Embed Size (px)

Citation preview

Slide 1© Student Lending Analytics, LLC

SLA Webinar SeriesManaging Lender Selection in a Time of Financial Turmoil

This presentation does not constitute formal policy or legal

advice and should not be relied upon as such.

Slide 2© Student Lending Analytics, LLC

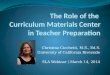

Managing Lender Selection in Time of Financial Turmoil Summary

Having a lender list for your students still matters

– Students looking for experts to help them

– All lenders are not created equal

Overall, market conditions remain challenging

– Multiple government programs propping up FFELP

– Availability of private loans has narrowed considerably

HEOA creates new requirements for lender lists

– The process matters

Important criteria to consider in your process

– Customer service

– Financial strength

List management requires ongoing vigilance

Slide 3© Student Lending Analytics, LLC

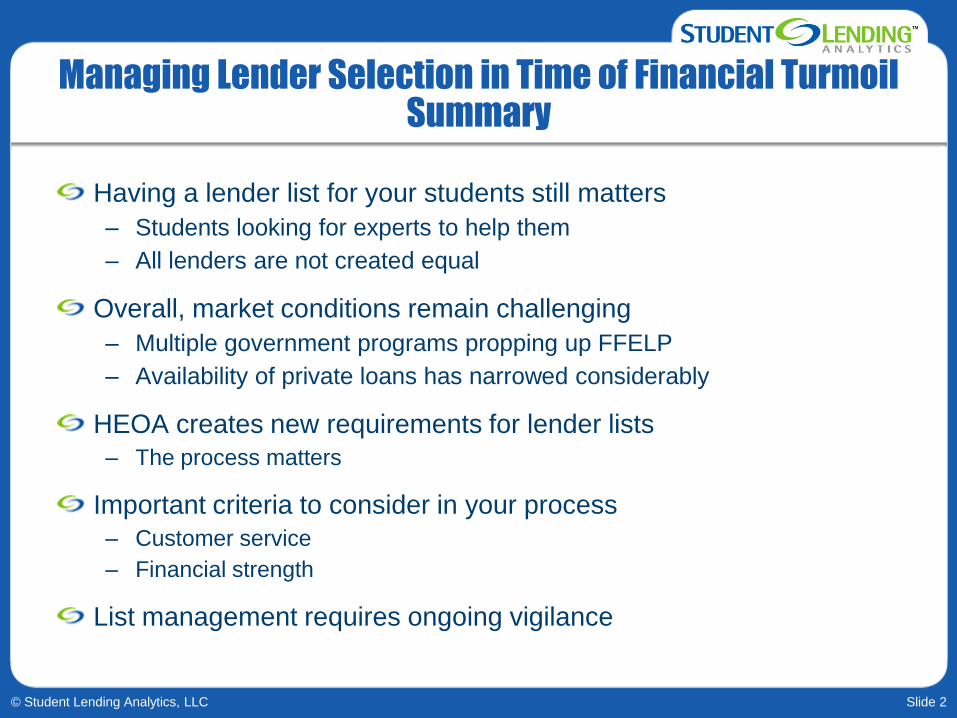

Managing Lender Selection in Time of Financial Turmoil Having a Lender List Matters

GMAC Bank, NextStudent, Xanthus Financial Services, EduCap, Graduate Loan Associates, Nelnet and Campus Door – Recently settled probe into “deceptive marketing practices”

Google “private student loans” and find over 900,000 results

First page of search results– Alternativestudentloan.com

• No Fafsa, instant decisions online, $40,000/year, Funds Direct to You

– Estudentloan.com

– Studentfinancialgroup.com

• Quick application. Quick response. The Quick-To-Learn loan

– Collegeloanstoday.com

• Fast and Easy Approval, Up to $40,000 per year.

Other popular reference sites list hundreds of lenders

Headline anxiety leads to search for experts

Slide 4© Student Lending Analytics, LLC

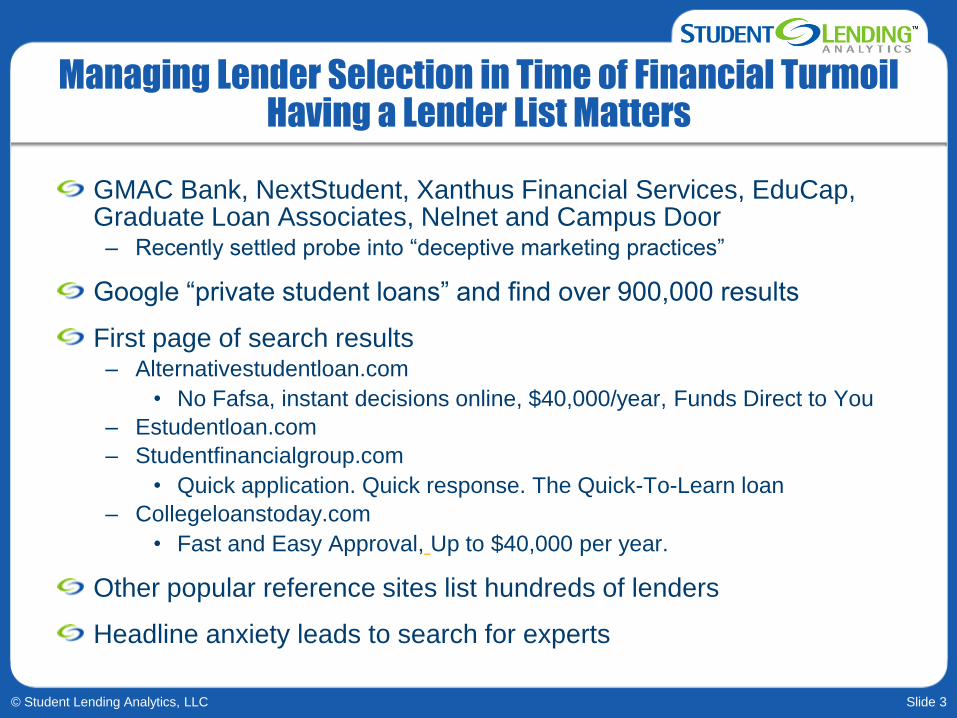

Managing Lender Selection in Time of Financial Turmoil What Has Changed in the Last Year?

FFELP loans– Large number of lenders have left market; some have returned

– Lenders have changed business models, including servicing relationships

– Ongoing credit crisis increases importance of short-term liquidity to fund loans

– Significant cutbacks in customer service require ongoing diligence

– Since Parent PLUS loans now have deferment option, be sure to check timing of capitalization of interest

– Mergers may reduce number of lenders further

Private loans– Lenders representing over 35% of private loan volume are no longer lending

– Interest rates and fees continue to change on ongoing basis

– Credit requirements have tightened in light of increasing defaults and delinquencies

– Some states have had success raising capital in bond markets for private loans while others have not

Slide 5© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial Turmoil Choosing Best Lenders Matters MORE not Less

To students, lender performance seen as extension of financial aid office

– Student satisfaction survey comments link financial aid office directly with lenders

