Embed Size (px)

Citation preview

Site Visit to Sishen Mine14 April 2010

2

Agenda

Overview of Kumba Iron Ore

Iron Ore market outlook

Kumba’s Growth pipeline

Q&A

3

Overview of Kumba Iron Ore

4

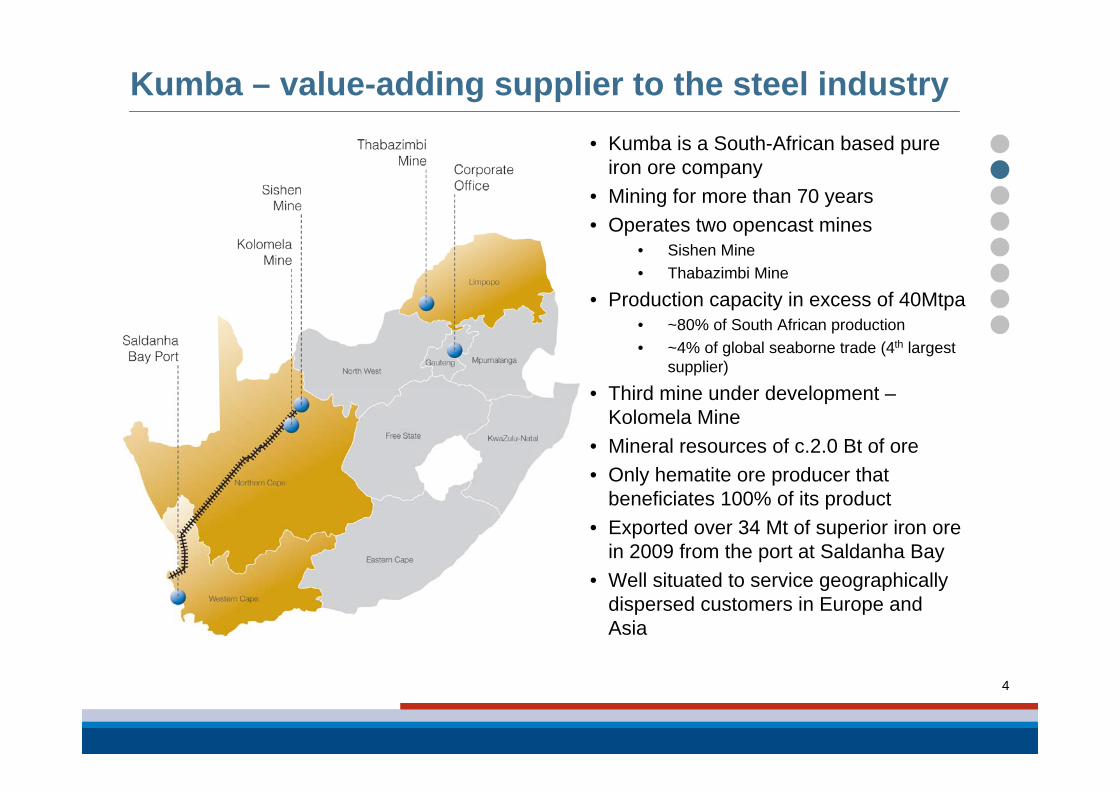

• Kumba is a South-African based pure iron ore company

• Mining for more than 70 years• Operates two opencast mines

• Sishen Mine • Thabazimbi Mine

• Production capacity in excess of 40Mtpa • ~80% of South African production• ~4% of global seaborne trade (4th largest

supplier)

• Third mine under development –Kolomela Mine

• Mineral resources of c.2.0 Bt of ore• Only hematite ore producer that

beneficiates 100% of its product• Exported over 34 Mt of superior iron ore

in 2009 from the port at Saldanha Bay• Well situated to service geographically

dispersed customers in Europe and Asia

Kumba – value-adding supplier to the steel industry

2.8

1.61.3

2.6

0

1

2

3

2006 2007 2008 2009

US$

bill

ion

1.71.1

0.1

2.5

0

1

2

3

2006 2007 2008 2009

US$

/sha

re1.5

0.80.8

1.6

0

1

2

2006 2007 2008 2009

US$

bill

ion

5

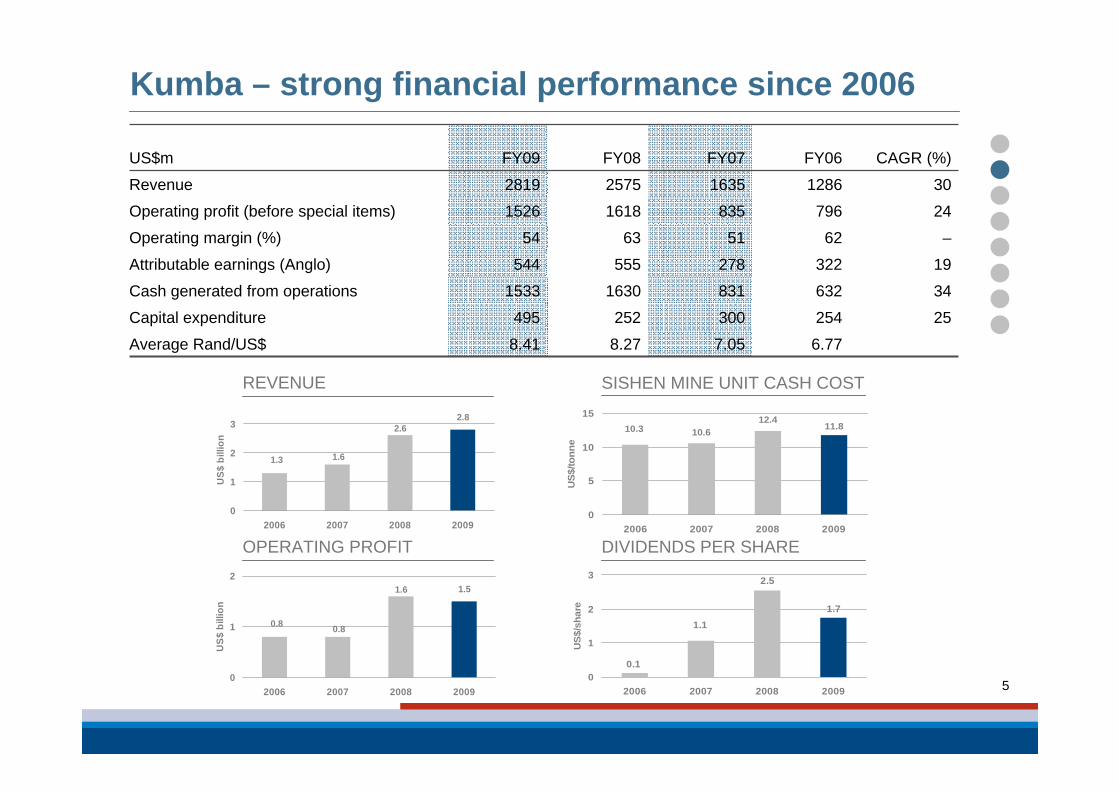

Kumba – strong financial performance since 2006

OPERATING PROFIT

11.812.4

10.3 10.6

0

5

10

15

2006 2007 2008 2009

US$

/tonn

e

SISHEN MINE UNIT CASH COST

DIVIDENDS PER SHARE

REVENUE

6.777.058.278.41Average Rand/US$

254

632

322

62

796

1286

FY06

25300252495Capital expenditure

3483116301533Cash generated from operations

US$m FY09 FY08 FY07 CAGR (%)

