Embed Size (px)

Citation preview

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Simulating and analyzing order book data:The queue-reactive model

Weibing Huang1,2, Charles-Albert Lehalle3 andMathieu Rosenbaum1

1University Paris 6, 2Kepler Chevreux, 3Capital Fund Management

June 2014

Huang, Lehalle, Rosenbaum The queue-reactive model 1

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Outline

1 Introduction

2 Dynamics of the LOB : constant reference price

3 Dynamic reference price and time consistent model

Huang, Lehalle, Rosenbaum The queue-reactive model 2

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Outline

1 Introduction

2 Dynamics of the LOB : constant reference price

3 Dynamic reference price and time consistent model

Huang, Lehalle, Rosenbaum The queue-reactive model 3

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Summary

Aim of this work

Understanding the behaviours of market participants atdifferent limits of the order book.

Providing a realistic market simulator, enabling to computeexecution costs of complex trading strategies.

Approach

State (order book) dependent order flow intensities, incontrast to the Poisson approach.

Empirical validation through full order book data analysis.

Huang, Lehalle, Rosenbaum The queue-reactive model 4

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Modelling order book dynamics

Order book models

Zero intelligence (Poisson flows) : Smith et al ; Cont, Stoikovand Talreja ; Cont and De Larrard ; Abergel and Jedidi.

Hawkes flows : Hewlett, Large.

Fokker-Planck dynamics with state dependence : Gareche,Disdier, Kockelkoren and Bouchaud.

Equilibrium models : Rosu ; Lachapelle, Lasry, Lehalle andLions.

Functional approaches : Lakner, Reed and Stoikov ; Horst.

Huang, Lehalle, Rosenbaum The queue-reactive model 5

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Modelling order book dynamics

Some missing elements in available models

Market participants intelligence.

Differences between traders behaviours at different limits.

Dynamic bid-ask spread.

Explaining the empirical shape of the order book.

Difficulties in building a complete order book model

Strong dependences between different limits.

Exogenous price movements.

Huang, Lehalle, Rosenbaum The queue-reactive model 6

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Our approach

We consider the two following steps :

First we model the dynamics of the order book for periodswhere a reference price stays constant.

Then we introduce the dynamics of the reference price.

Our model

No individual agent.

Intelligence is added through a mean field game typeapproach.

Empirical studies of traders average behaviours becomepossible.

Huang, Lehalle, Rosenbaum The queue-reactive model 7

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Outline

1 Introduction

2 Dynamics of the LOB : constant reference price

3 Dynamic reference price and time consistent model

Huang, Lehalle, Rosenbaum The queue-reactive model 8

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

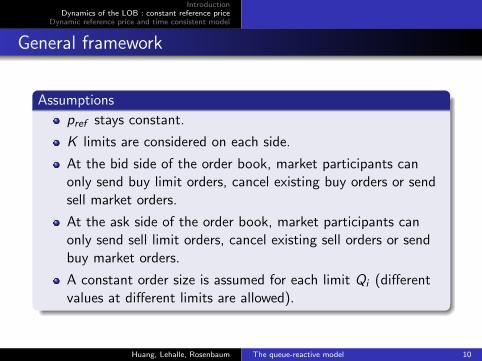

General framework

Limit order book in this framework

Huang, Lehalle, Rosenbaum The queue-reactive model 9

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

General framework

Assumptions

pref stays constant.

K limits are considered on each side.

At the bid side of the order book, market participants canonly send buy limit orders, cancel existing buy orders or sendsell market orders.

At the ask side of the order book, market participants canonly send sell limit orders, cancel existing sell orders or sendbuy market orders.

A constant order size is assumed for each limit Qi (differentvalues at different limits are allowed).

Huang, Lehalle, Rosenbaum The queue-reactive model 10

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

General framework

Limit order book as a continuous time Markov jump process

The 2K dimensional LOB state X (t) :X (t) = (Q−K (t), ...,Q−1(t),Q1(t), ...,QK (t)).

