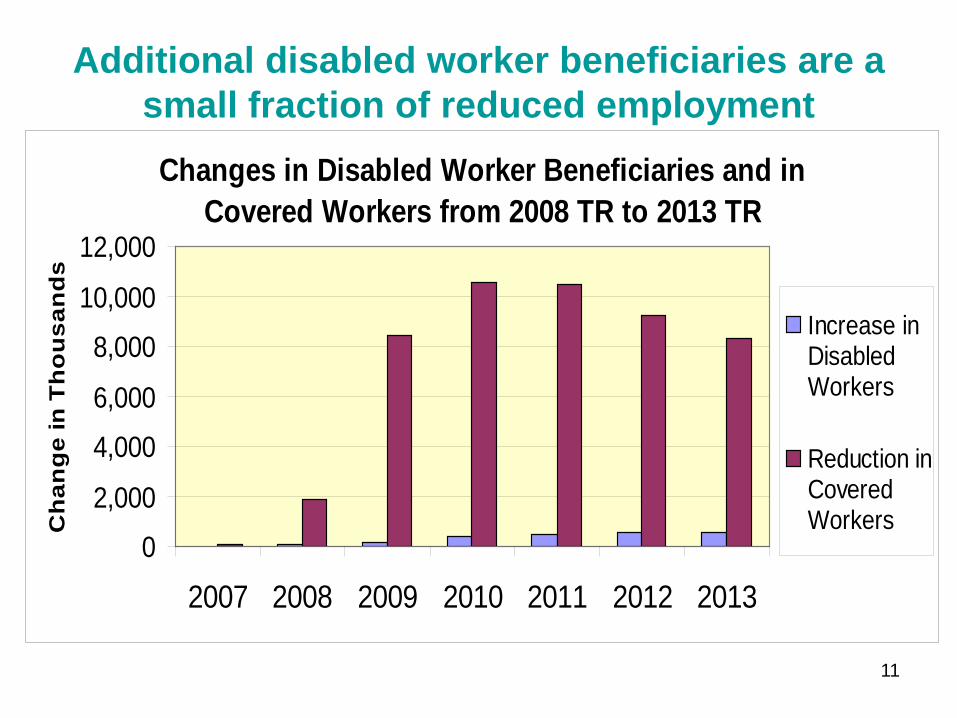

Additional disabled worker beneficiaries are a small fraction of reduced employment

Changes in Disabled Worker Beneficiaries and in Covered Workers from 2008 TR to 2013 TR

0

2,000

4,000

6,000

8,000

10,000

12,000

2007 2008 2009 2010 2011 2012 2013

Ch

ang

e in

Th

ou

san

ds

Increase inDisabledWorkers

Reduction inCoveredWorkers

12

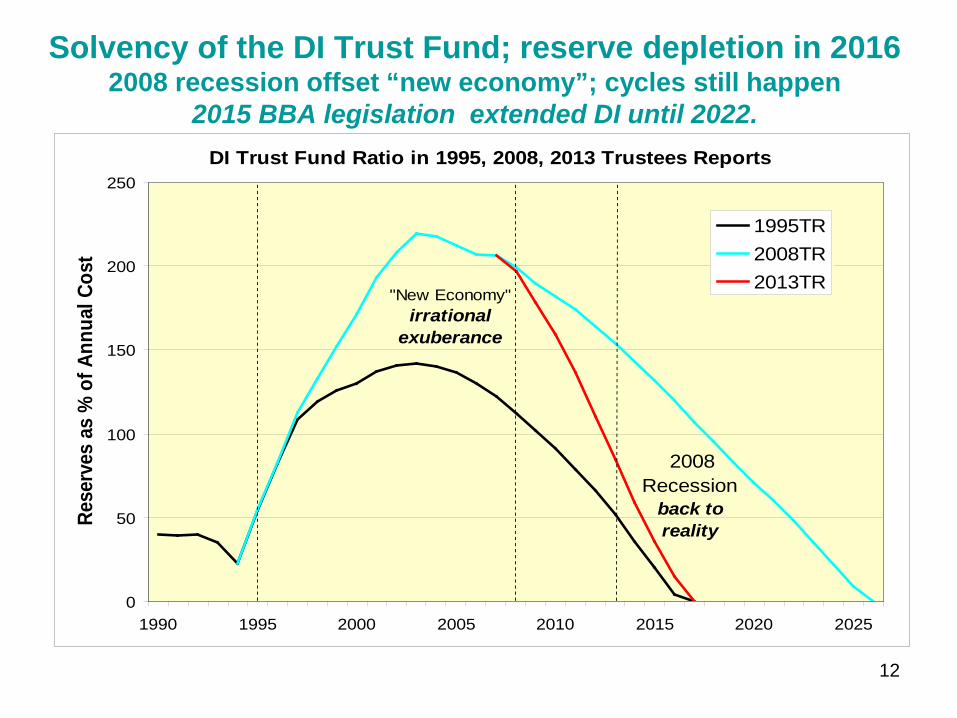

Solvency of the DI Trust Fund; reserve depletion in 20162008 recession offset “new economy”; cycles still happen

