Embed Size (px)

Citation preview

SKILLING INDIA

NOVEMBER 2010

THE BILLION PEOPLE CHALLENGE

Skilling India The Billion People Challenge

A report by CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010

Skilling India The Billion People Challenge

A report by CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010

Key messages

population 1.2 billion

1.5 billion

working-age population 749 million

962 million

423 million

unemployed unable to participate in the job market

•

•

•

•

•

•

•

•

•

With its forecast to rise from in 2010 to almost

in the next twenty years, India will become the world’s most

populous country by 2030.

India is also set to become the largest contributor to the global workforce.

Its (15-59 years) is likely to swell from

to over 2010 to 2030.

If India’s working-age population, its so-called demographic dividend, is

productively employed, India’s economic growth prospects will brighten.

India can create jobs in the scale required on a sustained basis only with

changes in its policy frameworks for education and workforce management.

If the current trends in India’s labour participation and unemployment rate

continue, about in India’s working-age population will be

or by 2030.

Since the job market is biased towards high-skill labour, the creation of jobs

for low-skill labour, who would continue to dominate its workforce, will

challenge India.

Closing the skill gaps of its qualified workforce will be critical, as India

depends more on human capital than its peer countries that have a similar

level of economic development.

The workforce will increase the most in states that are the poorest and offer

the lowest employment opportunity. Creating jobs for the swelling

workforce in these states will be a major challenge.

Labour skill-mismatch and shortage could adversely impact India’s

economic growth and wage costs; India would have to bear a greater fiscal

burden to support its unemployed.

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 1

Analytical contacts

Dharmakirti JoshiVidya Mahambare

Poonam Munjal

[email protected]@[email protected]

Errata - Earlier print run of the report had a data error in the third paragraph of page 11. This error has been rectified in this soft copy

Key messages

population 1.2 billion

1.5 billion

working-age population 749 million

962 million

423 million

unemployed unable to participate in the job market

•

•

•

•

•

•

•

•

•

With its forecast to rise from in 2010 to almost

in the next twenty years, India will become the world’s most

populous country by 2030.

India is also set to become the largest contributor to the global workforce.

Its (15-59 years) is likely to swell from

to over 2010 to 2030.

If India’s working-age population, its so-called demographic dividend, is

productively employed, India’s economic growth prospects will brighten.

India can create jobs in the scale required on a sustained basis only with

changes in its policy frameworks for education and workforce management.

If the current trends in India’s labour participation and unemployment rate

continue, about in India’s working-age population will be

or by 2030.

Since the job market is biased towards high-skill labour, the creation of jobs

for low-skill labour, who would continue to dominate its workforce, will

challenge India.

Closing the skill gaps of its qualified workforce will be critical, as India

depends more on human capital than its peer countries that have a similar

level of economic development.

The workforce will increase the most in states that are the poorest and offer

the lowest employment opportunity. Creating jobs for the swelling

workforce in these states will be a major challenge.

Labour skill-mismatch and shortage could adversely impact India’s

economic growth and wage costs; India would have to bear a greater fiscal

burden to support its unemployed.

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 1

Analytical contacts

Dharmakirti JoshiVidya Mahambare

Poonam Munjal

[email protected]@[email protected]

Errata - Earlier print run of the report had a data error in the third paragraph of page 11. This error has been rectified in this soft copy

Contents

Introduction ........................................................................................ 3

India’s demographic edge in the global context ................................. 4

India’s labour supply ........................................................................... 5

India’s labour demand ........................................................................10

The outcome........................................................................................13

Conclusion...........................................................................................16

Introduction

Evolving demographics unambiguously point out that India will remain a young

nation and the largest contributor to the global workforce over the next few

decades - an exceptional strength compared to the rapidly ageing population in

the Western countries, and that in China, owing to its one-child policy. Although

investment, reforms and infrastructure are likely drivers of India’s economic

growth, no growth driver is as certain as the availability of people in India’s

working-age group. A young population is India’s demographic dividend. It

gives India the potential to become a global production hub as well as a large

consumer of goods and services. Further, since the age-group of 45-60 years is

the key contributor to household savings, India’s savings rate, which has

increased rapidly in the last decade, will get a further boost thereby supporting

investment.

The rise in its working-age population, however, is necessary but not sufficient

for India to sustain its economic growth. If India does not create enough jobs

and its workers are not adequately prepared for those jobs, its demographic

dividend may turn into a liability.

This report examines the pros and cons of the swelling working-age population

by taking stock of India’s likely demand for labour. It analyses India’s labour-

market imbalances and highlights how skill mismatch and shortage can impact

productivity growth which is critical for India to enhance its long-term growth.

And finally, it identifies fiscal implications of India’s population dynamics.

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 3

Quality Quantity

Educati no

il sSk l

Yo n nu g a dl gar e

o f rw rk o ce

2

Contents

Introduction ........................................................................................ 3

India’s demographic edge in the global context ................................. 4

India’s labour supply ........................................................................... 5

India’s labour demand ........................................................................10

The outcome........................................................................................13

Conclusion...........................................................................................16

Introduction

Evolving demographics unambiguously point out that India will remain a young

nation and the largest contributor to the global workforce over the next few

decades - an exceptional strength compared to the rapidly ageing population in

the Western countries, and that in China, owing to its one-child policy. Although

investment, reforms and infrastructure are likely drivers of India’s economic

growth, no growth driver is as certain as the availability of people in India’s

working-age group. A young population is India’s demographic dividend. It

gives India the potential to become a global production hub as well as a large

consumer of goods and services. Further, since the age-group of 45-60 years is

the key contributor to household savings, India’s savings rate, which has

increased rapidly in the last decade, will get a further boost thereby supporting

investment.

The rise in its working-age population, however, is necessary but not sufficient

for India to sustain its economic growth. If India does not create enough jobs

and its workers are not adequately prepared for those jobs, its demographic

dividend may turn into a liability.

This report examines the pros and cons of the swelling working-age population

by taking stock of India’s likely demand for labour. It analyses India’s labour-

market imbalances and highlights how skill mismatch and shortage can impact

productivity growth which is critical for India to enhance its long-term growth.

And finally, it identifies fiscal implications of India’s population dynamics.

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 3

Quality Quantity

Educati no

il sSk l

Yo n nu g a dl gar e

o f rw rk o ce

2

Indian demographics in the global context

India will be the world's most populous country by 2030…

…and have the largest working-age population

India’s share in world population in 2010, at 17.6 per cent, is the

largest, after China, according to UN World Population Prospects

2008. With India’s population forecast to grow at 1.0 per cent per

year, significantly faster than that of China at 0.4 per cent per year,

India will become the most populated country in the world by 2030.

India’s population is likely to rise from 1.21 billion in 2010 to 1.48

billion by 2030, and further to 1.6 billion by 2050 (figure 1).

More significantly, India will have the largest number of people in the

working age group of 15-59 years (figure 1). (The working age group,

as per the Indian definition, is taken as the age group of 15-59 years

throughout this report.) As on 2010, half of India’s population is

below 25 years of age, and 62 per cent of its population is in the

working-age group. India, thus, accounts for 17.5 per cent of the

world’s total working-age population. From 2010 to 2030, India’s total

working-age population is poised to rise from 749 million to 962

million, accounting for about 28 per cent of the increase in the

world’s total working-age population over the period. In contrast, the

working-age population of China will shrink by 45 million (figure 2).

India’s labour supply

How many?

Only 61 per cent of working-age population is available for work

Working women are a minority

India has a higher real-dependency ratio

According to the National Sample Survey Organisation’s (NSSO)

latest large-sample survey in 2004-05, India’s labour-force

participation rate was a mere 61 per cent for that year. The balance

39 per cent of the working-age population, consisting mostly of

women, kept away from the workforce for various reasons such as

studying further (9.3 per cent), raising children and managing

households (15.9 per cent), or engaging themselves in other

household duties (12.1 per cent).

