Embed Size (px)

Citation preview

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

1

SINGAPORE, THE

IMPACT INVESTING HUB OF ASIA?

A Comparison with Hong Kong

Maja Šoštarić September 2015

Lien Centre for Social Innovation White Paper

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

2

Copyright © 2015 by Maja Šoštarid All rights reserved. Published by the Lien Centre for Social Innovation. Singapore Management University, Administration Building, 81 Victoria Street, Singapore 188065 www.lcsi.smu.edu.sg

No part nor entirety of this publication may be reproduced or transmitted in any form or by any means, or stored in any retrieval system of any nature without the prior written permission of the Lien Centre. The views expressed by the author do not necessarily reflect those of the Lien Centre. Readers should be aware that internet websites offered as citations and/ or sources for further information may have changed or disappeared between the time this was written and when it is read. Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best efforts in preparing this publication, they make no representations and/ or warranties with respect to the accuracy and/ or completeness of the contents of this publication and specifically disclaim any implied warranties of appropriateness, merchantability and/ or fitness for any particular purpose. No warranty (whether express and/ or implied) is given. The advice and strategies contained herein may not be suitable for your situation. You should consult with a professional, as appropriate. Cover photo and design by Jared Tham

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

3

Contents About the Author 4

Acknowledgements 5

Executive Summary 6

Recommendations 7

Chapter 1 – Introduction 9

Chapter 2 – Impact Investing: An Honest Attempt to Debunk Some Common Myths 11

2.1 Basic Definitions 13

2.2 A Case for Venture Philanthropy and Impact Investing 15

2.3 Global Impact Investing Market 18

2.4 Challenges of Impact Investing 20

Chapter 3 – Impact Investing Potential of Singapore and Hong Kong 23

3.1 Market Size of Impact Investing in Asia 23

3.2 Philanthropy in Singapore and Hong Kong 25

3.3 Impact Investors Based in Singapore and Hong Kong 27

3.3.1 Impact Investing Funds in Singapore 29

3.3.2 Impact Investing Funds in Hong Kong 31

3.4 Commercial Impact Investors 34

3.5 Intermediaries 35

3.5.1 Regional Intermediaries Based in Singapore 35

3.5.2 Regional Intermediaries Based in Hong Kong 37

Chapter 4 – Government Activities in the Field of Social Enterprise and Impact Investing 38

4.1 Singapore Government 40

4.2 Hong Kong SAR Government 42

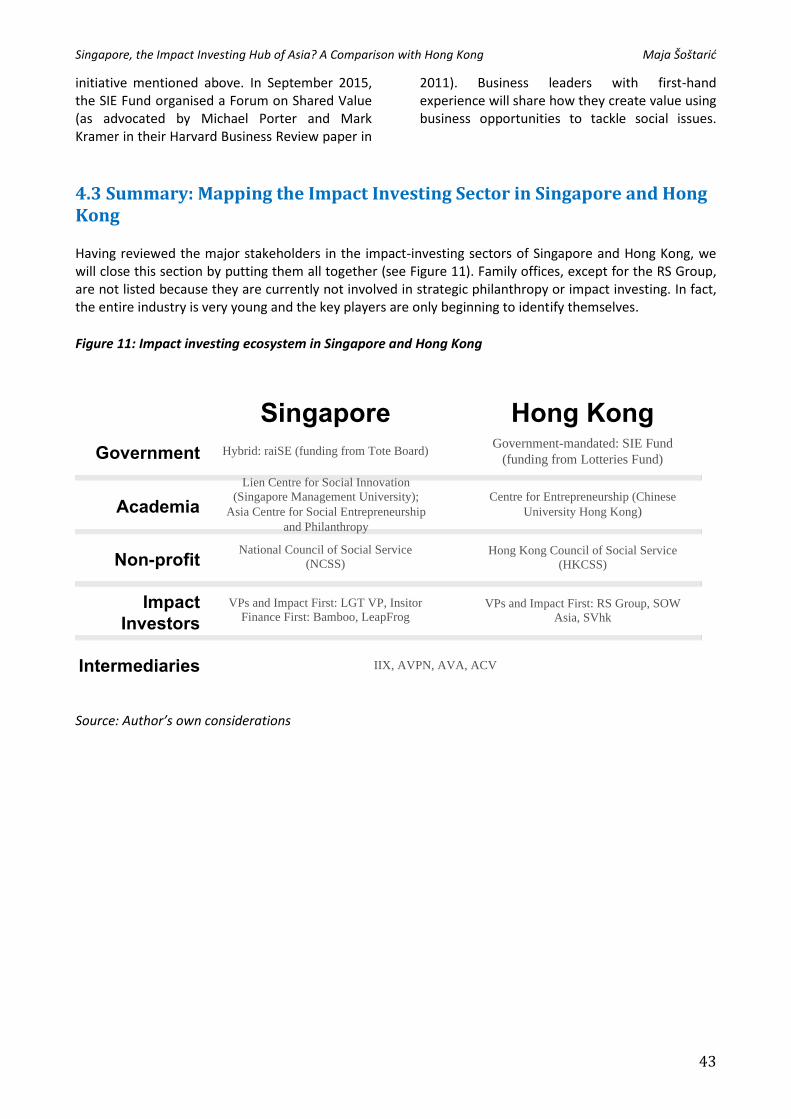

4.3 Summary: Mapping the Impact Investing Sector in Singapore and 42

Hong Kong

Chapter 5 – Conclusion: The Future of Venture Philanthropy and Impact Investing in 44

Singapore and Southeast Asia

References 46

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

4

About the Author

Dr Maja Šoštarić From June-August 2015, Maja did a residency at the Lien Centre, researching on impact investing in Asia. Besides her upcoming Master in Public Administration (MPA) degree from Harvard Kennedy School (expected in 2016), Maja has a PhD in Political Science (University of Vienna, with research stays in Paris and Osaka) and MA in Economics (Vienna University of Economics and Business Administration). She also attended the Diplomatic Academy of Vienna. At Harvard, Maja is focusing on business and government (finance in particular). She is also a CFA candidate. Currently, Maja works as a researcher at Harvard Kennedy School and is co-president of the Harvard Kennedy School Finance and Macro Professional Interest Council. In total, she has six years of work experience in finance, diplomacy, research and non-profit consulting. Maja is fluent in six languages and working toward fluency in further four. So far she has lived, worked and studied in nine countries of Europe, Asia and North America.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

5

Acknowledgements The author is deeply indebted to the following people (in alphabetical order) for their generosity over the course of this study:

Singapore

Asian Venture Philanthropy Network Kevin Teo

BagoSphere Lee Zhihan

Harvard Kennedy School alumni Kevin Tan

LGT Venture Philanthropy En Lee

Lien Centre for Social Innovation, SMU Jonathan Chang, Jared Tham,

Watanan Petersik, Shirley Pong

National Council for Social Service Ria Bhatnagar

National University of Singapore Rob John

raiSE, Singapore Centre for Social Enterprise Chloe Huang, Xin Yun Lim, Anna Fu

Singapore Economic Development Board Agnes Chew, Isabella Oh

Hong Kong

Asia Value Advisors Philo Alto

J.P. Morgan Chase, Global Philanthropy Asia-Pacific Arian Hassani

RS Group Annie Chen

Social Ventures Hong Kong Lehui Liang

Social Innovation And Entrepreneurship

Development Fund (SIE) Fund

Patricia Lau, Susanna Chui

SOW Asia Scott Lawson

UBS, Global Philanthropy Asia-Pacific Mario Knoepfel

I wish to express my appreciation and sincere gratitude to the Lien Centre for Social Innovation for hosting me with the purpose of conducting this research. In particular, thanks to Director Jonathan Chang for inviting me to Singapore to experience, first-hand, the joy of living in the Little Red Dot; Jared Tham for his invaluable help in connecting me to many relevant stakeholders and providing me with excellent research suggestions; Board member Watanan Petersik for her useful review of my initial research outline; as well as Shirley Pong for her fantastic administrative assistance. I am also grateful to everyone who reviewed my first draft. Of course, special thanks goes to Harvard Kennedy School. Generous funding from its Summer Internship Fund as well as the Mossavar-Rahmani Center for Business and Government made my research stays in Singapore and Hong Kong possible.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

6

Executive Summary

Impact investing is a nascent subsector within social finance. It can be summarised as “doing good while doing well”, or achieving social impact by supporting social enterprises while generating financial returns. While being an innovative concept, impact investing bears a number of challenges: Who can qualify as an impact investor? How are investees selected? How do investors and investees find each other? How is social impact measured? What financial returns are acceptable?

Attempting to answer these and other questions, this report looks at the impact investing potential of Singapore, home to regional impact investing intermediaries such as the Asian Venture Philanthropy Network (AVPN) and Impact Investing Exchange (IIX Asia). Four international impact investing funds, often Finance First investors, have their offices in Singapore. Local initiatives in this sense, such as DBS Foundation and the Singapore Centre for Social Enterprise (raiSE), are new but certainly welcome.

Singapore has around 300 social enterprises, many of which focus on Southeast Asia. The Singapore government has so far opted for a series of smaller, sporadic and decentralised initiatives to promote impact investing.

For the sake of comparison, the report looks at a comparable economy that is also an advanced financial centre. Hong Kong’s social enterprises as well as impact investing intermediaries are primarily focused on local issues. Its impact investors, unlike Singapore’s, are similar to venture philanthropists and can be categorised as Impact First investors. The Hong Kong SAR Government also manages a proper centralised impact investing fund.

In a society with an entrenched culture of giving, most of Singapore’s philanthropy comes from corporations and family offices. Unsurprisingly, this report has several target audiences, notably Singapore’s family offices, foundations and high net worth individuals (HNWIs).

Given a high number of social enterprises which lack funding and find themselves in between the early and scale-up stages (the “Missing Middle”, see Section 2.2), the report advises family offices and HNWIs to move from traditional philanthropy to venture philanthropy, and eventually to impact investing. The report also addresses a growing number of intermediaries in impact investing as well as the Singapore government.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

7

Recommendations

To the Singapore government, in particular the Ministry of Family and Social Development and the Singapore Economic Development Board: 1. In line with the London Principles for better

governance in impact investing, promote the Clarity of Purpose of impact investing (see Section 4). Towards this end, consider drafting a document entitled “Impact Investing Roadmap for Singapore 2015–2020” or the like, to clearly articulate the government’s ambitions for the sector’s development.

2. With the objective of building Institutional Capacity, consider either repurposing the existing National Council of Social Service (NCSS) unit for New and Emerging Initiatives, or setting up a new unit within the Ministry of Social and Family Development (MSF) or the Singapore Economic Development Board (EDB). That unit could serve as a focal point between the investors, the non-profit sector, the intermediaries and the Government. Its creation would also serve to avoid the risk of bubble creation in Singapore’s growing impact investment market by channelling existing and future resources more efficiently.

3. With the scope of promoting the principles of

Stakeholder Engagement and Market Stewardship and aiming at a higher level of resource centralisation, consider creating a central impact investing fund that could incorporate and expand the existing

resources of raiSE and would also be financed through the Tote Board. Also, consider creating a task force comparable to that of the Hong Kong Social Innovation and Entrepreneurship Fund (SIE Fund), consisting of relevant public officials, entrepreneurs, investors and academics. The task force would advise on the optimal way of structuring the potential fund, and could alternatively substitute creating the unit from point 2 above.

