Embed Size (px)

Citation preview

ECOC – Cannes, September 22, 2014

Silicon Photonics and

Skorpios’ Technology Platform

Market Watch

ECOC – Cannes - September 22, 2014

A. Viglienzoni

ECOC – Cannes, September 22, 2014

Agenda

• Preamble

• Need for Photonics and Integrated Optics

• Why Current Models Cannot Deliver on Promises

• Why CMOS Photonics

• Why Skorpios Delivers on The Promises of Silicon Photonics

• Conclusions

2

ECOC – Cannes, September 22, 2014

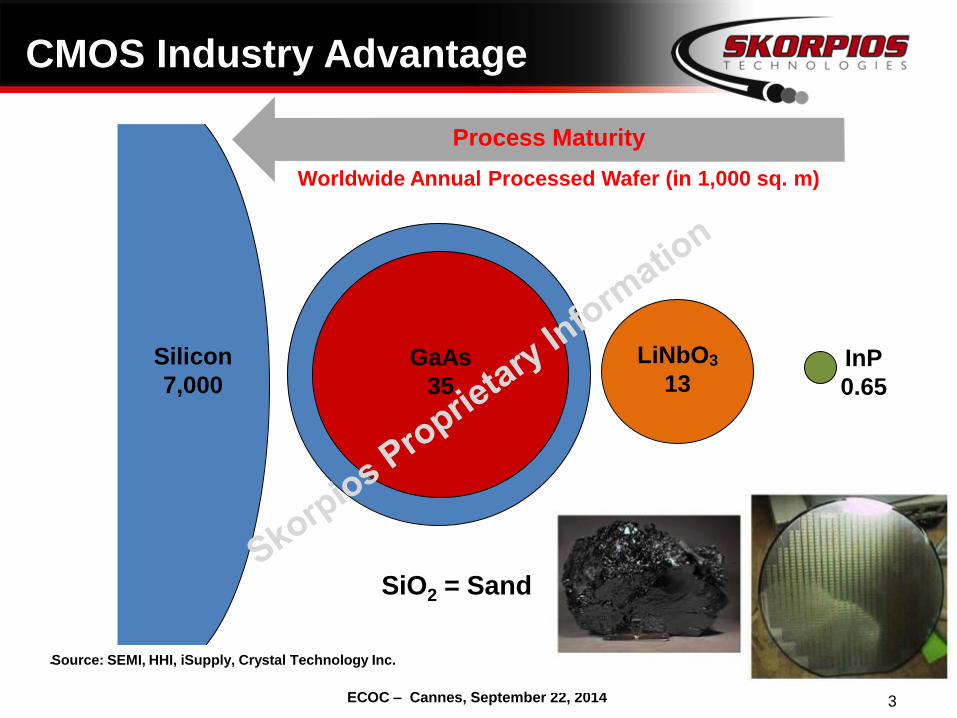

SiO2 = Sand

3

Silicon

7,000

.

Silicon

7,000

Process Maturity

Worldwide Annual Processed Wafer (in 1,000 sq. m)

Source: SEMI, HHI, iSupply, Crystal Technology Inc.

GaAs

35

LiNbO3

13 InP

0.65

CMOS Industry Advantage

ECOC – Cannes, September 22, 2014

©

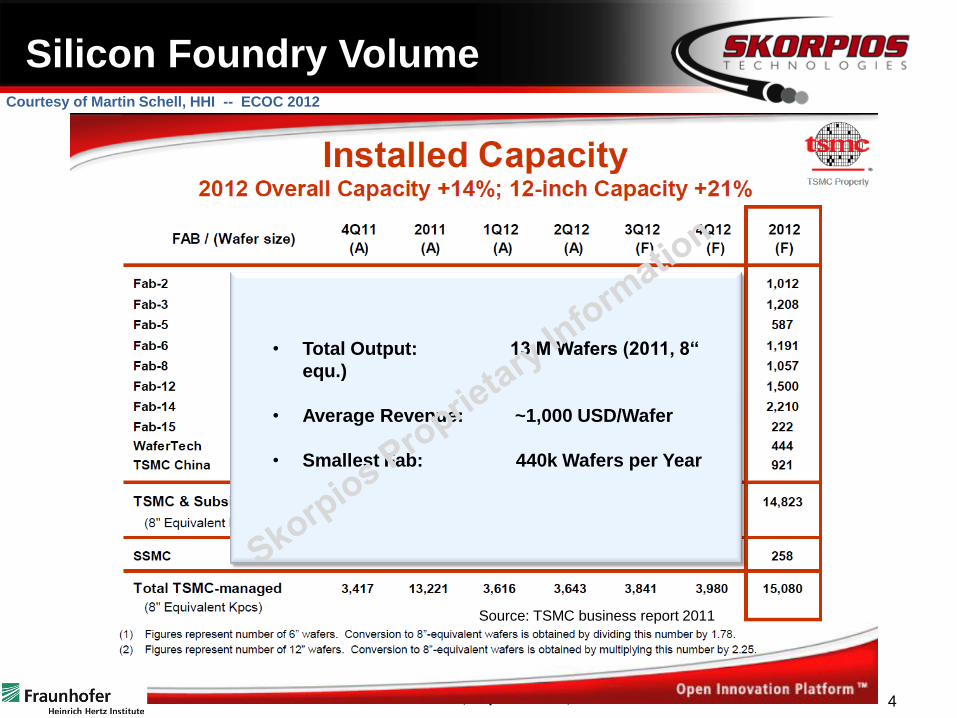

• Total Output: 13 M Wafers (2011, 8“

equ.)

