Embed Size (px)

Citation preview

1

Setco Automotive Ltd.Setco Automotive Ltd.Setco Automotive Ltd.Setco Automotive Ltd.

2

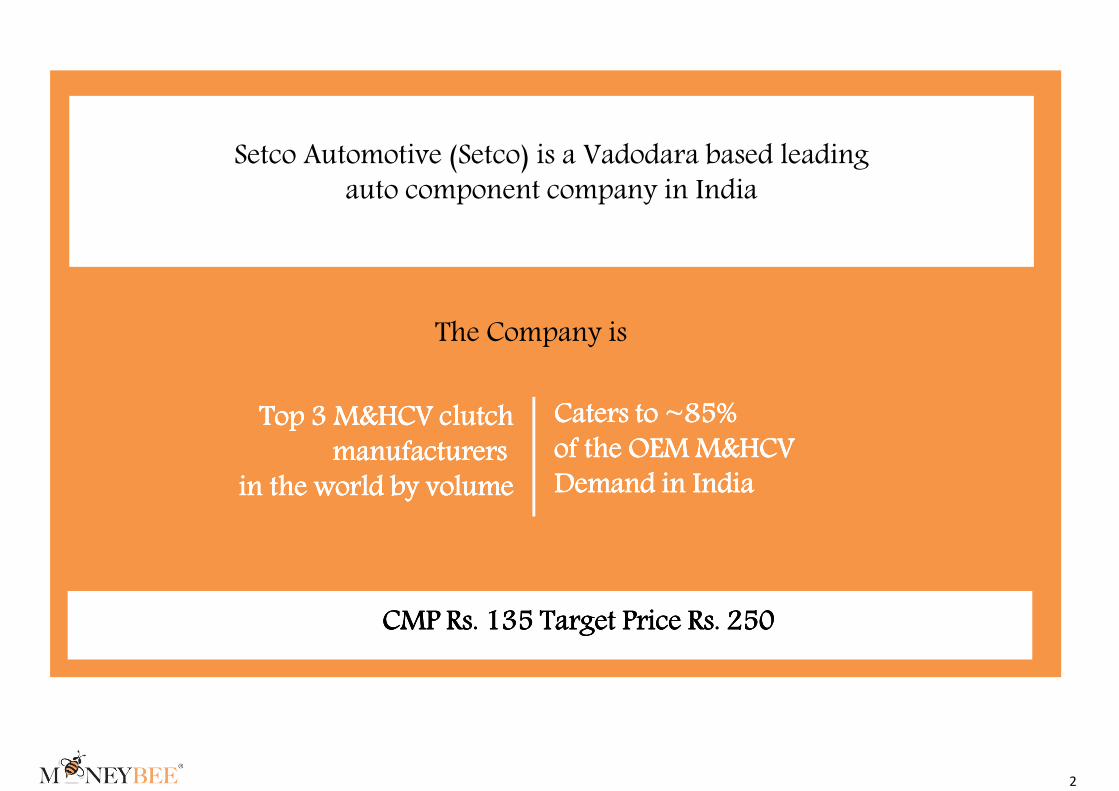

Setco Automotive (Setco) is a Vadodara based leading auto component company in India

The Company is

Top 3 M&HCV clutchTop 3 M&HCV clutchTop 3 M&HCV clutchTop 3 M&HCV clutchmanufacturers manufacturers manufacturers manufacturers

in the world by volumein the world by volumein the world by volumein the world by volume

Caters to ~85% Caters to ~85% Caters to ~85% Caters to ~85% of the OEM M&HCVof the OEM M&HCVof the OEM M&HCVof the OEM M&HCVDemand in IndiaDemand in IndiaDemand in IndiaDemand in India

CMP Rs. 135 Target Price Rs. 250CMP Rs. 135 Target Price Rs. 250CMP Rs. 135 Target Price Rs. 250CMP Rs. 135 Target Price Rs. 250

3

� Expanding Product PortfolioExpanding Product PortfolioExpanding Product PortfolioExpanding Product Portfolio

Entry into LCV which is not adversely affected by economic slowdown & proposed foray into farm equipment sector

� Revival of CV IndustryRevival of CV IndustryRevival of CV IndustryRevival of CV Industry

The CV industry which was in downtrend for the last two years is expected to pick up from this year. Setco by being the market leader in the MHCV space will benefit from this

� Thrust on ExportsThrust on ExportsThrust on ExportsThrust on Exports

Currently Exports contribute 7-8% of sales and the company expects this to grow to 15% in the coming years. The Company has reached a breakthrough level where they will be able to push the new developments along with the diaphragm springs.