According to the NSSO survey, while only 13.8 per cent of working-

age men stayed out of India’s workforce in 2004-05, most of whom

did so to study further, about 65.4 per cent of working-age women

kept away from work. Hence, of the 282 million working-age

women, only around 94 million were employed and another 4.3

million women were looking for work.

India’s real dependency ratio of 1.67 dependents per employed

person in 2010 far exceeds the conventional dependency ratio of

0.62. A cause for optimism is, the real and conventional dependency

ratios are both set to decline over the next few decades - while the

conventional dependency ratio will come down from 0.62 in 2010 to

0.54 in 2030, the real dependency ratio will fall from 1.67 to 1.54 over

the period.

In India, the working-age population

represents the total number of people in the

working-age group of 15-59 years. 'Labour-force participation rate' refers to the share

of people in this group, who are working or are willing to work, in total working-age population.

213

14

-11-45 -54

340

Africa India US Japan China Europe

Figure 2

Addition to working age population between 2010

and 2030

0-14 years

15-59 years

60+ years

2040 2050

0

600

1,200

1,800

2010 2020 2030

millionFigure 1

India’s bulging

working-age population

Source: UN World Population Prospects, 2008 Revision

Source: UN World Population Prospects, 2008 Revision

Given India's low rate of labour-force

participation, its dependency ratio (DR) - a conventional measure of the number of

children and old-aged persons supported by

each working-age person - masks the extent of dependency. Real dependency ratio

(RDR), measured as the proportion of non-working population - children, old-age and working-age people who are not working -

to working population, would be a more appropriate measure of the dependency.

million

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 5

4

India is set to become the largest

contributor to the global workforce.

Indian demographics in the global context

India will be the world's most populous country by 2030…

…and have the largest working-age population

India’s share in world population in 2010, at 17.6 per cent, is the

largest, after China, according to UN World Population Prospects

2008. With India’s population forecast to grow at 1.0 per cent per

year, significantly faster than that of China at 0.4 per cent per year,

India will become the most populated country in the world by 2030.

India’s population is likely to rise from 1.21 billion in 2010 to 1.48

billion by 2030, and further to 1.6 billion by 2050 (figure 1).

More significantly, India will have the largest number of people in the

working age group of 15-59 years (figure 1). (The working age group,

as per the Indian definition, is taken as the age group of 15-59 years

throughout this report.) As on 2010, half of India’s population is

below 25 years of age, and 62 per cent of its population is in the

working-age group. India, thus, accounts for 17.5 per cent of the

world’s total working-age population. From 2010 to 2030, India’s total

working-age population is poised to rise from 749 million to 962

million, accounting for about 28 per cent of the increase in the

world’s total working-age population over the period. In contrast, the

working-age population of China will shrink by 45 million (figure 2).

India’s labour supply

How many?

Only 61 per cent of working-age population is available for work

Working women are a minority

India has a higher real-dependency ratio

According to the National Sample Survey Organisation’s (NSSO)

latest large-sample survey in 2004-05, India’s labour-force

participation rate was a mere 61 per cent for that year. The balance

39 per cent of the working-age population, consisting mostly of

women, kept away from the workforce for various reasons such as

studying further (9.3 per cent), raising children and managing

households (15.9 per cent), or engaging themselves in other

household duties (12.1 per cent).

According to the NSSO survey, while only 13.8 per cent of working-

age men stayed out of India’s workforce in 2004-05, most of whom

did so to study further, about 65.4 per cent of working-age women

kept away from work. Hence, of the 282 million working-age

women, only around 94 million were employed and another 4.3

million women were looking for work.

India’s real dependency ratio of 1.67 dependents per employed

person in 2010 far exceeds the conventional dependency ratio of

0.62. A cause for optimism is, the real and conventional dependency

ratios are both set to decline over the next few decades - while the

conventional dependency ratio will come down from 0.62 in 2010 to

0.54 in 2030, the real dependency ratio will fall from 1.67 to 1.54 over

the period.

In India, the working-age population

represents the total number of people in the

working-age group of 15-59 years. 'Labour-force participation rate' refers to the share

of people in this group, who are working or are willing to work, in total working-age population.

213

14

-11-45 -54

340

Africa India US Japan China Europe

Figure 2

Addition to working age population between 2010

and 2030

0-14 years

15-59 years

60+ years

2040 2050

0

600

1,200

1,800

2010 2020 2030

millionFigure 1

India’s bulging

working-age population

Source: UN World Population Prospects, 2008 Revision

Source: UN World Population Prospects, 2008 Revision

Given India's low rate of labour-force

participation, its dependency ratio (DR) - a conventional measure of the number of

children and old-aged persons supported by

each working-age person - masks the extent of dependency. Real dependency ratio

(RDR), measured as the proportion of non-working population - children, old-age and working-age people who are not working -

to working population, would be a more appropriate measure of the dependency.

million

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 5

4

India is set to become the largest

contributor to the global workforce.

Regional demographic diversity will be unfavourable

How good?

High levels of illiteracy

According to Census of India’s population projections, Uttar

Pradesh, Bihar, Madhya Pradesh and Rajasthan will account for more

than 50 per cent of the increase in India’s working age population

over 2011 to 2021. These states, also the poorest four states among

the 15 major states, based on per capita income (Net Domestic

Product), would add 54 million to India’s workforce, whereas the four

most affluent states - Haryana, Maharashtra, Punjab and Gujarat -

would together add only 21.6 million to the workforce (figure 3). The

maximum increase in working-age population will therefore take

place in states that are the poorest and offer the lowest employment

opportunity.

About 23.7 per cent of Indian men were illiterate in 2006-07 whereas

almost 46.6 per cent of women were illiterate. Although India’s

literacy has improved over the past four decades, the proportion of

its illiterate population, over 15 years of age continues to be much

more than in most other developing countries (figure 4).

The working-age population will increase

the most in states that are the poorest and

offer the lowest employment opportunity.

Persistent drop-out rates and lack of teachers plague India’s education system

India’s school drop-out rate continues to be alarming. As on 2006-07,

only 17 of 100 children who entered 1st grade completed 10th grade

(figure 5). Drop-out rates have, however, marginally declined over the

past two decades.

One-fifth of India’s primary schools are single-teacher schools. India,

similar to sub-Sahara African countries, has a pupil-teacher ratio of

45, which lags behind most Asian countries. According to the Global

Education Digest 2010, China and Japan have a pupil-teacher ratio

of 18, whereas Indonesia and Malaysia have a pupil-teacher ratio of

17 and 15. India’s pupil-teacher ratio in primary schools has been

rising over a period of time, which is worrisome (figure 6). The lack

of a sufficient number of teachers has adversely affected the quality

of learning in India’s schools (figure 7).

Figure 5

Share of children dropping out of

schools

Figure 3

State-wise incremental working-

age population over

2011 to 2021

0 5 10 15 20 25

Himachal Pradesh

Uttarakhand

Jammu & Kashmir

Kerala

PunjabTamil Nadu

ChhattisgarhOrissa

HaryanaJharkhand

Karnataka

Andhra Pradesh

Gujarat

West Bengal

Rajasthan

Madhya PradeshMaharashtra

Bihar

Uttar Pradesh

million

Source: Population Projections, Census of India

0

25

50

75

100

1980-81 2006-07P 1980-81 2006-07P 1980-81 2006-07P

Primary Middle High

%Boys Girls

Source: Selected Socio-Economic Statistics, India, 2008

Figure 4

Share of population more than 15 years of

age, without schooling

0

14

28

42

56

70

1980 2010 1980 2010 1980 2010 1980 2010 1980 2010India China Malaysia Korea Thailand

%

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 7

6

Source: Barro-Lee Dataset 2010

Due to neglect of basic education, a large proportion of working-age people are not

equipped to compete in the job market.