• Average Revenue: ~1,000 USD/Wafer

• Smallest Fab: 440k Wafers per Year

Source: TSMC business report 2011

Courtesy of Martin Schell, HHI -- ECOC 2012

Silicon Foundry Volume

4

ECOC – Cannes, September 22, 2014

©

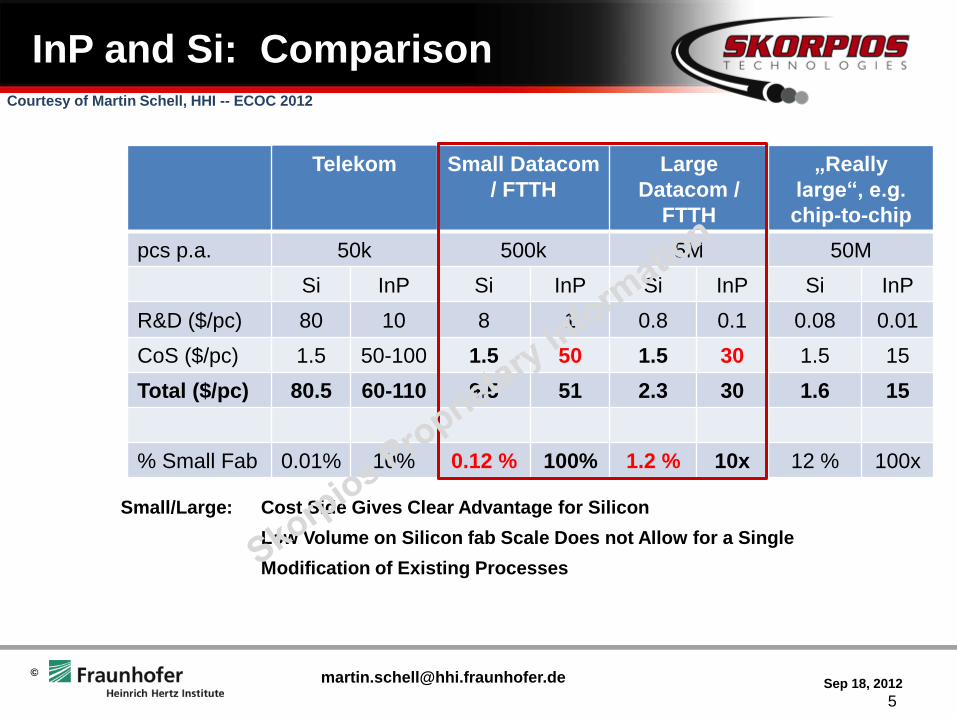

Telekom Small Datacom

/ FTTH

Large

Datacom /

FTTH

„Really

large“, e.g.

chip-to-chip

pcs p.a. 50k 500k 5M 50M

Si InP Si InP Si InP Si InP

R&D ($/pc) 80 10 8 1 0.8 0.1 0.08 0.01

CoS ($/pc) 1.5 50-100 1.5 50 1.5 30 1.5 15

Total ($/pc) 80.5 60-110 9.5 51 2.3 30 1.6 15

% Small Fab 0.01% 10% 0.12 % 100% 1.2 % 10x 12 % 100x

Small/Large: Cost Side Gives Clear Advantage for Silicon

Low Volume on Silicon fab Scale Does not Allow for a Single

Modification of Existing Processes

Sep 18, 2012 [email protected]

Courtesy of Martin Schell, HHI -- ECOC 2012

InP and Si: Comparison

5

ECOC – Cannes, September 22, 2014

Photonics: Major Impact On Our Lives

6

Optical Coherence Tomography Metrology: Compact

Frequency-Comb Generator

Readout units for fiber sensors

Skin Analysis

Smart Lighting

Systems

Fiber Systems: Telecom, Datacom, …. Avionics

NG Sensors

ECOC – Cannes, September 22, 2014

Enable NG Consumer Applications

7

ECOC – Cannes, September 22, 2014

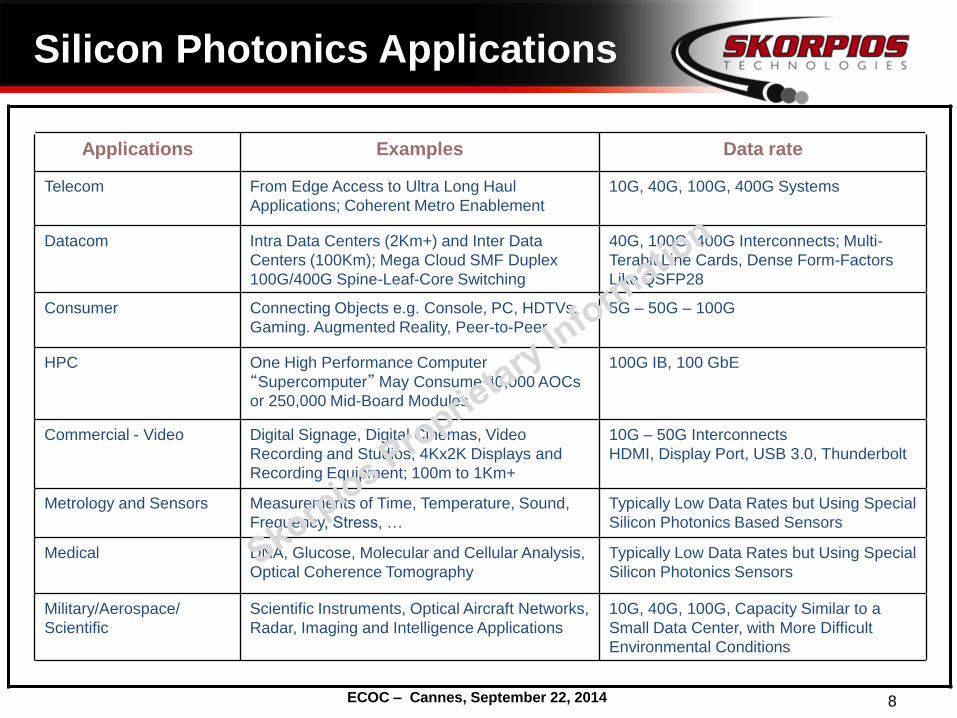

Applications Examples Data rate

Telecom From Edge Access to Ultra Long Haul

Applications; Coherent Metro Enablement

10G, 40G, 100G, 400G Systems

Datacom Intra Data Centers (2Km+) and Inter Data

Centers (100Km); Mega Cloud SMF Duplex

100G/400G Spine-Leaf-Core Switching

40G, 100G, 400G Interconnects; Multi-

Terabit Line Cards, Dense Form-Factors

Like QSFP28

Consumer Connecting Objects e.g. Console, PC, HDTVs.