� New JVNew JVNew JVNew JV

Recently entered into a JV with Lingotes Especiales S.A and formed Lava Cast Pvt. Ltd. This will manufacture fully machined ferrous casting products and ensure steady and high quality supply for Setco

� Shareholder Shareholder Shareholder Shareholder FriendlyFriendlyFriendlyFriendly

Setco has always rewarded shareholders by way of regular Dividends and Bonus. It announced two bonuses in last 4 years. (1:1 in 2010 and 1:2 in 2012)

� Attractive Valuation: Attractive Valuation: Attractive Valuation: Attractive Valuation:

We are re-initiating coverage on Setco with a target price of Rs. 250, thus giving an upside potential of 85%. We expect the standalone EPS to go up from Rs. 8.7 in FY14 to Rs.10.5 in FY15 and Rs.16.8 in FY16. At the CMP of Rs.135, the stock is presently trading at 12.8x its FY15 and 8.0x its FY16 earnings

Investment Rationale

4

Steady Steady Steady Steady Replacement Replacement Replacement Replacement demanddemanddemanddemand

MHCV clutches need to be changed every 2-2.5 years and this is a high margin business.

Recent foray into Independent After Market (IAM) with 40 distributors pan India is likely to boost sales in the unorganized aftermarket.

Investment Rationale

0000 1111 3333 5555 7777 9999 11111111 13131313YearsYearsYearsYears

Source: company

5

Price Date Price Date Price Date Price Date 21/08/201421/08/201421/08/201421/08/2014 RsRsRsRs

Face Value 10

Market Price 130

Market Cap (Rs. Mn) 3,468

Equity Shares O/S (Mn) 26.7

Book Value (per share) 70.7

52 Week High/Low 147.3/ 61.9

All time High/Low 169.93/ 3.74

P/E Ratio (TTM) 19.02

PromoterPromoterPromoterPromoter

63.01%63.01%63.01%63.01%

FIIFIIFIIFII

16.32%16.32%16.32%16.32%

DIIDIIDIIDII

0.03%0.03%0.03%0.03%

OthersOthersOthersOthers

20.64%20.64%20.64%20.64%

Shareholding Shareholding Shareholding Shareholding PatternPatternPatternPattern

June 2014June 2014June 2014June 2014

We have included PE investment of New Vernon in FIIWe have included PE investment of New Vernon in FIIWe have included PE investment of New Vernon in FIIWe have included PE investment of New Vernon in FII

Market Information

0

2

4

6

8

10

12

14

16

25

45

65

85

105

125

145

165Fe

b-0

8

Ap

r-0

8

Jun

-08

Au

g-0

8

Oct

-08

Dec

-08

Feb-

09

Ap

r-0

9

Jun

-09

Au

g-0

9

Oct

-09

Dec

-09

Feb-

10

Ap

r-1

0

Jun

-10

Au

g-1

0

Oct

-10

Dec

-10

Feb-

11

Ap

r-1

1

Jun

-11

Au

g-1

1

Oct

-11

Dec

-11

Feb-

12

Ap

r-1

2

Jun

-12

Au

g-1

2

Oct

-12

Dec

-12

Feb-

13

Ap

r-1

3

Jun

-13

Au

g-1

3

Oct

-13

Dec

-13

Feb-

14

Ap

r-1

4

Jun

-14

Au

g-1

4

Setco TTM PE(x)

6

�Among the top three M&HCV clutch manufacturers in the world by volume

It is the preferred supplier for clutches in India both by domestic & MNC players like Daimler and MAN

� Commands ~85% of the OEM M&HCV clutch market

~100% requirement of Tata Motors, Eicher Volvo & AMW~65% demand of Ashok Leyland

� Controls major share of the Organised Replacement Market through OES and Own Distribution networks

� Enjoys a strategic global presence and sells its clutches under , a world renowned brand

Business Overview

7

OEMOEMOEMOEM

(29.8%)(29.8%)(29.8%)(29.8%)

OE After Sales OE After Sales OE After Sales OE After Sales

(OES)(OES)(OES)(OES)

(53.3%)(53.3%)(53.3%)(53.3%)

Independent Independent Independent Independent

After MarketAfter MarketAfter MarketAfter Market

(IAM) (IAM) (IAM) (IAM)

(8.5%)(8.5%)(8.5%)(8.5%)

ExportsExportsExportsExports

(8.4%)(8.4%)(8.4%)(8.4%)

Standalone Segmental Revenue (FY14)Standalone Segmental Revenue (FY14)Standalone Segmental Revenue (FY14)Standalone Segmental Revenue (FY14)

(Rs. Mn)