4. To further facilitate social entrepreneurship

and impact investing in Singapore, consider introducing a new and improved legal framework that would enable potential social entrepreneurs to set up legal entities equivalent to hybrids of charities and commercial entities, and potentially even outsource them to the region. Such a framework, incorporating tax exemptions, deductions and other benefits, would be equally beneficial to the corporations, foundations and family offices contemplating shifting their endowments towards venture philanthropy and impact investing.

5. Finally, remain open to various innovations of

social finance. Consider and evaluate the feasibility of introducing emerging pay-for-success schemes such as social impact bonds (SIBs).

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

8

To HNWIs, angel investors, family offices, family and corporate foundations, banks, aspiring venture philanthropists and existing impact investors:

1. Following the (so far) unique example of the DBS Foundation, consider creating a ”made-in-Singapore” venture philanthropy and impact investing fund out of your existing endowments and resources. Such fund(s) would demonstrate the determination of Singapore’s banks, family offices and corporations to position the country as the regional and/or Asian hub for impact investing and development finance.

2. Acknowledge that the current opportunities for Finance First impact investing and market-rate returns are rather scarce in Southeast Asia. Streamline more resources

towards promoting seed and early-stage ventures to multiply the number of business accelerators, and mentoring and coaching programmes.

3. Consider experimenting with dual structure

funds, consisting of both a charitable foundation and an investment fund. Such a structure would greatly contribute to filling the current gap in the impact investing market by catering to the needs of early stage companies in need for venture philanthropy as well as advanced enterprises looking for more sophisticated forms of impact investing.

To impact investing intermediaries:

1. Promote further research on the sector to fill the current gap in thought leadership in impact investing in Southeast Asia. Work towards educating potential venture philanthropists on opportunities of the sector, rather than contributing to the current hype around impact investing. If you are a commercial bank, make an effort to educate your HNWI-clients on the benefits of strategic philanthropy and impact investing.

2. Work together with existing and aspiring venture philanthropists and investors to build efficient and all-encompassing business pipelines, incubators and accelerators for

early-stage businesses because they are the backbone of the nascent impact investing sector.

3. With regard to deal flow, work closely with

investors to facilitate more sophisticated stages of the investment process, such as deal execution and impact assessment. Many potential investors do not end up closing otherwise attractive deals due to lack of information and high transaction costs. More efficient and succinct methods of intermediation would help to significantly reduce those costs.

To social entrepreneurs based and/or active in Singapore and the region:

1. Make use of all existing resources (mentors, accelerators, trainings) and available networks in order to better position yourself and make your enterprise more investable. Consider diversifying your product range because that will greatly facilitate your attractiveness to investors.

2. If your enterprise is in a more advanced or mature stage and capable of addressing regional social issues, consider expansion into the less developed but very large regional markets such as China, India or Indonesia.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

9

Chapter 1 – Introduction Bliss Restaurant and Catering Pte Ltd is a Singapore-based restaurant chain with multiple outlets hiring disadvantaged and disabled persons. Based on a job integration model, the company won the 2013 President’s Challenge Social Enterprise Award. As with any growing enterprise, it is also contemplating expansion.

Yet Bliss also needs cash to survive. The fact that it does good for the community will not influence its financial statements or impress its auditors. If it encounters a cash flow situation, traditional banking services1 with high interest rates will not be of help, unless Bliss can provide them with substantial loan guarantees. That is where impact investing comes in.

Several events have helped shape impact investing globally. Besides the rise of microfinance with Grameen Bank, the emergence of global impact investing funds like Acumen have begun to substitute traditional international development organisations. Another push for impact investing came from a totally different corner - the global financial crisis that started in 2007/2008. With major banks in ruins and the global financial sector near collapse, some investors turned to social finance and became more vocal about socially responsible investing (i.e. staying away from ‘sinful’ industries such as alcohol, tobacco or gambling).

Gradually, what some consider a brand new asset class, impact investments have seen the light of day. Such investments are placed in companies, organisations and funds with the intention to generate social and/or environmental impact alongside a financial return. They can be made in both emerging and developed markets, and target a range of returns from below-market to market rate, depending upon circumstances. Despite much interest globally, the sector is still in the relatively nascent stage outside the United States (US) and United Kingdom (UK). The belief that one can either do good (in terms of charity) or do well (in terms of commercial success), but not both, still seems to be widespread.

1 Some banks are the exception. Singapore’s DBS Bank has

preferential interest rates for social enterprises.

Upon reflection, are social enterprises like Bliss necessary? In the 50 years since its independence, Singapore has turned from a third-world nation to the world’s third-richest country by GDP per capita (PPP) and a global financial centre with the staggering figure of S$1.4 trillion (ca. US$1 trillion) of total assets under management (AUM) on its territory.2

Having said that, Singapore is not without problems either. According to previous research from the Lien Centre for Social Innovation (LCSI)3 Singapore has one of the highest Gini coefficients (0.472 in 2012) among developed countries, indicating very high levels of inequality. Similarly, 12–14% of Singaporeans were reported to live under the unofficial poverty line of S$1,500 (ca. US$1,000) per month, as the official poverty line does not exist. Moreover, almost one-third of Singapore’s total labour force of 3.44 million people are foreign low-skilled migrant workers living in relative poverty. Especially disadvantaged populations are the elderly, single parents, disabled and migrants.4 Therefore, the argument that Singapore does not need social enterprises does not hold; local initiatives such as Bliss are more than welcome.

Social enterprises based in Singapore have a much larger regional market at their disposal. In Southeast Asia5, the disparity in wealth is even greater. The richest country after Singapore and (gas- and petroleum-abundant) Brunei is Malaysia, with GDP per capita (PPP) about one-third of Singapore’s (US$82,000 vs. US$24,000).

2 See Monetary Authority of Singapore,

www.mas.gov.sg/Singapore-Financial-Centre/Overview/Wealth-Management-and-Insurance.aspx.

3 See Lien Centre for Social Innovation (2015): A Handbook

on Inequality, Poverty and Unmet Social Needs in Singapore.

4 See the most recent research of the Lien Centre on unmet

social needs in Singapore: Elderly Population in Singapore (2015), People with Physical Disabilities in Singapore (2015) and Single-Parent Families in Singapore (2015), http://lcsi.smu.edu.sg/research/.

5 Throughout this report, when referring to Southeast Asia,

we refer to Indonesia, Malaysia, Singapore, Philippines, East Timor, Brunei, Cambodia, Laos, Myanmar, Thailand and Vietnam.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

10

Other Southeast Asian GDPs are far lower when compared to the Malaysian figure.6

The objective of this paper is to investigate whether Singapore has the potential of becoming a successful rival to global impact investing hubs like New York, Geneva or San Francisco.7 Previous research from LCSI suggests that the philanthropic culture is substantial in Singapore due to a large number of HNWIs and family offices and foundations engaged in traditional philanthropy.

To assess the potential of the impact investing market in a well-developed financial environment, Hong Kong (population 7.2 million), an economy of comparable size and with somewhat more serious social problems, will be investigated (Chapters 3 and 4). This will help us draw relevant conclusions for the future of impact investing in Southeast Asia (Chapter 5) and give recommendations to relevant Singapore stakeholders.

6 See International Monetary Fund, World Economic

Outlook Database (2014). 7 See Straits Times, “S’pore ‘can be a good impact investing

hub’”, http://business.asiaone.com/personal-finance/news/spore-can-be-good-impact-investing-hub

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

11

Chapter 2 – Impact Investing: An Honest Attempt to Debunk Some Common Myths

The hype around impact investing which has caused many to jump on the bandwagon, in the opinion of the author, is rather unfortunate. Nowadays, many potential investors dismiss impact investing as just another trendy buzzword, while others do not really understand it.

Adaptive learning often gets confounded with blindly joining the hype. Reckless attempts at exporting ideas at any cost run the risk of blatantly generalising both the problem and solution. Such trends often produce crowds of enthusiasts without resulting in tangible impact.

What is more, traditional investors are often baffled by impact investing, and they are not entirely to blame. With three-quarters of impact investors targeting and achieving market-rate returns (see Section 2.3), are we not merely talking about standard commercial investing? What is so altruistic about market-rate investments? Why invent another name to make it all sound better?

This paper sheds light on why impact investing is not just another buzzword, why it deserves to survive the hype around it, what its different facets are and the extent to which it is distinct from other types of social finance. Having said that, one should remember that impact investing is a small subsector of social finance, and not its equivalent, as will be discussed below. Impact investing is thus a specific, narrow concept that targets only a small range of social enterprises. Equating impact investing to any type of investment in a social enterprise is one of the most common misunderstandings of the concept.

Also, proper impact investing should never be one-size-fits-all. Different social problems require tailored solutions, which can be found in philanthropy, development finance or commercial investments. Impact investing is not a panacea. There are many myths around impact investing and, for this purpose, some common ones are summarised in Box 1.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

12

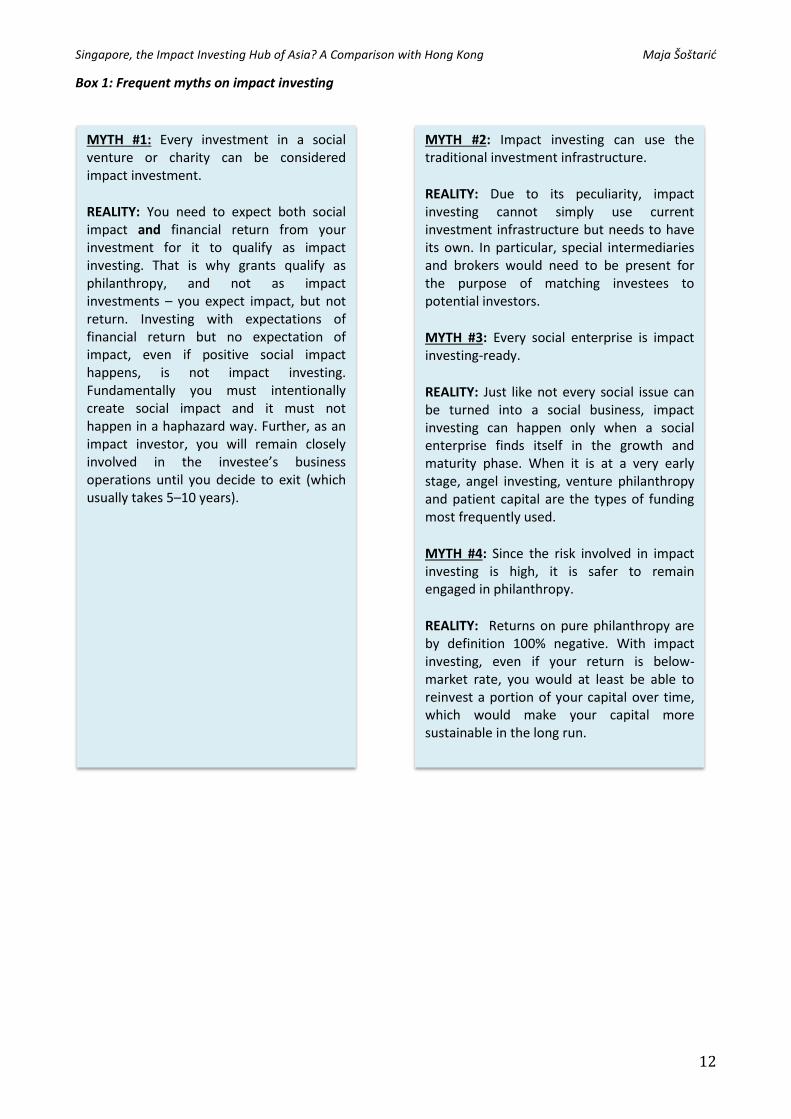

Box 1: Frequent myths on impact investing

MYTH #1: Every investment in a social venture or charity can be considered impact investment.