Order flow intensities : λMbuy/sell(x) (market orders), λLi (x)

(limit orders at Qi ) and λCi (x) (cancellations at Qi ).

The associated infinitesimal generator matrix Qx ,y is

Qx ,x+ei = λLi (x)

Qx ,x−ei = λCi (x) + λMbuy (x)1bestbid(x)=i , if i > 0

Qx ,x−ei = λCi (x) + λMsell(x)1bestask(x)=i , if i < 0

Qx ,x = −∑

y∈Ω,y 6=x

Qx ,y

Qx ,y = 0, otherwise.

Huang, Lehalle, Rosenbaum The queue-reactive model 11

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Ergodicity conditions

Assumptions on the generator matrix Qx ,y

(Bound on the total flow) The intensity of the total order flowof the queuing system is a bounded function on Ω : Thereexists a finite real number H > 0 such that for any x ∈ Ω,∑

i∈[−K ,...,−1,1,...,K ]

[Qx ,x+ei + Qx ,x−ei ] ≤ H.

(Negative individual drift) There exists a positive integerCbound and δ > 0, such that for all i and all x ∈ Ω, ifxi > Cbound ,

Qx ,x+ei − Qx ,x−ei < −δ.

Huang, Lehalle, Rosenbaum The queue-reactive model 12

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Ergodicity

Interpretation of these two assumptions

The order arrival/consumption speed stays bounded for anygiven state of the order book.

Market participants send eventually less limit orders thanmarket orders and cancellations to large queues.

Huang, Lehalle, Rosenbaum The queue-reactive model 13

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Theorem

Under these two assumptions, the 2K dimensional Markov jumpprocess X is ergodic, which means that there exists a probabilitymeasure π that satisfies πP(t) = π (π is called invariant measure,and Pxy (t) the transition probability from state x to state y in atime t) and for every x and y :

limt→∞

Pxy (t) = πy .

Huang, Lehalle, Rosenbaum The queue-reactive model 14

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Data description

Data base

Data used in our empirical studies are collected fromCheuvreux’s Data base of order book from Jan 2010 to March2012.

For each trading venue, the data base records the order bookdata (prices, quantities) up to the fifth best limit on bothsides whenever some market event happens and changes theorder book state.

We focus only on the primary market data in this study.

First and last hour of trading are removed, as they usuallyhave specific features because of the opening/closing auctionphases.

Huang, Lehalle, Rosenbaum The queue-reactive model 15

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Data description

Large tick stocks

A large tick asset is defined as an asset whose bid-ask spreadis almost always equal to one tick.

Two French large tick stocks (France Telecom, now known asOrange, and Alcatel-Lucent) are studied in this work, andthey exhibit very similar results.

The stock France Telecom is chosen as an illustration examplein this presentation.

stock number of number of spread sizeorders per day trades per day (ticks)

France Telecom 159250 7282 1.43

Alcatel Lucent 129400 8626 1.99

Huang, Lehalle, Rosenbaum The queue-reactive model 16

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Estimating pref

Estimation method

When the spread is odd (in tick unit) :

pref = pmid =(pbestbid + pbestask)

2.

When it is even, we use either

pmid +tick size

2or pmid −

tick size

2,

choosing the one which is closer to the previous value of pref .

More complex methods can be used for the estimation of pref .For large tick assets, remark that the estimated generatormatrix remains stable under various methods of estimatingpref (since it is essentially pmid).

Huang, Lehalle, Rosenbaum The queue-reactive model 17

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Model I : Collection of independent queues

Assumptions

Order flow arrival rates are functions of the target queue size.

Market orders can be sent directly to Qi (to removedependences between different limits).

Ergodicity condition

Birth and death process for each queue.

Non-explosion.

∞∑k=1

k∏n=1

[λLi (n − 1)

λCi (n) + λMi (n)] <∞.