Gaming. Augmented Reality, Peer-to-Peer

5G – 50G – 100G

HPC One High Performance Computer

“Supercomputer” May Consume 40,000 AOCs

or 250,000 Mid-Board Modules

100G IB, 100 GbE

Commercial - Video Digital Signage, Digital Cinemas, Video

Recording and Studios; 4Kx2K Displays and

Recording Equipment; 100m to 1Km+

10G – 50G Interconnects

HDMI, Display Port, USB 3.0, Thunderbolt

Metrology and Sensors Measurements of Time, Temperature, Sound,

Frequency, Stress, …

Typically Low Data Rates but Using Special

Silicon Photonics Based Sensors

Medical DNA, Glucose, Molecular and Cellular Analysis,

Optical Coherence Tomography

Typically Low Data Rates but Using Special

Silicon Photonics Sensors

Military/Aerospace/

Scientific

Scientific Instruments, Optical Aircraft Networks,

Radar, Imaging and Intelligence Applications

10G, 40G, 100G, Capacity Similar to a

Small Data Center, with More Difficult

Environmental Conditions

Silicon Photonics Applications

8

ECOC – Cannes, September 22, 2014 9

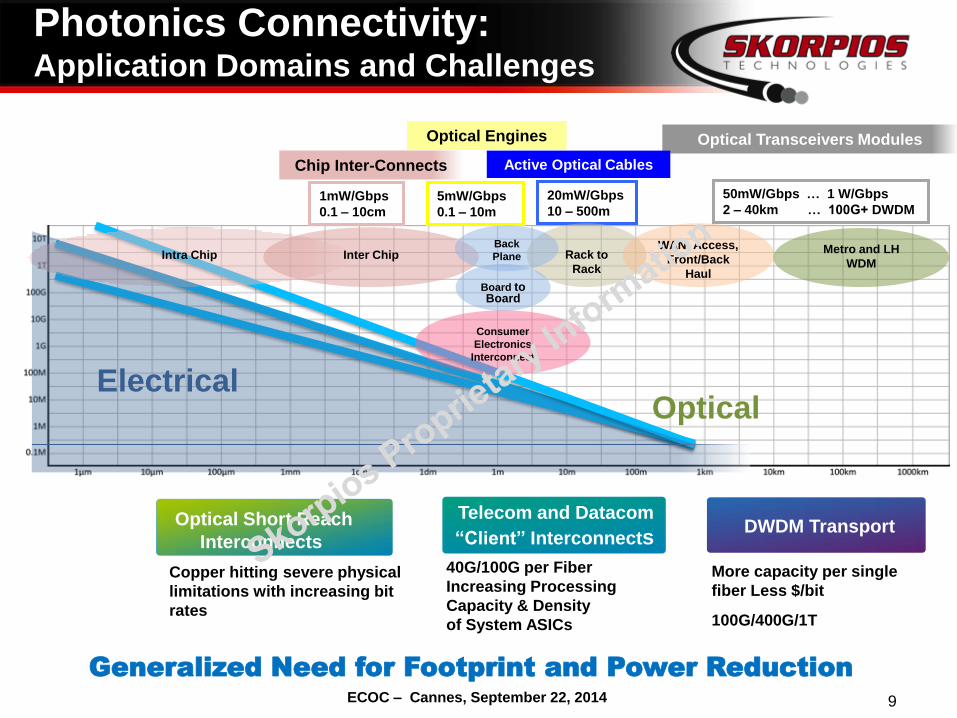

Photonics Connectivity: Application Domains and Challenges

DWDM Transport

More capacity per single

fiber Less $/bit

100G/400G/1T

Telecom and Datacom

“Client” Interconnects

40G/100G per Fiber

Increasing Processing

Capacity & Density

of System ASICs

Optical Short Reach

Interconnects

Copper hitting severe physical

limitations with increasing bit

rates

Generalized Need for Footprint and Power Reduction

Optical Transceivers Modules

Active Optical Cables

Optical Engines

Chip Inter-Connects

1mW/Gbps

0.1 – 10cm

5mW/Gbps

0.1 – 10m

20mW/Gbps

10 – 500m

50mW/Gbps … 1 W/Gbps

2 – 40km … 100G+ DWDM

Optical

Metro and LH

WDM

Rack to

Rack

WAN, Access,

Front/Back

Haul

Board to Board

Intra Chip

Inter Chip Back

Plane

Consumer

Electronics

Interconnect

Electrical

ECOC – Cannes, September 22, 2014

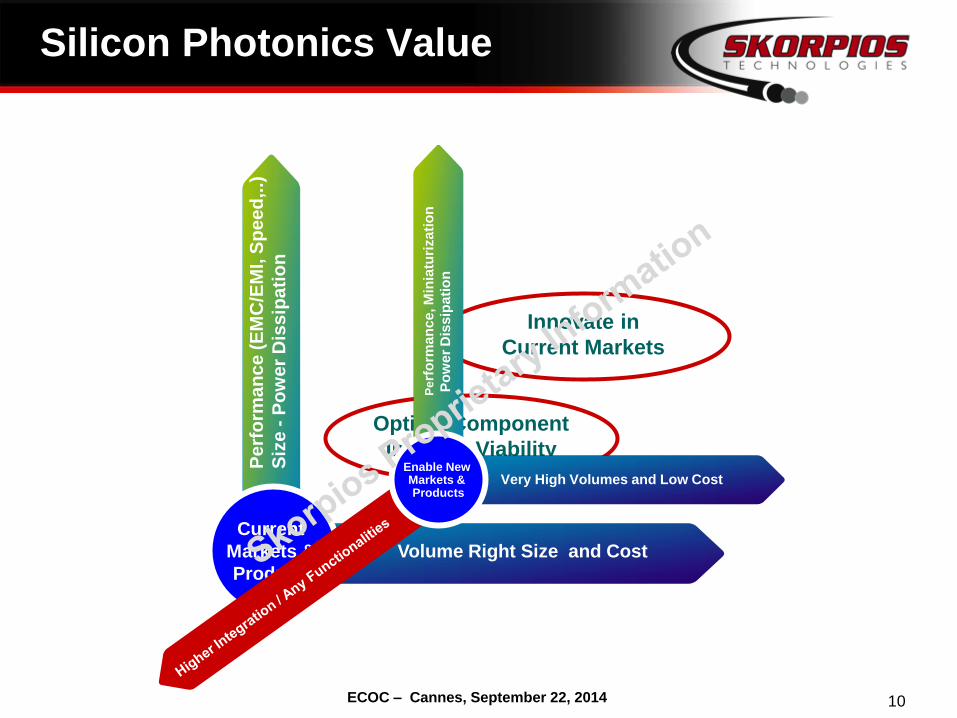

Silicon Photonics Value

Volume Right Size and Cost

Current

Markets &

Products

Pe

rfo

rma

nc

e (

EM

C/E

MI, S

pe

ed

,..)