REALITY: You need to expect both social impact and financial return from your investment for it to qualify as impact investing. That is why grants qualify as philanthropy, and not as impact investments – you expect impact, but not return. Investing with expectations of financial return but no expectation of impact, even if positive social impact happens, is not impact investing. Fundamentally you must intentionally create social impact and it must not happen in a haphazard way. Further, as an impact investor, you will remain closely involved in the investee’s business operations until you decide to exit (which usually takes 5–10 years).

MYTH #2: Impact investing can use the traditional investment infrastructure.

REALITY: Due to its peculiarity, impact investing cannot simply use current investment infrastructure but needs to have its own. In particular, special intermediaries and brokers would need to be present for the purpose of matching investees to potential investors.

MYTH #3: Every social enterprise is impact investing-ready.

REALITY: Just like not every social issue can be turned into a social business, impact investing can happen only when a social enterprise finds itself in the growth and maturity phase. When it is at a very early stage, angel investing, venture philanthropy and patient capital are the types of funding most frequently used.

MYTH #4: Since the risk involved in impact investing is high, it is safer to remain engaged in philanthropy.

REALITY: Returns on pure philanthropy are by definition 100% negative. With impact investing, even if your return is below-market rate, you would at least be able to reinvest a portion of your capital over time, which would make your capital more sustainable in the long run.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

13

2.1 Basic Definitions

This section elaborates on three essential questions: the what, the who and the how of impact investing. More sophisticated questions will be addressed later.

a) What is impact investing?

Impact investing as a term was coined in 20078, but the concept itself has existed for centuries. Bugg-Levine and Emerson (2011) note that investing with the purpose of creating some sort of social impact was rather common even to 17th-century Quakers who sought to align their social values and investments.9

So what is impact investing? A report by J.P. Morgan defines it as “investments intended to create positive impact beyond financial return”. As such, these investments “require the management of social and environmental performance (…) in addition to financial risk and return.” 10

This definition was very welcome due to a flood of other terms being used interchangeably to denote various forms of social finance, namely: socially responsible investing; mission-driven investing; value-based investing; sustainable and responsible investing; triple bottom-line; blended value; environmental, social and governance (ESG)-oriented finance; venture philanthropy; and many more synonyms.

Three main elements distinguish impact investing from these other notions:

(1) Intentionality: a proactive stance that minimises the potentially negative effects

8 See Bugg-Levine and Emerson (2011), Impact Investing:

Transforming How We Make Money While Making a Difference.

9 Moreover, large multilateral development organisations

such as the International Finance Corporation, or country-specific investment offices such as the London-based Commonwealth Development Corporation, the US Overseas Private Investment Corporation, the German Investment Corporation and the Netherlands Development Finance Corporation have in fact been making impact investments since their inception; only back then, nobody thought of calling their transfers “impact investing”.

10 See J.P. Morgan (2010), Impact Investments:– An Emerging Asset Class.

of investments (detected during “negative screening”);

(2) positive social and/or environmental impact which is measurable; and

(3) clear expectation of financial returns as much as social impact.

In 2009, the Global Impact Investing Network (GIIN) was launched by J.P. Morgan, the Rockefeller Foundation and USAID. That same year, the first of two pioneer reports on impact investing was released. Investing for Social and Environmental Impact: A Design for Catalyzing the Emerging Industry was drafted by Monitor Institute, which is part of Deloitte Consulting. The first of its kind, this report demonstrated an impressive level of objectivity, correctly predicting potential short- to mid-term challenges for the impact investing industry. It showed how impact investing is bound to remain a very small niche: while 2009 global AUM equalled US$50 trillion and socially responsible investing US$7 trillion, the potential market size of impact investing was estimated at “only” US$500 billion, which is still larger than the estimated US$310 billion philanthropy sector in the US.

The second pioneer report on impact investing is the aforementioned J. P. Morgan report from 2010 that represents the first attempt to quantify impact investing in a more elaborate manner. It argued for impact investing as a separate asset class that could not simply be categorised under “fixed income”, “equity” or “cash”. The report famously estimated the figures that are to-date always mentioned in the context of impact investing: the US$400 billion to US$1 trillion market potential in impact investments until 2020, with potential profits reaching US$667 billion. Since that report, J. P. Morgan has regularly surveyed fund managers and other impact investors, and findings from their 2015 survey will be briefly mentioned in Section 2.3.

b) Who is involved in impact investing?

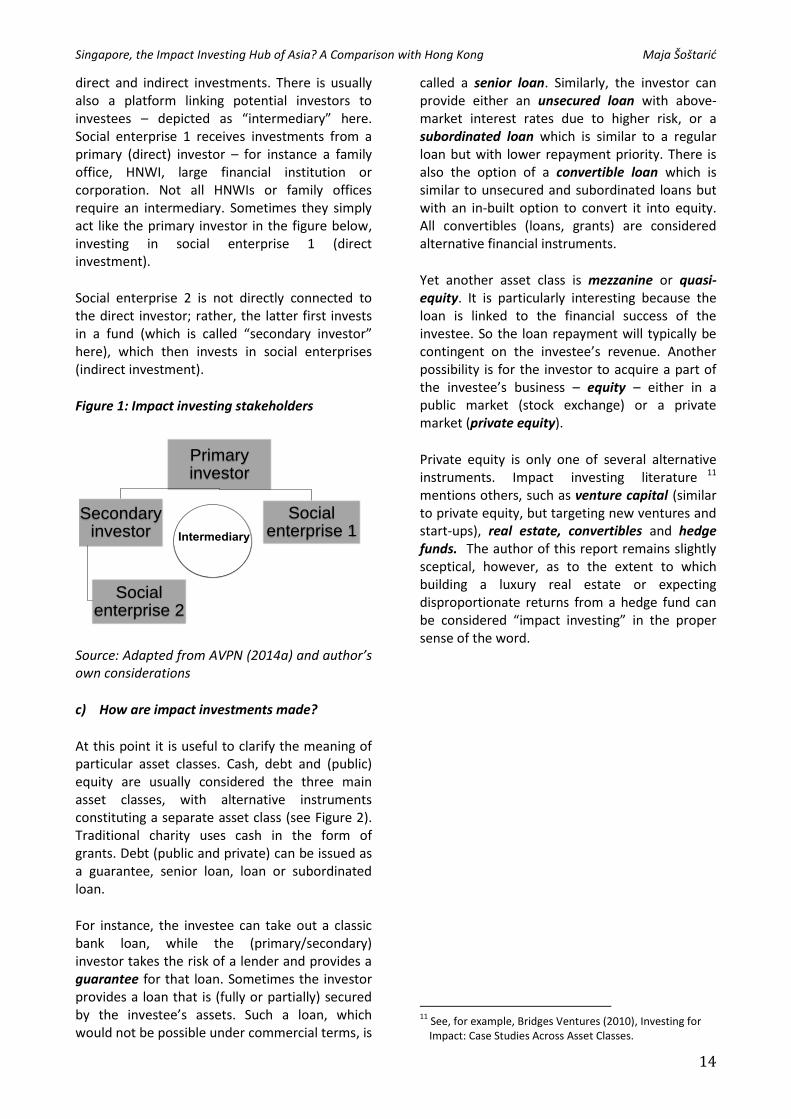

The figure below shows two social enterprises in

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

14

direct and indirect investments. There is usually also a platform linking potential investors to investees – depicted as “intermediary” here. Social enterprise 1 receives investments from a primary (direct) investor – for instance a family office, HNWI, large financial institution or corporation. Not all HNWIs or family offices require an intermediary. Sometimes they simply act like the primary investor in the figure below, investing in social enterprise 1 (direct investment).

Social enterprise 2 is not directly connected to the direct investor; rather, the latter first invests in a fund (which is called “secondary investor” here), which then invests in social enterprises (indirect investment).

Figure 1: Impact investing stakeholders

Source: Adapted from AVPN (2014a) and author’s own considerations

c) How are impact investments made?

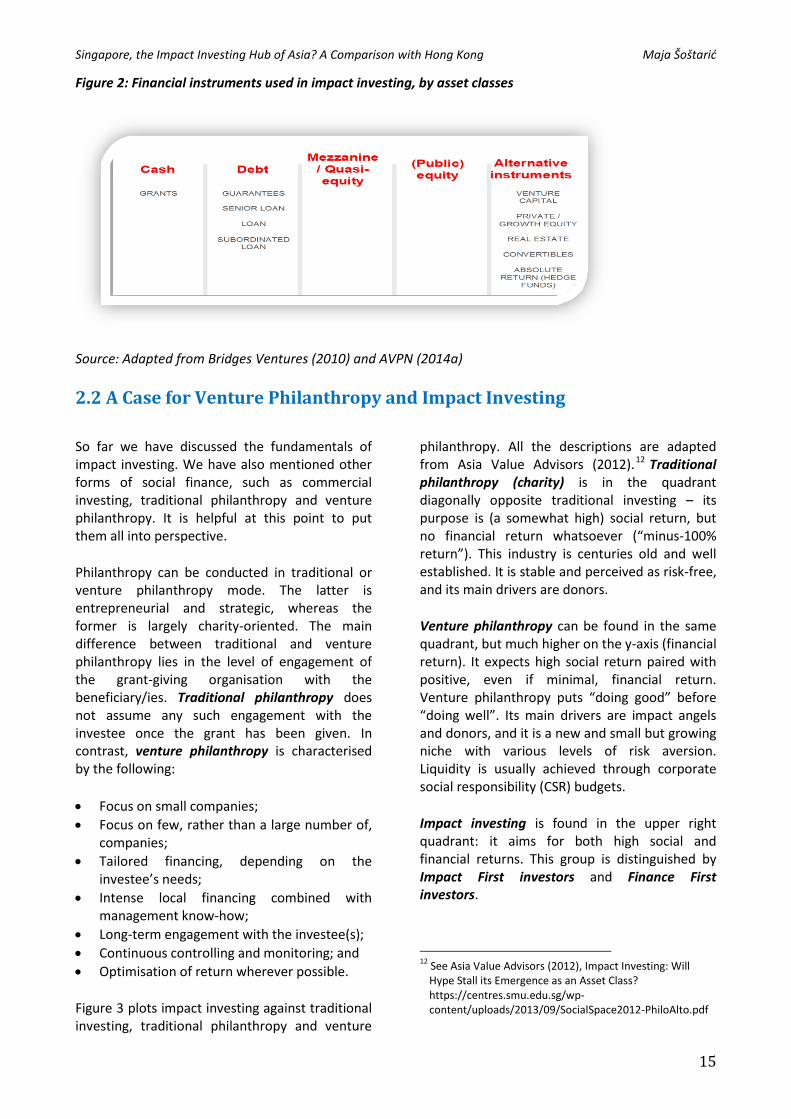

At this point it is useful to clarify the meaning of particular asset classes. Cash, debt and (public) equity are usually considered the three main asset classes, with alternative instruments constituting a separate asset class (see Figure 2). Traditional charity uses cash in the form of grants. Debt (public and private) can be issued as a guarantee, senior loan, loan or subordinated loan.

For instance, the investee can take out a classic bank loan, while the (primary/secondary) investor takes the risk of a lender and provides a guarantee for that loan. Sometimes the investor provides a loan that is (fully or partially) secured by the investee’s assets. Such a loan, which would not be possible under commercial terms, is

called a senior loan. Similarly, the investor can provide either an unsecured loan with above-market interest rates due to higher risk, or a subordinated loan which is similar to a regular loan but with lower repayment priority. There is also the option of a convertible loan which is similar to unsecured and subordinated loans but with an in-built option to convert it into equity. All convertibles (loans, grants) are considered alternative financial instruments.