#IAM was started in H2FY14

OEM OEM OEM OEM

981981981981

OES OES OES OES

1,7511,7511,7511,751

IAM IAM IAM IAM

280280280280

Exports Exports Exports Exports

276276276276

Business Overview – Sales Breakup

8

Global Clientele

9

Product

Range

Clutch Cover

Assembly

Push Type

Diaphragm

TypeCoil Type

Pull Type

Diaphragm

TypeCoil Type

Clutch Disc

Assembly

Organic Lining Ceramic Lining

� Only clutch manufacturer in the world to design & manufacture both coil spring & diaphragm spring both coil spring & diaphragm spring both coil spring & diaphragm spring both coil spring & diaphragm spring � Both types validated and approved by OEM vehicle manufacturers

Product Range

10

17/430 SingleDiaphragm Spring

280 MM Single Diaphragm Spring

16/400 TwinDiaphragm Spring

395 Single PushDiaphragm Spring

Off-Highway, ConstructionHydraulics (Pressure Converters)

14/352 Single & TwinDirect Pressure Coil Spring

170 MM Single Diaphragm Spring

12/310 SingleDiaphragm Spring

13/330 SingleDirect Pressure Coil Spring

380 Single PushCoil Spring

15/380 Single & TwinDirect Pressure Coil Spring

Technical Capabilities

11

SegmentsSegmentsSegmentsSegments 2010201020102010 2014201420142014 RemarksRemarksRemarksRemarks

Heavy CV Y Y Dominant Player

Medium CV Y Y Dominant Player

Light CV N Y Recent Entry

OEM Y Y Dominant Player

OES Y Y Dominant Player

IAM N Y Recent Entry

Farm Equipment Sector N N Proposed Entry

REMAN N N Plans for near future

Enhanced Product Offerings

12

Design & TechnologyDesign & TechnologyDesign & TechnologyDesign & Technology

(Updated with the latest (Updated with the latest (Updated with the latest (Updated with the latest

technological changes)technological changes)technological changes)technological changes)

Cost Cost Cost Cost

CompetitiveCompetitiveCompetitiveCompetitive

(Priced far (Priced far (Priced far (Priced far

lower than lower than lower than lower than

MNC players)MNC players)MNC players)MNC players)

Delivery & TimelinessDelivery & TimelinessDelivery & TimelinessDelivery & Timeliness

(preferred supplier of Top (preferred supplier of Top (preferred supplier of Top (preferred supplier of Top

OEMs)OEMs)OEMs)OEMs)

QualityQualityQualityQuality---- Latest Latest Latest Latest

CertificationsCertificationsCertificationsCertifications

((((ISO/TS 16949ISO/TS 16949ISO/TS 16949ISO/TS 16949

VDA VDA VDA VDA –––– 6.36.36.36.3

ISO 14001ISO 14001ISO 14001ISO 14001

OHSAS 18001OHSAS 18001OHSAS 18001OHSAS 18001)