Revenue 2819 2575 1635 30

Operating profit (before special items) 1526 1618 835 24

Operating margin (%) 54 63 51 –

Attributable earnings (Anglo) 544 555 278 19

6

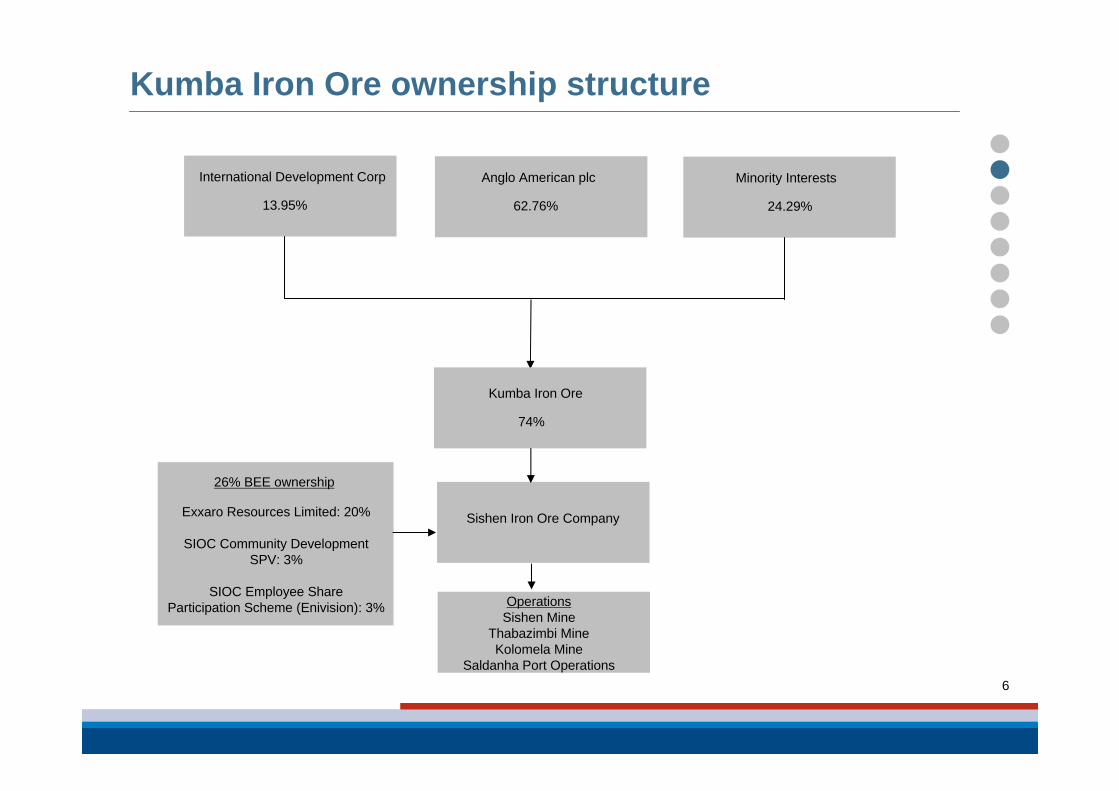

Kumba Iron Ore ownership structure

Anglo American plc

62.76%

International Development Corp

13.95%

Minority Interests

24.29%

Kumba Iron Ore

74%

Sishen Iron Ore Company

OperationsSishen Mine

Thabazimbi MineKolomela Mine

Saldanha Port Operations

26% BEE ownership

Exxaro Resources Limited: 20%

SIOC Community DevelopmentSPV: 3%

SIOC Employee ShareParticipation Scheme (Enivision): 3%

0

2500

5000

7500

10000

2006 2007 2008 2009

US$

mill

ion

31

88

16

0

10

20

30

2006 2007 2008 2009

%

7

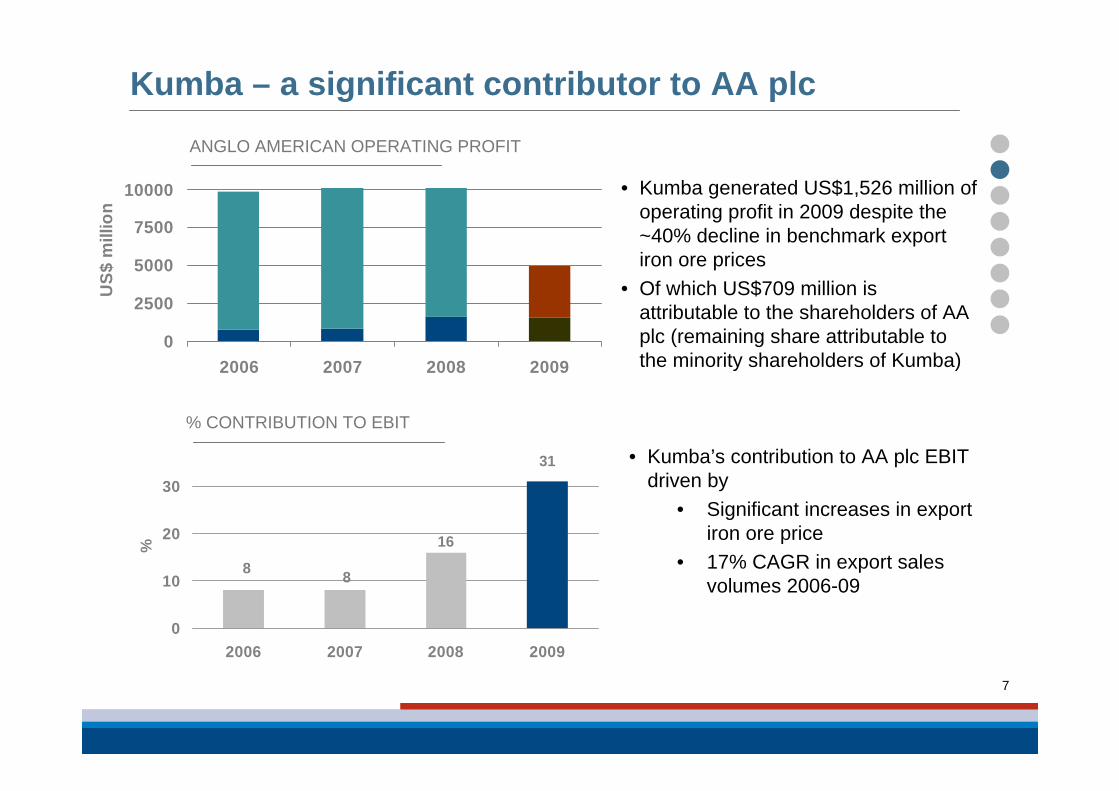

Kumba – a significant contributor to AA plc

% CONTRIBUTION TO EBIT

ANGLO AMERICAN OPERATING PROFIT

• Kumba’s contribution to AA plc EBIT driven by

• Significant increases in export iron ore price

• 17% CAGR in export sales volumes 2006-09

• Kumba generated US$1,526 million of operating profit in 2009 despite the ~40% decline in benchmark export iron ore prices

• Of which US$709 million is attributable to the shareholders of AA plc (remaining share attributable to the minority shareholders of Kumba)

8

Safety

9

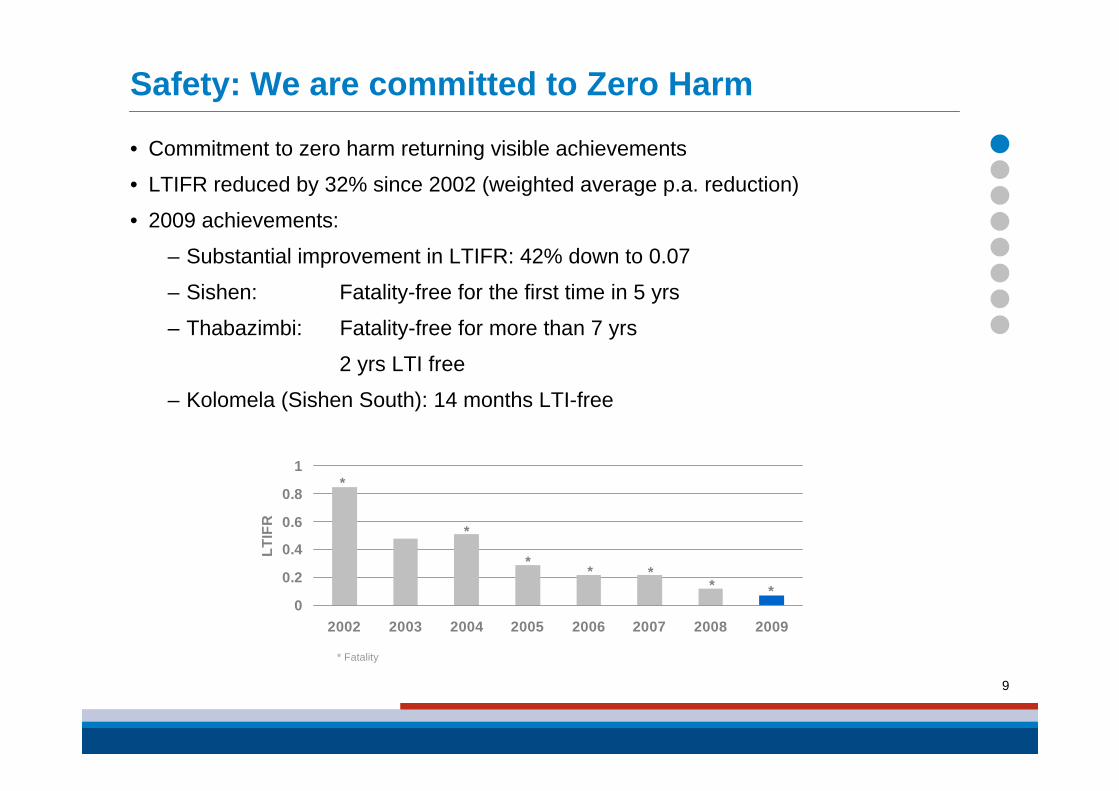

Safety: We are committed to Zero Harm

• Commitment to zero harm returning visible achievements

• LTIFR reduced by 32% since 2002 (weighted average p.a. reduction)

• 2009 achievements:

– Substantial improvement in LTIFR: 42% down to 0.07

– Sishen: Fatality-free for the first time in 5 yrs

– Thabazimbi: Fatality-free for more than 7 yrs

2 yrs LTI free

– Kolomela (Sishen South): 14 months LTI-free

*****

*

*

0

0.2

0.4

0.6

0.8

1

2002 2003 2004 2005 2006 2007 2008 2009

LTIF

R

* Fatality

10

Kumba’s operations

11

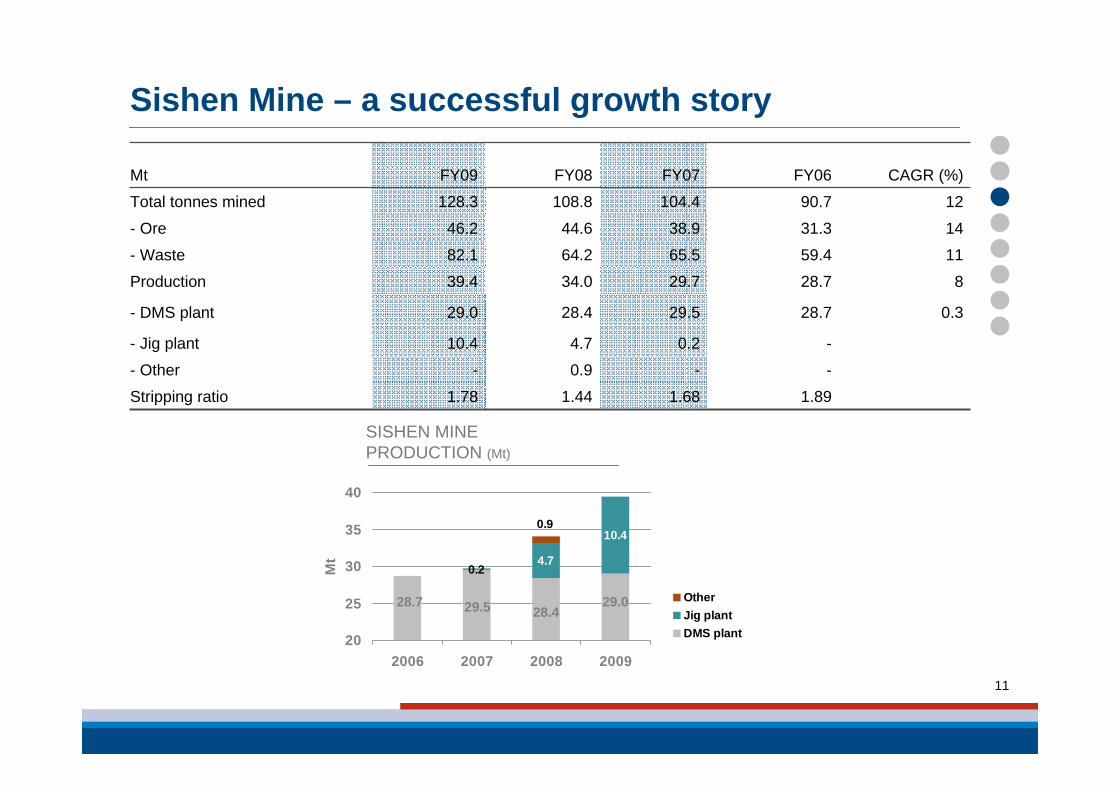

Sishen Mine – a successful growth story

--0.9-- Other

0.328.729.528.429.0- DMS plant

1.89

-

28.7

59.4

31.3

90.7

FY06

1.681.441.78Stripping ratio

0.24.710.4- Jig plant

Mt FY09 FY08 FY07 CAGR (%)

Total tonnes mined 128.3 108.8 104.4 12

- Ore 46.2 44.6 38.9 14

- Waste 82.1 64.2 65.5 11

Production 39.4 34.0 29.7 8

0.2

29.029.528.728.4

4.7

10.40.9

20

25

30

35

40

2006 2007 2008 2009

Mt

OtherJig plantDMS plant

SISHEN MINE PRODUCTION (Mt)

12

Sishen Mine – export sales 17% CAGR 2006-9

1227.430.530.538.2Total sales

1721.524.024.934.2- Export

5.9

24.3

FY06

(12)6.55.64.0- Domestic

Mt FY09 FY08 FY07 CAGR (%)

Railed to port 34.6 27.8 24.6 13

34.2

24.021.5

24.9

20

25

30

35

2006 2007 2008 2009

Mt

EXPORT SALES (Mt)