2015 BBA legislation extended DI until 2022.DI Trust Fund Ratio in 1995, 2008, 2013 Trustees Reports

0

50

100

150

200

250

1990 1995 2000 2005 2010 2015 2020 2025

Rese

rves

as

% o

f Ann

ual C

ost

1995TR2008TR2013TR

"New Economy" irrational

exuberance

2008 Recession

back to reality

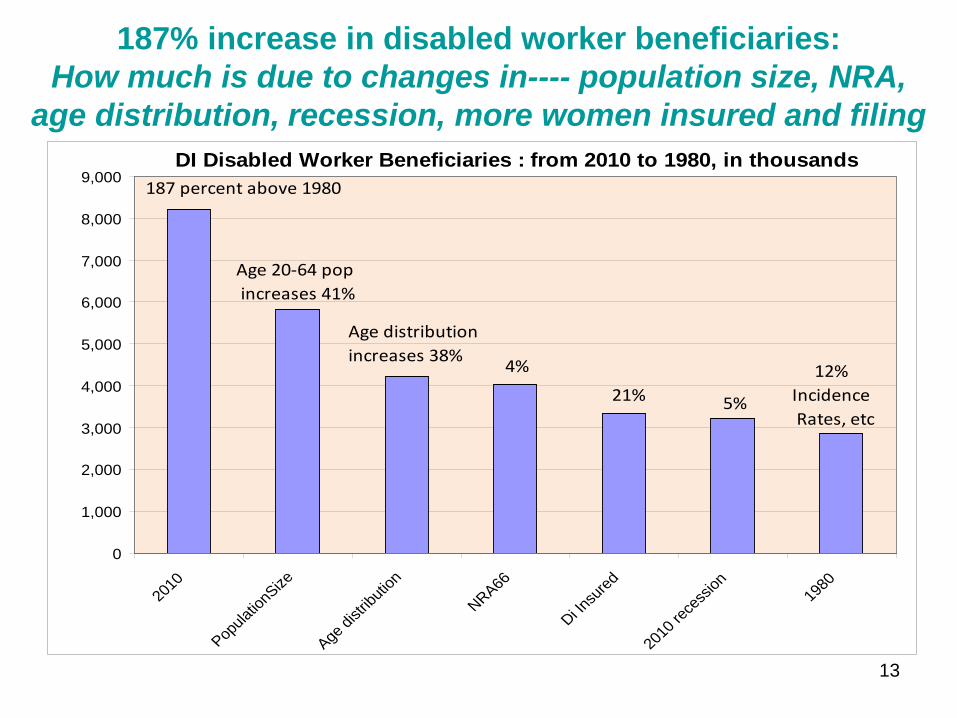

187% increase in disabled worker beneficiaries: How much is due to changes in---- population size, NRA,