Valeo,LuK,

Eaton,Sachs

Valeo,LuK,

Eaton,Sachs

Competitive Scenario

13

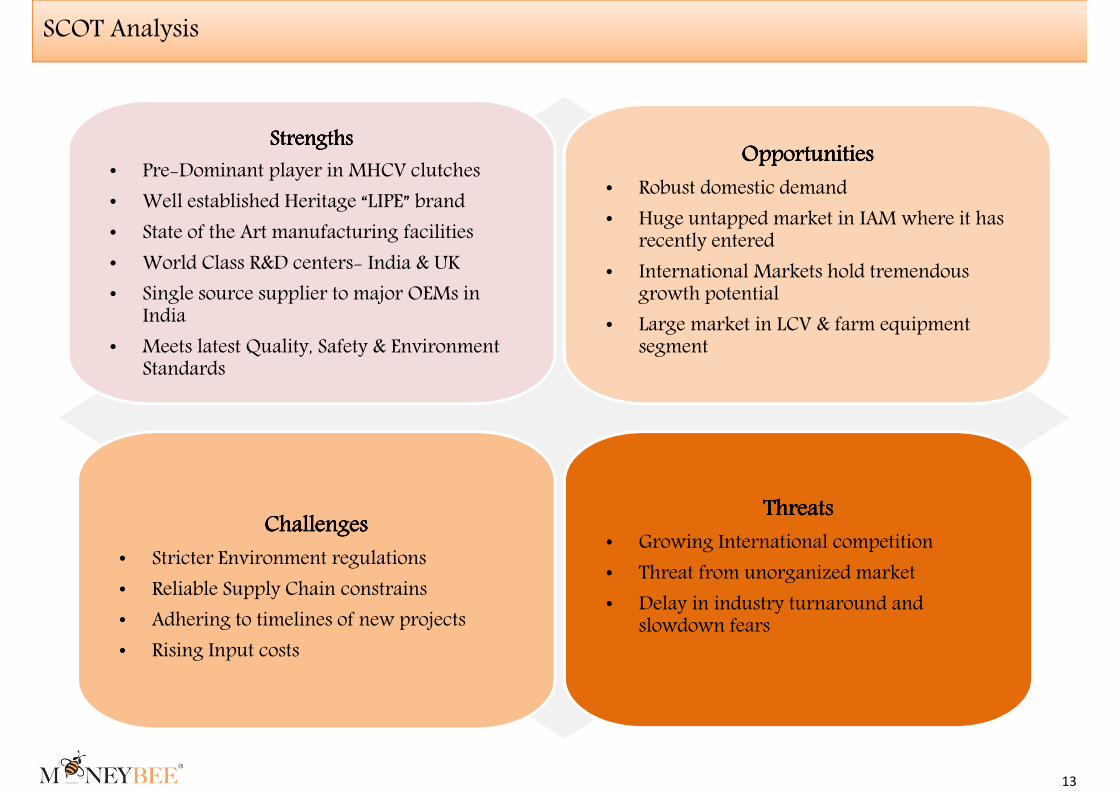

StrengthsStrengthsStrengthsStrengths

• Pre-Dominant player in MHCV clutches

• Well established Heritage “LIPE” brand

• State of the Art manufacturing facilities

• World Class R&D centers- India & UK

• Single source supplier to major OEMs in India

• Meets latest Quality, Safety & Environment Standards

OpportunitiesOpportunitiesOpportunitiesOpportunities

• Robust domestic demand

• Huge untapped market in IAM where it has recently entered

• International Markets hold tremendous growth potential

• Large market in LCV & farm equipment segment

ChallengesChallengesChallengesChallenges

• Stricter Environment regulations

• Reliable Supply Chain constrains

• Adhering to timelines of new projects

• Rising Input costs

Threats Threats Threats Threats

• Growing International competition

• Threat from unorganized market

• Delay in industry turnaround and slowdown fears

SCOT Analysis

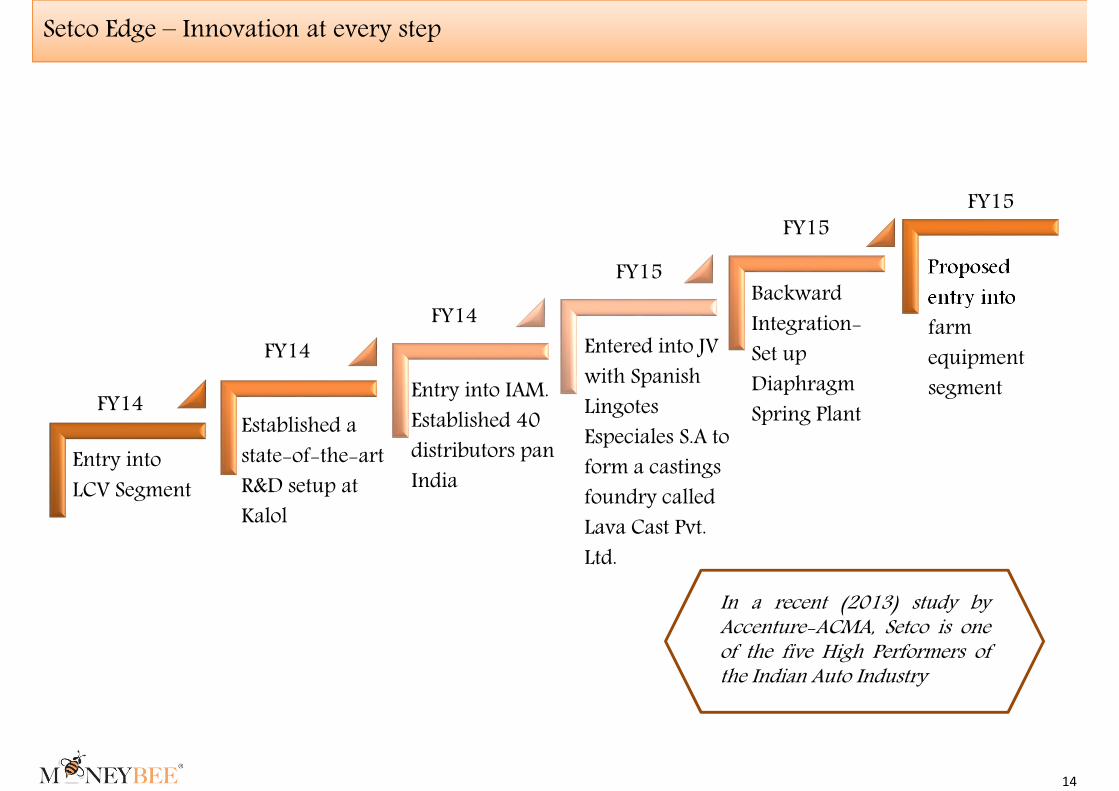

14

Entry into

LCV Segment

Established a

state-of-the-art

R&D setup at

Kalol

Proposed

entry into

farm

equipment

segmentEntry into IAM.