Yet another asset class is mezzanine or quasi-equity. It is particularly interesting because the loan is linked to the financial success of the investee. So the loan repayment will typically be contingent on the investee’s revenue. Another possibility is for the investor to acquire a part of the investee’s business – equity – either in a public market (stock exchange) or a private market (private equity).

Private equity is only one of several alternative instruments. Impact investing literature 11 mentions others, such as venture capital (similar to private equity, but targeting new ventures and start-ups), real estate, convertibles and hedge funds. The author of this report remains slightly sceptical, however, as to the extent to which building a luxury real estate or expecting disproportionate returns from a hedge fund can be considered “impact investing” in the proper sense of the word.

11

See, for example, Bridges Ventures (2010), Investing for Impact: Case Studies Across Asset Classes.

94

Primary investor

Secondary investor

Social enterprise 2

Social enterprise 1 Intermediary

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

15

Figure 2: Financial instruments used in impact investing, by asset classes

Source: Adapted from Bridges Ventures (2010) and AVPN (2014a)

2.2 A Case for Venture Philanthropy and Impact Investing

So far we have discussed the fundamentals of impact investing. We have also mentioned other forms of social finance, such as commercial investing, traditional philanthropy and venture philanthropy. It is helpful at this point to put them all into perspective.

Philanthropy can be conducted in traditional or venture philanthropy mode. The latter is entrepreneurial and strategic, whereas the former is largely charity-oriented. The main difference between traditional and venture philanthropy lies in the level of engagement of the grant-giving organisation with the beneficiary/ies. Traditional philanthropy does not assume any such engagement with the investee once the grant has been given. In contrast, venture philanthropy is characterised by the following:

Focus on small companies;

Focus on few, rather than a large number of, companies;

Tailored financing, depending on the investee’s needs;

Intense local financing combined with management know-how;

Long-term engagement with the investee(s);

Continuous controlling and monitoring; and

Optimisation of return wherever possible.

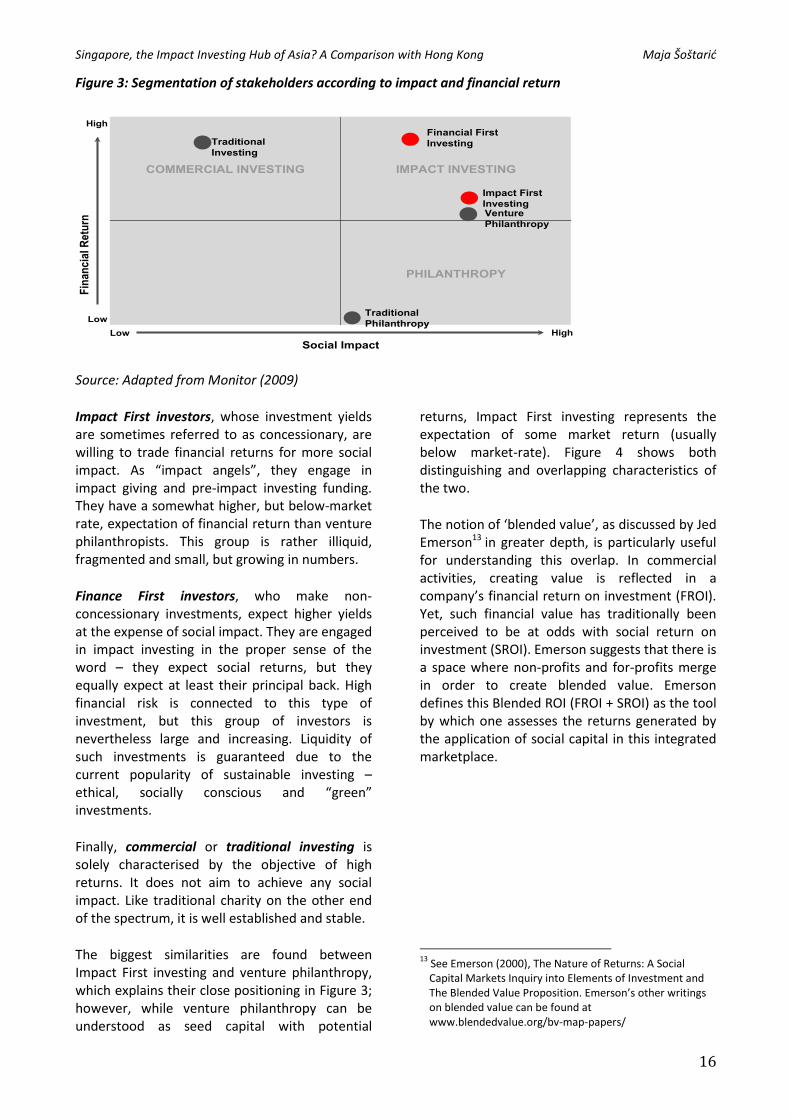

Figure 3 plots impact investing against traditional investing, traditional philanthropy and venture

philanthropy. All the descriptions are adapted from Asia Value Advisors (2012).12 Traditional philanthropy (charity) is in the quadrant diagonally opposite traditional investing – its purpose is (a somewhat high) social return, but no financial return whatsoever (“minus-100% return”). This industry is centuries old and well established. It is stable and perceived as risk-free, and its main drivers are donors.

Venture philanthropy can be found in the same quadrant, but much higher on the y-axis (financial return). It expects high social return paired with positive, even if minimal, financial return. Venture philanthropy puts “doing good” before “doing well”. Its main drivers are impact angels and donors, and it is a new and small but growing niche with various levels of risk aversion. Liquidity is usually achieved through corporate social responsibility (CSR) budgets.

Impact investing is found in the upper right quadrant: it aims for both high social and financial returns. This group is distinguished by Impact First investors and Finance First investors.

12

See Asia Value Advisors (2012), Impact Investing: Will Hype Stall its Emergence as an Asset Class? https://centres.smu.edu.sg/wp-content/uploads/2013/09/SocialSpace2012-PhiloAlto.pdf

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

16

Figure 3: Segmentation of stakeholders according to impact and financial return

Source: Adapted from Monitor (2009)

Impact First investors, whose investment yields are sometimes referred to as concessionary, are willing to trade financial returns for more social impact. As “impact angels”, they engage in impact giving and pre-impact investing funding. They have a somewhat higher, but below-market rate, expectation of financial return than venture philanthropists. This group is rather illiquid, fragmented and small, but growing in numbers.

Finance First investors, who make non-concessionary investments, expect higher yields at the expense of social impact. They are engaged in impact investing in the proper sense of the word – they expect social returns, but they equally expect at least their principal back. High financial risk is connected to this type of investment, but this group of investors is nevertheless large and increasing. Liquidity of such investments is guaranteed due to the current popularity of sustainable investing – ethical, socially conscious and “green” investments.

Finally, commercial or traditional investing is solely characterised by the objective of high returns. It does not aim to achieve any social impact. Like traditional charity on the other end of the spectrum, it is well established and stable.

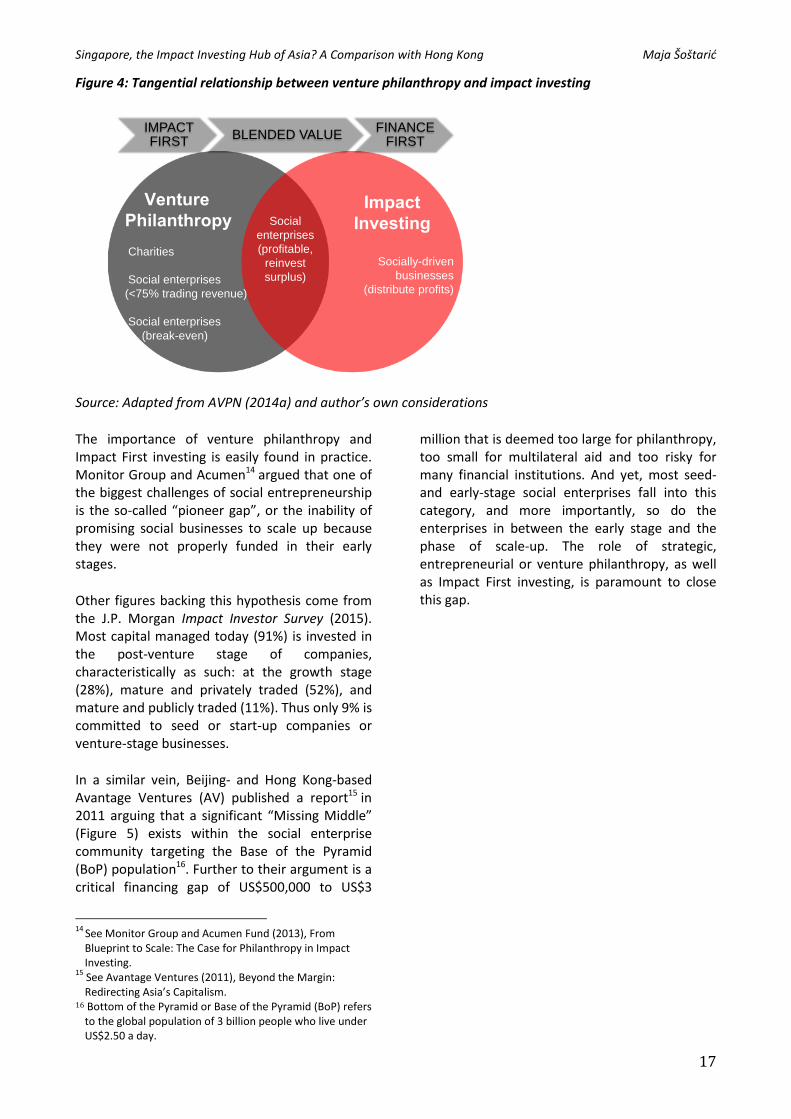

The biggest similarities are found between Impact First investing and venture philanthropy, which explains their close positioning in Figure 3; however, while venture philanthropy can be understood as seed capital with potential

returns, Impact First investing represents the expectation of some market return (usually below market-rate). Figure 4 shows both distinguishing and overlapping characteristics of the two.

The notion of ‘blended value’, as discussed by Jed Emerson13 in greater depth, is particularly useful for understanding this overlap. In commercial activities, creating value is reflected in a company’s financial return on investment (FROI). Yet, such financial value has traditionally been perceived to be at odds with social return on investment (SROI). Emerson suggests that there is a space where non-profits and for-profits merge in order to create blended value. Emerson defines this Blended ROI (FROI + SROI) as the tool by which one assesses the returns generated by the application of social capital in this integrated marketplace.

13

See Emerson (2000), The Nature of Returns: A Social Capital Markets Inquiry into Elements of Investment and The Blended Value Proposition. Emerson’s other writings on blended value can be found at www.blendedvalue.org/bv-map-papers/

COMMERCIAL INVESTING IMPACT INVESTING

PHILANTHROPY

High

Low

Low High

Fin

an

cia

l R

etu

rn

Social Impact

Traditional

Investing

Financial First

Investing

Impact First

Investing Venture

Philanthropy

Traditional

Philanthropy

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

17

Figure 4: Tangential relationship between venture philanthropy and impact investing

Source: Adapted from AVPN (2014a) and author’s own considerations

The importance of venture philanthropy and Impact First investing is easily found in practice. Monitor Group and Acumen14 argued that one of the biggest challenges of social entrepreneurship is the so-called “pioneer gap”, or the inability of promising social businesses to scale up because they were not properly funded in their early stages.