Huang, Lehalle, Rosenbaum The queue-reactive model 18

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Empirical study : Collection of independent queues

Arrival/departure ratio ρi (n)

The order arrival/departure ratio ρi (n), defined by

ρi (n) =λLi (n)

(λCi (n + 1) + λMi (n + 1)).

plays an important role in the stationarity and long term behaviourof the order book. We have that :

The queue size tends to increase when ρ > 1.

The queue size tends to decrease when ρ < 1.

Huang, Lehalle, Rosenbaum The queue-reactive model 19

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Statistical properties of the order flow : first limits

Intensities as functions of the target queue size : first limits

Huang, Lehalle, Rosenbaum The queue-reactive model 20

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Statistical properties of the order flow : first limits

Comments

Limit order insertion : almost a constant function, with aparticularly smaller value observed at Q1 = 0 : limit orderinsertion within the bid-ask spread is risky.

Cancellation : approximately an increasing concave function,due to the priority value of limit orders.

Market order insertion : decreases exponentially with theavailable quantity at Qi : rushing for liquidity when it is rareand waiting for better price when liquidity is abundant.

Huang, Lehalle, Rosenbaum The queue-reactive model 21

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Statistical properties of the order flow

Intensities as functions of the target queue size : second limits

Huang, Lehalle, Rosenbaum The queue-reactive model 22

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Statistical properties of the order flow : second limits

Comments

Limit order insertion : a decreasing function of the queue size.A common strategy used in practice : posting orders atnon-best limits when the queue size is small to seize thepriority.

Cancellation : increases more rapidly, attains its asymptoticlimit for a queue size around 5 AES (average event size).

Market order insertion : market orders can arrive at Q2 onlywhen Q1 = 0. The shape is very similar to that of Q1 but itsabsolute values are much smaller.

Huang, Lehalle, Rosenbaum The queue-reactive model 23

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Statistical properties of the order flow

Intensities as functions of the target queue size : third limits

Huang, Lehalle, Rosenbaum The queue-reactive model 24

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Statistical properties of the order flow : third limits

Comments

Limit order insertion : remains a decreasing function as for thecase of Q2, but market participants seem to stop rushing forfuture priority when the size becomes larger than 5 AES.

Cancellation : now increases almost linearly as the queue sizegrows.

Market order insertion : in some rare cases, one can still findmarket orders arriving at Q3 (cross market orders or marketorders occurring when the spread is large).

Huang, Lehalle, Rosenbaum The queue-reactive model 25

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Asymptotic shape of the LOB

Stationary Distribution

We denote by πi (n) the stationary distribution of the queue size Qi ,the following result for the invariant distribution is easily obtained :

πi (n) = πi (0)n∏

j=1

ρi (j − 1)

πi (0) =(1 +

∞∑n=1

n∏j=1

ρi (j − 1))−1

.

Remark

The long term behaviour of the order book is completelydetermined by the order arrival/departure ratio vector ρi (n).

Huang, Lehalle, Rosenbaum The queue-reactive model 26

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Asymptotic form of the LOB

Invariant Distribution vs. empirical distribution

Huang, Lehalle, Rosenbaum The queue-reactive model 27

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Asymptotic form of the LOB

Conclusion

For large tick assets, the empirical LOB distribution is actually anasymptotic equilibrium created by the different behaviours ofmarket participants towards various states of the order book.

Huang, Lehalle, Rosenbaum The queue-reactive model 28

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Model II : Two sets of dependent queues

Assumptions

Market orders are only sent to first and second limits.

Market orders consume quantities at best limits.

Dynamics at second limit depend also on whether the firstlimit is empty.

Huang, Lehalle, Rosenbaum The queue-reactive model 29

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Statistical properties of the order flow

Intensities at Q2

Huang, Lehalle, Rosenbaum The queue-reactive model 30

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Statistical properties of the order flow

Comments

Limit order insertion : both curves are decreasing functions ofthe queue size, however, when Q2 is the best ask limit, theorder arrival rate reaches a much higher asymptotic value.