13

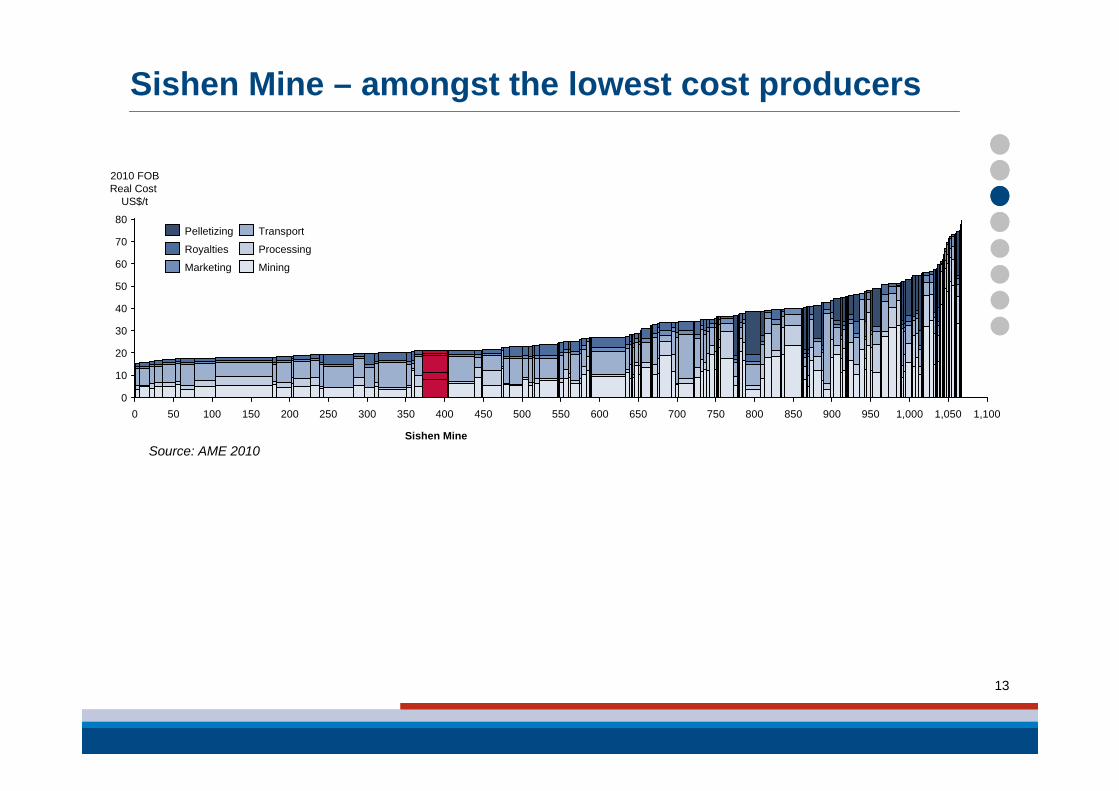

Sishen Mine – amongst the lowest cost producers

Source: AME 2010

Transport

Marketing

Royalties

Pelletizing

Mining

Processing

500400300200

80

1000 9000

350

20

250

40

1,000150

60

50

2010 FOBReal Cost

US$/t

800700600

Sishen Mine

450 550 650 850 950 1,050

10

30

50

70

1,100750

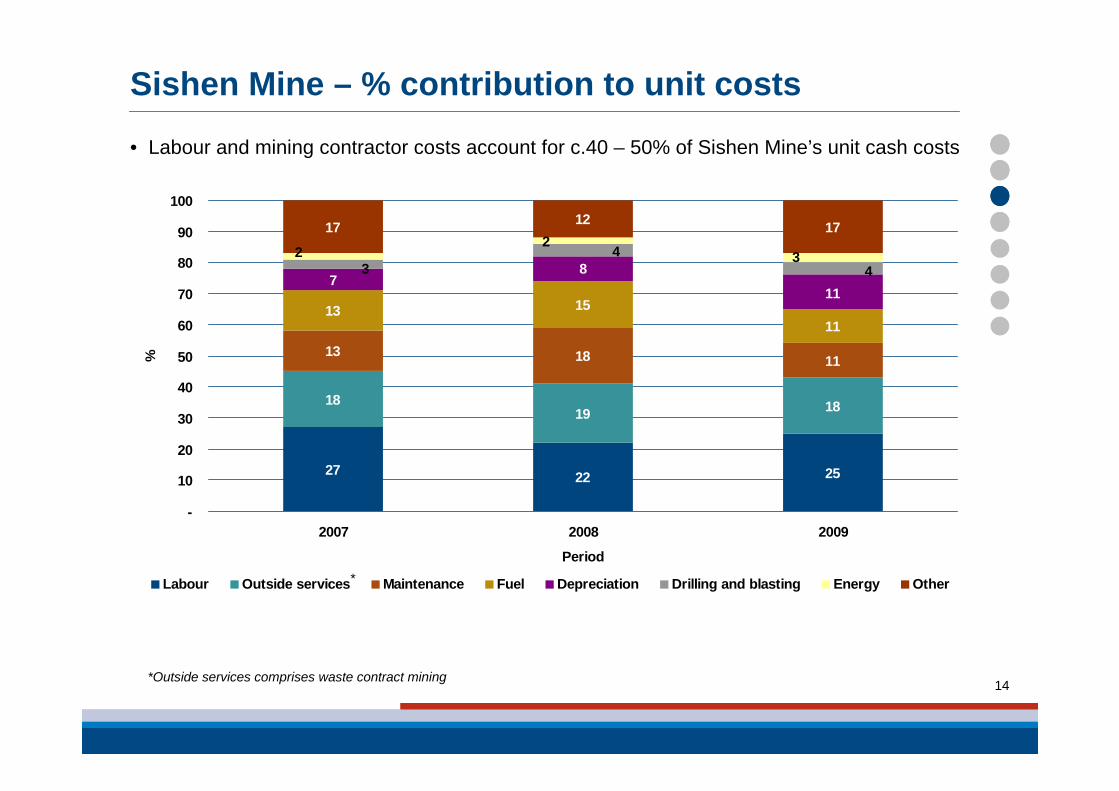

• Labour and mining contractor costs account for c.40 – 50% of Sishen Mine’s unit cash costs

14

Sishen Mine – % contribution to unit costs

27 22 25

1819 18

13 18 11

13 1511

17 12 17

11

87 4

43

32

2

-

10

20

30

40

50

60

70

80

90

100

2007 2008 2009

Period

%

Labour Outside services Maintenance Fuel Depreciation Drilling and blasting Energy Other*

*Outside services comprises waste contract mining

15

70

75

80

85

90

95

100

60% 62% 64% 66% 68% 70%

BrazilAustraliaAfricaIndiaCanada

Tumble index*

Iron content (%)

Sishen

Faleme

Vale – Corumba

Vale – Northern SystemVale – Southern System

Rio – Hamersley

BHP – Mt. Newman

Rio – West Angelas

Portman –Koolyanobbing

Rio – Hope Downs

Sesa Goa

Baffinland

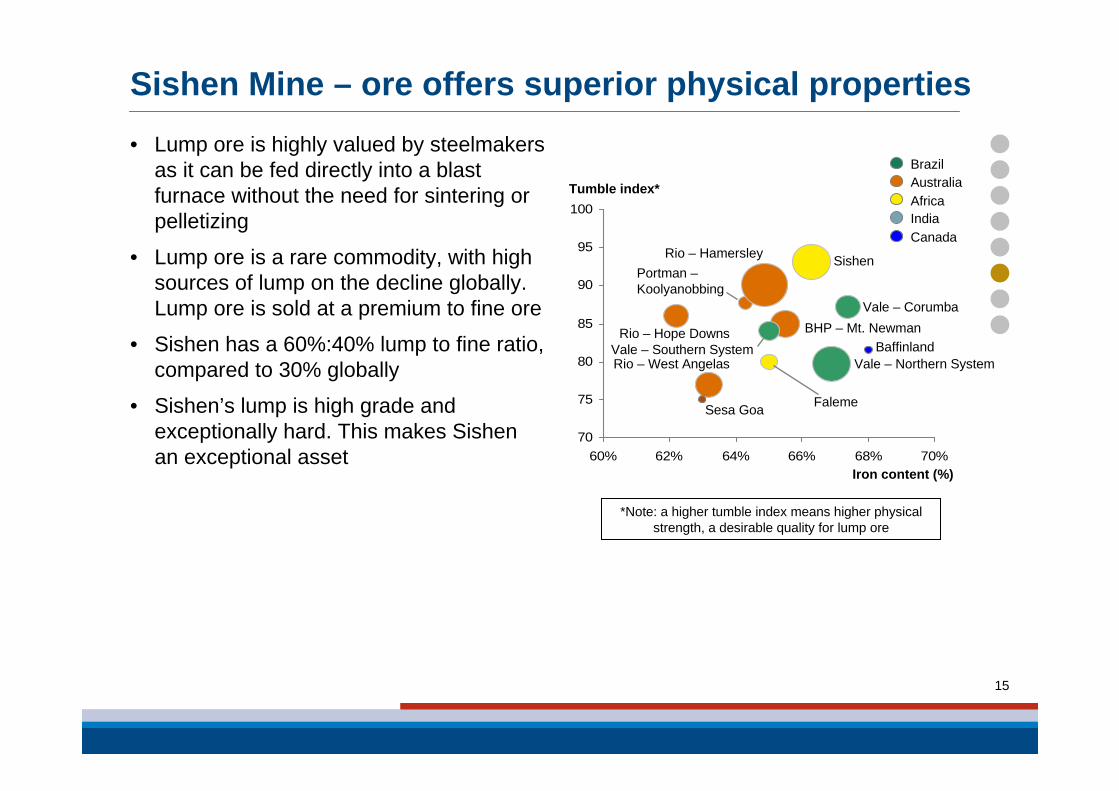

*Note: a higher tumble index means higher physical strength, a desirable quality for lump ore

• Lump ore is highly valued by steelmakers as it can be fed directly into a blast furnace without the need for sintering or pelletizing

• Lump ore is a rare commodity, with high sources of lump on the decline globally. Lump ore is sold at a premium to fine ore

• Sishen has a 60%:40% lump to fine ratio, compared to 30% globally

• Sishen’s lump is high grade and exceptionally hard. This makes Sishen an exceptional asset

Sishen Mine – ore offers superior physical properties

16

Sishen Mine – niche product’s capture value

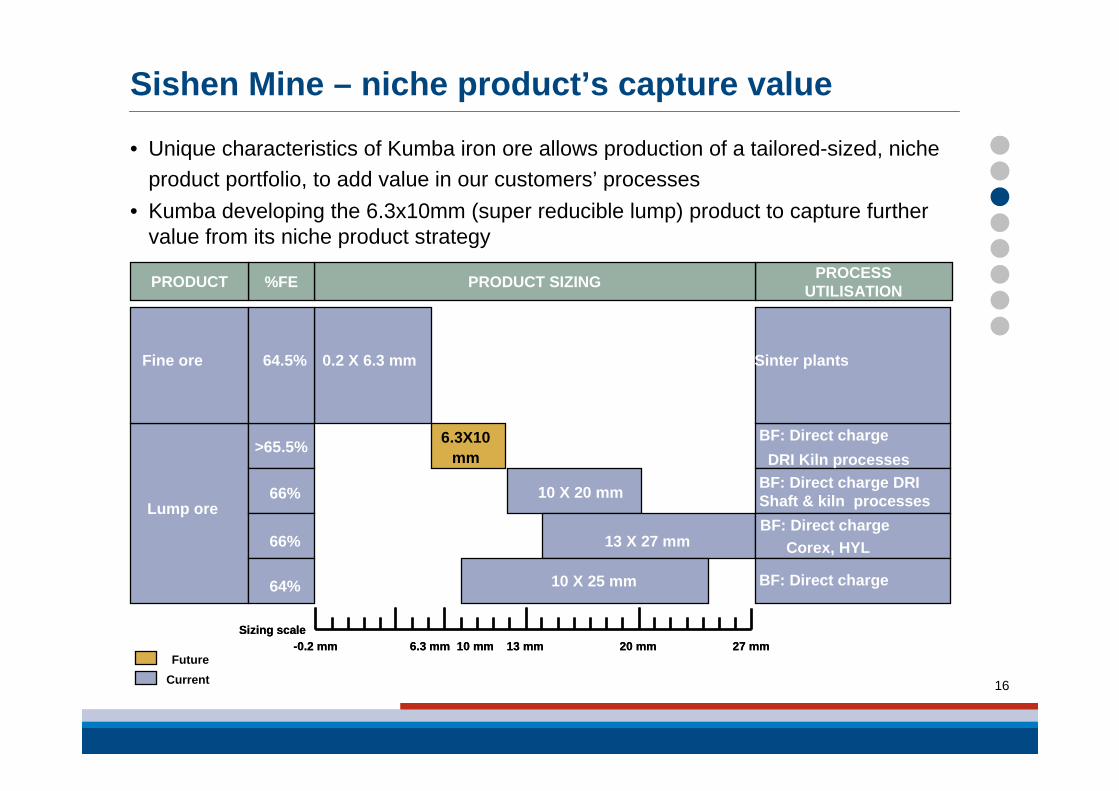

• Unique characteristics of Kumba iron ore allows production of a tailored-sized, niche product portfolio, to add value in our customers’ processes

• Kumba developing the 6.3x10mm (super reducible lump) product to capture further value from its niche product strategy