Other figures backing this hypothesis come from the J.P. Morgan Impact Investor Survey (2015). Most capital managed today (91%) is invested in the post-venture stage of companies, characteristically as such: at the growth stage (28%), mature and privately traded (52%), and mature and publicly traded (11%). Thus only 9% is committed to seed or start-up companies or venture-stage businesses.

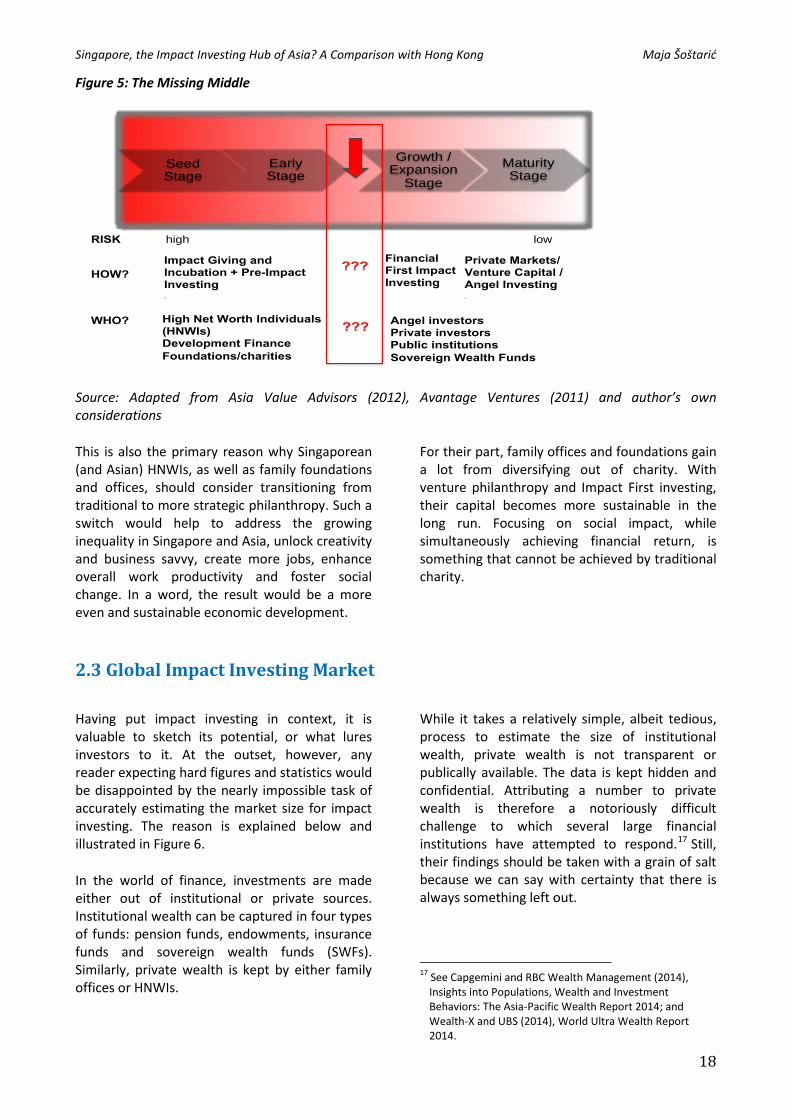

In a similar vein, Beijing- and Hong Kong-based Avantage Ventures (AV) published a report15 in 2011 arguing that a significant “Missing Middle” (Figure 5) exists within the social enterprise community targeting the Base of the Pyramid (BoP) population16. Further to their argument is a critical financing gap of US$500,000 to US$3

14

See Monitor Group and Acumen Fund (2013), From Blueprint to Scale: The Case for Philanthropy in Impact Investing.

15 See Avantage Ventures (2011), Beyond the Margin: Redirecting Asia’s Capitalism.

16 Bottom of the Pyramid or Base of the Pyramid (BoP) refers to the global population of 3 billion people who live under US$2.50 a day.

million that is deemed too large for philanthropy, too small for multilateral aid and too risky for many financial institutions. And yet, most seed- and early-stage social enterprises fall into this category, and more importantly, so do the enterprises in between the early stage and the phase of scale-up. The role of strategic, entrepreneurial or venture philanthropy, as well as Impact First investing, is paramount to close this gap.

Social

enterprises

(profitable,

reinvest

surplus)

Venture

Philanthropy

Charities

Social enterprises

(<75% trading revenue)

Social enterprises

( (break-even)

)

•

Impact

Investing

Socially-driven

businesses

(distribute profits)

117

IMPACT FIRST

BLENDED VALUE FINANCE

FIRST

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

18

Figure 5: The Missing Middle

Source: Adapted from Asia Value Advisors (2012), Avantage Ventures (2011) and author’s own considerations

This is also the primary reason why Singaporean (and Asian) HNWIs, as well as family foundations and offices, should consider transitioning from traditional to more strategic philanthropy. Such a switch would help to address the growing inequality in Singapore and Asia, unlock creativity and business savvy, create more jobs, enhance overall work productivity and foster social change. In a word, the result would be a more even and sustainable economic development.

For their part, family offices and foundations gain a lot from diversifying out of charity. With venture philanthropy and Impact First investing, their capital becomes more sustainable in the long run. Focusing on social impact, while simultaneously achieving financial return, is something that cannot be achieved by traditional charity.

2.3 Global Impact Investing Market

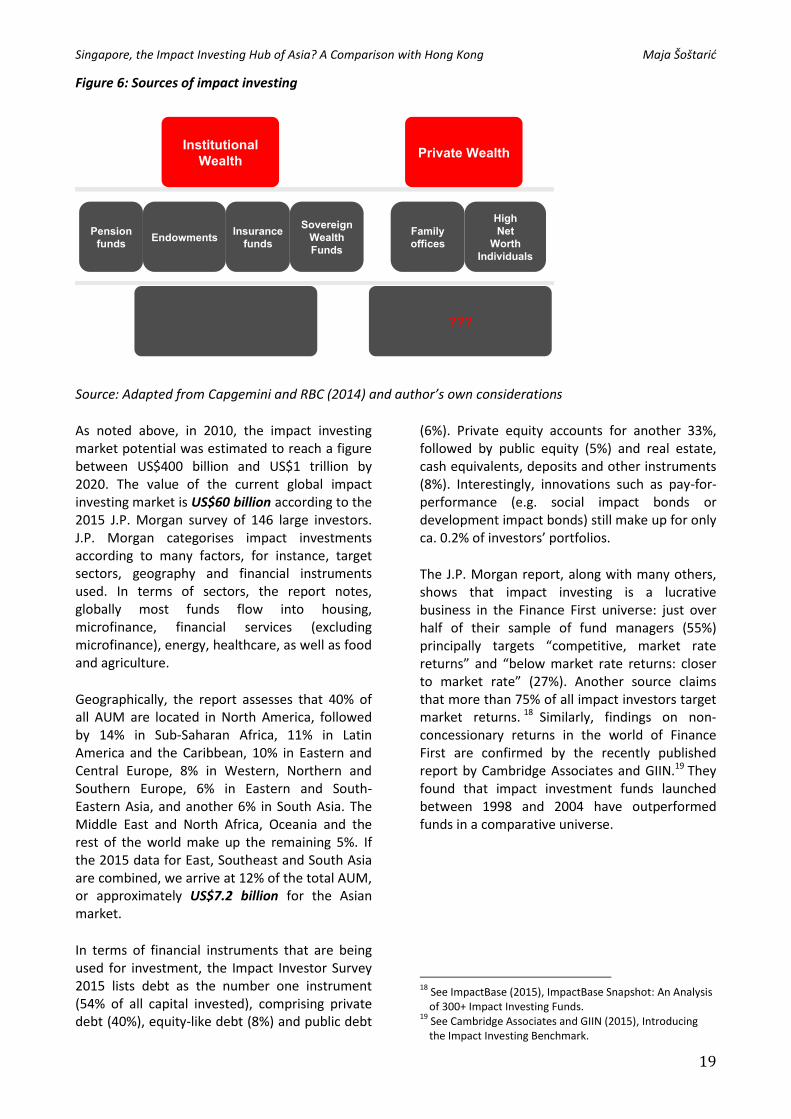

Having put impact investing in context, it is valuable to sketch its potential, or what lures investors to it. At the outset, however, any reader expecting hard figures and statistics would be disappointed by the nearly impossible task of accurately estimating the market size for impact investing. The reason is explained below and illustrated in Figure 6.

In the world of finance, investments are made either out of institutional or private sources. Institutional wealth can be captured in four types of funds: pension funds, endowments, insurance funds and sovereign wealth funds (SWFs). Similarly, private wealth is kept by either family offices or HNWIs.

While it takes a relatively simple, albeit tedious, process to estimate the size of institutional wealth, private wealth is not transparent or publically available. The data is kept hidden and confidential. Attributing a number to private wealth is therefore a notoriously difficult challenge to which several large financial institutions have attempted to respond.17 Still, their findings should be taken with a grain of salt because we can say with certainty that there is always something left out.

17

See Capgemini and RBC Wealth Management (2014), Insights into Populations, Wealth and Investment Behaviors: The Asia-Pacific Wealth Report 2014; and Wealth-X and UBS (2014), World Ultra Wealth Report 2014.

Impact Giving and Incubation + Pre-Impact

Investing .

Financial

First Impact

Investing

Private Markets/Venture Capital /

Angel Investing .

124

Seed Stage

Early Stage

Growth / Expansion

Stage

Maturity Stage

High Net Worth Individuals

(HNWIs)

Development Finance

Foundations/charities

Angel investors

Private investors

Public institutions

Sovereign Wealth Funds

HOW?

WHO?

RISK high low

???

???

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

19

Figure 6: Sources of impact investing

Source: Adapted from Capgemini and RBC (2014) and author’s own considerations

As noted above, in 2010, the impact investing market potential was estimated to reach a figure between US$400 billion and US$1 trillion by 2020. The value of the current global impact investing market is US$60 billion according to the 2015 J.P. Morgan survey of 146 large investors. J.P. Morgan categorises impact investments according to many factors, for instance, target sectors, geography and financial instruments used. In terms of sectors, the report notes, globally most funds flow into housing, microfinance, financial services (excluding microfinance), energy, healthcare, as well as food and agriculture.

Geographically, the report assesses that 40% of all AUM are located in North America, followed by 14% in Sub-Saharan Africa, 11% in Latin America and the Caribbean, 10% in Eastern and Central Europe, 8% in Western, Northern and Southern Europe, 6% in Eastern and South-Eastern Asia, and another 6% in South Asia. The Middle East and North Africa, Oceania and the rest of the world make up the remaining 5%. If the 2015 data for East, Southeast and South Asia are combined, we arrive at 12% of the total AUM, or approximately US$7.2 billion for the Asian market.

In terms of financial instruments that are being used for investment, the Impact Investor Survey 2015 lists debt as the number one instrument (54% of all capital invested), comprising private debt (40%), equity-like debt (8%) and public debt

(6%). Private equity accounts for another 33%, followed by public equity (5%) and real estate, cash equivalents, deposits and other instruments (8%). Interestingly, innovations such as pay-for-performance (e.g. social impact bonds or development impact bonds) still make up for only ca. 0.2% of investors’ portfolios.

The J.P. Morgan report, along with many others, shows that impact investing is a lucrative business in the Finance First universe: just over half of their sample of fund managers (55%) principally targets “competitive, market rate returns” and “below market rate returns: closer to market rate” (27%). Another source claims that more than 75% of all impact investors target market returns. 18 Similarly, findings on non-concessionary returns in the world of Finance First are confirmed by the recently published report by Cambridge Associates and GIIN.19 They found that impact investment funds launched between 1998 and 2004 have outperformed funds in a comparative universe.