Established 40

distributors pan

India

Entered into JV

with Spanish

Lingotes

Especiales S.A to

form a castings

foundry called

Lava Cast Pvt.

Ltd.

Backward

Integration-

Set up

Diaphragm

Spring Plant FY14

FY14

FY14

FY15

FY15FY15

In a recent (2013) study byAccenture-ACMA, Setco is oneof the five High Performers ofthe Indian Auto Industry

Setco Edge – Innovation at every step

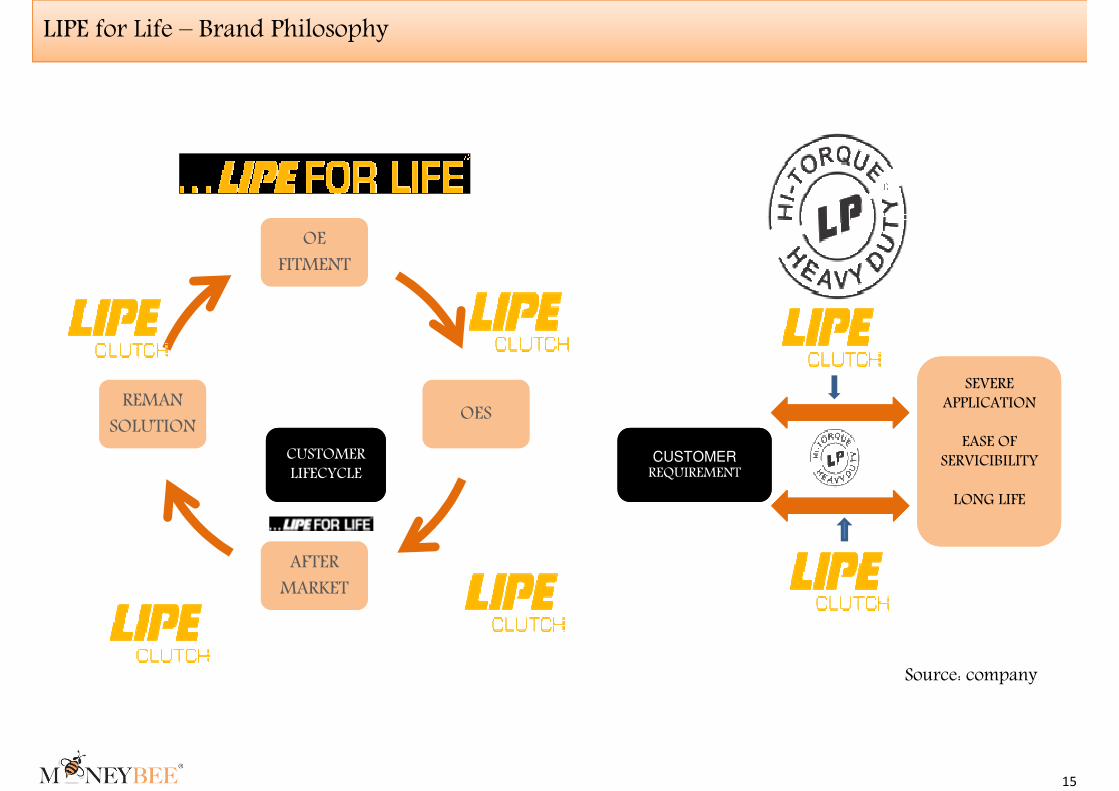

15

OE

FITMENT

OES

AFTER

MARKET

REMAN

SOLUTION

CUSTOMER LIFECYCLECUSTOMER LIFECYCLE

CUSTOMER

REQUIREMENTCUSTOMER

REQUIREMENT

SEVERE APPLICATION

EASE OF SERVICIBILITY

LONG LIFE

SEVERE APPLICATION

EASE OF SERVICIBILITY

LONG LIFE

Source: company

LIPE for Life – Brand Philosophy

16

Indian Automotive IndustryIndian Automotive IndustryIndian Automotive IndustryIndian Automotive Industry

17

� The Indian automotive industry offers great potential considering the low penetration along with rising income levels and a rapidly growing middle class