Departure of lenders has wide-ranging impact on operations

– Communicate change directly to affected students and parents

– Serial borrowers need help selecting new lender and sign new promissory notes

– Change all marketing collateral with lender list printed on it

– Change on-line lender list

– Front-line team members stressed by volume of calls

– Business office must be notified that payments may be delayed

Even with diminished set of lenders, recognize that all lenders are NOT the same

Slide 6© Student Lending Analytics, LLC

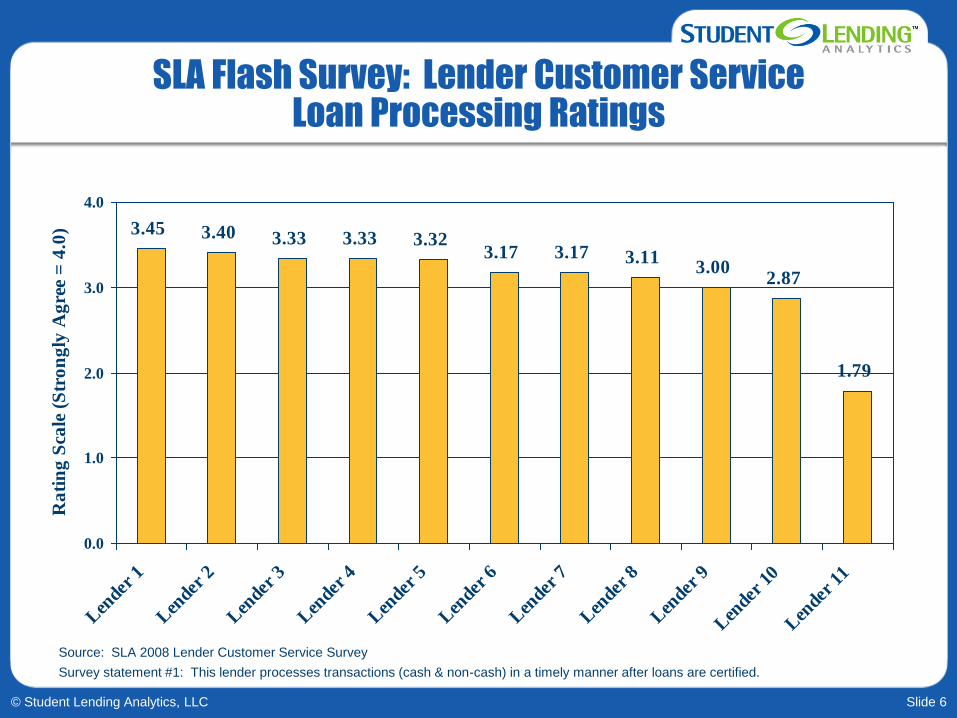

SLA Flash Survey: Lender Customer Service Loan Processing Ratings

3.45 3.40 3.33 3.33 3.323.17 3.17 3.11

3.002.87

1.79

0.0

1.0

2.0

3.0

4.0

Len

der 1

Len

der 2

Len

der 3

Len

der 4

Len

der 5

Len

der 6

Len

der 7

Len

der 8

Len

der 9

Len

der 10

Len

der 11

Ra

tin

g S

cale

(S

tro

ng

ly A

gre

e =

4.0

)

Source: SLA 2008 Lender Customer Service Survey

Survey statement #1: This lender processes transactions (cash & non-cash) in a timely manner after loans are certified.

Slide 7© Student Lending Analytics, LLC

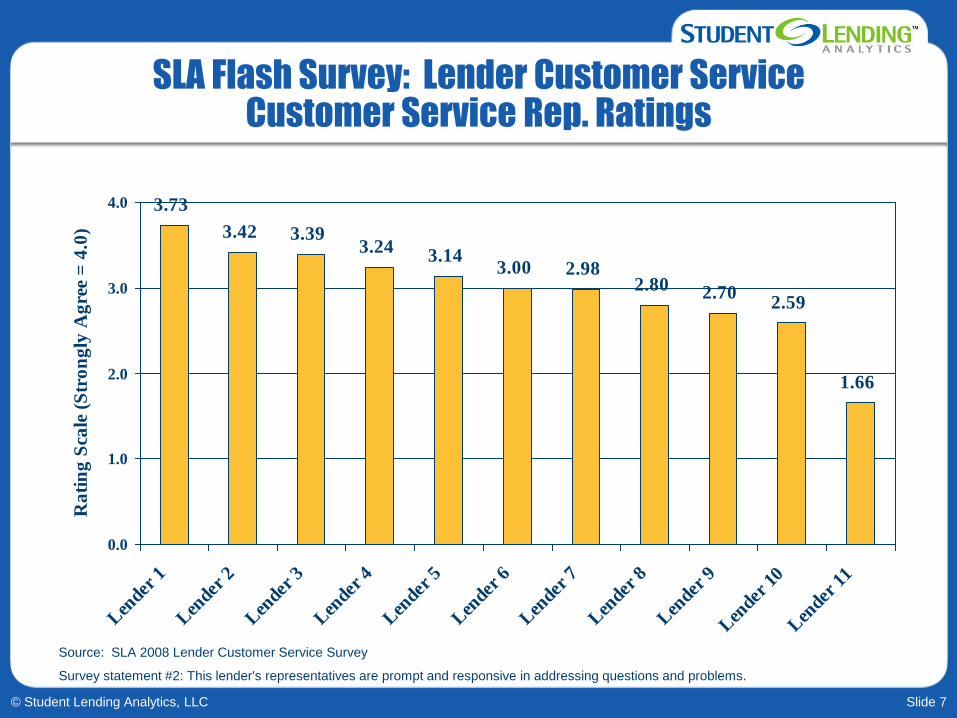

SLA Flash Survey: Lender Customer Service Customer Service Rep. Ratings

3.73

3.42 3.393.24

3.143.00 2.98

2.80 2.702.59

1.66

0.0

1.0

2.0

3.0

4.0

Len

der 1

Len

der 2

Len

der 3

Len

der 4

Len

der 5

Len

der 6

Len

der 7

Len

der 8

Len

der 9

Len

der 10

Len

der 11

Ra

tin

g S

cale

(S

tro

ng

ly A

gre

e =

4.0

)

Source: SLA 2008 Lender Customer Service Survey

Survey statement #2: This lender's representatives are prompt and responsive in addressing questions and problems.

Slide 8© Student Lending Analytics, LLC

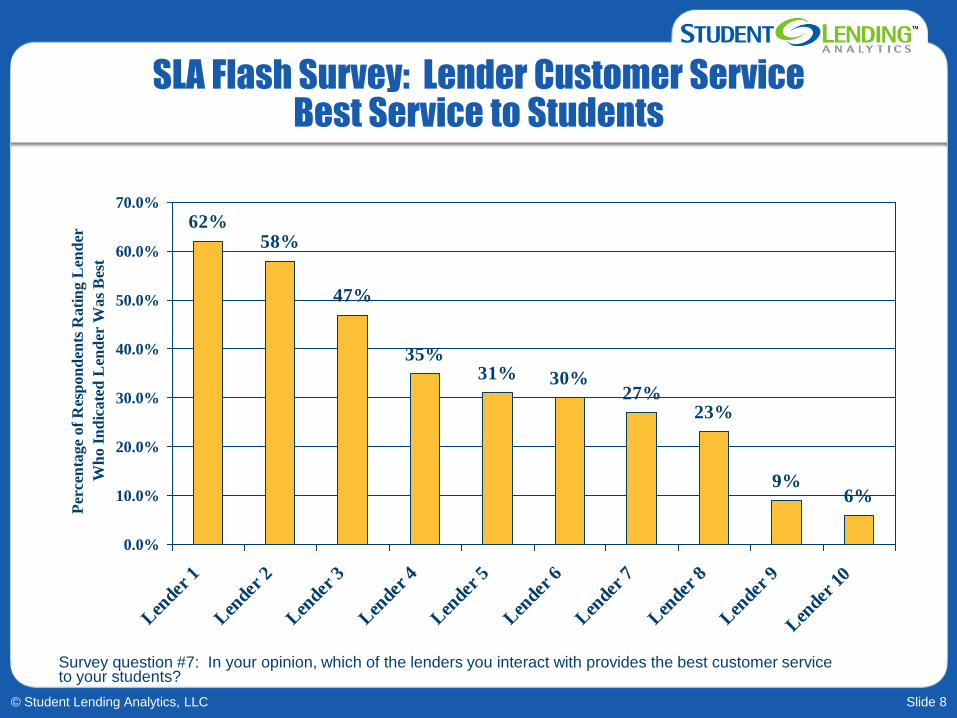

SLA Flash Survey: Lender Customer Service Best Service to Students

62%58%

47%

35%31% 30%

27%23%

9%6%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Len

der 1

Len

der 2

Len

der 3

Len

der 4

Len

der 5

Len

der 6

Len

der 7

Len

der 8

Len

der 9

Len

der 10

Per

cen

tag

e o

f R

esp

on

den

ts R

ati

ng

Len

der

Wh

o I

nd

ica

ted

Len

der

Wa

s B

est

Survey question #7: In your opinion, which of the lenders you interact with provides the best customer service to your students?