India’s drop-out rates are declining, but not fast enough.

High pupil-teacher ratio impacts quality of

schooling.

(Grade I-IV) (Grade V-VII) (Grade VII-X)

Regional demographic diversity will be unfavourable

How good?

High levels of illiteracy

According to Census of India’s population projections, Uttar

Pradesh, Bihar, Madhya Pradesh and Rajasthan will account for more

than 50 per cent of the increase in India’s working age population

over 2011 to 2021. These states, also the poorest four states among

the 15 major states, based on per capita income (Net Domestic

Product), would add 54 million to India’s workforce, whereas the four

most affluent states - Haryana, Maharashtra, Punjab and Gujarat -

would together add only 21.6 million to the workforce (figure 3). The

maximum increase in working-age population will therefore take

place in states that are the poorest and offer the lowest employment

opportunity.

About 23.7 per cent of Indian men were illiterate in 2006-07 whereas

almost 46.6 per cent of women were illiterate. Although India’s

literacy has improved over the past four decades, the proportion of

its illiterate population, over 15 years of age continues to be much

more than in most other developing countries (figure 4).

The working-age population will increase

the most in states that are the poorest and

offer the lowest employment opportunity.

Persistent drop-out rates and lack of teachers plague India’s education system

India’s school drop-out rate continues to be alarming. As on 2006-07,

only 17 of 100 children who entered 1st grade completed 10th grade

(figure 5). Drop-out rates have, however, marginally declined over the

past two decades.

One-fifth of India’s primary schools are single-teacher schools. India,

similar to sub-Sahara African countries, has a pupil-teacher ratio of

45, which lags behind most Asian countries. According to the Global

Education Digest 2010, China and Japan have a pupil-teacher ratio

of 18, whereas Indonesia and Malaysia have a pupil-teacher ratio of

17 and 15. India’s pupil-teacher ratio in primary schools has been

rising over a period of time, which is worrisome (figure 6). The lack

of a sufficient number of teachers has adversely affected the quality

of learning in India’s schools (figure 7).

Figure 5

Share of children dropping out of

schools

Figure 3

State-wise incremental working-

age population over

2011 to 2021

0 5 10 15 20 25

Himachal Pradesh

Uttarakhand

Jammu & Kashmir

Kerala

PunjabTamil Nadu

ChhattisgarhOrissa

HaryanaJharkhand

Karnataka

Andhra Pradesh

Gujarat

West Bengal

Rajasthan

Madhya PradeshMaharashtra

Bihar

Uttar Pradesh

million

Source: Population Projections, Census of India

0

25

50

75

100

1980-81 2006-07P 1980-81 2006-07P 1980-81 2006-07P

Primary Middle High

%Boys Girls

Source: Selected Socio-Economic Statistics, India, 2008

Figure 4

Share of population more than 15 years of

age, without schooling

0

14

28

42

56

70

1980 2010 1980 2010 1980 2010 1980 2010 1980 2010India China Malaysia Korea Thailand

%

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 7

6

Source: Barro-Lee Dataset 2010

Due to neglect of basic education, a large proportion of working-age people are not

equipped to compete in the job market.

India’s drop-out rates are declining, but not fast enough.

High pupil-teacher ratio impacts quality of

schooling.

(Grade I-IV) (Grade V-VII) (Grade VII-X)

Lack of vocational training is a hurdle for India’s youth

In 2004-05, only 28 million of India’s 257 million job-seeking

population in the age group of 15-29 received any form of vocational

training. And, only 9 million of these 28 million received formal

vocational training from training institutes; the others acquired skills

informally from their preceding generation or other household

members (figure 8).

Mathematics

Language

Environmental studies/Science

20

45

70

Class V Class VII

Figure 7

Percentage of

students with

learning achievement

4.39.5

86.2

3.0 5.9

91.1

Formally skilled

Non-formallyskilled

Unskilled Formallyskilled

Non-formallySkilled

Unskilled

%Figure 8

Percentage of youth population

with vocational training

Inadequate education and skills make a large proportion of educated youth unemployable

Looking ahead…

As on 2004-05, only 78 million of the 257 million youth were

qualified in the secondary level - 10th grade or above. Only 23 per

cent of these qualified youth held at least a diploma or a graduate

degree. Even within this minority of graduate youth, a large

proportion remained unemployed (figure 9).

During the economic upturn in the past decade, unemployment was

the highest for diploma and certificate holders, followed closely by

graduates and postgraduates. More than 30 per cent of India’s

engineering postgraduate diploma holders were unemployed (figure

9). This implies that, despite sufficient educational qualification, the

workforce does not have skills that are required by the job market.

Although India will have the world’s largest pool of working-age

people by 2030, if the current trend in labour participation continues,

only 539 million out of 962 million people of working age would be

working by 2030. In the absence of any significant reforms in school

and higher education, the quality of India’s labour force would

remain below par.

CRISIL Research’s study on India’s education services industry,

August 2010, points out, rather disturbingly, that although engineer

turnout from India’s institutes will almost double over 2011 to 2015 -

from 0.37 million to 0.65 million engineers, their employability will

diminish further. As a result, most industries, including IT services,

will face a talent bottleneck.

21.4 22.625.7

19.715.9

25.7

36.5

30.2

Agri Engg/Tech Medicine Agri Engg/Tech MedicineTechnicaldegree

Diploma - Undergraduate Diploma - Graduate and above

Total - Educated

youth

Figure 9

Unemployment rates among

educated youth

Lack of vocational training diminishes employability.

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 9

8

Primary

Middle

Secondary

25

30

35

40

45

50

1980-81 1990-91 2000-01 2006-07P

nos

Source: Selected Socio-Economic Statistics, India, 2008

Figure 6

P upils per teacher

Source: Selected Socio-Economic Statistics, India, 2008

stSource: National Sample Survey Organisation, 61 Round, 2004-05

stSource: National Sample Survey Organisation, 61 Round, 2004-05

%

Only a minority of Indian youth receive education up to degree or diploma level and

a significant proportion of these youth are

unemployed. An employable individual is one who has the necessary skill sets to

undertake a job, requiring minimal additional training.

FemaleMale

%

Poor quality of schooling affects skill competency of India’s labour force.

Lack of vocational training is a hurdle for India’s youth

In 2004-05, only 28 million of India’s 257 million job-seeking

population in the age group of 15-29 received any form of vocational

training. And, only 9 million of these 28 million received formal

vocational training from training institutes; the others acquired skills

informally from their preceding generation or other household

members (figure 8).

Mathematics

Language

Environmental studies/Science

20

45

70

Class V Class VII

Figure 7

Percentage of

students with

learning achievement

4.39.5

86.2

3.0 5.9

91.1

Formally skilled

Non-formallyskilled

Unskilled Formallyskilled

Non-formallySkilled

Unskilled

%Figure 8

Percentage of youth population

with vocational training

Inadequate education and skills make a large proportion of educated youth unemployable

Looking ahead…

As on 2004-05, only 78 million of the 257 million youth were

qualified in the secondary level - 10th grade or above. Only 23 per

cent of these qualified youth held at least a diploma or a graduate

degree. Even within this minority of graduate youth, a large

proportion remained unemployed (figure 9).

During the economic upturn in the past decade, unemployment was

the highest for diploma and certificate holders, followed closely by

graduates and postgraduates. More than 30 per cent of India’s

engineering postgraduate diploma holders were unemployed (figure

9). This implies that, despite sufficient educational qualification, the

workforce does not have skills that are required by the job market.

Although India will have the world’s largest pool of working-age

people by 2030, if the current trend in labour participation continues,

only 539 million out of 962 million people of working age would be

working by 2030. In the absence of any significant reforms in school

and higher education, the quality of India’s labour force would

remain below par.