18

See ImpactBase (2015), ImpactBase Snapshot: An Analysis of 300+ Impact Investing Funds.

19 See Cambridge Associates and GIIN (2015), Introducing the Impact Investing Benchmark.

Three Layer Block Diagram Use to describe a three layered system or architecture

High

Net

Worth

Individuals

Institutional

Wealth

94

Private Wealth

Pension

funds

Family

offices

???

Endowments Insurance

funds

Sovereign

Wealth

Funds

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

20

2.4 Challenges of Impact Investing

The impact investing market potential of up to US$1 trillion in capital invested and up to US$667 billion in profits sounds wonderful, but is it realistic? What are the principal obstacles to the development of the impact investing market? In this report we identify four such major obstacles.

1. Challenges with measuring impact

What exactly defines the impact of an investment? There has been a lot of confusion in distinguishing between the social and environmental return (SER) and the non-financial impact of impact investing. 20 Whereas the “impact” in impact investing denotes changes to outcomes over any timescale compared to what would have occurred without any action taking place, SER affects beneficiaries who may or may not have a connection to the impact investor (i.e. if the process is a three-level one like depicted in Figure 1). SER may also have negative aspects.

It is beyond the scope of this paper to dig into all the intricacies of impact measurement. For readers interested in that aspect, an excellent introduction can be found in Reeder and Colantonio (2013). More pertinent to our discussion, however, are the three main frameworks used by impact investors: Impact Reporting and Investment Standards (IRIS), Pulse and Global Impact Investing Rating System (GIIRS). These offer standardised definitions of impact performance and contain the performance standards of various funds and companies.21

All impact measurement is problematic due to the tension between subjective criteria that determine impact on a case-to-case basis, and a standardised framework. Moreover, investors

20

See Reeder and Colantonio (2013): Measuring Impact and Non-financial Returns in Impact Investing: A Critical Overview of Concepts and Practice.

21IRIS contains standardised definitions and produces benchmark reports that capture major trends across the impact investing industry. PULSE is a portfolio management tool that uses IRIS metrics. Finally, GIIRS, which is also based on IRIS metrics, is an impact ratings tool and analytics platform that assesses companies and funds on the basis of their social and environmental performance. IRIS is far from being a universally used benchmark, though. The 2015 J.P. Morgan report shows that 60% of all investors surveyed used metrics aligned with IRIS, while 58% use their own metrics (many investors use both).

and investees often have different priorities in measuring impact. For instance, many investors only focus on short-term impact without taking into account what could potentially occur afterwards.

2. Lack of proper education on impact investing

Impact investing remains a mystery to many stakeholders but this does not mean that information is unavailable. As one respondent from Hong Kong reported, “If I want, I can go to an event, a workshop, a seminar or a conference on impact investing every day.” So, claiming that more “buzz” is needed to get impact investing going would absolutely miss the point.

More research needs to be conducted to clarify the very basics of impact investing – what it really is, which niche of companies it affects, where it stands in comparison to venture philanthropy and commercial investing, and how impact is defined and measured.22 This report constitutes an attempt in that direction.

3. Lack of proper intermediation

In 2009, the Monitor report correctly identified the lack of proper intermediation as one of the biggest potential threats to impact investing. Again, the keyword here is “proper”. Impact First investors who are willing to put in some patient capital and accept concessionary returns find this challenge particularly important to address. They are therefore well aware of the risk of waiting indefinitely for returns on their investment.

Impact First investors are looking for investees who will get the job done and do not want to debate the social impact of their investments. With information asymmetry the biggest source of concern here, Finance First investors are even

22

The European Investment Bank Institute is currently funding a three-year study (2013-2015) entitled “Measuring Impact Beyond Financial Returns”.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

21

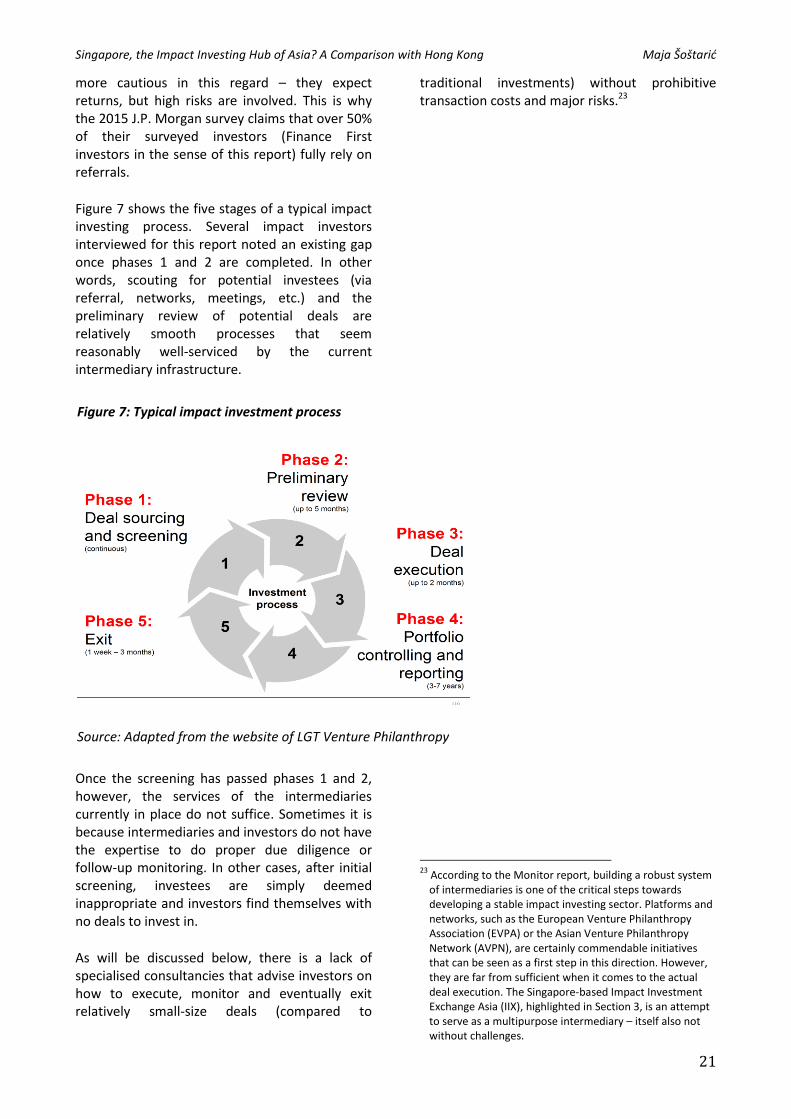

Figure 7: Typical impact investment process

Source: Adapted from the website of LGT Venture Philanthropy

more cautious in this regard – they expect returns, but high risks are involved. This is why the 2015 J.P. Morgan survey claims that over 50% of their surveyed investors (Finance First investors in the sense of this report) fully rely on referrals.

Figure 7 shows the five stages of a typical impact investing process. Several impact investors interviewed for this report noted an existing gap once phases 1 and 2 are completed. In other words, scouting for potential investees (via referral, networks, meetings, etc.) and the preliminary review of potential deals are relatively smooth processes that seem reasonably well-serviced by the current intermediary infrastructure.

Once the screening has passed phases 1 and 2, however, the services of the intermediaries currently in place do not suffice. Sometimes it is because intermediaries and investors do not have the expertise to do proper due diligence or follow-up monitoring. In other cases, after initial screening, investees are simply deemed inappropriate and investors find themselves with no deals to invest in.

As will be discussed below, there is a lack of specialised consultancies that advise investors on how to execute, monitor and eventually exit relatively small-size deals (compared to

traditional investments) without prohibitive transaction costs and major risks.23

23

According to the Monitor report, building a robust system of intermediaries is one of the critical steps towards developing a stable impact investing sector. Platforms and networks, such as the European Venture Philanthropy Association (EVPA) or the Asian Venture Philanthropy Network (AVPN), are certainly commendable initiatives that can be seen as a first step in this direction. However, they are far from sufficient when it comes to the actual deal execution. The Singapore-based Impact Investment Exchange Asia (IIX), highlighted in Section 3, is an attempt to serve as a multipurpose intermediary – itself also not without challenges.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

22

4. Lack of the investors’ willingness to take risks and the investees’ absorptive capacity

Only ca. 1%24 of all impact investing deals make it to the actual execution stage. Investors often say that money is not a problem, whereas social entrepreneurs never seem to have that impression. Clearly, there is a mismatch between the supply of and demand for impact investment capital.

Impact investors have the money but are also very risk-averse – funding itself is not a problem but risk-friendly funding is. Impact investing is a generational project that requires a lot of patience. Whoever enters the sector hoping for quick returns is probably in the wrong place.

Even so, investors often complain that there are no deals to invest in. By that they mean the lack of scalability of their investees stemming from poor business acumen, bad planning or flawed financial projections. That is why many impact investors and intermediaries are slowly coming to realise the importance of business accelerators that empower social enterprises to scale.

As one interlocutor put it, it is often a chicken-and-egg problem: investors want to find investable opportunities but rarely take the first step to creating those opportunities to build the ecosystem. Nevertheless, the investors in Singapore and Hong Kong are increasingly aware of the need to invest more in coaching, mentoring and business accelerators.

24

See Asia Value Advisors (2012), op. cit.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

23

3. Impact Investing Potential of Singapore and Hong Kong

As the world’s number one wealth destination with fast-growing giants such as China and India, but home to 62% of the world’s hungry, Asia is a continent of mindboggling contradictions. Roughly 1.6 billion of Asia’s population lives under US$2 a day while the total wealth held by its HNWIs reached a staggering US$14.2 trillion25 in 2013 to surpass both North America and Europe. How can the gap be closed?

Clearly, new ways of channelling such impressive resources are required to create a more egalitarian Asia. The next section investigates the possibility of finding those new channels in Singapore, ranked third-richest in the world with a GDP per capita (PPP) of US$82,762. We also take a closer look at Hong Kong (GDP per capita in PPP of US$54,722, slightly ahead of the US) to determine how it can inspire potential strategic philanthropists in Singapore.

3.1 Market Size of Impact Investing in Asia

Even with private wealth as a big unknown at the global level, attempts have been made to estimate the size of the global and regional impact investing market(s). The author is aware of three methods to do so and discusses them in the Asian context below.

The most common survey method was used by J.P. Morgan in the 2010 report and all its subsequent impact investor surveys. The 2010 report surveyed 24 impact investors, a figure that grew to 146 in 2015. Most of the respondents were fund managers while others were asset owners (foundations, banks and development finance institutions). 26 While this approach is

25

See Capgemini and RBC (2014), op. cit. 26

Several other regional studies have been conducted using the survey method: Bain has attempted to estimate the size of the impact investing market in Latin America in this manner; the Global Impact Investing Network (GIIN) has tried to do the same for South Asia; and the Asian Development Bank (ADB), in cooperation with Shujog, has used a similar approach to estimate the impact investing trends in Asia in general. See: Leme, Martins and Hornberger (2014), The State of Impact Investing in Latin America: Regional Trends and Challenges Facing a Fast-growing Investment Strategy; ADB and Shujog (2011),

probably the most accurate and closest to the true market value, it is limited by its selectivity since only some fund managers and asset owners were surveyed.