� The Indian and Chinese markets make up nearly half of the world`s truck demand and India ranks 7th in CV production

� India is amongst the most competitive auto component manufacturers in the world and this industry has the potential to reach $85 bn by 2015 and $113 bn by 2020

� Domestic market is projected to grow at 8-10% per annum in the next 10 years

� Exports projected to grow at over 20-30% per annum

� The growth expected in the domestic automobile industry will give a fillip to the auto component industry

� De-regulation and the Government’s policy initiatives have facilitated growth and focus has now shifted towards attracting foreign direct investments

� Road development is a priority sector for India and the investment in road sector during the 12th five year plan is projected at 20% of the total investment of USD 1tn which will give a boost to demand for vehicles and indirectly auto components

Industry Facts

18

TwoTwoTwoTwo----wheelers wheelers wheelers wheelers

Mopeds

Scooters

Motorcycles

Electric two-

wheelers

Passenger vehicles Passenger vehicles Passenger vehicles Passenger vehicles

Passenger cars

Utility vehicles

Multi-purpose

vehicles

Commercial Commercial Commercial Commercial

vehicles vehicles vehicles vehicles

Light commercial

vehicles

Medium and heavy

commercial vehicles

Farm Equipment

ThreeThreeThreeThree----wheelers wheelers wheelers wheelers

Passenger

carriers

Goods

carriers

Automotive Automotive Automotive Automotive SegmentSegmentSegmentSegment

Source: IBEF

Industry Overview

19Source: SIAM

549549549549 417417417417 568568568568761761761761

929929929929 832832832832630630630630 687687687687

1,4201,4201,4201,420

2,3502,3502,3502,350

2007-082007-082007-082007-08 2008-092008-092008-092008-09 2009-102009-102009-102009-10 2010-112010-112010-112010-11 2011-122011-122011-122011-12 2012-132012-132012-132012-13 2013-142013-142013-142013-14 2014-15E2014-15E2014-15E2014-15E 2015-16E2015-16E2015-16E2015-16E 2020-21E2020-21E2020-21E2020-21E

Growth in the number of units Commercial Growth in the number of units Commercial Growth in the number of units Commercial Growth in the number of units Commercial VehiclesVehiclesVehiclesVehicles (in’000)

275275275275

184184184184245245245245

323323323323 348348348348

269269269269201201201201 213213213213216216216216 201201201201

288288288288362362362362

461461461461524524524524

432432432432 458458458458

2007-082007-082007-082007-08 2008-092008-092008-092008-09 2009-102009-102009-102009-10 2010-112010-112010-112010-11 2011-122011-122011-122011-12 2012-132012-132012-132012-13 2013-142013-142013-142013-14 2014-15E2014-15E2014-15E2014-15E

MHCVMHCVMHCVMHCV LCVLCVLCVLCV

(in’000)

Industry Trend

20

Wabco (9)Wabco (9)Wabco (9)Wabco (9) Bosch (10)Bosch (10)Bosch (10)Bosch (10) MothersonMothersonMothersonMotherson

SumiSumiSumiSumi

Systems (14)Systems (14)Systems (14)Systems (14)

LumaxLumaxLumaxLumax

IndustriesIndustriesIndustriesIndustries

(15)(15)(15)(15)

ZF SteeringZF SteeringZF SteeringZF Steering

(20)(20)(20)(20)

ExideExideExideExide

IndustriesIndustriesIndustriesIndustries

(23)(23)(23)(23)

Setco (28)Setco (28)Setco (28)Setco (28)

53.7253.7253.7253.72

44.3944.3944.3944.3939.639.639.639.6 38.6638.6638.6638.66

28.5628.5628.5628.5623.3923.3923.3923.39

19.3819.3819.3819.38

TTM PETTM PETTM PETTM PE

Wabco (3)Wabco (3)Wabco (3)Wabco (3) Bosch (6)Bosch (6)Bosch (6)Bosch (6) ExideExideExideExide

IndustriesIndustriesIndustriesIndustries

(18)(18)(18)(18)

ZF SteeringZF SteeringZF SteeringZF Steering

(19)(19)(19)(19)

MothersonMothersonMothersonMotherson

SumiSumiSumiSumi

Systems (26)Systems (26)Systems (26)Systems (26)

Setco (29)Setco (29)Setco (29)Setco (29) LumaxLumaxLumaxLumax

IndustriesIndustriesIndustriesIndustries

(71)(71)(71)(71)