Siz

e -

Po

we

r D

iss

ipa

tio

n

Innovate in

Current Markets

Optical Component

Industry Viability

Very High Volumes and Low Cost Enable New Markets & Products

Perf

orm

an

ce

, M

inia

turi

za

tio

n

Po

we

r D

iss

ipa

tio

n

10

ECOC – Cannes, September 22, 2014

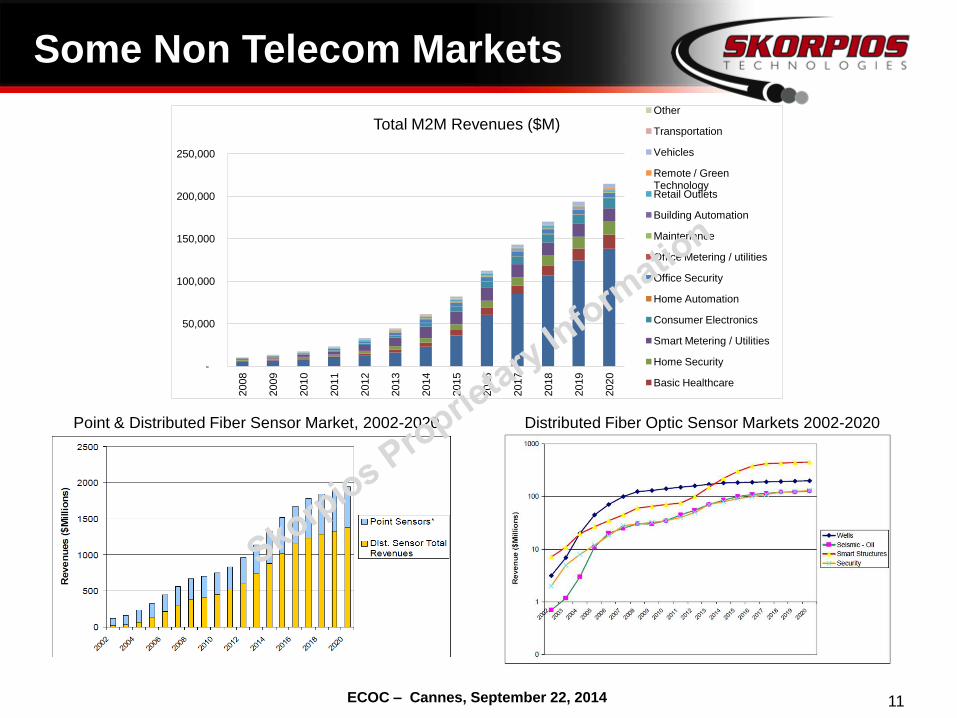

Some Non Telecom Markets

11

-

50,000

100,000

150,000

200,000

250,000

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Total M2M Revenues ($M) Other

Transportation

Vehicles

Remote / Green Technology Retail Outlets

Building Automation

Maintenance

Office Metering / utilities

Office Security

Home Automation

Consumer Electronics

Smart Metering / Utilities

Home Security

Basic Healthcare

Point & Distributed Fiber Sensor Market, 2002-2020 Distributed Fiber Optic Sensor Markets 2002-2020

ECOC – Cannes, September 22, 2014

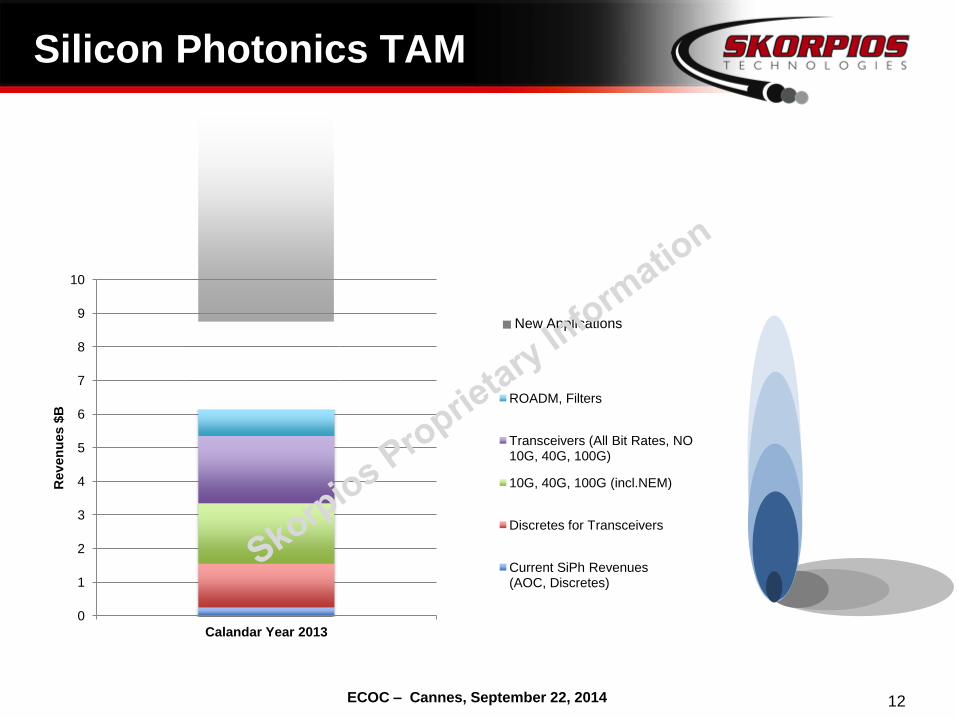

New Applications

Silicon Photonics TAM

0

1

2

3

4

5

6

7

8

9

10

Calandar Year 2013

Rev

en

ues $

B

Non Telco Applications

ROADM, Filters

Transceivers (All Bit Rates, NO 10G, 40G, 100G)

10G, 40G, 100G (incl.NEM)

Discretes for Transceivers

Current SiPh Revenues (AOC, Discretes)

12

ECOC – Cannes, September 22, 2014

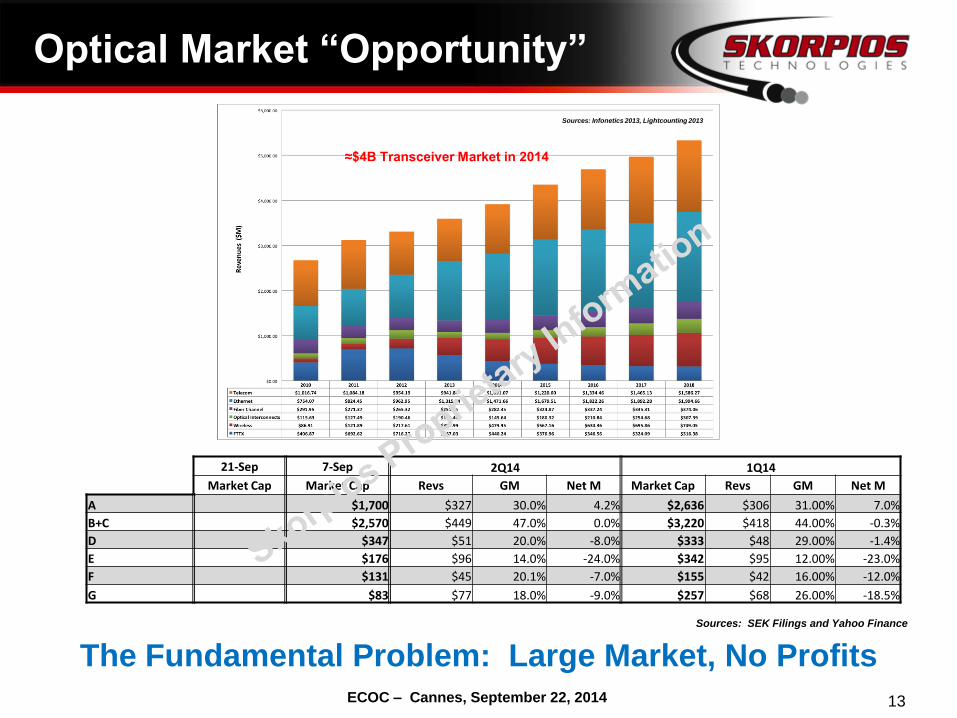

Optical Market “Opportunity”

