Embed Size (px)

Citation preview

Sheila NordonIrish Charities Tax Research Ltd

6th April 2009

In Ireland there is no specific legal form for a Foundation

Public benefit or Philanthropic Foundations generally set up as Charities

The legal form that a charity can take is not prescribed in law – can be incorporated (company limited by guarantee), a trust, unincorporated association, co-operative etc.

Charitable status depends on having charitable purposes and being for public benefit – all purposes must be charitable and all resources applied solely for charitable purposes

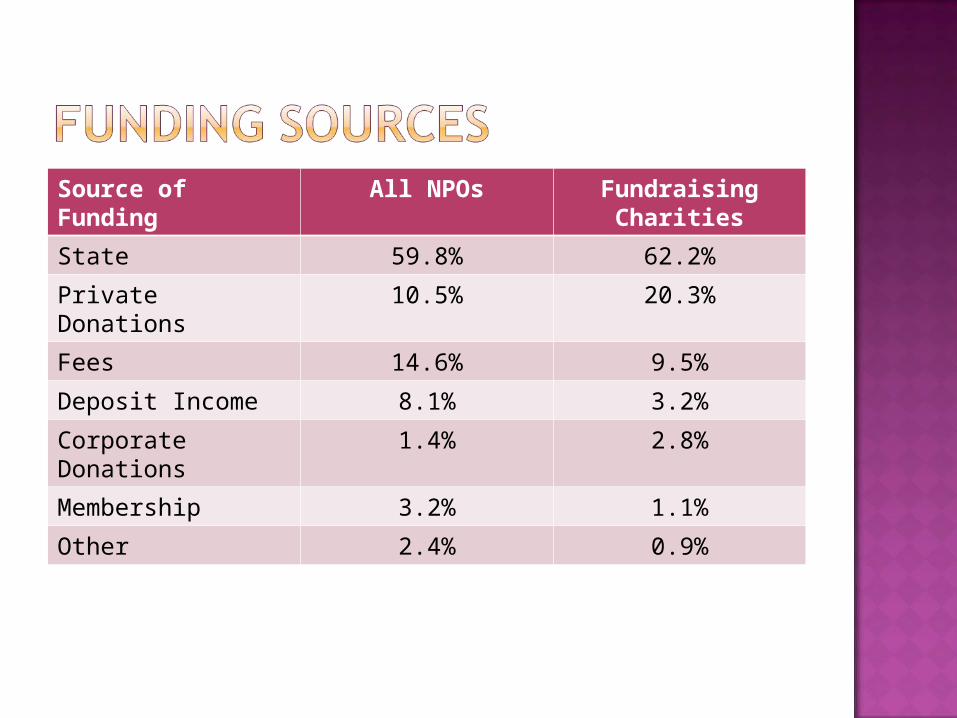

Source of Funding

All NPOs Fundraising Charities

State 59.8% 62.2%

Private Donations 10.5% 20.3%

Fees 14.6% 9.5%

