Embed Size (px)

Citation preview

STOCKSTOCK

24 May 2012

Singapore

PICPICKKSS

We have based this document on information obtained from sources we believe to be reliable, but we do not make any representation or warranty nor accept any responsibility or liability as to its accuracy, completeness or correctness. Expressions of opinion contained herein are those of UOB Kay Hian Research Pte Ltd only and are subject to change without notice. Any recommendation contained in this document does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. This document is for the information of the addressee only and is not to be taken assubstitution for the exercise of judgement by the addressee. This document is not and should not be construed as an offer or a solicitation of an offer to purchase or subscribe or sell any securities. UOB Kay Hian and its affiliates, their Directors, officers and/or employees may own or have positions in any securities mentioned herein or any securities related thereto and may from time to time add to or dispose of any such securities. UOB Kay Hian and its affiliates may act as market maker or have assumed an underwriting position in the securities of companies discussed herein (or investments related thereto) and may sell them to or buy them from customers on a principal basis and may also perform or seek to perform investment banking or underwriting services foror relating to those companies.

UOB Kay Hian (U.K.) Limited, a UOB Kay Hian subsidiary which distributes UOB Kay Hian research for only institutional clients, is an authorised person in the meaning of the Financial Services and Markets Act 2000 and is regulated by Financial Services Authority (FSA).

In the United States of America, this research report is being distributed by UOB Kay Hian (U.S.) Inc (“UOBKHUS”) which accepts responsibility for the contents. UOBKHUS is a broker-dealer registered with the U.S. Securities and Exchange Commission and is an affiliate company of UOBKH. Any U.S. person receiving this report who wishes to effect transactions in any securities referred to herein should contact UOBKHUS, not its affiliate. The information herein has been obtained from, and any opinions herein are based upon sources believed reliable, but we do not represent that it is accurate or complete and it should not be relied upon as such. All opinions and estimates herein reflect our judgement on the date of this report and are subject to change without notice. This report is not intended to be an offer, or thesolicitation of any offer, to buy or sell the securities referred to herein. From time to time, the firm preparing this report or its affiliates or the principals or employees of such firm or its affiliates may have a position in the securities referred to herein or hold options, warrants or rights with respect thereto or other securities of such issuers and may make a market or otherwise act as principal In transactions in any of these securities. Any such non-U.S. persons may have purchased securities referred to herein for their own account in advance of release of this report. Further information on the securities referred to herein may be obtainedfrom UOBKHUS upon request.

http://research.uobkayhian.comMICA (P) 048/03/2011RCB Regn. No. 198700235E

DISCLAIMER

IEV HOLDINGS

AGENDA

OSIM INTERNATIONAL

BUMITAMA AGRI

A

B

C

Innovative Engineering Ventures (IEV)

• Offshore engineering services to the oil and gas sector in Asia-Pac

• Mobile natural gas distribution in Indonesia and Vietnam

BACKGROUND

BACKGROUND

Offshore engineering services:

- Evolved from a niche subcontractor to a full-fledged turnkey operator

- Expanding product portfolio beginning with Marine Growth Preventer (1986)

BACKGROUND

Mobile natural gas distribution:

- Provides virtual pipeline to deliver gas via CNG trailers to customers without pipeline access

- 20.5% stake in CNG Vietnam

BACKGROUND

Asian fixed platform capex to grow 39.4% in 2010-14F

INDUSTRY

Asia to attract 1/3 of global capex and ¼ of new installations worldwide

Total capex in Asia to amount to USD 25.8 billion

Mainly in China, Indonesia, Malaysia, Thailand

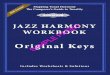

Asia-Pac offshore platforms ripe for decommissioning

INDUSTRY

Age Profile of Asia-Pac Installations

Asia-Pac offshore platforms ripe for decommissioning

INDUSTRY

Regulations require proper disposal of offshore installations in accordance with international standards