-0.2 mm 20 mm6.3 mm 13 mm10 mm 27 mmSizing scale

-0.2 mm 20 mm6.3 mm 13 mm10 mm 27 mmSizing scale

PROCESS UTILISATIONPRODUCT SIZING%FEPRODUCT

Lump ore

>65.5% 6.3X10mm

10 X 20 mm66%

66%

64%

BF: Direct chargeDRI Kiln processes

BF: Direct charge DRI Shaft & kiln processesBF: Direct charge

Corex, HYL

BF: Direct charge

Fine ore 64.5% 0.2 X 6.3 mm Sinter plants

13 X 27 mm

10 X 25 mm

FutureCurrent

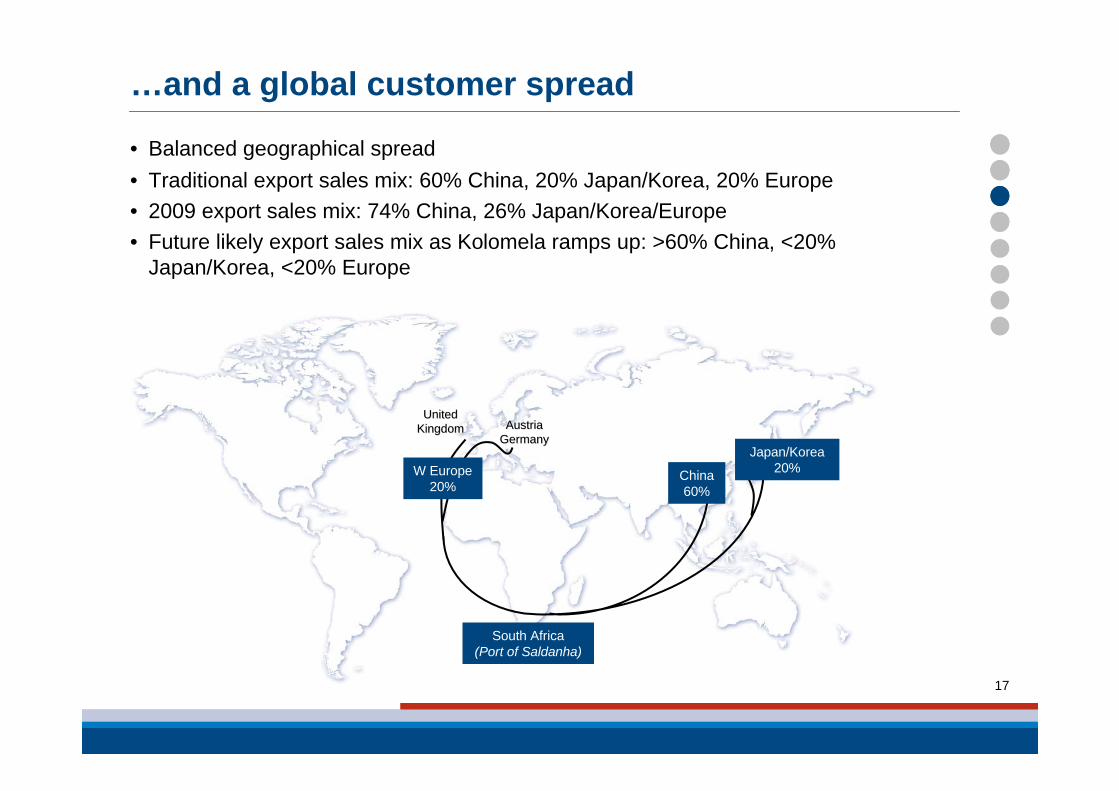

• Balanced geographical spread• Traditional export sales mix: 60% China, 20% Japan/Korea, 20% Europe• 2009 export sales mix: 74% China, 26% Japan/Korea/Europe• Future likely export sales mix as Kolomela ramps up: >60% China, <20%

Japan/Korea, <20% Europe

17

…and a global customer spread

United United KingdomKingdom AustriaAustria

GermanyGermanyJapan/Korea

20%China60%

W Europe20%

South Africa (Port of Saldanha)

18

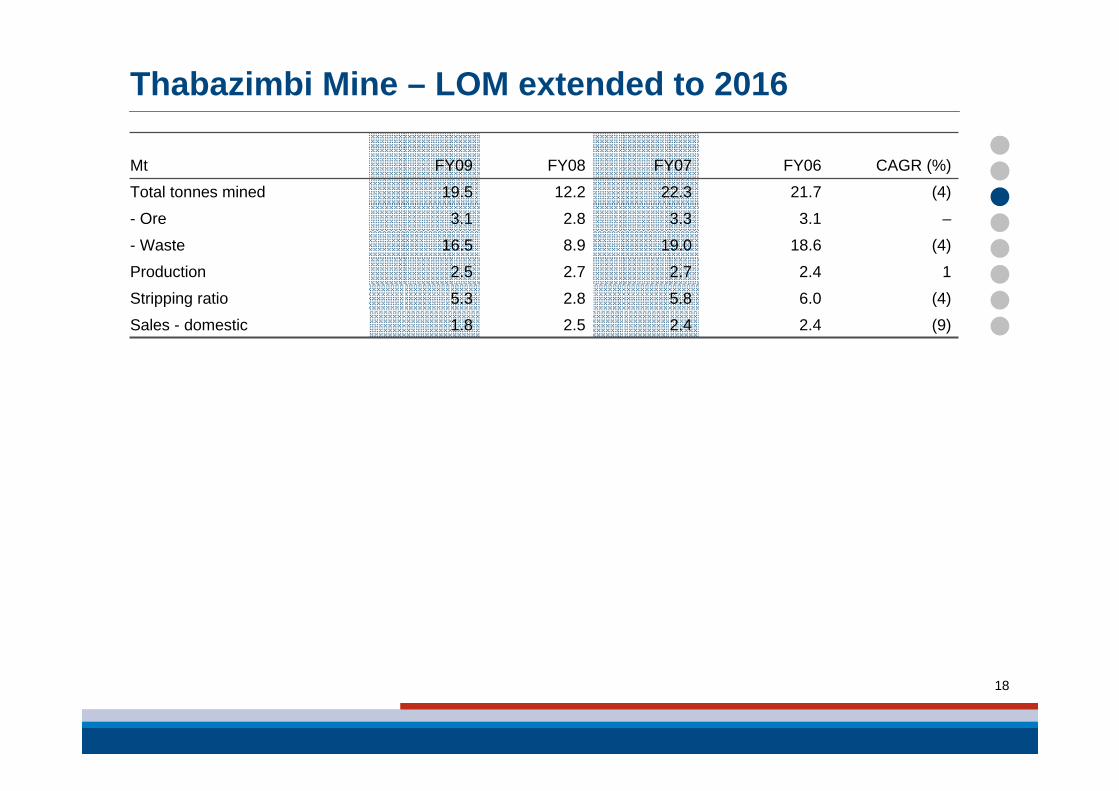

Thabazimbi Mine – LOM extended to 2016

(4)6.05.82.85.3Stripping ratio

2.4

2.4

18.6

3.1

21.7

FY06

(9)2.42.51.8Sales - domestic

Mt FY09 FY08 FY07 CAGR (%)

Total tonnes mined 19.5 12.2 22.3 (4)

- Ore 3.1 2.8 3.3 –

- Waste 16.5 8.9 19.0 (4)

Production 2.5 2.7 2.7 1

$24

$16

$32

Capex savings Opex savingsOnce off projects

19

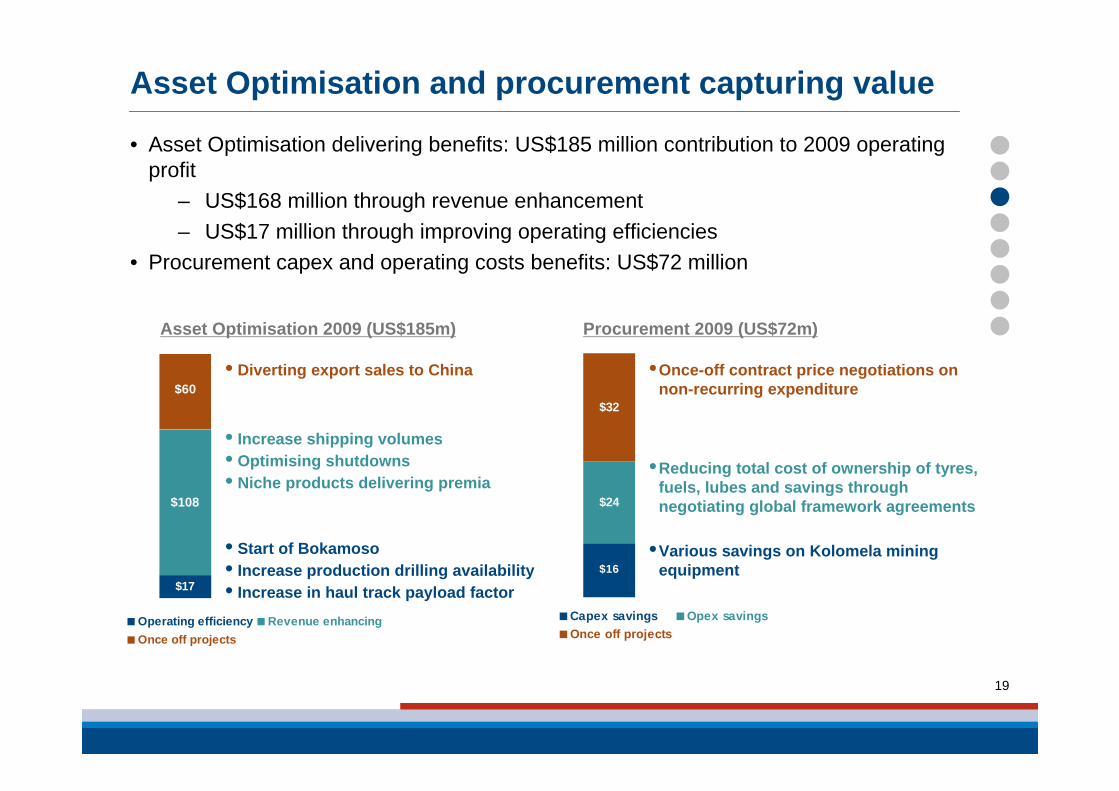

Asset Optimisation and procurement capturing value

• Asset Optimisation delivering benefits: US$185 million contribution to 2009 operating profit

– US$168 million through revenue enhancement– US$17 million through improving operating efficiencies

• Procurement capex and operating costs benefits: US$72 million

$108

$17

$60

Operating efficiency Revenue enhancingOnce off projects

Asset Optimisation 2009 (US$185m) Procurement 2009 (US$72m)

• Increase shipping volumes• Optimising shutdowns• Niche products delivering premia

• Start of Bokamoso• Increase production drilling availability• Increase in haul track payload factor

• Diverting export sales to China •Once-off contract price negotiations on non-recurring expenditure

•Reducing total cost of ownership of tyres, fuels, lubes and savings through negotiating global framework agreements