CRISIL Research’s study on India’s education services industry,

August 2010, points out, rather disturbingly, that although engineer

turnout from India’s institutes will almost double over 2011 to 2015 -

from 0.37 million to 0.65 million engineers, their employability will

diminish further. As a result, most industries, including IT services,

will face a talent bottleneck.

21.4 22.625.7

19.715.9

25.7

36.5

30.2

Agri Engg/Tech Medicine Agri Engg/Tech MedicineTechnicaldegree

Diploma - Undergraduate Diploma - Graduate and above

Total - Educated

youth

Figure 9

Unemployment rates among

educated youth

Lack of vocational training diminishes employability.

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 9

8

Primary

Middle

Secondary

25

30

35

40

45

50

1980-81 1990-91 2000-01 2006-07P

nos

Source: Selected Socio-Economic Statistics, India, 2008

Figure 6

P upils per teacher

Source: Selected Socio-Economic Statistics, India, 2008

stSource: National Sample Survey Organisation, 61 Round, 2004-05

stSource: National Sample Survey Organisation, 61 Round, 2004-05

%

Only a minority of Indian youth receive education up to degree or diploma level and

a significant proportion of these youth are

unemployed. An employable individual is one who has the necessary skill sets to

undertake a job, requiring minimal additional training.

FemaleMale

%

Poor quality of schooling affects skill competency of India’s labour force.

India’s labour demand

Economic cycles create mismatch between labour demand and

supply

India’s unconventional economic development has led to excess

employment in agriculture

During an economic upturn, when demand in an economy rapidly

grows, demand for labour exceeds the supply of employable

workforce. The reverse of this happens during a downturn. The

consequent mismatch between labour demand and supply is normal,

and not a cause of concern.

When an economy is in the initial stages of development, the share

of the agriculture sector tends to be high. Then, the share of industry

increases, and eventually, services account for a dominant share of

the GDP. In this pattern of economic development, labour is

transferred from agriculture to industry and finally to services. India’s

pattern of economic development has, however, been quite

unconventional.

The share of agriculture in India’s GDP came down sharply from 30

per cent in 1993-94 to 18.9 per cent in 2004-05 (figure 10).

Agriculture’s contribution to total employment, however, reduced

narrowly from 62.3 per cent to 56.1 per cent. In contrast, the share of

industry and services in GDP together rose by just over 11

percentage points to 81.1 per cent whereas the share of employment

in these sectors grew only by 6 percentage points. Thus, more than

half of India’s total employed population remains occupied in

agriculture even though the sector currently contributes less than 20

per cent to GDP.

Neither has industry expanded fast enough nor has it been able to absorb labour to its

fullest potential, owing partly to India's rigid labour laws that discourage employment by

the organised sector.

Policy barriers curtail labour demand in industry

Unanticipated growth in services increases demand for skilled

labour

Looking ahead…

In 2004-05, industry contributed 28 per cent to GDP and employed

19 per cent of India’s workforce Even as far back as 1983-84,

industry’s share in GDP and employment was about 24 and 14 per

cent. India’s restrictive labour laws are partly responsible for

discouraging growth in industry and employment. For instance,

labour laws restrict units that employ more than 100 workers from

firing employees.

The restrictive labour laws impact employment in three ways - i)

entrepreneurs get discouraged from entering the industrial sector; ii)

industry tries to substitute labour with capital, thereby reducing the

employment intensity of industrial production, an undesirable

outcome in a labour-surplus economy; iii) smaller-than-optimal-size

firms proliferate in the formal sector as industry tries to go around

labour laws by outsourcing work to the informal sector. It is therefore

of little surprise that despite an accelerated GDP growth,

employment by the organised sector has decreased during the past

few years.

The expansion of service industries such as IT/ITeS and financial

services over the past decade created a major discontinuity in India’s

pattern of economic development. A sudden and sharp rise in labour

demand in these industries sparked a scarcity of skilled manpower,

and pushed up wages of skilled manpower beyond the growth in

their productivity. Employment in the IT/ITeS export industry alone

increased from 0.38 million in 2002-03 to 1.77 million in 2009-10.

If the current pattern of employment distribution across agriculture,

industry and services continues, employment in services would rise

from 135.5 million in 2010 to around 177.4 million in 2030, whereas

labour demand in the industrial sector would only increase from 91

million to 119 million over the period.

Owing to advances in technology and

differences in regulations, the high-skilled

services sector has expanded rapidly relative to industry, creating a demand for a specific

type of skill-set, which, in turn, has resulted in skill mismatch.

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 11

10

Economic cycles and India's development

pattern, which is governed by economic policies, determine the nature of India's

labour demand.

%

30.0

62.3

18.9

56.1

25.2

15.4

28.0

18.8

44.8

22.4

53.1

25.1

1993-94 2004-05 1993-94 2004-05 1993-94 2004-05

Agriculture Industry Services

GDP EmploymentFigure 10

Share of major sectors in GDP and

employment

Source: Central Statistical Organisation, National Sample Survey Organisation

A disproportionately large share of

population continues to depend on

agriculture for employment.

India’s labour demand

Economic cycles create mismatch between labour demand and

supply

India’s unconventional economic development has led to excess

employment in agriculture

During an economic upturn, when demand in an economy rapidly

grows, demand for labour exceeds the supply of employable

workforce. The reverse of this happens during a downturn. The

consequent mismatch between labour demand and supply is normal,

and not a cause of concern.

When an economy is in the initial stages of development, the share

of the agriculture sector tends to be high. Then, the share of industry

increases, and eventually, services account for a dominant share of

the GDP. In this pattern of economic development, labour is

transferred from agriculture to industry and finally to services. India’s

pattern of economic development has, however, been quite

unconventional.

The share of agriculture in India’s GDP came down sharply from 30

per cent in 1993-94 to 18.9 per cent in 2004-05 (figure 10).

Agriculture’s contribution to total employment, however, reduced

narrowly from 62.3 per cent to 56.1 per cent. In contrast, the share of

industry and services in GDP together rose by just over 11

percentage points to 81.1 per cent whereas the share of employment

in these sectors grew only by 6 percentage points. Thus, more than

half of India’s total employed population remains occupied in

agriculture even though the sector currently contributes less than 20

per cent to GDP.

Neither has industry expanded fast enough nor has it been able to absorb labour to its

fullest potential, owing partly to India's rigid labour laws that discourage employment by

the organised sector.

Policy barriers curtail labour demand in industry

Unanticipated growth in services increases demand for skilled

labour

Looking ahead…

In 2004-05, industry contributed 28 per cent to GDP and employed

19 per cent of India’s workforce Even as far back as 1983-84,

industry’s share in GDP and employment was about 24 and 14 per

cent. India’s restrictive labour laws are partly responsible for

discouraging growth in industry and employment. For instance,

labour laws restrict units that employ more than 100 workers from

firing employees.

The restrictive labour laws impact employment in three ways - i)

entrepreneurs get discouraged from entering the industrial sector; ii)

industry tries to substitute labour with capital, thereby reducing the

employment intensity of industrial production, an undesirable

outcome in a labour-surplus economy; iii) smaller-than-optimal-size

firms proliferate in the formal sector as industry tries to go around

labour laws by outsourcing work to the informal sector. It is therefore

of little surprise that despite an accelerated GDP growth,

employment by the organised sector has decreased during the past

few years.

The expansion of service industries such as IT/ITeS and financial

services over the past decade created a major discontinuity in India’s

pattern of economic development. A sudden and sharp rise in labour

demand in these industries sparked a scarcity of skilled manpower,

and pushed up wages of skilled manpower beyond the growth in

their productivity. Employment in the IT/ITeS export industry alone

increased from 0.38 million in 2002-03 to 1.77 million in 2009-10.

If the current pattern of employment distribution across agriculture,

industry and services continues, employment in services would rise

from 135.5 million in 2010 to around 177.4 million in 2030, whereas

labour demand in the industrial sector would only increase from 91

million to 119 million over the period.