age distribution, recession, more women insured and filing

13

DI Disabled Worker Beneficiaries : from 2010 to 1980, in thousands

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2010

Popula

tionS

ize

Age di

stribu

tion

NRA66

Di Insu

red

2010

rece

ssion 19

80

187 percent above 1980

Age 20-64 pop increases 41%

Age distribution increases 38% 4%

21% 5%

12% Incidence Rates, etc

14

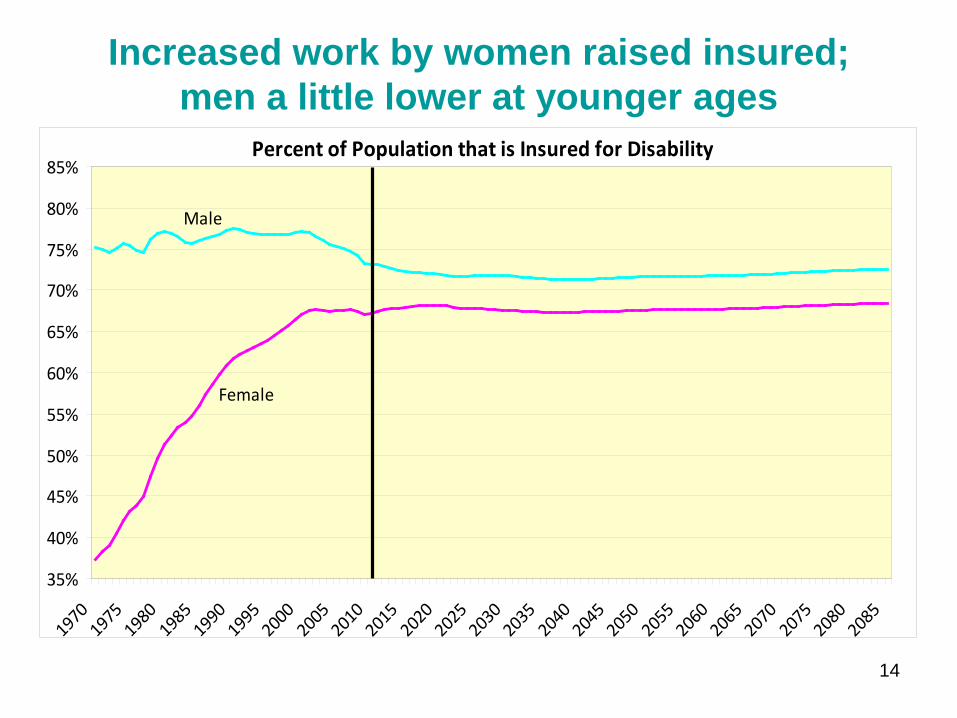

Increased work by women raised insured; men a little lower at younger ages

Percent of Population that is Insured for Disability

35%

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

19701975

19801985

19901995

20002005

20102015

20202025

20302035

20402045

20502055

20602065

20702075

20802085

Male

Female

15

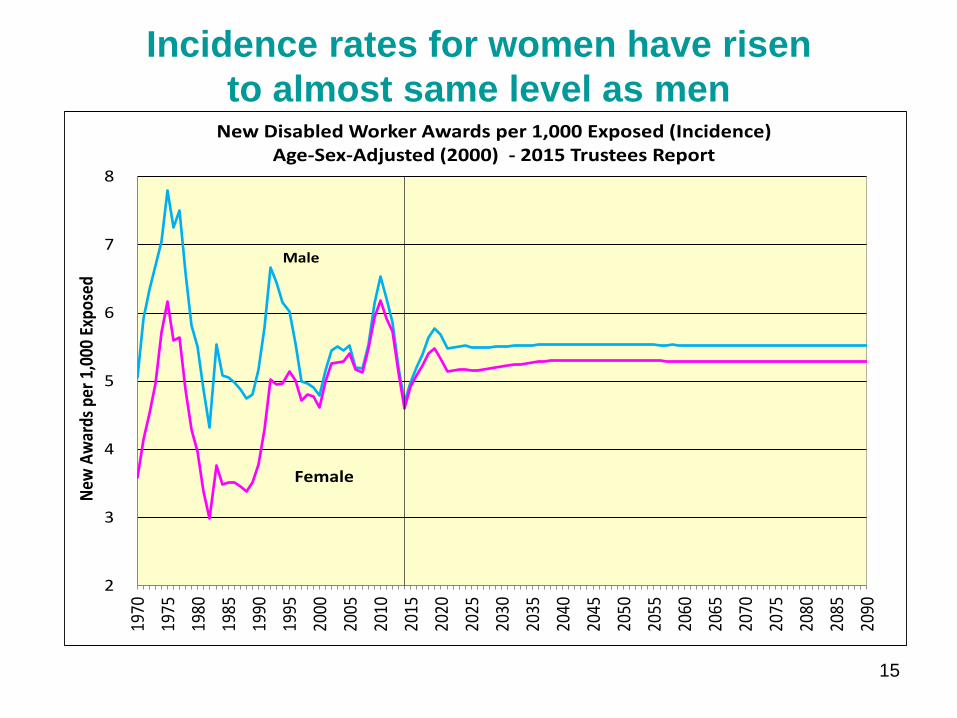

Incidence rates for women have risen to almost same level as men

2

3

4

5

6

7

8

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

2055

2060

2065

2070

2075

2080

2085

2090

New

Aw

ards

per

1,0

00 E

xpos

ed

New Disabled Worker Awards per 1,000 Exposed (Incidence) Age-Sex-Adjusted (2000) - 2015 Trustees Report

Male

Female

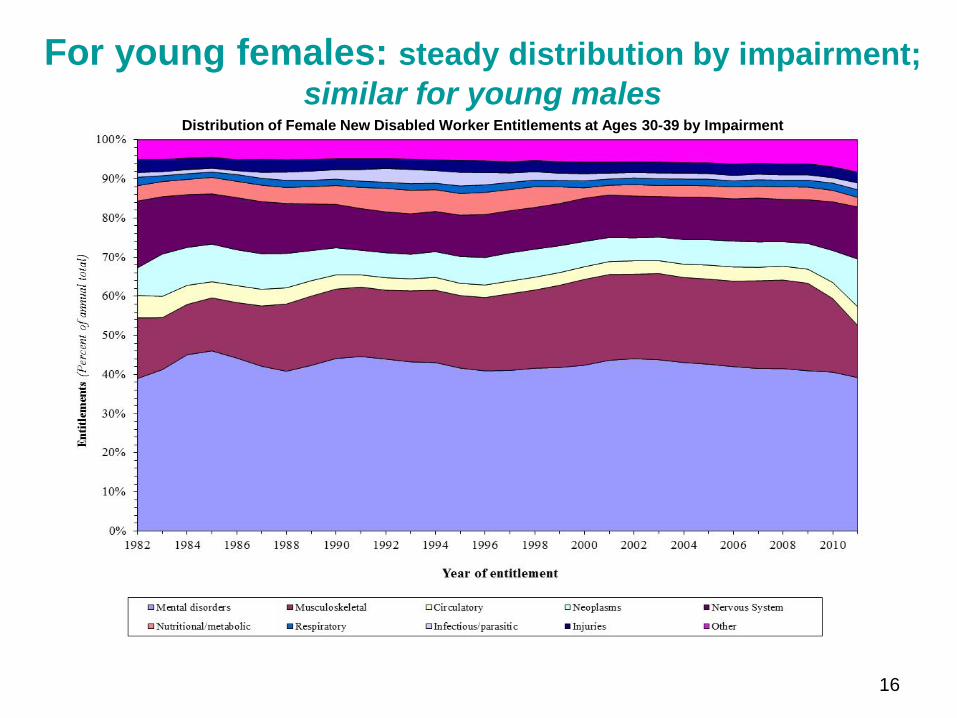

For young females: steady distribution by impairment;similar for young males

Distribution of Female New Disabled Worker Entitlements at Ages 30-39 by Impairment