•Various savings on Kolomela mining equipment

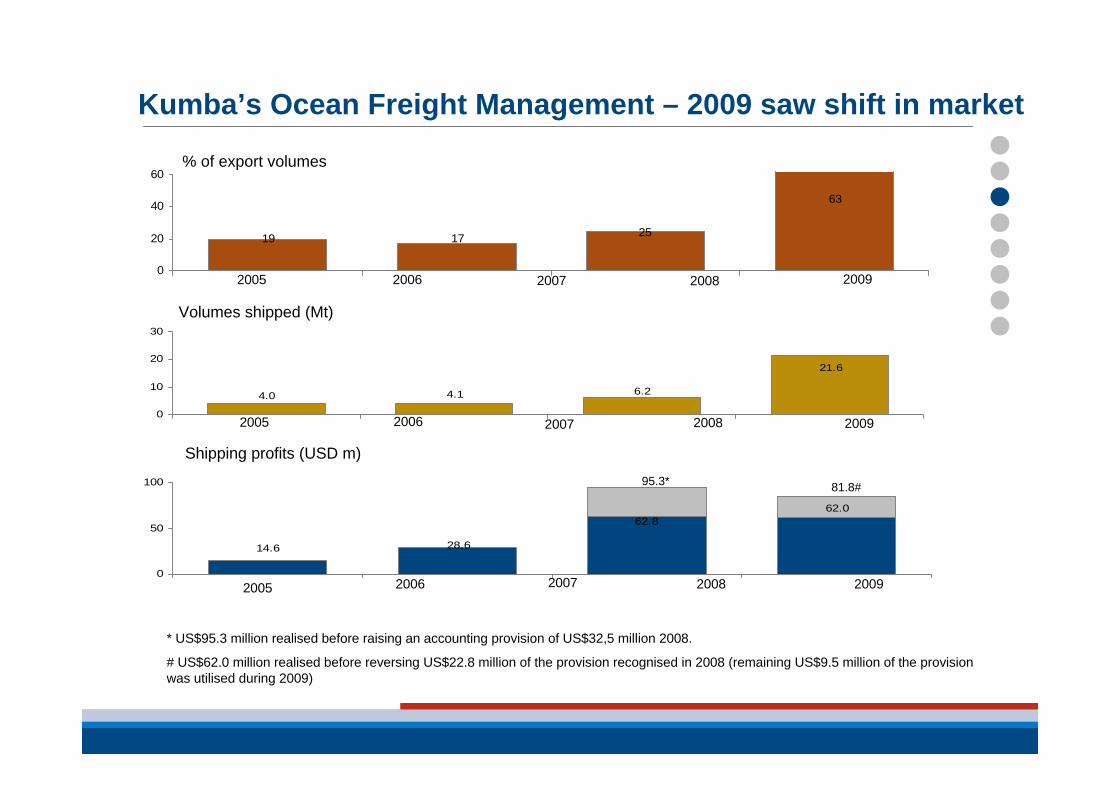

Kumba’s Ocean Freight Management – 2009 saw shift in market

63

251719

0

20

40

60

2005 2006 2007 2008 2009

% of export volumes

21.6

6.24.14.0

0

10

20

30

2005 2006 2007 2008 2009

Volumes shipped (Mt)

14.6 28.6

62.862.0

0

50

100

2005 2006 2007 2008 2009

Shipping profits (USD m)95.3*

* US$95.3 million realised before raising an accounting provision of US$32,5 million 2008.

# US$62.0 million realised before reversing US$22.8 million of the provision recognised in 2008 (remaining US$9.5 million of the provision was utilised during 2009)

81.8#

21

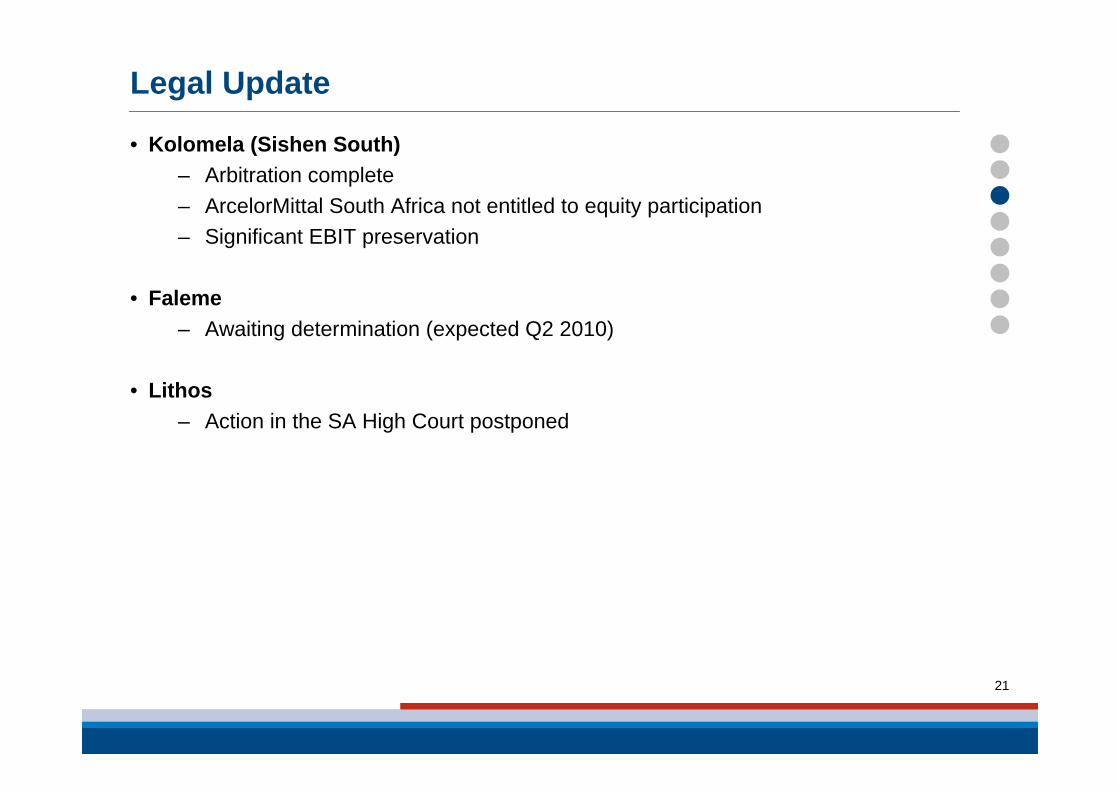

Legal Update

• Kolomela (Sishen South) – Arbitration complete– ArcelorMittal South Africa not entitled to equity participation– Significant EBIT preservation

• Faleme– Awaiting determination (expected Q2 2010)

• Lithos– Action in the SA High Court postponed

22

ArcelorMittal South Africa – Sishen Supply agreement

• 5th February 2010: Sishen Iron Ore Company (‘SIOC’) notified ArcelorMittal South Africa (‘Mittal’) that, as Mittal had failed to convert its 21.4% undivided share in the old order mining rights which it held in relation to the Sishen Mine, Kumba would no longer supply iron ore at cost plus 3%, but at market related prices

• 25th February 2010: SIOC offered an interim pricing agreement to Mittal

• 26th February 2010: Mittal released a SENS announcement declaring a dispute with SIOC

• 17th March 2010: SIOC announced it applied for the residual 21.4% mining right previously held by Mittal, on 1st May 2009. However, the Department of Mineral Resources had granted a prospecting right over the 21.4% interest to a third party, Imperial Crown Trading

• Kumba has appealed the grant of these prospecting rights, through the appeal process provided for in the MPRDA

23

Iron Ore market outlook

24

Iron Ore: Outlook is robust• Global GDP to recover from 2009 levels, driven by China and recovery in RoW

• Steel demand to recover robustly, partly due to restocking

• New projects expected to be approved in medium-term but long lead-times could result in effective deficit for number of years

• A sustained deficit will draw in high cost supply from China

• Higher prices in medium-term are supported

25

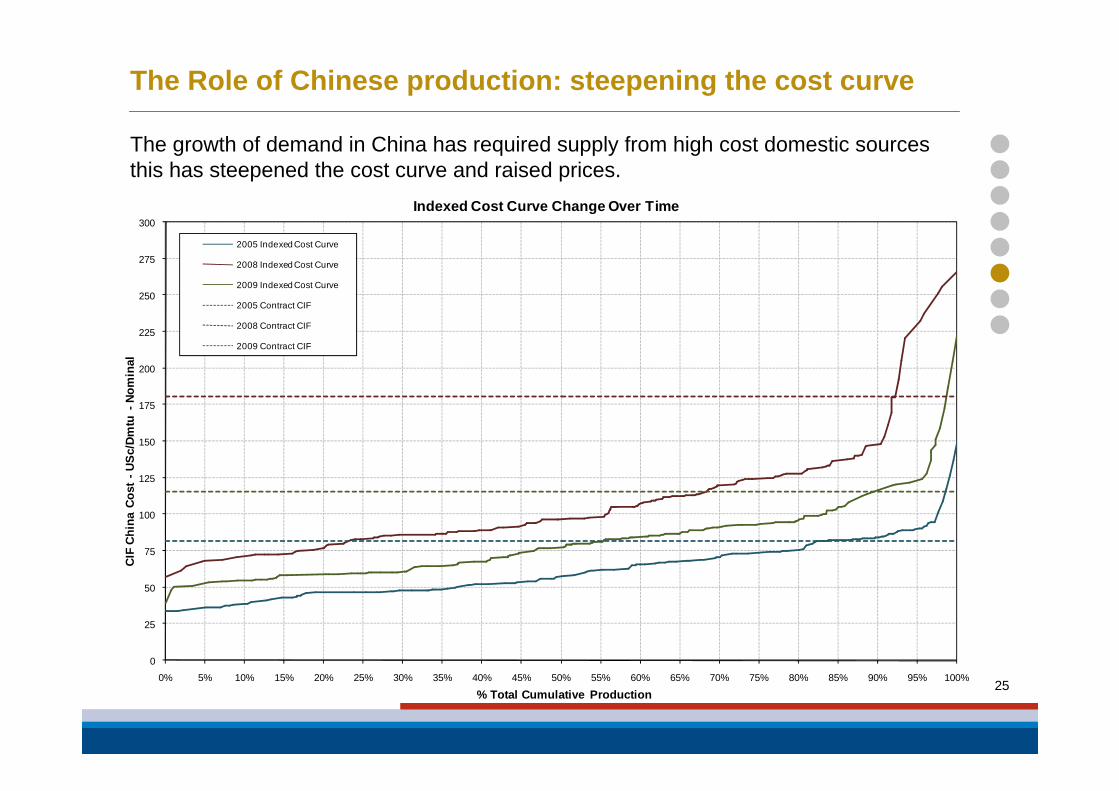

The Role of Chinese production: steepening the cost curve

The growth of demand in China has required supply from high cost domestic sources this has steepened the cost curve and raised prices.

0

25

50

75

100

125

150

175

200

225

250

275

300

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60% 65% 70% 75% 80% 85% 90% 95% 100%

CIF

Chi

na C

ost -

USc

/Dm

tu -

Nom

inal

% Total Cumulative Production

Indexed Cost Curve Change Over Time

2005 Indexed Cost Curve

2008 Indexed Cost Curve

2009 Indexed Cost Curve

2005 Contract CIF

2008 Contract CIF

2009 Contract CIF

26

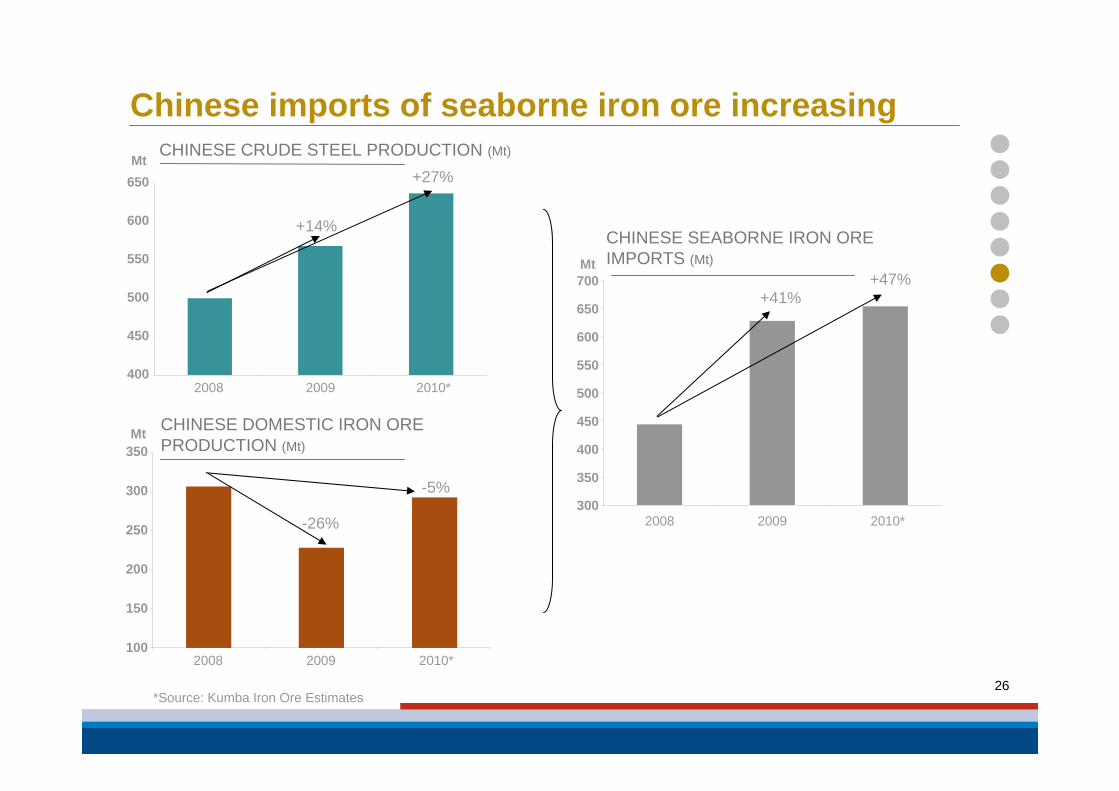

Chinese imports of seaborne iron ore increasing

400

450

500

550

600

650

2008 2009 2010*

CHINESE CRUDE STEEL PRODUCTION (Mt)