13

Sources: SEK Filings and Yahoo Finance

The Fundamental Problem: Large Market, No Profits

Sources: Infonetics 2013, Lightcounting 2013

≈$4B Transceiver Market in 2014

21-Sep 7-Sep 2Q14 1Q14

Market Cap Market Cap Revs GM Net M Market Cap Revs GM Net M

A $1,700 $327 30.0% 4.2% $2,636 $306 31.00% 7.0%

B+C $2,570 $449 47.0% 0.0% $3,220 $418 44.00% -0.3%

D $347 $51 20.0% -8.0% $333 $48 29.00% -1.4%

E $176 $96 14.0% -24.0% $342 $95 12.00% -23.0%

F $131 $45 20.1% -7.0% $155 $42 16.00% -12.0%

G $83 $77 18.0% -9.0% $257 $68 26.00% -18.5%

ECOC – Cannes, September 22, 2014

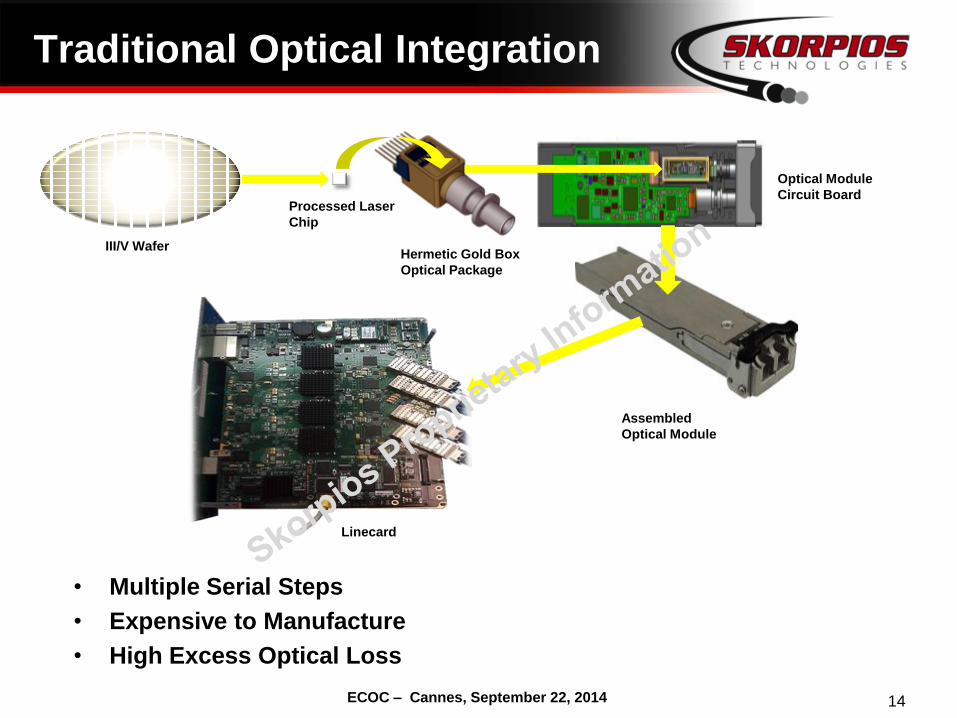

Traditional Optical Integration

14

III/V Wafer Hermetic Gold Box

Optical Package

Processed Laser

Chip

Optical Module

Circuit Board

Assembled

Optical Module

Linecard

• Multiple Serial Steps

• Expensive to Manufacture

• High Excess Optical Loss

ECOC – Cannes, September 22, 2014

Hermetic Gold Box

Optical Package

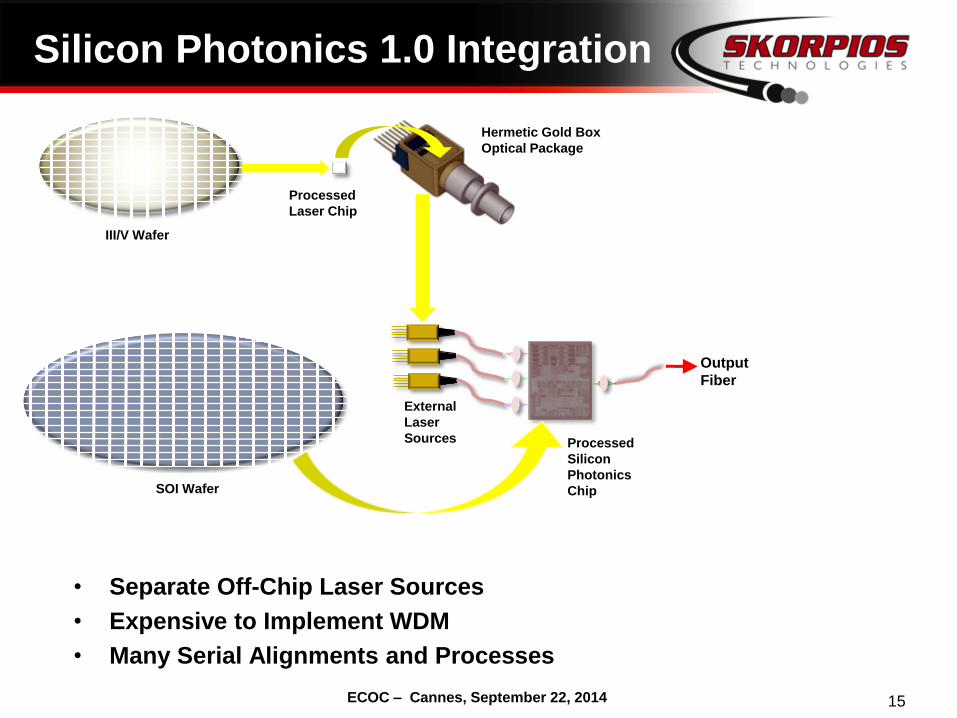

Silicon Photonics 1.0 Integration

15

III/V Wafer

SOI Wafer

Processed

Laser Chip

Processed

Silicon

Photonics

Chip

External

Laser

Sources

Output

Fiber

• Separate Off-Chip Laser Sources

• Expensive to Implement WDM

• Many Serial Alignments and Processes

ECOC – Cannes, September 22, 2014

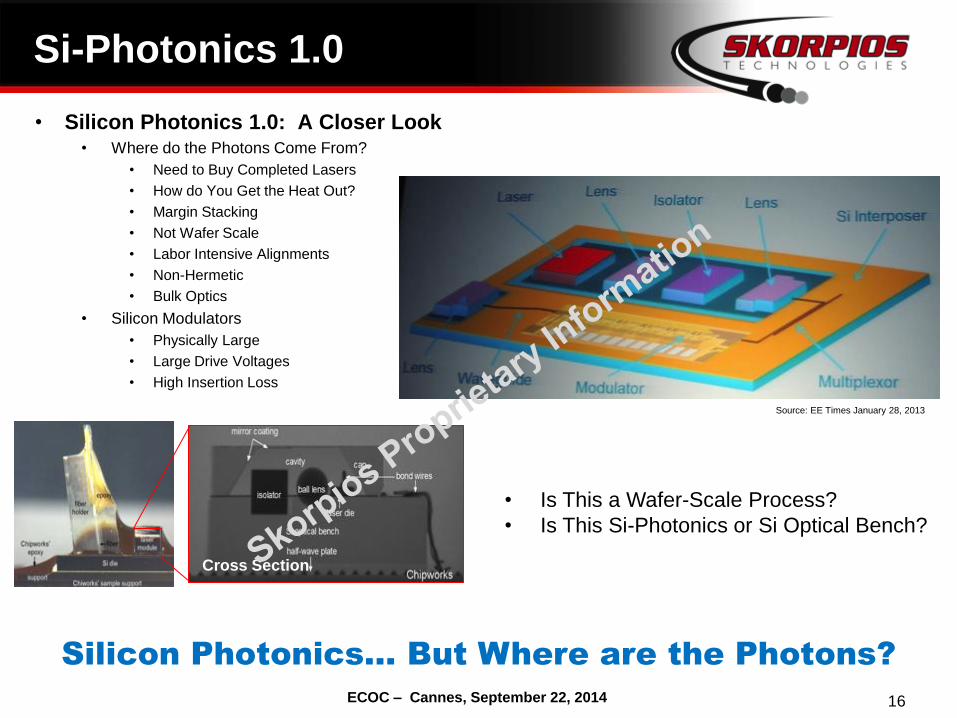

• Silicon Photonics 1.0: A Closer Look • Where do the Photons Come From?

• Need to Buy Completed Lasers

• How do You Get the Heat Out?