Slide 9© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial Turmoil Summary

Rationale for lender lists

Market conditions for FFELP and private loans

HEOA and new requirements for lender lists

RFI considerations for 2009-10

Successful management of lender relationships

Slide 10© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial Turmoil FFELP Market Update

One-two punch of CCRA and credit crunch has floored over 100 FFELP lenders

Government has intervened aggressively to prop up FFELP lenders– ECASLA

– Short-Term Loan Purchase Program

– Commercial Paper Conduit

– TALF

No student who needed a federal loan was denied one, but…– Lender list shake-up created confusion, uncertainty and extra work

– Some lenders delayed their disbursements

– Lenders significantly restructured their staffing levels to reflect new market realities

Current structure – Bank/Student lender originates loan

– Department of Education purchases loans or a participation right

Servicing rights for loans involved in government programs: different answer for different programs

Slide 11© Student Lending Analytics, LLC

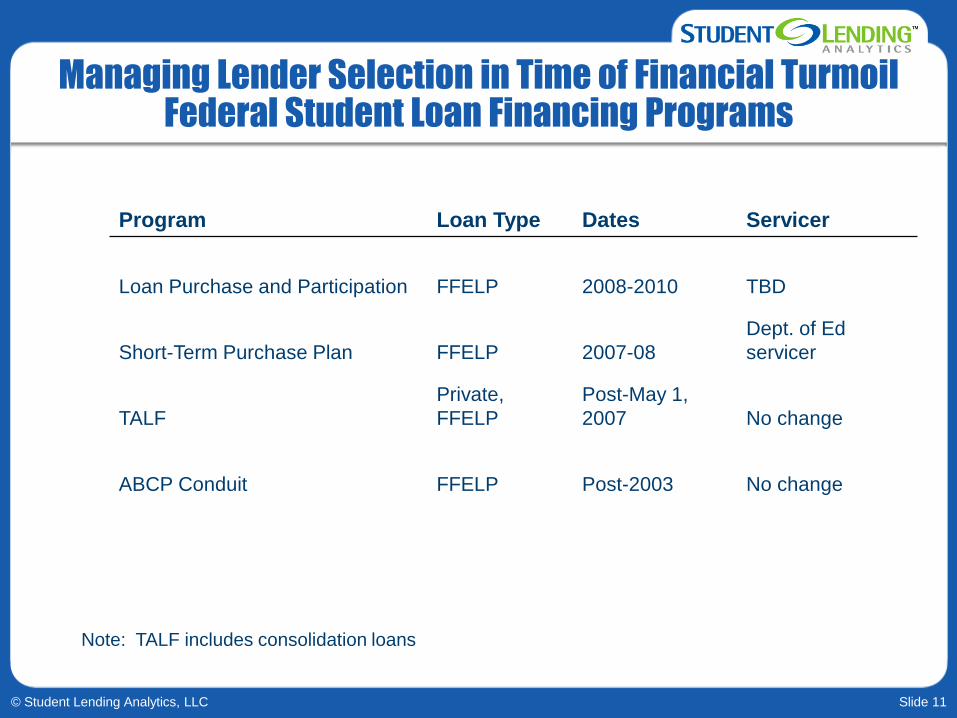

Managing Lender Selection in Time of Financial Turmoil Federal Student Loan Financing Programs

Program Loan Type Dates Servicer

Loan Purchase and Participation FFELP 2008-2010 TBD

Short-Term Purchase Plan FFELP 2007-08

Dept. of Ed

servicer

TALF

Private,

FFELP

Post-May 1,

2007 No change

ABCP Conduit FFELP Post-2003 No change

Note: TALF includes consolidation loans

Slide 12© Student Lending Analytics, LLC

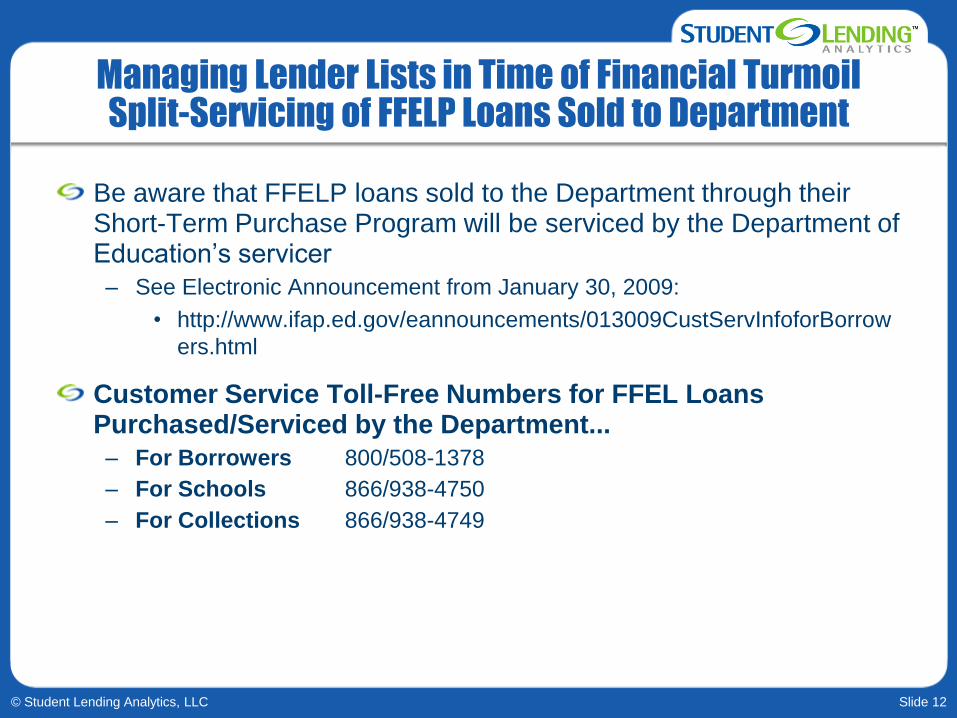

Managing Lender Lists in Time of Financial Turmoil Split-Servicing of FFELP Loans Sold to Department

Be aware that FFELP loans sold to the Department through their Short-Term Purchase Program will be serviced by the Department of Education’s servicer

– See Electronic Announcement from January 30, 2009:

• http://www.ifap.ed.gov/eannouncements/013009CustServInfoforBorrow

ers.html

Customer Service Toll-Free Numbers for FFEL Loans Purchased/Serviced by the Department...

– For Borrowers 800/508-1378

– For Schools 866/938-4750

– For Collections 866/938-4749

Slide 13© Student Lending Analytics, LLC

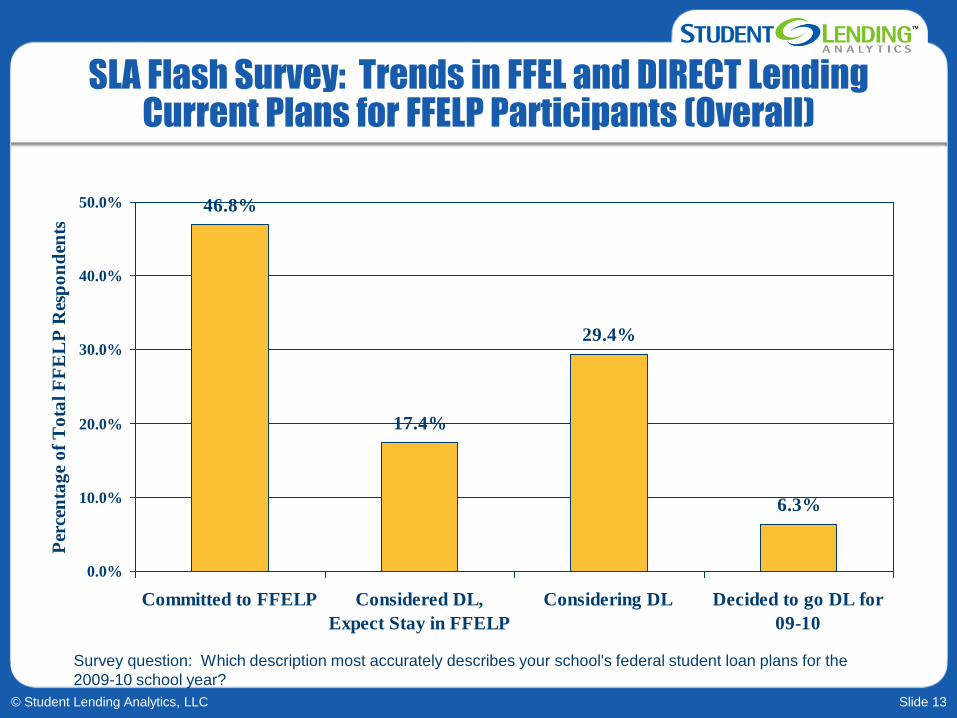

SLA Flash Survey: Trends in FFEL and DIRECT Lending Current Plans for FFELP Participants (Overall)

46.8%

17.4%

29.4%

6.3%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

Committed to FFELP Considered DL,

Expect Stay in FFELP

Considering DL Decided to go DL for

09-10

Per

cen

tag

e o

f T

ota

l F

FE

LP

Res

po

nd

ents

Survey question: Which description most accurately describes your school's federal student loan plans for the

2009-10 school year?