Deposit Income 8.1% 3.2%

Corporate Donations

1.4% 2.8%

Membership 3.2% 1.1%

Other 2.4% 0.9%

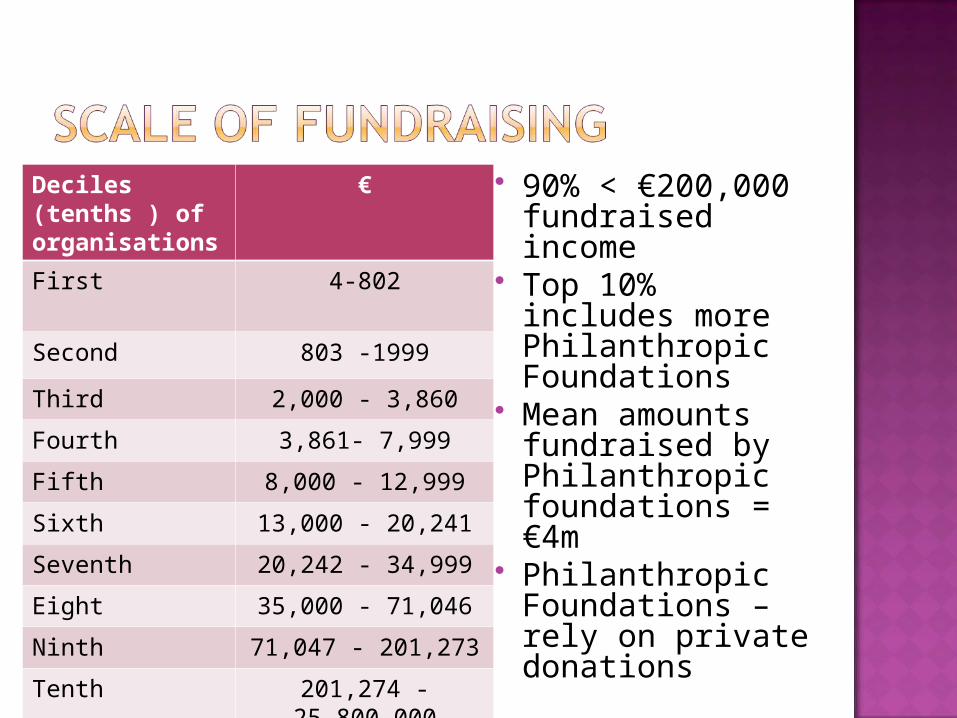

Deciles (tenths ) of organisations

€

First 4-802

Second 803 -1999

Third 2,000 - 3,860

Fourth 3,861- 7,999

Fifth 8,000 - 12,999

Sixth 13,000 - 20,241

Seventh 20,242 - 34,999

Eight 35,000 - 71,046

Ninth 71,047 - 201,273

Tenth 201,274 - 25,800,000

90% < €200,000 fundraised income

Top 10% includes more Philanthropic Foundations

Mean amounts fundraised by Philanthropic foundations = €4m

Philanthropic Foundations – rely on private donations

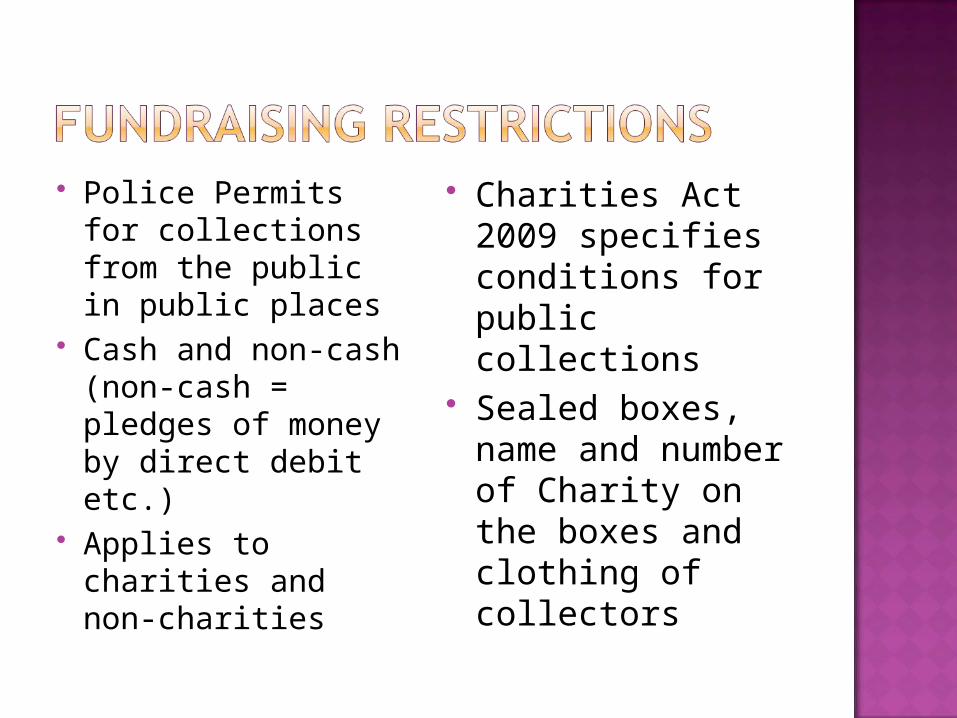

Police Permits for collections from the public in public places

Cash and non-cash (non-cash = pledges of money by direct debit etc.)