The supply and demand method is an interesting but fairly complex one. The abovementioned AV report attempts to overcome the selectivity of a survey by using the logic of demand and supply. Realising that the pure survey method only informs about the current consumption trends, the report develops a compelling framework to first estimate the demand for capital in Developing Asia27 in six sectors that they believe would particularly benefit from impact investing – affordable housing, water and sanitation, rural energy, rural and elderly healthcare, primary and special needs education, as well as agriculture and agribusiness.

The report does not limit the potential demand to the traditional BoP population, but to all populations serviced by the six sectors. It estimates the capital supply and potential market size for impact investing in the whole Asia-Pacific.28 Consequently, for that region, estimates for the total investment needs of social enterprises in the six sectors are US$44–74 billion.

Even if the survey method is selective and limited

Impact Investors in Asia: Characteristics and Preferences for Investing in Social Enterprises in Asia and the Pacific; GIIN and Dalberg (2015), The Landscape for Impact Investing in South Asia: Understanding the Current Status, Trends, Opportunities and Challenges in Bangladesh, India, Myanmar, Nepal, Pakistan and Sri Lanka.

27 The following countries are considered part of Developing Asia: Afghanistan, Bangladesh, Bhutan, Brunei Darussalam, Cambodia, China, Fiji, India, Indonesia, Kiribati, Laos, Malaysia, Maldives, Myanmar, Nepal, Pakistan, Papua New Guinea, Philippines, Samoa, Solomon Islands, Sri Lanka, Thailand, Timor-Leste, Tonga, Vanuatu and Vietnam.

28 To estimate the demand, AV undertakes four crucial steps: they estimate the current underserved population, target per capita expenditures, target sector penetration by 2020, and finally, they calculated total market demand by sector to be captured by impact investing. On the other hand, for the invested capital supply, they use a specially designed formula that multiplies total market demand by sector, calculated in the previous step, by an estimated profit margin of the sector, taking into account a projected Return on Equity and a sector-specific cost of capital.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

24

to current investments only, the demand and supply method is equally imperfect since the choice of sectors, cost of capital and profit margins are subjective. Also, the supply and demand calculations are made assuming perfect markets in which the supply always satisfies the demand.

Using the “the 1% historical success rate” method, Asia Value Advisors (2012) reminds us that the regularly quoted range of US$400 billion to US$1 trillion should only be considered the market potential or market opportunity. In other words, it represents an aspirational figure. The reality, they argue, is closer to a benchmark of around 1% historical success rate of the potential total market size. Based on the AV report’s figures above, this would translate to a US$440–740 million Asian market by 2020. This is well below the 2015 J.P. Morgan estimate for East, South-East and South Asia (US$7.2 billion).

If, on the other hand, we accept the figures suggested by the AV report (US$44-74 billion between 2010 and 2020), and put the current J.P. Morgan estimate in that context, then the picture altogether potentially makes sense. However, it should be noted that the AV report sector-specific estimates do not include financial services and microfinance, which are usually considered the largest two impact investing target sectors.

Even if accurate, none of the above figures are purposeful unless put in perspective. Assuming a current US$7.2 billion market size of impact investments in Asia and its ten-fold market potential by 2020, fundamental considerations that follow include: Where can that money come from? Who does it go to? What is that money for? There are many ways to approach these questions in the Asian context.

The next section attempts to provide some answers focusing on the Singapore- and Hong Kong-based philanthropists and impact investors. Two former investment bankers, Philo Alto and Ming Wong, have written extensively on some of those issues in the context of Hong Kong.29 We

29

See Alto and Wong (2013), Mind the Gap: Lessons and Findings from EngageHK; and Alto and Wong (2014), Adopting the London Principles: Policy Considerations to Grow Impact Investing in Hong Kong.

turn to both to sketch their impact investing landscapes at the moment and to cite some lessons Singapore can learn from Hong Kong in this regard.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

25

3.2 Philanthropy in Singapore and Hong Kong

The debate on innovation in Asian social finance can certainly focus on strategic philanthropy only. With a number of other research documents already written on the subject, this paper does not go in that particular direction. Professor Rob John from the National University of Singapore (NUS) has written several very informative working papers on Asian philanthropy. 30 Also, SMU’s LCSI has published two reports – Levers for Change (2014) and From Charity to Change (2014) – discussing Singapore among some other countries. I will thus briefly summarise the state of the field in the philanthropic sectors of Singapore and Hong Kong as a prelude to discussing impact investing in the two cities.

Singapore has 105,000 HNWIs worth US$523 billion combined (2013)31 and its residents are no strangers to philanthropic giving. According to the National Volunteer & Philanthropy Centre (NVPC)32 charitable donations in Singapore had more than tripled from S$341 million in 2006 to S$1.1 billion in 2012. Coutts, reporting for 201333, identified 38 donations ofS$1 million and more in Singapore that totalled S$713 million. Ten per cent of the dollar value of all philanthropic grants were gifted by individuals, 16% by foundations and 74% by corporations (see Figure 8). Three-quarters of grants were made by the private sector.

30

Interview with Rob John, July 2015. See John (2013), Innovation in Asian Philanthropy; and John (2014), Virtuous Circles: New Expressions of Collective Philanthropy in Asia Entrepreneurial Social Finance in Asia.

31 See Capgemini and RBC (2014), op. cit.

32 See NVPC (2014), Individual Giving Survey 2014.

33 See Coutts (2014), Philanthropy: Million Dollar Donor Reports. (Case studies: Singapore, Hong Kong).

Figure 8: Philanthropy in Singapore

Source: Coutts (2014)

Corporations, as the principal philanthropic stakeholders, have their own foundations set up particularly for that purpose. The most important ones are Temasek Foundation, SPH Foundation, DBS Foundation, NTUC FairPrice Foundation, Banyan Tree Global Foundation, CapitaLand Hope Foundation and Hong Leong Foundation. Combined, these foundations have so far donated or pledged more than S$280 million (almost US$200 million) 34 in various sectors, notably in education, environment, healthcare, sports, arts and welfare.

Some family offices in Singapore donate across the board, whereas others have identified niches that they especially care about. For example, Lee Foundation and Shaw Foundation give grants in areas spanning from medicine to arts and culture. In contrast, Lien Foundation is particularly active in promoting early childhood education and palliative care; Tsao Foundation donates to causes of the elderly; and Tan Chin Tuan Foundation works to promote community development and education.

34

Akulinicheva, Dua and Gupta (2015), Corporate Foundation Landscape in Singapore. Unpublished research by three INSEAD MBA students, courtesy of Aparna Dua.

Donations (in %)

Individuals10%

Foundations16%

Corporations74%

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

26

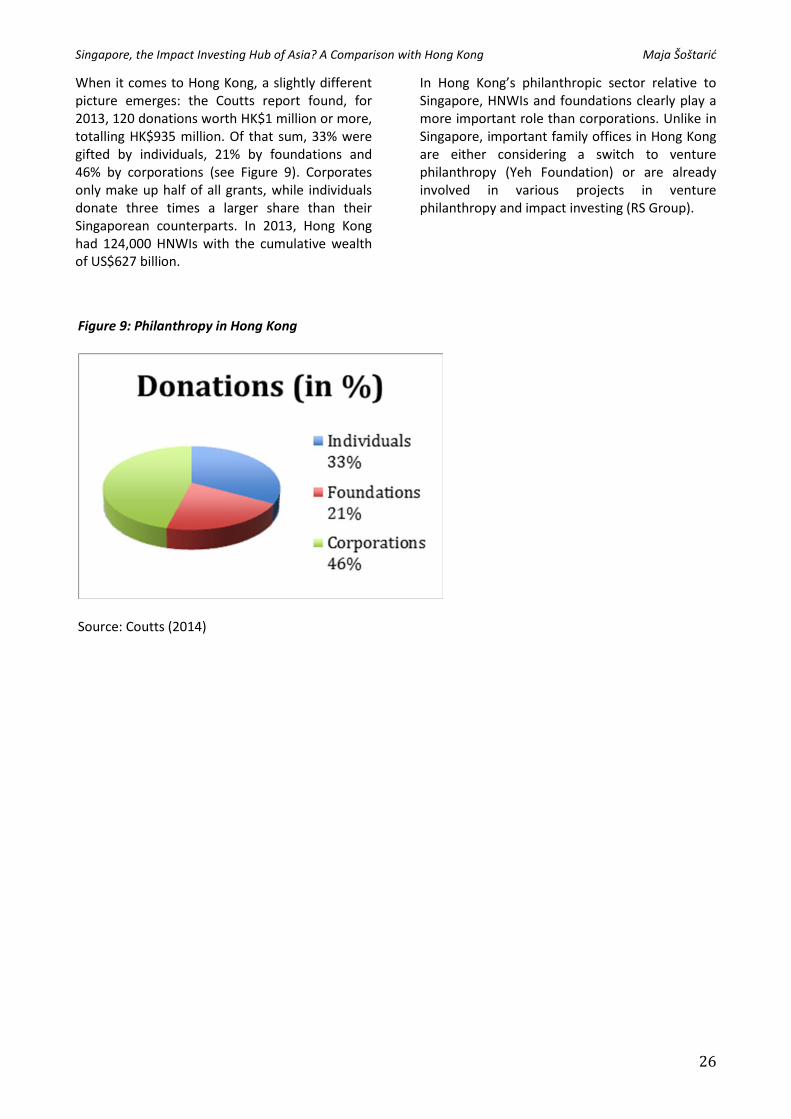

When it comes to Hong Kong, a slightly different picture emerges: the Coutts report found, for 2013, 120 donations worth HK$1 million or more, totalling HK$935 million. Of that sum, 33% were gifted by individuals, 21% by foundations and 46% by corporations (see Figure 9). Corporates only make up half of all grants, while individuals donate three times a larger share than their Singaporean counterparts. In 2013, Hong Kong had 124,000 HNWIs with the cumulative wealth of US$627 billion.

In Hong Kong’s philanthropic sector relative to Singapore, HNWIs and foundations clearly play a more important role than corporations. Unlike in Singapore, important family offices in Hong Kong are either considering a switch to venture philanthropy (Yeh Foundation) or are already involved in various projects in venture philanthropy and impact investing (RS Group).

Figure 9: Philanthropy in Hong Kong

Source: Coutts (2014)

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

27

3.3 Impact Investors based in Singapore and Hong Kong

This section discusses the proper impact investing funds and the social enterprises turning to them (see Box 2). For angel investors aiming to respond to the “pioneer gap” in the region, see John (2015).35 At this point, we will only mention angel investor networks like Business Angel Network of Southeast Asia, BANSEA (Singapore) and Social Investors’ Club, later Giinseng (Hong Kong).

Box 2: Investee’s Story – Singapore & the Philippines: BagoSphere36

35

See John (2015), Asia’s Impact Angels: How Business Angel Investing can Support Social Enterprise in Asia. 36

Interview with Zhihan Lee, July 2015.

Zhihan Lee has a high level of social awareness. As a student at the National University of Singapore (NUS), he volunteered in Thailand and Laos, and participated in compelling projects like the Harvard Model UN. Working to create employment opportunities for the BoP population in India had also really inspired him.

While he was working in Laos, two other Singaporeans from NUS, Ellwyn Tan and Ivan Lau, were volunteering in Bago City, a rural area over 650 kilometres from Manila with around 50% unemployment rate. Paradoxically, job opportunities are actually growing in the Philippines due to the blossoming of foreign-owned call centers. In fact, the Philippines is now No.1 in the world in providing voice services, which make up most of the business process outsourcing industry.