Owing to advances in technology and

differences in regulations, the high-skilled

services sector has expanded rapidly relative to industry, creating a demand for a specific

type of skill-set, which, in turn, has resulted in skill mismatch.

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 11

10

Economic cycles and India's development

pattern, which is governed by economic policies, determine the nature of India's

labour demand.

%

30.0

62.3

18.9

56.1

25.2

15.4

28.0

18.8

44.8

22.4

53.1

25.1

1993-94 2004-05 1993-94 2004-05 1993-94 2004-05

Agriculture Industry Services

GDP EmploymentFigure 10

Share of major sectors in GDP and

employment

Source: Central Statistical Organisation, National Sample Survey Organisation

A disproportionately large share of

population continues to depend on

agriculture for employment.

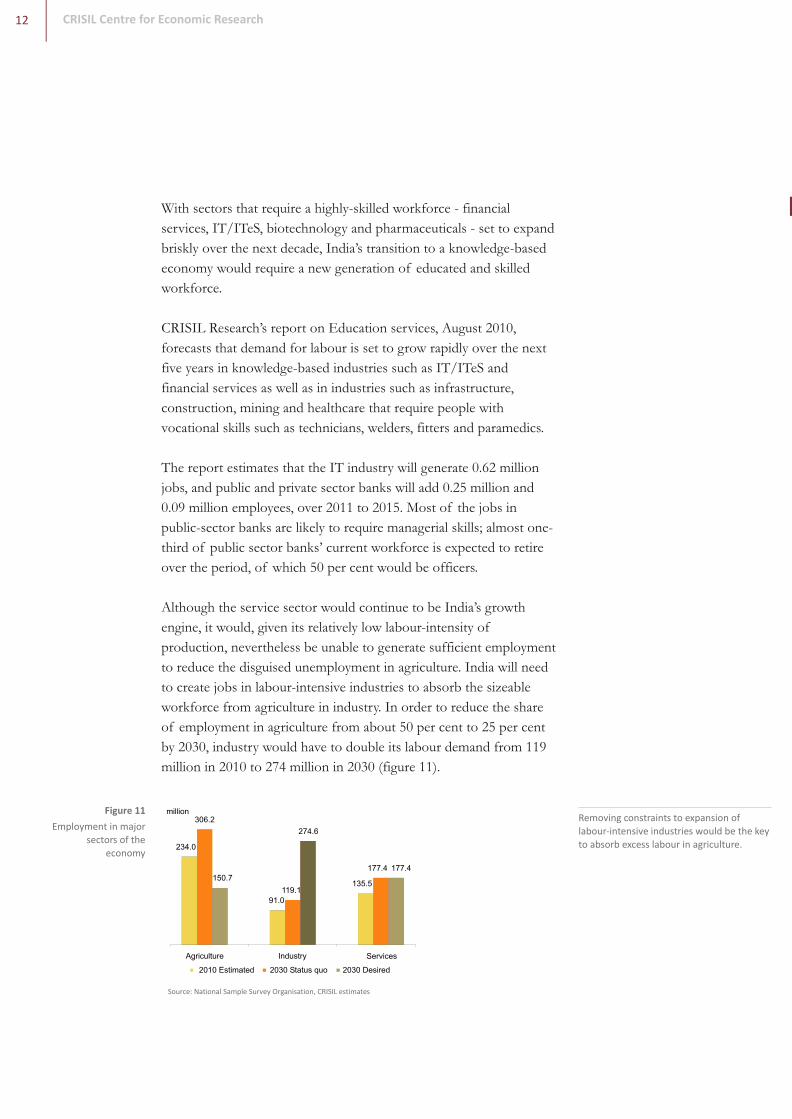

With sectors that require a highly-skilled workforce - financial

services, IT/ITeS, biotechnology and pharmaceuticals - set to expand

briskly over the next decade, India’s transition to a knowledge-based

economy would require a new generation of educated and skilled

workforce.

CRISIL Research’s report on Education services, August 2010,

forecasts that demand for labour is set to grow rapidly over the next

five years in knowledge-based industries such as IT/ITeS and

financial services as well as in industries such as infrastructure,

construction, mining and healthcare that require people with

vocational skills such as technicians, welders, fitters and paramedics.

The report estimates that the IT industry will generate 0.62 million

jobs, and public and private sector banks will add 0.25 million and

0.09 million employees, over 2011 to 2015. Most of the jobs in

public-sector banks are likely to require managerial skills; almost one-

third of public sector banks’ current workforce is expected to retire

over the period, of which 50 per cent would be officers.

Although the service sector would continue to be India’s growth

engine, it would, given its relatively low labour-intensity of

production, nevertheless be unable to generate sufficient employment

to reduce the disguised unemployment in agriculture. India will need

to create jobs in labour-intensive industries to absorb the sizeable

workforce from agriculture in industry. In order to reduce the share

of employment in agriculture from about 50 per cent to 25 per cent

by 2030, industry would have to double its labour demand from 119

million in 2010 to 274 million in 2030 (figure 11).

The outcome

The challenge of skill mismatch

The potential trends in labour supply and demand indicate the nature

of imbalances in the labour market. The imbalances are likely to have

the following effects on the labour market.

The mismatch in India’s workforce demand and supply is as much in

jobs that require basic vocational skills like welding, plumbing and

paramedics as it is in jobs that require well-qualified manpower.

If the current trends in the nature of labour demand and supply

continue, skill mismatch would continue to plague the Indian labour

market. The mismatch would continue to stem from skill shortages,

where there are not enough people with a specific type of skill to

meet demand. For example, even at present, knowledge-based

industries such as IT/ITeS have trouble recruiting the kind of

information technology specialists they need. A new generation of

educated and skilled people, who are in short supply, will be required

to spearhead India’s transition to a knowledge-based economy.

Consequently, wages and attrition rates would continue to rise in

industries that face the skill mismatch.

At the same time, a vast number of qualified workers, who are a

correct fit, on paper, for knowledge-based jobs, would continue to

remain unemployed. This suggests that skill shortage relates, in part,

to a scarcity of people with the required skills, experience and quality

of education.

Skill shortage would also persist in jobs requiring vocational skills.

Opportunities in infrastructure, construction, mining and healthcare

have increased the demand for vocationally-trained workers. As

formal vocational training has not been widespread, skilled workers

to meet the rising demand from these sectors are likely to remain in

short supply.

Agriculture Industry Services

234.0

150.7

306.2

91.0

119.1

274.6

135.5

177.4 177.4

million

2010 Estimated 2030 Status quo 2030 Desired

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 13

12

Source: National Sample Survey Organisation, CRISIL estimates

Figure 11

Employment in major

sectors of the economy

Skill shortage in knowledge-based jobs relates, in part, to a scarcity of people with

the required skills, experience and quality of education.

Removing constraints to expansion of labour-intensive industries would be the key to absorb excess labour in agriculture.

With sectors that require a highly-skilled workforce - financial

services, IT/ITeS, biotechnology and pharmaceuticals - set to expand

briskly over the next decade, India’s transition to a knowledge-based

economy would require a new generation of educated and skilled

workforce.

CRISIL Research’s report on Education services, August 2010,

forecasts that demand for labour is set to grow rapidly over the next

five years in knowledge-based industries such as IT/ITeS and

financial services as well as in industries such as infrastructure,

construction, mining and healthcare that require people with

vocational skills such as technicians, welders, fitters and paramedics.

The report estimates that the IT industry will generate 0.62 million

jobs, and public and private sector banks will add 0.25 million and

0.09 million employees, over 2011 to 2015. Most of the jobs in

public-sector banks are likely to require managerial skills; almost one-

third of public sector banks’ current workforce is expected to retire

over the period, of which 50 per cent would be officers.