Applies to charities and non-charities

Charities Act 2009 specifies conditions for public collections

Sealed boxes, name and number of Charity on the boxes and clothing of collectors

Allowed if directly in support of charitable purpose (no special legal requirements except for tax exemption)

Trading Tax Exemption more restricted than charitable tax exemption

Trade must be a primary purpose OR ancillary to the primary purpose of the charity

Non primary purpose trading activity if small relative to overall trading may qualify or if only 10% of turnover of the primary trade

Charity Shops – selling donated goods

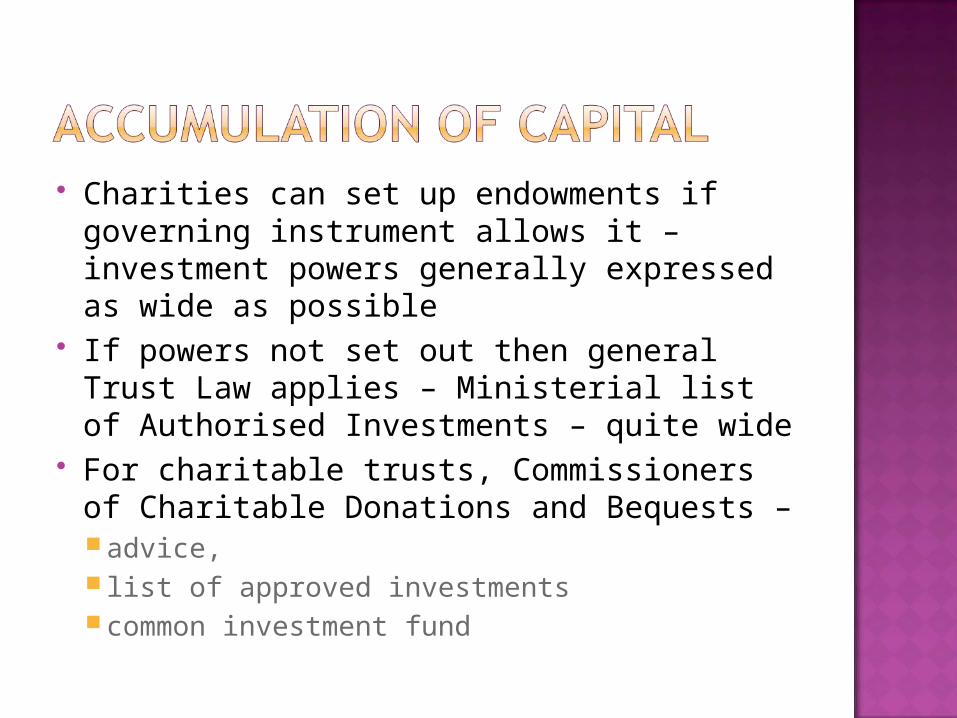

Charities can set up endowments if governing instrument allows it – investment powers generally expressed as wide as possible

If powers not set out then general Trust Law applies – Ministerial list of Authorised Investments – quite wide

For charitable trusts, Commissioners of Charitable Donations and Bequests – advice, list of approved investments common investment fund