CHINESE DOMESTIC IRON ORE PRODUCTION (Mt)

100

150

200

250

300

350

2008 2009 2010*

-5%

+27%

-26%

+14%

300

350

400

450

500

550

600

650

700

2008 2009 2010*

CHINESE SEABORNE IRON ORE IMPORTS (Mt)

*Source: Kumba Iron Ore Estimates

Mt

Mt

Mt

+41%+47%

27

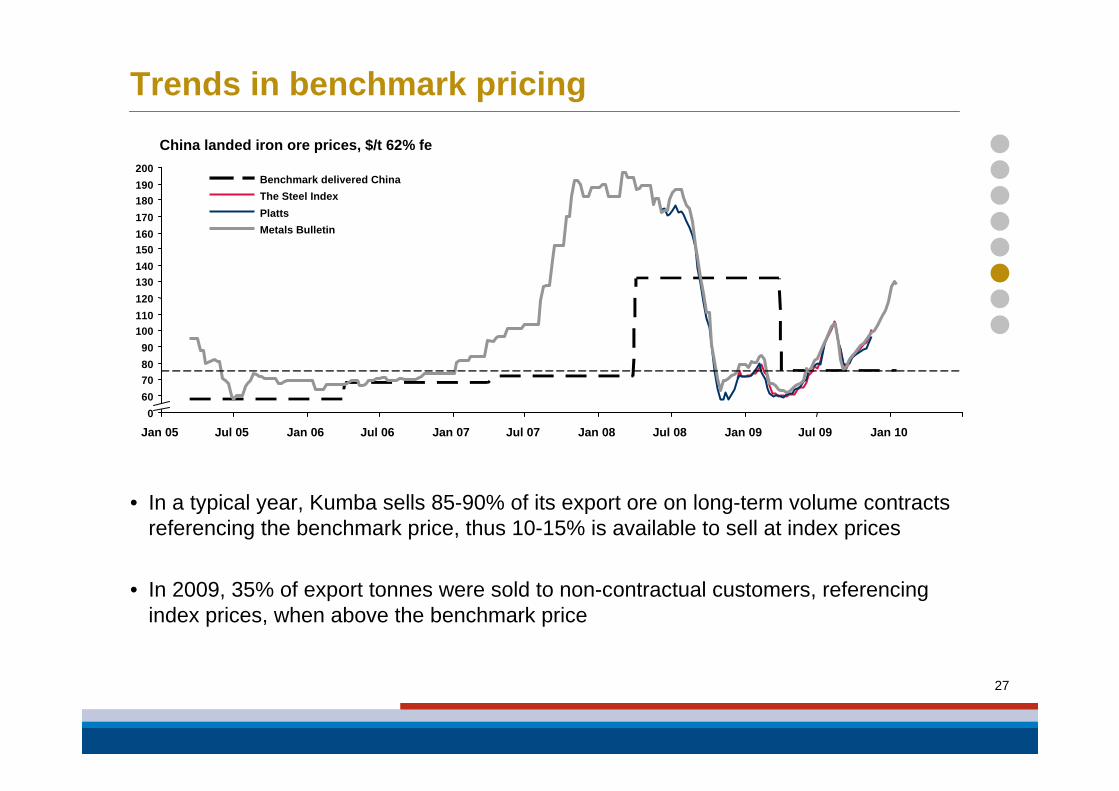

Trends in benchmark pricing

Jul 05 Jan 06Jan 05 Jul 09Jul 08

100

0

Jan 10Jan 08Jul 07Jan 07Jul 06

200

60

9080

110120130140

160

Jan 09

170180190

150

70

Metals BulletinPlattsThe Steel IndexBenchmark delivered China

China landed iron ore prices, $/t 62% fe

• In a typical year, Kumba sells 85-90% of its export ore on long-term volume contracts referencing the benchmark price, thus 10-15% is available to sell at index prices

• In 2009, 35% of export tonnes were sold to non-contractual customers, referencing index prices, when above the benchmark price

28

Projects

29

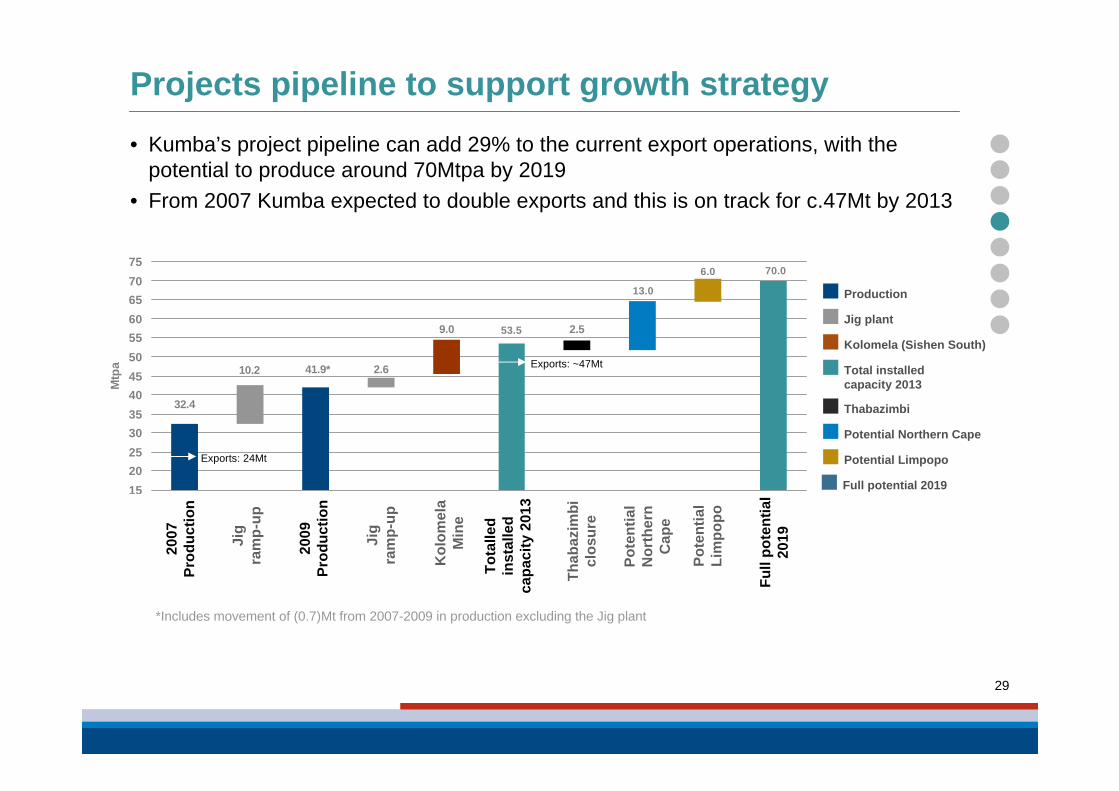

Projects pipeline to support growth strategy• Kumba’s project pipeline can add 29% to the current export operations, with the

potential to produce around 70Mtpa by 2019• From 2007 Kumba expected to double exports and this is on track for c.47Mt by 2013

9.0

6.0

2.610.2

13.0

2.553.5

70.0

32.4

41.9*

15202530354045505560657075

2007

Prod

uctio

n

Jig

ram

p-up

2009

Prod

uctio

n

Jig

ram

p-up

Kol

omel

aM

ine

Tota

lled

inst

alle

dca

paci

ty 2

013

Thab

azim

bicl

osur

e

Pote

ntia

lN

orth

ern

Cap

e

Pote

ntia

lLi

mpo

po

Full

pote

ntia

l20

19

Mtp

a

Potential Northern Cape

Thabazimbi

Total installedcapacity 2013

Kolomela (Sishen South)

Jig plant

Production

Full potential 2019

Potential LimpopoExports: 24Mt

Exports: ~47Mt

*Includes movement of (0.7)Mt from 2007-2009 in production excluding the Jig plant

2007

Pr

oduc

tion

Jig

ram

p-up

2009

Pr

oduc

tion

Jig

ram

p-up

Kol

omel

a M

ine

Tota

lled

inst

alle

d ca

paci

ty 2

013

Thab

azim

bi

clos

ure

Pote

ntia

l N

orth

ern

Cap

e

Pote

ntia

l Li

mpo

po

Full

pote

ntia

l 20

19

30

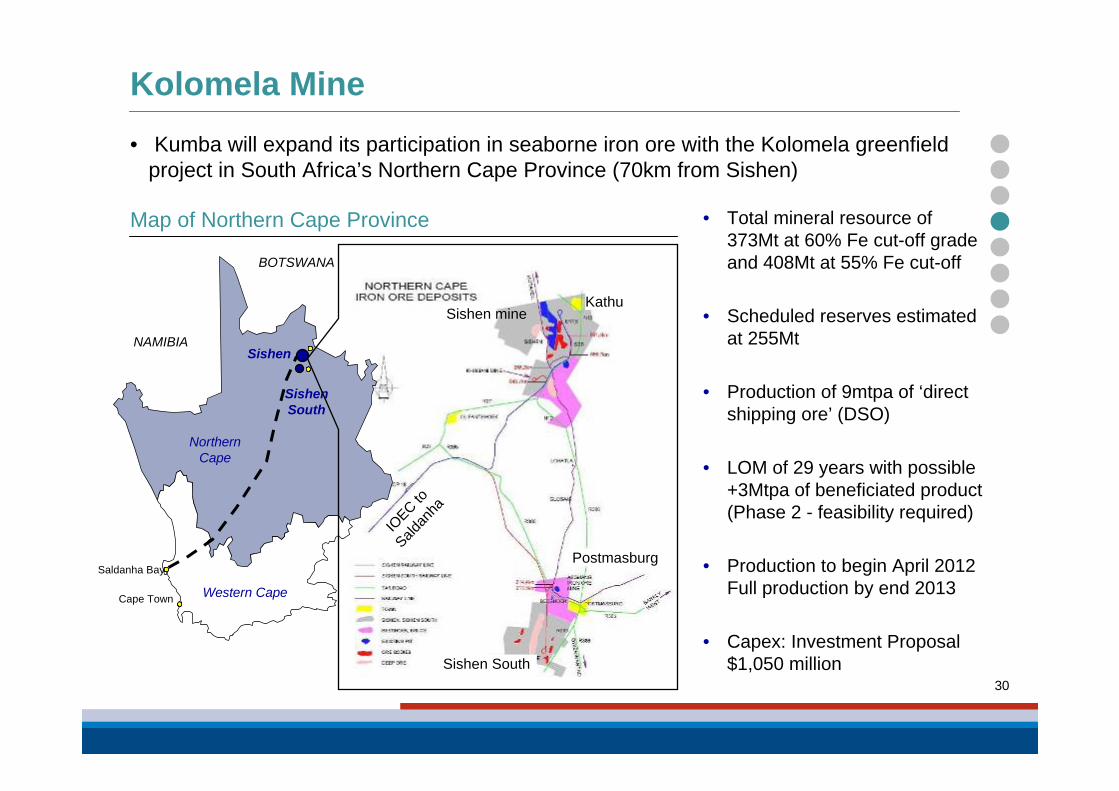

Kolomela Mine• Kumba will expand its participation in seaborne iron ore with the Kolomela greenfield

project in South Africa’s Northern Cape Province (70km from Sishen)