Although the service sector would continue to be India’s growth

engine, it would, given its relatively low labour-intensity of

production, nevertheless be unable to generate sufficient employment

to reduce the disguised unemployment in agriculture. India will need

to create jobs in labour-intensive industries to absorb the sizeable

workforce from agriculture in industry. In order to reduce the share

of employment in agriculture from about 50 per cent to 25 per cent

by 2030, industry would have to double its labour demand from 119

million in 2010 to 274 million in 2030 (figure 11).

The outcome

The challenge of skill mismatch

The potential trends in labour supply and demand indicate the nature

of imbalances in the labour market. The imbalances are likely to have

the following effects on the labour market.

The mismatch in India’s workforce demand and supply is as much in

jobs that require basic vocational skills like welding, plumbing and

paramedics as it is in jobs that require well-qualified manpower.

If the current trends in the nature of labour demand and supply

continue, skill mismatch would continue to plague the Indian labour

market. The mismatch would continue to stem from skill shortages,

where there are not enough people with a specific type of skill to

meet demand. For example, even at present, knowledge-based

industries such as IT/ITeS have trouble recruiting the kind of

information technology specialists they need. A new generation of

educated and skilled people, who are in short supply, will be required

to spearhead India’s transition to a knowledge-based economy.

Consequently, wages and attrition rates would continue to rise in

industries that face the skill mismatch.

At the same time, a vast number of qualified workers, who are a

correct fit, on paper, for knowledge-based jobs, would continue to

remain unemployed. This suggests that skill shortage relates, in part,

to a scarcity of people with the required skills, experience and quality

of education.

Skill shortage would also persist in jobs requiring vocational skills.

Opportunities in infrastructure, construction, mining and healthcare

have increased the demand for vocationally-trained workers. As

formal vocational training has not been widespread, skilled workers

to meet the rising demand from these sectors are likely to remain in

short supply.

Agriculture Industry Services

234.0

150.7

306.2

91.0

119.1

274.6

135.5

177.4 177.4

million

2010 Estimated 2030 Status quo 2030 Desired

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 13

12

Source: National Sample Survey Organisation, CRISIL estimates

Figure 11

Employment in major

sectors of the economy

Skill shortage in knowledge-based jobs relates, in part, to a scarcity of people with

the required skills, experience and quality of education.

Removing constraints to expansion of labour-intensive industries would be the key to absorb excess labour in agriculture.

Shortage of high-skill labour can constrain productivity and

economic growth

Skill shortage could raise inequality and inflation

If India is to achieve and sustain double-digit economic growth in the

near future, the key would be to raise the supply potential of the

economy. The number of hours of work and the productivity of

workforce, measured as output per unit of workforce, affect the

supply of goods and services. Keeping the number of working hours

unchanged, India will need to increase employment or productivity to

maintain its current growth rate. Growth in labour productivity

would be especially critical in high-end service sectors.

Three factors determine growth in labour productivity - more capital

per unit of workforce, advances in technology, and quality of

workforce. Notwithstanding a rise in investment rate and advances in

technology, India is likely to fall short of skilled workers, which

would adversely affect the rate at which its labour productivity rises.

As the demand for skilled workers increases, if relatively low-quality

workers are added to the workforce, they would drag down overall

workforce quality and impact productivity growth. Further, skilled

workers would have to put in longer hours for sustaining the current

growth rate, which, in turn, would adversely affect their productivity.

Thus, given its shortage of skilled workers, the growth in productivity

of India’s workforce could slow down in future.

The bargaining power of companies with their skilled employees is

severely restricted during phases of skill shortage. Wages hence

increase at a greater rate than productivity growth. Excessive wage

growth for a section of population would impact income inequality

and inflation. Also, if shortages in skills are significant, companies

would avoid investing in new technologies which may require a

specific type of skilled labour. The companies would thus produce

relatively less-differentiated and lower-quality products.

Disguised employment will continue in agriculture

Fiscal burden of a young and unemployed population

A large army of undereducated, unskilled and hence unemployable

labour is unable to meaningfully plug into the fast-growing service

sector. Without deliberate policy efforts to expand the labour-

intensive industrial sector, a majority of India’s workforce would

remain trapped in the agricultural sector.

The fiscal burden of an ageing population is a phenomenon that will

plague Western economies in the coming years. As their working-age

population shrinks and their ageing population expands, the Western

governments would have to spend more on social security, health

care and welfare programmes.

Although India, in contrast, has a relatively younger population, the

youth-dominated population will yield an economic dividend only if

it finds gainful employment. If it does not, the economy will be

fraught with social tensions and instability.

India is currently addressing the issue of unemployment through

social security schemes such as Mahatma Gandhi NREGA (National

Rural Employment Guarantee Act), which is at best a ‘stop-gap’

solution. If the Indian economy is unable to generate employment

for its swelling working-age population over the next decade, the

government will need to transfer more funds through social security

schemes to provide income to the unemployed and underemployed.

The likely increased transfers to employment-generating schemes

would create a permanent fiscal burden and crowd out expenditures

on education, healthcare and infrastructure.

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 15

14

Given its shortage of skilled workers, the

growth in productivity of India’s workforce

could slow down in future.

India’s likely increased transfers to

employment-generating schemes would create a permanent fiscal burden and crowd

out expenditures on education, healthcare and infrastructure.

Shortage of high-skill labour can constrain productivity and

economic growth

Skill shortage could raise inequality and inflation

If India is to achieve and sustain double-digit economic growth in the

near future, the key would be to raise the supply potential of the

economy. The number of hours of work and the productivity of

workforce, measured as output per unit of workforce, affect the

supply of goods and services. Keeping the number of working hours

unchanged, India will need to increase employment or productivity to

maintain its current growth rate. Growth in labour productivity

would be especially critical in high-end service sectors.

Three factors determine growth in labour productivity - more capital

per unit of workforce, advances in technology, and quality of

workforce. Notwithstanding a rise in investment rate and advances in

technology, India is likely to fall short of skilled workers, which

would adversely affect the rate at which its labour productivity rises.

As the demand for skilled workers increases, if relatively low-quality

workers are added to the workforce, they would drag down overall

workforce quality and impact productivity growth. Further, skilled

workers would have to put in longer hours for sustaining the current

growth rate, which, in turn, would adversely affect their productivity.

Thus, given its shortage of skilled workers, the growth in productivity

of India’s workforce could slow down in future.

The bargaining power of companies with their skilled employees is

severely restricted during phases of skill shortage. Wages hence

increase at a greater rate than productivity growth. Excessive wage

growth for a section of population would impact income inequality

and inflation. Also, if shortages in skills are significant, companies

would avoid investing in new technologies which may require a

specific type of skilled labour. The companies would thus produce

relatively less-differentiated and lower-quality products.

Disguised employment will continue in agriculture

Fiscal burden of a young and unemployed population

A large army of undereducated, unskilled and hence unemployable

labour is unable to meaningfully plug into the fast-growing service

sector. Without deliberate policy efforts to expand the labour-

intensive industrial sector, a majority of India’s workforce would

remain trapped in the agricultural sector.

The fiscal burden of an ageing population is a phenomenon that will

plague Western economies in the coming years. As their working-age

population shrinks and their ageing population expands, the Western

governments would have to spend more on social security, health

care and welfare programmes.

Although India, in contrast, has a relatively younger population, the

youth-dominated population will yield an economic dividend only if

it finds gainful employment. If it does not, the economy will be

fraught with social tensions and instability.

India is currently addressing the issue of unemployment through

social security schemes such as Mahatma Gandhi NREGA (National

Rural Employment Guarantee Act), which is at best a ‘stop-gap’

solution. If the Indian economy is unable to generate employment

for its swelling working-age population over the next decade, the

government will need to transfer more funds through social security

schemes to provide income to the unemployed and underemployed.