Slide 14© Student Lending Analytics, LLC

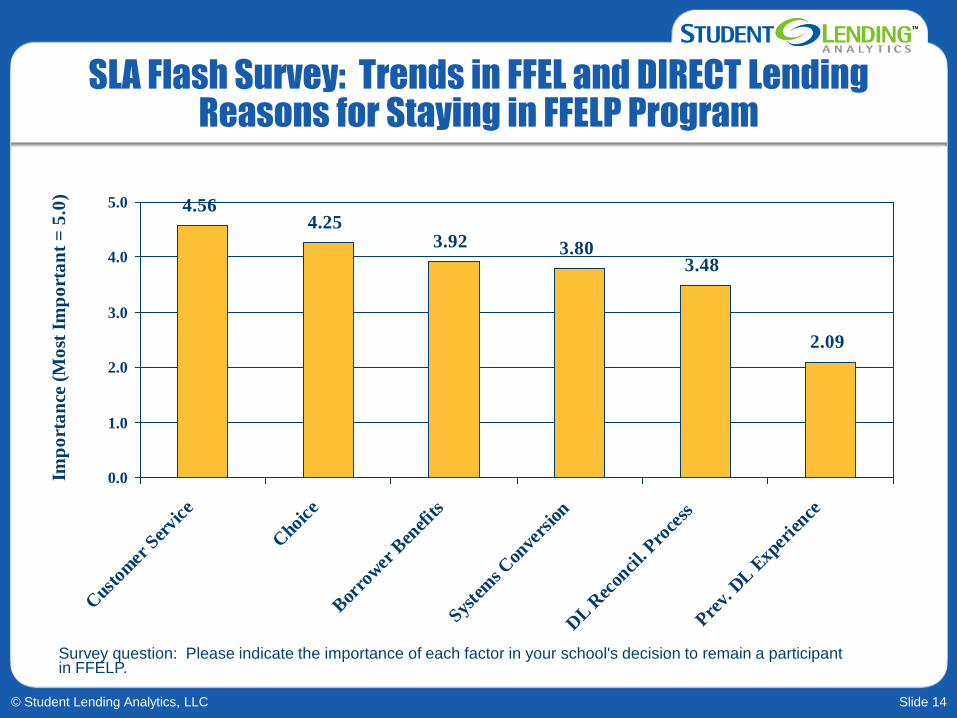

SLA Flash Survey: Trends in FFEL and DIRECT Lending Reasons for Staying in FFELP Program

4.564.25

3.92 3.803.48

2.09

0.0

1.0

2.0

3.0

4.0

5.0

Cus

tom

er S

ervi

ce

Cho

ice

Bor

rower

Ben

efits

Syste

ms C

onve

rsio

n

DL R

econ

cil.

Proce

ss

Prev.

DL E

xper

ience

Imp

ort

an

ce (

Mo

st I

mp

ort

an

t =

5.0

)

Survey question: Please indicate the importance of each factor in your school's decision to remain a participant in FFELP.

Slide 15© Student Lending Analytics, LLC

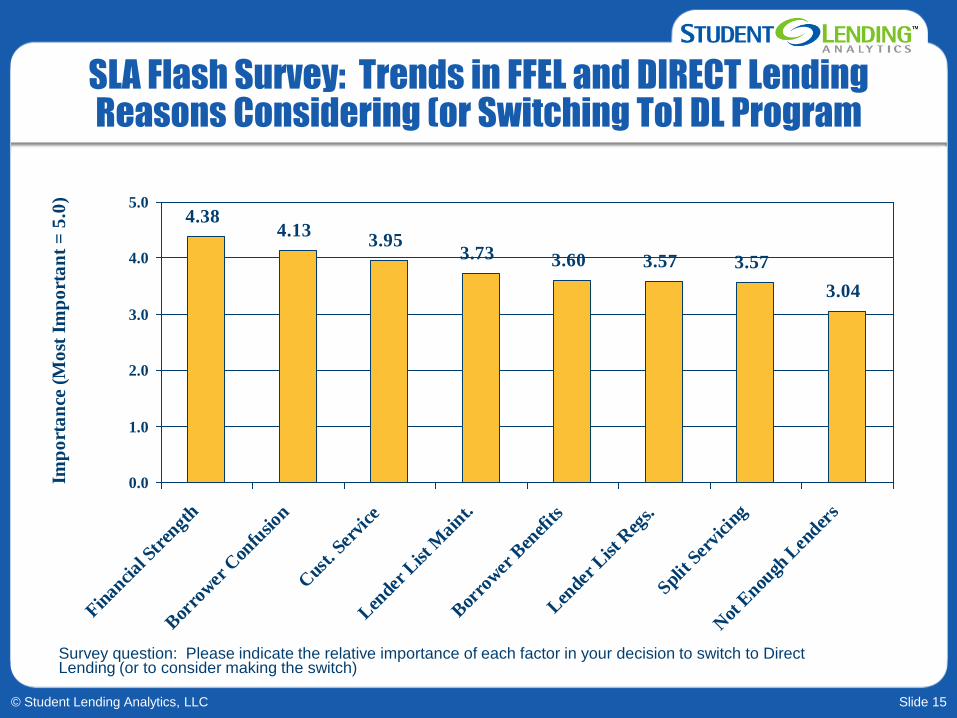

SLA Flash Survey: Trends in FFEL and DIRECT Lending Reasons Considering (or Switching To] DL Program

4.384.13

3.953.73 3.60 3.57 3.57

3.04

0.0

1.0

2.0

3.0

4.0

5.0

Finan

cial

Str

engt

h

Bor

rower

Con

fusio

n

Cus

t. Se

rvic

e

Len

der List

Mai

nt.

Bor

rower

Ben

efits

Len

der List

Reg

s.

Split

Serv

icin

g

Not

Enou

gh L

ender

s

Imp

ort

an

ce (

Mo

st I

mp

ort

an

t =

5.0

)

Survey question: Please indicate the relative importance of each factor in your decision to switch to Direct Lending (or to consider making the switch)

Slide 16© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial Turmoil Private Student Loan Markets Blinking Red

Availability of private loans declining rapidly…

– Lenders representing over 35% of private loan market have departed in 2008

• Credit line pulled: College Loan Corp., Education Finance Partners

• Parent company afflicted by sub-prime issues: Wachovia, CampusDoor

• Inability to access ABS market: Key Bank, Bank of America (TERI)

• Rising delinquencies overall have limited investor appetite for securities

– Other lenders narrowing loan activities to most creditworthy clients as fears mount over deteriorating consumer credit situation

• Largest private lender Sallie Mae (over 40% market share) had 20%

drop in private loan originations in 2008.

• Citibank and Sallie Mae both continue to see increasing

delinquencies based on most recent quarterly reports.

Slide 17© Student Lending Analytics, LLC

Managing Lender Lists in Time of Financial Turmoil Outlook for Private Loans

Do not expect much growth in supply from existing lenders – Largest player, Sallie Mae, has forecast originations of $5-$6 billion in 2009 vs. $6.3 billion in 2008

– Citibank undergoing restructuring

– Banks likely to remain risk-adverse in light of rising delinquencies

Expect credit unions to become more active players in private student loans

Proprietary schools lending directly to their students– Will non-profit institutions follow their lead?