• Margin Stacking

• Not Wafer Scale

• Labor Intensive Alignments

• Non-Hermetic

• Bulk Optics

• Silicon Modulators

• Physically Large

• Large Drive Voltages

• High Insertion Loss

Si-Photonics 1.0

• Is This a Wafer-Scale Process?

• Is This Si-Photonics or Si Optical Bench?

Source: EE Times January 28, 2013

16

Cross Section

Silicon Photonics… But Where are the Photons?

ECOC – Cannes, September 22, 2014

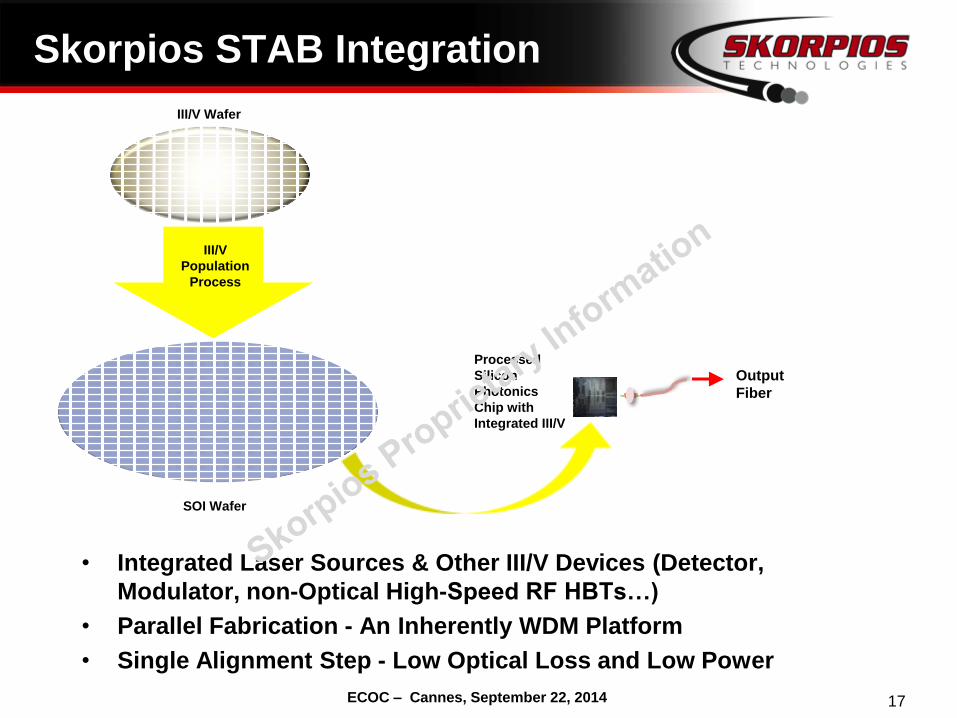

Skorpios STAB Integration

17

III/V Wafer

SOI Wafer

Output

Fiber

III/V

Population

Process

Processed

Silicon

Photonics

Chip with

Integrated III/V

• Integrated Laser Sources & Other III/V Devices (Detector,

Modulator, non-Optical High-Speed RF HBTs…)

• Parallel Fabrication - An Inherently WDM Platform

• Single Alignment Step - Low Optical Loss and Low Power

ECOC – Cannes, September 22, 2014

Si-Photonics 2.0

Skorpios – Single Chip Solution

• Silicon Photonics 2.0: A Closer Look

• LASERS Integrated in a Wafer-Scale Process

• No Need to Buy Completed Lasers

• No Margin Stacking

• Wafer Scale

• No Labor Intensive Alignments

• Hermetic

• No Bulk Optics

• Skorpios STAB-Silicon Modulators

• Physically Small

• Low Drive Voltages

• Low Insertion Loss

18

Skorpios: Silicon Photonics… With the Photons

ECOC – Cannes, September 22, 2014

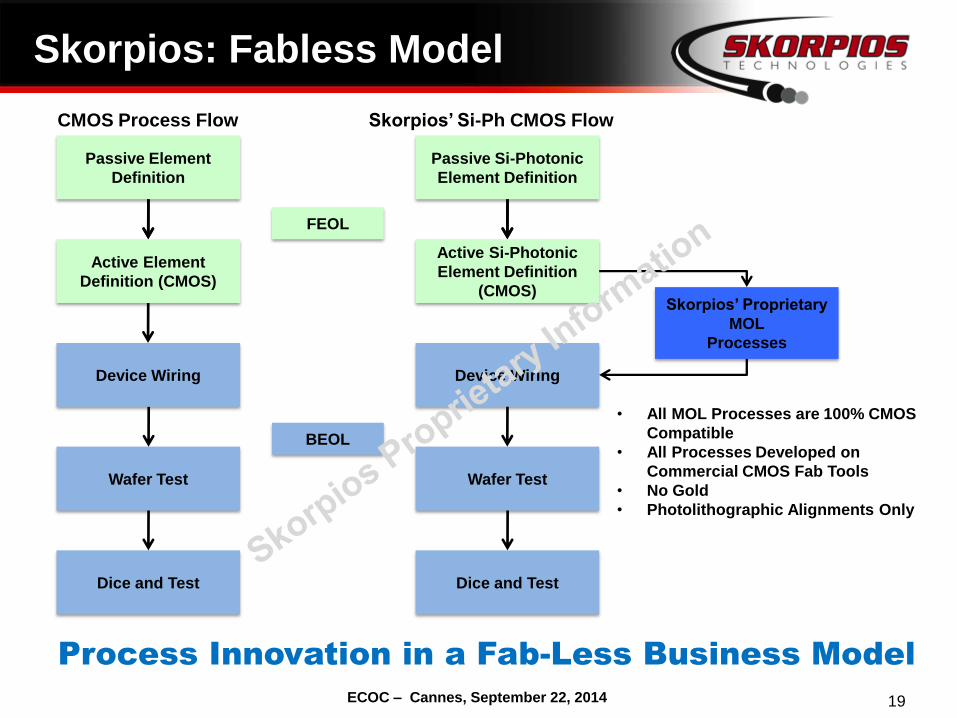

Skorpios: Fabless Model

19

Passive Element

Definition

Active Element

Definition (CMOS)