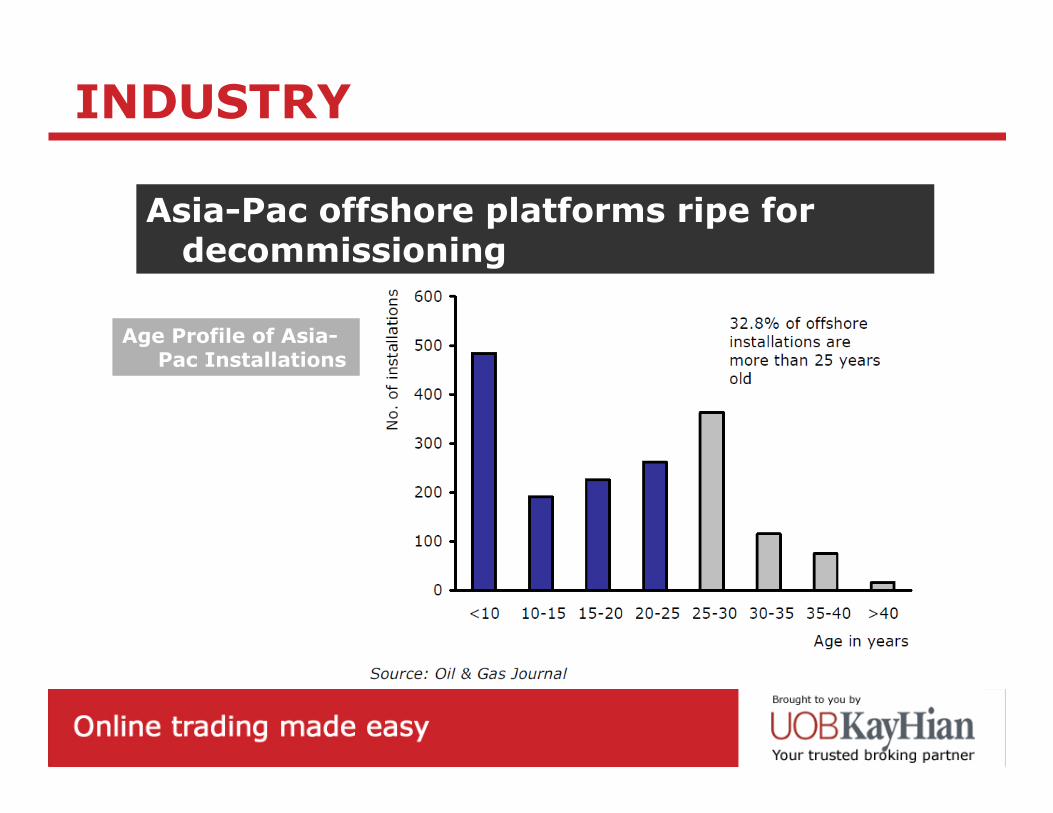

Indonesia’s “Golden Age” of gas

INDUSTRY

Indonesia’s Energy Consumption by Fuel Type

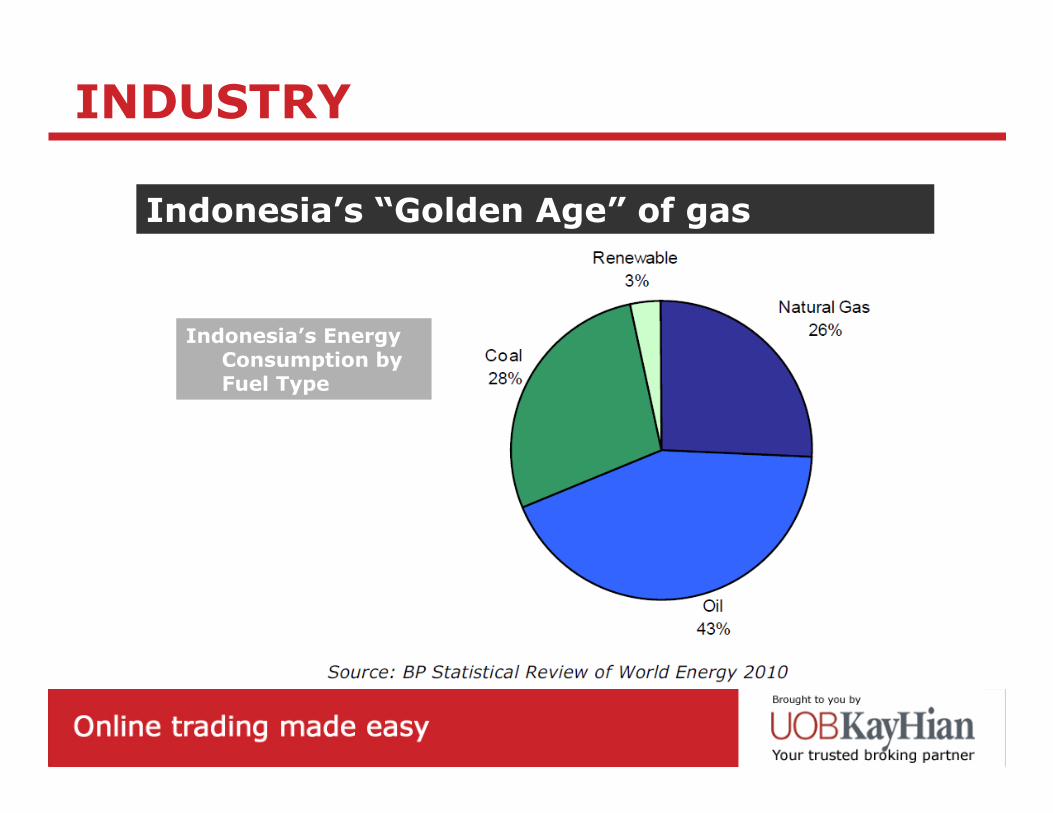

Indonesia’s “Golden Age” of gas

INDUSTRY

Indonesia’s Fuel Prices

Indonesia’s unique geography

INDUSTRY

Limited domestic access to piped gas

Opportunities for alternative modes of gas transportation

Beneficiary of increased Asian platform capex

INVESTMENT RATIONALE

1

2 Riding on bright prospects for offshore decommissioning

3 Constant innovation a hallmark of the group

Poised to leverage on “Golden Age” of gas

INVESTMENT RATIONALE

4

5 Capacity expansion to drive volume growth

Expansion of CNG processing facility

New supply chain

6 Margin expansion through development of lower cost gas sources

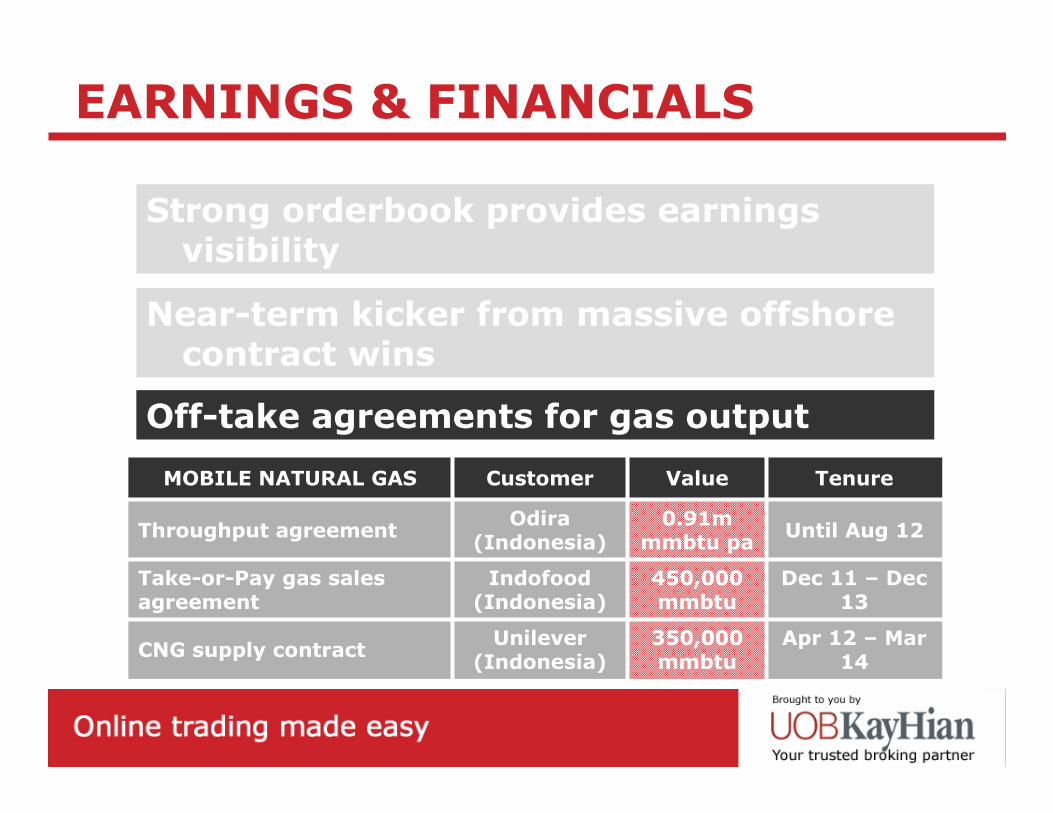

Strong orderbook provides earnings visibility

EARNINGS & FINANCIALS

-

RM 5-10m

(India)MGP installation on 7 jackets (2x)

-Sempec

(Indonesia)Wire-cutting services to remove a fixed platform

2H13-Pertamina(Indonesia)

15-year Oil & Gas concession

Rig Decom (2x)

Rig Reuse

OFFSHORE

May 2012 (Completed)

RM 27mPetronas(Malaysia)

2H12RM 262mPetronas(Malaysia)

Expected Completion

ValueCustomer

Strong orderbook provides earnings visibility

EARNINGS & FINANCIALS

Near-term kicker from massive offshore contract wins

Strong orderbook provides earnings visibility

EARNINGS & FINANCIALS

Near-term kicker from massive offshore contract wins

Off-take agreements for gas output

Apr 12 – Mar 14

350,000 mmbtu

Unilever (Indonesia)

CNG supply contract

Dec 11 – Dec 13

450,000 mmbtu

Indofood (Indonesia)