6.036.036.036.03

4.764.764.764.76

1.531.531.531.53 1.381.381.381.38 1111 0.940.940.940.940.270.270.270.27

Mkt Cap/ SalesMkt Cap/ SalesMkt Cap/ SalesMkt Cap/ Sales

Mcap/ Sales ratio Mcap/ Sales ratio Mcap/ Sales ratio Mcap/ Sales ratio of 1.5 will ensure of 1.5 will ensure of 1.5 will ensure of 1.5 will ensure entry into top 20 entry into top 20 entry into top 20 entry into top 20 companiescompaniescompaniescompanies

Industry Positioning

21

Setco is able to manage the increase in input costs and pass on the differential to its end clients

Presence in the OEM & Aftermarket acts as a natural hedge against

cyclical fluctuations of economy

Stays ahead of the Technological shifts through its R&D centers in

India & UK and is well equipped to meet new norms well in time

It is the preferred supplier to major OEMs with an established brand

name “LIPE”

VUCA in Setco

VVVVolatility olatility olatility olatility in in in in

Input Input Input Input CostsCostsCostsCosts

UUUUncertaintyncertaintyncertaintyncertaintyabout macro about macro about macro about macro

economic factorseconomic factorseconomic factorseconomic factors

CCCComplexity omplexity omplexity omplexity related to tech related to tech related to tech related to tech

changes, changes, changes, changes, regulatory shiftsregulatory shiftsregulatory shiftsregulatory shifts

AAAAmbiguity about mbiguity about mbiguity about mbiguity about customer customer customer customer

preferencespreferencespreferencespreferences

22

The Black boundary depicts Setco’s presence

Five Axes

Value Chain

Geography

Adjacent Industries

Automobile Sector

Key Customers

After SalesService

Manufacturing

IAM OESOEM

Manufacturing & Sales abroad

Exports India

Aerospace & Defense

Power

2/3 Wheeler & Cars

Utility Vehicles

CVs

Farm Equipment

Construction Equipment

Railways

REMAN

Training

R & D

Value ChainSetco present in entire Value Chain from Manufacturing to After Sales Service

GeographyPresent in all 3 geographies & focusing on increasing Manufacturing & sales abroad

Adjacent IndustryNo plans to enter adjacent industries but may explore option in distant future

Automobile SectorPlans to foray into tractors this year. No plans to enter Passenger segment

Key CustomersCaters to entire Life Cycle with recent foray into IAM. Future plans to enter REMAN as well

23

� Harish Sheth – Founder, Chairman & Managing Director

� Udit Sheth – Executive Director

� Shvetal Vakil – Executive Director

� Ronobir Kumar Ghosh- Director - Technical

� Niraj Kumar Mittal – Chief Operating Officer

� A. V. Srinivas – Vice President - Manufacturing

� Jatinder Singh Gujral – Vice President - Commercial

� Vinay Shahane – Asst. Vice President – Finance

� Hans Gramberger – Director - International Marketing (Europe)

� Steve Haworth – Executive Director (Setco United Kingdom)

� Rajiv Iyer – Vice President (Setco North America)

Global Leadership Team

24

Setco Setco Setco Setco KalolKalolKalolKalol Complex, GujaratComplex, GujaratComplex, GujaratComplex, Gujarat Setco Haslingden, Lancashire, UKSetco Haslingden, Lancashire, UKSetco Haslingden, Lancashire, UKSetco Haslingden, Lancashire, UK

Setco, Sitarganj, UttarakhandSetco, Sitarganj, UttarakhandSetco, Sitarganj, UttarakhandSetco, Sitarganj, Uttarakhand Setco Paris, TN, USASetco Paris, TN, USASetco Paris, TN, USASetco Paris, TN, USA

Global Manufacturing Presence

25

Road Ahead…Road Ahead…Road Ahead…Road Ahead…

Cross Rs. 10 Cross Rs. 10 Cross Rs. 10 Cross Rs. 10 bnbnbnbn turnover by FY turnover by FY turnover by FY turnover by FY 2017201720172017----18 on consolidated basis18 on consolidated basis18 on consolidated basis18 on consolidated basis

26

� CV Industry (Source: SIAM)CV Industry (Source: SIAM)CV Industry (Source: SIAM)CV Industry (Source: SIAM)

CV industry is poised to grow on the back of recovery in the Indian economy and revival in the industrial and mining sectors

CV industry is likely to grow at 7-9% in FY15 and register a CAGR of 16% during FY2013–20

� MHCV IndustryMHCV IndustryMHCV IndustryMHCV Industry

Domestic OEM sales to pick up from mid-FY15E with a sharp recovery in M&HCVs (volume growth of ~25-30%). Also the replacement cycle is expected to pick up pace

� LCV IndustryLCV IndustryLCV IndustryLCV Industry

LCVs are estimated to grow 4-7% in FY15

� Tractor Industry (Source: ICRA)Tractor Industry (Source: ICRA)Tractor Industry (Source: ICRA)Tractor Industry (Source: ICRA)