Map of Northern Cape Province • Total mineral resource of 373Mt at 60% Fe cut-off grade and 408Mt at 55% Fe cut-off

• Scheduled reserves estimated at 255Mt

• Production of 9mtpa of ‘direct shipping ore’ (DSO)

• LOM of 29 years with possible +3Mtpa of beneficiated product (Phase 2 - feasibility required)

• Production to begin April 2012Full production by end 2013

• Capex: Investment Proposal $1,050 million

Northern Cape

Western Cape

BOTSWANA

NAMIBIA

Cape Town

Sishen

Sishen South

Saldanha Bay

Sishen South

Postmasburg

Sishen mineKathu

IOEC to

Saldan

ha

31

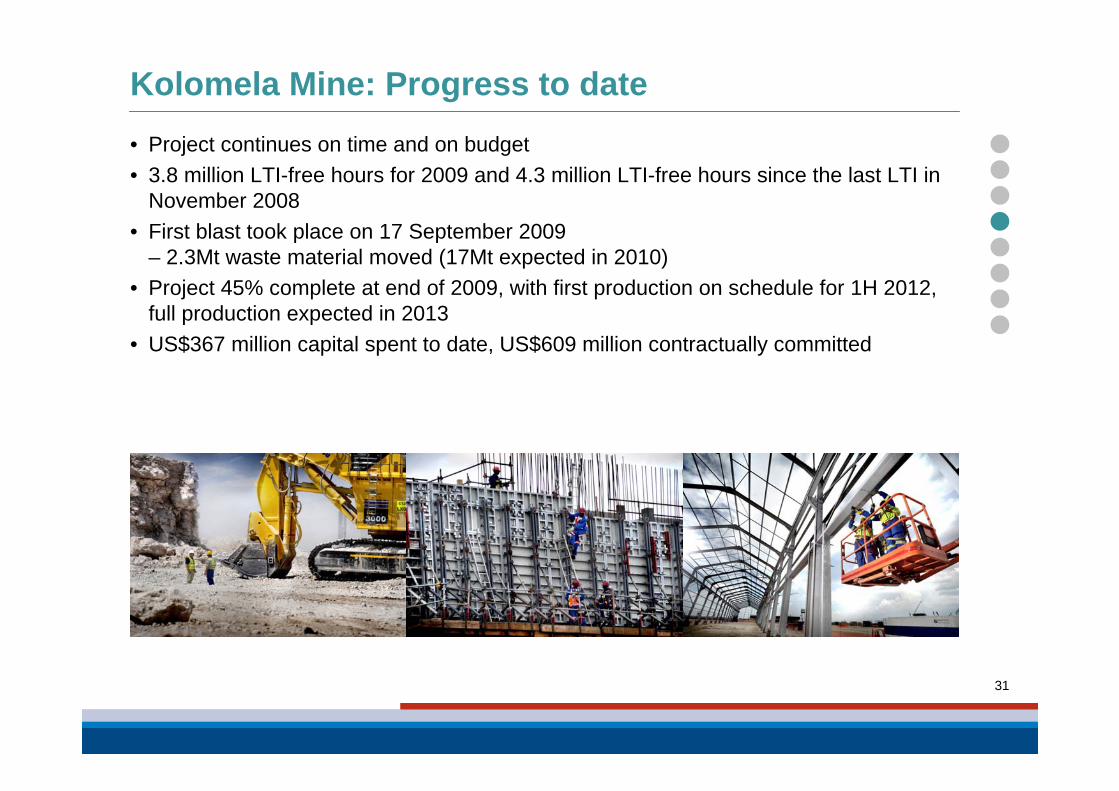

Kolomela Mine: Progress to date• Project continues on time and on budget• 3.8 million LTI-free hours for 2009 and 4.3 million LTI-free hours since the last LTI in

November 2008• First blast took place on 17 September 2009

– 2.3Mt waste material moved (17Mt expected in 2010)• Project 45% complete at end of 2009, with first production on schedule for 1H 2012,

full production expected in 2013• US$367 million capital spent to date, US$609 million contractually committed

256 151158

96

410395

156

2779*

-

500

1,000

2008 2009 2010 2011

US$

m

SIB Expansion Total capital expenditure

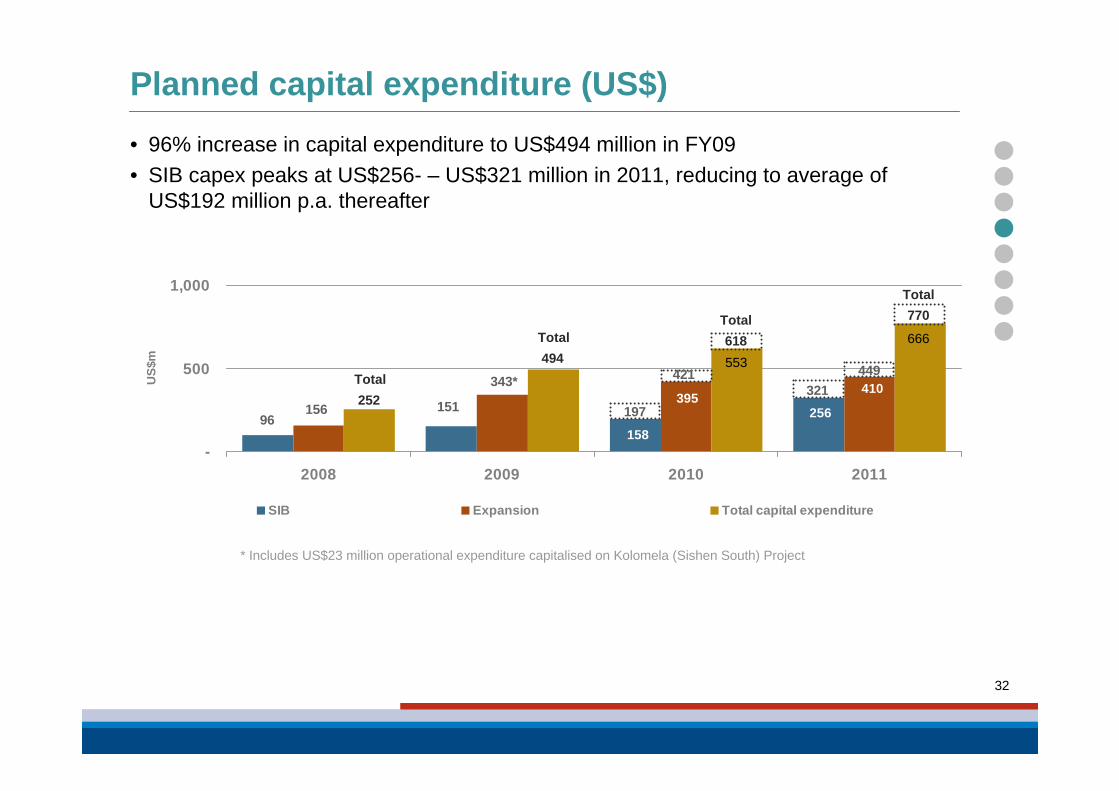

• 96% increase in capital expenditure to US$494 million in FY09• SIB capex peaks at US$256- – US$321 million in 2011, reducing to average of

US$192 million p.a. thereafter

32

Planned capital expenditure (US$)

Total494

Total618

Total770

* Includes US$23 million operational expenditure capitalised on Kolomela (Sishen South) Project

Total252

197

421553

321449

666

343*

15115696

33

In Summary

• Kumba is a leading value-adding iron ore supplier to the global steel industry

• Kumba has low-cost, long-life mining assets, supported by a significant growth pipeline

• Kumba is focused on revenue enhancement and cost management through Asset Optimisation, with savings already delivered and stretch targets being met

• Kumba has delivered significant cash to shareholders

• Kumba is fully committed to the achievement of zero harm for all its employees

34

Questions and Answers

“We see what could be”

35

Appendix

36

Kumba – executive committee

Chris GriffithKumba

CEO

Vincent Uren

Kumba CFO

Francois Louw

ExecutiveHead,

Projects

Christo van Loggerenberg

ExecutiveHead,

Technical Services

Virginia Tyobeka

Executive Head,

Human Resources

Tebello ChabanaExecutive

Head, Public Affairs

Vusani Mali

Company secretary

Andrew LootsGM of

Sishen Mine

Emmy LeekaGM of

Thabazimbi Mine

Aart van den

BrinkGM of

Kolomela Mine

12.9

6.05.4

13.5

0

5

10

15

2006 2007 2008 2009

R b

illio

n

37

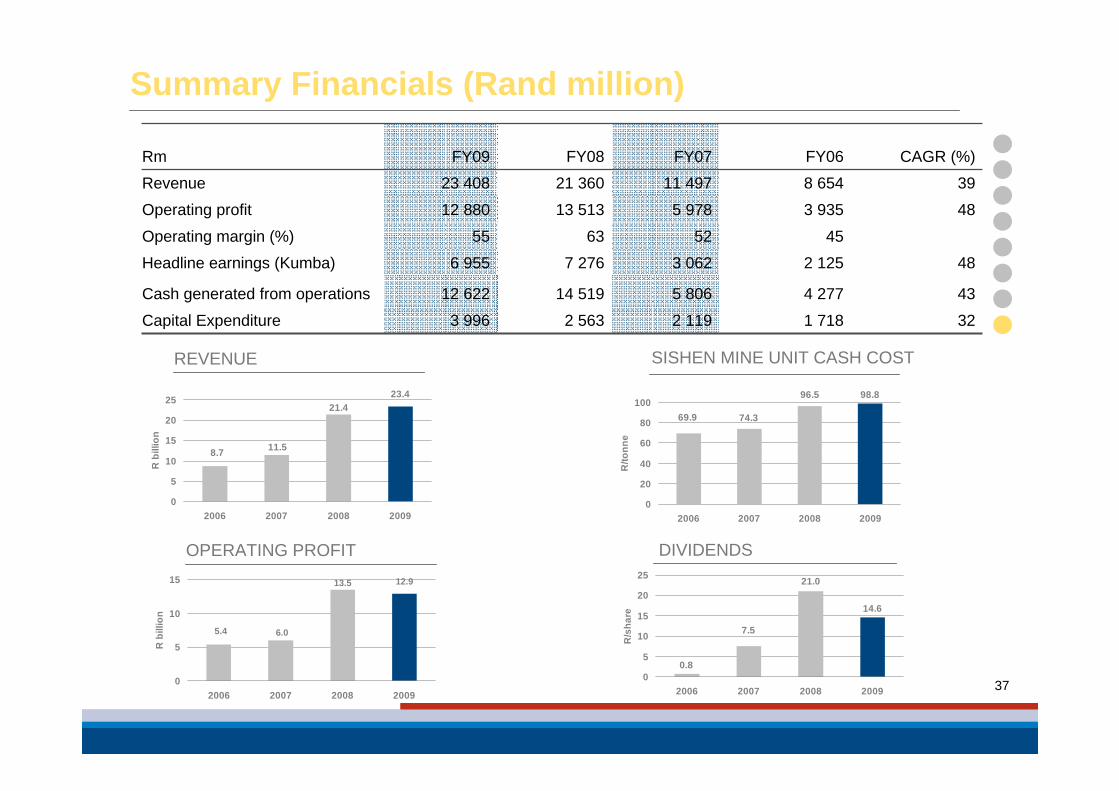

Summary Financials (Rand million)