Take-or-Pay gas sales agreement

Until Aug 120.91m

mmbtu paOdira

(Indonesia)Throughput agreement

TenureValueCustomerMOBILE NATURAL GAS

Strong orderbook provides earnings visibility

EARNINGS & FINANCIALS

Near-term kicker from massive offshore contract wins

Off-take agreements for gas output

Processing capacity growth over the medium term

Margin improvement arising from a switch to cheaper stranded gas sources

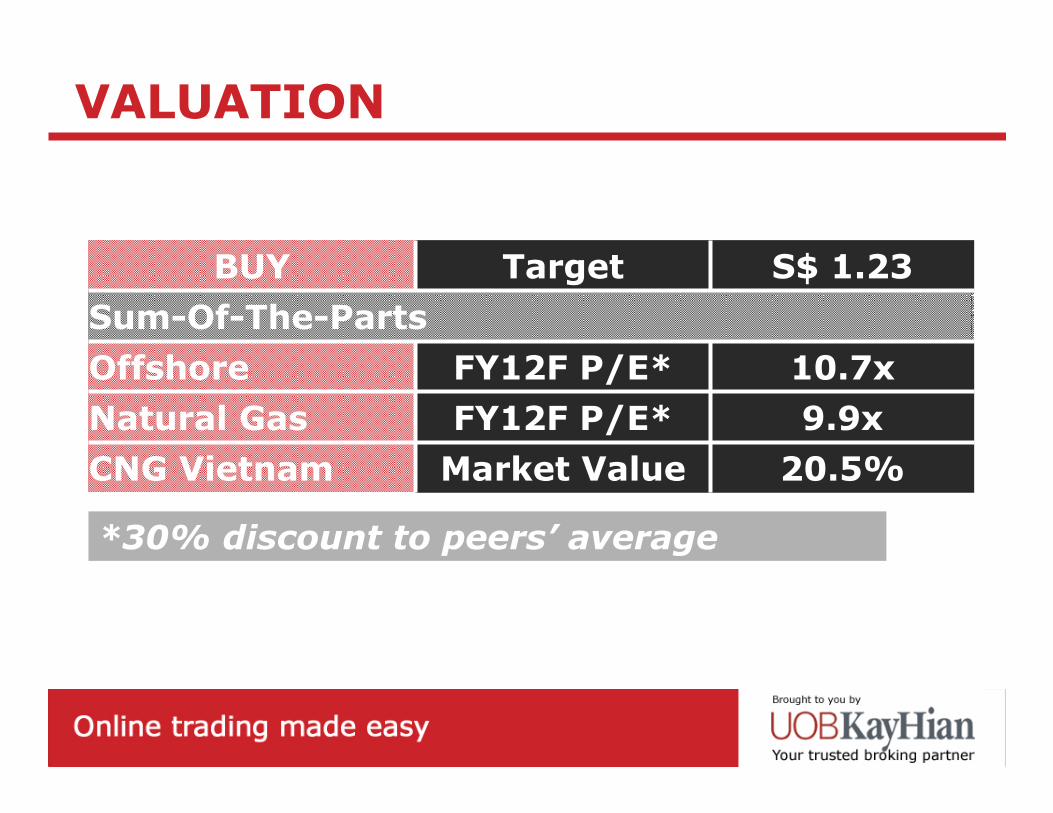

VALUATION

Sum-Of-The-Parts

10.7xFY12F P/E*Offshore

9.9xFY12F P/E*Natural Gas

20.5%Market ValueCNG Vietnam

S$ 1.23TargetBUY

*30% discount to peers’ average

RISKS & CATALYSTS

RISKS • Foreign exchange risk

• Fuel pricing risks

• Intellectual property risks

• Contract renewal risks

RISKS & CATALYSTS

CATALYSTS • Order wins surprise on the upside

• More turnkey contracts

IEV HOLDINGS

AGENDA

OSIM INTERNATIONAL

BUMITAMA AGRI

A

B

C

Asia’s leading luxury lifestyle and healthcare product retailer

Brand portfolio:-

Osim | GNC | RichLife | Brookstone | TWG Tea

BACKGROUND

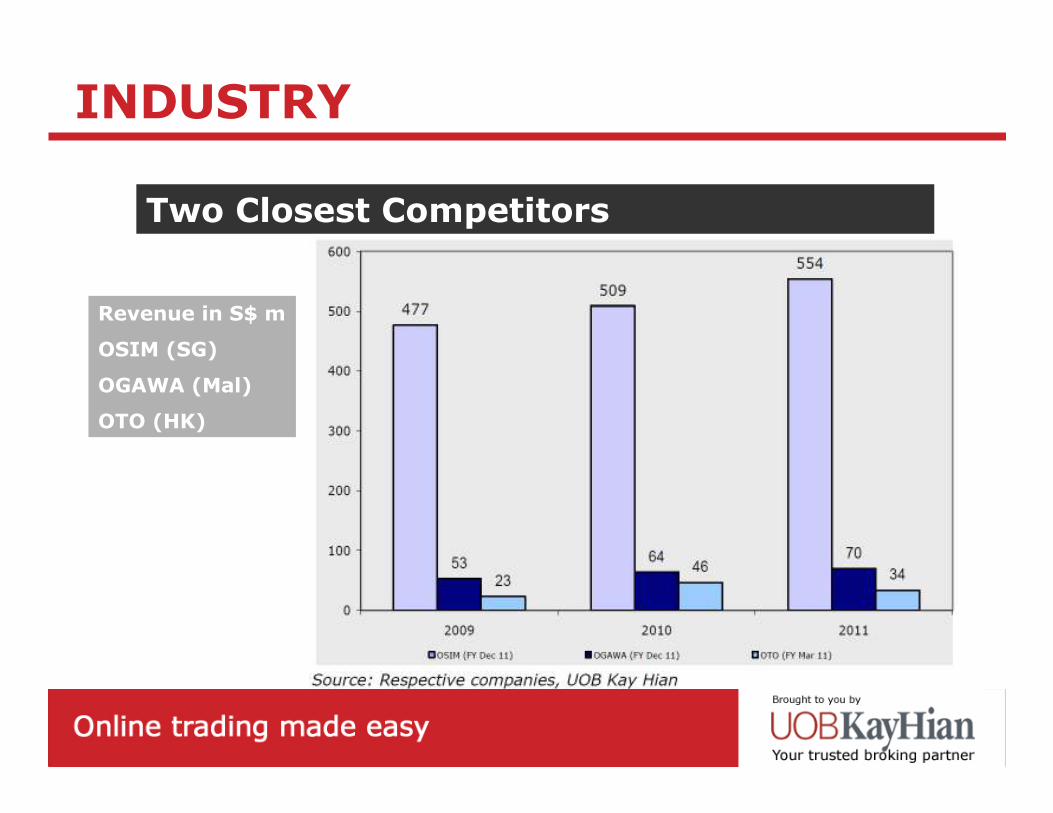

Two Closest Competitors

INDUSTRY

Revenue in S$ m

OSIM (SG)

OGAWA (Mal)

OTO (HK)

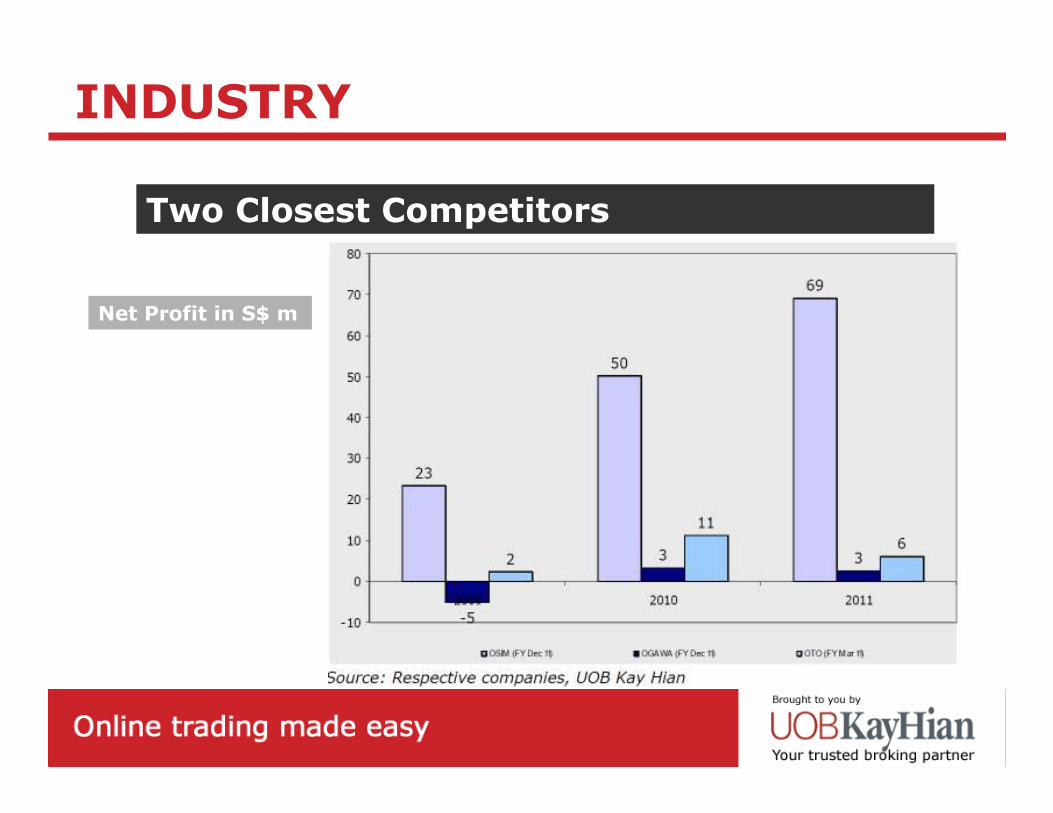

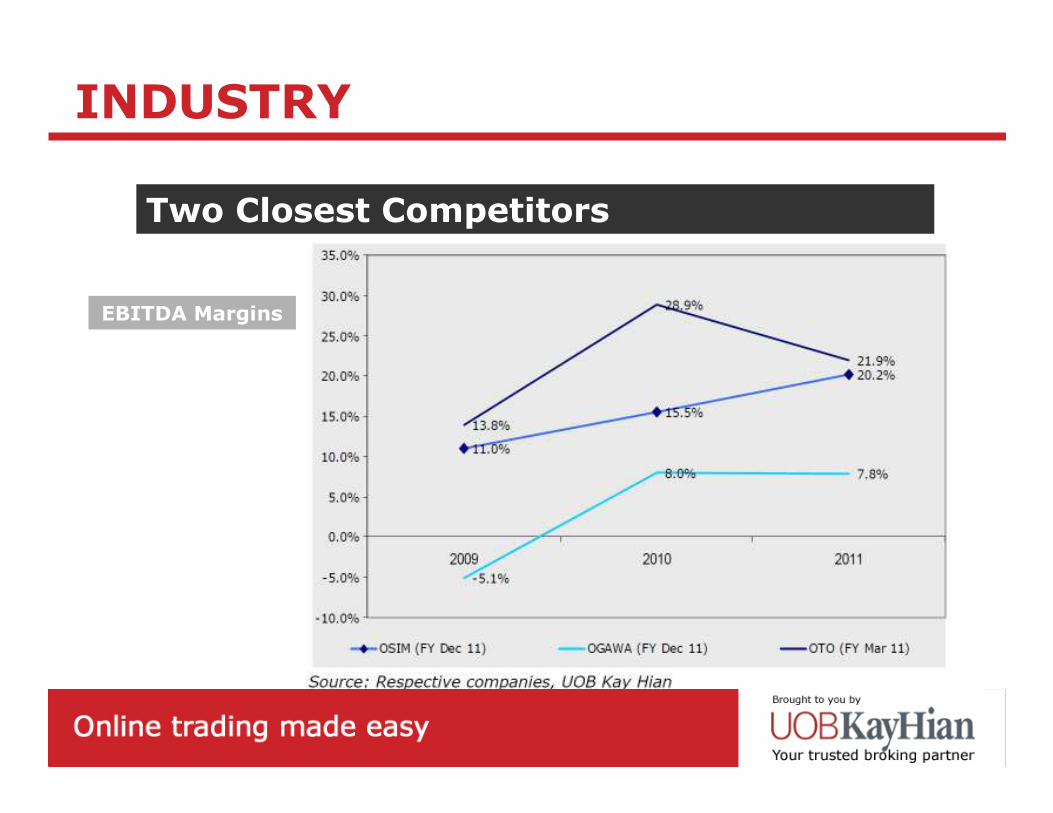

Two Closest Competitors

INDUSTRY

Net Profit in S$ m

Two Closest Competitors

INDUSTRY

EBITDA Margins

50 new OSIM outlets in China by 2012

500 OSIM outlets in China over the next 5-7 years

(267 outlets as of 1Q12)