Call centres generally look for college graduates while many of the unemployed Philippine youth are either only high-school graduates or college dropouts. Zhihan, Ellwyn and Ivan decided to pilot a small job-training programme for the Filipino youth in Bago City in order to make their skills marketable for employment in call centres. Such jobs guarantee a salary four times higher than the monthly average in Bago City.

Starting a business straight out of college, even if one remains in Singapore, is considered imprudent. Graduating and then relocating to a rural area in the Philippines is hardly heard of. “The hardest pitch I ever had to make was the one to my parents,” Zhihan reveals.

Despite the scepticism they encountered, Zhihan and his friends managed to collect slightly over US$15,000 in grants from NUS and a philanthropic foundation. They went on to set up a social enterprise, BagoSphere, and pilot their training programme for a total of 14 students. The programme lasted four months and included classes on English language, financial literacy, motivation, confidence-building and leadership. The results were impressive: 13 of their initial 14 students were employed at a call centre.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

28

After launching the pilot, everything seemed to be working out perfectly for BagoSphere. It won an award at the Start-up@Singapore’s Social Enterprise competition in 2012; and in 2013, their company was among the top 20 hottest start-ups in Singapore selected by the Singapore Business Review and received a grant from the Singapore International Foundation. BagoSphere gathered its initial investors – Kickstart Ventures, xchange and the Small World Group Incubator – with help from Singapore-based Impact Investment Exchange Asia. These investors provided a low six-figure convertible loan. s

BagoSphere measures its social impact by the employment of its programme graduates, as well as their job retention upon graduation and increase in income. So far, the programme has had 474 graduates, and they expect more than 1,000 graduates in total by 2016. 80% of programme alumni find a job two months upon graduation, and 70% remain in the job for 6 months or more. Another beauty of the BagoSphere programme is that it is highly affordable: almost everything, from transportation to stationery, is provided for. The only upfront payment is a commitment fee, equivalent to ca. US$10, which can be paid for after graduation with the supporting framework of microfinance loans like Kiva.

Despite evident progress, legal and financial problems began to emerge. In the Philippines, only up to 40% of company ownership is allowed to be in foreign hands. After consulting their Singaporean and Philippine lawyers, Zhihan and his co-founders decided to set up the company in both countries. Currently, the company is raising its second round of investments. Since BagoSphere is in the very early stage with rather high levels of risk, its investors are predominantly individual angels. The only institutional investor in this second round is a leading Swiss philanthropic impact investment organisation. A third round of investments is expected in 2017.

So where can the company seek potential investment at this point – in Singapore, the Philippines or both? Certainly not so much in Singapore as entities registered in Singapore need to have Singaporean beneficiaries in order to benefit from any type of funding, especially those coming from foundations or government. Speaking with prospective investors can also be problematic, as Zhihan says, “We sometimes have to stress that we can’t guarantee a 15% return on their investment. After all, it’s about trying to find investors who would make a good fit for BagoSphere.” Education is currently one of the hot topics in the Philippines, but there are few active education start-ups. “What we need”, Zhihan continues, “are philanthropic investors who understand social enterprises, and how to grow them. And there are not many of them. We aim to have our investors see a form of exit after five years, with positive returns”. By “philanthropic”, Zhihan does not intend charity, but patient capital and expectations of below-market returns.

Promising Singaporean social start-ups like BagoSphere are therefore in urgent need of Impact First investors such as family offices, HNWIs and foundations. The cost of potential failure of BagoSphere would not be tremendously high for Zhihan, Ellwyn and Ivan, because the whole project has never really been about them. Rather, the biggest losers in that scenario would be hundreds of successful graduates whose lives BagoSphere has transformed, as well as their families and dozens of satisfied call centre employers.

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

29

Who or where can seed/ early-stage enterprises like BagoSphere turn to for investment funding? Besides angel investors and family or corporate foundations, the first address would be venture philanthropists and proper impact investing funds. The latter have been created to fill the gap

and provide the “Missing Middle” with more opportunities to attain growth, expansion and maturity. Such funds usually operate at the intersection of venture philanthropy, Impact First and Finance First investments. Some are also pure Finance First investors, as we will see below.

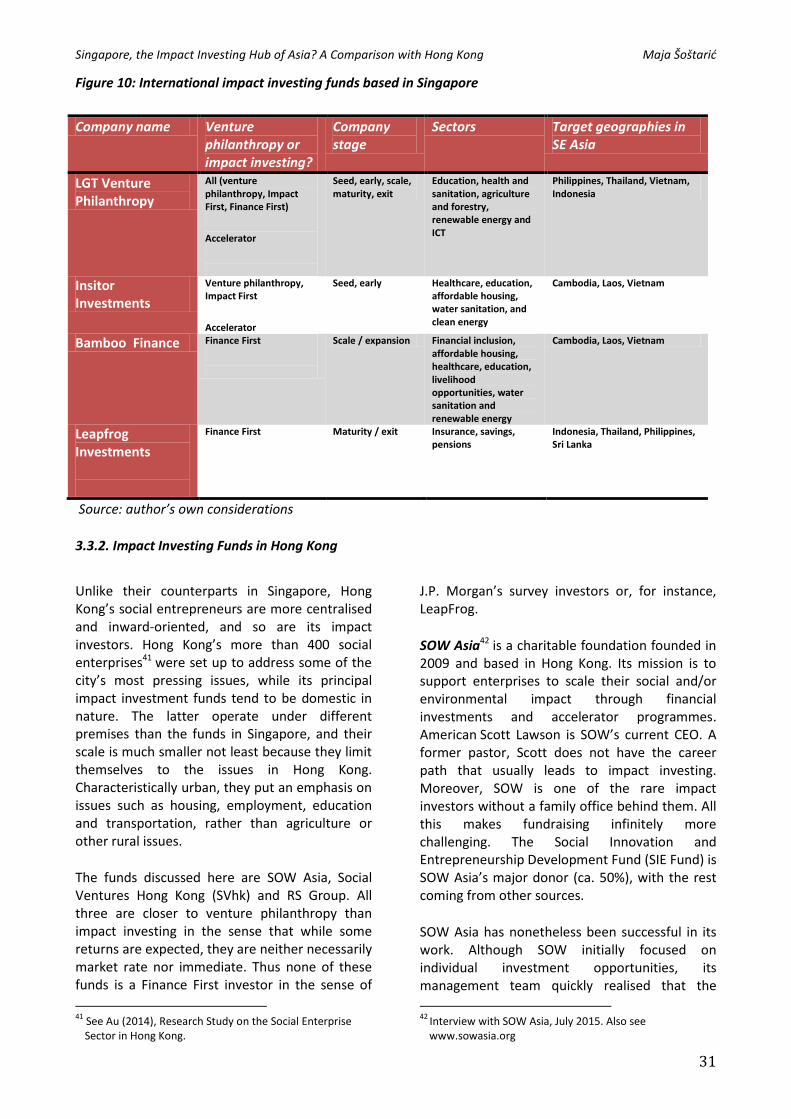

3.3.1 Impact Investing Funds in Singapore

Currently, there are four impact investing funds operating in Singapore, all of which have an international outlook and global headquarters: LGT Venture Philanthropy (Zurich), Bamboo Finance (Luxembourg and Zurich), Insitor Fund (Luxembourg) and Leapfrog Investments (London). Some of their main investments in Southeast Asia are discussed below.

LGT Venture Philanthropy, founded in 2007, is a global impact investor supporting organisations with outstanding social and environmental impact. LGT VP is owned by the Princely Family of Liechtenstein and the LGT Group. The fund focuses on education, health and sanitation, agriculture and forestry, renewable energy, and information and communications technologies (ICT). They support their target organisations through grants, debt and equity, transfer of business and management know-how, as well as access to relevant networks.

To date, LGT VP has invested and donated more than US$55 million and sent over 100 catalyst-for-change (ICats) Fellows into 50 organisations. On average, it invests between US$200,000 and US$10 million in each portfolio company over the course of three to seven years. In Southeast Asia, LGT VP has so far been active in the Philippines, Vietnam, Thailand and Indonesia.

In 2011, LGT VP realised they were facing a significant challenge: after three years of deal sourcing and screening, they were only able to invest in three companies in Southeast Asia. That was because most of the companies they reviewed lacked vital qualities like a business model, impact or financial sustainability, sufficient documentation to clear the due diligence process or a strong management team.

Unlike many other impact investors, LGT VP invests in early-stage companies. To better prepare such early-stage social enterprises for investment, LGT VP launched its Accelerator Program,37 providing up to US$50,000 in grants, loans, convertible debt, or equity, as well as hands-on support from an Accelerator Fellow for 12–24 months. The first investees of the Accelerator Program were six Southeast Asian companies. Globally, a total of 12 enterprises have benefitted from the programme. The financial instruments used have mainly been convertible debt, debt and equity. Today, the majority of Accelerator Program beneficiaries have received follow-up investment and half are profitable.

Similarly, the Insitor Impact Fund 38 has also launched a Seed Fund in South and South East Asia. Insitor finances companies that offer low-income families options for increased access to healthcare, education, water and sanitation, affordable housing and clean energy. The Fund also invests in companies whose business models increase the earning potential of vulnerable communities. So far, Insitor has financed 10 early-stage social businesses with operations in Cambodia, Laos, Vietnam and India through a mix of equity, mezzanine and straight debt. Sectors include healthcare, education, energy, water and sanitation, affordable housing and income-generating activities.

On the Finance First end, two funds are active: Bamboo and LeapFrog. Bamboo Finance, 39 established in 2007, is a commercial private equity firm with offices in Luxembourg, Geneva, Bogota, Nairobi and Singapore. It specialises in

37 Interview with LGT VP, July 2015. Also see LGT VP (2015),

Lessons from the Field. 38 See www.insitormanagement.com/ 39

See www.bamboofinance.com/

Singapore, the Impact Investing Hub of Asia? A Comparison with Hong Kong Maja Šoštarid

30

investing in business models that benefit low-income communities in emerging markets. Bamboo Finance uses a market-oriented approach to deliver social and environmental value and provide attractive financial returns to investors. So far managing US$250 million, the firm has made 46 investments in mature-stage companies in 30 emerging markets.

Bamboo groups its investments around several themes, with funds dedicated to financial inclusion (Bamboo Financial Inclusion Fund); affordable housing, healthcare, education, livelihood opportunities and water sanitation (Oasis Fund); and renewable energy (Bamboo Global Energy Fund – Solar for All). In Southeast Asia, Bamboo has one investee – the Joma Bakery chain in Laos, Vietnam and Cambodia. The Bakery provides employment for severely disadvantaged women who are at risk or victims of domestic abuse, sexual violence or trafficking.

LeapFrog Investments40 focuses on high-growth companies in Africa and Asia. In Southeast Asia, the fund has invested in companies in Indonesia and Thailand. LeapFrog’s companies offer empowering financial tools such as insurance, savings and investment products to emerging consumers. LeapFrog’s investment strategy is backed by some of the world’s leading institutional investors, including J.P. Morgan, Prudential, Swiss Re, and Teachers Insurance and Annuity Association – College Retirement Equities Fund (TIAA CREF).

LeapFrog is a good example of a Finance First impact investor that builds companies which maximise both financial and social returns. Traditionally, LeapFrog invests in businesses which fall into one of three groups: i) financial institutions, ii) distributors for financial products, or iii) enablers of financial services, such as administrators or technology platforms. LeapFrog makes equity investments of US$10-50 million in each company, allowing high-growth businesses to expand within and across markets.

Figure 10 summarises the basic data on the four funds. Finance First investors are traditionally more oriented towards technology and financial services, industries where higher profits are also more likely. These companies are also more