Cancellation : the cancellation rate is higher when Q1 = 0.

Market order : no market order can arrive at Q2 when thereare still quantities available at Q1. Note that we treat crosslimit market orders (that consume several limits) as asequence of market orders arriving within a very short timeperiod in our data.

Huang, Lehalle, Rosenbaum The queue-reactive model 31

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

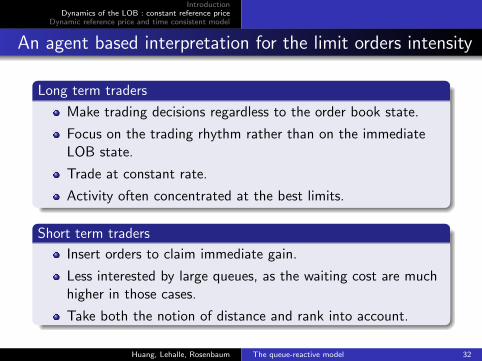

An agent based interpretation for the limit orders intensity

Long term traders

Make trading decisions regardless to the order book state.

Focus on the trading rhythm rather than on the immediateLOB state.

Trade at constant rate.

Activity often concentrated at the best limits.

Short term traders

Insert orders to claim immediate gain.

Less interested by large queues, as the waiting cost are muchhigher in those cases.

Take both the notion of distance and rank into account.

Huang, Lehalle, Rosenbaum The queue-reactive model 32

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

An agent based interpretation for the limit orders intensity

A typical strategy for arbitragers

Insert orders at Q2 when the queue size is small, wait for it tobecome the best limit, then stay if the queue size at that momentis large enough so that it covers the risk of short term markettrend, or cancel orders if the queue size is too small.

Huang, Lehalle, Rosenbaum The queue-reactive model 33

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Model II as a Quasi birth and death process

Assumption

(Independent Poisson Flows at Q1) There are two positiveconstants λ1 and µ1, with λ1 < µ1, such that for k ≥ 1 :

λC1 (k) + λMbuy (k) = µ1

λL1(k) = λ1

λL1(0) = λ1.

Huang, Lehalle, Rosenbaum The queue-reactive model 34

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Asymptotic behaviours in Model II

Joint distribution of Q1,Q2, Model II

Huang, Lehalle, Rosenbaum The queue-reactive model 35

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Model III : Modelling bid-ask dependences

Assumptions

Market participants adjust their trading rate not onlyaccording to the the target queue size, but also to whetherthe opposite queue size is small, usual or large.

The regime switching in Model II still applies at Q±2.

The problem is reduced to the study of the 4-dimensionalprocess (Q−2,Q−1,Q1,Q2).

Huang, Lehalle, Rosenbaum The queue-reactive model 36

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Empirical study : Modelling bid-ask dependences

Intensity functions at Q1

Huang, Lehalle, Rosenbaum The queue-reactive model 37

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Empirical study : Modelling bid-ask dependences

Comments

Limit order insertion : a decreasing function of the oppositelimit size.

Cancellation : similar forms but different asymptotic values. Itis not surprising that the cancellation rate, being an indicatorof market participants patience, is a decreasing function of theliquidity level at the opposite side.

Market orders : when the volume available at Q−1 isabundant, more market orders are sent to Q1. The reason isthat in that case, transactions at Q1 are relatively cheap asthe fair price is temporarily closer to the price of Q1.

Huang, Lehalle, Rosenbaum The queue-reactive model 38

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Asymptotic behaviours in Model III, by Monte-Carlomethod

Joint Distribution of Q−1,Q1

Huang, Lehalle, Rosenbaum The queue-reactive model 39

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Example of application : Probability of execution

Problem

At t = 0, a trader posts a buy limit order at Q−1 and waits untileither the order is executed or the opposite queue Q1 is totallydepleted. Estimate the probability of executing an order before themid price moves, under different initial state of order book.