The likely increased transfers to employment-generating schemes

would create a permanent fiscal burden and crowd out expenditures

on education, healthcare and infrastructure.

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 15

14

Given its shortage of skilled workers, the

growth in productivity of India’s workforce

could slow down in future.

India’s likely increased transfers to

employment-generating schemes would create a permanent fiscal burden and crowd

out expenditures on education, healthcare and infrastructure.

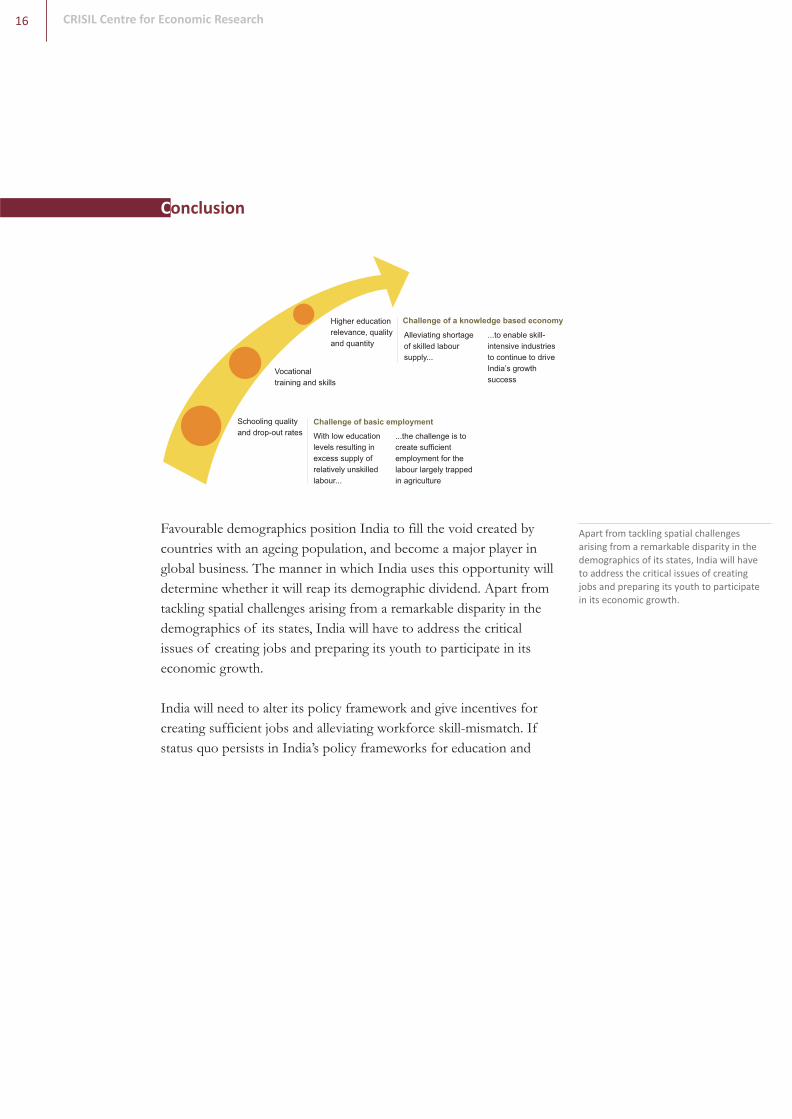

Conclusion

Favourable demographics position India to fill the void created by

countries with an ageing population, and become a major player in

global business. The manner in which India uses this opportunity will

determine whether it will reap its demographic dividend. Apart from

tackling spatial challenges arising from a remarkable disparity in the

demographics of its states, India will have to address the critical

issues of creating jobs and preparing its youth to participate in its

economic growth.

India will need to alter its policy framework and give incentives for

creating sufficient jobs and alleviating workforce skill-mismatch. If

status quo persists in India’s policy frameworks for education and

training, and workforce management, economic growth will soon hit

a speed breaker. If labour and industrial policies are not reformed,

people with different education and skill levels, or from different

states, would have unequal economic prospects. India’s industrial

sector may not be able to scale up to absorb the excess workforce in

agriculture. This could, in turn, block efforts to reduce income

inequality in India.

In addition to government initiatives, corporate investment in

employee education and training would continue to play a critical role

to meet the rising demand for high-skilled workers. A number of

Indian corporates, especially from IT/ITeS, already provide focused

training to improve their people’s skills. Also, some corporates, like

CRISIL, have a study-work programme that equips a graduate with

analytical and financial skills, and then absorb the trained candidate in

their operations.

Although an increased rate of savings and investment, which India

has achieved and sustained since the early 2000s, is essential for

ensuring a rapid pace of economic growth, an educated workforce

and job opportunities are critical for sustaining the growth over a

long period, and for realising the demographic dividend. This would

be especially true for India since it depends more on its human

capital than its peer countries that are at a similar level of economic

development.

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 17

16

Challenge of a knowledge based economy

Alleviating shortage

of skilled labour

supply...

...to enable skill-

intensive industries

to continue to drive

India’s growth

success

Higher education

relevance, quality

and quantity

Vocational

training and skills

Schooling quality

and drop-out rates ...the challenge is to

create sufficient

employment for the

labour largely trapped

in agriculture

With low education

levels resulting in

excess supply of

relatively unskilled

labour...

Challenge of basic employment

Apart from tackling spatial challenges arising from a remarkable disparity in the

demographics of its states, India will have to address the critical issues of creating jobs and preparing its youth to participate

in its economic growth.

In addition to government initiatives,

corporate investment in employee education and training would continue to

play a critical role to meet the rising

demand for high-skilled workers.

Conclusion

Favourable demographics position India to fill the void created by

countries with an ageing population, and become a major player in

global business. The manner in which India uses this opportunity will

determine whether it will reap its demographic dividend. Apart from

tackling spatial challenges arising from a remarkable disparity in the

demographics of its states, India will have to address the critical

issues of creating jobs and preparing its youth to participate in its

economic growth.

India will need to alter its policy framework and give incentives for

creating sufficient jobs and alleviating workforce skill-mismatch. If

status quo persists in India’s policy frameworks for education and

training, and workforce management, economic growth will soon hit

a speed breaker. If labour and industrial policies are not reformed,

people with different education and skill levels, or from different

states, would have unequal economic prospects. India’s industrial

sector may not be able to scale up to absorb the excess workforce in

agriculture. This could, in turn, block efforts to reduce income

inequality in India.

In addition to government initiatives, corporate investment in

employee education and training would continue to play a critical role

to meet the rising demand for high-skilled workers. A number of

Indian corporates, especially from IT/ITeS, already provide focused

training to improve their people’s skills. Also, some corporates, like

CRISIL, have a study-work programme that equips a graduate with

analytical and financial skills, and then absorb the trained candidate in

their operations.

Although an increased rate of savings and investment, which India

has achieved and sustained since the early 2000s, is essential for

ensuring a rapid pace of economic growth, an educated workforce

and job opportunities are critical for sustaining the growth over a

long period, and for realising the demographic dividend. This would

be especially true for India since it depends more on its human

capital than its peer countries that are at a similar level of economic

development.

CRISIL Centre for Economic Research

CRISIL, Skilling India: The Billion People Challenge, November 2010 17

16

Challenge of a knowledge based economy

Alleviating shortage

of skilled labour

supply...

...to enable skill-

intensive industries

to continue to drive

India’s growth

success

Higher education

relevance, quality

and quantity

Vocational

training and skills

Schooling quality

and drop-out rates ...the challenge is to

create sufficient

employment for the

labour largely trapped

in agriculture

With low education

levels resulting in

excess supply of

relatively unskilled

labour...

Challenge of basic employment

Apart from tackling spatial challenges arising from a remarkable disparity in the

demographics of its states, India will have to address the critical issues of creating jobs and preparing its youth to participate

in its economic growth.