1000 RichLife outlets by 2020

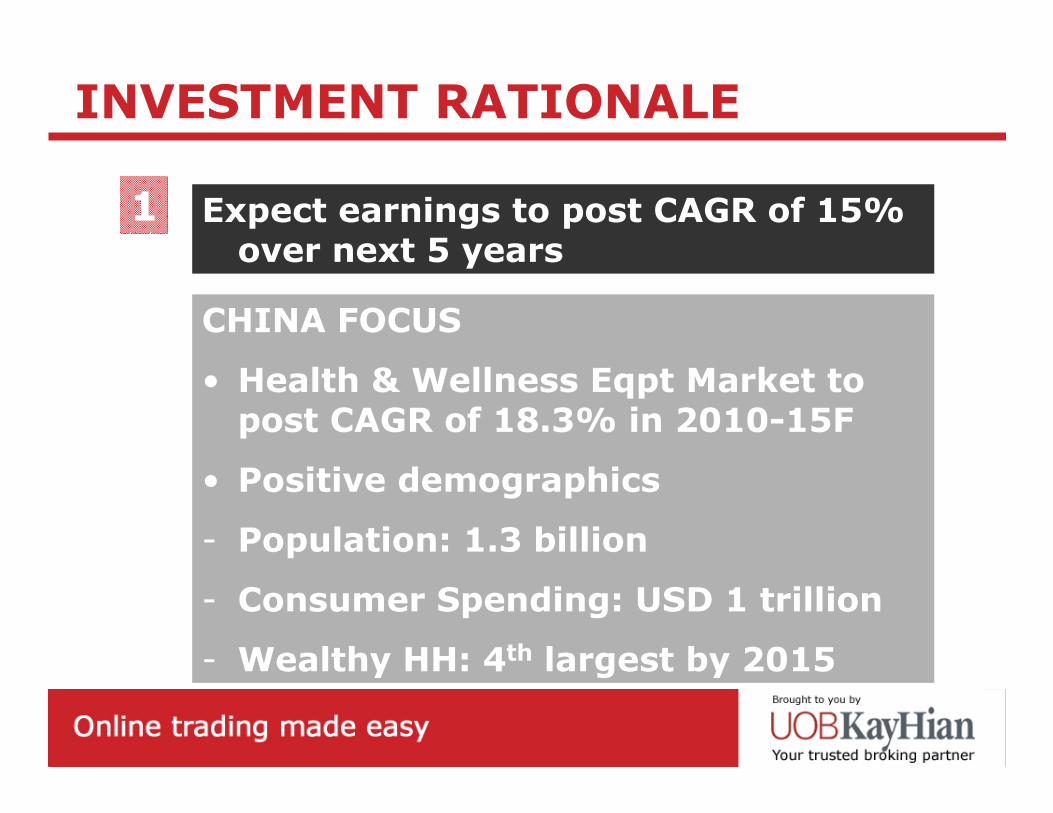

Expect earnings to post CAGR of 15% over next 5 years

INVESTMENT RATIONALE

1

CHINA FOCUS

• Health & Wellness Eqpt Market to post CAGR of 18.3% in 2010-15F

- Rising luxury consumption

- Increasing health consciousness

- Rising product awareness as the country urbanizes

Expect earnings to post CAGR of 15% over next 5 years

INVESTMENT RATIONALE

1

CHINA FOCUS

• Health & Wellness Eqpt Market to post CAGR of 18.3% in 2010-15F

• Positive demographics

- Population: 1.3 billion

- Consumer Spending: USD 1 trillion

- Wealthy HH: 4th largest by 2015

Expect earnings to post CAGR of 15% over next 5 years

INVESTMENT RATIONALE

1

Spend 2% of Revenue on R&D

Success of new product rollouts in 2011

Product enhancements to be carried out yearly, with life cycles of 3-5 years

Bestsellers uDivine, uPhoria still good for 24 months

Better margins on new product enhancements

INVESTMENT RATIONALE

2

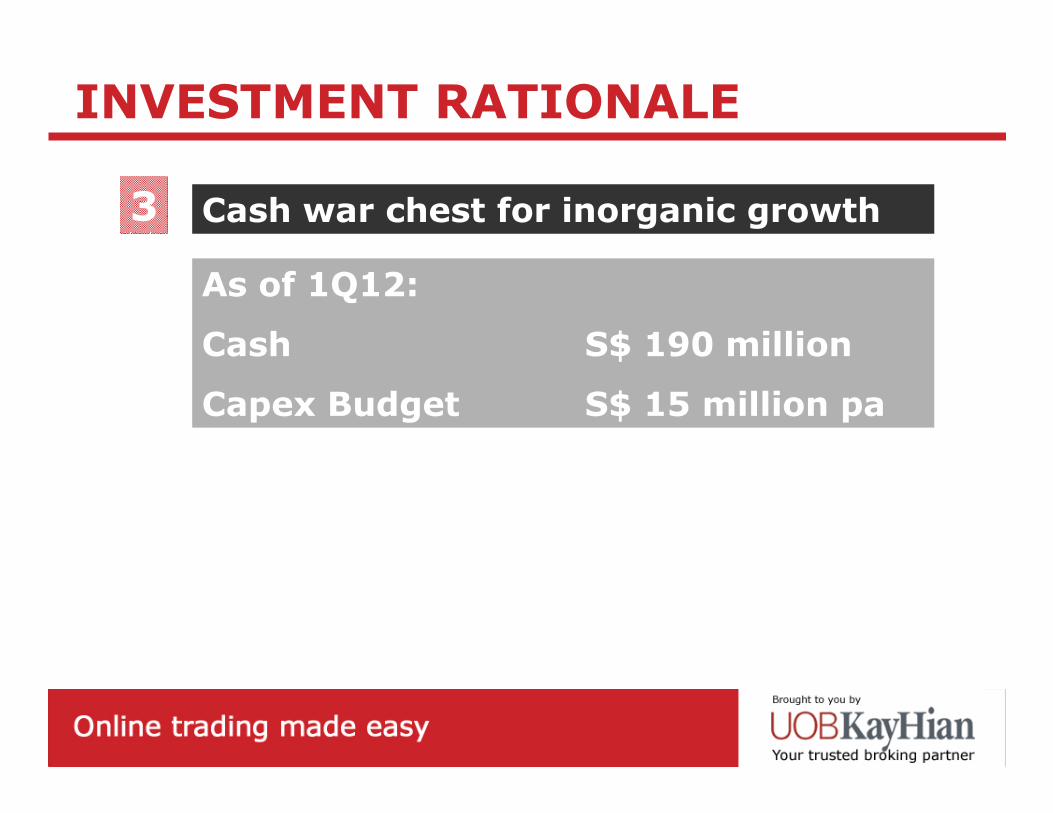

As of 1Q12:

Cash S$ 190 million

Capex Budget S$ 15 million pa

Cash war chest for inorganic growth

INVESTMENT RATIONALE

3

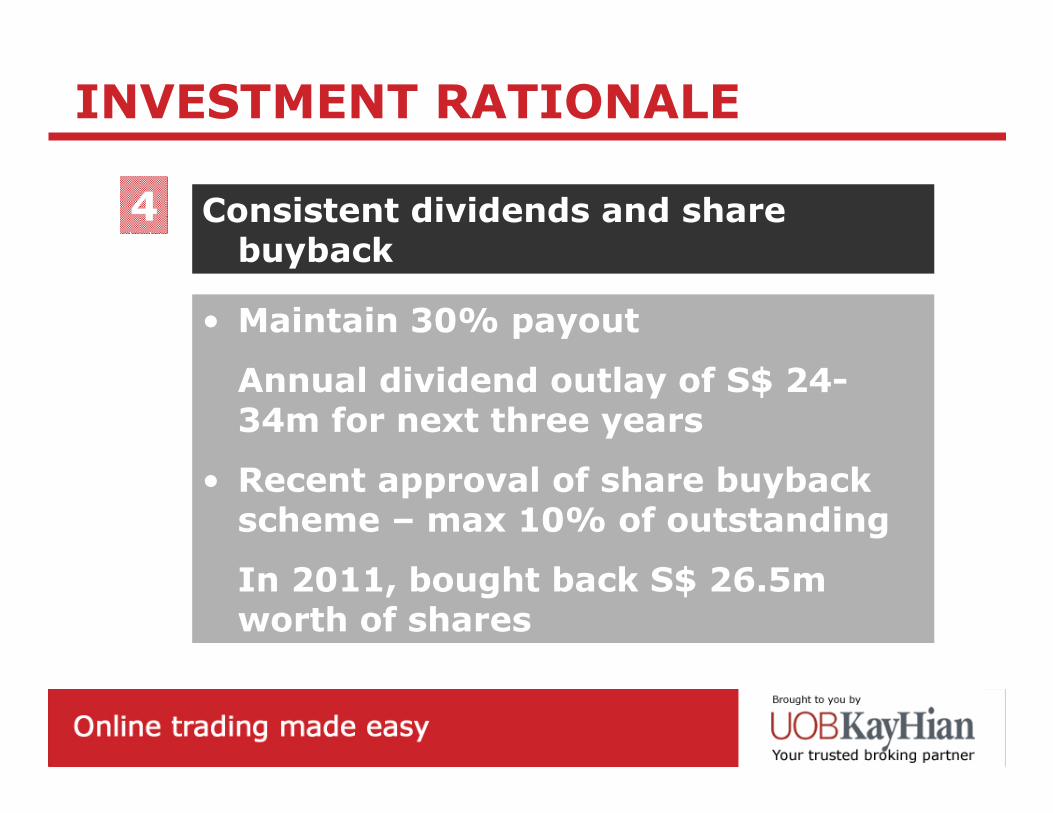

• Maintain 30% payout

Annual dividend outlay of S$ 24-34m for next three years

• Recent approval of share buyback scheme – max 10% of outstanding

In 2011, bought back S$ 26.5m worth of shares

Consistent dividends and share buyback

INVESTMENT RATIONALE

4

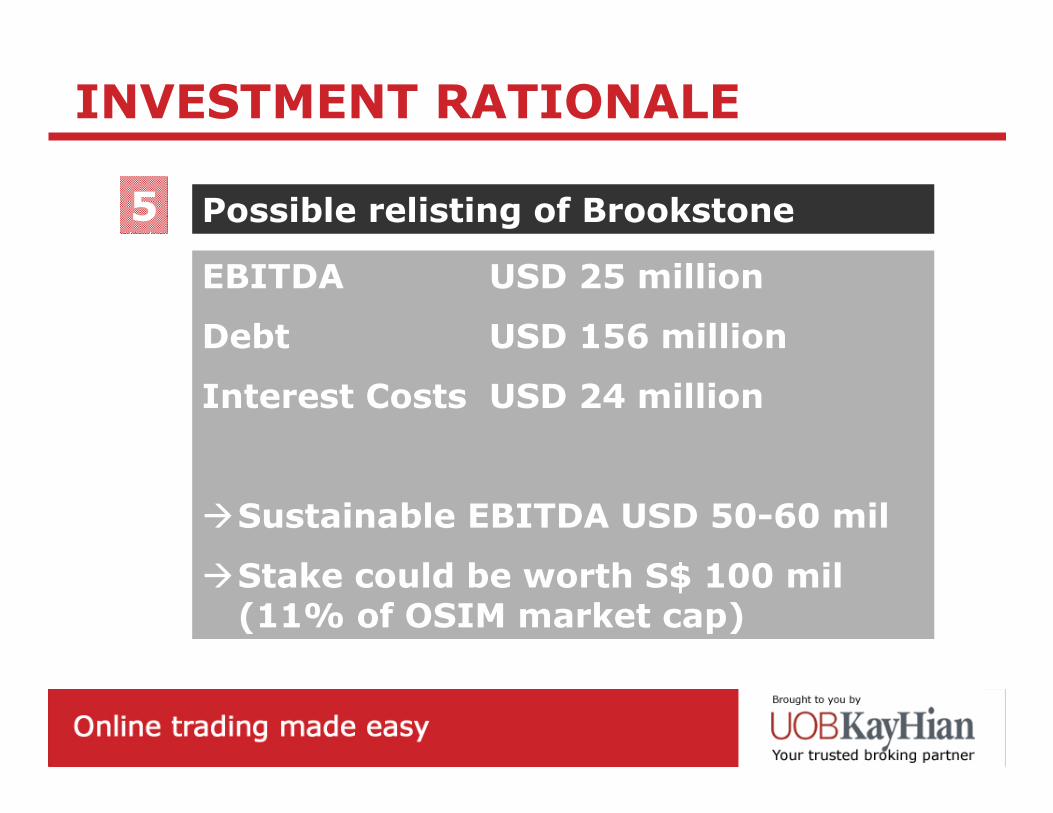

EBITDA USD 25 million

Debt USD 156 million

Interest Costs USD 24 million

�Sustainable EBITDA USD 50-60 mil

�Stake could be worth S$ 100 mil (11% of OSIM market cap)