Expect loan terms to be restructured by lenders reliant on securitization markets– Interest-only payments while in school to eliminate negative amortization loans

– Shorter terms

– Co-signers required for all but the most creditworthy students

States also looking for innovative solutions to fill the gap– Connecticut and Iowa developed partnerships with credit unions

– North Carolina received $1.1 billion investment SECU for funding their 2008-09 programs

– Largest state-based programs in New Jersey and Massachusetts able to raise $350-$400 Million

– New York has proposed private loan program for in-state students

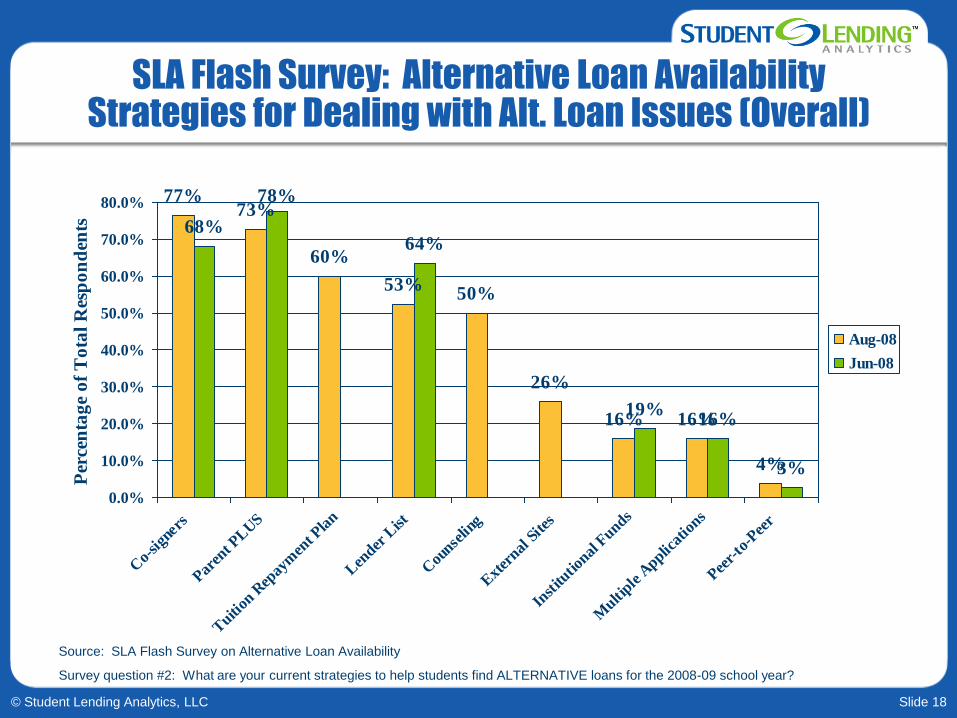

Slide 18© Student Lending Analytics, LLC

SLA Flash Survey: Alternative Loan Availability Strategies for Dealing with Alt. Loan Issues (Overall)

77%73%

60%

53%50%

26%

16% 16%

4%

68%

78%

64%

19%16%

3%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Co-

sign

ers

Paren

t PLUS

Tuiti

on R

epay

men

t Pla

n

Len

der L

ist

Cou

nselin

g

Ext

ernal

Site

s

Inst

itutio

nal F

unds

Multi

ple A

pplicat

ions

Peer-

to-P

eer

Per

cen

tag

e o

f T

ota

l R

esp

on

den

ts

Aug-08

Jun-08

Source: SLA Flash Survey on Alternative Loan Availability

Survey question #2: What are your current strategies to help students find ALTERNATIVE loans for the 2008-09 school year?

Slide 19© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial Turmoil Summary

Rationale for lender lists

Market conditions for FFELP and private loans

HEOA and new requirements for lender lists

RFI considerations for 2009-10

Successful management of lender relationships

Slide 20© Student Lending Analytics, LLC

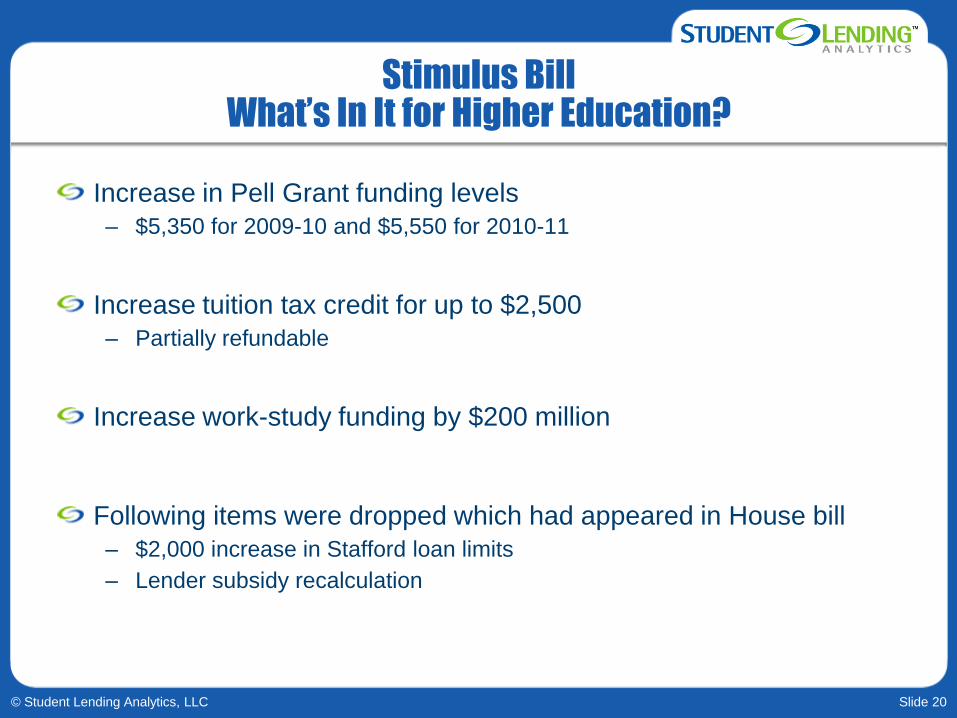

Stimulus BillWhat’s In It for Higher Education?

Increase in Pell Grant funding levels

– $5,350 for 2009-10 and $5,550 for 2010-11

Increase tuition tax credit for up to $2,500

– Partially refundable

Increase work-study funding by $200 million

Following items were dropped which had appeared in House bill

– $2,000 increase in Stafford loan limits

– Lender subsidy recalculation

Slide 21© Student Lending Analytics, LLC

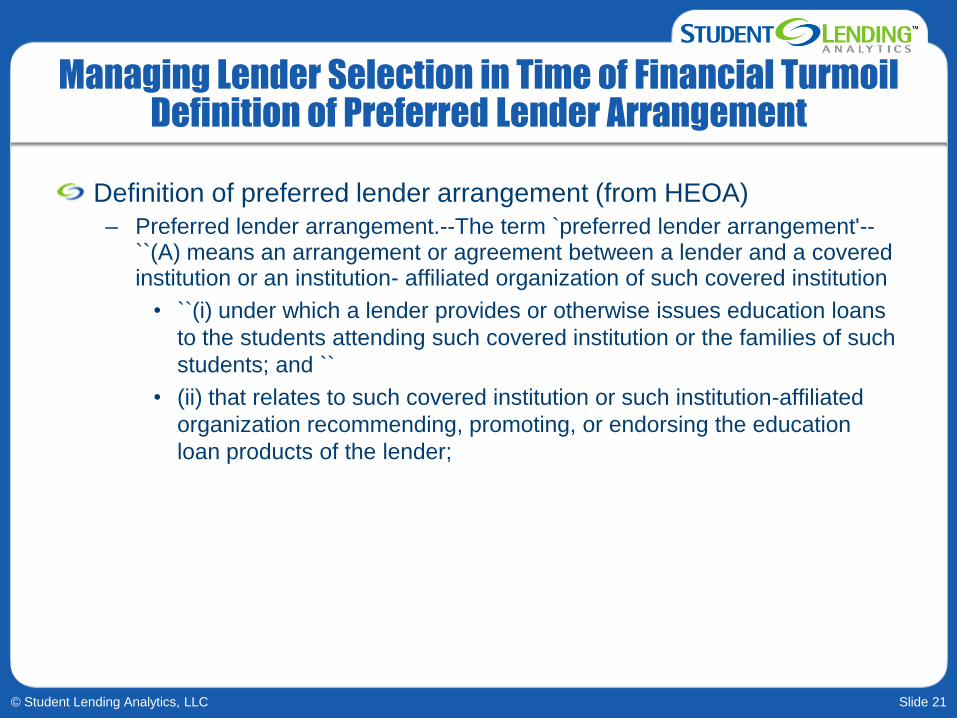

Managing Lender Selection in Time of Financial Turmoil Definition of Preferred Lender Arrangement

Definition of preferred lender arrangement (from HEOA)

– Preferred lender arrangement.--The term `preferred lender arrangement'--``(A) means an arrangement or agreement between a lender and a covered institution or an institution- affiliated organization of such covered institution

• ``(i) under which a lender provides or otherwise issues education loans

to the students attending such covered institution or the families of such

students; and ``

• (ii) that relates to such covered institution or such institution-affiliated

organization recommending, promoting, or endorsing the education

loan products of the lender;