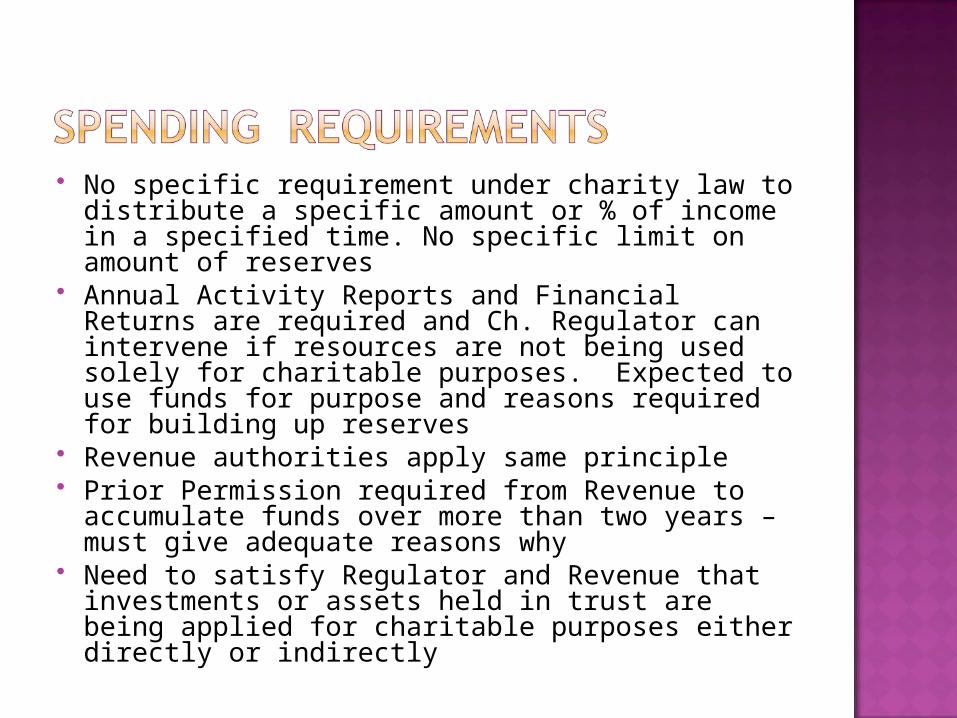

No specific requirement under charity law to distribute a specific amount or % of income in a specified time. No specific limit on amount of reserves

Annual Activity Reports and Financial Returns are required and Ch. Regulator can intervene if resources are not being used solely for charitable purposes. Expected to use funds for purpose and reasons required for building up reserves

Revenue authorities apply same principle Prior Permission required from Revenue to

accumulate funds over more than two years – must give adequate reasons why

Need to satisfy Regulator and Revenue that investments or assets held in trust are being applied for charitable purposes either directly or indirectly