Possible relisting of Brookstone

INVESTMENT RATIONALE

5

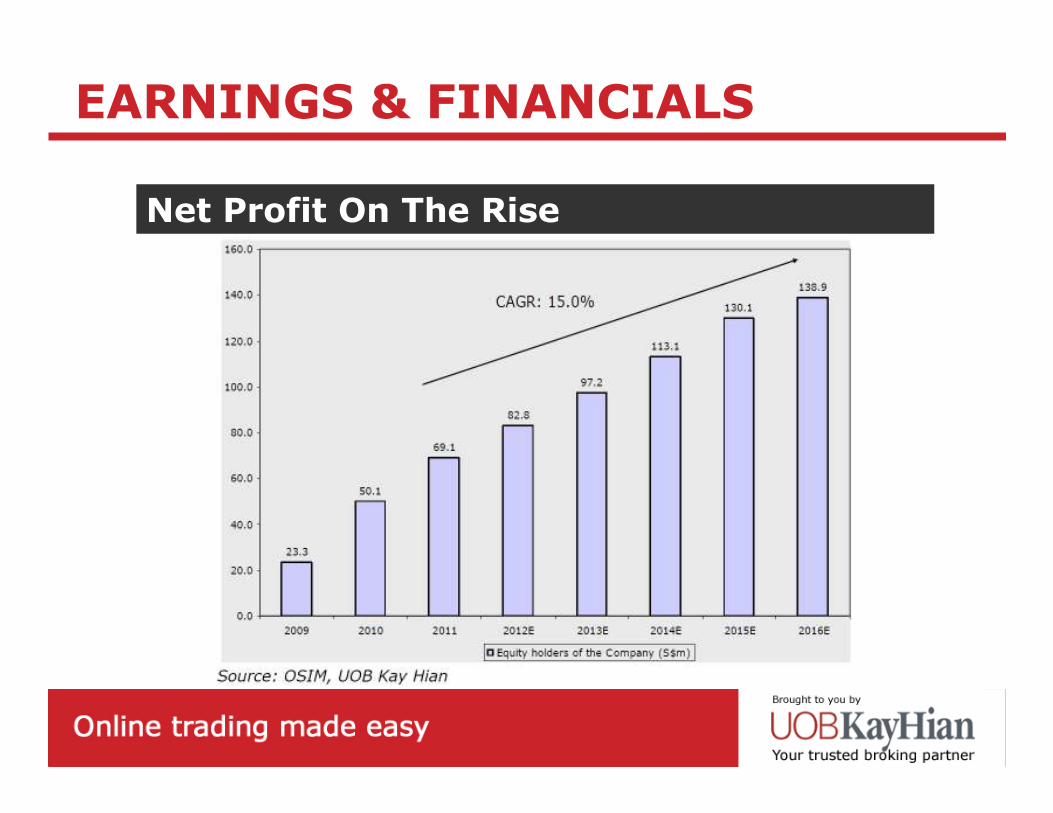

Net Profit On The Rise

EARNINGS & FINANCIALS

Net Profit On The Rise

EARNINGS & FINANCIALS

Expanding store network in China

Higher same-store sales

Improved margins from product innovation

Net Profit on the rise

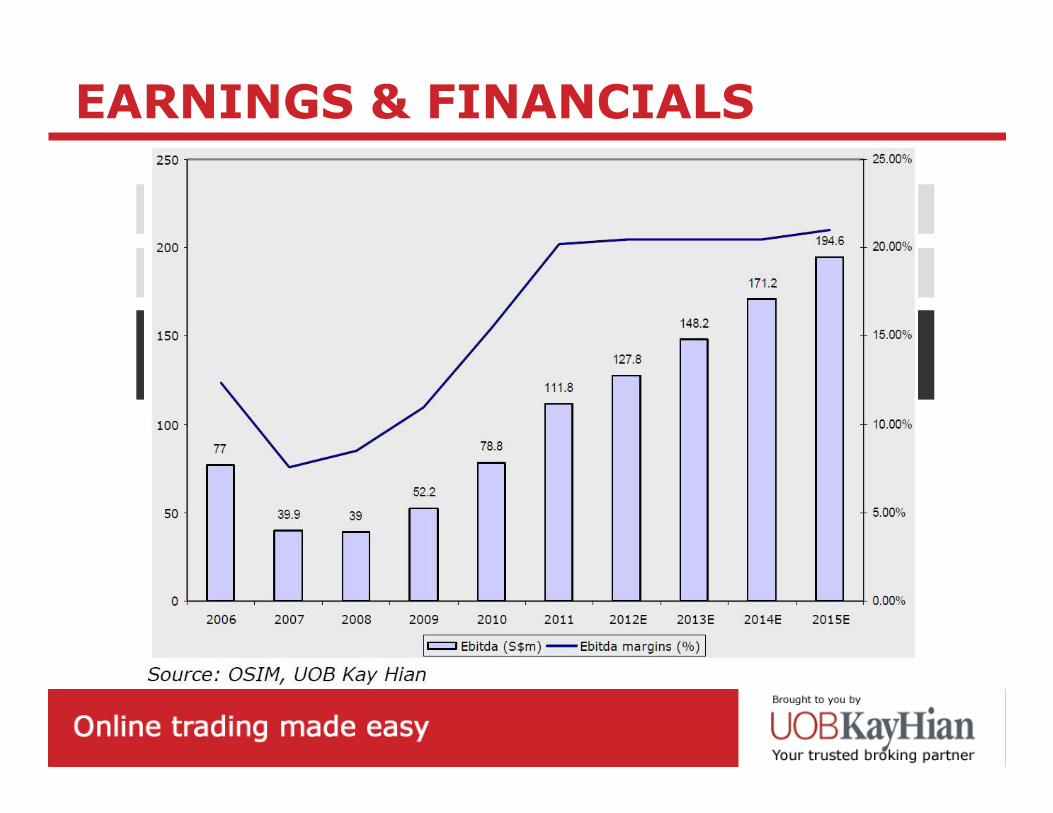

EARNINGS & FINANCIALS

Expanding retail points to drive sales

Strong EBITDA but margins should stabilize

Net Profit on the rise

EARNINGS & FINANCIALS

Expanding retail points to drive sales

Strong EBITDA but margins should stabilize

Net Profit on the rise

EARNINGS & FINANCIALS

Expanding retail points to drive sales

Strong EBITDA but margins should stabilize

Net Profit on the rise

EARNINGS & FINANCIALS

Better product mix

Higher productivity per man per outlet

Shift in manufacturing base from Japan to China

Expanding retail points to drive sales

Strong EBITDA but margins should stabilize

Net Profit on the rise

EARNINGS & FINANCIALS

Expanding retail points to drive sales

ROE to decline due to stronger equity base

Strong EBITDA but margins should stabilize

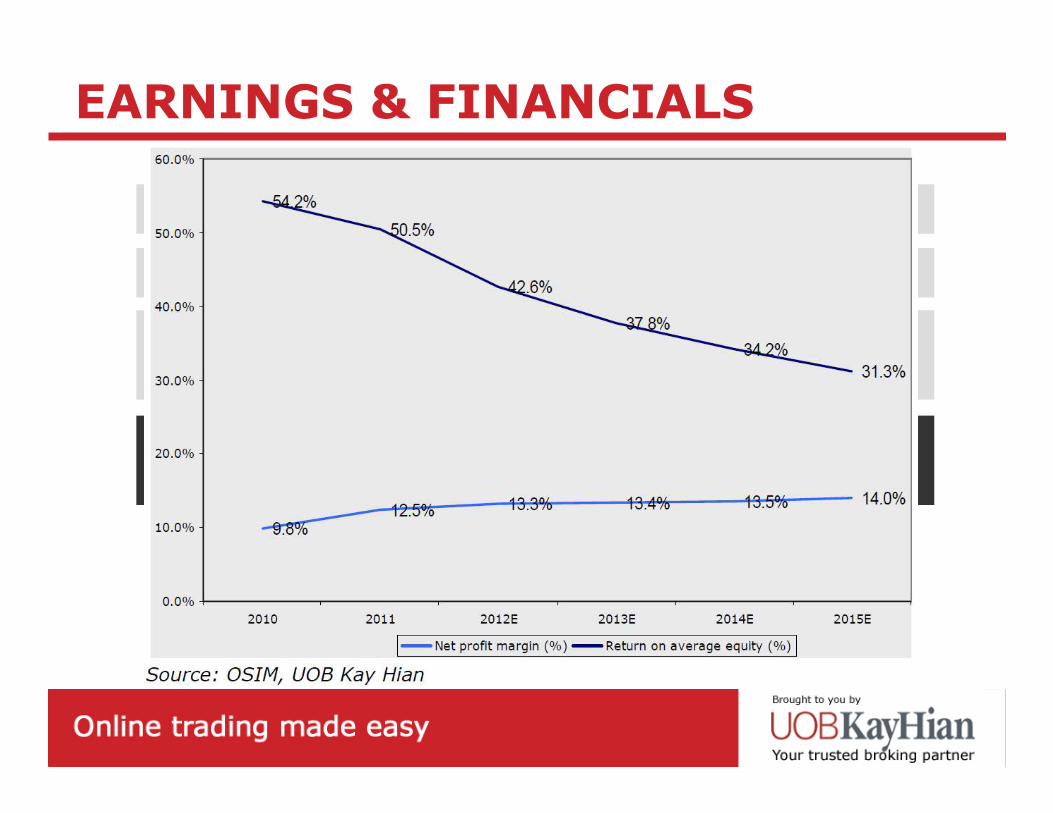

Net Profit on the rise

EARNINGS & FINANCIALS

Expanding retail points to drive sales

ROE to decline due to stronger equity base

VALUATION

S$ 1.61Target

15.0xP/E (3yr Histo)

BUY

a)Strong earnings growth on China expansion

b)Improvement in EBITDA margins from luxury products and leveraging on premium brand equity

c)Consistent dividends and share buyback

VALUATION

Premium valuation to peers:

RISKS & CATALYSTS

RISKS • China slowdown

• Increasing competition

• Execution risks in organic and inorganic expansion

RISKS & CATALYSTS

CATALYSTS • Earnings growth

• Strategic acquisitions

IEV HOLDINGS

AGENDA

OSIM INTERNATIONAL

BUMITAMA AGRI

A

B

C

Associate of IOI Corp (30.4% stake)

Indonesia-based pure upstream plantation player

Listed on Singapore Exchange on 12 Apr 2012

BACKGROUND

BACKGROUND

BACKGROUND

72,786119,162191,948Total

38%62%

1,6912,3094,000Riau

71,095116,853187,948Kalimantan

UnplantedPlantedLandbank(ha)

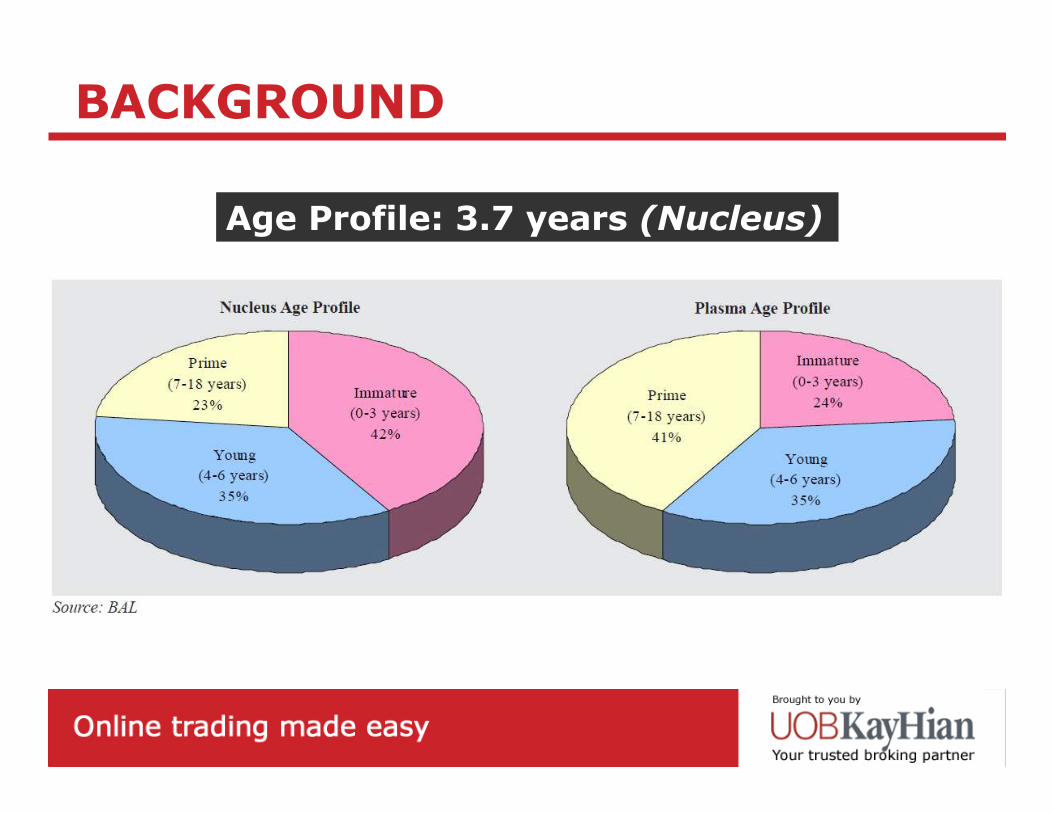

BACKGROUND

Age Profile: 3.7 years (Nucleus)