Slide 22© Student Lending Analytics, LLC

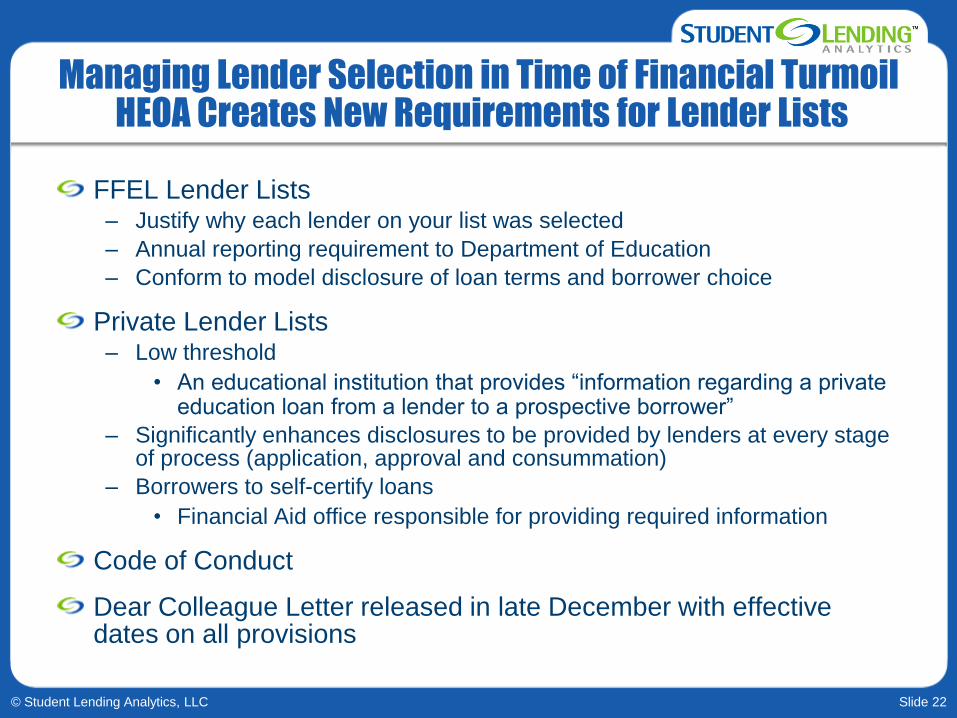

Managing Lender Selection in Time of Financial Turmoil HEOA Creates New Requirements for Lender Lists

FFEL Lender Lists– Justify why each lender on your list was selected

– Annual reporting requirement to Department of Education

– Conform to model disclosure of loan terms and borrower choice

Private Lender Lists– Low threshold

• An educational institution that provides “information regarding a private education loan from a lender to a prospective borrower”

– Significantly enhances disclosures to be provided by lenders at every stage of process (application, approval and consummation)

– Borrowers to self-certify loans

• Financial Aid office responsible for providing required information

Code of Conduct

Dear Colleague Letter released in late December with effective dates on all provisions

Slide 23© Student Lending Analytics, LLC

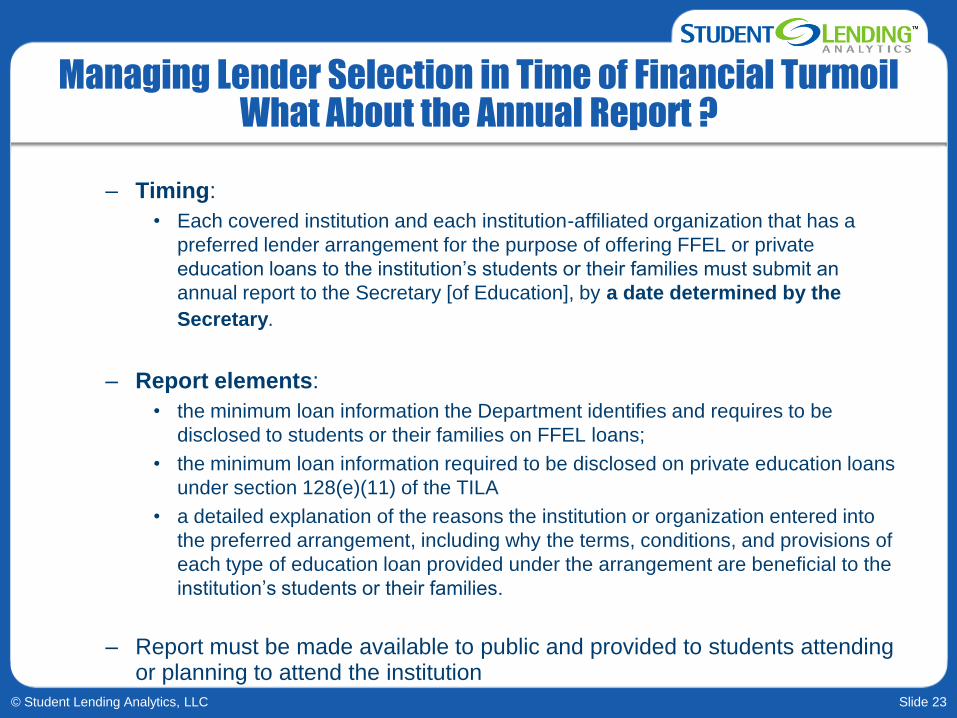

Managing Lender Selection in Time of Financial Turmoil What About the Annual Report ?

– Timing:

• Each covered institution and each institution-affiliated organization that has a

preferred lender arrangement for the purpose of offering FFEL or private

education loans to the institution’s students or their families must submit an

annual report to the Secretary [of Education], by a date determined by the

Secretary.

– Report elements:

• the minimum loan information the Department identifies and requires to be

disclosed to students or their families on FFEL loans;

• the minimum loan information required to be disclosed on private education loans

under section 128(e)(11) of the TILA

• a detailed explanation of the reasons the institution or organization entered into

the preferred arrangement, including why the terms, conditions, and provisions of

each type of education loan provided under the arrangement are beneficial to the

institution’s students or their families.

– Report must be made available to public and provided to students attending or planning to attend the institution

Slide 24© Student Lending Analytics, LLC

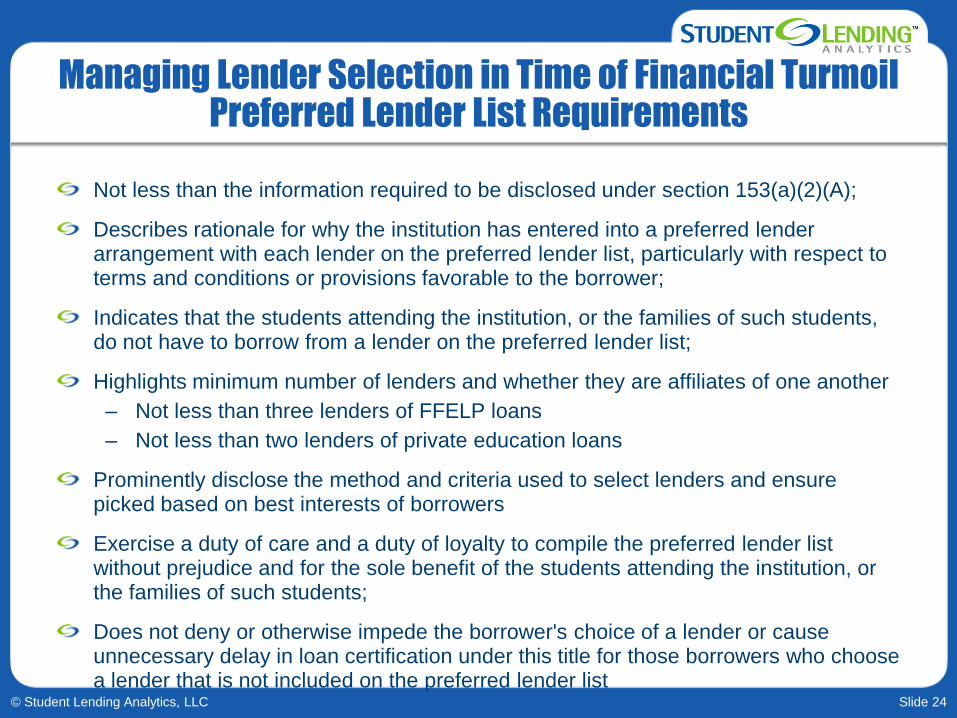

Managing Lender Selection in Time of Financial Turmoil Preferred Lender List Requirements

Not less than the information required to be disclosed under section 153(a)(2)(A);

Describes rationale for why the institution has entered into a preferred lender arrangement with each lender on the preferred lender list, particularly with respect to terms and conditions or provisions favorable to the borrower;

Indicates that the students attending the institution, or the families of such students, do not have to borrow from a lender on the preferred lender list;