16

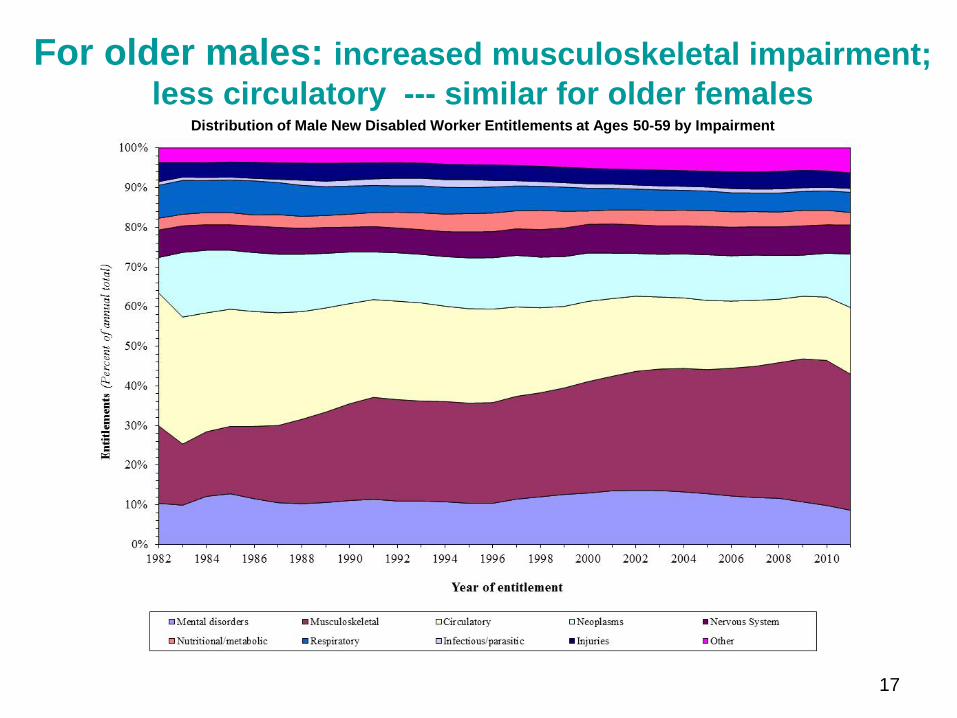

For older males: increased musculoskeletal impairment; less circulatory --- similar for older females

Distribution of Male New Disabled Worker Entitlements at Ages 50-59 by Impairment

17

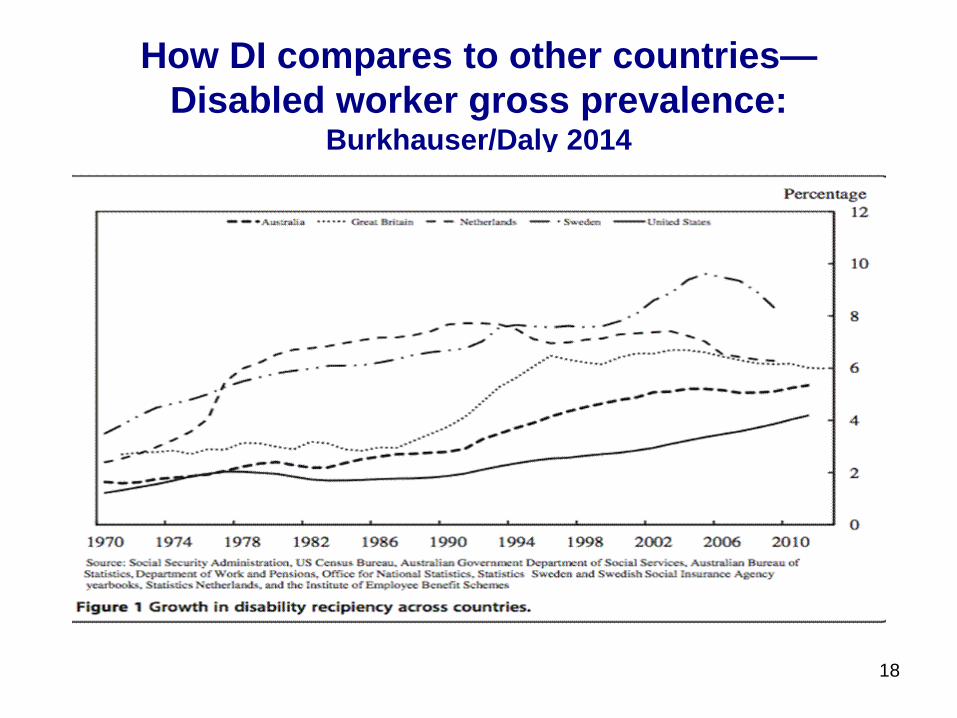

How DI compares to other countries—Disabled worker gross prevalence:

Burkhauser/Daly 2014

18

19

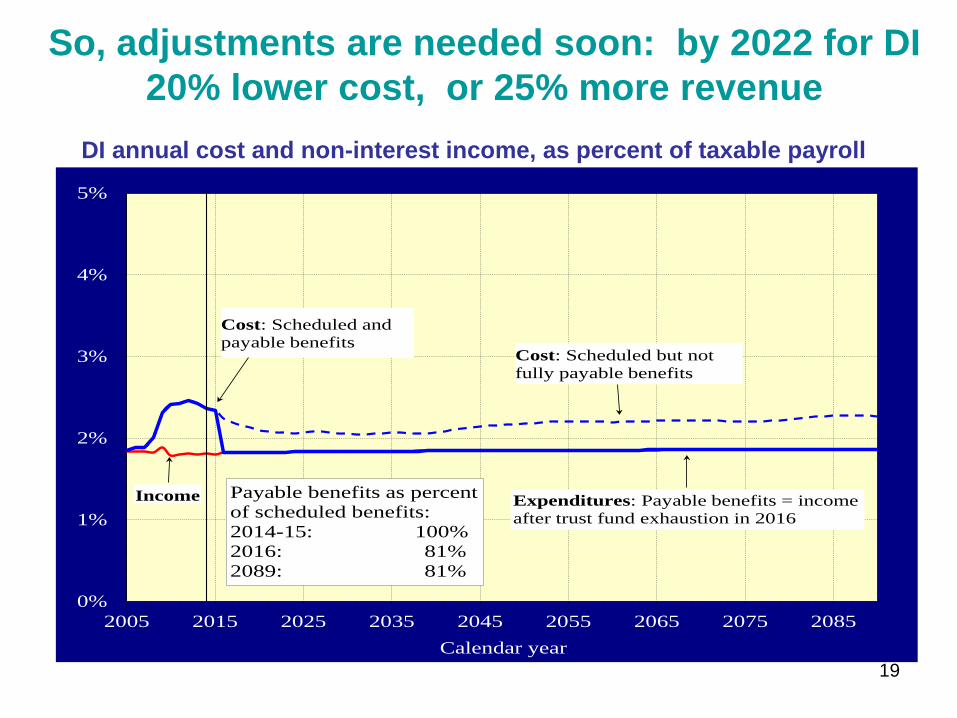

So, adjustments are needed soon: by 2022 for DI20% lower cost, or 25% more revenue

0%

1%

2%

3%

4%

5%

2005 2015 2025 2035 2045 2055 2065 2075 2085Calendar year

Cost: Scheduled and payable benefits

Income Payable benefits as percentof scheduled benefits:2014-15: 100%2016: 81%2089: 81%

Cost: Scheduled but not fully payable benefits

Expenditures: Payable benefits = income after trust fund exhaustion in 2016

DI annual cost and non-interest income, as percent of taxable payroll

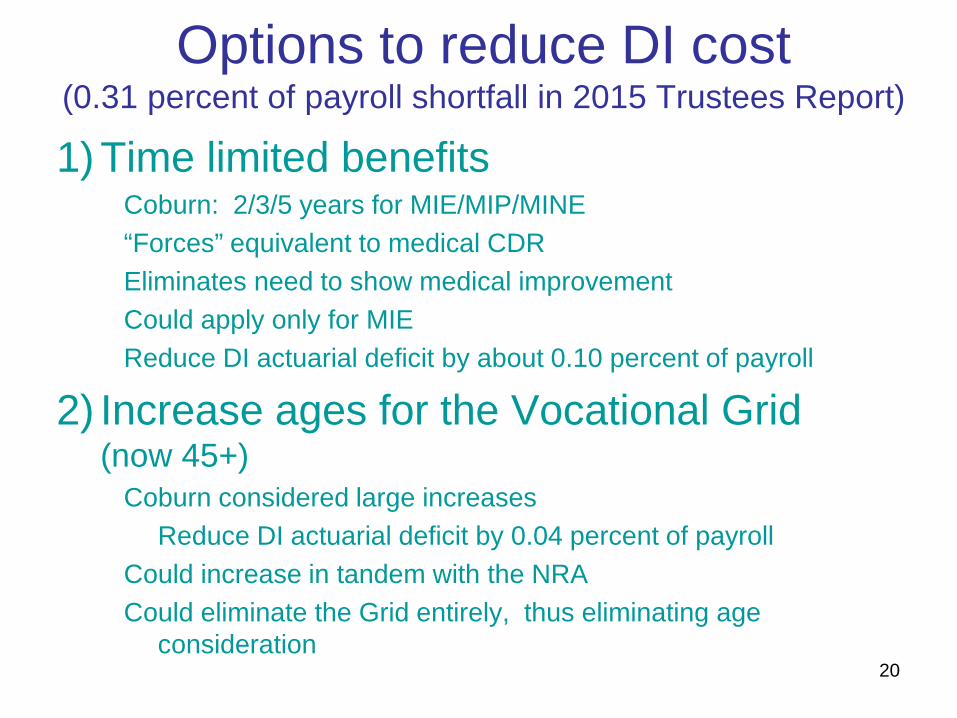

Options to reduce DI cost (0.31 percent of payroll shortfall in 2015 Trustees Report)

1) Time limited benefitsCoburn: 2/3/5 years for MIE/MIP/MINE“Forces” equivalent to medical CDREliminates need to show medical improvementCould apply only for MIE Reduce DI actuarial deficit by about 0.10 percent of payroll

2) Increase ages for the Vocational Grid (now 45+)

Coburn considered large increasesReduce DI actuarial deficit by 0.04 percent of payroll