Device Wiring

Wafer Test

Dice and Test

Passive Si-Photonic

Element Definition

Active Si-Photonic

Element Definition

(CMOS)

Wafer Test

Dice and Test

CMOS Process Flow Skorpios’ Si-Ph CMOS Flow

Skorpios’ Proprietary

MOL

Processes

Device Wiring

• All MOL Processes are 100% CMOS

Compatible

• All Processes Developed on

Commercial CMOS Fab Tools

• No Gold

• Photolithographic Alignments Only

FEOL

BEOL

Process Innovation in a Fab-Less Business Model

ECOC – Cannes, September 22, 2014

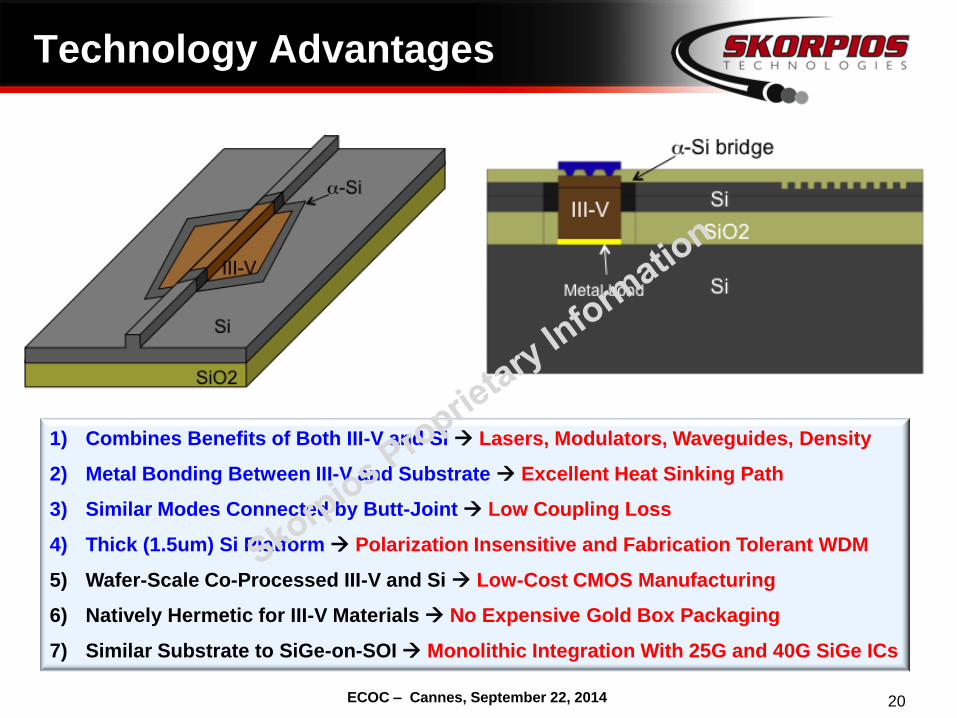

Technology Advantages

20

1) Combines Benefits of Both III-V and Si Lasers, Modulators, Waveguides, Density

2) Metal Bonding Between III-V and Substrate Excellent Heat Sinking Path

3) Similar Modes Connected by Butt-Joint Low Coupling Loss

4) Thick (1.5um) Si Platform Polarization Insensitive and Fabrication Tolerant WDM

5) Wafer-Scale Co-Processed III-V and Si Low-Cost CMOS Manufacturing

6) Natively Hermetic for III-V Materials No Expensive Gold Box Packaging

7) Similar Substrate to SiGe-on-SOI Monolithic Integration With 25G and 40G SiGe ICs

ECOC – Cannes, September 22, 2014

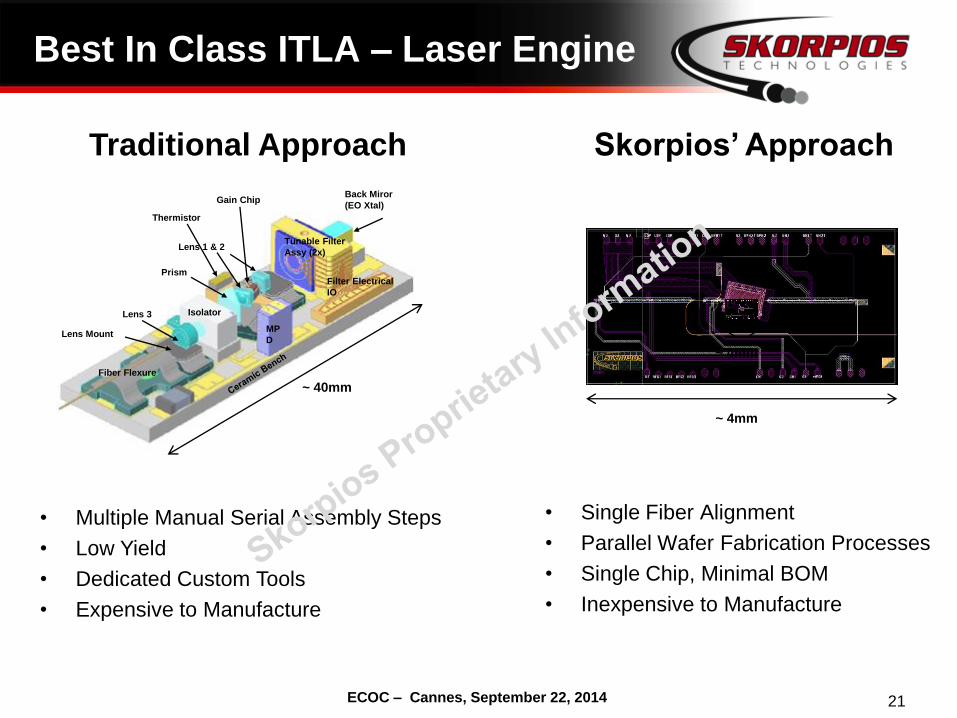

Best In Class ITLA – Laser Engine

21

• Multiple Manual Serial Assembly Steps

• Low Yield

• Dedicated Custom Tools

• Expensive to Manufacture

~ 40mm

Lens 3

Lens 1 & 2

Prism

Isolator

MP

D

Tunable Filter

Assy (2x)