In addition to government initiatives,

corporate investment in employee education and training would continue to

play a critical role to meet the rising

demand for high-skilled workers.

Dharmakirti Joshi Chief EconomistSunil K. Sinha Senior EconomistVidya Mahambare Senior EconomistPoonam Munjal EconomistParul Bhardwaj EconomistDipti Saletore Economist

CRISIL Centre for Economic Research (C-CER)

l Macroeconomics:

l Financial Economics:

l Public Finance:

l Environmental Economics:

“CRISIL EcoView”

The Centre for Economic Research is a division of CRISIL. Set up in April 2002,

C-CER reflects CRISIL’s commitment to provide an integrated research offering

to help corporates and policy makers take more informed business decisions.

C-CER applies sound economic principles to real world applications, creating

conceptual and contextual linkages that are unique to CRISIL. C-CER also

supports Standard & Poor’s Asia Pacific by analysing and forecasting

macroeconomic variables for 14 countries in the region.

C-CER’s core strengths emerge from a strong understanding of and capabilities

in the following areas:

Regular monitoring and forecasting of macroeconomic

indicators, assessment of domestic and global events, and analysis of long-

term structural changes in the economy.

Analysis and forecasting of interest rates and

exchange rates.

Analysis and forecasting of central and state government

revenues, expenditures and borrowing requirements.

Analysis of Indian firms’ impact on

environmental, social and governance parameters.

C-CER reviews developments in the Indian economy on a monthly basis and

provides its outlook on the economy through a dedicated publication

. CRISIL EcoView is used by CEOs, CFOs, economists,

corporate strategy teams, marketing teams, treasuries and knowledge

management teams of various corporates and management consultancy firms to

make appropriate strategy level decisions.

The C-CER team comprises senior economists with over a decade’s experience

of working with premier research institutes.

Dharmakirti Joshi Chief EconomistSunil K. Sinha Senior EconomistVidya Mahambare Senior EconomistPoonam Munjal EconomistParul Bhardwaj EconomistDipti Saletore Economist

CRISIL Centre for Economic Research (C-CER)

l Macroeconomics:

l Financial Economics:

l Public Finance:

l Environmental Economics:

“CRISIL EcoView”

The Centre for Economic Research is a division of CRISIL. Set up in April 2002,

C-CER reflects CRISIL’s commitment to provide an integrated research offering

to help corporates and policy makers take more informed business decisions.

C-CER applies sound economic principles to real world applications, creating

conceptual and contextual linkages that are unique to CRISIL. C-CER also

supports Standard & Poor’s Asia Pacific by analysing and forecasting

macroeconomic variables for 14 countries in the region.

C-CER’s core strengths emerge from a strong understanding of and capabilities

in the following areas:

Regular monitoring and forecasting of macroeconomic

indicators, assessment of domestic and global events, and analysis of long-

term structural changes in the economy.

Analysis and forecasting of interest rates and

exchange rates.

Analysis and forecasting of central and state government

revenues, expenditures and borrowing requirements.

Analysis of Indian firms’ impact on

environmental, social and governance parameters.

C-CER reviews developments in the Indian economy on a monthly basis and

provides its outlook on the economy through a dedicated publication

. CRISIL EcoView is used by CEOs, CFOs, economists,

corporate strategy teams, marketing teams, treasuries and knowledge

management teams of various corporates and management consultancy firms to

make appropriate strategy level decisions.

The C-CER team comprises senior economists with over a decade’s experience

of working with premier research institutes.

www.crisil.com

Head office

Regional offices in India

CRISIL House Central Avenue, Hiranandani Business Park Powai, Mumbai - 400 076Phone : 91-22-3342 3000 Fax : 91-22-3342 3001

AhmedabadUnit No.706, 7th Floor,Venus Atlantis, Near Reliance Petrol Pump,Prahladnagar, Ahmedabad 380 015. Phone: 91-79-4024 4500Fax: 91-79-2755 9863

BengaluruW-101, Sunrise Chambers, 22, Ulsoor Road, Bengaluru - 560 042Phone: 91 (80) 2558 0899, 2559 4802 Fax: 91 (80) 2559 4801

ChennaiThapar House, 43/44, Montieth Road, Egmore, Chennai - 600 008Phone: 91-44-2854 6205 - 06, 2854 6093Fax: 91-44-2854 7531

New DelhiThe Mira, G-1, 1st Floor, Plot No. 1 & 2Ishwar Nagar, Mathura Road,New Delhi - 110 065, India Phone: +91 (11) 4250 5100, 2693 0117-121Fax: +91 (11) 2684 2212/ 13

Hyderabad3rd Floor, Uma ChambersPlot No. 9&10, Nagarjuna Hills,(Near Punjagutta Cross Road) Hyderabad - 500 482Phone: 91-40-2335 8103 - 05Fax: 91-40-2335 7507

KolkataHorizon, Block 'B', 4th Floor57 Chowringhee RoadKolkata - 700 071Phone: 91-33-2289 1949-50, 5529 4501Fax: 91-33-2283 0597 Pune1187/17, Ghole Road,Shivaji Nagar, Pune - 411 005Phone: 91-20-2553 9064 - 67 Fax: 91-20-4018 1930

CRISIL Privacy Notice

Contacting us via e-mail or registering with CRISIL reveals your e-mail address and any other information you include

such as phone number and/or mailing address. We will use this information to help us process your registration, fulfill

your request or respond to your inquiry. All of your personal information will be stored in a secure database in India.

Access to this database is limited to authorized persons.

Occasionally, we use data collected about customers and prospects to inform them about products or services from

CRISIL, and our parent company Standard & Poor’s (a subsidiary of The McGraw-Hill Companies), and reputable

outside companies that may be of interest to them. Many of our customers find these e-mail promotions valuable,

whether they are shopping for merchandise, taking advantage of a special offer, or purchasing unique services. On

rare occasions, and subject to applicable laws, CRISIL may also share your information with outside “3rd Party”

vendors who will be authorized to use this information solely to perform services (such as a “mailing” house) on our

behalf.

If at any time you would like your name removed from lists that are shared for promotional reasons within CRISIL,

Standard & Poor’s, and with other units of The McGraw-Hill Companies, or with third parties simply send a written

request to [email protected] or Privacy Official, 5th floor, CRISIL House, Central Avenue Road, Hiranandani

Business Park, Powai, Mumbai - 400 076, India.

You can also send a written request to [email protected] if you would like to confirm the accuracy of the information

we have collected from you, or if you have questions about the uses of this information.

For more information about The McGraw-Hill Companies Privacy Policy, please visit www.mcgrawhill.com/privacy.html.

Last updated: 1 January, 2010

DisclaimerThe Centre for Economic Research, CRISIL (C-CER), a division of CRISIL Limited has taken due care in preparing this

Report. Information has been obtained by C-CER from sources it considers reliable. However, CCER does not

guarantee the accuracy, adequacy or completeness of any information and is not responsible for any errors or

omissions or for the results obtained from the use of such information. CRISIL Limited especially states that it has no

financial liability whatsoever to the subscribers/ users/ transmitters/ distributors of this Report. C-CER operates

independently of and does not have access to information obtained by CRISIL’s Ratings Division, which may in its

regular operations obtain information of a confidential nature and is not available to C-CER. No part of this Report may

be published/ reproduced in any form without CRISIL’s prior written approval.

© 2010 - CRISIL - All rights reserved.

About CRISIL Limited

CRISIL is India’s leading Ratings, Research, Risk and Policy Advisory company.

CRISIL offers domestic and international customers a unique combination of local insights and global perspectives, delivering independent information, opinions and solutions that help them make better informed business and investment decisions, improve the efficiency of markets and market participants, and help shape infrastructure policy and projects. Its integrated range of capabilities includes credit ratings and risk assessment; research on India’s economy, industries and companies; investment research outsourcing; fund services; risk management and infrastructure advisory services.