Could increase in tandem with the NRACould eliminate the Grid entirely, thus eliminating age

consideration20

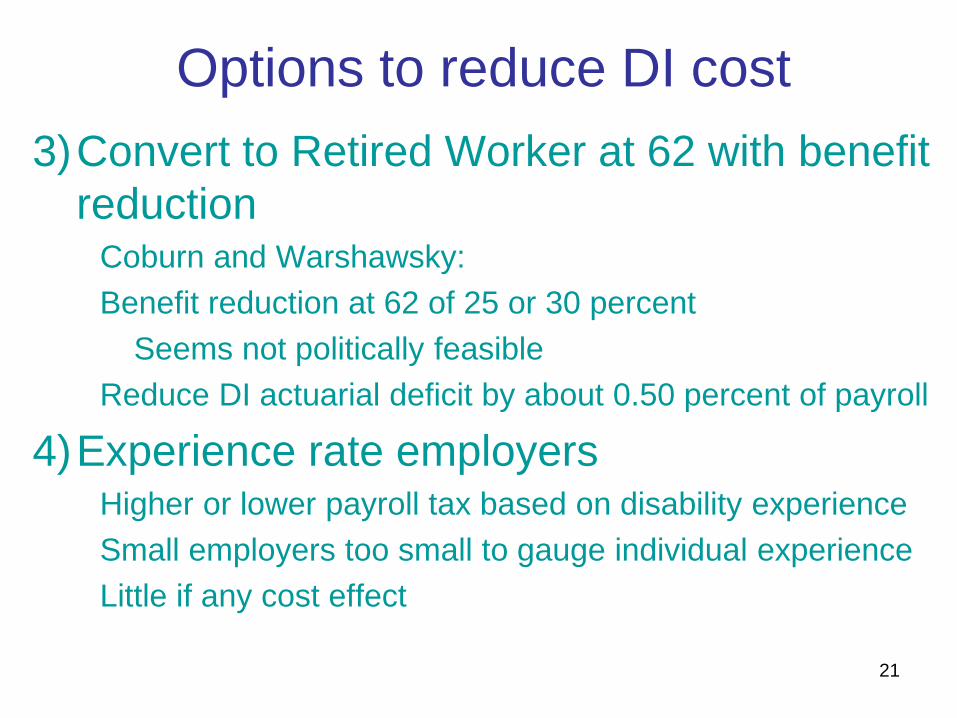

Options to reduce DI cost3)Convert to Retired Worker at 62 with benefit

reductionCoburn and Warshawsky:Benefit reduction at 62 of 25 or 30 percent

Seems not politically feasibleReduce DI actuarial deficit by about 0.50 percent of payroll

4)Experience rate employersHigher or lower payroll tax based on disability experience Small employers too small to gauge individual experienceLittle if any cost effect

21

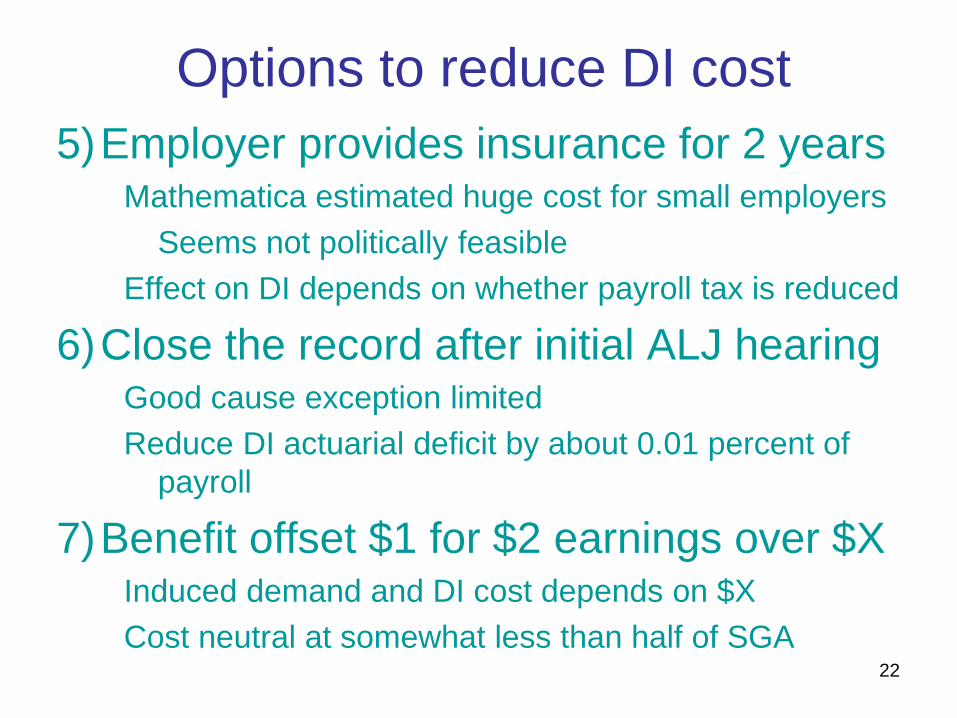

Options to reduce DI cost5)Employer provides insurance for 2 years

Mathematica estimated huge cost for small employersSeems not politically feasible

Effect on DI depends on whether payroll tax is reduced

6)Close the record after initial ALJ hearingGood cause exception limitedReduce DI actuarial deficit by about 0.01 percent of

payroll

7)Benefit offset $1 for $2 earnings over $XInduced demand and DI cost depends on $X Cost neutral at somewhat less than half of SGA