Back Miror

(EO Xtal)

Fiber Flexure

Lens Mount

Thermistor

Gain Chip

Filter Electrical

IO

• Single Fiber Alignment

• Parallel Wafer Fabrication Processes

• Single Chip, Minimal BOM

• Inexpensive to Manufacture

Traditional Approach Skorpios’ Approach

~ 4mm

~ 4mm

ECOC – Cannes, September 22, 2014

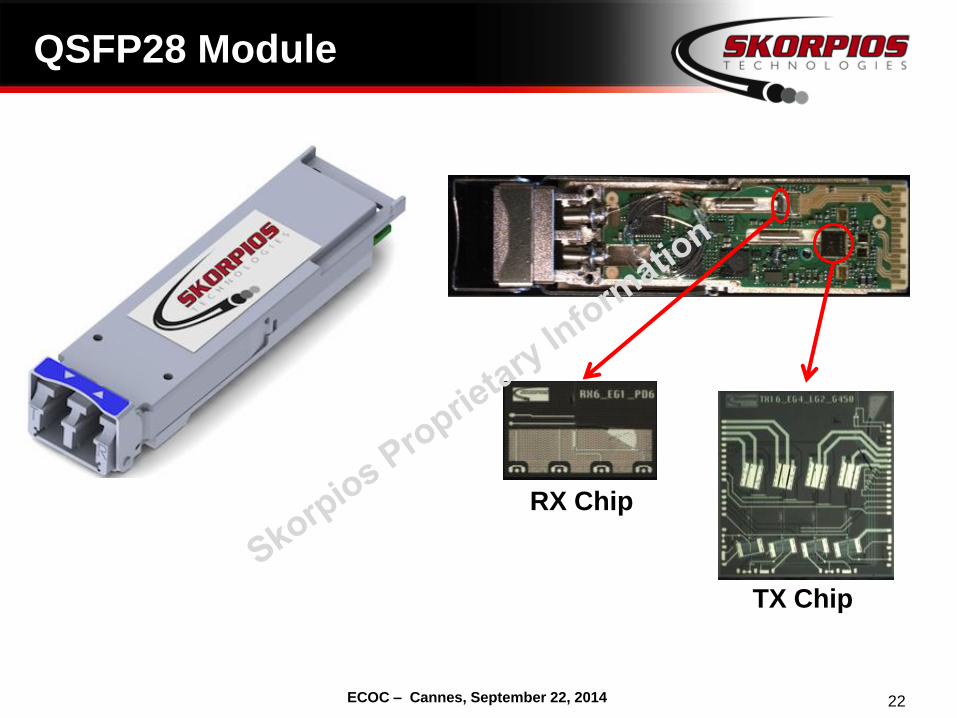

QSFP28 Module

22

RX Chip

TX Chip

ECOC – Cannes, September 22, 2014

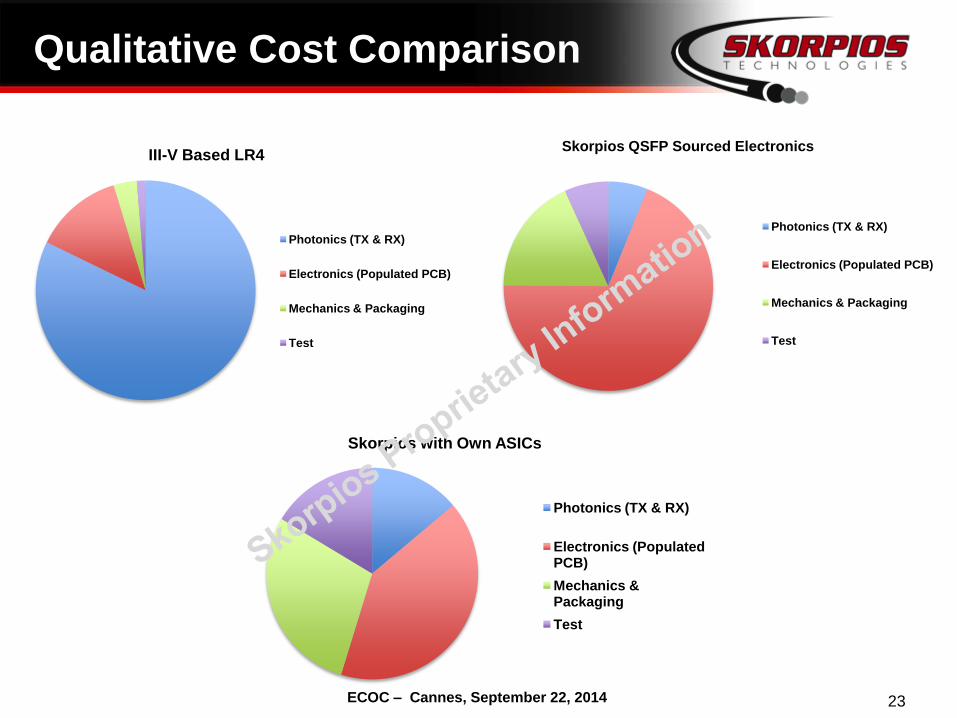

Qualitative Cost Comparison

23

III-V Based LR4

Photonics (TX & RX)

Electronics (Populated PCB)

Mechanics & Packaging

Test

Skorpios QSFP Sourced Electronics

Photonics (TX & RX)

Electronics (Populated PCB)

Mechanics & Packaging

Test

Skorpios with Own ASICs

Photonics (TX & RX)

Electronics (Populated PCB)

Mechanics & Packaging

Test

ECOC – Cannes, September 22, 2014

• Near Term Drivers for Silicon Photonics: Toolkits for Transceivers, Active Optical Cables and

Backplanes for Both Telecom and Datacom

- Optical Component Industry Cannot Keep Up With the Pace of Applications and Price/Cost Trends

- ASICs Can Process More Information Than Optical I/O’s Can Handle

• Data Rates Keep Increasing

- Electrical Links are Loss-Limited at High Data Rates

- Photonic Links Will Progressively Displace Electrical Ones

- Optical Links Have Now Entered a New Phase:

CMOS Photonics Now Competes Directly with Copper/VCSELs for Short Reach Applications: No Longer

Limited to LAN/MAN/WAN

• Volumes Growth

- Telecom: 10k-100k Units/Yr

- Datacom/HPC: >1M Units/Yr

• Silicon is the Best and Only Mature Platform:

- New Architectures Can be Enabled by Silicon Photonics

- Low Cost - Need a Process Compatible with CMOS Foundries

Skorpios Can Deliver All Such Requirements

Conclusions

24

ECOC – Cannes, September 22, 2014

Conclusions

“Future is not what it used to be.”

- Arthur C. Clarke

ECOC – Cannes, September 22, 2014

Thanks!

26