Expect CPO price to climb

INDUSTRY

• End of peak production growth

Expect CPO price to climb

INDUSTRY

• Declining inventory level given low production growth

Expect CPO price to climb

INDUSTRY

• Persistent weather woes

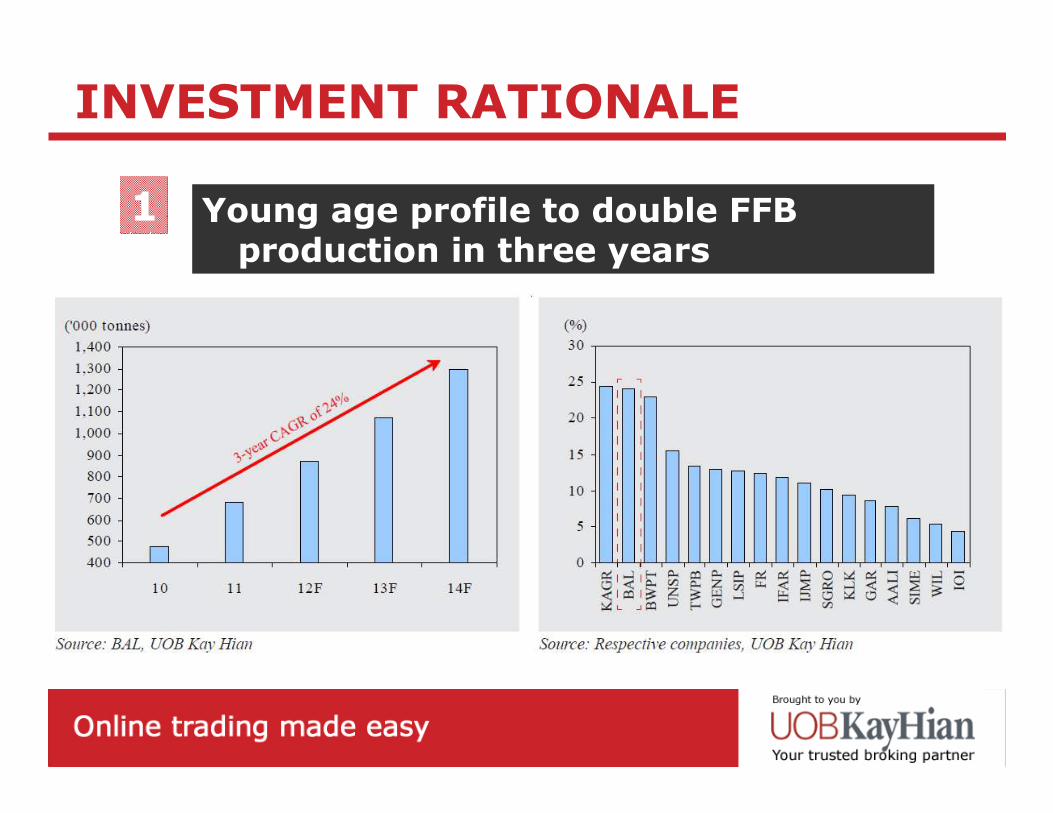

Young age profile to double FFB production in three years

INVESTMENT RATIONALE

1

Young age profile to double FFB production in three years

INVESTMENT RATIONALE

1

Young age profile to double FFB production in three years

INVESTMENT RATIONALE

1

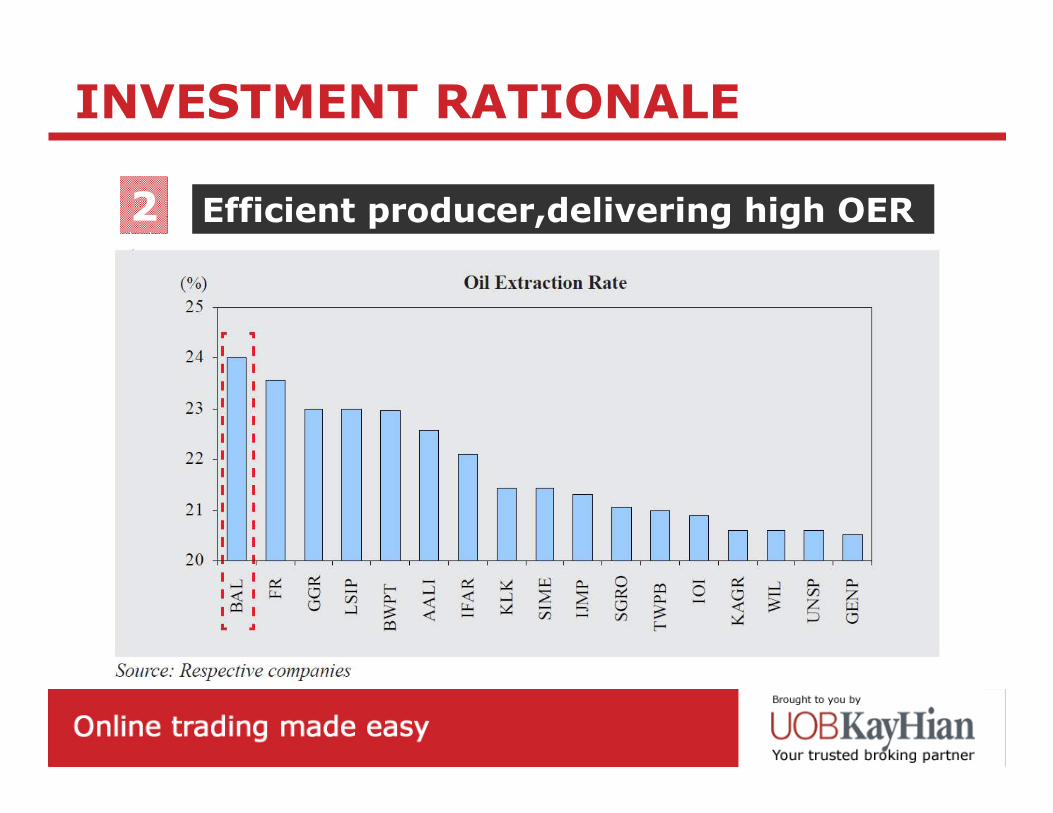

Efficient producer,delivering high OER

INVESTMENT RATIONALE

2

INVESTMENT RATIONALE

2

Newer mills

Good estate practice for harvesting and loose fruit collection

Efficient producer,delivering high OER

INVESTMENT RATIONALE

2 Efficient producer,delivering high OER

EBITDA margin to improve with more nucleus contributions

INVESTMENT RATIONALE

3

35.94423332009

EBITDA Margin (%)ExternalPlasmaNucleusFFB Processed (%)

41.92627472011

35.13525412010

15-18%13-15%45-65%EBITDA Margin

42.31925562014F

46.91328592013F

45.81529562012F

MillingPalm Plantation

+ Milling

Strong correlation between share price performance and production

INVESTMENT RATIONALE

4

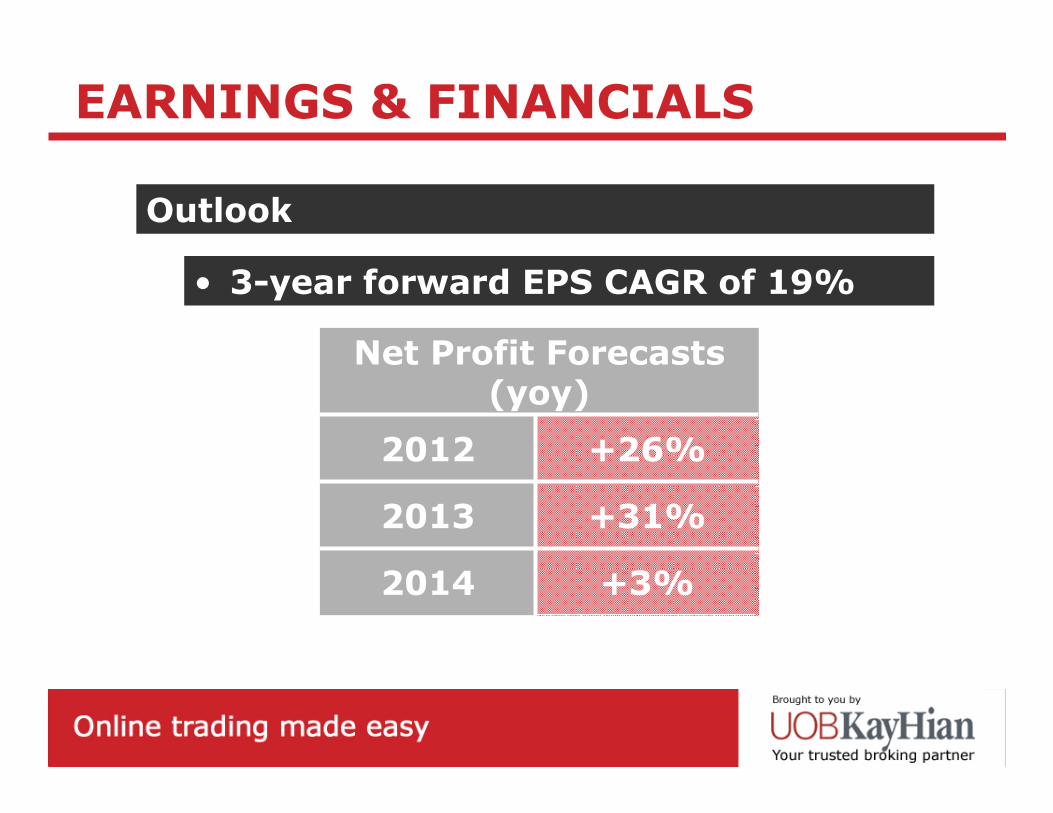

Outlook

EARNINGS & FINANCIALS

• 3-year forward EPS CAGR of 19%

Net Profit Forecasts (yoy)