Highlights minimum number of lenders and whether they are affiliates of one another

– Not less than three lenders of FFELP loans

– Not less than two lenders of private education loans

Prominently disclose the method and criteria used to select lenders and ensure picked based on best interests of borrowers

Exercise a duty of care and a duty of loyalty to compile the preferred lender list without prejudice and for the sole benefit of the students attending the institution, or the families of such students;

Does not deny or otherwise impede the borrower's choice of a lender or cause unnecessary delay in loan certification under this title for those borrowers who choose a lender that is not included on the preferred lender list

Slide 25© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial Turmoil Summary

Rationale for lender lists

Market conditions for FFELP and private loans

HEOA and new requirements for lender lists

RFI considerations for 2009-10

Successful management of lender relationships

Slide 26© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial Turmoil The Process Matters

Appoint scribe at outset of process to detail the process

Determine the targeted number of lenders on the list

Identify most important criteria and determine their weightings

Craft RFI questions based on criteria you determine are the most important

– Yes/No questions vs. open-ended ones

Develop comprehensive list of lenders to invite

Receive confirmation from lenders that they will be responding

– Bank of America has indicated they will not be responding to RFIs

– Chase will respond to Alt. Loan RFIs now and FFEL RFIs at some point in future

Analyze lender responses in objective, analytical fashion

Develop scorecard for lender responses

Select lenders based on scorecard

Slide 27© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial TurmoilLender Comparison Table and Disclosures

Disclosure of process

– San Francisco State provided actual lender scorecards

• http://www.sfsu.edu/~finaid/lenscoreSALLIEMAE.html

– SUNY Fredonia provides actual lender RFIs on their website

• http://www.fredonia.edu/finaid/LenderRFI.asp

Include key factors to enable students and families to more easily compare their options

– Private loan examples

• College for Financial Planning: http://fa.cffp.edu/lenderlist/private/

• University of California:

http://www.ucop.edu/sas/sfs/loans/privgrad_cosign.pdf

Slide 28© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial Turmoil Find Savings for Students Where You Can

ECASLA has diminished opportunity for borrower benefits with FFELP loans

– Most offering just 0.25% interest rate reduction for auto-debit in order to be eligible for sale to Department of Education

– Still one lender out there with no-fee Stafford loan

• For 2009-10 standard origination fee for Stafford loans drops to 0.5%

The 1% opportunity

– Ask lenders to partner with guarantors that are offering to waive the federal default fee

– Guarantors typically announce their policies in December

• Global fee waiver policy

• Selective fee waiver policy

– Analyze guarantor financial position to ensure long-term viability of fee waiver

– Saving 1% of $10 million FFEL loan portfolio equates to $100,000

Slide 29© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial Turmoil Financial Strength of Lenders MUST be Evaluated

Use your Business Office to assist with this analysis

Persistence in lending activities– Any issues with delayed disbursements

Source of financing– Internal– External

• Participation in Dept. of Education’s liquidity plan

• Even with all government programs, lines of credit still imperative

External bond ratings provide clue to cost of capital– Moody’s, Fitch, S&P

Loan growth over 2-3 year period provides signal on access to capital

Default and delinquency rates

Stock price – Performance relative to other student lenders– Trends

Slide 30© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial Turmoil Innovative Ways To Measure Customer Service

Student/Parent Surveys– Time as close to disbursement as possible

– Measure performance of lender during each stage of process and each touch point

– Determine criteria that are most important to them in selecting lenders

Financial Aid Team Members– Gauge quality of loan processing and responsive of lender representatives

– Good source for student issues also

Call Center quality– Measure quality of interaction with customer service representatives

– Develop standardized situations to ensure “apples to apples” comparison

Website reviews– Assess user-friendliness and ability of borrowers to self-service

– Assess transparency of lender’s disclosures

Slide 31© Student Lending Analytics, LLC

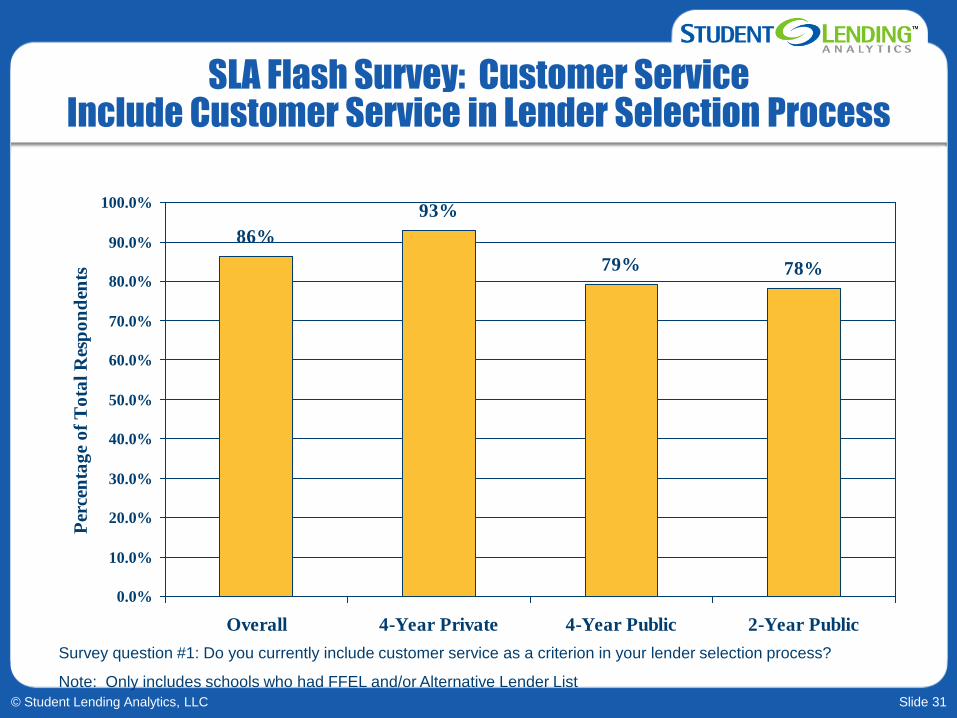

SLA Flash Survey: Customer Service Include Customer Service in Lender Selection Process

86%

93%

79% 78%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Overall 4-Year Private 4-Year Public 2-Year Public

Per

cen

tag

e o

f T

ota

l R

esp

on

den

ts

Survey question #1: Do you currently include customer service as a criterion in your lender selection process?

Note: Only includes schools who had FFEL and/or Alternative Lender List

Slide 32© Student Lending Analytics, LLC

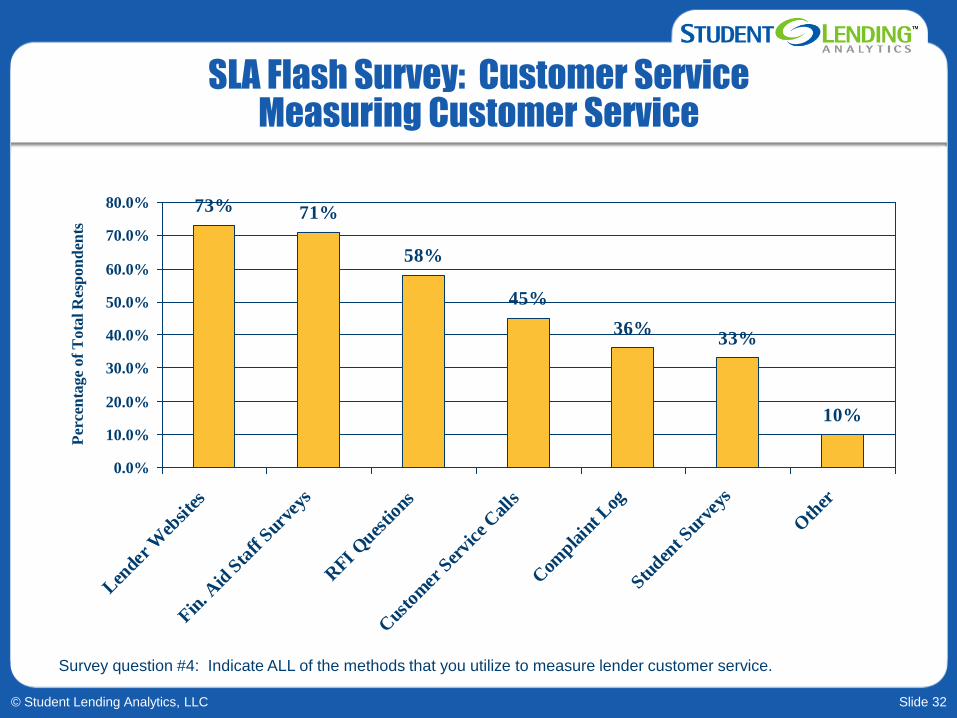

SLA Flash Survey: Customer Service Measuring Customer Service

73% 71%

58%

45%

36%33%

10%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Len

der W

ebsite

s

Fin. A

id S

taff

Surve

ys

RFI

Ques

tions

Cus

tom

er S

ervi

ce C

alls

Com

plain

t Log

Studen

t Sur

veys

Oth

er

Per

cen

tag

e o

f T

ota

l R

esp

on

den

ts

Survey question #4: Indicate ALL of the methods that you utilize to measure lender customer service.