22

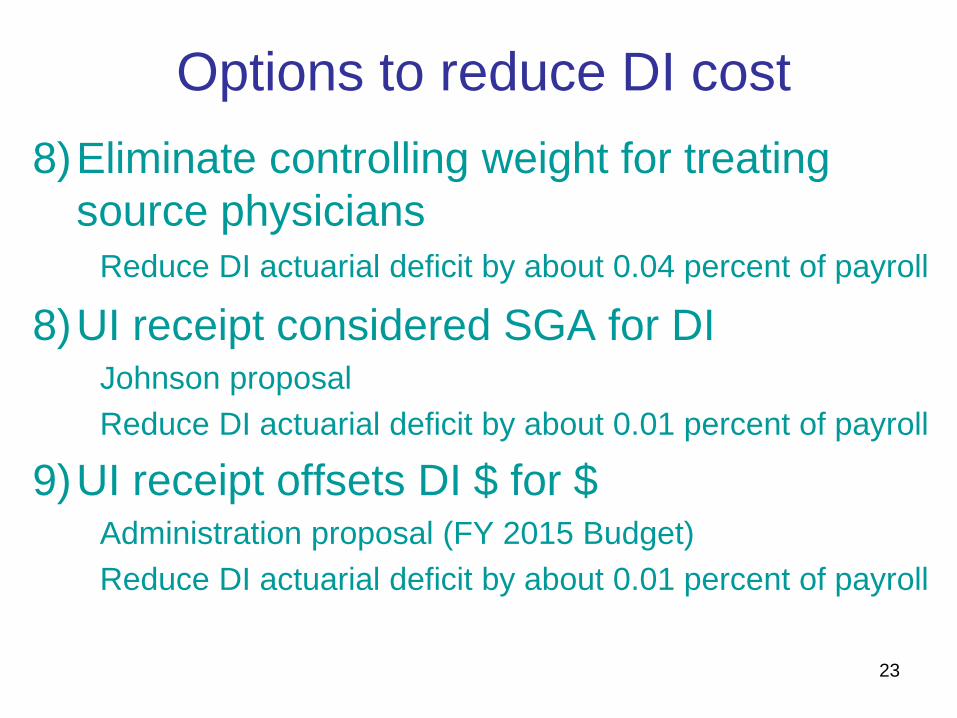

Options to reduce DI cost8)Eliminate controlling weight for treating

source physiciansReduce DI actuarial deficit by about 0.04 percent of payroll

8)UI receipt considered SGA for DIJohnson proposal Reduce DI actuarial deficit by about 0.01 percent of payroll

9)UI receipt offsets DI $ for $Administration proposal (FY 2015 Budget)Reduce DI actuarial deficit by about 0.01 percent of payroll

23

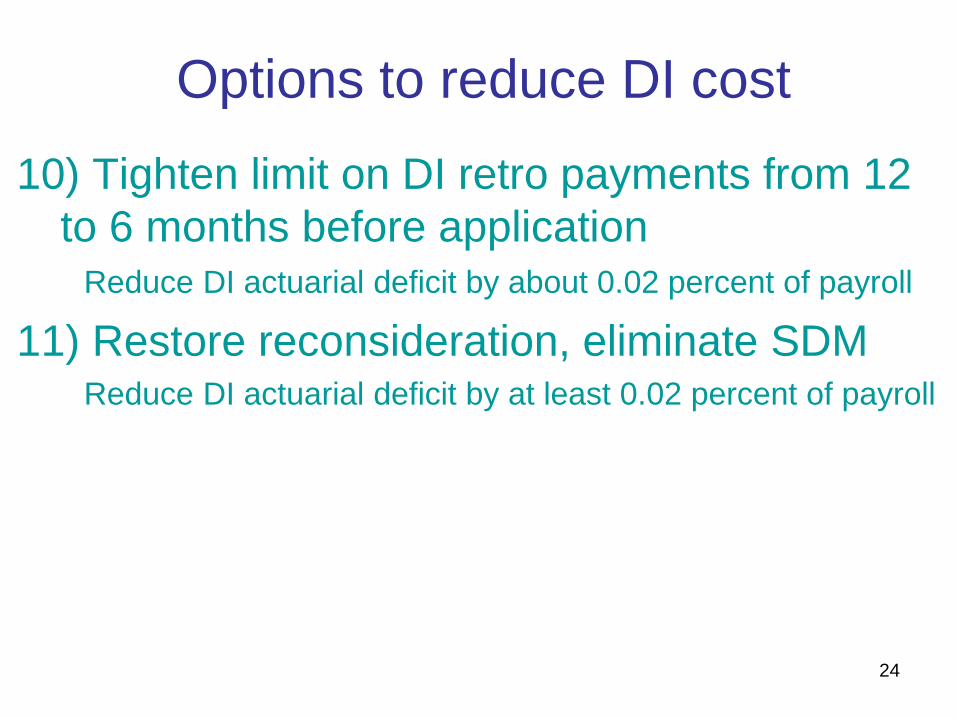

Options to reduce DI cost

10) Tighten limit on DI retro payments from 12 to 6 months before application

Reduce DI actuarial deficit by about 0.02 percent of payroll

11) Restore reconsideration, eliminate SDMReduce DI actuarial deficit by at least 0.02 percent of payroll