Huang, Lehalle, Rosenbaum The queue-reactive model 40

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Execution probability of a buying order placed at Q−1 att = 0 (Monte-Carlo method)

Huang, Lehalle, Rosenbaum The queue-reactive model 41

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Conclusion on the first part

Conclusion

Three different models are presented in this part, each withdifferent assumptions on the information set used by traders.

Empirical results on the intensities functions under theseassumptions are shown, and the comments we made for theseresults apply also to other large tick assets.

Empirical facts

The sub-linear, concave increasing cancellation rate.

The decreasing limit order insertion rate for non-best limits.

For large tick assets, the empirical LOB distribution is actuallyan asymptotic equilibrium created by the different behaviorsof market participants towards various states of the LOB.

Huang, Lehalle, Rosenbaum The queue-reactive model 42

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Outline

1 Introduction

2 Dynamics of the LOB : constant reference price

3 Dynamic reference price and time consistent model

Huang, Lehalle, Rosenbaum The queue-reactive model 43

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Purely order book driven model

Dynamics of pref in the purely order book driven model

We consider times of mid price move for changes in pref .More precisely, they are triggered with probability θ by one ofthe three following events :

The insertion of a buy (sell) limit order within the bid-askspread, while Q1 (Q−1) is empty at the moment of thisinsertion.A cancellation of the last limit order at the best offer queue.A market order that consumes all the available quantity at thebest offer queue.

Qi becomes either Qi+1 or Qi−1 depending on the direction ofprice move.

Huang, Lehalle, Rosenbaum The queue-reactive model 44

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Purely order book driven model

Remarks

Price fluctuations are completely generated by the order bookdynamics.

Its volatility is naturally an increasing function of θ, and isconstrained to lie in the interval [0, σ(θ = 1)].

Strong mean-reverting behaviour of the price process.

The maximum achievable volatility (mechanical volatility) isoften smaller than the empirical volatility.

Huang, Lehalle, Rosenbaum The queue-reactive model 45

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

The queue-reactive model

Dynamics of pref in the queue-reactive model

Changes of pref are triggered by changes in the mid price,with probability θ.

Qi becomes either Qi+1 or Qi−1 when pref changes.

The whole LOB is redrawn from its invariant distribution withprobability θreinit around the new pref when pref changes.

Remarks

We consider that, with probability θreinit , changes of price aredue to exogenous informations, in which case marketparticipants adjust very quickly their order flows around thenew pref , as if a new LOB is redrawn from its invariantdistribution.

Huang, Lehalle, Rosenbaum The queue-reactive model 46

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

The queue-reactive model

Calibration of θ and θreinit

10-minute price volatility of the asset.

One-step mean-reversion ratio η of the mid price.

Huang, Lehalle, Rosenbaum The queue-reactive model 47

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

A simulated bid-ask trajectory

Huang, Lehalle, Rosenbaum The queue-reactive model 48

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Theorem

After suitable rescaling, we obtain the diffusive behaviour at largescales for the price in the queue reactive model.

Huang, Lehalle, Rosenbaum The queue-reactive model 49

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Example of application : order placement analysis

The general optimal execution framework

Trading horizon is divided into small slices (5-10 minutes).

An execution algorithm determines, at the start of each slice,the quantity to be executed in that slice.

Order scheduling problem

Almgren-Chriss approach.

Optimal solution depends notably on the market impactfunction and the risk aversion ratio.

Huang, Lehalle, Rosenbaum The queue-reactive model 50

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Example of application : order placement analysis

Order placement problem

In each of these slices, how should the algorithm place orders ?

Micro-structural version of the volume scheduling problem,but is much more difficult to solve.