Slide 33© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial Turmoil Summary

Rationale for lender lists

Market conditions for FFELP and private loans

HEOA and new requirements for lender lists

RFI considerations for 2009-10

Successful management of lender relationships

Slide 34© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial Turmoil Lender Management Not a Once Per Year Event

Selecting lenders is the beginning of the process not the end

Keys to effectively managing lender relationship– Information shared by lenders

• Approval rates

• Tiering distribution

• Changes to loan terms/eligibility requirements

– Information shared by schools

• Feedback from students/parents/financial aid staff

• Identify systemic issues early

Establish service expectations in the RFI to avoid misunderstandings– Can’t manage it if you do not measure it

Adjust lender list based on new developments– Importance of casting a wide net to have back-ups available

Slide 35© Student Lending Analytics, LLC

Managing Lender Selection in Time of Financial Turmoil Lender List Can Be a Competitive Advantage

Parents and students appreciate it

– Time savings

– Positive customer service experience affects opinion of financial aid

– Increased confidence about the choices they made

– Provides confidence that they will have access to loans

Financial aid team members appreciate it

– Streamlined operations

– Minimize time spent helping borrowers “find the best lender”

– Opportunity to provide input to process

– Recognize value of lender list to students

Slide 36© Student Lending Analytics, LLC

Student Lending AnalyticsBackground

Founded in 2007

Independent Research and Advisory Service with NO lender affiliations

Mission: Find best lenders for students through an analytically rigorous and comprehensive process

Services– RFI Management of FFEL and Private Loans– Research

Successes to Date– Managed RFI process at institutions with over $850 million in loan volume– Inside Student Lending, our monthly newsletter, reaches over 5,000 financial aid

administrators– Student Lending Analytics Blog has become the go-to source for breaking

developments and analysis on the student lending industry– SLA Flash Surveys have included the insights from over 1,500 financial aid

professionals on a variety of timely topics– Private Loan Options and the SLA’s 2008 Alternative Loan Guide provides

students and financial aid offices with an objective and focused list of private lenders

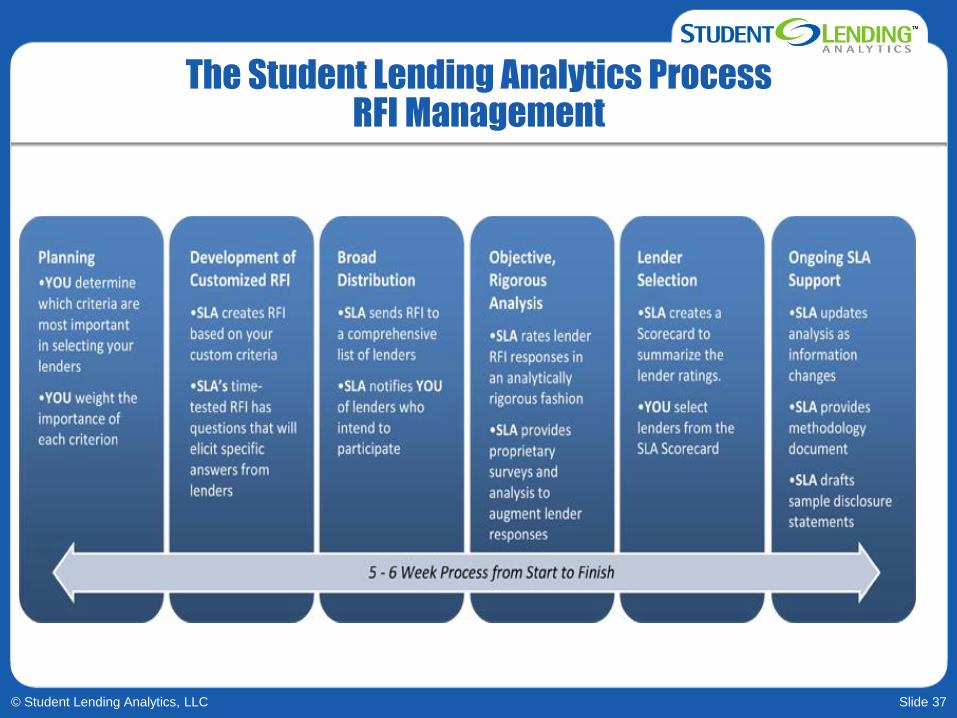

Slide 37© Student Lending Analytics, LLC

The Student Lending Analytics ProcessRFI Management

Slide 38© Student Lending Analytics, LLC

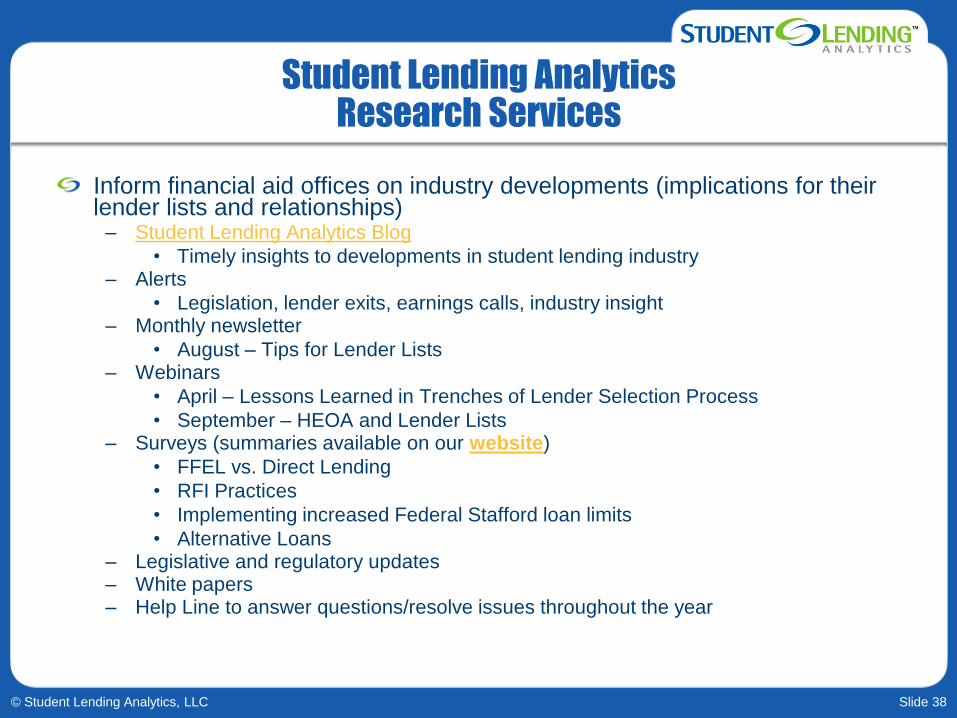

Student Lending AnalyticsResearch Services

Inform financial aid offices on industry developments (implications for their lender lists and relationships)

– Student Lending Analytics Blog

• Timely insights to developments in student lending industry– Alerts

• Legislation, lender exits, earnings calls, industry insight– Monthly newsletter

• August – Tips for Lender Lists– Webinars

• April – Lessons Learned in Trenches of Lender Selection Process

• September – HEOA and Lender Lists– Surveys (summaries available on our website)

• FFEL vs. Direct Lending

• RFI Practices

• Implementing increased Federal Stafford loan limits

• Alternative Loans– Legislative and regulatory updates– White papers– Help Line to answer questions/resolve issues throughout the year

Slide 39© Student Lending Analytics, LLC

Student Lending AnalyticsContact Information

For more information about SLA and our RFI+ services, please contact us at:

Tim Ranzetta

Student Lending Analytics LLC

1000 Elwell Court, Suite 203

Palo Alto, CA 94303

(650) 858-2724 X10

www.studentlendinganalytics.com