+31%2013

+3%2014

+26%2012

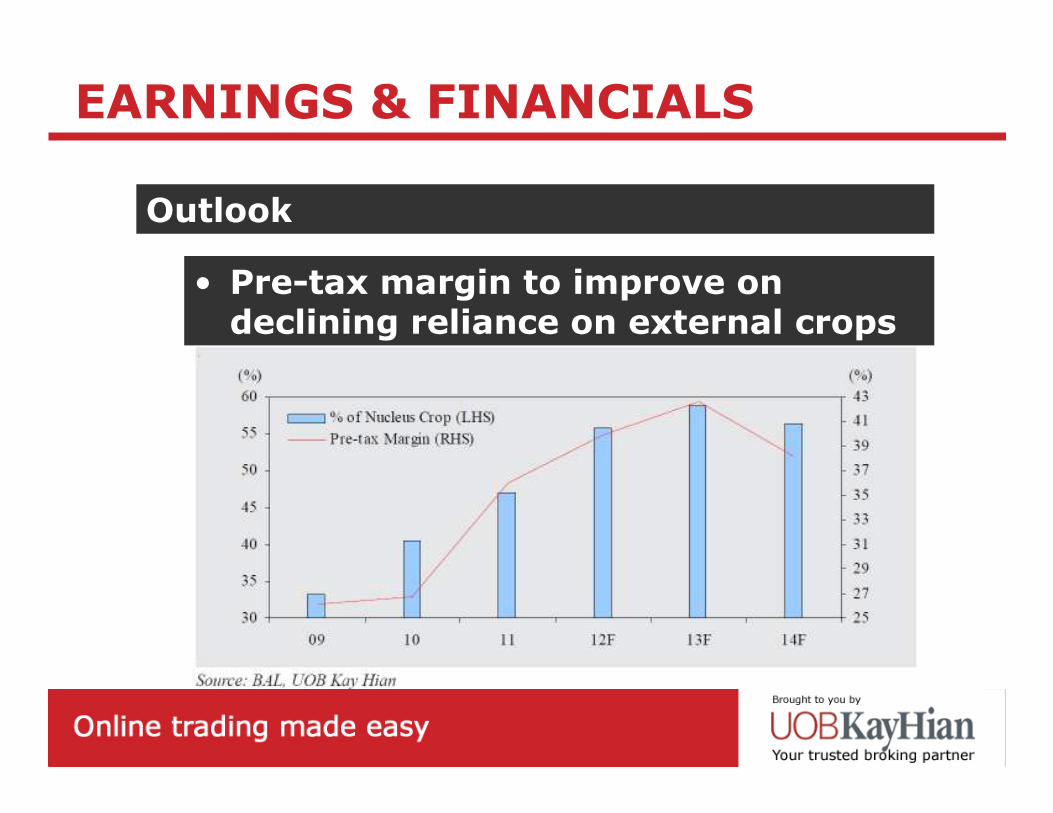

Outlook

EARNINGS & FINANCIALS

• Revenue to grow as production increases

Outlook

EARNINGS & FINANCIALS

• Pre-tax margin to improve on declining reliance on external crops

Outlook

EARNINGS & FINANCIALS

• High leverage to CPO price movement

Change In EPS For Every RM400/tonne Increase In CPO Price

+10.5%

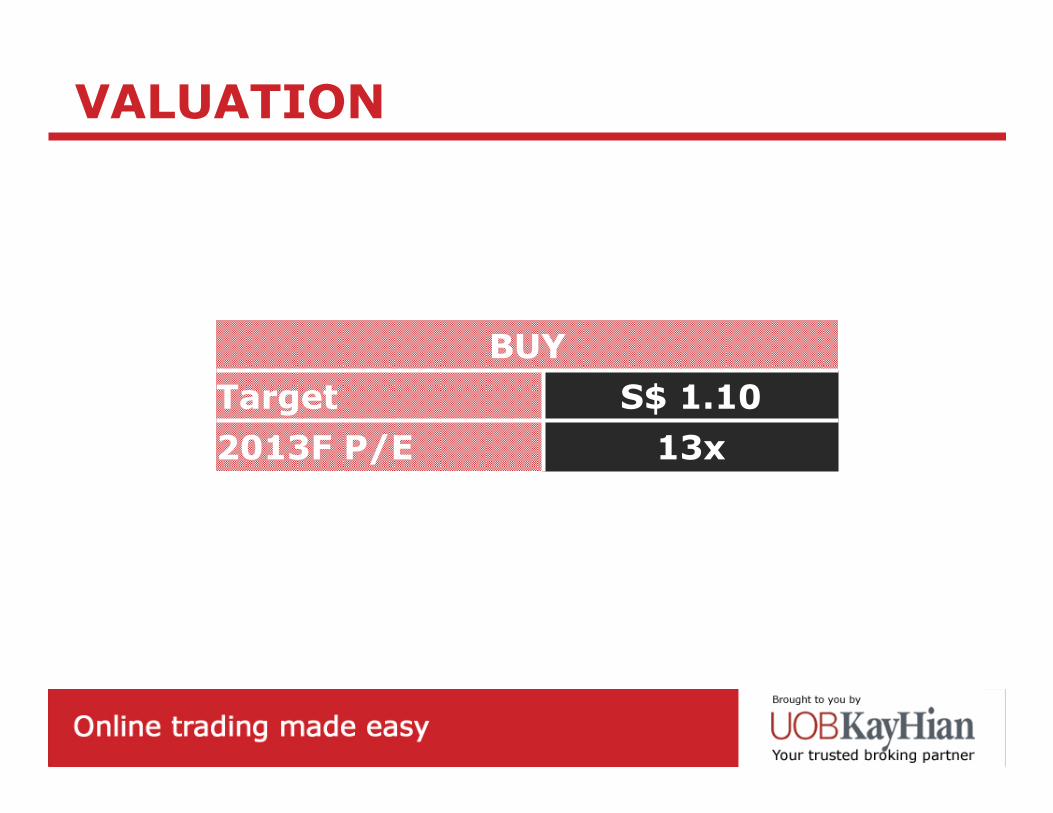

VALUATION

S$ 1.10Target

13x2013F P/E

BUY

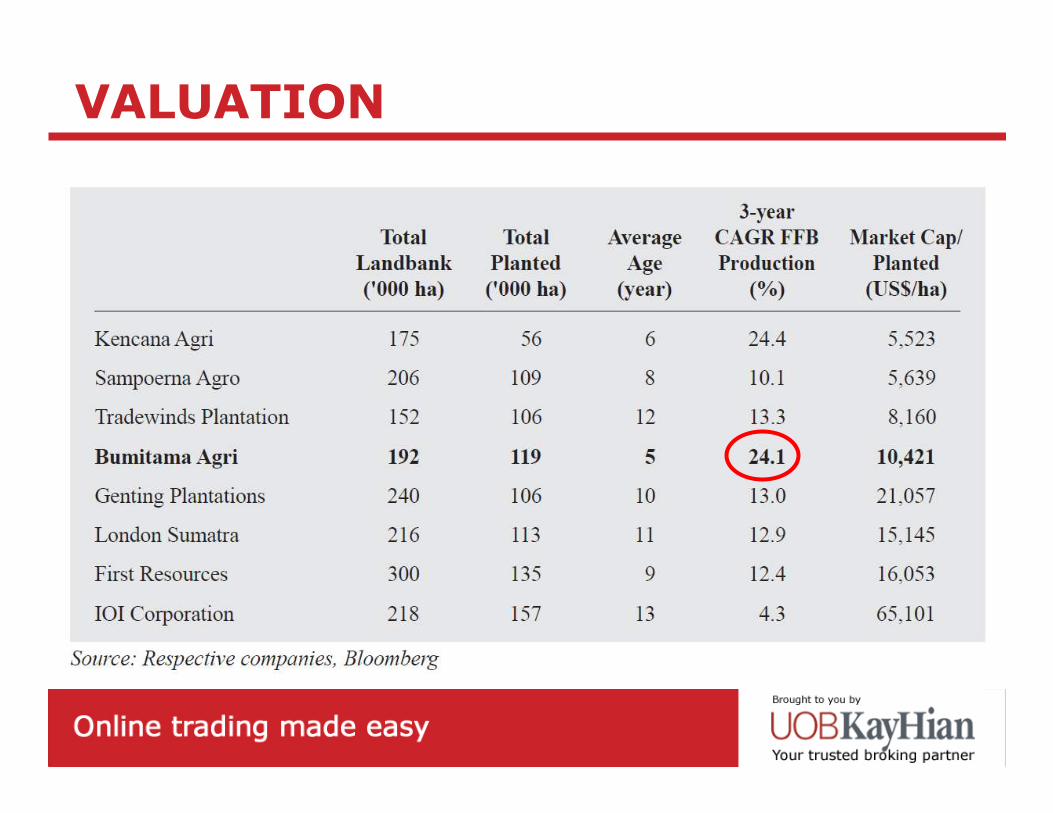

VALUATION

VALUATION

VALUATION

VALUATION

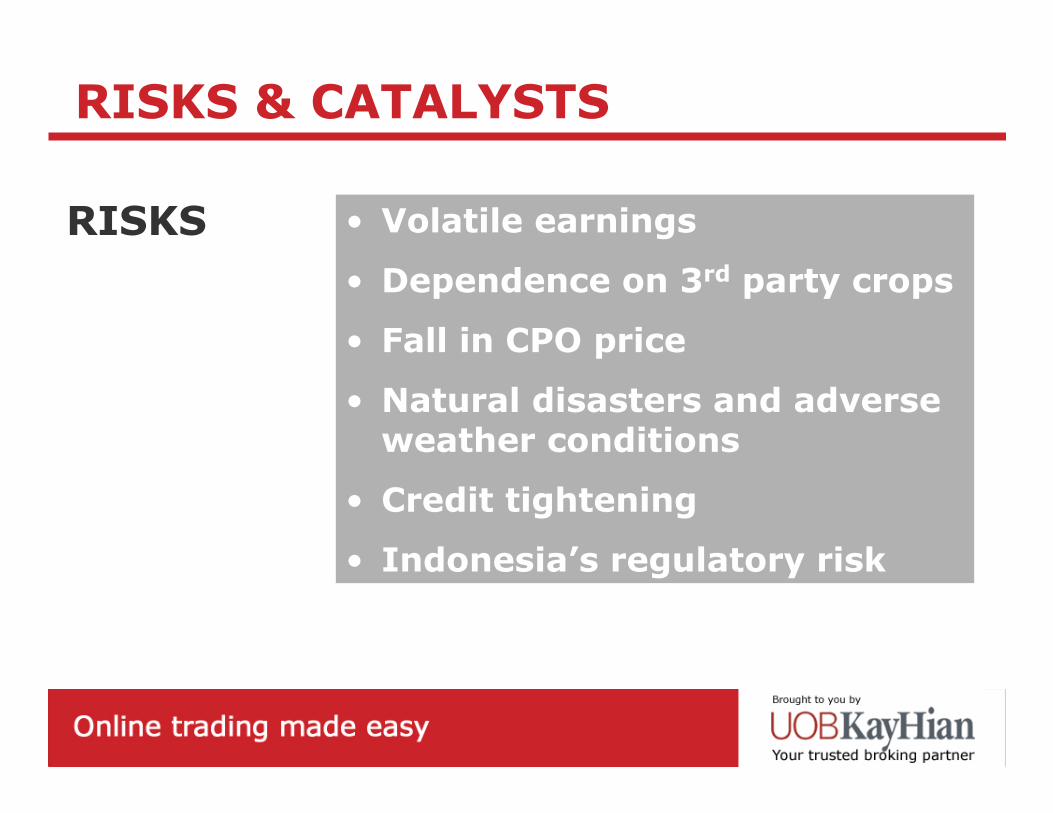

RISKS & CATALYSTS

RISKS • Volatile earnings

• Dependence on 3rd party crops

• Fall in CPO price

• Natural disasters and adverse weather conditions

• Credit tightening

• Indonesia’s regulatory risk

RISKS & CATALYSTS

CATALYSTS • Surge in CPO price

• High CPO demand in Indonesia

THANK YOUTHANK YOU