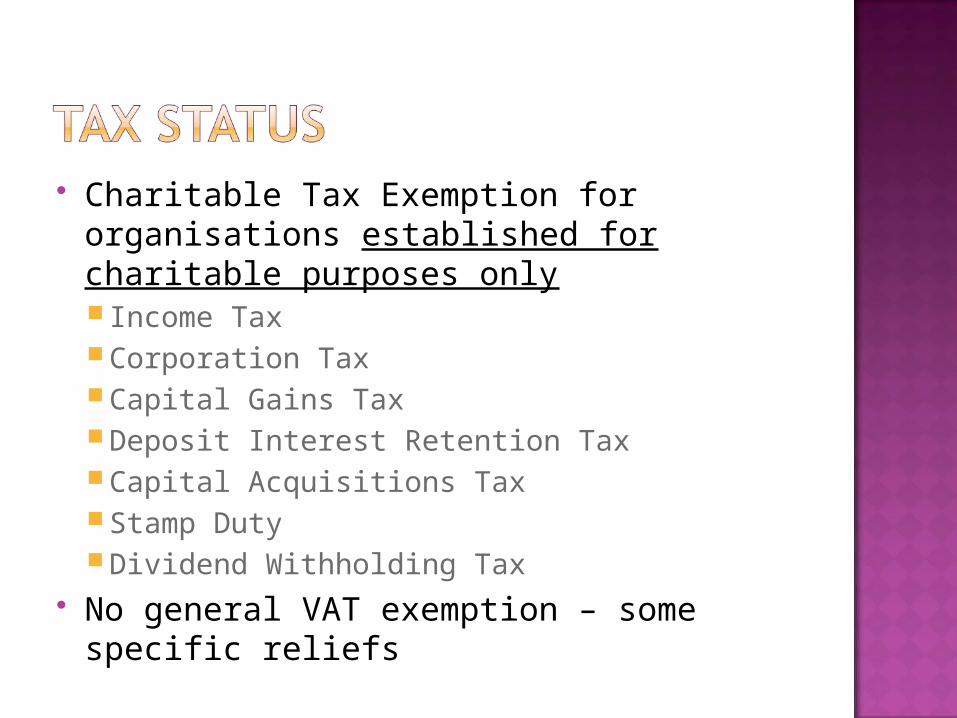

Charitable Tax Exemption for organisations established for charitable purposes only Income Tax Corporation Tax Capital Gains Tax Deposit Interest Retention Tax Capital Acquisitions Tax Stamp Duty Dividend Withholding Tax

No general VAT exemption – some specific reliefs

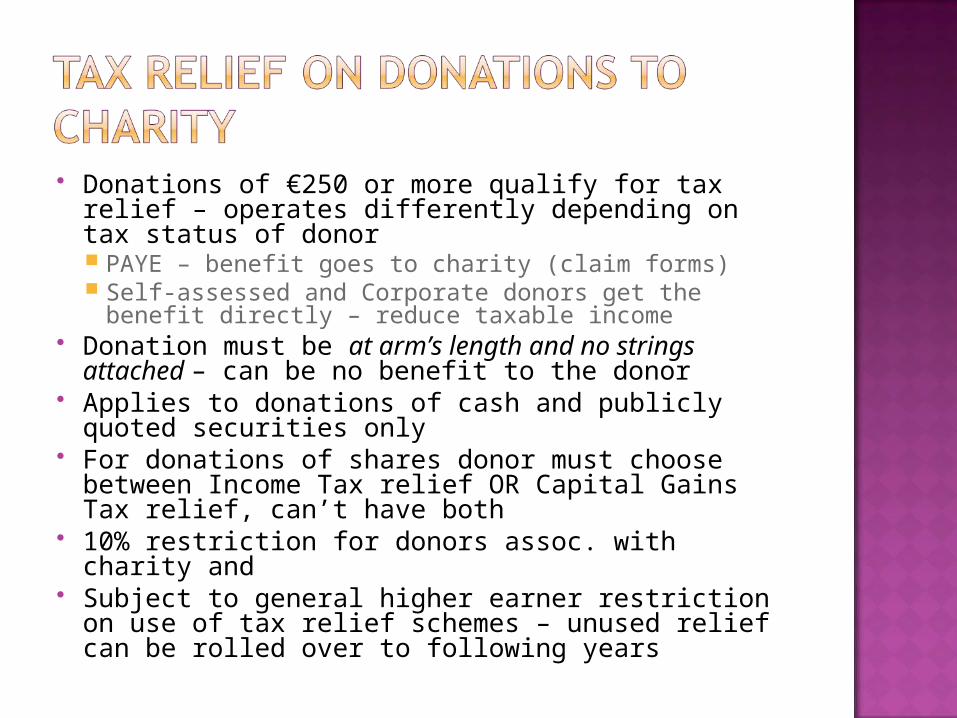

Donations of €250 or more qualify for tax relief – operates differently depending on tax status of donor PAYE – benefit goes to charity (claim forms) Self-assessed and Corporate donors get the benefit

directly – reduce taxable income Donation must be at arm’s length and no strings

attached – can be no benefit to the donor Applies to donations of cash and publicly quoted

securities only For donations of shares donor must choose

between Income Tax relief OR Capital Gains Tax relief, can’t have both

10% restriction for donors assoc. with charity and Subject to general higher earner restriction on use

of tax relief schemes – unused relief can be rolled over to following years