Tractor industry expected to grow by 4-6% in FY15 and of 8-9% in sales by volume for the tractor industry over the next five year

Driven by Industry growth

27

The recent JV of Setco’s subsidiary with Lingotes, Especiales – Spain to manufacture fully machined castingsWill cater to Setco’s Captive Consumption and additional Capacity will cater to outside customers

Lava Cast ProjectLava Cast ProjectLava Cast ProjectLava Cast Project

Plans to go for Backward IntegrationThis critical raw material is currently being imported from Europe and will help bring technology in India , control Quality and help reduce cost

Diaphragm Spring PlantDiaphragm Spring PlantDiaphragm Spring PlantDiaphragm Spring Plant

Up-gradation and modernization of plant to help capacity buildingExpansion in Expansion in Expansion in Expansion in KalolKalolKalolKalol & & & & UttarakhandUttarakhandUttarakhandUttarakhand plantsplantsplantsplants

In order to stay ahead of technology and offer world class products to customers in India and globallyInvestment in R& DInvestment in R& DInvestment in R& DInvestment in R& D

Exploring the vast opportunity in Remanufacturing market which is a high margin business

REMANREMANREMANREMAN

Driven by Expansion

Capex of

Rs. 2,790 M [FY 13 – 15]

28

ParticularsParticularsParticularsParticulars 2012201220122012----13 A 13 A 13 A 13 A 2013201320132013----14 A 14 A 14 A 14 A 2014201420142014----15 P 15 P 15 P 15 P 2015201520152015----16 P 16 P 16 P 16 P 2016201620162016----17 P 17 P 17 P 17 P 2017201720172017----18 P 18 P 18 P 18 P

Sales 3,408 3,287 4,776 5,823 7,002 8,554Raw material Cost 2,050 1,988 2,852 3,465 4,159 5,081Other Expenses 611 653 835 961 1,120 1,369Personnel exp 269 305 407 437 525 599EBITDA 478 342 683 961 1,197 1,506Other Income 85 132 81 80 100 100Depreciation 92 105 149 168 172 175Interest 174 202 281 321 290 259Tax 64 63 86 143 217 304Extraordinary Item 0 77 0 0 0 0

PAT 273 232 281 448 619 867EPS 10.3 8.7 10.5 16.8 23.2 32.5

EBITDA (M) 14.0% 10.4% 14.3% 16.5% 17.1% 17.6%PAT (M) 8.0% 7.1% 5.9% 7.7% 8.8% 10.1%

Financial Snapshot

Standalone Profit and Loss StatementRs in Mn

29

Dhiren Shah, MD

M. Com, LL. B, FCA, Grad CWA

dir: +91 22 4030 2001 m: +91 98337 70404

Moneshi Shah, Partner

B. Com, ACA

dir: +91 22 4030 2005 m: +91 98337 70402

1. This Report is prepared on the basis of the sources of information provided by the management of the Company. We have not independently verified any of the information so provided.2. We assume no responsibility for the accuracy and completeness of information presented in this Report and will not be held liable for it under any circumstances. We have not made an appraisal or

independent valuation of any of the assets or liabilities of the Company and have not conducted an audit, or due diligence, or reviewed/ validated the projections/ financial data provided by the Management. We have relied on the judgment of the Management and auditors of the respective companies in understanding the contingency nature of liabilities; accordingly our valuation does not consider the assumption of contingency liabilities materializing.

3. Our analysis is based on the market conditions and the regulatory environment that currently exists. However, changes to the same in the future could impact the Company and the industry it operates in which may impact our valuation analysis.

4. For our analysis, we have relied on published and secondary sources of data, whether or not made available by the Company. We have not independently verified the accuracy or timelines of the same.5. Neither Moneybee nor any of its affiliates are responsible for updating this Report because of events or transactions occurring subsequent to the date of this Report. Any updates or second opinions on

this Report cannot be sought by the Management from external agencies including other offices of Moneybee without its prior written permission

Ipshita Roy, Sr. Associate

CFA, MS(Finance)

dir: +91 22 4030 2052 m: +91 99876 57415

Moneybee Advisors Pvt Ltd

303, Tower A, Peninsula Business Park, G. K. Marg,

Lower Parel (W), Mumbai 400 013

b: +91 22 4030 2010 f: +91 22 4030 2000

e: [email protected] w: www.moneybee.in

skype: moneybee.advisors tweet:@MoneybeeAdvisor

blog: moneybeeadvisors.com

facebook: MoneybeeAdvisors linkedin: Moneybee Group

Contact

21st August 2014