OPERATING PROFIT

98.896.5

69.9 74.3

0

20

40

60

80

100

2006 2007 2008 2009

R/to

nne

SISHEN MINE UNIT CASH COST

DIVIDENDS

14.6

7.5

0.8

21.0

0

5

10

15

20

25

2006 2007 2008 2009

R/s

hare

23.4

11.58.7

21.4

0

5

10

15

20

25

2006 2007 2008 2009

R b

illio

n

REVENUE

1 718

4 277

2 125

45

3 935

8 654

FY06

322 1192 5633 996Capital Expenditure

435 80614 51912 622Cash generated from operations

Rm FY09 FY08 FY07 CAGR (%)

Revenue 23 408 21 360 11 497 39

Operating profit 12 880 13 513 5 978 48

Operating margin (%) 55 63 52

Headline earnings (Kumba) 6 955 7 276 3 062 48

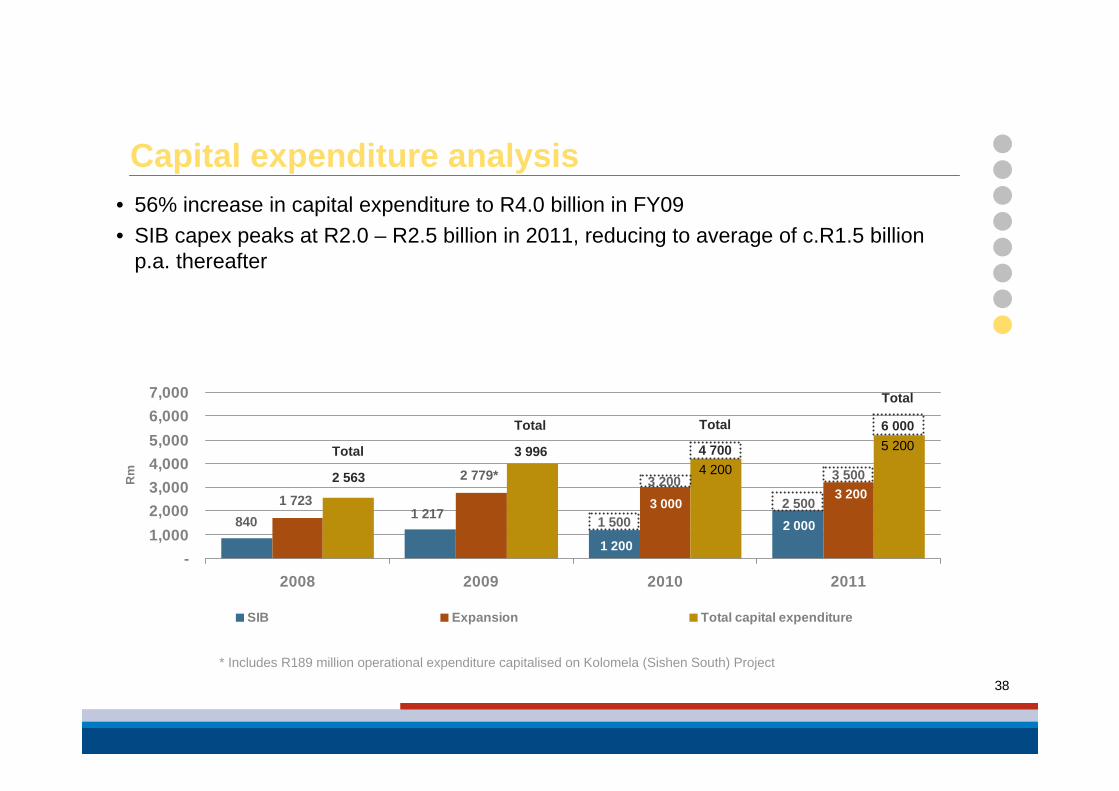

• 56% increase in capital expenditure to R4.0 billion in FY09• SIB capex peaks at R2.0 – R2.5 billion in 2011, reducing to average of c.R1.5 billion

p.a. thereafter

2 0001 217

1 200 840

3 2003 0001 723

2779*

-1,0002,0003,0004,0005,0006,0007,000

2008 2009 2010 2011

Rm

SIB Expansion Total capital expenditure

38

Capital expenditure analysis

Total

3 996

Total

4 700

Total

6 000

* Includes R189 million operational expenditure capitalised on Kolomela (Sishen South) Project

Total

2 563

1 500

3 2004 200

2 500

3 500

5 200

2 779*

1 2171 723

840

39

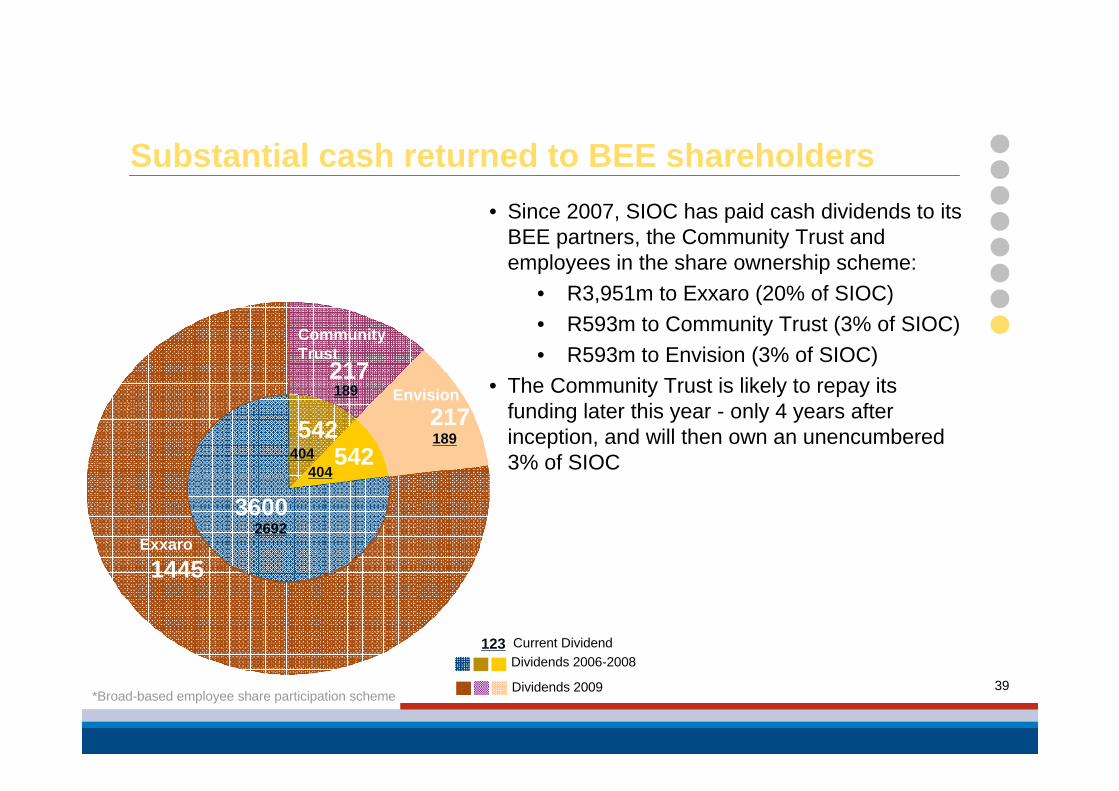

Substantial cash returned to BEE shareholders• Since 2007, SIOC has paid cash dividends to its

BEE partners, the Community Trust and employees in the share ownership scheme:

• R3,951m to Exxaro (20% of SIOC)• R593m to Community Trust (3% of SIOC)• R593m to Envision (3% of SIOC)

• The Community Trust is likely to repay its funding later this year - only 4 years after inception, and will then own an unencumbered 3% of SIOC

Dividends 2006-2008

Dividends 2009*Broad-based employee share participation scheme

Envision

123 Current Dividend

1445

3600

217

217542

542

Exxaro

Community Trust

2692

404404

189

189

Envision

40

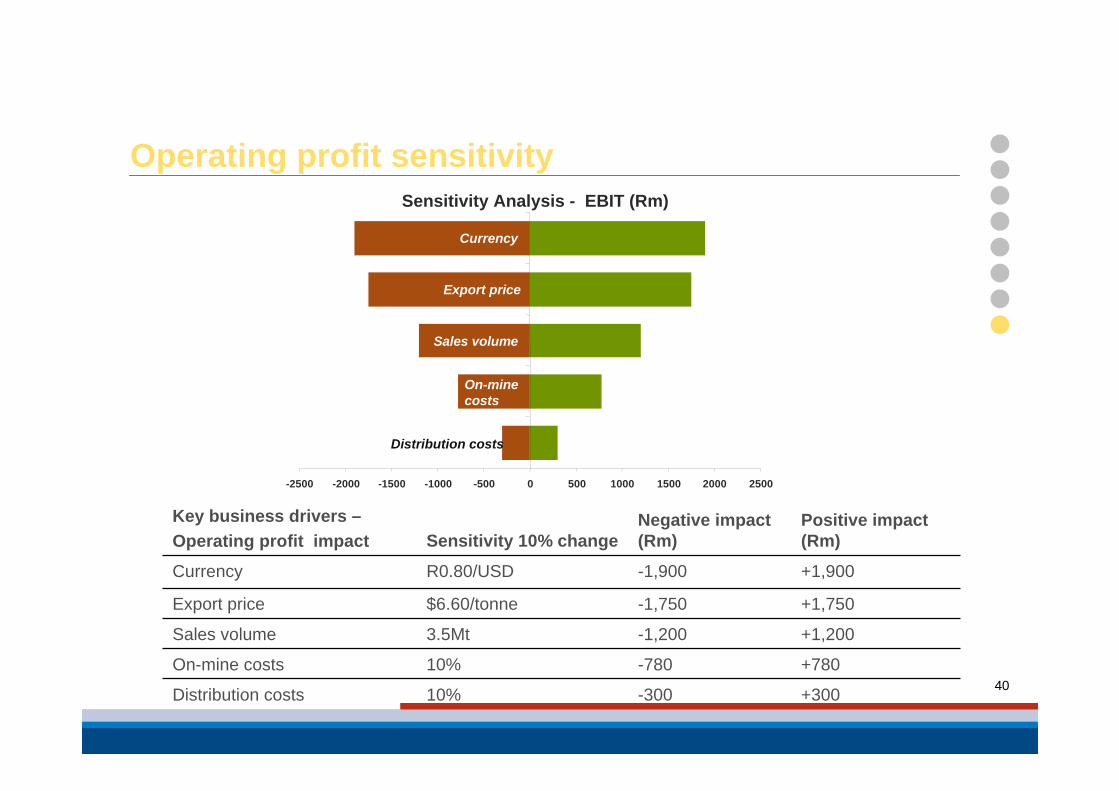

Operating profit sensitivity

+300-30010%Distribution costs

+780-78010%On-mine costs

+1,200-1,2003.5MtSales volume

+1,750-1,750$6.60/tonneExport price

+1,900-1,900R0.80/USDCurrency

Positive impact (Rm)

Negative impact (Rm)Sensitivity 10% change

Key business drivers –Operating profit impact

Sensitivity Analysis - EBIT (Rm)

-2500 -2000 -1500 -1000 -500 0 500 1000 1500 2000 2500

Distribution costs

On-minecosts

Sales volume

Export price

Currency