Price dynamics are no longer a Brownian motion.Queue priority starts to play an important role, as well as othermicro-structural features (tick size, order book state, tradingspeed).

Huang, Lehalle, Rosenbaum The queue-reactive model 51

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Example of application : order placement analysis

Our approach

The queue-reactive model can be used as a market simulator foranalyzing order placement tactics.

Major axes in an order placement analysis

Fill rate : the speed of order filling.

Relative performance : the average execution price comparedto the average market price during the execution period.

Market impact profile : the average price drift caused by theplacements of orders.

Huang, Lehalle, Rosenbaum The queue-reactive model 52

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Example of application : order placement analysis

Two simple order placement tactics

T1 : “Fire and forget” At t = 0, post a limit order at thebest offer queue. When the mid price changes, cancel the limitorder and send a market order at the opposite side with all theremaining quantities if any. At t = T , send all the remainingquantities at the opposite side to finish the execution.

T2 : “Pegging to the best”. At t = 0, post a limit order atthe best offer queue, and then “peg” to it : if the best offerprice changes, cancel the existing order and repost all theremaining quantities at the new best offer queue. If our orderis the only remaining order in the best offer queue, cancel itand repost the remaining quantities at the newly revealed bestoffer queue. At t = T , send all the remaining quantities at theopposite side to finish the execution.

Huang, Lehalle, Rosenbaum The queue-reactive model 53

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Example of application : order placement analysis

Order scheduling strategy

These two order placement tactics will be used together with twovolume scheduling strategies (ni denotes quantity to be trade atthe i-th slice, and M is the number of slices.) :

ntotal = 60 AES, length of the subtrading periods : 10minutes, M = 20.

S1 : a linear scheduling (ni = ntotal/M), VWAP benchmark.

S2 : an exponential schedulingni+1 − ni = ntotal(e

−(i+1)/4 − e−i/20), S0 benchmark.

Huang, Lehalle, Rosenbaum The queue-reactive model 54

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Example of application : order placement analysis

Decomposition of slippage

Slippage =Pbenchmark − Pexec

Pbenchmark

Ptheoexec =

M∑i=1

niVWAPi

Slippagetheo =Pbenchmark − Ptheo

exec

Pbenchmark.

Huang, Lehalle, Rosenbaum The queue-reactive model 55

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Simulation results

Huang, Lehalle, Rosenbaum The queue-reactive model 56

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Example of application : order placement analysis

Comments

The tactic “Pegging to the best” performs better than thetactic “Fire and forget” for an execution target at the VWAP.Higher passive execution rate, better average price comparedto market VWAP, but larger impact.

The tactic “Fire and forget” slightly outperforms the tactic“Pegging to the best” for an execution targets at the arrivalprice S0. Lower passive execution rate, worse average pricecompared to market VWAP, but smaller impact.

Huang, Lehalle, Rosenbaum The queue-reactive model 57

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Example of application : order placement analysis

Market impact profiles

An order placement tactic has two parameters : the periodlength T and the quantity to execute n. In the followingexperiments, T will be set to 10 minutes, and we vary thevalue of n from 1 to 60 AES.

We denote by MIi (t, n) the market impact of Tactic i withtarget quantity n at the moment t, defined by :MIi (t, n) = E [St−S0

S0].

Huang, Lehalle, Rosenbaum The queue-reactive model 58

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Example of application : order placement analysis

Market impact profiles of these two tactics

Huang, Lehalle, Rosenbaum The queue-reactive model 59

IntroductionDynamics of the LOB : constant reference price

Dynamic reference price and time consistent model

Market impact profiles

Comments

The market impact curves are concave both in time andvolume in our simulations.

Price impact of the tactic “Fire and forget” is quiteinstantaneous and depends essentially on the target quantityn.

Price impact of the tactic “Pegging to the best” is a moreprogressive process, depending both on the target quantity nand the duration t.

Huang, Lehalle, Rosenbaum The queue-reactive model 60