24

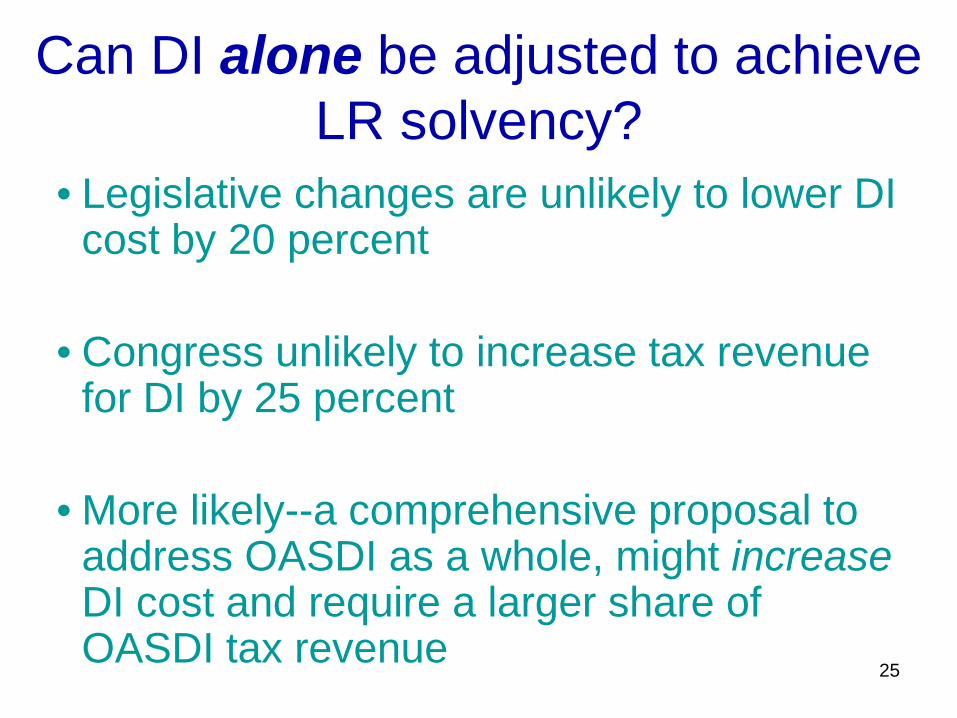

Can DI alone be adjusted to achieve LR solvency?

• Legislative changes are unlikely to lower DI cost by 20 percent

• Congress unlikely to increase tax revenue for DI by 25 percent

• More likely--a comprehensive proposal to address OASDI as a whole, might increaseDI cost and require a larger share of OASDI tax revenue

25

For more information, go tohttp://www.ssa.gov/oact/pubs.html

There you will find—• Current and all prior OASDI Trustees Reports• Detailed single-year tables for recent reports• Our estimates for comprehensive proposals• Our estimates for the individual provisions• Actuarial notes; including replacement rates• Actuarial Studies; including stochastic• Extensive data bases• Congressional testimonies

26

2016 SOA Health Meeting

Doug Vrooman, FSA, MAAA

Private Disability Insurance:Past, Present, and Future

June 15th, 2016

Private Disability Insurance:Past, Present, and Future

2

Risks Covered

• Quality of Life through Income Protection

• More than just “expense” or “indemnity” reimbursement

3

Who Covers These Risks

• Federal Government

• State Government

• Employers

• Private Industry

4

How Does Private Sector Cover Risks

• Employer Benefits• Salary/Bonus

• Major Medical

• 401(K)/Pension

• PTO

• Life Insurance/Supplemental Medical

• Disability

• LTD/STD Coverages that Join with Other Plans• Plenty of Bells and Whistles to Differentiate

5

How Well Does Private Sector Cover Risks• Private insurance covers much more than abject

poverty

• Covers risk well when there is access

• Need access/education/wallet share

6

The Future:Opportunities and Challenges For Private DI

7

Possible Federal Legislation

• The ACA Pathway

• “Medical” -vs- “Disability”

• SSDI Legislation• Budget Act of 2015

• Future Legislation

8

Possible State Legislation

• Disability Insurance positive laws

• Interstate Compact Risk

• Risks• Mental Health Parity

• Offsets

• Pre Ex

• MN Limits

• 2012 GLTD Table

9

Education

• Employers/Employees/Legislators/Regulators

• Different education needed for each group

• Insurance sold not bought

10

Pricing Opportunities and Challenges

• Federal Issues• SSDI

• Budget Act of 2015 extended solvency

• Need significant action

• Impact on Private Industry

• McCrery Pomeroy Solutions

• Fund backed by US Treasuries

• Incidence/Terminations of SSDI after Budget Act

11

Pricing Opportunities and Challenges

• State Issues• PERS/STRS

• Under stress due to Boomer exodus

• Some states have altered plans

• Lower offsets -> Higher prices

12

Changing US Demographics and Attitudes• Baby Boomers

• Longevity Risk

• Increasing diagnoses

• Purchasing behaviors

13

Economy

• Low Interest Rate Environment

• Unemployment Rates

• State Budgets

14

Growth Opportunities

• Worksite is getting crowded

• Wallet Share Issues

• How to capitalize on growth opportunities

• Marketing Platform

15

ACA Impacts

• Competition Increasing in DI

• Part-Time Employees

• Employer Paid –vs- Voluntary

16

![Petrology and Origin of Intrusive Masses of Zaker Located ... · The selected samples of intrusives in the Middlemost (1985) classification [5] diagram is located in monzonite to](https://img.pdfslide.net/doc/110x75/5e8cc449b93b141aed311ca3/petrology-and-origin-of-intrusive-masses-of-zaker-located-the-selected-samples.jpg)